applied corporate finance - wordpress.com · disclaimer the contents of this course are inspired by...

TRANSCRIPT

Applied Corporate Finance

Unit 1

Introduction to Corporate Finance

• Principles of Corporate Finance – real world focus• Objectives in Decision making

• Choosing the right objective• Classical Objective• Maximize Stock prices• Alternatives to Stock Price Maximization

• The Limits of Corporate Finance

Disclaimer

The contents of this course are inspired by Prof Aswath Damodaran’s course on AppliedCorporate Finance. The examples and contents have been suitably modified for thestudents at RVS IMSR. We would however thank Prof Damodaran for making his materialavailable on the web for all learners. Some of the slides used have the content from Prof.Damodaran’s slides.

What is Corporate Finance?

Everything that a business does, has financial implications. Thus any decision that affectsthe financials of a business is a Corporate Finance Decision.

What is Corporate Finance?

There are three major decision points in Corporate Finance• The Investment Decision• The Financing Decision• The Dividend Decision

What is Corporate Finance?

The Investment Decision

• Resources in any business are limited, while opportunities unlimited. The decision to deploy these resources is the investment decision

The Financing Decision

• Where do we raise money from for the investments?

• What should be the debt and equity mix

The Dividend Decision

• How much of a firm’s funds should be reinvested in the business and how much should be returned to the owners?

The View of a Firm

Assets in Place

Debt

Growth Assets

Equity

Assets Liabilities

The View of a Firm

Assets in Place

Debt

Growth Assets

Equity

Assets Liabilities

Assets that the company has already invested into

Expected Value to be created from growth via investments

Fixed Claim on cash flows, usually with fixed maturity

Residual Claim on cash flows, usually perpetual

First Principles

The Investment DecisionInvest in assets that earn a

return greater than the minimum acceptable hurdle

rate

The Financing DecisionFind the right kind of debt for your firm and the right mix of debt and equity to

fund your operations

The Dividend DecisionIf you cannot find investments

that make your minimum acceptable rate, return the cash

to owners of your business

The hurdle rate should reflect the riskiness of the investment and the mix of debt and equity used

to fund it.

The return should reflect the magnitude and the timing of the

cashflows as welll as all side effects.

The optimal mix of debt and equity

maximizes firm value

The right kind of debt

matches the tenor of your

assets

How much cash you can

return depends upon

current & potential

investment opportunities

How you choose to return cash to the owners will

depend on whether they

prefer dividends or buybacks

Maximize the value of the business (firm)

Source: Applied Corporate Finance, Aswath Damodaran

Questions

• Discuss the major decision points in Corporate Finance.• What are growth Assets?

Applied Corporate Finance

Unit 1

The Objective in Decision Making

In traditional corporate finance, the objective in decision making is to maximize the value of the firm. A more specific objective is to maximize stockholder wealth. When the stock is traded and markets are viewed to be efficient, the objective is to maximize the stock price.

The Objective in Decision Making

Assets in Place

Debt

Growth Assets

Equity

Assets Liabilities

Assets that the company has already invested into

Expected Value to be created from growth via investments

Fixed Claim on cash flows, usually with fixed maturity

Residual Claim on cash flows, usually perpetual

The Criticism

• Many critics believe that the objective of maximizing stock prices is not in cohesion with employee welfare – For example, when some companies announce job cuts, or fire employees, stock prices jump because of rationalization of costs.

• Another criticism is that to maximize stock prices, you will have to care less about customer satisfaction. • There is also criticism that in a bid to maximize stock prices, the company will care less about society in

general.

The Support

• Companies which are successful over the longer run are likely to have happy employees, and happy customers. In the longer run, it s difficult to have a successful company that does not care about employees and customers.

• Companies which do not care about society also face bans, penalties etc in the long run, which reduce shareholder wealth. So to maximize shareholder wealth, the company will have to follow best practices according to the society.

• Finally, fuzzy objectives do not work. We have to be clear in stating the objective of the success of a company. Stock prices work well there, since they give instantaneous feedback.

• It is also most easily observable and constantly updated.

Stock Prices give fast feedback

Can we have another objective?

Firms can always focus on a different objective function. Examples would include• maximizing earnings• maximizing revenues• maximizing firm size• maximizing market share• maximizing EVA

Note the impact of these functions. Most of them seem to be means rather than ends. To the extent these objectives fit in to the longer term value of the company, they work well. For example, if you give away services for free, you will make a market share, but how will you continue the business – example – Air DeccanIf your idea is maximization of market share, there is a huge cost attached to it – Flipkart, e-commerce

So we return to our objective function

Source: Applied Corporate Finance, Aswath Damodaran

Managers

Stock Holders

Society

Financial Markets

Bond Holders

Hire & fire managers- Board- Annual Meeting

Maximizestockholder wealth

Lend Money

ProtectbondholderInterests

Reveal informationhonestly and on time

Markets are efficient and assess effect onValue

No Social Costs

All costs can be traced to firm

But in reality things can go wrong

Source: Applied Corporate Finance, Aswath Damodaran

Managers

Stock Holders

Society

Financial Markets

Bond Holders

Have little control over managers

Managers put their interests over stockholders

Lend Money

Bondholders are not protected.

Do not reveal information correctly

Markets are not efficient and make mistakes

High Social Costs

Some costs cannot be traced to firm

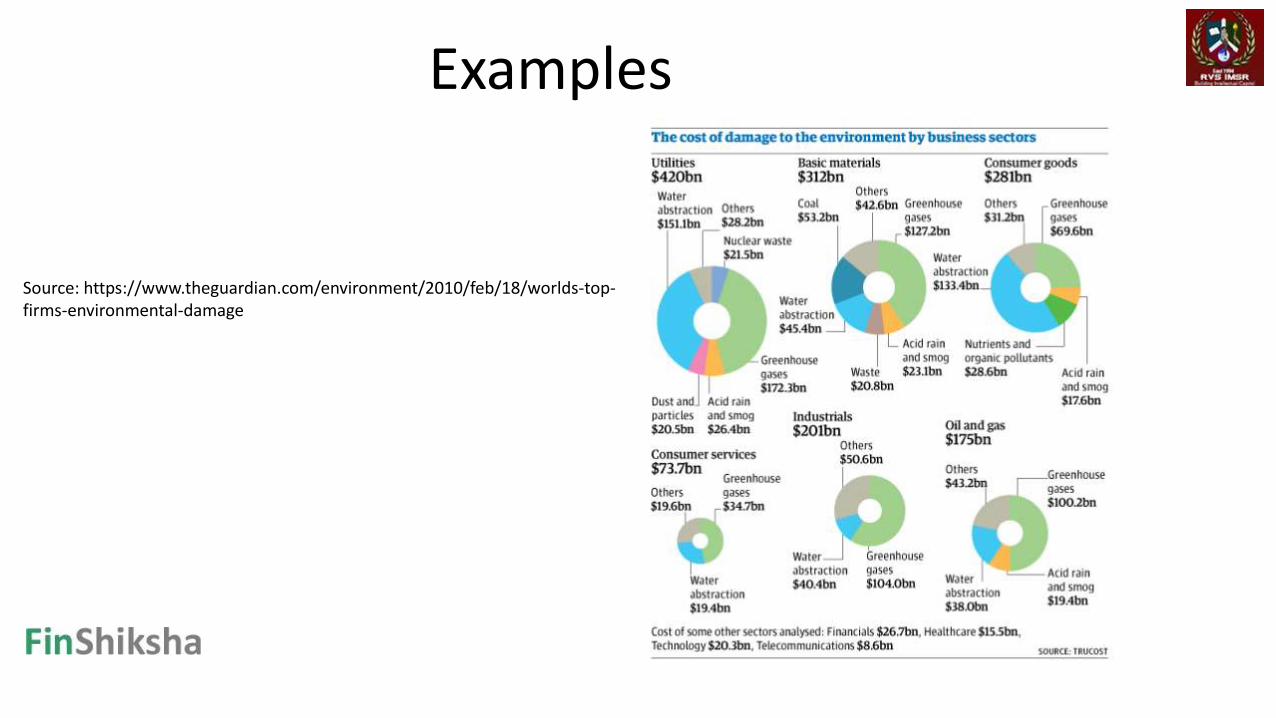

Examples

• Stockholders having little control over managers• Bondholders are left unprotected• Provide misleading information to markets, or markets react incorrectly to information• Huge societal costs

Examples

Examples

Source: https://www.theguardian.com/environment/2010/feb/18/worlds-top-firms-environmental-damage

Questions

• Discuss why stock price maximization is the best objective function to have• Discuss how relationships in the objective function for corporate finance can go wrong

Applied Corporate Finance

Unit 1

Stockholders vs Managers

Ideally, the stockholders can control the managers in theory in the following 2 ways• A Board of Directors is working on behalf of the shareholders to ensure that managers

act in the best interest of the shareholders• The stockholders can act during the annual general meeting of companies, and use

their voting rights to ensure that managers act in their best interests.

Stockholders vs Managers

Ideally, the stockholders can control the managers in theory in the following 2 ways• A Board of Directors is working on behalf of the shareholders to ensure that managers

act in the best interest of the shareholders• The stockholders can act during the annual general meeting of companies, and use

their voting rights to ensure that managers act in their best interests.

However, in real life – this may not work.

Stockholders vs Managers

Some of the reasons this may not work is• The Board of Directors is made up of shareholders who are related to the management.

After all, who chooses the Board of Directors? In most cases, the promoter is also themanagement, and why would they want to have a Board overseeing everything theydo.

• Most small stockholders do not go the Annual Meetings• Annual meetings are also tightly scripted and controlled events, making it difficult for

outsiders and rebels to bring up issues that are not to the management’s liking

Stockholders vs Managers

The problems with the Board of Directors is• The Board of Directors is made up of shareholders who are related to the management.• The CEO is the head of the Board, so the Board cannot make a decision that overrules

the CEO• The compensation committee and audit committee are also appointed by the

management in many cases (one of the ways management can work against theshareholders is by fixing high salary for management, thereby reducing profits forshareholders)

• The Directors serve on multiple companies, reducing the amount of time they canspend on one company.

Stockholders vs Managers

One of the easiest and quickest ways for the management to take away money fromshareholders is to go for an expensive acquisition.• Time and again we have examples when companies go overboard while making an

acquisition, only to lose money later.

Stockholders vs Managers

Great Offshore acquisition byBharati Shipyard

Source: http://www.rediff.com/money/report/abg-to-counter-bharati-bid-for-great-offshore/20090918.htm

Stockholders vs Managers

Great Offshore acquisition byBharati Shipyard

Stockholders vs Managers

Great Offshore acquisition byBharati Shipyard

Stockholders vs Bondholders

• In theory: there is no conflict of interests between stockholders and bondholders.• In practice: Stockholder and bondholders have different objectives. Bondholders are

concerned most about safety and ensuring that they get paid their claims. Stockholders are more likely to think about upside potential

Stockholders vs Bondholders

So how can managers work against the bondholders • A huge dividend or buyback may take cash out of the firm, making it riskier. This could be

against the best interest of the bondholders• When a firm takes riskier projects than those agreed to at the outset, lenders are hurt.

Lenders base interest rates on their perceptions of how risky a firm’s investments are. If stockholders then take on riskier investments, lenders will be hurt.

• It is in the benefit of stockholders to take excessive risks – they get paid to do so, and have limited liability. But not so for bondholders

Stockholders vs Bondholders

So how can managers work against the bondholders • A huge dividend or buyback may take cash out of the firm, making it riskier. This could be

against the best interest of the bondholders• When a firm takes riskier projects than those agreed to at the outset, lenders are hurt.

Lenders base interest rates on their perceptions of how risky a firm’s investments are. If stockholders then take on riskier investments, lenders will be hurt.

• It is in the benefit of stockholders to take excessive risks – they get paid to do so, and have limited liability. But not so for bondholders

Stockholders vs Bondholders

Source: http://zeenews.india.com/business/news/companies/shocking-banks-can-recover-just-rs-6-crore-out-of-rs-7000-crore-loan-lent-to-kingfisher_1856241.html

Stockholders vs Bondholders

Source: http://www.economist.com/node/14921343

Questions

• Explain how can managers work against the shareholders of the company. Give an example

• Explain how the objectives of shareholders and bondholders are different

Applied Corporate Finance

Unit 1

Firms and Financial Markets

Source: http://www.livemint.com/Companies/LYCML5Yyyb8E8AYUIAc2HJ/Bharati-ABG-surge-on-Great-Offshore-open-offer.html

Firms and Financial Markets

• In theory: Financial markets are efficient. Managers convey information honestly and and in a timely manner to financial markets, and financial markets make reasoned judgments of the effects of this information on 'true value'. As a consequence-o A company that invests in good long term projects will be rewarded.o Short term accounting gimmicks will not lead to increases in market value.o Stock price performance is a good measure of company performance.

• In practice: There are some holes in the 'Efficient Markets' assumption.

Firms and Financial Markets

Why is actual experience different?

That is because sometimes the firms manage the information given out to markets (such asdelay bad news) and sometimes they resort to give misleading or incorrect information.

The second problem is with the investor reaction to news. There tends to be overreaction –on either side. We have to be aware of such limitations.

Finally, there seems to be evidence of insider trading – that is, company insiders may tradeon news before it is made public. This is however illegal.

Firms and Financial Markets

However, what works in the favour of markets, is the following

Fast reaction or overreaction to news is better than some other metrics which may notreact to news at all. For example, a news of a merger will have no impact on any othermetric like profits or sales in the immediate term.

Also, someone has to make this judgement, on whether the news is good or bad. Marketsmay be imperfect, but they do this better than managers or governments.

Firms and Financial Markets

And while markets are considered more short term in nature – they are supposed tooverreact to news, the following points tell that markets may be able to look beyond theshort run

1. The market is able to value small and young companies, even though they may not haveenough revenues or profits today. This shows that markets can look in the long run

2. Markets reaction to investments in R&D is usually good. Markets reaction toinvestments also points to the fact that they are able to look beyond the short term.

Firms and Society

• In theory: All costs and benefits associated with a firm’s decisions can be traced back tothe firm.

• In practice: Financial decisions can create social costs and benefits.• A social cost or benefit is a cost or benefit that accrues to society as a whole and not

to the firm making the decision. Environmental costs (pollution, health costs, etc..) Quality of Life' costs (traffic, housing, safety, etc.)

• Examples of social benefits include: creating employment in areas with high unemployment supporting development in inner cities creating access to goods in areas where such access does not exist

Firms and Society

However, socials costs may be difficult to quantify• For example – what is the quantified impact on society on account of tobacco / cigarette

smoking. How much of it would have happened even without ITC selling cigarettes?Have they actually increased it, or reduced it, since the user may have otherwiseresorted to using unregulated tobacco sources.

• Eyes of the beholder: They are ‘person-specific’, since different decision makers can lookat the same social cost and weight them very differently.

• Cannot know the unknown: The costs may not be known at the time of the decision. Inother words, a firm may think that it is delivering a product that enhances society, at thetime it delivers the product but discover afterwards that there are very large costs. Forexample – nuclear power.

Tradition Corporate Finance Break Down

Traditional corporate financial theory breaks down when• Managers look at their interest first and firm interest later.• Bondholders are not protected against shareholders• Financial markets do not operate efficiently, and stock prices do not reflect the

underlying value of the firm.• Significant social costs can be created as a by-product of stock price maximization.

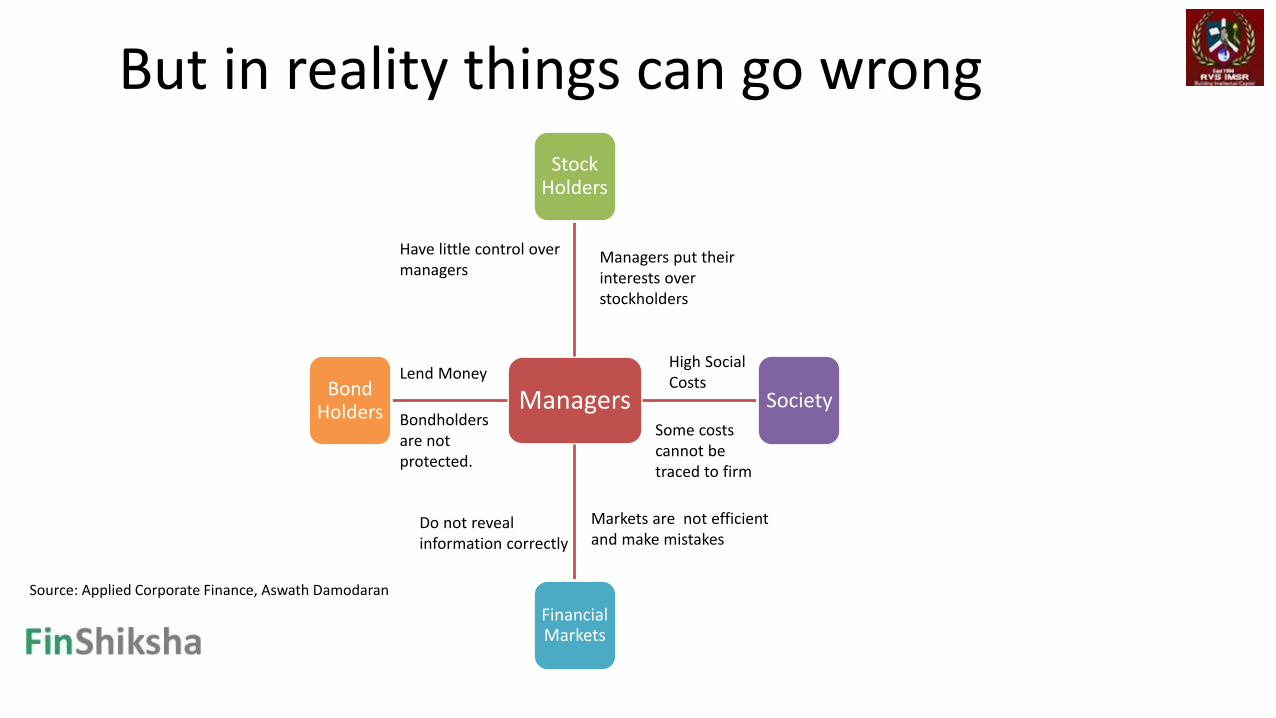

But in reality things can go wrong

Source: Applied Corporate Finance, Aswath Damodaran

Managers

Stock Holders

Society

Financial Markets

Bond Holders

Have little control over managers

Managers put their interests over stockholders

Lend Money

Bondholders are not protected.

Do not reveal information correctly

Markets are not efficient and make mistakes

High Social Costs

Some costs cannot be traced to firm

Self correcting mechanisms

Source: Applied Corporate Finance, Aswath Damodaran

Managers

Stock Holders

Society

Financial Markets

Bond Holders

1. More activist investors2. Hostile takeovers

Managers of poorly run firms are puton notice.

Protect themselves

New Bond Covenants

Firms are punishedfor misleading markets

Investors and analysts become more skeptical

Corporate Good Citizen Constraints

1. More laws2. Investor/Customer Backlash

Questions

• Explain what is the criticism of the relationship between the firm and the markets• Explain why it is difficult to quantify the impact of the firm’s business on the society.