april 9, 2008 turmoil in the contracting business a contractor’s perspective james f davis, p.e....

TRANSCRIPT

April 9, 2008

Turmoil in the Contracting

Business

A Contractor’s Perspective

James F Davis, P.E.SNC-Lavalin Houston

The information contained herein is gathered from public and non-confidential sources and is offered only within the context of this non-authoritative Presentation. The material is subject to frequent and substantial change over time and some sources cannot be independently verified. This information is not not suited for technical basis of design nor for financial, business or investment decisions. The format and content including forward projections are that of the Author.

April 9, 2008

Overview What is the Manifestation of this Turmoil?

What is Causing it?

Impact upon Capital Projects

What can be done about it?

What does the Future look Like?

April 9, 2008

Stating the Obvious • Extensive capital project activity in infrastructure,

energy, power, refining

• Cost of Materials have increased by 25 – 90 % since 3rd Qtr 2004

• Equipment lead times have stretched out

• Competent and qualified consultants, engineers and contractors are busy

• Lump sum turnkey (LSTK) with full wrap contracts are very rare

• “Project Costs have risen by 35% from 2004 to 4th Qtr 2007” – C.E.R.A.

$1 trillion by 2014

April 9, 2008

Turmoil in the Contracting Business

External forces have reduced stability in equipment, material and labor cost and equipment lead times to a point at which traditional estimating and forecasting methods utilizing historical information (and financing) models may no longer apply.

April 9, 2008

These external forces have upset the

supply / demand balance that caused

“perfect storm waves” in . . .

. . . availability, cost and lead times resulting in the loss of predictability.

April 9, 2008

What Happened?

85 90 95 00 05 10

1.0

15

Relative Capacity

850.0

43%10%

Creeping Demand Growth

Low Sulfur Fuels

Greenhouse Gases

Fugitive Emissions-NESHAP

Reduction of Sox and NOx

De-Bottlenecked Capacity

Un-satis

fied D

emand = New C

apacity

April 9, 2008

Sustained External Forces • Global & Regional Energy Capital Project Activity ($1.3 t USD)

– $100 b in Mid-East gas monetization: Gas production; LNG; GTL

– $65 b in West Africa gas & oil production

– 2 x $3.5 b U.S. refineries (Motiva; Marathon)

– Multiple oil sands projects in Canada

– ExxonMobil alone will spend $52 billion by 2012

• Major Infrastructure & Energy Projects with Global Impact

– China: Three Gorges Dam; IGCC; CTL

– India: refineries, energy imports, transportation

– Russia: energy; infrastructure

2010 = 2.9 mm bpd; $30+b CA

5.8% annually

April 9, 2008

Unexpected External Forces

Ivan $4.6 b

Rita $9.2 b

Katrina$5.8b Nebraska, January 2007

April 9, 2008

Most Significant Impact

• Equipment & Bulk Material – Turbines, pumps, compressors

– Alloy, structural steel shapes, cable

• Experienced Craft Labor

• Pressure vessel fabrication capacity

• Limited supply of experienced

engineers & constructors

April 9, 2008

Schedule ExamplesGas Turbines 36 mo

Compressors 30 mo

Gasifier Vessel 26 mo

Hydrotreater Vessel 30 mo

Air Separation unit 34 mo

Ethanol Dryer 22 mo

Field-erected Tank (306ss) 30mo

ANSI 900 Pipe 22 mo

April 9, 2008

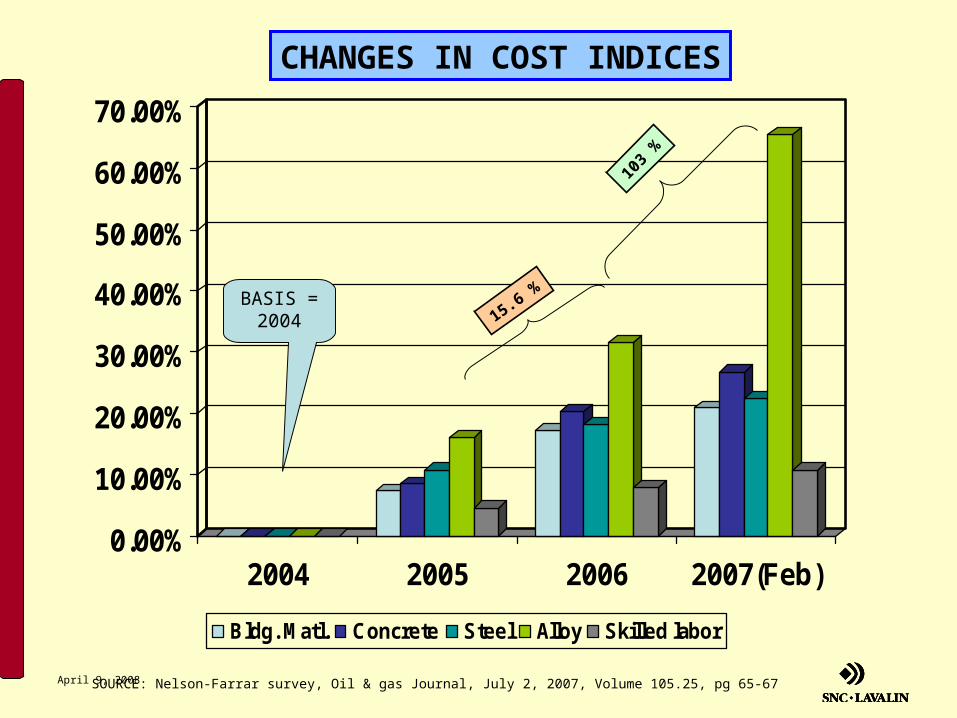

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

2004 2005 2006 2007(Feb)

Bldg. Matl. Concrete Steel Alloy Skilled labor

BASIS =2004 15.6 %

SOURCE: Nelson-Farrar survey, Oil & gas Journal, July 2, 2007, Volume 105.25, pg 65-67

CHANGES IN COST INDICES

103

%

April 9, 2008

Examples 2006 vs. 2002• Craft Labor

– Hourly USGC Rate from $17 to $25 ($24 to $34)– Availability of sufficient numbers: concrete, carpentry– Qualifications in critical skills: welding, pipefitters– South of Interstate I-40 is the same labor pool

• Engineering: Global Demand = Global Shortage– Delayed salary impact until late 2005 as slack absorbed– “Catch-up” rates Jan ’06 to Jan ’07 = +10% (Houston)– Forecast @ 8-10% annually through 2008 *– Aging workforce: estimated average age = 47– Competing projects in refining; coal; chemicals; renewables, E&P,

infrastructure

*Source: Houston E&C Salary Survey, Trace Consultants, Inc.

April 9, 2008

Gulf Coast Project Activity*

* Modified for Regional Activity

Company Project Value DateConstruction Hours-peak

Motiva Refinery Expansion $7.0 billion 2011 5,950

Eastman Chemical

Coal Gasification Plant $1.6 billion 2011 1,360

Marathon Garyville Expansion $5.0 billion 2012 4,250

Eastman Chemical

Coal to Chemicals (2) $3.6 billion 2012 2,550

Total Refinery Expansion $1.8 billion 2010 1,530

Valero Refinery Expansion $1.4 billion 2010 1,190

Sempra LNG Terminal $1.0 billion 2010 850

$20.2 billion 17,680

$1b over 24 months = 3.0 mm work hours = 850 peak; 700 avg.

April 9, 2008

NET EFFECT

Today’s capital market is in turmoil with minimal opportunity to properly forecast costs and schedules more than 2-3 quarters in advance.

This lack of predictability must be considered in every capital project decision to assure continued financial viability.

April 9, 2008

??? = Risk = $$$

Unless extraordinary actions are taken to understand actual risk exposure –

- the absence of any reasonable degree of predictability in the market will inevitably result in significantly higher financial risk and hence project costs.

April 9, 2008

Major Project Cost BreakdownCategory $ %Equipment 650 52Bulk Materials 225 19Transportation 35 3Construction Mgmnt 75 6Craft Labor 175 14Engineering 80 6

Total 1240 100Project Risk* 384 31

* Contingency, escalation, growth, risk fee - from historical project experience

April 9, 2008

New Objective

Minimize the uncertainty in both final cost and schedule of capital projects:

– Step-wise / gated project development procedure

– Quantitative risk assessment of design

– Shared-risk contracts

April 9, 2008

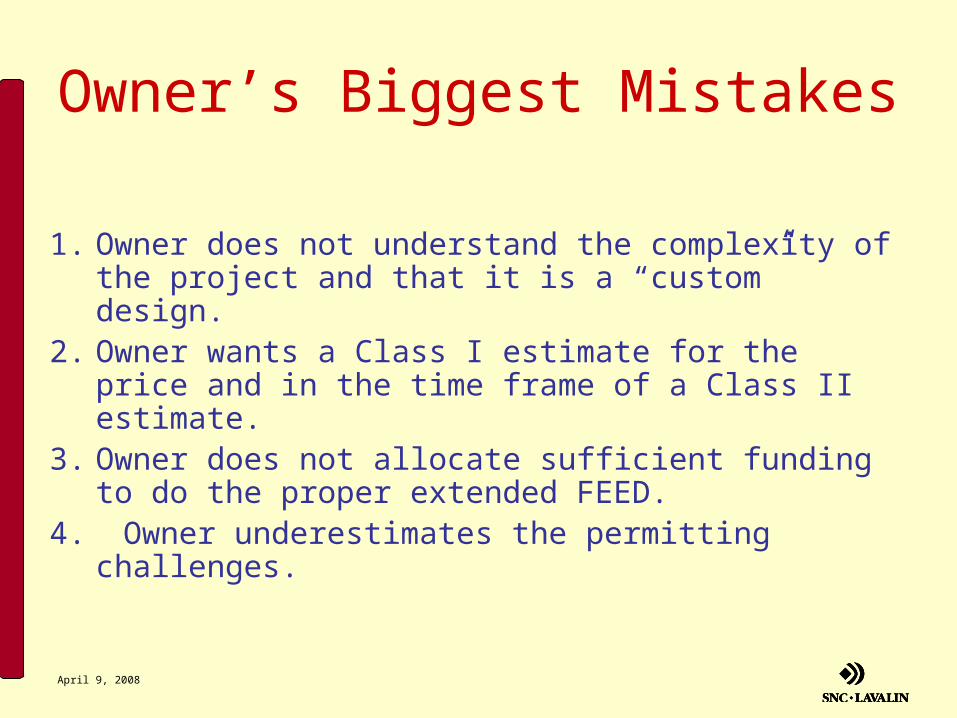

Owner’s Biggest Mistakes

1. Owner does not understand the complexity of the project and that it is a “custom” design.

2. Owner wants a Class I estimate for the price and in the time frame of a Class II estimate.

3. Owner does not allocate sufficient funding to do the proper extended FEED.

4. Owner underestimates the permitting challenges.

April 9, 2008

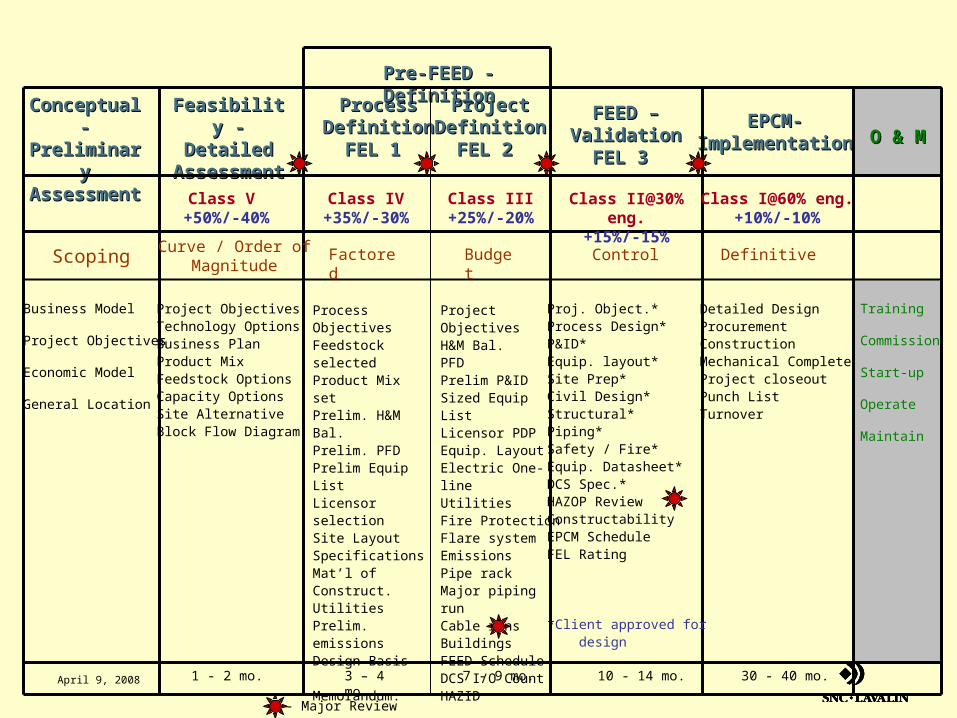

Conceptual -Conceptual -Preliminary Preliminary AssessmentAssessment

Feasibility -Feasibility -Detailed Detailed

AssessmentAssessment

ProcessProcessDefinitionDefinition

FEL 1 FEL 1

ProjectProjectDefinitionDefinition

FEL 2 FEL 2

FEED –FEED –ValidationValidation

FEL 3 FEL 3

EPCM-EPCM-ImplementationImplementation O & MO & M

Pre-FEED - DefinitionPre-FEED - Definition

Class V +50%/-40%

Class IV+35%/-30%

Class III+25%/-20%

Class II@30% eng.+15%/-15%

Class I@60% eng.+10%/-10%

ScopingCurve / Order of

MagnitudeBudget DefinitiveControl

Process Objectives Feedstock selectedProduct Mix setPrelim. H&M Bal. Prelim. PFDPrelim Equip ListLicensor selectionSite LayoutSpecificationsMat’l of Construct.UtilitiesPrelim. emissionsDesign Basis Memorandum.

Project Objectives H&M Bal. PFDPrelim P&IDSized Equip ListLicensor PDPEquip. LayoutElectric One-lineUtilitiesFire ProtectionFlare systemEmissionsPipe rackMajor piping runCable runsBuildingsFEED ScheduleDCS I/O CountHAZID

Project ObjectivesTechnology OptionsBusiness PlanProduct MixFeedstock OptionsCapacity OptionsSite AlternativeBlock Flow Diagram

Business Model

Project Objectives

Economic Model

General Location

1 - 2 mo. 3 – 4 mo. 7 - 9 mo. 10 - 14 mo. 30 - 40 mo.

Detailed Design ProcurementConstructionMechanical CompleteProject closeoutPunch ListTurnover

Proj. Object.* Process Design* P&ID*Equip. layout*Site Prep*Civil Design*Structural*Piping*Safety / Fire*Equip. Datasheet*DCS Spec.*HAZOP ReviewConstructability EPCM ScheduleFEL Rating

*Client approved for design

Factored

Training

Commission

Start-up

Operate

Maintain

- Major Review

April 9, 2008

• Fair & balanced allocation of risk– Identify all major risks: formal process– Quantify and Prioritize Impact upon Project– Resolve: design out, mitigate, insure, fund– Probabilistic (Monte Carlo) quantification– Allocate mitigation to appropriate Party

Risk Value – Net Mitigation – Funding = Net Risk Exposure*

* Risk Resolution White Paper; Westney Consulting Group;2007

Quantitative Risk Assessment*

April 9, 2008

Deferred Conversion Contract“Open book” conversion from reimbursable extended

FEED into fixed price EPC:– Continue FEED (pre-EPC) on reimbursable basis

against Class II (15%) estimate at end of typical FEED– Execute 50-60% of detailed engineering to fix bulk

quantities – order pipe & steel (19%)– All major equipment ordered (52% of TIC)– Fix engineering and project management (12% of TIC)– Fix craft labor costs (14% of TIC)

$40 mm

= 97% of TICRi$k

April 9, 2008

Deferred Conversion ContractsAlternative Approaches during FEED• Commitment / order of major equipment

• Order certain bulk items: pipe, steel

FEED EPC

50% eng.

Equipment

Bulk Material

Convert toFixed price

GapFunding

FixedPrice

Risk Capital

FINANCIALCLOSE

+/-15%

+/- 10%

Extend

$20mm $35mm

April 9, 2008

New Approach - Owner• Negotiated contracts through an extended FEED

to achieve “true” Class I estimate– $30mm - $35mm vs. $18mm - $20mm

• QRA to quantify risk and identify Fuzzy areas • Early order / commitment of equipment• Contingent Equity – Gap Financing• Neutral balance payment programs• Contingency financing for residual risk

April 9, 2008

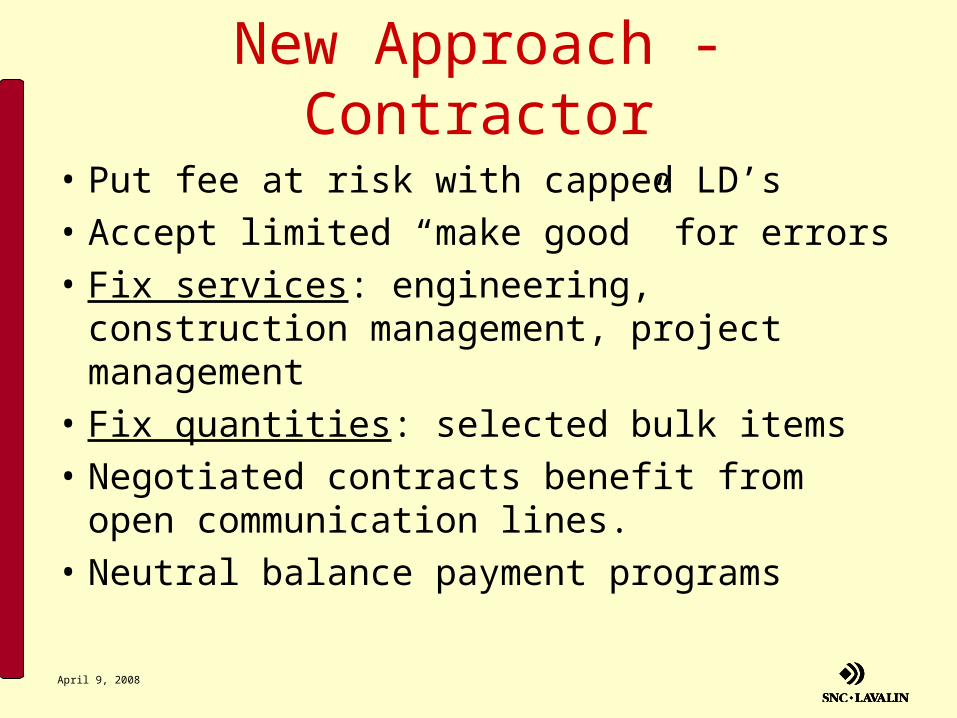

New Approach - Contractor

• Put fee at risk with capped LD’s

• Accept limited “make good” for errors

• Fix services: engineering, construction management, project management

• Fix quantities: selected bulk items

• Negotiated contracts benefit from open communication lines.

• Neutral balance payment programs

April 9, 2008

What does The Future Look Like?

April 9, 2008

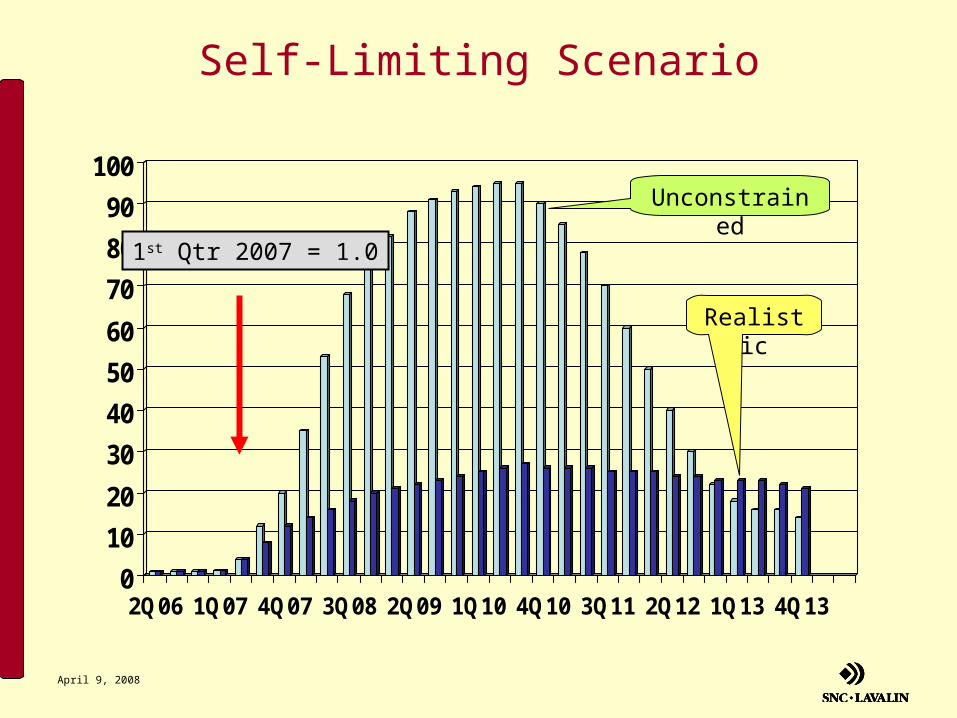

Self-Limiting Scenario

0

10

20

30

40

50

60

70

80

90

100

2Q06 1Q07 4Q07 3Q08 2Q09 1Q10 4Q10 3Q11 2Q12 1Q13 4Q13

Unconstrained

Realistic

1st Qtr 2007 = 1.0

April 9, 2008

Summary

• The capital project market is in turmoil

• Major capital projects can be financed w/ marginal projects deferred / cancelled

• Limited resource scenario is a 4-5 year self-limiting plateau vs. bubble

• Owner, contractor and lender relationships are changing

April 9, 2008

Thought of the Day

Intellect distinguishes between

the possible and impossible;

Reason distinguishes between sensible

and senseless.

Even the possible can be senseless.

Max Born

- AUTHOR UNKNOWN