astra industrial group company and its … q1 2017 (e).… · astra industrial group company and...

TRANSCRIPT

ASTRA INDUSTRIAL GROUP COMPANY AND ITSSUBSIDIARIES

(A Saudi Joint Stock Company)

INTERIM CONDENSED CONSOLIDATED FINANCIALSTATEMENTS (UNAUDITED)

31 MARCH 2017

ASTRA INDUSTRIAL GROUP COMPANY AND ITS SUBSIDIARIES(A Saudi Joint Stock Company)INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTSFOR THE THREE-MONTH PERIOD ENDED 31 MARCH 2017

INDEX PAGE

Independent Auditors’ Review Report 1

Interim Condensed Consolidated Statement of Income 2

Interim Condensed Consolidated Statement of Comprehensive Income 3

Interim Condensed Consolidated Statements of Financial Position 4-5

Interim Condensed Consolidated Statements of Changes in Equity 6

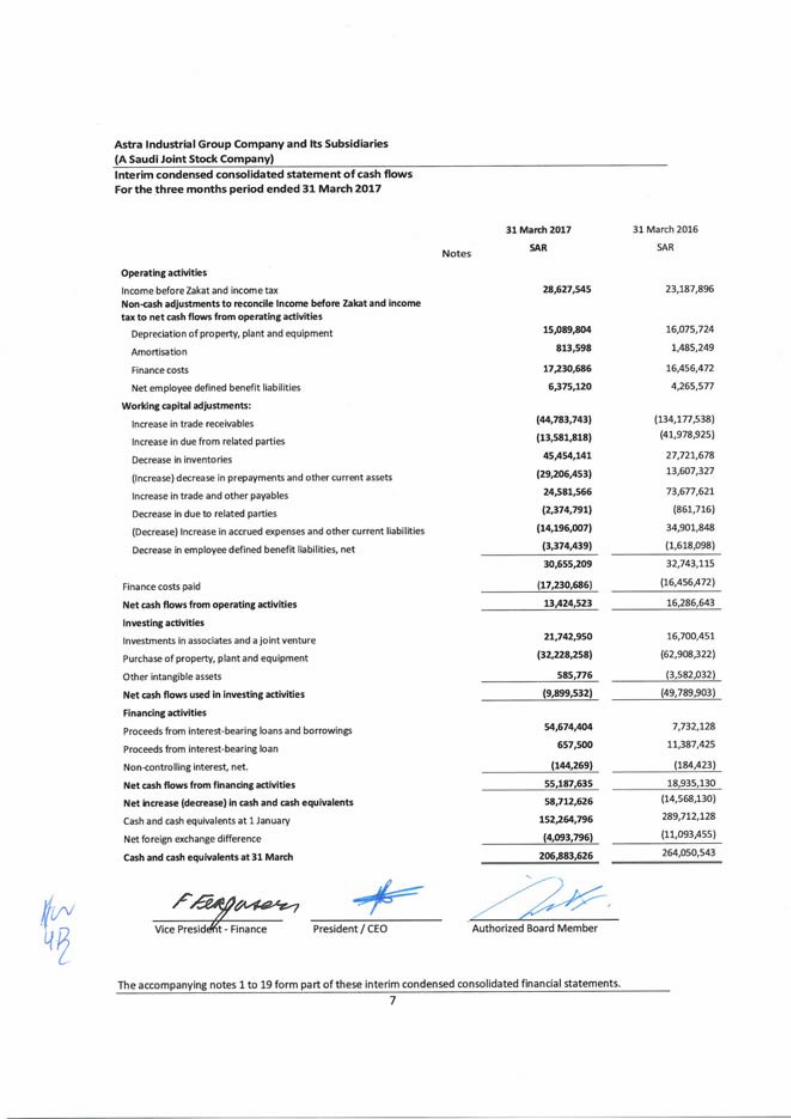

Interim Condensed Consolidated Statement of Cash Flows 7

Notes to the Interim Condensed Consolidated Financial Statements 8 – 52

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements31 March 2017

8

1 ORGANIZATION AND ACTIVITIES

Astra Industrial Group Company (the “Company”) is a Saudi Joint Stock Company licensed under foreign investmentlicense number 030114989-01 issued in Riyadh by Saudi Arabian General Investment Authority (SAGIA) andoperating under commercial registration number 1010069607 issued in Riyadh on 9 Muharram 1409H (22 August1988). The address of the Group’s head office is as follows:

Astra Industrial GroupP.O. Box 1560Riyadh 11441Kingdom of Saudi Arabia (KSA)

The Group is engaged in the following activities:

a) Building, managing, operating and investing in industrial plants after obtaining approvals from the SaudiArabian General Investment Authority (SAGIA) for each project.

b) The wholesale and retail trade in clothing, towels, blankets, fertilizers, animal feed, insecticides, irrigationequipment, agricultural machinery and equipment, greenhouses, agricultural and animal products andgardening contracts.

The principal activities of the subsidiaries are as follows:

· Production, marketing and distribution of medicine and pharmaceutical products.· Production of polymer compounds, plastic additives, color concentrates and other plastic products.· Metal based construction of industrial buildings and building frames.· Production of compounded fertilizers and agriculture pesticides and the wholesale and retail trading of

fertilizers, forages and insecticides. Also, execution of agricultural projects contracts.· Production of steel pallets and steel rebar and generation of the required power of such activity.· Exploration of all ores and minerals in all regions of the Kingdom of Saudi Arabia except for those land and

marine areas that ate out of the scope of application of the mining investment regulations as stipulated inArticle (8) of the said regulation.

2 SIGNIFICANT ACCOUNTING POLICIES

2.1 Statement of compliance

These interim condensed consolidated financial statements have been prepared in accordance with InternationalAccounting Standard (IAS), “Interim Financial Reporting” (“IAS 34”) as endorsed in KSA. These are also the Group’s firstinterim condensed consolidated financial statements in accordance with International Financial Reporting Standards(“IFRS”), for part of the period covered by the first annual financial statements prepared in accordance with IFRSendorsed in KSA and other standards and pronouncements that are issued by the Saudi Organization for Certified PublicAccountants (“SOCPA”) (collectively referred to “IFRS as endorsed in KSA”), and accordingly IFRS 1 “First-time Adoptionof International Financial Reporting Standards” endorsed in KSA has been applied. Refer to Note 4 for furtherinformation. The interim condensed consolidated financial statements do not include all the information anddisclosures required in annual financial statements to be prepared in accordance with IFRS as endorsed in KSA, whichwould be prepared for the year ending 31 December 2017.

These interim condensed consolidated financial statements have been prepared under the historical cost convention.The interim condensed consolidated financial statements are presented in Saudi Riyals and all values are rounded tothe nearest one Saudi Riyal, except when otherwise indicated.

Results for the interim reporting period are not necessarily indicative of future periods.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

9

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.2 Basis of consolidation

The subsidiary companies incorporated into these interim condensed consolidated financial statements are asfollows:

Subsidiary CompanyCountry of

incorporation

Percentage of ownership (directly orindirectly)

%31

March2017

31December

2016

1January

2016Tabuk Pharmaceutical Manufacturing Company (“TPMC”)TPMC has the following subsidiaries:

Kingdom of Saudi Arabia 100 100 100

- Tabuk Pharmaceutical Research Company Kingdom of Jordan 100 100 100- Tabuk Pharmaceutical Company Limited Republic of the Sudan 100 100 100- Tabuk Pharmaceutical Manufacturing Company Arab republic of Egypt 100 100 100- Tabuk Eurl Algeria People's Democratic

Republic of Algeria100 100 100

- Al Bareq Pharmaceutical Manufacturing Factory CompanyLimited Kingdom of Saudi Arabia 100 100 100

Astra Polymer Compounding Company Limited (“Polymer”)Polymer has the following subsidiaries:

Kingdom of Saudi Arabia 100 100 100

- Astra Polymers free zone Imalat Sanayi Ve Ticaret AnonimSirketi.

Republic of Turkey 100 100 100

- Astra Polymer Pazarlama San. Ve Tic. A.Ş Republic of Turkey 100 100 100- Astra Specialty Compounds India Private Limited Republic of India 100 100 100

International Building Systems Factory Company Limited(“IBSF”)IBSF has the following subsidiary:

Kingdom of Saudi Arabia 100 100 100

- Astra Heavy Industries Factory Limited (“AHI”) Kingdom of Saudi Arabia 100 100 100

Astra Industrial Complex Co. Ltd. for Fertilizer andAgrochemicals (“AstraChem”)AstraChem has the following foreign subsidiaries:

Kingdom of Saudi Arabia 100 100 100

- AstraChem Saudia People's DemocraticRepublic of Algeria

100 100 100

- AstraChem Morocco Kingdom of Morocco 100 100 100- Aggis International Limited British Virgin Islands 100 100 100- AstraChem Turkey Republic of Turkey 100 100 100- AstraChem Syria Syrian Arab Republic 100 100 100- AstraChem Tashqand Republic of Uzbekistan 100 100 100- Astra Industrial Complex Co. Ltd. for Fertilizer and

Agrochemicals, JordanKingdom of Jordan 50 50 50

- Astra Nova, Turkey Republic of Turkey 92.4 92.4 92.4- AstraChem Ukraine Ltd. Ukraine 100 100 100

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

10

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.2 Basis of consolidation (continued)

Subsidiary Company Country ofincorporation

Percentage of ownership (directly orindirectly)

31March

2017

31December

2016

1January

2016- AstraChem Saudi Jordan Co. Arab republic of Egypt 100 100 100- Astra Agricultural Saudi Jordan Co. Arab republic of Egypt 100 100 100

Astra Industrial Complex for Fertilizers and Agrochemicals andInvestments

Sultanate of Oman 99 99 99

Green Highland Seeds Company Limited - Jordon Kingdom of Jordan 100 100 100

Astra Energy LLC (“Astra Energy”)Astra Energy has the following subsidiary:

Kingdom of Jordan76 76 76

- Fertile Crescent for Electricity Generation Company Republic of Iraq 100 100 100

Astra Mining Company Limited (“Astra Mining”) Kingdom of Saudi Arabia 60 60 60

The interim condensed consolidated financial statements comprise the financial statements of the Company and itssubsidiaries as at 31 March 2017.

Control is achieved when the Group is exposed, or has rights, to variable returns from its involvement with theinvestee and has the ability to affect those returns through its power over the investee. Specifically, the Groupcontrols an investee if, and only if, the Group has:

• Power over the investee (i.e., existing rights that give it the current ability to direct the relevant activities ofthe investee)

• Exposure, or rights, to variable returns from its involvement with the investee• The ability to use its power over the investee to affect its returns

Generally, there is a presumption that a majority of voting rights results in control. To support this presumption andwhen the Group has less than a majority of the voting or similar rights of an investee, the Group considers allrelevant facts and circumstances in assessing whether it has power over an investee, including:

· The contractual arrangement(s) with the other vote holders of the investee· Rights arising from other contractual arrangements· The Group’s voting rights and potential voting rights

The Group re-assesses whether or not it controls an investee if facts and circumstances indicate that there arechanges to one or more of the three elements of control. Consolidation of a subsidiary begins when the Groupobtains control over the subsidiary and ceases when the Group loses control of the subsidiary. Assets, liabilities,income and expenses of a subsidiary acquired or disposed of during the period are included in the interim condensedconsolidated financial statements from the date the Group gains control until the date the Group ceases to controlthe subsidiary.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

11

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.2 Basis of consolidation (continued)

Income and each component of other comprehensive income (OCI) are attributed to the equity holders of the parentof the Group and to the non-controlling interests, even if this results in the non-controlling interests having a deficitbalance. Financial statements of subsidiaries are prepared using accounting policies which are consistent with thoseof the Group. All intra-group assets and liabilities, equity, income, expenses and cash flows relating to transactionsbetween members of the Group are eliminated in full on consolidation.

A change in the ownership interest of a subsidiary, without a loss of control, is accounted for as an equitytransaction. If the Group loses control over a subsidiary, it derecognises the related assets (including goodwill),liabilities, non-controlling interest and other components of equity, while any resultant gain or loss is recognisedin interim condensed consolidated statement of income. Any investment retained is recognised at fair value.

2.3 Summary of significant accounting policies

The following are the significant accounting policies applied by the Group in preparing its interim condensedconsolidated financial statements:

2.3.1 Business combination and goodwill

Business combinations are accounted for using the acquisition method. The cost of an acquisition ismeasured as the aggregate of the consideration transferred, which is measured at the acquisition date fairvalue and the amount of any non-controlling interest in the acquiree. For each business combination, theGroup elects to measure the non-controlling interest in the acquiree at the proportionate share of theacquiree’s identifiable net assets. Acquisition-related costs are expensed as incurred and included in generaland administrative expenses.

When the Group acquires a business, it assesses the financial assets acquired and liabilities assumed forappropriate classification and designation in accordance with the contractual terms, economiccircumstances and pertinent conditions as at the acquisition date.

Any contingent consideration, if any, to be transferred by the acquirer will be recognised at fair value at theacquisition date. Contingent consideration that is classified as equity is not remeasured and subsequentsettlement is accounted for within equity.

Goodwill is initially measured at cost (being the excess of the aggregate of the consideration transferred andthe amount recognised for non-controlling interests) and any previous interest held, over the net identifiableassets acquired and liabilities assumed. If the fair value of the net assets acquired is in excess of the aggregateconsideration transferred, the Group re-assesses whether it has correctly identified all of the assets acquiredand all of the liabilities assumed and reviews the procedures used to measure the amounts to be recognisedat the acquisition date. If the reassessment still results in an excess of the fair value of net assets acquiredover the aggregate consideration transferred, then the gain is recognised in profit or loss.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

12

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.1 Business combination and goodwill (continued)

After initial recognition, goodwill is measured at cost less any accumulated impairment losses. For thepurpose of impairment testing, goodwill acquired in a business combination is, from the acquisition date,allocated to each of the Group’s cash-generating units that are expected to benefit from the combination,irrespective of whether other assets or liabilities of the acquiree are assigned to those units.

Where goodwill has been allocated to a cash-generating unit (CGU) and part of the operation within thatunit is disposed of, the goodwill associated with the disposed operation is included in the carrying amountof the operation when determining the gain or loss on disposal of the operation. Goodwill disposed in thesecircumstances is measured based on the relative values of the disposed operation and the portion of thecash- generating unit retained.

2.3.2 Investments in associates and joint venture

An associate is an entity over which the Group has significant influence. Significant influence is the power toparticipate in the financial and operating policy decisions of the investee, but is not control or joint controlover those policies.

A joint venture is a type of joint arrangement whereby the parties that have joint control of the arrangementhave rights to the net assets of the joint venture. Joint control is the contractually agreed sharing of controlof an arrangement, which exists only when decisions about the relevant activities require the unanimousconsent of the parties sharing control.

The considerations made in determining whether significant influence or joint control are similar to thosenecessary to determine control over subsidiaries.

The Group’s investments in its associates and joint venture are accounted for using the equity method.Under the equity method, the investment in an associates or a joint venture is initially recognised at cost.The carrying amount of the investment is adjusted to recognise changes in the Group’s share of net assetsof the associate or joint venture since the acquisition date. Goodwill relating to the associate or joint ventureis included in the carrying amount of the investment and is not tested for impairment separately.

The interim condensed statement of income reflects the Group’s share of the results of operations of theassociates and joint venture. Any change in OCI of those investees is presented as part of the Group’s OCI.In addition, when there has been a change recognised directly in the equity of the associates or joint venture,the Group recognises its share of any changes, when applicable, in the statement of changes in equity.Unrealised gains and losses resulting from transactions between the Group and the associates or jointventure are eliminated to the extent of the interest in the associate or joint venture.

The aggregate of the Group’s share of profit or loss of an associates or joint venture is shown on the face ofthe interim condensed statement of income outside operating profit and represents profit or loss and non-controlling interests in the subsidiaries of the associate or joint venture, if any.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

13

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.2 Investments in associates and joint venture (continued)

The financial statements of the associate or joint venture are prepared for the same reporting period as theGroup. When necessary, adjustments are made to bring the accounting policies in line with those of theGroup.

After application of the equity method, the Group determines whether it is necessary to recognise animpairment loss on its investments in its associate. The Group determines at each reporting date whetherthere is any objective evidence that the investment in the associate is impaired. If this is the case, the Groupcalculates the amount of impairment as the difference between the recoverable amount of the associateand its carrying value and recognises the loss as ‘Share of profit of an associates’ in the interim condensedstatement of income.

Upon loss of significant influence over the associate, the Group measures and recognises any retainedinvestment at its fair value. Any difference between the carrying amount of the associate upon loss ofsignificant influence or joint control and the fair value of the retaining investment and proceeds fromdisposal is recognised in interim condensed consolidated statement of income.

2.3.3 Current versus non-current classification

The Group presents assets and liabilities in the statement of financial position based on current/non-currentclassification. An asset is current when it is:

· Expected to be realised or intended to be sold or consumed in the normal operating cycle· Held primarily for the purpose of trading· Expected to be realised within twelve months after the reporting period, or· Cash or cash equivalent unless restricted from being exchanged or used to settle a liability for at least twelve

months after the reporting period.All other assets are classified as non-current.

A liability is current when:• It is expected to be settled in the normal operating cycle• It is held primarily for the purpose of trading• It is due to be settled within twelve months after the reporting period, or• There is no unconditional right to defer the settlement of the liability for at least twelve months after the

reporting period.

The Group classifies all other liabilities as non-current.

2.3.4 Revenue recognition

Revenue is recognised to the extent that it is probable that the economic benefits will flow to the Group andthe revenue can be reliably measured, regardless of when the payment is received. Revenue is measured atthe fair value of the consideration received or receivable, taking into account contractually defined terms ofpayment. The Group assesses its revenue arrangements against specific criteria to determine if it is acting asprincipal or agent. The Group has concluded that it is the principal in all of its revenue arrangements since it is theprimary obligor in all the revenue arrangements, has pricing latitude, and is also exposed to inventory and creditrisks.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

14

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.4 Revenue recognition (continued)

The following specific recognition criteria must also be met before revenue is recognised:

2.3.4.1 Sale of goods

Sale of goods represent the invoiced value of goods supplied and services rendered by the Group during theyear. Revenue from the sale of goods is recognised when the significant risks and rewards of ownership ofthe goods have passed to the buyer, usually on delivery of the goods. Revenue from the sale of goods ismeasured at the fair value of the consideration received or receivable, net of returns and allowances, tradediscounts and volume rebates.

The Group provides normal warranty provisions on all its products sold, in line with industry practice. Aliability for potential warranty claims is recognised at the time the product is sold.

2.3.4.2 Revenue from contracted services

Revenues from rendering of services are recognised when contracted services are performed. Contractrevenue includes the unbilled contract revenue during the period. For long term contracts, revenue isrecognised on the basis of costs incurred to date, using the percentage of completion method. Stage ofcompletion is measured by reference to costs incurred to date as a percentage of total estimated cost foreach contract. In the case of unprofitable contracts, provision is made for foreseeable losses in full. Whenthe contract outcome cannot be measured reliably, revenue is recognised only to the extent that theexpenses incurred are eligible to be recovered.

2.3.4.3 Royalty and other income

Royalty income is generated from providing right to use Group’s production facilities and related royaltyincome is recognized on an accrual basis in accordance with the substance of agreements. Other incomeincludes income from toll manufacturing including income from product repackaging for third parties. Somearrangements include collection of receipts on behalf of third parties.

2.3.5 Foreign currencies

The Group’s interim condensed consolidated financial statements are presented in Saudi Riyals, which is alsothe Group’s functional currency. For each entity, the Group determines the functional currency and itemsincluded in the financial statements of each entity are measured using that functional currency. The Groupuses the direct method of consolidation and on disposal of a foreign operation, the gain or loss that isreclassified to profit or loss reflects the amount that arises from using this method.

2.3.5.1 Transactions and balances

Transactions in foreign currencies are initially recorded by the Group entities at their respective functionalcurrency spot rate at the date the transaction first qualifies for recognition.

Monetary assets and liabilities denominated in foreign currencies are retranslated at the functional currencyspot rate of exchange ruling at the reporting date.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

15

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.5.1 Transactions and balances (continued)

Differences arising on settlement or translation of monetary items are recognised in interim condensedstatement of income with the exception of monetary items that are designated as part of the hedge of theGroup’s net investment of a foreign operation. These are recognised in OCI until the net investment isdisposed of, at which time, the cumulative amount is classified to interim condensed statement of income.Tax charges and credits, if any, attributable to exchange differences on those monetary items are alsorecorded in OCI.

Non-monetary items that are measured in terms of historical cost in a foreign currency are translated usingthe exchange rates as at the dates of the initial transactions.

2.3.5.2 Group companies

On consolidation, the assets and liabilities of foreign operations are translated into Saudi Riyals at the rateof exchange prevailing at the reporting date and their interim condensed statement of income are translatedat exchange rates prevailing at the dates of the transactions. The exchange differences arising on thetranslation are recognised in OCI. On disposal of a foreign operation, the component of OCI relating to thatparticular foreign operation is recognised in the interim condensed statement of income.

2.3.6 Zakat and income tax

2.3.6.1 Current income taxCurrent income tax assets and liabilities for the current period are measured at the amount expected to berecovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amountare those that are enacted, or substantively enacted at the reporting date in the countries where the Groupoperates and generates taxable income.

Management periodically evaluates positions taken in the tax returns with respect to situations in whichapplicable tax regulations are subject to interpretation, and it establishes provisions where appropriate.

2.3.6.2 Deferred tax

Deferred tax is provided using the liability method on temporary differences between the tax bases of assetsand liabilities and their carrying amounts for financial reporting purposes at the reporting date.

Deferred tax liabilities are recognised for all taxable temporary differences, except:· When the deferred tax liability arises from the initial recognition of goodwill or an asset or liability

in a transaction that is not a business combination and, at the time of the transaction, affects neitherthe accounting profit nor taxable profit or loss

· In respect of taxable temporary differences associated with investments in subsidiaries, associates,when the timing of the reversal of the temporary differences can be controlled and it is probablethat the temporary differences will not reverse in the foreseeable future

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

16

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.6.2 Deferred tax (continued)

Deferred tax assets are recognised for all deductible temporary differences, the carry forward of unused taxcredits and unused tax losses, to the extent that it is probable that taxable profit will be available againstwhich the deductible temporary differences. The carry forward of unused tax credits and unused tax lossescan be utilised, except:

· When the deferred tax asset relating to the deductible temporary difference arises from the initialrecognition of an asset or liability in a transaction that is not a business combination and, at the timeof the transaction, affects neither the accounting profit nor taxable profit or loss

· In respect of deductible temporary differences associated with investments in subsidiaries,associates and interests in joint arragements, deferred tax assets are recognised only to the extentthat it is probable that the temporary differences will reverse in the foreseeable future and taxableprofit will be available against which the temporary differences can be utilized

The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extentthat it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferredtax asset to be utilised. Unrecognised deferred tax assets are reassessed at each reporting date and arerecognised to the extent that it has become probable that future taxable profits will allow the deferred taxasset to be recovered.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the year whenthe asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted orsubstantively enacted at the reporting date.

Deferred tax relating to items recognised outside profit or loss is recognised outside profit or loss. Deferredtax items are recognised in correlation to the underlying transaction either in other comprehensive incomeor directly in equity.

Deferred tax assets and deferred tax liabilities are offset if a legally enforceable right exists to set off currenttax assets against current income tax liabilities and the deferred taxes relate to the same taxable entity andthe same taxation authority.

Tax benefits acquired as part of a business combination, but not satisfying the criteria for separaterecognition at that date, are recognised subsequently if new information about facts and circumstanceschange. The adjustment is either be treated as a reduction to goodwill (as long as it does not exceedgoodwill) if it is incurred during the measurement period or recognised in profit or loss.

2.3.6.3 Zakat

Zakat is provided for in accordance with the Saudi Arabian fiscal regulations. The liability is charged tointerim condensed consolidated statement of income.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

17

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.7 Property, plant and equipment

Property, plant and equipment are stated at cost, net of accumulated depreciation and accumulatedimpairment losses, if any, except for land and construction work in progress which are stated at cost. Suchcost includes the cost of replacing parts of the property, plant and equipment and borrowing costs forqualifying assets if the recognition criteria are met. When significant parts of property, plant and equipmentare required to be replaced at intervals, the Group recognises such parts as individual assets with specificuseful lives and depreciates them accordingly. Likewise, when a major inspection is performed, its cost isrecognised in the carrying amount of the plant and equipment as a replacement if the recognition criteria issatisfied. All other repair and maintenance costs are recognised in the profit or loss as incurred. The presentvalue of the expected cost for the decommissioning of the asset after its use, is included in the cost of therespective asset if the recognition criteria for a provision are met. Refer to Significant accountingjudgements, estimates and assumptions (Note 3).

Contributions by customers of items of property, plant and equipment received, which require an obligationto supply goods to the customer in the future, are recognised at the fair value when the Group has controlof the item. A corresponding credit to deferred revenue is made. Revenue is subsequently recognised overthe contractual period, in the absence of which revenue is recognised over the useful lives of the transferredassets. In the absence of an ongoing obligation to supply goods in future, contributions are recognised asrevenue immediately.

A units of production method of depreciation is applied to operations in their start-up phase, as this reflectsthe expected pattern of consumption of the future economic benefits embodied in the assets.

Depreciation on a straight-line basis is calculated over the estimated useful lives of the assets as follows:Years

Buildings 10 - 33Leasehold improvements 4 - 10Machinery and equipment 5 - 20Furniture, fixtures and office equipment 3 - 10Vehicles 4

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits areexpected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the differencebetween the net disposal proceeds and the carrying amount of the asset) is included in the interim condensedconsolidated statement of income when the asset is derecognised.

The residual values, useful lives and methods of depreciation of property, plant and equipment are reviewed at eachperiod end and adjusted accordingly, if appropriate.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

18

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.7 Property, plant and equipment (continued)

Leasehold improvements are amortised over the shorter of the estimated useful life or the remaining term of thelease. The capitalised leased assets are depreciated over the shorter of the estimated useful life of the asset or thelease term.

2.3.8 LeasesThe determination of whether an arrangement is, or contains, a lease is based on the substance of thearrangement at the inception date. The arrangement is assessed for whether fulfilment of the arrangementis dependent on the use of a specific asset or assets and the arrangement conveys a right to use the asset orassets, even if that right is not explicitly specified in an arrangement.

2.3.8.1 Group as a lesseeFinance leases that transfer to the Group substantially all of the risks and benefits incidental to ownershipof the leased item, are capitalised at the commencement of the lease at the fair value of the leased propertyor, if lower, at the present value of the minimum lease payments. Lease payments are apportioned betweenfinance charges and a reduction in the lease liability so as to achieve a constant rate of interest on theremaining balance of the liability. Finance charges are recognised in finance costs in the interim condensedconsolidated statement of income.

A leased asset is depreciated over the useful life of the asset. However, if there is no reasonable certaintythat the Group will obtain ownership by the end of the lease term, the asset is depreciated over the shorterof the estimated useful life of the asset and the lease term.

An operating lease is a lease other than a finance lease. Operating lease payments are recognised as anoperating expense in the interim condensed consolidated statement of income on a straight-line basis overthe lease term.

2.3.8.2 Group as a lessorLeases in which the Group does not transfer substantially all the risks and benefits of ownership of the assetare classified as operating leases. Initial direct costs incurred in negotiating and arranging an operating leaseare added to the carrying amount of the leased asset and recognised over the lease term on the same basesas rental income. Contingent rents are recognised as revenue in the period in which they are earned.

2.3.9 Financial guarantee contractsFinancial guarantee contracts issued by the Group are those contracts that require a payment to be madeto reimburse the holder for a loss it incurs because the specified debtor fails to make a payment when duein accordance with the terms of a debt instrument. Financial guarantee contracts are recognised initially asa liability at fair value, adjusted for transaction costs that are directly attributable to the issuance of theguarantee. Subsequently, the liability is measured at the higher of the best estimate of the expenditurerequired to settle the present obligation at the reporting date and the amount recognised less cumulativeamortization.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

19

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.10 Borrowing costsBorrowing costs directly attributable to the acquisition, construction or production of an asset thatnecessarily takes a substantial period of time to get ready for its intended use or sale are capitalised as partof the cost of the respective asset. All other borrowing costs are expensed in the period in which they occur.Borrowing costs consist of interest and other costs that an entity incurs in connection with the borrowing offunds.

2.3.11 Intangible assetsIntangible assets acquired separately are measured on initial recognition at cost. The cost of intangible assetsacquired in a business combination is their fair value as at the date of acquisition. Following initialrecognition, intangible assets are carried at cost less accumulated amortisation and accumulatedimpairment losses, if any. Internally generated intangible assets, excluding capitalised development costs,are not capitalised and expenditure is recognised in the interim condensed consolidated statement ofincome when it is incurred.

The useful lives of intangible assets are assessed as either finite or indefinite.

Intangible assets with finite lives are amortised over their useful economic lives, which ranges from 4 to 7years, and assessed for impairment whenever there is an indication that the intangible asset may beimpaired. The amortisation period and the amortisation method for an intangible asset with a finite usefullife are reviewed at least at the end of each reporting period. Changes in the expected useful life or theexpected pattern of consumption of future economic benefits embodied in the asset are accounted for bychanging the amortisation period or method, as appropriate, and are treated as changes in accountingestimates. The amortisation expense on intangible assets with finite lives is recognised in the interimcondensed consolidated statement of income in the expense category consistent with the function of theintangible assets.

Intangible assets with indefinite useful lives are not amortised, but are tested for impairment annually, eitherindividually or at the cash-generating unit level. The assessment of indefinite life is reviewed annually todetermine whether the indefinite life continues to be supportable. If not, the change in useful life fromindefinite to finite is made on a prospective basis.

Gains or losses arising from derecognition of an intangible asset are measured as the difference betweenthe net disposal proceeds and the carrying amount of the asset and are recognised in the interim condensedconsolidated statement of income when the asset is derecognised.

Research costsResearch costs are expensed as incurred.

Patents and licencesThe Group made upfront payments to purchase patents and licences. The patents have been granted for aperiod of 10 years by the relevant government agency with the option of renewal at the end of this period.Licences for the use of intellectual property are granted for periods ranging between five and ten yearsdepending on the specific licences. The licences may be renewed at little or no cost to the Group. As a result,the licences are assessed as having an indefinite useful life.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

20

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.11 Intangible assets (continued)

A summary of the policies applied to the Group’s intangible assets is as follows:

Licences Patents

Useful lives Finite (10 years) Finite (5-10 years)

Amortisation method used Amortised on a straight- line basis overthe period of the patent

Amortised on a straight- line basis overthe period of the patent

Internally generatedor acquired

Acquired Acquired

2.3.12 Financial instruments:A financial instrument is any contract that gives rise to a financial asset of one entity and a financial liabilityor equity instrument of another entity.

2.3.12.1 Financial assets2.3.12.1.1 Initial recognition and measurementFinancial assets are classified, at initial recognition, as financial assets at fair value through profit or loss,loans and receivables, held-to-maturity investments, Available for Sale (AFS) financial assets. The Groupdetermines the classification of its financial assets at initial recognition. All financial assets are recognisedinitially at fair value plus, in the case of assets not at fair value through profit or loss, transaction costs thatare attributable to the acquisition of the financial asset.

Purchases or sales of financial assets that require delivery of assets within a time frame established byregulation or convention in the marketplace (regular way trades) are recognised on the trade date, i.e. thedate on which the Group commits to purchase or sell the asset.

2.3.12.1.2 Subsequent measurementThe subsequent measurement of financial assets depends on their classification as described below:

2.3.12.1.3 Financial assets at fair value through profit or lossFinancial assets at fair value through profit or loss include financial assets held for trading and financial assetsdesignated upon initial recognition at fair value through profit or loss. Financial assets are classified as held-for- trading if they are acquired for the purpose of selling or repurchasing in the near term. Subsequent toinitial recognition, they are remeasured at fair value. Changes in fair value are recorded in ‘Fair value gainsand losses’.

2.3.12.1.4 Loans and receivablesThis category is the most relevant to the Group. Loans and receivables are non-derivative financial assetswith fixed or determinable payments that are not quoted in an active market. After initial measurement,such financial assets are subsequently measured at amortised cost using the effective interest rate (EIR)method, less impairment. Amortised cost is calculated by taking into account any discount or premium onacquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is included in financecost in the interim condensed consolidated statement of income, except for short-term receivables whenthe recognition of interest would be immaterial. The losses arising from impairment are recognised in the

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

21

interim condensed consolidated statement of income in finance costs for loans and in cost of sales or otheroperating expenses for receivables.

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.14.1.4 Loans and receivables (continued)Effective interest method:The effective interest method is a method of calculating the amortised cost of a debt instrument and of allocatinginterest income over the relevant period. The effective interest rate is the rate that exactly discounts estimated futurecash receipts (including all fees paid or received that form an integral part of the effective interest rate, transactioncosts and other premiums or discounts) through the expected life of the debt instrument, or, where appropriate, ashorter period, to the net carrying amount on initial recognition. Income is recognised on an effective interest basisfor debt instruments other than those financial assets classified as at FVTPL.

2.3.12.1.5 DerecognitionA financial asset (or, where applicable, a part of a financial asset or part of a group of similar financial assets)is derecognised when:

· The rights to receive cash flows from the asset have expired, or· The Group has transferred its rights to receive cash flows from the asset or has assumed an

obligation to pay the received cash flows in full without material delay to a third party under a ‘pass-through’ arrangement, and either

a) Group has transferred substantially all the risks and rewards of the asset, orb) Group has neither transferred nor retained substantially all the risks and rewards of the

asset, but has transferred control of the asset.

When the Group has transferred its rights to receive cash flows from an asset or has entered into a pass-through arrangement, it evaluates if and, to what extent, it has retained the risks and rewards of ownership.When it has neither transferred nor retained substantially all of the risks and rewards of the asset nortransferred control of it, the asset is recognised to the extent of its continuing involvement in it. In that case,the Group also recognises an associated liability. The transferred asset and the associated liability aremeasured on a basis that reflects the rights and obligations that the Group has retained.

Continuing involvement that takes the form of a guarantee over the transferred asset is measured at thelower of the original carrying amount of the asset and the maximum amount of consideration that the Groupcould be required to repay.

2.3.12.1.6 Impairment of financial assetsThe Group assesses, at each reporting date, whether there is any objective evidence that a financial asset ora group of financial assets is impaired. An impairment exists if one or more events that has occurred sincethe initial recognition of the asset (an incurred ‘loss event’), has an impact on the estimated future cashflows of the financial asset or the group of financial assets that can be reliably estimated. Evidence ofimpairment may include indications that the debtors or a group of debtors is experiencing significantfinancial difficulty, default or delinquency in interest or principal payments, the probability that they willenter bankruptcy or other financial reorganisation and where observable data indicate that there is ameasurable decrease in the estimated future cash flows, such as changes in arrears or economic conditionsthat correlate with defaults.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

22

2 SIGNIFICANT ACCOUNTING POLICIES

2.3.12.1.7 Financial assets carried at amortised costFor financial assets carried at amortised cost, the Group first assesses whether impairment exists individuallyfor financial assets that are individually significant, or collectively for financial assets that are not individuallysignificant. If the Group determines that no objective evidence of impairment exists for an individuallyassessed financial asset, whether significant or not, it includes the asset in a group of financial assets withsimilar credit risk characteristics and collectively assesses them for impairment. Assets that are individuallyassessed for impairment and for which an impairment loss is, or continues to be, recognised are not includedin a collective assessment of impairment.

The amount of any impairment loss identified is measured as the difference between the asset’s carryingamount and the present value of estimated future cash flows (excluding future expected credit losses thathave not yet been incurred). The present value of the estimated future cash flows is discounted at thefinancial asset’s original effective interest rate.

The carrying amount of the asset is reduced through the use of an allowance account and the amount of theloss is recognised in the interim condensed consolidated statement of income. Interest income continues tobe accrued on the reduced carrying amount using the rate of interest used to discount the future cash flowsfor the purpose of measuring the impairment loss. The interest income is recorded as part of finance incomein the interim condensed consolidated statement of income. Loans, together with the associated allowanceare written off when there is no realistic prospect of future recovery and all collateral has been realised orhas been transferred to the Group. If, in a subsequent year, the amount of the estimated impairment lossincreases or decreases because of an event occurring after the impairment was recognised, the previouslyrecognised impairment loss is increased or reduced by adjusting the allowance account. If a write-off is laterrecovered, the recovery is credited to finance costs in profit or loss.

2.3.12.2 Financial liabilities

2.3.12.2.1 Initial recognition and measurementFinancial liabilities are classified, at initial recognition, as financial liabilities at fair value through profit orloss, loans and borrowings and payables.

All financial liabilities are recognised initially at fair value and, in the case of loans and borrowings andpayables, net of directly attributable transaction costs.

The Group’s financial liabilities include trade and other payables, loans and borrowings including bankoverdrafts.

2.3.12.2.2 Subsequent measurementThe measurement of financial liabilities depends on their classification, as follows:

2.3.12.2.3 Financial liabilities at fair value through profit or lossFinancial liabilities at fair value through profit or loss include financial liabilities held-for-trading and financialliabilities designated upon initial recognition as at fair value through profit or loss.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

23

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

Gains or losses on liabilities held-for-trading are recognised in the interim condensed consolidatedstatement of income. Financial liabilities designated upon initial recognition at fair value through profit orloss are designated at the initial date of recognition, and only if the criteria in IAS 39 are satisfied. The Grouphas not designated any financial liabilities as at fair value through profit or loss.

2.3.12.2.4 Loans and borrowingsThis is the category most relevant to the Group. After initial recognition, interest bearing loans andborrowings are subsequently measured at amortised cost using the effective interest rate method. Gainsand losses are recognised in the interim condensed consolidated statement of income when the liabilitiesare derecognised as well as through the EIR method amortisation process.

Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or coststhat are an integral part of the EIR. The EIR amortisation is included in finance costs in the interim condensedconsolidated statement of income.

This category generally applies to interest-bearing loans and borrowings, and trade and other payables(liabilities recognised for amounts to be paid in the future for goods or services received, whether or notbilled to the Group.)

2.3.12.2.5 DerecognitionA financial liability is derecognised when the obligation under the liability is discharged or cancelled orexpires. When an existing financial liability is replaced by another from the same lender on substantiallydifferent terms, or the terms of an existing liability are substantially modified, such an exchange ormodification is treated as a derecognition of the original liability and the recognition of a new liability. Thedifference in the respective carrying amounts is recognised in the interim condensed consolidated statementof income.

2.3.13 Offsetting of financial instrumentsFinancial assets and financial liabilities are offset with the net amount reported in the interim condensedconsolidated statement of financial position only if there is a current enforceable legal right to offset therecognised amounts and an intent to settle on a net basis, or to realise the assets and settle the liabilitiessimultaneously.

2.3.14 InventoriesInventories are stated at the lower of cost or net realisable value. Cost of raw and packing materials, spareparts, consumables and finished goods is principally determined on a weighted average cost basis.Inventories of work in progress and finished goods include cost of materials, labor and an appropriateproportion of direct overheads based on normal level of activity. When inventories become old or obsolete,a provision for slow moving and obsolete inventories is provided and charged to the interim condensedconsolidated statement of income.

Net realisable value is the estimated selling price in the ordinary course of business, less estimated costs ofcompletion and the estimated costs to sell.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

24

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.15 Impairment of non-financial assetsThe Group assesses at each reporting date whether there is an indication that an asset may be impaired. Ifany indication exists, or when annual impairment testing for an asset is required, the Group estimates theasset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or CGU’s fair valueless costs of disposal and its value in use. It is determined for an individual asset, unless the asset does notgenerate cash inflows that are largely independent of those from other assets or groups of assets. Wherethe carrying amount of an asset or CGU exceeds its recoverable amount, the asset is considered impairedand is written down to its recoverable amount.

In assessing value in use, the estimated future cash flows are discounted to their present value using adiscount rate that reflects current market assessments of the time value of money and the risks specific tothe asset. In determining fair value less costs of disposal, recent market transactions are taken into account.If no such transactions can be identified, an appropriate valuation model is used. These calculations arecorroborated by valuation multiples, quoted share prices for publicly traded subsidiaries or other availablefair value indicators.

The Group bases its impairment calculation on detailed budgets and forecasts which are prepared separatelyfor each of the Group’s CGU to which the individual assets are allocated. These budgets and forecastcalculations are generally covering a period of five years. A long-term growth rate is calculated and appliedto project future cash flows after the fifth year.

Impairment losses of continuing operations are recognised in the interim condensed consolidated statementof income in those expense categories consistent with the function of the impaired asset.

For assets excluding goodwill, an assessment is made at each reporting date as to whether there is anyindication that previously recognised impairment losses may no longer exist or may have decreased. If suchindication exists, the Group estimates the asset’s or CGU’s recoverable amount. A previously recognisedimpairment loss is reversed only if there has been a change in the assumptions used to determine the asset’srecoverable amount since the last impairment loss was recognised. The reversal is limited so that thecarrying amount of the asset does not exceed its recoverable amount, nor exceed the carrying amount thatwould have been determined, net of depreciation, had no impairment loss been recognised for the asset inprior years. Such reversal is recognised in the interim condensed consolidated statement of income.

The following criteria are also applied in assessing impairment of specific assets:

2.3.16 Impairment of GoodwillGoodwill is tested for impairment annually as at 31 December and when circumstances indicate that thecarrying value may be impaired.Impairment is determined for goodwill by assessing the recoverable amount of each CGU (or group of CGUs)to which the goodwill relates. Where the recoverable amount of the cash-generating unit is less than theircarrying amount, an impairment loss is recognised.

Impairment losses relating to goodwill cannot be reversed in future periods.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

25

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.17 Impairment of intangible assets with indefinite useful livesIntangible assets with indefinite useful lives are tested for impairment annually as at 31 December eitherindividually or at the CGU level, as appropriate and when circumstances indicate that the carrying value maybe impaired.

2.3.18 Cash and cash equivalentsCash and cash equivalents in the statement of financial position comprise cash at banks and on hand andshort-term deposits including Murabaha investments with a maturity of three months or less, which aresubject to an insignificant risk of changes in value.

For the purpose of the interim condensed consolidated statement cash flows, cash and cash equivalentsconsist of cash and short-term deposits as defined above, as they are considered an integral part of theGroup’s cash management.

2.3.19 ExpensesSelling and marketing expenses are those that mainly relate to salesmen and sales department, whereresearch and development expenses specifically relate to costs related to the research and developmentdepartment. All other expenses are allocated on a consistent basis to cost of sales and general andadministration expenses in accordance with allocation factors determined as appropriate by the Group.

2.3.20 Cash dividend and non-cash distribution to equity holders of the parentThe Group recognises a liability to make cash or non-cash distributions to equity holders of the parent whenthe distribution is authorised and the distribution is no longer at the discretion of the Company. As per thecompanies regulations of Saudi Arabia, a distribution is authorised when it is approved by the shareholders.A corresponding amount is recognised directly in equity.

Non-cash distributions are measured at the fair value of the assets to be distributed with fair valueremeasurement recognised directly in equity.

Upon distribution of non-cash assets, any difference between the carrying amount of the liability and thecarrying amount of the assets distributed is recognised in the interim condensed consolidated statement ofincome.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

26

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.3.21 Provision2.3.21.1 GeneralProvisions are recognised when the Group has a present obligation (legal or constructive) as a result of apast event, it is probable that an outflow of resources embodying economic benefits will be required tosettle the obligation and a reliable estimate can be made of the amount of the obligation. Where the Groupexpects some or all of a provision to be reimbursed, for example under an insurance contract, thereimbursement is recognised as a separate asset but only when the reimbursement is virtually certain. Theexpense relating to a provision is presented in the interim condensed consolidated statement of income netof any reimbursement, if any. If the effect of the time value of money is material, provisions are discountedusing a current rate that reflects, when appropriate, the risks specific to the liability. When discounting isused, the increase in the provision due to the passage of time is recognised as a finance cost.

2.3.21.2 Net employee defined benefit liabilitiesThe Group operates a defined benefit scheme for its employees in accordance with labor regulationsapplicable in the Kingdom of Saudi Arabia. The cost of providing the benefits under the defined benefits planis determined using the projected unit credit method. Actuarial gains and losses are recognized in full in theperiod in which they occur in other comprehensive income. Such actuarial gains and losses are alsoimmediately recognized in the retained earnings and are not reclassified to profit or loss in subsequentperiods. Re-measurements are not reclassified to profit or loss in subsequent periods.

Interest expense is calculated by applying the discount rate to the net defined benefit liability. The Grouprecognises the following changes in the net defined benefit obligation under ‘cost of sales’, ‘general andadministration expenses’ and ‘selling and distribution expenses’ in the interim condensed consolidatedstatement of income (by function).

· Service costs comprising current service costs, past-service costs, gains and losses on curtailmentsand non-routine settlements, and

· Net interest expense or income

The defined benefit asset or liability comprises the present value of the defined benefit obligation, less pastservice costs and less the fair value of plan assets out of which the obligations are to be settled. However,currently the plan is unfunded and has no assets.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

27

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.4 First time adoption of IFRS

For all periods up to and including the year ended 31 December 2016, the Group prepared and published itsaudited consolidated financial statements in accordance with Generally Accepted Accounting Principles(GAAP) issued by SOCPA in KSA (“SOCPA GAAP”). As noted in note 2.1, these interim condensed consolidatedfinancial statements are the Group’s first such financial statements in accordance with the IFRS as endorsedin KSA.

Accordingly, the Group has applied the IFRS as endorsed in KSA for preparation of its interim consolidatedfinancial statements for the period beginning 1 January 2017, as well as for presenting the relevantcomparative period data. In compliance with requirements of IFRS 1 endorsed in KSA, the Group’s openingstatement of consolidated financial position was prepared as at 1 January 2016 after incorporating requiredadjustments to reflect the transition to IFRS as endorsed in KSA from the previous SOCPA GAAP. The Grouphas analysed the impact on the statement of consolidated financial positions as at 1 January 2016, 31December 2016 and also the interim consolidated financial statements for the three month period ended31 March 2016, and following are the significant adjustments in transitioning from SOCPA GAAP to IFRS asendorsed in KSA..

Exemptions applied:IFRS 1 allows first-time adopters certain exemptions from the retrospective application of certain requirementsunder IFRS.

The Group has applied the following exemptions:· IFRS 3 Business Combinations has not been applied to either acquisitions of subsidiaries that are considered

businesses under IFRS, or acquisitions of interests in associates and joint ventures that occurred before 1January 2016. The use of this exemption means that the SOCPA GAAP carrying amounts of assets andliabilities, that are required to be recognised under IFRS, is their deemed cost at the date of the acquisition.After the date of the acquisition, measurement is in accordance with IFRS. Assets and liabilities that do notqualify for recognition under IFRS are excluded from the opening IFRS statement of financial position. TheGroup did not recognise or exclude any previously recognised amounts as a result of IFRS recognitionrequirements. IFRS 1 also requires that the SOCPA GAAP carrying amount of goodwill must be used in theopening IFRS statement of financial position (apart from adjustments for goodwill impairment andrecognition or derecognition of intangible assets). In accordance with IFRS 1, the Group has tested goodwillfor impairment at the date of transition to IFRS. No goodwill impairment was deemed necessary at 1January 2016.

· The Group has not applied IAS 21 retrospectively to fair value adjustments and goodwill from businesscombinations that occurred before the date of transition to IFRS. Such fair value adjustments and goodwillare treated as assets and liabilities of the parent rather than as assets and liabilities of the acquiree.Therefore, those assets and liabilities are already expressed in the functional currency of the parent or arenon-monetary foreign currency items and no further translation differences occur.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

28

2 SIGNIFICANT ACCOUNTING POLICIES (continued)

2.4 First time adoption of IFRS (continued)In preparing its opening statement of financial position as at 1 January 2016, the consolidated financial statements for the year ended 31 December 2016 and theinterim consolidated financial statements for the three month period ended 31 March 2016 in accordance with IFRS as endorsed in KSA, the Group has analyzed theimpact and noted the following adjustments are required to the amounts reported previously in these financial statements that were prepared in accordance withSOCPA GAAP.

2.4.1 Group reconciliation of equity as at 1 January 2016

SOCPA GAAP1 January 2016 Re-classification Re-measurement

Effect ofdeconsolidationof a subsidiary IFRS as endorsed in KSA

1 January 2016 Notes SAR SAR SAR SAR SAR

(Note 2.4-C) Equity Issued capital 800,000,000 - - - 800,000,000 Statutory reserve 406,568,677 - - - 406,568,677 Retained earnings A B C D 630,344,934 (14,338,537) (370,232,751) - 245,773,646 Foreign currency translation reserve B (105,884,797) - 105,884,797 - - Effect of acquisition transaction withminority interest without change in control D (14,338,537) 14,338,537

-- -

Equity attributable to equity holders ofthe parent 1,716,690,277 - (264,347,954) - 1,452,342,323

Non-controlling interests C (300,140,920) - 317,019,898 16,878,978 Total equity 1,416,549,357 - (264,347,954) 317,019,898 1,469,221,301

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

29

2.4.2 Group reconciliation of equity as at 31 March 2016

SOCPA GAAP31 March 2016 Re-classification Re-measurement

Effect ofdeconsolidationof a subsidiary IFRS as endorsed in KSA

31 March 2016Notes SAR SAR SAR SAR SAR

(Note 2.4-C)

EquityIssued capital 800,000,000 - - - 800,000,000Statutory reserve 406,568,677 - - - 406,568,677Retained earnings A B C D 637,546,038 (14,338,537) (367,569,896) - 255,637,605Foreign currency translation reserve B (116,978,252) - 105,884,797 - (11,093,455)Effect of acquisition transaction withminority interest without change incontrol D (14,338,537) 14,338,537 - - -Equity attributable to equity holdersof the parent 1,712,797,926 - (261,685,099) - 1,451,112,827

Non-controlling interests C (326,486,097) 404,398 345,036,430 18,954,731Total equity 1,386,311,829 - (261,280,701) 345,036,430 1,470,067,558

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

30

2.4.3 Group reconciliation of equity as at 31 December 2016

SOCPA GAAP31 December 2016 Re-classification Re-measurement

Effect ofdeconsolidationof a subsidiary IFRS as endorsed in KSA

31 December 2016 SAR SAR SAR SAR SAR

(Note 2.4-C)

Equity NotesIssued capital 800,000,000 - - 800,000,000Statutory reserve 406,568,677 - - 406,568,677Retained earnings A B C D 533,631,787 (14,338,537) (367,323,505) - 151,969,745Foreign currency translationreserve B (230,393,670) - 105,884,797 - (124,508,873)

Effect of acquisition transactionwith non-controlling interestwithout change in control D (14,338,537) 14,338,537 - - -Equity attributable to equityholders of the parent 1,495,468,257 - (261,438,708) - 1,234,029,549

Non-controlling interests C (399,176,257) - (2,030) 424,263,398 25,085,111Total equity 1,096,292,000 - (261,440,738) 424,263,398 1,259,114,660

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

31

2.4.4 Group reconciliation of total comprehensive income for the period ended 31 March 2016

SOCPA GAAP31 March 2016 Re-measurement

Effect ofdeconsolidation of a

subsidiaryIFRS as endorsed

in KSA31 March 2016

Notes SAR SAR SAR SAR(Note 2.4-C)

Revenue C 511,092,829 - (7,782,011) 503,310,818Cost of revenue A, C (319,556,586) 1,716,028 39,066,398 (278,774,160)Gross profit 191,536,243 1,716,028 31,284,387 224,536,658

Selling and distribution expenses A, C (110,567,207) 1,039,870 148,672 (109,378,665)General and administrative expenses A, C (54,018,727) 393,918 3,434,605 (50,190,204)Research and development expenses A (6,530,662) 37,379 - (6,493,283)Income from operations 20,419,647 3,187,195 34,867,664 58,474,506Share in loss of associates and a joint venture - - (17,572,527) (17,572,527)Finance costs C (19,717,667) - 3,261,195 (16,456,472)Other (expenses) income C (8,717,812) - 7,460,201 (1,257,611)(Loss) / income before zakat and income tax expense (8,015,832) 3,187,195 28,016,533 23,187,896Zakat and income tax expense E - (8,131,248) - (8,131,248)(Loss) / income for the period (8,015,832) (4,944,053) 28,016,533 15,056,648

Attributable to:Equity holders of the parent 18,153,482 (5,357,010) - 12,796,472Non-controlling interests (26,169,314) 412,957 28,016,533 2,260,176

(8,015,832) (4,944,053) 28,016,533 15,056,648

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

32

2.4.4 Group reconciliation of total comprehensive income for the period ended 31 March 2016 (continued)

SOCPA GAAP31 March 2016 Re-measurement

Effect ofdeconsolidationof a subsidiary

IFRS as endorsedin KSA

31 March 2016Notes SAR SAR SAR SAR

(Note 2.4-C)Other comprehensive income

(Loss)/income for the period C - (12,959,885) 28,016,533 15,056,648Other comprehensive income to be reclassified to profit orloss in subsequent periods:Exchange differences on translation of foreign operations B - (11,277,878) - (11,277,878)

Re-measurement gains and (losses) on defined benefit plans A - (111,384) - (111,384)

Total comprehensive income for the period - (24,349,147) 28,016,533 3,667,386

Attributable to:Equity holders of the parent - 1,591,633 - 1,591,633Non-controlling interests - (25,940,780) 28,016,533 2,075,753

- (24,349,147) 28,016,533 3,667,386

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

33

2.4.5 Group reconciliation of total comprehensive income for the year ended 31 December 2016

SOCPA GAAP31 December 2016 Re-measurement

Effect ofdeconsolidation of a

subsidiaryIFRS as endorsed

in KSA31 December 2016

Notes SAR SAR SAR SAR(Note 2.4-C)

Revenue C 1,753,898,773 - (12,385,814) 1,741,512,959Cost of revenue A, C (1,092,018,101) 1,793,121 129,074,766 (961,150,214)Gross profit 661,880,672 1,793,121 116,688,952 780,362,745

Selling and distribution expenses A, C (409,332,403) 634,344 4,874,932 (403,823,127)General and administrative expenses A, C (220,197,771) 343,096 13,203,945 (206,650,730)Research and development expenses A (19,931,223) 15,720 - (19,915,503)Income from operations 12,419,275 2,786,281 134,767,829 149,973,385Share in loss of associates and a joint venture - (90,468,301) (90,468,301)Finance costs C (74,825,063) - 38,836,880 (35,988,183)Other income C 7,689,844 - 24,107,092 31,796,936(Loss) / income before zakat and income tax expense E (54,715,944) 2,786,281 107,243,500 55,313,837Zakat and income tax expense - (141,924,137) - (141,924,137)(Loss) / income for the period (54,715,944) (139,137,856) 107,243,500 (86,610,300)

Attributable to:Equity holders of the parent 45,210,990 (139,153,641) - (93,942,651)Non-controlling interests (99,926,934) 15,785 107,243,500 7,332,351

(54,715,944) (139,137,856) 107,243,500 (86,610,300)

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

34

2.4.5 Group reconciliation of total comprehensive income for the year ended 31 December 2016 (continued)

SOCPA GAAP31 December 2016 Re-measurement

Effect ofdeconsolidationof a subsidiary

IFRS as endorsedin KSA

31 December 2016Notes SAR SAR SAR SAR

(Note 2.4-C)

Other comprehensive income

(Loss)/income for the period C - (193,853,800) 107,243,500 (86,610,300)Other comprehensive income to be reclassified to profit orloss in subsequent periods:Exchange differences on translation of foreign operations B - (125,629,582) - (125,629,582)

Re-measurement gains and (losses) on defined benefit plans A - 138,752 - 138,752

Total comprehensive income for the period - (319,344,630) 107,243,500 (212,101,130)

Attributable to:Equity holders of the parent - (220,307,264) - (220,307,264)Non-controlling interests - (99,037,366) 107,243,500 8,206,134

- (319,344,630) 107,243,500 (212,101,130)

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

35

2.4 First time adoption of IFRS

EXPLANATION OF TRANSITION TO IFRS

A - Net employee defined benefit liabilitiesUnder SOCPA GAAP, the Group recognized costs related to post-employment benefits of employees as current valueof the vested benefits to which an employee is entitled. Under IFRS as endorsed in KSA, such liabilities are recognizedon actuarial basis under projected unit of credit method. As at 1 January, 2016, the difference between the provisionas per SOCPA GAAP and provision as per actuarial valuation is SAR 19 million (31 March 2016: SAR 16 million, 31December 2016: SAR 16 million) is recognized in retained earnings (refer to Note 11).

B – Foreign currency translationThe Group has opted for the exemption provided in IFRS 1” First-time Adoption of International FinancialReporting Standards” where:

a) the cumulative translation differences for all foreign operations are deemed to be zero at the dateof transition to IFRSs; and

b) the gain or loss on a subsequent disposal of any foreign operation shall exclude translationdifferences that arose before the date of transition to IFRSs and shall include later translationdifferences

The cumulative translation difference amounting to SAR 106 million as at 1 January 2016 were assumed zero byapplying the above exemption.

C – Deconsolidation of a subsidiaryAs part of the conversion process, the Group has reassessed the accounting of its subsidiaries, and as result,and based on new information that came to the attention of the management, it has concluded that theGroup did not exercise control over Al-Tanmiya Company for Steel Manufacturing (Al-Tanmiya).Accordingly, Al-Tanmiya was accounted for as a joint venture, given that the Group has a joint control overthis entity. After the application of the equity method at the date of transition, the Group has considered aloan to Al-Tanmiya of SAR 586 M, as part of the carrying value of its investment in this entity, and determinedthat it is necessary to recognize an impairment loss on this investment of SAR 245 M as part of openingretained earnings (refer to Note 4).

D – Effect of acquisition transaction with non-controlling interest without change in controlOn date of transition, the Group has reclassified effect of acquisition transaction with non-controllinginterest, which was shown as a separate item in equity, amounting to SAR 14 million to retained earnings.

E – Zakat and income tax expenseUnder the revised Zakat and tax standard under IFRS as endorsed in KSA, zakat and tax is considered as theGroup’s expense and accordingly comparative interim condensed statement of income is re-measuredresulting in zakat and income tax charge of SAR 141.9 million for the year 31 December 2016 (SAR 32 millionrelates to charge for the year and SAR 109 million relates to the assessment of the prior years) and SAR 8.1million in the period ended 31 March 2016.

Astra Industrial Group Company and Its Subsidiaries(A Saudi Joint Stock Company)Notes to the interim condensed consolidated financial statements (continued)31 March 2017

36

3 SIGNIFICANT ACCOUNTING ESTIMATES AND ASSUMPTIONS

The preparation of the Group’s interim condensed consolidated financial statements requires managementto make estimates and assumptions that affect the reported amounts of revenues, expenses, assets andliabilities, and the accompanying disclosures, and the disclosure of contingent liabilities. Uncertainty aboutthese assumptions and estimates could result in outcomes that require a material adjustment to the carryingamount of asset or liability affected in future periods. The Group based its assumptions and estimates onparameters available when the interim condensed consolidated financial statements were prepared.Existing circumstances and assumptions about future developments, however, may change due to marketchanges or circumstances arising beyond the control of the Group. Such changes are reflected in theassumptions when they occur. The estimates at 31 March 2017 are consistent with those made for the 1 January2016 and 31 March 2016 in accordance with SCOPA GAAP (after adjustments to reflect any differences in accountingpolicies) apart from the employee defined benefits. The estimates used by the Group to present these amounts inaccordance with IFRS as endorsed in KSA reflect conditions at 1 January 2016, the date of transition to IFRS asendorsed in KSA and as of 31 March 2017.

The key assumptions concerning the future and other key estimates made regarding uncertainty at thereporting date, and that have a significant risk of causing a material adjustment to the carrying amounts ofassets and liabilities within the next financial year, are described below.

3.1.1 Defined benefit planThe cost of defined benefit plan and the present value of the obligation are determined using actuarialvaluations. An actuarial valuation involves making various assumptions which may differ from actualdevelopments in the future. These include the determination of the discount rate, future salary increases,and mortality rates.

3.1.2 Going concernManagement has made an assessment of the Group’s ability to continue as a going concern and is satisfiedthat the Group has the resources to continue in business for the foreseeable future. Furthermore,management is not aware of any material uncertainties that may cast significant doubt upon the Group’sability to continue as going concern. Therefore, the financial statements continue to be prepared on thegoing concern basis.

3.1.3 Useful lives of property, plant and equipmentThe Group's management determines the estimated useful lives of its property, plant and equipment forcalculating depreciation. This estimate is determined after considering the expected usage of the asset orphysical wear and tear.

Management reviews the useful lives and residual value of the assets at least once per year and always atthe end of each financial year and future depreciation charge would be adjusted where the managementbelieves the useful lives differ from previous estimates.