around the world in 80 days - uli...

TRANSCRIPT

David Morley

February 09 2010

Around the world in 80 days Africa

Actis at a glance

Sao Paulo

London

Cairo

Lagos

Johannesburg

Nairobi

Mumbai

Singapore

Beijing Portfolio employees

Returned from $1.7bn invested

FUM

portfolio companies

Investors

Staff

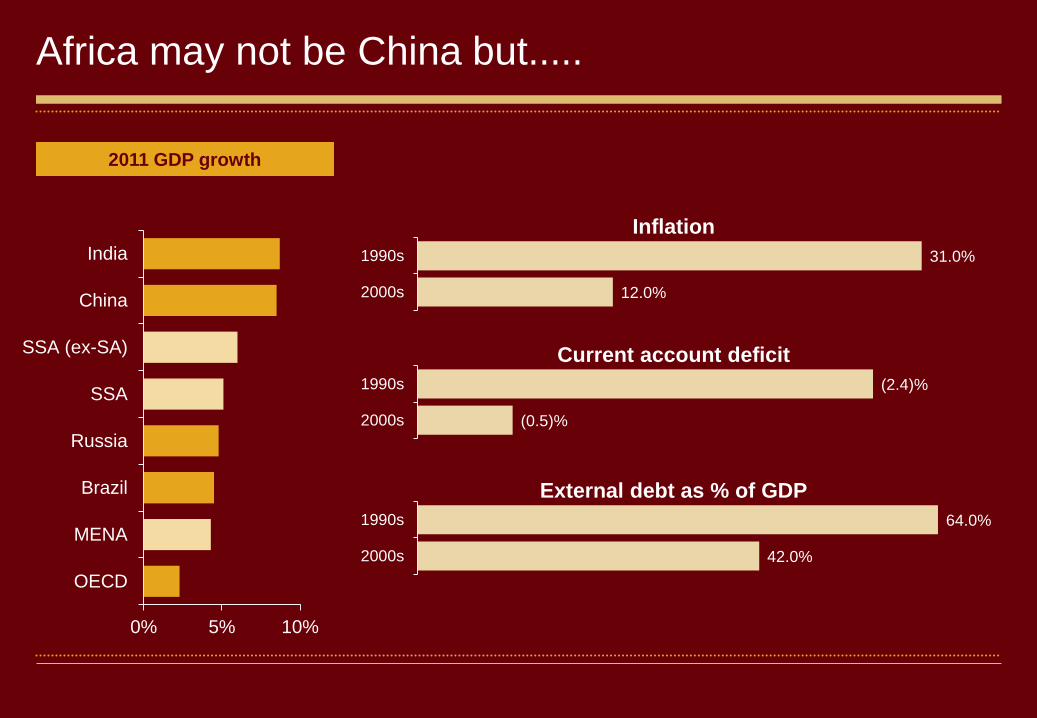

Africa may not be China but.....

0% 5% 10%

OECD

MENA

Brazil

Russia

SSA

SSA (ex-SA)

China

India

2011 GDP growth

Inflation

31.0%

12.0%

1990s

2000s

Current account deficit

External debt as % of GDP

(2.4)%

(0.5)%

1990s

2000s

64.0%

42.0%

1990s

2000s

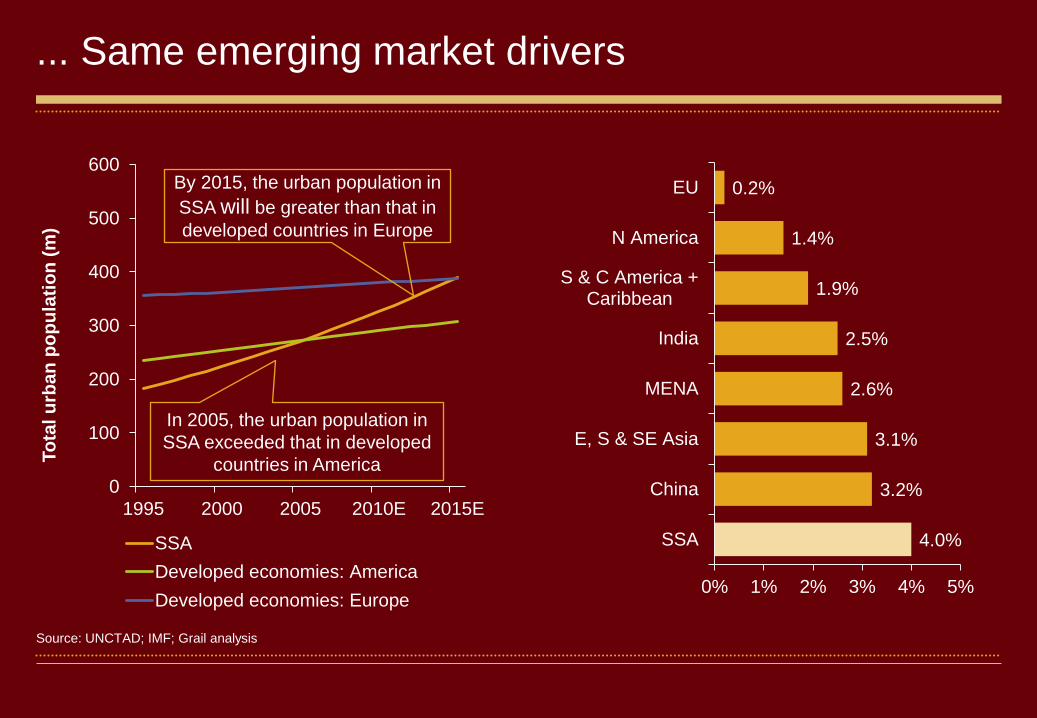

... Same emerging market drivers

Source: UNCTAD; IMF; Grail analysis

4.0%

3.2%

3.1%

2.6%

2.5%

1.9%

1.4%

0.2%

0% 1% 2% 3% 4% 5%

SSA

China

E, S & SE Asia

MENA

India

S & C America +Caribbean

N America

EU

0

100

200

300

400

500

600

1995 2000 2005 2010E 2015E

To

tal u

rba

n p

op

ula

tio

n (

m)

SSA

Developed economies: America

Developed economies: Europe

By 2015, the urban population in

SSA will be greater than that in

developed countries in Europe

In 2005, the urban population in

SSA exceeded that in developed

countries in America

Urban areas in 2020

Source: http://www.citymayors.com/statistics/urban_2020_1.html

0

5

10

15

20

25

mill

ions

Clear opportunity

Source: UNCTAD; IMF; Grail analysis

1.6m

2.5m

17.0m

2.3m

1.0m

0 2 4 6

Uganda

Tanzania

Nigeria

Kenya

Ghana

69

1

1

2

1

0 20 40 60 80

Jo'burg

Kampala

Lagos

Nairobi

Accra

0.003

0.004

0.041

0.032

0.047

0 0.02 0.04 0.06

Tokyo

South Africa

Tanzania

Ghana

Nigeria

Housing deficit (m units) Office rental per GNI per

capita

Number of A-grade

shopping malls

Without the wall of capital

Source: EMPEA

0 20 40 60 80 100 120 140

Africa

Emerging markets

Global

$bn

Fragmented markets (Mckinsey)

Diversified economies Oil exporters

Transition economies Pre-transition economies

Where we play

Lagos Growth

mill

ions

0

4

8

12

16

20

24

Lagos

Office stock

0 5 10 15 20 25 30

Lagos

Barcelona

Milan

Rome

Madrid

Frankfurt

London

Berlin

Munich

Paris

million m2

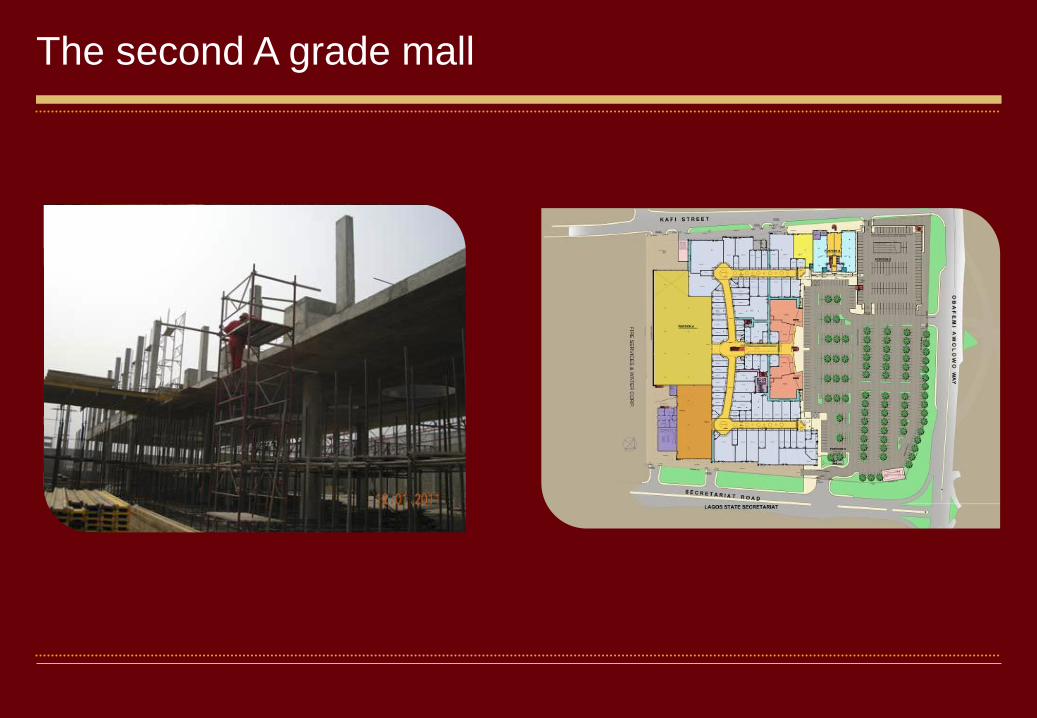

The second A grade mall

Perceived risks

Limited number of

established GPs

Political risk

Weak exit environments

Challenging regulatory /

tax environments

Scale of opportunity to

invest is too small 27%

29%

34%

58%

60%

2010 EMPEA/Coller Capital Survey % respondents

And what do we think about it?

Execution

Liquidity

ESG

Emerging markets ‘risk’

Source: RREEF 0 1 2 3 4 5

Emerging Asia

Mature Asia

East Europe

Latin America

West Eurpore

North America

2012f

2007

Change in value of global real estate market by region, 2007-2012f

(real estate invested stock)

% change 2007-2012f

-17%

-8%

+86%

+43%

-6%

+125%

Thank you