apoorva javadekar - my comments on bori verdelhan

TRANSCRIPT

Sovereign Risk Premia(Nicola Borri and Adrien Verdelhan)

Presented byApoorva Javadekar and Jean Fleming

April 19, 2012

Introduction - Motivation

I Sovereign bonds’ excess returns are related to their quantitiesof risk

I Emerging countries tend to default in bad times; if bad timesin the borrowing country overlap with bad times in the lendingcountry, then sovereign bonds are even more risky

I Risk averse lenders are a more plausible assumption than therisk neutrality assumed previously in the literature

Sovereign Risk Premia - 2/29

Introduction

I Lenders’ risk aversion implies that optimal borrowing anddefault decisions by emerging countries depend on both theborrowing and lending countries’ economic conditions

I As risk aversion of lenders and the correlation of businesscycles in the two countries increase:

I The risk premium and the interest rate on sovereign bondsincrease

I Borrowing becomes less attractive to the emerging country

Sovereign Risk Premia - 3/29

Introduction - Contribution

I If investors were risk neutral, the average excess return wouldbe 0, but the data shows that countries with high defaultprobabilities return about 5% more than countries with lowdefault probabilities)

I This paper extends the Eaton & Gersovitz (1981) model byadding

I Heterogeneity in borrowing countries’ correlations with thelending country’s business cycle

I Time varying risk aversion in lending country’s representativeagent (CC habit)

Sovereign Risk Premia - 4/29

Introduction - Model

I Each period, borrowing country decides to default and beexcluded from credit markets or to repay its debts and be ableto borrow again

I As lending country experiences negative consumption shocks,consumption decreases toward habit level and risk aversionincreases ⇒ risk premia and interest rates increase ⇒borrowing becomes more costly, so borrowers will default assoon as they experience a negative shock

I If shocks are positively correlated, the bond yield increasesand price decreases

I Bond issuances and defaults are endogenous in the model: asthe cost of borrowing (bond yield) increases → the amount ofborrowing decreases → the probability of default decreases

Sovereign Risk Premia - 5/29

Data

I US investor’s self-financed portfolio: borrows in $, invests indollar denominated sovereign bonds from emerging economies

I Bonds: JP Morgan emerging market bond index (EMBI)I total returns on a weighted aggregate of dollar denominated

bonds that are actively traded, at least 1 year left to maturityI 36 countries, daily data from Dec 1993 to May 2009

I Default Probabilities: S&P credit ratings - from AAA+ toDDD-, SD

I Get ratings for all 36 countries in EMBI and rank them from 1(best rating) to 23

Sovereign Risk Premia - 6/29

Notation

I log excess return on country i ’s bond can be written asr e,it+1 = pit+1 − pit − r ft

I regress excess return on US BBB corporate bond excessreturn:

r e,it+1 = αi + βiEMBI re,BBB + εt

I βi is ”bond beta,” used to construct portfolios

Sovereign Risk Premia - 7/29

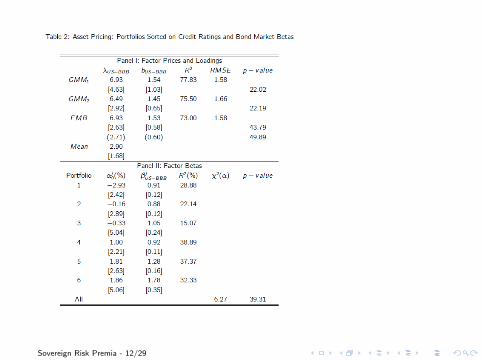

Portfolio Regressions

Build portfolios of 36 emerging countries by sorting by probabilityof default (L,M,H) and bond β (L,H) ⇒ 6 portfolios total - 1,2,3have low β

I Rebalance portfolios at the end of each month

I r e,jt+1 = excess return on portfolio j

I Portfolios show that r e ↑ as β ↑ and as the probability ofdefault ↑

I as default probability increases, bootstrapped distribution ofportfolio returns become farther from normal, but the samepattern is not apparent as β increases

Sovereign Risk Premia - 8/29

Sovereign Risk Premia - 9/29

Asset Pricing Theory

Factor model of asset pricing - average excess returns can beexplained by risk premia on factors

I By NA, Et(Mt+1Re,jt+1) = 0

I The log SDF can be written as mt+1 = 1− b(ft+1 − µ)linear in factors ⇒ beta pricing model

I ft+1 is one-dimensional in the model = log total return onMerrill Lynch US BBB corporate bond index

I Let λ be the factor price (market price of risk). ThenE (r̃ e,j) = λβj

Sovereign Risk Premia - 10/29

Asset Pricing Results

I Estimate λ and β by GMM and 2 stage OLS

I Market price of risk ≈ 6.93% per year (significant)

I Cross sectional R2 ≈ 73%

I Cannot reject that pricing errors are 0

I Since ft is also a return, the NA equation should also hold forUS BBB corporate bonds ⇒ β = 1 on factor, but this gives ahigher λ than when regressing the j portfolio returns, thoughnot significantly ⇒ cannot reject NA

Sovereign Risk Premia - 11/29

Sovereign Risk Premia - 12/29

Asset Pricing Results

I Recall r e,jt+1 = αj + βjBBB re,BBB + εt

I Estimate αj and βjBBB by OLS

I Cannot reject that αj ’s are jointly zero, but all are small andindividually not significantly different from zero

I As default probability increases, β estimate increases

Sovereign Risk Premia - 13/29

Robustness check

I Country-level results - estimate λ, β, αi , βi for all 36 countries,find that results from portfolio regressions still hold

I Conditional Euler equation - previous regressions assumedexpectation was unconditional, but can writeEt(Mt+1R

e,jt+1) = 0 as E (Mt+1ztR

e,jt+1) = 0 where zt is the

investor’s information set at time t (VIX)

I Multiplying returns and risk factor by zt generates 6 newportfolios, and estimating λ as before shows that λ is timevarying and increases in bad times - can be interpreted astime varying risk aversion or low market liquidity

Sovereign Risk Premia - 14/29

Liquidity or Credit Risk?

I add 2 more risk factors: ∆ log VIX index and TED spread -both proxies for liquidity risk

I Find that both factors have a negative and significant affecton λ, but only explain a small share of the cross section ofreturns

I R2 is lower that using BBB as the only factor, and still cannotreject that pricing errors αj are jointly zero

I Conclude that we cannot rule out liquidity risk as anexplanation of EMBI returns, but it is more likely to be acredit risk explanation with time varying risk aversion

Sovereign Risk Premia - 15/29

Model - Motivation

I Result: Countries with high Bond betas offer higher excessreturns on sovereign bonds

I Why? Higher betas imply positively correlated business cycleswith USA, which makes bonds risky for US investor.

I A macroeconomic dynamic model to understand timevariation in risk premia, and link between lender’s risk aversionand default decisions.

I Objective: Study the behaviour of simulated model andmatching it with the data.

Sovereign Risk Premia - 16/29

Model - Set-Up

I CountriesI Small Open Economy (SOE)I Borrowing and default decisions of SOE has no impact on large

economiesI N-1 SOE and 1 Large economy

I Borrower in SOEI Representative risk averse maximizes

U i = E0

∞∑t=0

βt (C it )1−γ

1− γ(1)

subject toC it = Y i

t − Q itB

it,t+1 + B i

t−1,t (2)

Sovereign Risk Premia - 17/29

Model - Set-Up Continued

I Nature of endowment Y it

I Stochastic exogenous endowmentI Transitory part (z it) + time varying mean (Γi

t) (Aguiar andGopinath, 2006)

Y it = exp(z it)Γi

t (3)

I z it and log of Γit are AR-1 (with orthogonal shocks)

I All emerging economies have same persistence and volatility ofendowments

I Advanced economy Consumption process: exogenouslygiven, ct = g + εt

I Heterogeneity: For country i, E (εz,iε) = ρi

Sovereign Risk Premia - 18/29

Model - Lenders

I Risk Averse Lenders (departure from earlier literature)

I Why? Risk neutral agents imply expected return on bondsequal risk free rate (which is not the case in the data)

I Standard Habit Preferences (Campbell, Cochrane 1999)

U = Et

∞∑t=0

δt(C i

t − Ht)1−γ

1− γ(4)

I Why? Generate time varying risk aversion and hence riskpremia

I Which is magnified in the synchronized downturns because ofhigh MU

I Data: Market price of risk is high in bad times ⇒ Habitpreferences a good proxy

Sovereign Risk Premia - 19/29

Model - Briefly

I N-1 SOE, 1 large economy, risk averse borrowers and lenders

I Benevolent SOE government borrows from large economy

I Incomplete Markets: Can issue only one period non -contingent bonds

I Govt. decides each period whether to default or repay andstay in contract

I Default CostsI Direct loss of output: C i

t = min{Y it , (1− θ)Y i

}I Penalty: Exclusion from international markets for random

number of periodsI Timing of default matters: Default costly in good times.

Hence defaults more likely in bad times and easy borrowings ingood time

Sovereign Risk Premia - 20/29

Optimality - Default Set and Bond Prices

I For given current debt Bt , default set in decreasing in z itI For given z it , default set is increasing in Bt

I Bond Prices

Q(B′, x) = E

[M

′11−dp(B′ ,x)

]= E (M

′)E

[11−dp(B′ ,x)

]+ CoV

[M

′, 11−dp(B′ ,x)

]I Bond prices lower if cov is negative. (or if c and default

probability are negatively related)

I cov. indicates required risk premia

I For risk neutral lender, cov = 0. Hence bond pricing does notvary with systemic risk.

Sovereign Risk Premia - 21/29

Model Mechanism

I Borrower’s Risk Aversion: Desire to smooth theconsumption

I Lender’s Risk AversionI Demands risk premium on bonds depending upon covariance

of bond returns with his SDF (or MRS)I Controls Probability of Default: If risk premia is high ⇒

Borrowing is costly ⇒ Cost of default is low

I Habit Preferences: Countercyclical risk premia

I Heterogeneity in correlation structure: countries with highcorrelation with lender’s shocks give higher expected returns.

Sovereign Risk Premia - 22/29

Results: Default Sets

set.pdf

Sovereign Risk Premia - 23/29

Results: Bond Pricing

price.pdf

Sovereign Risk Premia - 24/29

Results: Business Cycle an Pricing

I Bond pricesI Temporary Shocks affect bond prices more than Permanent

shocksI Prices will be depressed in bad economic times for borrowers

even if Lender is risk neutralI Impact of risk aversion appears to be small

I Business Cycles: Matches business cycle facts more or less,except usual suspect (nx/gdp)

I Foreign Debt: b/gdp of 25 to 30%. (consistent with dataon public debt)

I Default probabilities: 3 to 6%. Consistent with some of theAsian and African countires.

I Returns spread: 3.4% between high ρ and low ρ countries.(wrt USA). This is little lower than the data

Sovereign Risk Premia - 25/29

Results: Portfolio Simulations

Table: Portfolios of Simulated Data

Characteristics Low Beta Portfolio High Beta Portfolio

β -0.25 0.13Default Probability 5.85 3.84

Excess Returns -1.24 0.65Debt/Output 30.14 28.52

Sovereign Risk Premia - 26/29

Comments

I How is it different from Lizarazo’s paper(2005) on Sovereigndefaults?

I Assumption of Risk Averse Lender: Is it well motivated?I Impact of risk aversion on bond prices is smallI Risk premium could be the result of friction, not risk aversion

of lenders (See Adrian& Shin on Currency premium)

I Assuming Habit preferences makes model a tautology:There is no real search for underlying reasons. (and moreparametric than Lizarazo’s work)

I Only risk considered is correlation of endowments: Howabout other risks? A more broad factor model is required tosupport the fact. For example inflation risk.

Sovereign Risk Premia - 27/29

Comments: Behaviorally equivalent to Risk Aversion

maxEt

[Y

′t rt+1

](5)

subject to

κ

√Var(Y

′t rt+1) ≤ 1 (6)

The optimal portfolio is given by

Yt =1

φtκ(Vart(rt+1))−1Et(rt+1) (7)

I A risk neutral agent’s demand is observationally equivalent torisk averse agent with risk aversion equal to φtκ

I Hence observing risk premia 6= Risk Aversion necessarily

Sovereign Risk Premia - 28/29

Comments III External habit takes as given the level of habit, aka ”keeping

up with the Joneses;” internal habit formation makes moresense in this case

I Ferson and Constantinides (1991) find support for shortterm/internal habit (quarterly and annual data) in US postwardata, and Grishchenko (2010) tests internal against externalhabit preferences and finds that postwar data strongly supportsinternal habit formation

I Current consumption affects future marginal utility - model’smechanism would be even more pronounced

I Model predicts excess returns to be too low and too smooth -internal habit would improve this since consumption todayaffects future periods’ marginal utility

I Model does not account for home bias - average investorholds a small fraction of their total portfolio in foreign assets,therefore a foreign default would not have a very largenegative impact on the surplus consumption ratio, and riskaversion would not decrease much

Sovereign Risk Premia - 29/29