assessing the chrysler bankruptcy - university of michigan

TRANSCRIPT

Michigan Law Review Michigan Law Review

Volume 108 Issue 5

2010

Assessing the Chrysler Bankruptcy Assessing the Chrysler Bankruptcy

Mark J. Roe Harvard Law School

David Skeel Pennsylvania Law School

Follow this and additional works at: https://repository.law.umich.edu/mlr

Part of the Banking and Finance Law Commons, Bankruptcy Law Commons, and the Business

Organizations Law Commons

Recommended Citation Recommended Citation Mark J. Roe & David Skeel, Assessing the Chrysler Bankruptcy, 108 MICH. L. REV. 727 (2010). Available at: https://repository.law.umich.edu/mlr/vol108/iss5/3

This Essay is brought to you for free and open access by the Michigan Law Review at University of Michigan Law School Scholarship Repository. It has been accepted for inclusion in Michigan Law Review by an authorized editor of University of Michigan Law School Scholarship Repository. For more information, please contact [email protected].

ASSESSING THE CHRYSLER BANKRUPTCY

Mark J. RoeDavid Skeel*

Chrysler entered and exited bankruptcy in forty-two days, making itone of the fastest major industrial bankruptcies in memory. It en-tered as a company widely thought to be ripe for liquidation if lefton its own, obtained massive funding from the United States Treas-ury, and exited via a pseudo-sale of its main assets to a newgovernment-funded entity. The unevenness of the compensation toprior creditors raised concerns in capital markets, which we evalu-ate here. We conclude that the Chrysler bankruptcy cannot beunderstood as complying with good bankruptcy practice, that it re-surrected discredited practices long thought interred in thenineteenth- and early twentieth-century equity receiverships, andthat its potential for disrupting financial markets surrounding trou-bled companies in difficult economic times, if the decision isfollowed, is more than small.

TABLE OF CONTENTS

IN TRODU CTIO N ...................................................................................... 728I. CHRYSLER'S § 363 PROBLEM .................................................... 733

A . The D eal Structure ............................................................ 733B. The § 363 vs. § 1129 Problem: Concept ........................... 734

II. THE PRE-CHRYSLER APPELLATE CASES ................................... 736A. Reconciling § 363 Sales with § 1129 Protections ............. 736B. Makeshift Remedies that Validate Priority ........................ 739

1. Judicial Valuation and Priority Determination ........... 7392. C lass C onsent ............................................................. 7403. A M arket Test .............................................................. 740

III. THE CHRYSLER SALE ............................................................... 741A . Valuation ............................................................................ 742B . C onsent .............................................................................. 743C . The M arket Test ................................................................. 746

* Professors, Harvard and University of Pennsylvania Law Schools, respectively. Special

thanks to A. David Lander for research assistance. Barry Adler, Douglas Baird, Martin Bienenstock,Bill Bratton, David Carlson, Mihir Desai, Jesse Fried, Howell Jackson, Lynn LoPucki, StephenLubben, Ronald Mann, Harvey Miller, Ed Morrison, John Pottow, Eric Rasmussen, Robert Rasmus-sen, Alan Schwartz, George Triantis, Ronald Trost, Alvin Warren, Elizabeth Warren, threebankruptcy judges, and participants in faculty workshops at Harvard Law School, the University ofMichigan Law School, and Notre Dame Law School were generous with their comments. We thankHarvard Law School, the Kauffman Foundation, and University of Pennsylvania Law School forresearch support.

Michigan Law Review

D. The Emergency-How Immediate? ................................... 749IV. WAS CHRYSLER REORGANIZED OR SOLD? ............................... 751

A. The Case That Chrysler Was Reorganized, Not Sold ........ 7511. Old Chrysler's Mandates to New Chrysler ................. 7512. The Before-and-After Resemblance ............................ 7533. A Rule of Thumb to Sort Legitimate § 363 Sales from

§ 1129 Reorganizations .............................................. 755B. Consequences of a Nonsale: Valuation Inconsistencies .... 756C. Could the Treasury Have Acted Any Differently? .............. 760

V. Chrysler AS CHAPTER 11 TEMPLATE? ............... . . .. . . .. . . .. . . . .. . . . .. . 761A. Replication Without Government Funding ........................ 763B . Recom m endations .............................................................. 766

V I. THE B IG PICTURE ..................................................................... 767C ON CLU SION ......................................................................................... 770

INTRODUCTION

The Chrysler Chapter 11 proceeding went blindingly fast. One of thelarger American industrial operations entered Chapter 11 and exited forty-two days later. Clearly this speed was propelled by the government's cashinfusion of $15 billion on noncommercial terms into a company whose as-sets were valued at only $2 billion.' The influx came at a time when theAmerican economy was sinking, financial institutions were failing, and thegovernment feared that a collapse of the auto industry would have graveconsequences for the rest of the economy. Never before had the governmentused bankruptcy to bail out a major industrial corporation. As a matter ofbankruptcy technique, the rapidity of the Chrysler Chapter 11 was a tour deforce.

The economic policy and political background is worthy of its ownanalysis, but we note that level of policy and politics only in passing, whenthey interact with the Bankruptcy Code. Briefly, Chrysler was a weak pro-ducer, making cars that had limited consumer acceptance, in an industrysuffering from substantial domestic and worldwide overcapacity. Industriesfacing such pressure normally need to shrink, and their weakest producers,like Chrysler, are the first candidates for shrinkage.

We focus primarily on the technical structure of the Chrysler bankruptcyunder the Code. Did the bankruptcy introduce, or did it magnify, tactics,procedures, and doctrines that would facilitate sound, fast bankruptcies inthe future? Or did the Chrysler reorganization reveal defects latent in theChapter 11 mechanisms? Could the rapid results be obtained in the future

1. "The Governmental Entities loaned the Debtors at least $4 billion prepetition, and nearly$5 billion postpetition, all of which is a secured debt obligation of the Debtors." In re Chrysler LLC(Chrysler 1), 405 BR. 84, 108 (Bankr. S.D.N.Y. 2009), aff'd, 576 F.3d 108 (2d Cir. 2009), vacatedby 78 U.S.L.W. 3359 (Dec. 14, 2009). In addition, governmental entities provided $6 billion insecured loans to New Chrysler. Id. at 92. Sticklers for form might state that Chrysler did not exit in42 days, but is still, as of this writing, in Chapter 11. In form, that is correct, but in substance the caroperations left Chapter II via the sale, 42 days after filing.

[Vol. 108:727

Assessing the Chrysler Bankruptcy

only if the government is willing to flood the bankrupt firm with cash onsubsidy-type terms? Was the process sufficiently innovative as to be new?And, if new, is it desirable?

Our overall conclusions are not favorable to the process, results, andportents for the future. The Chrysler bankruptcy process used undesirablemechanisms that federal courts and Congress struggled for decades to sup-press at the end of the nineteenth and first half of the twentieth centuries,ultimately successfully. If the mechanisms are not firmly rejected (or forgot-ten), then future reorganizations in Chapter 11 will be at risk, in ways thatcould affect capital markets. Although the government's presence com-manded judicial deference, its presence is not needed for the defectiveprocedures to be part of future reorganizations. Every reorganization inChapter 11 can use the same, defective process.

Two creditor groups were sharply cut off in the Chrysler reorganization.Products-liability claimants with claims for damage caused by Chrysler'scars on the road were barred in the reorganization from suing the reorgan-ized Chrysler.2 And credit markets reacted negatively to the Chryslerreorganization process and results. George J. Schultze, a manager of a hedgefund holding Chrysler debt, said "one reason we went into it was becausewe expected normal laws to be upheld, normal bankruptcy laws that weredeveloped and refined over decades, and we didn't expect a change in thepriority scheme to be thrust upon us."3 He warned:

People who make loans to companies in corporate America will thinktwice about secured loans due to the risk that junior creditors might leapfrog them if things don't work out. It puts a cloud on capital markets andthe riskiest companies that need capital will no longer be able to get capi-tal .4

Warren Buffett worried in the midst of the reorganization that there wouldbe "a whole lot of consequences" if the government's Chrysler planemerged as planned, which it did.5 If priorities are tossed aside, as he im-plied they were, "that's going to disrupt lending practices in the future. Ifwe want to encourage lending in this country," Buffett added, "we don'twant to say to somebody who lends and gets a secured position that thatsecured position doesn't mean anything. 7

2. In the face of continuing complaints after the Chrysler reorganization was completed,Chrysler said it would accept claims for future products-liability lawsuits, but held fast to walkingaway from lawsuits in place at the time of the reorganization. Chrysler Revises Stance on Liability,N.Y TIMES, Aug. 28, 2009, at B2.

3. Tom Hals, Chrysler secured creditor tofight "illegal" plan, REUTERS, May 7, 2009.

4. Id.

5. Lou Whiteman, Buffett warns of Chrysler cramdown ramifications, THEDEAL.COM, May5, 2009, http://www.thedeal.comdealscape/2009/05/buffett-wams-of-chrysler-cram.php.

6. Id.

7. Id. These were not isolated comments in capital markets. Cf Nicole Bullock, Painfullessons for lenders in Chrysler debacle, FIN. TIMES, MAY 7, 2009. Bullock interviewed the financialplayers:

March 20 10]

Michigan Law Review

Were they right? Were priorities violated?Perhaps priorities were breached, perhaps not. The most troubling Code-

based aspect of the Chrysler bankruptcy is that this is difficult, perhaps im-possible, to know from the structure of the reorganization. Yet obtaining thatknowledge is one of the core goals of Chapter 11 in practice. Chryslerbreached appropriate bankruptcy practice in ways that made opaque bothChrysler's value in bankruptcy and the plan's allocation to the company'sprebankruptcy creditors. The requirement in § 1129(a)(8) that each class ofcreditors consent or receive full payment wasn't used. A market test wasn'tused. There was no judicial valuation of the firm. Chrysler went through themotions of selling its principal assets to a newly formed entity controlled byits preexisting principal creditors, a process that has been historically sus-pect in bankruptcy.

Stunningly, the bankruptcy court did not analyze the § 1129 issues. In-deed, that section-the core of the modem Bankruptcy Code, outlining theconditions the judge must find prior to confirming a plan of reorganiza-tion-is not mentioned once in the bankruptcy court's opinion. If thepseudo-sale was a de facto plan of reorganization because it did so muchmore than simply sell assets for cash, then it was incumbent on the bank-ruptcy process to assess the deal's terms for consistency with § 1129. If acapable bankruptcy judge does not see fit to mention § 1129 in a sale thatdetermines many reorganization outcomes normally made in Chapter 11under § 1129, something peculiar is happening. The most obvious hypothe-sis is that one could not mention it, if one feared that one were witnessing areorganization that could not comply with § 1129. On appeal, the Second

"Given that so much of total borrowing across all asset classes is first lien in nature, thedamage that would occur to the economy as a result of higher first lien borrowing costs result-ing from lenders requiring a higher return to compensate them for an unknown interpretationof claim priorities could be substantial," says Curtis Arledge, co-head of US fixed income atBlackRock, Inc.

"It is particularly important at this stage of the distressed cycle for lenders to have confidencein pre-existing contracts and mles. We are entering a period of record corporate defaults andthe need for bankruptcy financing and financing for distressed companies will only continue togrow," says Greg Peters, global head of credit research at Morgan Stanley.

"People are pretty comfortable with the bankruptcy rules. What they are trying to do in theChrysler situation is unprecedented," says Jeff Manning, a managing director specialising inbankruptcy and restructuring at Trenwith Securities, the investment bank. "This isn't the waythe game is supposed to be played."

•.. Steve Persky, managing director of Dalton Investors, a Los-Angeles-based hedge fund thatspecialises in distressed debt[,] ... [says] "Now there is a new risk: government interventionrisk[.]"... And it is very hard to hedge."

[Vol. 108:727

Assessing the Chrysler Bankruptcy

Circuit, rather than signaling concern, affirmed the bankruptcy court deci-sion and adopted its analysis."

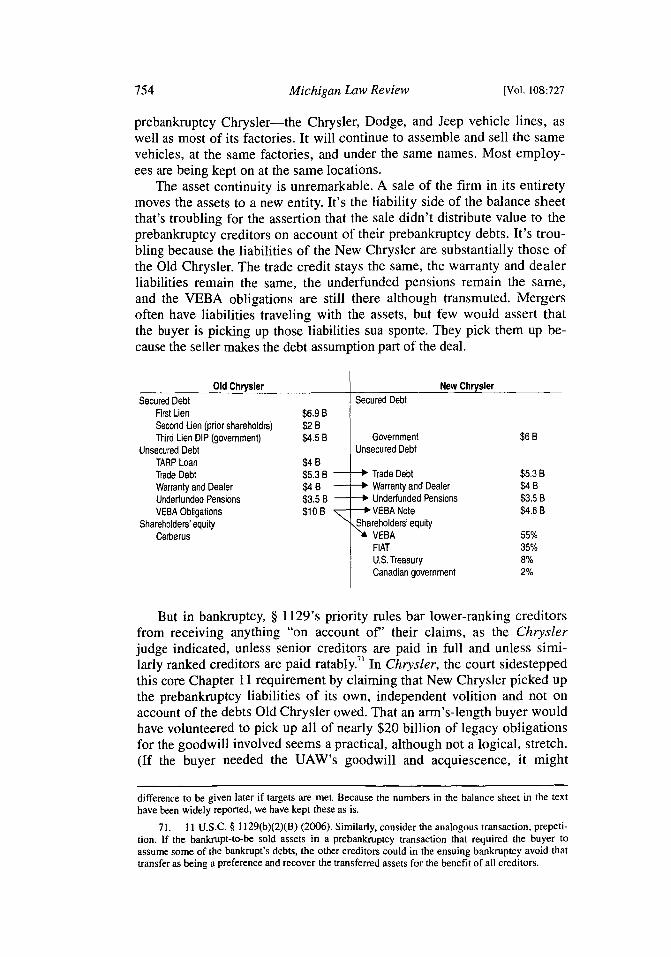

Worse, the Chrysler bankruptcy in core respects does not look like asimple sale, but a reorganization. The new Chrysler balance sheet re-markably resembles the old one, with only a couple of priorities, involvinglarge dollar amounts, sharply adjusted. Courts will need to develop rulesof thumb to distinguish true § 363 sales from bogus ones that are reallyreorganizations. We take a step toward doing so.

We can hope that the breach of proper practice will be confined toChrysler. But the structure of the deal is not Chrysler-specific. Not onlydid the subsequent General Motors opinion rely heavily on Chrysler,9 butother courts and plan proponents will inevitably cite Chrysler as prece-dent)0 Some already have.

The Chrysler process may have revealed conceptual fault lines in thedeeper structure of Chapter 11: the government's presence as a noncom-mercial lender isn't needed, as a matter of Code structure, for interestedplayers to use the Chrysler mechanism. Any coalition of creditors andmanagers can use the § 363 sale in the same way, if they can persuade ajudge to approve their proposed fictional sale.

Hence, Chrysler could become the template for the next generation oflarge scale corporate reorganizations. Even before the Chrysler bank-ruptcy, Chapter 11 cases were increasingly resolved through § 363 salesthat did not always carefully consider § 1129 priority issues. But by bless-ing an artificial sale that carried over and restructured the bulk ofChrysler's creditors' claims, the Second Circuit's Chrysler opinion radi-cally expands this strategy's potential scope. If it becomes the pattern,Chrysler could displace the traditional Chapter 11 process, potentially af-fecting both lending markets and vulnerable nonfinancial creditorsadversely.

Its impact will need to be confined. We can hope that the bankruptcybench and bar come to a consensus view of Chrysler as a one-off, suigeneris bankruptcy, and we seek here to start us toward that consensus.But because the Chrysler techniques resonate enough with prior practice,and can be seen as extreme extensions of that prior practice, effort will berequired to reach that consensus.

8. Ind. State Police Pension Trust v. Chrysler LLC (In re Chrysler LLC) (Chrysler II), 576F.3d 108, 118 (2d Cir. 2009) (rejecting concerns about the failure to comply with Chapter I I's pro-tections with the statement that the "bankruptcy court's findings constitute an adequate rebuttal"),vacated by 78 U.S.L.W. 3359 (Dec. 14, 2009). How much force is left in the Second Circuit's judg-ment after the Supreme Court vacated it is yet to be determined. See infra text accompanying notes95-98.

9. In re Gen. Motors Corp., 407 B.R. 463,497-98 (Bankr. S.D.N.Y. 2009).

10. See Ashby Jones & Mike Spector, Creditors Cry Foul at Chrysler Precedent, WALL ST.J., June 13, 2009, at B 1 ("It's going to happen," [Peter Kaufman, president of investment bank Gor-dian Group LLC, said, questioning the sui generis view]. "The excuse that [the auto cases] are,special circumstances,' I'm sure [is] right until the next time it's a 'special circumstance."').

March 20 10]

Michigan Law Review

A roadmap for the Article: in Part I, we outline the structure of theChrysler bankruptcy, which was effectuated as a § 363 sale under theCode's authorization to bankruptcy courts to sell all or part of a firm, uponthe bankrupt's motion, without the creditors' consent. We analyze the besttheoretical structure for how § 363 should interact with the rest of theCode, particularly § 1129. Section 363 has the potential to do muchgood-by repositioning companies quickly in the merger market-and thepotential to do much damage, by running roughshod over the rest of thewell-honed Chapter 11 structure.

We then in Part II examine the appellate cases, which largely conformto the theoretical structure for § 363 sales that we first outline in Part I. Tosubstitute for the usual creditors' protections of § 1129, courts had devel-oped makeshift safeguards in § 363 sales, requiring adequate valuation,consent, or a genuine market test. In Part III, we show that the Chryslersale failed to use such checks properly. In Part IV, we demonstrate thatwhile cast as a sale, the Chrysler transaction had so many presale creditorsreemerging on the other side of the transfer of its assets to the newly-formed firm that the transaction can, and should, better be characterized asnot being a sale to a third party, but as an ordinary reorganization, but onenot done in accordance with best Chapter 11 practice. We suggest a roughrule of thumb for courts to sort presumed reorganizations (which need toproceed under alternative Code provisions) from plausible § 363 sales.

Then, after briefly exploring in Part IV how the government mighthave structured its investment in Chrysler differently and still reached itspolicy goals without distorting bankruptcy practice, we put Chrysler intobroader perspective. We speculate in Part V about Chrysler's implicationsfor future bankruptcy practice and remark in Part VI on the similarity ofChrysler's reorganization to nineteenth century reorganizations via theequity receivership. On the positive side, the Chrysler reorganization han-dled a practical business problem via a sale format as did the equityreceivership's reconstruction of the American railroad system. On thenegative side, the Chrysler reorganization reintroduced the equity receiv-ership's most objectionable attributes, particularly its casual regard forpriority-attributes that the reorganization machinery regularly rejectedfor more than a century, until now. Before concluding, we speculate onbusiness features that could push toward more Chrysler-like bankruptciesin the future: if major creditor groups increasingly supply not only funds,but also critical goods and services for the debtor's business, Chryslercould represent a new direction, one for which Chapter 11 as now consti-tuted is not fully prepared.

The damage will need to be undone. Other courts can, and should, re-quire proper safeguards for sales that substitute for Chapter 11. We outlinewhat those need to be. Chrysler needs to be seen as an anomaly, but as oftoday there's risk that it will not be. Courts need to change direction tohandle § 363 sales better than they were handled in Chrysler or Congressneeds to act.

[Vol. 108:727

Assessing the Chrysler Bankruptcy

I. CHRYSLER'S § 363 PROBLEM

A. The Deal Structure

The deal's basic structure is straightforward to summarize. Prebank-ruptcy, Chrysler was a private firm, owned by Cerberus, a large privateequity fund. As of the bankruptcy, its two largest creditors were securedcreditors owed $6.9 billion and an unsecured employee benefit plan, owed$10 billion." It also owed trade creditors $5.3 billion, and it had warrantyand dealer obligations of several billion dollars. 2

The government created and funded a shell company that, through a§ 363 sale from Chrysler, bought substantially all of Chrysler's assets for$2 billion, giving the secured creditors a return of 29 cents on the dollar.FIAT was brought in to manage the new firm and was given a slice of thenew company's stock. New Chrysler (formally: New CarCo AcquisitionLLC) then assumed the old company's debts to the retirees, most dealers,and trade creditors. The $10 billion of unsecured claims owed to the retir-ees' benefits plan were replaced with a new $4.6 billion note as well as 55percent of the new company's stock.

Priority seemed violated. Unsecured retiree claims were promised wellover 50 cents on the dollar, along with control of the New Chrysler, andunsecured trade creditors were promised full payment. The secured credi-tors, however, were getting 29 cents on the dollar, and future products-liability claims relating to Chrysler cars already on the road would receivenothing at all under the plan, as the pseudo-sale made no provision forthem. Claims could be brought against only Old Chrysler, which was ex-pected to soon have no assets.

In an ordinary bankruptcy, the structure would be prima facie im-proper. The secured creditor would get the value of its security-hereperhaps $2 billion--and its unsecured deficiency claim of nearly $5 billionwould be paid proportionately with the other unsecured creditors. But thiswas not an ordinary bankruptcy, because the government was lending onnoncommercial, policy-oriented terms. The United States Treasury and thegovernment of Canada had lent roughly $4 billion to Chrysler prior tobankruptcy, and then agreed to provide $5 billion to fund the bankruptcy,and another $6 billion in exit financing. Some of the excess promised tothe retiree trust was surely spilling over from the government's conces-sionary lending. The difficulty-the core Chrysler bankruptcy problem--is that the bankruptcy process failed to reveal how much. Its structure wasconsistent with several sharply differing real results. Maybe the retirees'payout came solely from the government's new money as funneled

11. Affidavit of Ronald E. Kolka in Support of First Day Pleadings 27, 39, In re ChryslerLLC (Chrysler 1), 405 B.R. 84 (S.D.N.Y. 2009) (No. 09 B 50002 (AJG)), 2009 WL 1266134 [here-inafter "Kolka Affidavit"].

12. Id. (H 30,35.

13. Chrysler 1, 405 B.R. at 92, 108.

March 2010]

Michigan Law Review

through New Chrysler, maybe some of it came from the prior securedcreditors, maybe the deal created unusually lucrative synergies, or maybethe government even subsidized the secured creditors as well. It's impos-sible to tell because the process was opaque, with none of the standardmechanisms used to validate the process: a judicial valuation, an arm's-length bargained-for settlement, or a genuine market test.

Simply stated, although the secured creditors received $2 billion ontheir $6.9 billion claim, there is nothing in the structure of Chrysler'sbankruptcy process inconsistent with the proper number for the securedbeing not $2 billion, but $5 billion, or $1 billion. Or zero. Whoever wonand whoever lost, the process was a defective one, because it was oneunlikely to reveal whether the Chrysler bankruptcy adhered to basic priori-ties.

B. The § 363 vs. § 1129 Problem: Concept

Section 363 of the Bankruptcy Code authorizes the debtor to sell assetsout of the ordinary course of business at any point in the bankruptcy case,upon obtaining the bankruptcy court's approval. The section is short, withno conditions other than that there be a hearing. But § 1129-arguably thecore of Chapter 11-requires that, before the court approves a plan of re-organization, it ascertain that the plan complies with the usual priorities,absent creditor consent to a plan deviating from those priorities. 14

In a simple sale, these two sections do not conflict. The debtor sells,say, a subsidiary that the firm cannot manage well and that's deterioratingin value. The asset leaves the debtor's estate, but cash comes back in. Thecash for the sale is then available to all of the prebankruptcy creditors,who can thereafter litigate, negotiate, and jockey among themselves overpriority, over whether any of them are entitled to receive interest pay-ments, over whether any received preferential transfers prior to bankruptcythat must be returned, whether one should be equitably subordinated toanother, and so on.

A complex sale, however, can determine priorities and terms that theCode is structured to determine under § 1129, and is not structured to de-termine under § 363. For example, consider the possibility that in additionto the sale, some prebankruptcy creditors come over to the purchasingfirm, but others do not. The purchaser buys the debtor's principal operat-ing subsidiary, say, and agrees to pay one of the subsidiary's creditors in

14. Section 1129 priorities contemplate that secured creditors obtain the value of their secu-rity, that unsecured creditors be paid before stockholders, that intercreditor contractual priorities berespected, and that creditors at the same level obtain the same proportion of their claim paid. Credi-tors can consent to deviations from priority, via a vote of the affected creditor class. An individualcreditor can sometimes upset a class-approved deal via § I 129(a)(7), which requires that any non-consenting creditor receive as much under the plan as the creditor would get if the debtor wereliquidated under Chapter 7. For those unfamiliar with the basic priority structure of § 1129, it isoutlined in bankruptcy casebooks and treatises. See, e.g., MARK J. ROE, BANKRUPTCY AND CORPO-RATE REORGANIZATION 87-117 (2d ed. 2007); ELIZABETH WARREN & JAY LAWRENCE WESTBROOK,

THE LAW OF DEBTORS AND CREDITORS 396-402 (6th ed. 2009).

[Vol. 108:727

Assessing the Chrysler Bankruptcy

full, but not pay its other creditors anything. Some of the subsidiary'sdealers are terminated, left behind, and have damage claims left unpaid bythe old company, but others move over to the purchaser and remain in op-eration. The purchaser agrees to assume some of the subsidiary's ongoingwarranty claims, but not its current collection of lawsuits or its liability forpreviously sold products that turn out to be defective. Or, the purchaserearmarks some of the consideration used in the sale as being usable byonly a particular set of previous creditors of the subsidiary.

All these sales terms would then determine core aspects that wouldnormally be handled under § 1129, with disclosure, voting under§ 1129(a)(8), and if voting fails, via a judicial cram-down under§ 1129(b).15 If the restructuring is done via § 363, courts need to resolvehow to reconcile such sales with § 1129.

The simplest reconciliation would be to bar such sales that determinecore Chapter 11 terms, on the theory that § 363 cannot be allowed to eatup the rest of Chapter 11. Section 363 would be limited to simple sales ofassets for cash. Congress intended, in this view, that the Chapter 11 pro-ceeding end with the bankruptcy judge going through the long, precise§ 1129 checklist for compliance, typically including full disclosure of thecompany's business operations and the impact of the plan on the creditorgroups, with creditors thereafter voting and the judge evaluating the plan.

But that kind of formalistic reconciliation isn't good enough for tworeasons, one theoretical and one practical. The theoretical one is that everysale affects the § 1129 bargaining. Behind the § 1129(a)(8) process is the"what if' alternative-what if the parties cannot bargain to a settlement? Ifthey cannot settle, the judge can cram the plan down, but that cram-downultimately needs a judicial valuation of the firm and its claims, a processthat is usually thought to be highly inaccurate. By reducing the valuationuncertainty, a sale affects the reorganization, but beneficially if the salevalue is proper.1

6

The second, practical problem with rejecting all sub rosa plans as notbeing good enough is quite important: a sale is too attractive a businessdisposition for many bankrupts to give up. Bankrupt companies come dis-proportionately from declining industries that should shrink. An excellentway for a declining industry to consolidate capacity is via merger, so thatthe strongest parts of each partner can be molded together. And bankruptfirms, if poorly managed, can be repositioned to be managed by a bettermanagerial team. If a few terms have to be handled in the § 363 sale that

15. The judge can cram the plan down on objecting creditors by finding that the objectingcreditors obtained their due under a § 1129 plan, thereby allowing the judge to confirm the plan,notwithstanding the creditors' dissent.

16. See, e.g., Walter J. Blum, The Law and Language of Corporate Reorganization, 17 U.CHI. L. REV. 565, 572 (1950) ("[Reorganization value] is a fictional value .... It is set by the esti-mates of persons who are not standing back of them with a willingness to invest their own funds.");Kerry O'Rourke, Valuation Uncertainty in Chapter 11 Reorganizations, 2005 COLUM. Bus. L. REv.403, 427 (2005); Mark J. Roe, Bankruptcy and Debt: A New Model for Corporate Reorganization,83 COLUM. L. REV. 527 (1983).

March 2010]

Michigan Law Review

would ordinarily be handled under § 1129, then courts, and bankruptcydoctrine, should find a way to accommodate the quick sale, but withoutscuttling the entire § 1129 structure of protections and priorities. One po-tential negative fallout from the Chrysler bankruptcy is that the eventualpush back to its casualness in handling priority could become an attack on§ 363 in its entirety, as opposed to its specific implementation. If saleswere sharply curtailed, instead of conditioned and properly structured,then bankruptcy would be set back. As a matter of bankruptcy policy, weshould want sales that reposition the bankrupt's operations quickly andwell. We do not want those sales to strongly violate priority expectations.

But fast sales with some priority determinations can be reconciled. Thecourt can identify the offending feature of the § 363 sale and ascertainwhether it's small and whether the priority determination would havepassed muster under § 1129. For example, if a single creditor objects tothe sale, because some prior creditors are going over to the new entity, thecourt can determine that the creditor received liquidation value(§ 1129(a)(7)) and that the creditor class to which the dissenter belongsproperly consented to any deviation in priority in allocation of the goingconcern value (§ 1129(a)(8)). If a class consented overall but a dissenterwould clearly be getting liquidation value, then the court could determinethat even though the sale had aspects of a sub rosa plan, those features ifdone above-board would still have permitted plan confirmation under§ 1129.

II. THE PRE-CHRYSLER APPELLATE CASES

Overall, the prior appellate cases conformed to the concepts laid outabove. Bankruptcy law, based on leading 1980s decisions in the Secondand Fifth Circuits, was largely in good shape doctrinally before Chrysler.These decisions established that there must be an appropriate businessjustification for the sale, as exemplified by a business emergency or a de-teriorating business situation best handled by a sale; the sale cannot be asub rosa plan of reorganization that de facto determines core terms moreproperly determined under § 1129 via its creditor protections; and if theplan does determine core § 1129 features, it can do so only if the courtfashions a makeshift safeguard-a substitute that's overall consistent withthe mandates of § 1129.

A. Reconciling § 363 Sales with § 1129 Protections

Prior to the modern Bankruptcy Code, asset sales were allowed onlywhen the asset was wasting away. In In re Lionel Corp., the Second Cir-cuit freed Code sales from that restriction, but firmly stated when rejectingthe proposed sale in the case that, although "the new Bankruptcy Code nolonger requires such strict limitations on a bankruptcy judge's authority toorder disposition of the estate's property ... it does not go so far as to

[Vol. 108:727

Assessing the Chrysler Bankruptcy

eliminate all constraints on that judge's discretion."" The court establishedthe modem test for approving a § 363 sale: "The rule we adopt requiresthat a judge determining a § 363(b) application expressly find from theevidence presented before him at the hearing a good business reason togrant such an application."'8 And, importantly for the Chrysler reorganiza-tion, the court in Lionel also stated that:

[Ilt is easy to sympathize with the desire of a bankruptcy court to expe-dite bankruptcy reorganization proceedings for they are frequentlyprotracted. "The need for expedition, however, is not a justification forabandoning proper standards."

In fashioning its findings, a bankruptcy judge must not blindly follow thehue and cry of the most vocal special interest groups; rather, he shouldconsider all salient factors pertaining to the proceeding and, accordingly,act to further the diverse interests of the debtor, creditors and equityholders, alike.'9

While the Lionel decision evinces skepticism toward the § 363 sale, intime courts became more comfortable with sales, partly because theymake so much business sense for a failing business and partly because thegeneral merger market deepened and thickened in the 1980s. Such salesbecame frequent in Chapter 11.20

By relaxing the standard for a § 363 sale, the courts introduced the riskthat § 363 could be used to circumvent the carefully crafted Chapter 11protections emanating from § 1129. The court addressed this issue in In reBraniff Airways, stating that "[t]he debtor and the Bankruptcy Courtshould not be able to short circuit the requirements of Chapter 11 for con-firmation of a reorganization plan by establishing the terms of the plan subrosa in connection with the sale of assets."'"

The Braniff court concluded that the proposed sale before it-whichwould have distributed travel coupons, promissory notes, and a share ofprofits in specified amounts to different groups of creditors-was a defacto plan of reorganization, explaining that "[w]ere this transaction ap-proved, and considering the properties proposed to be transferred, little

17. Comm. of Equity Sec. Holders v. Lionel Corp. (In re Lionel Corp.), 722 F.2d 1063, 1069(2d Cir. 1983).

18. Id. at 1071.

19. Id. (quoting Protective Comm. for Indep. Stockholders of TMT Trailer Ferry, Inc. v.Anderson, 390 U.S. 414, 450 (1968)).

20. See Douglas G. Baird & Robert K. Rasmussen, Chapter 11 at Twilight, 56 STAN. L. REV.673 (2003); Douglas G. Baird, The New Face of Chapter 11, 12 AM. BANKR. INST. L. REV. 69, 73(2004) ("[S]ales are now part of the warp and woof of [C]hapter 11 practice. Of the 10 largest[C]hapter I Is of 2002, eight used the bankruptcy court as a way of selling their assets to the highestbidder, whether piecemeal or as a going concern."); cf Lynn M. LoPucki & Joseph W. Doherty,Bankruptcy Fire Sales, 106 MSCH. L. REV. 1, 24-25 (2007) (sharply criticizing sales).

21. Pension Benefit Guar. Corp. v. Braniff Airways, Inc. (In re Braniff Airways, Inc.), 700F.2d 935, 940 (5th Cir. 1983).

March 2010]

Michigan Law Review

would remain save fixed based equipment and little prospect or occasionfor further reorganization. These considerations reinforce our view thatthis is in fact a reorganization."22 Courts continue to reaffirm and interpret• 21

the Braniff standard•.In 2007, the Second Circuit, in In re Iridium Operating LLC, affirmed

the same standard, barring a bankruptcy transaction because of its similar-ity to sale cases "if [the sale] would amount to a sub rosa plan ofreorganization ... based on a fear that a [bankrupt] will enter into transac-tions that will, in effect, 'short circuit the requirements of [C]hapter 11 forconfirmation of a reorganization plan."' 24 Equally importantly, the SecondCircuit emphasized the importance of ascertaining compliance with thestatute's priority requirements:

[W]hether a particular settlement's distribution scheme complies withthe Code's priority scheme must be the most important factor for thebankruptcy court to consider when determining whether a settlement is"fair and equitable".... The court must be certain that parties to a set-tlement have not employed a settlement as a means to avoid the priority

21strictures of the Bankruptcy Code.

Although courts regularly indicate the impermissibility of sub rosaplans, they do not bar all plans that make § 1129 determinations in the§ 363 sale. The sale may go through, but only if an appropriate, even ifmakeshift, protection is used to substitute for the forgone conditions toplan confirmation. The court states in In re Continental Air Lines:

[W]e hold that when an objector to a proposed transaction under§ 363(b) claims that it is being denied certain protection because ap-proval is sought pursuant to § 363(b) instead of as part of areorganization plan, the objector must specify exactly what protection isbeing denied. If the court concludes that there has in actuality been such

22. Id.

23. Clyde Bergemann, Inc. v. Babcock & Wilcox Co. (In re Babcock & Wilcox Co.), 250F.3d 955, 960 (5th Cir. 2001) ("Braniff stands ... for the proposition that the provisions of § 363permitting a trustee to use, sell, or lease the assets do not allow a debtor to gut the bankruptcy estatebefore reorganization or to change the fundamental nature of the estate's assets in such a way thatlimits a future reorganization plan."); see also Craig A. Sloane, The Sub Rosa Plan of Reorganiza-tion: Side-stepping Creditor Protections in Chapter 11, 16 BANKR. DEV. J. 37 (1999) (surveyingcases through 1999).

24. Motorola, Inc. v. Official Comm. of Unsecured Creditors (In re Iridium Operating LLC),478 F.3d 452, 466 (2d Cir. 2007) (quoting In re BraniffAirways, 700 F.2d at 940). Two years earlier,the Southern District of New York rejected a sale, stating that "it is well established that section363(b) is not to be utilized as a means of avoiding Chapter I l's plan confirmation procedures.Where it is clear that the terms of a section 363(b) sale would preempt or dictate the terms of aChapter 11 sale, the proposed sale is beyond the scope of section 363(b) and should not be approvedunder that section." Contrarian Funds, LLC v. Westpoint Stevens, Inc. (In re Westpoint Stevens,Inc.), 333 B.R. 30, 52 (S.D.N.Y. 2005).

25. In re Iridium, 478 F.3d at 464.

[Vol. 108:727

Assessing the Chrysler Bankruptcy

a denial, it may then consider fashioning appropriate protective meas-26

ures modeled on those which would attend a reorganization plan.

A commentator summarizes the cases as follows:

[A] debtor [must] establish four elements: (1) a sound business purposejustifying the sale of assets outside the ordinary course of business, (2)accurate and reasonable notice provided to interested persons, (3) a fairand reasonable price obtained by the debtor, and (4) a good faith salewithout offering lucrative deals to insiders."

Keep in mind the cautionary indication about "lucrative deals to insiders,"because the Chrysler sale could be interpreted as a lucrative deal to non-standard insiders (the standard ones being management and controllingstockholders; the nonstandard ones being creditors who de facto controlledChrysler), one that the judge would ordinarily want to examine carefully.

When a firm sells nearly all of its assets to a shell company that as-sumes many but not all of its prior liabilities, we are not seeing a valid salesolely to benefit creditors as a group. Instead, the sale is a de facto reor-ganization plan, which courts had previously regularly rejected asrequiring makeshift remedies to ensure that the § 1129 standards to con-firmation were not violated.

B. Makeshift Remedies that Validate Priority

Three makeshift safeguards can reconcile a § 363 sale with core pro-tections of § 1129: judicial valuation, creditor consent, and a contestedauction.

1. Judicial Valuation and Priority Determination

The most straightforward, but most cumbersome, makeshift remedywould be for the bankruptcy court to hear valuation evidence, ascertainpriorities, and determine whether the plan conformed to what would havebeen distributed had the plan gone through § 1129(b). Valuation, though,is not a favored process, partly because judicial valuation is itself oftenseen to be inaccurate and slow" and, accordingly, courts rarely rely onvaluation alone.

26. Institutional Creditors of Cont'l Air Lines, Inc. v. Cont'l Air Lines, Inc. (In re Cont'l AirLines, Inc.), 780 F.2d 1223, 1228 (5th Cir. 1986) (emphasis added); cf In re Crowthers McCallPattern. Inc., 114 B.R. 877, 885 (Bankr. S.D.N.Y. 1990).

27. Scott D. Cousins, Chapter II Asset Sales, 27 DEL. J. CORP. L. 835, 839-40 (2002). Mul-tiple circuits have explicitly required that these conditions be satisfied prior to a § 363 sale. Id.

28. See H.R. REP. No. 95-595, at 227 (1977), reprinted in 1978 U.S.C.C.A.N. 5963, 6186-87; H.R. Doc. No. 93-137, pt. 1, at 256 (1973).

March 20101

Michigan Law Review

2. Class Consent

Section 1129(a)(8) allows plans to deviate from absolute priority, if theimpaired class consents, by a vote of two-thirds in dollar amount and morethan one-half in the number of claims. Few modem reorganizations reacha bargaining impasse-eventually the classes usually make a deal. Theconcept behind the consent procedure is that value may be uncertain andparties often compromise their claims to get a deal done so that thebusiness can move on. The court can look to whether the creditors con-sented to the terms of the plan in a way that would pass muster under§ 1129.29

But that consent must be valid and in good faith, i.e., not distorted bysevere conflicts of interest, as § 1126(e) states that "the court may desig-nate any entity whose acceptance or rejection of such plan was not in goodfaith."3° That lack of good faith exists if a claim holder is acting "in aid ofan interest other than an interest as a creditor."3'

3. A Market Test

The main safeguard in most § 363 sales comes from the bidding rulesthat facilitate an auction, or some lesser market test of the sale. In 2006,the Southern District of New York posted general guidelines for bank-ruptcy sales. 32 These guidelines-which require that bidders be givenaccess to relevant information, that the debtor market the property ade-quately and show that the price received will be "the highest or best underthe circumstances," and that the insider status of any buyer be disclosed-appear to be consistent with the practice in other courts as well.33

Courts usually agree to a sale, but often stretch out the auction's timeframe, during which they remove problematic provisions from the debtor'sproposed bidding procedures and give the creditors' committee an oppor-tunity to investigate and to object to any problems with the proposed sale.In the Lifestream Technologies bankruptcy, for instance, the parties re-quested that the § 363 sale be conducted shortly after the case was firstfiled. The judge refused the request, which induced the parties to renegoti-

29. See David Arthur Skeel, Jr., The Nature and Effect of Corporate Voting in Chapter 11Reorganization Cases, 78 VA. L. REV. 461, 497-501 (1992) (recommending that such consent berequired).

30. 11 U.S.C. § 1126(e) (2006).

31. In re Allegheny Int'l, Inc., 118 B.R. 282, 289 (Bankr. W.D. Pa. 1990) (quoting In re P-RHolding Corp., 147 F.2d 895, 897 (2d Cir. 1945)); see also In re Dune Deck Owners Corp., 175B.R. 839, 845 (Bankr. S.D.N.Y 1995); cf In re Iridium Operating LLC, 478 F.3d 452, 465 (2d Cir.2007) (emphasizing that only a single creditor objected).

32. In re Adoption of Guidelines for the Conduct of Asset Sales, General Order M-331(Bankr. S.D.N.Y. Sept. 5, 2006), available at http://www.nysb.uscourts.gov/orders/m331 .pdf.

33. Id. at 7.

[Vol. 108:727

Assessing the Chrysler Bankruptcy

34ate the terms of the sale. As the Supreme Court said in an analogous set-ting in 203 North LaSalle: "Under a plan granting an exclusive right,making no provision for competing bids or competing plans, any determi-nation that the price was top dollar would necessarily be made by a judgein bankruptcy court, whereas the best way to determine value is exposureto a market."35

III. THE CHRYSLER SALE

The Chrysler sale violated all of these principles. The § 363 sale de-termined the core of the reorganization, but without adequately valuing thefirm via § 1129(b), without adequately structuring a § 1129(a)(8) bargain,and without adequately market testing the sale itself. Although the bank-ruptcy court emphasized an emergency quality to the need to act quickly,stating that "if a sale has not closed by June 15th, Fiat could withdraw itscommitment,"3 there was no immediate emergency. Chrysler's businessposture in early June did not give the court an unlimited time to reorgan-ize, but it gave the court weeks, not just a few days, to sort out priorities,even if in a makeshift way.

That core terms to § 1129 were determined should not be in doubt, al-though neither the bankruptcy court nor the Second Circuit indicated thatthey grasped this basic fact of the Chrysler reorganization and, hence,failed to fully analyze its import. The sale terms effectively determined theconsideration to Chrysler's secured creditors and its ongoing products-liability claims. It promised the retirees' VEBA a payment of $4.6 billionand made them substantial owners of the New Chrysler.37 The sale didmuch more than just move Chrysler's assets to a new owner for cash. Be-cause it also decided which creditors would get paid and how much they'dbe paid, the Chrysler sale was a sub rosa reorganization plan. The onlyserious question is whether the makeshift procedures the judge used ade-quately substituted for a real § 1129 confirmation. In most cases theanswer is clearly no, because no substitute was attempted. For a few fea-tures, a partial substitute was employed-such as a market test-but wasinadequate.

34. See, e.g., Debtor's Supp. Brief in Support of Motion for Order Pursuant to Section 363 ofthe Bankr. Code, In re Lifestream Techs., Inc. (Bankr. D. Nev. Dec. 5, 2006) (No. BK-S-06-13589BAM) (noting that principal lender agreed to give 25 percent of any overbid to unsecured creditorsand to extend the auction for four additional weeks).

35. Bank of Am. Nat'l Trust & Sav. Ass'n v. 203 N. LaSalle St. P'ship, 526 U.S. 434, 457(1999).

36. Chrysler 1, 405 B.R. at 96-97.

37. Id. at 92. VEBA is the acronym for the trust that handles the retiree health benefits-thevoluntary employees' benefit association.

March 20 10]

Michigan Law Review

A. Valuation

Had the judge determined after a contested valuation hearing that thevalue of Chrysler's automotive assets that secured Chrysler's $6.9 billionsecured loan was $2 billion and that nothing further was allocable to theunsecured $4.9 billion deficiency" (and had the judge done the same forthe other creditors left behind, such as the products-liability claims), thenthe court would have found a plausible makeshift alternative. The courtscould have said that a cram-down under § 1129(a)(7) and § 1129(b) wouldhave led to the secured creditors getting $2 billion, so that the sale, al-though determining core terms under § 1129, was not defective.

Chrysler did present a valuation to the court, with the liquidation valuecentered near $2 billion, although with a range that went as high as $3.2billion, with a predicted net recovery of up to $2.6 billion for the securedcreditors." The range was wide enough to suggest that even Chrysler'svaluation experts saw it as possible that a liquidation could yield apprecia-bly more than $2 billion, despite the understandable tendency of expertfinancial opinions in bankruptcy to trend toward the client's interest.0

Chrysler's original numbers could have indicated to the court that it wouldneed to be cautious if it allowed Chrysler's self-valuation to stand as thecourt's makeshift valuation.

Shortly before the hearing on the proposed sale, Capstone, Chrysler'sfinancial advisor, revised its valuation downward (to 0-$1.2 billion),pointing to a decrease in Chrysler's cash, a general decrease in car sales,and Chrysler's unprofitability as warranting the adjustment. 4' The courtconsidered no other valuations.

The court did not give the objecting creditors time to present an alter-native valuation from their experts or require that such a valuation besubsidized by the bankruptcy estate as Chrysler's was, although the object-ing creditors could have anticipated prior to Chrysler's filing that therewould be a valuation contest and borne the expenses of getting their ownvaluation. Such valuation contests are notoriously difficult, as each partycomes to court with experts sporting a number remarkably supportive ofthe client's interests. But that's the system we're saddled with, and judges

38. Or decided that the security was worth less and the difference was the portion allocablefor the deficiency claim.

39. The valuation submitted by Chrysler's experts gave a range of $900 million to $3.2 bil-lion, with a likely recovery to the first liens of between $654 million and $2.6 billion. See Motion ofDebtors and Debtors in Possession, Pursuant to Sections 105, 363 and 365 of the Bankruptcy Codeand Bankruptcy Rules 2002, 6004 and 6006, Chrysler 1, 2009 WL 1227661.

40. E.g., In re New York, New Haven & Hartford R.R., 4 B.R. 758, 773 (D. Conn. 1980)("The parties urge acceptance of the valuation procedures ... which best conform to their views ofthe applicable law and which, coincidentally, establish the most favorable standing with respect totheir own cause.").

41. Chrysler 1, 405 B.R. at 97.

[Vol. 108:727

Assessing the Chrysler Bankruptcy

have done the best they can under the circumstances. Here, though, the42judge saw evidence from only one side's expert.

Yet in retrospect, this aspect of the reorganization may be the best jus-tification for judicial approval of the sale: the proponents presentedvaluation evidence and the objecting creditors did not. The objectingcreditors indicated that they lacked time to do so, but regardless, the litiga-tion posture at the time of the judge's decision was that a single valuationwas available to the judge and it stood unrebutted by better evidence.43

B. Consent

Sale proponents could analogize to § 1129(a)(8) consent, positing that,parallel to that section, the Chrysler deal had the secured creditors-thecreditors entitled to the proceeds from the sale of the assets-consentingde facto to the sale.

On the surface, there was a favorable informal vote. While the credi-tors initially objected strongly in negotiations with the U.S. Treasury, fourmajor creditors-Citigroup, J.P. Morgan Chase, Goldman Sachs, andMorgan Stanley-holding 70 percent of the dollar amount of the claimseventually acceded to the $2 billion number.44

The difficulty with crediting such a vote as informally satisfying§ 1129(a)(8) is that these creditors were beholden to the U.S. Treasury,which was emerging as Chrysler's principal creditor, and the Federal Re-serve, not just as their regulators, but as the banks' key financial patronsvia the government's bank-rescue program. The four banks had recentlyreceived $90 billion in investments from the Treasury.4' Their vote wassufficiently tainted under § 1126(e) to be a bad-faith vote, which wouldrequire that the tainted voters either be classified apart from the creditorsnot beholden to the Treasury or that the tainted votes just be dropped incalculating whether the class consented.

There's another, more severe, way to look at the big banks' votes. Oneor more of these banks could plausibly be viewed as controlled by the U.S.Treasury at the time. Not only did they depend on the Treasury for financ-ing, but serious talk had it that major banks, particularly Citigroup, wouldneed to be nationalized. Bank executives had reason to be wary, as Treas-ury-induced management changes or compensation mandates were beingdiscussed. Senior bank management had good reason not to annoy theTreasury.

42. Id. The problem may lie with the plan opponents. They did not have their own valuationready to put before the judge in the first week of bankruptcy, as the plan proponents did.

43. The dissenting creditors did, however, contest the credibility of the valuation and theadvisory-opinion author's incentives. See Brief of Appellants Indiana State Police Pension Trust etal., at * 15-19, Chrysler 11, 2009 WL 1560029 ["Brief of Indiana State Police Pension Trust"].

44. Neil King, Jr. & Jeffrey McCracken, USA Inc.: U.S. Forced Chrysler's Creditors ToBlink, WALL ST. J., May 11, 2009, at Al.

45. Id.

March 20 101

Michigan Law Review

If the Treasury was a controlling person of one or more the majorbanks, how should we look at the banks' consent? We'd then have to seeChrysler's major bankruptcy lender as controlling the votes of Chrysler'smajor prebankruptcy creditors, on a plan the lender itself designed. Nor-mally this conflict is reason for serious concern-one that's too large tokeep the various minority creditors in the same voting class as the fourmajor banks. The classes would need to vote separately on whether to ac-cept the reorganization plan proposed by the conflicted players and, then,without class consent, no plan could be confirmed without a judicial de-termination under § 1129(b) that priorities had been complied with.

The principal prebankruptcy bank lenders and the government, as bothdebtor-in-possession and exit-finance-lender, were too tightly related atthe height of the financial crisis to be fully independent actors. De facto,the same party controlled the purchase and the sale. As such, with thesame player on both sides of the sale, the best result conceptually wouldbe to view the lenders' votes as tainted under § 1126 (and therefore ex-cluded) or to separately classify the conflicted lenders' prebankruptcyloans from the others.'46

That § 1126 is designed to police these kinds of conflicts is clear bothfrom the legislative history and from prior case law. In the House Report,lawmakers emphasized that the votes of creditors who have conflictinginterests should be excluded, and explicitly disapproved of a case that hadupheld a creditor vote outside of bankruptcy, despite an apparent conflict.47

If a claimant acted "in aid of an interest other than an interest as a credi-tor," as a well-known case puts it,48 or had some "ulterior purpose" for its• 49

approval or disapproval, in the words of the leading treatise, its vote

46. Business-media hype about government pressure on the lenders to accede to the govern-ment's plan is beside the point. See, e.g., Michael J. de la Merced, Creditors Opposing Chrysler'sOverhaul Plan End Alliance, N.Y. TIMES, May 9, 2009, at B2. While not admirable if the acts oc-curred, such pressure isn't needed to make the case that a conflicted vote was in play. That somepressure was put on the banks is clear. While the administration may wisely have not explicitlyreminded the banks, "[llawmakers weren't so shy. Rep. Gary Peters [D-Mich.] ... wrote to the bankCEOs listing their [bailout] loans and asking them to extinguish most of Chrysler's debt." King &McCracken, supra note 44. These considerations could also have discouraged the banks from pro-posing alternatives to the government's favored transaction. Since the big banks were unpopularthen, they had a conflicted position even without the government in play, as they had reason not tobe tough with Chrysler, its operations, and its employees, to reduce the chance that public opinionwould turn further against the big banks.

Once the secured facility's controlling lenders had repaid the Treasury, their renewed freedomto move independently of government opinion was noticed. Robin Sidel, Loan Paid, J.P MorganSwagger Returns, WALL ST. J., July 15, 2009, at CI ("J.P. Morgan Chase & Co., freed from thegovernment's strictures after repaying $25 billion in federal money, is back to playing hardball [withthe government].").

47. H.R. REP. No. 95-595, at 411 (1977), reprinted in 1978 U.S.C.C.A.N. 5963, 6367; seealso In re Dune Deck Owners Corp., 175 B.R. 839, 845 n.13 (Bankr. S.D.N.Y. 1995).

48. In re Allegheny Int'l, Inc., 118 B.R. 282, 289 (Bankr. W.D. Pa. 1990) (quoting In re P-RHolding Corp., 147 F.2d 895, 897 (2d Cir. 1945)).

49. 7 COLLIER ON BANKRUPTCY 1126.06[l] (Alan N. Resnick & Henry J. Sommer eds.,15th ed. rev. 2009); cf. In re Holly Knoll Partnership, 167 B.R. 381, 385 (Bankr. ED. Pa. 1994)(favorably quoting similar statement in prior edition of COLLIER ON BANKRUPTCY).

[Vol. 108:727

Assessing the Chrysler Bankruptcy

should not be included. 0 True, courts do not treat every conflict of interestas bad faith, and bankruptcy courts have been more lax than tough in po-licing conflicts. But if the big banks' approval of the Chrysler sale wasmotivated by factors other than their interests as creditors, some courtswould have, and should have, disqualified their votes for Chapter 11 pur-poses or separately classified the two creditor groups.

Although the bankruptcy court considered consent, it did so in a dif-ferent context and misunderstood the full range of reasons for it to havebeen wary of the majority banks' consent as binding the minority credi-tors."' Because the creditors were acting of their own volition and were notmere alter egos of the Treasury, the bankruptcy court asserted, their con-

52sent was real and not a capitulation due to pressure. That instrumentality,alter-ego standard, if met, would indeed have been sufficient to disqualifythe tainted vote, but wasn't a necessary hurdle. The court needed to haveconsidered that a calculating creditor could have possessed the capacity toreject the Treasury's plan, but still cast a severely tainted vote, if the credi-tor understood that to do so would jeopardize other ongoing rescuearrangements, discourage regulatory forbearance, and constrict cash con-duits from the Treasury worth more to it than fully contesting the Chryslerplan.

While the court said no one brought forth evidence that the banks de-cided due to their conflicted position-that the conflict was merespeculation-this is a weak, possibly nafve standard here. Wiser judging canbe found in analogous state corporate-law conflict decisions. When a board

50. For a succinct history of the good faith provision, see Patrick D. Fleming, Credit Deriva-tives Can Create a Financial Incentive for Creditors to Destroy a Chapter 11 Debtor: Section1126(e) and Section 105(a) Provide a Solution, 17 AM. BANKR. INST. L. REV. 189, 200-09 (2009).

51. While we focus here on § 1129(a)(8)-based consent as a basis for approving the sale, theChrysler court considered the ostensible consent of Chrysler's senior creditors in deciding whetherto release their liens pursuant to § 363(f)(2) when the assets moved over to New Chrysler; if not,New Chrysler would be subject to the liens. Consent was considered under the senior creditors' loanagreement, which arguably allowed the creditors' agent-JP Morgan Chase, as it happens, one ofthe major lenders-to release collateral and sell it, even without the consent of the creditors. First,the court understood that a threshold issue was whether there was a valid sale. (It concluded thatthere was and that there was no sub rosa plan embedded in the sale-mistakenly in our view.) Thecourt then wondered whether it had jurisdiction to resolve any intercreditor, state-law-based disputeand offered the no-evidence-of-being-incapable-of-resisting-the-Treasury standard indicated in thetext. It viewed the creditor class as a single creditor, with its agent consenting. Hence, it didn't needto look behind that agent's consent and even wondered whether it had jurisdiction to do so. But thedissenting creditor argued that the agreement required each affected party to consent to a release ofcollateral.

Even if the agent's consent sufficed under the loan agreement, however, once the sale is a subrosa plan because it de facto determined distributions, case law demands that the § 363 sale either beabandoned (Brani)fi or comply with § 1129 (Continental). Creditors would vote by their dollarclaims and individually under § 1129(a)(8) (the agent would not cast the sole vote on behalf of thecreditor class), with those votes subject to § 1126(e) exclusion, and individual creditors would have§ I 129(a)(7) rights. The § 363 result removes the collateral from the bankrupt estate under § 363(f),if the sale itself is otherwise proper, but neither validates the transaction's other terms nor justifiesthe treatment of the products-liability and other claims left behind in Old Chrysler.

52. Chrysler 1, 405 B.R. at 103-04. More precisely, it concluded that the evidence to thecontrary--that the banks lacked volition-was speculation.

March 2010]

Michigan Law Review

litigation committee decided not to pursue a remedy in derivative litigation,the corporate law court examined the conflicts afflicting a Stanford lawprofessor on the board committee. The court saw the benefits the companyand its other directors could have, and had, provided the director's univer-sity. The judge did not, as the Chrysler judge appears to, look primarily for amoney trail leading to the professor's bank account. Nor did the corporatelaw judge view the conflict as speculative, one needing evidence of actualpressure from inside interests on the professor to favor his board colleaguesand alma mater. The judge saw a conflict, knew that the pressure and con-flict could be inside the director's head and, hence, concluded that thedirector's actions were not entitled to deference."

So it was in Chrysler, in all but the judge's conclusions. No one shouldhave had to show either a money trail running to the controlling banksfrom the U.S. Treasury or explicit pressure via a smoking-gun memo,email or phone call to the banks. That the banks might have overcometheir conflict is surely true, but equally surely not good enough for thecourt to dismiss the conflict as speculative. All the judge needed to knowwas that the conflicts were severe-and quite possibly inside the heads ofthe decision makers at Citibank and the others then dependent on the U.S.Treasury-to conclude that the court had before it a serious § 1126 prob-lem. The notion that the level of conflict of interest needed to be takenseriously under § 1126 was one that the banks lacked any will of theirown-that they were mere instrumentalities-is too low a standard.

Best view: the class consent was inadequate to bind the dissenters un-der § 1129(a)(8).

C. The Market Test

An alternative to a judicial valuation or a bargained-for result is a mar-ket test. If Chrysler were put up for sale in a suitable market and no onebid more than $2 billion, then that plausibly was its value. Creditors wouldhave had their makeshift substitute, and the § 363 sale would have beenproper. The courts' deference to the sale proponents' weak market test wasthe single most disturbing feature of the Chrysler bankruptcy. Because theostensible consent was at least tainted and perhaps inadequate, becausejudicial valuation assessments are inherently difficult, and because thedeal was more a reorganization than a true sale as Part IV, next, shows, themarket test was the key way by which the Chrysler plan could have fullyjustified itself, removing the taints. But it did not.

There was a market test of the Chrysler plan, but unfortunately no onecould believe it adequately revealed Chrysler's underlying value, as whatwas put to market was the sub rosa plan itself. Chrysler and the govern-ment asked the court to permit the firm to be marketed only with multipleprebankruptcy claims on Chrysler intact, including the United AutomotiveWorkers' ("UAWs") retiree claims. But that's exactly what was at stake:

53. In re Oracle Corp. Derivative Litig., 824 A.2d 917 (Del. Ch. 2003).

[Vol. 108:727

Assessing the Chrysler Bankruptcy

whether Chrysler's assets were more valuable without those claims. Thebankruptcy court turned down the objecting creditors' request to marketthe assets alone. 4

Here is the weakest link in the government's and Chrysler's case. Theyargued that the firm was worth no more than $2 billion. As such, theyshould not have stymied the Chrysler creditors from seeking to sell theassets for more than $2 billion, as they-the government and Chrysler-believed that the creditors would fail.

The government and Chrysler argued that they had scoured the worldfor a bidder for Chrysler and had found only one, FIAT." But they weremarketing variants of the bankruptcy plan actually used, one that didn'tseparate Chrysler's assets from its largest preexisting liabilities. As such,their efforts were efforts to market the plan they preferred, not the alterna-tive plans the Code requires the court to test. 6

And the Chrysler bankruptcy bidding procedures discouraged compet-ing bids-and, indeed, no competing bid was received. Bankruptcy courtsdo often require that bids be "qualified," but they do so mainly to screenout frivolous bids and to encourage bids that improve on the bid from theinitial, stalking horse bidder (who typically wants to deter others frombidding, a motivation that induces courts to police proposed conditions).

The Chrysler qualifications went much further than deterring frivolousbids. To be deemed "qualified" in the Chrysler bankruptcy, a bid had to,among other things, conform substantially to the terms set out in theTreasury's proposed Purchase Agreement. Bidders were bound by thegovernment's deal, which included agreeing to take on Chrysler's collec-tive-bargaining agreements and much of its prebankruptcy debt but not the$6.9 billion secured facility and the ongoing products-liability claims.

Bidders were not free to bid on Chrysler's assets alone, nor were theyreadily able to bid on other configurations of a reorganized Chrysler. A

54. Order, Pursuant to Sections 105, 363 and 365 of the Bankruptcy Code and BankruptcyRules 2002, 6004 and 6006, at 18, Chrysler 1, 2009 WL 1360869 ["Order Approving Bidding Pro-cedures"].

55. Motion of Debtors and Debtors in Possession, Pursuant to Sections 105, 363 and 365 ofthe Bankruptcy Code and Bankruptcy Rules 2002, 6004 and 6006 at 46, Chrysler 1, 2009 WL1227661 ["Motion of Chrysler to Approve Bidding Procedures"].

56. General Order M-331 [of the Southern District's Bankruptcy Court], supra note 32, at 3(Bidding procedures "must not chill the receipt of higher and better offers ...."); see also In rePresident Casinos, Inc., 314 B.R. 784, 786 (Bankr. E.D. Mo. 2004) ("Structured bid proceduresshould provide a vehicle to enhance the bid process and should not be a mechanism to chill prospec-tive bidders' interests."). More generally, as the Supreme Court has said, "the best way to determinevalue is exposure to a market." Bank of Am. Nat'l Trust & Sav. Ass'n v. 203 N. LaSalle St. P'ship,526 U.S. 434, 457 (1999). That implies a real exposure to the market, not one designed to chillmarket reaction.

57. Qualified bid requirements aim to "eliminate potential overbidders who are not seriousabout purchasing the debtor's assets, ensure the sale can be rapidly closed if an overbidder shouldpurchase the assets, and ensure that the net purchase price is higher than the original bid shouldoverbidding occur." Ronald L. Liebow, Steven F. Werth, N. Lynn Hiestand, Jeffery Steinle, andAlexa Palival, Distressed Asset Sales: Selling and Acquiring Assets from the Debtor's Estate, Prac-ticing Law Institute Commercial Law and Practice Handbook Series, PLI Order No. 5989, at 85, 87(Mar.-Apr. 2005).

March 20101

Michigan Law Review

nonconforming bid would be considered only if the debtor, after consult-ing with creditors, the Treasury, and the UAW, accepted it as qualified.While one must assume that had a party, sua sponte, come into the courtwith a competing bid on differing terms, the court would not have ignoredthe bid, nothing in the court's approval of the bidding procedures indicatedthat the court would welcome such a bidder offering a check for the assetsalone. Bids proposing alternative configurations of the UAW and VEBAobligations were discouraged or, more realistically, barred. Even if an out-sider valued the assets alone at more than $2 billion, it had to know thatneither the court nor the central parties would allow those assets to bepried loose.5"

This is a serious defect in the bidding procedures. First, with the gov-ernment having committed itself to rescuing Chrysler, bidders whocontemplated buying pieces of Chrysler-the Jeep product line, for exam-ple, or piecemeal equipment or Chrysler's new $1 billion car-bodystamping plant-had to know that they were not competing with a com-mercial bidder who realistically could be outbid. Since the Treasury wouldnot be outbid, why should a commercial bidder bother to study the com-pany carefully enough to place a bid? Given this baseline, getting a validbidding process for Chrysler was not going to be easy, but the court tooreadily accepted Chrysler's, the government's, and the UAW's preferencesthat there not be a serious bidding process at all. With the Treasury and theUAW as parties who would evaluate the bids under the court-approvedprocedures, the court signaled that there would not be a substantial, seri-ous bidding process, thereby chilling whatever outside interest existed inalternative configurations. Conditioning that outside bids be acceptable tothe Treasury and the UAW was peculiar, or at least nonstandard. Sales inwhich a single entity is both lender and bidder, as was the government inChrysler, warrant special vigilance, such as a robust market test, not aweak one. 9

This auction defect extended back to the prebankruptcy marketing:since bidders knew that the government had a structure in mind-keepingChrysler's operations and employment as intact as possible-bids for theassets alone, or with a different labor configuration, would not have beenforthcoming. The problem has its analogue in more usual bidding informa-tional problems: if insiders have better information, outsiders have reasonto fear that if they value the firm more highly than insiders, they'll over-pay. So they do not investigate and bid in the first place. Here the insidershad not just better information, but policy goals that made a wide range ofChrysler's potential sales configurations unacceptable to those that thecourt allowed to control the firm's disposition.

58. The Chrysler auction differed starkly in this respect from the sale of TWA's assets toAmerican Airlines, which some have cited as an analogue to Chrysler. The bidding procedures inTWA explicitly invited "alternative transactions" and bids for any part of the company. In re TransWorld Airlines, Inc., No. 01-00056(PJW), 2001 WL 1820326, at *6 (Bankr. D. Del. Apr. 2, 2001).

59. See, e.g., Kenneth Ayotte & David A. Skeel, Jr., An Efficiency-Based Explanation forCurrent Corporate Reorganization Practice, 73 U. CHI. L. REv. 425, 465-67 (2006).

[Vol. 108:727

Assessing the Chrysler Bankruptcy

Moreover, with the court accepting the proponents' request that Chrys-ler be sold quickly, outside bidders were given little more than a week toplace bids, which did not make for easy due diligence or financing. Bid-ders were required to put down a cash deposit of 10 percent of thepurchase price proposed. Chrysler reserved "the right, after consultationwith the Creditors' Committee, the U.S. Treasury and the UAW, to rejectany bid if such bid" was "on terms that are materially more burdensome orconditional than the terms of the Purchase Agreement."6 The PurchaseAgreement stated the terms to be accorded the majority of Chrysler's pre-bankruptcy debts. The reality was that the deal as proposed was goingforward.

A good market test could have validated the § 363 sale process, butChrysler lacked one. True, even a workable market test is not a cure-all. Itwill never perfectly ensure that a company receives top value for its assets,and there are inherent defects in any auction. And it does not by itself re-solve the plan-determination issues of how the sales proceeds would bedistributed. These issues were particularly acute for Chrysler because itsbidding plan largely determined the distribution in the Chrysler Chapter11. But the bidding structure in Chrysler was far removed from a genuinemarket test that could validate the actual § 363 sale that occurred.

D. The Emergency-How Immediate?

Lionel requires that sales be made only if there is a valid business pur-pose. The posture of the Chrysler case seemed to rely on the businessemergency--Chrysler would, it was said, be forced to liquidate shortlyafter June 15 if the sale to FIAT did not close by then. Indeed, plan propo-nents in places seemed to rest solely on an emergency standard assufficient in itself to justify cutting § 1129 priority comers and doing soquickly,6' despite that Lionel had the emergency justifying a business pur-pose for a sale, but not justifying ignoring priority. The proponents'aggressive interpretation is one that courts had not previously promul-gated.

Much was made early in June of the fact that FIAT had agreed to pur-chase Chrysler's core on June 15. This was portrayed as providing boththe business justification for the sale-a buyer who might turn the com-pany around-and the pressing need to approve that sale immediately,because any stay to the proceedings that went past June 15 jeopardized thesale.

But the emergency status was greatly exaggerated, with the threat thatChrysler would promptly liquidate if the FIAT deal did not go forward onJune 15 implausible. To understand why the liquidation threat was over-played-which seemed to move the courts both in quickly approving the

60. Chrysler I Order Approving Bidding Procedures, supra note 54, at *6, *20.

61. Brief for Debtors-Appellees Chrysler LLC, et al., Chrysler 1!, 2009 WL 1560030, at*22-24.

March 2010]

Michigan Law Review

sale and in not staying its closing for a closer look-we need to follow themoney in the Chrysler deal.

While a deadline from a typical purchaser who is providing, say, $2billion in fresh money is something bankruptcy courts must take very seri-ously, Chrysler was not in that situation and FIAT was not that kind ofcash purchaser. The cash came from the U.S. Treasury, not from FIAT.

Without FIAT, Chrysler and the Treasury could have used the GM tem-plate, without a figurehead outsider as a purchaser that provides no cash.Moreover, FIAT's chief executive conceded that FIAT would never walk

12away from the deal. And why would it? It was not asked to pay anything.The Treasury could have pulled the plug, not FIAT. But the Treasury

was not about to. While the judge stated a fear that the Treasury wouldwalk if the June 15 deadline were missed, one wonders how credible thisfear was, when the Treasury was a major architect of the plan and was si-multaneously actively preparing an analogous reorganization of GeneralMotors.6 3

If Chrysler's operations were like the melting-ice-cube metaphor that'sbeen used in this setting64-about to collapse and only the sale could allowany value to be obtained-then a court would have to weigh competing con-siderations. Since Chrysler had already shut down its plants due to weakdemand, a limited delay was unlikely to affect production. Chrysler did nothave all the time in the world, but there was sufficient time-weeks, maybea month-for the courts to fashion the makeshift checks that prior case lawdemanded, to confirm that the plan complied with § 1129 and, if it did not,to induce the parties to reshape the plan.

Moreover, the emergencies in the past have been judicially cited to sup-port a § 363 sale instead of a full-scale § 1129 reorganization, but not tosupport the idea that no protections, makeshift or substantial, are needed in a

62. See, e.g., Serena Saitto, Fiat Will 'Never' Walk Away From Chrysler CEO Says, BLOOM-BERG.COM, June 8, 2009, http://www.bloomberg.com/apps/news?pid=20601087&sid=aS-6UyCqlJmA. The record before the court included the concession,

63. See, e.g., David E. Sanger & Bill Vlasic, Chrysler's Fall May Help Obama to ReshapeG.M., N.Y. TIMES, May 2, 2009. The Treasury itself, and not FIAT, created the June 15 deadline inits DIP financing. If it wanted to extend a few weeks, while the plan was adequately vetted under§ 1129 for compliance, it could have. FIAT would, the indicators strongly suggest, have waited.Given that the Treasury was sponsoring the Chrysler rescue, it's unlikely it would have walked awaydisgruntled if it had to wait a few more weeks for a real auction. Still, alternate scenarios haduncertain outcomes if the delay got out of hand: one economic advisor, who opposed anyChrysler bail-out, believes that without FIAT the government would not have bailed Chryslerout. Ryan Lizza, The Political Scene-Inside the Crisis, THE NEW YORKER, Oct. 12, 2009, 80,95.

64. E.g., In re Summit Global Logistics, Inc., 2008 Bankr. LEXIS 896 at *31 (Bankr. D.N.J.Mar. 26, 2008); see also Chrysler II, 576 F.3d at 114 ("[An automobile manufacturing business canbe within the ambit of the 'melting ice cube' theory .... ").

65. See, e.g., Michael McKee, Chrysler Bankruptcy May Not Dent Economy as CutbacksWere Set, BLOOMBERG.COM, May 5, 2009, http://www.bloomberg.com/apps/news?pid=20601 110&sid=aOofvGXOZKk4 ("[Due to weak demand,] Chrysler probably would have had to shut downtemporarily anyway, said Mark Zandi, chief economist at Moody's Economy.com .... Chrysler,which filed for the fifth-biggest U.S. bankruptcy last week, already had been ... closing factoriesbecause of the industry's slump.").

[Vol. 108:727

Assessing the Chrysler Bankruptcy