apresentação do powerpoint - ri.multiplan.com.brri.multiplan.com.br/ptb/2025/discussion...

TRANSCRIPT

May 2018

Discussion MaterialMay, 2018

May 2018

This presentation is only indicative of the Company's intention to develop the mentioned projects. The images presented are

merely illustrative, and the projects could be modified in whole or in part, at Multiplan's discretion. Many factors and

assumptions that establish the feasibility of these projects are not in the control or expectation of the Company. The

reader/investor should not rely solely on the information herein to make decisions with respect to trading the securities issued

by Multiplan.

The document may also contain prospective statements, which are subject to risks and uncertainties as they are based on

expectations of the company’s management and on available information. The company is under no obligation to update these

statements.

The Company’s future financial situation, operating results, market share and competitive position may differ substantially from

those expressed or suggested by forward-looking statements. Many factors and values that may impact these results are

beyond the company’s ability to control. Future projects could differ materially due to market conditions, changes in laws or

government policies, changes in operational conditions and costs, changes in project schedules, operating performance,

demands by tenants and consumers, commercial negotiations or other technical and economic factors. These projects may be

altered in part or totally by the company with no prior warning.

For more detailed information, please check our Financial Statements, Reference Form (Formulário de Referência) and other

relevant information on our investor relations website ir.multiplan.com.br.

Disclaimer

May, 2018

May 2018

Growth

May 2018

Future GrowthOctober, 2017

4

Multiplan's GLA growth over the years ('000 sq.m)

A seasoned Company with a proven tack record...

...in spite of the storm

May 2018

Future GrowthOctober, 2017

5

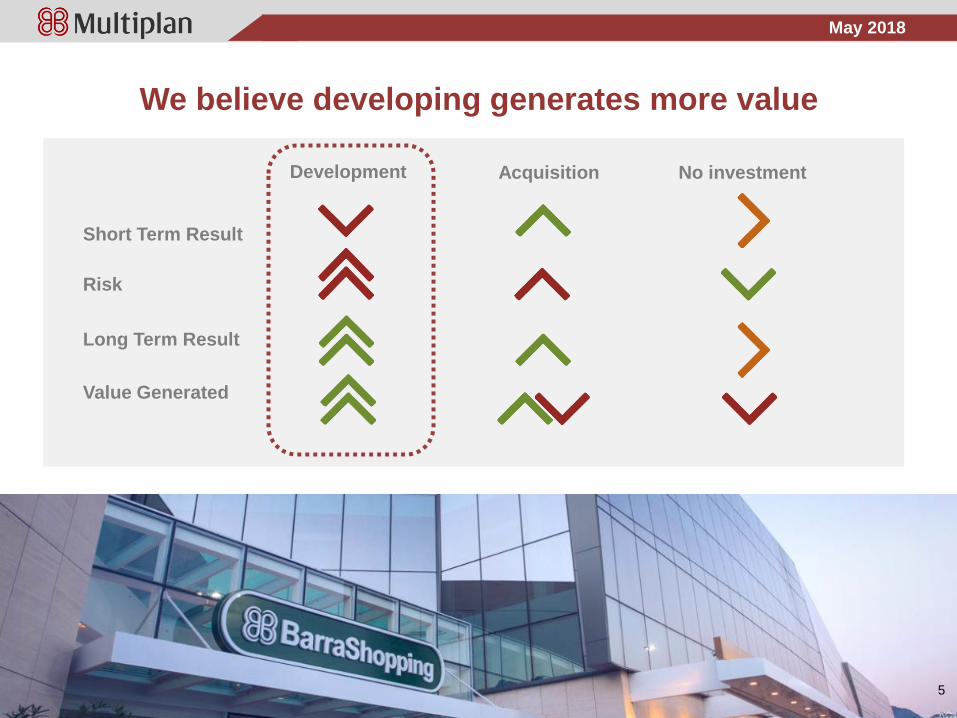

We believe developing generates more value

Short Term Result

Risk

Long Term Result

Value Generated

Development Acquisition No investment

May 2018

6

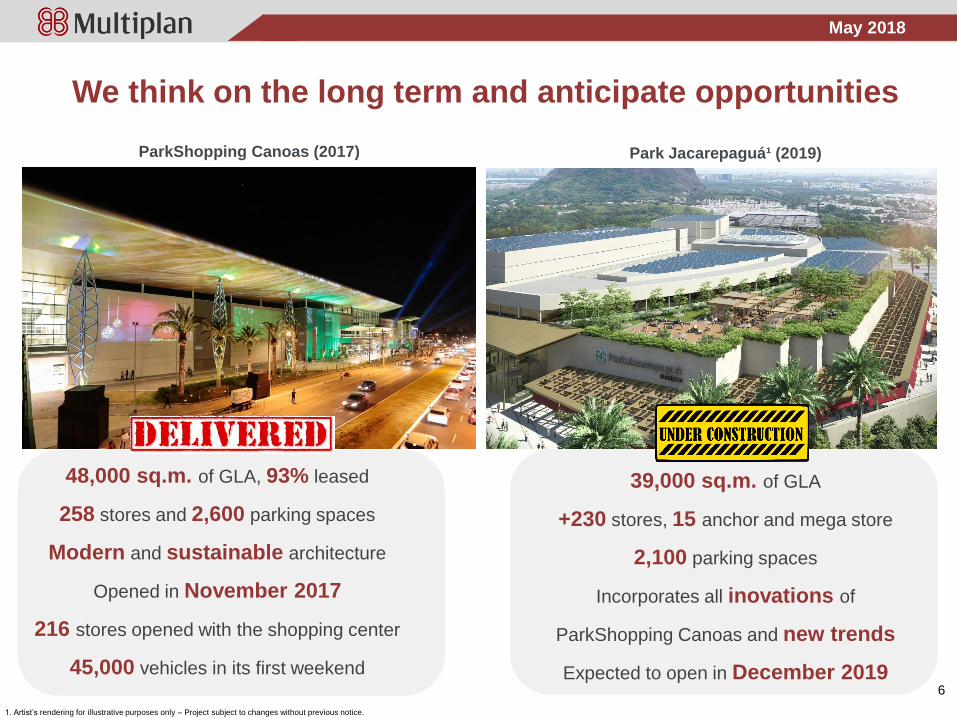

We think on the long term and anticipate opportunities

1. Artist’s rendering for illustrative purposes only – Project subject to changes without previous notice.

ParkShopping Canoas (2017)

48,000 sq.m. of GLA, 93% leased

258 stores and 2,600 parking spaces

Modern and sustainable architecture

Opened in November 2017

216 stores opened with the shopping center

45,000 vehicles in its first weekend

39,000 sq.m. of GLA

+230 stores, 15 anchor and mega store

2,100 parking spaces

Incorporates all inovations of

ParkShopping Canoas and new trends

Expected to open in December 2019

Park Jacarepaguá¹ (2019)

May 2018

7

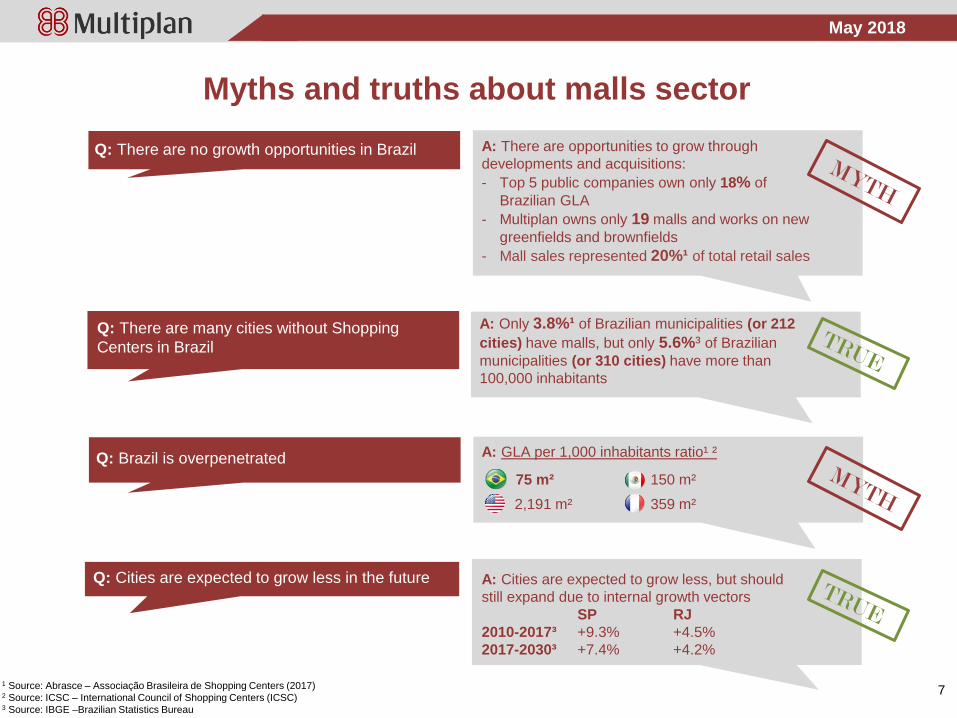

Q: There are many cities without Shopping

Centers in Brazil

Q: There is potential for building a Shopping

Center in every city

A: Only 3.8%¹ of Brazilian municipalities (or 212

cities) have malls, but only 5.6%³ of Brazilian

municipalities (or 310 cities) have more than

100,000 inhabitants

Q: Brazil is overpenetrated

Q: There are no growth opportunities in Brazil

A: GLA per 1,000 inhabitants ratio¹ ²

75 m²

2,191 m² 359 m²

150 m²

1 Source: Abrasce – Associação Brasileira de Shopping Centers (2017)2 Source: ICSC – International Council of Shopping Centers (ICSC)3 Source: IBGE –Brazilian Statistics Bureau

Myths and truths about malls sector

A: There are opportunities to grow through

developments and acquisitions:

- Top 5 public companies own only 18% of

Brazilian GLA

- Multiplan owns only 19 malls and works on new

greenfields and brownfields

- Mall sales represented 20%¹ of total retail sales

Q: Cities are expected to grow less in the future A: Cities are expected to grow less, but should

still expand due to internal growth vectors

SP RJ

2010-2017³ +9.3% +4.5%

2017-2030³ +7.4% +4.2%

May 2018

Location, Location, Location + Quality, Quality, Quality

Source: Multiplan, Abrasce and IBGE

0.2%

3.2%

8.7%

Multiplan vs Brazil average (2017)

84%

64%

GDP per capita (Exposure to States)

R$25,814

R$19,901

Exposure to A/B classes

Average GLA by mall

Total sales (R$/sq.m.)

Multiplan’s share in Brazil (2017)

Number of

municipalities

Number of

malls

GLA (sq.m.)

Shopping

center

sales (R$)

5,570 cities

571 malls

R$167.7 billion

11 cities

19 malls

R$14.7 billion

8

43.851 m²

27,285 m²

20.439 R$/m²

10.764 R$/m²

5.3%15,580,379 m²

833,165 m²

May 2018

E-commerce

May 2018

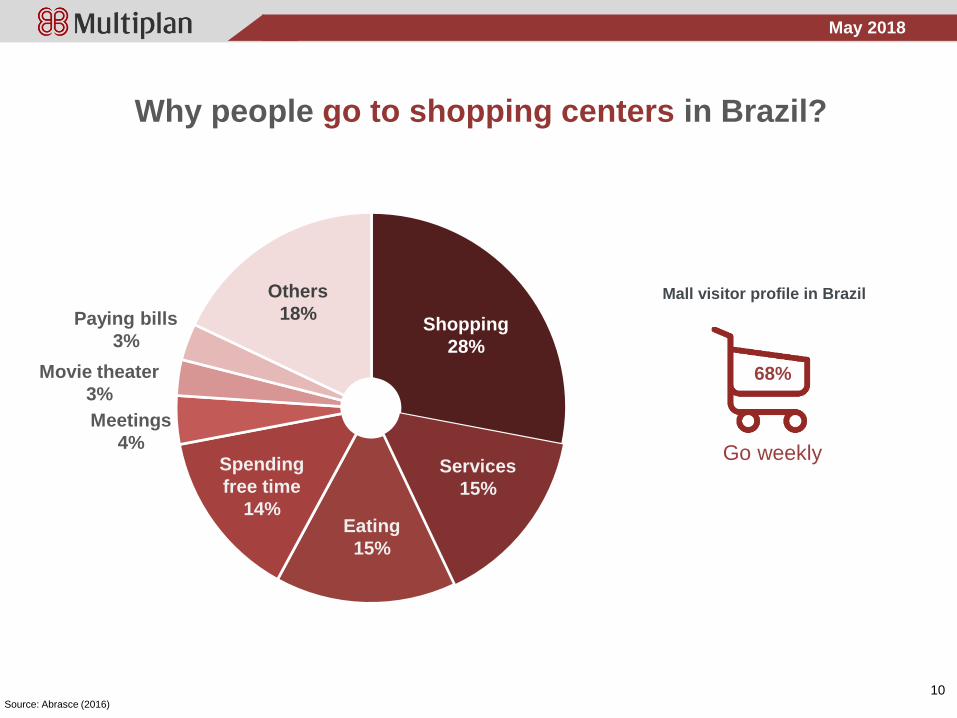

Why people go to shopping centers in Brazil?

Source: Abrasce (2016)

Shopping

28%

Others

18%

Meetings

4%

Movie theater

3%

Paying bills

3%

Eating

15%

Services

15%

Spending

free time

14%

68%

Go weekly

Mall visitor profile in Brazil

10

May 2018

E-commerce In-storeExperience, “touch and feel”

Fill an immediate need or desire

Provide a “one-stop” shopping

trip

Better for expensive shipping

goods

Fresh products

People interactions

Omni-channel is

the futureOnline purchase with in-store

pickups, returns and upsale

Internet retailers expanding their

physical footprint

Shopping centers convenience

Convenience

Assortment of products

Decision-making: online reviews

Bargain hunting: find the best

possible price

Useful functions: manage

shopping lists and set up

shopping baskets over time

Innovative technologies adding value to the in-store shopping experience

“The consumer does not care where a sale is booked, but demands excelent incentivised

service at all stages of the shopping experience.”1

1 Source: ICSC – International Council of Shopping Centers (ICSC) –

Exploring New Leasing Models in a Omni-Channel World (2016)

11Source: Multiplan

Present

May 2018

We own and manage a high productive portfolio

Tenants sales: Multiplan & Brazilian malls

Tenants sales: Multiplan & USA malls

Tenants sales – USD/sq.f.³ (anchor +

satellite stores) - 2017

Tenants sales – USD/sq.f. ³

(satellite stores only) - 2017

12

1 Source: ICSC – International Council of Shopping Centers2 Source: Abrasce – Associação Brasileira de Shopping Centers.3 Source: Bloomberg. 2017 final Exchange rate of R$3.1921/ US$.

1. Location, location, location: we are well positioned inside the

largest cities;

2. Consumer experience: Food + Service segments represented

35.1% of Multiplan’s GLA, equal to Apparel;

3. Mixed-use: integrate other types of real estate with malls,

generating synergies;

4. Organic growth: 46 mall expansions delivered in 44 years;

5. Innovation: constant mix change antecipating consumers need

and trendspotting;

6. Efficiency: High productivity, low tenant concentration.

Store Segment GLA Distribution

USA (2017)¹Multiplan (2017)

467

799

USA malls¹ Multiplan'smalls

313

574

Brazilianmalls²

Multiplan'smalls

May 2018

MULT3 Valuation

May 2018

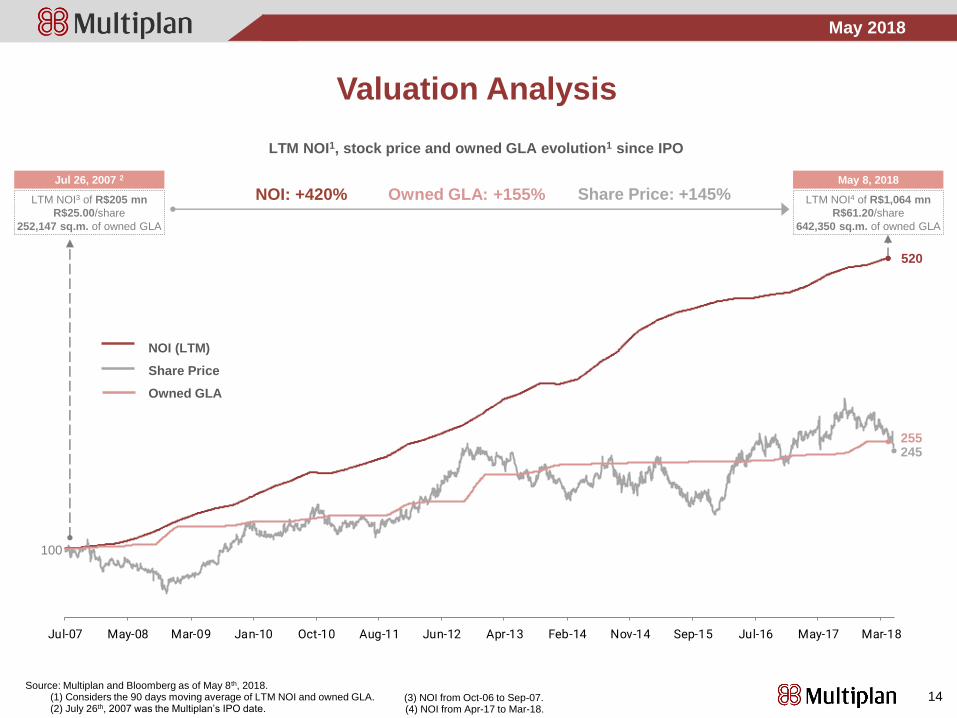

Jul-07 May-08 Mar-09 Jan-10 Oct-10 Aug-11 Jun-12 Apr-13 Feb-14 Nov-14 Sep-15 Jul-16 May-17 Mar-18

14

NOI (LTM)

Share Price

520

245

LTM NOI1, stock price and owned GLA evolution1 since IPO

100

Source: Multiplan and Bloomberg as of May 8th, 2018.(1) Considers the 90 days moving average of LTM NOI and owned GLA.(2) July 26th, 2007 was the Multiplan’s IPO date.

(3) NOI from Oct-06 to Sep-07. (4) NOI from Apr-17 to Mar-18.

255

Owned GLA

Jul 26, 2007 2

LTM NOI3 of R$205 mn

R$25.00/share

252,147 sq.m. of owned GLA

May 8, 2018

LTM NOI4 of R$1,064 mn

R$61.20/share

642,350 sq.m. of owned GLA

NOI: +420% Share Price: +145%Owned GLA: +155%

Valuation Analysis

May 2018

80

90

100

110

120

130

140

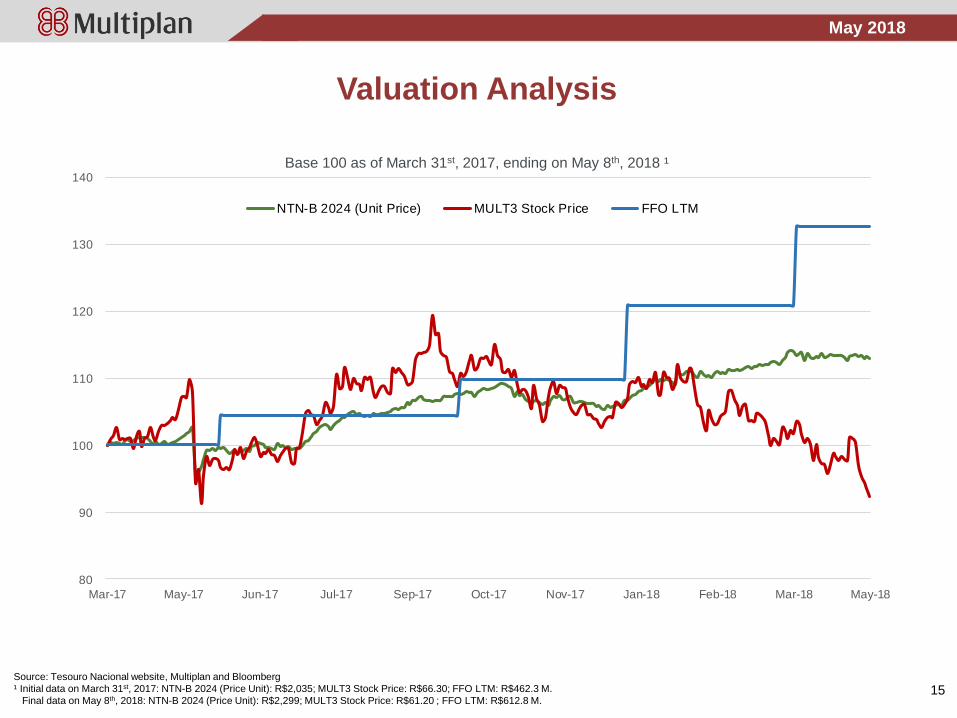

Mar-17 May-17 Jun-17 Jul-17 Sep-17 Oct-17 Nov-17 Jan-18 Feb-18 Mar-18 May-18

NTN-B 2024 (Unit Price) MULT3 Stock Price FFO LTM

Valuation Analysis

Base 100 as of March 31st, 2017, ending on May 8th, 2018 ¹

Source: Tesouro Nacional website, Multiplan and Bloomberg

¹ Initial data on March 31st, 2017: NTN-B 2024 (Price Unit): R$2,035; MULT3 Stock Price: R$66.30; FFO LTM: R$462.3 M.

Final data on May 8th, 2018: NTN-B 2024 (Price Unit): R$2,299; MULT3 Stock Price: R$61.20 ; FFO LTM: R$612.8 M.15

May 2018

5

6

2

4

3

2

3.5%-

4.3%

4.3%-

4.9%

5.0% 5.1%-

5.8%

5.8%-

6.5%

6.5%-

7.4%

FFO Yield

Recent (May 8, 2018)

5

11

1

3

1 1

5.3%-

6.3%

6.3%-

7.4%

7.5% 7.6%-

8.3%

8.3%-

9.3%

9.3%-

10.3%

NOI Yield

Recent(May 8, 2018)

2 2

4

7

5

2

4.1%-

4.5%

4.6% 4.7%-

5.5%

5.6%-

6.2%

6.2%-

6.8%

6.8%-

7.4%

NTN-B 2024 Yield (Gov. Bond)

Recent (May 8, 2018)

Valuation Analysis

5-year histogram of quarterly yield figures

Source: Tesouro Nacional website, Multiplan and Bloomberg

16

May 2018

1Q18 Results

May 2018

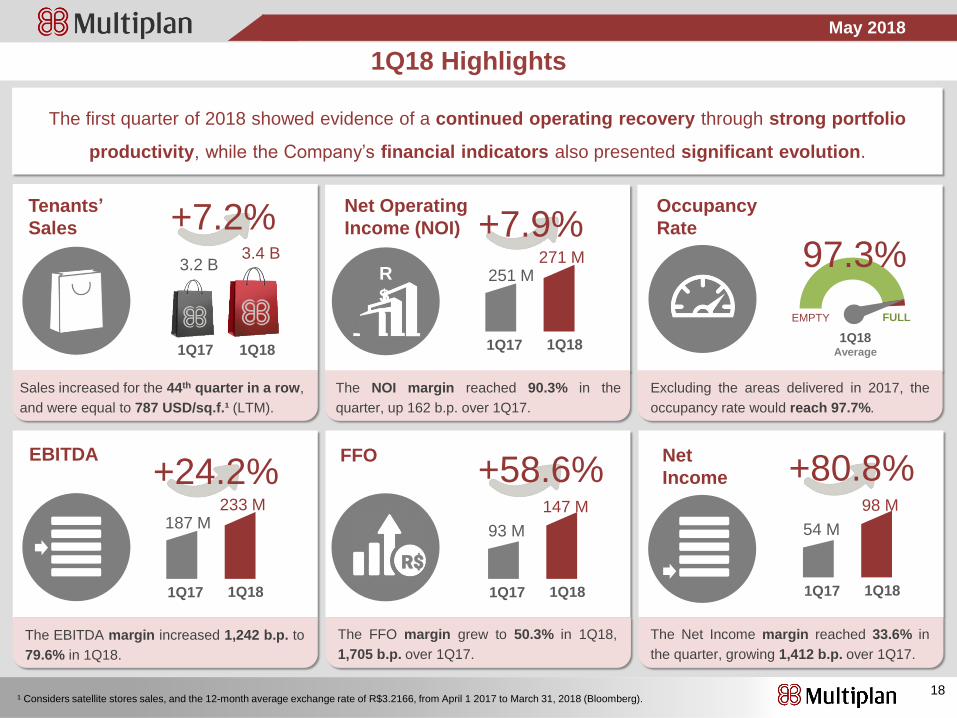

¹ Considers satellite stores sales, and the 12-month average exchange rate of R$3.2166, from April 1 2017 to March 31, 2018 (Bloomberg).

The first quarter of 2018 showed evidence of a continued operating recovery through strong portfolio

productivity, while the Company’s financial indicators also presented significant evolution.

1Q18 Highlights

97.3%

EMPTY FULL

Net Operating

Income (NOI)

EBITDA

1Q17 1Q18

Occupancy

Rate

1Q17 1Q18

233 M187 M

3.4 B3.2 B

+24.2%FFO

1Q17 1Q18

147 M

93 M

+58.6%

Tenants’

Sales +7.2%

1Q18Average

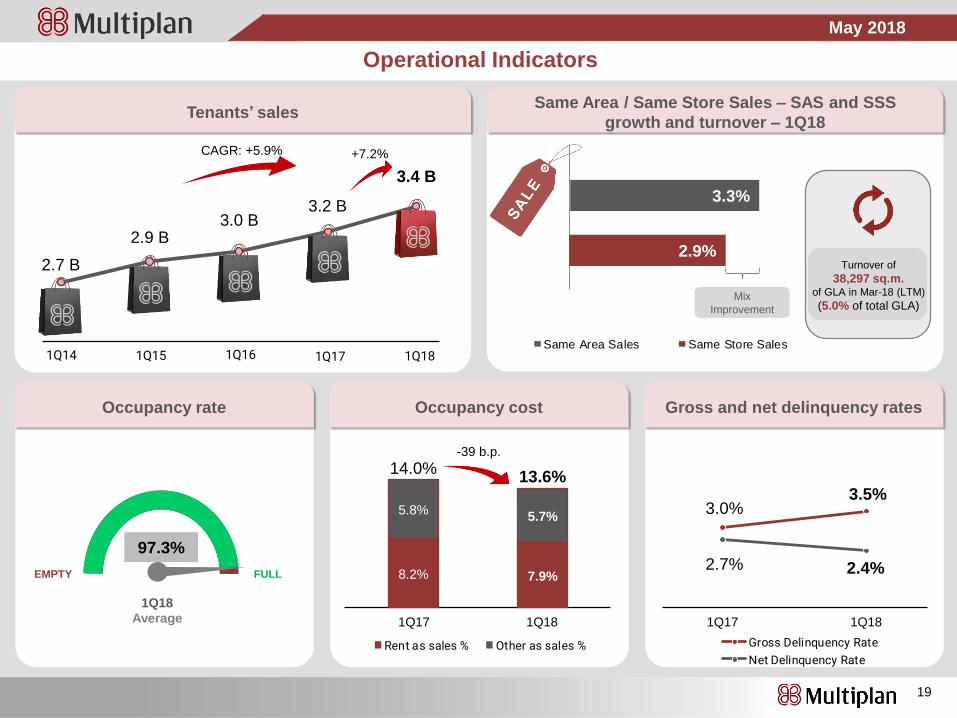

Sales increased for the 44th quarter in a row,

and were equal to 787 USD/sq.f.¹ (LTM).

The NOI margin reached 90.3% in the

quarter, up 162 b.p. over 1Q17.

Excluding the areas delivered in 2017, the

occupancy rate would reach 97.7%.

The Net Income margin reached 33.6% in

the quarter, growing 1,412 b.p. over 1Q17.

The FFO margin grew to 50.3% in 1Q18,

1,705 b.p. over 1Q17.

The EBITDA margin increased 1,242 b.p. to

79.6% in 1Q18.

R

$

1Q17 1Q18

271 M251 M

+7.9%

Net

Income

1Q17 1Q18

98 M

54 M

+80.8%

R$

18

May 2018

1Q14 1Q15 1Q16 1Q17 1Q18

Operational Indicators

19

Mix

Improvement

3.3%

2.9%

Same Area / Same Store Sales – SAS and SSS

growth and turnover – 1Q18Tenants’ sales

Occupancy rate Gross and net delinquency ratesOccupancy cost

97.3%

EMPTY FULL 8.2% 7.9%

5.8%5.7%

14.0%13.6%

-39 b.p.

1Q181Q17

1Q151Q14 1Q16 1Q17 1Q18

+7.2%

3.4 B

3.2 B3.0 B

2.9 B

2.7 B

CAGR: +5.9%

‘Turnover of

38,297 sq.m. of GLA in Mar-18 (LTM)

(5.0% of total GLA)

2.4%

3.0% 3.0%2.8%

2.5%

0.9%

2.7%

1.3%

2.2% 1.1%

4Q16 1Q17 2Q17 3Q17 4Q17

Gross Delinquency Rate

Net Delinquency Rate

1Q18

Average

9.3%

5.7%

4.2%

5.6%

3.3%8.3%

4.3%

1.6%3.2% 2.9%

1Q14 1Q15 1Q16 1Q17 1Q18

Same Area Sales Same Store Sales

7.6% 7.5% 7.6% 7.8% 7.7% 7.6%

5.3% 5.3% 4.9% 5.3% 5.2% 5.2%

12.9% 12.7% 12.6%13.1% 12.9% 12.8%

2013 2014 2015 2016 2017 5-yearaverage

Rent as sales % Other as sales %

3.5%3.0%

2.7% 2.4%

1Q181Q17

May 2018

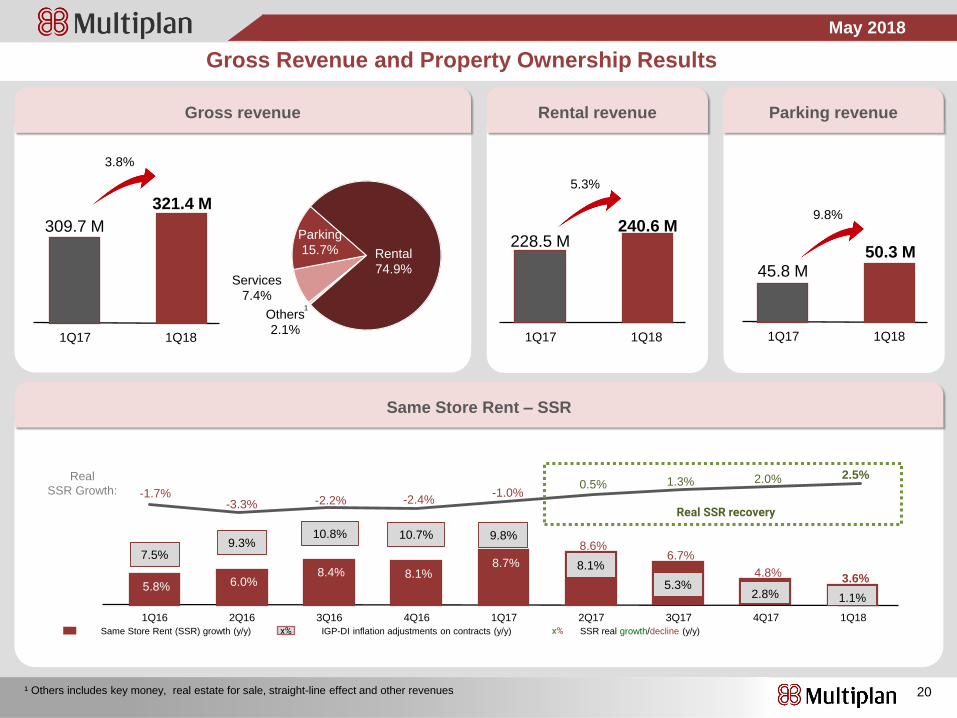

Gross Revenue and Property Ownership Results

20

Rental revenueGross revenue

Same Store Rent – SSR

1Q181Q17

309.7 M

321.4 M

3.8%

Base rent

69.1%

Overage2.5%

Merchand.5.5%

Rental

74.9%

Parking

15.7%

1Q181Q17

228.5 M240.6 M

5.3%

Others

2.1%

Services

7.4%

¹ Others includes key money, real estate for sale, straight-line effect and other revenues

1

Parking revenue

1Q181Q17

45.8 M50.3 M

9.8%

Real

SSR Growth:

5.8% 6.0%8.4% 8.1%

8.7%

8.6%

1Q16 2Q16 4Q16 1Q17 2Q173Q16

SSR real growth/decline (y/y)Same Store Rent (SSR) growth (y/y) x% IGP-DI inflation adjustments on contracts (y/y) x%

3.6%

6.7%

4.8%

-1.7%

7.5%9.3%

10.8% 10.7% 9.8%

8.1%

1.1%5.3%

2.8%

Real SSR recovery-3.3% -2.2% -2.4%

-1.0%0.5% 1.3% 2.0% 2.5%

3Q17 4Q17 1Q18

May 2018

1T17 2T17 3T17 4T17 1T18

Remuneração baseada em ações

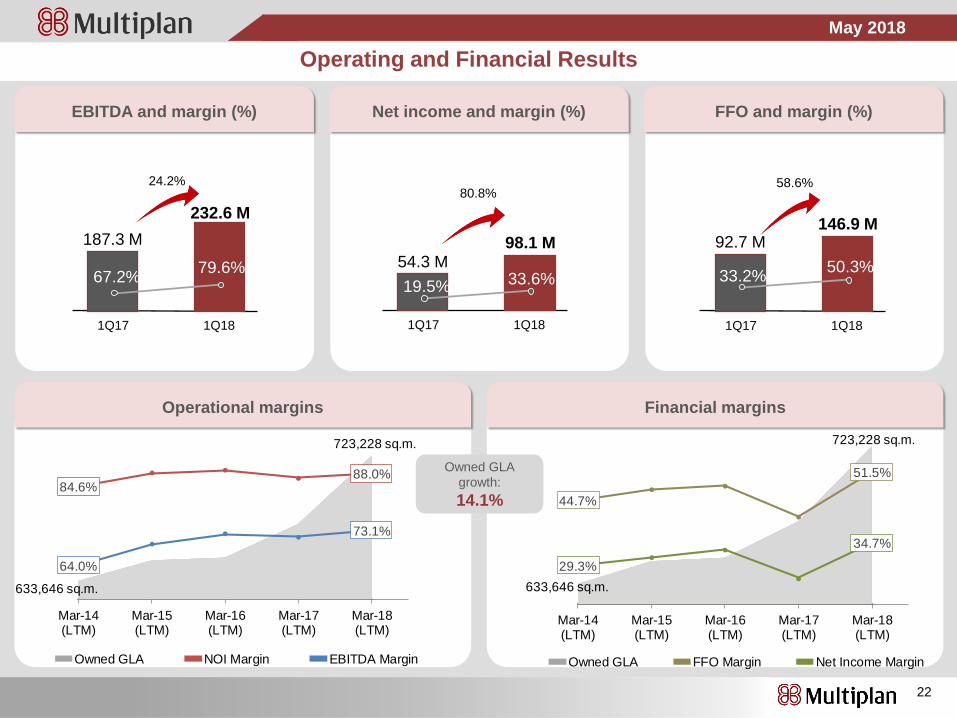

Operating and Financial Results

21

Net Operating Income – NOI and margin

Evolution of G&A and as % of net

revenue

Shopping center expenses and as

% os shopping center revenues1

Share-based compensations and

stock price (R$)

1Q181Q17

31.0 M28.0 M

-9.7%

2016 2017

11.8%10.2%

¹ Mall rental and parking revenues.

26.1 M

(9.1 M)

1Q17 2Q17 3Q17 4Q17 1Q18

3.3 M

24.5 M

1Q181Q17

31.8 M30.5 M

-4.0%

20162017

11.4% 10.5%

707.8 M

879.6 M944.9 M 986.5 M

1,065.2 M

8.0%CAGR: +10.8%

Mar-14

(LTM)

Mar-16

(LTM)

Mar-17

(LTM)

Mar-18

(LTM)

Mar-15

(LTM)

(1.7 M)

66.30 65.32

73.33 70.9068.68

1Q181Q17

251.2 M271.0 M

7.9%

2016

2017

88.6%90.3%

84.6%88.1% 88.8%

86.8% 88.0%

26.1 M

3.3 M

24.5 M

(9.1 M)

(1.7 M)

66.3065.32

73.3370.90

68.68

1Q17 2Q17 3Q17 4Q17 1Q18

Share-based compensations Stock price

May 2018

633,646 sq.m.

723,228 sq.m.

84.6%88.0%

64.0%

73.1%

Mar-14(LTM)

Mar-15(LTM)

Mar-16(LTM)

Mar-17(LTM)

Mar-18(LTM)

Owned GLA NOI Margin EBITDA Margin

Operating and Financial Results

22

EBITDA and margin (%) FFO and margin (%)Net income and margin (%)

1Q181Q17

92.7 M146.9 M

58.6%

2016

2017

33.2%50.3%

1Q181Q17

187.3 M

232.6 M

24.2%

2016

2017

67.2%79.6%

Operational margins Financial margins

1Q181Q17

54.3 M98.1 M

80.8%

2016

2017

19.5% 33.6%

Owned GLA

growth:

14.1%

633,646 sq.m.

723,228 sq.m.

44.7%

51.5%

29.3%

34.7%

Mar-14(LTM)

Mar-15(LTM)

Mar-16(LTM)

Mar-17(LTM)

Mar-18(LTM)

Owned GLA FFO Margin Net Income Margin

May 2018

11.53% 12.29% 12.81%13.09% 13.22% 13.23% 13.50% 13.18%

12.18%10.61%

9.18%8.24%

7.79%

12.75%

13.75% 14.25% 14.25% 14.25% 14.25% 14.25% 13.75%

12.25%

10.25%

8.25%7.00% 6.50%

Mar-15 jun/15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18

Cost of Funding (gross debt) Selic Rate

CDI63.0%

TR34.9%

Others2.1%

Debt Indexes

on March 31, 2018

Lowest Covenant

4.00x

2.39x 2.40x 2.35x 2.34x 2.33x

1.00x

2.00x

3.00x

4.00x

Mar-17 Jun-17 Sep-17 Dec-17 Mar-18

Debt and Cash

23

Evolution of Net Debt to EBITDA Financial expenses and coverage ratio

Weighted average cost of funding (% p.a.)

223.0 M 231.9 M 226.9 M

199.8 M

172.7 M

3.62x 3.55x 3.62x

4.13x

5.04x

Mar-17

(LTM)

Jun-17

(LTM)

Sep-17

(LTM)

Dec-17

(LTM)

Mar-18

(LTM)

Net Financial Expenses EBITDA / Net Financial Expenses

Lowest

Covenant

2.00x

May 2018

Debt and Cash

24

Multiplan’s debt amortization schedule on March 31, 2018

776 M

613 M

294 M

394 M

504 M

437 M

413 M

421 M

120 M

89 M

26 M

26 M

26 M

26 M

26 M

7 M

Cash (Mar-18)

FFO (LTM)

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

1

1 Debt amortization schedule from Apr-18 to Dec-18.

May 2018

IR Contact

Armando d’Almeida NetoCFO and IRO

Hans MelchersInvestor Relations and Planning Director

Franco CarrionInvestor Relations Manager

Leandro VigneroInvestor Relations Analyst

Nathalia BoiseauxInvestor Relations Analyst

Tel.: +55 (21) 3031-5600

Fax: +55 (21) 3031-5322

E-mail: [email protected]

ir.multiplan.com.br