at 3,/c ,- - world bankdocuments.worldbank.org/curated/en/936211468267320712/...acc - associated...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

At 3,/c ,- /A/

Report No. 8422-IN

STAFF APPRAISAL REPORT

INDIA

CEMENT INDUSTRY RESTRUCTURING PROJECT

APRIL 10, 1990

Industry and Finance DivisionAsia IV Country Department

This document has a restricted disttibution and may be used by ecipients only in the performance oftheir oflicial dudes. Its contents may not othenwise be disdosed without Wodd Bank auhOt

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTSRs 1 - US$ 0.059Rs 17 - US$ 1.00

FISCAL YEARSGovernment of India - April 1 - March 31IDBI - April 1 - March 31ICICI - April 1 - March 31

WEIGHTS ANID MEASURESMetric System

ABBREVIATIONS AND ACRONYMS

ACC - Associated Cement Companies, Ltd.AICD - Assam Industrial Development CorporationATI - Advanced Training InstituteBIFR - Board for Industrial and Financial RestructuringCCI - Cement Corporation of IndiaCMA - Cement Manufacturers AssociationCTI - Century Textile and Industries, Ltd.DANIDA - Danish International Development AgencyDCCI - Development Commissioner for Cement IndustryDFI - Development Finance InstitutionEIA - Environmental Impact AssessmentFOR - free on railGOI - Government of IndiaHED - Human Resource Development (Component)ICB - International Competitive BiddingICICI - Industrial Credit and Investment Corporation of IndiaIDBI - Industrial Development Bank of IndiaIMR - Industry Modernization and Restructuring (Component)JIL - Jaiprakash Industries, Ltd.MRTP - Monopolies and Restrictive Trade Practices ActNDC - Northeast Development Councilnm3 - Norm Cub'a MetersNVTS - National Vocational Training SystemOPC - Ordinary Portland CementPBCT - Pilot Bulk Cement Transport (Component)PC - Program CoordinatorPPC - Pozzolana Portland CementPSC - Portland Slag CementRBI - Reserve Bank of IndiaRITES - Rail India Techno-Economic ServiceRTC - Regional Training CenterSAIL - Steel Authority of India, Ltd.SC - Steering CommitteeSFC - State Financial CorporationSIDC - State Industrial Development CorporationSOE - Statement of ExpenditureSPCB - State Pollution Control BoardTA - Technical Assistance (Component)TISCO - Tata Iron and Steel Companytpd - ton per daytpy - ton per year

FOR OMCIL USE ONLYINDIA

CEMENT INDUSTRY RESTRUCTURING PROJECT

Lsoan and Prolect Summary

Borrower: India, acting by its President

BenefiLiaries: Industrial Development Bank of India (IDBI); theIndustrial Credit and Invastment Corporation of IndiaLimited (ICICI) and Office of Development Commissionerfor Cement Industry (DCCI).

Loan Amount: $300 million equivalent.

Terms: The loan would be made at the Bank's standard variableinterest rate and would be repaid over 20 yearsincluding 5 years of grace.

Relending Terms: The Government of India (GOI) would utilize theproceeds of the loan as follows:

Part A: GOI would relend $298 million equivalent ofthe Bank loan in rupees to IDBI and ICICI in equalproportions to finance part of the Industry Moderniza-tion and Restructuring component and the Pilot BulkCement Transport component. The relending rate fromGOI to IDBI and ICICI would be 12 percent p.a. Theon-lending rate to subborrowers from IDBI and ICICIwould be development finance institutions' (DFI) termlending rate, currently 14 percent p.a. GOI wouldbear the foreign exchange and interest rate risks.

?axrt : GOI would provide $1.6 million equivalent ofthe Bank loan as budgetary allocations through DCCI tofinance part of the Human Resource Developmentcomponent.

Zart C: GOI would provide $400,000 equivalent of theBank loan as budgetary allocations to DCCI to financepart of the Technical Assistance component.

Irotect Description: The proposed project is designed to support cementindustry restructuring following the complete decon-trol of pricing and elimination of freight equaliza-tion for cement, implemented 1:, the Government inMarch 1989. The project has the following components-(a) the Industry Modernization and Restructuringcomponent, which would finance capacity expansion incement-deficit regions and modernization andrestructuring of existing cement companies throughoutIndia, and assist the industry in adjusting to a

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

competitive environment; (b) the Pilot Bulk CementTransort component, which would help establish andfinance a pilot bulk cement transport system includingloading facilities at participating cement plants,special bulk cement rail wagons, and unloading anddistribution systems at Kalamboli Railway Terminalnear Bombay; (c) the Human Resource Developmentcomponent, which would assist and finance a demand-driven, in-plant training system at selected regionaltraining centers (RTC) to be established, at respect-ive lead plants, for groups of cement plants havinggeographic proximity; and (d) the Technical Assistancecomponent, which would assist DCCI in studying policyoptions for the mini-cement sector, coal washery anduse of lignite for the cement industry, environmentalprotection and pollution control measures for theindustry, and future bulk cement transport andapplications.

Benefits and Risks: The project would improve the regional productionstructure by adding about 5 million tpy productioncapacity in the cement-deficit regions, bringslgnificant savings in cement transport and reduce thecost of this vital commodity in some of the poorestregions of the country. The project would supportmodernization and restructuring of existing cementcompanies, thereby reducing energy and other produc-tion costs and improving the economic efficiency ofoperations. The project would finance installation ofpollution control equipment, ensure better environ-mental assessments, and encourage productive use ofslag, a waste product from steel plants which must bedisposed of in an ecologically acceptable ma-ner.Financing the pilot bulk cement transport componentwould pave the way for significant efficiency improve-ment in the cement distribution system and produc-tivity increase in the construction industry. Theproject would also finance training programs foroperating personnel and environmental professionals inmuch-needed skill categories for both new plants andexisting plants under modernization. No unusual riskshave been identified in subprojects in the proposedpipeline under the Modernization and Restructuringcomponent. Introducing a bulk cement transport systemrequires the development of a new marketing anddistribution systems and involves many players withsubstantial investment: it is therefore inherentlyrisky. Measures designed to minimize risk are theprovision of limited bagging facilities at theunloading terminal, phased implementation of theproject, and the provision of further technicalassistance for market development of bulk cement. Im-plementation of the Human Resource Development com-ponent is likely to be slow due to the innovativenature of the approach and the necessity of having

- iii -

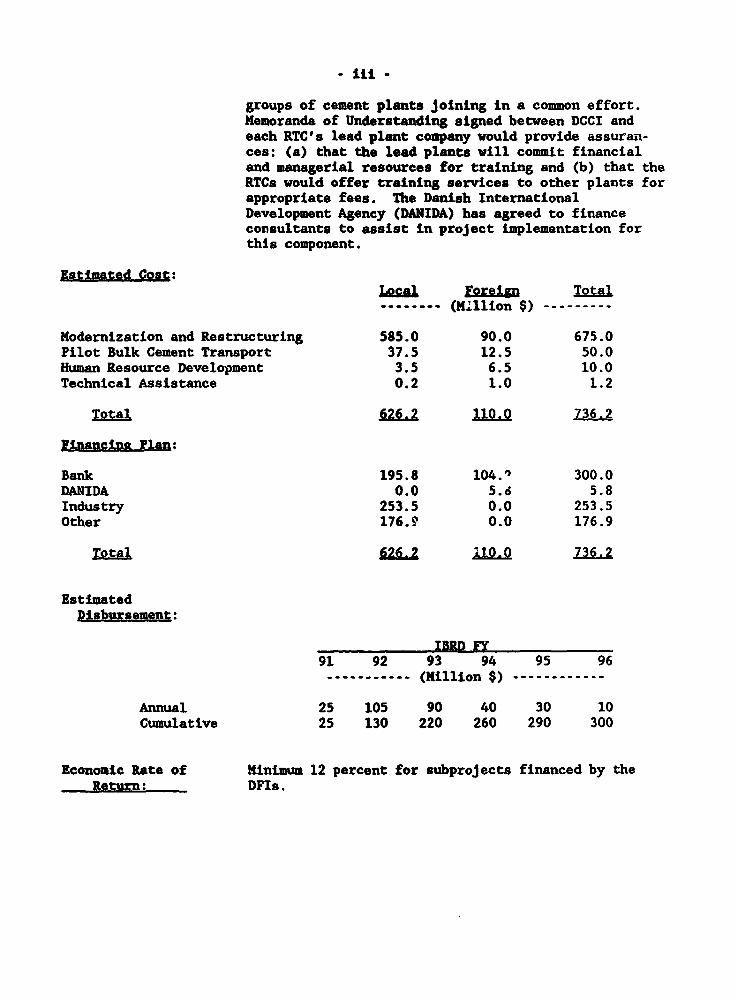

groups of cement plants joining in a common effort.Memoranda of Understanding signed between DCCI andeach RTC's lead plant company would provide assuran-ces: (a) that the lead plants will commit financialand managerial resources for training and (b) that theRTCs would offer training services to other plants forappropriate fees. The Danish InternationalDevelopment Agency (DANIDA) has agreed to financeconsultants to assist in project implementation forthis component.

Estimated Cost:J&cal Foreign Total-...---- (M'llion $)-------

Modernization and Restructuring 585.0 90.0 675.0Pilot Bulk Cement Transport 37.5 12.5 50.0Human Resource Development 3.5 6.5 10.0Technical Assistance 0.2 1.0 1.2

Total 626.2 110.0 736.2

Financing Plan:

Bank 195.8 104.1 300.0DANIDA 0.0 5.6 5.8Industry 253.5 0.0 253.5Other 176.9 0.0 176.9

Total 62672 110.0 736.2

EstimatedDisbussement:

IBRD FY91 92 93 94 95 96----------- (Million $) ------------

Annual 25 105 90 40 30 10cumulative 25 130 220 260 290 300

Economic Rate of Minimum 12 percent for subprojects financed by theReturn: DFIs.

INDo

CEMENT INDUSTRY RESTRUCTURING PROJECT

STAFF APPRAISAL REPORT

Table of Contents

I. INTRODUCTION ................................................... 1

II. INpIAN CEMENT MANUFACTURING INDUSTRY ....... ...................... 2

A. Present Structure of the Industry ......... ............... 2B. Past Policy Environment and Its Impact ...... ............. 4C. Policy Reforms and Industry Responses ...... .............. 5D. Economic Considerations .................................. 7E. Demind and Supply Projections .......... .................. 9

1II. RESTRUCTURING OF THE CEMENT INDUSTRY AND ROLE OF THE BAK ........ 14

A. Cement Industry Restructuring Strategy ..... ............. 14B. Bank Lending to Industry ................................ 19

IV. THE PROWECT AND THE PROPOSED LOAN .I.............................. 22

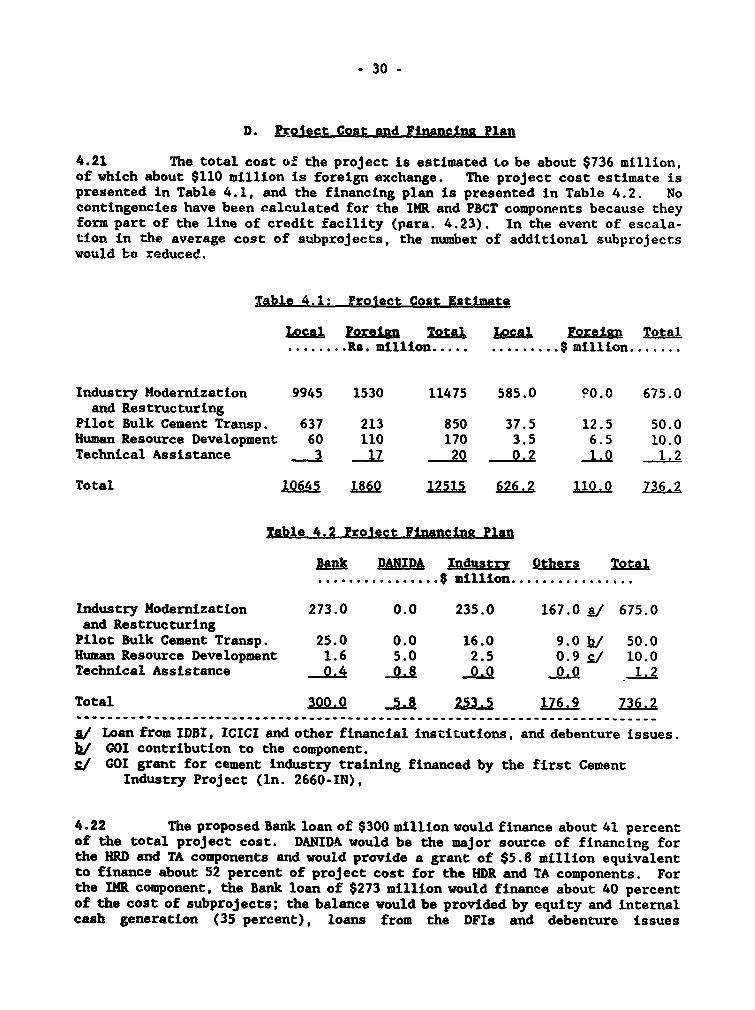

A. Project Objectives ...................................... 22B. Project Description ..................................... 22C. Environmental Aspects of the Project ..... ............... 27D. Project Cost and Financing Plan ......................... 30E. The Loan ............ .................................... 31F. Procurement ........... .................................. 32G. Disbursement .......... .................................. 34H. Reporting and Audits .................................... 34

This report is based on the findings of a World Bank appraisal mission whichvisited India January 8-29, 1990. Mission members were Messrs. S. Wu(Financial Analyst), M. Fog (Senior Cement Industry Specialist), M. Pherwani(Senior Industrial Specialist), W. Futur (Senior Economist), J. Segerstrom(Technical Education Specialist), T. Loomis (Environmental Consultant),0. P. Hansen (Senior Advisor, DANIDA), M. Bregnbak (Technical Adviser,DANIDA) and A. Austen (Consultant). Mr. G. Thomas (Consultant) also joinedthe mission as a resource person. The report was prepared by Messrs. S. Wu,M. Fog, M. Pherwani, W. Futur and J. Segerstrom.

V. IMPLEKEKTATION AR GME S. PARTICIPATING ORGANIZATIONS.AND PROJECT BENEFITS AND RISKS . .................................. 36

A. Development Commissioner for Cement Industry ..... ............. 36B. Participating Financial Institutions .......................... 36C. Organizational Arrangements for Human Resource Development

Component ..................................................... 41D. Project Benefits and Risks ......... ........................... 42

VI. AGREEMENTS. UNDERSTANDINGS AND RECOMMENAIO ..... ............... 44

A. Agreements and Understandings ................................. 44B. Conditions of Effectiveness and Disbursement ...... ............. 45C. Recommendation . ............................................... 45

ANNEXES

Annex 1 Input Costs Increases ............. ............................ 46Annex 2 Shadow Prices and Conversion Factors .......................... 47Annex 3 Projection of Cement Production ............................... 50Annex 4 Technical Assistance Component ................................ 52Annex 5 Guidelines fc. Preparing Environmental Impact Assessments for

Major Cement Subprojects ........... ........................... 54Annex 6 Disbursement Schedule and Projection .......................... 58

STAFF APPRAISAL REPORT

IzD

CEMENT INDUSTRY RESTRUCTURING PROJECT

I. IN!RODUCTION

1.01 Policy reform in the cement sector in the 1980s comprised phaseddecontrol of cement pricing and distribution and relaxation in industrial re-gulatory controls. These reforms have resulted in impressive growth andsubstantial modernization of the industry. Cement production grew from18 million tons in 1980 to about 43 million tons in 1988. Cement supply insevere shortage only ten years ago, has now caught up with demand and createda competitive cement market. India now produces cement at a cost below thelanded import price and has begun to export a limited amount of cement toneighboring countries. The current per capita consumption of cement ir. Indiais about 47 kg, low in comparison with other developing countries of similarincome. There is immense scope for cement consumption growth, as the cement-consuming sectors (irrigation, power and housing) continue to expand. Thesituation presents an excellent opportunity for the development of a modern andefficient cement industry in India.

1.02 In its 1989 budget, the Government of India (GOI) announced the com-plete removal of price and distribution controls for cement. This policy deci-sion has eliminated all subsidies to cement users in the public sector and allcross-subsidies relating to freight equalization and differences in levy quotasamong cement manufacturers, and it has provided an environment that is conduciveto rational investment and increased efficiency in cement production anddistribution. The sustainability of liberalization and further improvement ofeconomic efficiency in this sector will depend on the industry's ability to ad-just, through industrial restructuring, to the new and more competitiveenvironment. To support the adjustment process in this recently liberalizedsubsector, GOI requested the Bank and the Danish International Development Agency(DANIDA) to prepare the Cement Industry Restructuring Project.

1.03 The proposed project would finance production capacity expansionsin the cement-deficit regions and modernization and restructuring of the existingcement companies throughout India. The project would help to establish andfinance demand-driven, in-plant training programs to support human resourcedevelopment compatible with the substantial technological and structuraltransformation in the industry. The project would also help develop and financea pilot scheme for transporting cement in bulk from a number of plants toKalamboli Railway Terminal near Bombay. Successful implementation of this pilotscheme would introduce bulk movement of cement across the country, and potentialproductivity improvement for the construction industry. Finally, the projectwould assist DCCI in studying policy options for the mini-cement sector, coaiwasheries and use of lignite for the cement industry, environmental protectionand pollution control measures for the industry, and future bulk cement transportand consumption. Overall, the proposed project is expected to enhance theindustry's economic efficiency and pave the way for sustained growth to meetincreasing demand in the 1990s.

- 2 -

II. ITDIAN CEMENT MANUFACTURING INDUSTRY

A. Present Structure of the Industrv

2.01 Production Structure. The Indian cement industry has achievedconsiderable success in establishing adequate production capacity. As of March1988, this industry consisted of 94 large and medium-size plants, 5 white cementplants and 135 mini-cement plants (i.e., clinker capacity less than 200 tpd).The large and medium-size plants produced 37 million tons of cement in 1987,95 percent of the total cement production in the country. The mini-cementplants, although large in number, produced less than 2 million tons (less than5 percent of total production) in the same year. About 25 million tons ofenergy-efficient, dry-process production capacity was added during theunprecedented growth which followed partial decontrol in 1982. As a result,the share of installed capacity based on the dry process increased from53 percent in FY83 to 72 percent in FY88. With the expected further expansionin dry-process capacity and completion of a number of major wet-to-dry conversionprojects in 1989 and 1990, about 80 percent of the country's cement productioncapacity will be based on the dry process. By 1988, around 26 percent of theinstalled production capacity was in plants of one million ton per year, a scalethat is considered optimal based on today's technology. All new plants will beof this scale in the coming years. Conversion of the remaining wet-processplants to dry process, and expansion and modernization of old plants to reachoptimal economies of scale and production technology will continue as theindustry adjusts to the increasingly competitive market created by decontrol ofcement pricing and distribution.

2.02 Regional Distribution of Capacity. India's installed cementproduction capacity is concentrated in the western and southern regions, wherelimestone deposits are abundant and adequate supporting infrastructure (such asrail and road network) is available. In 1988, about 85 percent of cement wasproduced in the states of Madhya Pradesh (26.0 percent), Andhra Pradesh(13.8 percent), Rajasthan (11.3 percent), Tamil Nadu (9.3 percent), Gujarat(8.7 percent), Karnataka (8.9 percent) and Maharashtra (7.2 percent). Between1982 and 1988, the share of cement production in the western and southern regionsincreased from 68.8 percent to 74.8 percent. Conversely, not only did theproduction share of eastern states decrease from 13.6 percent to 6.9 percent,but also their production in absolute terms also decreased from 3.1 million tonsper year to 2.8 million tons, due to suspension of production of two plants inBihar. The regional cement production-consumption pattern for 1988 is presentedin Table 2.1. The regi-nal imbalance of production capacity and demandcontribute to high transpurt costs for the distribution of cement, which amountto an estimate of Rs. 8 billion per year.

2.03 Ownership Structure. The industry has been developed primarily bythe private sector. Private firms accounted for 84 percent of installed capacityand 87 percent of total cement production at tL. end of FY88. The publicsector's entry into the cement industry goes back several decades (the first suchplant was built in 1938), but significant capacity was not added until the late1960s and 1970s. At present, the public sector produces about 13 percent of

India's cement output (down from 14 percent in FY85), the Cement Corporation ofIndia (CCI) accounts for 5.7 percent, and 7 state government-owned companiesproduce the remaining 7.3 percent. Moreover, GOI has moved away from itsprevious policy of supporting large capacity expansions in the public sector;i.e., the Government has abandoned its previous objective of reaching 25 percentpublic ownership of total installed capacity by the end of Seventh Plan. Thedistribution of capacity and production of cement by type of ownership duringFY88 are summarized in Table 2.2.

Table 2.1

9eaional Production and Conwumption, Jj8

Production Consumplo Surnlus/(Deficit)

North 7.44 11.89 (4.45)East 2.81 7.10 (4.29)West 17.06 10.53 6.53South 1341 10.86 2.55Total 40.72 40.38 0.34

Source: Cement Manufacturers' Association (C_A) Cement Statistics 1988.

Regions are de ined as: West GuJarat, Maharashtra, Madhya Pradesh and Goa;'South: Andhr-. Pradesh, Karnataka, Tamil Nadu and Kerala; East: Bihar, Orissa,West Bengal and Northeastern states; North: Rajasthan, Uttar Pradesh and othernorthern states.

Table 2.2

Distribution of Canacity and Production

According to Ownership. 1987/88(In million tons)

Caoacitv gercent Production percentPublic SectorCCI 3.75 6.8 2.23 5.7State-owned 4.98 9_Q 2j.9 7.3Total 8.73 15.8 5.12 13.0

Private SectorACC 8.83 16.1 7.62 19.3Others A/ 37.38 6..1 26L68 67.7

Total 46.21 84.2 34.30 87.0TOTAL 54.94 100.0 39.42 100.0a/ Including mini and white cement plant but excluding Rohtas,

Sonevalley and Sewree which were closed down.

Source: CMA, Performance of Cement Industry, 1987/88.

- 4 -

B. Past Policy Environment and Its Impact

2.04 The industry grew ralatively slowly during most of the 1970s.Between FY70 and FY74 (the Fourth Plan), annual growth rates of capacity andproduction were 5.7 percent, and 3.7 percent, respectively. During the FifthPlan, capacity growth fell to 2.6 percent p.a. As a result, between 1978 and1983 the country experienced considerable shortage of cement (10-25 percent ofannual consumption) and had to import 1-3 million tons of cement per year. Theslow expansion of capacity and associated chronic shortages of cement experiencedduring the 1970s were caused by restrictive sectoral policies includingcontrolled prices, rigid capacity licensing and freight equalization fordistribution.

2.05 Price Control and Canacitv Licensing. For 40 years (1942-82),Indian cement prices had been were controlled by the Government, except for 1966and 1967. The pricing policy over this period fixed the retention price (theex-factory price of bulk cement) and the free on rail (FOR) destination priceof bagged cement. Freight cost, packaging and incidental charges, and exciseduties and sales taxes were then added to arrive at the retail price to theconsumer. These pricing policies had a serious adverse impact on the profitabi-lity of investment in the cement industry. The decline in the expansion ofcement production capacity during the Fourth and Fifth Plan periods was causedby the low return on investments because of controlled prices and to some extentthe restrictive capacity licensing policies toward large industrial houses (MRTPcompanies). In the 1970s, particularly during 1970-77, retention prices failedto provide an adequate return on investment in the sector, which resulted inconsiderable slowing of expansion capacity during the Fifth Plan p.riod. Thecombined impact of all these, together with low capacity utilization attributedto power and coal shortages, resulted in chronic shortages of cement throughoutthe 1970s.

2.06 Freight Egualization and Remional Distribution of Capacities. Thefreight equalization scheme was introduced in 1956 to ensure uniform cementprices throughout the country. A pooled average freight charge was built intothe free-on-rail (FOR) destination price of cement. Actual freight chargesincurred were notional in that they only helped to define the average freightcharge from all production locations. Under this system, cement transport froma given plant to the market was subsidized (or taxed) to the extent that actualfreight charges exceeded (or fell short of) the notional average freight chargesper ton of cement transported from all plants. Because of this policy, planningof cement production capacities gave little importance to location of markets.The cost of moving large volumes of cement to the eastern and northeastern states(cement-deficit regions) and coal in the opposite direction were not adequatelytaken into account when plant location decisions were made. This situation ledto unwarranted concentration of production of capacities in the western andsouthern regions where limestone deposits are abundant and better basicinfrastructure is more readily available (para. 2.02). The consequences of thisregional production pattern are painfully evident today following the decontrolof cement prices and the elimination of the freight equalization scheme. As

would be expected, cement prices in the deficit regions have risen sharply. Onthe other hand, given the sizable excess capacity, cement prices in the surplusregions are very depressed. This situation constrains the financial performanceof many cement producers in the surplus regions and cement users in the deficitregions.

C. Policv Reforms a#d ndustry Res2onses

2.07 Recent Reforms. Efforts to reform restrictive cement sector policiescommenced in 1976. Measures adopted in 1977 attempted to improve return oninvestment and stimulate creation of production capacities to meet growingdemand. Towards this objective, a decision was made to change the basis forfixing cement prices from the 14 percent pre-tax return on total capital employedto a 12 percent post-tax return on net worth. The higher expected return oninvestments associated with this new pricing principle was sufficient tostimulate investments in the cement secror in the late 1970s. In the meantime,the Government imported cement to cover the shortage and to keep competition andprice of cement in check. Subsequently, GOI took an important step to open thesector by allowing new entry and expansion of existing capacities by MRTPcompanies in the cement industry. As a result, by the end of 1981 about12 million tons of capacity expansion was under implementation for commissioningduring the early and mid-1980s. This major expansion, and the resulting easingof supply constraints, encouraged the Government to continue to liberalize itscement pricing and distribution policies leading to complete decontrol in March1989.

2.08 The timing of these policy reforms for the cement sector coincidedwith, and formed an integral part of, the general industrial policy liberaliza-tion in the country. Of all the measures taken, the most important for thecement industry were relaxation of investment licensing, permission for entryof MRTP companies, the gradual reduction and elimination ef the requirements oflevy cement, and elimination of the freight equalization scheme. These reformsallowed the industry to modernize and expand more easily in response to changingmarket conditions. Another important area of policy reform was the relaxationof foreign technology transfer and collaboration, which helped enhance thecompetitiveness of the domestic cement machinery manufacturing industry.

2.09 Industry Response. The cement industry responded well to thesepolicy reforms (Table 2.3). Installed capacity and production of cement haveexpanded by about 11 percent p.a. since 1982; the share of the energy-efficient,dry-process units increased from 53 percent to 72 percent, due to bothconversions from wet to dry process and installation of new capacities; acompetitive cement market has emerged, as seen in Table 2.3: the free market(non-levy) cement price remained practically constant below Rs. 70 per bag duringthe last 6 years. The intensity of market competition was reflected in thedeclining market share of pozzolana portland cement (PPC) from 57 percent in FY83to about 25 percent in FY88, as the consumers began to take advantage of thebuyer's market situation to demand higher-quality ordinary portland cement (OPC)at a price very close to that of PPC.

Table 2,3

Industry's Response to Recent Policy

Reform Policy Parameters

Policy Parameters 82/83 83/84 8I485 85Z86 87/88

Levy Quota ( percent)pre-1982 plants 67 65 60 40 30post-1982 plants 67 45 40 30 15Levy Price (Rs./ton)(ex-factory) 335 375 375 400 435

Industry ResRonse

Capacity (MT) 34.4 37.0 41.2 44.3 57.0Production (MT) 23.3 27.0 30.1 33.1 39.4Utilization (percent) 68 73 73 79 70

Nonlevy cement 68 64 70 67 70price (Rs/bag) a/

Dry-Process Capaci. 53 56 60 65 72as percent of total

PPC as percent of total 57.1 58.5 55.1 45.1 25cement output

Operating Profit 15.8 13.5 11.1 9.3 8.0Margin b/

a/ In 50 kg bag, including excise tax, sales tax, bagging costs, transport anddealers profit margin.

hi Based on ICICI financed sample plants.

Source: CMA, ICICI and staff estimates.

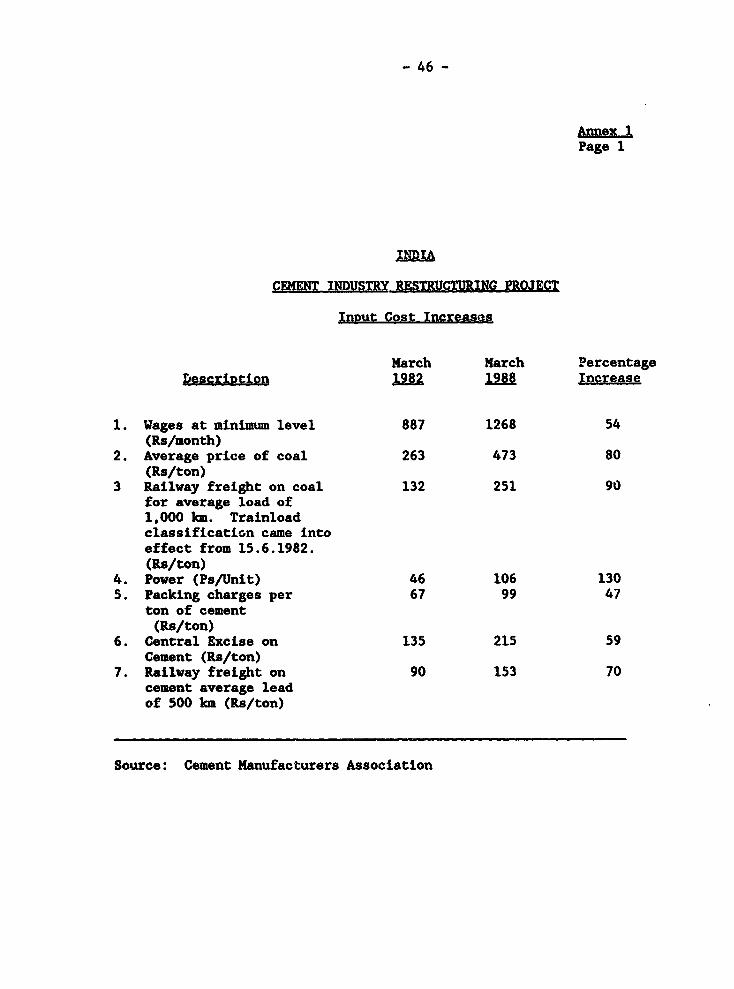

2.10 The industry fared less well in capacity utilization, partly becauseof power shortages caused by drought in 1985-87, initial technical difficultieswith some of the new plants, and market constraints for plants in surplusregions. An analysis of ICICI-assisted cement companies shows that the combinedimpact of low capacity utilization, competitive pressure and the significantincreases in the cost of inputs (Annex 1) have reduced the profitability of thecement industry. Many cement producers are experiencing serious financialdistress, and there have been only a few capacity expansion projects since 1986.Unless investments are undertaken now for commissioning between 1992 and 1995,India may experience cement shortage as demand expands and exceeds supplycapabilities (para. 2.21).

D. Economic Considerations

2.11 Although cement manufacturing is both capital- and energy-intensiveand India is a net importer of both, it is economic and efficient by interna-tional standardF India's comparative advantage is attributable to itsrelatively abundant limestone and coal resources, established labor force withtechnical and managerial experience, and a well-established and competent cementmachinery manufacturing industry with long-standing foreign technologycollaboration.

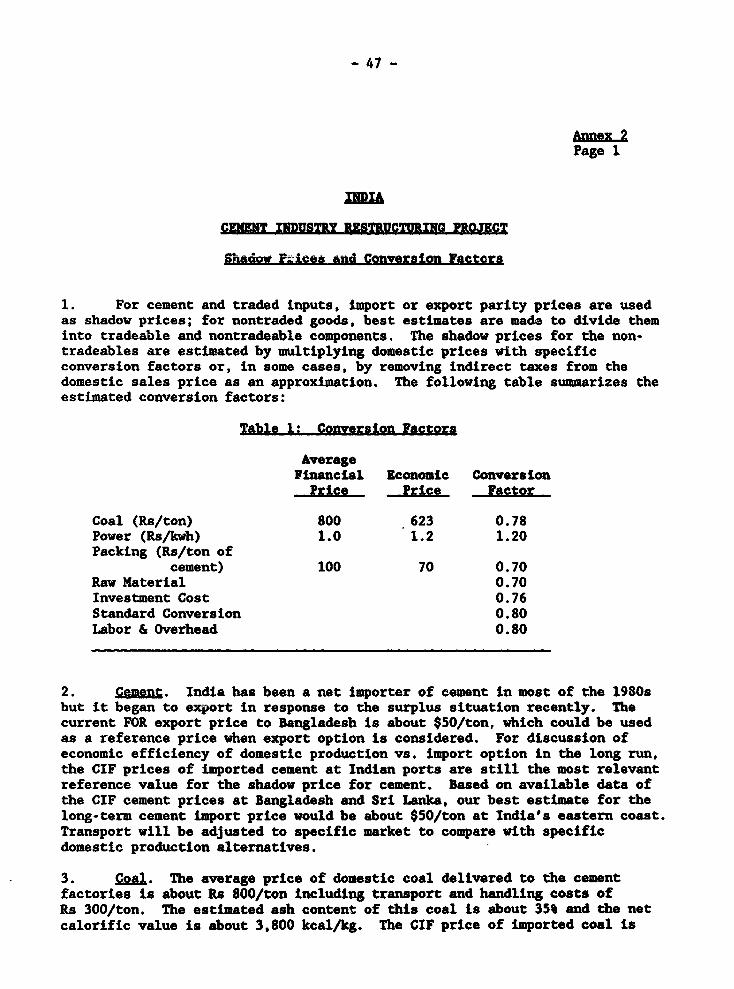

2.12 Production Cost. A sample financial and economic production coststructure of both wet-process and dry-process plants is shown in Table 2.4. Thefinancial costs are estimated on the basis of the average of the FY88 productioncosts of six cement plants (three dry and three wet plants). The economic costis derived from financial cost data using conversion factors estimated by theappraisal staff (Annex 2). In economic terms, the average production cost ofthe wet-process plants (excluding capital charges) is Rs. 567 per ton of cementcompared to Rs. 427 per ton for new, dry-process units. The full production costof new dry-process plants (including provisions for capital charges) is aboutRs. 580 per ton. These cost parameters are below the CIF value of importedcement estimated to be about Rs. 730 per ton ($50 at exchange rate of in FY88).This is a broad indication that domestic production of cement is economicallyefficient for meeting domestic demand.

Table 2.4: Financial & Economic Cost of Production(.Rs. per ton cement)

get Process Drv Process

Financial Economic Financial Economic

Raw Material 91.4 64.0 93.0 65.1Packing Materials 102.2 71.5 100.0 70.0Coal 189.6 166.8 110.5 97.2Power 107.2 128.7 98.5 118.2Store & Spares 38.1 28.9 34.5 26.2Labor 90.8 72.7 39.0 31.2Factory Overhead 43.4 339 23.5 18.8Operating Cost 661.7 566.5 499.0 426.8Capital Cost 64.4 A/ 134.5 A/ 152.8 /Total Cost 726.1 633.5 579.5

a/ Book value of depreciation and financial charges.k/ Replacement cost based on shadow price, Annex 2.

- 8 -

2.13 Imoorted Cement. Cement is imported only by government agencies(canalized). During the years of 1978-1984, when the cement shortage was mostacute, 001 allowed Imported cement at a low (15 percent) tariff rate to cover'he expected shortage and stabilize cement prices. Since 1985, the Governmentnas not imported cement (except special oil-well cement). Domestic productionis meeting demand, and domestic competition has kept the domestic price belowthe landed cost of imports, even in coastal cities like Bombay and Calcutta.The recent manufacturer's realizations (ex-factory price plus transport excludingexcise tax, sales tax and dealers margin) at Bombay and Calcutta were Rs. 750and Rs. 900 per ton, respectively. These prices ar. competitive with theprobable price of imported cement at port of Rs. 900/ton at today's exchange rate($50 CIF plus at least Rs. 50/ton port handling and distribution). Moreover,the Indian ports now are congested and lack bulk handling facilities. Therefore,expansion of domestic cement production capacity is the lowest-cost option formeeting domestic demand.

2.14 Capital Cost. Production of cement is an energy- and capital-intensive proce3s. As shown in Table 2.4, capital charges are the second largestcost item in the production cost of cement. India has acquired a comparativeadvantage in the manufacture of modern cement machinery and therefore has anadvantage in the construction of cement plants at international standards. Theaverage investment cost per annual ton of cement capacity installed in India isestimated to be within the range of $100-130, compared to $150-200 in developedcountries. This cost advantage is attributed to the existence of aninternationally competitive cement machinery manufacturing industry with reputedforeign technology collaborators. Competition among these manufacturers is sostrong that their foreign collaborators continue to transfer their latesttechnology to maintain and improve the market position of their local partners.Due to the combined effects of domestic competition and strong support fromforeign technology collaborators, the Indian cement machinery industry has amplecapability to supply turnkey cement plants with critical equipment imported fromtheir collaborators.

2.15 Raw Material. Limestone is the principal raw material in themanufacture of cement. The relative abundance of cement-grade limestone depositsin different parts of the country permitted development and rapid expansion ofthe Indian cement industry. At present, India's limestone reserves are estimatedat about 60 billion tons, of which 13 billion are proven, 4 billion are indicatedana 43.2 billion are inferred. India's limestone deposits are, however, highlyconcentrated within the states of Andhra Pradesh, Karnataka, Gujarat and MadhyaPradesh, which together account for over 80 percent of known reserves. Thisconcentration of deposits was originally responsible for the concentration ofcement production capacities in the western and southern regions of the country.But the freight equalization system intensified the regional supply-demandimbalance to an unwarranted degree (paras. 2.02 and 2.06).

2.16 EnergI Inputs. Energy is the most important input in the manufactureof cement in India. Although India is a net energy-importing country, it hasample coal reserves to meet the requirements of the cement industry for theforeseeable future. Indian coal is, however, low quality and must be transportedlong distances to cement plants in the western and southern states. The ashcontent of Indian coal is high and is expected to increase in view of thedeclining quality of known coal deposits and production methods being used.

- 9 -

Even though the cost of domestic coal per unit of energy contained is close tothat of imported coal, it has a negative impact on the quality of cement producedand the productivity of the cement industry. To overcome this problem, theindustry and GOI are exploring options to reduce the ash content of coal for thecement industry (para. 3.15). Power has been a major constraint on the cementindustry for years. However, the magnitude of the problem has been graduallyreduced over the last few years by the installation of captive power plants whichnow supply about 15 percent of the industry's total power requirement. Whilesupply of power still remains a binding constraint for sustained capacityutilization of many cement plants, it is not expected to be as critical as inthe past.

2.17 Transport Cost. Given the imbalance in the location of limestonereserves, coal mines and major cement markets and past sectoral policies,development of the cement industry has been plagued by high transport cost(paras. 2.02, 2.06 and 2.15). Cement produced in India has to travel an averageof 650 km to the final user, at an average freight cost of more than Rs. 250/ton.For the northeastern states, cement has to be transported around 1,000 km fromMadhya Pradesh at an estimated cost of Rs. 400/ton. Transport cost addssignificantly to the total delivered cost of cement. In fact, freight cost, andexcise and sales taxes make the delivered cost of cement twice the ex-factoryprice. Transport cost is largely responsible for the price differentialsobserved in different parts of the country. In the present free-marketenvironrment, individual plant viability will largely depend on the distancebetween the plant's location and the market it serves.

E. Demand and SUDD1 Proiections

2.18 'Consumtion. Apparent annual cement consumption in India increasedfrom 14.5 million tons in FY75 to about 42 million tons in FY89, correspondingto a compound annual growth rate of 7.3 percent. The current 47 kg per capitaannual consumption of cement in India is still low compared to other countries,as shown in Table 2.5. The long-standing price and distribution controls, thelack of incentive to market cement in rural areas, the failure to promotepotential markets in areas such as concrete roads, and the lack of financing forhousing development have all contributed to India's low per capita consumptionof cement. As these constraints ease and the GNP grows, there is immense scopefor cement consumption growth.

- 10 -

hible 2.5: Cement Per Caoita Consumption. 1987

GNP per Capita Industrial VA Per capita cement(8 eauivalent) A/ as percent of GDP h/ consumption (kg) Q/

Turkey 1200 36 454Egypt 670 25 335Mexico 1820 34 230Brazil 2020 38 182China 290 49 167Zimbabwe 590 43 81Pakistan 350 28 66India 300 30 47Kenya 330 19 39

Source: a/ World Table 1988-89k/ World Development Report, 1989Al World Statistical Review, CemBureau, 1989

2.19 Demand Projectioa. Four major studies on cement demand projection,by Mangesh International Service, by Tata Economic Consultancy, by ICICI and byIDBI were made available to the Bank. Their projections up to FY95 arepresented, along with the appraisal staff's estimate, in Table 2.6:

Table 2.6: Cement Demand Prolection(million tons)

Mangesh Studs Tata Study4.1% GNP 5.1% GNP Econo- End-User ICICI IDBI Staff EstimateGrowth matric Nethod Study Sig&y Case I Case II

1989-90 44.5 45.5 43.1 46.0 45.9 45.6 46.6 45.81990-91 47.3 49.1 47.4 50.0 49.8 49.7 50.2 48.81991-92 50.3 53.1 52.3 54.4 54.0 53.9 54.3 51.91992-93 53.6 57.4 58.0 60.4 58.6 58.7 58.7 55.91993-94 57.1 62.0 64.4 64.3 63.6 63.9 63.5 58.91994-95 58.6 67.1 72.5 69.9 69.0 69.5 68.6 62.7

Source: Mangesh International Services, March 1987Tata Economic Consultancy Services, February, 1989ICICI, December 1989; IDBI, September, 1989.

2.20 To relate historical cement consumption with general economicvariables, the Mangesh study chose GNP and the effect of the Green Revolution(between FY76 to FY86) and the price index, which might have had an impact onprivate consumption of cement. The Tata study chose gross domestic fixed capitalformation, which correlated most closely with the cement consumption. The Tatastudy also tried to project the cement demand in major end-user sectors. In both

- 11 -

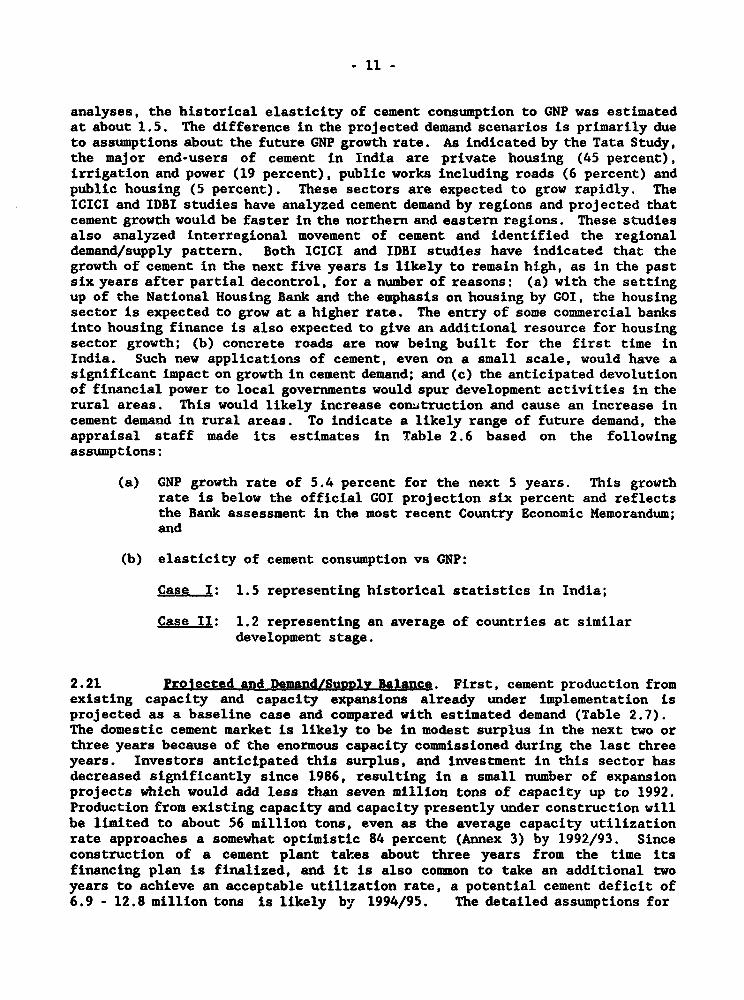

analyses, the historical elasticity of cement consumption to GNP was estimatedat about 1.5. The difference in the projected demand scenarios is primarily dueto assumptions about the future GNP growth rate. As indicated by the Tata Study,the major end-users of cement in India are private housing (45 percent),irrigation and power (19 percent), public works including roads (6 percent) andpublic housing (5 percent). These sectors are expected to grow rapidly. TheICICI and IDBI studies have analyzed cement demand by regions and projected thatcement growth would be faster in the northern and eastern regions. These studiesalso analyzed interregional movement of cement and identified the regionaldemand/supply pattern. Both ICICI and IDBI studies have indicated that thegrowth of cement in the next five years is likely to remain high, as in the pastsix years after partial decontrol, for a number of reasons: (a) with the settingup of the National Housing Bank and the emphasis on housing by GOI, the housingsector is expected to grow at a higher rate. The entry of some commercial banksinto housing finance is also expected to give an additional resource for housingsector growth; (b) concrete roads are now being built for the first time inIndia. Such new applications of cement, even on a small scale, would have asignificant impact on growth in cement demand; and (c) the anticipated devolutionof financial power to local governments would spur development activities in therural areas. This would likely increase conatruction and cause an increase incement demand in rural areas. To indicate a likely range of future demand, theappraisal staff made its estimates in Table 2.6 based on the followingassumptions:

(a) GNP growth rate of 5.4 percent for the next 5 years. This growthrate is below the official GOI projection six percent and reflectsthe Bank assessment in the most recent Country Economic Memorandum;and

(b) elasticity of cement consumption vs GNP:

Case I: 1.5 representing historical statistics in India;

Case I1: 1.2 representing an average of countries at similardevelopment stage.

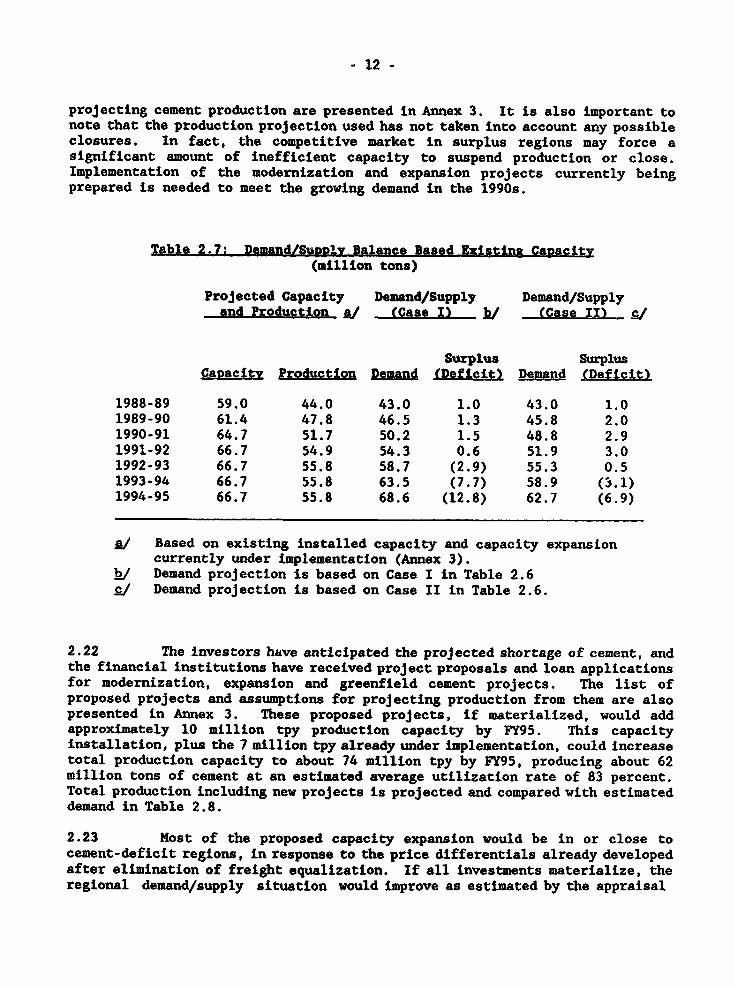

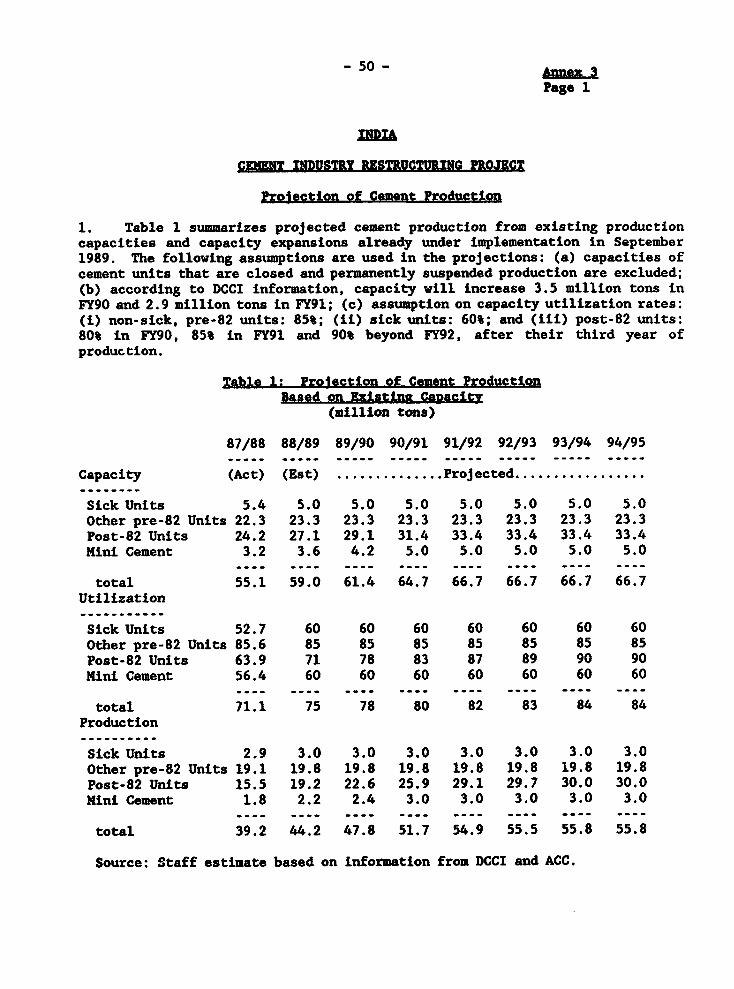

2.21 Projected and Demand/Supply Balance. First, cement production fromexisting capacity and capacity expansions already under implementation isprojected as a baseline case and compared with estimated demand (Table 2.7).The domestic cement market is likely to be in modest surplus in the next two orthree years because of the enormous capacity commissioned during the last threeyears. Investors anticipated this surplus, and investment in this sector hasdecreased significantly since 1986, resulting in a small number of expansionprojects which would add less than seven million tons of capacity up to 1992.Production from existing capacity and capacity presently under construction willbe limited to about 56 million tons, even as the average capacity utilizationrate approaches a somewhat optimistic 84 percent (Annex 3) by 1992/93. Sinceconstruction of a cement plant takes about three years from the time itsfinancing plan is finalized, and it is also common to take an additional twoyears to achieve an acceptable utilization rate, a potential cement deficit of6.9 - 12.8 million tons is likely by 1994/95. The detailed assumptions for

- 12 -

projecting cement production are presented in Annex 3. It is also important tonote that the production projection used has not taken into account any possibleclosures. In fact, the competitive market in surplus regions may force asignificant amount of inefficient capacity to suspend production or close.Implementation of the modernization and expansion projects currently beingprepared is needed to meet the growing demand in the 1990s.

Table 2.7: DemandZSupplX Balance Based Existing Capacity(million tons)

Projected Capacity Demand/Supply Demand/Supplyand Production A/ (Case I) L k/ (Case II) C/

Surplus SurplusCapacity Production Demand (Deficit) Demand (Deficit)

1988-89 59.0 44.0 43.0 1.0 43.0 1.01989-90 61.4 47.8 46.5 1.3 45.8 2.01990-91 64.7 51.7 50.2 1.5 48.8 2.91991-92 66.7 54.9 54.3 0.6 51.9 3.01992-93 66.7 55.8 58.7 (2.9) 55.3 0.51993-94 66.7 55.8 63.5 (7.7) 58.9 (3.1)1994-95 66.7 55.8 68.6 (12.8) 62.7 (6.9)

a/ Based on existing installed capacity and capacity expansioncurrently under implementation (Annex 3).Demand projection is based on Case I in Table 2.6

e/ Demand projection is based on Case II in Table 2.6.

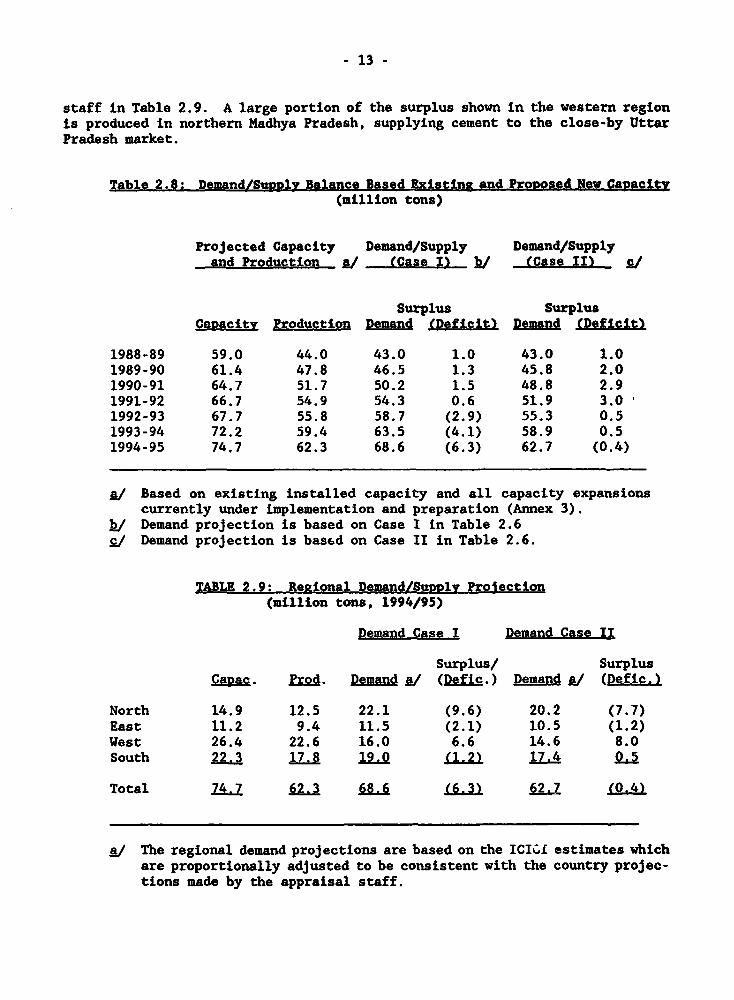

2.22 The investors have anticipated the projected shortage of cement, andthe financial institutions have received project proposals and loan applicationsfor modernization, expansion and greenfield cement projects. The list ofproposed projects and assumptions for projecting production from them are alsopresented in Annex 3. These proposed projects, if materialized, would addapproximately 10 million tpy production capacity by FY95. This capacityinstallation, plus the 7 million tpy already under implementation, could increasetotal production capacity to about 74 million tpy by FY95, producing about 62million tons of cement at an estimated average utilization rate of 83 percent.Total production including new projects is projected and compared with estimateddemand in Table 2.8.

2.23 Most of the proposed capacity expansion would be in or close tocement-deficit regions, in response to the price differentials already developedafter elimination of freight equalization. If all investments materialize, theregional demand/supply situation would improve as estimated by the appraisal

- 13 -

staff in Table 2.9. A large portion of the surplus shown in the western regionis produced in northern Madhya Pradesh, supplying cement to the close-by UttarPradesh market.

Table 2.8: Demand/Supply Balance Based Existing and Prolosed New Cavacitv(million tons)

Projected Capacity Demand/Supply Demand/Supplyand Production (Ca / , (Case II) £/

Surplus SurplusCa2acitx Production Demand (Peficit) Demand IDefleft.

1988-89 59.0 44.0 43.0 1.0 43.0 1.01989-90 61.4 47.8 46.5 1.3 45.8 2.01990-91 64.7 51.7 50.2 1.5 48.8 2.91991-92 66.7 54.9 54.3 0.6 51.9 3.01992-93 67.7 55.8 58.7 (2.9) 55.3 0.51993-94 72.2 59.4 63.5 (4.1) 58.9 0.51994-95 74.7 62.3 68.6 (6.3) 62.7 (0.4)

L/ Based on existing installed capacity and all capacity expansionscurrently under implementation and preparation (Annex 3).

h/ Demand projection is based on Case I in Table 2.6./ Demand projection is based on Case II in Table 2.6.

TABLE 2.9: Retional Demand/SuDlv Pro1ection(million tons, 1994/95)

Demand Case I Demand Case II

Surplus/ SurplusCapac. Prod. Demand Al (Defic.) Demand A/ (Defic.)

North 14.9 12.5 22.1 (9.6) 20.2 (7.7)East 11.2 9.4 11.5 (2.1) 10.5 (1.2)West 26.4 22.6 16.0 6.6 14.6 8.0South 22.3 1 19.0 (1.2) 17.4 0.5

Total 74.7 62.3 68. (6.3) 6Z (0.4)

a/ The regional demand projections are based on the ICICI estimates whichare proportionally adjusted to be consistent with the country projec-tions made by the appraisal staff.

- 14 -

III. RESTRUCTURING OF THE CEMENT INDUSTRY AND ROLE OF THE BANR

A. CEMENT INDUSTRY RESTRUCTURING STRATEGY

Actions Already Under Implementation

3.01 The competitive domestic cement market created by the decontrol ofcement pricing and the elimination of the freight equalization scheme, and thecurrent excess capacity and regional demand-supply imbalances, are forcing theindustry to rationalize and balance its operations, reduce waste and allocateresources more efficiently. To improve their long-term market position andensure financial viability, many companies are considering or have alreadyimplemented measures to modernize and expand their productions facilities, tointroduce product differential and quality, and to explore new markets andmarketing techniques.

3.02 The important changes already under way include (a) Expansion andModernization, i.e., conversion of existing wet-process cement production unitsto the more efficient dry process, accompanied by significant capacity expansionand energy and other operating cost savings; (b) Corporate Restructuring andPlant Closure. A number of companies have consolidated operations by sellingplants, to reduce cash losses and refocus resources on more profitable parts ofthe operations, closing financially troubled and uneconomic units with laborsettlements approved by the state governments, the courts and/or the Board ofIndustrial and Financial Restructuring (BIFR), or suspending production pendinglegal approval; (c) Improvement in Labor Productivity by providing earlyretirement and voluntary separation packages; and (d) Aggressive Marketing giventhe competitive market pressure and current regional demand-supply imbalances,Indian cement producers are resorting to increased advertising, quality and branddifferentiation, and improvement of distribution networks.

Planned Restructuring Measures

3.03 The policy environment is conducive for operational and corporaterestructuring, and firms are now more willing to take steps to improve theirlong-term position than before decontrol. Moreover, to encourage domestic cementproducers to undertake additional steps to adjust to the competitive environ-ment, DCCI is developing a modernization and restructuring strategy for theindustry. Implementation of this strategy would provide a mix of incentives andpenalties to induce companies to ensure their financial viability and supply theIndian cement market more economically. The major elements of this strategy arediscussed below.

3.04 Nodernization Scheme for Wet-Process Plants. A working group wasestablished by the Ministry of Industry under the chairmanship of DCCI to developa modernization plan for wet-process cement plants. The working group completedits final report in December 1989 with the following major findings andrecommendations: (a) as of January 1988, there were 33 wet-process cementplants. Seven are already implementing vet-to-dry conversion schemes withassistance from the first World Bank loan. Seven cannot be convertedeconomically because of limitations in technology and limestone reserves. The

- 15 -

remaining plants can be converted to modern dry-process plants; (b) to encouragemodernization of these plants, incentives were recommended for substantial moder-nization projects at the same level as for greenfield plants (including salestax holidays and power supply priority). Consultation and coordination withstate governments would be needed in this regard; (c) to complement positiveincentives, penalties were also recommended. One such proposal was to provideallocated coal to cement plants according to energy efficiency norms (specificamount of coal per ton of cement produced). Inefficient plants would have topurchase their additional coal requirements on the retail market, presumably athigher prices; (d) to ensure production costs of the modernized plants are com-petitive with the new plants, labor restructuring with fair compensation, suchas early retirement and/or separation packages, would have to be implemented;and (e) it was recommended that plants identified with inherent limitationsshould be allowed to close. These measures, if implemented, would form thebasic framework for further modernization of this segment of the industry.However, most wet-process plants are operating unprofitably, and their financialposition is weak. Modernization of these plants would usually require corporaterestructuring and prudent case-by-case appraisal.

3.05 Regional Production Camacitv. To minimize the average transportcost of cement, the industry will need to rationalize the distribution of pro-duction capacities and their utilization in response to the actual marketdemands. Elimination of the freight-equalization scheme, and the resultingregional cement price differential, is already inducing the industry to considerinvestments to establish new production facilities in the projected deficitareas. Capacity expansions currently under consideration in Assam, Bihar,Himachal Pradesh and northern Madhya Pradesh are consistent with this trend.To encourage investments to the backward northeastern states, the Government ofIndia, through the Northeast Development Council (NDC) and the state governmentsis planning to provide basic infrastructure (power, rail connections and roads)and training.

3.06 Human Resource Development. With the rapid growth of the cementindustry over the last decade, the demand for trained personnel has increasedconsiderably, and shortages of skilled operators and middle-level techniciansare increasing. Many cement producers are experiencing high turnover at theoperational and technical level due to strong competition among companies forskilled personnel. Unless steps are taken now to develop a large pool of skilledoperators and managerial cadres capable of handling the growing demand of energyconservation, pollution control, development of new products and marketing tech-niques, the growth and efficiency improvement of the industry might fall shortof expectations.

3.07 The cement industry is now revising its human resource developmentapproach to put more emphasis on sector-specific and plant operational trainingwhile relying on established institutions for training of a more general nature.The strategy to develop trained manpower for the sector rapidly and efficientlyrequires a flexible, demand-driven training system such as the system proposedby a consultant studyl} financed by the First Cement Project (Ln. 2660-IN). Thestudy proposed that RTCs be established around modern cement plants to providedemand-driven, in-plant training for 'clusters" or groups of plants with geogra-

I/ Manpower Development Study by Holdenbank Consultant.

- 16 -

phic proximity and common languages. The proposal has won wide support fromcement manufacturers and its implementation has been made part of this project(para. 4.12). The proposed sector-specific training would complement and buildon the general technical training provided by the advanced training institutes(ATI). These institutes are also being supported under the Bank-financed Voca-tional Training Project (Cr. 2008/Ln. 3045-IN), with a particular focus onimproving linkages with industry.

3.08 DevelopMent of Bulk Cement Transport. Considering the divergencebetween the location of limestone reserves, coal mines and the major cementmarkets (paras. 2.14 and 2.17), the Indian cement industry is today charac-terized by high transport cost and will probably remain so. A study by RailIndia Techno-Economic Service (RITES) concluded that transport of cement overdistances above 220 km is cheapest by rail. Due to lack of rolling stock andlimitations of track capacity, the railways cannot meet the demand for wagonsfrom the cement industry. During the 1980s, 4)-50 percent of cement was movedby trucks. Truck transport is high cost, wastes scarce energy resources andoverloads India's road system. Nonavailability of railway wagons has at timesforced cement manufacturers to curtail production. In view of the anticipatedincrease in cement consumption in the 1990s, if 70 percent of cement were to bemoved by rail, the railways would need to increase the availability of wagonsdedicated to cement by almost 200 percent.

3.09 With a view to achieving economies of scale during the 1980s, theIndian cement industry preferred to build large plants with capacities at asingle location of 1-2 million tons per year, an output of 3,000-6,000 tons perday. Most cement in India is distributed in 50-kg bags, and the output of asingle location can require semi-manual loading and unloading of 60,000 to120,000 bags per day. The operation is time consuming, ties up scarce railwayrolling stock, and results in seepage and environmental pollution. Rail movementof bulk cement through the introduction of high-capacity, dedicated, speciallydesigned wagons will be essential in order to achieve economy in the transportof cement and to avoid serious bottlenecks.

3.10 Achieving economies in transport costs is not the only driving factorfor introduction of bulk cement in India. Delivery of cement in bulk form isa prerequisite for improving the productivity of the construction industry. Withthe exception of a few very large projects, the Indian construction industrycontinues to use manual methods of mixing cement, sand and aggregates at theproject site. The quality of the concrete therefore varies with the skill andintegrity of the workers. This method of construction also has a significantimpact on the time required for completion of the civil works and, consequently,has a major impact on overall project completion schedules and costs. It istherefore imperative for the country to adopt modern methods of constructionincluding rapid delivery of ready-mixed concrete. The ready-mixed concreteindustry depends on the availability of bulk cement. Experience from indus-trialized countries shows that 35-90 percent of cement produced is shipped inbulk, and 60 percent of bulk cement is sold to the ready-mixed concrete industry,and th'.e balance to buildi-.g product manufacturers and large job-site projects.The marketing of bulk cement in India would be likely to follow a similarpattern. A broad compariscn of cement movement in bulk and bagged form inselected countries is given in Table 3.1.

- 17 -

Table 3.1 Movement and Distribution of Cement (19851

Percentages

S. No. Country In b?ulk In Basa

1. U.S.A. 90 102. Sweden 80 203. Japan 70 304. U.K. 68 325. West Germany 54 466. France 46 547. Algeria 40 608. Italy 34 669. India 1 99

Source: Cement Data Book by CMA.Staff estimate.

3.11 Bulk movement of cement in India is economically desirable. It isrecognized that the present system of movrement of cement in bags would createsevere system constraints and strain both rail and road transport in light ofthe anticipated increase in cement production from 42 million tons to about 80million tons by 2000. A pilot scheme to develop bulk cement transport has beenprepared by GOI with DANIDA assistance and is included in the proposed project(para. 4.09).

3.12 Pollution Contr,ol. With the tightening of environmental standardsand enforcement by GOI since the early 1980s and the substantial modernizationof the industry during this period, most cement plants have installed environ-mental protection equipment and have therefore greatly improved their prospectsfor meeting Indian environmental standards. According to a task force appointedby the Central Pollution Control Board in 1988, out of 94 cement plants, 58 hadadequate pollution control equipment for their kilns and were maintaining theexhaust dust content within the Indian emission standards. A further 25 unitshave already submitted time-bound programs to meet pollution control standards.Of the remaining 11 plants, 5 have already been closed due to uneconomic opera-tion, and 2 have been closed through legal actions based on environmental viola-tions. For the remaining four plants that had not submitted time-bound programsfor pollution control, efforts were being made by the respective state pollutioncontrol boards under the direction of the Central Pollution Control Board toforce these units to implement required actions. Since 1984, GOI has also madeenvironmental clearance a condition of project approval in many industries in-cluding cement, thereby ensuring that new capacity meets the country's environ-mental protection standards.

3.13 Despite the impressive progress made by the industry and the commit-ment of the Government, particulate emission remains a serious problem for manycement plants. Installed pollution control equipment may not operatecontinuously because of power cuts and other technical and operational problems;the technical design of some old plants and mini-plants makes it impossible toinstall adequate pollution control equipment without major alterations of theplants; technical and financial constraints may also delay the promised pollu-tlon control programs (para. 3.12); and monitoring systems in most plants are

- 18 -

inadequate. GOI invited a team of Danish environmental specialists financed byDANIDA to India in September 1989 to identify environmental and occupationalhealth problems in the cement industry. It was agreed that a comprehensive study(para. 4.14) would be carried out as part of the proposed project to analyze theenvironmental problems in the industry and recommend options for theirresolution.

3.14 Coal Beneficiation. The low quality (i.e., high ash content) of In-dian coal raises specific concerns for the cement industry. The high asn con-tent, frequently 40-45 percent, affects the industry by (a) reducing the economiclife of limestone deposits, since only higher grades of limestone can be usedwith high-ash coal; (b) lowering cement quality because of high ash content andalso because of the inherent variations in ash affecting the chemical compositionof the raw mix; and (c) reducing process efficiency and increasing cost. Giventhe impact of the increasing ash content of Indian coal on the economics of thecement industry, the need for coal beneficiation to supply the industry withbetter-quality coal of higher calorific value and reduced ash content is becomingcritical. However, the economics would depend on the cost of coal beneficiationitself and the benefits that can be derived from improvements in the specificways cited above.

3.15 Two options are to be explored by the Government and the industryindependently in the next few years:

(a) Associated Cement .'ompanies Ltd. (ACC) and Birla-Jute and IndustriesLtd. are installing captive coal washeries based on two differenttechnologies. Both combine the washery with a captive thermal powerplant, which allows optimal thermal efficiency. ACC and Birla-Jute'sexperience will provide valuable technical information for the designof future large-scale applications.

(b) DCCI proposes to undertake a study to determine the economic viabi-lity and organizational arrangements for setting up pit-head coalwasheries that can be linked to a number of operating cement plants.This option has the advantage of scale and lower transport cost andcould potentially benefit a large number of plants. However, inorder for the scheme to be viable, a pithead thermal power plant withfluidized bed combustion has to be included in the scheme. Thisstudy is proposed as part of the project (para. 4.14)

3.16 The cement industry restructuring strategy being developed by DCCI(paras. 3.4-3.15) would guide the industry through the next five years ofadjustment following total decontrol. In the long run, provided the currentsectoral policy environment is maintained, competitive market forces are expectedto ensure efficient allocation of resources in the settor, gradually reducingregional imbalances and eliminating suboptimal operations. One critical issuethat may pose difficulties to the desired adjustment process for the cementindustry concerns plant closure when an operation is proven unsustainable in acomretitive market. Plant closure in a timely manner is constrained by laborlegislation and the courts' interpretation thereof. However, there is increasingrecognition by Indian policy makers and the public of the economic costsassociated with these constraints. The Government's decision not to take overmore "sick units" and the establishment of BIFR have provided a framework tobegin dealing with closure problems. In the cement industry, where 85 percent

- 19 -

is in the private sector, market forces have, in the absence of direct subsidyand government bailout, resulted in a number of closures with the approval ofstate governments. There are indications that a plant can be closed with lesssocial difficulty when satisfactory labor settlements are worked out. Laborrestructuring including early retirement schemes has become a common practicein many cement companies. The Bank will continue to discuss the plant closureissue with the Government in the context of implementation of this project andmore general dialogue on industrial policy in India.

B Bank-Leadin_ to the Industrv

3.17 The Bank has made 23 development finance loans totaling $1.8 billionthrough financial intermediaries (mainly ICICI and IDBI) for on-lending toprivate and joint-sector firms. Two loans have been specifically for export de-velopment, and one for technology development, in part through the provision ofventure capital. The Bank's experience with ICICI in implementing past projectshas been discussed in several Project Completion Reports (PRCs). The most recentPCR, dated April 1989, for the Fourteenth Industrial Credit and InvestmentProject (Ln. 2051-IN, signed on October 8, 1981), indicated that, while the 14loans were successful in supporting ICICI's institutional development, they didnot seriously address the policy environment within which its lending took place.This is no longer the case. Major policy reform has taken place in the cementsector, and a satisfactory lending environme.-t has been created in preparationfor this proposal.

3.18 The Bank has also provided $3.4 billion for projects in thefertilizer, cement, petrochemicals and electronics sub.sectors where opportunitiesexisted for the bank to support policy reforms at the subsector level and fin-ance economic investments using modern technology. Implementation of theseprojects has been generally satisfactory. All projects currently under imple-mentation are expected to have satisfactory rates of economic return and, des-pite some initial delays, most are expected to be completed on time. Loansthrough financia'L intermediaries are also being implemented well, and the Bankis working closely with them to improve their project appraisal capabilities,foreign asset/liability management and portfolio quality.

3.19 Lessons from the Cement Sector Experience. In the cement sector,the Bank's involvement began in 1980 with a cement subsector study (India: CementSubsector Study, Report No. 3141-IN), which became the basis for a.n active policydialogue between the Bank and GOI. This dialogue contributed to GOI's policydecision of partial decontrol of cement pricing and distribution in 1982. TheBank approved $200 million loans (Cement Industry Project - Lns. 2660-IN/2661-IN), which became effective in November 10, 1986, to support modernization ofthe cement industry. This project has been successful in achieving its basicobjectives. First, the project-supported policy environment continued toimprove, and the complete decontrol has been implemented. Second, the projecthas financed the modernization projects that converted wet-process plants with1.8 million tpy total capacity to the more energy-efficient dry process. Third,energy conservation and pollution control objectives are being realized as theproject is significantly reducing coal consumption and improving the pollutioncontrol standards of the supported cement plants. Fourth, the technical assist-ance has resulted in formulation of a manpower development strategy and a HumanResource Development component to be included in this proposed project. Fifth,

- 20 -

the project has increased the industry's awareness of deterioration of coalquality and its impact on energy efficiency and productivity of cement produc-tion and the economic life of limestone deposits. As a result, two pilot coalwasheries are being set up by private cement companies with Bank financing. DCCIhas also proposed a study for setting up mine-mouth washeries for the cementindustry.

3.20 Implementation of the project is proceeding reasonably well. As ofApril 1990, $160 million of the total loan had already been committed, anddisbursements amounted to about $75 million. The loans are expected to be fullycommitted by September 1990 when thie proposed proJect would become effective.Overall, this operation has enabled the Bank to maintain active policy dialoguein the cement sector and to finance priority projects that supported the reformprocess. Lessons learned from the first cement project have been incorporatedinto the design of this proposed project. First, the proposed project would,as did the first project, support continued policy reform and resultingadjustments. Second, as in the first project, the Bank has been working closelywith IDBI and ICICI in subproject identification and preparation. IDBI and ICICIhave demonstrated their appraisal capability during independent appraisals forall subprojects and would take full responsibility of subproject appraisal forthe proposed project. The Bank would not appraise individual subprojects, asit did for the first project, but would provide support in special areas suchas environmental assessment.

3.21 Future Lending. The Bank has had an active industrial sector workprogram and has prepared a number of sector reports on such subjects as indu-strial regulation, technology policy, export promotion, public enterprisemanagement and credit and capital markets, as well as a number of subsectorreports including cement, electronics, automotive products, steel, capital goodsand fertilizer. The 1987 CEM, India: An Industrializing Economy in Transition(Report No. 6633-IN, March 23, 1987) focused on the development of the industrialsector and supplied the broad outlines of a reform program. Many of the issuesin these reports will continue to be discussed with the Government in the contextof future operations.

3.22 The Bank's future lending program for industry is based primarilyon sector work and will be designed to support the Indian Government's policyreforms of promoting competition and operational efficiency. The Bank's medium-term industrial lending program includes:

(a) industrial finance projects which will serve as a focal point forevaluating and discussing with GOI overall progress on industrial andfinancial policy reform as well as addressing issues in the financialinstitutions;

(b) technology, industrial pollution control and energy conservationprojects which will serve as a focal point for evaluating and dis-cussing with GOI overall progress and improve the policy, financialand institutional suipport for activities in these key areas; and

(c) subsector projects which will provide policy, technical and financialsupport for economic investments in areas where improved

- 21 -

efficiency will have implications for the growth of the wholeindustrial sector and economy (e.g., petrochemicals, cement andcapital goods).

3.23 In all of these areas, loans are linked to policy reforms that arebeing undertaken either in designated policy areas such as t chnology, or in thepolicies that affect a specific subsector such as in cement. The basic criterionthat determines the decision to go ahead with a loan is whether or not the policyenvironment is conducive to efficient investment in the sector or subsector beingsupported. That is, the lending strategy involves supporting investments inareas where policy improvements have already been undertaken, consistent withthe conclusions of the previous sector and subsector work. In the cement sec-tor, the most important sector-specific issues (rigid capacity licensing schemeand cement pricing and distribution) that were identified in the 1980 CementSubsector Report have now been largely resolved. The rationale for Bank supportfor the proposed project, therefore, is to continue support for the moderniza-tion and adjustment efforts which started with the first project (Ln. 2660-IN)by further assisting cement companies to undertake needed restructuring measures.The subsector restructuring strategy is at a formative stage, and the Bank canprovide substantive assistance based on experience in other countries inindustrial restructuring of wet-process plants and the mini-cement sector,industrial training, and bulk cement transport.

-22-

IV. THE PROJECT AND THE PROPOSED LOAN

A. Erolect Objectives

4.01 The proposed project is designed to support GOI's recent policydecision for complete elimination of cement pricing and distribution controlsand would assist the industry in adjusting to a more competitive environment inthe following ways. First, the project would finance investment projects whichare important for the modernization and restructuring of the industry. Second,the project would help establish and finance a pilot bulk cement transport systemto transport bulk cement to the greater Bombay area. Stuccessful implementationof this pilot scheme would pave the way to introduce bulk cement transportsystems in India. Third, the project would help establish and finance demand-driven training systems and programs to support human resource developmentcompatible with the significant technological transformation of the industry.Fourth, the project would assist DCCI in studying policy and strategic optionsfor mini-cement sector, coal washing, use of lignite, pollution control andenvironmental protection for the cement industry, and further tevelopment of bulkcement transport and applications.

B. Proiect Descrigtion

4.02 The proposed project comprises four components: an IndustryModernization and Restructuring component, a Pilot Bulk Cement Transportcomponent, a Human Resource Development component and a Technical Assistancecomponent.

Industry Modernization and Restructuring (IHR)

4.03 This component would finance (a) capacity expansion in the cement-deficit regions to alleviate regional demand/supply imbalance, reduce excessivetransport of cement and lower the cost of this basic commodity in some of thepoorest regions of the country; and (b) modernization and restructuring projectswith existing cement companies throughout India to reduce energy cost, enhanceutilization and operating efficiency and improve pollution control stancdards.Included in the component are four large subprojects which constitute about80 percent of the proposed Bank loan. These four subprojects would not onlyreduce regional demand/supply imbalance, but they would also improve marketcompetition: two of the subprojects represent new entries to the cement sector,and the market share of Associated Cement Companies (ACC), the largest in India,would be reduced due to restructuring. Descriptions of these four subprojectsare available in the project files and are summarized below.

4.04 ACC Corporate Restructuring. ACC is privately owned and the largestcement company in India; many of its plants utilize outdated, wet-processtechnology. Because of increasing competition from new plants, ACC's financialperformance has deteriorated over the last few years resulted in a lack ofresources to undertake much-needed modernization. The project would support acorporate restructuring plan developed over the last two years. The plan

- 23 -

includes (a) selling 4 operating plants (Kistna, Khalari, Shahabad and Porbandarhave already been sold) to reduce the company's operating plants from 14 to 10in order to concentrate the company's limited financial resources; (b) expansionof Gagal plant, which was responsible for half of the company's profit in FY89,to support ACC's growth strategy in cement-deficit regions; (c) implementationof pollution control programs and smaller high-return projects for selectedmining operations, pilot coal beneficiation and energy conservation; (d) majormodernization of potentially viable existing plants of Kymore, Wadi, Jamul andMancherial, if resources permit; (e) reorganization of ACC's Technical ServiceDepartment to make it outward looking and profit oriented; and (f) cot'tinuationof revised trainitig programs and early retirement schemes to restructure thelabor force. The corporate restructuriag plan was discussed and agreed with theappraisal mission, and its implementation has already begun.

4.05 The restructuring plan includes a major investment in ACC's modernGagal plant, which presently has a capacity of 560,000 tpy. The Gagal plant isfavorably located in Himachal Pradesh and serves a fast-growing market regionin Punjab, Haryana, Delhi and part of Uttar Pradesh. The forecasts of thesupply/demand balance in this region indicates a deficit of 3.5 million tons in1994-95, according to the recent ICICI study. This major market advantage plusthe availability of the existing infrastructure and well-developed limestonequarry to support the proposed expansion will offset the high delivered cost ofcoal and give the Gagal expansion a definite cost advantage. The projectincludes two parts. Part one consists of a new, modern, dry-process productionline with a capacity of 1 million tpy. The estimated cost is $90 million, ofwhich the Bank would finance $50 million. Part two comprises upgrading andmodification of the existing plant to increase its capacity to 1 million tpy (anincrease of 440,000 tpy) and substantially improve pollution control. The costof the second part is being estimated and will be presented to IDBI and ICICIshortly. The new production line will be located on an open area immediatelynext to the exiting production unit, and construction of this component will beundertaken first in order to avoid loss of production during construction.Gagal is located in an environmentally sensitive area, and measures will be takento ensure that the environmental impact will be minimal and acceptable accordingto both Indian and international standards. The present limestone deposit willsupport the resulting 2 million-tpy plant's capacity for more than 20 years, andno new mining lease will be required in connection with the project.

4.06 Tata Iron and Steel Company (TISCO0 Slau Cement Project. Withsurplus slag from its present steel operation and a major blast furnace expansionunder way, it is natural, from both economic and environmental poi.ats of view,for TISCO to build a slag cement plant. The proposed project consists of (a) a1 million-tpy clinkerization unit along with a 300,000-tpy OPC grinding unit atSonadih, Madhya Pradesh; and (b) a 1.4 million-tpy Portland slag cement (PSC)grinding unit (based on clinker from Sonadih) near the TISCO steel complex atJamshepur, Bihar. The bulk of the output of this project is targeted for themajor Bihar-West Bengal cement-deficit regions, including Calcutta. Currently,cement is being transported to this region at a considerable cost. Inacccordance with the split-location design of this project, the clinker, whichmakes up 50 percent of the slag cement produced, is transported from MadhyaPradesh to Bihar to be ground with slag and other additives at the more favorablemarket location. The project puts blast furnace slag, a waste material and

- 24 -

potential pollutant, to productive use, and produces significant economic andsocial benefits. The estimated project cost is about $147 million, of whichabout $70 million would be financed by the proposed loan.