appendix c-1. appendix c-2 appendix c using financial calculators intermediate accounting principles...

TRANSCRIPT

Appendix C-1

Appendix C-2

APPENDIX C

USING FINANCIAL CALCULATORS

INTERMEDIATE ACCOUNTING

Principles and Analysis

2nd Edition

Warfield Wyegandt

Kieso

Appendix C-3

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Illustration C-1Financial calculator keys

N = number of periods

I = interest rate per period

PV = present value

PMT = payment

FV = future value

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-4

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

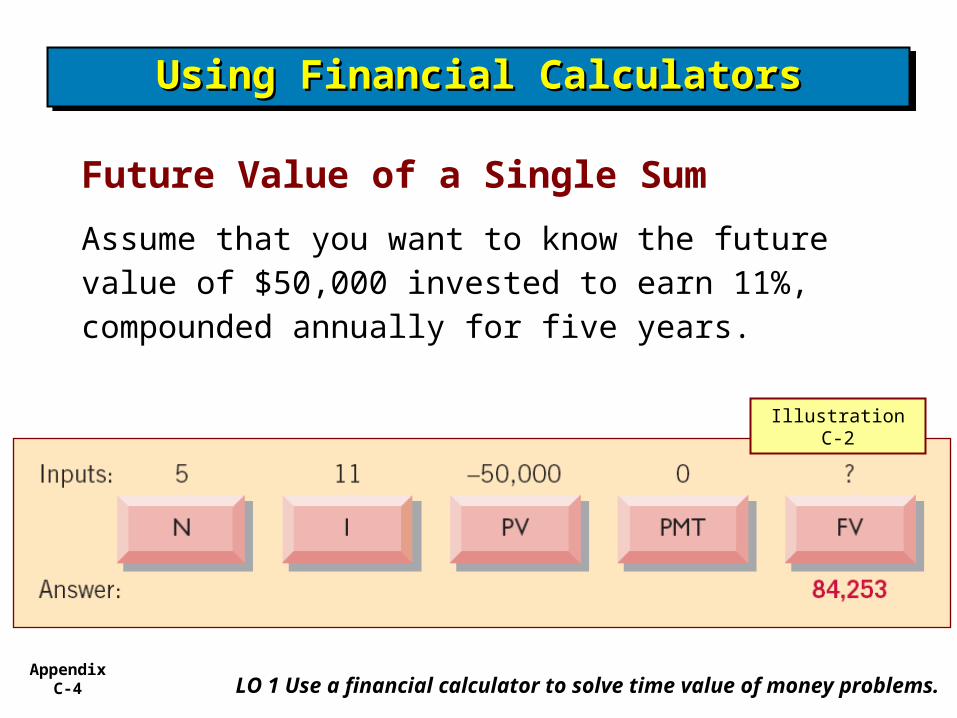

Future Value of a Single Sum

Assume that you want to know the future value of $50,000 invested to earn 11%, compounded annually for five years.

Illustration C-2

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-5

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Present Value of a Single Sum

Assume that you want to know the present value of $84,253 to be received in five years, discountedat 11% compounded annually.

Illustration C-3

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-6

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Future Value of an Ordinary AnnuityAssume that you are asked to determine the

future value of five $5,000 deposits made at the end of each of the next five years, each of which earns interest at 12%, compounded annually.

Illustration C-4

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-7

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Future Value of an Annuity DueAssume Sue plans to deposit $800 per year on her son’s birthdays, starting today (his tenth birthday). Amounts on deposit will earn 6% compounded annually. What amount will have accumulated by Sue’s son’s eighteenth birthday. (Assume no deposit will be made on the eighteenth birthday.)

Illustration C-5

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-8

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Present Value of an Ordinary AnnuityAssume that you are asked to determine the

present value of rental receipts of $6,000 each to be received at the end of each of the next five years, when discounted at 12%.

Illustration C-6

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-9

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Useful Applications – Auto Loan

The loan has a 9.5% nominal annual interest rate, compounded monthly. The price of the car is $6,000, and you want to determine the monthly payments, assuming that the payments start one month after the purchase.

Illustration C-7

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-10

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Useful Applications – Auto Loan - NoteIf your solution was -592.59 your financial calculator is set for annual versus monthly values of I (C/Y=1, P/Y=1). You can “manually” insert I as 9.5/12 =, which results in 0.79167.Monthly payments requires payments to be set as P/Y=12, monthly interest compounding requires compounding to be set to C/Y=12. Illustration C-7

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-11

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Useful Applications – Mortgage LoanYou decide that the maximum mortgage

payment you can afford is $700 per month. The annual interest rate is 8.4%. If you get a mortgage that requires you to make monthly payments over a 15-year period, what is the maximum purchase price you can afford? Illustration C-8

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-12

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Useful Applications – Mortgage LoanYou decide that the maximum mortgage

payment you can afford is $700 per month. The annual interest rate is 8.4%. If you get a mortgage that requires you to make monthly payments over a 15-year period, what is the maximum purchase price you can afford? Illustration C-8

LO 1 Use a financial calculator to solve time value of money problems.

Appendix C-13

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Useful Applications – Individual Retirement Account (IRA)Assume you opened an IRA on April 15, 2006, with a deposit of $2,000. Since then you have deposited $100 in the account every two weeks with the first $100 deposit made on April 29, 2006. The account pays 7.6% annual interest compounded semi-monthly. How much will be in the account on April 15, 2016?

LO 1 Use a financial calculator to solve time value of money problems.

43,129.39

Illustration C-9

Appendix C-14

Using Financial CalculatorsUsing Financial CalculatorsUsing Financial CalculatorsUsing Financial Calculators

Useful Applications – Individual Retirement Account (IRA)The solution to this problem requires payments (P/Y) to be set to 26 while interest compounding periods (C/Y) be set to 24.

LO 1 Use a financial calculator to solve time value of money problems.

43,129.39

Illustration C-9

Appendix C-15

Copyright © 2008 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

CopyrightCopyrightCopyrightCopyright