ashcae - log into your online media solutions...

TRANSCRIPT

9/6/2011

ASHCAEProvider Tax WebinarSeptember 6, 2011

ASHCAEProvider Tax WebinarJohn Poirier, NH

September 6, 2011

ASHCAEProvider Tax WebinarBill Hartung, AHCA

September 6, 2011

9/6/2011

ASHCAEProvider Tax WebinarJoseph M. Lubarsky, CPA, Eljay, LLC

September 6, 2011

Provider Taxes are a Legitimate Funding

Mechanism5

� Provider taxes are a bona fide legal funding source

eligible for federal matching funds when used to

reimburse Medicaid covered services

� Specific rules and regulations in place since 1993

� Regulations revised in February 2008

� 18 classes of health services and providers can be

taxed

Taxes Have Increased Federal

Medicaid Matching Funds6

Source: Kaiser Commission on Medicaid and the Uninsured

9/6/2011

Provider Tax Rules and

Regulations7

� Provider taxes must:� Be imposed at uniform rate

� Be broad-based

Notes:

(1) State may exclude all or part of Medicare and/or Medicaid payments (patient days) from the tax

(2) “Public” (Governmental) providers may be exempted from the tax without a waiver

Provider Tax Rules and

Regulations8

� Provider tax must not:

� Include direct or indirect hold harmless guaranteeing repayment of tax to providers in Medicaid rates or other payments

� States can indicate through their legislative process that tax proceeds will be used to increase Medicaid payment

� Federal law does not mandate that provider tax proceeds must be used to enhance Medicaid payments to providers that paid the tax

Provider Tax Rules and Regulations

9

� Indirect hold harmless presumed if:

� Tax exceeds more than 5.5% (6.0%-

10/01/11) of patient revenues; and

� 75% or more of taxpayers receive 75% or

more of tax payments back in enhanced

Medicaid or other state payments

� Patient service revenues measured on an

annual state fiscal year basis

9/6/2011

Provider Tax Rules and Regulations

10

� Waivers

� “Broad-based” and “uniformity” may be

waived if non-broad-based and non-

uniform tax is “generally redistributive”

� Mathematical formula to waivers

� Hold harmless provisions still apply

Provider Tax Waivers

11

� Broad-based waiver (exclude certain

providers)

� Uniformity waiver (charge variable tax

rates)

� Combination of both

� 21 states have provider tax waiver

programs - 19 approved; 2 pending

CMS Role Relative to Waiver Requests

12

� Examines whether waiver classes are

appropriate

� Approved classes include CCRCs,

hospital-based facilities and smaller and

larger facilities

� Determines if statistical test has been met

� Determines if combination of waiver

structure and rate increase violates hold

harmless

9/6/2011

Key Criteria for Waiver Approval

13

� Waiver class has variation in Medicaid volume among providers – not all low or no Medicaid volume

� No hold harmless� Increased Medicaid payments can be used to enhance rates but cannot result in providers being repaid dollar for dollar (or part of a dollar) for their tax cost

� If every provider in the state is guaranteed through Medicaid payment (or waiver) to be reimbursed all or part of their tax cost, waiver will not likely be approved

Acceptable Reimbursement Approaches

14

� Rate increase must be based upon the

overall costs incurred for providing

Medicaid services

� Payment methodology must be designed

to recognize volume or nature of services

to Medicaid individuals

� Subject to Medicare UPL test

Acceptable Reimbursement

Approaches - Continued15

� Medicaid portion of tax is a pass-through

� Additional rate increase either as:

� A flat amount per Medicaid patient day

(supplemental payments); or

� Enhancements to the Medicaid rate system

or financing the existing methodology such

as rebasing, inflationary increases, and pay

for performance incentives

9/6/2011

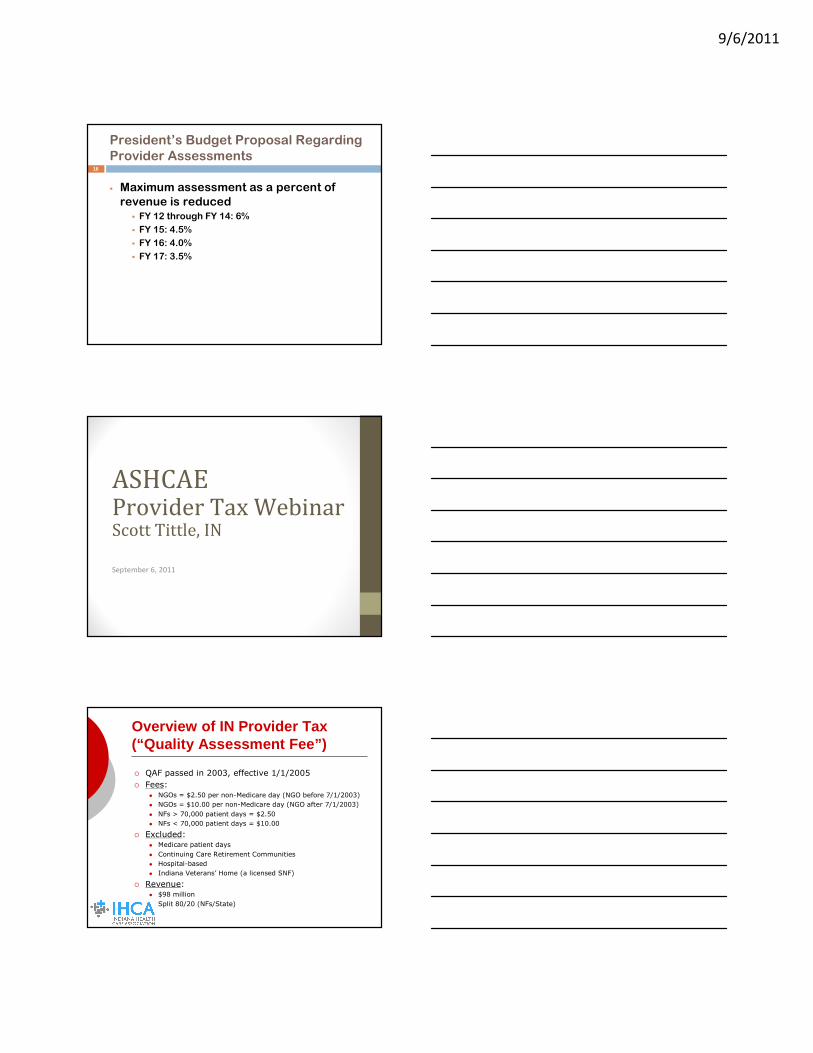

President’s Budget Proposal Regarding

Provider Assessments16

� Maximum assessment as a percent of

revenue is reduced� FY 12 through FY 14: 6%

� FY 15: 4.5%

� FY 16: 4.0%

� FY 17: 3.5%

ASHCAEProvider Tax WebinarScott Tittle, IN

September 6, 2011

Overview of IN Provider Tax (“Quality Assessment Fee”)

� QAF passed in 2003, effective 1/1/2005

� Fees:� NGOs = $2.50 per non-Medicare day (NGO before 7/1/2003)

� NGOs = $10.00 per non-Medicare day (NGO after 7/1/2003)

� NFs > 70,000 patient days = $2.50

� NFs < 70,000 patient days = $10.00

� Excluded:� Medicare patient days

� Continuing Care Retirement Communities

� Hospital-based

� Indiana Veterans’ Home (a licensed SNF)

� Revenue:� $98 million

� Split 80/20 (NFs/State)

9/6/2011

2011 Legislative Session

� Opportunity: Maximize to from current appx 4.2% to federal

allowable amount of 5.5% (7/1) and 6% (10/1)

� “QAX” passed in April 2011, effective 7/1/2011 (10/1/2011)

� Fees:

� NFs > 70,000 patient days = $3.68 (7/1); $4.00 (10/1)

� NFs < 70,000 patient days = $14.70 (7/1); $16.00 (10/1)

� Excluded:

� Medicare patient days

� Continuing Care Retirement Communities

� Hospital-based

� “green houses”

� Revenue:

� $150 million

� Splits 67/33 (YR1), 66.5/33.5 (YR2), 71/29 (YR3)

Final QAX Agreement

� $20M for open audit appeals (appx. 4,000 since 1987)

� Use of $8M closure and conversion fund

� New QAX monies used for “quality”

� Payment for common audit appeal items (rental medical equipment, cable TV, pet supplies, software licensing direct patient care), dentures, increase in capitalization threshold)

� $.75 administrative add-on 10/1/11-6/30/12

� “Allowed” in cost reports 7/1/12

� Value based purchasing

� Staff turnover, retention, satisfaction surveys, certified medical director

Challenges

� Increased number of “losers”

� State budget considerations

� Fiscal leaders looking for revenue from providers

� State budget staff filling budget / Medicaid holes

� Advocates

� Pushing for more funds for HCBS

� Press� Focusing on more money to bottom line and not on quality

� Other priority LTC bills used as leverage

� Other health care provider tax initiation / maximization efforts

9/6/2011

ASHCAEProvider Tax WebinarHeath Boddy, NE

September 6, 2011

Nebraska LB 600 (2011)Nebraska LB 600 (2011)Implementation of a

Quality Assurance Assessment

for Nursing Facilities

23

BackgroundBackground

a. 2008, Nebraska NFs reject proposed provider tax

b. 2008, NHCA Board “Tables” Issue

c. 2010, NFs face 7.9% rate cuts

d. NHCA Board agrees to reconsider provider tax

e. Hired Joe Lubarsky, President of Eljay, LLCto re-develop a model (First hired after M&S study)

24

9/6/2011

Internal PoliticsInternal Politics

1. Modeling estimated 12 “losers”, but only 4 after

netting within multi-facility chains.

2. Nebraska conservative model: 1.9% of revenues.

• Helped in light of news of potential Federal budget cuts.

3. NHCA Board votes to move forward… almost

unanimously.

25

XYZ Corporation Gain / Loss

Facility A +350,000

Facility B (140,000)

Facility C +85,000

XYZ Corporation Net Balance +295,000

What

about

the four

losers?

26

Internal PoliticsInternal Politics

THE SO-CALLED LOSERS:1. Fraternal Order NF. Not Medicare or Medicaid certified. Provides uncompensated care. NHCA Member.

2.Urban facility. Member. Advocate for a provider tax as husband long time management company.

3.Urban facility. Administrator understood challenges for Nebraska NFs. NHCA Member.

4.Owned by long-time, solid NHCA Member. Former Board member. Very opposed.

27

9/6/2011

Internal PoliticsInternal Politics

1. Travel to “Loser” facilities.

2. Seek joint initiative ◦ Joint Board Meeting

3. Buy-in from

28

Legislative StrategyLegislative Strategy

1. Modeled legislation after Iowa.

• No quality-based add-on.

2. Lobbied for committee to which LB would be referenced…Health Comm.

3. Sought Sponsoring Senator

• Kathy Campbell, HHS Committee Chair, Bipartisan reputation and respected.

29

Legislative StrategyLegislative Strategy

MOST IMPORTANT STEPS IN NE

1. Met with each and every State Senator• Nebraska has a “Unicameral” Legislature with

only a 49 member Senate.

• We are on a first name, friendly basis withh all 49.

• Asked all to “co-sign”. Got 1/3.

2. Engaged NF Members, and even some ALF (whoever works).

• Pivotal with Speaker & Appropriations Chair.

• Opponents happened to be absent at votes.

30

9/6/2011

Legislative StrategyLegislative Strategy

OVERRIDING GOVERNOR’S VETO1. Our message with legislature: People

don’t ask for “taxes” as in our case. This is not a tax.

2. Grassroots campaign with members.3. Atmosphere in Legislature: Governor is

playing Tea Party politics. We leveraged that issue.

4. Governor did not “work” his veto.• We feel he knew we needed the funding but

wanted political cover.

31

ASHCAEProvider Tax WebinarJoseph M. Lubarsky, CPA, Eljay, LLC

September 6, 2011

Major Risks Associated With Provider

Tax Programs33

� Not all proceeds used to enhance NF rates

� States reduce existing rates and simply use provider taxes to backfill

� The “split” of tax proceeds changes in future years

� Disagreement on how rate enhancements should be allocated among providers

� May not achieve provider, state agency, gubernatorial or legislative consensus

� Waiver tax programs are not necessarily equitable relative to tax rates and enhanced Medicaid payments

9/6/2011

Major Benefits Associated With Provider

Tax Programs34

� Ability to provide rate increases or mitigate rate reductions in tough economic times

� Flexibility in directing payments to providers with greatest need

� Ability to fund major modifications to a new rate system

� Ability to provide permanent or temporary rate enhancements outside the daily rate

� Ability to “wear the white hat” politically by sharing part of the tax proceeds to fund other Medicaid services or programs

ASHCAEProvider Tax Webinar

Questions?