attitude of bank personnel and customers towards new...

TRANSCRIPT

CHAPTER SIX

ATTITUDE OF BANK PERSONNEL AND CUSTOMERS

TOWARDS NEW PRODUCTS

Society and culture are external factors that influence consumer

behaviour, whereas psychological and personal factors are those that

operate from within. The consumer behaviour is strongly influenced by

learning. Learning is the process of acquiring knowledge and

information. A vast majority of perception is acquired through learning.

But learning does not always mean bookish knowledge. A man learns

through many sources and from many things. In a true sense, learning is

a process in which total functions are altered and rearranged to make

them more useful. Attitude represents a person's feeling towards a

particular object or situation. In the banking industry, a study of attitude

is found important provided the sources used for the study are reliable.

The information regarding the innovative peripheral services if

transmitted through reliable sources would simplify the motivation

process.

Motivation is an internal emerging force that orients a person's

activities towards satisfying needs or achieving goals'. The motivation

process starts with an unsatisfied need. That need is the part that

23 1

initiates the chain of events leading to a certain behaviour. For banking

organisation it is not :So difficult, provided the services promised are

made available to the users without any distortion. The banking

organisation needs to innovate their services since this simplifies the

process of motivation.

Conditioning is considered to be a way of learning. The

conditioned response establishes a behavioural pattern but of temporary

nature. It may disappear if the reinforcement is not upto the mark. The

banking organisation needs to assure their customers that the services

offered to them are internationally competitive and world class. Social,

economic and psychological factors cannot remain static due to the

influence of internal and external factors. This compels the bank

professionals to be vigilant and to conduct intensive studies on the

changing, emerging trend.

Psychological factor is also an important element which

influences customers in dealing with the bank. Hence these factors

were also taken for study. Important factors taken for study are

awareness of the product, motivation and conditioning. The data

furnished in Tables 6.1 and 6.2 disclose awareness of the product in

location wise and region wise.

Table 6.1

Location of bank arid Bank personnel's response to customer's

behaviour on Psycl~iological factors - awareness of the product

I - I I I

Source: Field survey Pearson Chi-square: 3,59261, df=4, p=,463951

(Figures in percentage)

Table 6.2

Location of Bank Medium

Urban 62.22

Semi-urban 50.00

Rural 57.78

Region wise bank personnel's response to customer behaviour on

Psychological factor - awareness of the product

Low

18.89 20.00

18.89

Total

100 100

100

\- ..- r-*.

Pearson Chi-square: 13,3081, dg4, p=,009874

Northern 18.89

Central 36.67

Southern 16.67

Total 24.07

The data contained in the Table reveals that there is no

-

- 1 High

statistically significant relation between awareness of the product by the

Low Medium

Source: Field survey

57.78

51.1 1

61.11

56.67

customers and customers' behaviour on banks. The Table also discloses

Total

that the influence of the awareness of the product has 'Medium' impact

23.33

12.22

22.22

19.26

100

100

100

100.00

in customers' behaviour on banks. Among the locations, the urban area

comes first in the category of 'Medium'.

In region wise analysis also the Table reveals that there is

statistically significant relation between awareness of product and

behaviour of customeris in region wise. Respondents from bank

personnel opined that influence on customer behaviour due to awareness

of the product is 'medium'. And among regions, the southern region

comes first in this regard. Interaction with bank personnel revealed that

regular customers are ready to accept bank products/services only after

making thorough verification because it will affect their goodwill in the

market.

Table 6.3

Location of bank and Bark personnel's response to customers behaviour

on Psychological factors- motivation

1 Urban 1 4.44 1 52.22 1 43.34 1 100 1

(Figures in percentage)

1 Semi-urban 1 7.78 1 38.89 1 53.33 1 ;:: Rural 13 33 26.67 60 .OO -- Total 8.52 39.26 52.22 100.00

Source: Field survey Pearson Chi-square 14.1770, df=4, p=,006759

[-rank7 - 2 7 ~ e d i u m Low Total

Table 6.4

Region wise bank personnel's behaviour on Psychological factor- Motivation

The second psychological factor taken for study is motivation.

(Figures in percentage)

The data contained in Tables 6.3 and 6.4 give the result of the study

--

Northern 13.33 Central 10.00

Southern Total --

location wise and region wise. Chi-square at 5 per cent level and 'p'

value reveals that the relation between motivation and customer

Source: Field survey Pearson Chi-square 55,2461, df=4, p=,000000

- Medium

61.44 31.11 22.22 39.26

behaviour in location wise is statistically significant. The Table also

reveals that more than 52 per cent of the bank personnel are of the view

Low 22.23 58.89 75.56 52.22

that motivation has 'low' impact on customers' behaviour towards

Total 100 100 100

100.00

banks. Among the locations, 'rural area' comes first (60 per cent) in this

regard.

In region wise analysis also, the information in the Table reveals

that there is statistically significant relation between motivation and

customers' behaviour. The data contained in the Table further reveals

that in region wise the influence of motivation on customer behaviour is

'low'. And among the regions, the southern region comes first in this

regard.

Table 6.5

Location of bank and Bank personnel's response to customer's

behaviour on Psycholo~ical factors - conditionina - - - - -- -- - - --- - D

(Figures in percentage)

, Pearson Chi-square: 5,50000, df=4, p=,239756

-

'Table 6.6

Urban Semi-urban 10.00

Rural 5.56 -- Total

Region wise bank personnel's response to customer behaviour on

Psychological factor - Conditioning

Source: Field survev

Medium 23.33 15.56 15.56 18.15

The third factor taken for study is 'conditioning'. The data

contained in Tables 6.5 and 6.6 gives the outcome of the study in

location wise and region wise. In location wise statistically significant

relation exists between conditioning and location wise behaviour of the

customers. Further, bank personnel opined that conditioning of a

product of the bank has 'low' influence on the behaviour of the

Low 73.34 74.44 78.88 75.55

(Figures in percentage)

Total 100 100 100

100.00

Re ion Northern 13.33 Central

Southern Total 6.30

Source: Field survey Pearson Chi-square: 15,3139, dt=4, p=,004098

Medium 20.00 21.11 13.33 18.15

Low 66.67 74.45 85.56 75.55

Total 100 100 100

100.00

customers. Among the locations, this impact is more than 78 per cent in

rural areas and more than 70 per cent in other locations also. In region

wise analysis the Table reveals that chi-square value at 5 per cent

significant level and 'p" value reveal statistically significant relation

exists between conditioning bank products and customers' behaviour.

As per the Table, more than 75 per cent of the bank personnel opined

that conditioning has very little influence on customer's behaviour.

Furthermore, the southern region comes first in this regard.

Similar questions were asked to customers directly to assess their

views about the influence of psychological factors. The data furnished

in Tables 6.7 and 6.8 give:s the outcome of the study.

Table 6.7

Location wise influence of psychological factors on customer in

dealing with bank- awareness of product

(Figures in percentage) -~ -

o a t High -- Medium Low Total

Semi-urban

Rural 9.00 54.67 36.33

Source: Field Survey Pearson Chi-square: 17,8746, dl=4, p=,001308

Table 6.8

Region wise influence of psychological factors on customers in

dealing with bank - awareness of the product

1 Central 1 6.67 1 56.00 1 37.33 1 100 1

(Figures in percentage) I H i g j Low Total

I Southern / .34 1 38.33 1 61.33 1 100 1

Northern 17.67 100

Pearson Chi-square: 143,036, df=4, p=.000000

Total

Inorder to assess whether there is any statistically significant

relation between awareness of the product and customers' attitude

7.44

towards banks, chi-square value at 5 per cent significant level and 'p'

--

value were calculated and the outcome of the calculation discloses that

J 53.78

the relation is statistically significant. The Table further states that

among the customers from three location more than 53 per cent are of

Source: Field Survey

the view that the influence on customers' behaviour is 'Medium', and

38.78

among the locations, the urban area comes first in this regard.

100.00

Chi-square value and 'p' value reveal that statistically significant

relation exists between the awareness of the product and customers'

behaviour on banks. The Table further shows that the influence of

customers' behaviour due to awareness of the products is 'Medium'. It

is also clear from the Table that among the regions the Northern Region

comes first in this regard.

As was the case ,with bank personnel, the second psychological

factor taken for study with customers was 'motivation'. Data contained

in Tables 6.9 and 6.10 reveal the outcome of the study.

Table 6.9

Location wise influence of psychological factors on customer in

dealing with bank - motivation

(Figures in percentage)

Urban 1 1.67 1 50.00 1 48.33 1 100 / Location

Semi-urban 1 1.67 1 50.33 1 48.00 1 100 1 Rural 1 3.67 1 63.00 1 33.33 1 100 1

High

Pearson Chi-square: 19,6667, d+4, p=,000582

Table 6.10

Region wise influence of psychological factors on customers in

dealing with bank- motivation

(Figures in percentage)

- Medium

Total

I

Total 2.33 -- 1 43.23 100.00

Low

Source: Field Survey 2.33

Region High

Central --

2.00

I - I I I I

Source: Field Survey Pearson Chi-square: 35.4424. dF=4. p=,000000

Total

54.44

Medium 47.00

48.33

68.00

43.23

Low 49.67

50.00

30.00

100.00 I

Total 100

100

100

The chi-square value and 'p' value reveal that statistically

significant relation exists between motivation and influence on

customers' behaviour. The Table also reveals that the influence of

motivation on customer behaviour is medium. And among locations,

rural areas comes first (63 per cent) in this regard.

In region wise also, statistically significant relation is exposed at 5

per cent level of' significance. Furthermore, the influence of motivation

on customers' dealings with bank is 'Medium' and among the regions,

the southern region comes first in this regard.

Table 6.1 1

Location wise influence of psychological factors on customer in

dealing with bank- conditioning

(Figures in percentage)

Semi-urban 2.67 10.33 87.00

Rural 1.33 22.33 76.34

Total 1.67 14.44 83.89 100.00 .

Source: ~ i z d Survcy Pearson Chi-square: 25,2940, df=4, p=,000044

Table 6.12

Region wise influence of psychological factors on customers in

dealing with bank - conditioning

(Figures in percentage)

I Central ; 0.33 1 11.00 1 88.67 1 100 1 Northern

/ Southern 1 1.00 1 5.00 1 94.00 1 100 1

Low

69.00

Conditioning is the final psychological factor taken for study.

Total

100

I Total / 1.67 1 14.44 ---

83.89

The data furnished in Tables 6.1 1 and 6.12 give the results of the study

~100.00 I

in location wise and region wise. Location wise analysis by chi-square

Source: Field Survey Pearson Chi-square: 79,0923. df=4, p=,000000

test and calculating 'p' value reveals that there is statistically significant

relation between conditioning a bank product and customer behaviour.

The Table further reveals that 83.89 per cent of customers are of the

view that the influence of conditioning on customers' behaviour is low.

More than 75 per cent is all locations have opined in the same way.

Region wise analysis was also conducted and it was found that

statistically significant relation exists between conditioning service of

the bank and customer behaviour. More than 83 per cent of the

customers opined that the influence of conditioning on customer

behaviour is 'low'. Among the regions, the southern region comes first

in this regard.

pp~~

Employees Customers Factors

Social

Medium Medium Medium Medium

1 Age ( Medium 1 Medium 1 Medium 1 Medium ( Status of the family

Opinion leaders

/ Economic 1 I 1 1 1 I I I

H i g h High High 1 High

Expenditure

I Psychological factors I I I I I I I

Motivation Low 1 Medium I Medium

I Conditioning / Low I Low I Low I Low I

Figure 6.1. Influence of different factors on bank marketing

Threc major factors taken for study are social, economic and

psychological. In social hctors, except opinion leaders, influence of all

other factors are medium both in region wise and location wise and also

242

by bank personnel and customers. In the case of economic factors the

level of income and saving is high in location wise and region wise and

also among bank personnel and customers, but in the case of

expenditure, the employee's point of it is 'low' but 'medium' in the case

of customers. Among the psychological factors, awareness of the

product is 'medium' in location wise and region wise and also among

bank personnel and customers. As a factor, motivation is low as far as

the employees are concerned but it is medium for customers in location

wise and region wise. In the case of conditioning it is 'low' for all cases

i.e. both for employees and customers and also in location wise and

region wise.

Promotion of Bank Marketing

It is a fact that banking services have witnessed a number of

turning points. The perception of customer services and customer

satisfaction is now found substantially changed. The sophisticated

information technologies have started showing their influence on the

quality of' banking services. '['he promotional measures are sizably

influenced by the emergrng new trends in the development and use of

new generation of information technologies. The banking organisations

using advanced and sopt~isticated technologies have been successfbl in

243

establishing an edge over the banks managed manually. Big budgets for

promotion are not the basis for success. It is much more impact

generating, proactive and productive.

Promotion includes all marketing activities aimed at stimulating

demand and demand can be stimulated by communicating with market2.

Thus the genesis of promotion or promotional efforts lies in effectively

communicating with the market. The word communication is derived

from a Latin word which means 'to share' and more fundamentally from

the rootword 'communize', which means common communication

involving sharing specific message with a target audience3.

Sorrels defined communication as "a process of transmitting

meaning through written, oral and non-verbal message4". The process

of communication can be illustrated by figure 6.2.

Receiver Branch Customer

Figure 6.2. The process of communication

244

The communication has five elements. The sources is the

originator of the promotion. In terms of promotion strategy the source is

the bank or its branch, which desires to transmit some idea to its

customers through any vehicle that is verbal or non-verbal. The

message is the idea being communicated. It may be the scheme at its

theme. The vehicle is the means of carrying the message from the

sources to the receiver i.e. bank or its branches to the customer or

customers. The vehicle may be a person or impersonal mode like

television, newspaper and radio.

The receiver is the customer or customers to whom messages are

directed. Feedback is the signal received by the sender from the

receiver indicating the effect of the message. In promotion, all forms of

process of communication are made use of. The purpose of promotion

is to convince and compete through communication and according to

Rachrnan and Romano promotion is to 'inform and remind individuals

and persuade them to accept, recommend or use a product, service or

idea5. Promotion can be personal and non-personal. Inorder to achieve

the maximum effect of promotion, in a particular target market a

combination of various promotional tools are applied which is

commonly known as promotional mix.

245

In the fortnulation of marketing mix, the bank professionals are

also supposed to blend the promotion mix in which different

components of promotion such as advertising, publicity, sales

promotion, word of month promotion, personal selling and

telemarketing are given due weightage. The different components of

promotion help bank professional in promoting the bank business.

Advertising

The American Marketing Association defines advertising as,

"placement of announcement and persuasive messages in time or space

purchased in any of ihe mass media by business firms, non-profit

organisations, Government agencies and individuals who seek to inform

andor persuade members of a particular target market or audience about

their products, services, organisations or ideas6". In other words, the

goal of advertising is to inform, influence and persuade the target

market.

Advertisements have costs and therefore they must contribute to

the business growth. According to Daniel Starch, a good advertisement

must be seen, read, heard, believed, remembered and acted upon by the

target audience as its objectives are to create awareness, exposure,

bringing attitudinal change in the target and ultimately increase in sales7.

246

Message generation and selection of the theme are crucial in advertising

strategy.

There are four general advertising goals for all financial

institutions.

- To stimulate increased awareness and use of profitable

products and sources.

- To achieve a diversified financial base by attracting a steady

influx of new customers including small business, corporation

of all size and individuals.

- 'I'o promote special events such as the opening of a new branch

and

- To promote a favourable public reaction to the bank and to

issues affecting banks8.

Special goals must be set when initiating any advertising

campaign, especially when large amounts are to be spent. These goals

should support the overall marketing goals of the bank.

Philip Kotler defines, a product is anything that can be offered to

a market for attention, acquisition, use or consumption that might satisfy

a want or need9. In banking context, all banking services are also

products. In Indian setting, banks are operating in a highly regulated

environment where product range is controlled by the Banking

247

Regulation Act, Reserve Bank of India, and Govt. of India. Inspite of

these constraints, a perceptible change has taken place in the products of

the banks. The banks primarily deal in services and therefore the

formulation of product mix is required to be in the face of changing

business environmental conditions. The changing psychology, the

increasing expectations, the rising income, the changing life styles, the

increasing domination of foreign banks and the changing needs and

requirements of custonlers at large make it essential that they innovate

their service mix, and make them of world c l a s ~ ' ~ .

It is generally assumed that two guidelines must be taken into

consideration while formulating service mix. The first is related to the

processing of products to market needs and the second is concerned with

the processing of market needs to products. In the first process, the

needs of the target market are anticipated and visualised, therefore the

process is likely to be productive. In the second process, the banks react

to the expressed needs. Therefore, the process is reactive. Along with

these i t is essential that every product is measured upto the technical

standards. This is due to the fact that no consumer would buy a product

which contains technical faults. Technical perfection in service means

248

prompt delivery, quick disposal, presentation of right facts and figures,

right filing, proper documentation etc.

Marketing aims at not only offering but also creatinglor

innovating services and/or schemes to the customers. The enhanced

customer patronage would be a reward to the bank. The additional

attractions, the product attractiveness would be a plus point of product

mix, which would help the bank in many ways. This makes it essential

that the banking organisations are sincere to the innovation process and

try to enrich their peripheral services much earlier than the competitors.

While formulating service mix it is also pertinent that the bank

professional make possible a fair synchronisation of core and

peripherals. In other words, the peripheral services need an intensive

care since the core services are found by and large the same. Innovating

peripheral services thus appears to be an important functional

responsibility.of marketing professionals. Thus the development of new

generic products, specially when the business environment is regulated

is found a difficult task. However it is pertinent that banks formulate

new products in time with the changing business conditions. Against

this background, the researcher analysed the influence of new products

in bank marketing.

249

Public Relation

Public relation has become a recognised function in banks for

several decades. It has grown tremendously now. The relationship

between public relation and marketing should be close. The two

functions are closely related and the practitioners of each must work

together if either function is to be carried out effectively. The Public

Relations Society of America (PRSA) developed a definition of what

public relation is today. "Public relations helps an organisation and its

publics adapts mutually to each other"". This definition was crafted to

encompass the essential functions in public relations. Public relation is

a communication intensive activity with a special emphasis on the

securing of favourable publicity for the bank. This kind of activity is

significant because banks operate in a climate of opinion. If the climate

of opinion surrounding a bank is unfavourable, a bank may find its plans

thwarted, it achievement stunted, and its customers taking their business

elsewhere.

Besides communications, the task of public relation is to conduct

activities that will create a favourable image for the bank in the

community, it services. In the parlance of public relations, the word

'public' is used in piural as 'publics'. All those who are associated with

250

branch have common interest constitute different publics. Therefore

public relations efforts have to be target and objective oriented with the

aim of creating a positive image of the branch. In service industry like

banks, the image of banks branches in the eye of public is more

important than the corporate image because a prospective customer is

not concerned with what the banks have done at macro level, in

economic and social sphere. He is concerned with the image of the

branch with whom he is going to deal with. It is in this background

bank executives, unlike the executives of other consumer good

manufacturing organisations, focus on public relations.

Individual relationships which resulted in promoting banking

business otherwise known as personal selling is now a dominating factor

in bank marketing. 'The main reason why personal selling is so

important in banking is because there is no product for the consumer to

see, hear, taste or touch. Therefore the seller must earn the confidence

of the customer by clearly explaining the product or service and how it

will benefit the customer. It is just a process of communication in which

an individual exercises the personal potential, tact, skill and ability to

influence the buying of the customers.

25 1

Personal selling has been defined by O.C. Ferrel and W.M. Pride

as, 'a process of informing the customers and persuading them to

purchase products through personal communications in an exchange

situation"'. Personal sales are simply communications aimed at

satisfying consumer needs with the services. Being interpersonal, this

communication is extremely flexible and provides a one to one

communication which can be customised to provide the right volume

and complexity of informations for each potential c~s tomer '~ . Nothing

happens unless somebody sells something and nothing is sold unless the

buyers are motivated'! The task of motivating the customer is found

difficult, if the forces managing the selling activities lack professional

excellence. The oral presentation in conversation bear the efficacy of

turning motivation into persuasion provided the management of sales

force is sound. Personal selling is an art of persuasion. Actually

personal selling is an art of telling and selling in which an individual

based on his or her expertise attempts to transform prospects into

customers. In personnel selling there is interpersonal or two way

communication that makes the way for a feedback. The selling of bank

services is no larger limited to certain employees, rather every one in the

bank sells elther directly or indirectly. In a marketing-oriented bank,

252

cvery one sees his 01. her job as being involved in selling the bank and

its services because every job in a bank can be traced ultimately to some

point of contact with the customer.

Telemarketing

An important component of the promotion mix is telemarketing,

which has gained popularity particularly in the developed countries. In

Indian perspective, it is just in the initial stage and it has already been

initiated by the foreign banks.

Telemarketing is a process of promoting business with the help of

sophisticated communication net work. The Television actually fuels

the process of telemarketing significantly. Thus the telephonic services

and the telecast services determine the instrumentality of telemarketing.

Telemarketing blossomed in the late 1960s with the introduction

of inbound and outbound Wide Area Telephone Services (W.A.T.).

With in Wide Area Telephone Services, the marketers can offer

customers and prospects toll-free numbers to place orders for goods or

services stimulated by print or broad cast advertisements, direct main

catalogues or to make coniplaints and suggestions. Without WATS they

can use phone calls to sell directly to consumers and businesses generate

253

or quality sales leads reach more distant buyers or selvices current

customers or accounts. The automatic dialing and recorded message

players (ADRMI') can dial numbers, play voice activated advertising

message and take orders from machine device or by forwarding the call

to an operator.

Television is found to be a growing medium for direct marketing

both through network and cable channels. In Indian prospective

telemarketing is of recent origin just after the 1990s. In banking, foreign

banks introduced telemarketing which is now initiated by Indian

commercial banks particularly by high-tech newly constituted private

sector banks. It is now being initiated by public sector commercial

banks also.

The telemarketing also helps in activating the process of

advertisement. The banking organisation telecasting their messages on

the T.V. screen are benefited in two ways. The first is that customers

come to know the information regarding the services or schemes, their

salient features and relative merits and second, they are also persuaded

in the right way. The transmission of information regarding the services

or schemes helps the customers in developing their awareness, specially

regarding the new service:; or schemes. Now banking organisations can

254

use telemarketing as a tool of the promotion mix both for advertising

and selling. Now there is an incremental role for telemarketing in

banking services in India indiscriminately, whether it is public, private

or foreign banks. Due to privatisation, liberalisation and globalisation,

under the new economic policy, telemarketing has tremendous

opportunity in banking both for selling and advertising of bank services.

In addition they can also use telemarketing for the redressal of the

grievances of customers,,

Price Mix

In the formulation of product mix pricing decision occupies a

place of outstanding significance. The pricing decisions related to

interest and fee or commission charged by banks are found instrumental

in motivating or influencing the target market. But Indian banks are

operating under regulated status. The RBI and Indian Banking

Association are concerned with regulation. The rate of interest is

regulated by the RBI and other charges are controlled by the Indian

Banking Association. Furthermore in India, the component of

marketing mix is significant because banking organisations are also

supposed to subserve the interest of the weaker section and backward

region. It is because of this specific role of the public sector commercial

banks complicate the problem'5 of pricing.

255

Pricing policy of banks is considered important for increasing the

number of customers. Eventhough there are a number of factors

influencing pricing, it is right to mention that of this a key role is played

by RBI. The non-banking organisations and foreign banks have been

found attracting customers by offering to them a number of incentives.

The potential customers or investors frame their investment plan in the

face of pricing decisions made by banking organisations. It is right that

policy makers consider price as an important variable to be traded off

against product quality and promotion rather than as an absolute where

the lowest price is most desirableI6. While formulating the pricing

strategies, the banks have also to take the value satisfaction variable into

consideration. The value and satisfaction cannot be quantified in terms

of money since it differs from person to person. Keeping in view the

level of satisfaction of a particular segment, the banks have to frame

their pricing strategy. In a competitive market, the buyers and sellers

must have the feeling of winning the transactions. If this is not possible,

the transaction would hardly take place. The policy makers are required

to be sure that the service:; offered by them are providing satisfaction to

the customers concerned.

256

In the case of pricing, the banking organisations are required to

frame two fold strategies. First the strategy is concerned with the

interest charged and second, the strategy is related to the interest paid.

It is right to mention that in a highly controlled banking industry, the

task of formulating the price mix is critical as well as challenging.

Place mix

Place mix is related to offering of services. The services are sold

through bank branches. One of the important decisions to be taken is to

select a suitable place for bank branches. The selection of a suitable

place for the establishment of a branch is significant with the view point

of making the place accessible and in addition the safety and security

provisions are also found important. The banking organisations are not

free to open a branch since the RBI regulates the subject of branch

expansion. But so far as the management of a branch is concerned,

branch management have open to select a place which is convenient to

both the parties such as users and the bankers. The task of selecting a

place for a branch is significant and requires to be considered carefully.

The place easily accessible is the first consideration. The availability of

infrastructural facilities cannot be under estimated, since in today's

prospective, the frequent use of sophisticated information technologies

257

to implove quality of service is quite essential. In the Indian

perspective, the protection to the banks assets and safety to the users and

bankers need due weightage. The management of office is also found

significant with the viewpoint of making the services attractive. This

draws attention to beautiljring the office and its premises and making the

place, environment friendly. Another important decision is related to

the offering of services. This draws attention to the behavioural profile

of bankers. The bank professionals or a branch manager is required to

be sure that whatever the promises have been made regarding quality of

service they are not distorted. The RBI and banks are required to

manage the distribution process intelligently and professionally. Thus

place mix is found to be an important area which requires attention at

micro and macro levels. If the banking organisation sells the promises,

it is essential that in the end users get the same without any distortion.

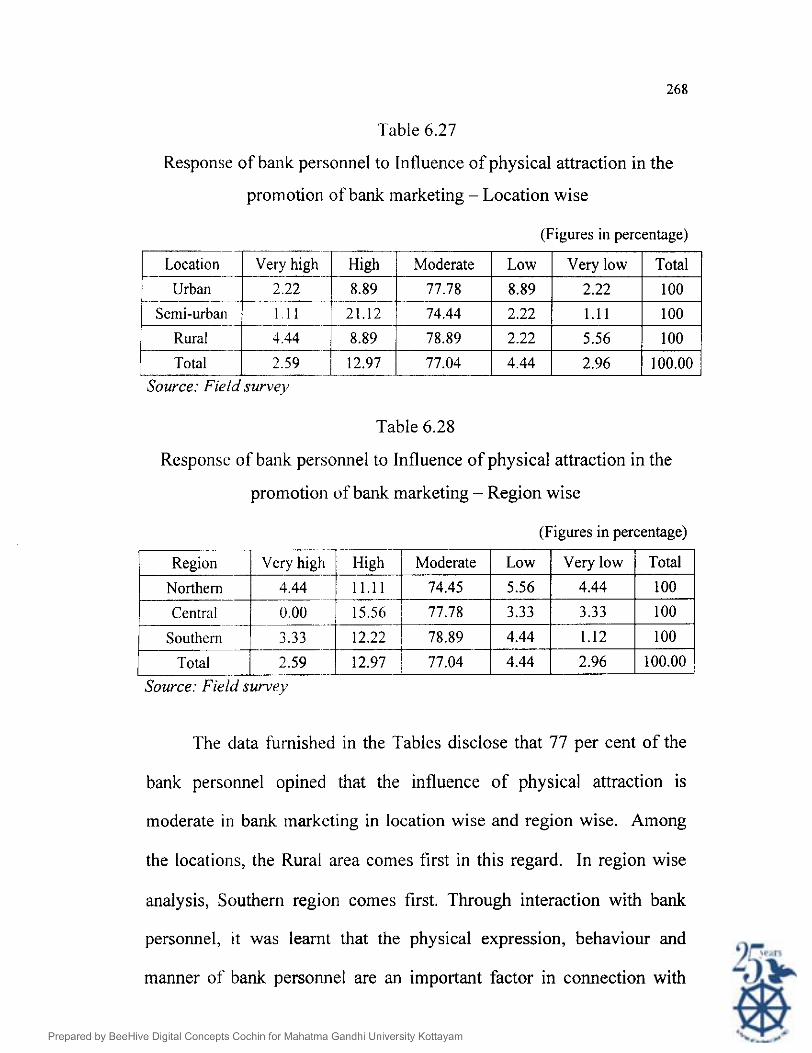

The Physical Attraction

With the developnlent of corporate sector and with the emergence

of corporate culture, the physical attraction of people is getting a new

place in marketing mix. The physical attraction puts emphasis on the

employees' smart look, handsomeness and impressiveness. This draws

our attention to the management of the body which helps in projecting

258

the personality and adding to physical attraction. The personal care

service would help employees in developing their physique and looking

impressive and attractive. In banking organisation, due priority must be

given to physical attraction mainly because this would help bankers to

attract the customers and to promote banking business. Attraction in

product is quite essential but at the same time attraction in sales people

is also found impact generating and in this case there is no exception to

banking business. It is against this background that the influence of

physical attraction is also verified in the study. Hence the study has

been conducted in order to see the influence of these factors in bank

marketing. The data contained in Tables 6.13 and 6.14 give the outcome

of the study in connection with the influence of advertisements in the

promotion of bank marketing.

Table 6.13

Bank personnel's response to Influence on advertising in the promotion

of bank marketing - Location wise

(Figures in percentage)

Total 100 100 100

100.00 Source: Field survey Pearson Chi-square: 7,00429, d k 8 , p=,536182

23.33 Rural 5.56 13.33 Total 16.67

Low 10.00 5.56 10.00 8.52

Moderate 73.33 66.67 70.00 70.00

Very low 0.00 1.11 1.11 0.74

Bank personnel's response to Influence on advertising in the promotion

of bank marketing - Region wise

(Figures in percentage)

The data contained in the Table reveals that 70 per cent of the

bank personnel are of the view that the influence of advertising in bank

marketing is 'moderate' in location wise and region wise. In location

wise analysis, the Table ]reveals that the influence of advertisement is

'moderate' [n location. Among the locations urban areas come first in

this regard (73.33 per cent). In region wise analysis it is found that the

'central region' comes first in influence (78.89 per cent) and the lowest

influence is in Northern region. Interaction with bank personnel

revealed that simply by having mega advertisement customers are not

ready to deal with the banks. It is really on the basis of acceptance of

service by customers. For acceptance, the main factors to be taken into

High Northern 26.67 Central 2.22 11.11 1

Southern 12.22 Total 4.07 16.67

consideration are the attitude of bank personnel, the type of services

Source: Field surve,y Pearson Chi-square: 20,2571, df=8, p=,009421

Moderate 60.00 78.89 71.11 70.00

Low 4.44 7.78 13.34 8.52

Very low 1.11 0.00 1.1 1 Q.74

Total 100 100 100

100.00

required and provided and confidence in financial health particularly to

co-operative banks.

The second factor taken for study is "Developing new products".

Results of the study in location wise and region wise are disclosed in

Tables 6.15 and 6.16.

Table 6.15

Bank personnel's response to Influence of developing new product in

the promotion of bank marketing - Location wise

(Figures in percentage)

Semi-urban 12.22 80.00

Rural 5.56 80.00 13.33 0.00

Total 7.41 80.74 10.37 1.11 0.37 100.00

Source: Field survey

Table 6.16

Bank personnel's response to Influence of developing new product in

the promotion of bank marketing - Region wise

(Figures in percentage)

p g i o n E;: I M:;;te 1 LOW 1 Verylow / Total

Northern 1 1.11 1 0.00 1 100

1 Central 1 8.89 1 78.89 12.22 1 0.00 1 0.00 1 100 1

Source: Field survey

26 1

The data furnished in the Tables reveals that the influence of new

products in promotion of bank marketing is 'high' (80.76 per cent) both

in location wise and region wise. In location wise analysis the table

further reveals that more than 80 per cent of the bank personnel opined

that developing new products is one of the important factors for bank

marketing. In region wise analysis also more than 78 per cent of bank

personnel are for developing new products and among the regions, the

southern region comes first in this regard. By interacting with bank

personnel it was understood that many of the products introduced by

banks are readymade and they are not in the right form of their

requirements. In additi'on to this, there are a lot of changes in the

outlook of customers due to the external and internal environment

towards their attitude to deposits and their financial requirements.

Hence developing new products is essential to satisfy customers.

The third factor taken for analysis is 'public relation'. The data

contained in Tables 6.17 and 6.18 give the outcome of the study in

location wise and region wise.

Table 6.17

Bank personnel's response to Influence of public relation in the

promotion of bank marketing - location wise

(Figures in percentage)

-

Semi- urban .-

48.89 48.89

Rural 23.3.3 71.11 5.56 0.00 0.00 100

Total 34.82 60.74 3.70 0.74 0.00 100.00 Source: Field survey

'Table 6.18

Bank personnel's response to Influence of public relation in the

promotion of bank marketing - Region wise

(Figures in percentage)

~ n ~ ~ e ~ ~ ~ ~ H i g h e r a t e / Low ( Very low I Total I

Source: Field survey

.The data furnished in the Table reveals that the influence of

public relation is 'high'. With regard to the promotion of bank

marketing (60.74 per cent) i.e. creating positive image about the branch

is a core aspect in public relation, bank personnel opined that its

influence is high both in location wise and region wise in bank

marketing. Further, the Table states that among the locations rural area

comes first in this regard (7 1.1 1 per cent). Bank personnel in rural areas

reveal that rural folk do not voluntarily approach the bank due to their

inability to interact with bank personnel for presenting their

requirements. Thus public relation activities give confidence to the

public particularly to rural people to deal with banks. In region wise

analysis it is interesting to note that it is not only high but the influence

of public relation is somewhat equal in all regions.

Apart from public relation, another factor taken for analysis is

personal relation. The relevance of personal selling arises due to the fact

that in bank marketing there is no product to see, hear, taste or touch.

Therefore the buyer gets the confidence by getting a clearcut explanation

directly from bank personnel. The data furnished in Tables 6.19 and

6.20 give the outcome of the study in location wise and region wise.

Table 6.19

Bank personnel's response to Influence of personnel relation in the

promotion of bank marketing - Location wise

(Figures in percentage)

Location High

Urban 28.89

Semi-urban 86.67 12.22

Rural 48.89

Total Source: Field survey

Moderate

3.33

1.11

3.33

2.59

Low

1.11

0.00

0.00

0.37

Very low

0.00

0.00

0.00

0.00

Total

100

100

100

100.00

Table 6.20

Bank personnel's response to Influence of personnel relation in the

promotion of bank marketing - Region wise

(Figures in percentage) I Region I VA Hi;: 1 M;d;;te 1 Low 1 Very low I Total

Northern 1 0.00 1 0.00 1 100

( ~ o l r l ~ i z z - ) ~ . ~ ~ ~ j 0.37 j o.Oo 1 l ~ ~ . ~ ~ Source: Field survey

1 central 1 ii4.45 1 34.44 1 1 ~~~ -

l'he data contained in the Table discloses that the influence of

personal relation is very high in the promotion of bank marketing both

in location wise and region wise (67.03 per cent). It is also found that

86.67 per cent of the bank personnel in semi-urbans area are in favour of

personal relat~on and it is 47.78 per cent in rural area. In rural areas

48.89 per cent of the bank personnel opined that the influence of

personal relation 'high' in bank marketing. In region wise analysis it is

found that the influence of personal relation is very high and further

more it is somewhat equal.

0.00

Telemarketing is another method taken for study as a factor for

promoting bank marketing. The data contained in Tables 6.21 and 6.22

show the outcome of the study in location wise and region wise.

0.00 1 100

I Southern 68.89 27.78 1 1.11 1 0.00 1 100

Table 6.2 1

Response of bank personnel to Influence of telemarketing in the

promotion. of bank marketing - Location wise

(Figures in percentage)

.-

Semi-urban 14.44 34.45 42.22

Rural 6.67 2.22 2.22 13.33 75.56 ~~

Total 3.33 5.56 10.37 32.22 48.52 100.00 - Source: Field survey

Table 6.22

Response of bank personnel to Influence of telemarketing in the

promotion of bank marketing - Region wise

(Figures in percentage)

Central 14.44 63.33

Southern 4.44 33.33 51.11

Total 5.56 10.37 32.22

Source: Field survey

The study reveals that the influence of telemarketing is 'very low'

in bank marketing both in location wise and region wise. Among the

locations it is the rural area and among regions, it is the central region

that records the least influence.

The other two factors taken for study with regard to promotion of

bank marketing are price mixing and place mixing. The information

contained in Tables 6.2.1 to 6.26 give the outcome of the study in

location wise and region wise.

'Table 6.23

Response of bank personnel to Influence of price mixing in the

promotion of bank marketing - Location wise

1 Rural / 4.44 1 1.11 1 2.22 1 26.67 1 65.56 1 100 1

(Figures in percentage)

Moderate

- . ~

30.00

Semi-urban 8.89 16.67

Table 6.24

59 1 4.81 1 16.30 1 34.44 1 /-I-?- . -. 41.86

Response of bank personnel to Influence of price mixing in the

Low

33.34

43.33

100.00

promotion of bank marketing - Region wise

Source: Field survejv

(Figures in percentage)

Very low

30.00

30.00

Total

100

100

Source: Field survey

Very high High rP-1, Northerr1 6.67

Central .

3.33

Southcr~l 2.22 4.44 .

Total 2.59 4.81

Moderate

20.00

13.33 -- 15.56

16.30

Low

38.89

14.44

50.00

34.44

Very low

30.00

67.79

27.78

41.86

Total

100

100

100

100.00

Table 6.25

Response of bank personnel to Influence of place mixing in the promotiorl of bank marketing - Location wise

Table 6.26

(Figures in percentage)

Response of bank personnel to Influence of place mixing in the

Location

Urban --

Semi-urban -.

28.89

Rural 12.22

Total 25.93

promotion of bank marketing - Region wise

source: ~ i e i d survey

Low

23.33

31.11

22.23

25.56

These studies reveal that the influence of these factors in

promoting bank marketing is very low both in location wise and region

wise.

(Figures in percentage)

Another factor takcn for study with regard to the promotion of

bank marketing is physical attraction. The data contained in the Tables

6.27 and 6.28 give the outcome of the study location wise and region

Very low

30.00

26.67

58.89

38.51

Total

100

100

100

100.00

Region Very high High

5.56

Central 6.67

Source: ~ Z i d swvejl

Very low

22.22

68.89

24.44

38.51

Total

100

100

100

100.00

Moderate

36.67

10.00

Low

31.11

12.22

Southern 6.68 , 31.11 -. .. --

Total 3.70 6.30 25.93 .

33.33

25.56

Table 6.27

Response of bank personnel to Influence of physical attraction in the

promotion of bank marketing - Location wise

(Figures in percentage)

ILoca t ionTvGhiah rHigh I Moderate I LOW I Verv low I Total I - F - F t - 8.89 Semi-urban 21.12

Table 6.28

: 1 78.89 1 2.22 1 5.56 1 100

Response of bank personnel to Influence of physical attraction in the

I~ 77.04

promotion of bank marketing - Region wise

77.78

(Figures in percentage)

2.22

1.11

8.89

Source: Field survey 4.44

100

100 74.44 1 2.22

The data furnished in the Tables disclose that 77 per cent of the

bank personnel opined that the influence of physical attraction is

moderate in bank marketing in location wise and region wise. Among

the locations, the Rural area comes first in this regard. In region wise

analysis, Southern region comes first. Through interaction with bank

personnel, it was learnt that the physical expression, behaviour and

manner of bank personnel are an important factor in connection with

2.96

I Moderate

74.45

-- . Southern 3.33 12.22 / 78.89

~-

Total 2.59 12.97 77.04 -.

100.00

Source: Field survey

Low

5.56

3.33

4.44

4.44

Very low

4.44

3.33

1.12

2.96

Total

100

100

100

100.00

bank marketing. It'the bank personnel are very tough in their expression

and resemed in nature, customers are reluctant to deal with them. So a

pleasing countenance and amiable behaviour of the bank personnel will

help in promoting bank marketing.

A study was also conducted to verify the influence of ATM,

which is now gradually entering Kerala banking. The data furnished in

Tables 6.29 and 6.30 disclose the outcome of the study.

Table 6.29

Response of bank personnel to Influence of ATM in the promotion of

bank marketing - Location wise

(Figures in percentage)

Urban

Rural 4.44 2.22

Table 6.30

Response of bank personnel to Influence of ATM in the promotion of

bank marketing - Region wise

Total

(Figures in percentage)

Moderate

28.89

24.44

6.67

3.33 1 4.07 20.00 1 26.67 1 45.93 1 100.00

Very high High 1 Moderate I Low I Very low I Total

5.56 1 12.22 1 38.88 1 37.78 1 100

Source: Field survey

-

v e n t r a l I ;:) 1 4.44 37.78 16.67 41.11 1 100

Southern 2.23 10.00 1 24.44 1 58.89 1 100

Low

40.00

24.44

15.56

Total 3.33 1.07 j 20.00 26.67 1 45.93 1 1oo.00

Source: Field survey

Very low

22.23

44.44

71.11

Total

100

100

100

270

The information contained in the Table reveals that the influence

of ATM in promotion of bank marketing is very low in location wise

and region wise (46.1 per cent). In location wise it is a weak factor for

promoting bank marketing in rural areas i.e. very low (71.1 1 per cent)

but the same opinion is not shared by the urban and semi-urban areas.

In region wise analysis the influence is very low in the southern region.

The last factor taken for study in connection with the promotion

of bank marketing IS that of professionalisation. In the present

competitive world bank:j are in search of different alternatives for

promoting bank marketing. Professionalism in bank means application

of trained and specialiseti knowledge for performing banking services.

Thus professionalisation in bank marketing also analysed in the study.

The data contained in 'Fables 6.3 1 and 6.32 give the results of the study

in location wise region wise.

Table 6.3 1

Response of bank personnel to Influence of professionalism in the

promotion of bank marketing - Location wise

(Figures in percentage)

i - x z & n n n ~ ' y h i g h h i g h ~ ~ Moderate 1 Low 1 Very low 1 Total

Urban 10.00 73.33 11.12, 1 3.33 1 2.22 1 100

Semi-urban

30.00

18.52 1.85 2.96 100.00

Source: Field survey

Table 6.32

Response of bank personnel to Influence of professionalism in the

promotion of bank marketing - Region wise

(Figures in percentage)

~ -

Central 57.77 28.89

Southrn~ 67.78 16.67 4.44 2.22

Total 65.93 18.52 1.85 2.96 100.00

Source: Field survey

The data contained in the Tables reveals that the influence of

professionalisation in bank marketing is 'High'. Among the locations,

the greatest influence is in Semi-urban area 74.44 per cent, and the

lowest in Rural area (50.00 per cent). In region wise analysis also it is

found that the greatest influence is in the Northern region (72.22 per

cent).

The same factors were taken for study to assess the attitude of

customers also. The data furnished in Tables 6.33 and 6.34 give the

attitude of customers regarding the influence of advertising for bank

marketing.

Table 6.33

Customer's response to influence of advertising on bank marketing- location wise

(Figures in percentage)

Semi-urban 0.33 22.67 64.33 12.67 0.00 -.

Rural 1.33 14.00 0.34 100

Table 6.34

I Total 1 1.89 24.56 / I L - 61.33

Customer's response to influence of advertising on bank marketing- Region wise

(Figures in percentage)

Source: Field Survev 12.11

~~ ..

Total 1.89 2456 61.33 12.11 0.1 1 100.00

Source: Field Surve)~

0.11 1 100.00

h 1 Moderate 1 Low I Very low ( Total

The data contained in the Tables reveal that more than 6 1 per cent

Northern / 66.67 1 19.00 1 0.33

of the customers opined that the influence of advertisement is

100

'moderate' in bank marketing both location wise and region wise. And

among the locations, the semi-urban area comes first in respect of

stating that the influence of advertising is 'moderate'. Similarly, the

Northern region comes first among the regions. The attitude of

customers is similar to that of bank personnel regarding the influence of

advertising in bank marketing.

The second factor taken for analysis is the influence of

developing new products in bank marketing. The data contained in

Tables 6.35 and 6.36 disclose the outcome of the study in location wise

and region wise.

Table 6.35

Customer's response to influence of developing new products on bank marketing- Location wise

(Figures in percentage)

Table 6.36

9.00

Rural 12.00 79.67 7.33 .-

Total 9.1 I 83.34 , 6.44 --

Customer's response to influence of developing new product on bank marketing - Region wise

(Figures in percentage)

Source: 17ieli/ Survcly

Low

1.33

0.33

0.67

0.78

Low Very low Total

0.34 0.00 100

8.67 1.67 1 .OO 100 - Southern 18.67 79.67 1.33 0.33 0.00 100

Total 83.34 6.44 0.78 0.33 100.00 - Source: Field Survey

Very low

0.67

0.00

0.33

0.33

Total

100

100

100

100.00

274

The data furnished in the Table reveals that developing new

products have 'high' influence in bank marketing (83.33 per cent).

Among the locations, the study reveals that Semi urban area comes first

(88.67 per cent) in this regard. Among the locations, the Rural area

records the lowest influence but this also is more than 79 per cent. In

region wise analysis, the Northern region comes first in the case of

influence of new products in bank marketing (88 per cent) and the

lowest influence is in the Southern region, but it is more than 79 per

cent.

Table 6.37

Customer's response to influence of public relation on bank

marketing- Location wise

(Figures in percentage)

Table 6.38

Customer's response to influence of public relation on bank

Total 100 100 100

100.00

Low 1.33 0.00

38.67 2.66 0.00 50.67 45.89 2.78 0.44

marketing- Region wise

Source: Field Survey

Very low 0.33 0.33 0.00 0.22

Source: Field Survey

275

In the case of public relation, the information contained in Tables

6.37 and 6.38 reveal the outcome of the study. The data contained in the

Tables reveal that in the point of view of customers, the influence of

public relation in bank marketing occupies 'very high' influence (50 per

cent). By close verification it is clear from the Table that more than 96

per cent of customers opined that the influence of public relation is 'very

high or high' in bank marketing. In location wise analysis, it is found

that among the locations, the rural area comes first and in region wise

analysis it is clear that the Southern region comes first in the case of

influence in bank marketing.

Table 6.39

Customer's response to influence of personal relation on bank marketing

- Location wise

(Figures in percentage) m T ~ - ; ; T E m / 1 Semi-urban 8 0 , 0 0 ~ 16.67 1 1.67 1.33 0.33 1 ::: 1 - Rural 68.67 25.00 4.00 2.33 0.00

Total 74.22 - -- 1.56 0.44 100.00

Source: Field Survey

l'able 6.40

Customer's response to influence of Personal relation on bank

marketing - Region wise

Source: Field Survey

The next factor taken for study is the 'personal relation' in bank

(Figures in percentage)

marketing. The data contained in Tables 6.39 and 6.40 reveal that more

Region , Very hlgh . High 1 Moderate FI:i+ iic 5.00

Central 76.67 14.67 / 6.00

than 76 per cent opined that the influence of 'personal relation' in bank

marketing is very high (76.44 per cent) both in location wise and region

Low

1.33

1.66

wise. In location wise analysis, the semi-urban area comes first in this

regard (80 per cent). In region wise analysis, the Southern region comes

Very low

0.34

1 .OO

first (93 per cent) in this regard. Both bank personnel and customers

Total

100

100

respond in the same way regarding the influence of personal relation on

bank marketing and they give the highest preference for personal

relation in bank marketing. The customer's accessibility to bank

personnel to express their requirements and to get the right direction is

considered the prime aspect of bank marketing.

Table 6.4 1

Custonler's response to influence of telemarketing on bank

marketing- Location wise

Semi-urban 0.67 47.33 42.67 ~

Rural 1.67 0.67 11.33 52.33 34.00

Total 1.50 1.33 1 1.56 50.88 I L - . I I I I J

Source: Field Survey

Table 6.42

Customer's response to influence of telemarketing on bank

marketing- Region wise

(Figures in percentage)

In the case of telemarketing, the data contained in Tables 6.41 and

6.42 reveal that the influence in bank marketing is 'low' both in location

wise and region wise (50.89 per cent). Further, the data contained in the

Table reveals that more than 88 per cent of the customers both in

location wise and region wise opined that telemarketing as a factor for

3.00

Southern 2.00 18.67

Total 1.56 I .33 1 1.56

Source: Field Survczv

Low

40.33

45.00

67.33

50.88

Very low

54.33

38.00

1 1.67

34.67

Total

100

100

100

100.00

influencing bank marketing has 'low' or 'very low' effect in bank

marketing. Even though it has been introduced in Indian marketing, its

influence is confined to a few customers coming under high income

bracket particularly from urban area.

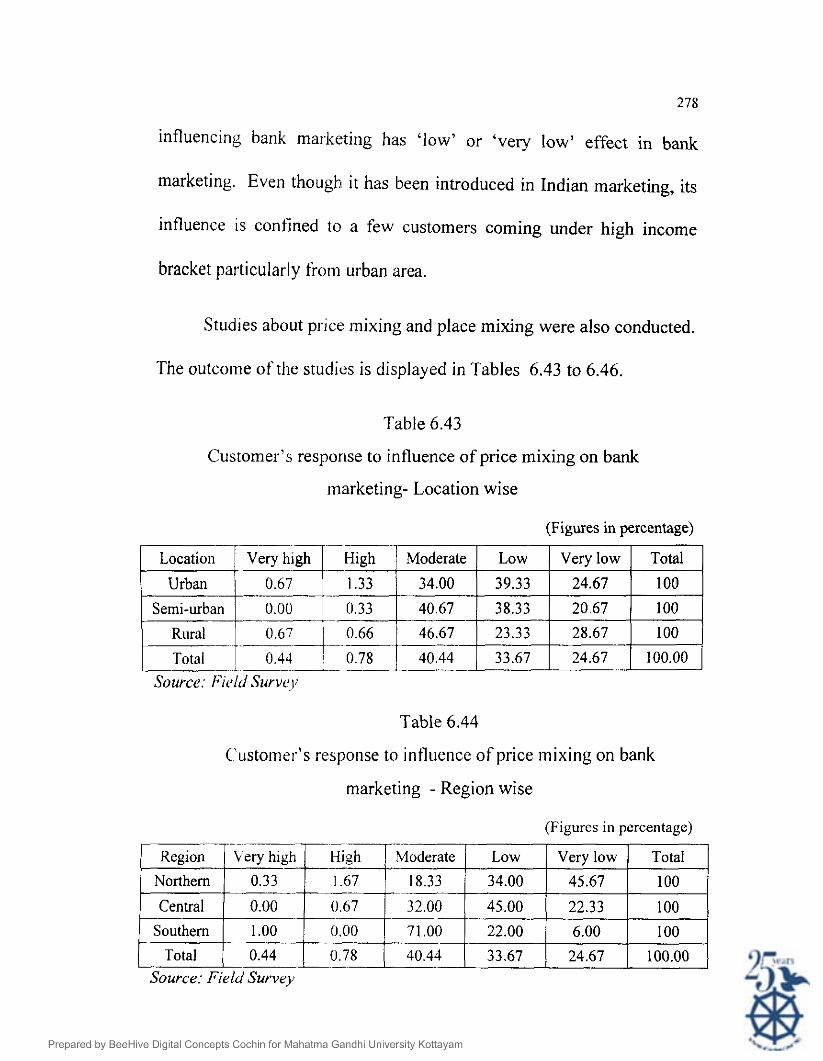

Studies about price mixing and place mixing were also conducted.

The outcome of the studies is displayed in Tables 6.43 to 6.46.

Table 6.43

Customer's response to influence of price mixing on bank

marketing- Location wise

(Figures in percentage)

/ Total _! 0.43 1 0.78 1 40.44 1 --

24.67 100.00 1 Source: Ficld Survrv

Location Very h ~ g h High

1.33 .-

Semi-urban --- -- 0.33

Rural - -E71- 0 66

Table 6.44

C'ilstome~.'~ response to influence of price mixing on bank

marketing - Region wise

Moderate

34.00

40.67

46.67

(Figures in percentage) 1 ~ e ~ i o n 1 vph3:gh 1 High I Moderate 1 .-

Low I Very low ( Total

Northern 1.67 1 18.33 1 34.00 1 45.67 1 100

Low

39.33

38.33

23.33

100

Southern 71 .00 22.00 1 6.00 100

1 Total 1 0.44 1 0.78 / 40.44 1 33.67 1 24.67 1 100.00 Source: Field Survey

Very low

24.67

20 67

28.67

Total

100

100

100

Table 6.45

Customer's response to influence of place mixing on bank

marketing - Location wise

(Figures in percentage) - -

Low 1 Very low I Total

/ 26.00 1 20.34 1 100

1 I I I 1 I I

Source: Field Surve,y

Table 6.46

Customer's response to influence of place mixing on bank

marketing - Region wise

(Figures in percentage)

1 ;;rm 1 ~ e ; ~ : g w ~- High

1 Moderate I Low I Very low I Total

.3 .OO / 35.67 1 21.33 1 39.00 1 100

Total 0.56 1.66 58.1 1 19.89 19.78 100.00

Source: Field Survey

The data furnished in the Table reveals that the influence of price

mixing and place mixing are 'moderate' in location wise and region

wise. In location wise analysis of price mixing, the Table shows that

among the locations, the rural area comes first (46.67 per cent) and

among the regions, the southern region comes first in this regard. The

data contained in the Table shows that more than 74 per cent of the

customers opined that the influence of price mixing is either 'moderate'

or 'low'. In the case of' place mixing the information furnished in the

Table reveals that among the locations, the semi-urban area comes first

in the influence in bank marketing.

Another factor taken for study with regard to the influence on

bank marketing is physical attraction. The outcome of the study in

connection with physical attraction is described in Tables 6.47 and 6.48

in location wise and region wise.

Table 6.47

Customer's response to influence of physical attraction on bank marketing- Location wise

(Figures in percentage)

Source: Field Survey

Moderate 75.33 78.00 78.67 77.33

Table 6.48

Low 10.67 6.00 7.67 8.1 1

Customer's response to influence of physical attraction on bank marketing - Region wise

(Figures in percentage)

Very low 3.33 1.33 2.66 2.44

Total 100 100 100

100.00

Total

100

100

100

100.00

Source: ~ i e i d Survey

Vcry low

2.33

4.00

1 .OO

2.44

.~

Central 0.00 7.00 78.00

Southern 0.34 84.33

.- [,ow

3.33

11.00

10.00

Total 0.56 1156 77.33 8.1 1

28 1

The data contained in the Table shows that more than 77 per cent

are of the view that the influence of physical attraction in bank

marketing is 'moderate'. In location wise analysis it is found that both

in the rural area and the semi-urban area the influence of physical

attraction is somewhat the same, that is, 78.67 per cent and 78 per cent.

In region wise analysis, the Southern region comes first (84.37 per cent)

and the lowest is in the Northern region (69.67 per cent). The studies

clearly show that physical attraction of bank personnel is also a factor

which influences bank marketing that is it is not a negligible factor in

banking.

In the case of A'I'MI, bank personnel responded that its influence

in bank marketing is 'very low'. But by analysing customers' attitude

towards ATM as a factor For bank marketing, the outcome of which can

be seen in the data contained in Tables 6.49 and 6.50, it was seen that

the influence is low in location wise and region wise (59.11 per cent).

Table 6.49

customer"^ response to influence of ATM on

bank marketing - Location wise

Table 6.50

Customer's response to influence of ATM on bank

(Figures in percentage)

marketing - Region wise

13.00

Rural 10.33

Total 0.67 2.77 11.89

It is also found that more than 86 per cent come under the

Source: Field Surve,?

Low

56.00

64.67

58.00

59.56

(Figures in percentage)

category of both 'low' and 'very low'. In location wise analysis the data

Low

35.33

Central 16.00 57.33

Southern 0.34 2.33 6.33 86.00

Total 0.67 1 1.89 59.56

contained in the Table reveals that among the locations, more than 64.67

Very low

28.00

19.00

28.33

25.1 1

per cent 01' the customers from Semi-urban area opined that the

Total

100

100

100

100.00

Source: Field Survey

Very low

48.33

22.00

5.00

25.1 1

influence is low and in region wise studies, 86 per cent customers from

Total

100

100

100

100.00 -

the Southern region also state that the influence of ATM in bank

marketing is low.

Among the factors analysed to identify the influences on bank

marketing, the last factor is professionalism. The data contained in the

Tables 6.51 and 6.52 reveal the outcome of the study in location wise

and region wise.

Table 6.5 1

Customer's response to influence of Professionalism on bank

marketing - Location wise

(Figures in percentage)

F-1 Eryh igq- -? - l igh -- 1 Moderate ( LOW I very low I ~ o t a l

1 Urban 1 2.67 1 66.67 1 27.00 / 1.00 1 2.66 1 100 /

Table 6.52

Customer's response to influence of Professionalism on

1 Semi-urban 1 1 . 6 7 t 80.33 -- ---

Rural 3 .OO 77.00

Total 2.44 74.68

bank marketing - Region wise

(Figures in percentage)

Source: Field Survey

13.67

16.33

19.00

- - I -

Very Region 1 High 1 Moderate 1 Low I Very low I Total 1

N o h 4.34 k 7 9 . 3 3 4 I%! 1.33 1 1.00 1 :!i 1 Central 2.67 64.33 28.67 0.33 4.00

~~

Southern 0.33 XO.:i4 14.33 2.67 2.33

2.33

1 .OO

1.44

2.00

2.67

2.44

13 2.44 / 74.08 1 19.00 1 -- -

100

100

100.00

1.44 2.44 1 100.00

Source: Field Survey

284

The data contained in the Tables show the influence of

professionalism in bank marketing is 'high' in location wise and region

wise (73.64 per cent). Location wise it was found that, the Semi-urban

area comes first in this regard (80.33 per cent) and in region wise

analysis, the Southern region comes first (80.33 per cent) and it is only

one per cent more than the Northern region.

Out of all the factors taken for study, both bank personnel and

bank customers have opined that 'personal relation' is the most

important factor in bank marketing and is ranked by both groups as

'very high'. Customers ranked public relation also under 'very high'

category, but bank personnel categorised it under 'high'. In the case of

developing new products imd professionalism, both bank personnel and

customers have the same point of view and they grouped these factors

under the category of 'high'. Advertising and physical attraction have

moderate influence and all other factors that is Telemarketing, price

mixing and ATM are considered by bank personnel as having 'very low'

influence in bank marketing but customers gave a 'low' rating to these

factors.

These conclusions are displayed in Figure 6.3.

Employees Customers Factors

Location I I- Region

Advertising - 1 Moderate I Moderate 1 Moderate 1 Moderate 1 New product 1 High 1 High I High I High 1 Public relation I High 1 High 1 Very High I Very High I

( Personal relation 1 Very High I Very High I Very High I Very High ] I Telemarketing ; Very Low / Very Low I Low I Low I Price mixing 1 Very Low I Very Low / Moderate I Moderate ]

--

I Place mixing I Low I Low I Moderate I Moderate I

1 ATM I Very Low I Very Low I Low I Low I Physical attraction

Figure 6.3. Factors influencing promotion of bank marketing

Moderate -

Professionalism

Nationalisation of lcommercial banks marked an important mile

stone in the history of banking in India. Since nationalisation, dramatic

changes have occurred in the profile of Indian banking. Banking has

thus emerged as an effective catalytic agent of socio-economic change.

Moderate I Moderate I Moderate

~ i ~ h 1 High High High --

In the period following nationalisation, the Indian banking system

has made phenomenal strides in the volume of its business. It has

diversified its activities in a significant fashion. One of the major

objectives of developmental credit policy, as enunciated at the time of

bank nationalisation was to seek to extend the reach of bank credit both

286

geographically and functionally. Geographically, in the sense of

covering the unbanked and underbanked regions of the country

especially rural areas and functionally, to extend credit to agriculture,

smallscale and cottage industries and selfemployed sector which were

deemed important in tenns of their contribution to national economic

growth, expansion of employment opportunities and widening the base

of economic power but which were also neglected upto that time in

terms of their access to institutional, especially bank credit. Functional

expansion obviously needs a physical presence and this was the logic

behind the massive effort at branch expansion. Banking system thus

emerged as an effective catalytic agent of socio-economic change. This

massive and speedy expansion and diversification of banking resulted in

its own weakness also. In the process, what was designed to be socially

oriented credit, degenerated into irresponsible lending. Nationalisation

of banking was meant to bring about a measure of socialisation of credit

and politicisation of lending which unfortunately has come to increase

the loan waivers. The end result of these is that it gradually affected the

productivity, efficiency and profitability of the bank.

With the liberalisation of Indian economy, there has been a sea

change in the socio-economic scenario in our country. Banking

287

business in general and credit administration in particular has become

more complex. There is huge demand from different comers to make

structural change in the banking system including dematerialisation to

cope with presentday economic needs and wants. Hence a study was

conducted to assess the attitude of bank personnel with regard to

nationalisation. The data contained in Tables 6.53 and 6.54 give the

outcome of the study.

Table 6.53

Views on nationalisation - Location wise

(Figures in percentage)

I Not favouring I No command I Total 14.44 28.89

Table 6.54

Views on nationalisation -- Region wise

(Figures in percentage)

0.00 2.22

1.11 1 100.00 --

100 100

Rural 71.11 27.78

- Source: Field survey Pearson Chi-square: 8,86884, df=4, p=,064540

Total

Region Favouring / Not favouring

Northern 25.56 mi 35.56 Central

Southern 90.00 10.00

I I .- 1 I I

Source: Field survey Pearson Chi-square: 19,0075, dg4, p=,000785

1.11 75.19

1 I I I

100 23.70

No command

2.22

1.11

0.00

Total

Total

100

100

100

75.19 23.70 1.11 1 100.00

288

The data furnished in the Table reveals that there is no statistically

significant relation between location and views on Nationalisation. The

data contained in the Table further shows that more than 78 per cent of

the bank personnel support nationalisation of banks and among the

locations urban area comes first in this regard (85.56%). It is 68.89 per

cent in semi urban areas and 71.1 I per cent in rural areas.

In region wise analysis the data contained in the Table reveals that

there is statistically significant relation between the region and views on

nationalisation. The data furnished in the Table further shows that bank

personnel are favouring nationalisation in all regions, and among the

regions, the Southern region comes first (90 per cent) in this regard.

Arguments abound in support of and against Nationalisation. The

data contained in the Table reveals that among the bank personnel more

than 75 per cent are even now for nationalised banking system in India.

The study also analysed why they were in favour of nationalisation. On

the basis of pilot study the., two major reasons were identified. They are

social control and surplus coming to exchequer. One more choice is

also given to bank personnel to state any reason other than the reasons

identified for study. The data firnished in Tables 6.55 and 6.56 give the

outcome of the study in location wise and region wise.

Table 6.55

Location wise categorisation of reason for supporting nationalisation

(Figures in percentage)

Table 6.56

Location

Semi-urban 93.54 Rural 98.44 Total 95.07

Reason for supporting nationalisation- Region wise

(Figures in percentage)

Source: Field survey Pearson Chi-square: 10,5051, dP6, p=,104970

Surplus coming to exchequer

2.60 3.23 0.00 1.97

-

Source: Field survey Pearson Chi-square: 20,8861, df=6, p=,001927

Social control & Surplus coming to

exchequer 3.90 3.23 1.56 2.96

In the study it was verified whether there is any statistically

significant relation between the location and reason for supporting

nationalisation by applying chi-square test and calculating 'p' value.

The results reveal that there is no statistically significant relation

between location and reason for supporting nationalisation. The data

Total

100 100 100 100

Social Region 1 control

contained in the Table hrther reveals that from the supporters of

Surplus coming to exchequer

3.08 3.51 0.00 1.97

Northern Central

Southern Total

93.84 92.98 97.53 95.07

Social control & Surplus coming to

exchequer 3.08 3.51 2.47 2.96

Total

100 100 100 100

290

nationalisation more than 95 per cent opined that social control over the

bank is the major reason for it. Concentration of money power with

individuals and will result in increased social evils like corruption

manipulation; for their individual benefits. Again, by close verification

it can also be seen that support for nationalisation is the highest in rural

areas and it is gradually coming down to urban areas. More than 98 per

cent of the bank personnel from rural area are of the opinion that social

control is the major reason for supporting Nationalisation and it is 93 per

cent in urban area. The greatest beneficiaries of nationalisation are rural

folk. Opening of branches in villages has helped rural people from

falling into the clutches of moneylenders. Further, they are protected

from many social evils.

In region wise analysis also the data furnished in the Table reveals

that statistically significant relation exists between the Region and

reason for supporting nationalisation. From the Table it is also clear that

bank personnel support riationalisation mainly because of the social

control.

It is already identified that more than 24 per cent of bank

employees do not support nationalisation. On the basis of pilot study,

two major reasons were identified. One is 'avoid bureaucracy' and

29 1

second is 'competitivene~s' and their choice left open to bank personnel

to state thcir opinion other than the two reasons identified in the study.

Table 6.57

Reason for not supporting nationalisation-Location wise

Source: Field survqy

Table 6.58

Reason for not supporting nationalisation-Region wise

(Figures in percentage)

(Figures in percentage)

ILY

76.00 100.00 Central 12.50 87.50 100.00

Southern 10.00 90.00 100.00 16.42 83.58 100.00

2 1.43 Semi-urban

Rural 23.08 Total 16.42

Source: Field survey

The data contained in Tables 6.57 and 6.58 reveal that more than

83 per cent opined that they do not support nationalisation because in

the present world of competition their priority is to provide

competitiveness. Among the locations, the semi-urban area comes first

in this regard (92.59 per cent). In region wise analysis also creation of

Provide competitiveness

78.57 92.59 76.92 83.58

Total

100 100 100

100.00

competitiveness is the basic reason for not supporting nationalisation

(90 per cent).

Similar questions were asked to bank customers also regarding

Nationalisation. The data furnished in Tables 6.59 and 6.60 give the

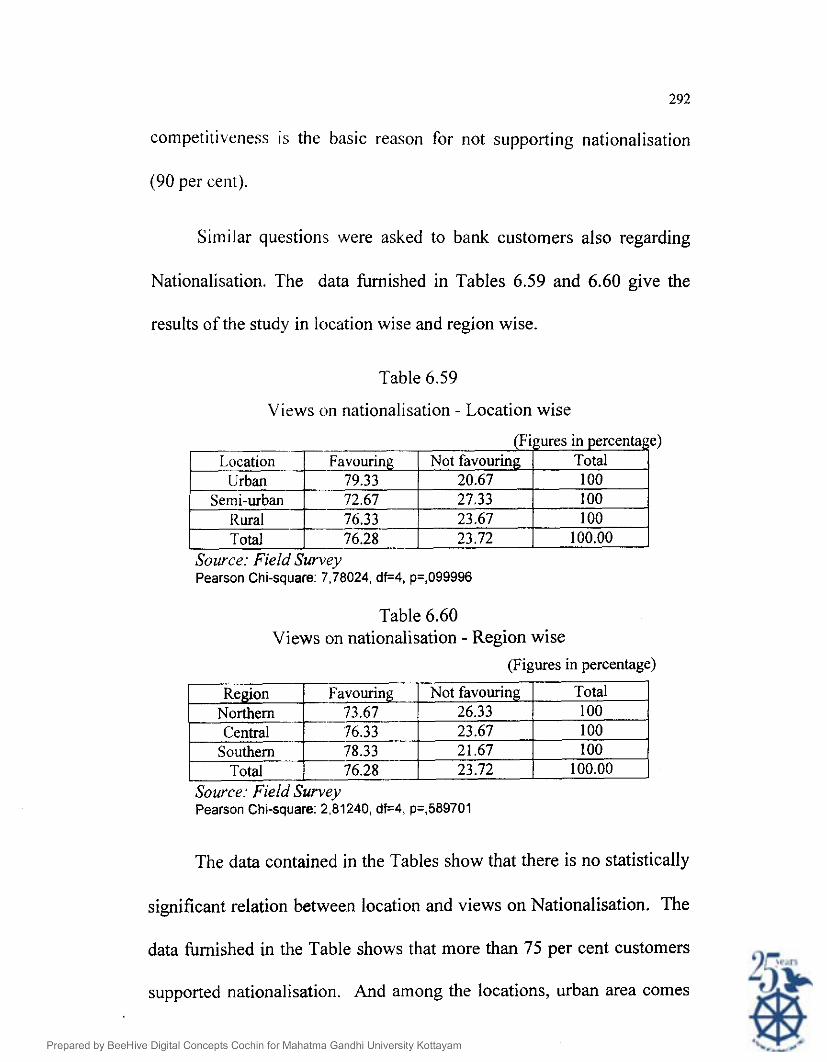

results of the study in location wise and region wise.

Table 6.59

Views on nationalisation - Location wise

Table 6.60 Views on nationalisation - Region wise

(Figures in percentage)

(Figures in percentage)