assets, growth and development strategies

TRANSCRIPT

assets, growth and development strategies

Ebbie Haan, managing director, Sasol Petroleum International

leveraging first mover advantage

2

Forward-looking statements: Sasol may, in this document, make certain statements that are not historical facts and

relate to analyses and other information which are based on forecasts of future results and estimates of amounts

not yet determinable. These statements may also relate to our future prospects, developments and business

strategies. Examples of such forward-looking statements include, but are not limited to, statements regarding

exchange rate fluctuations, volume growth, increases in market share, total shareholder return and cost reductions.

Words such as “believe”, “anticipate”, “expect”, “intend”, “seek”, “will”, “plan”, “could”, “may”, “endeavour” and

“project” and similar expressions are intended to identify such forward-looking statements, but are not the exclusive

means of identifying such statements. By their very nature, forward-looking statements involve inherent risks and

uncertainties, both general and specific, and there are risks that the predictions, forecasts, projections and other

forward-looking statements will not be achieved. If one or more of these risks materialise, or should underlying

assumptions prove incorrect, our actual results may differ materially from those anticipated. You should understand

that a number of important factors could cause actual results to differ materially from the plans, objectives,

expectations, estimates and intentions expressed in such forward-looking statements. These factors are discussed

more fully in our most recent annual report under the Securities Exchange Act of 1934 on Form 20-F filed on 09

October 2013 and in other filings with the United States Securities and Exchange Commission. The list of factors

discussed therein is not exhaustive; when relying on forward-looking statements to make investment decisions, you

should carefully consider both these factors and other uncertainties and events. Forward-looking statements apply

only as of the date on which they are made, and we do not undertake any obligation to update or revise any of

them, whether as a result of new information, future events or otherwise.

forward-looking statements

3

leveraging our first mover advantage

Mozambique resource potential presents new opportunities and challenges

Mozambique prioritising in-country monetisation

Could Qatar’s growth trend be mirrored in Mozambique?

Sasol: acting as a catalyst for development in Mozambique

Sasol is well positioned to leverage its first mover advantage

Conclusion

4

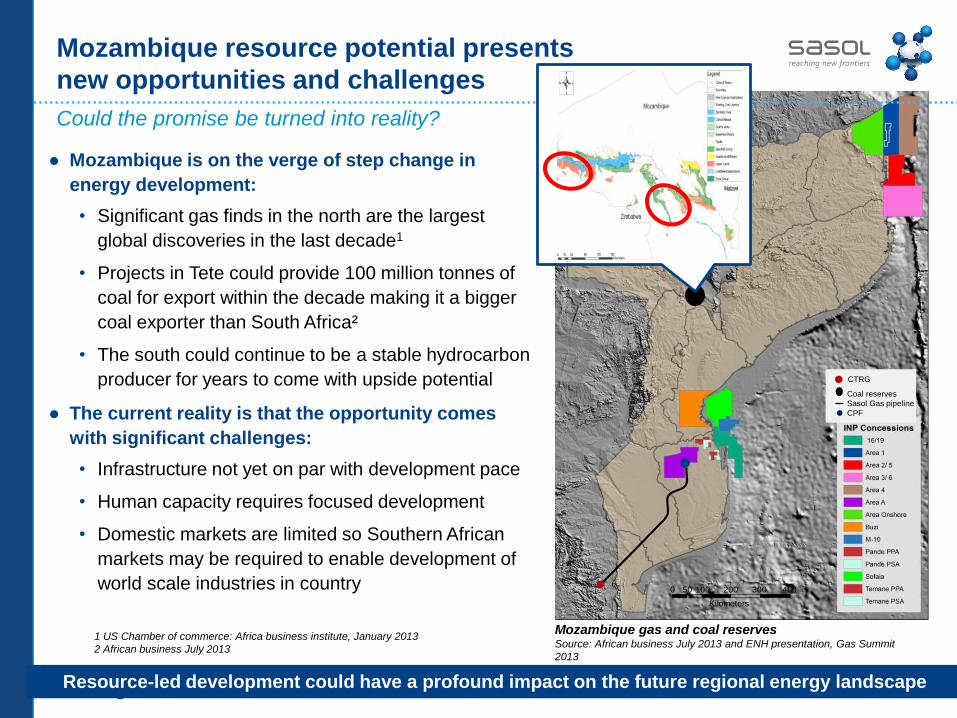

● Mozambique is on the verge of step change in

energy development:

• Significant gas finds in the north are the largest

global discoveries in the last decade1

• Projects in Tete could provide 100 million tonnes of

coal for export within the decade making it a bigger

coal exporter than South Africa²

• The south could continue to be a stable hydrocarbon

producer for years to come with upside potential

● The current reality is that the opportunity comes

with significant challenges:

• Infrastructure not yet on par with development pace

• Human capacity requires focused development

• Domestic markets are limited so Southern African

markets may be required to enable development of

world scale industries in country

Resource-led development could have a profound impact on the future regional energy landscape

Mozambique resource potential presents

new opportunities and challenges

Could the promise be turned into reality?

1 US Chamber of commerce: Africa business institute, January 2013

2 African business July 2013

Mozambique gas and coal reservesSource: African business July 2013 and ENH presentation, Gas Summit

2013

0 50 100 200

Kilometers

300 400

Coal reserves

Sasol Gas pipeline

CPF

CTRG

5

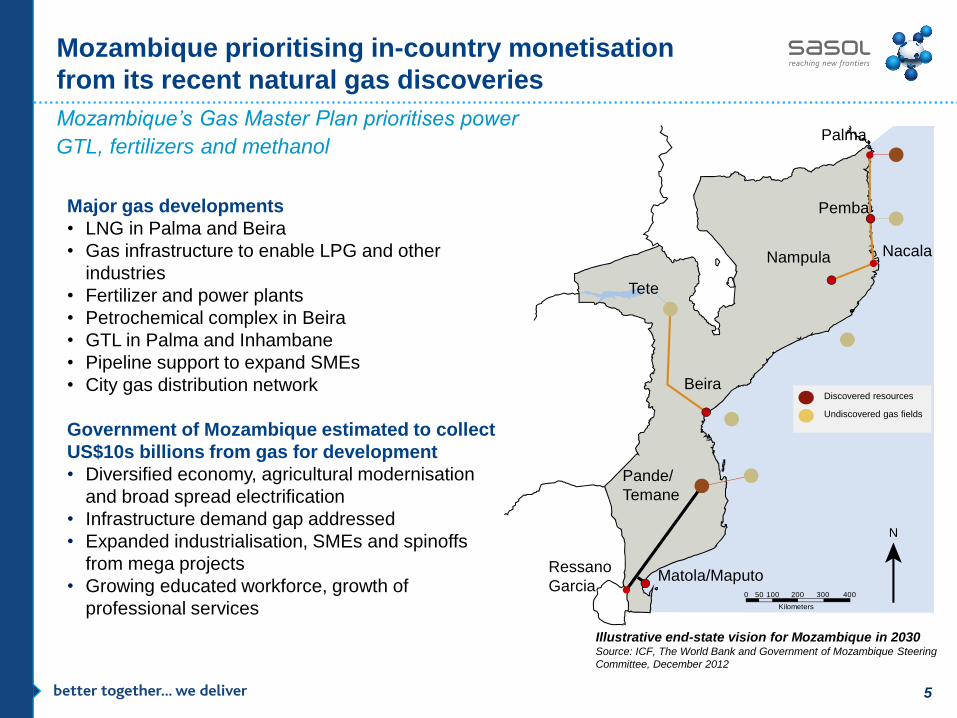

Mozambique’s Gas Master Plan prioritises power

GTL, fertilizers and methanol

Mozambique prioritising in-country monetisation

from its recent natural gas discoveries

Major gas developments

• LNG in Palma and Beira

• Gas infrastructure to enable LPG and other

industries

• Fertilizer and power plants

• Petrochemical complex in Beira

• GTL in Palma and Inhambane

• Pipeline support to expand SMEs

• City gas distribution network

Government of Mozambique estimated to collect

US$10s billions from gas for development

• Diversified economy, agricultural modernisation

and broad spread electrification

• Infrastructure demand gap addressed

• Expanded industrialisation, SMEs and spinoffs

from mega projects

• Growing educated workforce, growth of

professional services0 50 100 200

Kilometers

300 400

N

Palma

Pemba

NacalaNampula

Tete

Beira

Pande/

Temane

Matola/MaputoRessano

Garcia

Discovered resources

Undiscovered gas fields

Illustrative end-state vision for Mozambique in 2030 Source: ICF, The World Bank and Government of Mozambique Steering

Committee, December 2012

6

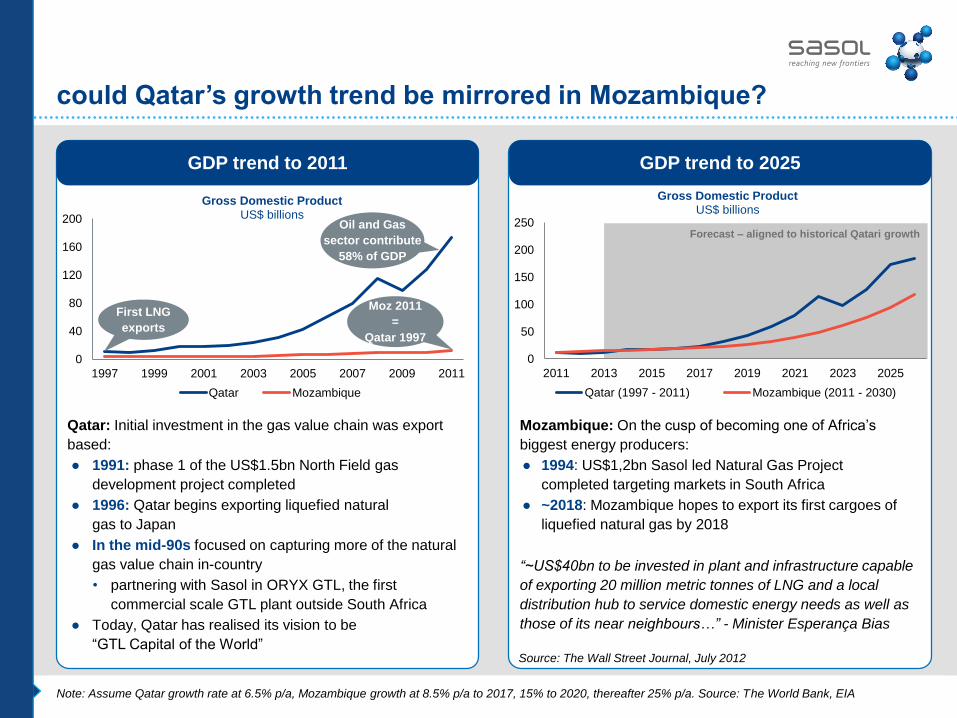

could Qatar’s growth trend be mirrored in Mozambique?

GDP trend to 2025 GDP trend to 2011

Qatar: Initial investment in the gas value chain was export

based:

● 1991: phase 1 of the US$1.5bn North Field gas

development project completed

● 1996: Qatar begins exporting liquefied natural

gas to Japan

● In the mid-90s focused on capturing more of the natural

gas value chain in-country

• partnering with Sasol in ORYX GTL, the first

commercial scale GTL plant outside South Africa

● Today, Qatar has realised its vision to be

“GTL Capital of the World”

Mozambique: On the cusp of becoming one of Africa’s

biggest energy producers:

● 1994: US$1,2bn Sasol led Natural Gas Project

completed targeting markets in South Africa

● ~2018: Mozambique hopes to export its first cargoes of

liquefied natural gas by 2018

“~US$40bn to be invested in plant and infrastructure capable

of exporting 20 million metric tonnes of LNG and a local

distribution hub to service domestic energy needs as well as

those of its near neighbours…” - Minister Esperança Bias

Source: The Wall Street Journal, July 2012

Note: Assume Qatar growth rate at 6.5% p/a, Mozambique growth at 8.5% p/a to 2017, 15% to 2020, thereafter 25% p/a. Source: The World Bank, EIA

Forecast – aligned to historical Qatari growth

0

50

100

150

200

250

2011 2013 2015 2017 2019 2021 2023 2025

Gross Domestic Product US$ billions

Qatar (1997 - 2011) Mozambique (2011 - 2030)

0

40

80

120

160

200

1997 1999 2001 2003 2005 2007 2009 2011

Gross Domestic Product US$ billions

Qatar Mozambique

First LNG

exports

Oil and Gas

sector contribute

58% of GDP

Moz 2011

=

Qatar 1997

7

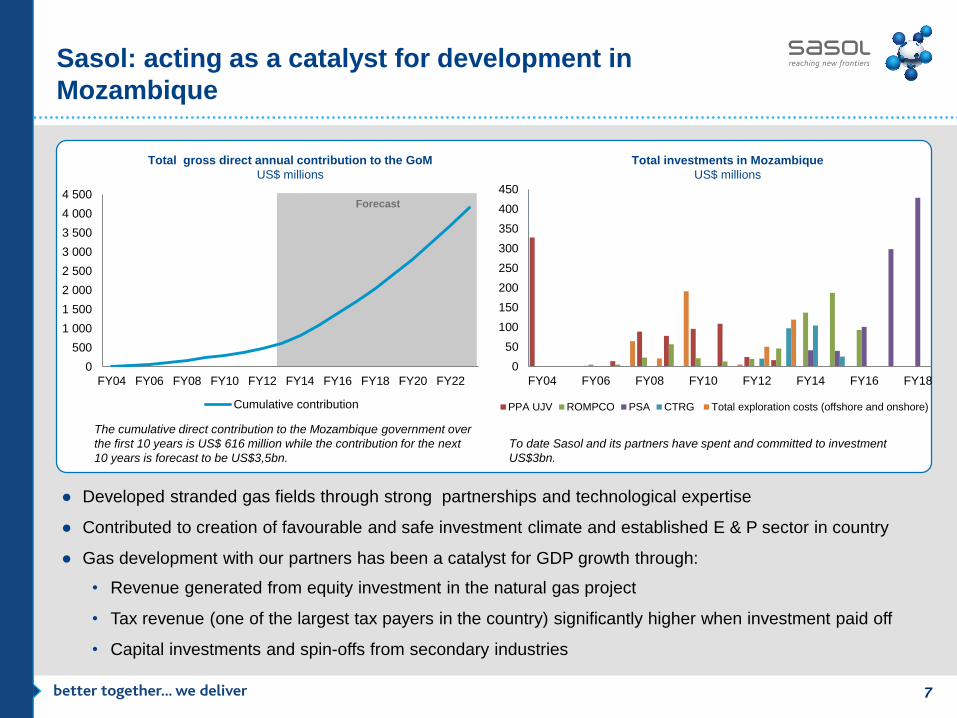

● Developed stranded gas fields through strong partnerships and technological expertise

● Contributed to creation of favourable and safe investment climate and established E & P sector in country

● Gas development with our partners has been a catalyst for GDP growth through:

• Revenue generated from equity investment in the natural gas project

• Tax revenue (one of the largest tax payers in the country) significantly higher when investment paid off

• Capital investments and spin-offs from secondary industries

Sasol: acting as a catalyst for development in

Mozambique

To date Sasol and its partners have spent and committed to investment

US$3bn.

Total investments in Mozambique

US$ millions

0

50

100

150

200

250

300

350

400

450

FY04 FY06 FY08 FY10 FY12 FY14 FY16 FY18

PPA UJV ROMPCO PSA CTRG Total exploration costs (offshore and onshore)

Forecast

The cumulative direct contribution to the Mozambique government over

the first 10 years is US$ 616 million while the contribution for the next

10 years is forecast to be US$3,5bn.

Total gross direct annual contribution to the GoM

US$ millions

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

FY04 FY06 FY08 FY10 FY12 FY14 FY16 FY18 FY20 FY22

Cumulative contribution

8

Our unique combination of capabilities enabled by effective partnerships demonstrates our

ability to unlock significant benefit for all stakeholders

Sasol is well positioned to leverage its first mover

advantage in Mozambique’s hydrocarbon space

● Gas

● Condensate

● Oil

Operations

A decade of sustained gas

production – access to proven

gas and oil resources

● Natural gas Central Processing Facility in Temane

● Cross country, cross border pipeline

● Building gas to power plant

Infrastructure

We have competence in

building, managing and

maintaining pipelines

● Base load – RSA

● Partnering in developing

domestic markets

Markets and technology

We have proven monetisation

technologies and established

markets in the region

The foundation of Sasol’s competitive advantage in the region

Strategic and sustainable

partnerships

Capacity building

and skills development

Extensive

market presence

9

building on our strategic partnerships

leveraging our first mover advantage

● Natural gas Central Processing Facility in Temane

● Cross country, cross border pipeline

● Building gas to power plant

Infrastructure

We have competence in

building, managing and

maintaining pipelines

● Base load – RSA

● Partnering in developing

domestic markets

Markets and technology

We have proven monetisation

technologies and established

markets in the region

● Gas

● Condensate

● Oil

Operations

A decade of sustained gas

production – access to proven

gas and oil resources

The foundation of Sasol’s competitive advantage in the region

Strategic and sustainable

partnerships

Capacity building

and skills development

Extensive market

presence

10

● Partners in the central processing facility (CPF): Sasol 70% (Operator), CMH 25%, IFC 5%

● Equity in pipeline company (ROMPCO): Sasol Gas 50% (Operator), CMG (25%), iGAS (25%)

● CTRG – joint venture for power generation at Ressano Garcia: EDM, Sasol New Energy

● ENH – natural gas reticulation project agreement signed

● PESS is a joint venture between Sasol and Petromoc

• PeSS supplies liquid fuel and lubricant products to the mining, road haulage, construction

and agricultural segments throughout Mozambique

• Currently PESS sells approximately 80 million litres of petroleum product annually

leveraging our first mover advantage

building on our strategic partnerships: the platform upon which

we have grown our presence in Mozambique

11

● Gas

● Condensate

● Oil

Operations

A decade of sustained gas

production – access to proven

gas and oil resources

● Base load – RSA

● Partnering in developing

domestic markets

Markets and technology

We have proven monetisation

technologies and established

markets in the region

The foundation of Sasol’s competitive advantage in the region

Strategic and sustainable

partnerships

Extensive regional

market presence

● Natural gas Central Processing Facility in Temane

● Cross country, cross border pipeline

● Building gas to power plant

Infrastructure

We have competence in

building, managing and

maintaining pipelines

Capacity building

and skills development

In partnership with Government of Mozambique, we are contributing to

building a talent pipeline to resource the oil and gas industry.

leveraging our first mover advantage

12

driving the development of expertise and skills

In partnership with Government of Mozambique, we are contributing

to building a talent pipeline to resource the oil and gas industry. Over

the next five years we forecast spend of over US$12.4 million for:

● Bursary programme, in partnership with MIREM, aimed at

developing 30 students per annum, to study in the areas of

geology, petroleum, drilling and reservoir engineering;

• Designed to ensure industry knowledge and develop

life skills to prepare the bursars for life beyond university

● Sasol’s learnership programme is fast tracking the

development of sought after artisans, in the fields of electrical,

instrumentation, mechanical fitting and production;

• Programme started in 2011, the first learners completed their

training and will be appointed as artisans at the CPF in 2014

● Leveraging Sasol’s university collaboration approach to build the

necessary value adding capabilities within Mozambican

universities

Vania Martinho, 18, Nampula Province, Mozambique.

studying Petroleum Engineering in South Africa

13

Sasol is playing a key role in the development of a domestic

gas market and enabling energy security

leveraging our first mover advantage

● Gas

● Condensate

● Oil

Operations

A decade of sustained gas

production – access to proven

gas and oil resources

● Natural gas Central Processing Facility in Temane

● Cross country, cross border pipeline

● Building gas to power plant

Infrastructure

We have competence in

building, managing and

maintaining pipelines

The foundation of Sasol’s competitive advantage in the region

Strategic and sustainable

partnerships

Capacity building

and skills development

Markets and technology

We have proven monetisation

technologies and established

markets in the region

Extensive

market presence

● Base load – RSA

● Partnering in developing

domestic markets

14

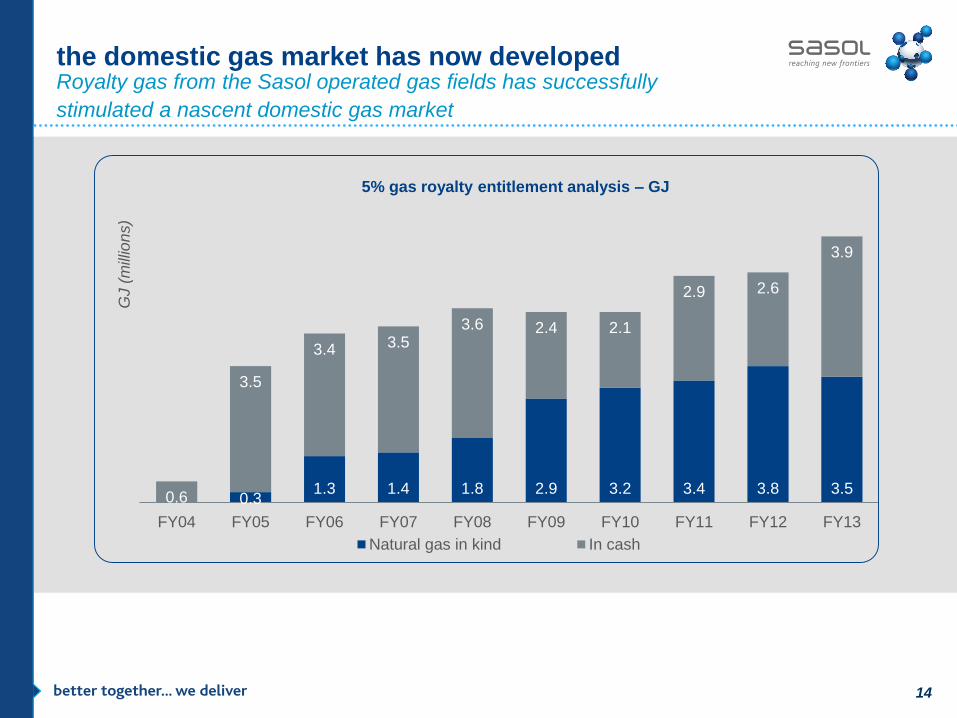

Royalty gas from the Sasol operated gas fields has successfully

stimulated a nascent domestic gas market

the domestic gas market has now developed

0.31.3 1.4 1.8 2.9 3.2 3.4 3.8 3.5

0.6

3.5

3.4 3.53.6 2.4 2.1

2.9 2.6

3.9

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

GJ (

mill

ion

s)

5% gas royalty entitlement analysis – GJ

Natural gas in kind In cash

15

leveraging our first mover advantage

Sasol is playing a key role in developing a

domestic gas market and enabling energy

security

Assisting in driving the domestic energy industry

geared to service the region as a whole:

● 25 MGJ/a of the CPF’s expanded capacity sold

to industries in Mozambique for power

generation

● ENH has contracted to purchase 6 MGJ/a for

gas reticulation in the Maputo area

● The US$246m, 140 MW-capacity gas engine

project – due to be operational first half of

2014 calendar year

● This partnership between Sasol New Energy

and EDM will be the first long-term large-

scale gas to power plant

Gas to power plant,

Ressano Garcia

Gas reticulation in

Inhambane Province

16

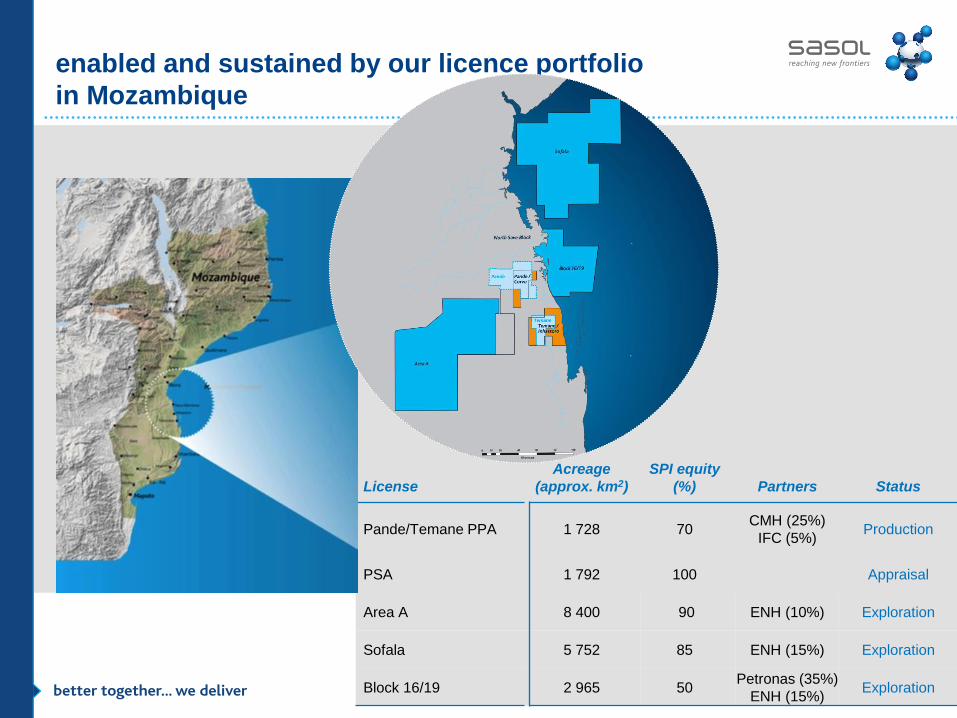

enabled and sustained by our licence portfolio

in Mozambique

License

Acreage

(approx. km2)

SPI equity

(%) Partners Status

Pande/Temane PPA 1 728 70CMH (25%)

IFC (5%)Production

PSA 1 792 100 Appraisal

Area A 8 400 90 ENH (10%) Exploration

Sofala 5 752 85 ENH (15%) Exploration

Block 16/19 2 965 50Petronas (35%)

ENH (15%)Exploration

17

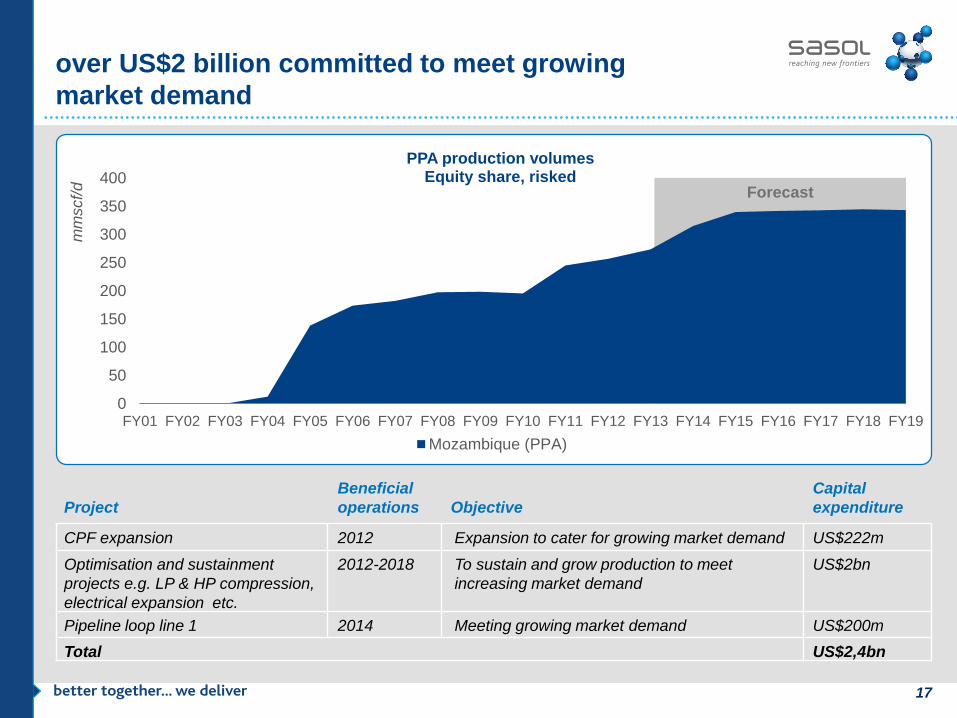

over US$2 billion committed to meet growing

market demand

Project

Beneficial

operations Objective

Capital

expenditure

CPF expansion 2012 Expansion to cater for growing market demand US$222m

Optimisation and sustainment

projects e.g. LP & HP compression,

electrical expansion etc.

2012-2018 To sustain and grow production to meet

increasing market demand

US$2bn

Pipeline loop line 1 2014 Meeting growing market demand US$200m

Total US$2,4bn

Forecast

0

50

100

150

200

250

300

350

400

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

mm

scf/

d

PPA production volumesEquity share, risked

Mozambique (PPA)

18

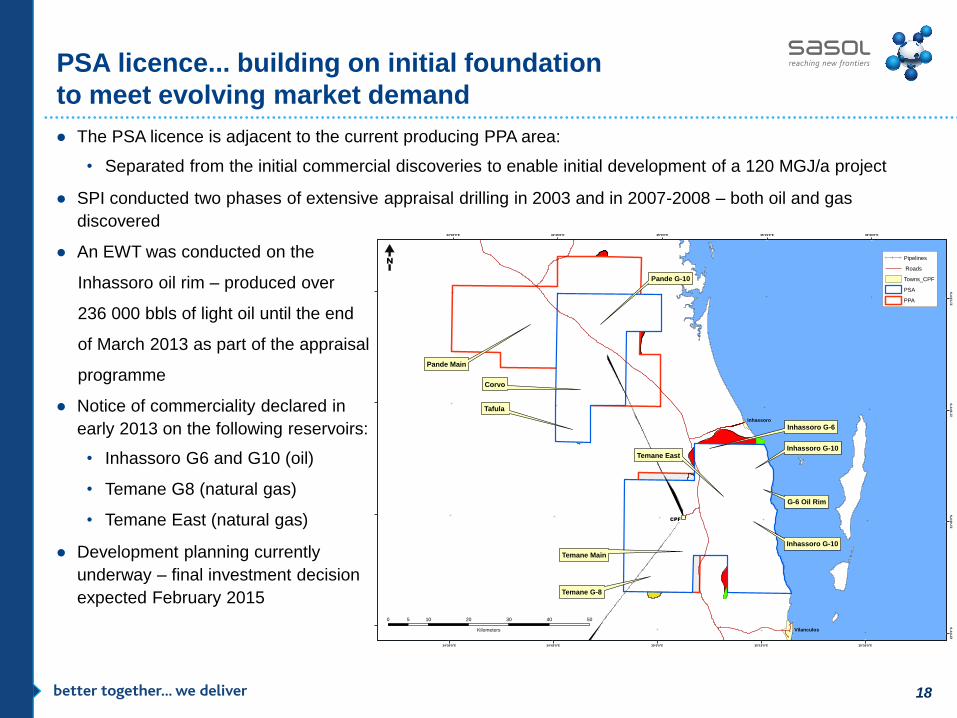

PSA licence... building on initial foundation

to meet evolving market demand

● The PSA licence is adjacent to the current producing PPA area:

• Separated from the initial commercial discoveries to enable initial development of a 120 MGJ/a project

● SPI conducted two phases of extensive appraisal drilling in 2003 and in 2007-2008 – both oil and gas

discovered

● An EWT was conducted on the

Inhassoro oil rim – produced over

236 000 bbls of light oil until the end

of March 2013 as part of the appraisal

programme

● Notice of commerciality declared in

early 2013 on the following reservoirs:

• Inhassoro G6 and G10 (oil)

• Temane G8 (natural gas)

• Temane East (natural gas)

● Development planning currently

underway – final investment decision

expected February 2015

!!

!!

!

!

!

!!

!!

!!

!!

!!

!!

!!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

35°30'0"E

35°30'0"E

35°15'0"E

35°15'0"E

35°0'0"E

35°0'0"E

34°45'0"E

34°45'0"E

34°30'0"E

34°30'0"E

21

°15

'0"S

21

°15

'0"S

21

°30

'0"S

21

°30

'0"S

21

°45

'0"S

21

°45

'0"S

22

°0'0

"S

22

°0'0

"S

! ! ! Pipelines

Roads

Towns_CPF

PSA

PPA

0 10 20 30 40 505

Kilometers

N

Inhassoro

Vilanculos

CPF

Pande G-10

Temane G-8

Temane East

Inhassoro G-6

Temane Main

G-6 Oil Rim

Inhassoro G-10

Inhassoro G-10

Tafula

Corvo

Pande Main

19

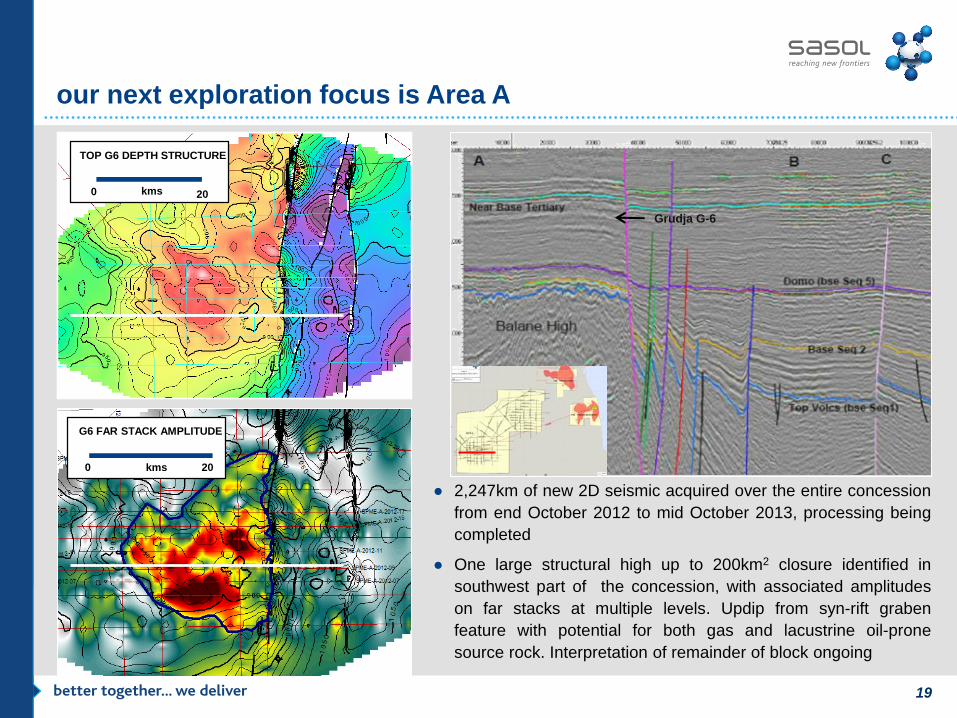

● 2,247km of new 2D seismic acquired over the entire concession

from end October 2012 to mid October 2013, processing being

completed

● One large structural high up to 200km2 closure identified in

southwest part of the concession, with associated amplitudes

on far stacks at multiple levels. Updip from syn-rift graben

feature with potential for both gas and lacustrine oil-prone

source rock. Interpretation of remainder of block ongoing

our next exploration focus is Area A

TOP G6 DEPTH STRUCTURE

0 20kms

G6 FAR STACK AMPLITUDE

0 20kms

Grudja G-6

20

looking ahead

● Pursue exploration

activities

● Optimise current assets

● Explore additional

opportunities to monetise

natural gas in country

● Explore for partnership

opportunities to leverage

Sasol’s gas monetisation

technology

● Build local skills and

supplier capacity

● Pursue sustainable

relations with community

stakeholders

● Continue to align our

activities with government

drivers, e.g., education,

health, energy security

and food security

Operations

Continue

growing

our

heartland

Licence to thrive

thank you