arrow electronics presentation 2008 2nd

DESCRIPTION

TRANSCRIPT

Second Quarter 2008 Earnings Call

July 23, 2008

WELCOME

Sabrina Weaver

Director, Investor Relations

Second Quarter EarningsJuly 23, 2008Page 3

SAFE HARBOR STATEMENT

Some of the comments to be made on today’s call may include forward-looking statements, including statements addressing future financial results. These statements are subject to a number of risks and uncertainties that could cause actual results or facts to differ materially from such statements for a variety of reasons including, but not limited to: industry conditions, the company’s implementation of its new global financial system and the company’s planned implementation of its new enterprise resource planning system, changes in product supply, pricing and customer demand, competition, other vagaries in the global components and global ECS markets, changes in relationships with key suppliers, increased profit margin pressure, the effects of additional actions taken to become more efficient or lower costs, the company’s ability to generate additional cash flow and the other risks described from time to time in the company’s reports to the Securities and Exchange Commission (including the company’s Annual Report on Form 10-K and Quarterly Reports on Form 10-Q). Forward- looking statements are those statements, which are not statements of historical fact. These forward-looking statements can be identified by forward-looking words such as "expects," "anticipates," "intends," "plans," "may," "will," "believes," "seeks," "estimates," and similar expressions. Shareholders and other readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. The company undertakes no obligation to update publicly or revise any of the forward-looking statements.

BUSINESS OVERVIEW

Bill Mitchell

Chairman & CEO

Second Quarter EarningsJuly 23, 2008Page 5

OVERVIEW

Sales and EPS exceeded expectationsStrong performance in both Global Components and Global ECS

Near record levels of performance across the board

Macro conditions remain challenging, but we continue to run our business for consistent performance

Global Enterprise Computing SolutionsSales above expectations and operating margin at industry leading levelMajor ERP milestone achieved with successful transition of NorthAmerican Sun group

Impressive results in a challenging environment…

Second Quarter EarningsJuly 23, 2008Page 6

OVERVIEWImpressive results in a challenging environment…

Global ComponentsPerformance above expectations+ Above-seasonal growth in Asia Pacific

- Significantly outgrew the market+ North America stable+ Europe softMarket has continued to be relatively stable, yet cautiousMoving forward with efficiency initiatives and vertical market objectives

Second Quarter EarningsJuly 23, 2008Page 7

IN SUMMARY…

Continue to invest in the long-term future of Arrow

Strategic priorities are clearPursue growth opportunities across products, markets and geographiesLeverage efficiencies of scale and build best-in-class capabilitiesBuild world class systems and processes to enable strategic initiatives and change value proposition

Continue to manage the company in a prudent, fiscally disciplined mannerIncrease profitabilityMaintain positive cash flowContinue to strengthen balance sheet

FINANCIAL OVERVIEW

Paul Reilly

Senior Vice President & CFO

Second Quarter EarningsJuly 23, 2008Page 9

CONSOLIDATED SALES($ in millions)

Sales $4.3Bn

+8% Y/Y and Q/Q

+6%Y/Y and Q/Q excluding LOGIX

+1% Y/Y and +5% Q/Q excluding LOGIX and FX

$2,768

$3,437

$4,038$4,347

Q2-05 Q2-06 Q2-07 Q2-08

Second Quarter EarningsJuly 23, 2008Page 10

GLOBAL ENTERPRISE COMPUTING SOLUTIONS

$528$625

$1,269$1,389

Q2-05 Q2-06 Q2-07 Q2-08

($ in millions)

Sales $1.4Bn

+9% Y/Y, +26% Q/Q

+4%Y/Y and +19% Q/Q excluding LOGIX

18th consecutive quarter of Y/Y growth

Increased operating margin 160 bps Q/Q to 4.4%

Grew earnings 4x faster than sales Q/Q

ROWC increased more than 50% Q/Q

Second Quarter EarningsJuly 23, 2008Page 11

GLOBAL COMPONENTS

$2,239

$2,812 $2,769$2,958

Q2-05 Q2-06 Q2-07 Q2-08

($ in millions)

Sales $3.0Bn

+7% Y/Y, +1% Q/Q

+2% Y/Y, Flat Q/Q excluding FX

Decreased operating expense/sales 40 bps Y/Y

Operating margin pressure due to softness in Europe and geographic mix

Second Quarter EarningsJuly 23, 2008Page 12

ASIA PAC COMPONENTS

$325

$569 $562

$743

Q2-05 Q2-06 Q2-07 Q2-08

($ in millions)

Sales $743MM

+32% Y/Y, 14% Q/Q

Increased operating income more than 40% Y/Y

Grew earnings 5x faster than sales Q/Q

Improved ROWC by almost 700 bps Q/Q

2x normal seasonal increase

Second Quarter EarningsJuly 23, 2008Page 13

NORTH AMERICAN COMPONENTS

$1,076

$1,255$1,165 $1,125

Q2-05 Q2-06 Q2-07 Q2-08

($ in millions)

Sales $1.1Bn

-4% Y/Y, -3% Q/Q

Continued focus on efficiency initiatives

Increased operating margin 30 bps Y/Y

Second Quarter EarningsJuly 23, 2008Page 14

EUROPE COMPONENTS

$838$988 $1,041 $1,090

Q2-05 Q2-06 Q2-07 Q2-08

($ in millions)

Sales $1.1Bn

+5% Y/Y, -2% Q/Q

-8% Y/Y, -5% Q/Q excluding FX

Market conditions remain soft, in line with expectations

Focused on initiatives to drive profitability

Second Quarter EarningsJuly 23, 2008Page 15

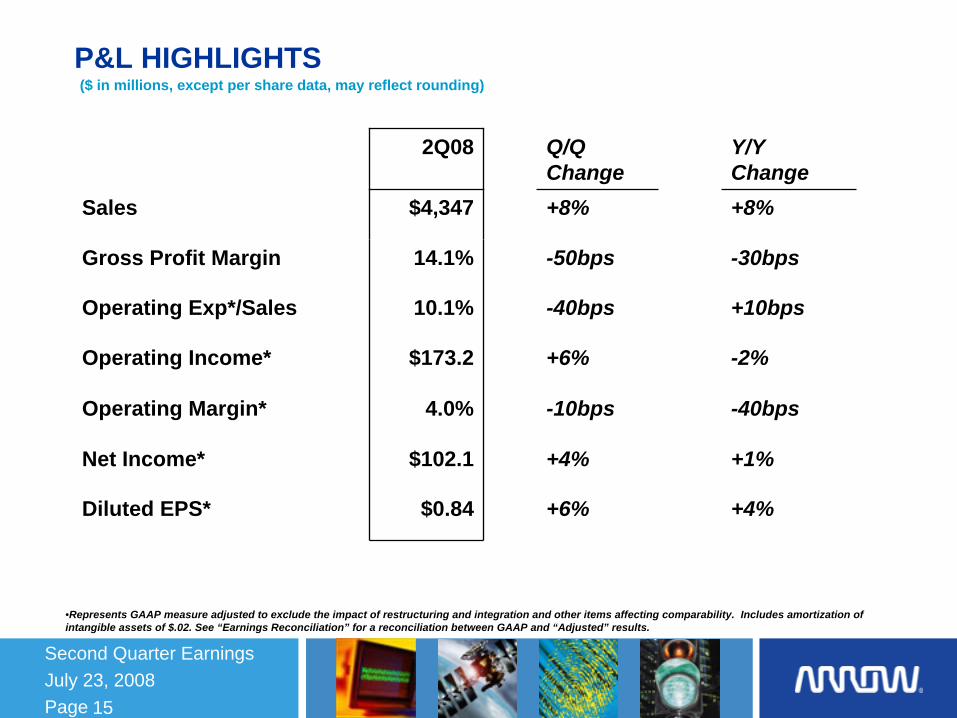

P&L HIGHLIGHTS($ in millions, except per share data, may reflect rounding)

2Q08 Q/Q Change

Y/Y Change

Sales $4,347 +8% +8%

Gross Profit Margin 14.1% -50bps -30bps

Operating Exp*/Sales 10.1% -40bps +10bps

Operating Income* $173.2 +6% -2%

Operating Margin* 4.0% -10bps -40bps

Net Income* $102.1 +4% +1%

Diluted EPS* $0.84 +6% +4%

•Represents GAAP measure adjusted to exclude the impact of restructuring and integration and other items affecting comparability. Includes amortization of intangible assets of $.02. See “Earnings Reconciliation” for a reconciliation between GAAP and “Adjusted” results.

Second Quarter EarningsJuly 23, 2008Page 16

STRONG FINANCIAL POSITION

Cash flow of $101MM in Q27th consecutive quarter of positive cash flow generation

Financial StabilityStrong balance sheetConservative debt levelsDebt to capital near record low level

Focused management of working capitalMaintained near record low level of working capital to sales

ROIC* exceeded cost of capital for the 18th consecutive quarter

*ROIC = Annualized, tax effected op. income and equity in earnings of affiliates excluding restructuring and other charges - annualized minority interest /( Avg Debt + Avg Equity – Avg Cash over $150MM).

BUSINESS UNIT REVIEW

Mike Long

President & COO

Second Quarter EarningsJuly 23, 2008Page 18

ENTERPRISE COMPUTING SOLUTIONS

Need for complex solutions remains strongDouble-digit Y/Y increases in storage, software, and services; and growth in proprietary serversSequential growth in all segments+ Significant gains in proprietary servers

Performance demonstrates leverage we have created in modelGrew earnings at almost 4x sales> 90% of incremental gross profit dollars fell to bottom line

Excellent results exceeding expectations…

Second Quarter EarningsJuly 23, 2008Page 19

ENTERPRISE COMPUTING SOLUTIONSExcellent results exceeding expectations…

We will continue to build scope and efficiency level in EuropeLOGIX acquisition closed on June 2+ Almost doubles size of our European operations; now in the top 3

economies in Europe+ Adds talented management and strong relationships with key

vendors

ERP implementation on trackTechnology will create the infrastructure to provide best-in-class services to our partners Sun transition exceeded expectations

Second Quarter EarningsJuly 23, 2008Page 20

Arrow ECS Seasonality

Q1 vs. Q4 -25% to -30%

Q2 vs. Q1 +15% to +20%

Q3 vs. Q2 -5% to -10%

Q4 vs. Q3 +30% to +35%

Q/Q Revenue Growth Pre LOGIX*

*Based on historical seasonality pro forma for acquisitions and anticipated seasonality in 2008. Represents current mix of business, which could materially change with future acquisitions or changes in customer or supplier mix.

Q/Q Revenue Growth Post LOGIX*Q1 vs. Q4 -30% to -35%

Q2 vs. Q1 +15% to +20%

Q3 vs. Q2 -5% to -15%

Q4 vs. Q3 +35% to +45%

Second Quarter EarningsJuly 23, 2008Page 21

GLOBAL COMPONENTS REGIONAL PERFORMANCE

Asia PacificStronger than seasonal growth driven by China, Taiwan, Australia/NZ, and ASEAN region Significantly outgrew the marketInvestments paying off with consistent gains in profitabilityAnnounced closing of Achieva acquisition on July 7th

North AmericaStable market with book-to-bill higher than second quarter of last yearY/Y weakness driven by transportation end marketStrong double-digit growth in defense and aerospace segmentContinued to focus on operational excellence

EuropePerformance in line with expectations + Weak macro conditions and less competitive export marketBroaden existing customer base and increase productivity

Solid quarter with sales above expected range…

Second Quarter EarningsJuly 23, 2008Page 22

GLOBAL COMPONENTS LEADING INDICATORS

Lead times stable and within normal range of 8 to 12 weeks

Cancellation rates within normal levels

Book-to-bill near parityDecreased Q/Q in line with normal seasonal trendsEurope flatNA above one and stronger than Q207 despite macro weaknessAsia Pac declined slightly

Quarterly customer survey in North AmericaInventory well positioned heading into Q3Outlook for purchase requirements modestly softened for second consecutive quarter

Market continues to be relatively stable, yet cautious

CLOSING COMMENTS

Bill Mitchell

Chairman & CEO

Second Quarter EarningsJuly 23, 2008Page 24

IN CLOSING…

Results exceeded our expectations Strong performance in a cautious marketplaceRaising the bar at ECS; returned to industry-leading level

Continue to manage company conservatively and prudently Maintain flexibility to take advantage of opportunities

Repositioned ArrowStrong balance sheetStable earningsConsistent cash flow generationDiverse revenue streamNumerous growth opportunities

Perform consistently regardless of market conditions

Second Quarter EarningsJuly 23, 2008Page 25

THIRD QUARTER 2008 GUIDANCE

Consolidated Sales $4.10Bn to $4.40Bn

Global Components $2.85Bn to $3.05Bn

Global ECS $1.25Bn to $1.35Bn

Diluted EPS* $0.73 to $0.78

*Excluding charges, including $.02 to $.03 estimated amortization of intangible assets.

Second Quarter EarningsJuly 23, 2008Page 26

ARROW’S VALUE PROPOSITION

Occupy a unique, value-added space in the supply chain with growth opportunities across every customer segment, end market, geography, and technology

Connect suppliers and customers with value-added services that can't be done any other way

“Arrow puts together demand generation, leads, customer seminars,education programs…to be able to go out and create that reach, that's real value” - Key Supplier at Arrow Investor Day 2008

We will continue to create value for our business partners and shareholders

QUESTIONS & ANSWERS

Second Quarter EarningsJuly 23, 2008Page 28

EARNINGS RECONCILIATION$ in thousands, except per share data

Q208 Q108 Q207

Operating income, as Reported $164,958 $144,143 $173,154

Restructuring and integration charges 8,196 6,478 3,425

Preference claim from 2001 -- 12,491 --

Operating income, as Adjusted $173,154 $163,562 $176,579

Net income, as Reported $96,215 $85,871 $99,211

Restructuring and integration charges 5,929 4,159 2,286

Preference claim from 2001 -- 7,822 --

Net income, as Adjusted $102,144 $97,852 $101,497

Diluted EPS, as Reported $.79 $.69 $.79

Restructuring and integration charges .05 .03 .02

Preference claim from 2001 -- .06 --

Diluted EPS, as Adjusted $.84 $.79 $.81

The sum of the components for net income per share, as Adjusted, may not agree to totals, as presented, due to rounding.

Second Quarter EarningsJuly 23, 2008Page 29

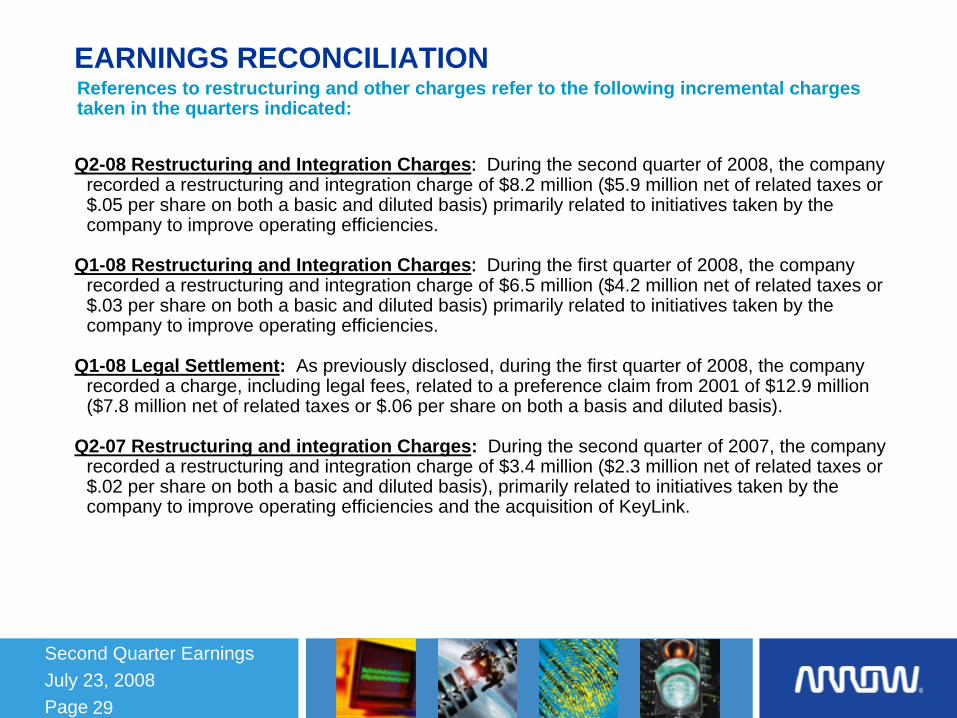

EARNINGS RECONCILIATIONReferences to restructuring and other charges refer to the following incremental charges taken in the quarters indicated:

Q2-08 Restructuring and Integration Charges:

During the second quarter of 2008, the company recorded a restructuring and integration charge of $8.2 million ($5.9 million net of related taxes or $.05 per share on both a basic and diluted basis) primarily related to initiatives taken by the company to improve operating efficiencies.

Q1-08 Restructuring and Integration Charges:

During the first quarter of 2008, the company recorded a restructuring and integration charge of $6.5 million ($4.2 million net of related taxes or $.03 per share on both a basic and diluted basis) primarily related to initiatives taken by the company to improve operating efficiencies.

Q1-08 Legal Settlement: As previously disclosed, during the first quarter of 2008, the company recorded a charge, including legal fees, related to a preference claim from 2001 of $12.9 million ($7.8 million net of related taxes or $.06 per share on both a basis and diluted basis).

Q2-07 Restructuring and integration Charges: During the second quarter of 2007, the company recorded a restructuring and integration charge of $3.4 million ($2.3 million net of related taxes or $.02 per share on both a basic and diluted basis), primarily related to initiatives taken by the company to improve operating efficiencies and the acquisition of KeyLink.

Second Quarter 2008 Earnings Call

July 23, 2008