ascent of real assets - perspectives from the economist

TRANSCRIPT

WRITTEN BY

THE ASCENT OF REAL ASSETSGAUGING GROWTH AND GOALS IN INSTITUTIONAL PORTFOLIOS

FOREWORD

[ 2 ] T H E A S C E N T O F R E A L A S S E T S

“What are our peers doing?”

For institutional investors the question is both timeless and timely. Investors have always sought to learn from organizations facing challenges similar to theirs. Lately, our conversations with clients indicate that the desire to do so is stronger than ever—not surprising during a pivotal period of rethinking and reassessment for many of them.

The topic of real assets is a particular focus. The growing appeal of real estate and infrastructure investments was one of the major trends highlighted by the institutional portfolio rebalancing survey we conducted late last year and released in January, and the interest has only grown since then. That was a broad survey, however, and didn’t explore the goals and practices of investors as they put real assets to work—matters that we know are of great interest to our clients.

This report, the fruit of a collaboration between BlackRock and The Economist Intelligence Unit, is a deep dive into those issues. We think the research has yielded some significant findings, and we thank the 201 organizations around the world participating in our survey, and the eight senior investors who agreed to be interviewed, for helping us uncover them.

Among other things, the survey sheds new light on the interplay between interest rates and flows into real assets. Readers will want to consider the results for themselves, but our view is that there is more going on than a short-term tactical shift. Years of near-zero rates have led investors to look to real assets for return and income. But their intention to accelerate their allocations (and staff accordingly) probably signals a more strategic role for real assets in institutional portfolios in the future.

Not that the road to this future is necessarily a straight one. High valuations, though far from universal, are one concern. Lack of supply in infrastructure is another. Real assets pose real challenges as well as real opportunities, and our report also features commentary from three BlackRock experts on how to think about the complete picture.

We hope this report will be helpful to you as you get on with the task of making real asset investments that move you closer to your objectives. As many of you know, we are strong believers in the power of collective intelligence—and in the partnerships that contribute to it.

Mark McCombeGlobal Head of BlackRock’s Institutional Client Business and Chairman of BlackRock Alternative Investors

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 3 ]

CONTENTS

About the research ����������������������������������������������������������������������������������������������������������������4

Executive summary ���������������������������������������������������������������������������������������������������������������5

Introduction ��������������������������������������������������������������������������������������������������������������������������7

Section 1: Real assets on the rise ������������������������������������������������������������������������������������������8

Section 2: Real estate rules ������������������������������������������������������������������������������������������������� 14

Section 3: Building up infrastructure ����������������������������������������������������������������������������������� 20

Section 4: Considering commodities ����������������������������������������������������������������������������������� 24

Conclusion �������������������������������������������������������������������������������������������������������������������������� 26

BlackRock commentators ��������������������������������������������������������������������������������������������������� 27

THE ASCENT OF REAL ASSETSGauging Growth and Goals in Institutional Portfolios

[ 4 ] T H E A S C E N T O F R E A L A S S E T S

In September 2014, The Economist Intelligence Unit, on behalf of BlackRock, conducted a global survey of 201 executives from institutional investment organizations in 30 countries to ascertain their level of interest in and strategies related to real-asset investment.

In terms of geographic distribution, 80 respondents were located in North America, 80 in Europe, the Middle East and Africa and 41 in Asia-Pacific. Approximately one-third of the organizations represented in the survey have assets under management (AUM) of more than $75bn, with a similar proportion reporting between $1bn and $5bn.

As a qualifier, all of the respondents indicated that they have significant responsibility for investment decisions and that their organization currently invests in real assets. Moreover, the survey findings were complemented by in-depth interviews with eight senior financial executives at institutional investors across the globe.

Our thanks to the following individuals for their time and insight (listed alphabetically):

`` Christopher Ailman, chief investment officer, California State Teachers Retirement System

`` Raphael Arndt, chief investment officer, Future Fund of Australia

`` Patrick Baumann, assistant treasurer, Harris Corporation

`` Hans de Ruiter, chief investment officer, Stichting Pensioenfonds TNO

`` Craig Lewis, director of private markets, The duPont Trust

`` Ben Mahon, alternatives investment officer, Oregon State Treasury

`` Susan Martin, chief executive officer, London Pensions Fund Authority

`` Marcel Roberts, chief investment officer, Stichting Pensioenfonds Medisch Specialisten

About the research

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 5 ]

Real assets—primarily real estate, infrastructure and commodities—are an increasing focus of the world’s institutional investors, according to a global survey of 201 organizations conducted by The EIU. The trend is part of a broader move into alternative investments by institutions that are seeking to lessen their reliance on traditional stocks and bonds amid the challenging conditions of the post-crisis years.

Against a backdrop of ultra-low interest rates, sluggish growth and ongoing uncertainty, nearly half of these investors have increased their allocations to at least one real asset category in the last three years, the survey results show. More than half expect to increase in one or more categories within the next 18 months. They cite two main drivers for their greater investment: a desire to increase returns and their view of the macroeconomic environment. Many are also motivated by a need for income. Other objectives commonly associated with real assets—notably, diversification and protection against possible inflation—are cited as well, but rank lower.

Investors are using a variety of vehicles and strategies to get exposure to real assets, a diverse category that also includes timber and farmland. (See box at right for definitions.) Nearly all respondents (96%) invest in real estate, which has long played a role in institutional portfolios. Infrastructure, the newest and fastest-growing segment, is owned by 66% of the respondents. Just under one-third of the respondents (29%) invest in commodities.

The median allocation to real assets was 11% of the total portfolio, a percentage that will rise further if the respondents maintain their current course. Overall, the survey results signal the continued evolution of real assets as building blocks in institutional portfolios, with many organizations adding staff to support such effort. However, there is an important caveat resulting from the same unusual financial conditions that have been a tailwind for this asset class. A majority of respondents say that a significant rise in interest rates would cause them to rethink some of their allocations to real assets.

The key findings from the research are as follows:

Real assets have a significant and growing presence in institutional portfolios� Close to half (46%) of the institutions surveyed have increased allocations in at least one category in the last three years. In the next 18 months, 60% will increase in at least one category. Looking within categories, 49% of infrastructure investors, 48% of real estate investors and 46% of commodities investors expect to increase in the next year and a half.

The need to increase returns is a—if not the—major motivation for adding to real-asset allocations� In real estate, 63% of investors planning to grow allocations rank ‘increasing returns’ among the three most important factors in their decision. The same percentage cite macro-environment considerations, while 38% say a need for income is a major factor. In infrastructure, 49% of those planning to

Executive summary

REAL ASSETS DEFINED

This survey defines real-asset investments as follows:

`` Real Estate: real estate debt; private real estate equity; public real estate securities (REITS)

`` Infrastructure: debt and equity in hard assets (e.g. power plants and toll roads) that generate cash flows by providing essential services

`` Commodities: exposure to energy, metals or agricultural products via physical commodities, natural resource equities or private commingled funds

`` Timber and farmland: also considered to be real assets, but with relatively few investors owning them, allocation trends are not explored in depth here

[ 6 ] T H E A S C E N T O F R E A L A S S E T S

increase allocations indicate a desire for returns, with 55% citing the macro environment and 43% referencing a need for income. For those that plan on increasing allocations in commodities, 70% give returns as a reason.

Low interest rates are a tailwind for investment in real assets; a spike in rates could be a headwind� Nearly half (47%) of survey respondents say low interest rates influence their investments in real assets. Almost two-thirds (62%) say they would rethink some of their allocations to real assets if a ‘significant’ rise in interest rates were to occur. In some sub-sectors, concerns about lofty valuations are influencing investment choices.

Many institutions have real-asset teams, and they expect to add staff to them� Nearly one-third (32%) of respondents have a real-assets team, sometimes working within a larger alternatives team. A similar number (30%) plan to increase the number of employees dedicated to real assets in the next 18 months. Of those without a dedicated real-assets team, 14% indicate that they will put one in place in the next 18 months. Nearly all respondents (96%) have staff dedicated to specific real-asset strategies.

In real estate, core equity strategies draw the most interest, but value-added equity and opportunistic equity also have appeal� More than half (59%) of investors increasing allocations to real estate are either somewhat or very interested in core strategies, which are the most conservative and income-oriented. Nearly half of those increasing allocations (47%) express interest in value-added equity, with 34% expressing interest in opportunistic equity strategies—the highest-risk/highest-return investments.

Most real estate investors have some non-domestic exposure; a significant minority show strong geographic diversification� Close to half (44%) of real estate investors currently have between 1% and 10% of their portfolios invested outside their domestic markets, compared with 22% that have more than one-quarter of their portfolio invested outside their home countries.

In infrastructure, equity investments and brownfield projects are preferred� Among infrastructure investors expecting to increase allocations, 75% expect to increase equity exposures and 38% expect to increase debt. Existing (brownfield) projects are preferred: In developed markets, 51% of those expecting to increase allocations are at least somewhat interested in brownfield projects vs 23% that are interested in new (greenfield) projects.

Infrastructure investors express noteworthy interest in emerging-market opportunities� Investors planning to increase infrastructure allocations find emerging markets almost as attractive as developed ones. Nearly half (45%) are at least somewhat interested in emerging-market brownfield investments, and 23% are interested in emerging-market greenfield opportunities—the same percentage interested in new developed-market projects.

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 7 ]

Introduction

The highly unusual economic and financial conditions of recent years have spurred a variety of changes to institutional investors’ portfolio management. A climate of sluggish growth, near-zero interest rates and general uncertainty has led investors to rethink their approaches in traditional asset classes and to increase allocations outside traditional categories—to so-called alternative investments.

A major trend in alternatives has been the growth of allocations to real assets, an investment arena that spans real estate, infrastructure, commodities and less-common holdings such as timber and farmland. (See box on page 5 for definitions.) These assets all share an underlying physicality, and many (but by no means all) of the instruments used to access them are less liquid than traditional investments. Historically, diversification and inflation protection have ranked high among the reasons for owning them. But investors have other objectives, too—notably, returns and income—and the goals can vary considerably by investment type.

Real-asset classes differ in other ways as well. Real estate, for example, has long played a role in institutional portfolios, and investors use a range of instruments and strategies to invest in it, from highly liquid REITS to direct ownership of specific properties. Commodities are less widely owned but equally familiar—modes of access include exchange-traded futures and stock in natural resource companies. Infrastructure, rooted in project finance, is relatively new, highly diverse and still evolving. The sector is attempting to connect the growing institutional appetite for infrastructure exposure with the vast global need for infrastructure capital. (See, for example, “Institutional investors and infrastructure financing,” published in 2013 by the Organization for Economic Cooperation and Development.)

Given these differences, should these alternative investment types be considered one asset class? Are institutional investors thinking of real assets in those terms? What are their objectives, strategy preferences and allocation plans in the three major sectors? How do investment patterns differ around the globe? How deep—and how durable—is the recent expansion of interest in real assets?

This report explores the answers to these questions. Like the survey on which it is based, the report has four main parts: an overview that maps trends across the real-assets spectrum, followed by sections that delve into how institutions are using each of the three major segments. The survey results are supplemented by qualitative interviews with eight senior executives at institutional investors across the globe.

SEC

TIO

N 1

[ 8 ] T H E A S C E N T O F R E A L A S S E T S

Real assets on the riseInstitutional investment in real assets has grown in the last three years and is likely to accelerate, our survey suggests. It also shows that the level of ownership of the different investment types varies, with real estate owned by 96%, infrastructure by 66% and commodities by 29%. (See Chart 1.)

CHART 1: CURRENT OWNERSHIP OF REAL ASSETS% of all respondents invested in each sector

Commodities

Infrastructure

Real estate

% 0 10 20 30 40 50 60 70 80 90 100

(n=201)Source: The Economist Intelligence Unit, 31 October 2014.

But, as shown in Chart 2, recent and expected increases for each segment are similar. About one-third of the investors in each category have increased their allocations since 2011; about half in each category expect to increase allocations further over the next 18 months.

CHART 2: INCREASES IN REAL ASSET ALLOCATIONS% of respondents increasing in past three years/next 18 months

Real estate(n=192)

Infrastructure(n=132)

Commodities(n=59)

% 0 10 20 30 40 50

Will increase over the next 18 months Increased over past three years

Source: The Economist Intelligence Unit, 31 October 2014.

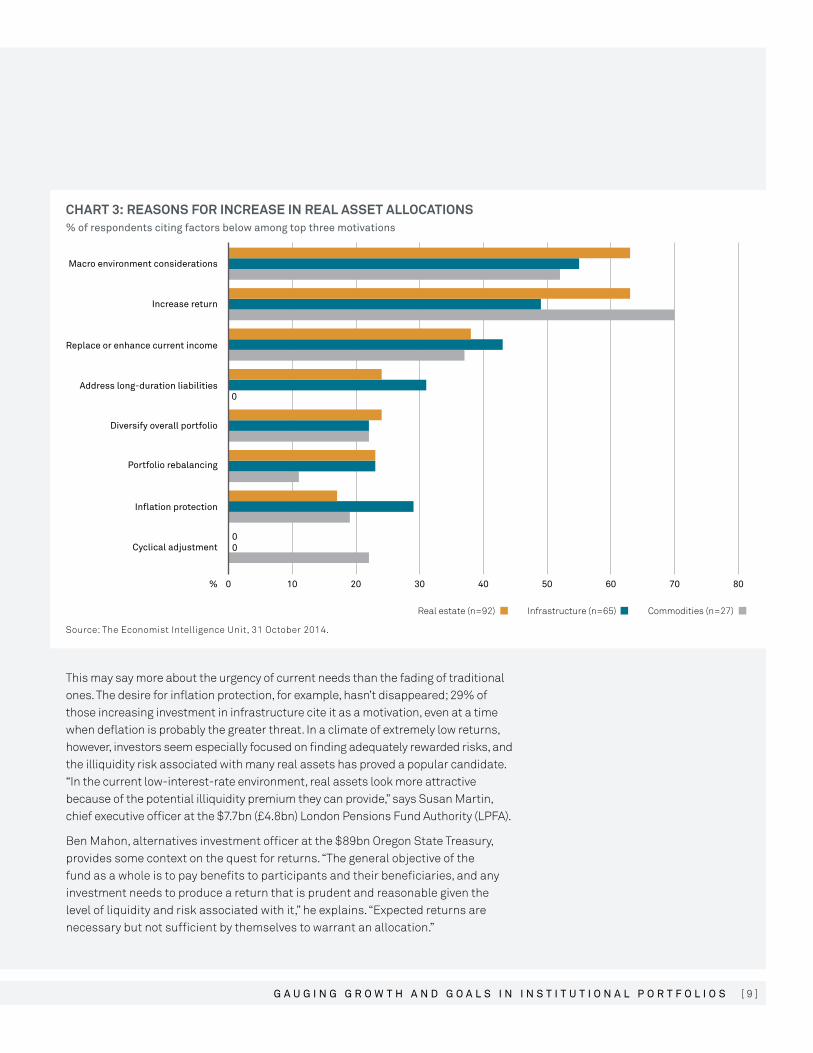

Survey respondents in each segment reveal similar motivations for investing. As shown in Chart 3, their reasons relate more to current market conditions than to a desire for inflation protection or even diversification, two objectives traditionally associated with real assets. Asked to name up to three motivating factors for expected increases, investors in all three segments cite ‘increase return’ and ‘macro environment considerations’ most often and in similar proportions. Income seeking is the third most common motivation in all three segments.

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 9 ]

CHART 3: REASONS FOR INCREASE IN REAL ASSET ALLOCATIONS% of respondents citing factors below among top three motivations

% 0 10 20 30 40 50 60 70 80

Macro environment considerations

Increase return

Replace or enhance current income

Address long-duration liabilities

Diversify overall portfolio

Portfolio rebalancing

Inflation protection

Cyclical adjustment

0

00

Real estate (n=92) Infrastructure (n=65) Commodities (n=27)

Source: The Economist Intelligence Unit, 31 October 2014.

This may say more about the urgency of current needs than the fading of traditional ones. The desire for inflation protection, for example, hasn’t disappeared; 29% of those increasing investment in infrastructure cite it as a motivation, even at a time when deflation is probably the greater threat. In a climate of extremely low returns, however, investors seem especially focused on finding adequately rewarded risks, and the illiquidity risk associated with many real assets has proved a popular candidate. “In the current low-interest-rate environment, real assets look more attractive because of the potential illiquidity premium they can provide,” says Susan Martin, chief executive officer at the $7.7bn (£4.8bn) London Pensions Fund Authority (LPFA).

Ben Mahon, alternatives investment officer at the $89bn Oregon State Treasury, provides some context on the quest for returns. “The general objective of the fund as a whole is to pay benefits to participants and their beneficiaries, and any investment needs to produce a return that is prudent and reasonable given the level of liquidity and risk associated with it,” he explains. “Expected returns are necessary but not sufficient by themselves to warrant an allocation.”

[ 1 0 ] T H E A S C E N T O F R E A L A S S E T S

Clearly, low rates have been a tailwind for real-asset investments: Nearly half (47%) of respondents say that low interest rates influence their investments. A spike in rates, moreover, could be a headwind. Almost two-thirds (62%) say they would rethink their allocations to real assets if there were a significant rise in interest rates. As shown in Chart 4, perceived sensitivity to interest rates varies by segment, with real estate seen as most sensitive. By region, respondents in Asia-Pacific felt most exposed to rising interest rates, with nearly three-quarters (73%) agreeing that their real asset allocations were particularly sensitive.

CHART 4: “OUR STRATEGY IS PARTICULARLY SENSITIVE TO RISING INTEREST RATES”% of respondents

% 0 10 20 30 40 50 60

Agree

Disagree

Not sure

Real estate Infrastructure Commodities

(n=201)Source: The Economist Intelligence Unit, 31 October 2014.

What might it signal that half the group expects to increase allocations, while nearly two-thirds say they would rethink allocations if rates rise significantly? Respondents weren’t asked for interest rate predictions, but the mainstream view is that rates will rise gradually.

Raphael Arndt, chief investment officer of the $93bn (AUS$104bn) Future Fund of Australia, looks ahead: “The acid test [for real assets] will be when bond yields rise in a few years. We are seeing the start of that cycle now and how real assets perform for us in the coming years, and through the rest of the cycle, will prove to be the most important thing for us.”

As investors consider what the effects of higher rates might be, they are already mindful of the manner in which strong investment flows spurred by low rates have elevated valuations in various real-asset sub-sectors. Income-generating investments in real assets may be affected if rising rates make bonds more attractive. As we explore in subsequent sections, these concerns are shaping investor decisions about strategies and target geographies.

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 1 1 ]

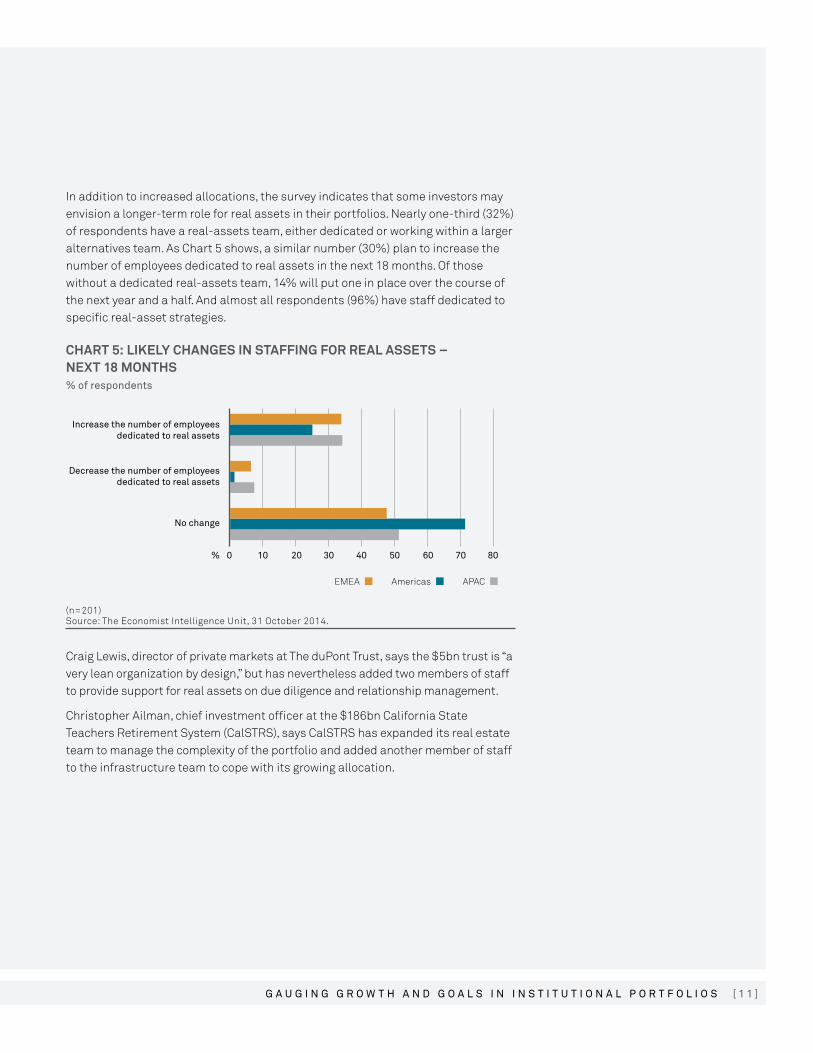

In addition to increased allocations, the survey indicates that some investors may envision a longer-term role for real assets in their portfolios. Nearly one-third (32%) of respondents have a real-assets team, either dedicated or working within a larger alternatives team. As Chart 5 shows, a similar number (30%) plan to increase the number of employees dedicated to real assets in the next 18 months. Of those without a dedicated real-assets team, 14% will put one in place over the course of the next year and a half. And almost all respondents (96%) have staff dedicated to specific real-asset strategies.

CHART 5: LIKELY CHANGES IN STAFFING FOR REAL ASSETS – NEXT 18 MONTHS% of respondents

% 0 10 20 30 40 50 60 70 80

Increase the number of employeesdedicated to real assets

Decrease the number of employeesdedicated to real assets

No change

EMEA Americas APAC

(n=201)Source: The Economist Intelligence Unit, 31 October 2014.

Craig Lewis, director of private markets at The duPont Trust, says the $5bn trust is “a very lean organization by design,” but has nevertheless added two members of staff to provide support for real assets on due diligence and relationship management.

Christopher Ailman, chief investment officer at the $186bn California State Teachers Retirement System (CalSTRS), says CalSTRS has expanded its real estate team to manage the complexity of the portfolio and added another member of staff to the infrastructure team to cope with its growing allocation.

[ 1 2 ] T H E A S C E N T O F R E A L A S S E T S

BlackRock view

A beneficial rebalancing into real assetsWe think most investors are significantly overweight financial assets and underweight real assets. There are reasons for that—it’s much harder to invest in real assets than it is to buy stocks and bonds. It’s probably a fair reading of the survey results to say that, with ultra-low interest rates driving a shift in relative value between things with CUSIPS and things that are real, investors have begun a strategic rebalancing. If so, we believe that’s a good thing for them.

The trend toward adding real assets staff is also a positive one. There are both liquid and illiquid ways of getting exposure to real assets, and there’s a place for both in most portfolios. But the purer exposures tend to come via the less liquid vehicles, which pose their own unique challenges. For example, illiquidity premia are highly unstable. They can be quite large when an asset type is out of favor, then erode sharply or even go negative when those assets come into demand. We’re seeing this effect now with trophy properties in major real estate markets and stabilized, core infrastructure in developed countries.

We take a very price-aware view of real asset investments. In the current climate, we find that more complicated situations or assets that involve development or repositioning may often deliver better relative value. To be sure, there are a lot of variables to consider—not just which sectors look attractive, but the different ways available to express a view, and the costs and benefits of each. Most fundamentally, we advocate portfolios that are broadly constructed and aligned with an investor’s actual liabilities.

One survey finding that was a bit of a surprise was the relatively low rank of inflation protection as a motivation. Perhaps it was less cited because inflation currently seems like such a distant possibility. Unexpected inflation is, however, exactly what one wants to guard against, since expected inflation tends to be priced into nominal return expectations. Investors in real assets today are generally benefitting from competitive current returns with significant inflation protection, whether they fully value that today or not.

Income, return, diversification, inflation protection: A well constructed real assets portfolio can enhance a broader portfolio by contributing in all four dimensions.

Matthew BoteinGlobal Co-Head and CIO, BlackRock Alternative Investors

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 1 3 ]

SEC

TIO

N 2

[ 1 4 ] T H E A S C E N T O F R E A L A S S E T S

Real estate rulesReal estate dominates the real-asset allocations, with nearly all survey respondents (96%) saying they have some allocation to the sector. That nearly one-third (31%) increased their allocations over the last three years is consistent with the strong commercial and residential property markets in many parts of the world. In the US, for example, strong inflows from institutional investors have pushed valuations in some cities (as measured by cap rates) close to 2008 levels, as data from the National Council of Real Estate Investment Fiduciaries show.

The survey signals that the flows are likely to accelerate. Over the next 18 months, 48% of respondents expect to make either moderate (38%) or substantial (10%) allocations. (See Chart 6.) Indications are that institutions will be selective about where they invest, however. Real estate is seen as more sensitive to rising interest rates than infrastructure or commodities, with 59% of respondents agreeing that their strategies are ‘particularly sensitive’.

By region, Asia-Pacific has the largest proportion of investors who plan to substantially increase real estate allocations—20%, compared with 13% for Europe, the Middle East and Africa (EMEA) and just 1% in North America. Slightly more than one-third (35%) of investors in EMEA are planning a moderate increase, compared with two-fifths in North America and Asia-Pacific.

CHART 6: CHANGES IN REAL ESTATE ALLOCATIONS OVER PAST THREE YEARS/NEXT 18 MONTHS% of real estate investors reporting:

Substantial increase(10%+)

Moderate increase(1 - 9%)

No significantchange

Moderate decrease(1 - 9%)

Substantial decrease(10%+)

% 0 10 20 30 40 50 60

Next 18 months Past three years

(n=192)Source: The Economist Intelligence Unit, 31 October 2014.

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 1 5 ]

KEY DRIVERS

As with all real-asset classes, the two strongest motivations for increasing real estate holdings are the need to boost return and macro-environment considerations, with nearly two-thirds (63%) of respondents ranking these factors among their top three considerations (See Chart 7.) Diversification (cited by 24%) and managing inflation (cited by 17%) are less important motivations. Absolute return is the most popular method for assessing the performance of real estate investments, with nearly three-quarters (72%) opting for this approach.

Investors also see real estate as a means of providing stable sources of income. More than one-third (38%) of respondents plan to increase real estate investment as a means of replacing or enhancing current income. As Hans de Ruiter, chief investment officer of the $3.3bn (€2.6bn) TNO pension plan in the Netherlands, explains: “The income part [of real estate] is important. We are looking for more or less stable cash flows. [Real estate] is a good match with the liability structure of the pension fund.”

CHART 7: REASONS FOR INCREASE IN REAL ESTATE ALLOCATIONS% of respondents who plan to increase real estate investment citing factors below among top three motivations:

% 0 10 20 30 40 50 60 70 80 90

Macro environment considerations

Increase return

Replace or enhance current income

Address long-duration liabilities

Diversify overall portfolio

Portfolio rebalancing

Inflation protection

EMEA (n=36) Americas (n=32) APAC (n=24)

Source: The Economist Intelligence Unit, 31 October 2014.

[ 1 6 ] T H E A S C E N T O F R E A L A S S E T S

STRATEGY AND GEOGRAPHY

The most popular type of real estate investment planned in the next 18 months is private equity, with nearly three-quarters (74%) expecting to increase allocations. Just over 40% expect to add investments in debt, while 42% expect to invest more in public real estate securities, or REITS.

Among those planning to add investments in real estate debt is Marcel Roberts, chief investment officer at the $9.9bn (€7.8bn) Dutch pension plan Stichting Pensioenfonds Medisch Specialisten. “We think that equities are overvalued and we expect the returns in the near future to be lower than in the past,” says Mr Roberts, whose organization invests 10% of its total portfolio in real estate. “We also think the spreads are too low on credit and we should diversify; real estate debt is a nice alternative.”

Asked which strategies they favor, 59% of respondents planning to add to their real estate allocations said they were either somewhat or very interested in core equity strategies, which are the most conservative and income-oriented. (See Chart 8.) Nearly half (47%) of those that are increasing allocations expressed interest in value-added equity, while 34% expressed interest in opportunistic equity strategies, which are the higher risk/higher return investments.

Mr Ailman of CalSTRS says he favors core strategies as a way to reduce risk. As he puts it, “We have reduced the risk profile of real estate and we are decreasing investment in opportunistic while increasing the allocation to core.”

CHART 8: REAL ESTATE STRATEGY PREFERENCE – NEXT 18 MONTHS% of respondents increasing real estate allocations and somewhat/very interested in:

Core equity

Value-added equity

Opportunistic equity

% 0 10 20 30 40 50 60

(n=92)Source: The Economist Intelligence Unit, 31 October 2014.

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 1 7 ]

Almost all respondents have some geographic diversification in their real estate portfolios, and some have a lot. Close to half (44%) of real estate investors currently have between 1% and 10% of their portfolios invested outside their domestic markets, while 22% have more than one-quarter of their portfolios invested outside their home countries. (See Chart 9.) Respondents in the Americas had the lowest non-domestic real estate holdings, with 42% saying they had more than 10% of their portfolios invested outside their home markets, compared with 50% for EMEA and 53% for Asia-Pacific respondents.

Many see a clear advantage in being able to cast a wide geographic net. “At this point, we like Europe more than the US, as the US is starting to become a bit more expensive on valuations,” explains Mr de Ruiter of the TNO pension plan.

Ms Martin of the London Pensions Fund Authority adds: “There are still plenty of opportunities in the UK, Europe and Southeast Asian countries. The risk is the same as in most real assets—too much money chasing opportunities, which may lead to bubbles and drive down return to an uneconomic level.”

CHART 9: “WHAT PROPORTION OF YOUR REAL ESTATE PORTFOLIO IS OUTSIDE YOUR HOME MARKET?”% of respondents

Between 10% and 24%

Between 25% and 49%

More than 50%

Less than 10%

None

% 0 10 20 30 40 50

(n=192)Source: The Economist Intelligence Unit, 31 October 2014.

[ 1 8 ] T H E A S C E N T O F R E A L A S S E T S

BlackRock view

Real Estate: Value varies between—and within—regions This report shows investors planning to increase allocations to commercial real estate, but concerned about valuations in the sector. We think they are right on both counts.

In recent years, ultra-low interest rates have pushed investors into real estate for income and return not available elsewhere. They’ve found both. The middle of a cycle, however, calls for finer distinctions than might be required earlier on. In our view, this is a time when real estate investors need to be especially clear on their objectives, and especially attuned to the significant differences in valuation that now exist between—and within—regions.

Objectives, of course, come first. Real estate is a versatile asset class, with a wide menu of strategies and exposure types. Choosing among them entails setting priorities and making tradeoffs among benefits they deliver in different measure: income, total potential return, liquidity, diversification and inflation protection.

Today’s valuation picture is also multidimensional. While prime cap rates in global gateway cities such as London, Hong Kong and New York are at or near record lows, cap rates in second-tier metros have not returned to pre-recession levels. Even within gateway cities, valuations in areas that are regenerating may be significantly lower than those in prime locations. A historical comparison of cap rates to yields on other assets adds further perspective: The spread between cap rates and local risk-free rates is generally at or above long-term averages. In many markets and sectors, moreover, occupancy and rents are likely to rise as moderately expanding economies strengthen demand.

Thus, there’s no shortage of attractive opportunities. Income oriented investors may want to consider high yield debt or selected core assets in developed markets like the US, the UK and Northern Europe. Opportunistic, return-seeking investors may want to consider development in the US or Europe (where little has been built in the wake of the financial crisis) or deals in Asia-Pacific, where growth prospects are better and some over-leveraged projects need equity injections.

It’s true that major markets have seen major inflows of capital. But it’s not unreasonable for real estate investors to believe they can still find reasonably priced investments that can help them reach their goals.

Marcus Sperber Head of BlackRock’s Global Real Estate Business

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 1 9 ]

SEC

TIO

N 3

[ 2 0 ] T H E A S C E N T O F R E A L A S S E T S

Building up infrastructureInfrastructure investment by institutions has grown briskly in the years since the global financial crisis, as investors looked to the sector for return and income in a low-rate environment. Adding impetus to the trend has been a post-crisis deleveraging by banks, especially in Europe, where banks have historically provided much of the sector’s capital. This has encouraged the infrastructure sector to seek out new sources of finance.

Almost two-thirds of respondents to the survey have an allocation to infrastructure, and, as in real estate, these investments are set to accelerate in the next year and a half. Nearly half plan to increase infrastructure investment over the coming months. (See Chart 10.) Asia-Pacific was the region where investors are most likely to have increased allocations to infrastructure in the past three years, with 43% reporting that they did so. This compares with 24% in North America and 32% in Europe, the Middle East and Africa (EMEA).

CHART 10: CHANGES IN INFRASTRUCTURE ALLOCATIONS OVER PAST THREE YEARS/NEXT 18 MONTHS% of infrastructure investors reporting:

Substantial increase(10%+)

Moderate increase(1 - 9%)

No significantchange

Moderate decrease(1 - 9%)

Substantial decrease(10%+)

% 0 10 20 30 40 50 60 70

Next 18 months Past three years

0

(n=132)Source: The Economist Intelligence Unit, 31 October 2014.

KEY DRIVERS

Macro-environment concerns are the biggest motivation for respondents to increase their infrastructure allocations, especially among investors in the Americas. Almost 9 out of 10 (87%) respondents in the Americas cite macro-environment considerations among their top three reasons for increasing in infrastructure, compared with just 31% in Asia-Pacific and 41% in Europe and the Middle-East. (See Chart 11.)

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 2 1 ]

CHART 11: REASONS FOR INCREASE IN INFRASTRUCTURE ALLOCATIONS% of respondents who plan to increase infrastructure investment citing factors below among top three motivations

% 0 10 20 30 40 50 60 70 80 90

Macro environment considerations

Increase return

Replace or enhance current income

Address long-duration liabilities

Diversify overall portfolio

Portfolio rebalancing

Inflation protection

EMEA (n=29) Americas (n=23) APAC (n=13)

Source: The Economist Intelligence Unit, 31 October 2014.

Respondents are less concerned about the effect of rising rates on infrastructure investments than they are for real estate, but rates are still an issue for many. Slightly more than two-fifths of respondents (41%) agree that their infrastructure strategies are particularly sensitive to rising interest rates, while 34% disagree. One-quarter of respondents (25%) are unsure.

At the Future Fund of Australia, Mr Arndt says interest rates are a critical consideration in selecting infrastructure projects and strategies. “Low-risk infrastructure, like a regulated utility or an airport, is very expensive at the moment,” he says. “We think that those assets are very susceptible to rising interest rate cycles.”

As with real estate, higher returns are a major motivation for increasing investment in infrastructure. This is most pronounced among investors in the Americas, where 74% put returns among their chief motivations, compared with only 39% and 34%, respectively, for Asia-Pacific and EMEA. Investors in those two geographies instead stressed income—a primary motivation for 55% of EMEA investors, 54% of Asia-Pacific investors, but only 22% of Americas investors.

[ 2 2 ] T H E A S C E N T O F R E A L A S S E T S

Liability matching is also a goal for many investors, including the London Pensions Fund Authority. “Similar to many of our other illiquid allocations, we look to our infrastructure investments to provide long-term liability matching cash flows alongside excess return to help us hit our return targets,” says the LPFA’s Ms Martin.

Concern about lofty valuations is not limited to the Asia-Pacific region. Ben Mahon at Oregon State Treasury echoes the Future Fund’s Mr Arndt: “It is a competitive market for investment opportunities and that increased demand could bid asset prices up, thereby hurting future returns.”

STRATEGY AND GEOGRAPHY

Investors planning to increase investment in infrastructure show a marked preference for equity investments. Three-quarters (75%) expect to add equity, compared with 38% expecting to add infrastructure debt.

Valuation concerns notwithstanding, respondents remain most interested in the lowest risk, most income-oriented investments: brownfield (or established) projects in developed markets. More than half of those planning to increase such investment (51%) say they are at least somewhat interested in such projects. (See Chart 12.)

CHART 12: MOST ATTRACTIVE INFRASTRUCTURE TYPES – NEXT 18 MONTHS% of respondents increasing infrastructure allocations and somewhat/very interested in:

Brownfield (existing),developed market

Brownfield (existing),emerging market

Greenfield (new),emerging market

Greenfield (new),developed market

% 0 10 20 30 40 50 60

(n=65)Source: The Economist Intelligence Unit, 31 October 2014.

However, infrastructure investors also express noteworthy interest in emerging-market opportunities. Those planning to increase investment in infrastructure find emerging markets almost as attractive as developed ones. Nearly half (45%) are at least somewhat interested in emerging-market brownfield investments, with 23% interested in emerging-market greenfield opportunities—the same proportion interested in new projects in developed markets.

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 2 3 ]

The choice between new and established projects, and between developed and emerging markets, highlights the different kinds of risk that infrastructure investors must consider. One of these is political risk. “We don’t like to invest in projects that are highly dependent on political decisions,” says TNO’s Hans de Ruiter. Government subsidies to a project, he notes, “may be stopped overnight”.

Adds Mr Ailman of CalSTRS: “Infrastructure investment is always about revenue and the governance structure: ownership, rule of law, will it deliver stability of cash flow.” Most of CalSTRS’ infrastructure investments are in brownfield projects, he says. They are, however, geographically diversified. “We are investing in [infrastructure] funds focused on the whole globe rather than a particular geography,” he says.

BlackRock view

Infrastructure: Emerging opportunitiesAs we speak to investors globally, we are consistently struck by their varying objectives for infrastructure investment, and their determination to match investment types to those objectives. We find the survey results, including the relatively high level of interest in emerging market infrastructure, to be quite consistent with those conversations. Overall, this report reflects both the strong growth of private sector participation in infrastructure and the increased segmentation in the sector as it develops.

In a market that is growing and can be accessed in multiple ways, the idea of a one-size-fits-all infrastructure allocation is increasingly outmoded. Instead, by understanding the characteristics of specific infrastructure investments, investors can tailor allocations to desired outcomes. If absolute return is the goal, participation in the US energy sector may be a good course. For long-term steady income, equity buy-and-hold investments are one possible option. Another is investing in infrastructure debt to capture the illiquidity premium it offers compared to similarly rated bonds.

The interest in a broader geographic approach has several drivers, in our view. Traditionally infrastructure allocations have focused on brownfield (or operating) assets in mature markets such as Western Europe, Australia and North America. Strong flows into these kinds of investments have pushed valuations up in recent years, offering one reason for investors to consider casting a wider net.

But there are other forces at work as well. As investors gain experience and comfort with infrastructure investments, the risk-reward calculus for seeking greater returns in emerging markets becomes more favorable.

Perhaps most significant is the maturation of local economies, in terms of both financial depth and governance. In Mexico, for example, the Peña Nieto administration is focused on infrastructure development to spur growth and is seeking to fund 37% of infrastructure spending from the private sector. The government’s National Infrastructure Plan calls for infrastructure spending to grow from 3.5% of GDP today to 4.9% by 2018. A number of once-in-a-generation reforms and policy changes have been enacted, and international private capital is starting to flow to previously inaccessible opportunities.

Jim BarryGlobal Head of BlackRock’s Infrastructure Investment Group

SEC

TIO

N 4

[ 2 4 ] T H E A S C E N T O F R E A L A S S E T S

Considering commodities

Commodity performance has lagged that of the other two major real-asset categories in recent years. Bearish observers cite signals such as lower oil prices and argue that a so-called supercycle—a period of steadily rising prices dating back to the 1990s, fuelled in large measure by surging demand from China—gave way in 2010 to what may be an extended period of oversupply. Optimists look for continued growth in other emerging markets to sustain demand.

Commodities are the least-owned sector among our survey respondents, with less than one-third (29%) investing in them. But those who do invest have increased allocations and expect to invest more in the future in about the same proportions as real estate and infrastructure investors. More than one-third (35%) of respondents who allocate to commodities made moderate or substantial allocations in the past three years, while nearly half (45%) of respondents say they will boost allocations to commodities in the next 18 months, with 5% of those expecting to make substantial increases. (See Chart 13.)

CHART 13: CHANGES IN COMMODITIES ALLOCATIONS OVER PAST THREE YEARS/NEXT 18 MONTHS% of commodities investors reporting:

Substantial increase(10%+)

Moderate increase(1 - 9%)

No significantchange

Moderate decrease(1 - 9%)

Substantial decrease(10%+)

% 0 10 20 30 40 50 60 70

Next 18 months Past three years

0

0

(n=59)Source: The Economist Intelligence Unit, 31 October 2014.

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 2 5 ]

KEY DRIVERS

Seventy percent of respondents say that boosting returns is among their top three reasons for increasing commodity allocations, while 52% rank macro-environment considerations among their main motivations. More than one-third (37%) cite a desire to replace or increase income.

The survey sample was too limited to draw conclusions on which sub-sectors of commodities were set to be the biggest growth areas in the next 18 months. However, our qualitative research helps to illuminate how investors are thinking about the sector.

For Oregon State Treasury’s Mr Mahon, the choice of a sub-sector is partly influenced by the ease with which money can be invested. “Take energy, for example,” he says, “there is a lot of capital raised and the capital need is great. There are established managers and plenty of capacity.”

Just 19% of those respondents who plan to increase commodity investments will do so as a hedge against inflation, traditionally one of the chief reasons for institutions to hold commodities. Still, owning commodities to protect against inflation retains some appeal, particularly among pension investors, who, by definition, must take a long view.

CalSTRS’ Mr Ailman says his fund’s limited allocation to commodities is part of a small ‘inflation-sensitive’ portfolio that also contains global inflation securities and infrastructure investments. “We have a very small allocation to commodities,” he explains. “We are worried about inflation in the distant future, so we have the ability to increase the allocation. Right now we are testing the performance of the asset class.”

Patrick Baumann, assistant treasurer at the Harris Corporation, an electronics manufacturer, says his company’s $3.5bn defined contribution plan has recently added real assets—including commodities—to its suite of funds.

“The typical fund line-up offered by a lot of DC plan sponsors are traditional equity and fixed income,” Mr Baumann explains. “We are interested in offering members a fund option that has a high correlation to inflation that goes beyond TIPS [US government inflation-linked bonds]. Funds that combine TIPS with commodities and real estate in one place that can be assessed on a daily basis and which are managed professionally are very appealing.”

Where investors choose not to invest in commodities, half say they do not expect a suitable return from the asset class. Nearly half (49%) say they are prevented from investing by internal governance or policy guidelines. Two-fifths cite macroeconomic considerations as an obstacle to such investment.

[ 2 6 ] T H E A S C E N T O F R E A L A S S E T S

The ascent of real assets appears to be well under way.

Over the next 18 months, irrespective of size or location, nearly half of organizations surveyed that invest in real estate, infrastructure and commodities expect to increase their allocations, thus accelerating a trend established over the past three years. The expansion of real-asset teams and the recruitment of specialists to manage these strategies further underline the importance of real assets to today’s institutional investors.

Nevertheless, it is probably premature to conclude that real assets have come of age as an asset class. Although institutional investment in real assets predates the global financial crisis by many years, there’s no mistaking the powerful role that ultra-low interest rates in the post-crisis years have played in driving investment in real assets. Now, as monetary policies diverge around the world—with tightening on the horizon in the US and UK but easing likely in the EU and loose conditions prevailing in Japan—investors continue to rely on real assets for returns and income that they can’t find elsewhere. At the same time, they remain closely attuned to trends in valuation and the macroeconomic environment.

It is often remarked that markets climb a wall of worry. Such may prove to be the case with real assets. ‘Returns’ and ‘macro-environment considerations’ are the chief motivations for real-asset investment today. But income is also important. Diversification still matters, and even inflation figures in the thinking of executives operating with long time horizons.

Investors such as Mr Lewis of The duPont Trust are already thinking of real assets in holistic terms. “We are seeking to generate a strong risk/return profile with an inflation-hedging benefit, while providing diversification,” he explains. “The real-asset exposure should not have a high correlation over a long period of time with the other assets.”

If real assets continue to develop as our research suggests, another survey a few years hence might show a different balance of motivations—and an incrementally larger role for real assets in institutional portfolios.

Conclusion

G A U G I N G G R O W T H A N D G O A L S I N I N S T I T U T I O N A L P O R T F O L I O S [ 2 7 ]

Mark McCombe, Senior Managing Director, Global Head of BlackRock’s Institutional Client Business and Chairman of BlackRock Alternative InvestorsMr. McCombe is responsible for driving the growth of BlackRock’s institutional business and alternatives presence globally. He is also a member of BlackRock’s Global Executive Committee and Global Operating Committee. Previously BlackRock’s Asia Pacific Chairman, Mr. McCombe has had an international career in finance spanning more than 20 years.

Matthew Botein, Managing Director, Global Co-Head and Chief Investment Officer of BlackRock Alternative Investors Mr. Botein’s responsibilities at BlackRock Alternative Investors include hedge funds and opportunistic funds, private equity, hedge fund and private equity solutions, and real assets, including real estate and infrastructure. Mr. Botein also serves as a member of BlackRock’s Global Operating Committee and leads BlackRock Private Markets. Prior to joining the firm in 2009, Mr. Botein was a Managing Director and member of the Management Committee at Highfields Capital Management, a Boston-based private investment partnership.

Marcus Sperber, Managing Director, Head of BlackRock Global Real EstateMr. Sperber is responsible for the strategy and performance of BlackRock’s global real estate platform. Prior to this appointment, Mr. Sperber was Head of BlackRock’s EMEA Real Estate business, where he led a team of investment professionals dedicated to the management of the platform across EMEA. Mr. Sperber has 25 years of experience in real estate and has led many significant corporate and real estate transactions, including the acquisition of MGPA by BlackRock in 2013.

Jim Barry, Managing Director, Global Head, BlackRock Infrastructure Investment GroupMr. Barry leads BlackRock’s direct investing initiatives in infrastructure equity and debt. Prior to joining BlackRock in 2011, Mr. Barry was CEO of NTR plc, a leading international developer, owner and operator of a portfolio of diverse infrastructure businesses.

BlackRock commentators

Why BlackRockBlackRock was built to provide the global market insight, breadth of capabilities, unbiased investment advice and deep risk management expertise these times require. With access to every asset class, geography and investment style, and extensive market intelligence, we help investors of all sizes build dynamic, diverse portfolios to achieve better, more consistent

returns over time.

BlackRock. Investing for a New World.®

This paper is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The content of this paper is based on The Economist Intelligence Unit’s September 2014 global survey of 201 executives from institutional investment organizations in 30 countries. The information contained herein is not a full representation of all survey results.

The opinions expressed are as of September 2014 and may change as subsequent conditions vary. The information and opinions contained in this paper are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. Not all opinions contained herein may be attributable to BlackRock. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This paper may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this paper is at the sole discretion of the reader. The information provided here is neither tax nor legal advice. Investors should speak to their tax professional for specific information regarding their tax situation.

Real Estate Risks: Many factors may affect real estate values. These factors include both the general and local economies, vacancy rates, tenant bankruptcies, the ability to re-lease space under expiring leases on attractive terms, the amount of new construction in a particular area, the laws and regulations (including zoning, environmental and tax laws) affecting real estate and the costs of owning, maintaining and improving real estate. The availability of mortgage financing and changes in interest rates also affect real estate values.

Commodity Risks: Commodity investing is subject to greater volatility than investments in traditional securities, particularly if the instruments involve leverage. The value of commodity instruments may be affected by changes in overall market movements, commodity index volatility, changes in interest rates, or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments.

©2014 BlackRock, Inc. All rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, iSHARES, SO WHAT DO I DO WITH MY MONEY, INVESTING FOR A NEW WORLD, and BUILT FOR THESE TIMES are registered and unregistered trademarks of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

Lit. No. INST-REALASET-1114 2845A-INST-NOV14 / UIM-0073

blackrock.com

Want to know more?