asia-pac telecom tracker -...

TRANSCRIPT

Deutsche Bank Markets Research

Asia

Telecommunications

Industry

Asia-Pac Telecom tracker

Date

31 March 2016

Periodical

Fears eroding, value remains

New entrant and regulatory fear easing, time to buy GARPy telcos

________________________________________________________________________________________________________________

Deutsche Bank AG/Hong Kong

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 124/04/2015.

Peter Milliken, CFA

Research Analyst

(+852 ) 2203 6190

Top picks

China Telecom Corp (0728.HK),HKD4.05 Buy

Bharti Airtel Limited (BRTI.BO),INR354.90 Buy

SK Telecom (017670.KS),KRW209,500.00 Buy

PLDT (TEL.PS),PHP1,979.00 Buy

SoftBank (9984.T),¥5,436 Buy

Source: Deutsche Bank

This is the second of our Tracker reports, which provide a snapshot on valuation, street positioning, momentum, and business trends. We conclude that the fears that have held back many telco stocks are fading, which should allow the attractive valuations of these generally higher growth telcos to now attract attention. We believe GARP is underpriced currently, and suggest investors skew positions towards BRTI, IDEA, CT and CM, CITIC Tel, DTAC, LGU, PLDT, SKT and to an extent Softbank.

December quarter trends Consensus earnings have generally declined since our last Tracker, but fears over new entrants, spectrum costs, and price controls have eased, allowing the telco index to rise 2% since our last Tracker, following recent gains. Better performers have been in more competitive markets that showed profit improvement, such as XL, ISAT, NTT, Docomo and HKT.

Key themes to pursue and consider We prefer the following themes: 1) Profit convergence – with high profit markets (MY, TH, SG, AU) coming under competitive and regulatory pressure, and low profit markets being repaired (ID, IN, KR, CH fixed). 2) Restructuring preferred (CT, CU, PLDT, DTAC, SKT), 3) Growth over dividends – as growth is cheaper and in our view, 4) Data monetization. We expect telcos to get through 4G build-out pain, and achieve data monetization. Bharti, CT, ISAT, LGU, SKT, PLDT and XL appear to have a solid combination of network in place and operating leverage to add value from this trend And 5) Valuation lift, as falling risk-free rates mean that DY less the local 10-year bonds are at sharply higher levels than pre-GFC – as highlighted in our March 10 sector report, To Infinity and Beyond.

Fears fade Fear has ruled the sector. We have been discussing the risks of new entrants and government involvement for 18 months, specifically in our Rate Risk and New Alpha Champions FITT reports. We believe these fears are now more than in the price, and we have seen new entrant risk drop in TH and PH, and government price controls ease as a fear in China and Japan. We believe data monetization is starting to come through – and that hype on IoT, digital content and e-commerce will build. We expect the sector to rise 40%+ to prior peaks on data monetization, digital services belief, and IoT. Our top picks are Bharti, CT, PLDT, SKT and Softbank. We suggest investors reduce exposure to high-payout names, which tend to be at historically high multiples.

Valuation and risks We value the telecoms on DCF, and the holdcos on SOTP. Our WACCs are typically based on local 10-year bonds, with risk premiums of 4.5%-5.5%, and terminal growth rates of 0%-2%. Key downside risks include: 1) Interest rates rebounding, cutting sector value, 2) Competition worsening, 3) Risk of spectrum pricing rising on competitive or regulatory change. Key upside risks include: 1) Hype on IoT, e-commerce, and data monetization driving earnings estimates and multiples, and 2) Low, and even negative, interest rates leading to an upward squeeze in valuations.

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 2 Deutsche Bank AG/Hong Kong

Key issues by market

Generally positive

The market is currently fixated on the negatives in each country. Our

discussions tend to be on why investors should be interested in the various

telcos we’re recommending, despite commonly held concerns. This to us

indicates the market is overly-pessimistic, and opportunity exists.

Figure 1: Key debates

Market Key issue Opportunity Our take

。Rising competition 。Optus network better, TLS worse

。TLS network outages 。TLS reinvestment 。TLS under pressure to invest NBN cash well

TLS DPS at risk in LT, but supportive ST

。Govt. price setting 。Lighter touch in 2016 / data monetization

。CT & CU cooperation 。CT & CU to catch up on CM, take share slowly

Bundling/CU co-operation, position CT well

。OTT & HKBN-led 。HKT to avoid BB price war, but under pressure

。Mobile repricing 。Mobile profits to step up

HKT integrating CSL well, but mobile preferred

。Jio launch 。Consolidation 。Jio a force for consolidation

。Data-led growth 。Data-led profit growth expected

Oligopoly developing, Bharti well placed

。Interconnect change 。Rising pricing 。IC not a big issue, sector profitability improving

。Network sharing 。XL and ISAT narrowing quality gap to Tsel

Profit focus encourages, but ISAT, XL have run up

。Govt. price setting 。Above average earnings risk

。Bond to equity switch 。More yield compression due

Could squeeze up in NIRP world to 30x P/Es

。ARPU stickiness 。Sector becoming more profit focused

。Content 。Content monetization to show through ahead

Shareholder alignment bubbling under. Add

。Rising competition 。N/A 。#4 becoming credible threat

。Spectrum 。Spectrum to be auctioned

Avoid mobile sector. TM strongly preferred

。New entrant 。Low legacy revenues/ mkt to grow > share loss

。PLDT digital pivot 。PLDT well positioned off low earnings

PLDT's US$0.5bn 2016 NPAT, low vs. peers. BUY

。New entrant 。Mobile pressure, but in the price

。N/A 。New entrant to struggle, but destabilize

BUY Singtel, but for EM and Oz opportunity

。New entrants next move 。Price rises 。$499 plans hurting mobile and fixed BB volume

。$499 plans deflationary 。Consolidation 。Price rise due by May

Yield compression play, but weak earnings

。AIS and DTAC losing 。JVs with TOT & CAT 。AIS and DTAC resolving issues

。JAS and True weakened 。JAS weakened, True over-invested

DTAC upside high on spectrum/infra solution

Australia

China

HK

India

Indonesia

Japan

Phils

Singapore

Taiwan

Thailand

Malaysia

Korea

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 3

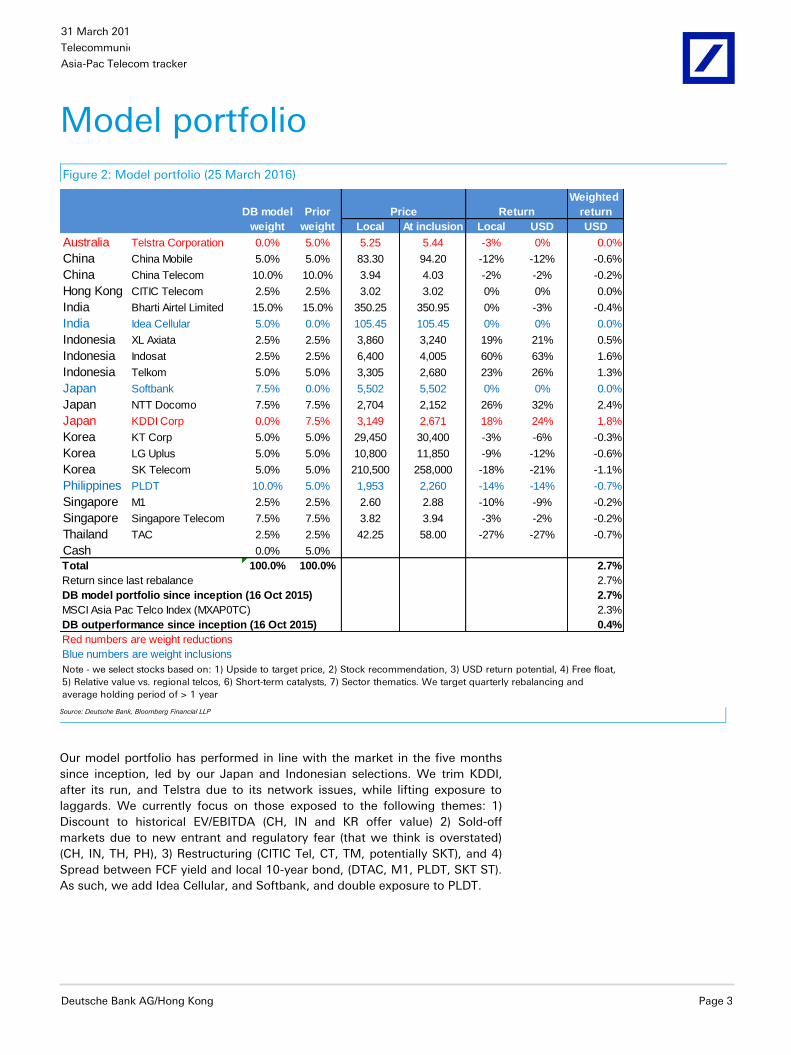

Model portfolio

Figure 2: Model portfolio (25 March 2016)

Weighted

DB model Prior return

weight weight Local At inclusion Local USD USD

Australia Telstra Corporation 0.0% 5.0% 5.25 5.44 -3% 0% 0.0%

China China Mobile 5.0% 5.0% 83.30 94.20 -12% -12% -0.6%

China China Telecom 10.0% 10.0% 3.94 4.03 -2% -2% -0.2%

Hong Kong CITIC Telecom 2.5% 2.5% 3.02 3.02 0% 0% 0.0%

India Bharti Airtel Limited 15.0% 15.0% 350.25 350.95 0% -3% -0.4%

India Idea Cellular 5.0% 0.0% 105.45 105.45 0% 0% 0.0%

Indonesia XL Axiata 2.5% 2.5% 3,860 3,240 19% 21% 0.5%

Indonesia Indosat 2.5% 2.5% 6,400 4,005 60% 63% 1.6%

Indonesia Telkom 5.0% 5.0% 3,305 2,680 23% 26% 1.3%

Japan Softbank 7.5% 0.0% 5,502 5,502 0% 0% 0.0%

Japan NTT Docomo 7.5% 7.5% 2,704 2,152 26% 32% 2.4%

Japan KDDI Corp 0.0% 7.5% 3,149 2,671 18% 24% 1.8%

Korea KT Corp 5.0% 5.0% 29,450 30,400 -3% -6% -0.3%

Korea LG Uplus 5.0% 5.0% 10,800 11,850 -9% -12% -0.6%

Korea SK Telecom 5.0% 5.0% 210,500 258,000 -18% -21% -1.1%

Philippines PLDT 10.0% 5.0% 1,953 2,260 -14% -14% -0.7%

Singapore M1 2.5% 2.5% 2.60 2.88 -10% -9% -0.2%

Singapore Singapore Telecom 7.5% 7.5% 3.82 3.94 -3% -2% -0.2%

Thailand TAC 2.5% 2.5% 42.25 58.00 -27% -27% -0.7%

Cash 0.0% 5.0%

Total 100.0% 100.0% 2.7%

Return since last rebalance 2.7%

DB model portfolio since inception (16 Oct 2015) 2.7%

MSCI Asia Pac Telco Index (MXAP0TC) 2.3%

DB outperformance since inception (16 Oct 2015) 0.4%

Red numbers are weight reductions

Blue numbers are weight inclusions

ReturnPrice

Note - we select stocks based on: 1) Upside to target price, 2) Stock recommendation, 3) USD return potential, 4) Free float,

5) Relative value vs. regional telcos, 6) Short-term catalysts, 7) Sector thematics. We target quarterly rebalancing and

average holding period of > 1 year Source: Deutsche Bank, Bloomberg Financial LLP

Our model portfolio has performed in line with the market in the five months

since inception, led by our Japan and Indonesian selections. We trim KDDI,

after its run, and Telstra due to its network issues, while lifting exposure to

laggards. We currently focus on those exposed to the following themes: 1)

Discount to historical EV/EBITDA (CH, IN and KR offer value) 2) Sold-off

markets due to new entrant and regulatory fear (that we think is overstated)

(CH, IN, TH, PH), 3) Restructuring (CITIC Tel, CT, TM, potentially SKT), and 4)

Spread between FCF yield and local 10-year bond, (DTAC, M1, PLDT, SKT ST).

As such, we add Idea Cellular, and Softbank, and double exposure to PLDT.

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 4 Deutsche Bank AG/Hong Kong

Top picks

Our sector thoughts were outlined in To Infinity and Beyond, published March

10tth, which highlighted how the telco sector value is increasing, along with

falling risk-free-rates. Valuation multiples should be higher in this cycle,

because of the lower WACCs, so we believe new highs can be made in the

telco index, offering 40%+ upside. Generally, high pay-out telcos are richly

priced vs. history, but lower pay-out, higher growth offers value. We expect

that value to be realized when investors see signs of earnings improving, as

data monetization comes through. We recommend to buy GARP, such as the

five stocks below, while among small caps, we are very keen on CITIC Tel.

Bharti Airtel

We expect Jio to be a force for consolidation, driving the sector towards more

of an oligopoly than the more perfect competition of today. Bharti’s relatively

strong spectrum position, and superior franchise, positions it to succeed

despite Jio’s likely pricing pressure. In USD market cap, and EV/EBITDA it is

coming off multi-year lows.

China Telecom

One standard deviation cheap on EV/EBITDA, and not far from the 3x multiple

it has bounced strongly off in the past. The cooperation with Unicom should

lift its competitive positioning, and we expect it and Unicom to benefit from

the triple driver of TowerCo, MNP and our expectation of a full merger, which

we believe can add 50-60% in value combined in the medium-term.

PLDT

2016 earnings are likely to be a low, as the company’s efforts to rebuild to

become the premium network and content provider pay-off. At 5%+ DY on just

a 75% pay-out ratio, and likely trough earnings, we like the company. The

Philippines also looks better insulated to a China slowdown, than most.

SK Telecom

A value play, with its DY yield premium to government bonds trading 1 s.d.

cheap. SK Telecom can benefit from content and video-led ARPU growth, from

the sector effort to lift profitability, which started with the Handset Distribution

Bill, and from improving its corporate structure, which is a consideration.

Softbank

We believe it will benefit from two technical drivers, the ¥500bn buy-back,

which should soak up around 7-8% of shares, and May’s MSCI rebalance,

which should drive up key asset, Alibaba, with we estimate 11 days buying

required. The caveat to this is that the stock’s discount to SOTP has narrowed

to below average levels, making this more a short-term top pick.

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 5

Street Positioning

The Street sees most upside in Chinese, Korean and Indian telcos, and least in

Malaysia, Taiwan and Indonesia. This may partly reflect that TW and ID telcos

have performed well, while CH, KR and IN telcos have been weak.

Figure 3: Companies Vs Consensus Rec Score

0

1

2

3

4

5

6

Ch M

ob

HK

T

SK

T

KT C

orp

NTT

CIT

IC

TLK

M

Sin

gte

l

LG

U

Ch T

el

XL

Indosat

KD

DI

Ch U

ni

AIS

Bharti

Docom

o

Glo

be

Idea

FE

T

Tw

n M

ob

M1

Chunghw

a

Axia

ta

Tel M

al

PLD

T

DTA

C

Tels

tra

Rel C

om

Sta

rhub

Jasm

ine

Source: Deutsche Bank, Bloomberg Financial LLP

Figure 4: Street recommendations

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ch M

ob

HK

T

CIT

IC

SK

T

KT C

orp

TLK

M

NTT

M1

Ch T

el

XL

LG

U

DTA

C

Bharti

KD

DI

Ch U

ni

Indosat

PLD

T

Idea

Sta

rhub

Docom

o

Chunghw

a

Sin

gte

l

FE

T

Jasm

ine

AIS

Axia

ta

Tels

tra

Rel C

om

Glo

be

Maxis

Tel M

al

Tw

n M

ob

Sell

Hold

Buy

Source: Deutsche Bank, , Bloomberg Financial LLP

Figure 5: TP upside/downside

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

SK

T

Ch M

ob

Idea

Rel C

om

CIT

IC

Ch U

ni

Ch te

l

KT C

orp

NTT

LG

U

XL

KD

DI

Sin

gte

l

HK

T

TLK

M

Docom

o

M1

Bharti

Axia

ta

Tels

tra

Sta

rhub

Jasm

ine

Tel M

al

Tw

n M

ob

AIS

FE

T

Glo

be

Indosat

PLD

T

Chunghw

a

DTA

C

Maxis

Source: Deutsche Bank, Bloomberg Financial LLP

The sector is generally well

loved by the Street – but

TWM and TM lacking buyers

– and telcos in AU, MY, TH

and TW failing to generate

much interest

The sector remains well loved

by the Street – We are

generally in line with the

Street - but are more bullish

on DTAC, PLDT and TM, and

less bullish on HKT and KT

Street appears to be expecting valuation

multiples to both normalize and

converge, rising in China, while most

other telcos track earnings growth

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 6 Deutsche Bank AG/Hong Kong

Earnings beats and misses

Figure 6: Prior quarter EBITDA vs consensus Figure 7: Prior quarter revenue vs. consensus

0%

20%

40%

60%

80%

100%

120%

AIS

Chunghw

a

DTA

C

Sin

gte

l

KT C

orp

Maxis

Sta

rhub

Rel C

om

Tels

tra

M1

PLD

T

DiG

i

Ch M

ob

CIT

IC

SK

T

Ch T

el

HK

T

LG

U

Tw

n M

ob

Axia

ta

Bharti

Indosat

Docom

o

NTT

Tel m

al

KD

DI

TLK

M

Glo

be

SoftB

ank

XL

FE

T

Idea

Jasm

ine

80%

85%

90%

95%

100%

105%

KD

DI

Sin

gte

l

DTA

C

AIS

KT c

orp

Chunghw

a

Rel C

om

Maxis

FE

T

LG

U

SK

T

Docom

o

TW

n M

ob

Bharti

Indosat

XL

TLK

M

Idea

Source: Deutsche Bank, , Bloomberg Financial LLP

Source: Deutsche Bank, , Bloomberg Financial LLP

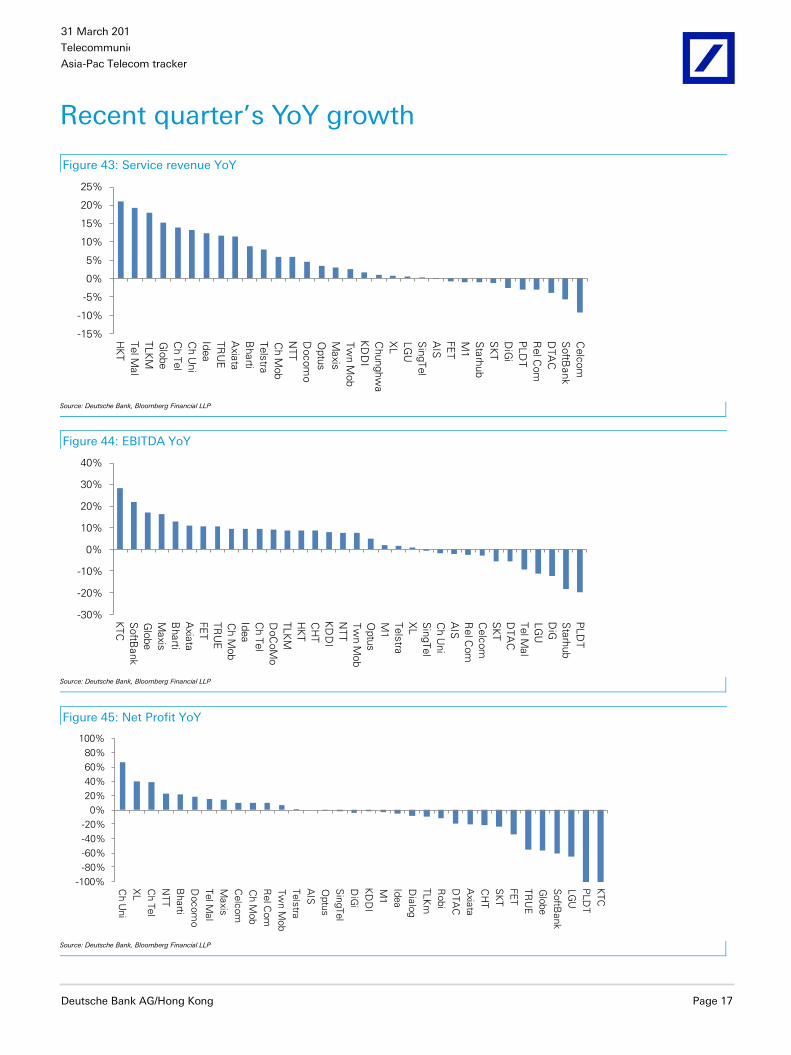

Interestingly, Japanese telcos, which have been consistently

delivering, have started to slightly miss consensus, while operators

undergoing sector or corporate repair, such as the Indian operators,

Maxis, KT and Indosat beat consensus.

Chinese telcos disappointed the market, but were generally on our

forecasts, with CM stronger than we expected, we have been

consistently arguing that 4G ramp up costs would be a much bigger

drag that the market anticipated.

Stocks that have consistently been favorite of ours (but not the Street),

CITIC and Docomo have seen EPS forecasts lifted most – while mature

fixed line operators are also defying the general EPS cuts across the

sector. PLDT had the most disappointing earnings season, given its

2016 guidance for an 18% earnings drop– before rebounding on

Telstra’s decision to not invest in the third operator. AIS and DTAC

have seen their EPS forecasts cut sharply following the spectrum

auction debacle, which now seems to be turning up. LGU had sharply

higher earnings growth baked, in, which was always going to difficult

to deliver on.

Figure 8: 3M consensus EPS change

-35%-30%-25%-20%-15%-10%

-5%0%5%

10%

CIT

IC

Docom

o

KT C

orp

NTT

HK

T

Chunghw

a

TLK

M

KD

DI

Sin

gte

l

Tels

tra

Tw

n M

ob

Axia

ta

M1

Maxis

FE

T

Sta

rhub

Glo

be

Tel M

al

Ch U

ni

XL

Ch M

ob

Bharti

Idea

Indosat

Rel C

om

LG

U

PLD

T

SK

T

Ch T

el

AIS

DTA

C

Source: Deutsche Bank, Bloomberg Financial LLP

The unloved mature market

fixed-line focused operators

– the only operators to see

EPS lifts in the quarter

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 7

Sector valuation

Figure 9: MSCI Asia Pac ex Japan Telecom P/E Figure 10: MSCI Asia Pac Telecom P/E

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank, Bloomberg Finance LP

Source: Deutsche Bank, Bloomberg Finance LP

Sector valuation is half a standard deviation above average, but ex the GFC-

through-EFC, valuations are below average, and we remind investors that 2G,

ADSL, and 3G/iPhone excitement led to much higher index levels in prior

cycles that we expect to be revisited in the medium-term as IoT, digital

content, e-commerce and 4G data monetization become a sector focus. While

Japan has had a strong run, Asia-Pac ex Japan telcos have generally not

moved much in recent years. We note that the telco DY premium to utilities is

the narrowest in several years, so telcos are relatively expensive vs. utilities vs.

their history – but this may reflect utility capex and opex rises ahead as they

move to less-polluting plant.

The telco stand out globally has been Japan, which now looks relatively

expensive, but buy-backs and negative rates should be supportive.

Figure 11: Fwd DY of Asian telcos vs. utilities and REITs Figure 12: Telecom prices of Asia vs. EU vs. US vs. JPN

0%

1%

2%

3%

4%

5%

6%

Oct-

12

Feb-1

3

Jun-1

3

Oct-

13

Feb-1

4

Jun-1

4

Oct-

14

Feb-1

5

Jun-1

5

Oct-

15

Feb-1

6

REITS

Telcos

Utilities

60

110

160

210

260

310

Oct-

12

Feb-1

3

Jun-1

3

Oct-

13

Feb-1

4

Jun-1

4

Oct-

14

Feb-1

5

Jun-1

5

Oct-

15

Feb-1

6

JPN

Asia

EU

US

Source: Deutsche Bank, Bloomberg Financial LLP

Source: Deutsche Bank, Bloomberg Financial LLP

Valuation fair – and we expect it to

cycle up on 4G/ IoT excitement

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 8 Deutsche Bank AG/Hong Kong

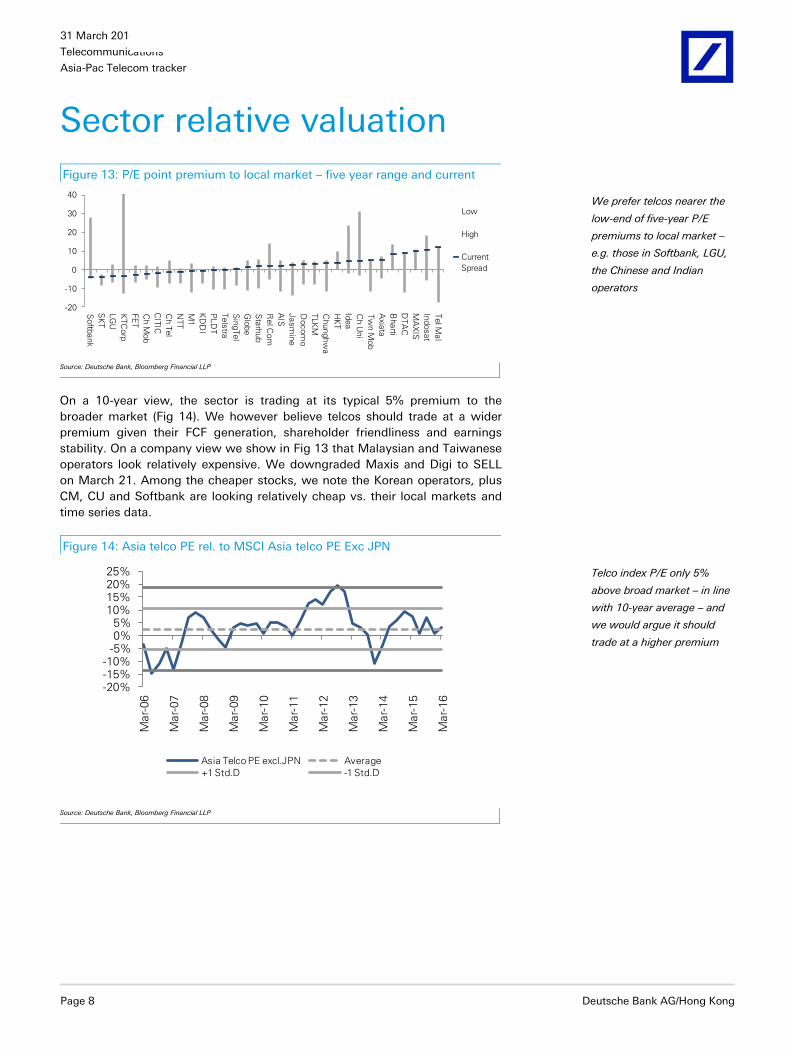

Sector relative valuation

Figure 13: P/E point premium to local market – five year range and current

-20

-10

0

10

20

30

40

Softb

ank

SK

T

LG

U

KTC

orp

FE

T

Ch M

ob

CIT

IC

Ch T

el

NTT

M1

KD

DI

PLD

T

Tels

tra

Sin

gTel

Glo

be

Sta

rhub

Rel C

om

AIS

Jasm

ine

Docom

o

TLK

M

Chunghw

a

HK

T

Idea

Ch U

ni

Tw

n M

ob

Axia

ta

Bharti

DTA

C

MA

XIS

Indosat

Tel M

al

Low

High

Current

Spread

Source: Deutsche Bank, Bloomberg Financial LLP

On a 10-year view, the sector is trading at its typical 5% premium to the

broader market (Fig 14). We however believe telcos should trade at a wider

premium given their FCF generation, shareholder friendliness and earnings

stability. On a company view we show in Fig 13 that Malaysian and Taiwanese

operators look relatively expensive. We downgraded Maxis and Digi to SELL

on March 21. Among the cheaper stocks, we note the Korean operators, plus

CM, CU and Softbank are looking relatively cheap vs. their local markets and

time series data.

Figure 14: Asia telco PE rel. to MSCI Asia telco PE Exc JPN

-20%-15%-10%

-5%0%5%

10%15%20%25%

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Asia Telco PE excl.JPN Average

+1 Std.D -1 Std.D

Source: Deutsche Bank, Bloomberg Financial LLP

We prefer telcos nearer the

low-end of five-year P/E

premiums to local market –

e.g. those in Softbank, LGU,

the Chinese and Indian

operators

Telco index P/E only 5%

above broad market – in line

with 10-year average – and

we would argue it should

trade at a higher premium

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 9

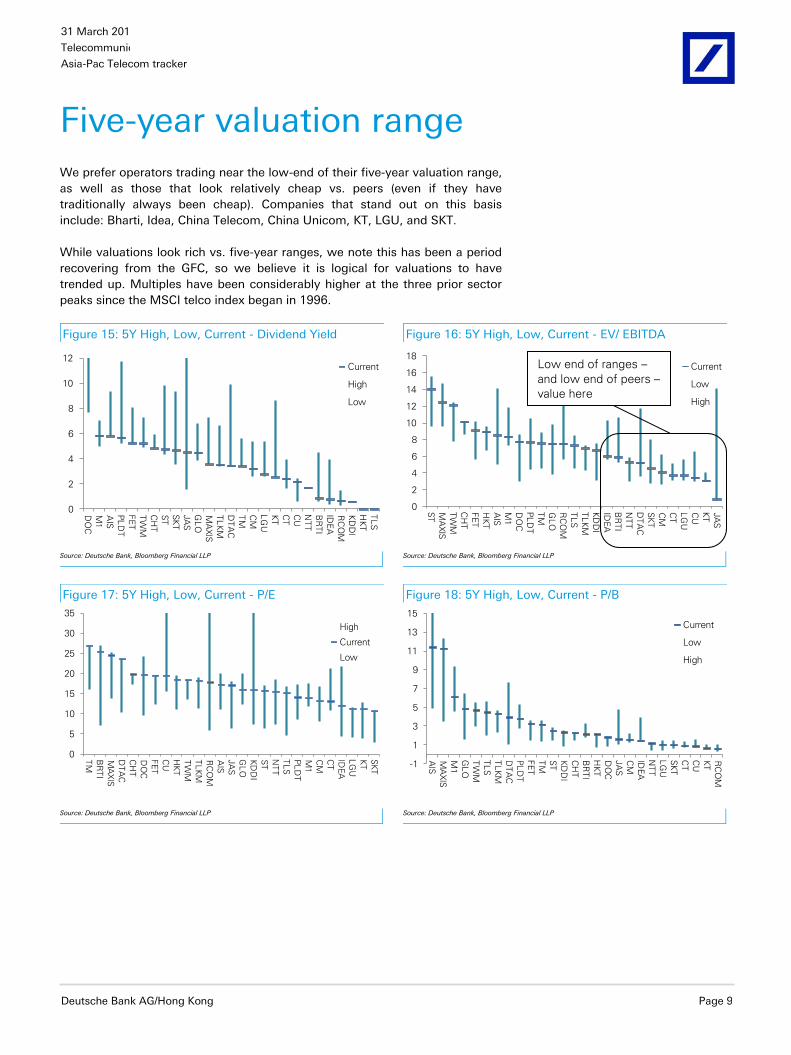

Five-year valuation range

We prefer operators trading near the low-end of their five-year valuation range,

as well as those that look relatively cheap vs. peers (even if they have

traditionally always been cheap). Companies that stand out on this basis

include: Bharti, Idea, China Telecom, China Unicom, KT, LGU, and SKT.

While valuations look rich vs. five-year ranges, we note this has been a period

recovering from the GFC, so we believe it is logical for valuations to have

trended up. Multiples have been considerably higher at the three prior sector

peaks since the MSCI telco index began in 1996.

Figure 15: 5Y High, Low, Current - Dividend Yield Figure 16: 5Y High, Low, Current - EV/ EBITDA

0

2

4

6

8

10

12

DO

C

M1

AIS

PL

DT

FE

T

TW

M

CH

T

ST

SK

T

JA

S

GL

O

MA

XIS

TL

KM

DT

AC

TM

CM

LG

U

KT

CT

CU

NT

T

BR

TI

IDE

A

RC

OM

KD

DI

HK

T

TL

S

Current

High

Low

0

2

4

6

8

10

12

14

16

18S

T

MA

XIS

TW

M

CH

T

FE

T

HK

T

AIS

M1

DO

C

PL

DT

TM

GL

O

RC

OM

TL

S

TL

KM

KD

DI

IDE

A

BR

TI

NT

T

DT

AC

SK

T

CM

CT

LG

U

CU

KT

JA

S

Current

Low

High

Source: Deutsche Bank, Bloomberg Financial LLP

Source: Deutsche Bank, Bloomberg Financial LLP

Figure 17: 5Y High, Low, Current - P/E Figure 18: 5Y High, Low, Current - P/B

0

5

10

15

20

25

30

35

TM

BR

TI

MA

XIS

DT

AC

CH

T

DO

C

FE

T

CU

HK

T

TW

M

TL

KM

RC

OM

AIS

JA

S

GL

O

KD

DI

ST

NT

T

TL

S

PL

DT

M1

CM

CT

IDE

A

LG

U

KT

SK

T

High

Current

Low

-1

1

3

5

7

9

11

13

15

AIS

MA

XIS

M1

GL

O

TW

M

TL

S

TL

KM

DT

AC

PL

DT

FE

T

TM

ST

KD

DI

CH

T

BR

TI

HK

T

DO

C

JA

S

CM

IDE

A

NT

T

LG

U

SK

T

CT

CU

KT

RC

OM

Current

Low

High

Source: Deutsche Bank, Bloomberg Financial LLP

Source: Deutsche Bank, Bloomberg Financial LLP

Low end of ranges –

and low end of peers –

value here

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 10 Deutsche Bank AG/Hong Kong

Sector performance

Upside and downside to prior highs and lows

We prefer telcos that have potential to rise sharply back to prior highs, rather

than those high in unchartered territory. The Chinese, Indian, Korean and

Philippine operators have greater upside to 52-week highs, while the Japanese

operators, Indosat and XL are stretched by recent standards. As can be seen

from Fig 20, the high-payout telcos in HK, TW and JP, are testing 10-year

highs.

Figure 19: Upside and downside to 52 week high and low

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

DTA

C

Idea

Rel C

om

Jasm

ine

Ch T

el

Ch U

ni

PLD

T

CIT

IC

Ch M

ob

SK

T

AIS

Glo

be

Bharti

Tels

tra

Axia

ta

LG

U

Sin

gte

l

Tel M

al

Maxis

XL

KT C

orp

NTT

Docom

o

KD

DI

HK

T

Tw

n M

ob

TLK

M

FE

T

Chunghw

a

Indosat

Upside Downside

Source: Deutsche Bank, Bloomberg Financial LLP

Figure 20: Upside and downside to 10-year high and low

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Rel C

om

DTA

C

Idea

Jasm

ine

XL

Ch T

el

PLD

T

Ch U

ni

Bharti

AIS

Ch M

ob

CIT

IC

KT C

orp

SK

T

Indosat

Glo

be

LG

U

Axia

ta

Tels

tra

Sin

gte

l

Maxis

Tel M

al

Docom

o

NTT

KD

DI

HK

T

TLK

M

FE

T

Tw

n M

ob

Chunghw

a

Upside Downside

Source: Deutsche Bank, Bloomberg Financial LLP

More upside to prior highs Substantially rerated

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 11

Sector Balance

Figure 21: Market Cap breakdown country-wise Figure 22: Profit share breakdown country-wise

TLS

CM

HK

T

BH

TI

TLK

M

NTT

SK

T

PLD

T

STE

L

CH

T

AIS

MA

X

OP

T

CT

HT

IDE

A

XL

DO

C

KT G

LO

STH

TW

M

TR

U

DIG

CU

SM

T

VO

D

ISAT

KD

DI

LG

U

M1

FE

T

TA

C

AX

RCOTH

SB

APT JASTM

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

AUS CHN HKG IND IDN JPN KOR PHP SGP TWN THL MLY

TLS

CM

HK

T

BH

TI TLK

M

NTT

SK

T

PLD

T

STE

L

CH

T

AIS

MA

X

OP

T

CT

HT

IDE

A

XL

DO

C

KT

GLO

STH

TW

M TRU

DIG

CUSMT

VOD

ISAT

KDDI LGU

M1

FET TAC

AX

RCOM

OTH

SB

APT

JAS TMOTH

-40%

-20%

0%

20%

40%

60%

80%

100%

AUS CHN HKG IND IDN JPN KOR PHP SGP TWN THL MLY

Source: Deutsche Bank

Source: Deutsche Bank

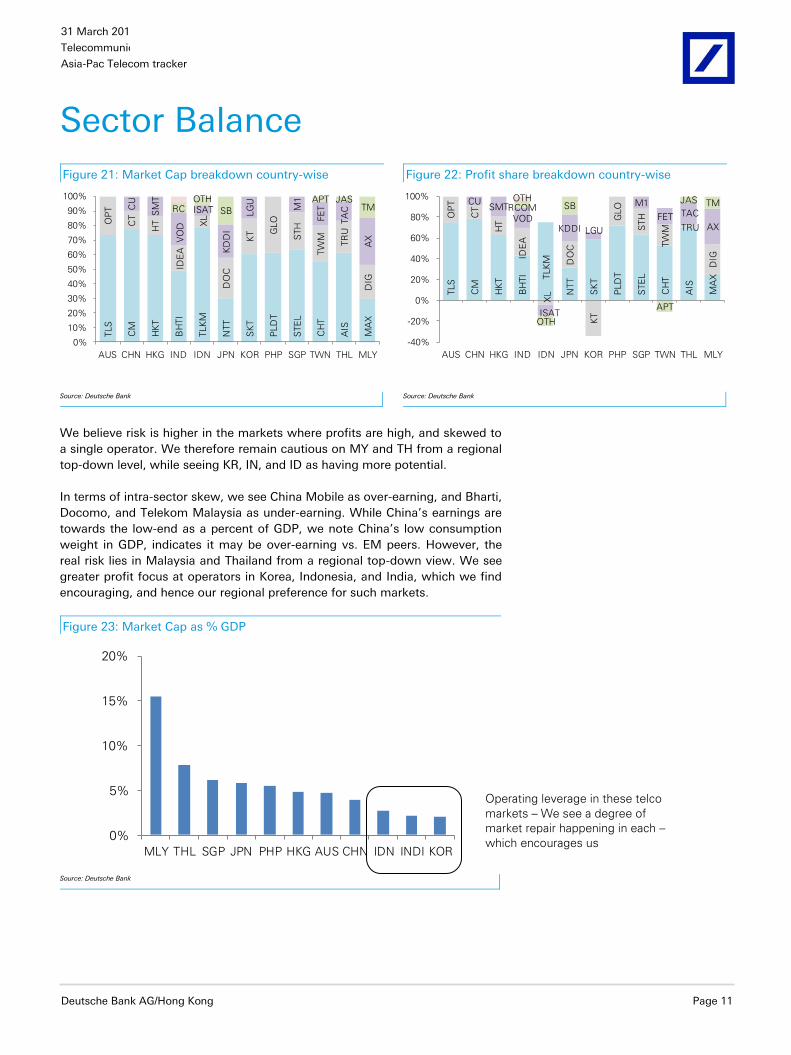

We believe risk is higher in the markets where profits are high, and skewed to

a single operator. We therefore remain cautious on MY and TH from a regional

top-down level, while seeing KR, IN, and ID as having more potential.

In terms of intra-sector skew, we see China Mobile as over-earning, and Bharti,

Docomo, and Telekom Malaysia as under-earning. While China’s earnings are

towards the low-end as a percent of GDP, we note China’s low consumption

weight in GDP, indicates it may be over-earning vs. EM peers. However, the

real risk lies in Malaysia and Thailand from a regional top-down view. We see

greater profit focus at operators in Korea, Indonesia, and India, which we find

encouraging, and hence our regional preference for such markets.

Figure 23: Market Cap as % GDP

0%

5%

10%

15%

20%

MLY THL SGP JPN PHP HKG AUS CHN IDN INDI KOR

Source: Deutsche Bank

Operating leverage in these telco

markets – We see a degree of

market repair happening in each –

which encourages us

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 12 Deutsche Bank AG/Hong Kong

Dividends

Figure 24: DY(bubble) vs. Real Yld(X) vs. Payout(Y) in DM Figure 25: DY(bubble) vs. Real Yld(X) vs. Payout(Y) in EM

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Payout

ratio

Premium over local 10Y

HKT

TWM

FET

TLS

CHT

ST

SKT

DOC

NTT

KT

KDDI

LGU

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-8.0% -5.0% -2.0% 1.0% 4.0% 7.0% 10.0%

Payout

Ratio

Premium over local 10Y

AIS

PLDT

GLO

CM

DTAC

TLKM

CT

CU

BRTI

IDEA

RCOM

Source: Deutsche Bank, Bloomberg Financial LLP

Source: Deutsche Bank, Bloomberg Financial LLP

We prefer operators that have high dividend yield premiums to the local 10-

year bonds, but room to lift payouts further. Docomo, PLDT, Singtel, SK

Telecom all look good to us on such measures.

We also note that growth tends to be picking up, which may lead to valuation

multiples rising - as valuation is basically price/(WACC-growth). We believe

telcos have been caught out by OTT, and priced data too low. We believe that

operators are now generally trying to monetize investments more aggressively,

and that earnings growth should follow, encouraging investors to pay higher

valuation multiples ahead, and driving more yield compression.

Figure 26: DY spread vs. DPS 3 yr CAGR Figure 27: EY spread vs. EPS 3 yr Backward CAGR

-8%-6%-4%-2%0%2%4%6%8%

10%

Oct-1

2

Feb-1

3

Jun-1

3

Oct-1

3

Feb-1

4

Jun-1

4

Oct-1

4

Feb-1

5

Jun-1

5

Oct-1

5

Feb-1

6

DY Spread DPS 3yr CAGR

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Oct-1

2

Feb-1

3

Jun-1

3

Oct-1

3

Feb-1

4

Jun-1

4

Oct-1

4

Feb-1

5

Jun-1

5

Oct-1

5

Feb-1

6

EY Spread EPS 3yr CAGR

Source: Deutsche Bank, Bloomberg Financial LLP

Source: Deutsche Bank, Bloomberg Financial LLP

Growth momentum turning up, which may

encourage investors to lift earnings yields

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 13

Drivers

Figure 28: Mobile ARPU (US$/month) Figure 29: Data as % of mobile service revenue

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Dec-1

2

Mar-

13

Jun-1

3

Sep-1

3

Dec-1

3

Mar-

14

Jun-1

4

Sep-1

4

Dec-1

4

Mar-

15

Jun-1

5

Sep-1

5

Dec-1

5

SKT US$

SingTel US$

Docomo US$

SmarTone US$

FET US$

Celcom US$

China Mobile US$

AIS US$

Bharti US$

Telkomsel US$

PLDT US$

0%

20%

40%

60%

80%

100%

120%

140%

160%

Ch T

el

Docom

o

Optu

s

XL

Sin

gTel

DIG

I

Bharti

Indosat

Source: Deutsche Bank, Company data

Source: Deutsche Bank, Company data

Figure 32: Mobile ARPU YoY 4Q15 –

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

KD

DI

AIS

TLK

M

DTA

C

Maxi

s

Ch U

ni

Docom

o

Chunghw

a

SK

T

Sta

rHub

TW

M

KTC

Soft

bank

Sin

gTel

Idea

FE

T

PLD

T

Celc

om

Bhart

i

DIG

I

LG

U

Indosat

Ch M

ob

Ch T

el

Glo

be

M1

TR

UE

Source: Deutsche Bank, Company data

Figure 30: Mobile net adds YoY (last reported quarter) Figure 31: Mobile net add breakdown (last quarter)

-4%

-2%

0%

2%

4%

6%

KO

R

IDN

AU

S

TW

N

IND

MLY

PH

P

HK

G

JP

N

SG

P

TH

L

CH

N

.

Optus CM Bharti Excl

Doc

KTDigi GLO M1

CHTAIS

Telstra

CT BSNLISAT

KDDI

LGU

Maxis

SmartSTEL

FET

DTAC

CU

Idea

Others

Softbank

SK Tel

STH

TWM

TRUE

Others

RCOM

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

AU

S

CH

N

IND

I

IDN

JP

N

KO

R

MLY

PH

P

SG

P

TW

N

TH

L

Source: Deutsche Bank, Company data

Source: Deutsche Bank, Company data

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 14 Deutsche Bank AG/Hong Kong

EBITDA margin trends

Figure 53: Australia Figure 54: China Figure 55: Hong Kong

0%

10%

20%

30%

40%

50%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

Telstra

0%

10%

20%

30%

40%

50%

60%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

China Mobile China Telecom China Unicom

0%

10%

20%

30%

40%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

HKT

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 56: India Figure 57: Indonesia Figure 58: Japan

0%

10%

20%

30%

40%

50%

60%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

Bharti Airtel Idea Cellular RCOM

0%

10%

20%

30%

40%

50%

60%

70%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

XL Axiata Telkom

0%

20%

40%

60%

80%

100%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

SoftBank NTT (fixed) NTT DoCoMo KDDI

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 59: Korea Figure 60: Malaysia Figure 61: Philippines

-50%

0%

50%

100%

150%

200%

250%

300%

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

KT Corporation LG Uplus SK Telecom

0%

10%

20%

30%

40%

50%

60%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

DiGi.Com Maxis

Telekom Malaysia Celcom

0%

10%

20%

30%

40%

50%

60%

70%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

Globe Telecom PLDT

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 62: Singapore Figure 63: Taiwan Figure 64: Thailand

0%

10%

20%

30%

40%

50%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

M1 Singtel Domestic Starhub

0%

10%

20%

30%

40%

50%

60%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

CHT Far EasTone TWM

0%

10%

20%

30%

40%

50%

60%

4Q

09

2Q

10

4Q

10

2Q

11

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

AIS DTAC True Corp

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 15

EBITDA by Country (in local currency billion)

Markets appearing to see margins improving, or near cyclical lows, include

China, Malaysia, Philippines and Thailand, while those appearing set to slow or

near margin peaks include India, Indonesia, Japan and Taiwan.

Figure 33: China Figure 34: India

-15%

-10%

-5%

0%

5%

10%

15%

0

20

40

60

80

100

120

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

CT

CU

CM

Total

-30%

-20%

-10%

0%

10%

20%

30%

0

20

40

60

80

100

120

140

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

RCOM

IDEA

BHRT

Total

Source: Deutsche Bank

Source: Deutsche Bank

Figure 35: Indonesia Figure 36: Japan

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

5,000

10,000

15,000

20,000

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

XL

ISAT

TLKM

Total

-10%

-5%

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

KDDI

DOC

NTT

(fixed)SB

Total

Source: Deutsche Bank

Source: Deutsche Bank

Figure 37: Korea Figure 38: Malaysia (Change TKOM to TM, D Gi to DIGI)

-60%

-40%

-20%

0%

20%

40%

60%

80%

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

LGU

KT

SKT

Total

-6%

-4%

-2%

0%

2%

4%

6%

8%

0

1

2

3

4

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

DIGI

CEL

TM

MAX

Total

Source: Deutsche Bank

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 16 Deutsche Bank AG/Hong Kong

Figure 39: Philippines Figure 40: Singapore

-10%

-5%

0%

5%

10%

15%

0

5

10

15

20

25

30

35

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

GLO

PLDT

Total

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

0.0

0.2

0.4

0.6

0.8

1.0

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

M1

STH

ST

dom

Total

Source: Deutsche Bank

Source: Deutsche Bank

Figure 41: Taiwan Figure 42: Thailand

-10%

-5%

0%

5%

10%

15%

0

5

10

15

20

25

30

35

40

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

TWM

FET

CHT

Total

-10%

-5%

0%

5%

10%

15%

0

5

10

15

20

25

30

35

4Q

11

2Q

12

4Q

12

2Q

13

4Q

13

2Q

14

4Q

14

2Q

15

4Q

15

TRUE

DTAC

AIS

Total

Source: Deutsche Bank

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 17

Recent quarter’s YoY growth

Figure 43: Service revenue YoY

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

HK

T

Tel M

al

TLK

M

Glo

be

Ch T

el

Ch U

ni

Idea

TR

UE

Axia

ta

Bharti

Tels

tra

Ch M

ob

NTT

Docom

o

Optu

s

Maxis

Tw

n M

ob

KD

DI

Chunghw

a

XL

LG

U

Sin

gTel

AIS

FE

T

M1

Sta

rhub

SK

T

DiG

i

PLD

T

Rel C

om

DTA

C

SoftB

ank

Celc

om

Source: Deutsche Bank, Bloomberg Financial LLP

Figure 44: EBITDA YoY

-30%

-20%

-10%

0%

10%

20%

30%

40%

KTC

SoftB

ank

Glo

be

Maxis

Bharti

Axia

ta

FE

T

TR

UE

Ch M

ob

Idea

Ch T

el

DoC

oM

o

TLK

M

HK

T

CH

T

KD

DI

NTT

Tw

n M

ob

Optu

s

M1

Tels

tra

XL

Sin

gTel

Ch U

ni

AIS

Rel C

om

Celc

om

SK

T

DTA

C

Tel M

al

LG

U

DiG

Sta

rhub

PLD

T

Source: Deutsche Bank, Bloomberg Financial LLP

Figure 45: Net Profit YoY

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Ch U

ni

XL

Ch T

el

NTT

Bharti

Docom

o

Tel M

al

Maxis

Celc

om

Ch M

ob

Rel C

om

Tw

n M

ob

Tels

tra

AIS

Optu

s

Sin

gTel

DiG

i

KD

DI

M1

Idea

Dia

log

TLK

m

Robi

DTA

C

Axia

ta

CH

T

SK

T

FE

T

TR

UE

Glo

be

SoftB

ank

LG

U

PLD

T

KTC

Source: Deutsche Bank, Bloomberg Financial LLP

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 18 Deutsche Bank AG/Hong Kong

Sector price performance

Figure 46: 1M Price performance –

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Idea

Rel C

om

Maxis

SK

T

M1

LG

U

Axia

ta

Bharti

Ch M

ob

CIT

IC

Sta

rhub

KTC

orp

KD

DI

Sin

gTel

Tel M

al

Jasm

ine

Ch M

ob

Ch T

el

Indosat

Tels

tra

Tw

n M

ob

Glo

be

XL

Chunghw

a

FE

T

DO

CO

MO

HK

T

NTT

PLD

T

DTA

C

AIS

Source: Deutsche Bank, Bloomberg Financial LLP

Figure 47: 3M Price performance

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

DTA

C

Jasm

ine

AIS

Idea

SK

T

LG

U

M1

Glo

be

Bharti

CIT

IC

Rel C

om

KTC

orp

Maxis

Sin

gTel

Ch T

el

Ch M

ob

Axia

ta

Ch M

ob

Sta

rhub

FE

T

Tw

n M

ob

Tel M

al

Chunghw

a

PLD

T

KD

DI

Tels

tra

DO

CO

MO

HK

T

NTT

XL

Indosat

Source: Deutsche Bank, Bloomberg Financial LLP

Figure 48: 12M Price performance

-80%

-60%

-40%

-20%

0%

20%

40%

60%

DTA

C

Jasm

ine

M1

Idea

AIS

SK

T

LG

U

Ch M

ob

PLD

T

XL

Bharti

Axia

ta

Ch T

el

Maxis

Sta

rhub

Rel C

om

Ch M

ob

Sin

gTel

KTC

orp

Tels

tra

FE

T

Tw

n M

ob

Tel M

al

HK

T

Chunghw

a

Glo

be

KD

DI

CIT

IC

DO

CO

MO

Indosat

NTT

Source: Deutsche Bank, Bloomberg Financial LLP

Fear of new entrants has

abated – as has been a strong

theme of ours – helping AIS,

DTAC and PLDT lead the

sector recently - we expect

Bharti can also do well ahead

as it holds up vs. Jio

The sector has been weak

due to fears of new entrants,

and bidding wars – but those

turning around tarnished

reputations have been

rewarded – e.g. XL and

Indosat – helped by price lifts

and regulatory improvement,

HKT on a successful CSL

integration, and the NTT

group on Docomo’s

turnaround

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 19

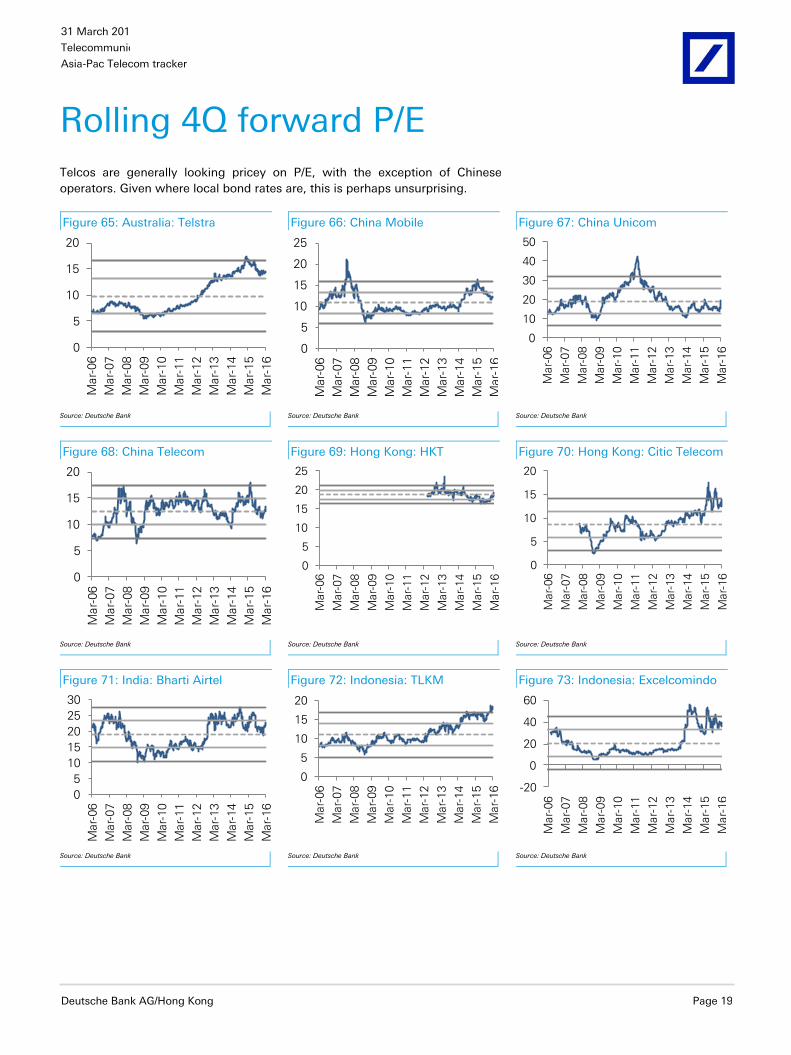

Rolling 4Q forward P/E

Telcos are generally looking pricey on P/E, with the exception of Chinese

operators. Given where local bond rates are, this is perhaps unsurprising.

Figure 65: Australia: Telstra Figure 66: China Mobile Figure 67: China Unicom

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

10

20

30

40

50

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 68: China Telecom Figure 69: Hong Kong: HKT Figure 70: Hong Kong: Citic Telecom

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 71: India: Bharti Airtel Figure 72: Indonesia: TLKM Figure 73: Indonesia: Excelcomindo

0

5

10

15

20

25

30

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

-20

0

20

40

60

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 20 Deutsche Bank AG/Hong Kong

Figure 74: Indonesia: Indosat Figure 75: Japan: NTT Figure 76: Japan: Docomo

0

10

20

30

40

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 77: Japan: KDDI Figure 78: Korea: SK Telecom Figure 79: Korea: LG Uplus

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

-10

-5

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 80: Korea: KT Corp Figure 81: Malaysia: Maxis Figure 82: Telkom Malaysia

-10

0

10

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

30

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

-10

0

10

20

30

40

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 83: Malaysia: Axiata Figure 84: Philippines: Globe Figure 85: Philippines: PLDT

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 21

Figure 86: Singapore: M1 Figure 87: Singapore Telecom Figure 88: Singapore: Starhub

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 89: Taiwan: CHT Figure 90: Taiwan: FET Figure 91: Taiwan Mobile

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 92: Thailand: Jasmine Figure 93: Thailand: DTAC Figure 94: Thailand: AIS

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

25M

ar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 22 Deutsche Bank AG/Hong Kong

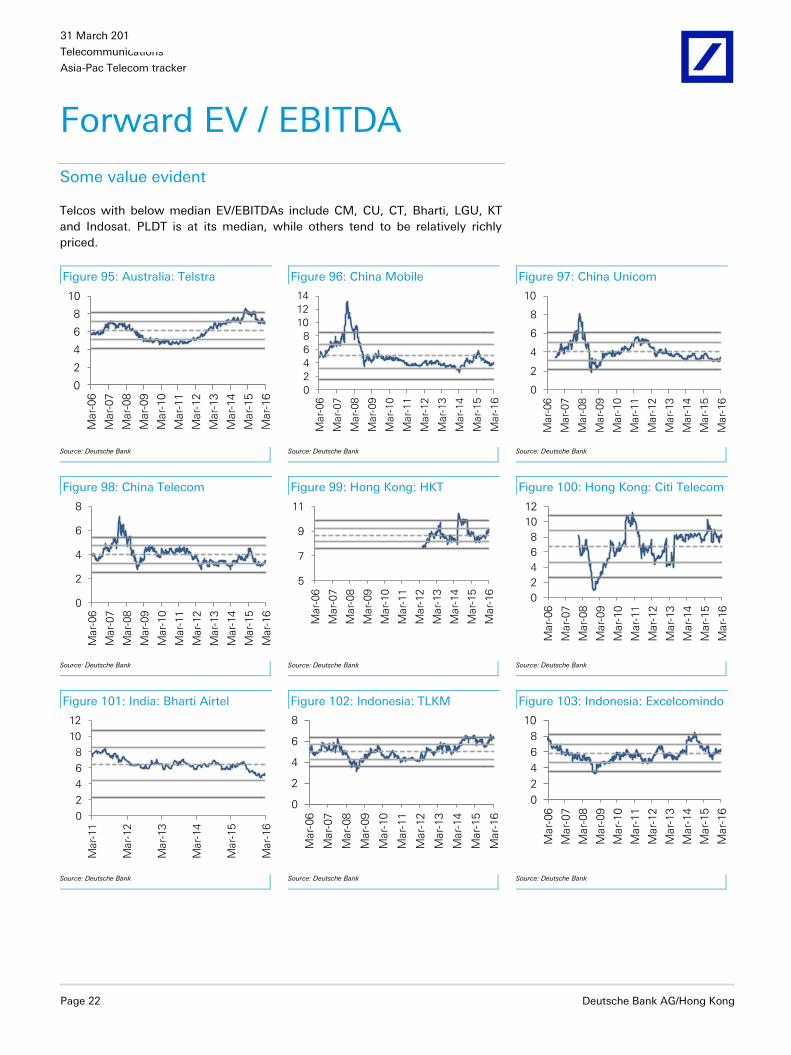

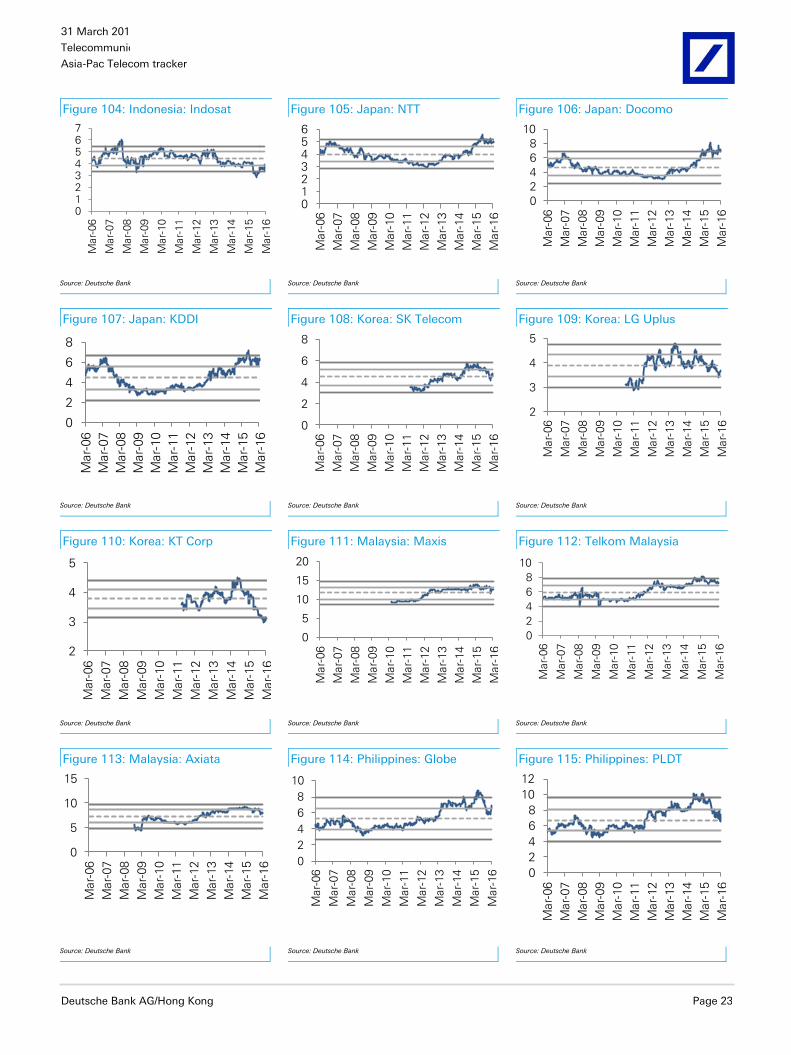

Forward EV / EBITDA

Some value evident

Telcos with below median EV/EBITDAs include CM, CU, CT, Bharti, LGU, KT

and Indosat. PLDT is at its median, while others tend to be relatively richly

priced.

Figure 95: Australia: Telstra Figure 96: China Mobile Figure 97: China Unicom

0

2

4

6

8

10

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

12

14

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 98: China Telecom Figure 99: Hong Kong: HKT Figure 100: Hong Kong: Citi Telecom

0

2

4

6

8

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

5

7

9

11

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

12

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 101: India: Bharti Airtel Figure 102: Indonesia: TLKM Figure 103: Indonesia: Excelcomindo

0

2

4

6

8

10

12

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Deutsche Bank AG/Hong Kong Page 23

Figure 104: Indonesia: Indosat Figure 105: Japan: NTT Figure 106: Japan: Docomo

01234567

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0123456

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 107: Japan: KDDI Figure 108: Korea: SK Telecom Figure 109: Korea: LG Uplus

0

2

4

6

8

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

2

3

4

5

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 110: Korea: KT Corp Figure 111: Malaysia: Maxis Figure 112: Telkom Malaysia

2

3

4

5

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 113: Malaysia: Axiata Figure 114: Philippines: Globe Figure 115: Philippines: PLDT

0

5

10

15

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

12

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

31 March 2016

Telecommunications

Asia-Pac Telecom tracker

Page 24 Deutsche Bank AG/Hong Kong

Figure 116: Singapore: M1 Figure 117: Singapore Telecom Figure 118: Singapore: Starhub

0

2

4

6

8

10

12

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

12

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 119: Taiwan: CHT Figure 120: Taiwan: FET Figure 121: Taiwan Mobile

0

2

4

6

8

10

12

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

2

4

6

8

10

12

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

20

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Figure 122: Thailand: Jasmine Figure 123: Thailand: DTAC Figure 124: Thailand: AIS

0

5

10

15

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

0

5

10

15

Mar-…

Mar-…

Mar-…

Mar-…

Mar-…

Mar-…

Mar-…

Mar-…

Mar-…

Mar-…

Mar-…

0

5

10

15

Mar-

06

Mar-

07

Mar-

08

Mar-

09

Mar-

10

Mar-

11

Mar-

12

Mar-

13

Mar-

14

Mar-

15

Mar-

16

Source: Deutsche Bank

Source: Deutsche Bank

Source: Deutsche Bank

Asia

-Pac T

ele

com

tracker

Tele

co

mm

un

icatio

ns

31

Marc

h 2

01

6

Deu

tsch

e B

an

k A

G/H

on

g K

on

g

Pag

e 2

5

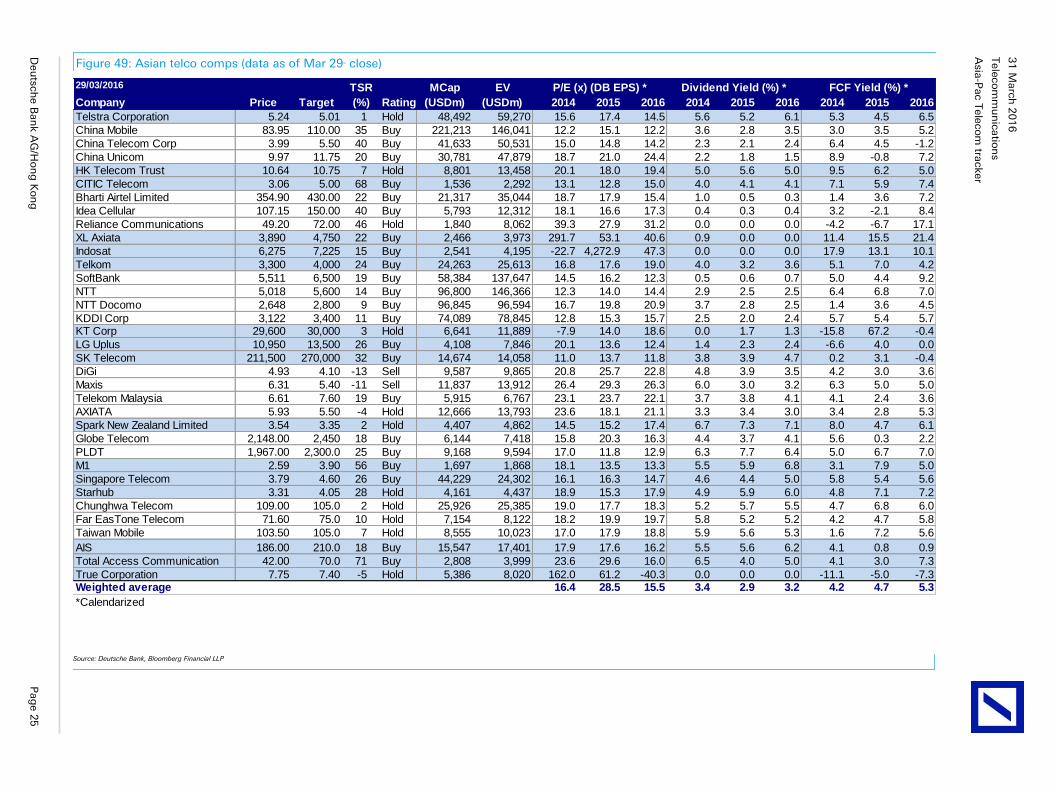

Figure 49: Asian telco comps (data as of Mar 29th close)

29/03/2016 TSR MCap EV

Company Price Target (%) Rating (USDm) (USDm) 2014 2015 2016 2014 2015 2016 2014 2015 2016

Telstra Corporation 5.24 5.01 1 Hold 48,492 59,270 15.6 17.4 14.5 5.6 5.2 6.1 5.3 4.5 6.5

China Mobile 83.95 110.00 35 Buy 221,213 146,041 12.2 15.1 12.2 3.6 2.8 3.5 3.0 3.5 5.2

China Telecom Corp 3.99 5.50 40 Buy 41,633 50,531 15.0 14.8 14.2 2.3 2.1 2.4 6.4 4.5 -1.2

China Unicom 9.97 11.75 20 Buy 30,781 47,879 18.7 21.0 24.4 2.2 1.8 1.5 8.9 -0.8 7.2

HK Telecom Trust 10.64 10.75 7 Hold 8,801 13,458 20.1 18.0 19.4 5.0 5.6 5.0 9.5 6.2 5.0

CITIC Telecom 3.06 5.00 68 Buy 1,536 2,292 13.1 12.8 15.0 4.0 4.1 4.1 7.1 5.9 7.4

Bharti Airtel Limited 354.90 430.00 22 Buy 21,317 35,044 18.7 17.9 15.4 1.0 0.5 0.3 1.4 3.6 7.2

Idea Cellular 107.15 150.00 40 Buy 5,793 12,312 18.1 16.6 17.3 0.4 0.3 0.4 3.2 -2.1 8.4

Reliance Communications 49.20 72.00 46 Hold 1,840 8,062 39.3 27.9 31.2 0.0 0.0 0.0 -4.2 -6.7 17.1

XL Axiata 3,890 4,750 22 Buy 2,466 3,973 291.7 53.1 40.6 0.9 0.0 0.0 11.4 15.5 21.4

Indosat 6,275 7,225 15 Buy 2,541 4,195 -22.7 4,272.9 47.3 0.0 0.0 0.0 17.9 13.1 10.1

Telkom 3,300 4,000 24 Buy 24,263 25,613 16.8 17.6 19.0 4.0 3.2 3.6 5.1 7.0 4.2

SoftBank 5,511 6,500 19 Buy 58,384 137,647 14.5 16.2 12.3 0.5 0.6 0.7 5.0 4.4 9.2

NTT 5,018 5,600 14 Buy 96,800 146,366 12.3 14.0 14.4 2.9 2.5 2.5 6.4 6.8 7.0

NTT Docomo 2,648 2,800 9 Buy 96,845 96,594 16.7 19.8 20.9 3.7 2.8 2.5 1.4 3.6 4.5

KDDI Corp 3,122 3,400 11 Buy 74,089 78,845 12.8 15.3 15.7 2.5 2.0 2.4 5.7 5.4 5.7KT Corp 29,600 30,000 3 Hold 6,641 11,889 -7.9 14.0 18.6 0.0 1.7 1.3 -15.8 67.2 -0.4

LG Uplus 10,950 13,500 26 Buy 4,108 7,846 20.1 13.6 12.4 1.4 2.3 2.4 -6.6 4.0 0.0

SK Telecom 211,500 270,000 32 Buy 14,674 14,058 11.0 13.7 11.8 3.8 3.9 4.7 0.2 3.1 -0.4

DiGi 4.93 4.10 -13 Sell 9,587 9,865 20.8 25.7 22.8 4.8 3.9 3.5 4.2 3.0 3.6

Maxis 6.31 5.40 -11 Sell 11,837 13,912 26.4 29.3 26.3 6.0 3.0 3.2 6.3 5.0 5.0

Telekom Malaysia 6.61 7.60 19 Buy 5,915 6,767 23.1 23.7 22.1 3.7 3.8 4.1 4.1 2.4 3.6

AXIATA 5.93 5.50 -4 Hold 12,666 13,793 23.6 18.1 21.1 3.3 3.4 3.0 3.4 2.8 5.3

Spark New Zealand Limited 3.54 3.35 2 Hold 4,407 4,862 14.5 15.2 17.4 6.7 7.3 7.1 8.0 4.7 6.1

Globe Telecom 2,148.00 2,450 18 Buy 6,144 7,418 15.8 20.3 16.3 4.4 3.7 4.1 5.6 0.3 2.2

PLDT 1,967.00 2,300.0 25 Buy 9,168 9,594 17.0 11.8 12.9 6.3 7.7 6.4 5.0 6.7 7.0

M1 2.59 3.90 56 Buy 1,697 1,868 18.1 13.5 13.3 5.5 5.9 6.8 3.1 7.9 5.0

Singapore Telecom 3.79 4.60 26 Buy 44,229 24,302 16.1 16.3 14.7 4.6 4.4 5.0 5.8 5.4 5.6

Starhub 3.31 4.05 28 Hold 4,161 4,437 18.9 15.3 17.9 4.9 5.9 6.0 4.8 7.1 7.2