ar, tax evasion, fci, fraud, intl standards, ethics 8 22-14

DESCRIPTION

Slides for the CFCS prep session conducted August 22ndTRANSCRIPT

Part 3: Asset Recovery

Tax Evasion and EnforcementFinancial Crime Investigations

FraudInternational Standards

Ethics

CFCS Examination Preparation SeriesAugust 22, 2014

Presented ByBrian Kindle

Brian KindleExecutive Director

Association of Certified Financial Crime SpecialistsMiami

Asset Recovery

CFCS Examination Preparation SeriesAugust 22, 2014

Making the Case for Asset Recovery Operations

• Many financial crimes create the opportunity or necessity to recover assets

• Estimates suggest very little stolen in financial crime schemes is ever recovered – In US, 5% to less than 2%

• Expense of asset recovery operations can sometimes exceed amount recovered

• However, if assets remain with financial criminals, they effectively “win,” even if arrested

• To justify asset recovery operation, professionals should prepare:

• List of assets for which recovery is sought• Actual or appraised value for each asset• Names and contact information of persons who may

have interest in asset• Listing of registered owners, lien holders on assets• Statement explaining legal theory or justification behind

freezing each asset• Copies of all investigative or analysis reports in the case• Copies of all court orders previously issued in the case

Making the Case for Asset Recovery Operations

• Investigators • Forensic accountants • Lawyers • Analysts and support staff

Typical Members of Asset Recovery Team

Initial Considerations for Asset Recovery Team

• Does asset have value? Heavily encumbered What will it cost to preserve it during process

• Are there innocent owners who may impede recovery?

Equitable Weapons of Courts

• Restraining and mandatory injunctions

• Civil search warrants

• Break and search orders

• Accounting

• Constructive trust

• Appointment of receivers

•Many others found in CFCS manual

Other evidence-gathering tools

• Production orders

• Search warrants

• Customer information orders

• Account monitoring orders

• Disclosure orders, subpoenas or summons

10

Receivership

• Serve to locate, safeguard, recover assets

• Trustees, receivers, administrators, liquidators, officeholders

• Step in shoes of directors, entitled to all information

11

Asset forfeiture

• Criminal forfeiture- against the defendant or person

• Civil forfeiture- in rem - against property - proceeds, instrumentality of crime

• Substitute assets

12

Asset forfeiture

13

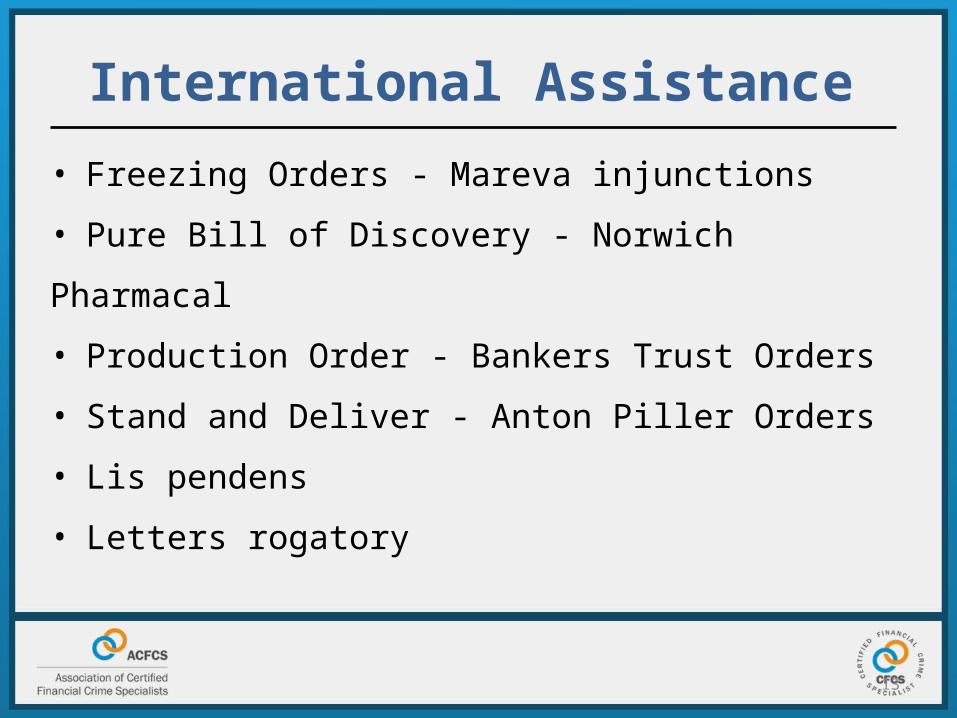

International Assistance

• Freezing Orders - Mareva injunctions

• Pure Bill of Discovery - Norwich Pharmacal

• Production Order - Bankers Trust Orders

• Stand and Deliver - Anton Piller Orders

• Lis pendens

• Letters rogatory

14

International Assistance

Mutual Legal Assistance Treaties (MLATs)

• Taking testimony of persons• Providing documents, records and evidence• Service of documents• Locating or identifying persons• Executing requests for search and seizure• Identifying, seizing and tracing proceeds of crime

15

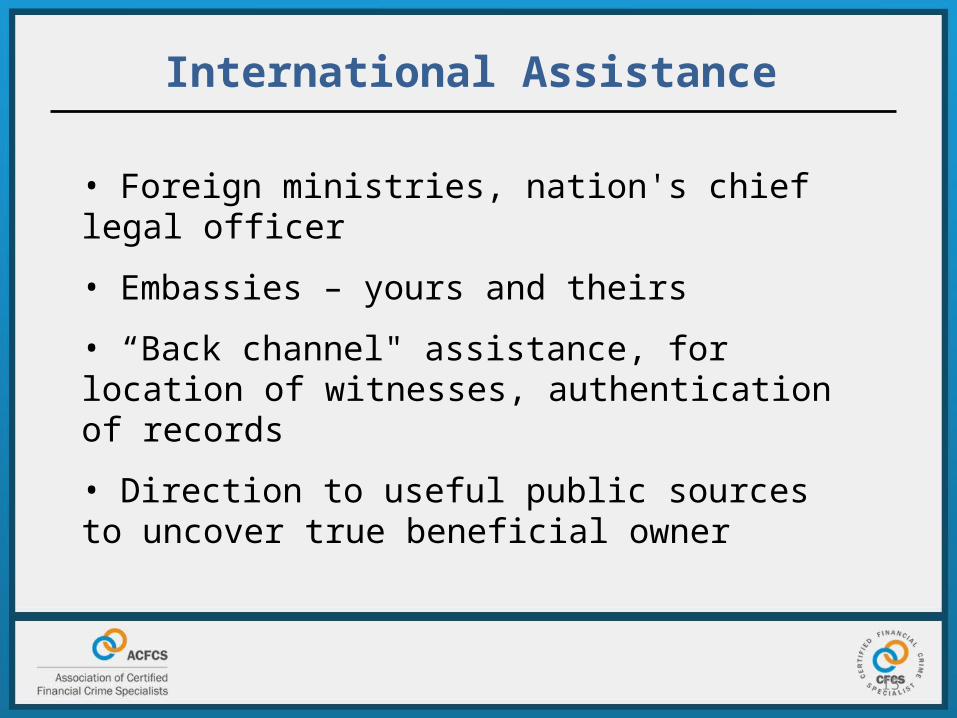

International Assistance

• Foreign ministries, nation's chief legal officer

• Embassies – yours and theirs

• “Back channel" assistance, for location of witnesses, authentication of records

• Direction to useful public sources to uncover true beneficial owner

16

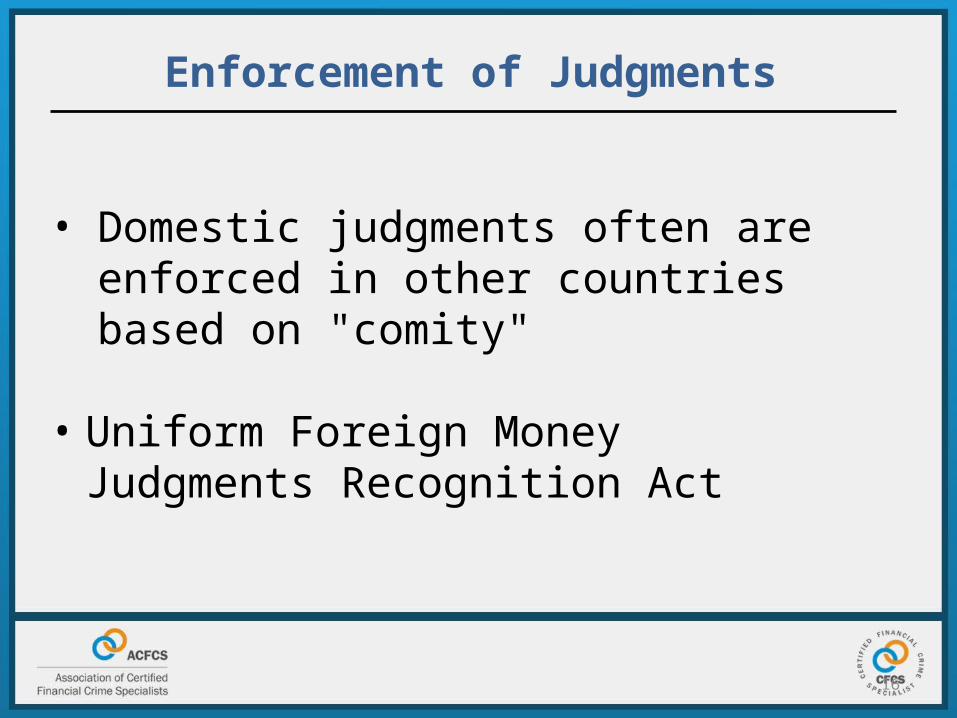

Enforcement of Judgments

• Domestic judgments often are enforced in other countries based on "comity"

• Uniform Foreign Money Judgments Recognition Act

Third Party Targets

• Third parties can be valuable, if difficult, targets for asset recovery operations

Possible third party targets• Banks • Broker-dealers, investment advisers, etc. • Company directors • Employees• Lawyers • Auditors and certified public accountants

Key Lessons

• Understand viable targets for asset recovery options

• Understand information sources, including open sources like corporate registries

• Many asset recovery operations have cross-border component – recognizing international tools is essential

Review Question

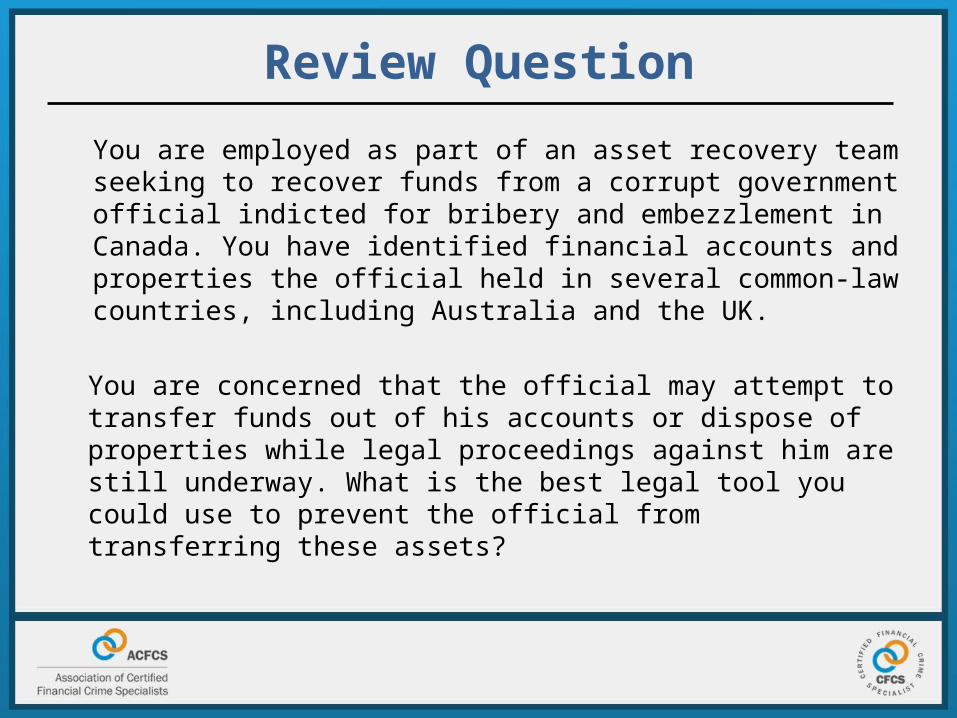

You are employed as part of an asset recovery team seeking to recover funds from a corrupt government official indicted for bribery and embezzlement in Canada. You have identified financial accounts and properties the official held in several common-law countries, including Australia and the UK.

You are concerned that the official may attempt to transfer funds out of his accounts or dispose of properties while legal proceedings against him are still underway. What is the best legal tool you could use to prevent the official from transferring these assets?

Review Question

A. Letters rogatory

B. Anton Piller order

C. Mareva injuction

D. Production order

Review Question

XYZ Industries, Inc., is incorporated in the British Virgin Islands and is indebted to a US-based company. You are a private financial investigator for a US-based company and are aware of many properties owned by XYZ Industries both domestically and internationally.

You have been hired to uncover the beneficial owner in order to identify available assets for repayment of outstanding debts and restitution of victims.

Which document would best assist the investigator to identify the beneficial owner?

Review Question

A. A power of attorney or designation of corporate agent.

B. A mail forwarding notice related to the property filed with the local postal service.

C. Articles of incorporation and board minutes for XYZ Industries, Inc. filed in the BVI.

D. A copy of a Mutual Legal Assistance Treaty request filed with the BVI seeking all beneficial ownership records.

Tax Evasion and Enforcement

CFCS Examination Preparation SeriesAugust 22, 2014

24

Overview and Definition

• Conduct designed to intentionally and illicitly avoid paying tax liabilities

• Often a thin line between tax evasion and legal “tax avoidance”

• Evasion is a financial crime itself and a common element of all other financial crimes

Convergence of Tax & Money Laundering Enforcement

• Global trend toward criminalization of tax compliance, enforcement will continue

• Convergence with other areas of law -- criminal law, money laundering, asset forfeiture, international evidence gathering

25

Convergence of Tax & Money Laundering Enforcement

26

• In February 2012, FATF issued revised recommendations on anti-money laundering

• For first time, tax offenses expressly listed as predicate for money laundering crimes

27

Tax Shelters

• Mechanism by which taxpayer may protect assets or income from taxation, or delay tax application

• Investments in pension plans and real estate are common examples, many shelters are completely legal

• Shelters can be deemed abusive by tax authorities when designed solely for avoiding or evading taxes

28

Tax or Secrecy Havens

• Jurisdictions that provide secrecy or other means of protecting assets from taxation• Individuals, corporations, other entities can shift

assets to havens through physical relocation, subsidiaries, shell corporations• Havens have been subject to increasing global

pressure

29

Characteristics of Tax or Secrecy Havens

• No or nominal taxes• Lack of effective exchange of tax information• Lack of transparency in the operation of legislative,

legal or administrative processes• Anonymous company formation• Negotiated tax rates• Inconsistent application of tax laws• Little or no regulatory oversight

30

Characteristics of Tax or Secrecy Havens

• No requirement for physical presence, allowing for shell corporations

• Self promotion as offshore financial center

• Examples of tax or secrecy havens• Seychelles• Panama• US states of Delaware, Nevada

31

Methods of Tax Evasion and Tax Fraud

• Income tax evasion can be straightforward as under-reporting income, overstating deductions, or not declaring offshore accounts

• Can be extraordinarily complex, involving offshore accounts and layers of corporate entities

• Tax codes of many jurisdictions are complicated, proving tax evasion requires willful intent to defraud

32

Methods of Tax Evasion and Tax Fraud

• Smuggling and evasion of customs duties• Employment tax fraud• Falsified worker status• Pyramiding• Third-party withholding• Cash payments

• Evasion of value added tax (VAT)• “Missing trader” fraud, carousel fraud

33

Methods of Tax Evasion and Tax Fraud

• Smuggling and evasion of customs duties• Employment tax fraud• Falsified worker status• Pyramiding• Third-party withholding• Cash payments

• Evasion of value added tax (VAT)• “Missing trader” fraud, carousel fraud

34

Red Flags of Tax Evasion

• Can be generally grouped into five categories

1. Behaviors or characteristics• Failing to follow advice of accountant, attorney or preparer• Failing to inform a tax professional of relevant facts • Repeated loss of government ID or other identifying materials• Use of many tax numbers by single person or entity• Unusual interest in tax reporting policies• Unusual customer relations with an institution – requests not to be contacted

directly, contact with institution is largely or only in person with long spans of time

2. Documentation or entity operations• Submission of suspicious wage and other statements• Missing/altered books and records • Variations in signature on duplicate tax returns• Submission of suspicious wage statements

35

Red Flags of Tax Evasion

3. Financial arrangements and analysis• Funds transfers to tax or secrecy havens• Income claimed does not match occupation• Tax withholding does not match income paid to employees

4. Timing• Tax and related documents appear to be backdated• Multiple returns submitted simultaneously by persons/entities

that appear to be connected – businesses with similar naming conventions, repeated patterns of digits in TINs, etc.

• “Other category” that encompasses wide array of hard and “soft” indicators of tax evasion

• Essentially enlists ‘Foreign Financial Institutions (FFIs)’ to act as extension of IRS enforcement network• Identifying US Taxpayers holding financial accounts or

investments in their institutions

• Reporting financial assets, US source income annually to IRS

• Withholding 30%, on behalf of the IRS, on certain payments coming from US for noncompliant accounts, institutions

• Reporting, withholding on accounts and payments to other FFIs that do not comply with FATCA

FATCA Overview

• March 2010 – FATCA signed into US law• February 2012 – Temporary IRS Regulations Issued• Numerous IRS Notices Since • January 17, 2013 – Final IRS Regulations Issued• Key Effective Date – July 1,2014

FATCA

38

Intergovernmental Agreements

Model I and Model II Agreements

• Model I requires FFIs to report information on US accountholders to their tax authorities, which collect and deliver it to IRS

• Model II requires FFIs to report information on US accountholders directly to the IRS.

• IGAs will require some countries to change their tax, privacy laws

• Some IGAs require reciprocal reporting – US institutions must report accountholders to tax authorities of signatory nations

39

FATCA Gains Worldwide Adoption

• FATCA Partners now include nearly 100

countries (including major economies like UK,

Mexico, China, Germany, Ireland, Italy,

Switzerland, Spain, Norway; many smaller

jurisdictions)

• Tax transparency now a worldwide initiative

• Participation ‘not an option’

40

G20, Tax Reform and Financial Transparency

41

OECD Automatic Exchange Standard

42

Key Lessons

• Understand structures used to evade taxes,

especially offshore legal entities

• Understand common types and red flags of tax

fraud schemes – employment tax fraud, VAT

• Recognize how FATCA works and how it is laying

groundwork for international tax enforcement

regime

43

Practice Question

Your bank holds a business account for a local tax preparation service.

What would MOST likely trigger further investigation by the compliance department in the bank?

A. Numerous deposits of tax refund checks in the names of different individuals but with common addresses

B. Multiple deposits of checks in the same amount written by different tax service customers

C. Variances in the frequency of transactions depending on the calendar cycleD. A request by the customer to have payments made to the Tax Office

through a certified check process

44

Practice Question

• Answer A is the correct answer due to the fact that this is a classic red flag for tax fraud. Multiple tax refund checks for different individuals going to the same address should set off warning alarms in nearly every jurisdiction.

• Answer B is incorrect because this perfectly fits the customer’s profile. The deposit of checks from different tax service customers is what you would expect as each customer paid their bill for the service. You would also expect many of them to be in the same amount for a typical tax preparation service since the fee for tax preparation would be the same for many customers.

45

Practice Question

• Answer C is incorrect because, once again, this fits the customer profile. You would expect variances depending on the calendar cycle as this is largely a seasonal business based on tax reporting deadlines.

• Answer D is incorrect because there is no indication of tax fraud in this response. The customer is making payments to his jurisdiction’s tax authorities using a certified check, which is simply a check for which a bank has confirmed sufficient funds exist to cover the amount of the check. This is not a viable means to commit tax fraud, and would more likely indicate no fraud is taking place.

Financial Crime Investigations

CFCS Examination Preparation SeriesAugust 22, 2014

47

Legal Underpinnings

• Common law systems• Rely on case law, precedent• Legal remedies not in statutes are available• Examples – UK, US, Canada, India, Australia

• Civil law systems• Written laws determine rights, remedies and actions• Examples – Latin America, Continental Europe, Japan

• Helps evaluate ground rules of place where investigation and possible litigation is conducted, costs, likelihood of success

48

Public vs. Private Investigations

• Public investigation by law enforcement agency, grand jury, regulatory body• Deploys all powers, authority of government

• Private investigations by civilians without government powers• Can obtain powerful tools from courts, equitable

remedies, bankruptcy and insolvency laws

49

Investigative Tools and Techniques

• Compulsory power to obtain documents and testimony• Telephone, electronic wire intercepts by government

agencies• Search warrants• Mutual Legal Assistance Treaties (MLATs) and less

formal mutual assistance• Undercover operations• Physical surveillance• Whistleblowers, anonymous tips, informants

50

Open-Source Intelligence

• Publically available information, often online• Many sources, often free and easily discoverable• Online searching and web content• Media outlets and news sources• Public records• Geospatial open source• Professional conferences, live events• Observation and reporting

• Investigation should usually start with exhaustive OSINT before moving to more time-consuming methods

51

Online Open-Source Tools

• Online information increasingly critical in financial crime investigations• Advanced web searching• Searching social networks, blogs• Utilizing free and paid online databases• “Deep web” sources• Reverse image searches• Archived web sites

• Financial criminal use online tools, investigator should take steps to remain secure and anonymous online

52

Interviewing Techniques

• Usually best to begin interviews with persons farthest removed from suspected crime

• Differences between interrogation and interview. In interview, investigator should establish rapport with witness and seek detailed responses.

• Look for knowledge of event, persons or entities involved, physical and intangible evidence

• Plan all elements of interview: location, objectives, needs of the witness

53

Intelligence vs. Evidence

• Intelligence furthers investigation but is not generally admissible in court

• Photos posted online• Information in a news article• Hearsay statements

• Evidence must meet legal rules of admissibility, be material and prove or disprove some relevant matter

• Commercial records obtained by subpoena• Statements made freely to law enforcement agent• Facts observed by enforcement agent conducting lawful

surveillance

54

Investigations Across National Borders

• Many financial crime investigation require assistance from other nations and jurisdictions

• When requesting assistance from another nation for, consider:• Its legal and statutory requirements • How to assure that the information will be admissible as evidence• Will investigative subject be notified of request for assistance? Are

you legally compelled to inform the subject?• Level of probable cause needed to authorize investigative

techniques and enforce court orders

55

Tips and Whistleblowers

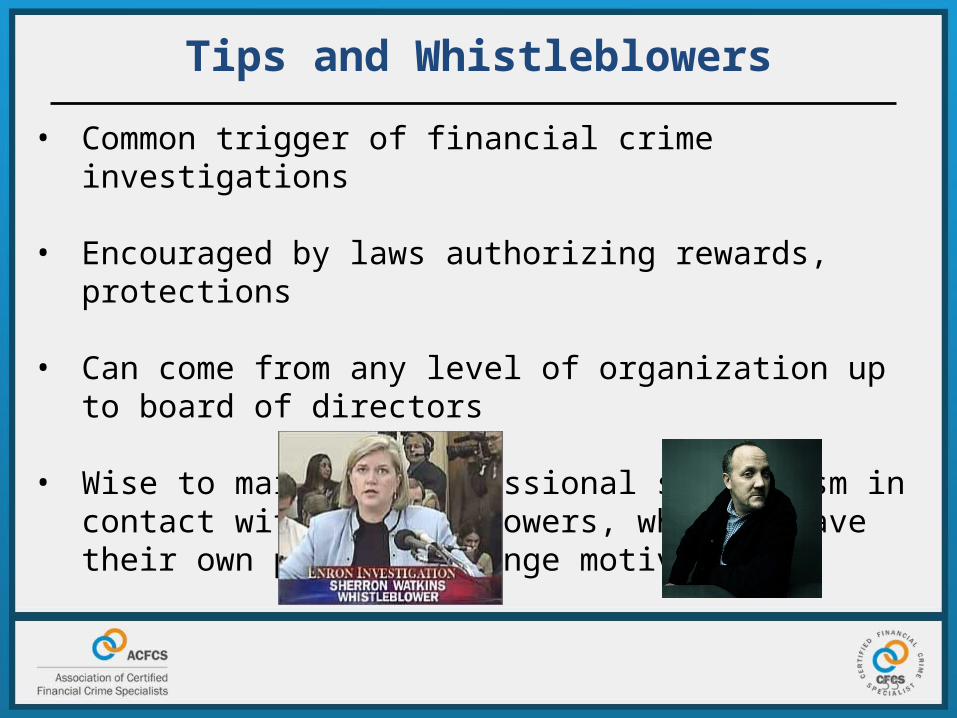

• Common trigger of financial crime investigations

• Encouraged by laws authorizing rewards, protections

• Can come from any level of organization up to board of directors

• Wise to maintain professional skepticism in contact with whistleblowers, who may have their own profit, revenge motives

56

Investigating Employees• Some companies have rules on employee cooperation in

internal investigations, but they must not conflict with laws

• Employee usually has no legal obligation to agree to an interview

• Employer may usually provide employee e-mail, phone logs and computer usage without employee permission, knowledge

• Investigator should consult lawyer on whether it is legal, advisable to obtain employee records without consent

57

Court Orders

• Search warrants • Granted by judge to government agencies, • Specify time, place and items to search• Failure to follow terms may render evidence useless

• Subpoena• Compels a person or entity to produce records, items or

testimony at a place and time• Considerable variation on process among countries

• Preservation orders or litigation holds• Prevent electronic evidence from being deleted or altered

58

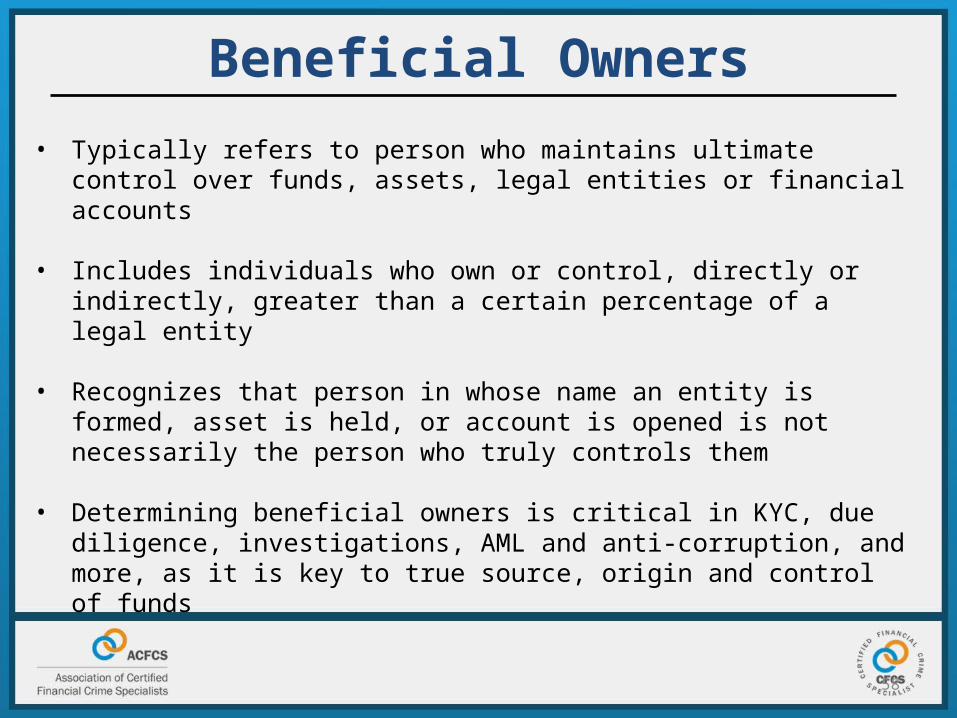

Beneficial Owners

• Typically refers to person who maintains ultimate control over funds, assets, legal entities or financial accounts

• Includes individuals who own or control, directly or indirectly, greater than a certain percentage of a legal entity

• Recognizes that person in whose name an entity is formed, asset is held, or account is opened is not necessarily the person who truly controls them

• Determining beneficial owners is critical in KYC, due diligence, investigations, AML and anti-corruption, and more, as it is key to true source, origin and control of funds

59

Corporate Registries

• Collect and store information pertaining to corporations and other legal entities created within a given jurisdiction

• Typically maintained by a government agency or department

• May be a single registry for an entire nation, or multiple registries for different states, regions or cities, depending on jurisdiction

• Serve several purposes:• Record creation or incorporation of new legal entity• Collect required information on legal entities• Make some or all collected information publicly available

60

Corporate Registries

•The following information is usually available from corporate registries: •The name and type of the legal entity•Date of the company formation, and date when the company was dissolved

if no longer in existence•Articles of incorporation and other company formation documents•A physical address of the corporation, or address of formation agent•Name and address of a registered agent for the company

•Some jurisdictions will provide: •Names and addresses of the legal entity’s directors or officers•Names and addresses of the shareholders, members or other legal owners

of the legal entity

•Beneficial owner of legal entity is very rarely available

61

Corporate Registries

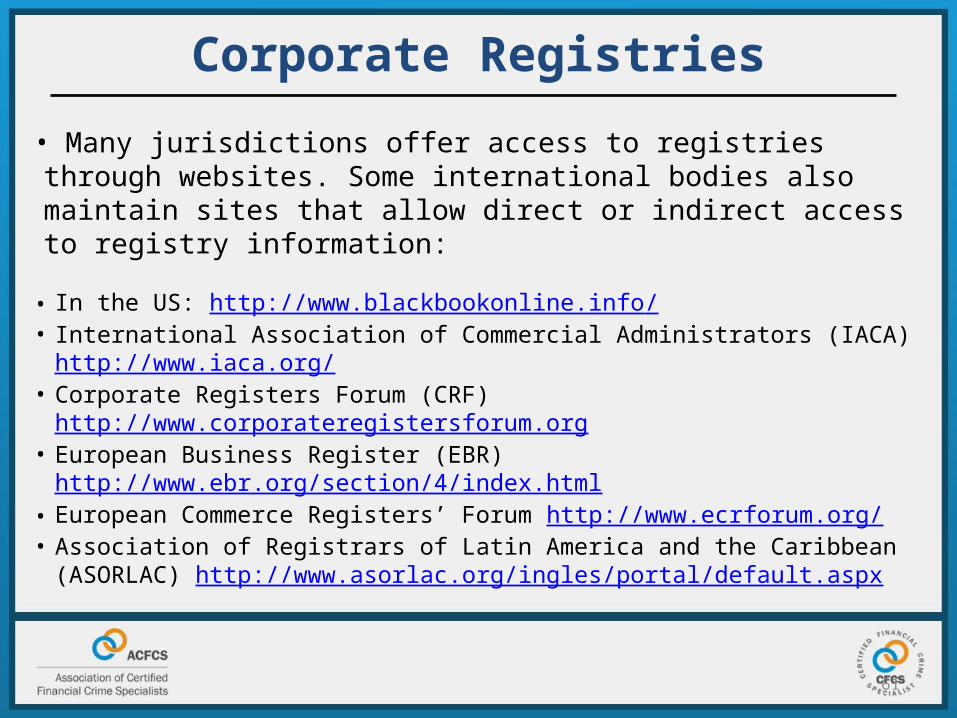

• Many jurisdictions offer access to registries through websites. Some international bodies also maintain sites that allow direct or indirect access to registry information:

• In the US: http://www.blackbookonline.info/• International Association of Commercial Administrators (IACA)

http://www.iaca.org/ • Corporate Registers Forum (CRF) http://www.corporateregistersforum.org • European Business Register (EBR) http://www.ebr.org/section/4/index.html • European Commerce Registers’ Forum http://www.ecrforum.org/ • Association of Registrars of Latin America and the Caribbean (ASORLAC)

http://www.asorlac.org/ingles/portal/default.aspx

62

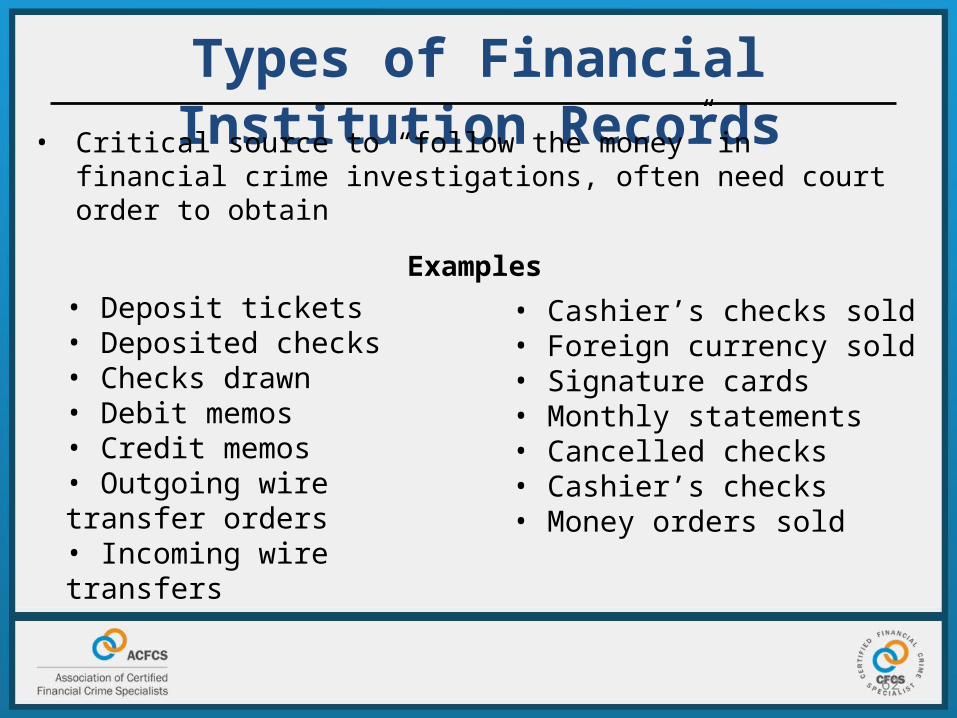

Types of Financial Institution Records• Critical source to “follow the money” in financial crime

investigations, often need court order to obtain

Examples

• Deposit tickets • Deposited checks• Checks drawn • Debit memos • Credit memos • Outgoing wire transfer orders • Incoming wire transfers

• Cashier’s checks sold • Foreign currency sold • Signature cards • Monthly statements • Cancelled checks• Cashier’s checks • Money orders sold

63

Summarizing Financial Institution Records

• Investigator should prepare summaries of information in documents from an institution, including:

• Deposits and withdrawals• Checks written on the account• Wire transfers into or out of the account• Fluctuations in account balances

• Obtain all documents related to account opening and customer onboarding: application, customer ID, signature card, due diligence and Know Your Customer records

64

What Financial Institution Records Show

• Some leads that a financial account analysis can provide: • Names of persons, entities that received funds• Names of persons, entities that deposited money • Sources, amounts of income or revenue• Cash withdrawals and purchase of cashier’s checks• Activities of previously unknown businesses and ventures• Wire transfers to, from offshore havens, accounts, nominees• Previously unknown accounts• Liabilities, which lead to other financial statements• Asset acquisition, disposition

65

Other Financial and Commercial Records

Examples

• Commercial invoices• Cancelled checks• Receipts, related expense

documentation• Journal entries

• Statement of cash flows• Vendor and customer lists• Physical inventory• Reconciliation of

intercompany accounts

• Tax returns are also a valuable source of information if they can be obtained legally

66

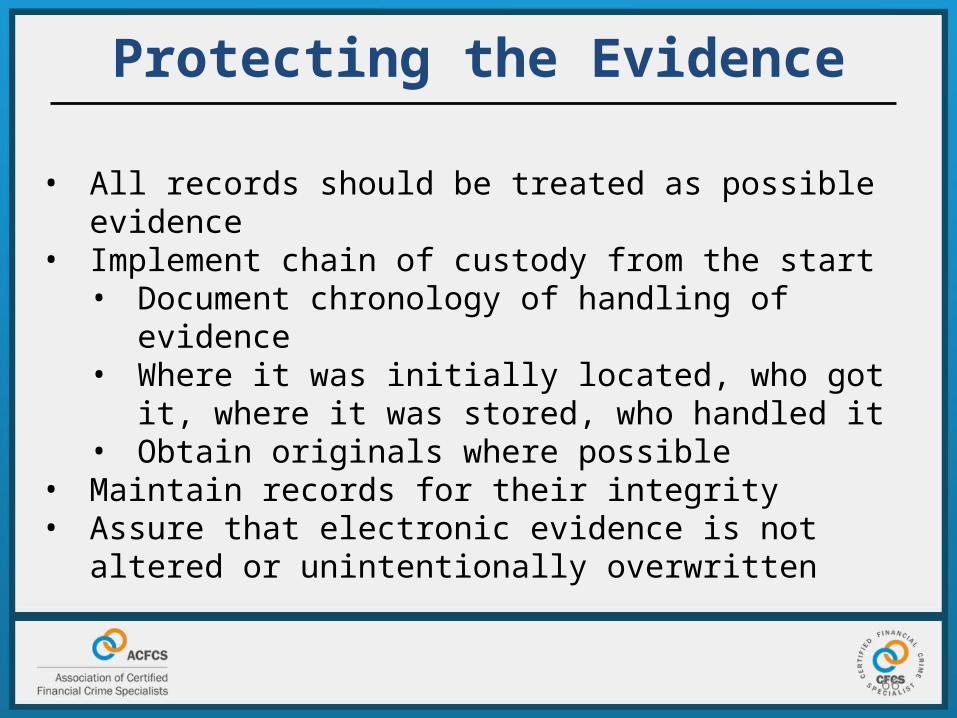

Protecting the Evidence

• All records should be treated as possible evidence • Implement chain of custody from the start• Document chronology of handling of evidence• Where it was initially located, who got it, where it was

stored, who handled it • Obtain originals where possible

• Maintain records for their integrity• Assure that electronic evidence is not altered or unintentionally

overwritten

67

Key Lessons

• Recognize the types of documents and records that can be employed in financial crime investigations

• Understand the differences between evidence and intelligence, and the proper role of each

• Open source intelligence is highly valuable – be familiar with open sources, online and otherwise

Review Question

68

Securities King was a stock brokerage that collapsed after it was revealed to be running a Ponzi scheme. The scheme has left behind numerous defrauded investors and the brokerage is now being liquidated in bankruptcy court. You are an investigative professional who has been asked to look into a lawyer suspected of involvement in the Ponzi scheme. The lawyer is thought to have handled funds for Securities King through his firm’s account. There has been no prior investigation of the lawyer, and you currently have little information him or his firm.

What would be the most appropriate first step to take in your investigation?

Review Question

69

A. Request that a bankruptcy court judge name you a

receiver of Securities King

B. Contact the lawyer to schedule an interview

C. Thoroughly research the lawyer and his firm online

and in public records

D. Conduct physical surveillance of the lawyer to

understand his movements

Review Question

70

Answer C is the correct answer. While all four responses may be appropriate at some point in the investigation, the question asks for the most appropriate first step.

As you currently have little information on the attorney, it would be inappropriate to approach a judge with a request to be named receiver. Likewise, conducting surveillance and interviewing the attorney are more time-consuming and potentially risky steps best left to later in the investigation, if conducted at all. Starting with thorough open-source research would be the investigative best practice.

Review Question

71

You are a financial crime specialist who has been retained as part of a cross-border investigation into a complex money laundering scheme. You have been asked to investigate a company that is suspected to have played a role in laundering funds. The company is incorporated in the US state of Nevada.

It is believed that the beneficial owner of the company is one of the key perpetrators behind the laundering scheme, and identifying him or her is a priority of the investigation.

Which source below would be the most likely to lead to information on the shell company’s beneficial owner?

Review Question

72

A. Records listing the company’s shareholders and directors.

B. Company information provided by the Nevada corporate registry.

C. Records provided by the offshore company service provider that assisted with incorporation.

D. Contact information for a company formation agent in the company’s records.

Fraud Detection and Prevention

CFCS Examination Preparation SeriesAugust 22, 2014

74

Overview and Definition

• Intentional misrepresentation, concealment or deception in pursuit of financial gain or to further a financial crime

• Recent fraud trends• Greater professionalization, smarter attacks• Increased “sharing” of fraud practices• More frauds perpetrated from offshore locations• Technical fraud or cybercrime combined with traditional skills• More collusion between merchants, fraudsters and organization

insiders

75

Understanding and recognizing types of fraud

• Ponzi schemes• Despite recent exposure, remain widespread type of fraud

• Some red flags • Investment returns “too good to be true”• Investment statements show growth or performance

contrary to market trends• Unusual or no fee structure• Lack of information or substance behind investment

• Securities fraud• Misrepresentation around a security, which can be

virtually any tradable asset or financial instrument• Inaccurate or misleading information to encourage

investment• Selling a security that is illegal or nonexistent• Insider trading

• Now facilitated by online communications, social networks, other tools

76

Understanding and recognizing types of fraud

• Common types of securities fraud include– Microcap or “penny stock” frauds, like pump and dump

schemes– Insider trading– Hidden terms and agreements– Fraud tied to falsified reporting or accounting

• In US alone, securities fraud estimated to total $10 – 40 billion annually

77

Understanding and recognizing types of fraud

• Fraud in loans and mortgages• Intentional, material misrepresentation or omission to

obtain loan or larger loan than lender typically grants• May also be perpetrated by lenders: loans with hidden or

predatory terms, unlicensed lenders

Common schemes

78

Understanding and recognizing types of fraud

• Income and employment fraud• Occupancy fraud• Appraisal fraud

• “Shot-gunning” fraud• Cash-back fraud• Foreclosure scams

• Credit and debit card fraud• Need not involve physical fraud; increasingly common to

steal numbers, personal information online• Tampering with card readers at ATM and other point-of-

sale locations through skimmers• Online theft of numbers through compromise of online

security or data breaches• Gathering personal information by sending fake

applications for cards to targets• Physical theft of card

80

Understanding and recognizing types of fraud

• Other types of fraud include:– Insurance– Health care– Government benefits

• Can be perpetrated by an entity against a customer or by customer against an entity

81

Understanding and recognizing types of fraud

• Health care insurance fraud includes:

– Upcoding – billing for a higher covered service than performed.

– Using the wrong procedure code to get something covered Breaking up a “package” into individual procedures usually more expensive

– Setting up fake clinics, often involving shell companies with no physical location

82

Understanding and recognizing types of fraud

• Fastest growing types of consumer fraud• A leading threat to accounts at banks and other

institutions• Common ways to steal identities • Social engineering• Creating fake online identities• Technological tools – skimmers, phishing, malware• Internal fraud and data theft

83

Identity Theft and Fraud

• Common signs indicating a stolen or compromised identity• Alerts and warnings from a credit reporting company• Suspicious documents, including forged or altered IDs• Inconsistent personal identifying information• New credit or debit card request immediately after

notification of change of address

• Identity theft furthers many other fraud schemes• Using stolen identities to obtain government benefits, tax refunds• Obtaining loans or mortgages with false identities• Opening accounts with stolen or false identities

84

Red Flags of Identity Theft

Preventing Fraud

85

• Similar measures as other compliance programs, but training, awareness are even more important in fraud prevention

• Starts with comprehensive fraud risk assessment• Create a team with necessary expertise• Identify organization’s universe of fraud risks

• Fraudulent financial reporting• Misappropriation of assets• Expenditures, liabilities for improper purpose• Revenue and assets obtained by fraud• Costs, expenses avoided by fraud• Financial misconduct by management

Preventing Fraud

86

• Assess likelihood of fraud schemes or scenarios• Assess materiality of risks: which schemes would

have greatest impact• Assess preexisting fraud controls, compare them

against risks• Consider how controls may be over-ridden or manipulated

by employees and others• Employee collusion is serious fraud risk

Key Lessons

87

• Preventing fraud is heavily reliant on awareness, training, and internal controls

• Financial crime professionals should be prepared to identify many types of fraud

• Fraud schemes are frequently linked – one element feeds into larger operation

Review Question

88

• Your institution has recently been dealing with a large number of identity theft cases, in which thieves have stolen sensitive customer data and used it to fraudulently apply for credit cards.

After an initial investigation, you suspect that an employee is participating in the identity theft scheme. What would be the most effective first step you could take to prevent further theft of customer information?

Review Question

89

A. Immediately notify customers whose data has been compromised

B. Restrict access to sensitive customer data, and monitor employee access on an ongoing basis

C. Impose strict alert thresholds in the automated monitoring system for all credit cards

D. Conduct a mandatory ethics seminar with all institution employees

Review Question

90

Answer B is the correct response. Like some other review questions, all of these answers could be considered good responses to a data breach or theft.

However, only Answer B will actually serve to prevent further theft of data, which is the focus of the question.

Review Question

91

A mortgage administrator has been dealing with a buyer attempting to obtain a large mortgage on a home from your institution. According to the buyer, he is seeking to purchase the home as an investment property.

The buyer has been behaving erratically and has been difficult to contact at times. Concerned about a potential fraud, the administrator has asked you to examine the mortgage application and accompanying documents.

You note the following information. Which is the best indicator that the buyer may be committing mortgage fraud?

Review Question

92

A. A real estate agent from a nearby city is helping to broker the sale

B. The seller is not currently listed as the occupant of the property

C. The buyer currently has a large mortgage outstanding on his own property

D. The buyer has no previous history of obtaining mortgages from your institution

Review Question

93

Answer C is the correct answer. In the question, it describes the loan applicant as seeking the home as an investment property. However, the applicant has a large mortgage outstanding on his own property, raising questions about his finances and ability to purchase an investment property.

Answer B may also be considered a red flag by some. However, in the question it describes the buyer’s behavior as erratic and potentially suspicious. Since the buyer is already under suspicion, the red flag in Answer C should be given priority. Answers A and D are not indicative of any suspicious or fraudulent activity.

International Standards

CFCS Examination Preparation SeriesAugust 22, 2014

95

Overview

• Combating financial crime is an international and cooperative affair

• Financial crime is global phenomenon, requires coordinated action at international level

• International standards set the pace for most of the formal financial sector

• Some national laws have an extra-territorial “international standards” effect

United Nations

• UN Security Council Resolutions– Sanctions programs

• United Nations Convention Against Corruption

96

UNODC

• IMOLIN database–Legal library of AML and related laws–https://www.imolin.org/

98

Transparency International

• Anti-corruption NGO with over 100 chapters worldwide

• Provides research, analysis and reporting on corruption, corporate and financial transparency issues globally

• Releases Corruption Perceptions Index annually• http://www.transparency.org/research/cpi/ove

rview

99

Corruption Perceptions Index

OECD

• OECD Anti-bribery Convention• Initiatives related to:– Anti-money laundering– Tax fairness and sharing• Database of tax sharing agreements

– Corporate transparency– Illicit financial flows

101

FATF• Outgrowth of OECD

• Formerly 40 + 9 Recommendations, now 40 Recommendations

• Sets standards for AML cooperation among countries• Peer reviews• “Non-cooperative” jurisdictions, black or grey lists

World Bank

• Stolen Asset Recovery Initiative (StAR)• http://star.worldbank.org/star/

• Doing Business Reports–Database of business laws, regulations and

data on business climate and transparency–www.doingbusiness.org

103

Basel Committee

• Establishes principles relating to banking supervision• http://www.bis.org/bcbs/• Basel III Accords• Customer Due Diligence for Banks• Consolidated KYC Risk Management

Wolfsberg Group

• Group of largest international banks– Set standards for private banking, correspondent

banking relationships• Wolfsberg AML Principles for Private Banking• Wolfsberg Principles for Intermediaries

– Maintains Due Diligence Repository database– http://www.wolfsberg-principles.com/diligence.ht

ml

105

EGMONT Group

• Organizations of FIUs meeting standards

• Provides cooperation between FIUs

INTERPOL• Cooperative effort among police of countries• Issue Notices to members that share

information, provide warnings, or request that members track or detain suspects

• Modeled after FATF on regional basis• APGML• Others

• Conduct peer reviews

FATF-style Regional Bodies

108

National Laws with International Effect

• US:

• USA Patriot Act

• FCPA

• FATCA

• UK:

• UK Bribery Act

• EU:

• Directives

109

Key Lessons

• May not be used on day-to-day basis, but international standards shape public and private efforts

• International best practices may not be your best practices

• Review source documents where possible

110

Review QuestionYou are conducting a country-level corruption risk assessment for a corporation planning to expand into several new jurisdictions.

Which of these sources would most likely provide the most useful starting point for your assessment?

A. World Bank Stolen Asset Recovery Initiative reports

B. Interpol Notices

C. Transparency International Corruption Perceptions Index

D. Wolfsberg International Due Diligence Repository

Ethics

CFCS Examination Preparation SeriesAugust 22, 2014

112

Overview

• There is no one accepted international standard

• Ethical standards for different professions and organizations – compliance, regulation, enforcement, law, investigation, etc.

• Financial crime professionals confront numerous ethical risks

• “If you have to ask about it, it’s probably wrong.”

113

Duties to Client

• Financial crime specialist owes highest duty of honesty, transparency and professionalism to constituents, client, organization, colleagues

• Identifying who is your client in broad terms, acting in their best interests is key to ethical behavior

• Does not permit unethical or illegal behavior to further “best interests” of client

114

Conflicts of Interest

• Take variety of forms – personal interests, current and past clients, multiple clients

• Maintaining ethical standards relies on finding fair and equitable resolution to conflicts

• In most cases, one client’s interests should not be privileged over another

115

Conflicts of Interest

• Organizations should screen for conflicts of interest at the start of relationships:

• Assess services, activities, types of employees to identify areas where conflicts of interest may arise

• Implement written disclosure policies• Designate conflict of interest officer or committee• Create “conflicts of interest database”• Training programs for employees on conflicts of

interest and their ethical resolution

116

Conflicts of Interest • Conflicts should be recognized early in relationship

• If not, timely response is required, which can include:

• Promptly disclosing to past or present colleagues, clients or organizations the nature of a potential conflict of interest

• Asking these persons and organizations to waive conflicts of interest that may exist, if it is appropriate

• Creating an information wall or other safeguards to assure that persons who were involved with a prior matter will not see or have access to files from the new matter, and will not participate in the new matter

• Declining to accept the prospective matter or case

117

Data and Privacy Concerns

• Financial sector professionals often have access to sensitive financial, personal information

• Organizations need policies and procedures to ensure information of customers, clients, and other parties is managed ethically

• “Information barriers” to separate sensitive data and reduce potential for conflicts of interest

• Multi-tiered access systems to limit information to essential staff• Processes to end relationships and purge or delete information

118

Ethics Policies and Procedures

• Code of ethics

• Employee training, ethics policies

• Confidential reporting, escalation policies

• Commitment, communication from top leadership

119

Key Lessons

• Acting in client’s best interests guides ethical behavior

• Information barriers are essential safeguard at financial institutions, other organizations

• Conflicts of interest are common ethical dilemma; understand how they can arise and how to resolve them

120

Review QuestionYou are part of a committee helping to review your organization’s ethics policies and procedures. As part of the review, you have been asked to make recommendations.

What is one recommended policy you should include?

A. Senior management approval for all new customer relationshipsB. Suspension or dismissal of any employees with conflicts of

interest C. Reporting of ethical violations that is escalated through business

linesD. Monthly messages on ethical policies and issues from senior

management

Your Questions

Thank you for attending