asset investment outlook - 3rd quarter 2016 management ... · investment outlook - 3rd quarter 2016...

TRANSCRIPT

Page 1 of 4

Asset

Management

Partners

Investment Outlook - 3rd quarter 2016

Investment Outlook – 3rd quarter 2016

Global macroeconomic environment

United States

The leading indicators both for the service and the manufacturing sectors are in expansionary territory. The latter accelerated disproportionally in recent months.

Consumer confidence retreated recently as economic growth is slowing (but remains solid). Employment data remain positive and are putting upward pressure on wages.

Market expectations of soon-to-come further interest rate hikes by the Fed have been put on hold as the central bank is becoming increasingly dovish.

Europe

Surprisingly for market participants, the UK has voted for the “Brexit”. This will raise uncertainty as the terms of Britain’s exit from the EU are negotiated.

The economy in the Eurozone is expanding but at a tepid pace. Unemployment is coming down gradually overall but with wide differences among the various countries.

Massive ECB QE expansion has a positive effect on financing costs but rising inflation expectations are lacking. The ECB’s credibility is increasingly questioned.

Fiscal debt remains a major problem as politicians refuse to address structural issues.

Switzerland

Swiss leading indicators point to an improving economic environment. Net exports and private consumption remain the main drivers.

The SNB has continued to intervene to prevent further Swiss franc appreciation, even more so following the “Brexit” vote.

Emerging markets

Emerging market currencies rebounded somewhat in recent months as commodity prices stabilized, but the GDP growth outlook remains mediocre.

Traditional investments 0-3M to 12M

Currencies

Trading range for USD/CHF: 0.94-1.00 and for EUR/CHF: 1.06-1.12.

Bonds

Yield curves are flattening further across the board. Positive yields are scarce. Over the medium term the trend towards more negative yield levels is expected to continue for both EUR and CHF bonds, while USD bonds will trade sideways. Strategy: Short to mid duration, avoid government and CHF-denominated bonds. Fixed income investments are showing more trading oriented patterns.

Equities

Equity markets continue to trade in vulnerable sideways trends. Valuations, while above historical averages, are not exorbitantly extended but do not provide support. Dividend yields remain appealing. Clearer earnings and sales growth trends would be needed for significant up moves.

Listed alternative investments

Private equity

Discounts to NAV have narrowed somewhat from 25% to roughly 20% but remain above historical averages. Dividend yields remain attractive at roughly 3.5%.

Infrastructure

Generally outperforming broad equity indices with lower volatility. Valuations remain below historical averages, hinting at stable underlying cash flows.

Commodities

Commodity prices are showing scant recovery signs. In the medium run, more stable economic growth in emerging countries would be needed.

Real estate

Risk/return potential remains limited but positive compared to bonds.

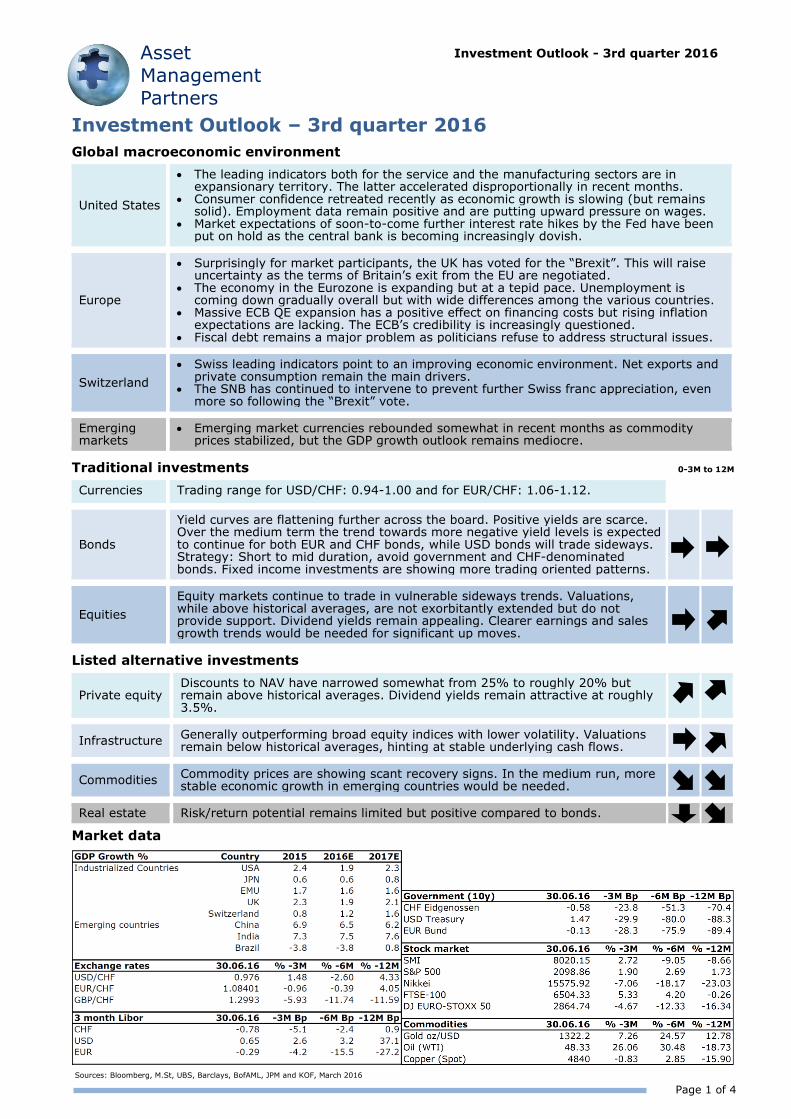

Market data

Sources: Bloomberg, M.St, UBS, Barclays, BofAML, JPM and KOF, March 2016

Page 2 of 4

Investment Outlook – 3rd quarter 2016

Asset

Management

Partners Macroeconomic environment

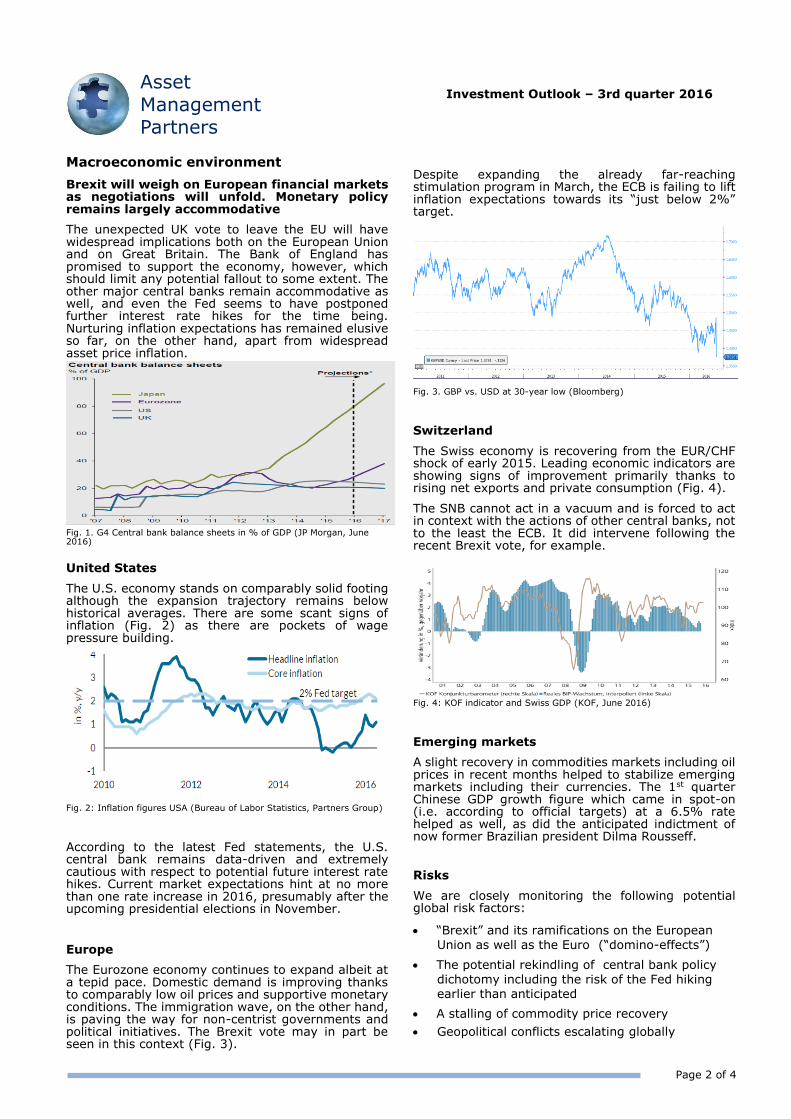

Brexit will weigh on European financial markets as negotiations will unfold. Monetary policy remains largely accommodative

The unexpected UK vote to leave the EU will have widespread implications both on the European Union and on Great Britain. The Bank of England has promised to support the economy, however, which should limit any potential fallout to some extent. The other major central banks remain accommodative as well, and even the Fed seems to have postponed further interest rate hikes for the time being. Nurturing inflation expectations has remained elusive so far, on the other hand, apart from widespread asset price inflation.

Fig. 1. G4 Central bank balance sheets in % of GDP (JP Morgan, June 2016)

United States

The U.S. economy stands on comparably solid footing although the expansion trajectory remains below historical averages. There are some scant signs of inflation (Fig. 2) as there are pockets of wage pressure building.

Fig. 2: Inflation figures USA (Bureau of Labor Statistics, Partners Group)

According to the latest Fed statements, the U.S. central bank remains data-driven and extremely cautious with respect to potential future interest rate hikes. Current market expectations hint at no more than one rate increase in 2016, presumably after the upcoming presidential elections in November.

Europe

The Eurozone economy continues to expand albeit at a tepid pace. Domestic demand is improving thanks to comparably low oil prices and supportive monetary conditions. The immigration wave, on the other hand, is paving the way for non-centrist governments and political initiatives. The Brexit vote may in part be seen in this context (Fig. 3).

Despite expanding the already far-reaching stimulation program in March, the ECB is failing to lift inflation expectations towards its “just below 2%” target.

Fig. 3. GBP vs. USD at 30-year low (Bloomberg)

Switzerland

The Swiss economy is recovering from the EUR/CHF shock of early 2015. Leading economic indicators are showing signs of improvement primarily thanks to rising net exports and private consumption (Fig. 4).

The SNB cannot act in a vacuum and is forced to act in context with the actions of other central banks, not to the least the ECB. It did intervene following the recent Brexit vote, for example.

Fig. 4: KOF indicator and Swiss GDP (KOF, June 2016)

Emerging markets

A slight recovery in commodities markets including oil prices in recent months helped to stabilize emerging markets including their currencies. The 1st quarter Chinese GDP growth figure which came in spot-on (i.e. according to official targets) at a 6.5% rate helped as well, as did the anticipated indictment of now former Brazilian president Dilma Rousseff.

Risks

We are closely monitoring the following potential global risk factors:

“Brexit” and its ramifications on the European Union as well as the Euro (“domino-effects”)

The potential rekindling of central bank policy

dichotomy including the risk of the Fed hiking earlier than anticipated

A stalling of commodity price recovery

Geopolitical conflicts escalating globally

Page 3 of 4

Investment Outlook – 3rd quarter 2016

Asset

Management

Partners Traditional investments

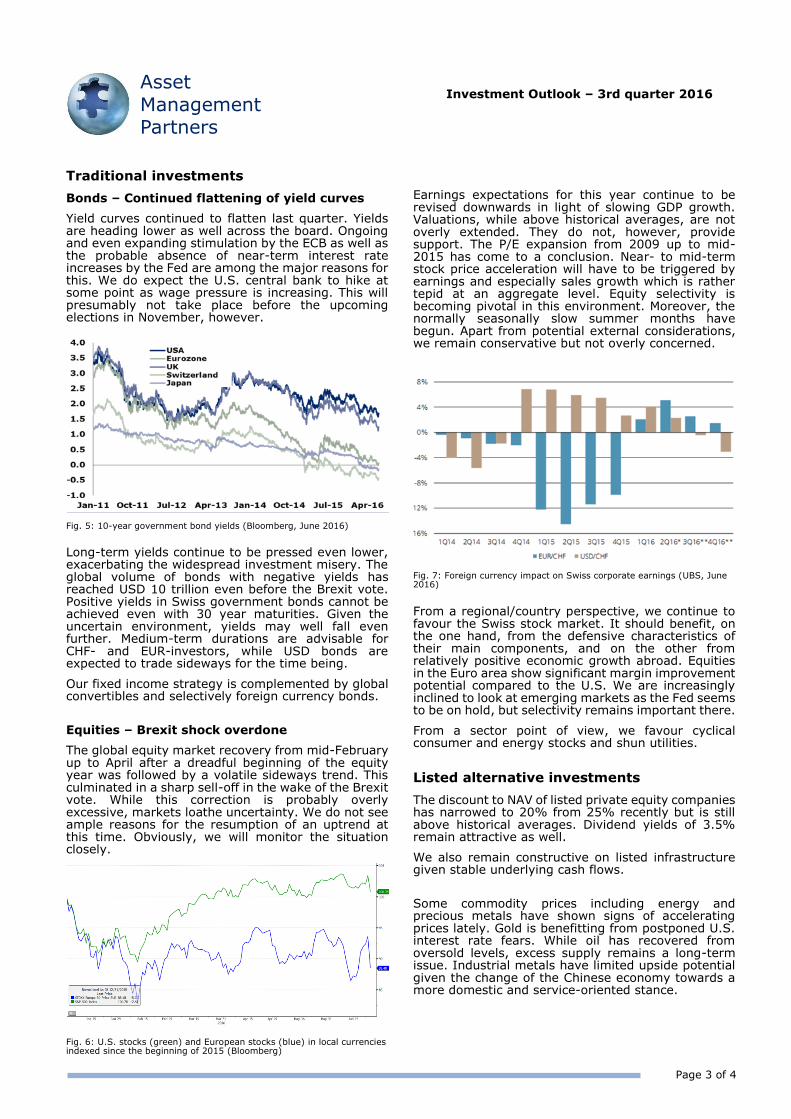

Bonds – Continued flattening of yield curves

Yield curves continued to flatten last quarter. Yields are heading lower as well across the board. Ongoing and even expanding stimulation by the ECB as well as the probable absence of near-term interest rate increases by the Fed are among the major reasons for this. We do expect the U.S. central bank to hike at some point as wage pressure is increasing. This will presumably not take place before the upcoming elections in November, however.

Fig. 5: 10-year government bond yields (Bloomberg, June 2016)

Long-term yields continue to be pressed even lower, exacerbating the widespread investment misery. The global volume of bonds with negative yields has reached USD 10 trillion even before the Brexit vote. Positive yields in Swiss government bonds cannot be achieved even with 30 year maturities. Given the uncertain environment, yields may well fall even further. Medium-term durations are advisable for CHF- and EUR-investors, while USD bonds are expected to trade sideways for the time being.

Our fixed income strategy is complemented by global convertibles and selectively foreign currency bonds.

Equities – Brexit shock overdone

The global equity market recovery from mid-February up to April after a dreadful beginning of the equity year was followed by a volatile sideways trend. This culminated in a sharp sell-off in the wake of the Brexit vote. While this correction is probably overly excessive, markets loathe uncertainty. We do not see ample reasons for the resumption of an uptrend at this time. Obviously, we will monitor the situation closely.

Fig. 6: U.S. stocks (green) and European stocks (blue) in local currencies indexed since the beginning of 2015 (Bloomberg)

Earnings expectations for this year continue to be revised downwards in light of slowing GDP growth. Valuations, while above historical averages, are not overly extended. They do not, however, provide support. The P/E expansion from 2009 up to mid-2015 has come to a conclusion. Near- to mid-term stock price acceleration will have to be triggered by earnings and especially sales growth which is rather tepid at an aggregate level. Equity selectivity is becoming pivotal in this environment. Moreover, the normally seasonally slow summer months have begun. Apart from potential external considerations, we remain conservative but not overly concerned.

Fig. 7: Foreign currency impact on Swiss corporate earnings (UBS, June 2016)

From a regional/country perspective, we continue to favour the Swiss stock market. It should benefit, on the one hand, from the defensive characteristics of their main components, and on the other from relatively positive economic growth abroad. Equities in the Euro area show significant margin improvement potential compared to the U.S. We are increasingly inclined to look at emerging markets as the Fed seems to be on hold, but selectivity remains important there.

From a sector point of view, we favour cyclical consumer and energy stocks and shun utilities.

Listed alternative investments

The discount to NAV of listed private equity companies has narrowed to 20% from 25% recently but is still above historical averages. Dividend yields of 3.5% remain attractive as well.

We also remain constructive on listed infrastructure given stable underlying cash flows.

Some commodity prices including energy and precious metals have shown signs of accelerating prices lately. Gold is benefitting from postponed U.S. interest rate fears. While oil has recovered from oversold levels, excess supply remains a long-term issue. Industrial metals have limited upside potential given the change of the Chinese economy towards a more domestic and service-oriented stance.

Page 4 of 4

Asset Management Partners AG Zugerstrasse 57, 6341 Baar-Zug/Schweiz Tel. +41 (0)41 768 83 83, Fax +41 (0)41 768 83 84 [email protected], www.assetmanagementpartners.ch

The material presented here is solely for purposes of illustration and discussion. The information contained in this document is in summary form for convenience of presentation. The information may be based in part or entirely on hypothetical assumptions, models and/or other analyses (which are in part contained in this document only) by Asset Management Partners AG or affiliated companies ("AMP"). No representation or warranty is made by AMP as to the reasonableness or correctness of the assumptions, models or analyses. The data set forth herein was gathered from various sources which AMP believes, but does not guarantee, to be accurate. The information contained herein is confidential and may not be reproduced in whole or in part.

Investment Outlook – 3rd quarter 2016

Asset

Management

Partners

Accelerating awareness

Companies, households and governments globally are becoming increasingly aware of the potential dangers of cyber attacks. Economic and operative losses as well as reputational damages are increasingly coming into the focus of potential casualties in an increasingly interconnected world. The growth of the “internet of things” has led to a situation where many cars, airplanes, household and office devices can be connected to the internet. This creates potential security vulnerability which has to be addressed.

Fig. 8: Live cyber attacks (map.norsecorp.com, June 2016)

Security breaches have grown by a compound average annual rate of 66% since 2009. According to PwC, in 2015 cyber attacks grew by 38%, while investments in the sector grew by only 24%. Roughly 28% of attacks originated in China, 22% in Turkey, 15% in the U.S. and 8% in South Korea. Roughly USD 76 bln were spent in 2015. The market is expected to grow to USD 170 bln by 2020. In May of 2016, the Central Bank of Bangladesh was hacked which resulted in USD 81 mln stolen (and not even in USD 951 mln thanks to a typing error).

Switzerland not immune

During the first few months of 2016 numerous online portals and websites in Switzerland have been attacked, including major retailers such as Migros or Coop including their subsidiaries’ online web portals Even the Swiss aviation and defense company Ruag, which offers cyber security services itself, was attacked for over a year without detecting the leak. Indirectly the Swiss Department of Defense was a victim as well.

Political and ideological motivations are the reason for roughly 40% of so-called “distributed denial of services” attacks (DDoS). Other, not financially motivated reasons include the disturbing of online gaming, personal rivalries or simply vandalism. Financial extortion is the reason in roughly 15% of the cases.

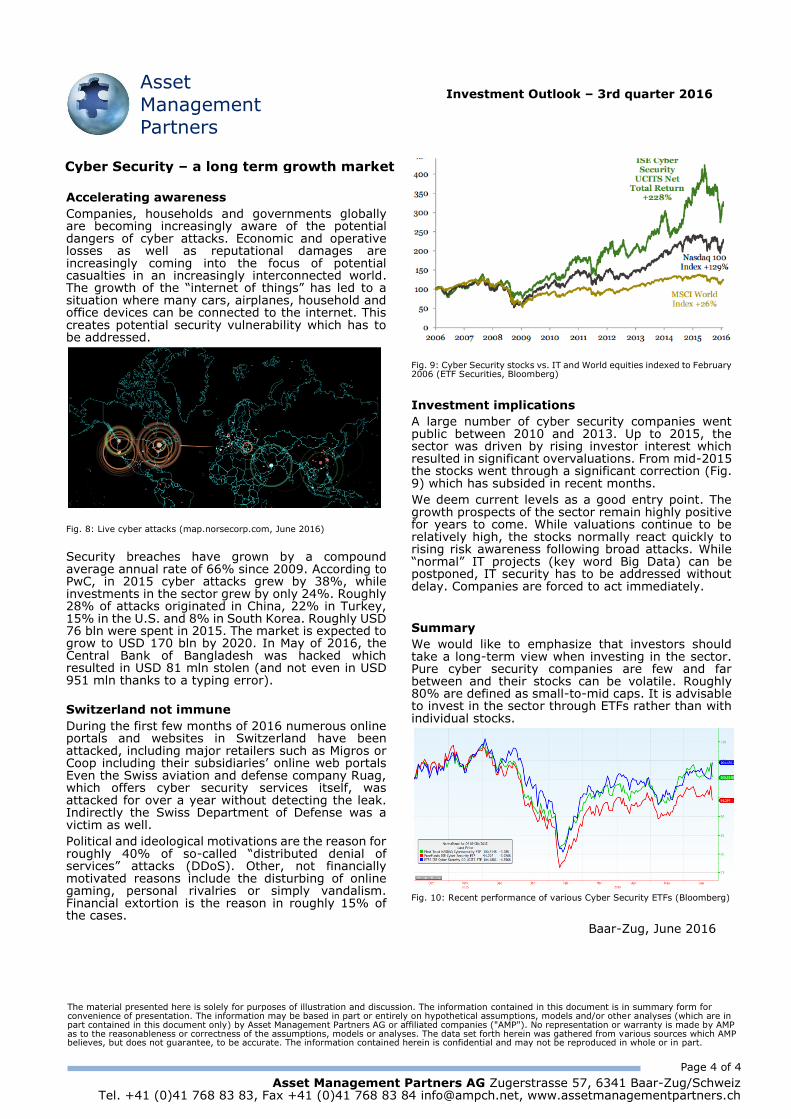

Fig. 9: Cyber Security stocks vs. IT and World equities indexed to February 2006 (ETF Securities, Bloomberg)

Investment implications

A large number of cyber security companies went public between 2010 and 2013. Up to 2015, the sector was driven by rising investor interest which resulted in significant overvaluations. From mid-2015 the stocks went through a significant correction (Fig. 9) which has subsided in recent months.

We deem current levels as a good entry point. The growth prospects of the sector remain highly positive for years to come. While valuations continue to be relatively high, the stocks normally react quickly to rising risk awareness following broad attacks. While “normal” IT projects (key word Big Data) can be postponed, IT security has to be addressed without delay. Companies are forced to act immediately.

Summary

We would like to emphasize that investors should take a long-term view when investing in the sector. Pure cyber security companies are few and far between and their stocks can be volatile. Roughly 80% are defined as small-to-mid caps. It is advisable to invest in the sector through ETFs rather than with individual stocks.

Fig. 10: Recent performance of various Cyber Security ETFs (Bloomberg)

Baar-Zug, June 2016

Cyber Security – a long term growth market