atty. justina f. callangan securities and exchange commission is for pse 2008-final.pdf ·...

TRANSCRIPT

April 29, 2009 Atty. Justina F. Callangan Director – Corporation Finance Department Securities and Exchange Commission SEC Building, EDSA Greenhills, Mandaluyong City Dear Atty. Callangan: This is in reference to your letter dated April 20, 2009 requiring Aboitiz Transport System (ATSC) Corporation (the “Company”) to amend its Information Statement and Management Report, which were submitted to the Commission on April 14, 2009. In reply, please see attached responses of the Company to the non-compliance noted by the Commission, the Company’s Definitive Information Statement and the accompanying Management Report, as well as the following additional requirements: 1. Letter of Undertaking to distribute to the Stockholders the 17Q - Interim Financial

Statements on the Annual Stockholder's Meeting on May 28, 2009 2. Certification that the accounting firm Sycip Gorres Velayo & Company (SGV) was

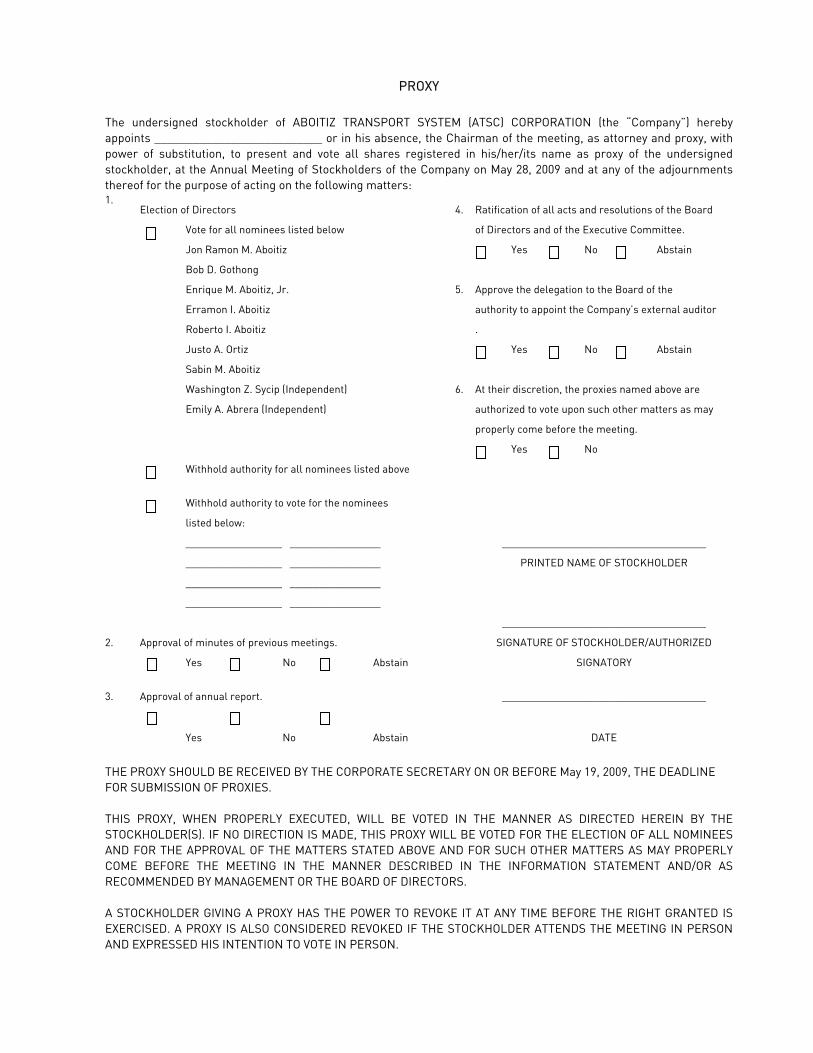

engaged by the Company in 1977. Kindly also note the following changes we made to the Definitive Information Statement: 1. Inclusion of Proxy Form in page 4 of the Definitive Statement. The pages affected by

this are page 3 Notice of Annual Stockholders Meeting and page 4 the Proxy form. 2. The ATS Board last April 23, 2009 regular meeting resolved to submit for the approval of

the stockholders during the Annual Stockholders’ Meeting a proposal to delegate to the Board of Directors the authority to appoint the Company’s external auditors for 2009. This resolution is disclosed under Item 7. Independent Public Accountants.

We hope that you will find the foregoing in order. Should you have further clarifications, please let us know. Thank you. Very truly yours,

Ismael R. Cabonse Officer In-Charge

1

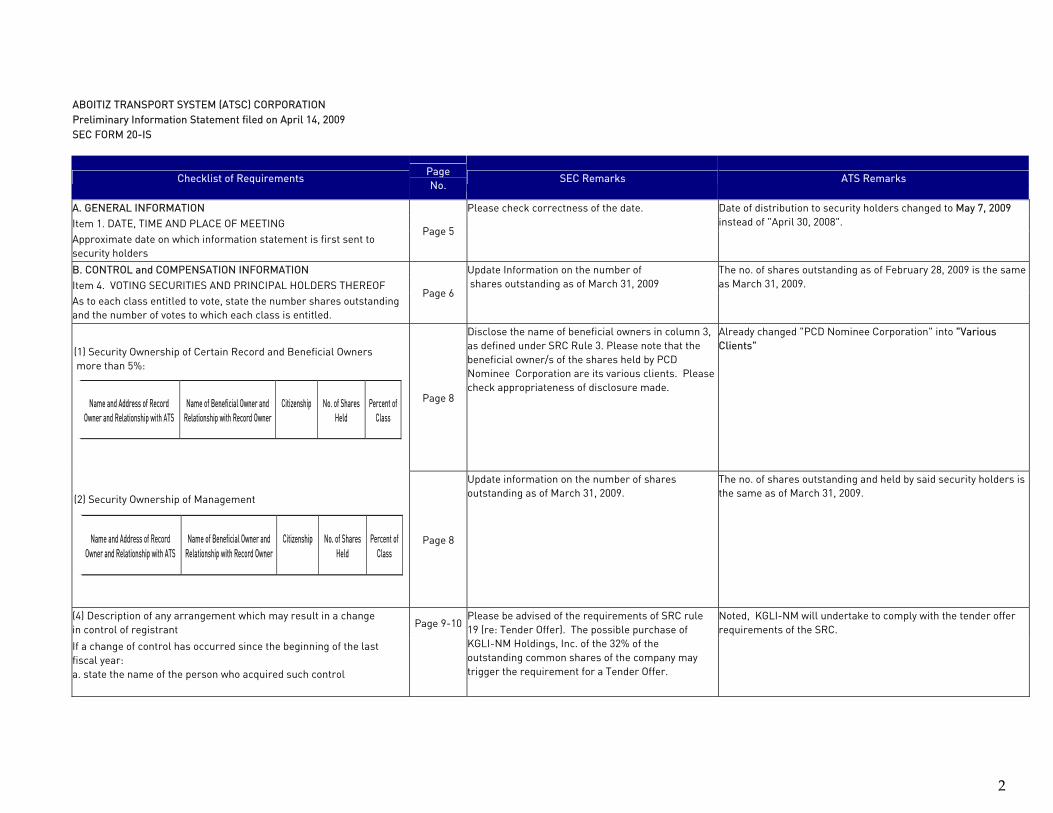

ABOITIZ TRANSPORT SYSTEM (ATSC) CORPORATION

Preliminary Information Statement filed on April 14, 2009 SEC FORM 20-IS

Checklist of Requirements Page No.

SEC Remarks ATS Remarks

A. GENERAL INFORMATION Item 1. DATE, TIME AND PLACE OF MEETING Approximate date on which information statement is first sent to security holders

Page 5

Please check correctness of the date. Date of distribution to security holders changed to May 7, 2009 instead of "April 30, 2008".

B. CONTROL and COMPENSATION INFORMATION Item 4. VOTING SECURITIES AND PRINCIPAL HOLDERS THEREOF As to each class entitled to vote, state the number shares outstanding and the number of votes to which each class is entitled.

Page 6

Update Information on the number of shares outstanding as of March 31, 2009

The no. of shares outstanding as of February 28, 2009 is the same as March 31, 2009.

(1) Security Ownership of Certain Record and Beneficial Owners more than 5%:

Page 8

Disclose the name of beneficial owners in column 3, as defined under SRC Rule 3. Please note that the beneficial owner/s of the shares held by PCD Nominee Corporation are its various clients. Please check appropriateness of disclosure made.

Already changed "PCD Nominee Corporation" into "Various Clients"

(2) Security Ownership of Management

Page 8

Update information on the number of shares outstanding as of March 31, 2009.

The no. of shares outstanding and held by said security holders is the same as of March 31, 2009.

(4) Description of any arrangement which may result in a change in control of registrant

If a change of control has occurred since the beginning of the last fiscal year: a. state the name of the person who acquired such control

Page 9-10 Please be advised of the requirements of SRC rule 19 (re: Tender Offer). The possible purchase of KGLI-NM Holdings, Inc. of the 32% of the outstanding common shares of the company may trigger the requirement for a Tender Offer.

Noted, KGLI-NM will undertake to comply with the tender offer requirements of the SRC.

Name and Address of Record

Owner and Relationship with ATS

Name of Beneficial Owner and

Relationship with Record Owner

Citizenship

No. of Shares

Held

Percent of

Class

Name and Address of Record

Owner and Relationship with ATS

Name of Beneficial Owner and

Relationship with Record Owner

Citizenship

No. of Shares

Held

Percent of

Class

2

b. amount and source of consideration used

c. basis of control

d. date and description of the transaction(s) which resulted in the change in control

e. Percentage of voting securites now beneficially owned directly/indirectly by the person who acquired control

f. Identify from whom control was assumed

Item 5. DIRECTORS & EXECUTIVE OFFICERS Page 10

If action is with respect to election of directors Information required by Part IV paragraphs (A), (D) (1) and (D) (3) of Annex C, as amended

Please be advised of the Notice of the Commission dated October 20, 2006 re: Certification of Qualification of Independent Directors

Noted.

(A)(1) Identify directors, including Independent Directors and Executive Officers

Page 14

(a) List the names, ages and citizenship of all directors, including independent directors, executive officers and all persons nominated or chosen to become such where required under Section 38 of the Code and SRC Rule 38.1 adopted thereunder; also provide the names of the incorporators in the case of an investment company.

(b) List the positions and offices that each such person held, or will hold, if known, with the registrant;

(c) Give the person's term of office as a director and the period during which the person has served;

(d)Briefly describe the person's business experience during the past five (5) years; and

(e) If a director, identify other directorships held in reporting companies, naming each company.

Incomplete. Please provide required information on Mr. Rafael L. Sanvictores, the company's SVP - Vessels and Hotel Operations

Already provided as follows: Mr. Rafael L. Sanvictores, 51 years old, Filipino, Senior Vice President – Hotel Operations since May 2006. He has been with the Aboitiz group since 1980. Previous positions in ATS include: Senior Vice President and Chief Operating Officer - SuperFerry Group; Senior Vice President and Chief Operating Officer - Passage Division and Assistant Vice President for Forwarding Operations, Sales and Aboitiz Inland Concarriers, Inc. He graduated with a degree in Bachelor of Science in Economics at San Beda College.

(5) Part IV, Paragraph (D) of "Annex C" as amended Page 18

Certain Relationships and Related transactions

(SEC MC No. 14, Series of 2004) (1) In addition to the disclosures in the financial statements which are required under SFAS/IAS No. 24 on Related Party Disclosures, registrants shall describe under this item the elements of the transactions that are necessary for an understanding of the transactions' business purpose and economic substance, their effects on the financial statements, and the special risks or contingencies arising from these transactions. The Commission considers the discussion of the following to be necessary:

Please change Note 20 to Note 21 Changed "Note 20" to "Note 21"

3

(a) the business purpose of the arrangement;

(b) identification of the related parties transacting business with the registrant and nature of the relationship;

(c) how transaction prices were determined by the parties;

(d) if disclosures represent that transactions have been evaluated for fairness, a description of how the evaluation was made; and

(e) any ongoing contractual or other commitments as a result of the arrangement.

(2) The disclosure shall also include information about parties that fall outside the definition of "related parties" under SFAS/IAS No. 24, but with whom the registrants or its related parties have a relationship that enables the parties to negotiate terms of material transactions that may not be available from other, more clearly independent, parties on an arm's length basis. For example, an entity may be established and operated by individuals that were former senior management of, or have some other current or former relationship with, a registrant. The purpose of the entity may be to own assets used by the registrant or provide financing or services to the registrant. Although former management or persons with other relationships may not meet the definition of a related party pursuant to SFAS/IAS 24, the former management positions may result in negotiation of terms that are more or less favorable than those available on an arm's-length basis from clearly independent third parties that are material to the registrant's financial position or financial performance.

In some cases, investors may be unable to understand the registrant's reported results of operations without a clear explanation of these arrangements and relationships.Items of similar nature may be disclosed in aggregate except when separate disclosure is necessary for an understanding of the effects of related party transactions on the financial statements.

Item 7. Independent Public Accountants

Page 19

Please refer to SRC Rule 68, Paragraph (3)(b)(iv) (re:compliance with the 5 year rotation of external auditors)

Election, approval or ratification

Identify the Chairman and members of Audit Committee

Added name of Chairman and members as follows: The Audit Committee is composed of three Board members, namely, Washington Z. Sycip, chairperson and Jon Ramon R. Aboitiz and Bob D. Gothong, members.

4

Please indicate the year the company engaged the services of SGV & Co., as its Independent Public Accountant

Indicated the year ATS engaged SGV as follows: The accounting firm of Sycip, Gorres, Velayo & Company (SGV) has been ATS' Independent Public Accountant since year 1977. This is reckoned to be the approximate date based on the available records. Please see attached letter of Certification.

REPORT TO BE FURNISHED TO STOCKHOLDERS SRC Rule 20 - Disclosures to Stockholders prior to Meeting

If the Information Statement shall relate to an annual (or special meeting in lieu of the annual)meeting of stockholders at which directors shall be elected, it shall be accompanied or prededed by a management report to such stockholders containing the following:

MANAGEMENT REPORT

Audited Financial Statement and Interim Financial Statements, in accordance with SRC Rule 68, as ameded on February 2003

Considering that the Annual Stockholder's Meeting will be held on May 28, 2009, the Interim Financial Statements for the period ended March 31, 2009 should also be distributed.

The Company undertakes to distribute to its stockholders a copy of 17Q - Interim Financial Statements for the Period Ended March 31, 2009 on the Annual Stockholder's Meeting on May 28, 2009. Attached is the Letter of Undertaking.

Management's Discussion and Analysis (MD & A) or Plan of Operation (2) Management's Discussion and Analysis. MD&A helps explain financial results. A reader of the MD&A should understand the financial results of the registrant’s business as discussed in the “Business” section. It shall provide information with respect to liquidity, capital resources and other information necessary to understanding the registrant’s financial condition and results of operation.

Page 26

The discussion and analysis shall focus specifically on material events and uncertainties known to management that would cause reported financial information not to be necessarily indicative of future operating results or of future financial condition. This would include descriptions and amounts of matters that would have an impact on future operations and have not had an impact in the past, and matters that have had an impact on reported operations and are not expected to have an impact upon future operations.

5

For both full fiscal years and interim periods, disclose the company's and its majority-owned subsidiaries' top five (5) key performance indicators. It shall include a discussion of the manner by which the company calculates or identifies the indicators presented on a comparable basis.

Page 26 Incomplete. Provide qualitative data and discussion on how the company identifies such performance indicators.

The following KPI’s are used to evaluate the financial performance of ATS and its subsidiaries:a) Revenues – ATS revenues are mainly composed of freight and passage revenues and they are recognized when the related services are rendered. Total Revenue in 2008 is P10.3 billion compared to P8.2 billion in 2007.b) Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) - is calculated by adding back interest expense, amortization and depreciation into income before income tax, excluding extraordinary gains or losses. The Company’s EBITDA for 2008 is P947.1 million. c) Income before income tax (IBT) – is the earnings of the company before income tax expense. The Income Before Income Tax for 2008 is P119.3 million, 80% lower compared to P602.9 million in 2007 because mainly because vessel and other assets sales of P748.9 million in 2007. d) Debt-to-equity ratio – is determined by dividing total liabilities over stockholders’ equity. ATS’ debt-to-equity ratio in 2008 is 1.05:1:00.e) Current ratio – is measured by dividing total current assets by total current liabilities. The Company’s current ratio in 2008 is 0.89:1:00.

(a) Full fiscal years (3) Past and future financial condition and results of operation, with particular emphasis on the prospects of the future.

Page 33

Not complied with. Provide discussion as per higlighted portion.

This is provided under "Outlook" as follows: Strategies implemented in recent years have served well. Earning capacity of assets is maximized, costs are lowered, and its value-added businesses are gaining market acceptance. ATS believes its operating environment continues to be a challenging one as it faces uncertainties such as fuel prices and the purchasing power of its customers. Efforts are continuously placed on operational excellence at all levels of the organization with the aim of providing solutions to its customers at the lowest cost.

(4) Key variable and other qualitative and quatitative factors Pages 32-33, 35-36,

39

If material: (i) any known trends, events or uncertainties (material impact on liquidity

Please refer to "Other Information" and "Material changes in the Financial Statements" section.

6

(ii) Events that will trigger direct or contingent financial obligation thatis material to the company, including any default or acceleration of an obligation

(iii) All material off-balance sheet transactions, arrangements, obligations (including contingent obligations) and other relationships ofthe company with unconsolidated entities or other persons created during the reporting period

(iv) Description of any material commitments for capital expenditures, the general purpose of such commitments, and the expected sources of funds for such expenditures should be described;

Disclose, if any.

(v) any known trends, events or uncertainties (material impact on sales)

(vi) any significant elements of income or loss (from continuing operations)

(vii) causes for any material changes from period to period of FS which shall include vertical and horizontal analyses of any material item (5%)

Pages 31-32,35

(viii) seasonal aspects that has material effect on the FS

(b) Interim Periods: Comparable discussion to assess material changes (last fiscal year and comparable interim period in the preceding year). Disclose the required information under subpargraph (i) to (viii) above.

Update the information to March 31, 2009

Market Price of and Dividends required by Part V of Annex C, as amended Page 45-46

(1) Market Information (a) Identification of the principal market or markets where the registrant's common equity is traded.

If Principal market is stock exchange in the Philippines or a foreign exchange;

(1) State the name of the Exchange (2) Presentation of the High & Low Sales Prices for each quarter within the last two fiscal years and any subsequent interim period for which Financial Statements are required by SRC Rule 68.

(b) If the information called for by paragraph (A) of this Part is being presented, the document shall also include price information as of the latest practicable trading date, and, in the case of securities to be issued in connection with an acquisition, business combination or other reorganization, as of the trading date immediately prior to the public announcement of such transaction.

Update the price information as of the latest practicable date

Updated, market price is P 1.62.

7

(2) Holders (a) (i) Approximate number of holders of each class of common security as of the latest practicable date but in no event more than ninety (90) days prior to filing of the report. (ii) names of the top twenty (20) shareholders of each class

(iii) number of shares held

(iv) percentage of total shares outstanding held by each.

Page 46

(3) Dividends (a) Discussion of any Cash Dividends declared (two most recent years) (b) Description of any restriction that limit the payment of Dividend on Common Shares

Page 47

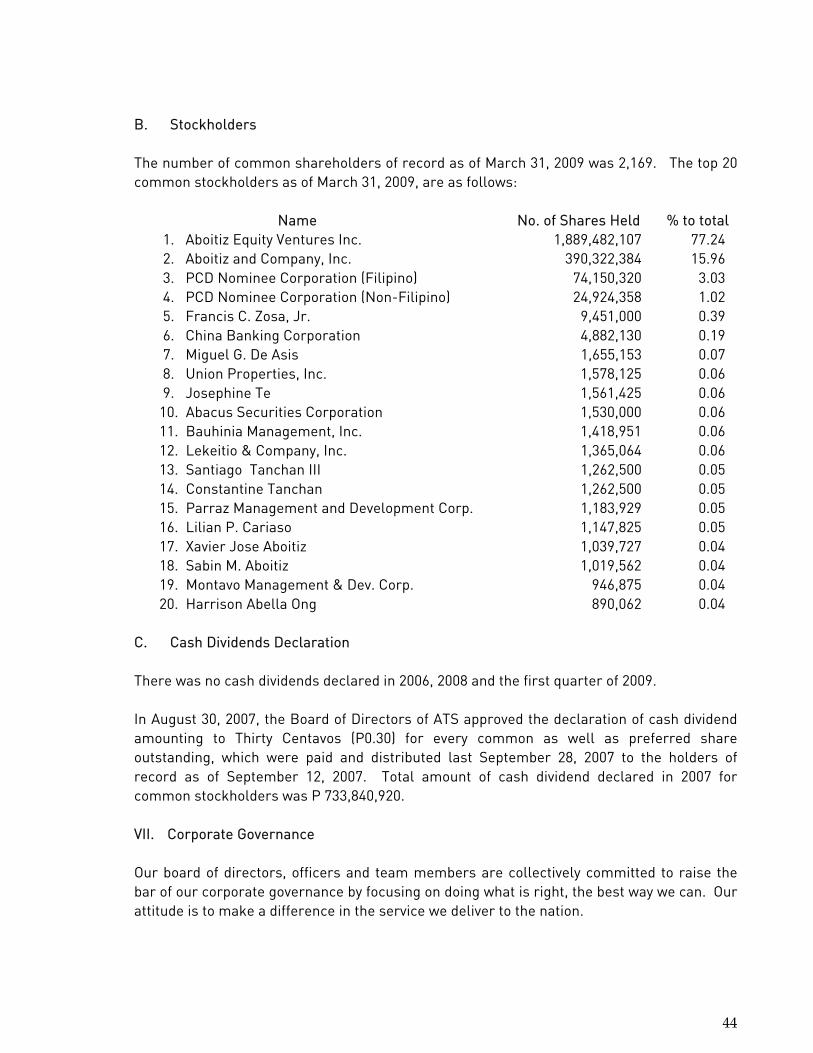

Not complied with. Already updated details on cash dividend declaration, as follows: There was no cash dividends declared in 2006, 2008 and the first quarter of 2009. In August 30, 2007, the Board of Directors of ATS approved the declaration of cash dividend amounting to Thirty Centavos (P0.30) for every common as well as preferred share outstanding, which were paid and distributed last September 28, 2007 to the holders of record as of September 12, 2007. Total amount of cash dividend declared in 2007 for common stockholders was P 733,840,920.

(4) Recent Sales of Unregistered or Exempt Securities, Including Recent Issuance of Securities Constituting an Exempt Transaction

(a) Date of sale and the Title and amount of Securities Sold (b) Name of the Underwriters or identity of persns to whom the Securities were sold (c) If sold for cash: Total offering price and Total underwriting discounts or commissions. Sold other than for cash: State the nature of the transaction and the type and amount of consideration received

(d) Exemption from Registration Claimed - Indicate section of the Code and state briefly the facts relied upon to make the exemption available.

Disclose, if any The Company has no exempt securities nor recent issuances of securities that constitute an exempt transaction.

8

April 29, 2009

Atty. Justina F. Callangan

Director – Corporation Finance Department Securities and Exchange Commission SEC Building, EDSA Greenhills, Mandaluyong City Dear Atty. Callangan: This is in compliance with the submission of the Definitive Information Statement of Aboitiz Transport System (ATSC) Corporation (the “Company”). The Company undertakes to distribute to its stockholders a copy of SEC Form 17-Q – Interim Financial Statements for the Period Ended March 31, 2009 pursuant to Section 17 of the Securities Regulation Code (SRC) and SRC Rule 17(2)(b) there under on the Annual Stockholder’s Meeting on May 28, 2009. Thank you. Very truly yours,

Ismael R. Cabonse Officer In-Charge

10

April 29, 2009 Atty. Justina F. Callangan Director – Corporation Finance Department Securities and Exchange Commission SEC Building, EDSA Greenhills, Mandaluyong City Dear Atty. Callangan: This refers to the compliance with the submission of the Definitive Information Statement of Aboitiz Transport System (ATSC) Corporation (the “Company”). This is to certify that the Company has engaged the accounting firm of Sycip, Gorres, Velayo & Company as its Independent Public Accountant since year 1977 based on the available records. Thank you. Very truly yours,

Ismael R. Cabonse Officer In-Charge

11

COVER SHEET

4 4 0 9 SEC Registration Number

A B O I T I Z T R A N S P O R T S Y S T E M ( A T S C )

C O R P O R A T I O N

(Company’s Full Name)

1 2 T H F L O O R T I M E S P L A Z A B U I L D I N G

U. N. A V E. C O R N E R T A F T A V E.

E R M I T A M A N I L A

(Business Address: No. Street City/Town/Province)

ISMAEL R. CABONSE 02-5287516 / 02-5287630 (Contract Person) (Company Telephone Number)

1 2 3 1 1 7 - I S 0 5 2 8Month Day (Form Type) Month Day

(Fiscal Year) (Annual Meeting)

Definitive Information Statement

(Secondary License Type, If Applicable)

Corporation Finance Department

N/A

Dept. Requiring this Doc. Amended Articles Number/Section

Total Amount of Borrowings

2,169 Total No. of Stockholders Domestic Foreign

To be accomplished by SEC Personnel concerned

File Number LCU

Document ID Cashier

S T A M P S Remarks: Please use BLACK ink for scanning purposes.

12

SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS

INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE

1. Check the appropriate box: [ ] Preliminary Information Statement [X] Definitive Information Statement 2. ABOITIZ TRANSPORT SYSTEM (ATSC) CORPORATION (formerly: William Gothong and Aboitiz, Inc.)______ Name of the Registrant as specified in its charter 3. PHILIPPINES Province, country or other jurisdiction of incorporation or organization 4. SEC Identification Number _____4409________

5. BIR Tax Identification Code ___000-313-401___ 6. 12th Floor, Times Plaza Building U.N. Ave. corner Taft Avenue Ermita, Manila Address of principal office Postal Code 1000 7. (02) 528-7171 / 528-7516 / 528-7630 and 528-7609 Registrant’s telephone numbers, including area code 8. May 28, 2009 at 4:00 PM Grand Ballroom 1 & 2, Mandarin Oriental Hotel, Makati Avenue, Makati City Date, time and place of the meeting of security holders 9. Approximate date on which the Information Statement is first to be sent or given to security holders May 7, 2009 10. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA

(information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding or Amount of Debt Outstanding Common Stock 2,446,136,400 Redeemable Preferred Stock 4,560,417 11. Are any or all of registrant's securities listed in a Stock Exchange? YES [X] NO [ ] If yes, disclose the name of such Stock Exchange and the class of securities therein: Philippine Stock Exchange - Common Stock and Redeemable PreferredStock

13

8.

9.

10. 11. Adjournment

ABOITIZ TRANSPORT SYSTEM (ATSC) CORPORATION (formerly William, Gothong & Aboitiz, Inc.)

NOTICE OF REGULAR ANNUAL MEETING OF STOCKHOLDERS PLACE:Grand Ballroom 1& 2, Mandarin Oriental Hotel

Makati Avenue, Makati City

DATE: May 28, 2009 TIME: 4:00 P.M.

Dear Stockholder: You are cordially invited to attend the Regular Annual Meeting of Stockholders of Aboitiz Transport System (ATSC) Corporation (the "Company"), which will be held on May 28, 2009 at Grand Ballroom 1 & 2, Mandarin Oriental Hotel, Makati Avenue, Makati City at 4:00 PM. The agenda for the meeting is as follows:

1. Call to Order 2. Certification of Notice 3. Determination and Declaration of Quorum 4. Approval of Minutes of the Stockholders’ Meeting held on May 22, 2008 5. Annual Report for the year ended December 31, 2008 6. Election of the Board of Directors 7. Appointment of External Auditor

Approval to mortgage corporate assets, to act as guarantor and/or surety, from time to time, for the benefit of the Company’s subsidiaries and affiliates. Approval and Ratification of all Acts and Resolutions of the Board of Directors and Management for the period covering 28 March 2008 to 29 March 2009 Such Other Matters as may properly come before it

Only stockholders of record in the books of the Company at the close of business on April 15, 2009 will be entitled to vote at said stockholders’ meeting. Manila, Philippines, April 14, 2009.

THE BOARD OF DIRECTORS By:

HELEN G. TIU

Corporate Secretary

========================================================================== We are not soliciting your proxy. However, if you would be unable to attend the meeting but would like to be represented thereat, you may accomplish the enclosed proxy form and submit the same on or before May 19, 2009 to the Office of the Corporate Secretary at 16th Floor Belvedere Tower, San Miguel Avenue, Ortigas Center, Pasig City. Validation of proxies shall be held on May 21, 2009 at 9:00 a.m. at the Office of the Corporate Secretary. Thank you.

PROXY

The undersigned stockholder of ABOITIZ TRANSPORT SYSTEM (ATSC) CORPORATION (the “Company”) herebyappoints __________________________ or in his absence, the Chairman of the meeting, as attorney and proxy, withpower of substitution, to present and vote all shares registered in his/her/its name as proxy of the undersignedstockholder, at the Annual Meeting of Stockholders of the Company on May 28, 2009 and at any of the adjournmentsthereof for the purpose of acting on the following matters: 1.

Election of Directors 4. Ratification of all acts and resolutions of the Board Vote for all nominees listed below of Directors and of the Executive Committee.

Jon Ramon M. Aboitiz Yes No Abstain Bob D. Gothong

Enrique M. Aboitiz, Jr. 5. Approve the delegation to the Board of the Erramon I. Aboitiz authority to appoint the Company’s external auditor Roberto I. Aboitiz . Justo A. Ortiz Yes No Abstain Sabin M. Aboitiz

Washington Z. Sycip (Independent) 6. At their discretion, the proxies named above are Emily A. Abrera (Independent) authorized to vote upon such other matters as may properly come before the meeting. Yes No Withhold authority for all nominees listed above

Withhold authority to vote for the nominees

listed below: _________________ ________________ ____________________________________ _________________ ________________ PRINTED NAME OF STOCKHOLDER _________________ ________________ _________________ ________________ ____________________________________

2. Approval of minutes of previous meetings. SIGNATURE OF STOCKHOLDER/AUTHORIZED

Yes No Abstain SIGNATORY

3. Approval of annual report. ____________________________________

Yes

No

Abstain DATE

THE PROXY SHOULD BE RECEIVED BY THE CORPORATE SECRETARY ON OR BEFORE May 19, 2009, THE DEADLINE FOR SUBMISSION OF PROXIES. THIS PROXY, WHEN PROPERLY EXECUTED, WILL BE VOTED IN THE MANNER AS DIRECTED HEREIN BY THESTOCKHOLDER(S). IF NO DIRECTION IS MADE, THIS PROXY WILL BE VOTED FOR THE ELECTION OF ALL NOMINEESAND FOR THE APPROVAL OF THE MATTERS STATED ABOVE AND FOR SUCH OTHER MATTERS AS MAY PROPERLYCOME BEFORE THE MEETING IN THE MANNER DESCRIBED IN THE INFORMATION STATEMENT AND/OR ASRECOMMENDED BY MANAGEMENT OR THE BOARD OF DIRECTORS. A STOCKHOLDER GIVING A PROXY HAS THE POWER TO REVOKE IT AT ANY TIME BEFORE THE RIGHT GRANTED ISEXERCISED. A PROXY IS ALSO CONSIDERED REVOKED IF THE STOCKHOLDER ATTENDS THE MEETING IN PERSONAND EXPRESSED HIS INTENTION TO VOTE IN PERSON.

INFORMATION STATEMENT (SEC FORM 20-IS)

A. GENERAL INFORMATION

WE ARE NOT ASKING YOU FOR A PROXY AND YOU ARE REQUESTED NOT TO SEND US A PROXY

Item 1. DATE, TIME AND PLACE OF MEETING OF SECURITY HOLDERS

Date of meeting : May 28, 2009 Time of meeting : 4:00 P.M. Place of meeting : Grand Ballroom 1 & 2, Mandarin

Oriental Hotel, Makati Avenue Makati City

Approximate date of mailing of this Statement

:

May 7, 2009

Registrant’s Mailing Address : 12th Floor, Times Plaza Bldg. UN Ave.

corner Taft Ave. Ermita, Manila

Item 2. DISSENTERS’ RIGHT OF APPRAISAL Under the Corporation Code, a dissenting stockholder shall have the right of appraisal or the right to demand payment of the fair value of his shares in the following instances:

a. any amendment to the articles of incorporation which has the effect of

changing or restricting the rights of any stockholder or class of shares, or of authorizing preferences in any respect superior to those of outstanding shares of any class, or of extending or shortening the term of corporate existence;

b. sale, lease, exchange, transfer, mortgage, pledge or other disposition of all or substantially all of the corporate property and assets;

c. merger or consolidation; d. investment in another corporation, business or for any purpose other than the

primary purpose for which the corporation was organized. In the foregoing cases, any stockholder who wishes to exercise his appraisal right must have voted against the proposed corporate action, made a written demand on the corporation within thirty (30) days after the date on which the vote was taken for payment of the fair value of his shares as well as complied with all other requirements provided under Title X of the Corporation Code. Failure to make the demand within such period or comply with the requirements provided under Title X of the Corporation Code shall be deemed a waiver of the appraisal right. If the proposed corporate action is implemented or effected, the corporation shall pay to such stockholder, upon surrender of the certificate or certificates of stock

2

representing his shares, the fair value thereof as of the day prior to the date on which the vote was taken, excluding any appreciation or depreciation in anticipation of such corporate action. If within a period of sixty (60) days from the date the corporate action was approved by the stockholders, the withdrawing stockholder and the corporation cannot agree on the fair value of the shares, it shall be determined and appraised by three (3) disinterested persons, one of whom shall be named by the stockholder, another by the corporation, and the third by the two thus chosen. The findings of the majority of the appraisers shall be final, and their award shall be paid by the corporation within thirty (30) days after such award is made. No payment shall be made to any dissenting stockholder unless the corporation has unrestricted retained earnings in its books to cover such payment. Upon payment by the corporation of the agreed or awarded price, the stockholder shall forthwith transfer his shares to the corporation. One of the Agenda during the stockholders’ meeting to be held on May 28, 2009 calls for the approval by stockholders representing at least two-thirds (2/3s) of the Registrant’s outstanding capital stock; more specifically, the Registrant’s authority to mortgage corporate assets and/or to act as guarantor and/or surety, from time to time, for the benefit of the Registrant’s subsidiaries and affiliates. This proposed corporation action may give rise to a possible exercise by stockholders of their appraisal right. Item 3. INTEREST OF CERTAIN PERSONS IN OR OPPOSITION TO MATTERS TO BE ACTED

UPON No director or officer of the Company at any time since the beginning of the last fiscal year or any nominee for election as a director of the Company or any associate of any of the foregoing persons has any substantial interest, direct or indirect, by security holdings or otherwise, in any matter to be acted upon in the stockholders’ meeting other than their re-election to their respective positions. No director has informed the Company in writing that he intends to oppose any action to be taken by the Company at the meeting.

B. CONTROL & COMPENSATION INFORMATION

Item 4. VOTING SECURITIES AND PRINCIPAL HOLDERS THEREOF

(1) The Registrant has 2,446,136,400 outstanding common shares and 4,560,417 outstanding

redeemable preferred shares as of April 15, 2009. Each common share shall be entitled to one vote with respect to all matters to be taken up during the annual stockholders’ meeting. Holders of redeemable preferred shares do not have the right to vote, except on matters specified in Section 6 of the Corporation Code with respect to which holders of non-voting shares shall nevertheless be entitled to vote, i.e.:

3

(1) Amendment of the articles of incorporation; (2) Adoption and amendment of by-laws; (3) Sale, lease, exchange, mortgage, pledge or other disposition of all or

substantially all of the corporate property; (4) Incurring, creating or increasing bonded indebtedness; (5) Increase or decrease of capital stock; (6) Merger or consolidation of the corporation with another corporation or other

corporations; (7) Investment of corporate funds in another corporation or business in

accordance with this Code; and (8) Dissolution of the corporation.

(2) The record date for determining stockholders entitled to notice and to vote during the

annual stockholders meeting and also to this information statement is April 15, 2009. (3) At each election for directors, every common stockholder shall have the right to vote, in

person or by proxy, the number of shares owned by him for as many persons as there are directors to be elected, or to cumulate his vote by giving one candidate as many votes as the number of such directors multiplied by the number of shares shall equal, or by distributing such votes on the same principle among any number of candidates.

(4) Security ownership of certain record and beneficial owners and management. Security ownership of certain record and beneficial owners of five per centum (5%) or more of the outstanding capital stock of the Registrant as of March 31, 2009:

Title of Class

Name and Address of Record

Owner and Relationship with ATS

Name of Beneficial Owner and

Relationship with Record Owner

Citizenship

No. of Shares

Held

Percent of

Class

Common 1. Aboitiz Equity Ventures Inc. Aboitiz Corporate Center Gov. Manuel A. Cuenco Avenue Kasambagan, Cebu City 6000 (PARENT COMPANY)

Aboitiz Equity Ventures Inc. PROXY: Authorized to vote on behalf of AEV are any of the following: Jon Ramon Aboitiz Chairman of the Board Roberto E. Aboitiz Director Erramon I. Aboitiz President & CEO Enrique M. Aboitiz Jr. Director Juan Antonio E. Bernad SVP Luis Miguel Aboitiz First Vice President

Filipino 1,889,482,107 77.10%

4

Common 3. Aboitiz and Company, Inc. Gov. Manuel A. Cuenco Avenue, Kasambagan, Cebu City 6000 (PRINCIPAL STOCKHOLDER)

Aboitiz and Company, Inc. PROXY: Authorized to vote on behalf of ACO are any of the following:

Jon Ramon Aboitiz Chairman Erramon I. Aboitiz President & CEO Roberto E. Aboitiz SVP Enrique M. Aboitiz, Jr. SVP

Filipino 390,322,384 15.93%

Preferred 4. PCD Nominee Corporation (Filipino) 37/f Enterprise Building Ayala Avenue, Makati City (STOCKHOLDER)

Various Clients Filipino 2,880,951 63.17%

Aboitiz Equity Ventures, Inc. (“AEV”) is a publicly listed company and as of March 31, 2009, Aboitiz and Company, Inc. (“ACO”) owns 43.48% of AEV. ACO is a corporation wholly owned by the Aboitiz family. No single stockholder, natural or juridical, owns five per centum (5%) or more of the shareholdings of ACO. Security Ownership of Management – Record and Beneficial Owners as of March 31, 2009:

Title of Class

Name of Beneficial Owner and Position

Citizenship Amount and nature of ownership

(Indicate record and/or beneficial) Percent of Class

COMMON Jon Ramon Aboitiz Chairman of the Board

Filipino 21 – “direct” 1,365,064 – “indirect”

Record Owner: Lekeitio & Company. Inc.

95,877 - “indirect” Record Owner: JIA Management Corp.

95,877 - “indirect” Record Owner: SOFO Management Inc.

95,877 - “indirect” Record Owner: EAA Management Corp.

0.06%

Common Bob D. Gothong Vice Chairman of the Board

Filipino 148 – “direct” 328,750 – “indirect”

Record Owner: One Wilson Place Holdings 1,561,425 – “indirect”

Record Owner: Josephine Te, wife

0.07%

Common Enrique M. Aboitiz, Jr. President and CEO

Filipino 102,010 – “direct” 0.00%

Common Erramon I. Aboitiz Director

Filipino 188,287 – “direct” 1,418,951 – “indirect”

Record Owner: Bauhinia Management, Inc.

0.07%

Common Roberto E. Aboitiz Director

Filipino 170,281 – “direct” 636,078 - “indirect”

0.04%

5

Record Owner: Amayana Mgt. & Dev.

Common Justo A. Ortiz Director

Filipino 1,250 – “direct” 0.00%

Common Sabin M. Aboitiz Director

Filipino 1,019,562 – “direct” 0.04%

Common Washington Z. SyCip Independent Director

American 12 – “direct” 0.00%

Common Emily A. Abrera Independent Director

Filipino 1,000 – “direct” 0.00%

Common Lilian P. Cariaso Treasurer, EVP-CFO and CIO

Filipino 1,147,825 – “direct” 0.05%

Common Susan V. Valdez EVP-CEO Freight

Filipino 575,679 – “direct” 0.02%

Common Evelyn L. Engel EVP-CEO Passage and CRO

Filipino 575,679 – “direct” 0.02%

Common Miguel A. Camahort SVP-COO 2GO Solutions

Filipino 216,662 – “direct” 0.01%

Common Shelley U. Rapes VP-Information Technology

Filipino 144,118 – “direct” 0.01%

Common Magdalena A. Anoos VP-Materials Management Division

Filipino 383,786 – “direct” 0.02%

Common Maribeth L. Marasigan SVP & CRO-Business Support & 2GO Brand Management

Filipino 191,893– “direct” 0.01%

Common Norissa L. Ridgwell VP-Freight Operations

Filipino 162,721 – “direct” 24,517 – “indirect”

Record Owner: PCD Nominee Corporation (Filipino)

0.01%

TOTAL 4,880,934”direct”; 5,689,328“indirect” Preferred Sabin M. Aboitiz

Director Filipino 2,650 – “direct” 0.00%

TOTAL 2,650 – “direct”

Security Ownership of the Directors and Officers in the Registrant as a Group: Common is 10,570,262 shares; Preferred – 2,650 shares.

Voting trust holders of 5% or More

No person holds more than five per centum (5%) of a class under a voting trust agreement or similar arrangement.

Changes in Control

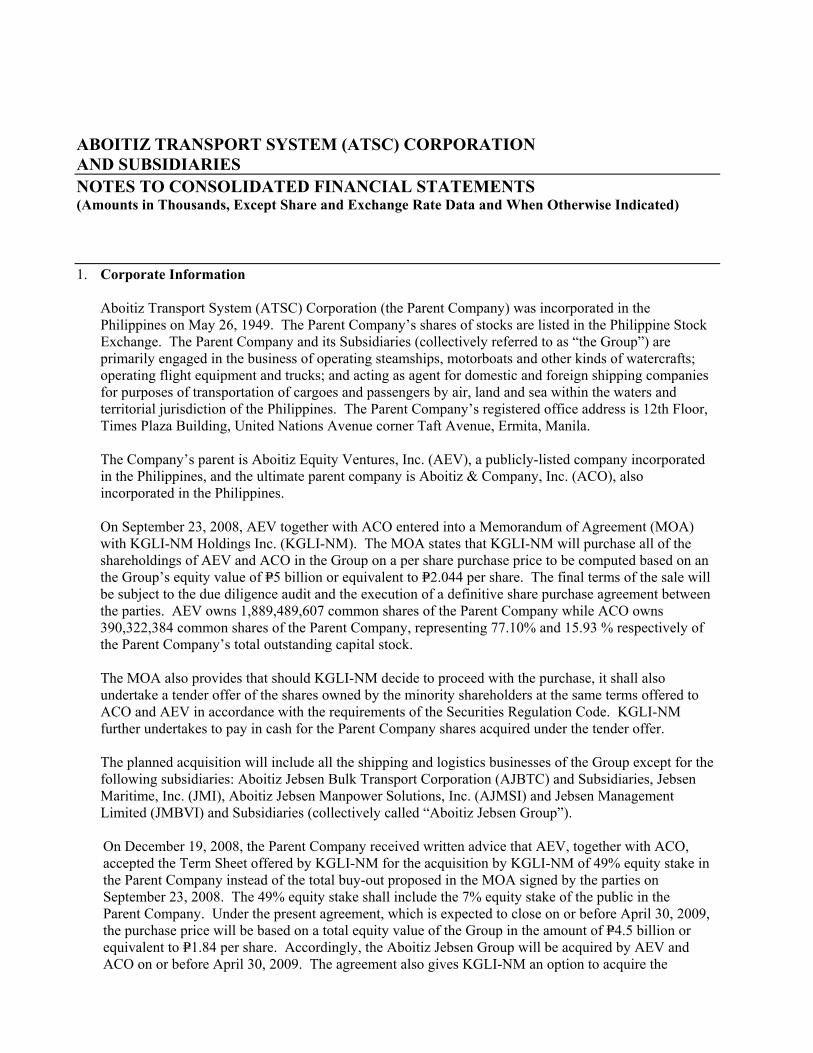

In September 2008, the major shareholders of ATS, AEV and ACO, accepted the unsolicited offer of KGLI-NM Holdings, Inc. (KGLI-NM) to purchase all of the shareholdings of AEV and ACO in ATS on a per share purchase price to be computed based on an ATS equity value of P5 billion or equivalent to P2.044 per share. AEV owns 1,889,489,607 common shares of ATS while ACO owns 390,322,384 common shares of ATS, representing 77.10% and 15.93 % respectively of the total outstanding ATS capital stock. This planned acquisition will include all of the shipping and logistics businesses of ATS except the Aboitiz Jebsen Group.

6

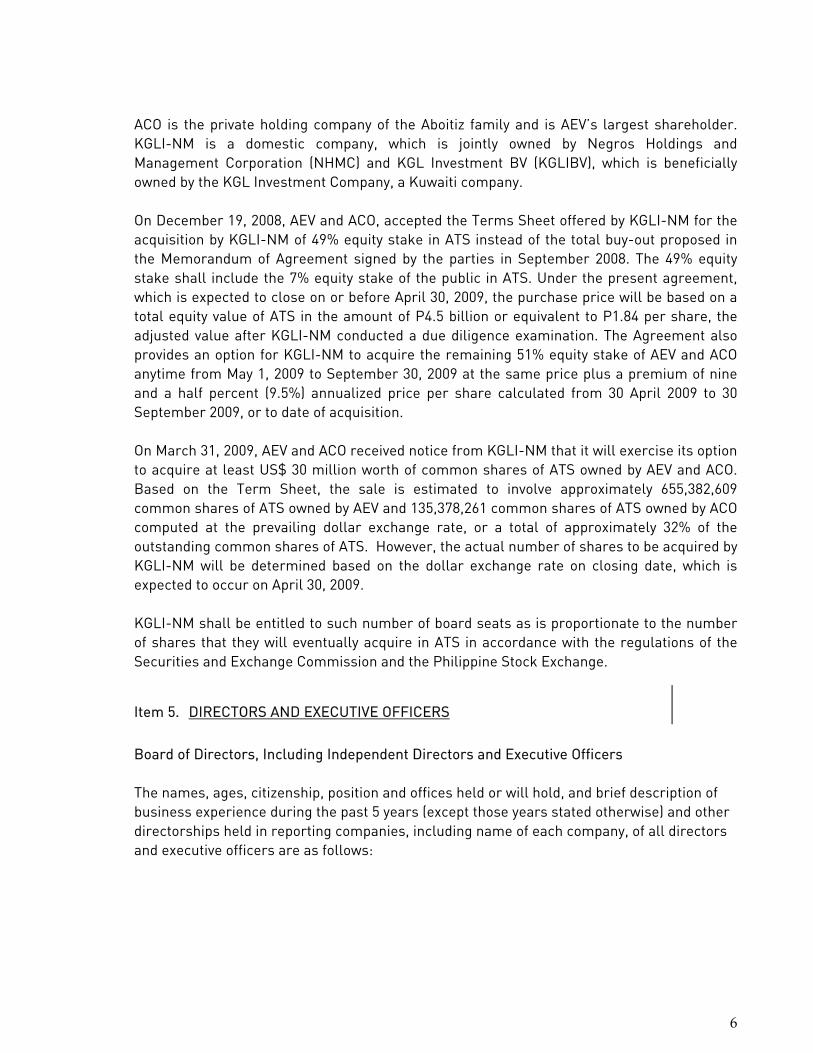

ACO is the private holding company of the Aboitiz family and is AEV’s largest shareholder. KGLI-NM is a domestic company, which is jointly owned by Negros Holdings and Management Corporation (NHMC) and KGL Investment BV (KGLIBV), which is beneficially owned by the KGL Investment Company, a Kuwaiti company. On December 19, 2008, AEV and ACO, accepted the Terms Sheet offered by KGLI-NM for the acquisition by KGLI-NM of 49% equity stake in ATS instead of the total buy-out proposed in the Memorandum of Agreement signed by the parties in September 2008. The 49% equity stake shall include the 7% equity stake of the public in ATS. Under the present agreement, which is expected to close on or before April 30, 2009, the purchase price will be based on a total equity value of ATS in the amount of P4.5 billion or equivalent to P1.84 per share, the adjusted value after KGLI-NM conducted a due diligence examination. The Agreement also provides an option for KGLI-NM to acquire the remaining 51% equity stake of AEV and ACO anytime from May 1, 2009 to September 30, 2009 at the same price plus a premium of nine and a half percent (9.5%) annualized price per share calculated from 30 April 2009 to 30 September 2009, or to date of acquisition. On March 31, 2009, AEV and ACO received notice from KGLI-NM that it will exercise its option to acquire at least US$ 30 million worth of common shares of ATS owned by AEV and ACO. Based on the Term Sheet, the sale is estimated to involve approximately 655,382,609 common shares of ATS owned by AEV and 135,378,261 common shares of ATS owned by ACO computed at the prevailing dollar exchange rate, or a total of approximately 32% of the outstanding common shares of ATS. However, the actual number of shares to be acquired by KGLI-NM will be determined based on the dollar exchange rate on closing date, which is expected to occur on April 30, 2009. KGLI-NM shall be entitled to such number of board seats as is proportionate to the number of shares that they will eventually acquire in ATS in accordance with the regulations of the Securities and Exchange Commission and the Philippine Stock Exchange.

Item 5. DIRECTORS AND EXECUTIVE OFFICERS

Board of Directors, Including Independent Directors and Executive Officers The names, ages, citizenship, position and offices held or will hold, and brief description of business experience during the past 5 years (except those years stated otherwise) and other directorships held in reporting companies, including name of each company, of all directors and executive officers are as follows:

7

DIRECTORS

Mr. Jon Ramon M. Aboitiz, 60 years old, Filipino, has served as Chairman of the Board of ATS since September 2002 and Director since 1996. Mr. Aboitiz is also Chairman of the Nominations Committee and the Remuneration and Compensation Committee and starting January 22, 2009, a member of the Company’s Audit Committee. He is also Chairman of the Board of Directors of Aboitiz Equity Ventures, Inc., Aboitiz Power Corporation and Aboitiz and Company, Inc. Other positions include: Chairman of the Board of Directors of Aboitiz Energy Solutions, Inc., Pilmico Foods Corporation, Philippine Hydropower Corporation, Aboitiz Jebsen Bulk Transport Corporation; Vice Chairman of the Board of Directors of Union Bank of the Philippines and Visayan Electric Company, Inc.; Director of Davao Light and Power Company, Inc., San Fernando Electric Light and Power Company, Inc., Cotabato Light and Power Company, Cotabato Ice Plant, Inc.; Chairman of the Board of Trustees of Aboitiz Foundation, Inc. and Trustee of the Ramon Aboitiz Foundation, Inc. He graduated with a degree of Bachelor of Science in Commerce major in Management from the University of Santa Clara, California, U.S.A. Mr. Bob D. Gothong, 53 years old, Filipino, has served as Vice Chairman of the Board of ATS since September 2002. Mr. Gothong is also a member of the Company’s Audit Committee. Chairman and Chief Executive Officer of One Wilson Place Holdings, Inc.; Director of Philippine National Oil Co.; Ramon Aboitiz Foundation, Inc., and Vice Chairman of Carlos A. Gothong Holdings, Inc. He graduated with a degree of Bachelor of Science in Commerce Major in Transportation and Utilities and Minor in Finance from the University of British Columbia, Vancouver, Canada. Mr. Enrique M. Aboitiz, Jr., 55 years old, Filipino, has served as President and Chief Executive Officer of ATS since May 1999 and Director since 1997. He is a member of the Nominations Committee and the Remuneration and Compensation Committee. He is also Director and Senior Vice President of Aboitiz and Company, Inc; Director and President of Aboitiz Jebsen Bulk Transport Corporation; Director of Aboitiz Equity Ventures, Inc. Aboitiz Power Corporation, Aboitiz One, Inc., Amanpulo Resorts, MacroAsia Corporation, E-Media Foundation, Pilmico Foods Corporation and Aboitizland, Inc. He graduated with a degree of Bachelor of Science in Business Administration (Major in Economics) from Gonzaga University, Spokane, Washington U.S.A. Mr. Erramon I. Aboitiz, 52 years old, Filipino, has served as Director of ATS since September 2002. He was an Audit Committee member until January 22, 2009. He is concurrently President and Chief Executive Officer of Aboitiz Equity Ventures, Inc., Aboitiz Power Corporation, Aboitiz and Company, Inc. and Philippine Hydropower Corporation; Chairman of the Board of Directors of Davao Light and Power Company, Inc., City Savings Bank, Subic EnerZone Corporation, San Fernando Electric Light and Power Company, Mactan Enerzone Corporation, Subic Enerzone Corporation, Balamban Enerzone Corporation and Pilmico

8

Animal Nutrition Corporation (formerly Fil-Am Foods, Inc.); Chairman and Chief Executive Officer of Hedcor, Inc. (formerly, Benguet Hydropower Corporation); Director and Vice President of Pilmico Foods Corporation; Director of Aboitizland Inc., UnionBank of the Philippines, Visayan Electric Company, Inc., Southern Philippine Power Corp., Aboitiz Energy Solutions, Inc., and Cotabato Light and Power Company; and President and Trustee of Aboitiz Foundation, Inc. He received a Bachelor of Science degree in Business Administration, major in Accounting and Finance from Gonzaga University, Spokane, U.S.A.

Mr. Roberto E. Aboitiz, 59 years old, Filipino, has been a Director of ATS since September 2002. He is an Audit Committee member. He is concurrently a Director and Senior Vice President of Aboitiz and Company, Inc.; Chairman and Chief Executive Officer of Aboitiz Construction Group, Inc., FBMA Marine, Inc. and Aboitizland, Inc.; Chairman of the Board of Directors of Balamban Enerzone Corporation, Mactan Enerzone Corporation, Cebu Industrial Park Developers, Inc. and Cebu Industrial Park Services, Inc.; Director of Aboitiz Equity Ventures, Inc., City Savings Bank, Cotabato Light and Power Company, Davao Light and Power Co., Inc., Tsuneishi Heavy Industries (Cebu), Inc., and Visayan Electric Company, Inc. He graduated from Ateneo de Manila University with a Bachelor of Arts degree in Behavioral Science. Mr. Justo A. Ortiz, 51 years old, Filipino, has served as Director of ATS since September 2002. He is also a Director of Aboitiz Equity Ventures, Inc. since 1994, Chairman and Chief Executive Officer of Union Bank of the Philippines. Prior to his stint in UBP, he was Managing Partner for Global Finance and Country Executive for Investment Banking at Citibank N.A. He graduated Magna Cum Laude with a degree in Economics from Ateneo de Manila University and completed his Masteral units in Business Administration in the same university. Mr. Sabin M. Aboitiz, 44 years old, Filipino, has been a Director of ATS since September 2002. His other positions include: President and Chief Executive Officer of Aboitiz One, Inc.; Director of Aboitiz and Company, Inc., Aboitiz Jebsen Bulk Transport Corporation, Reefer Van Specialist, Inc., and SN Aboitiz Power. Previous positions include: Marketing Manager, Assistant Vice President for Marketing, Vice President and Executive Vice President for TS Express, Senior Vice President and Chief Operating Officer of Aboitiz Air Transport Corporation. He graduated with a degree in Bachelor of Science in Business Administration, Major in Finance at Gonzaga University, Spokane, Washington U.S.A. Mr. Washington Z. Sycip, 87 years old, American, has been an Independent Director of ATS since 1996 and Audit Committee Chairperson since 2003. His other significant positions include: Founder and Chairman for 50 years - Sycip, Gorres and Velayo Group; Chairman Emeritus of the Board of Trustees and the Board of Governors of Asian Institute of Management; Chairman of the Board of Cityland Development Corp., Lufthansa Technik Philippines Inc., MacroAsia Corporation, and Steag State Power Inc.; Independent Director of Belle Corporation, Benpres Holdings Corporation, Commonwealth Foods, Inc., First

9

Philippine Holdings Inc., Global Business Holdings, Inc., Highlands Prime Inc., Philippine Hotelier Inc., Philamlife Inc., The PHINMA Group, and Stateland, Inc; He is also a Director of Philippine Airlines Inc. and Philippine National Bank. He graduated with a degree of Bachelor of Science in Commerce and Master of Science in Commerce from the University of Santo Tomas and further completed his Master of Science in Commerce from University of Columbia, New York, U.S.A.

Emily A. Abrera, 61 years old, Filipino, nominated as Independent Director of ATS since 2008. She is a member of the Company’s Compensation & Remuneration Committee and of the Nomination Committee. She is a Director of Bank of the Philippine Islands and Pioneer Insurance. She is the Chairman of the Cultural Center of the Philippines, and of CCI-Asia, the content-production company behind Living Asia Channel and Isla advocacy programs. She is President of the Foundation for Communication Initiatives and is a Trustee of Museo Pambata (Children’s Museum), Children’s Hour Inc., Philippine Board on Books for Young People and Philippine Eagle Foundation. She is a founding member of the Women’s Business Council. She has been a consultant and Chairman-Emeritus at McCann Manila from 2004 and non-executive Chairman of McCann World Group in the Asia-Pacific Region since 2008. She took up Mass Communication at Maryknoll College and Journalism at the University of the Philippines.

Atty. Helen G. Tiu, 48 years old, Filipino, has served as Corporate Secretary of ATS since September 2002. She is treasurer, corporate secretary and one of the managing directors of Lazaro, Bernardo, Tiu and Associates, Inc., a consultancy firm and practices law at H. G. Tiu Law Offices. Under H. G. Tiu Law Offices, she acts as corporate counsel, director, and/or corporate secretary of various clients. She is a certified public accountant and a member of the Philippine Bar. She received her Bachelor of Science in Business Administration and Accountancy (cum laude; 1981) and Bachelor of Laws (1987) from the University of the Philippines. In 1991, she obtained a Masters of Laws degree from Harvard University. Atty. Catherine R. Atay, 30 years old, Filipino, has served as Assistant Corporate Secretary of ATS since 2008. She also acts as the Corporate Secretary of various corporations of the Aboitiz group including Pilmico Animal Nutrition Corporation (formerly: Fil-Am Foods, Inc.), Davao Light and Power Corporation, Cotabato Light and Power Corporation, Aboitiz Construction Group and Metaphil International. Prior to joining the Aboitiz Group, Atty Atay was with Landicho and Associates Law Offices. She received her Bachelor of Science in Accountancy (cum laude; 1999) and Bachelor of Laws (2004) from the University of San Carlos.

EXECUTIVE OFFICERS Ms. Lilian P. Cariaso, 49 years old, Filipino, Treasurer, Executive Vice President - Chief Finance Officer, Corporate Information Officer since June 2004. She has been with the

10

Aboitiz group since 1979. Previous positions in ATS include: Director of SuperCat Fast Ferry Corporation and Senior Vice President and Chief Finance Officer of Aboitiz One, Inc. She graduated with degree in Bachelor of Science in Commerce, Major in Accounting (Summa Cum Laude) at University of San Carlos and earned her Master degree in Business Management at the University of the Philippines. Ms. Susan V. Valdez, 48 years old, Filipino, Executive Vice President - Chief Executive Officer of the Freight Division since January 2004. She has been with the Aboitiz group since 1981. Previous positions in ATS include: Treasurer, Executive Vice President - Chief Finance Officer, Corporate Information Officer. She graduated with a degree in Bachelor of Science in Commerce, Major in Accounting (Cum Laude) at St. Theresa’s College and earned her Masters degree in Management, Major in Business Management at the University of Philippines. She also completed the Program for Management Development at Harvard Business School, Boston, U.S.A.

Ms. Evelyn L. Engel, 56 years old, Filipino, Executive Vice President – Chief Resource Officer since May 1999, and Chief Executive Officer of the Passage Division since June 2004. Her other positions include Director of Catena Services, Inc. and SQL Wizard, Inc. She graduated with B.A. in Economics at St. Paul University.

Mr. Miguel A. Camahort, 46 years old, Filipino, Senior Vice President and Chief Operating Officer of the Express Division in Aboitiz One, Inc. since October 2004. He has been with the Aboitiz group since 1995. Previous positions in ATS include: Senior Vice President for Operations of Aboitiz One, Inc., Senior Vice President and Chief Operating Officer of Supply Chain Management; Senior Vice President and Chief Operating Officer of Freight Division. He graduated with a degree in Business Management and Economics from the Notre Dame College, Belmont, California. Mr. Rafael L. Sanvictores, 51 years old, Filipino, Senior Vice President –Hotel Operations since May 2006. He has been with the Aboitiz group since 1980. Previous positions in ATS include: Senior Vice President and Chief Operating Officer - SuperFerry Group; Senior Vice President and Chief Operating Officer - Passage Division and Assistant Vice President for Forwarding Operations, Sales and Aboitiz Inland Concarriers, Inc. He graduated with a degree in Bachelor of Science in Economics at San Beda College. Mr. Ramon G. Villordon, Jr., 56 years old, Filipino, President of SuperCat Fast Ferry Corporation since March 2002. He has been with the Aboitiz group since 1974. Previous positions in ATS include President of Philippine Fast Ferry Corporation. He is currently Director of United Southdockhandlers, Inc. and is one of the Commissioners of Cebu Ports Authority (private sector representative). He graduated with a degree in Bachelor of Science in Business Management at University of San Carlos.

11

Mr. Wilmer Jose A. Alfonso, 56 years old, Filipino, Vice President of Ports Services since May 2006. He has been with the Aboitiz group since 1971. Other positions in 2007 include: Chairman of the Board of Catena Services, Inc.; Chief Operating Officer of North Harbor Tugs Corporation; President of United South Dockhandlers, Inc. He is also Chairman of the Board of Attina Security Services, Inc. Previous positions in ATS include: Vice President and Chief Operating Officer of Passage Services Group; Vice President and Chief Operating Officer, President and Chief Operating Officer of WG&A SuperCommerce, Inc., President of Pilotage Integrated Services Corporation. Mr. Alfonso is a Certified Public Accountant. He graduated with a degree in Bachelor of Science in Commerce Major in Accounting at University of San Carlos. Ms. Magdalena A. Anoos, 52 years old, Filipino, Vice President of Materials Management since January 2003. She has been with the Aboitiz group since 1977. Previous positions in ATS include: Finance Vice-President of Strategic Support Center; Finance Vice-President of Aboitiz One, Inc. She graduated with a degree in Bachelor of Science in Commerce Major in Accounting (Cum Laude) at University of San Carlos. She also completed the Senior Executive Program at Columbia Business School, New York, USA.

Ms. Maribeth L. Marasigan, 46 years old, Filipino, Senior Vice President and Chief Resource Officer of Business Support and 2GO Brand Management since June 2008. She has been with the Aboitiz group since 1986. Previous positions in ATS include: Vice President of Projects and 2GO Brand Management; Vice President of Revenue Management; Vice-President of Aboitiz One, Inc. She graduated with a degree in Business Administration in Communication Arts, a consortium course from Saint Scholastica's College and De La Salle University. Ms. Charity Joyce S.D. Marohombsar, 42 years old, Filipino, Vice President of Customer Interaction Center since May 2003 and VP for RORO. She has been with ATS since 2003. Previous positions include: General Manager of Source One Asia an International BPO. She graduated with a degree in Bachelor of Arts at Ateneo de Naga.

Ms. Norissa L. Ridgwell, 53 years old, Filipino, Vice President of Freight Operations since October 2005. She has been with the Aboitiz group since 1994. Previous positions include: Vice President and Human Resource Director of ATS; Chief Operating Officer, Vice President for Sales and Marketing of Hapag Lloyd Philippines; and Head of JOSS Asian Feeders. She graduated with a degree in Bachelor of Science in Commerce Major in Management at Silliman University. Ms. Shelley U. Rapes, 50 years old, Filipino, Vice President of Information Technology since July 2005. She has been with the Aboitiz group since 1981. Previous positions include: Assistant Vice President–Information Technology and Information Services Manager of ATS. She graduated with a degree in Bachelor of Science in Mathematics (Cum Laude) from the

12

University of San Carlos, and finished the 3-month Management Development Program of the Asian Institute of Management. Ms. Annacel A. Natividad, 39 years old, Filipino, Vice President and Chief Finance Officer of the Passage Division since June 2005. She is also concurrently handling Risk Management Department since June 2007. She has been with the Aboitiz group since January 1998. Previous positions in ATS include: Assistant Vice President for Investor Relations, Corporate Finance, and the Finance Division of Passage Travel and Leisure. She finished her Masters in Business Administration from De La Salle University - Graduate School of Business and she graduated with a degree in Commerce major in Accounting from the University of Santo Tomas.

Mr. Oscar Y. Go, 58 years old, Filipino, Vice President of Sales-Special Accounts since May 2002. He has been with Aboitiz Transport System Corporation since May 2002. Prior to joining the company, he was Vice President of Lorenzo Shipping Corporation. He graduated with a degree in Business Management at Collegio de San Juan de Letran. Mr. Joel Jesus M. Supan, 51 years old, Filipino, Vice President of Security, Safety and Compliance since October 2004 which is also the year he joined ATS. He is a Founder and Proprietor of Stonewall Security Concepts; Director and President of Ethics Call System Inc., and Founder of Balikatan ng Mga Tanod Ng Ari-arian at Yaman (BANTAY). Previous positions include: Vice President and General Manager of Security Solutions of Solutions and Innovations Inc.; Estates Management Division Head of Moldex Group; Vice President for Training and Education of Independent Insights Inc., Naval Officer, Philippine Navy. He graduated with a degree in Bachelor of Science from the Philippine Military Academy in 1981. Nomination Committee and Nominees for Election as Members of the Board of Directors The incumbent directors will be nominated as members of the Board of Directors for the ensuing year (2009-2010).

In compliance with SEC Guidelines on the Nomination and Election of Independent Directors under SRC Rule 38, the Company Board created on February 26, 2003 a Nomination Committee. The current Nomination Committee is composed of the following directors: (1) Mr. Jon Ramon M. Aboitiz as chairman, (2) Mr. Enrique M. Aboitiz, Jr. as member and (3) Ms. Emily A. Abrera, an independent director, as member. The Nomination Committee had promulgated the guidelines which govern the conduct of the nomination of the members of the Company Board. It had pre-screened and short listed all candidates and came up with the following individuals as nominees for independent directors for the ensuing year (2009-2010): (1) Mr. Washington Z. Sycip as nominated by Mr. Erramon I. Aboitiz (2) Ms. Emily A. Abrera as nominated by Mr. Enrique M. Aboitiz Jr.

13

The nominating persons are not related to the nominees within the fourth degree of consanguinity. Further, the Commission approved last July 20, 2005 the Company’s Amended By-Laws incorporating the procedures for the nominations and elections of Independent Directors to be followed shall be in accordance to Rule 38 of the Securities Regulation Code. Period in Which Directors and Executive Officers Should Serve The directors and executive officers should serve for a period of one (1) year and until the election and qualification of their successors. Terms of Office of a Director The nine (9) directors shall be stockholders and shall be elected annually by the stockholders owning a majority of the outstanding common shares of the Registrant for a term of one (1) year and shall serve until the election and qualification of their successors. Any vacancy in the board of directors other than removal or expiration of term may be filled by a majority vote of the remaining members thereof at a meeting called for that purpose if they still constitute a quorum, and the director or directors so chosen shall serve for the unexpired term.

Significant Employees The Corporation considers the contribution of every employee important to the fulfillment of its goals. Family Relationships Messrs. Jon Ramon Aboitiz and Roberto E. Aboitiz are brothers and are, thus, related to each other within the fourth degree of consanguinity. Messrs. Erramon Aboitiz, Enrique M. Aboitiz, Jr. and Sabin M. Aboitiz are brothers and are, thus, also related to each other within the fourth degree of consanguinity. They are cousins to Messrs. Jon Ramon Aboitiz and Roberto E. Aboitiz and are therefore related within the fourth degree of consanguinity. Other than the ones that are disclosed above, there are no other family relationships known to the Registrant.

14

Involvement in Certain Legal Proceedings To the knowledge and/or information of ATS, none of its nominees for election as directors, the present members of its Board of Directors or its executive officers, is presently or during the last five (5) years been involved in any legal proceeding in any court or government agency on the Philippines or elsewhere which would put to question their ability and integrity to serve ATS and its stockholders. With respect to its nominees for election as directors, the present members of its Board of Directors and its executive officers, the Company is not aware that during the past five (5) years up to even date of: (a) any bankruptcy petition filed by or against any business of which such person was a general partner or executive officer either at the time of the bankruptcy or within two years prior to that time; (b) any conviction by final judgment of such person in a criminal proceeding, excluding traffic violations and other minor offenses; (c) such person being subject to any order, judgment, or decree, not subsequently reversed, suspended or vacated, of any court of competent jurisdiction, domestic or foreign, permanently or temporarily enjoining, barring, suspending or otherwise limiting such person’s involvement in any type of business, securities, commodities or banking activities; and (d) such person being found by a domestic or foreign court of competent jurisdiction (in a civil action), the Commission or comparable foreign body, or a domestic or foreign exchange or other organized trading market or self regulatory organization, to have violated a securities or commodities law or regulation and the judgment has not been reversed, suspended, or vacated. Certain Relationships and Related Transactions In the ordinary course of business, the Registrant has transactions with fellow subsidiaries, associates, and other related companies consisting of ship management services, charter hire, management services, purchases of steward supplies, availment of stevedoring, arrastre, trucking, rental and repair services. The Registrant needs these services to complement its services to the freight and passage customers. The identification of the related parties transacting business with the Registrant and how the transaction prices were determined by the parties are discussed in the Note 21 of the consolidated financial statements. The Registrant will continue to engage the services of these related parties as long as it is economically beneficial to both parties. The Corporation has no transaction during the last two years or proposed transaction to which it was or is to be a party in which any of its directors, officers, or nominees for election as directors or any member of the immediate family of any of the said persons had or is to have a direct or indirect material interest.

15

Resignation or Refusal to Stand for Re-election by Members of the Board of Directors No Director has resigned or declined to stand for re-election to the board of directors since the date of the last annual meeting of the Registrant because of a disagreement with the Registrant on matters relating to the Registrant operations, policies and practices.

Item 6. COMPENSATION OF DIRECTORS AND EXECUTIVE OFFICERS

The following table summarizes certain information regarding compensation paid or accrued during the last three fiscal years and to be paid in the ensuing fiscal year to the Registrant Chief Executive Officer and each of the Registrant four other most highly compensated executive officers:

SUMMARY OF COMPENSATION TABLE

Amounts in Thousands of Pesos (‘000s) SALARY BONUS

(13th and 14th Months Pay)

OTHER COMPENSATION

TOP FIVE HIGHLY COMPENSATED EXECUTIVES: ENRIQUE M. ABOITIZ JR. – CHIEF EXECUTIVE OFFICER EVELYN L. ENGEL – CHIEF EXECUTIVE OFFICER –

PASSAGE AND CHIEF RESOURCE OFFICER

SUSAN V. VALDEZ – CHIEF EXECUTIVE OFFICER – FREIGHT

LILIAN P. CARIASO – CHIEF FINANCE OFFICER AND CORPORATE INFORMATION OFFICER

MIGUEL A. CAMAHORT – SVP–COO 2GO SOLUTIONS

2007 17,395 2,989 - 2008 19,728 3,288 -

All above named officers as a group

Projected 2009

22,372 3,729 -

2007 16,175 2,696 - 2008 21,648 2,214 -

All officers and directors as group unnamed

Projected 2009

23,911 2,545 -

The Company has no significant or special arrangements of any kind as regard to the compensation of all officers and directors other than the funded, noncontributory tax-qualified retirement plans covering all regular employees. All of ATS directors effective February 1, 2008 receive a monthly allowance of P 80,000.00 per month. In addition, each director receives P 30,000 per diem for every Board meeting attended. Except for benefits under the regular company retirement plan, which by its very nature will be received by the officers concerned only upon retirement from the Company, the above-

16

mentioned directors and officers do not receive any profit sharing nor any other compensation in the form of warrants, options, bonuses, etc. Likewise, there are no standard arrangements that compensate directors directly or indirectly, for any services provided to the Company either as director or as committee member or both or for any other special assignments.

Item 7. INDEPENDENT PUBLIC ACCOUNTANTS

The accounting firm of Sycip, Gorres, Velayo & Company (SGV) has been ATS' Independent Public Accountant since year 1977. This is reckoned to be the approximate date based on the available records. Representatives of SGV will be present during the annual meeting and will be given the opportunity to make a statement if they so desire. They are also expected to respond to appropriate questions if needed. The Audit Committee is composed of three Board members, namely, Washington Z. Sycip, chairperson and Jon Ramon R. Aboitiz and Bob D. Gothong, members.

In its regular board meeting on April 23, 2009, the Board of Directors approved a resolution to submit for the approval of the stockholders during the Annual Stockholders’ Meeting a proposal to delegate to the Board of Directors the authority to appoint the Company’s external auditors for 2009. The proposal is intended to give the Board Audit Committee sufficient time to evaluate the different auditing firms who have submitted engagement proposals to act as ATS' external auditor for 2009. In compliance with SEC guidelines on the rotation of external auditors under its SRC Rule 68, Paragraph 3(b)(iv), ATS has already adopted and incorporated the said guidelines in its Code of Corporate Governance. Mr. Ladislao Z. Avila Jr. has been the signing partner since fiscal year 2006. He will be replaced starting fiscal year 2011 in compliance with the five years rotation requirement under SEC Memorandum Circular No. 8 Series of 2003. (1) External Audit Fees and Services

Estimates for

December 31, 2009 Year ended

December 31, 2008 Year ended

December 31, 2007 Audit Fees P 1,240,000 P 1,240,000 P 1,240,000 Audit-Related Fees 300,000 300,000 300,000 All Other Fees 60,000 60,000 60,000

TOTAL P 1,600,000 P 1,600,000 P 1,600,000

17

Audit Fees This represents professional fees for financial assurance services rendered for the Company’s Annual Financial Statements, review and opinion for SEC Annual Report. Audit-Related Fees This represents professional fees for technology and security risk services rendered by the external auditor in connection with the Audit on Company’s Annual Financial Statements. All Other Fees This represents fees for services rendered in reviewing and issuing opinion with regards to the Company’s annual reportorial requirement with Maritime Industry Authority (MARINA). Audit services provided to the Company by external auditor, SGV & Co. have been pre-approved by the Audit Committee. The Audit Committee has reviewed the magnitude and nature of these services to ensure that they are compatible with maintaining the independence of the external auditor. (2) Changes in and Disagreements With Accountants on Accounting and Financial

Disclosure There was no event in the past years where SGV and the Company had any disagreements with regard to any matter relating to accounting principles or practices, financial statement disclosure or auditing scope or procedure.

C. OTHER MATTERS

Item 8. ACTION WITH RESPECT TO REPORTS

The minutes of the last annual stockholders’ meeting held on May 22, 2008 and the Annual Report of Management for the year ended December 31, 2008 will be submitted to the stockholders for their approval. Item 9. MATTERS NOT REQUIRED TO BE SUBMITTED All corporate actions to be taken up at the annual stockholders’ meeting this May 28, 2009 will be submitted to the stockholders of the Registrant for their approval in accordance with the requirements of the Corporation Code.

18

Item 10. OTHER PROPOSED ACTIONS Other proposed action that is for approval and ratification by stockholders representing at least two-thirds (2/3s) of the Registrant’s outstanding capital stock is for the Registrant to mortgage corporate assets, to act as guarantor and/or surety, from time to time, for the benefit of the Registrant’s subsidiaries and affiliates. Also, the following agenda are also for approval and ratification by stockholders representing at least a majority of the outstanding voting capital stock of the Registrant:

a) Ratification of all acts of the Board of Directors and Management Committee for the period covering March 28, 2008 through March 26, 2009 adopted primarily in the ordinary course of business (including those which have been the subject of previous disclosures to the Securities and Exchange Commission and the Philippine Stock Exchange during said period), such as:

i. treasury matters related to the opening of accounts (including joint accounts),

transferring funds to employees payroll account through debit advice, and other appropriate transactions with banks and non-bank financial intermediaries;

ii. appointment and/or removal of signatories to operate accounts with banks and non bank financial institutions, and amendments thereto;

iii. approval for the availment by the Registrant of certain credit facilities, loans, bills purchase lines, foreign exchange lines, omnibus line, credit accommodations, check cutting services, products, and/or electronic facilities/systems of various banks and/or non-bank financial institutions;

iv. authority given to the Registrant’s subsidiaries and/or affiliates to avail of credit facilities extended to the Registrant;

v. authority given to the Registrant to act as a guarantor or surety, and/or to mortgage, pledge or hypothecate its properties for the benefit of its subsidiaries and/or affiliates in connection with loans or credit facilities extended to such subsidiaries and/or affiliates;

vi. authority given to the Registrant to apply with the appropriate utility companies for the Registrant’s power and water utility needs;

vii. approval for the acquisition (including to participate in related bidding process, if applicable), lease, bareboat charter, charter (including extension thereof), financing, transfer, assignment, rent, mortgage, repair and maintenance, drydock, and/or disposition of vessels, trailers and other real and/or personal properties of the Registrant (including to lease out spaces on board the Registrant’s vessels to allow the installation of antenna facilities);

19

viii. authority to secure, on full settlement of the Registrant’s obligations, the release and discharge of mortgages that were constituted over the Registrant’s assets in favor of the lender;

ix. authority to enter into certain arrangements with the Development Bank of the Philippines in connection with loans extended to subcontractors of the Registrant provided the Registrant does not in any way or manner assume any obligation to act as guarantor and/or surety for the benefit of such subcontractors;

x. appointment, election, and/or removal of corporate officers and agents as well as members of the Registrant’s board committees;

xi. appointment of lawyers and/or attorneys-in-fact in connection with legal proceedings affecting the Registrant and/or its assets (including related settlement proceedings);

xii. approval of the consolidated audited financial statements of the Registrant for the year ended December 31, 2008;

xiii. approval for securing temporary advances from the Registrant’s parent company and members of the Aboitiz Group of Companies to meet working capital requirements of the Registrant;

xiv. approvals related to regulatory proceedings concerning the Registrant and/or its assets that were before the relevant government offices such as the Intellectual Property Office, Board of Investments, the Bureau of Customs, the Maritime Industry Authority, the Philippine Ports Authority, the Bureau of Internal Revenue, the Philippine Stock Exchange, the Securities and Exchange Commission and/or relevant offices of city governments (e.g., Office of the Building Official, City Zoning Department);

xv. appointment of broker in connection with transactions involving shares of third party companies registered in the name of the Registrant; and

xvi. appointment of Registrant’s proxy at the stockholders’ meetings of its subsidiaries and/or affiliates.

b. Minutes of Stockholders Meeting held last May 22, 2008.

During the Annual Stockholders Meeting held last May 22, 2008, stockholders representing at least two-thirds of the outstanding capital stock of the Corporation approved the following:

1) Amendment to the Seventh Article of the Articles of Incorporation,

reclassifying 70,343,670 redeemable preferred shares into common shares so that the authorized capital stock of the Registrant remains at P4,074,908,000.00 but shall consist of 4,070,343,670 common shares with a par value of P1.00 per share and 4,564,330 redeemable preferred shares with a par value of P1.00 per share;

20

2) Revocation of previous resolutions decreasing the authorized capital stock to P4,004,564,330.00 as a result of the conversion of 70,343,670 redeemable preferred shares into common shares and retiring the same.

3) Approval to mortgage corporate assets, to act as guarantor and/or surety

from time to time, for the benefit of the Company’s subsidiaries and affiliates.

Item 12. VOTING PROCEDURES As to each matter, which is to be submitted to a vote of security holders, furnish the following information:

(a) Vote required for Approval

The affirmative vote of stockholders representing at least a majority of the outstanding voting common shares of the Registrant is required for the approval of the following matters:

i. Minutes of Previous Annual Stockholders’ Meeting;

ii. Management Annual Reports for the preceding year;

iii. Election of the Board of Directors;

iv. All Acts and Resolutions of the Board of Directors and Management since March 28, 2008; and

v. Delegation to the Board of Directors of the authority to Appoint the External Auditors of the Registrant.

The affirmative vote of stockholders representing at least two-thirds (2/3s) of the outstanding capital stock of the Registrant is required to authorize the Registrant to mortgage corporate assets, to act as guarantor and/or surety, from time to time, for the benefit of its subsidiaries and affiliates. (b) Method by which Votes will be counted

At each meeting of the stockholders, every stockholder shall be entitled to vote in person or by proxy, for each share of stock held by him, which has voting power upon the matter in question. As provided in Section 7, Article II

21

of the By-laws of the Registrant, except upon demand by any stockholder, the votes upon any question before the meeting, except with respect to procedural questions that shall be determined by the Chairman of the meeting, shall be by viva voce or show of hand.

The method and manner of counting the votes of shareholders shall be in accordance with the general provision of the Corporation Code of the Philippines. The counting of votes shall be witnessed by representatives from the Company’s external auditor, Sycip Gorres Velayo & Company (SGV), stock and transfer agent Securities Transfer Services, Inc. (STSI) and the Company’s Corporate Secretary.

22

SIGNATURE PAGE

After reasonable inquiry and to the best of my knowledge and belief, I certify that the

information set forth in this report is true, complete and correct. This report is signed in the

City of Manila on April 14, 2009.

Lilian P. Cariaso Corporate Information Officer

23

2008 MANAGEMENT REPORT

1 I. Consolidated Audited Financial Statements The Consolidated Audited Financial Statements for the year ended and as of December 31, 2008 are attached to this report. II. Disagreements with Accountants on Accounting and Financial Disclosures There was no event in the past years where Sycip Gorres Velayo and Company and the Corporation had any disagreements with regard to any matter relating to accounting principles or practices, financial statement disclosure or auditing scope or procedure III. Management’s Discussion and Analysis Key Performance Indicators (KPI) The following KPI’s are used to evaluate the financial performance of ATS and its subsidiaries:

Revenues – ATS revenues are mainly composed of freight and passage revenues and they are recognized when the related services are rendered. Total Revenue in 2008 is P10.3 billion compared to P8.2 billion in 2007.