atlantic energy group washington, d.c. 10 jan...

TRANSCRIPT

November 20, 2012 1

Richard O’NeillChief Economic Advisor

Federal Energy Regulation [email protected]

Atlantic Energy GroupWashington, D.C.

10 Jan 2008Views expressed are not necessarily those of

the Commission

November 20, 2012 2

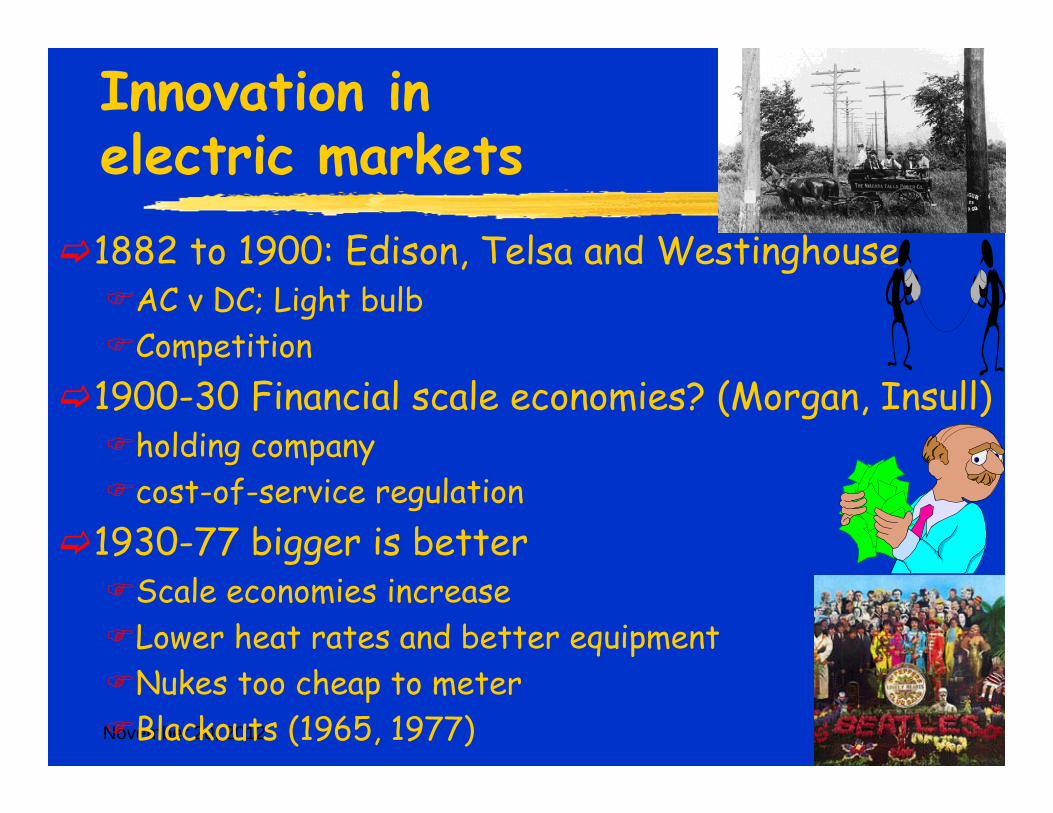

Innovation in electric markets

1882 to 1900: Edison, Telsa and WestinghouseAC v DC; Light bulbCompetition

1900-30 Financial scale economies? (Morgan, Insull) holding companycost-of-service regulation

1930-77 bigger is betterScale economies increaseLower heat rates and better equipmentNukes too cheap to meterBlackouts (1965, 1977)

November 20, 2012 3

for nuclear plants under cost-of-service regulation

November 20, 2012 4

Policy choicescirca 1977

Cost of service regulation isn’t working wellExcess capacity and blackoutsHigh costs

Let’s try market-based regulationProperly shifts riskStronger incentives

1978 PURPA produces independent powerPhysically possibleNon-Goldilocks prices: too high or too low

November 20, 2012 5

Technology eliminates some market failures 1980-2007

Computing hardware and softwareCommunication: fiber optics and the Internetvertical integration not required: ISOsallows the load to participate in the marketSmart grid [Who could ask for more]Faster response

Energy marketGenerator size small compared to marketQFs and IPPs

Market design: cost-based to market-based

November 20, 2012 6

Non-nukes sold at an average of twice bookNukes sold at less than 15% of bookWas this a mistake?Would these units be achieving the current

load factors and profits if not sold off? Do more efficient units lower the LMP? yes Should the ‘buy back’ contracts been longer?What should be done now? Redo?

November 20, 2012 7

Empirical mud slinging

Everyone has his/her counterfactual.Everyone has his/her factual!!!!!Is this displaced aggression?What if natural gas prices fell?What happens with a large carbon tax or a

renewable mandate?would ISOs and LMPs cause the resulting

prices?

Technical analysis can be fun

November 20, 2012 8

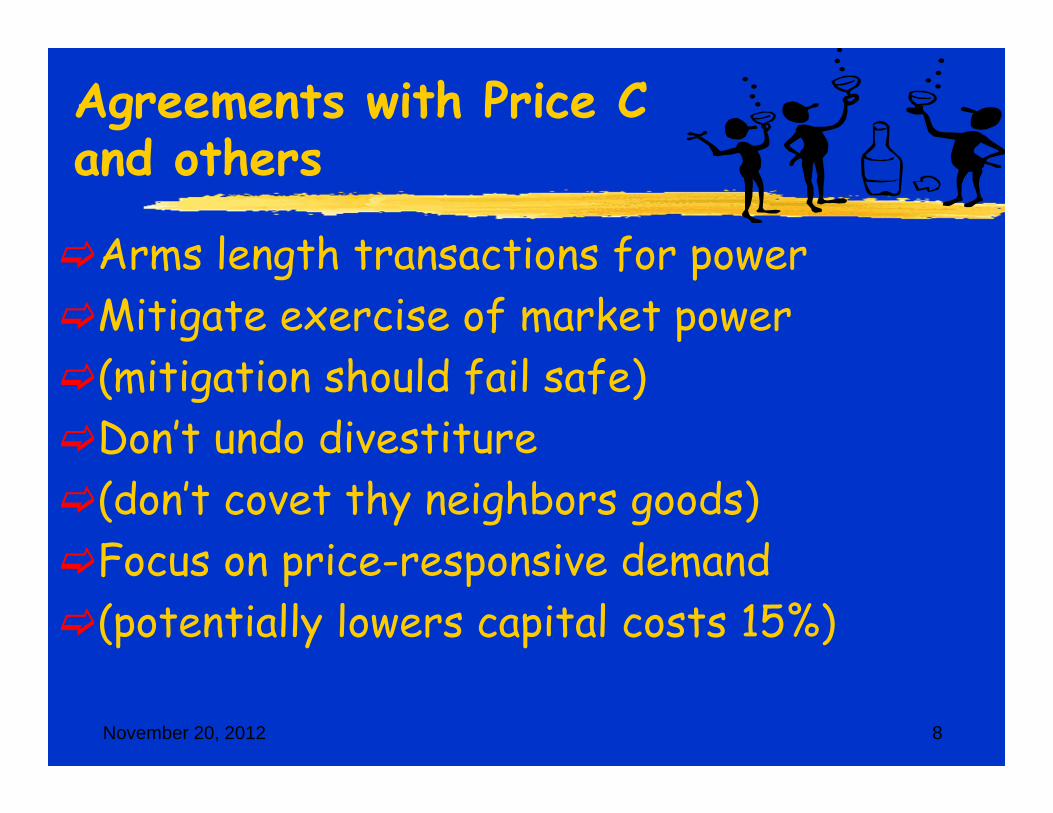

Agreements with Price C and others

Arms length transactions for powerMitigate exercise of market power(mitigation should fail safe)Don’t undo divestiture(don’t covet thy neighbors goods) Focus on price-responsive demand (potentially lowers capital costs 15%)

November 20, 2012 9

Myths and Shibboleths(truth)

FERC has deregulated (FERC has not deregulated anything)Broad socialization does not work(beneficiaries pays does)FERC discourages long term contracts(FERC encourages long term contracts)Deregulation caused the 2003 blackout(a day-two ISO would have prevented the blackout)ISOs are expensive (ISOs are cheap)

November 20, 2012 10

Myths and ShibbolethsCentral planning works better than marketsPrice volatility can be suppressed(Price volatility can be hidden or hedged)Static market shares indicate market power(the market can change and ISOs mitigate hourly)Pay-as-bid will lower prices (it will raise risks then prices )Risks should be borne by consumers(Can we avoid the next round of stranded costs?)

November 20, 2012 11

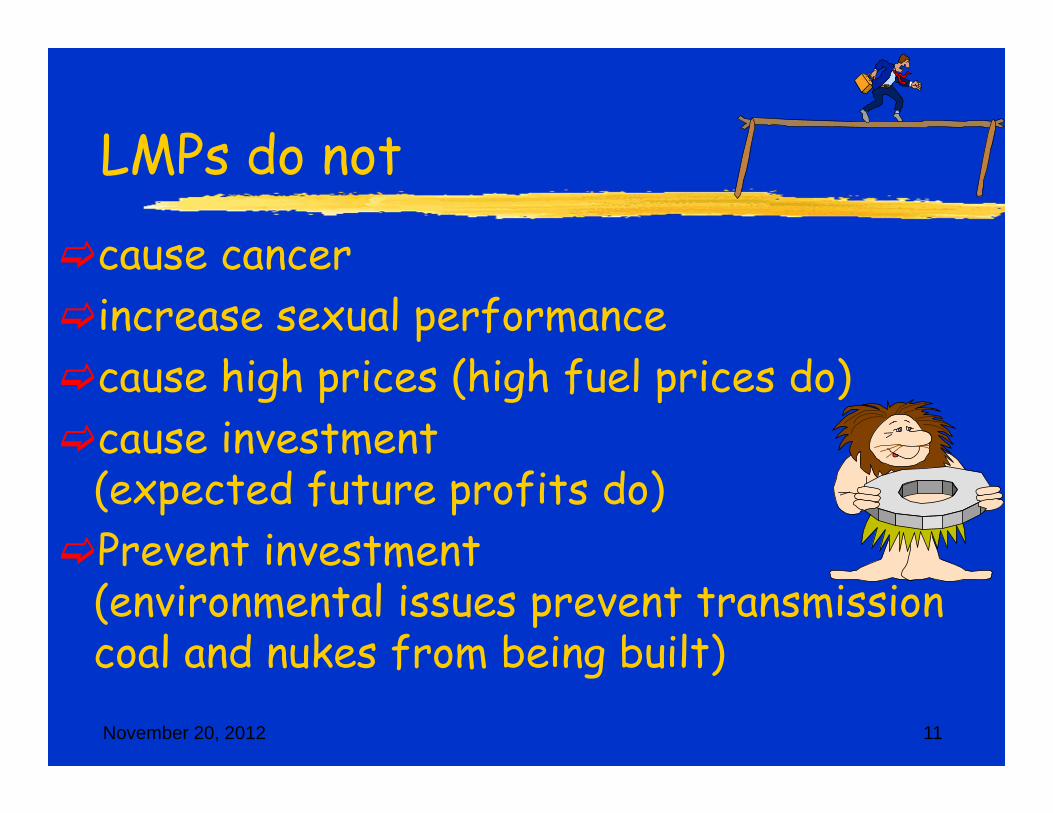

LMPs do not

cause cancerincrease sexual performancecause high prices (high fuel prices do)cause investment

(expected future profits do)Prevent investment

(environmental issues prevent transmission coal and nukes from being built)

November 20, 2012 12

electric end use prices (EIA)

6

7

8

9

10

1960 1965 1970 1975 1980 1985 1990 1995 2000 200year

real

(200

0$) p

rice

Did LMPs cause the 1970 to 1982 price increase?

November 20, 2012 13

UK

November 20, 2012 14

ISOs, LMPs, Efficiency and green power

transparencyAllow better integration of all resourcessolar and wind need real-time ISO markets to

realize full valueWind needs a large real-time balancing marketsolar’s highest output is during peak Send good short term price signals Improve short term efficiency

November 20, 2012 15

Analogies and their problems

analogy ownersCommodity/conduit

Displacement network

other issues pricing

highways public unbundled No congestion Gas tax and toll roads

water public bundled yes other uses usage

Natural gas

private unbundled yes storage and valves

Price caps and no withholding

Air traffic

public unbundled no No pricing Ticket tax

parks public unbundled no congestion Income tax

telecom private mixed No Busy signal Price caps

railroads private bundled no congestion Loose price caps

November 20, 2012 16

Structure conduct performance

StructureNumber of competitorsEntry Access rules

conduct Market power mitigation

PerformanceEfficiencyinnovation

Structure/regulation

cost-of-service

Market-based rates

competitors none one or moreEntry/Access hard easier

Conduct: market power mitigation

Price caps Bid capsAllocate fixed costs

Mitigate bids in an auction

Performance incentives incentivesEfficiency Weak strongInnovation Weak!!!!!!!!!! strong

November 20, 2012 17

ISO Competition Issues

Short-termVertical market power: ISO control Horizontal market power: bid mitigation

Long-term Entry barriersgenerationtransmission Price-responsive demand

Contracts differing expectations

November 20, 2012 18

The Coase paradox: Are efficient markets ‘free’?

“All exchanges regulate in great detail the activities of those who trade in these markets

these exchanges often used by economists as examples of a perfect competition,

for anything approaching perfect competition to exist, an intricate system of rules and regulations would be normally needed.

explanation for these regulations: that they exist in order to reduce transaction costs

Those operating in these markets have to depend, therefore, on the legal system of the State."

Coase, R.H. (1988), ‘The Firm, the Market and the Law’, in The Firm,

the Market and the Law, Chicago, U. of Chicago Press

November 20, 2012 19

What is needed for efficiency and innovation?

good information and market designmitigation of market powerrecognition of how electricity works understand the choicesfree market

market with market rulesadministrative rules

Regulation should encourage innovation and efficiency

November 20, 2012 20

What are the results of ISOs and market-based rates in first ten years

The ghosts of ISOs and

market-based rates past

November 20, 2012 21

Failed market designsZonal markets (Cal, PJM, NE, UK)Prohibit long-term contracts Sequential markets for energy and anc servicesOne settlement systemsInfeasible markets (Cal PX and UK)Ignore non-convexities (start-up and no-load) Ignore market powerall ended in administrative intervention

November 20, 2012 22

Market Design that works

Locational (locational marginal prices)Bid-based dispatchCo-optimizationEfficiencyreliability

Market power (bid) mitigationFreedom of ‘bilateral’ contractsLong term contractingShort-term contracting

November 20, 2012 23

Generation Capacity (up to 4 years) ensure Adequate compensation generation adequacy for reliability Call option in spot market

Transmission rights (up to 10 years) hedge transmission congestion costsOptions and obligations based on difference in LMPs

Day-ahead (24 hours): scheduling market efficiently and reliability (from bids) schedule generation, load and,

transmissionReal-time (5 Minutes): balancing market

efficiently and reliability (from bids) dispatch generation, load and transmission ancillary services

Freedom of bilateral contracting and opt out of above

November 20, 2012 24

Market Monitoring and Mitigation

analyze market design and market powerCorrect market designGive must run contracts for reliability

Ex ante mitigation in ISO is the generator bidding above marginal costs?If so mitigate to marginal costs plus error

Investigate physical withholdingphysical withholding: not available at rated capacity. good reason: scheduled maintenance or forced outagePenalties for violations physical withholding

November 20, 2012 25

Some numbers

Factsand

Counter facts

November 20, 2012 26

November 20, 2012 27-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

1990 1992 1994 1996 1998 2000 2002 2004

Cap

acity

Fac

tor I

ncre

men

t ove

r 199

0

All other units

Divested units

Capacity factors at nuclear plants

November 20, 2012 28

Recent studies are confirming the theory

Bushnell and Wolfram, “Ownership Change, Incentives and Plant Efficiency: The Divestiture of U.S. Electric Generation Plants,” 2006after divestiture ~2% lower heat rates.nationwide $4 billion per year.helps achieve environmental goals

Mansur and White, “Market Organization and Market Efficiency in Electricity Markets,” 2007 Examine PJM market expansion.Dramatic increase in flows from inexpensive in the

Midwest to classic PJM.savings of $180 million per year.

November 20, 2012 29

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

Non

fuel

Exp

ense

Gro

wth

Rel

ativ

e to

198

1

MUNI Plants

IOU: Non-restructured States

IOU: Restructured States

Figure 2: Nonfuel Expense Trends by Company Type and Restructuring Status

November 20, 2012 30

Results of ISOs and market-based rates in first ten years

More competitionLower heat rates Higher capacity factors Lower labor costsHigher profits for efficient generatorsHigher trading efficiencyBetter dispatch softwareBetter reliability software

November 20, 2012 31

What happens in next ten years?

The ghosts of ISOs and

market-based ratesfuture

November 20, 2012 32

Improvements in MIP (same hardware)

one day unit commitment problemyear Cplex version Time in sec B&B nodes1993 2.2 1646 (unsolved) 1107922007 11.0 1.1 75

And though the holes were rather small they had to count them all

one week unit commitment problemYear Cplex version Time in sec B&B nodes1998 6.0 8000 (unsolved) 44900

2007 11.0 103 2220Eight days a week is not enough to show I care.

November 20, 2012 33

Real-time market Survey ResultsLet me tell you how it will be

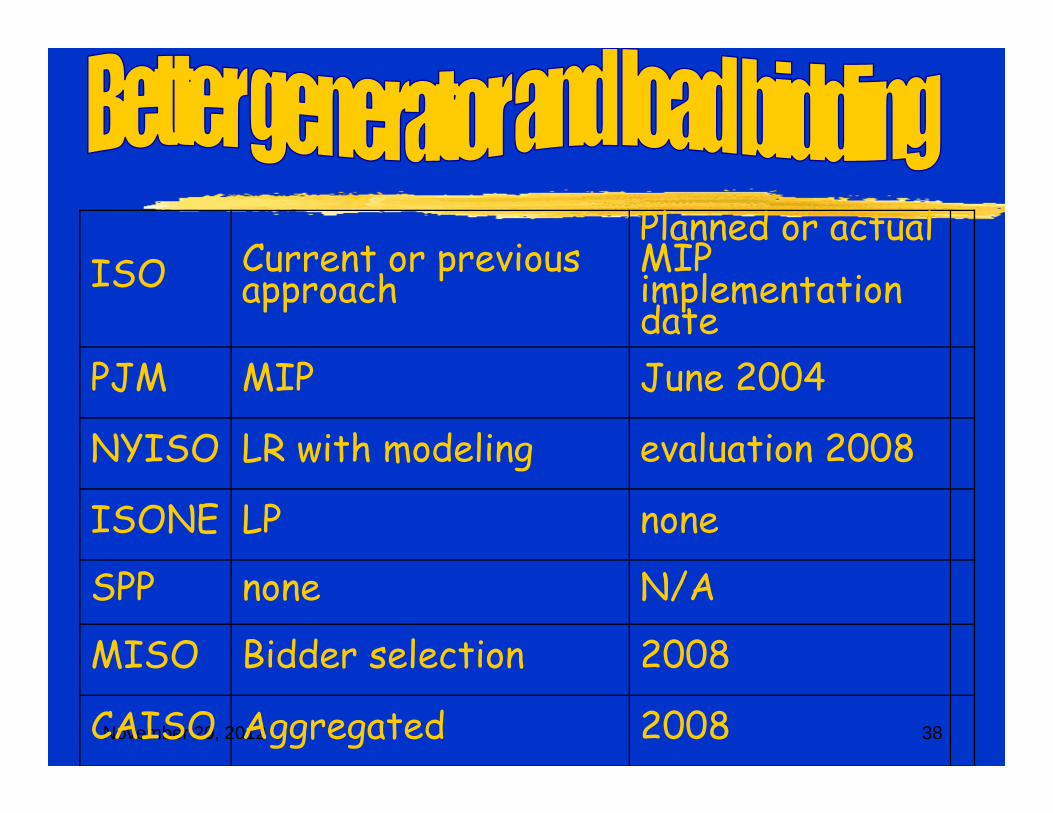

ISO Current or previous approach

Date or planned date of MIP

Estimated savings on an annual basis

PJM MIP 2006 $100 millionISONE LR/LP 2008 No estimateSPP LP none N/ANYISO LR/LP none N/AMISO judgment with LR 2008 No estimateCAISO LR. 2008 ~$1 million

November 20, 2012 34

End-use marketsgot to get you into my life

Vertical demand curve in ISO marketsConsumers receive very weak price signalsSee monthly average priceNo real time meter; No real time priceOn a hot summer day wholesale price = $1000/MWHRetail price = $100/MWH

Solution: real time pricing and Demand-side non-convex (MIP) bidding

Two-sided market using MIP!!!!!!!!!

He's as blind as he can be just sees what he wants to see

November 20, 2012 35

day-ahead market Survey ResultsLet me tell you how it will be

ISO Current or previous approach

Date or planned date of MIP-based implementation

Estimated savings on an annual basis

PJM LR 2004 $60 Million

ISONE LR/LP 2008 None

SPP N/A N/A N/A

NYISO LR/LP none N/A

MISO LR 2008 None

CAISO LP 2008 $23 million

November 20, 2012 36

Market Benefits of MIP ImplementationPJM Day Ahead Market uplift Costs 2003-2007 ($/MWh Load)

-

0.25

0.50

Jan-

03Fe

b-03

Mar

-03

Apr

-03

May

-03

Jun-

03Ju

l-03

Aug-

03Se

p-03

Oct

-03

Nov

-03

Dec

-03

Jan-

04Fe

b-04

Mar

-04

Apr

-04

May

-04

Jun-

04Ju

l-04

Aug-

04Se

p-04

Oct

-04

Nov

-04

Dec

-04

Jan-

05Fe

b-05

Mar

-05

Apr

-05

May

-05

Jun-

05Ju

l-05

Aug-

05Se

p-05

Oct

-05

Nov

-05

Dec

-05

Jan-

06Fe

b-06

Mar

-06

Apr

-06

May

-06

Jun-

06Ju

l-06

Aug-

06Se

p-06

Oct

-06

Nov

-06

Dec

-06

Jan-

07Fe

b-07

Mar

-07

Apr

-07

May

-07

Jun-

07Ju

l-07

Aug-

07Se

p-07

Oct

-07

$/M

Wh

Load

Lower cost to maintain operational reliability

Lower uplift payments

November 20, 2012 37

Linear Residual Demand and Local Optimal Solutions

Equilibrium Points - Local Optima

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

0 100 200 300 400 500 600 700

Quantity

Net

Ben

efit

-$20

-$10

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

Mar

gina

l Cos

t

Total Benefits Local Optima Marginal Costs Derived Demand Equilibrium Points

‘eco min’Happy ever after in the market place

November 20, 2012 38

ISO Current or previous approach

Planned or actual MIP implementation date

PJM MIP June 2004

NYISO LR with modeling evaluation 2008

ISONE LP none

SPP none N/A

MISO Bidder selection 2008

CAISO Aggregated 2008

November 20, 2012 39

Open or close circuit breakers using DCOPFIEEE 118 bus provided 25% savingsN-1 for IEEE 118 & RST 96 system showed

savings from 1% to 16%ISONE networks ranged from 5% to 15% savings or $500 Million annual (all solutions have gaps so higher savings may be found)

November 20, 2012 40

Benefits of better market modelingSay the words you long to hear

Benefit/cost can be over 100Bid modeling: CCCT ‘forbidden zones’Topology estimators for reliability:

pricelessBetter reactive power modeling and

marketsTransmission dispatch: 5 to 24% savingsBetter incentives for transmission Worldwide: $10 to $200 billion/year

“A new scientific truth does not triumph by convincing its opponents and making them see the light, but rather because its opponents eventually die, and a new generation grows up that is familiar with it.”

Max Planck, “Scientific Autobiography and Other Papers”

“The magical mystery tour is waiting to take you away,Waiting to take you away. “