asian paints (asipai) | 832content.icicidirect.com/mailimages/idirect_asianpaints_q3fy16.pdf ·...

TRANSCRIPT

January 19, 2016

ICICI Securities Ltd | Retail Equity Research

Result Update

Strong performance led by volume growth… • Asian Paints (APL) posted sales growth of 13.9% YoY driven by

similar YoY rise in volume growth led by festive demand and lower base of same period last year. Flattish realisation growth was due to higher proportion of lower end products in sales volume. APL passed on the benefit of lower raw material prices to customers

• Titanium di-oxide prices declined ~4% YoY while the lag impact of other raw materials prices led to saving in raw material cost to the tune of 332 bps YoY. As a result, operating margin improved ~327 bps YoY. Also, other income increased 12% YoY to | 35.8 crore mainly due to higher treasury income, helping PAT to grow 26% YoY

• We have introduced FY18E estimates with revenue, earning CAGR of ~12%, ~20% respectively. We estimate volume CAGR of 12% and limited realisation growth largely on the back of a change in the product mix

Leader in paint segment, economic recovery to drive volume growth APL is the industry leader in the decorative paint segment with ~53% market share and a dealer network of over 35,000 across India. It derives ~81% of its topline from the decorative segment while the rest comes from the industrial segment. With limited competition in the market, APL recorded revenue CAGR of 10% in FY11-15 driven by volume CAGR of ~8% (amid economic slowdown) during the same period. In spite of inflationary pressure in FY11-15, gross margins expanded ~110 bps clearly indicating APL’s pricing power. Slowing Indian GDP growth (paints volume growth is 1.5-1.7x real GDP growth) and a slowdown in discretionary expenditure (slight shift in repainting demand) took a toll on overall volume growth of the paint industry. We believe an economic recovery (albeit at a slow pace) and repainting demand coupled with the new government’s focus on increasing spending in infrastructure projects would lead to 12% volume growth (demand staying intact in tier II, tier III cities) and moderate revenue CAGR of 12% between FY15 and FY18E. Favourable raw material price movement to aid margin To avoid inflationary pressure, APL has successfully passed on the price hike (~6-7%) to its customers. However, the EBITDA margin tapered off in FY12-13 as raw material prices moved up sharply (~40% of raw material are imported) hit by elevated dollar value against the rupee (up 19% between FY11 and FY13) and bottoming out titanium di-oxide (TiO2) prices. In FY15, APL passed on the benefit of lower material cost to its customer by taking a minute price hike of 0.4% YoY. We have modelled a margin improvement of ~220 bps in FY15-18E (considering historical performance during FY10) supported by benign raw material prices. Strong fundamentals, revival in economy to drive valuation We have modelled moderate revenue CAGR of 12% for FY15-18E led by volume growth of ~12% during the same period. We believe the company will pass on some benefits to customers considering the benign raw material prices. We estimate PAT CAGR of ~19% for FY15-18E due to an expansion in EBITDA margin by 220 bps in FY15-18E. We roll over our valuation on FY18E considering lower crude oil prices, which will benefit the market leader as it is least likely to pass on the entire benefit of lower raw material prices. Also, high cash on the books could lead to an increase in dividend payout and improvement in RoEs. We reiterate our BUY rating on the stock with a target price of | 951/share (38x its FY18E earnings).

Rating matrix Rating : BuyTarget : | 951Target Period : 12 monthsPotential Upside : 14%

What’s Changed? Target UnchangedEPS FY16E UnchangedEPS FY17E Changed from |23.5 to | 21.9EPS FY18E Introudced at | 24.9Rating Unchanged

Quarterly Performance Q3FY16 Q3FY15 YoY (%) Q2FY16 QoQ (%)

Revenue 4,103.0 3,602.8 13.9 3,730.6 10.0EBITDA 800.6 583.5 37.2 620.8 29.0EBITDA (%) 19.2 16.0 327bps 16.4 282bpsPAT 463.3 368.2 25.8 399.0 16.1

Key Financials | Crore FY15 FY16E FY17E FY18ERevenue 14,183 15,878 17,782 19,701 EBITDA 2,235.4 2,898.9 3,204.3 3,541.9 Net Profit 1,395.2 1,835.9 2,099.6 2,385.6 EPS (|) 14.5 19.1 21.9 24.9

Valuation summary FY15 FY16E FY17E FY18E

P/E 58.4 44.4 38.8 34.2 Target P/E 65.4 49.7 40.6 38.2 EV / EBITDA 36.2 27.8 25.0 22.8 P/BV 17.2 14.6 12.4 11.2 RoNW (%) 32.5 36.6 35.6 35.4 RoCE (%) 44.9 50.4 47.6 46.6

Stock data Particular AmountMarket Capitalization (| Crore) 81,532.0Total Debt (FY15) (| Crore) 78.3Cash and Investments (FY15) (| Crore) 1,086.8EV (| Crore) 80,523.5 52 week H/L (|) 927/693Equity capital (| Crore) 95.9Face value (|) 1.0

Price performance (%) 1M 3M 6M 12M

Asian Paints (3.4) (3.6) 3.1 0.8 Berger Paints 2.2 9.1 14.6 8.4 Kansai Nerolac 1.0 2.6 (2.0) 14.4 Akzo Noble (3.6) (6.4) (0.2) (9.7)

Asian Paints (ASIPAI) | 832

Research Analyst

Sanjay Manyal [email protected]

Hitesh Taunk [email protected]

ICICI Securities Ltd | Retail Equity Research Page 2

Variance analysis Q3FY16 Q3FY16E Q3FY15 YoY (%) Q2FY16 QoQ (%) Comments

Revenue 4,103.0 3,852.1 3,602.8 13.9 3,730.6 10.0Recorded net sales growth of 13.9% YoY led by similar growth in volume (decorative segment) due to festive demand. However, volume growth marred by heavy rains in the coastal area of South India

Other Income 35.8 53.5 32.1 11.7 57.5 -37.8 Higher other income mainly on account of higher treasury income

Raw Material Exp 2,200.4 2,099.4 2,051.7 7.2 2,032.2 8.3Raw material cost to sales dip by 332 bps YoY due to benign raw material prices

Employee Exp 247.0 254.7 231.9 6.5 246.6 0.1Manufacturing & Other exp 912.1 886.0 785.5 16.1 879.7 3.7

EBITDA 800.6 673.3 583.5 37.2 620.8 29.0EBITDA Margin (%) 19.2 17.2 16.0 327 bps 16.4 282 bps Saving in raw material cost helps in expansion of EBITDA marginDepreciation 72.5 71.4 67.3 7.7 70.9 2.3Interest 7.6 9.9 9.8 -22.2 9.2 -17.5

Exceptional items 52.5 0.0 0.0 NM 0.0 NMIncurred an exceptional loss of | 52.5 crore mainly due to diminution of value of the investment made in Sleek International Pvt Ltd

PBT 703.8 645.5 538.4 30.7 598.2 17.7Total Tax 228.8 198.1 166.7 37.2 183.6 24.6PAT 463.3 431.8 368.2 25.8 399.0 16.1 Expansion in EBITDA margin coupled with higher other income translates to sharp

growth in PAT

Key MetricsVolume growth (%) 14.0 11.0 2 8.0

Strong volume growth led by festive demand and lower base same period last year. In addition, a change in product mix also helped in volume growth

Realisation growth (%) 0.0 -4.0 3 -4 Realisation growth remained subdued as the company passed on the benefit of lower raw material price coupled with higher sales of lower end products

Source: Company, ICICIdirect.com Research Change in estimates

FY18E

Old New % Change Old New % Change Introduced Comment

Revenue 15,877.8 15,877.8 0.0 17,952.1 17,782.3 -0.9 19,700.7 We have marginally tweaked our estimate for FY17E considering passing on the benefit of lower raw material prices to end customer. We have introduced FY18 estimates, building topline growth of ~11% YoY

EBITDA 2,898.9 2,898.9 0.0 3,380.7 3,204.3 -5.2 3,541.9

EBITDA Margin %18.3 18.3 0bps 18.8 18.0 -81bps 18.0

We believe the company would partially pass on the benefit of lower raw material prices and maintain margin in the range of 17-18%

PAT 1844.2 1835.9 -0.4 2258.7 2099.6 -7.0 2385.6EPS (|) 19.2 19.1 -0.4 23.5 21.9 -7.0 24.9

(| Crore)FY17EFY16E

Source: Company, ICICIdirect.com Research Assumptions

CommentsFY14 FY15 FY16E FY17E FY16E FY17E

Volume Growth (%) 6.0 9.7 11.0 13.3 13.2 11.0 11.3

Volume growth largely driven by sustained demand from tier II and tier IIIcities coupled with a demand recovery in the southern region. Volumeswould also be boosted by implementation of the government's Seventh PayCommission plan

Realisation Growth (%) 1.8 0.3 (1.3) (1.5) (1.0) (1.3) 1.5

EarlierCurrent Introduced FY18E

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 3

Company Analysis Leader in decorative paint segment with over ~53% market share

Asian Paints (APL) has remained the industry leader among top four players (i.e. Berger Paints, Kansai Nerolac and Akzo Nobel) with a market share of 53% followed by Berger Paints with ~19% and Kansai Nerolac with ~15%. Despite competition gaining momentum, in the last six years (2008-14), APL’s market share has improved 100 bps (in terms of value) supported by a strong dealer network, strong supply chain, brand building exercise and launch of premium products in domestic markets. The company has a strong dealer network of over 35,000 across India (~27,000 dealers with tinting machines), which is nearly double India’s No. 2 player Berger Paints in the decorative segment. The company has recorded revenue CAGR of 20% in FY05-08 led by ~16% volume growth supported by rising urbanisation, shorter repainting demand and launch of premium products. The volume growth in the paint segment has remained higher than real GDP growth and commands a multiplier of 1.7x (average FY02-08). We have modelled revenue CAGR of 12% in FY15-18E led by 12% volume growth during the same period. Our estimate of volume growth is largely supported by demand remaining intact for decorative paints in tier II and tier III cities coupled with shorter repainting demand that will help in driving volume growth.

Exhibit 1: Expect volume CAGR of ~12% in FY15-18E

-5

0

5

10

15

20

FY11 FY12 FY13E FY14E FY15E FY16E FY17E FY18E

(%)

Volume Growth Realisation growth

Source: Company, ICICIdirect.com Research

Exhibit 2: Net sales growth at ~12% CAGR in FY15-18E

0

5000

10000

15000

20000

25000

FY11 FY12 FY13 FY14 FY15E FY16E FY17E FY18E

(| c

rore

)

Domestic Overseas

Source: Company, ICICIdirect.com Research

Exhibit 3: Market share of leading paint companies (2008)

Asian Paints52%

Berger Paints17%

Kansai Nerolac16%Akzo Noble

11%

Shalimar Paints4%

Source: Company, ICICIdirect.com Research

Exhibit 4: Market share of leading paint companies (2015)

Asian Paints53%

Berger Paints19%

Kansai Nerolac15%

Akzo Noble11% Shalimar Paints

2%

Source: Company, ICICIdirect.com Research

Leader in decorative paints segment continues to grow at a

healthy pace with strong double digit volume growth

mainly contributed by decorative paints demand

ICICI Securities Ltd | Retail Equity Research Page 4

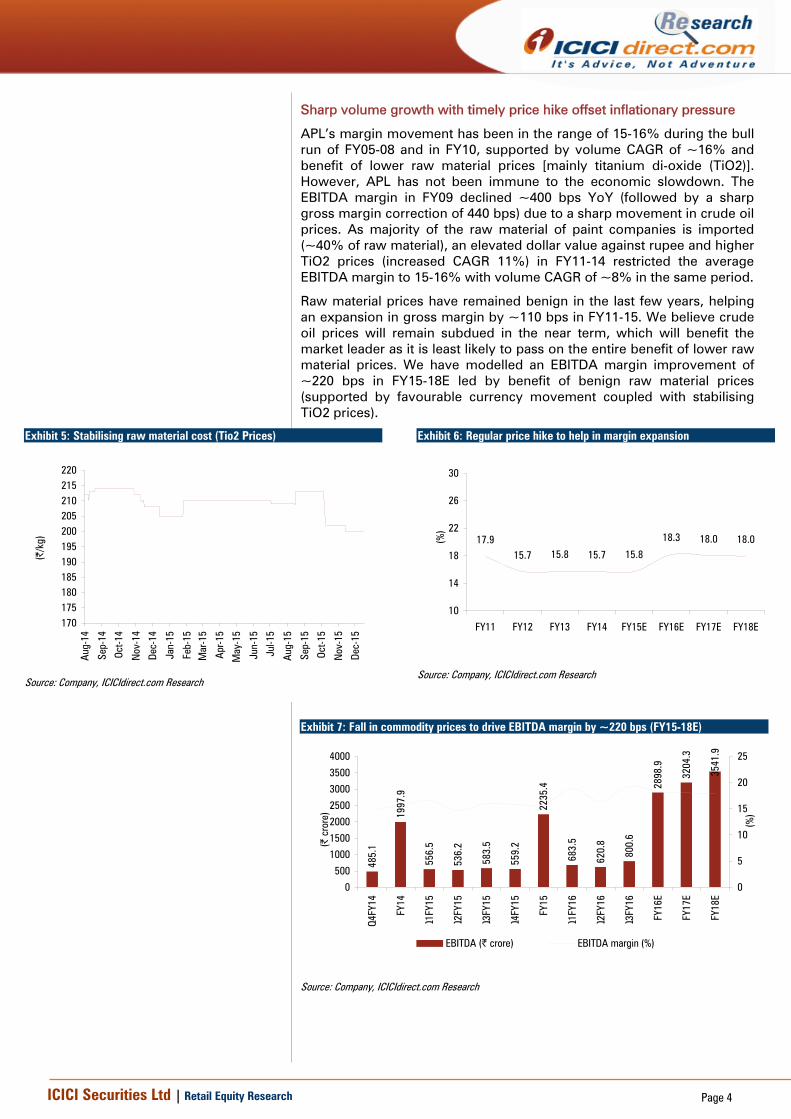

Sharp volume growth with timely price hike offset inflationary pressure

APL’s margin movement has been in the range of 15-16% during the bull run of FY05-08 and in FY10, supported by volume CAGR of ~16% and benefit of lower raw material prices [mainly titanium di-oxide (TiO2)]. However, APL has not been immune to the economic slowdown. The EBITDA margin in FY09 declined ~400 bps YoY (followed by a sharp gross margin correction of 440 bps) due to a sharp movement in crude oil prices. As majority of the raw material of paint companies is imported (~40% of raw material), an elevated dollar value against rupee and higher TiO2 prices (increased CAGR 11%) in FY11-14 restricted the average EBITDA margin to 15-16% with volume CAGR of ~8% in the same period.

Raw material prices have remained benign in the last few years, helping an expansion in gross margin by ~110 bps in FY11-15. We believe crude oil prices will remain subdued in the near term, which will benefit the market leader as it is least likely to pass on the entire benefit of lower raw material prices. We have modelled an EBITDA margin improvement of ~220 bps in FY15-18E led by benefit of benign raw material prices (supported by favourable currency movement coupled with stabilising TiO2 prices).

Exhibit 5: Stabilising raw material cost (Tio2 Prices)

170175180185190195200205210215220

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

Feb-

15M

ar-1

5

Apr-1

5

May

-15

Jun-

15

Jul-1

5

Aug-

15

Sep-

15

Oct-1

5

Nov

-15

Dec-

15

(|/k

g)

Source: Company, ICICIdirect.com Research

Exhibit 6: Regular price hike to help in margin expansion

17.915.7 15.8 15.7 15.8

18.3 18.0 18.0

10

14

18

22

26

30

FY11 FY12 FY13 FY14 FY15E FY16E FY17E FY18E

(%)

Source: Company, ICICIdirect.com Research

Exhibit 7: Fall in commodity prices to drive EBITDA margin by ~220 bps (FY15-18E)

485.

1

1997

.9

556.

5

536.

2

583.

5

559.

2

2235

.4

683.

5

620.

8

800.

6

2898

.9

3204

.3

3541

.9

0

500

1000

1500

2000

2500

3000

3500

4000

Q4FY

14

FY14

Q1FY

15

Q2FY

15

Q3FY

15

Q4FY

15

FY15

Q1FY

16

Q2FY

16

Q3FY

16

FY16

E

FY17

E

FY18

E

(| c

rore

)

0

5

10

15

20

25(%

)

EBITDA (| crore) EBITDA margin (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 5

Improvement in margin to drive PAT

We believe PAT is likely to record a CAGR of 19% in FY15-18E, supported by an improvement in EBITDA margin. The company has planned a total capex of ~ | 700 crore, which includes capacity addition of 2 lakh tonnes in the Rohtak plant and new capacity addition in southern India. We believe there would be near term pressure in free cash flows considering the capital outlay. Exhibit 8: PAT likely to grow at 19% CAGR in FY15-17E

275.

2

326.

8

329.

4

287.

4

1218

.8

338.

7

347.

3

368.

2

341.

0

1395

.2

455.

2

399.

0

463.

3

1835

.9

2099

.6

2385

.6

0

500

1000

1500

2000

2500

3000

Q1FY

14

Q2FY

14

Q3FY

14

Q4FY

14

FY14

Q1FY

15

Q2FY

15

Q3FY

15

Q4FY

15

FY15

E

Q1FY

16

Q2FY

16

Q3FY

16

FY16

E

FY17

E

FY18

E

(| c

rore

)

0

2

4

6

8

10

12

14

(%)

PAT (| crore) PAT Margin (%)

Source: Company, ICICIdirect.com Research

Exhibit 9: Lighter balance sheet to help in driving return ratios

15202530354045505560

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(%)

RoE RoCE

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 6

Outlook and valuation As APL is the market leader in the decorative segment with over 57% market share, the company has commanded rich valuations compared to peers in spite of volume pressure and the declining trend of margin and return ratios. The company recorded revenue, PAT CAGR of 19.6%, 33%, respectively, supported by ~16% volume CAGR in FY05-08. Better operating leverage led to EBITDA margin expansion of 200 bps during the same period. The company has commanded an average one year forward earnings multiple of 22x in FY05-08 with average RoE of 39%. For FY11-13, revenue, PAT CAGR was 12%, 10%, respectively, supported by ~7-8% volume growth. Despite an EBITDA margin erosion by ~142 bps due to lower operating leverage (higher fixed cost) and RoE on a declining trend, the stock has commanded average one year forward earnings multiple of 30x. We have introduced FY18E estimates with revenue, earning CAGR ~12%, ~20% respectively. We estimate volume CAGR of 12% and limited realisation growth largely on the back of a change in the product mix. Historically, in FY10, the company witnessed a sharp increase in gross margin on account of lower crude prices. We believe crude oil prices will remain at lower levels in the medium term, which will benefit the market leader as it is least likely to pass on the entire benefit of lower raw material prices. Also, high cash on the books could lead to an increase in dividend payout and improvement in RoEs. We roll over our valuation on FY18E considering the revival in the Indian economy. We value the stock at 38x its FY18E earnings and maintain our target price of | 951 per share with a BUY recommendation. Exhibit 10: Valuation

Sales Growth EPS Growth PE EV/EBITDA RoNW RoCE (| cr) (%) (|) (%) (x) (x) (%) (%)

FY15 14182.8 14.5 58.4 36.2 32.5 44.9FY16E 15877.8 12.0 19.1 31.6 44.4 27.8 36.6 50.4FY17E 17782.3 12.0 21.9 14.4 38.8 25.0 35.6 47.6FY18E 19700.7 10.8 24.9 13.6 34.2 22.8 35.4 46.6

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 7

Company snapshot

0

100

200

300

400

500

600

700

800

900

1,000

Jan-

11

Apr-1

1

Jul-1

1

Oct-1

1

Jan-

12

Apr-1

2

Jul-1

2

Oct-1

2

Jan-

13

Apr-1

3

Jul-1

3

Oct-1

3

Jan-

14

Apr-1

4

Jul-1

4

Oct-1

4

Jan-

15

Apr-1

5

Jul-1

5

Oct-1

5

Jan-

16

Apr-1

6

Jul-1

6

Oct-1

6

Source: Bloomberg, Company, ICICIdirect.com Research

Key events Date EventMar-10 Robust volume growth along with substantial improvement in operating margins ~18% (best in last six seven years) results in a rally in the stock

May-10 Commences operations in its new manufacturing facility at Rohtak, Haryana with a capacity of 1,50,000 kl at an investment of | 275 crore

Jan-11 Margin decline due to slow & steady inch up of key crude based raw material prices

Oct-11 Aggressive price hike to mitigate raw material pressure a respite to the stock price

May-12 Starts building a decorative paints plant in Khandala (Maharashtra) with a capacity of ~3,00,000 kl (scalable capacity of 4,00,000 kl)

Jan-13 Sustained volumes along with ~20% decline in Titanium dioxide lead to positive movement in the stock

Jul-13 Stock witnesses a steep decline in anticipation of adverse impact on results due to a volatile currency movement

Nov-13 With sustained volumes and strong margins in Q2FY14 contrary to expectation, the stock recovers and makes new high in November

Nov-13 Company closes down operation of its powder coating plant at Baddi (HP) for two years due to a significant decline in the processing volume

Feb-14 Unconditional cash offer for shares of Berger International (BIL), Singapore by Asian Paints (International) Ltd (APIL), Mauritius, to make BIL a wholly-owned subsidiary and delist from Singapore Exchange Securities Trading (SGX-ST)

Apr-14 Asian Paints (International) Ltd, Mauritius, subsidiary of Asian Paints acquires 51% stake in Kadisco Chemical Industry PLC, Ethiopia

May-14 Asian Paints acquires entire stake of Ess Ess Bathroom Products Pvt Ltd, a prominent player in the bath and wash business segment in India

Source: Company, ICICIdirect.com Research

Top 10 Shareholders Shareholding Pattern Rank Name Latest Filing Date % O/S Position (m) Change (m)1 Smiti Holding & Trading Company Pvt. Ltd. 30-Sep-15 0.06 54.1 0.02 Isis Holding & Trading Company Pvt. Ltd. 30-Sep-15 0.06 52.9 0.03 Life Insurance Corporation of India 30-Sep-15 0.05 51.5 0.04 Geetanjali Trading & Investments Pvt. Ltd. 30-Sep-15 0.05 49.3 0.05 Ojasvi Trading Pvt. Ltd. 30-Sep-15 0.05 47.0 0.06 Vakil (Abhay Arvind) 30-Sep-15 0.03 28.5 0.07 Elcid Investments, Ltd. 30-Sep-15 0.03 28.3 0.08 Gujarat Organics Ltd 30-Sep-15 0.02 22.8 0.09 Sudhanava Investments & Trading Company Pvt. Ltd. 30-Sep-15 0.02 19.0 0.010 Rupen Investment & Industries Pvt. Ltd. 30-Sep-15 0.02 18.8 0.0

(in %) Sep-14 Dec-14 Mar-15 Jun-15 Sep-15Promoter 52.8 52.8 52.8 52.8 52.8FII 18.1 17.3 18.1 17.0 17.4DII 9.2 9.9 8.8 9.8 9.5Others 19.9 20.1 20.3 20.4 20.3

Source: Reuters, ICICIdirect.com Research

Recent Activity

Investor name Value Shares Investor name Value SharesVontobel Asset Management, Inc. 54.56m 3.94m BNP Paribas Investment Partners Asia Ltd. -34.52m -2.80m Vakil (Amrita A) 25.79m 2.57m William Blair & Company, L.L.C. -17.43m -1.47m Vakil (Varun Amar) 22.01m 2.23m British Columbia Investment Management Corp. -10.74m -1.18m GMO LLC 19.13m 2.09m BlackRock Institutional Trust Company, N.A. -7.57m -0.59m Mirae Asset Global Investments (Hong Kong) Limited 17.22m 1.34m Fidelity Management & Research Company -6.78m -0.53m

Buys Sells

Source: Reuters, ICICIdirect.com Research

Target Price | 951

ICICI Securities Ltd | Retail Equity Research Page 8

.

Financial summary

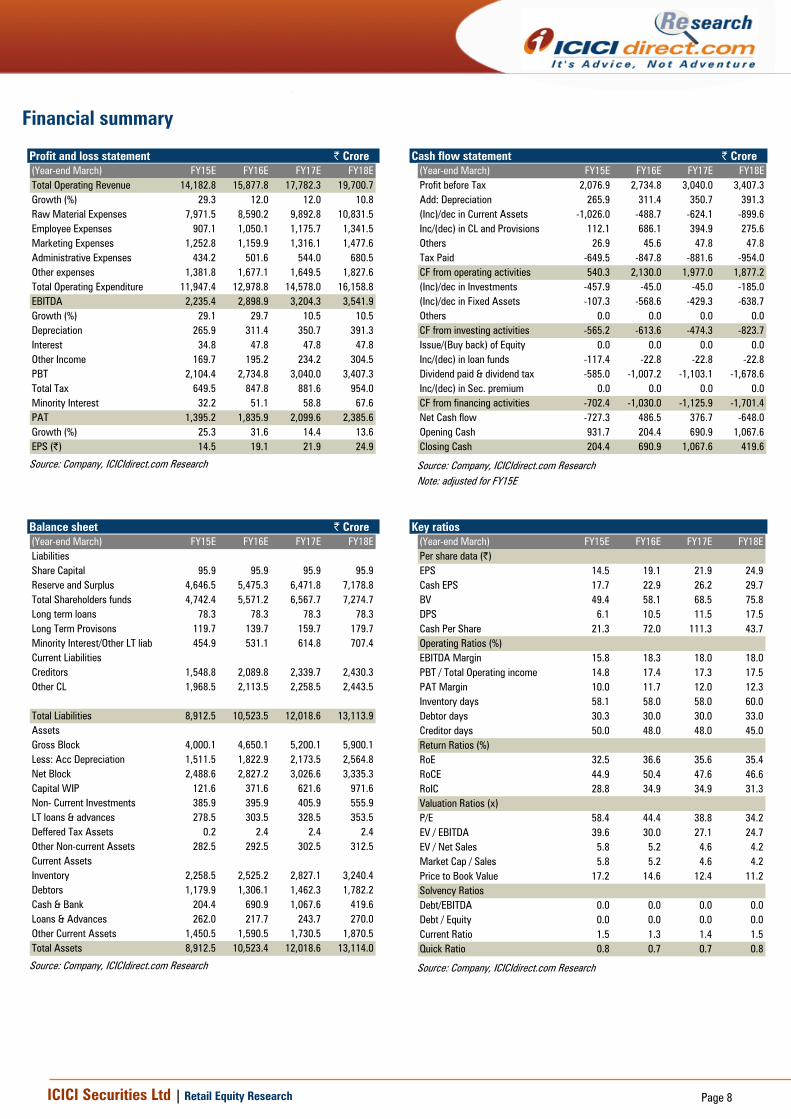

Profit and loss statement | Crore (Year-end March) FY15E FY16E FY17E FY18ETotal Operating Revenue 14,182.8 15,877.8 17,782.3 19,700.7Growth (%) 29.3 12.0 12.0 10.8Raw Material Expenses 7,971.5 8,590.2 9,892.8 10,831.5Employee Expenses 907.1 1,050.1 1,175.7 1,341.5Marketing Expenses 1,252.8 1,159.9 1,316.1 1,477.6Administrative Expenses 434.2 501.6 544.0 680.5Other expenses 1,381.8 1,677.1 1,649.5 1,827.6Total Operating Expenditure 11,947.4 12,978.8 14,578.0 16,158.8EBITDA 2,235.4 2,898.9 3,204.3 3,541.9Growth (%) 29.1 29.7 10.5 10.5Depreciation 265.9 311.4 350.7 391.3Interest 34.8 47.8 47.8 47.8Other Income 169.7 195.2 234.2 304.5PBT 2,104.4 2,734.8 3,040.0 3,407.3Total Tax 649.5 847.8 881.6 954.0Minority Interest 32.2 51.1 58.8 67.6PAT 1,395.2 1,835.9 2,099.6 2,385.6Growth (%) 25.3 31.6 14.4 13.6EPS (|) 14.5 19.1 21.9 24.9

Source: Company, ICICIdirect.com Research

Cash flow statement | Crore (Year-end March) FY15E FY16E FY17E FY18EProfit before Tax 2,076.9 2,734.8 3,040.0 3,407.3Add: Depreciation 265.9 311.4 350.7 391.3(Inc)/dec in Current Assets -1,026.0 -488.7 -624.1 -899.6Inc/(dec) in CL and Provisions 112.1 686.1 394.9 275.6Others 26.9 45.6 47.8 47.8Tax Paid -649.5 -847.8 -881.6 -954.0CF from operating activities 540.3 2,130.0 1,977.0 1,877.2(Inc)/dec in Investments -457.9 -45.0 -45.0 -185.0(Inc)/dec in Fixed Assets -107.3 -568.6 -429.3 -638.7Others 0.0 0.0 0.0 0.0CF from investing activities -565.2 -613.6 -474.3 -823.7Issue/(Buy back) of Equity 0.0 0.0 0.0 0.0Inc/(dec) in loan funds -117.4 -22.8 -22.8 -22.8Dividend paid & dividend tax -585.0 -1,007.2 -1,103.1 -1,678.6Inc/(dec) in Sec. premium 0.0 0.0 0.0 0.0CF from financing activities -702.4 -1,030.0 -1,125.9 -1,701.4Net Cash flow -727.3 486.5 376.7 -648.0Opening Cash 931.7 204.4 690.9 1,067.6Closing Cash 204.4 690.9 1,067.6 419.6

Source: Company, ICICIdirect.com Research Note: adjusted for FY15E

Balance sheet | Crore (Year-end March) FY15E FY16E FY17E FY18ELiabilitiesShare Capital 95.9 95.9 95.9 95.9Reserve and Surplus 4,646.5 5,475.3 6,471.8 7,178.8Total Shareholders funds 4,742.4 5,571.2 6,567.7 7,274.7Long term loans 78.3 78.3 78.3 78.3Long Term Provisons 119.7 139.7 159.7 179.7Minority Interest/Other LT liab 454.9 531.1 614.8 707.4Current LiabilitiesCreditors 1,548.8 2,089.8 2,339.7 2,430.3Other CL 1,968.5 2,113.5 2,258.5 2,443.5

Total Liabilities 8,912.5 10,523.5 12,018.6 13,113.9AssetsGross Block 4,000.1 4,650.1 5,200.1 5,900.1Less: Acc Depreciation 1,511.5 1,822.9 2,173.5 2,564.8Net Block 2,488.6 2,827.2 3,026.6 3,335.3Capital WIP 121.6 371.6 621.6 971.6Non- Current Investments 385.9 395.9 405.9 555.9LT loans & advances 278.5 303.5 328.5 353.5Deffered Tax Assets 0.2 2.4 2.4 2.4Other Non-current Assets 282.5 292.5 302.5 312.5Current AssetsInventory 2,258.5 2,525.2 2,827.1 3,240.4Debtors 1,179.9 1,306.1 1,462.3 1,782.2Cash & Bank 204.4 690.9 1,067.6 419.6Loans & Advances 262.0 217.7 243.7 270.0Other Current Assets 1,450.5 1,590.5 1,730.5 1,870.5Total Assets 8,912.5 10,523.4 12,018.6 13,114.0

Source: Company, ICICIdirect.com Research

Key ratios (Year-end March) FY15E FY16E FY17E FY18EPer share data (|)EPS 14.5 19.1 21.9 24.9Cash EPS 17.7 22.9 26.2 29.7BV 49.4 58.1 68.5 75.8DPS 6.1 10.5 11.5 17.5Cash Per Share 21.3 72.0 111.3 43.7Operating Ratios (%)EBITDA Margin 15.8 18.3 18.0 18.0PBT / Total Operating income 14.8 17.4 17.3 17.5PAT Margin 10.0 11.7 12.0 12.3Inventory days 58.1 58.0 58.0 60.0Debtor days 30.3 30.0 30.0 33.0Creditor days 50.0 48.0 48.0 45.0Return Ratios (%)RoE 32.5 36.6 35.6 35.4RoCE 44.9 50.4 47.6 46.6RoIC 28.8 34.9 34.9 31.3Valuation Ratios (x)P/E 58.4 44.4 38.8 34.2EV / EBITDA 39.6 30.0 27.1 24.7EV / Net Sales 5.8 5.2 4.6 4.2Market Cap / Sales 5.8 5.2 4.6 4.2Price to Book Value 17.2 14.6 12.4 11.2Solvency RatiosDebt/EBITDA 0.0 0.0 0.0 0.0Debt / Equity 0.0 0.0 0.0 0.0Current Ratio 1.5 1.3 1.4 1.5Quick Ratio 0.8 0.7 0.7 0.8

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 9

ICICIdirect.com coverage universe (Consumable) CMP M Cap(|) TP(|) Rating (| Cr) FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E FY15E FY16E FY17E

Asian Paints (ASIPAI) 850 951 Buy 81,532 19.1 21.9 24.9 44.4 38.8 34.2 27.8 25.0 22.8 50.4 47.6 46.6 36.6 35.6 35.4Bajaj Electricals (BAJELE) 175 327 Buy 2,324 -1.4 10.2 14.0 0.0 22.9 16.7 30.0 10.2 8.6 5.6 20.8 22.9 -2.0 13.5 16.2Havells India (HAVIND) 276 315 Hold 17,220 6.2 8.0 10.2 44.7 34.4 27.0 23.2 19.0 18.2 29.3 33.0 35.5 21.2 24.3 27.3Pidilite Industries (PIDIND) 556 645 Buy 28,503 10.0 13.9 15.9 55.6 40.1 35.0 36.7 25.6 22.4 29.4 38.1 38.6 22.9 27.6 27.8Essel Propack (ESSPAC) 151 160 Hold 2,372 9.0 11.5 13.2 16.9 13.1 11.5 7.7 6.3 5.5 17.7 21.0 22.6 18.0 19.3 19.7Symphony Ltd (SYMCOM) 2,118 2,745 Buy 7,408 33.1 33.5 58.7 63.9 63.2 36.1 55.3 48.7 27.3 38.7 36.8 50.0 35.3 29.7 39.5V-Guard Ind (VGUARD) 913 880 Hold 2,725 23.7 32.2 37.8 38.5 28.4 24.1 21.0 17.5 15.2 26.7 28.0 28.1 18.7 21.3 21.1Voltas Ltd (VOLTAS) 276 384 Buy 9,128 11.6 11.5 12.6 23.8 24.0 21.9 20.8 17.6 15.0 17.0 17.3 18.0 16.6 15.8 16.3

Sector / CompanyRoE (%)EPS (|) P/E (x) EV/EBITDA (x) RoCE (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 10

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction; Buy: >10%/15% for large caps/midcaps, respectively; Hold: Up to +/-10%; Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk, ICICI Securities Limited, 1st Floor, Akruti Trade Centre, Road No 7, MIDC, Andheri (East) Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 11

ANALYST CERTIFICATION We /I, Sanjay Manyal, MBA (Finance) and Hitesh Taunk, MBA (Finance), Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures: ICICI Securities Limited is a SEBI registered Research Analyst having registration no. INH000000990. ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com. ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances. This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction. ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months. ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any material conflict of interest at the time of publication of this report. It is confirmed that Sanjay Manyal, MBA (Finance) and Hitesh Taunk, MBA (Finance), Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. ICICI Securities or its subsidiaries collectively or Research Analysts do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report. Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. It is confirmed that Sanjay Manyal, MBA (Finance) and Hitesh Taunk, MBA (Finance), Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report. ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report. We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.