assessing the implementation of the small business …

TRANSCRIPT

SME Policy Index

Eastern Partner Countries 2020ASSESSING THE IMPLEMENTATION OF THE SMALL BUSINESS ACT FOR EUROPE

Eastern P

artner C

ou

ntries 2020 AS

SE

SS

ING

TH

E IM

PL

EM

EN

TAT

ION

OF T

HE

SM

AL

L BU

SIN

ES

S A

CT

FOR

EU

RO

PE

SM

E P

olicy In

dex

SME Policy Index: Eastern Partner Countries

2020

ASSESSING THE IMPLEMENTATION OF THE SMALL BUSINESS ACT FOR EUROPE

This work is published under the responsibility of the Secretary-General of the OECD. The opinions expressed andarguments employed herein do not necessarily reflect the official views of the OECD member countries, or the officialviews of the European Bank for Reconstruction and Development, the European Training Foundation and theEuropean Union.

This document, as well as any data and map included herein, are without prejudice to the status of or sovereignty overany territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

Note by TurkeyThe information in this document with reference to “Cyprus” relates to the southern part of the Island. There is no singleauthority representing both Turkish and Greek Cypriot people on the Island. Turkey recognises the Turkish Republic ofNorthern Cyprus (TRNC). Until a lasting and equitable solution is found within the context of the United Nations, Turkeyshall preserve its position concerning the “Cyprus issue”.

Note by all the European Union Member States of the OECD and the European UnionThe Republic of Cyprus is recognised by all members of the United Nations with the exception of Turkey. Theinformation in this document relates to the area under the effective control of the Government of the Republic of Cyprus.

Please cite this publication as:OECD et al. (2020), SME Policy Index: Eastern Partner Countries 2020: Assessing the Implementation of the Small Business Actfor Europe, SME Policy Index, European Union, Brussels/OECD Publishing, Paris, https://doi.org/10.1787/8b45614b-en.

ISBN 978-92-64-46173-4 (print)ISBN 978-92-64-33010-8 (pdf)

SME Policy IndexISSN 2413-6875 (print)ISSN 2413-6883 (online)

European UnionCatalogue number: OA-02-19-878-EN-C (print)Catalogue number: OA-02-19-878-EN-N (pdf)ISBN 978-92-78-42047-5 (print)ISBN 978-92-78-42046-8 (pdf)

Photo credits: Cover © Designed by Caroline Lee, Spielplatz 13.

Corrigenda to publications may be found on line at: www.oecd.org/about/publishing/corrigenda.htm.

© OECD, ETF, European Union and EBRD 2020

The use of this work, whether digital or print, is governed by the Terms and Conditions to be found at http://www.oecd.org/termsandconditions.

PREFACE 3

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Preface

Small and medium enterprises (SMEs) are a source of jobs and growth. They also have a

role to play in the diversification of output, export and employment, and are a vital source

of entrepreneurial human capital. This is particularly important at a time when the countries

of Eastern Europe and the South Caucasus strive to make their economies more inclusive

and more resilient to shocks. SME development has therefore been central to co-operation

within the framework of the Eastern Partnership (EaP), a joint initiative of the European

Union and six neighbours – Armenia, Azerbaijan, Belarus, Georgia, the Republic of

Moldova and Ukraine.

Today, SMEs generate about half of total business-sector value added in the EaP region,

and they account for slightly more than half of total business-sector employment. Their

innovation potential and ability to adapt to fast-changing market conditions makes them an

increasingly important source of entrepreneurial dynamism.

Since 2012, the SME Policy Index for Eastern Partner countries has been an important

source of support for policymakers in the region and for their external partners seeking to

design and deliver better SME-support policies. Structured around the ten principles of the

Small Business Act (SBA) for Europe, the Index is a unique benchmarking tool designed

by the OECD, the EBRD, the European Training Foundation and the European

Commission to assess countries’ institutions and SME policies against EU and international

best practices.

The report ‘SME Policy Index: Eastern Partner Countries 2020’ marks the third SBA

assessment for the EaP region on the basis of the Index. It provides a comprehensive

overview of SME policies in the region organised around the SBA principles, and it

monitors the progress made since 2016. Across the region, governments have worked to

promote better strategies for SME development and to build institutions that can help

translate those strategies into action and deliver tangible results. Many recommendations

provided in the 2016 assessment have been implemented; particularly those focusing on

regulatory policies, institutional frameworks and measures supporting entrepreneurial

skills and mindset of women and men.

However, important challenges remain. While the situation varies from country to country,

a few broad trends stand out. First, a more demand-driven, collaborative approach to

designing support programmes could help ensure a better fit between public action and

SME needs. Second, stronger monitoring and evaluation systems, underpinned by well-

designed key performance indicators, would enable governments to capture the impact of

policies on firms, as well as use public resources more efficiently and adapt and adjust SME

policies on the basis of better evidence. Finally, level playing field conditions are critical

to the success of any effort to promote entrepreneurship and small firm growth. EaP

countries still have much to do to fight corruption and to ensure business integrity,

competitive neutrality and equal access to inputs and markets for all firms, regardless of

size or ownership. The current report thus includes an assessment of three dimensions of

the business environment that transcend the traditional concerns of SME policy:

competition, contract enforcement and business integrity. This provides a basis for

4 PREFACE

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

identifying structural reform priorities that will create a better business environment for

firms of all sizes.

We commend the efforts of the Eastern Partner countries to foster private sector

development through better SME policies, as well as better implementation of those

policies, and look forward to continuing our work with them to deliver better opportunities

for firms and citizens across the region.

Angel Gurría

Secretary General,

OECD

Olivér Várhelyi

EU Commissioner

for Neighbourhood

and Enlargement

Negotiations

Suma Chakrabarti

President,

European Bank for

Reconstruction and

Development

Cesare Onestini

Director,

European Training

Foundation

FOREWORD 5

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Foreword

About a decade ago, in May 2009, Armenia, Azerbaijan, Belarus, Georgia, the Republic of

Moldova and Ukraine, together with the European Union launched a strategic and

ambitious partnership – the EU Eastern Partnership (EaP). In an effort to build a more

prosperous and resilient region, this endeavour is based on shared values, mutual interests

and commitments, bringing EaP countries closer to the European Union through economic

integration and by developing stronger ties among the partner countries themselves, to

deliver tangible results for their citizens.

Economic and private sector development play an essential role in achieving this objective.

Looking back at the past decade, significant efforts have been made to develop stronger,

more diversified and dynamic economies across the region. Small and medium-sized

enterprises (SMEs) have been instrumental in driving this agenda forward. In fact, thanks

to their capacity to innovate and adapt to fast-changing market conditions, SMEs can

facilitate the shift towards a modern, more diversified and demand-driven economy, acting

as an engine for higher-quality employment generation and sustainable growth. However,

their potential in the EaP region remains untapped. Although representing up to 99% of all

firms, they currently generate around half of total business-sector value added and account

for only half of total business sector employment.

The SME Policy Index: Eastern Partner Countries 2020 – Assessing the Implementation of

the Small Business Act for Europe is a unique benchmarking tool for assessing and

monitoring progress in the design and implementation of SME polices against EU and

international good practice. It is structured around the ten principles of the Small Business

Act for Europe (SBA), which provides a wide range of pro-enterprise measures to guide

the design and implementation of SME policies. This report marks the third edition in this

series, following assessments in 2012 and 2016. It provides a comprehensive overview of

the state of play in the implementation of the ten SBA principles, and monitors progress

made since 2016. It also identifies remaining challenges affecting SMEs in the EaP

countries and provides recommendations to address them based on EU and international

good practice examples. The 2020 edition also features a novelty: an assessment of three

new dimensions – competition, contract enforcement and business integrity – that goes

beyond core SME policy to look at key structural reform priorities that are critical to

establishing a level playing field for enterprises of all sizes.

The 2020 assessment reveals significant progress, with many of the 2016 recommendations

having been implemented. An essential precondition for SMEs to grow and prosper is the

existence of an adequate regulatory policy and institutional framework, an area in which

all six EaP countries have demonstrated sustained commitment to reform. Across the

region, governments have made considerable progress in designing strategies for SME

development and building strong institutions that can help deliver tangible results and

translate policies into action. They have acknowledged the crucial role of a responsive

government and effective institutions in promoting SME development, encouraging

investment, and reducing informality and corruption – laying the foundation for a healthy

business environment in which enterprises of all sizes and ownership types can thrive.

6 FOREWORD

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Nevertheless, more remains to be done to further build SME capacities, so that they become

more productive, more competitive and innovative, and better integrated into global

markets. Policies need to better match SME needs, which will require a demand-driven

approach to designing support programmes through a collaborative approach. Monitoring

and evaluation systems must be considerably strengthened and backed up by key

performance indicators, to capture the impact of policies on businesses, favouring the

optimal use of public resources and advancing evidence-based policy making. Lastly, all

the above-mentioned efforts would be in vain if level-playing-field conditions are not in

place to ensure competitive neutrality and equal access to inputs and markets for all firms,

regardless of their size and ownership type.

This report is the result of a collaborative effort by the Organisation for Economic Co-

operation and Development (OECD), the European Bank for Reconstruction and

Development (EBRD) and the European Training Foundation (ETF), with the support of

the European Commission and the governments involved. The views of a wide range of

stakeholders, including SMEs themselves, were sought and are reflected throughout the

publication.

ACKNOWLEDGEMENTS 7

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Acknowledgements

The SME Policy Index: Eastern Partner Countries 2020 – Assessing the Implementation of

the Small Business Act for Europe is the result of work conducted by the OECD and six

Eastern Partner countries (Armenia, Azerbaijan, Belarus, Georgia, Republic of Moldova,

and Ukraine), in co-operation with the European Bank for Reconstruction and

Development (EBRD), the European Commission and the European Training Foundation

(ETF).

The report was written under the guidance of Andreas Schaal, Director of the OECD Global

Relations Secretariat and William Tompson, Head of the OECD Eurasia Division.

The project was managed by Daniel Quadbeck, Senior Policy Analyst, OECD Eurasia

Division, and co-ordinated by Francesco Alfonso and Alena Frid, OECD Eurasia Division.

The project benefitted from the early guidance of Meryem Torun, former OECD Eurasia

Division. Extensive support in finalising the report for publication was provided by Carlotta

Moiso, OECD Eurasia Division. It further profited from inputs by Marzena Kisielewska,

Head of the OECD South East Europe Division, as lead reviewer of the publication.

The work of the partner institutions was overseen by Simone Zeh Atanasovski, Principal,

Svenja Petersen, Principal, and Christian Cronauer (all EBRD), Rafaella Boudron and

Kristi Raidma, Project Managers (European Commission), and Olena Bekh, Senior

Specialist in Human Capital Development (ETF). This report was made possible thanks to

the contributions of the National Small Business Act (SBA) co-ordinators who supported

the data-gathering and verification process. We extend our gratitude to all government

officials and other stakeholders who have been actively involved across the region, and

whose support and dedication have made the development of this publication possible. In

the EaP countries, the following SBA co-ordinators led their countries’ participation in all

stages of the project: Karen Gevorgyan (Armenia), Elchin Ibrahimov, Emil Ismaylkhanov

and Vusala Jafarova (Azerbaijan), Tatyana Bykova and Irina Babachenok (Belarus),

Ekaterina Mikabadze and Tsisnami Sabadze (Georgia), Iulia Costin, Constantin Turcanu

and Oxana Paladiciuc (Moldova), and Olexandr Palazov and Andriy Slabinskiy (Ukraine).

Principal authors of the report are:

Executive summary Alena Frid, Daniel Quadbeck

Policy framework and structure of the report

Francesco Alfonso, Carlotta Moiso

Overview of key findings Carlotta Moiso, Cecilia Trasi, Olena Bekh (ETF)

Economic context Déborah Pereira, Hubert Massoni, Carlotta Moiso

Level playing field Lyudmyla Tautiyeva; Sabine Zigelski (OECD Competition Division)

Pillar A – Responsive Government Antonio Fanelli (external consultant), Hubert Massoni

Pillar B – Entrepreneurial Human Capital Olena Bekh, Anthony Gribben, Pirita Vuorinen (all three from ETF)

Pillar C – Access to Finance Christian Cronauer, Jan Keller, Svenja Petersen, Simone Zeh Atanasovski (all from EBRD)

Pillar D – Access to Markets Patrik Pruzinsky; Knut Blind, Florian Münch, Simone Wurster (all three from Technische Universität Berlin); Daniel Ivarsson (external consultant)

8 ACKNOWLEDGEMENTS

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Pillar E – Innovation and Business Support

Alena Frid, Francesco Alfonso; Guy Halpern (OECD Environment)

SBA country profiles The general parts of the profiles were drafted by Lyudmyla Tautiyeva (Armenia, Ukraine), Alena Frid (Belarus, Georgia) and Patrik Pruzinsky (Azerbaijan, Moldova), while dimension-specific parts were drafted by the same authors as above. In addition, pillar B sections were written by Florian Kadletz (Armenia, Azerbaijan), Kristien Van den Eynde (Ukraine), Anthony Gribben (Georgia, Moldova) and Pirita Vuorinen (Belarus) (all four from ETF).

Annexes Alena Frid, Lyudmyla Tautiyeva, Carlotta Moiso

Note: All authors are from the OECD Eurasia Division, unless specified otherwise.

The report was reviewed and benefitted from further inputs provided by the OECD

Environment Directorate; the OECD Directorate for Enterprise and Financial Affairs (Anti-

Corruption Network, Competition and Investment Divisions); the OECD Centre for Tax

Policy and Administration; the OECD Directorate for Science, Technology and Innovation,

and OECD SIGMA (Support for Improvement in Governance and Management). At the

EBRD, inputs were provided by the SME Finance and Development Group; the Economic

Policy and Governance Department; the Office of the General Counsel, Local Currency

and Capital Markets; and the country teams in the Eastern Partner region. Pillar E benefitted

from additional comments provided by the Innovative Policies Development Section of the

UNECE.

The publication was also reviewed and supported by the European Commission’s

Directorate-General Neighbourhood and Enlargement Negotiations (DG NEAR);

Directorate-General Internal Market, Industry, Entrepreneurship and SMEs (DG GROW);

and the EU Delegations in the Eastern Partner countries. In particular, the OECD team is

grateful to the contributions from Hoa-Binh Adjemian (DG NEAR), Maxime Bablon and

Tom Diderich (DG GROW).

The independent assessments were conducted with the support of local consultants:

EV Consulting (Armenia), Yulia Aliyeva (Azerbaijan), UNITER (Belarus), Lali

Gogoberidze (Georgia), CIVIS (Moldova) and Institute for Economic Research and Policy

Consulting (Ukraine). The competition assessment was conducted with the support of

Maksym Nazarenko (Sayenko Kharenko Newlaw Firm). ETF’s national experts Jemma

Israyelyan (Armenia), Sadaqat Qambarova (Azerbaijan), Irina Tochitskaya (Belarus),

Giorgi Kobaladze (Georgia), Ghenadie Ivascenco (Moldova) and Bogdana Aleksandrova

(Ukraine) provided important support to the assessment of human capital dimensions.

The final report was edited and prepared for publication by Elisa Larrakoetxea, Kristin

Sazama, with the strategic support of Vanessa Berry-Chatelain (OECD Global Relations

Secretariat) and Carmen Biezma Fernandez (OECD Public Affairs and Communications

Directorate). It was edited and proofread by Chris Marquardt. The implementation of the

project was assisted by Eugenia Klimenka, Maria Ferreira, Mariana Tanova and Jolanta

Chmielik (OECD Global Relations Secretariat).

This SBA assessment project is implemented within the EU4Business initiative, benefitting

from the financial assistance of the European Union. The views herein can in no way be

taken to reflect the position of the European Union or the Member States.

TABLE OF CONTENTS 9

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Table of Contents

Preface .................................................................................................................................................... 3

Foreword ................................................................................................................................................ 5

Acknowledgements ................................................................................................................................ 7

Abbreviations and acronyms .............................................................................................................. 19

Executive summary ............................................................................................................................. 27

Policy framework, structure of the report and assessment process ................................................ 31

The Small Business Act for Europe as underlying policy framework ............................................... 31 The 2020 SBA assessment framework and structure of the report .................................................... 32 Supplementary data ............................................................................................................................ 36 The 2020 SBA assessment process .................................................................................................... 38 The Eastern Partnership and the Small Business Act for Europe ...................................................... 39 References .......................................................................................................................................... 43 Notes .................................................................................................................................................. 44

Overview: 2020 SME Policy Index scores and key findings ............................................................ 45

Overview of 2020 key findings for Eastern Partner countries ........................................................... 45 2020 SME Policy Index scores for Eastern Partner countries ........................................................... 68 References .......................................................................................................................................... 72 Notes .................................................................................................................................................. 72

Economic context ................................................................................................................................. 73

A heterogeneous region with a diverse economic structure .............................................................. 74 Regional recovery but uncertain prospects ........................................................................................ 78 Persistent cyclical and structural weaknesses .................................................................................... 78 Stronger level-playing field is needed to unleash the potential of SMEs .......................................... 86 References .......................................................................................................................................... 88 Notes .................................................................................................................................................. 89

Part I. Small Business Act assessment: Findings by pillar .............................................................. 91

Chapter 1. Level playing field in the Eastern Partner countries .................................................... 93

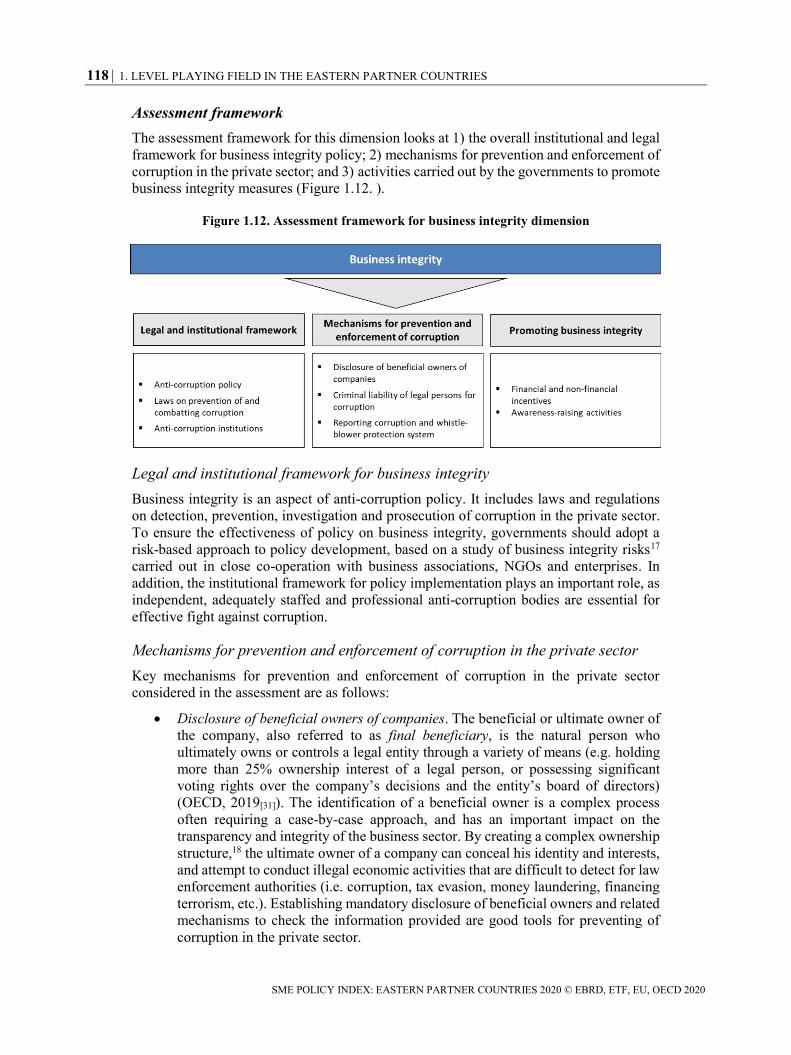

Introduction ........................................................................................................................................ 94 Competition ....................................................................................................................................... 95 Contract enforcement and alternative dispute resolution ................................................................. 106 Business integrity ............................................................................................................................. 116 Policy Instruments – Level playing field ......................................................................................... 125 References ........................................................................................................................................ 127 Notes ................................................................................................................................................ 131

Chapter 2. Pillar A – Responsive government ................................................................................ 133

10 TABLE OF CONTENTS

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Introduction ...................................................................................................................................... 134 Institutional and regulatory framework for SME policy .................................................................. 136 Operational environment for SMEs ................................................................................................. 148 Bankruptcy and second chance ........................................................................................................ 157 Policy instruments – Responsive Government ................................................................................ 167 References ........................................................................................................................................ 168 Notes ................................................................................................................................................ 170

Chapter 3. Pillar B – Entrepreneurial human capital ................................................................... 173

Introduction ...................................................................................................................................... 174 Entrepreneurial learning................................................................................................................... 176 Women’s entrepreneurship .............................................................................................................. 184 Enterprise skills ................................................................................................................................ 194 Policy instruments – Entrepreneurial Human Capital ...................................................................... 203 References ........................................................................................................................................ 204 Notes ................................................................................................................................................ 208

Chapter 4. Pillar C – Access to finance ........................................................................................... 209

Introduction ...................................................................................................................................... 210 Assessment framework .................................................................................................................... 212 Analysis ........................................................................................................................................... 213 Policy instruments – Access to finance ........................................................................................... 229 References ........................................................................................................................................ 230

Chapter 5. Pillar D – Access to markets .......................................................................................... 233

Introduction ...................................................................................................................................... 234 Public procurement .......................................................................................................................... 236 Standards and technical regulations ................................................................................................. 242 SME Internationalisation ................................................................................................................. 251 Policy instruments – Access to markets ........................................................................................... 264 References ........................................................................................................................................ 265 Notes ................................................................................................................................................ 268

Chapter 6. Pillar E – Innovation and Business Support ................................................................ 271

Introduction ...................................................................................................................................... 272 Business Development Services ...................................................................................................... 274 Innovation policy for SMEs ............................................................................................................. 284 SMEs in a green economy ............................................................................................................... 295 Policy instruments – Innovation and Business Support ................................................................... 304 References ........................................................................................................................................ 306 Notes ................................................................................................................................................ 308

Part II. Small Business Act assessment: Eastern Partner country profiles ................................. 309

Chapter 7. Armenia: Small Business Act country profile ............................................................. 311

Key findings ..................................................................................................................................... 312 Context ............................................................................................................................................. 313 SBA assessment by pillar ................................................................................................................ 317 The way forward .............................................................................................................................. 336 Conclusion ....................................................................................................................................... 339 References ........................................................................................................................................ 340

TABLE OF CONTENTS 11

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Notes ................................................................................................................................................ 342

Chapter 8. Azerbaijan: Small Business Act country profile ......................................................... 343

Key findings ..................................................................................................................................... 344 Context ............................................................................................................................................. 345 SBA assessment by pillar ................................................................................................................ 349 The way forward .............................................................................................................................. 368 Conclusion ....................................................................................................................................... 370 References ........................................................................................................................................ 371 Notes ................................................................................................................................................ 372

Chapter 9. Belarus: Small Business Act country profile ............................................................... 375

Key findings ..................................................................................................................................... 376 Context ............................................................................................................................................. 377 SBA assessment by pillar ................................................................................................................ 382 The way forward .............................................................................................................................. 404 Conclusion ....................................................................................................................................... 407 References ........................................................................................................................................ 408 Notes ................................................................................................................................................ 410

Chapter 10. Georgia: Small Business Act country profile ............................................................. 411

Key findings ..................................................................................................................................... 412 Context ............................................................................................................................................. 413 SBA assessment by pillar ................................................................................................................ 417 The way forward .............................................................................................................................. 438 Conclusion ....................................................................................................................................... 440 References ........................................................................................................................................ 441 Notes ................................................................................................................................................ 443

Chapter 11. Republic of Moldova: Small Business Act country profile ....................................... 445

Key findings ..................................................................................................................................... 446 Context ............................................................................................................................................. 447 SBA assessment by pillar ................................................................................................................ 451 The way forward .............................................................................................................................. 471 Conclusion ....................................................................................................................................... 473 References ........................................................................................................................................ 474 Notes ................................................................................................................................................ 476

Chapter 12. Ukraine: Small Business Act country profile ............................................................. 477

Key findings ..................................................................................................................................... 478 Context ............................................................................................................................................. 479 SBA assessment by pillar ................................................................................................................ 483 The way forward .............................................................................................................................. 506 Conclusion ....................................................................................................................................... 509 References ........................................................................................................................................ 510 Notes ................................................................................................................................................ 513

Annex A. Methodology for the Small Business Act assessment .................................................... 517

Scoring methodology ....................................................................................................................... 517 Notes ................................................................................................................................................ 520

12 TABLE OF CONTENTS

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Annex B. Organisation profiles ........................................................................................................ 521

Organisation for Economic Co-operation and Development (OECD), Eurasia Competitiveness

Programme ....................................................................................................................................... 521 European Commission, DG NEAR and DG GROW ....................................................................... 521 European Training Foundation ........................................................................................................ 522 European Bank for Reconstruction and Development ..................................................................... 523

Tables

Table 1. SME Policy Index strengths and weaknesses .......................................................................... 32 Table 2. The detailed SBA assessment framework and its links to the Small Business Act principles 33 Table 3. Assessment framework for the Level Playing Field pillar ...................................................... 35 Table 4. Progress in the institutional and regulatory framework dimension ......................................... 49 Table 5. Progress in the operational environment dimension................................................................ 50 Table 6. Progress in the bankruptcy and second chance dimension ...................................................... 51 Table 7. Progress in the entrepreneurial learning and women’s entrepreneurship dimensions ............. 53 Table 8. Progress in the SME skills dimension ..................................................................................... 54 Table 9. Progress in the access to finance dimension ............................................................................ 55 Table 10. Progress in the public procurement dimension ..................................................................... 56 Table 11. Progress in the standards and regulations dimension ............................................................ 57 Table 12. Progress in the internationalisation dimension ...................................................................... 58 Table 13. Progress in the business development services dimension .................................................... 59 Table 14. Progress in the innovation policy dimension ......................................................................... 60 Table 15. Progress in the green economy dimension ............................................................................ 61 Table 16. Overview of Armenia’s key reforms since 2016 and recommendations ............................... 61 Table 17. Overview of Azerbaijan’s key reforms since 2016 and recommendations ........................... 61 Table 18. Overview of Belarus’ key reforms since 2016 and recommendations .................................. 62 Table 19. Overview of Georgia’s key reforms since 2016 and recommendations ................................ 62 Table 20. Overview of Moldova’s key reforms since 2016 and recommendations .............................. 63 Table 21. Overview of Ukraine’s key reforms since 2016 and recommendations ................................ 63 Table 22. Summary of regional progress in SME policy development ................................................. 65 Table 23. Percentage change in each dimension between 2016 and 2020 ............................................ 66 Table 24. Summary of each country’s progress and main areas for improvement ............................... 67 Table 25. Policy development scale ...................................................................................................... 68 Table 26. 2020 SME Policy Index scores in the EaP countries ............................................................ 69 Table 27. Key data for the Eastern Partner countries, 2018 .................................................................. 75 Table 28. Key macroeconomic indicators for Eastern partner countries, 2018 ..................................... 78 Table 29. SME sector statistics, 2018 or latest available ...................................................................... 86 Table 1.1. Enforcing contracts in EaP countries, WB Doing Business 2020 ...................................... 111 Table 1.2. Property rights and intellectual property protection in EaP countries, 2019 ...................... 113 Table 1.3. EaP countries progress in Corruption Perception Index ranking ....................................... 120 Table 1.4. Dimension challenges and policy instruments – Level playing field ................................. 125 Table 2.1. Country scores by dimension and sub-dimension, 2020 .................................................... 135 Table 2.2. Scores for the Institutional framework sub-dimension....................................................... 140 Table 2.3. EaP and EU SME definitions ............................................................................................. 141 Table 2.4. SME Strategies in EaP countries ........................................................................................ 143 Table 2.5. Detailed information on SME agencies in EaP countries................................................... 144 Table 2.6. Scores for the Legislative simplification and RIA sub-dimension ...................................... 146 Table 2.7. Scores for the Public-Private Consultations sub-dimension .............................................. 147

TABLE OF CONTENTS 13

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Table 2.8. Scores for the E-government services sub-dimension ........................................................ 152 Table 2.9. Scores for the Business licenses and permits sub-dimension ............................................. 154 Table 2.10. Scores for the Company registration sub-dimension ....................................................... 155 Table 2.11. Scores for the Tax compliance procedures for SMEs sub-dimension .............................. 156 Table 2.12. Tax compliance procedures for SMEs in EaP countries .................................................. 156 Table 2.13. Scores for the Preventive measures sub-dimension ......................................................... 162 Table 2.14. Scores for the Survival bankruptcy procedures sub-dimension ....................................... 164 Table 2.15. Scores for the Promoting second chance sub-dimension ................................................. 166 Table 2.16. Dimension challenges and policy instruments – Pillar A ................................................. 167 Table 3.1. Country scores by dimension and sub-dimension, 2020 .................................................... 176 Table 3.2. Scores for the Entrepreneurial learning sub-dimension .................................................... 178 Table 3.3. Scores for the Women’s entrepreneurship sub-dimension ................................................. 187 Table 3.4. Scores for the Enterprise skills dimension ......................................................................... 197 Table 3.5. Dimension challenges and policy instruments – Entrepreneurial Human Capital ............. 203 Table 4.1. Country scores by dimension and sub-dimensions, 2020................................................... 211 Table 4.2. Key banking sector indicators (2008-18) ........................................................................... 215 Table 4.3. Scores for the Legal and regulatory framework sub-dimension ........................................ 216 Table 4.4. Credit information coverage in the EaP economies (2008-19) .......................................... 217 Table 4.5. Scores for the Bank financing sub-dimension .................................................................... 220 Table 4.6. Scores for the Non-bank financing sub-dimension............................................................. 223 Table 4.7. Venture capital by stage ..................................................................................................... 225 Table 4.8. Scores for the Venture capital sub-dimension .................................................................... 226 Table 4.9. Scores for the Financial literacy sub-dimension ................................................................ 228 Table 4.10. Dimension challenges and policy instruments – Pillar C ................................................. 229 Table 5.1. Country scores by dimension and sub-dimension, 2020 .................................................... 235 Table 5.2. Scores for the Public procurement dimension ................................................................... 239 Table 5.3. Scores for the Overall coordination and general measures sub-dimension ...................... 247 Table 5.4. Scores for the Approximation with the EU Acquis sub-dimension .................................... 248 Table 5.5. Scores for the SMEs Access to Standardisation sub-dimension ......................................... 249 Table 5.6. Scores for the Export promotion sub-dimension ................................................................ 258 Table 5.7. Scores for the Integration into GVCs sub-dimension ......................................................... 260 Table 5.8. OECD Trade Facilitation Indicators, scores by country (2017) ......................................... 261 Table 5.9. Scores for the Use of e-commerce sub-dimension ............................................................. 263 Table 5.10. Dimension challenges and policy instruments – Pillar D ................................................. 264 Table 6.1. Country scores by dimension and sub-dimension, 2020 .................................................... 273 Table 6.2. Provision of publicly (co-)funded business development services to SMEs (2017) .......... 278 Table 6.3. Scores for the Support services provided by the government sub-dimension .................... 281 Table 6.4. Scores for the Government support for private BDS sub-dimension ................................. 282 Table 6.5. Horizon 2020 – Participation of EaP countries .................................................................. 290 Table 6.6. Scores for the Policy framework for innovation sub-dimension ........................................ 291 Table 6.7. Scores for the Government support services sub-dimension .............................................. 292 Table 6.8. Scores for the Government financial support sub-dimension ............................................ 293 Table 6.9. Scores for the Policy framework for non-technical innovation sub-dimension ................. 294 Table 6.10. Scores for the Environmental policies sub-dimension ..................................................... 300 Table 6.11. Scores for the Incentives and instruments sub-dimension ................................................ 302 Table 6.12. Dimension challenges and policy instruments – Pillar E ................................................. 304 Table 7.1. SME Policy Index scores for Armenia, 2020 vs. 2016 ...................................................... 312 Table 7.2. Implementation progress on SME Policy Index 2016 priority reforms – Armenia ........... 313 Table 7.3. Armenia: Main macroeconomic indicators, 2013-18 ......................................................... 314 Table 7.4. Definition of micro, small and medium enterprises in Armenia ........................................ 316

14 TABLE OF CONTENTS

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Table 7.5. Roadmap for policy reforms – Armenia ............................................................................. 339 Table 8.1. SME Policy Index scores for Azerbaijan, 2020 vs. 2016 ................................................... 344 Table 8.2. Implementation progress on SME Policy Index 2016 priority reforms – Azerbaijan ........ 345 Table 8.3. Azerbaijan: Main macroeconomic indicators, 2013-18 ..................................................... 346 Table 8.4. Definitions of SMEs in Azerbaijan .................................................................................... 347 Table 8.5. Roadmap for policy reforms – Azerbaijan ......................................................................... 370 Table 9.1. SME Policy Index scores for Belarus, 2020 vs. 2016 ........................................................ 376 Table 9.2. Implementation progress on SME Policy Index 2016 priority reforms – Belarus ............. 377 Table 9.3. Belarus: Main macroeconomic indicators, 2013-18 ........................................................... 378 Table 9.4. The SME definition in Belarus ........................................................................................... 380 Table 9.5. Belarus: Roadmap for reforms ........................................................................................... 407 Table 10.1. SME Policy Index scores for Georgia, 2020 vs. 2016...................................................... 412 Table 10.2. Implementation progress on SME Policy Index 2016 priority reforms – Georgia ........... 413 Table 10.3.Georgia: Main macroeconomic indicators, 2013-18 ......................................................... 414 Table 10.4. The SME definition in Georgia ........................................................................................ 416 Table 10.5. Georgia: Roadmap for policy reforms .............................................................................. 440 Table 11.1. SME Policy Index scores for Moldova, 2020 vs. 2016 .................................................... 446 Table 11.2. Implementation progress on SME Policy Index 2016 priority reforms – Moldova ......... 447 Table 11.3. Moldova: Main macroeconomic indicators, 2013-18....................................................... 448 Table 11.4. Definition of micro, small and medium enterprises in Moldova ...................................... 450 Table 11.5. Roadmap for policy reforms – Moldova .......................................................................... 473 Table 12.1. SME Policy Index scores for Ukraine, 2020 vs. 2016...................................................... 478 Table 12.2. Implementation progress on SME Policy Index 2016 priority reforms – Ukraine ........... 479 Table 12.3. Ukraine: Main macroeconomic indicators, 2013-18 ........................................................ 480 Table 12.4. SME Definition in Ukraine .............................................................................................. 481 Table 12.5. Roadmap for policy reforms – Ukraine ............................................................................ 509 Table A.1. Example of thematic blocks for the "Institutional framework" sub-dimension ................ 518 Table A.2. Overview of changes to the SBA assessment sub-dimensions .......................................... 519

Figures

Figure 1. Structure of the SME Policy Index 2020 ............................................................................... 33 Figure 2. Progress towards SME-supportive policies in EaP countries 2016 and 2020 ........................ 64 Figure 3. Improvements by number of dimensions by EaP country ..................................................... 66 Figure 4. Real GDP growth, 2013-18 .................................................................................................... 74 Figure 5. Labour force participation rate, total (% of total population ages 15+; modelled ILO

estimate), 2018 .............................................................................................................................. 76 Figure 6. Gender disparities in labour force participation (modelled ILO estimate), 2018 .................. 76 Figure 7. Personal remittances, received (% of GDP) ........................................................................... 79 Figure 8. Product diversification in Eastern partner countries .............................................................. 80 Figure 9. Product concentration in the Eastern partner countries .......................................................... 80 Figure 10. Export to Russia and to EU, as share of GDP ...................................................................... 81 Figure 11. Foreign direct investment from EU and Russia, as share of GDP, 2009-17 ........................ 83 Figure 12. SMEs contribution to the economy in EaP countries is on par with EU levels ................... 84 Figure 13. Remaining gap in SME labour productivity in EaP countries vs. EU ................................. 85 Figure 1.1. Assessment framework – Competition ............................................................................... 96 Figure 1.2. Competition policy: Number of adopted criteria ................................................................ 99 Figure 1.3. Scope of action: Number of adopted criteria .................................................................... 100 Figure 1.4. Annual budget of competition authorities (2014-18) ........................................................ 101

TABLE OF CONTENTS 15

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Figure 1.5. Anti-competitive behaviour: number of adopted criteria .................................................. 102 Figure 1.6. Probity of investigation: number of adopted criteria ........................................................ 103 Figure 1.7. Advocacy: number of adopted criteria .............................................................................. 104 Figure 1.8. Assessment framework for contract enforcement and alternative dispute resolution ....... 107 Figure 1.9. Allocated budgets to judiciary .......................................................................................... 109 Figure 1.10. EaP countries in the WEF Global Competitiveness Index, selected indicators .............. 110 Figure 1.11. International Property Rights Index 2018 ....................................................................... 112 Figure 1.12. Assessment framework for business integrity dimension ............................................... 118 Figure 1.13. Corruption Perception Index ........................................................................................... 120 Figure 2.1 SME Policy Index scores for Pillar A: Responsive government ....................................... 135 Figure 2.2. Assessment framework – Institutional and regulatory framework for SME policy

making ......................................................................................................................................... 137 Figure 2.3. Scores for the Institutional and regulatory framework dimension compared to 2016 ..... 139 Figure 2.4. Assessment framework – Operational environment ......................................................... 149 Figure 2.5. Scores for the Operational environment dimension compared to 2016 ............................ 151 Figure 2.6. UN E-Government Development Index, 2018 .................................................................. 152 Figure 2.7. Assessment framework – Bankruptcy and second chance ................................................ 158 Figure 2.8. Scores for the Bankruptcy and second chance dimension compared to 2016 .................. 161 Figure 2.9. Performance of insolvency frameworks in EaP and OECD countries .............................. 161 Figure 3.1. SME Policy Index scores for Pillar B: Entrepreneurial human capital ............................. 175 Figure 3.2. Assessment framework – entrepreneurial learning ........................................................... 177 Figure 3.3. Scores for the Entrepreneurial learning dimension compared to 2016 ............................ 178 Figure 3.4. Assessment framework – Women’s entrepreneurship ...................................................... 186 Figure 3.5. Scores for the Women’s entrepreneurship dimension compared to 2016 ......................... 187 Figure 3.6. Assessment framework – SME skills ................................................................................ 195 Figure 3.7. Scores for the Enterprise skills dimension compared to 2016 .......................................... 197 Figure 4.1. SME Policy Index scores for Pillar C: Access to finance ................................................. 211 Figure 4.2. Assessment framework for Pillar C: Access to finance for SMEs .................................... 212 Figure 4.3. Scores for the Access to finance dimension compared to 2016 ........................................ 214 Figure 4.4. Domestic credit to private sector as percentage of GDP ................................................... 219 Figure 5.1 SME Policy Index scores for Pillar D: Access to markets ................................................. 235 Figure 5.2. Assessment framework – Public procurement .................................................................. 237 Figure 5.3. Scores for the Public procurement dimension compared to 2016 .................................... 239 Figure 5.4. Assessment framework – Standards and technical regulations ......................................... 244 Figure 5.5. Scores for the Standards and technical regulations dimension compared to 2016 .......... 246 Figure 5.6. Assessment framework – SME internationalisation ......................................................... 252 Figure 5.7. Value of exports from the EaP countries (Index, 2014=100) ........................................... 255 Figure 5.8. Scores for the SME internationalisation dimension compared to 2016 ............................ 256 Figure 5.9. Local supplier quality and state of cluster development, 2017 ......................................... 257 Figure 5.10. OECD Trade Facilitation Indicators, EaP, OECD and Visegrad averages (2017) ......... 262 Figure 6.1. SME Policy Index scores for Pillar E: Innovation and Business Support......................... 273 Figure 6.2. Business development services: topic areas and types of services ................................... 274 Figure 6.3. Assessment framework – Business Development Services .............................................. 276 Figure 6.4. SMEs’ uptake of BDS (2017) ........................................................................................... 278 Figure 6.5. Scores for the Business Development Services dimension compared to 2016 .................. 279 Figure 6.6. Assessment framework – Innovation policy for SMEs ..................................................... 285 Figure 6.7. Innovation performance in EaP countries, EU-13 and Visegrad, 2017 ............................ 288 Figure 6.8. Scores for the Innovation policy dimension compared to 2016 ........................................ 289 Figure 6.9. Assessment framework – SMEs in a green economy ....................................................... 297 Figure 6.10. Scores for the Green economy dimension compared to 2016 ......................................... 299

16 TABLE OF CONTENTS

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Figure 7.1. SME Policy Index scores for Armenia.............................................................................. 312 Figure 7.2. Business demography indicators in Armenia, by company size, 2018 ............................. 316 Figure 7.3. Sectoral distribution of SMEs in Armenia, 2018 .............................................................. 317 Figure 7.4. Competition Policy in Armenia ........................................................................................ 319 Figure 7.5. OECD Trade Facilitation Indicators for Armenia, 2017 ................................................... 332 Figure 8.1. SME Policy Index scores for Azerbaijan .......................................................................... 344 Figure 8.2. Business demography indicators in Azerbaijan, by company size, 2018 ......................... 348 Figure 8.3. Sectoral distribution of SMEs in Azerbaijan, 2018........................................................... 349 Figure 8.4. Competition policy in Azerbaijan ..................................................................................... 350 Figure 8.5. OECD Trade Facilitation Indicators for Azerbaijan, 2017 ............................................... 363 Figure 9.1. SME Policy Index scores for Belarus ............................................................................... 376 Figure 9.2. Business environment constraints in Belarus .................................................................... 379 Figure 9.3. Business demography indicators in Belarus by company size, 2018 ................................ 381 Figure 9.4. Sectoral distribution of SMEs in Belarus, 2018 ................................................................ 382 Figure 9.5. Competition policy in Belarus .......................................................................................... 383 Figure 9.6. Women participation in firms’ ownership and workforce in Belarus ............................... 390 Figure 9.7. OECD Trade Facilitation Indicators for Belarus, 2017 ..................................................... 399 Figure 10.1. SME Policy Index scores for Georgia ............................................................................. 412 Figure 10.2. Business demography indicators in Georgia, by company size, 2018 or latest available 416 Figure 10.3. Sectoral distribution of SMEs in Georgia, 2017 ............................................................. 417 Figure 10.4. Competition policy in Georgia ........................................................................................ 418 Figure 10.5. OECD Trade Facilitation Indicators for Georgia, 2017 .................................................. 433 Figure 11.1. SME Policy Index scores for Moldova ........................................................................... 446 Figure 11.2. Business environment constraints in Moldova ............................................................... 449 Figure 11.3. Business demography indicators in Moldova, 2018 or latest available .......................... 450 Figure 11.4. Sectoral distribution of SMEs in Moldova, 2018 ............................................................ 451 Figure 11.5. Competition policy in Moldova ...................................................................................... 453 Figure 11.6. OECD Trade Facilitation Indicators for Moldova, 2017 ................................................ 466 Figure 12.1. SME Policy Index scores for Ukraine ............................................................................. 478 Figure 12.2. Business demography indicators in Ukraine by company size, 2018 ............................. 482 Figure 12.3. Sectoral distribution of SMEs in Ukraine, 2017 ............................................................. 483 Figure 12.4. Competition Policy in Ukraine ....................................................................................... 485 Figure 12.5. OECD Trade Facilitation Indicators for Ukraine, 2017 .................................................. 501 Figure A.1. Questionnaire scoring at the level of sub-dimensions ...................................................... 518

Boxes

Box 1. The Eastern Partnership: Ready to Trade: an EU4Business initiative ....................................... 36 Box 2. What is new in the 2020 assessment framework? ..................................................................... 37 Box 3. COSME ...................................................................................................................................... 43 Box 4. Scoring SME policy development ............................................................................................. 68 Box 5. Economic snapshots of EaP countries ....................................................................................... 77 Box 1.1. The Business Ombudsman Council in Ukraine: Protecting business rights against the

malpractice of public authorities ................................................................................................. 114 Box 1.2. Incentives for anticorruption compliance: Implications for SMEs ....................................... 117 Box 1.3. Promoting private sector integrity: The Ukrainian Network of Integrity and Compliance .. 124 Box 2.1. Public-private consultations on regulatory reforms in Korea ............................................... 138 Box 2.2. SME agencies across the EaP region .................................................................................... 144 Box 2.3. E-government in Estonia ...................................................................................................... 153

TABLE OF CONTENTS 17

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Box 2.4. Early warning systems: building on EU best practices ......................................................... 163 Box 2.5. Giving entrepreneurs a second chance in the EU ................................................................. 165 Box 3.1. Embedding the entrepreneurship key competence in Ukraine’s school curriculum ............. 180 Box 3.2. Evaluation of women’s entrepreneurship support policies in Georgia ................................. 189 Box 3.3. Create your future at home (Moldova) ................................................................................. 200 Box 4.1. Credit guarantee schemes and their key design features....................................................... 220 Box 4.2. A literature review: The impact of microfinance on entrepreneurship and poverty

alleviation .................................................................................................................................... 222 Box 4.3. Money Wise Action Plan for financial literacy in the Netherlands ...................................... 227 Box 5.1. Facilitating SME participation in public procurement: the case of Georgia ......................... 240 Box 5.2. The new European approach to technical regulations and standards .................................... 244 Box 5.3. Financial support for standardisation in Germany ................................................................ 249 Box 5.4. EU programmes to support internationalisation of SMEs in the EaP region ........................ 258 Box 5.5. The CzechInvest Supplier Development Programme ........................................................... 261 Box 6.1. French Chambers of Commerce – IT platform for business diagnostics .............................. 280 Box 6.2. Developing a sustainable market for business development services:

Produce in Georgia ..................................................................................................................... 283 Box 6.3. Horizon 2020: EU support for research and innovation ....................................................... 290 Box 6.4. Indirect financial incentives for innovation in Italy’s Impresa 4.0 National Plan ................ 293 Box 6.5. The European Commission’s Green Action Plan for SMEs ................................................. 300 Box 6.6. Resource Efficient Scotland: A case study in access to green finance for SMEs ................. 303 Box 7.1. SME statistics production and dissemination in Armenia .................................................... 322 Box 8.1. Monitoring of the SME Roadmap ........................................................................................ 353 Box 8.2. Promoting women’s entrepreneurship in Azerbaijan............................................................ 357 Box 9.1. Hi-Tech Park in Belarus ....................................................................................................... 402 Box 10.1. Georgia’s Public Service Hall ............................................................................................. 424 Box 10.2. Georgia’s Innovation and Technology Agency .................................................................. 436 Box 11.1. The Organisation for Small and Medium Enterprises Sector Development (ODIMM) ..... 468 Box 12.1. Ukrainian electronic public procurement system ProZorro and DoZorro .......................... 499

18 TABLE OF CONTENTS

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Look for the StatLinks2at the bottom of the tables or graphs in this book.To download the matching Excel® spreadsheet, just type the link into your Internetbrowser, starting with the https://doi.org prefix, or click on the link from the e-bookedition.

This book has...A service that delivers Excel® files fromthe printedpage!

Follow OECD Publications on:

http://twitter.com/OECD_Pubs

http://www.facebook.com/OECDPublications

http://www.linkedin.com/groups/OECD-Publications-4645871

http://www.youtube.com/oecdilibrary

http://www.oecd.org/oecddirect/Alerts

ABBREVIATIONS AND ACRONYMS 19

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

Abbreviations and acronyms

AA Association Agreement (EU)

ABCA Annual Business Climate Assessment

ACAA Agreement on Conformity Assessment and Acceptance of Industrial Products

ACN Anti-Corruption Network for Eastern Europe and Central Asia

ADR alternative dispute resolution

AGEPI State Agency on Intellectual Property of the Republic of Moldova

AMCU Antimonopoly Committee of Ukraine

AMD Armenian dram (currency)

ARDA Agricultural and Rural Development Agency of Georgia

ARMA Agency for Recovery and Management of Assets of Ukraine

ArmStat

A

State Statistical Committee of Armenia

ASK National Confederation of Entrepreneurs (Employers) Organizations of the

Republic of Azerbaijan

ATM automated teller machine

AzAK Azerbaijan Accreditation Centre

AZPROMO Azerbaijan Export and Investment Promotion Agency

B2B business to business

BBTC Baku Business Training Centre

BDS business development services

BEEPS Business Environment and Enterprise Performance Survey

Belstat National Statistical Committee of the Republic of Belarus

BEROC Belarusian Economic Research and Outreach Center

BFFSE Belarusian Fund for Financial Support of Entrepreneurs

BLA bilateral agreement

BO business ombudsman

BSCA

Belarusian State Centre for Accreditation

BSI

Business Support Infrastructure

20 ABBREVIATIONS AND ACRONYMS

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

BSO Business support organisation

BYR Belarusian ruble (currency)

CA conformity assessment

CAERC Centre of Analysis of Economic Reforms and Communication of Azerbaijan

CAS Centres for Administrative Services of Ukraine

CC Competition Council of Moldova

CCAA Business Consultancy and Business Support Centre of Moldova

CCI Chambers of Commerce and Industry

CEDA Center for Entrepreneurial Education and Business Support

CEN European Committee for Standardization

CENELEC European Committee for Electrotechnical Standardization

CEPA Comprehensive and Enhanced Partnership Agreement

CETA Centralised Exchange Trading in Azerbaijan

CGS credit guarantee scheme

COSME Competitiveness of Enterprises and Small and Medium-Sized Enterprises

CPI corruption perception index

CU credit union

CUTIS Canada-Ukraine Trade & Investment Support Project

DCFTA Deep and Comprehensive Free Trade Area

DfID Department for International Development of the UK

DG GROW Director-General for Internal Market, Industry, Entrepreneurship and SMEs

DG NEAR Director-General for Neighbourhood and Enlargement Negotiations

DigComp European Digital Competence Framework

EA European co-operation for Accreditation

EAC Eurasian Conformity

EAEU Eurasian Economic Union

EaP Eastern Partner

EBRD European Bank for Reconstruction and Development

EC European Commission

EEAS European External Action Service

EEN Enterprise Europe Network

EIA environmental impact assessment

ABBREVIATIONS AND ACRONYMS 21

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

EIB European Investment Bank

EIC European Innovation Council

EIF Enterprise Incubator Foundation, Georgia

EIU Economist Intelligence Unit

EMS environmental management system

EntreComp European Entrepreneurship Competence Framework

EPO Export Promotion Office of Ukraine

EQF European Qualifications Framework

ETF European Training Foundation

ETSI European Telecommunications Standards Institute

EU European Union

EUR euro (currency)

EuroMed Euro-Mediterranean Partnership

FDI foreign direct investment

FX foreign exchange

GAF German-Armenian Fund

GAP Green Action Plan

GCA Competition Agency of Georgia

GCI Global Competitiveness Index (WEF)

GDP Gross domestic product

GEL Georgian lari (currency)

GENIE Georgia National Innovation Ecosystem Project

Geostat National Statistics Office of Georgia

GEOSTM Georgia’s National Agency for Standards and Metrology

GITA Georgia’s Innovation and Technology Agency

GIZ Gesellschaft für Internationale Zusammenarbeit

GNI Gross national income

GOST State Union Standard

GVC global value chain

HHI Hirschman Herfindahl Index

HTP High Technology Park in Belarus

IAF International Accreditation Forum

22 ABBREVIATIONS AND ACRONYMS

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

ICT information and communications technology

IDP internally displaced persons

IEC International Electrotechnical Commission

IFC International Finance Corporation

IFI International Finance Institution

IFRS International Financial Reporting Standards

ILAC International Laboratory Accreditation Co-operation

ILO International Labour Organisation

IMF International Monetary Fund

IP Intellectual property

IPR Intellectual property rights

ISIC International Standard Industrial Classification

ISO International Organisation for Standardisation

IT Information technology

ITC International Trade Center

KfW Kreditanstalt für Wiederaufbau

KPI key performance indicator

LED local economic development

LLL life-long learning

M&E monitoring and evaluation

MAF Ministry of Agriculture and Food of Ukraine

MART Ministry of Antimonopoly Regulation and Trade of Belarus

MDETA Ministry for Development of Economy, Trade and Agriculture of Ukraine

MFI microfinance institution

MIEPO Moldova Investment and Export Promotion Organisation

MLA multilateral agreement

MDL Moldovan leu (currency)

MNE multinational enterprises

MoESD Ministry of Economy and Sustainable Development of Georgia

MOLDAC National Accreditation Centre of the Republic of Moldova

MoU Memorandum of Understanding

MRA Multilateral Recognition Agreement

ABBREVIATIONS AND ACRONYMS 23

SME POLICY INDEX: EASTERN PARTNER COUNTRIES 2020 © EBRD, ETF, EU, OECD 2020

MSME micro, small and medium enterprises

NABU National Anti-corruption Bureau of Ukraine

NAC National Anti-corruption Centre of Moldova

NACP National Agency on Corruption Prevention of Ukraine

NAPR National Agency of Public Registry of Georgia

NARD National Agency for Research and Development of Moldova

NAUU National Accreditation Agency of Ukraine

NBG National Bank of Georgia

NBU National Bank of Ukraine

NEAP National Environmental Action Programme of Georgia

NGO Non-governmental organisation

NIS Newly Independent States

NPL non-performing loan

NQI national quality infrastructure

NSB national standardisation bodies

ODIMM Organisation for SME Sector Development of Moldova

OECD Organisation for Economic Cooperation and Development

OSCE Organisation for Security and Co-operation in Europe

PES Public Employment Services

PPC public-private consultation

PPD public private dialogue

PPJRAI Public-Private Joint Regulation Advancement Initiative

PPL Public Procurement Law

PPP purchasing power parity

QI quality infrastructure

R&D research and development

RIA regulatory impact analysis

SAPO Specialised Anticorruption Prosecutor Office of Ukraine

SARAS Service for Accounting, Reporting and Auditing Supervision of Georgia

SBA Small Business Act for Europe

SBDA Small Business Development Agency of Azerbaijan

SCPEC State Commission for Protection of the Economic Competition of Armenia

24 ABBREVIATIONS AND ACRONYMS