appzen & hackett final webinar slides-2

TRANSCRIPT

Presenters

Susie WestFounder & CEO

sharedserviceslink

Andy FosterVP Consulting Services

AppZen

Bryan DeGrawAssociate Principal, Finance

Advisory ServiceThe Hackett Group

• Send me your question early • Use this opportunity to get the answers/info you seek• The sooner you send me the question, the more likely it will be asked• Remember to stay on for Q&A in the last 10 minutes of the session

Questions

Your copy of the slides

The slides will be available after the webinar at

www.sharespace.digital

Context

If you were to review 100% of spend transactions manually before payment, the process could take weeks. Manual audits routinely happen after payment, but, by then, challenges are very difficult and clawbacks next to impossible.By using AI technology you can audit 100% of spend pre-payment, ensuring manual errors are removed, and duplicate payments, incorrect pricing and fraudulent invoices are discovered before any money has left the business.

Today we will:

• Examine the latest KPIs in P2P published by The Hackett Group for you to compare against• Discuss how Top Performers are “staying ahead” in AP by adopting new technologies to streamline their

processes, save money and drive value back into the business• Learn how AI-powered technology can help you manage your spend auditing, resulting in huge savings and, for

many enterprise companies, significant ongoing cost reductions

Poll

Are you able to identify duplicates in your spend processes?

1) Yes, across all systems

2) Yes, but only within individual systems e.g. receipts duplicated in expense claims

3) Sometimes, but only after both payments have been made

4) No, we find it very hard to spot duplicates at all

Poll

Canyoube100%surethatallcontractuallynegotiateddiscountsarereflectedinyourinvoicing?

1) Yes,we'reverysurewegetallthediscountswe'venegotiated

2)Yes,onthewholewethinkthatdiscountsareshownintheinvoiceswereceive

3)We'renotsurethateverydiscountcomesthrough,butwecertainlyseesome

4)No,wethinkwe'remissingquitealotofdiscounts

Appzen/sharedserviceslink Webcast

June 2020

The Hackett Group | P2P Top Performance

9© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

The Hackett Group measures P2P from an end-to-end process and service delivery model perspective

2019 Purchase-to-Pay Performance Study

§ The study covers a 12-month time period§ Participating organizations are across various industries and

geographies§ The Hackett Group utilizes a rolling sample of companies

and presents new benchmarks every 2 years

Service Delivery Model Components

SupplierMaster Mgmt

Verificationand Approval

InvoicePre-Processing

InvoiceProcessing

Discrepancy Resolution

SupplierPayment

Customer Inquiry and Response File, Store, & Retrieve

Reconciliation, Accrual and Compliance

Purchasing Operations

Accounts Payable

End-to-End Purchase to Pay Process

Requisition & PO Processing Supplier Scheduling Receipt

ProcessingItem Master/ Content

Mgmt Catalog Mgmt Contract Master Mgmt

Pcard Management

Study Methodology

10© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Cost-per-transaction is a primary comparative indicator of process and service efficiency across industries

2019 Purchase-to-Pay Performance Study

Req. & Purchase Order Processing process cost (labor + outsourcing) divided by the number of purchase order and order/blanket release transactions processed annually. 'Purchase orders' relate to ad-hoc purchases only, whereas 'order/blanket releases' are the number of releases (e.g. call-offs, delivery orders placed) against a blanket agreement. Blanket orders, blanket contracts, change orders, etc. are excluded from the transaction count.

Accounts Payable process cost (labor + outsourcing) divided by the number of invoices processed annually. For this metric, 'invoices' includes paper, electronics, and invoiceless ERS transactions. Transactions placed on a p-card without submission of an invoice by the supplier are excluded.

Receipt Processing process cost (labor + outsourcing) divided by the total number of receipts processed annually. Includes both materials and services.

Process Cost per Order Process Cost per Receipt Process Cost per Invoice

$15.10

$4.40

Peer Top Performer

$3.79 $1.53

Peer Top Performer

$4.57 $2.18

Peer Top Performer

11© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Supplier Master Data Management Process Cost per Supplier Master Update

Properly executed, master file maintenance drives information accuracy and purchasing compliance, but each update drives cost

2019 Purchase-to-Pay Performance Study

$12.73

$4.53

Median Top Quartile

Supplier Master Data Management process cost (labor + outsourcing) divided by the number of number of supplier file maintenance entries made annually. 'Maintenance' includes additions, deletions, and identifier field changes (e.g. contact details, bank information, etc.); multiple updates to the same supplier record are counted. Excludes item, catalog, and contract master data management.

12© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Fully-electronic buying means having automated approval workflow and order dispatch across all transaction types

2019 Purchase-to-Pay Performance Study

Electronic Requsitions1 Electronic Purchase Orders2

Electronic PO Change Orders1 Electronic Order / Blanket Releases2

1. Requisitions and PO change orders are considered electronic if they are completed online and approved via internal workflow2. Purchase orders and Order/blanket releases are considered electronic if they are disseminated to the supplier via EDI, Internet, or auto-fax (email is not electronic)

80%100%

Peer Top Performer

36%

96%

Peer Top Performer

64%95%

Peer Top Performer

31%66%

Peer Top Performer

13© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Top Performers use technology to create efficiency across the invoice-to-pay lifecycle and eliminate AP transactions where possible

2019 Purchase-to-Pay Performance Study

E-Invoices(electronic and invoice-less transactions)

Electronic Payments

Electronic includes invoices received in EDI, internet, and file-based formats. Imaged paper invoices are not considered electronic. Invoiceless transactions includes ERS (Evaluated Receipt Settlement), a PO-receipt match where no invoice is received. Purchasing card, travel card / employee expense report, and self-billing transactions are excluded from the metric.

Electronic payment includes EFT/ACH payments and wire transfers. Purchasing card and travel card / employee expense report transactions are excluded from the metric.

30%

85%

Peer Top Performer

55%

84%

Peer Top Performer

14© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

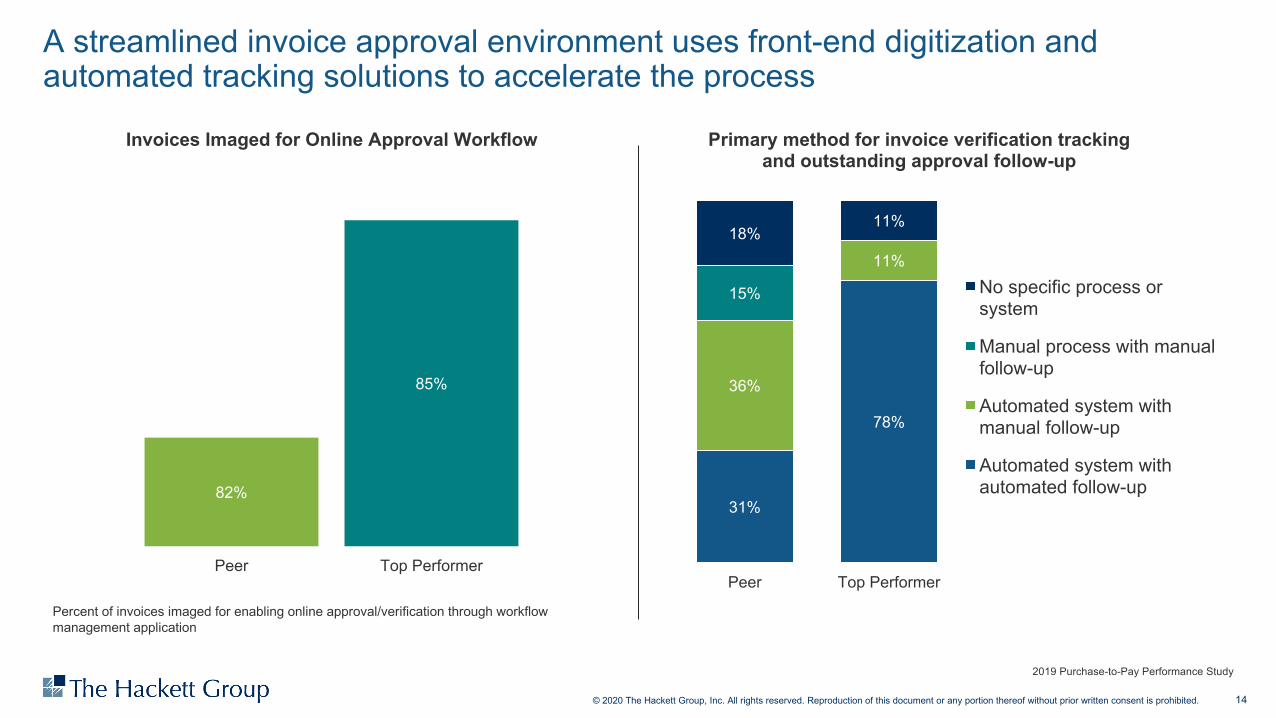

A streamlined invoice approval environment uses front-end digitization and automated tracking solutions to accelerate the process

2019 Purchase-to-Pay Performance Study

Invoices Imaged for Online Approval Workflow Primary method for invoice verification tracking and outstanding approval follow-up

31%

78%

36%

11%

15%

18%11%

Peer Top Performer

No specific process or system

Manual process with manual follow-up

Automated system with manual follow-up

Automated system with automated follow-up

Percent of invoices imaged for enabling online approval/verification through workflow management application

82%

85%

Peer Top Performer

15© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

More efficient invoice processing enables organizations to pay suppliers on time and maximize early-pay discount potential

2019 Purchase-to-Pay Performance Study

Invoice Processing Cycle Time: PO Invoices(in business days)

Invoice Processing Cycle Time: Non-PO Invoices(in business days)

Average number of elapsed business days from the invoice-received-date to when it is authorized-to-pay. Invoice authorization/approval does not mean the payment is actually made, as it may be held until term. The intent is to measure internal processing time. Excludes days that are "waiting to pay" (e.g. invoices held 30 days until payment, due to a conscious working capital decision) and "waiting for receipt" (e.g. in cases where an invoice is received before the actual goods/services).

5.7

3.0

Peer Top Performer

6.5

3.5

Peer Top Performer

16© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Streamlining processes and adopting best practices enable more touchless processing thereby increases the throughput capacity of each FTE

2019 Purchase-to-Pay Performance Study

Orders per FTE Invoices per FTE Receipts per FTE

Purchase order and order/blanket release transactions processed annually divided by the number of full-time equivalents for Requisition & Purchase Order Processing.

Invoices processed annually divided by the number of full-time equivalents for Accounts Payable. For this metric, 'invoices' includes paper, electronics, and invoiceless ERS transactions. Transactions placed on a p-card without submission of an invoice by the supplier are excluded.

Receipts processed annually divided by the number of full-time equivalents for Receipt Processing. Includes both materials and services.

9,846

24,121

Peer Top Performer

15,414

27,202

Peer Top Performer

4,225

14,678

Peer Top Performer

17© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Consistent on-time execution – order creation, delivery, and payment – drives credibility for strategic stakeholder relationships

2019 Purchase-to-Pay Performance Study

After-the-Fact Purchase Orders On-time Payment Rate

Percent of PO lines items that are created "after-the-fact" (i.e., supplier invoice is created before the associated PO). The intent is to measure policy non-compliance. Purchase order is considered non-compliant if the PO creation date is after the invoice date, in violation of the normal/prescribed purchasing processes (i.e. requestor is supposed to get an approved PO issued prior to committing spend).

Percent of payments made on time per organization’s payment policy. The intent is to measure consistency of timely payments, or payments paid differently than supplier expectation. For example, if the buyer has communicated to a supplier that payments will be issued on the 1st and the 15th of the month, a payment is considered on-time if it follows the schedule. However, if an invoice misses the next payment run (1st or 15th) following its due-date because the buyer is resolving invoice discrepancies, the payment would not be considered on time.

3%

1%

Peer Top Performer

82%

88%

Peer Top Performer

18© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

First-pass yield and the underlying causes of PO-invoice mismatch are major indicators of end-to-end process design and quality

2019 Purchase-to-Pay Performance Study

First-Pass Match Rate Which are among the top-3 reasons for first-pass match failure?

Overall first-pass match rate percentage for PO-based invoices. This is the number of entire invoices successfully matched to the PO on the first attempt as a percent of total attempted matches of invoices to POs. A successful first pass match occurs when all required documents are available and the data on the invoice matches the data on the PO (and the receipt if applicable), automatically and without any intervention or rework. Includes all PO invoices e.g., 3-Way-Match (PO, invoice, receipt) or 2-way-Match (PO, invoice for assumed receipt). Only invoices without a PO are excluded from the metric. If the PO and invoice match automatically without needing changes, it should be counted as a first pass match. If the match does not automatically occur, it should not be considered.

65%

60%

44%

42%

37%

6%

4%

4%

2%

12%

Price discrepancy

Quantity discrepancy

No receipt note

No PO

PO related information is not matched

Authorization limit of requestor

Quality of supplied product

Supplier not authorized

Payment terms non-compliance

Other

81%

87%

Peer Top Performer

19© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Tracking inquiry volumes and response times creates a strong stakeholder focus and focus on root-cause eradication

2019 Purchase-to-Pay Performance Study

AP Inquires Received per 10,000 Invoices Percent of AP Inquiries by Resolution Timeframe

40%29%

18%

21%

13% 33%

15%

7%14% 10%

Peer Top Performer

Resolved in more than 48 hours

Resolved within 24-48 hours

Resolved within 24 hours

Resolved on initial contact

Not Tracked (no case management system in place)

The number of inquiries received annually divided by the number of invoices processed annually multiplied by 10,000. For this metric, 'invoices' includes paper, electronics, and invoiceless ERS transactions. Transactions placed on a p-card without submission of an invoice by the supplier are excluded.

Percent of inquiries that were resolved within the given time period after they were initially opened. Resolved on initial contact is a resolution provided at the time of inquiry made by the supplier or requisitioner.

561

332

Peer Top Performer

20© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Self-service inquiry solutions improve efficiency, satisfaction, and responsiveness for suppliers and internal customers

2019 Purchase-to-Pay Performance Study

Self-service users

AP Inquiries by Response Method(for all participants)

AP Inquires Resolved Through Self-service(for companies using self-service tools)

18%

65%

Median Top Quartile

54%

17%

6%

9%

6%

8%

Live on the first call

Self-service on the Internet / Intranet

Automated voice response

Voice-mail, requiring a return call

Other means

Overall

21© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Driving more suppliers to standard payment terms is a first step towards better control over working capital and discount realization

2019 Purchase-to-Pay Performance Study

Percent of Suppliers on "Standard" Terms Percent of Spend on "Standard" Terms

Percent of suppliers and percent of total spend (direct + indirect) for which standard payment terms apply. 'Standard' implies the terms are set by the buyer organization as part of a formal payment strategy rather than a one-off negotiation or dictated by the supplier. 'Standard' may represent a set of standard payment terms depending on region, spend, or supplier category and not necessarily only one actual term.

68%

83%

Peer Top Performer

52%

73%

Peer Top Performer

22© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

33

47

Median Top Quartile

Optimize cash management by ensuring DPO and payment terms mix align with working capital objectives

2019 Purchase-to-Pay Performance Study

10%

38%

12%14%

3%1%

16%

7%

Net 15 Net 30 Net 45 Net 60 Net 90 Net 120 Due upon

receipt

Other

Overall Average

Percent of Spend by Net Payment Term Days Payable Outstanding (DPO)

Percent of total annual spend for which each “net” payment terms apply (even if early-payment discount term is attached to net term). Where regional differences exist, responses reflect company’s global average data.

Average number of days an organization takes to pay an expense, as defined by each company. Typically, DPO equals AP/(COGS/365) or trade payables excluding accrued expenses divided by cost of goods sold per day. An increase in DPO is an improvement, while a decrease is a deterioration.

23© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Discounts offer high savings potential, Top Performers are more likely to have a plan to capitalize on what has been negotiated

11%

5%

16%

0%

27%

41%

30%

30%

20%

0%

0%

20%

Aggressively pursue ALL available discounts and focus on expanding the availability of discounts through supplier negotiations

Aggressively pursue ALL available discounts with little focus on expanding the availability of discounts

Take discounts when earned with no specific goal of taking ALL available discounts

Always take available discounts regardless if paid within discount term

Little focus on taking discounts

No defined strategy for taking discounts

Peer Top Performer

Organization’s Strategy for Taking Early Payment Discounts

Source: Purchase-to-Pay Study, The Hackett Group, 2019

Inte

ntio

nal

Pass

ive

24© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Payment discounts, negotiated by procurement and executed by payables, require end-to-end collaboration to deliver savings

2019 Purchase-to-Pay Performance Study

Early Payment Discounts Taken as a % of Spend Early Payment Discounts Taken as a % of Available

Value of early-payment discounts actually taken as a percent of total spend (direct + indirect). Excludes companies not using early-pay discounts.

Value of early-payment discounts actually taken as a percent of early-payment discounts available. Excludes companies not using early-pay discounts.

0.02%

0.10%

Peer Top Performer

74%

94%

Peer Top Performer

25© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

§ Cost & Cash: Top Performers continue to maintain a significant efficiency advantage, with process costs that are less than half of peer organizations. Likewise, they are better at managing working capital, with 50% more suppliers on standard terms and higher rates of capturing early-pay discounts.

§ Productivity: By streamlining end-to-end processes and supporting the workforce with digital tools, Top Performers require less than half the full-time equivalents (FTEs) of other organizations and are 2.5 times more productive on a per-FTE basis. They also process invoices in 3 fewer business days.

§ Quality: Across several measures of process execution – order compliance, supply assurance, invoice accuracy, etc. – Top Performers exhibit an average of 7% greater quality, enabling the company to more effectively manage its supply chain and build strategic relationships.

§ Channel Strategy: Top Performers limit three-way match and invoice-only purchases where possible, guiding transactions to “optimal” channel paths that balance efficiency and spend control, nearly 2-to-1 relative to peers.

§ Technology: Leveraging a broad toolkit that includes e-catalogs, e-payables, touchless ordering, and self-service, Top Performers have double the adoption rate for impactful automation, compared to peers.

§ Analytics: Line-item purchase detail is electronically captured during the P2P process for 93% of Top Performer spend (compared to 41% for peers). This information drives improved spend analysis, sourcing negotiation, and consumption management.

§ Supply Base: By consolidating purchases with fewer suppliers, managing tail spend, and cleansing the vendor master, Top Performers report 38% fewer active suppliers than peers.

Summary Findings: Hackett’s 2019 P2P Performance Study

2019 Purchase-to-Pay Performance Study

Top performers increasingly apply technology and integrated solutions to conduct checks of invoice quality using machine learning and predictive analytics

67%

87%

33%

0%

32%

53%44%

16%

37%

18%

Ongoing compliance monitoring solution

Core ERP functionality enabled

Manual solution(spreadsheets)

Nothing in place

Top Performer Peer

ADVANCEDBASIC/MANUAL

SYSTEM FUNCTIONALITY TO DETECT AND REPORT ON RECOVERY / ERROR/FRAUD RISKS (PERCENT OF PARTICIPANTS)

Source: Hackett P2P PerformanceStudy© 2019 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited. 2

6

Payment analysis tool

Organizations implement controls and practices to manage compliance across accounts payable

PRACTICES FOR MANAGING COMPLIANCE ACROSSAP(PERCENT OF ALL PARTICIPANTS)

84%

Source: Hackett P2P PerformanceStudy© 2019 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited. 2

7

77%

46%

43%

System edits exist to prevent identical invoice numbers for the same supplier, even when the

invoice dates are different

System controls exist that track payments against a purchase order

Perform post payment review to analyse returned checks that represent duplicate payments to

determine the root cause

Process controls exist requiring original invoices and using copies and faxes only when necessary to

resolve a late payment issue

Accounts payable recoveries by type

26%

16%

15%

10%

9%

7%

7%

4%

5%

Duplicate Payments

Uncollected Credit Memos

Pricing Errors/Overpayments

Purchase Returns

Sales Tax Recovery

Missed Rebates (e.g. volume-based)

Unclaimed Property Escheatment

Missed Early PaymentDiscounts

Other

AP RECOVERIES BY TYPE (AVERAGE)

Source: Hackett P2P PerformanceStudy

Duplicate Payments are the most common types

of Accounts Payable recoveries.

28© 2019 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Payment losses and non-compliant payments that are driving the need for AP recovery audits are due to a number of reasons

§ Organizational, technology and process complexity e.g. different methods for paying vendors, complex contractual agreements, and multiple locations, business units and payment centres

§ High volume of transactions and a large supplier vendor master

§ Use of many service suppliers - Pricing structures for services tend to be more complex than for material purchases

§ Multiple ERP systems are used for payments

§ Roll-out of P-Cards, a new ERP system or implementation of any new system that touch Accounts Payable (increased possibility of duplicate and/or erroneous payments)

§ High levels of Accounts Payable staff turnover or temporary labor

§ Minimal Accounts Payable segregation of duties or decentralised AP operations

§ Significant disruptions or business events such as rapid growth, acquisitions, or transitioning work to a shared service center

Trend: AP recovery audits are widely recognized as a standard tool for process improvement as well a means to recapture lost cash…..However prevention/avoidance technology is quickly becoming an emerging best practice

29© 2019 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

30© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Atlanta | Chicago | Frankfurt | Hyderabad | London | Miami | Montevideo

New York | Paris | Philadelphia | Portland | San Francisco | Seattle | Sydney | Vancouver

For further information about this performance study, please contact:

Bryan DeGraw

Associate PrincipalFinance Advisory Services

+770 225 7238| [email protected]

31© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Statement of Confidentiality and Usage Restrictions

This document contains trade secrets and other information that is company sensitive, proprietary, and confidential, the disclosure of which would provide a competitive advantage to others. As a result, the reproduction, copying, or redistribution of this document or the contents contained herein, in whole or in part, for any purpose is strictly prohibited without the prior written consent of The Hackett Group.

Copyright © 2019 The Hackett Group, Inc. All rights reserved. World-Class Defined and Enabled.

www.thehackettgroup.com

Reproduction of this document or any portion thereof without prior written consent is prohibited.

32© 2020 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Poll

Are you confident that you pick up all potential compliance violations in your AP process?

1) Yes, 100% of our payments are compliant with external regulations and internal policy

2) Yes, but our focus is on external regulations rather than internal policy

3) Yes, but our focus is on internal policy rather than external regulations

4) No, we have compliance concerns in our AP process

Copyright @ 2020 AppZen, Inc. | All rights reserved.

Audit 100% of Spend with Artificial Intelligence

33

Copyright @ 2020 AppZen, Inc. | All rights reserved.

Becoming a Top Performer…..

• Eliminate duplicates and other invoicing errors such as incorrect pricing

• Implement controls and practices to manage compliance across accounts payable

• Payment discounts require end-to-end collaboration to deliver savings

• Touchless processing to increase the throughput capacity of each FTE

• Why AppZen recommend Discovery, rather than Recovery, audit

……requires controls and checks across the entire purchase-to-pay process

34

35

Finance teams are under pressureq Contain costs with fast-turn projects

q Find operational efficiencies

q Adapt to remote work

36

Spend control with AIq Review, understand and validate

every line of every transaction, before payment

q Automate & accelerate processes

q Real-time, line-level visibility across 100% of spend

q AI that sits along side existing investments in AP Automation

Copyright @ 2020 AppZen, Inc. | All rights reserved.

What do Top Performers aim to eliminate from their AP?

37

Copyright @ 2020 AppZen, Inc. | All rights reserved.

5 problems that Top Performers aim to eliminate

38

Duplicates Compliance issues Missing discounts

Incorrect payment terms Incorrect pricing

1 2 3

4 5

Copyright @ 2020 AppZen, Inc. | All rights reserved.

1a. Duplicates

39

$1,142.40 duplicate payment between invoice and expense systems

Copyright @ 2020 AppZen, Inc. | All rights reserved.

1b. Duplicates

40

Duplicate invoices billed by two different subsidiaries

• German invoice

$4,477.29

German invoice

UK invoice

Copyright @ 2020 AppZen, Inc. | All rights reserved.

2. Compliance issues

41

Invoice from debarred entity

Copyright @ 2020 AppZen, Inc. | All rights reserved.

3. Missing discounts

42

Overcharged by $3,000 per quarter

42

Copyright @ 2020 AppZen, Inc. | All rights reserved.

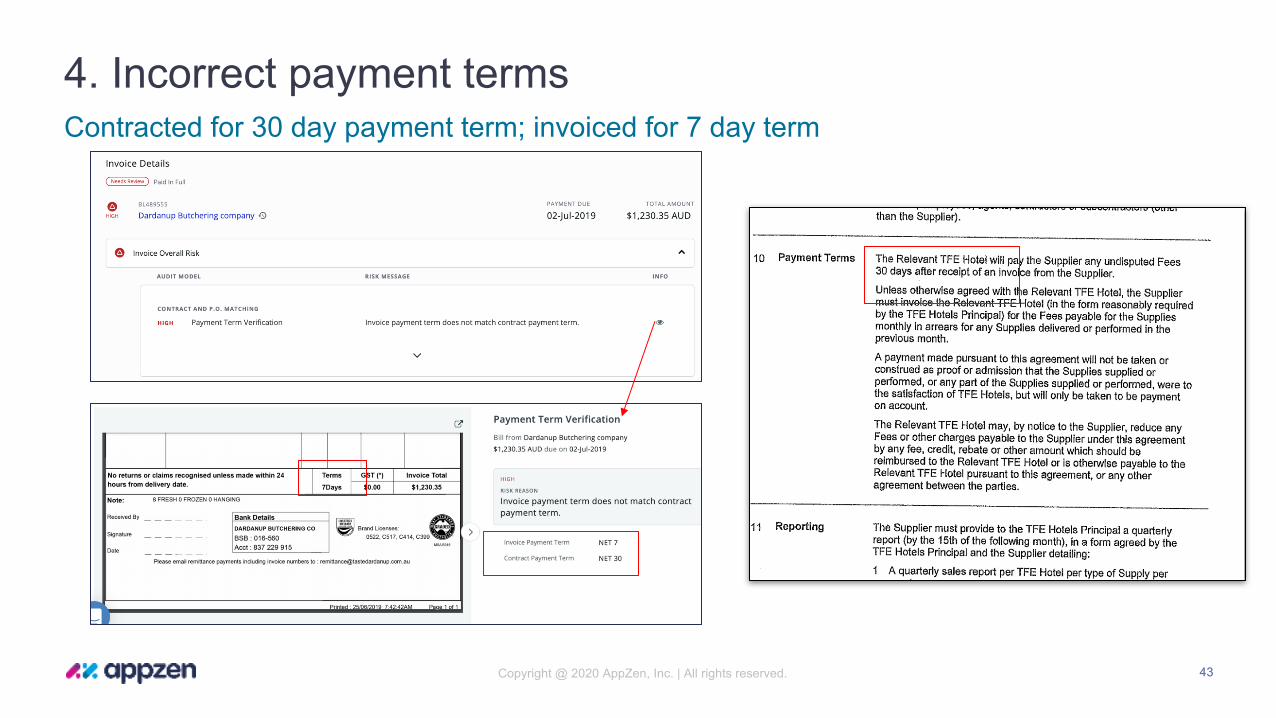

4. Incorrect payment terms

43

Contracted for 30 day payment term; invoiced for 7 day term

43

Copyright @ 2020 AppZen, Inc. | All rights reserved.

5. Incorrect pricing

44

Invoice price more than double the contracted price

• \Invoice Discrepancy ID’d by

AppZen

Price list

Copyright @ 2020 AppZen, Inc. | All rights reserved.

How we do it

45

Copyright @ 2020 AppZen, Inc. | All rights reserved.

1 2 3 4Understand documents

Enrich with intelligence

Assess and refine risk

Streamline process

How AppZen makes it possible

Copyright @ 2020 AppZen, Inc. | All rights reserved.

AppZen platform

47

S P E N D V A L I D A T I O N & A U T O M A T I O N100% of expenses & AP before you pay

P L A T F O R M

I N S I G H T S

Invoices Contracts Purchase Orders Packing slips Loan documents

Receipts CC statements P card statements Bank statements Commission

forms

Expense AP

Copyright @ 2020 AppZen, Inc. | All rights reserved.

AppZen fits seamlessly into your existing AP investment

48

100% Real-time

Audit

Assessand Assign

Risk

Spend automation

system

High risk: Major violations that need a human level review

Route back to employee or supplier

with reason

Internal review

Medium risk: Minor violations and/or approved risk

Auto-approved

Low risk: No violations found

Proceed to

payment

Auto-approved

Expense report and invoice submitted

Manually approve

for payment

Copyright @ 2020 AppZen, Inc. | All rights reserved.

Value of an AI driven approach

4949

REDUCE SPENDFind errors, waste and fraud,

before you pay

COMPLY WITH POLICYComply with corporate policy,

contracts and regulations

STREAMLINE PROCESSAutomatically ingest, classify, and

approve low-risk spend, erase complexity, and pay on time

Copyright @ 2020 AppZen, Inc. | All rights reserved.

One third of the Fortune 500 transform spend with AppZen

50

+1,650enterprise customers

+1,800customers

50B+audited spend

40+countries audit

coverage

Your Questions Answered

NextFromsharedserviceslinkwww.sharespace.digital

January23rdJanuary16th January30th

January23rdJanuary16th January30th

We want to hear how your organization is adapting!

We want to explore:• What have been the biggest impacts to finance, compliance and

shared services professionals?• Whether companies are seeing increase in attempts of fraud in

the supply chain.• What changes companies are making to working capital and

early payment programs• Has this event been a catalyst to automate and move away from

paper?

Covid-19 and Shared Services: How are you Responding?

Nearly everything is changing. Business strategies are evolving, and everyone is having to adapt.

We have seen a huge amount of resilience from shared services professionals – from working remotely, to adapting processes and doing what it takes to keep companies open for business.

Covid-19 and Shared Services: How are you Responding?

Are you happy to participate in our current study on P2P and Fraud? (It only takes 5 minutes and is multiple choice)

1) Yes – please call me and ask the questions

2) Yes – please email me the link

3) No thanks