assignment on old is gold by vijay sakya

DESCRIPTION

ÂTRANSCRIPT

Exam 2012 Fall Microeconomics

1

NEPAL COLLEGE OF INFORMATION TECHNOLOGY

ASSIGNMENT

(MICRO ECONOMICS)

SUBMITTED BY: SUBMITTED TO:

VIJAY SHAKYA TAK BADHADUR THAPA

DAYANIDHI TIMILSINA LECTURER, ECONOMICS

SURAJ DEO NCIT COLLEGE

Exam 2012 Fall Microeconomics

2

Assignment On

OLD IS GOLD EXAM 2012 FALL QUESTIONS

Submitted as per requirement of college assignment for BBA 2nd semester

Submitted By:

VIJAY SHAKYA

DAYANIDHI TIMILSINA

SURAJ DEO

Under Supervision Of

TAK BADHADUR THAPA

Date:

27 DEC 2015

Exam 2012 Fall Microeconomics

3

TABLE OF CONTENTS

SCARCITY “BEGINNING OF ECONOMIC ACTIVITIES”……….... 4

SOLVED EQUATION FOR ELASTICITY OF DEMAND………….... 4

SOLVED EQUATION FOR EQUILIBRIUM PRICE AND OUPUT... 6

DIFFERENCE BETWEEN TOTAL AND MARGINAL UTILITY…. 7

RELATIONSHIP OF TU AND MU WITH DIAGRAM…………….... 8

INCOME AND SUBSITUITION EFFECTS FOR A NORMAL

GOODS WHEN PRICE FALLS ……………………………………….. 9

SHORT RUN PRODUCTION FUNCTION WITH DIAGRAM

OF TP, AP AND MP…………………………………………………….. 10

PRODUCTION MAXIMIZATION……………………………………. 11

SOLVED EQUATION OF TOTAL COST FUNCTION…………….. 12

RELATIONSHIP OF AR AND MR IN PERFECTLY COMPETITIVE

AND MONOPOLY MARKET………………………………………… 14

PRICE AND OUTPUT DETERMINATION UNDER MONOPOLY.. 16

SHORT NOTES ON IC AND CROSS ELASTICITY OF DEMAND.. 17

REFERENCE………………………………………………………... 20

Exam 2012 Fall Microeconomics

4

1. a. Scarcity is not only problem but also the beginning of economic activities. Explain

The starting point of economic analysis is the existence of human wants. Human beings

have unlimited wants. That is to say that there is never such a time that a human being is

satisfied and not in need of anything. On the other hand, resources available in nature,

which should be used to meet those human wants, are limited. The available resources

can never be enough to satisfy all human needs. This phenomenon, where there are

unlimited human wants which are to be met by very limited resources, is essentially what

economists call scarcity. Scarcity is referred to as the fundamental economic problem,

and all economic activities revolve around trying to solve this problem.

Economics is basically born with scarcity of resources which leads to development of

other economic concepts, principles, theory and practice, since the scarcity makes the

people to act with rationality, scarcity (of resources) is a natural state that leads to explore

alternative.

Without Scarcity, the science of economic would not exit, economics is the study of

production, distribution and consumption of goods and services. If society did not have to

make choices about what to produce, distribute and consume, the study of those actions

would be relatively baring. Society would produced distribute and consume an infinite

amount of everything to satisfy the unlimited wants and needs of humans. Everyone

would get everything they wanted and it would all be free. But we all know that is not the

case. The decision and trade off society makes due to scarcity is what economics study.

b. Define the price elasticity of demand and measure it by are method when price changes

from Rs 20 to Rs 10 in the given example.

Price (Rs.) 20 10

Demand (units) 40 80

Other things being equal, price elasticity is the ratio of the percentage in the quantity

demanded with the percentage change in price. In other words, it is a measure of relative

change in the quantity demanded of goods in response to a relative change in the price.

Exam 2012 Fall Microeconomics

5

According to Ferguson, “price elasticity is the proportionate change in quantity

demanded divided by the proportionate change in price.”

Thus,

% change in quantity demanded

ep =

% change in price

In symbolic term,

Q p1

ep = - *

p q1

where Q= Q2– Q1, Q1= initial quantity demanded, Q2= new quantity demanded

P= P2 – P1, P1= initial price, P2= new price.

Here,

P1= 20, P2 = 10, Q1= 40, Q2=8

Q= Q2– Q1= 80- 40 = 40

P= P2– P1 = 10 – 20 = -10

We know that,

q p1

ep = - *

p q1

40 20

ep = - *

-10 40

= 2 > 1

Exam 2012 Fall Microeconomics

6

2. A market consists of three consumers, A, B, and C, whose individual demand equations

are as follows:

QdA = 30 – 1.00P, QdB = 22.5 – 0.75P, QdC= 37.5 – 1.25P, and the industry supply equation

is given by Qs = 40 + 3.5P

a. Find out the market demand function and derive the market demand curve.

b. Determine the equilibrium price and quality mathematically.

c. Determine the amount that will be purchased by each individual.

Market demand function = QdA +QdB+ QdC

= 30 – 1.00P + 22.5 – 0.75P + 37.5 – 1.25P

= 90 – 3P

Market demand schedule

Market demand curve

y

25

20

15

10

5 D

O 15 30 45 60 75 x

Quantity demanded

Price ( rs) Market demand( 90 – 3P)

5 75

10 60

15 45

20 30

25 15

P

rice

Exam 2012 Fall Microeconomics

7

b.

For market equilibrium price,

Qd = Qs

Or, 90 – 3P = 40 + 3.5P

Or, 50 = 6.5P

Or, P= 7.7

When p= 7.7 Qs = 40 + 3.5*7.7= 66.95 and Qd= 90 – 3*7.7 = 66.95

So, equilibrium price = Rs 7.7 and equilibrium quantity = 7.7

c.

when p = 7.7

QdA = 30 – 1.00* 7.7 = 22.3

QdB = 22.5 – 0.75*7.7= 16.725

QdC= 37.5 – 1.25* 7.7= 27.875

3. a. Distinguish between total utility and marginal utility. Show the relationship between

total utility and marginal utility.

Difference between total utility and marginal utility

TOTAL UTILITY MARGINAL UTILITY

1. It refers to the total satisfaction derived by the

consumer from the consumption of a given

quantity of goods.

1. It is defined as the addition made to the total

utility by consuming one more unit of a

commodity.

2. It is the aggregate of marginal utilities 2. It is the ratio of change in the total utility with

the change in the total consummation of units of

a commodity

3. Mathematically,

TU = MU1 + MU2 + …………. + MUN

3. Mathematically

TU

MU=

Q

Exam 2012 Fall Microeconomics

8

4. It has no types. 4. It has got 3 types.

i). Positive Utility

ii). Zero Utility

iii). Negative Utility

5.For example, a person consumes eggs and

gains 50 utils of total utility. This total utility is

the sum of utilities from the successive units (30

utils from the first egg, 15 utils from the second

and 5 utils from the third egg)

5, For example, when a person increases the

consumption of eggs from one egg to two eggs,

the total utility increases from 30 utils to 45 utils.

The marginal utility here would be the15 utils of

the 2nd egg consumed.

Relationship between total utility and marginal utility in diagram

Exam 2012 Fall Microeconomics

9

1. In figure (2), MU curve moves downward having negative slope while in figure (1) TC

curve, having negative positive slope moves upward but tendency to move is towards x-

axis, which shows decreasing rate.

2. A point F´ in figure (2) MU curve cuts the s-axis at the 6th unit and TU curve has its

maximum point F which is saturation point.

3. At 7th unit MU curve is below x-axis as in figure (2) and TU curve declines from point

'F' to 'G' as in figure (1).

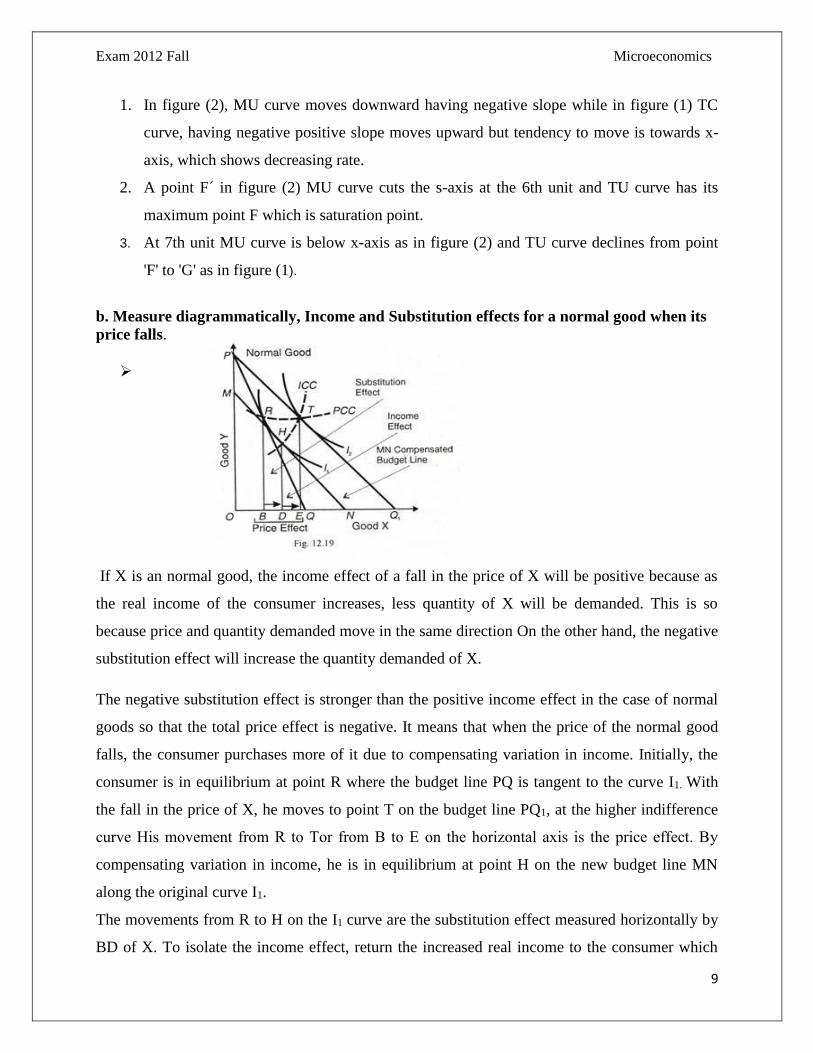

b. Measure diagrammatically, Income and Substitution effects for a normal good when its

price falls.

If X is an normal good, the income effect of a fall in the price of X will be positive because as

the real income of the consumer increases, less quantity of X will be demanded. This is so

because price and quantity demanded move in the same direction On the other hand, the negative

substitution effect will increase the quantity demanded of X.

The negative substitution effect is stronger than the positive income effect in the case of normal

goods so that the total price effect is negative. It means that when the price of the normal good

falls, the consumer purchases more of it due to compensating variation in income. Initially, the

consumer is in equilibrium at point R where the budget line PQ is tangent to the curve I1. With

the fall in the price of X, he moves to point T on the budget line PQ1, at the higher indifference

curve His movement from R to Tor from В to E on the horizontal axis is the price effect. By

compensating variation in income, he is in equilibrium at point H on the new budget line MN

along the original curve I1.

The movements from R to H on the I1 curve are the substitution effect measured horizontally by

BD of X. To isolate the income effect, return the increased real income to the consumer which

Exam 2012 Fall Microeconomics

10

was taken from him so that he is again at point T of the tangency of PQ; line and the curve l2.

The movement from H to T is the income effect of the fall in the price of X and is measured by

DE.

This income effect is positive because the fall in the price of the normal good X leads, via

compensating variation in income, to the decrease in its quantity demanded by DE. When the

relation between price and quantity demanded is direct via compensating variation in income, the

income effect is always positive.

In the case of an normal good, the negative substitution effect is greater than the positive

income effect so that the total price effect is negative. Thus the price effect (-) BE = (-) BD

(substitution effect) + DE (income effect). In other words, the overall price move from R to T

which comprises both the income and substitution effects has led to the increase in the quantity

demanded by BE after the fall in the price of X. This establishes the downward sloping demand

curve even in the case of an normal good.

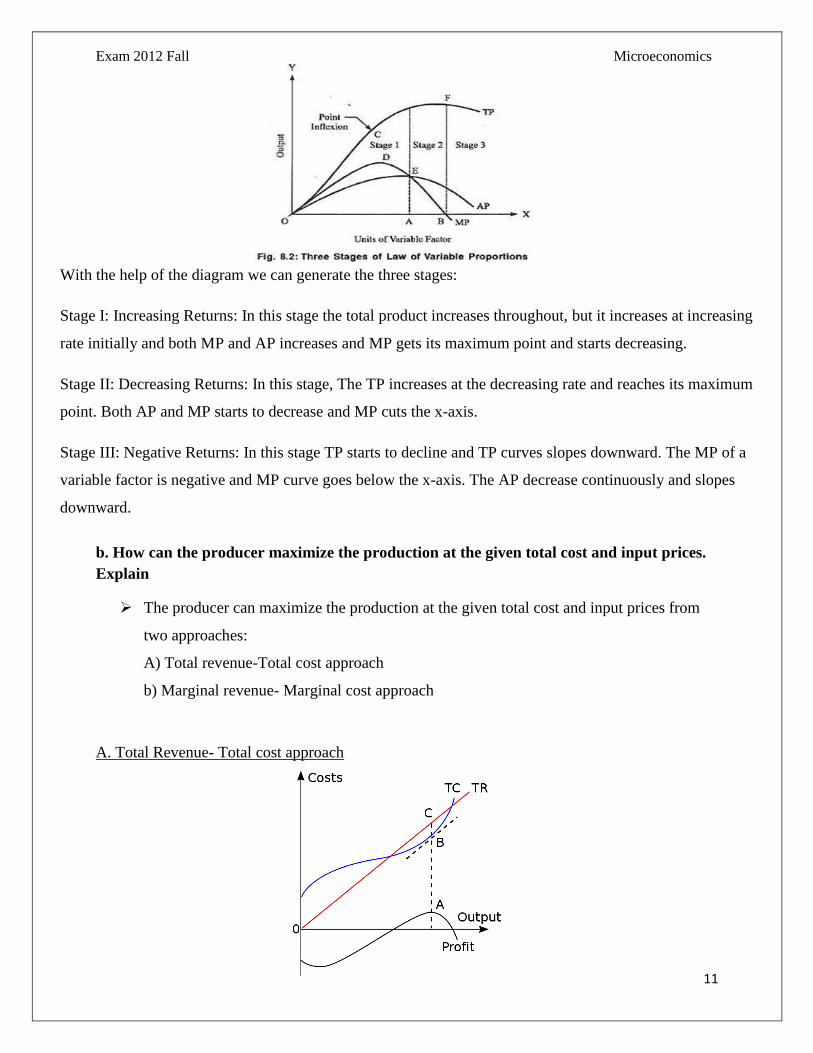

4.a What is the short run production function? Explain this with the help of a total product

curve, AP and MP curves.

Short run production function refers to the functional relationship between the units of

variable factors and the output. In short run production function, we study the effect of

change in the quantity of one variable input on the output, by keeping all other inputs

constant. It is also called single variable production function or production function with

one variable input.

Algebraically, it is written as:

Q=f (Nvf) K

Where Q= output, f= Function ,Nvf = Quantity of variable factors, K= constant units of

fixed inputs.

Exam 2012 Fall Microeconomics

11

b. How can the producer maximize the production at the given total cost and input prices.

Explain

The producer can maximize the production at the given total cost and input prices from

two approaches:

A) Total revenue-Total cost approach

b) Marginal revenue- Marginal cost approach

A. Total Revenue- Total cost approach

With the help of the diagram we can generate the three stages:

Stage I: Increasing Returns: In this stage the total product increases throughout, but it increases at increasing

rate initially and both MP and AP increases and MP gets its maximum point and starts decreasing.

Stage II: Decreasing Returns: In this stage, The TP increases at the decreasing rate and reaches its maximum

point. Both AP and MP starts to decrease and MP cuts the x-axis.

Stage III: Negative Returns: In this stage TP starts to decline and TP curves slopes downward. The MP of a

variable factor is negative and MP curve goes below the x-axis. The AP decrease continuously and slopes

downward.

Exam 2012 Fall Microeconomics

12

To obtain the profit maximizing output quantity, we start by recognizing that profit is equal to

total revenue (TR) minus total cost (TC). Given a table of costs and revenues at each quantity,

we can either compute equations or plot the data directly on a graph. The profit-maximizing

output is the one at which this difference reaches its maximum.

In the accompanying diagram, the linear total revenue curve represents the case in which the firm

is a perfect competitor in the goods market, and thus cannot set its own selling price. The profit-

maximizing output level is represented as the one at which total revenue is the height of C and

total cost is the height of B; the maximal profit is measured as CB. This output level is also the

one at which the total profit curve is at its maximum.

If, contrary to what is assumed in the graph, the firm is not a perfect competitor in the output

market, the price to sell the product at can be read off the demand curve at the firm's optimal

quantity of output.

B. Marginal Revenue-Marginal Cost Approach

An equivalent perspective relies on the relationship that, for each unit sold, marginal profit (Mπ)

equals marginal revenue (MR) minus marginal cost (MC). Then, if marginal revenue is greater

than marginal cost at some level of output, marginal profit is positive and thus a greater quantity

should be produced, and if marginal revenue is less than marginal cost, marginal profit is

negative and a lesser quantity should be produced. At the output level at which marginal revenue

equals marginal cost, marginal profit is zero and this quantity is the one that maximizes

profit.[2] Since total profit increases when marginal profit is positive and total profit decreases

when marginal profit is negative, it must reach a maximum where marginal profit is zero - or

Exam 2012 Fall Microeconomics

13

where marginal cost equals marginal revenue - and where lower or higher output levels give

lower profit levels.[2] In calculus terms, the correct intersection of MC and MR will occur

when:[2]

The intersection of MR and MC is shown in the next diagram as point A. If the industry is

perfectly competitive (as is assumed in the diagram), the firm faces a demand curve (D) that is

identical to its marginal revenue curve (MR), and this is a horizontal line at a price determined

by industry supply and demand. Average total costs are represented by curve ATC.

Total economic profit is represented by the area of the rectangle PABC. The optimum quantity

(Q) is the same as the optimum quantity in the first diagram.

5.a. Total cost function of a producer is given by TC= 1000 + 10Q – 0.9Q + 0.004Q3. Find

TFC, TVC, TC, AFC, and MC to produce 5 units.

Here,

TFC = 1000

TVC =10Q+ 0.004Q3- 0.9Q when q=5 TVC=10*5+ 0.004*(5)3-0.9*5 = 46

TC= TFC + TVC = 1000+46 = 1046

AFC= TFC/Q = 1000/5 = 200

AVC = TVC/Q = 46/5 = 9.2

MC = derivative of TC

= 10 – 0.9Q + 0.012Q2

When q=5

= 10 – 0.9*5 + 0.012 * 52

= 5.8

Exam 2012 Fall Microeconomics

14

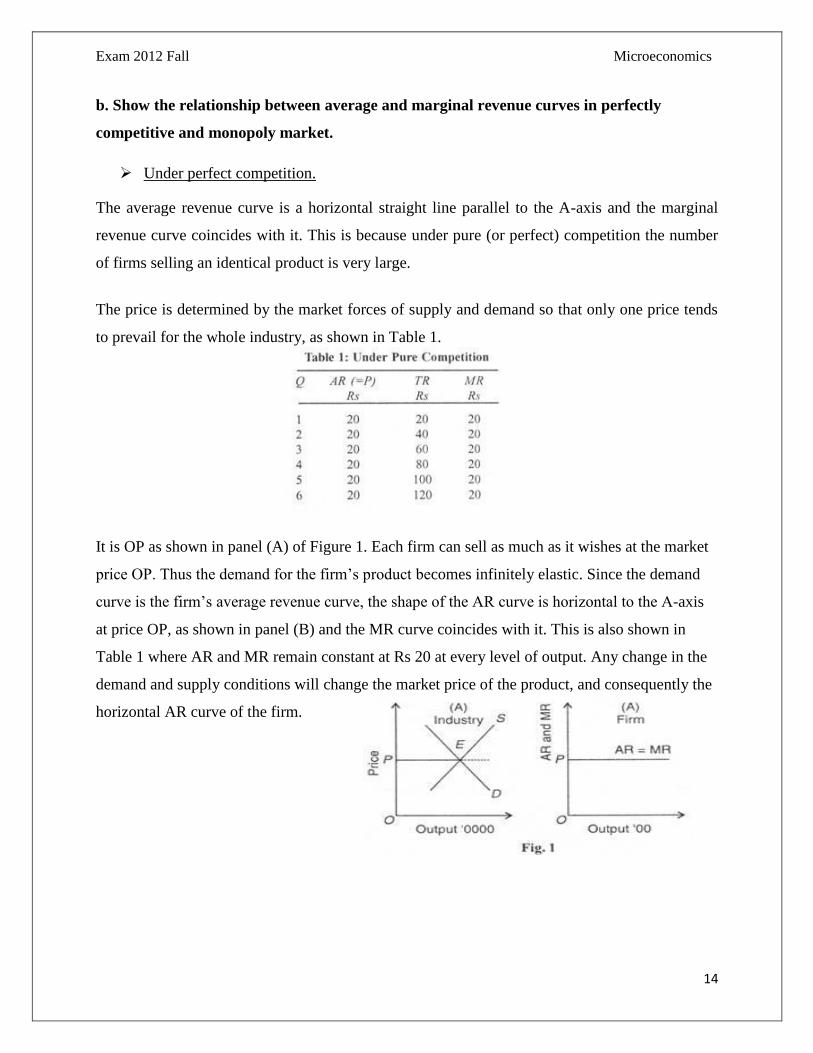

b. Show the relationship between average and marginal revenue curves in perfectly

competitive and monopoly market.

Under perfect competition.

The average revenue curve is a horizontal straight line parallel to the A-axis and the marginal

revenue curve coincides with it. This is because under pure (or perfect) competition the number

of firms selling an identical product is very large.

The price is determined by the market forces of supply and demand so that only one price tends

to prevail for the whole industry, as shown in Table 1.

It is OP as shown in panel (A) of Figure 1. Each firm can sell as much as it wishes at the market

price OP. Thus the demand for the firm’s product becomes infinitely elastic. Since the demand

curve is the firm’s average revenue curve, the shape of the AR curve is horizontal to the А-axis

at price OP, as shown in panel (B) and the MR curve coincides with it. This is also shown in

Table 1 where AR and MR remain constant at Rs 20 at every level of output. Any change in the

demand and supply conditions will change the market price of the product, and consequently the

horizontal AR curve of the firm.

Exam 2012 Fall Microeconomics

15

Under Monopoly

The average revenue curve is the downward sloping industry demand curve and its correspond-

ing marginal revenue curve lies below it. The relation between the average revenue and the

marginal revenue under monopoly can be understood with the help of Table 2. The marginal

revenue is lower than the average revenue.

Given the demand for his product, the monopolist can increase his sales by lowering the price,

the marginal revenue also falls but the rate of fall in marginal revenue is greater than that in

average revenue. In Table 2, AR falls by Rs. 2 at a time whereas MR falls by Rs. 4. This is

shown in Figure 2, in which the MR curve is below the AR curve and lies half way on the

perpendicular drawn from AR to the T-axis. This relation will always exist between straight line

downward sloping AR and MR curves.

In order to prove it, draw perpendiculars CA and CM to the У-axis and X-axis respectively from

point С on the AR curve. CA cuts MR at В and CM at D. We have to prove that AB = BC. In

Figure 2, the rectangle ACMO is the TR of OM output at CM price and the area. PDMO also

represents total revenue in terms of aggregate marginal revenue ( MR) at OM output.

Exam 2012 Fall Microeconomics

16

6.a Define Monopoly. How price and output is determined in the short run of the firm

under monopoly?

Monopoly is said to exist when one firm is the sole producer or seller of a product which

has no close substitutes. The following three condition are necessary to exist monopoly:

i. There is a single producer or seller of a product.

ii. There are no close substitutes for the product.

iii. Strong barriers to the entry of new firms in the industry exist.

Price and Output determination Under Monopoly

MC

AC

AR AR

MR MR MR

X

In Monopoly, Price is determined by the firm itself by the help of AR because AR is equals to

price and output is determined by firm when MC is equal to MR. In the above figure, there is a

firm which has got 3 situation:

i) Abnormal Profit (AR>AC)

ii) Normal Profit (AR=AC)

iii) Loss (AR<AC)

Y YY

MC F MC

E AC AC

P F H

G H

E

O OUTPUT OUTPUT

Fig (i) Fig (ii) Fig (iii)

P

O Y

G

P

E

O OUT PUT X

PR

ICE

PR

ICE

PR

ICE

Exam 2012 Fall Microeconomics

17

i) Abnormal Profit

Abnormal profit is that condition where AR is greater than AC which we can see in Fig i. In fig I

PFGH is the super normal profit where AR is greater than AC.

ii) Normal Profil

Normal profit is that stage where AR is equal to AC which we can see in fig ii. Though AC=AR

we say it normal profit because AC includes both AFC and AVC. In fig ii the point E is normal

Profit.

iii) Loss

Loss is that condition where AC is greater than AR. In the fig iii GFPH is the loss where AC is

greater than AR

7. Write short notes on any two:

a. Properties of indifference curve

i) IC convex to the origin

Indifference curves is usually convex to the origin. In other words, the indifference curve is

relatively flatter in its right-hand portion and relatively steeper in its left-hand portion.

Due to diminishing MRS, IC is always convex to the origin as

we can see in the figure.

Exam 2012 Fall Microeconomics

18

ii) Higher Indifference curve yields Higher level of satisfaction than lower

It is because that the higher IC3 contains more units of both goods

or more units of at least one good than IC2 and so on. So IC3 has

more level of satisfaction than the IC2 .

iii) IC do not intersect each other

If two indifference curves intersect each other, it would imply that an indifference curve

indicates two different levels of satisfaction or that two different combinations – one being larger

than the other yield same level of satisfaction.

iv) Indifference Curve always slopes downward to right

This property follows the assumptions of non-satiety, i.e. the consumer prefers more goods to

less of it. The negative slope of an indifference curve shows that the two goods are substitutes for

one another. This must be so if the level of satisfaction is to remain the same on an indifference

curve.

v) Indifference Curve never touches x-axis

If IC touches the x-axis then we can’t take x good i.e x good will be 0 which is against our

assumption. So, IC never touches x axis.

b. Cross elasticity of demand

Cross elasticity of demand (XED) measures the percentage change in quantity demand for a

good after the change in price of another.

XED = % change in Q.D. good A

% change in P good B

Exam 2012 Fall Microeconomics

19

Cross elasticity of demand for Coffee / Tea

For example: if there is an increase in the price of tea by 10%. and Q.D of coffee increases by

2%, then XED = +0.2

Substitute goods

For goods which are substitutes, we expect to see a positive cross elasticity of demand. If the

price of Asda bread increases, people will buy more of an alternative, such as Mother’s Pride

bread.

Weak substitutes like tea and coffee will have a low cross elasticity of demand

Alternative brands of chocolate, e.g. Dairy Milk vsWispa are quite similar, so will have a higher

cross elasticity of demand.

Complements goods

These are goods which are used together, therefore the cross elasticity of demand is negative. If

the price of one goes up, you will buy less of both goods.

For example, if the price of DVD players goes down, you will buy more DVD players and also

there will be a increase in demand for DVD disks.

If the price of Samsung mobile phones goes down, we will also buy more Samsung related

phone apps.

Using knowledge of cross elasticity of demand

When setting prices firms will have to look at what alternatives the consumer has, if there are no

close substitutes they will be able to increase the price. For this reason firms spend a lot of

money on advertising to differentiate their products and reduce cross elasticity of demand.

A firm may offer a loss leader to attract complementary sales. For example, a firm may offer a

printer, at a low price, because it knows this will lead to increased sales for the highly profitable

ink cartridges.

Exam 2012 Fall Microeconomics

20

REFERENCE

Managerial economics, dr. h.l ahuja

Micro economics, gyan ratna adhikari

www.wikipedia.com

www.2knomics.com