apresentação do powerpoint · fibria delivers one of the highest ebitda/t and ... bekp net price...

TRANSCRIPT

Financial Highlights

Guilherme Cavalcanti - CFO

Focus on Investment Grade

Main Achievements

• US$ 1.4 billion debt reduction in twelve months

• Net debt/EBITDA ratio in US$ of 3.0x, the lowest level since Fibria’s creation

• Cost of debt in US$ reduced to 4.7% p.a. (Jun/12: 5.4% p.a)

• Free cash flow in the LTM totaled R$956 million, 7% FCF yield

• Working Capital Improvements

• Hedging Strategy

• All rating agencies at one notch below Investment Grade:

• Outlook upgrade by Fitch (Feb/2013) and Moody’s (Sep/2013)

• Rating upgrade from “BB/Positive” to “BB+/Stable” by S&P (Mar/2013)

• Selected as sector leader in Dow Jones Sustainability Indices

2

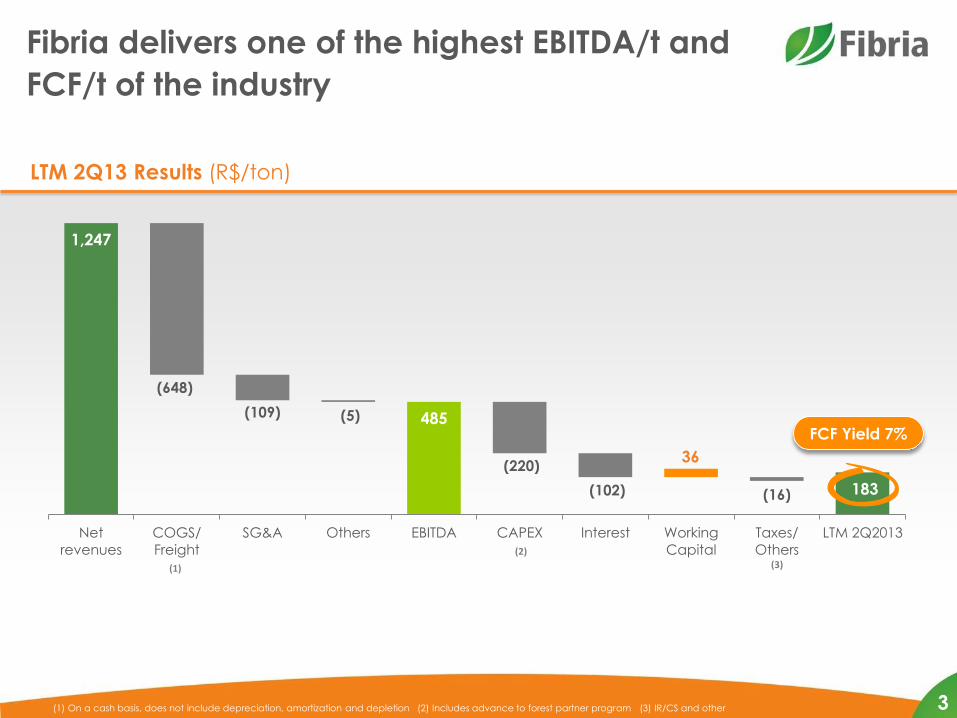

1,247

485

183

(648)

(109) (5)

(220)

(102)

36

(16)

Net

revenues

COGS/

Freight

SG&A Others EBITDA CAPEX Interest Working

Capital

Taxes/

Others

LTM 2Q2013

(1) On a cash basis, does not include depreciation, amortization and depletion (2) Includes advance to forest partner program (3) IR/CS and other

(2)

FCF Yield 7%

(1) (3)

LTM 2Q13 Results (R$/ton)

Fibria delivers one of the highest EBITDA/t and

FCF/t of the industry

3

Acknowledgements

4

Company of the year,

among all industries,

according to Valor

Econômico.

In the Pulp and Paper Sector:

1st place in Value Generation

1st place in Net Revenue

Valor 1000

XVII ANEFAC-FIPECAFI - SERASA

EXPERIAN Prize

Fibria is among the most

transparent public

companies (with revenue

of up to R$5 billions) in

Brazil; recognized for the

quality of its 2012

financial statements.

Fibria was ranked for the forth

consecutive year (2010, 2011,

2012 and 2013).

In 2013 Fibria was ranked in

four categories: CEO, CFO, IR

Team and IR Professional

2013 Institutional Investor Latam

Ranking - P&P Sector

Fibria was chosen by

RobecoSAM as one of the 10

Game Changers of tomorrow

among all the industries

worldwide analyzed at Dow

Jones Sustainability Index.

Fibria’s case was published in

the Sustainability Investing

Magazine.

Sustainability Investing

Fibria was elected by Época

Negócios 360º as 1st place in

the pulp & paper sector in the

corporate governance and future's vision categories.

Época Negócios 360º

Fibria is one of the 5

Brazilian companies

nominees to the Best

Corporate Governance

Award from London.

International Recognition by

Corporate Governance Report

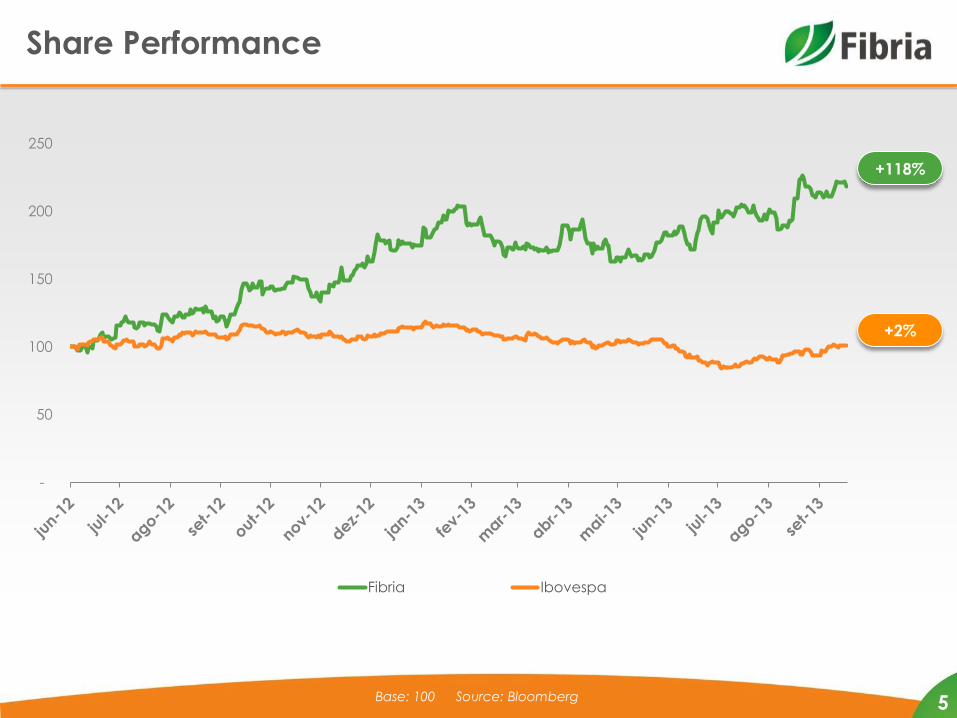

Share Performance

5

-

50

100

150

200

250

Fibria Ibovespa

Base: 100 Source: Bloomberg

+2%

+118%

MARKET PULP ENTERING A NEW AGE OF COMPETITION

2ND FIBRIA INVESTOR TOUR Três Lagoas, MS, October 2, 2013 João Cordeiro Pöyry Management Consulting

COPYRIGHT©PÖYRY

KEY QUESTIONS

02 OCT 2013

What has fundamentally changed in the

business of market pulp during the last

four decades ?

How to compete in the future given the

evolving dynamics of markets, clients

and competitors ?

How to innovate and create competitive

advantage while coping with rising

operating costs ?

FIBRIA INVESTOR TOUR 7

COPYRIGHT©PÖYRY

E-MEDIA KEVENNYS

02 OCT 2013 FIBRIA INVESTOR TOUR 8

COPYRIGHT©PÖYRY

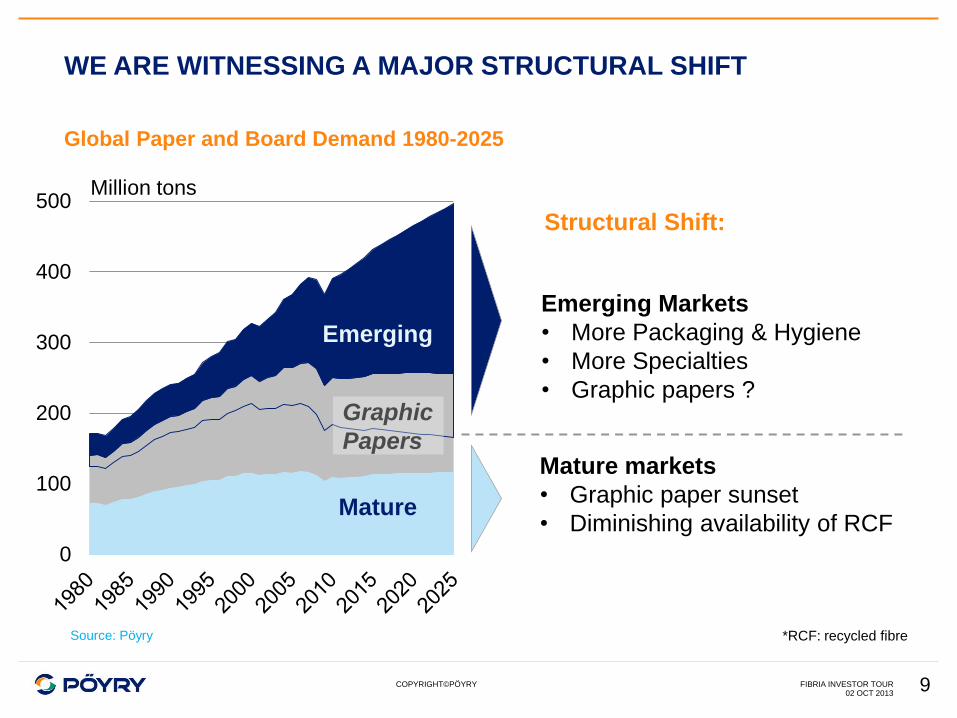

WE ARE WITNESSING A MAJOR STRUCTURAL SHIFT

0

100

200

300

400

500Million tons

Mature

Emerging

Structural Shift:

Mature markets

• Graphic paper sunset

• Diminishing availability of RCF

Emerging Markets

• More Packaging & Hygiene

• More Specialties

• Graphic papers ?

Global Paper and Board Demand 1980-2025

Graphic

Papers

*RCF: recycled fibre Source: Pöyry

02 OCT 2013 FIBRIA INVESTOR TOUR 9

COPYRIGHT©PÖYRY

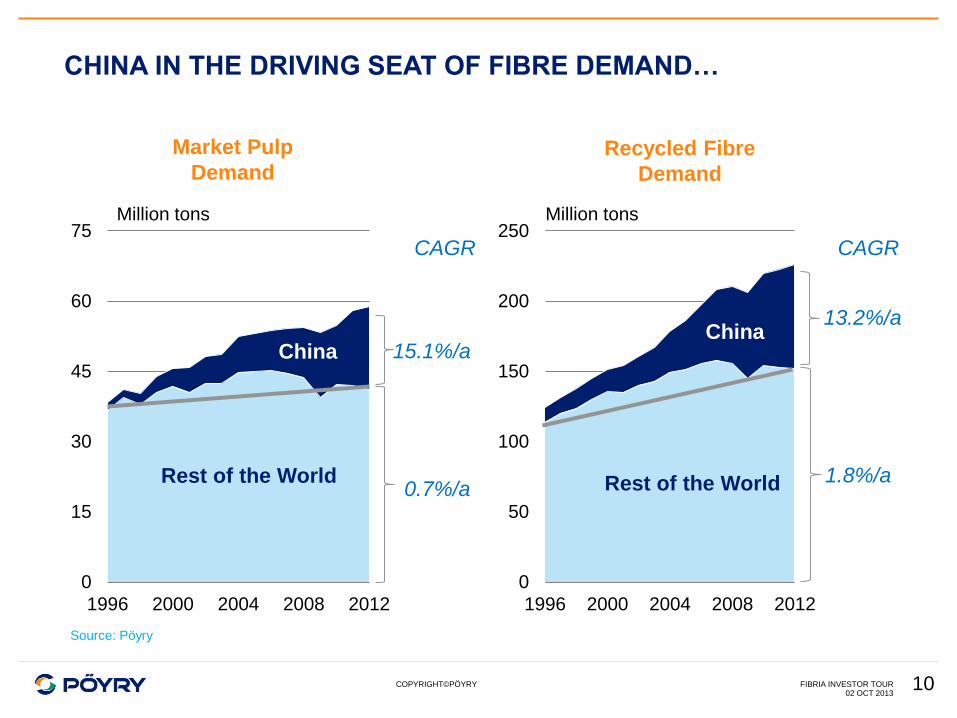

CHINA IN THE DRIVING SEAT OF FIBRE DEMAND…

0

50

100

150

200

250

1996 2000 2004 2008 2012

1.8%/a

13.2%/a China

0

15

30

45

60

75

1996 2000 2004 2008 2012

0.7%/a

15.1%/a

Recycled Fibre

Demand

China

Market Pulp

Demand

Rest of the World Rest of the World

CAGR CAGR

Million tons Million tons

Source: Pöyry

02 OCT 2013 FIBRIA INVESTOR TOUR 10

COPYRIGHT©PÖYRY

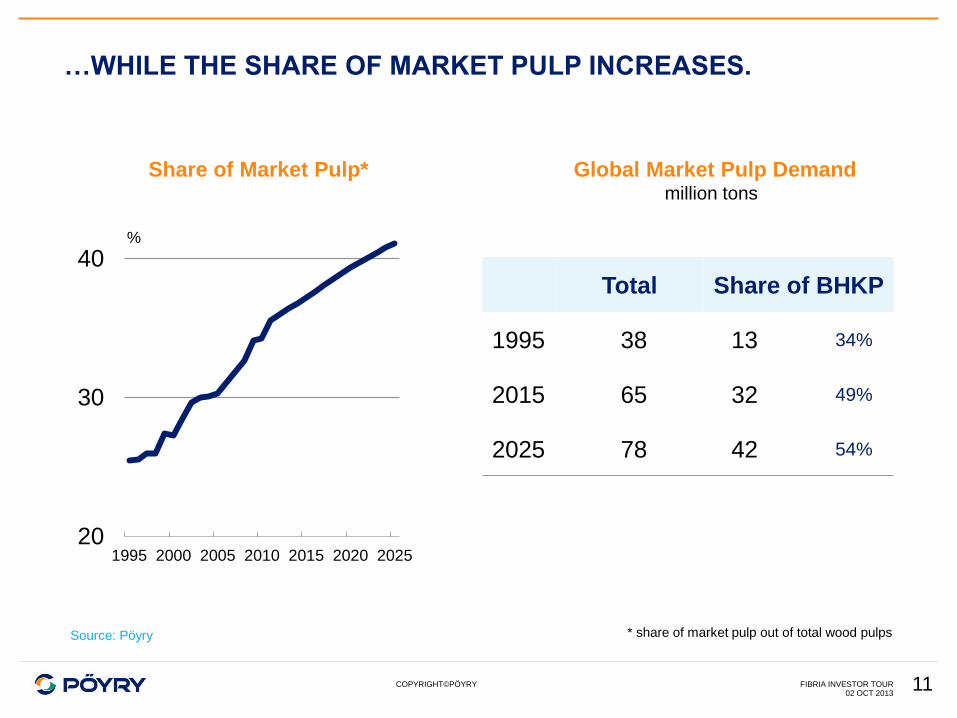

…WHILE THE SHARE OF MARKET PULP INCREASES.

02 OCT 2013 FIBRIA INVESTOR TOUR 11

20

30

40

1995 2000 2005 2010 2015 2020 2025

%

Share of Market Pulp*

* share of market pulp out of total wood pulps

Total Share of BHKP

1995 38 13 34%

2015 65 32 49%

2025 78 42 54%

Global Market Pulp Demand million tons

Source: Pöyry

COPYRIGHT©PÖYRY

WHAT HAVE BEEN THE MAIN CHANGES

IN MARKET PULP BUSINESS DURING THE LAST 40 YEARS

02 OCT 2013 FIBRIA INVESTOR TOUR

Wood

Quality & Cost

Technology and

Mill Size

and what is the future impact on Brazilian business ?

Louder

Client Voice

12

COPYRIGHT©PÖYRY

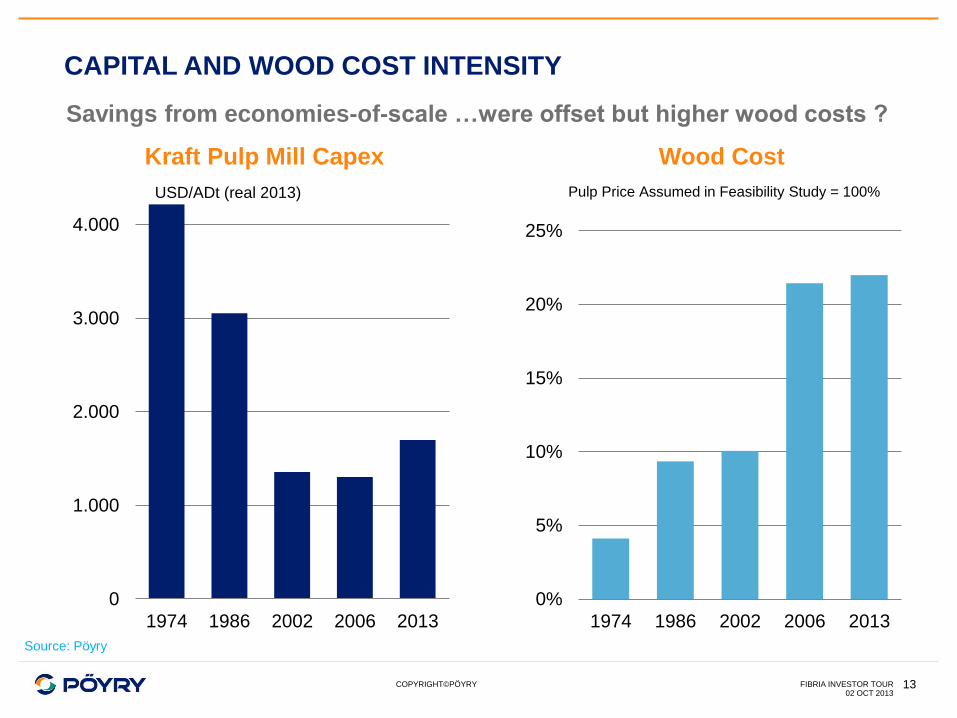

CAPITAL AND WOOD COST INTENSITY

02 OCT 2013 FIBRIA INVESTOR TOUR

Kraft Pulp Mill Capex Wood Cost

0%

5%

10%

15%

20%

25%

1974 1986 2002 2006 2013

Pulp Price Assumed in Feasibility Study = 100%

Savings from economies-of-scale …were offset but higher wood costs ?

Source: Pöyry

13

0

1.000

2.000

3.000

4.000

1974 1986 2002 2006 2013

USD/ADt (real 2013)

COPYRIGHT©PÖYRY

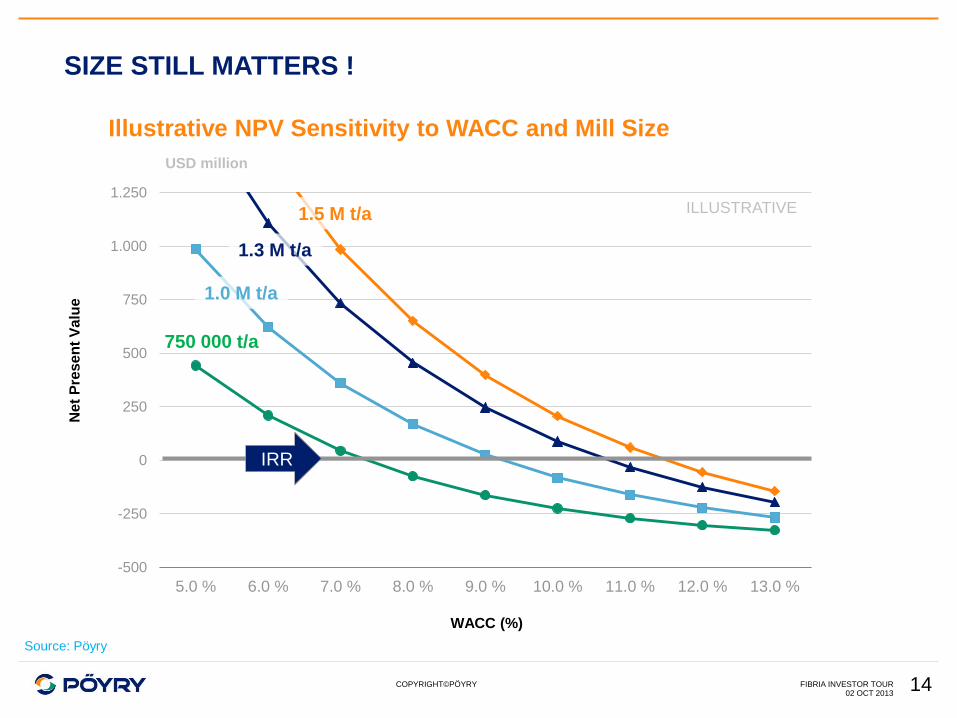

SIZE STILL MATTERS !

-500

-250

0

250

500

750

1.000

1.250

5.0 % 6.0 % 7.0 % 8.0 % 9.0 % 10.0 % 11.0 % 12.0 % 13.0 %

IRR

WACC (%)

Ne

t P

res

en

t V

alu

e

USD million

750 000 t/a

1.5 M t/a

1.3 M t/a

1.0 M t/a

ILLUSTRATIVE

02 OCT 2013 FIBRIA INVESTOR TOUR

Illustrative NPV Sensitivity to WACC and Mill Size

Source: Pöyry

14

COPYRIGHT©PÖYRY 02 OCT 2013

FIBRIA INVESTOR TOUR

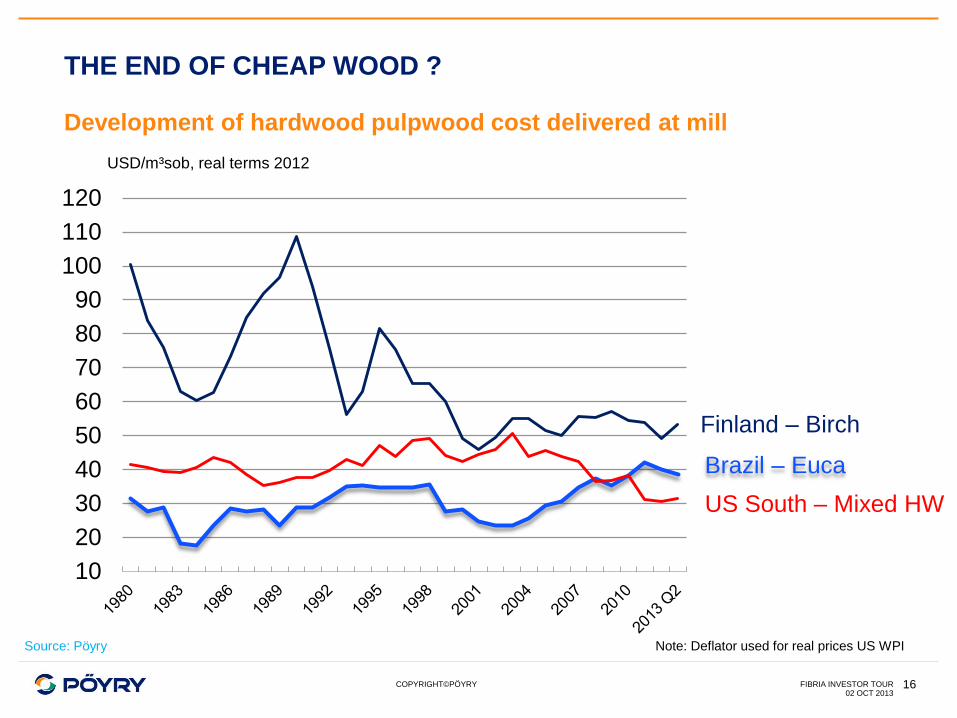

WHY WOOD COSTS ARE RISING ? 1979

15

COPYRIGHT©PÖYRY

10

20

30

40

50

60

70

80

90

100

110

120

02 OCT 2013 FIBRIA INVESTOR TOUR

THE END OF CHEAP WOOD ?

Development of hardwood pulpwood cost delivered at mill

USD/m³sob, real terms 2012

Source: Pöyry

16

Finland – Birch

Brazil – Euca

US South – Mixed HW

Note: Deflator used for real prices US WPI

COPYRIGHT©PÖYRY

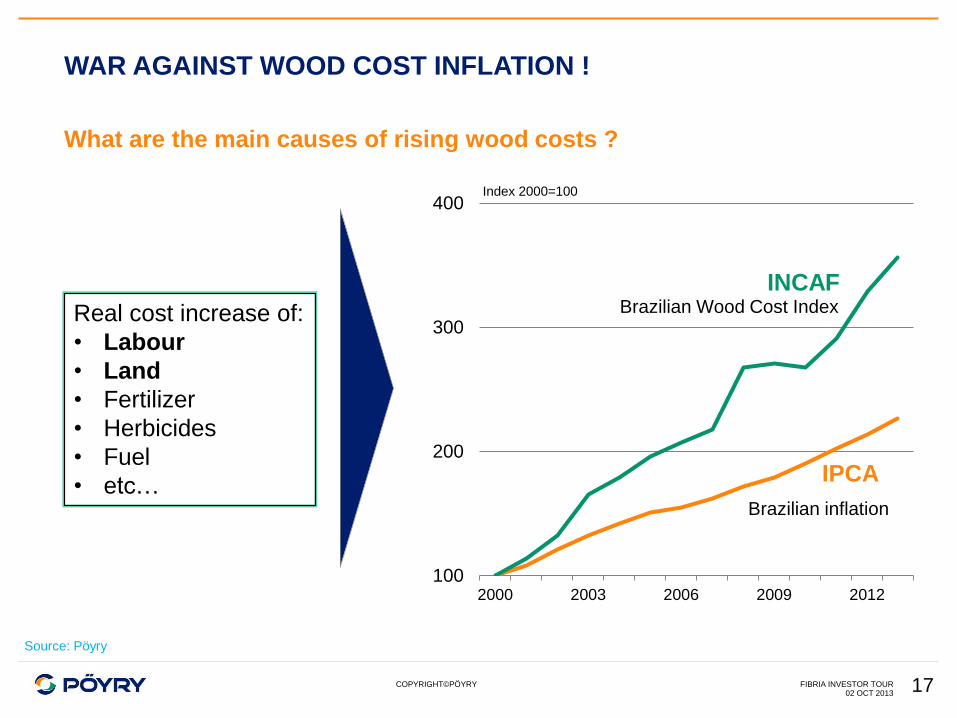

WAR AGAINST WOOD COST INFLATION !

02 OCT 2013 FIBRIA INVESTOR TOUR

Real cost increase of:

• Labour

• Land

• Fertilizer

• Herbicides

• Fuel

• etc…

What are the main causes of rising wood costs ?

Index 2000=100

100

200

300

400

2000 2003 2006 2009 2012

INCAF

IPCA

Brazilian Wood Cost Index

Brazilian inflation

Source: Pöyry

17

COPYRIGHT©PÖYRY

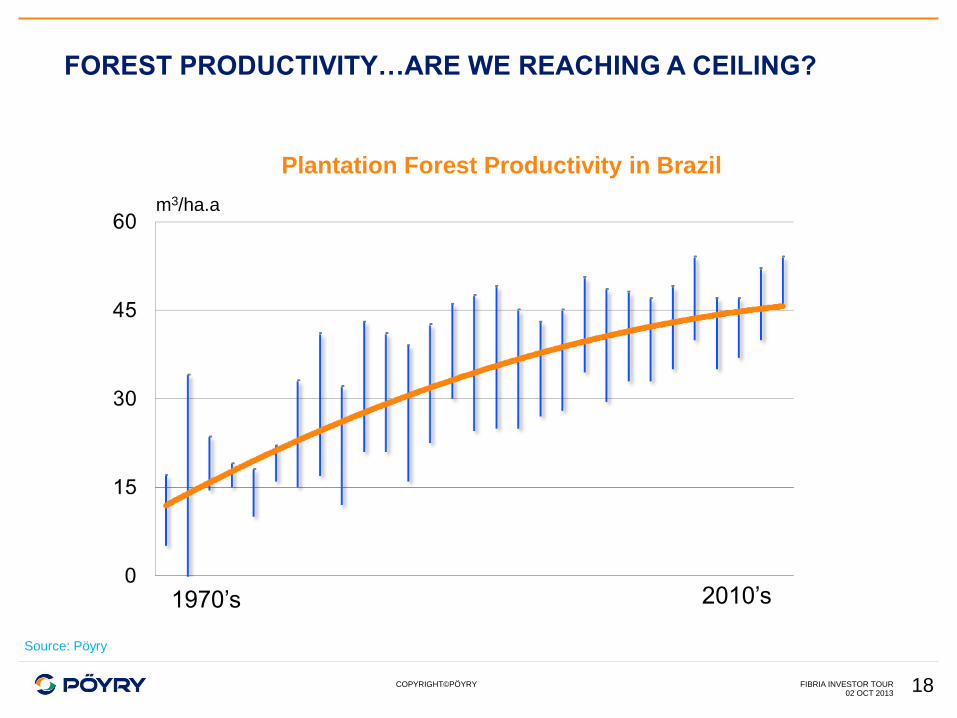

FOREST PRODUCTIVITY…ARE WE REACHING A CEILING?

02 OCT 2013 FIBRIA INVESTOR TOUR

1970’s 2010’s

m3/ha.a

Plantation Forest Productivity in Brazil

Source: Pöyry

18

COPYRIGHT©PÖYRY

GENETICS

KEY ASSET FOR FUTURE DIFFERENTIATION

02 OCT 2013 FIBRIA INVESTOR TOUR 19

COPYRIGHT©PÖYRY 02 OCT 2013

FIBRIA INVESTOR TOUR 20

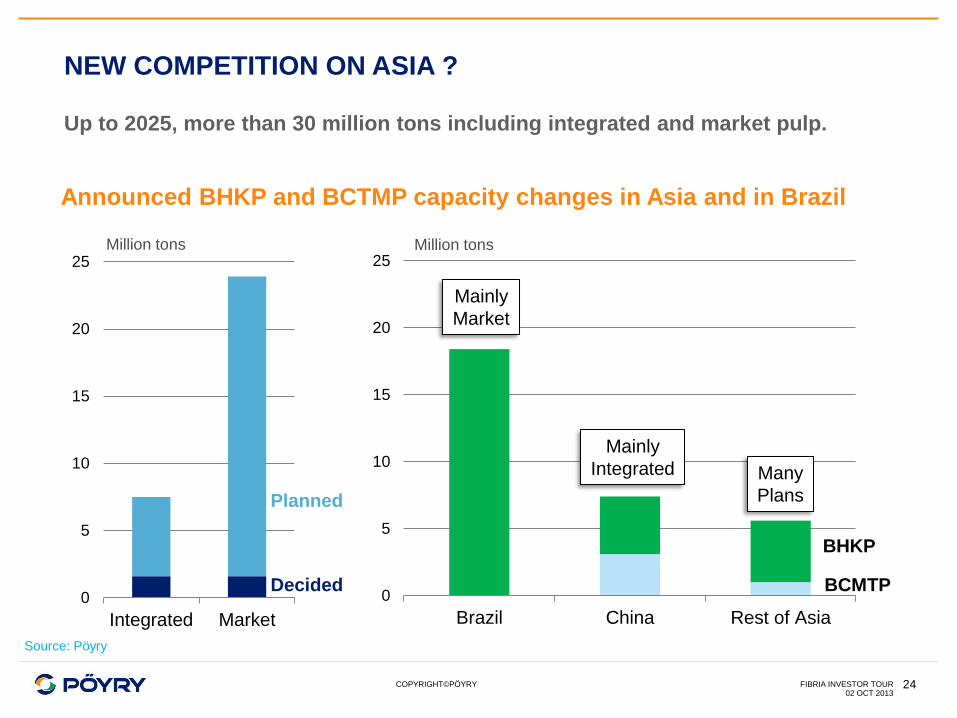

NEW COMPETITION ON ASIA?

COPYRIGHT©PÖYRY

0

200

400

600

800

1 000

1 200

1 400

1 600

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34

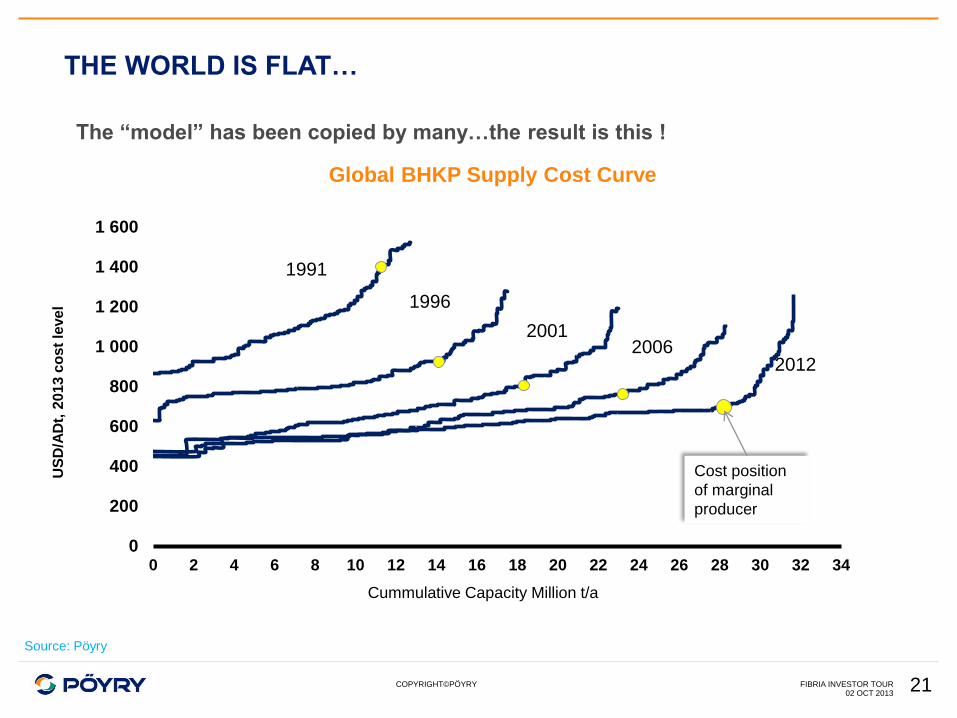

THE WORLD IS FLAT…

Global BHKP Supply Cost Curve

Cummulative Capacity Million t/a

1991

1996

2001 2006

2012

Cost position

of marginal

producer

The “model” has been copied by many…the result is this !

Source: Pöyry

02 OCT 2013 FIBRIA INVESTOR TOUR 21

US

D/A

Dt,

201

3 c

os

t le

ve

l

COPYRIGHT©PÖYRY

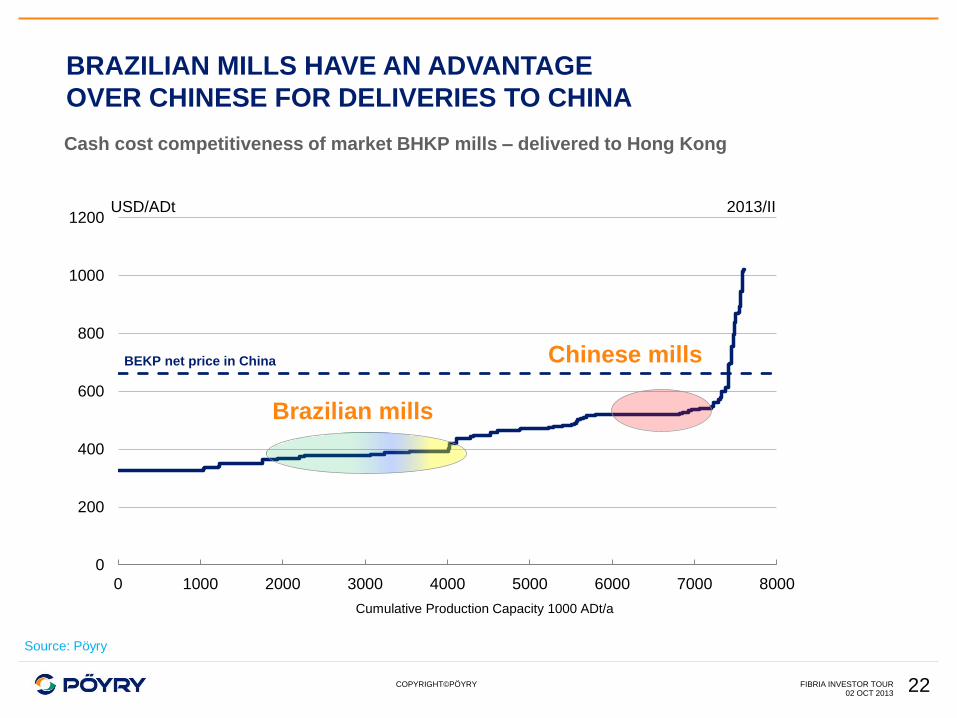

BRAZILIAN MILLS HAVE AN ADVANTAGE

OVER CHINESE FOR DELIVERIES TO CHINA

Cash cost competitiveness of market BHKP mills – delivered to Hong Kong

02 OCT 2013 FIBRIA INVESTOR TOUR

0

200

400

600

800

1000

1200

0 1000 2000 3000 4000 5000 6000 7000 8000

USD/ADt 2013/II

BEKP net price in China

Cumulative Production Capacity 1000 ADt/a

Brazilian mills

Chinese mills

Source: Pöyry

22

COPYRIGHT©PÖYRY

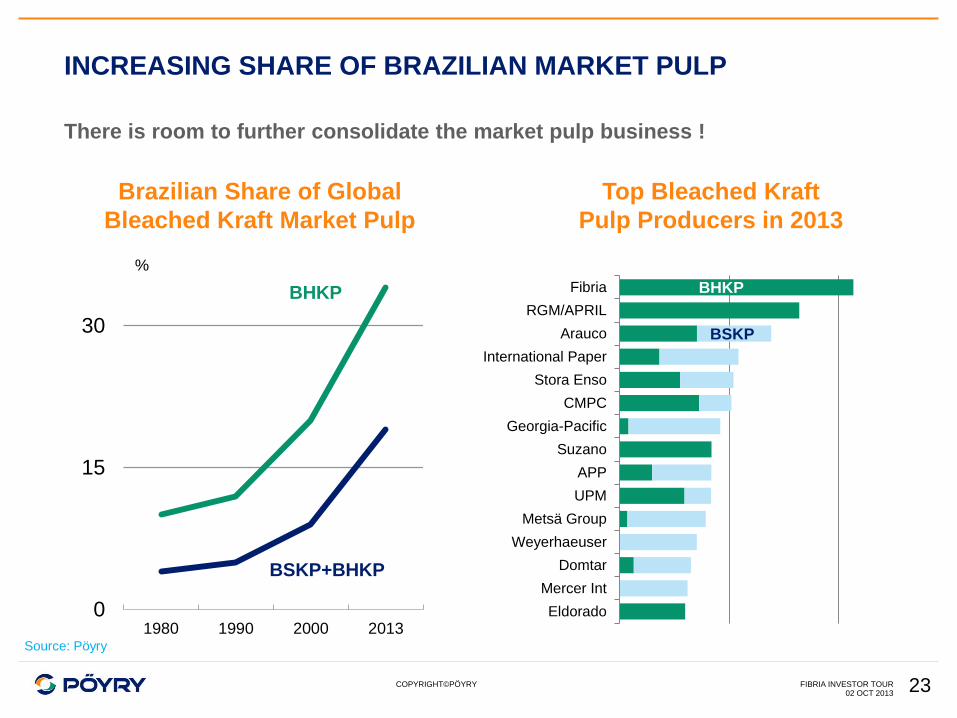

INCREASING SHARE OF BRAZILIAN MARKET PULP

02 OCT 2013 FIBRIA INVESTOR TOUR

There is room to further consolidate the market pulp business !

Eldorado

Mercer Int

Domtar

Weyerhaeuser

Metsä Group

UPM

APP

Suzano

Georgia-Pacific

CMPC

Stora Enso

International Paper

Arauco

RGM/APRIL

Fibria

Top Bleached Kraft

Pulp Producers in 2013

Brazilian Share of Global

Bleached Kraft Market Pulp

0

15

30

1980 1990 2000 2013

%

BHKP

BSKP+BHKP

BHKP

BSKP

Source: Pöyry

23

COPYRIGHT©PÖYRY

NEW COMPETITION ON ASIA ?

02 OCT 2013 FIBRIA INVESTOR TOUR

0

5

10

15

20

25

Integrated Market

Up to 2025, more than 30 million tons including integrated and market pulp.

0

5

10

15

20

25

Brazil China Rest of Asia

BHKP

BCMTP

Planned

Decided

Million tons Million tons

Mainly

Market

Mainly

Integrated Many

Plans

Source: Pöyry

Announced BHKP and BCTMP capacity changes in Asia and in Brazil

24

COPYRIGHT©PÖYRY

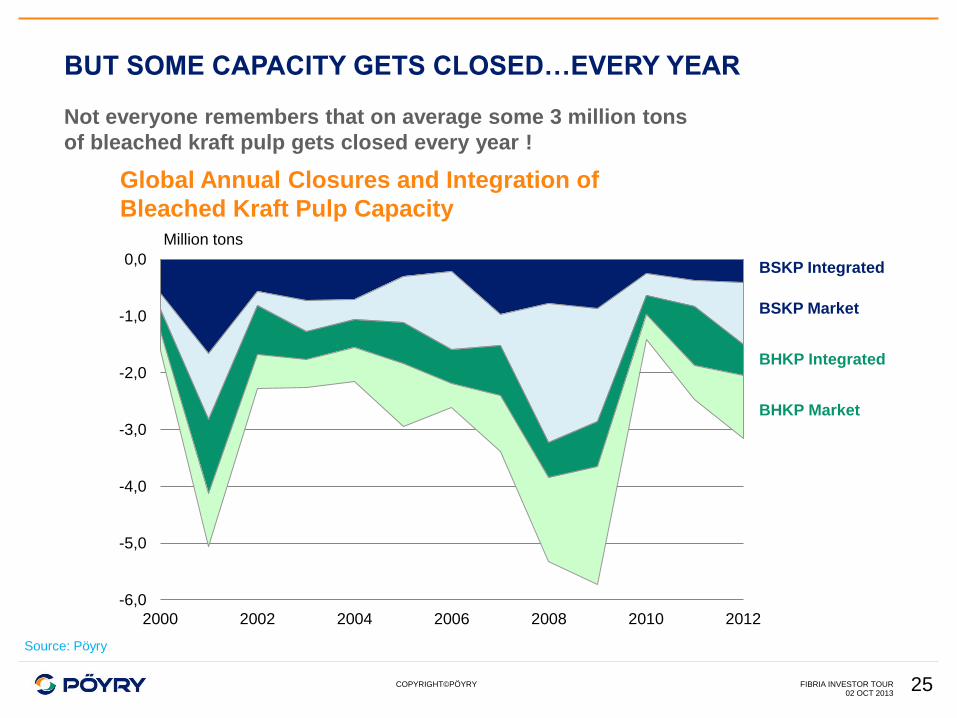

BUT SOME CAPACITY GETS CLOSED…EVERY YEAR

FIBRIA INVESTOR TOUR

Not everyone remembers that on average some 3 million tons

of bleached kraft pulp gets closed every year !

-6,0

-5,0

-4,0

-3,0

-2,0

-1,0

0,0

2000 2002 2004 2006 2008 2010 2012

Million tons

02 OCT 2013

Global Annual Closures and Integration of

Bleached Kraft Pulp Capacity

Source: Pöyry

BHKP Market

BHKP Integrated

BSKP Market

BSKP Integrated

25

COPYRIGHT©PÖYRY

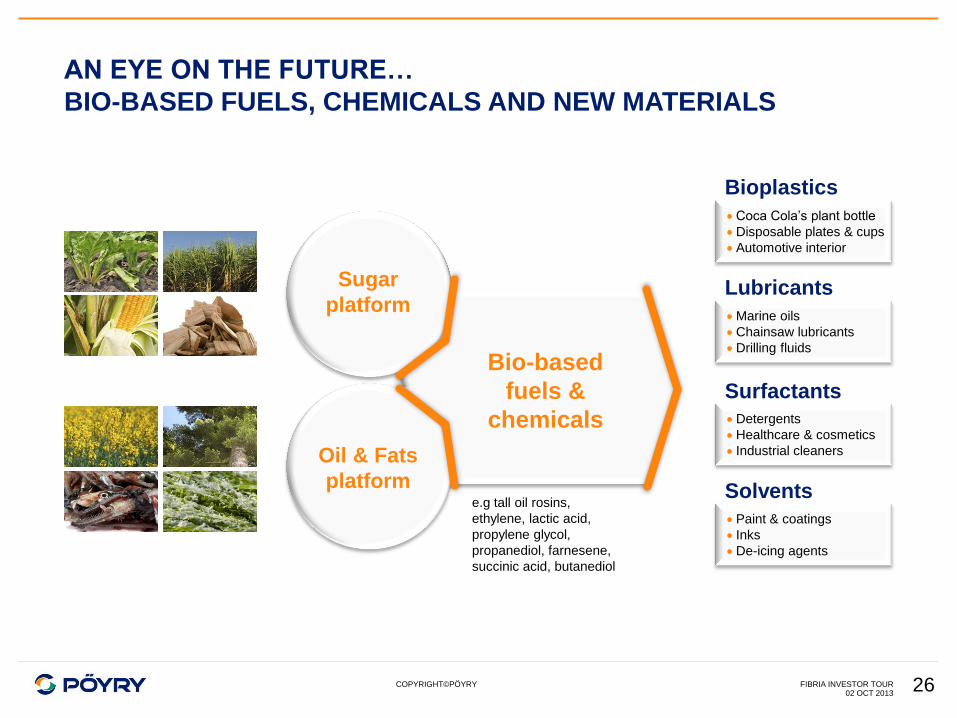

AN EYE ON THE FUTURE…

BIO-BASED FUELS, CHEMICALS AND NEW MATERIALS

02 OCT 2013 FIBRIA INVESTOR TOUR 26

Sugar

platform

Oil & Fats

platform

Bioplastics

Surfactants

Lubricants

Solvents

Bio-based

fuels &

chemicals

Coca Cola’s plant bottle

Disposable plates & cups

Automotive interior

Detergents

Healthcare & cosmetics

Industrial cleaners

Marine oils

Chainsaw lubricants

Drilling fluids

Paint & coatings

Inks

De-icing agents

e.g tall oil rosins,

ethylene, lactic acid,

propylene glycol,

propanediol, farnesene,

succinic acid, butanediol

COPYRIGHT©PÖYRY

ENTERING A NEW AGE OF COMPETITION

02 OCT 2013 FIBRIA INVESTOR TOUR

Are we ready to

reinvent our

Industry?

• Mill sizes will continue to increase.

• Declared war on wood cost inflation.

• Facing emerging competition from within

Brazil and from South East Asia.

• More differentiation and innovation

through intensive R&D from forest to product.

• Develop “Fit-for-client” product and

service portfolio in order to differentiate

• Taking an active role on consolidation while

bringing investment discipline to the industry.

27

COPYRIGHT©PÖYRY 28 02 OCT 2013

FIBRIA INVESTOR TOUR

Questions ?

Mr. João Cordeiro

“It is not the strongest of the species that survives, nor the most

intelligent, but the one most responsive to change.”

― Charles Darwin

Competitive Strategy

Marcelo Castelli - CEO

Since its creation, Fibria’s strategy has been

executed based on:

30

OPERATING EXCELLENCE LIABILITY MANAGEMENT GROWTH WITH DISCIPLINE

• Cost control

• Efficiency projects aiming at

reducing Fibria’s cash cost:

− Jacareí Energy Master

Plan

− Aracruz Revit “A“

• Operating stability

• Capex discipline

• Liquidity events

• Gross debt reduction

• Cost of debt reduction

• Leverage reduction

• Ready for organic growth

(licenses and basic

engineering)

• Continuous investment in

forest for capacity growth

• Industrial project at the rigor

moment for value creation

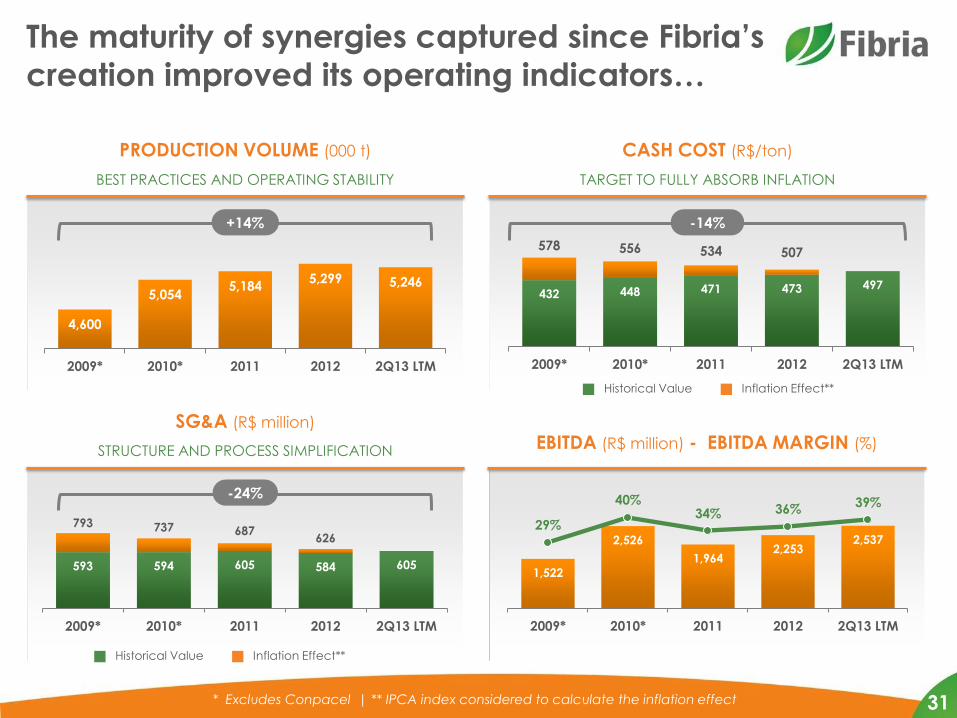

STRUCTURE AND PROCESS SIMPLIFICATION

SG&A (R$ million)

EBITDA (R$ million) - EBITDA MARGIN (%)

TARGET TO FULLY ABSORB INFLATION

CASH COST (R$/ton)

BEST PRACTICES AND OPERATING STABILITY

PRODUCTION VOLUME (000 t)

The maturity of synergies captured since Fibria’s

creation improved its operating indicators…

31

Historical Value Inflation Effect**

* Excludes Conpacel | ** IPCA index considered to calculate the inflation effect

4,600

5,054 5,184

5,299 5,246

2009* 2010* 2011 2012 2Q13 LTM

432 448 471 473 497

578 556 534 507

2009* 2010* 2011 2012 2Q13 LTM

+14% -14%

Historical Value Inflation Effect**

-24%

593 594 605 584 605

793 737 687 626

2009* 2010* 2011 2012 2Q13 LTM

1,522

2,526

1,964 2,253

2,537 29%

40% 34% 36%

39%

2009* 2010* 2011 2012 2Q13 LTM

* From June 30, 2012 on, net debt/EBITDA ratio for covenant purposes are calculated in US Dollars and the limit is 4.5x ** 2013 year end market consensus

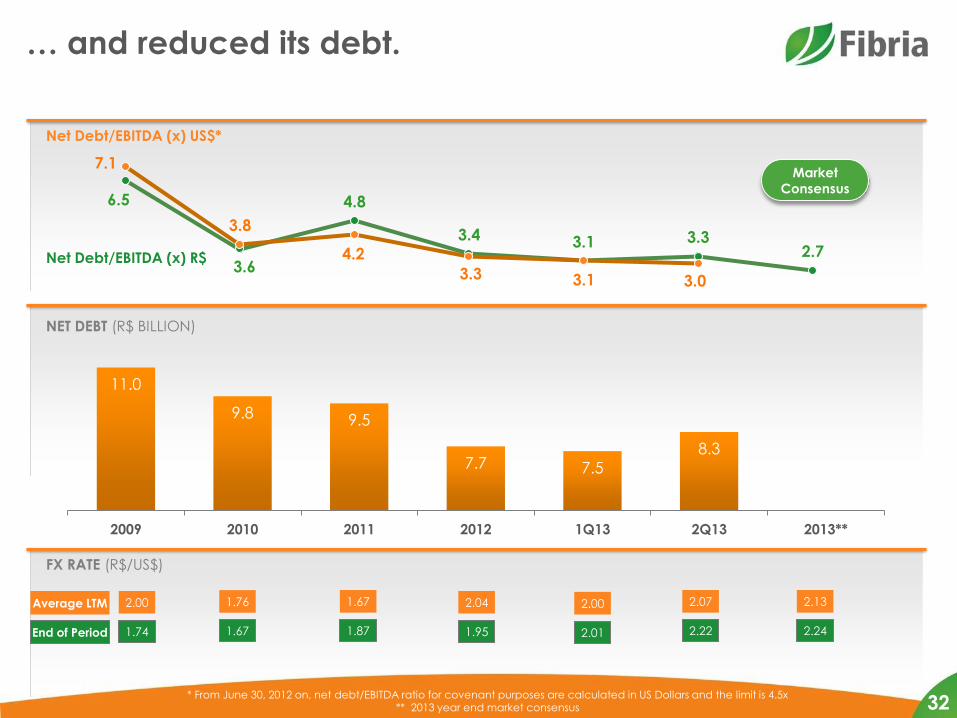

… and reduced its debt.

6.5

3.6

4.8

3.4 3.1 3.3 2.7

7.1

3.8

4.2

3.3 3.1 3.0

Net Debt/EBITDA (x) R$

Net Debt/EBITDA (x) US$*

Market

Consensus

11.0

9.8 9.5

7.7 7.5

8.3

2009 2010 2011 2012 1Q13 2Q13 2013**

NET DEBT (R$ BILLION)

FX RATE (R$/US$)

1.67

1.76

1.74

2.00 Average LTM

End of Period 1.87

1.67

1.95

2.04

2.01

2.00

2.22

2.07

32

2.24

2.13

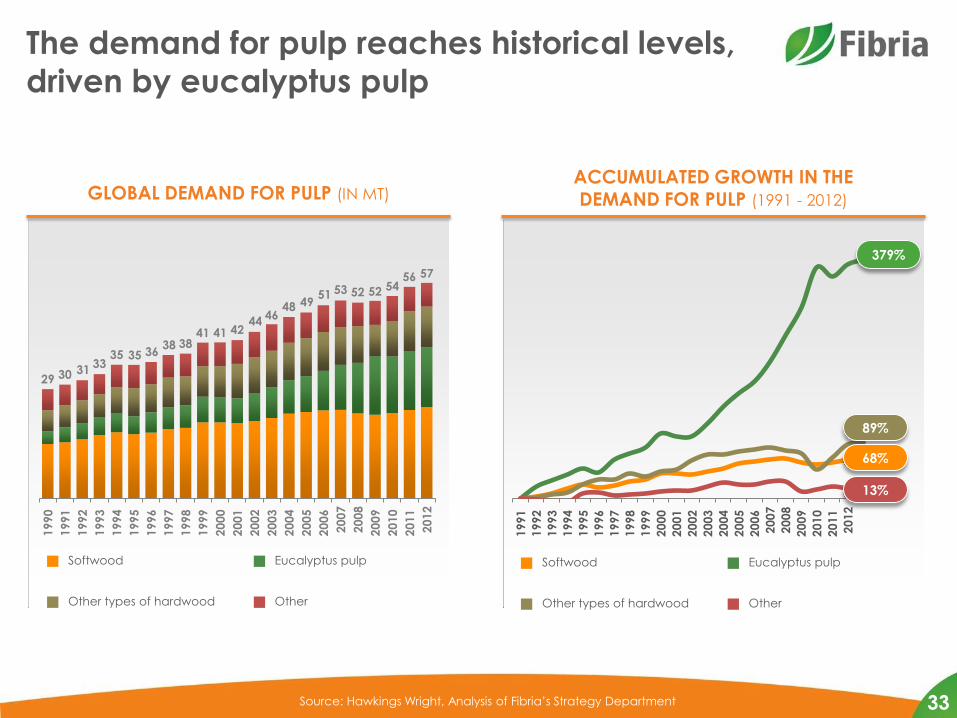

The demand for pulp reaches historical levels,

driven by eucalyptus pulp

33

GLOBAL DEMAND FOR PULP (IN MT) ACCUMULATED GROWTH IN THE DEMAND FOR PULP (1991 - 2012)

29 30 31 33

35 35 36 38 38

41 41 42 44

46 48 49

51 53 52 52 54 56 57

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Softwood Eucalyptus pulp

Other types of hardwood Other

68%

89%

13%

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Softwood Eucalyptus pulp

Other types of hardwood Other

Source: Hawkings Wright, Analysis of Fibria’s Strategy Department

379%

89%

68%

13%

Source: RISI, LCA, Analysis of Fibria’s Strategy Department

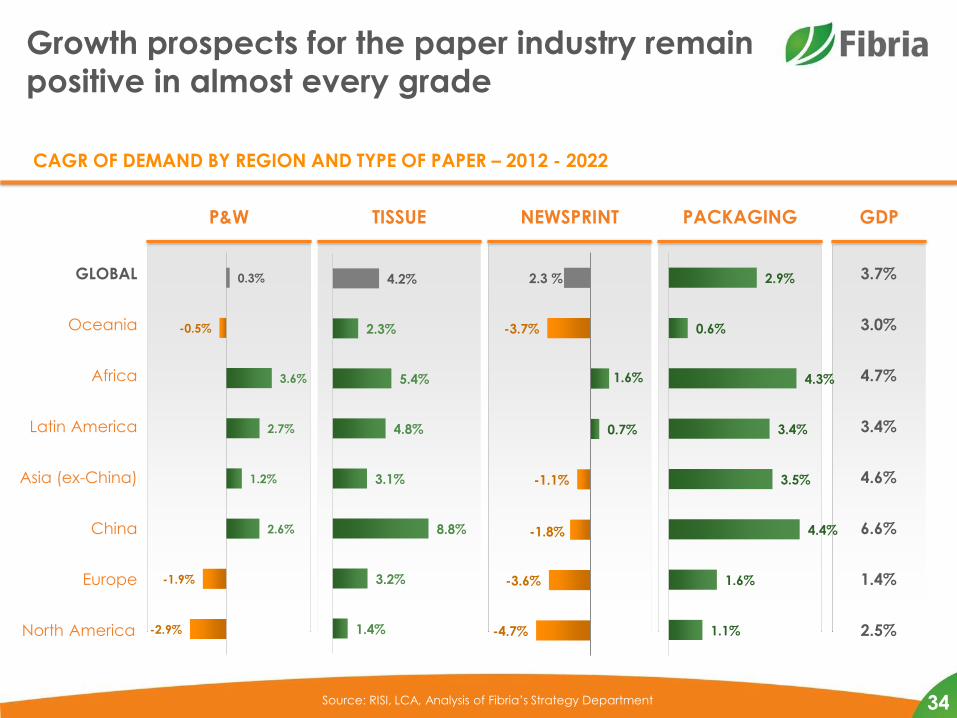

Growth prospects for the paper industry remain

positive in almost every grade

GDP TISSUE NEWSPRINT PACKAGING P&W

GLOBAL

Oceania

Africa

Latin America

Asia (ex-China)

China

Europe

North America -2.9%

-1.9%

2.6%

1.2%

2.7%

3.6%

-0.5%

0.3%

1.4%

3.2%

8.8%

3.1%

4.8%

5.4%

2.3%

4.2%

-4.7%

-3.6%

-1.8%

-1.1%

0.7%

1.6%

-3.7%

2.3 %

1.1%

1.6%

4.4%

3.5%

3.4%

4.3%

0.6%

2.9% 3.7%

4.7%

6.6%

4.6%

1.4%

3.4%

3.0%

2.5%

CAGR OF DEMAND BY REGION AND TYPE OF PAPER – 2012 - 2022

34

While the demand is not a problem, the industry

scenario is challenging

• Fragmented industry with lack of discipline in launching of new projects

• Scale of new projects keeps growing

• Flattish industry cost curve

35

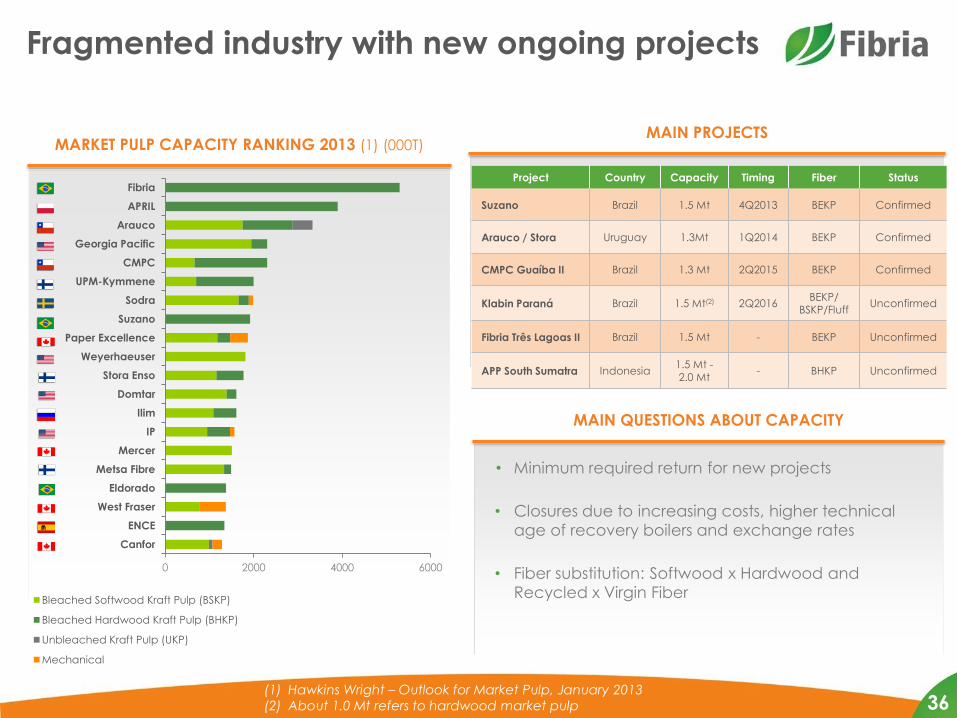

Fragmented industry with new ongoing projects

36

MARKET PULP CAPACITY RANKING 2013 (1) (000T) MAIN PROJECTS

0 2000 4000 6000

Canfor

ENCE

West Fraser

Eldorado

Metsa Fibre

Mercer

IP

Ilim

Domtar

Stora Enso

Weyerhaeuser

Paper Excellence

Suzano

Sodra

UPM-Kymmene

CMPC

Georgia Pacific

Arauco

APRIL

Fibria

Bleached Softwood Kraft Pulp (BSKP)

Bleached Hardwood Kraft Pulp (BHKP)

Unbleached Kraft Pulp (UKP)

Mechanical

Project Country Capacity Timing Fiber Status

Suzano Brazil 1.5 Mt 4Q2013 BEKP Confirmed

Arauco / Stora Uruguay 1.3Mt 1Q2014 BEKP Confirmed

CMPC Guaíba II Brazil 1.3 Mt 2Q2015 BEKP Confirmed

Klabin Paraná Brazil 1.5 Mt(2) 2Q2016 BEKP/

BSKP/Fluff Unconfirmed

Fibria Três Lagoas II Brazil 1.5 Mt - BEKP Unconfirmed

APP South Sumatra Indonesia 1.5 Mt -2.0 Mt

- BHKP Unconfirmed

MAIN QUESTIONS ABOUT CAPACITY

• Minimum required return for new projects

• Closures due to increasing costs, higher technical

age of recovery boilers and exchange rates

• Fiber substitution: Softwood x Hardwood and

Recycled x Virgin Fiber

(1) Hawkins Wright – Outlook for Market Pulp, January 2013

(2) About 1.0 Mt refers to hardwood market pulp

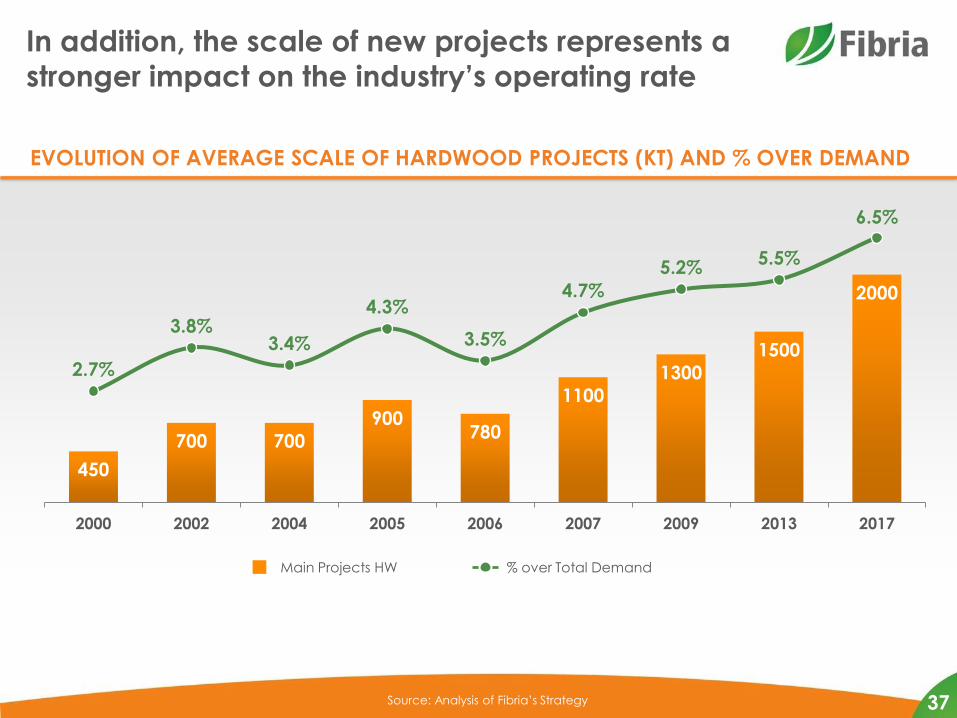

450

700 700

900 780

1100

1300

1500

2000

2.7%

3.8% 3.4%

4.3%

3.5%

4.7%

5.2% 5.5%

6.5%

2000 2002 2004 2005 2006 2007 2009 2013 2017

In addition, the scale of new projects represents a

stronger impact on the industry’s operating rate

37 Source: Analysis of Fibria’s Strategy

EVOLUTION OF AVERAGE SCALE OF HARDWOOD PROJECTS (KT) AND % OVER DEMAND

Main Projects HW % over Total Demand

Given the scenario, Fibria is diversifying its sources

of value creation.

• Drivers of continuous improvement and innovation

– Continuous search for operating excellence and cost control initiatives

– Forestry biotechnology

– Development of customized products - “fit for client”

– Actions to reduce employed capital

• Growth initiatives

• Complementary actions in the Value Chain

38

Fibria´s operational strategies to

competitiveness and growth

Incremental

Innovations Technologically

Advanced

Workforce

Control of

Internal

Inflation

Stability for Cost and Productivity

Performance

Specific

Projects for Cost Reduction

39

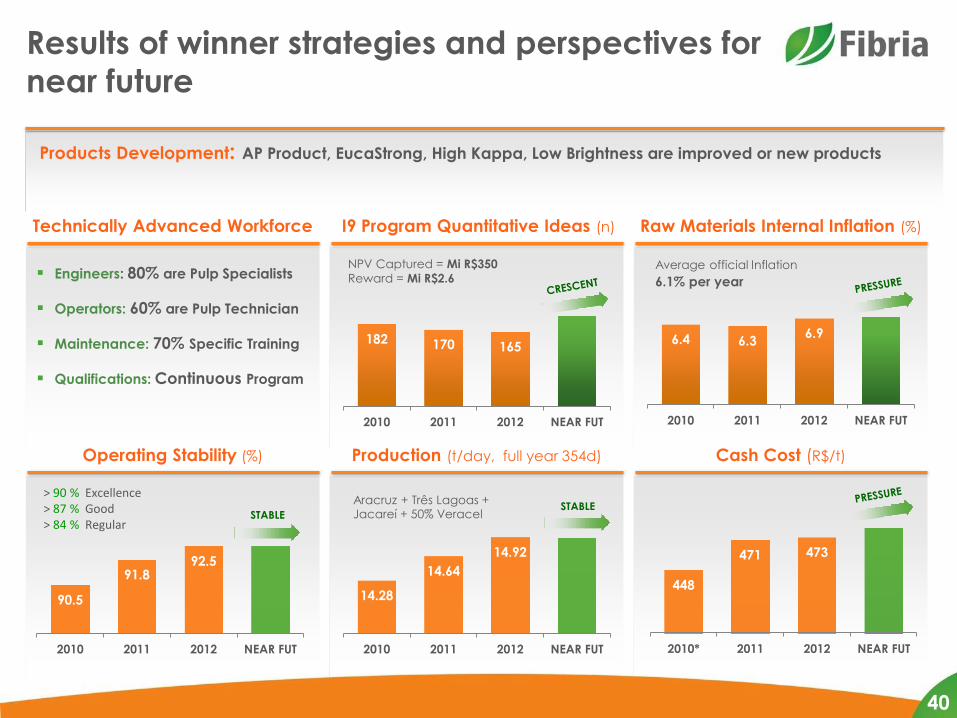

Results of winner strategies and perspectives for

near future

Technically Advanced Workforce I9 Program Quantitative Ideas (n) Raw Materials Internal Inflation (%)

Operating Stability (%) Production (t/day, full year 354d) Cash Cost (R$/t)

90.5

91.8 92.5

2010 2011 2012 NEAR FUT

14.28

14.64

14.92

2010 2011 2012 NEAR FUT

6.4 6.3 6.9

2010 2011 2012 NEAR FUT

448

471 473

2010* 2011 2012 NEAR FUT

182 170 165

2010 2011 2012 NEAR FUT

STABLE STABLE

NPV Captured = Mi R$350

Reward = Mi R$2.6 Engineers: 80% are Pulp Specialists

Operators: 60% are Pulp Technician

Maintenance: 70% Specific Training

Qualifications: Continuous Program

Products Development: AP Product, EucaStrong, High Kappa, Low Brightness are improved or new products

Aracruz + Três Lagoas + Jacareí + 50% Veracel

Average official Inflation

6.1% per year

> 90 % Excellence > 87 % Good > 84 % Regular

40

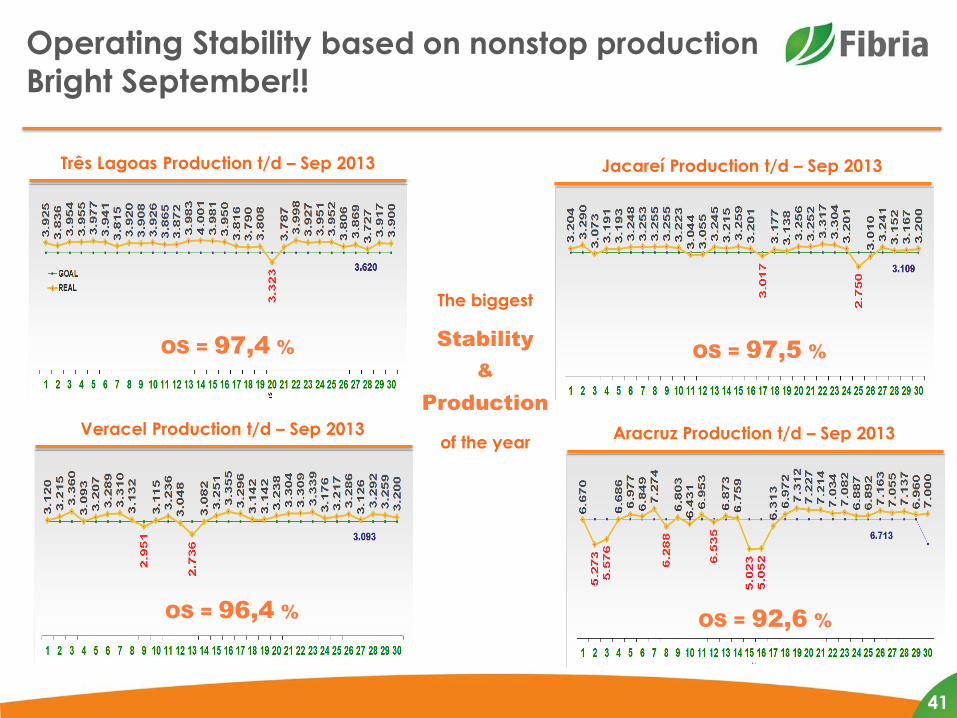

Jacareí Production t/d – Sep 2013

Operating Stability based on nonstop production

Bright September!!

Três Lagoas Production t/d – Sep 2013

41

Veracel Production t/d – Sep 2013 Aracruz Production t/d – Sep 2013

OS = 97,4 % OS = 97,5 %

OS = 96,4 % OS = 92,6 %

The biggest

Stability

&

Production

of the year

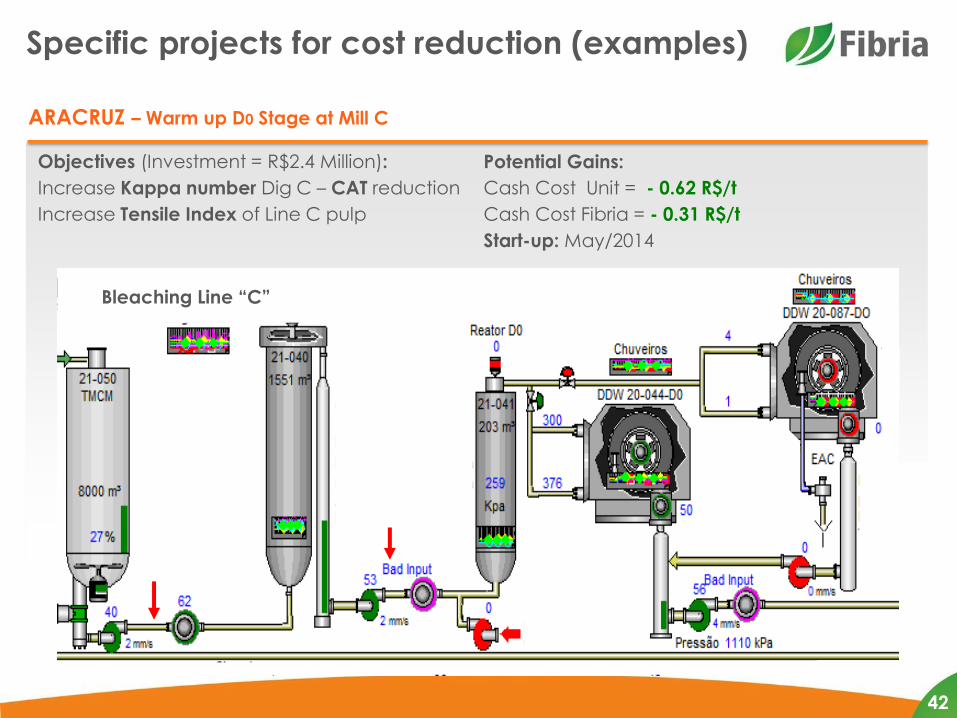

ARACRUZ – Warm up D0 Stage at Mill C

Specific projects for cost reduction (examples)

Objectives (Investment = R$2.4 Million):

Increase Kappa number Dig C – CAT reduction

Increase Tensile Index of Line C pulp

42

Potential Gains:

Cash Cost Unit = - 0.62 R$/t

Cash Cost Fibria = - 0.31 R$/t

Start-up: May/2014

Bleaching Line “C”

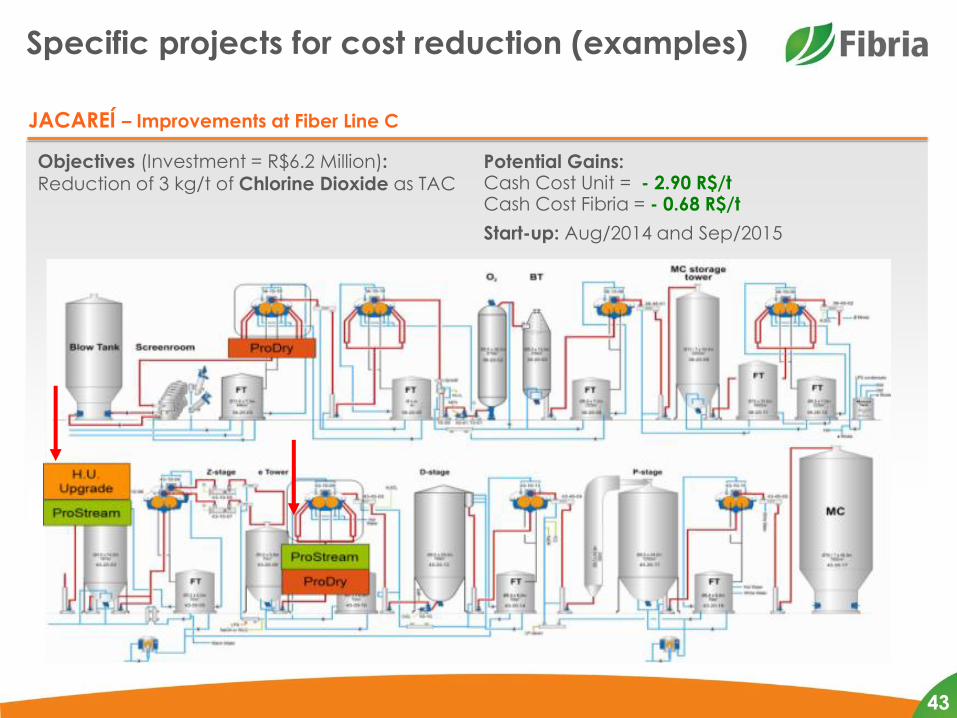

Specific projects for cost reduction (examples)

JACAREÍ – Improvements at Fiber Line C

Objectives (Investment = R$6.2 Million): Reduction of 3 kg/t of Chlorine Dioxide as TAC

43

Potential Gains: Cash Cost Unit = - 2.90 R$/t Cash Cost Fibria = - 0.68 R$/t

Start-up: Aug/2014 and Sep/2015

Specific projects for cost reduction (examples)

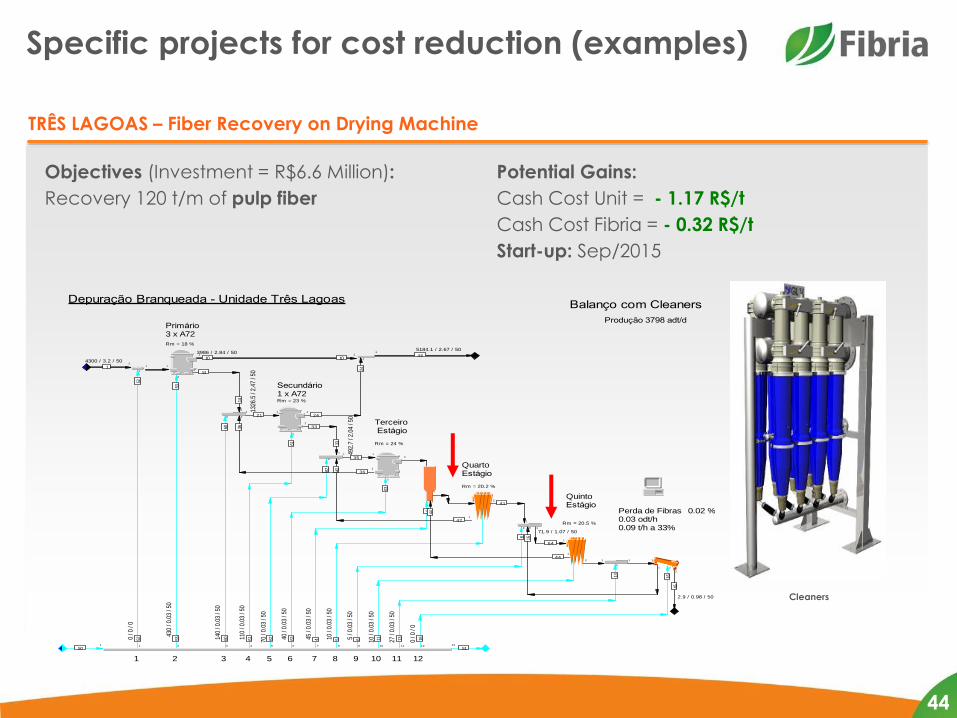

TRÊS LAGOAS – Fiber Recovery on Drying Machine

Objectives (Investment = R$6.6 Million):

Recovery 120 t/m of pulp fiber

Cleaners

1 1

2

2

53

5

3

430

/ 0.0

3 / 5

0

2

14

1

14

1 1

10 10

3986 / 2.84 / 50

1

50 13

51 12

16

2

16

0 / 0

/ 0

11

13

2

13

27 /

0.03

/ 50

10

11

2

10 /

0.03

/ 50

9

6

2

6

5 / 0

.03

/ 50

8

5

2

10 /

0.03

/ 50

7

4

2

4

45 /

0.03

/ 50

6

63

2

63

40 /

0.03

/ 50

5

62

3

62

70 /

0.03

/ 50

4

61

2

61

110

/ 0.0

3 / 5

0

3

3

60

6

0

140

/ 0.0

3 / 5

0

1

1

52

5

2

0 / 0

/ 0

1

42

2

42

2

33

1

33

1 1

35

492.

7 / 2

.04

/ 50

1

36

2

36

1 1

21

1326

.5 /

2.47

/ 50

1

24

2

24

1

46

5184.1 / 2.67 / 50

1

44

3

44

2

1

1

2 1 1 1

1

1

64

71.9 / 1.07 / 50

2

41

1

1

3 1

5

2

45

2.9 / 0.98 / 50

2

1

4300 / 3.2 / 50

12111098

Produção 3798 adt/d

0.02 %Perda de Fibras0.03 odt/h0.09 t/h a 33%

Rm = 20.5 %

Rm = 20.2 %

Rm = 24 %

Rm = 18 %

Rm = 23 %

7654321

Balanço com CleanersDepuração Branqueada - Unidade Três Lagoas

QuintoEstágio

QuartoEstágio

Terceiro Estágio

Secundário1 x A72

Primário3 x A72

44

Potential Gains:

Cash Cost Unit = - 1.17 R$/t

Cash Cost Fibria = - 0.32 R$/t

Start-up: Sep/2015

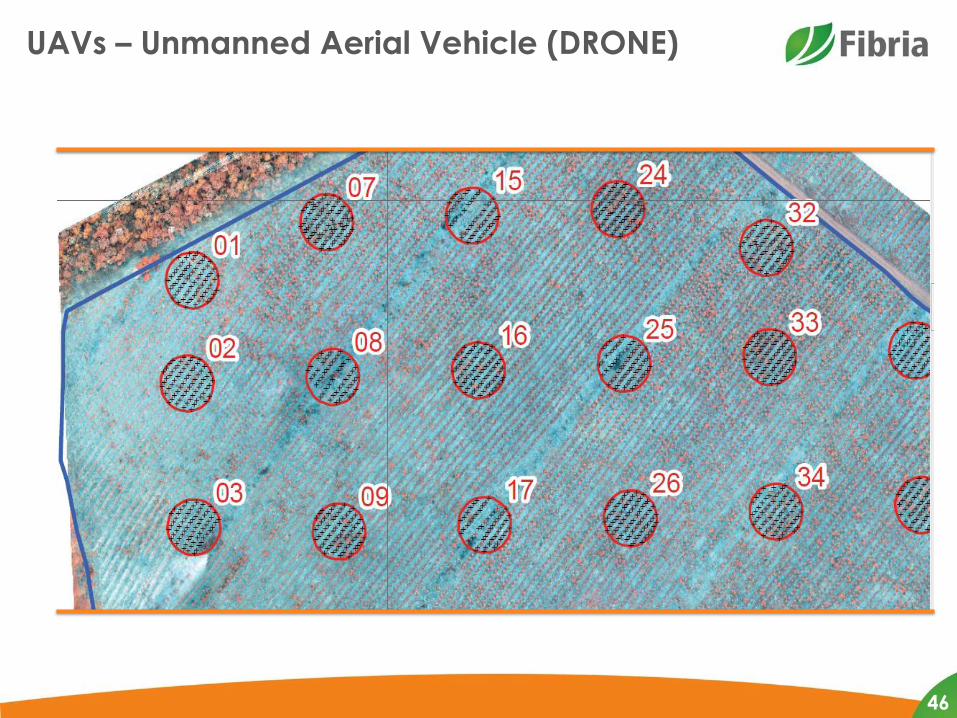

UAVs – Unmanned Aerial Vehicle (DRONE)

• 3 years of development – Operational Scale Oct/2013

• Productivity increase up to 700 ha/h

• Forest view from above

45

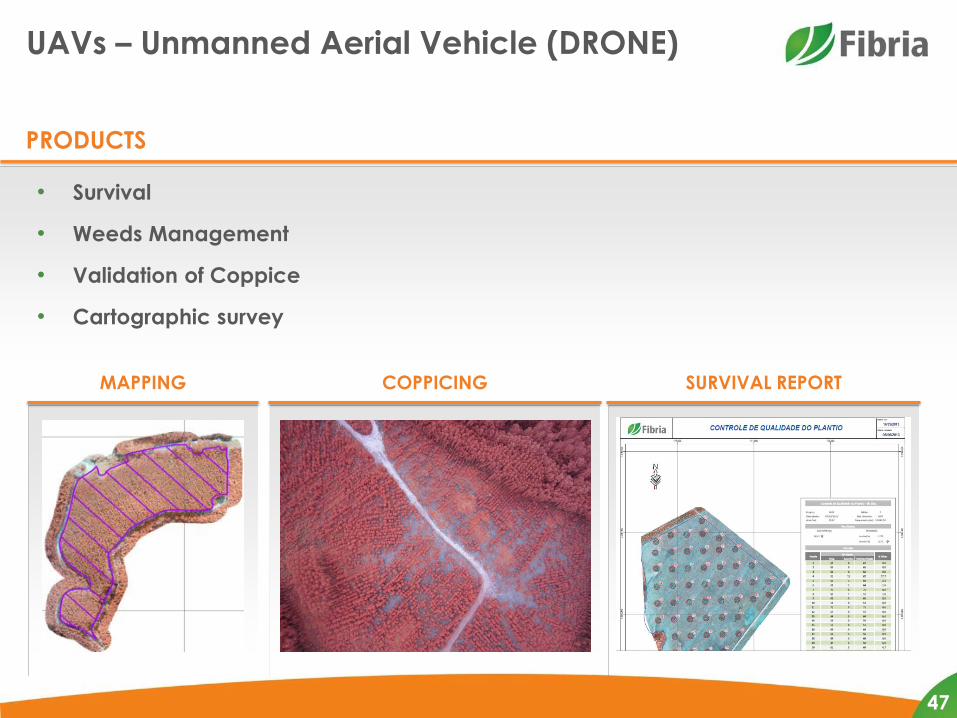

UAVs – Unmanned Aerial Vehicle (DRONE)

46

SURVIVAL REPORT COPPICING MAPPING

UAVs – Unmanned Aerial Vehicle (DRONE)

PRODUCTS

• Survival

• Weeds Management

• Validation of Coppice

• Cartographic survey

47

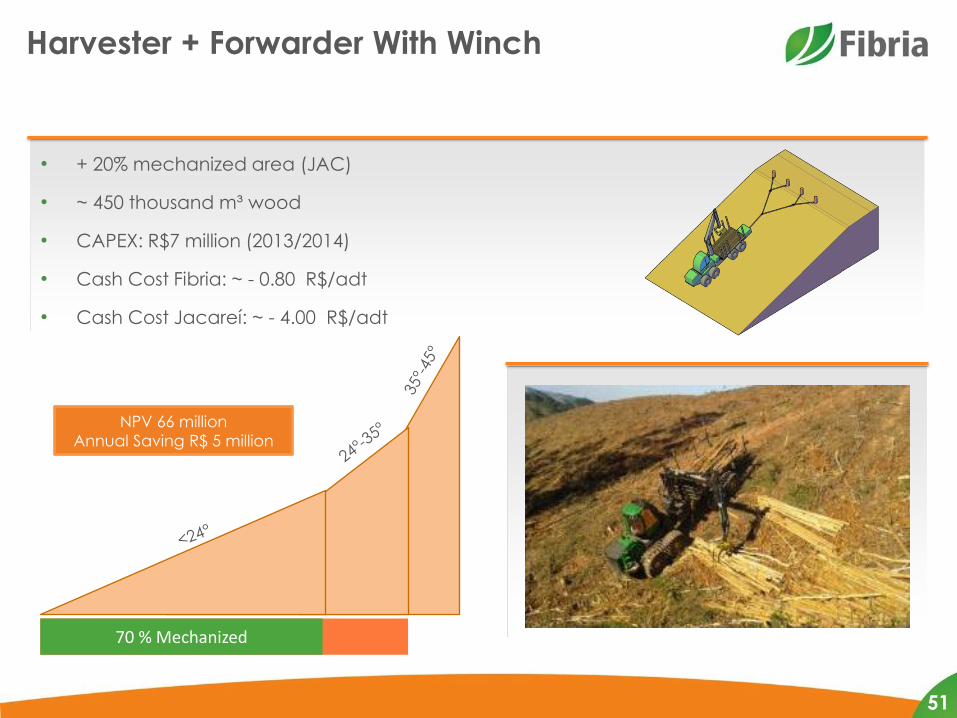

Harvester + Forwarder With Winch

Mooring system of forest machines in

their own trees from the edge of the field

48

Harvester + Forwarder With Winch

• + 20% mechanized area (JAC)

• ~ 450 thousand m³ wood

• CAPEX: R$7 million (2013/2014)

• Cash Cost Fibria: ~ - 0.80 R$/adt

• Cash Cost Jacareí: ~ - 4.00 R$/adt

NPV 66 million

Annual Saving R$ 5 million

90 % Mechanized 70 % Mechanized

51

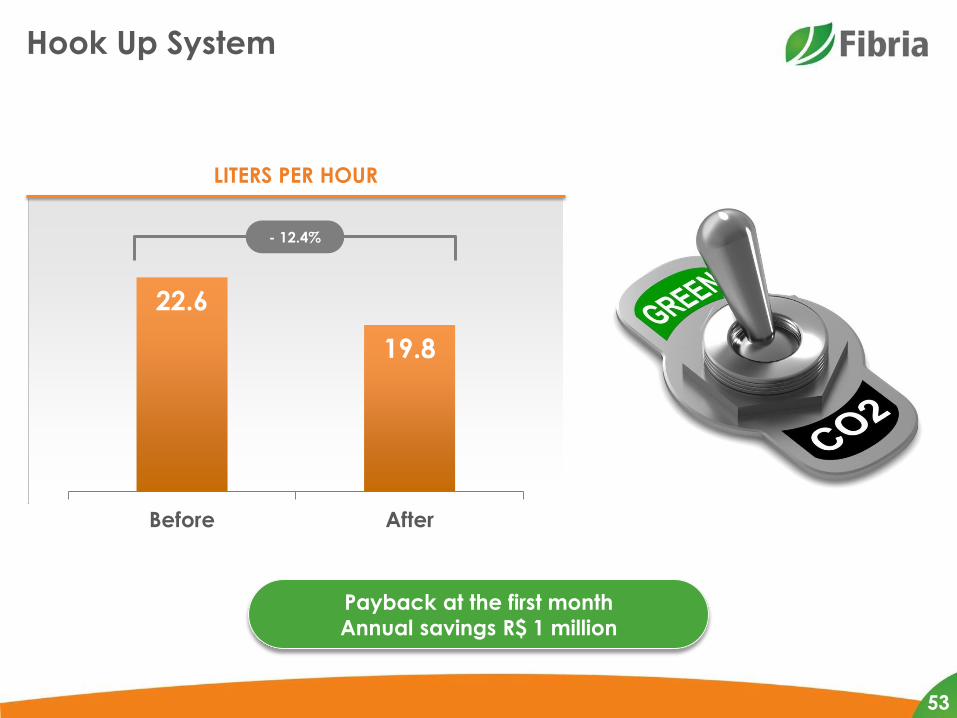

Hook Up System

"Hook up system" is a kit to optimize the flow of hydraulic oil from the base machine

to the head (74 machines)

• Reduction in diesel consumption

• Improved performance of the assembly.

Source: colheita ARA 52

LITERS PER HOUR

Hook Up System

22.6

19.8

Before After

Payback at the first month

Annual savings R$ 1 million

- 12.4%

53

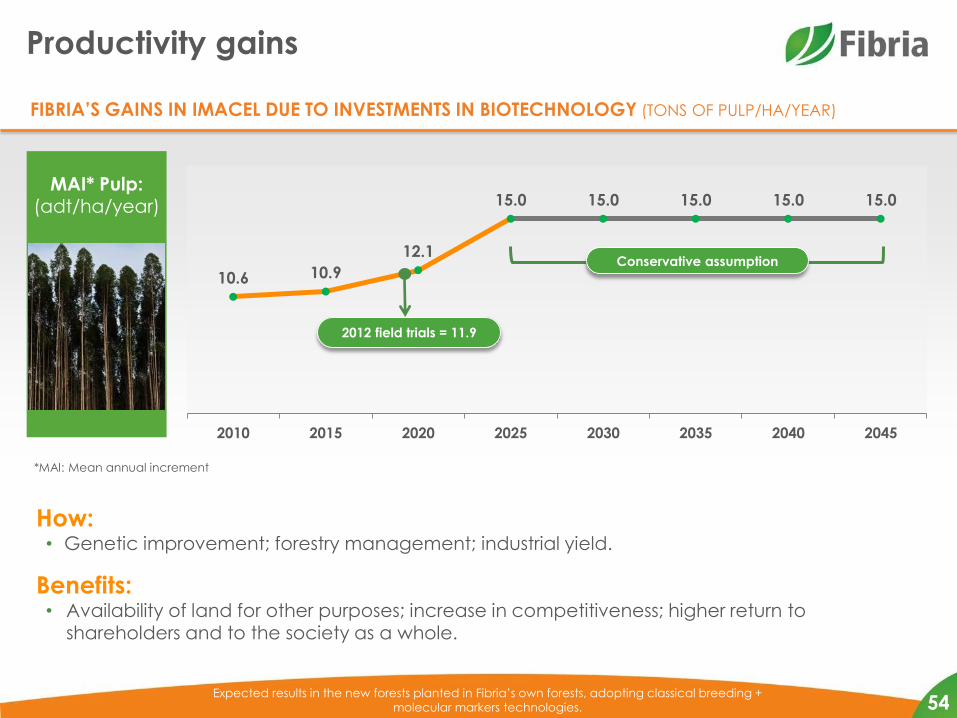

Productivity gains

MAI* Pulp: (adt/ha/year)

10.6 10.9

12.1

15.0 15.0 15.0 15.0 15.0

2010 2015 2020 2025 2030 2035 2040 2045

Expected results in the new forests planted in Fibria’s own forests, adopting classical breeding +

molecular markers technologies.

FIBRIA’S GAINS IN IMACEL DUE TO INVESTMENTS IN BIOTECHNOLOGY (TONS OF PULP/HA/YEAR)

2012 field trials = 11.9

Conservative assumption

*MAI: Mean annual increment

How: • Genetic improvement; forestry management; industrial yield.

Benefits: • Availability of land for other purposes; increase in competitiveness; higher return to

shareholders and to the society as a whole.

54

Innovation in the Core Business

The Technology Center (CT) operates within all company units and is directly involved with Fibria’s main operations, from the production of seedlings to the development of new products and

services.

The product portfolio is fully aligned with Fibria’s strategy and is managed by a system based on the “Stage and Gate” methodology.

In 2013, projects are distributed in the following dimensions:

• Operating excellence

• Differentiation through disruptive technologies

• Business sustainability (social and environmental development)

• New businesses

55

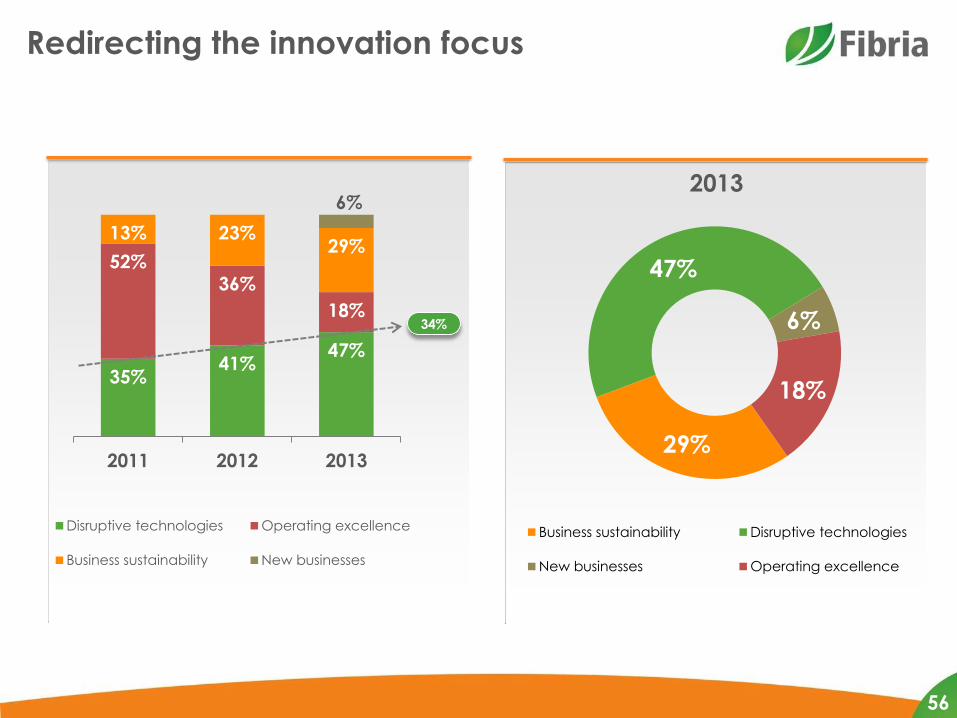

Redirecting the innovation focus

29%

47%

6%

18%

Business sustainability Disruptive technologies

New businesses Operating excellence

35% 41%

47%

52% 36%

18%

13% 23% 29%

6%

2011 2012 2013

Disruptive technologies Operating excellence

Business sustainability New businesses

34%

56

2013

Biotechnology: Plant Propagation

• Clone multiplication in laboratory: BIOUNITS

• “Successful Case” 2013 XIII ANPEI Conference on Technological Innovation

• Increase by 40 times in the clone multiplication rate

• 38% decrease in the seedling production time (cycle)

57

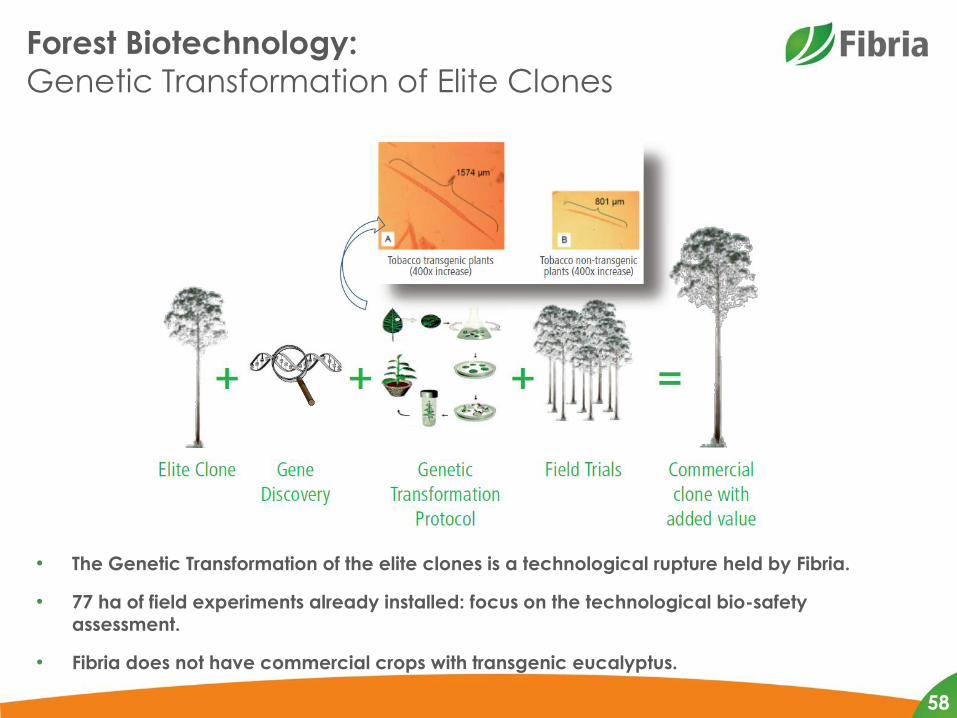

Forest Biotechnology:

Genetic Transformation of Elite Clones

• The Genetic Transformation of the elite clones is a technological rupture held by Fibria.

• 77 ha of field experiments already installed: focus on the technological bio-safety assessment.

• Fibria does not have commercial crops with transgenic eucalyptus.

58

Product Development

59

Fiber differentiation

through chemical

boosting

Fiber differentiation

through forest and/or

process tunning

Pulp application

engineering: Capabilities & Know-how

DRIVERS

1. Papermaking performance improvement

2. Paper performance improvement

3. Share increase by displacing RF, SWKP and/or other HWKP

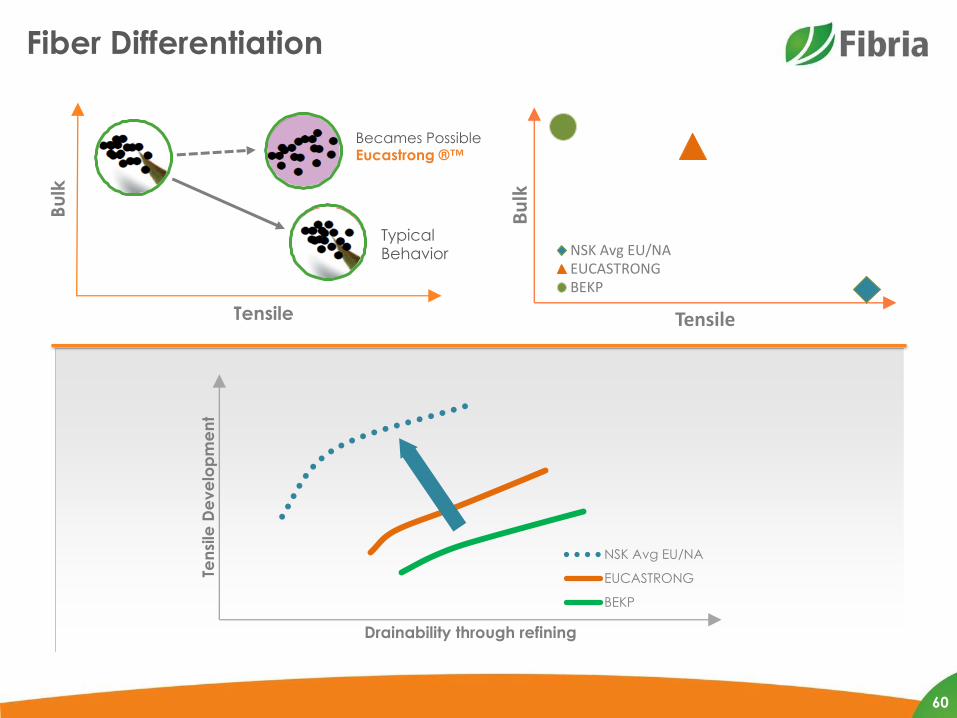

Fiber Differentiation

60

Ten

sile

De

ve

lop

me

nt

Drainability through refining

NSK Avg EU/NA

EUCASTRONG

BEKP

Bu

lk

Tensile

NSK Avg EU/NAEUCASTRONGBEKP

Bu

lk

Tensile

Becames Possible Eucastrong ®™

Typical Behavior

BEKP refined as usual

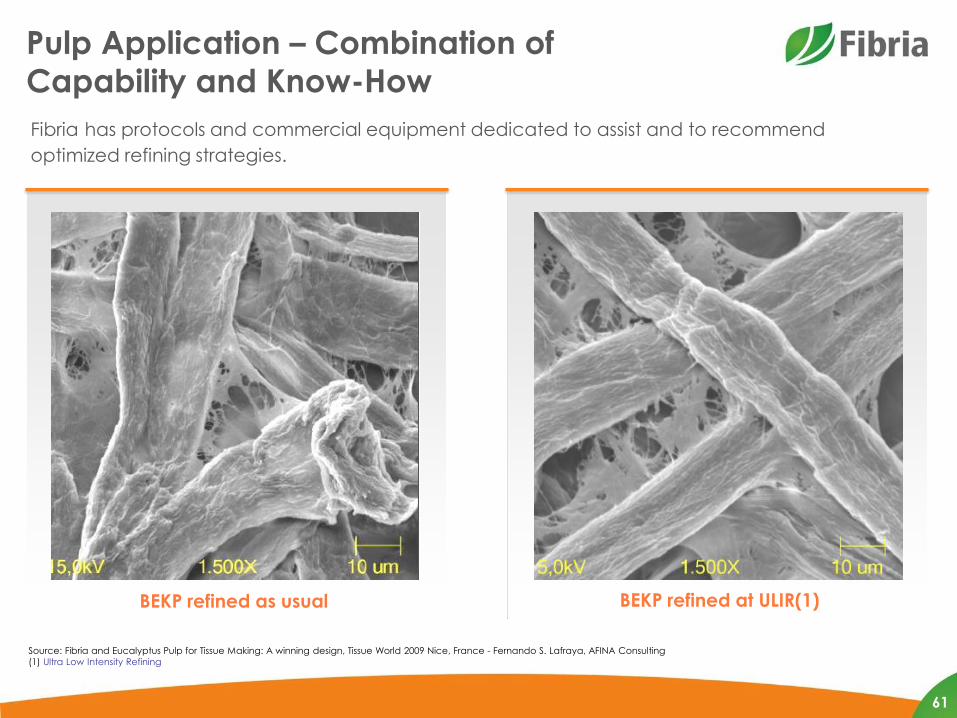

Pulp Application – Combination of

Capability and Know-How

61

Fibria has protocols and commercial equipment dedicated to assist and to recommend

optimized refining strategies.

BEKP refined at ULIR(1)

Source: Fibria and Eucalyptus Pulp for Tissue Making: A winning design, Tissue World 2009 Nice, France - Fernando S. Lafraya, AFINA Consulting

(1) Ultra Low Intensity Refining

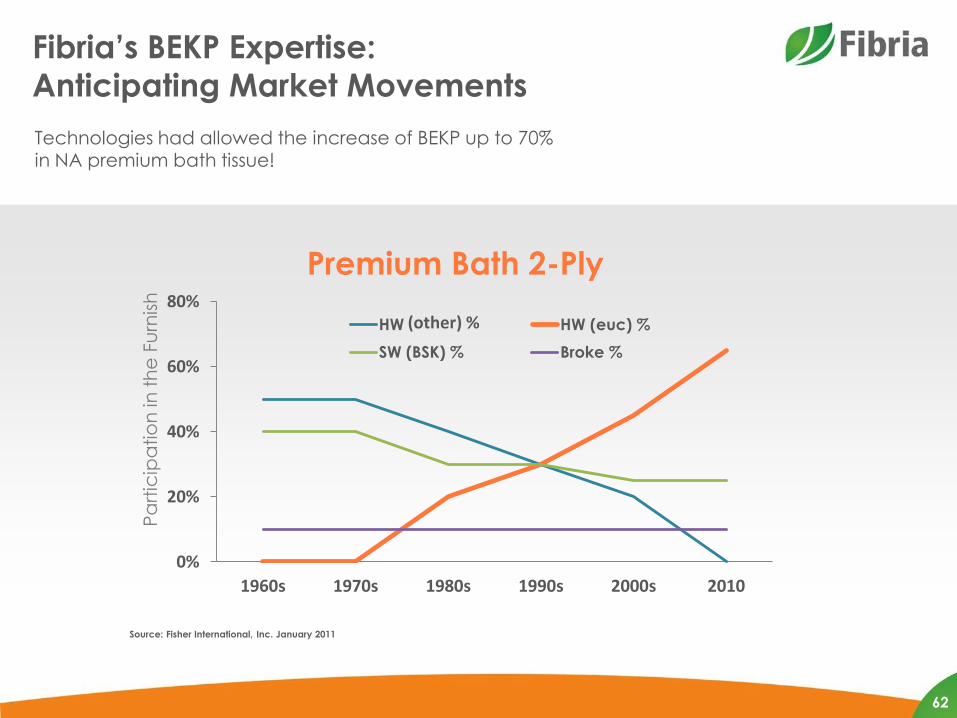

Fibria’s BEKP Expertise:

Anticipating Market Movements

62

Technologies had allowed the increase of BEKP up to 70% in NA premium bath tissue!

0%

20%

40%

60%

80%

1960s 1970s 1980s 1990s 2000s 2010

Pa

rtic

ipa

tio

n in

th

e F

urn

ish

Premium Bath 2-Ply

HW HW (euc) %

SW (BSK) % Broke %

Source: Fisher International, Inc. January 2011

(other) %

There are various options to reduce capital

expenditures in Fibria’s value chain

POTENTIAL ACTIONS TO REDUCE EMPLOYED CAPITAL

LAND

• Sales of areas with high real estate potential

• Real estate land funds

FOREST

• Creation of planting funds, defining purchase options for wood

(new and current areas)

INDUSTRY AND LOGISTICS

• Outsourcing of non-core production phases and logistics assets

63

Growth initiatives may take place through organic

expansion or consolidation

• Value drivers to improve on the current situation

• Growth Initiative

– Organic Expansion

– Consolidation

• Complementary actions in the Value Chain

64

Fibria is preparing for its organic expansion, based

on a model that creates different growth options

STRATEGY FOR POTENTIAL ORGANIC EXPANSION

1. Maintain forest formation through: − Implementation of new areas − Renting − Partnership with TIMO´s − Reinvestment of resources from assets divestments

2. Obtain licensing for all potential expansions

3. Continuous investigation of new low cost areas

Usage of wood for

organic growth

Wood sales in the

market or usage in new

businesses

Usage of areas

in M&A events

65

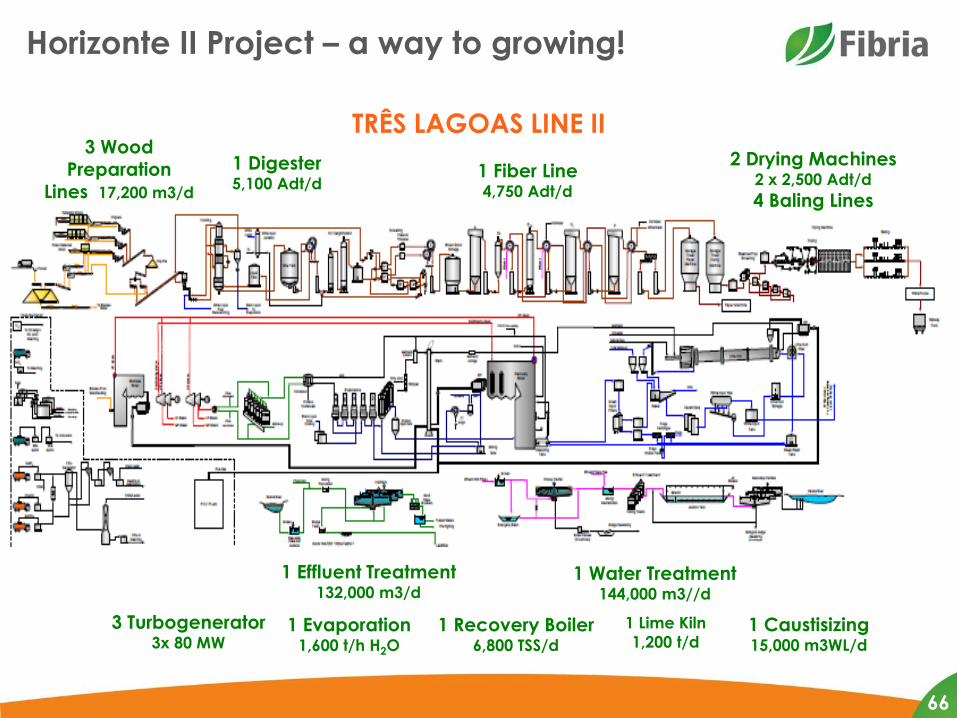

Horizonte II Project – a way to growing!

3 Wood

Preparation Lines 17,200 m3/d

1 Digester 5,100 Adt/d

1 Fiber Line 4,750 Adt/d

2 Drying Machines 2 x 2,500 Adt/d

4 Baling Lines

TRÊS LAGOAS LINE II

1 Effluent Treatment 132,000 m3/d

1 Water Treatment 144,000 m3//d

1 Recovery Boiler 6,800 TSS/d

3 Turbogenerator 3x 80 MW

1 Lime Kiln

1,200 t/d 1 Evaporation

1,600 t/h H2O

1 Caustisizing 15,000 m3WL/d

66

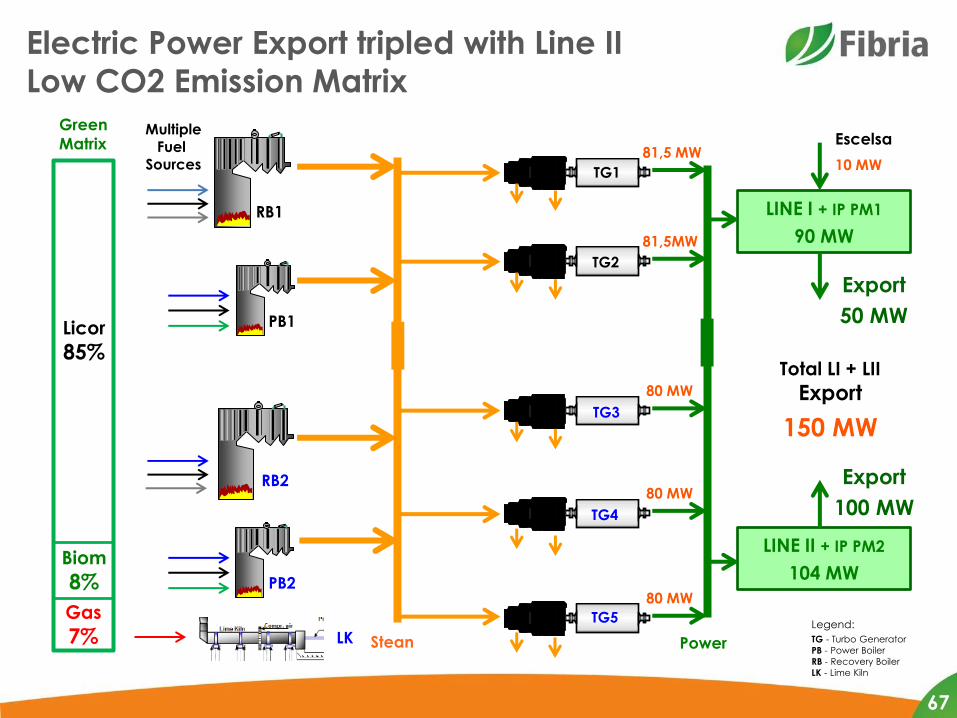

Electric Power Export tripled with Line II

Low CO2 Emission Matrix

LINE I + IP PM1

90 MW

RB1

RB2

PB1

PB2

TG1

TG2

TG3

TG4

TG5

81,5 MW

81,5MW

80 MW

80 MW

80 MW

Escelsa

Export

50 MW

Green

Matrix Multiple

Fuel Sources

Licor

85%

Gas

7%

Biom

8%

Total LI + LII

Export

150 MW

10 MW

LINE II + IP PM2

104 MW

Export

100 MW

LK Legend:

TG - Turbo Generator

PB - Power Boiler

RB - Recovery Boiler

LK - Lime Kiln

Stean Power

67

Fibria is prepared to grow

Installation License: L I n. 84/2011 revalidated to 2017

Authorized Capacity: 1,750,000 ADtB/year (4,794 tpd)

Total Capacity: 3,050,000 ADtB/year (8,616 tpd)

Other Authorizations:

Co-generation: 259,5 MW

Expansion & New Capacity of Landfill: 204,800 + 750,000 m3

Production of Soil Corrective from Residues: 31,000 t/year

Burns of Secondary Mud from ETE in Biomass Power Boiler

68

Growth from consolidation present challenges,

but benefits are undisputed

CHALLENGES

• Strategic motivation and timing of the other party

• Relative valuation

• Governance, control issues

• Debt level of players

BENEFITS

• Huge potential synergies

• Market and client portfolio consolidation

• Rationalization of pipeline of new project

GROWTH FROM CONSOLIDATION IS KEY DRIVER FOR

VALUE CREATION

69

Complementary actions include assessing

opportunities in biotechnology and in the logistics

chain

• Value drivers to improve on the current situation

• Growth Initiatives

• Complementary actions in the value chain

– Opportunities in the Bio-market

– Actions in the Logistics Chain

70

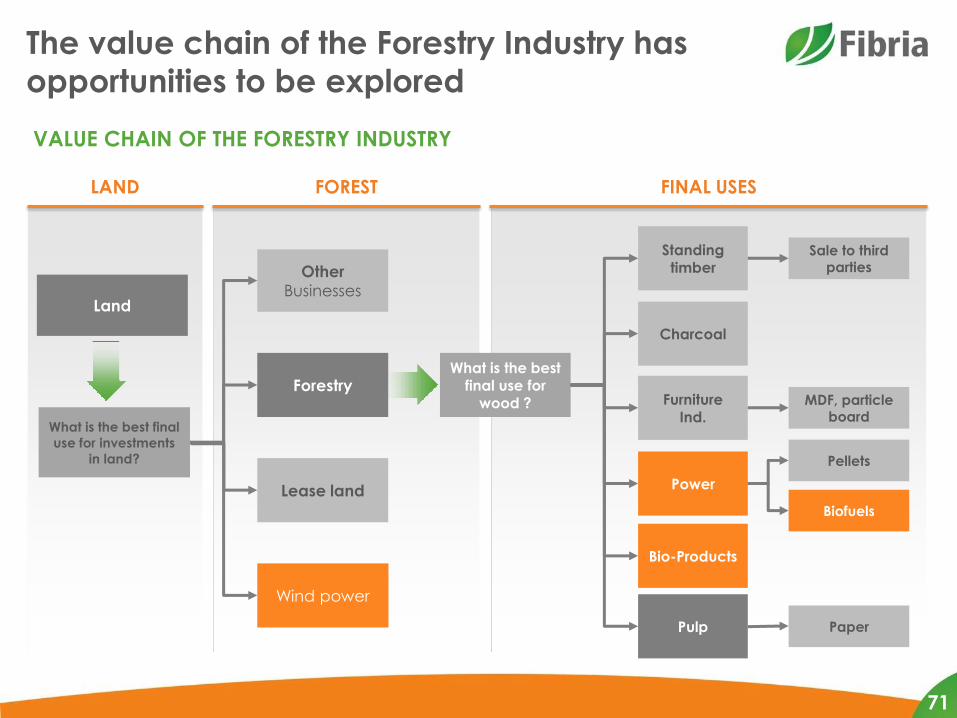

LAND

The value chain of the Forestry Industry has

opportunities to be explored

VALUE CHAIN OF THE FORESTRY INDUSTRY

FOREST FINAL USES

Land

What is the best final

use for investments

in land?

What is the best final use for

wood ? Furniture Ind.

Charcoal

Pulp

Standing timber

Power

MDF, particle board

Pellets

Biofuels

Other

Businesses

Sale to third parties

Bio-Products

Paper

Lease land

Wind power

Forestry

71

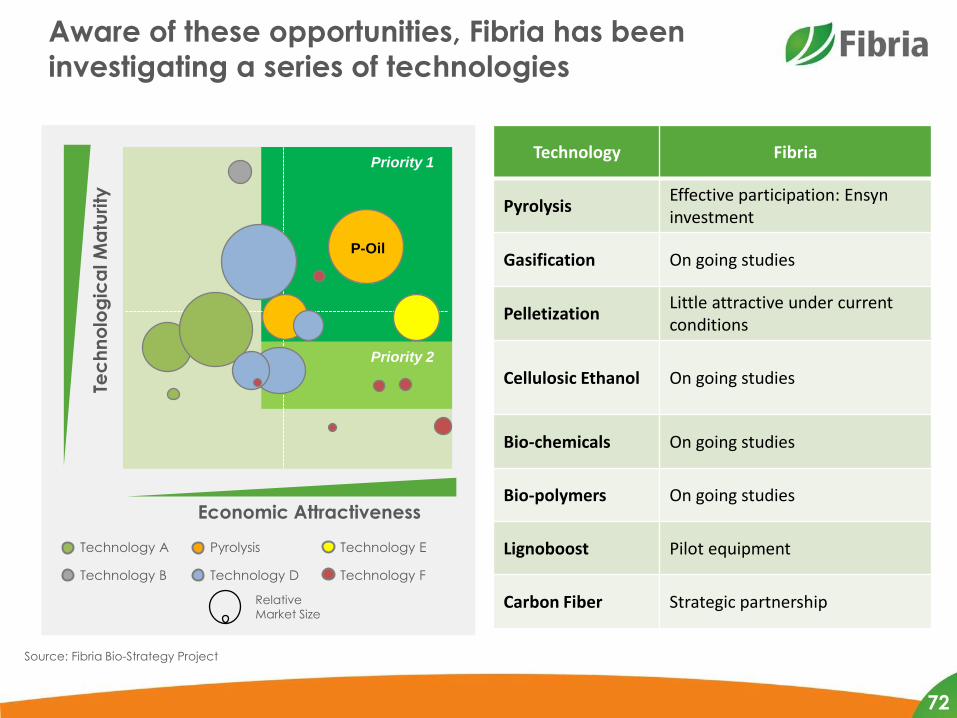

Aware of these opportunities, Fibria has been

investigating a series of technologies Te

ch

no

log

ica

l M

atu

rity

Economic Attractiveness

Technology A

Technology B

Technology E

Technology F

Pyrolysis

Technology D

Priority 1

P-Oil

Priority 2

Relative

Market Size

Source: Fibria Bio-Strategy Project

Economic Attractiveness

Technology Fibria

Pyrolysis Effective participation: Ensyn investment

Gasification On going studies

Pelletization Little attractive under current conditions

Cellulosic Ethanol On going studies

Bio-chemicals On going studies

Bio-polymers On going studies

Lignoboost Pilot equipment

Carbon Fiber Strategic partnership

72

73

Conceptual Layout – Bio-Oil Plant

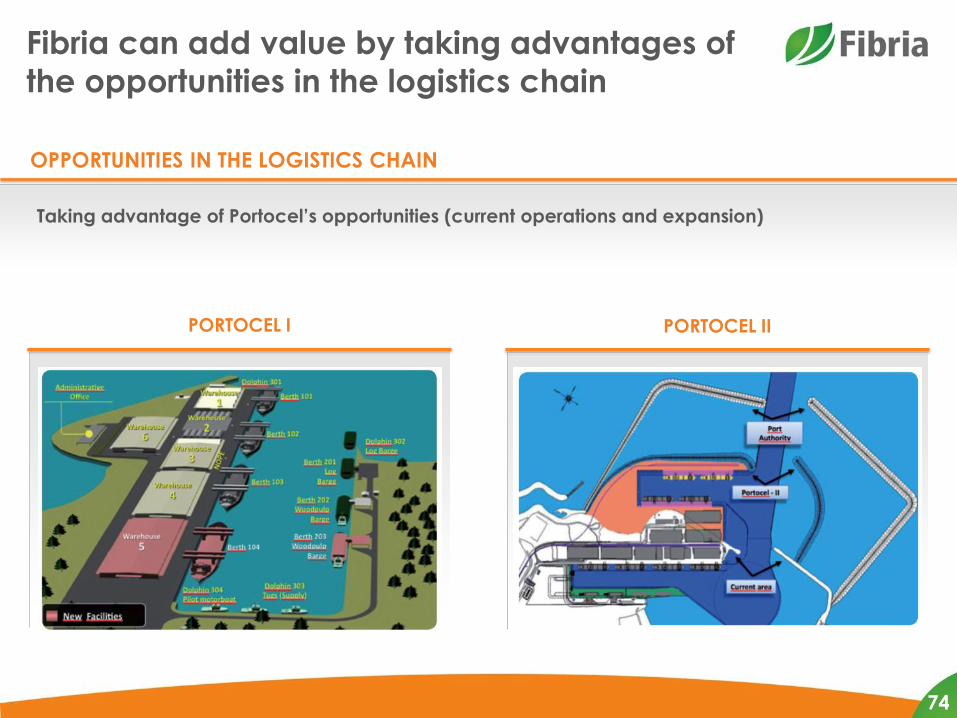

Fibria can add value by taking advantages of

the opportunities in the logistics chain

OPPORTUNITIES IN THE LOGISTICS CHAIN

Taking advantage of Portocel’s opportunities (current operations and expansion)

PORTOCEL I PORTOCEL II

74

RJ SP

BA

ES MG

GO

MT

Study area illustration

Portocel Expansion: many opportunities of

value creation

Rio de Janeiro/Niterói

Itaguaí/Angra dos Reis

Vitória/Tubarão/ Praia Mole

São Sebastião

Forno

Ilhéus

Barra do Riacho

Porto de Ubu

The Portocel Expansion Project study area consists of 4 states plus parts of 3 other states, reaching regions up to 1.500 km far from the future terminal

Criteria for defining the study area

• 1.000 km radius by road from Barra de Riacho;

• Additional 500 km radius from Anápolis (influence of the rail system) ;

• The study area covers the states of Rio de Janeiro, Espírito Santo, Minas Gerais, Goias and part of Mato Grosso, Sao Paulo and Bahia;

• 67% of Brazil's GDP is generated in the study area.

75

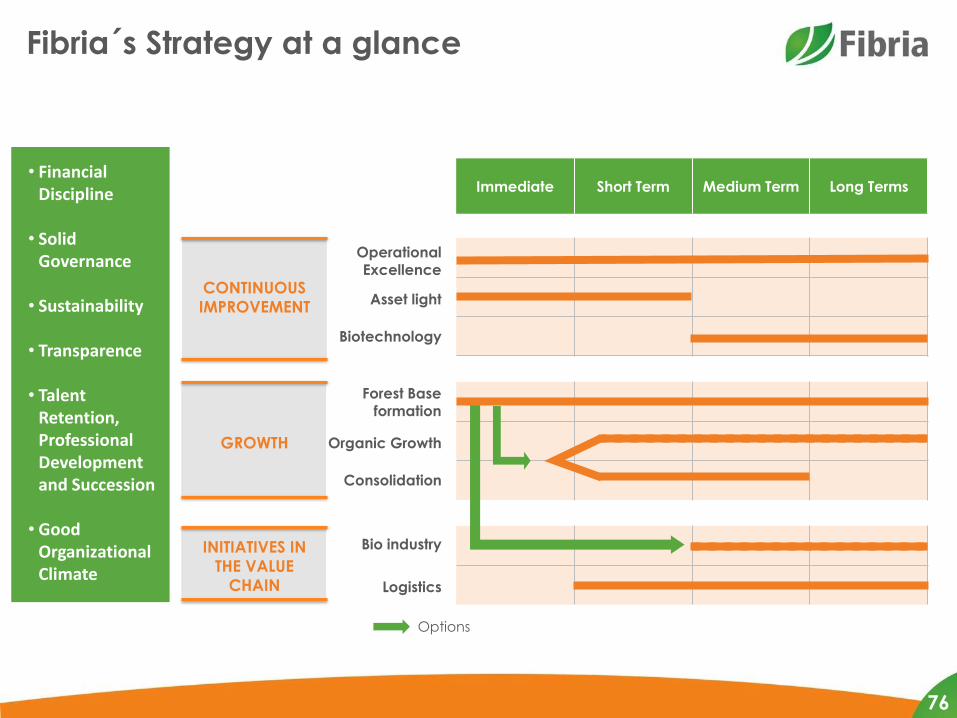

CONTINUOUS

IMPROVEMENT

Immediate Short Term Medium Term Long Terms

-

Fibria´s Strategy at a glance

Options

Operational Excellence

Asset light

Biotechnology

GROWTH

INITIATIVES IN

THE VALUE

CHAIN

Forest Base formation

Organic Growth

Consolidation

Bio industry

Logistics

• Financial Discipline

• Solid Governance

• Sustainability

• Transparence

• Talent Retention, Professional Development and Succession

• Good Organizational Climate

76