apital industry structure and business models for c ... · •growth strategies for industrial ......

TRANSCRIPT

FESTELCreating a Better

Future

APITALC

0 © 2010 FESTEL CAPITAL www.festel.com

FESTELCreating a Better

Future

APITALC

Industry Structure and Business Models for

Industrial Biotechnology

Research Methodology and Results for Discussion

© 2010 FESTEL CAPITAL www.festel.com

OECD Workshop on the Outlook on

Industrial Biotechnology Vienna, January 14, 2010

FESTELCreating a Better

Future

APITALC

1 © 2010 FESTEL CAPITAL www.festel.com

Copyright and Disclaimer

Copyright

• All rights for the use of all or parts of the information in this document, including reprinting

the whole document or parts thereof, the storage in databanks and translations remain with

FESTEL CAPITAL

• Individual charts can be reproduced stating FESTEL CAPITAL as source; please contact

FESTEL CAPITAL, should you wish to reproduce larger parts of this document

Disclaimer

• FESTEL CAPITAL has prepared this document to the best of FESTEL CAPITAL„s know-

ledge and belief based on all available information

• FESTEL CAPITAL takes no warranty for the accuracy and completeness of this information

• Before deducting individual conclusions, it is necessary to obtain additional data and

conduct further analyses

• Therefore, all liability for costs or damage resulting from information and conclusions in this

document is excluded

FESTELCreating a Better

Future

APITALC

2 © 2010 FESTEL CAPITAL www.festel.com

Contents

Research Methodology 2

Conclusion and Outlook 4

Goals and Objectives 1

Research Results 3

Industry Trends 3.1

Market Structure 3.2

Market Players 3.3

Business Models 3.4

FESTELCreating a Better

Future

APITALC

3 © 2010 FESTEL CAPITAL www.festel.com

The paper gives an overview of current industrial biotechnology industry structure and business models with special focus on innovation

General aspects

• Drivers and barriers for industrial biotechnology

• Size and growth of industrial biotech markets

• Characteristics and importance of market players

• Established and emerging business models for companies

• Growth strategies for industrial biotech companies

• Major trends and outlook for the most important sectors

• Recommendations including issue list for next steps

Special aspects

• Constraints of industry capacity for performing R&D or absorbing new technologies

• Dependence of large firms dependent on innovations from smaller companies

Goals and Objectives - Aspects

FESTELCreating a Better

Future

APITALC

4 © 2010 FESTEL CAPITAL www.festel.com

Contents

Research Methodology 2

Conclusion and Outlook 4

Goals and Objectives 1

Research Results 3

Industry Trends 3.1

Market Structure 3.2

Market Players 3.3

Business Models 3.4

FESTELCreating a Better

Future

APITALC

5 © 2010 FESTEL CAPITAL www.festel.com

FESTEL CAPITAL database Data sources

Additional desk research in October and November 2009 was performed using

typical key words to find relevant information

• Interviews with industrial

companies, research institutions

and investors

• Desk research (company

information, external market

studies, press clippings)

• Open discussions with key

market players

• Excel calculation model with data

between 2003 and 2009

- Sales per segment/sub-

segment

- Capital requirements for R&D

and infrastructure

A structured research approach using the existing FESTEL CAPITAL database was used to prepare the paper for further discussion

Research Methodology - Approach

Innovations in industrial biotechnology as focus topic of the

Working Group Start-ups within the Chair of Technology and

Innovation Management (Prof. Dr. Roman Boutellier)

Pap

er(s

)

Five market studies with with focus

on special industrial biotech areas

FESTELCreating a Better

Future

APITALC

6 © 2010 FESTEL CAPITAL www.festel.com

Starting point was the existing FESTEL CAPITAL database with relevant data which has been built up between 2003 and 2009

• About 50 interviews with managers and experts from industrial biotech companies as well

as additional interviews with experts from research institutions and the investment area

- Various rounds during the past 6 years

- Semi-structured nature to the interviews

• Periodical desk research using public sources (e.g. business databases) and company

disclosures (e.g. websites and press releases)

• Open discussions with persons from the industry to clarify open questions, which could not

be answered using other sources

More than 150 industrial biotechnology companies were analysed through desk research,

interviews or open discussions with FESTEL CAPITAL

Additional desk research in October and November 2009 was performed using typical key

words to find relevant information

Research Methodology - Data Sources

FESTELCreating a Better

Future

APITALC

7 © 2010 FESTEL CAPITAL www.festel.com

Four main regions are analysed to present and discuss the key insights and indicators in the paper

• Europe: EU-27 countries, whereby all of the larger countries are OECD members, and

Switzerland which is also an OECD member

• North America: NAFTA members Canada, Mexico and United States of America which are

all OECD members

• Asia: With China and India as well as including the OECD member states Australia and

Japan

• Rest of the world: All other countries not covered by the other categories

A separate category with the BRIC countries is currently not possible as the FESTEL

CAPITAL database does not yet fully include this category

Research Methodology - Regions

FESTELCreating a Better

Future

APITALC

8 © 2010 FESTEL CAPITAL www.festel.com

Contents

Research Methodology 2

Conclusion and Outlook 4

Goals and Objectives 1

Research Results 3

Industry Trends 3.1

Market Structure 3.2

Market Players 3.3

Business Models 3.4

FESTELCreating a Better

Future

APITALC

9 © 2010 FESTEL CAPITAL www.festel.com

The fast technological development within industrial biotechnology is a driver for industrial biotechnology

Fast technological development

• Technological development progressing at an enormous rate

- Development of basic technologies (e.g. directed evolution, genetical modification tools)

- Development of tailormade and high performance enzymes (especially in the number of

available enzymes)

- Improvement of efficiency through new developments in reactor and process design

• Implementation of new applications for existing and new enzymatic systems

• Increasing production of high-value products, such as nutraceuticals, cosmeceuticals and

performance chemicals

Industry Trends - Drivers

FESTELCreating a Better

Future

APITALC

10 © 2010 FESTEL CAPITAL www.festel.com

The need for sustainable development as well as the ongoing globalisation is a driver for industrial biotechnology

Need for sustainable development

• Consumers increasingly conscious about the impacts of their consumption and choosing

products with low negative impact on the environment (e.g. low-carbon economy)

• Need for a switch to clean and sustainable processes using renewable resources as a

sustainable raw material basis

• Contributes to the sustainable development of established industries as well global

economy

• Biomass-derived energy based on biotechnology expected to account for an increasing

share in energy consumption

Ongoing globalisation

• Global competition drives companies to biotech routes, especially in Europe and the US

• Processes to sustain competitiveness especially regarding Asian challenges

• Reduction of trade barriers towards global biotech markets (e.g. for biofuels)

Industry Trends - Drivers

FESTELCreating a Better

Future

APITALC

11 © 2010 FESTEL CAPITAL www.festel.com

High investment and production costs as well as critical raw material prices and limited availability are barriers facing industrial biotechnology

High investment and production costs

• Restrictions of biotechnological production processes from an economic viewpoint

- High investments in R&D and process development

- Massive new investments to build new production facilities

• Higher prices for products from biotechnology processes normally not achievable

Cyclical raw material prices and limited availability

• Almost 1:1 correlation of crude oil and biomass prices during the last years so no general

cost advantages of bio-based routes

• Hope that biomass shows less cyclicality compared to crude oil prices has not been

realised

• Rising food and feed demand is a critical driver and a significant limitation on the uptake of

industrial biotechnology (especially in debates around biofuels, land use has been a

controversial issue)

Industry Trends - Barriers

FESTELCreating a Better

Future

APITALC

12 © 2010 FESTEL CAPITAL www.festel.com

Complex innovation processes as well as critical social acceptance and regulations are barriers facing industrial biotechnology

Complex innovation processes

• Industrial biotechnology know-how mainly used in the early stages of the value chain

• Specialised companies cover normally only a small share of the value-added along the

value chain

• Combination of “technology push” and “market pull” along the value chain necessary

Critical social acceptance and regulations

• Social acceptance of industrial biotechnology normally high but some regions still have

rather a low acceptance of genetically modified organisms - in the field of genetic

engineering considerably more bureaucracy and legislation

• Problem accepting green biotechnology, especially in Europe, has a direct impact on

industrial biotechnology

- Growth depends very much on the development of green biotechnology

- Green and industrial biotechnology often combine to an integrated value chain

Industry Trends - Barriers

FESTELCreating a Better

Future

APITALC

13 © 2010 FESTEL CAPITAL www.festel.com

Contents

Research Methodology 2

Conclusion and Outlook 4

Goals and Objectives 1

Research Results 3

Industry Trends 3.1

Market Structure 3.2

Market Players 3.3

Business Models 3.4

FESTELCreating a Better

Future

APITALC

14 © 2010 FESTEL CAPITAL www.festel.com

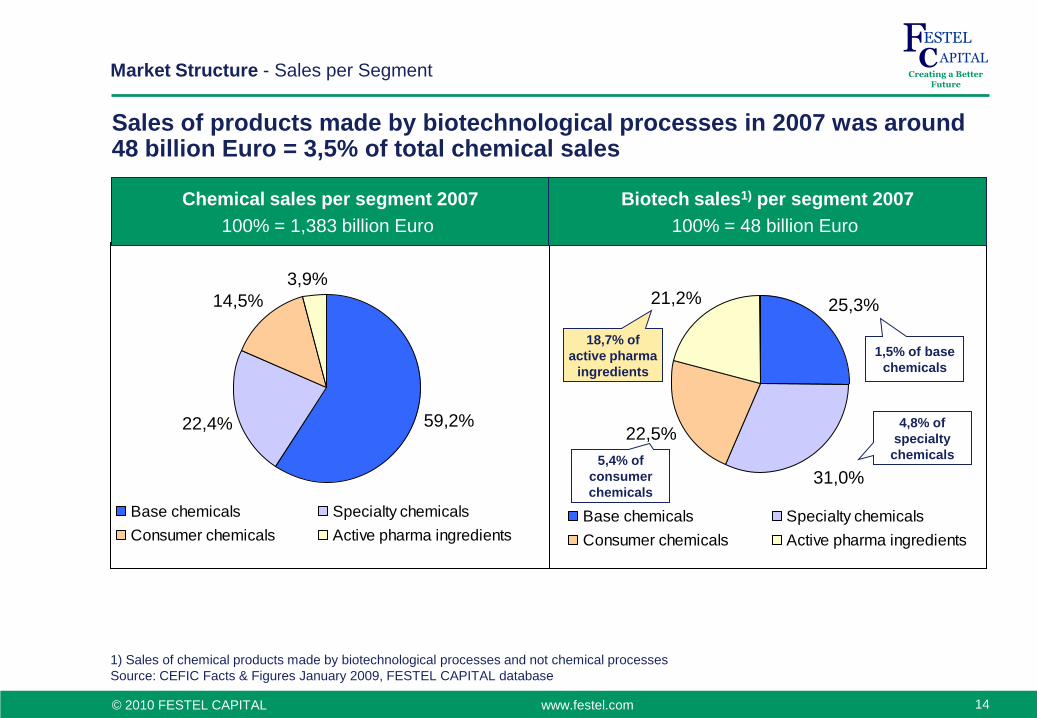

25,3%

31,0%

22,5%

21,2%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

59,2%22,4%

14,5%

3,9%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

Market Structure - Sales per Segment

Sales of products made by biotechnological processes in 2007 was around 48 billion Euro = 3,5% of total chemical sales

Chemical sales per segment 2007

100% = 1,383 billion Euro

Biotech sales1) per segment 2007

100% = 48 billion Euro

1,5% of base

chemicals

4,8% of

specialty

chemicals 5,4% of

consumer

chemicals

18,7% of

active pharma

ingredients

1) Sales of chemical products made by biotechnological processes and not chemical processes

Source: CEFIC Facts & Figures January 2009, FESTEL CAPITAL database

FESTELCreating a Better

Future

APITALC

15 © 2010 FESTEL CAPITAL www.festel.com

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

Ano

rgan

ics

Fertilis

ers

& g

ases

Org

anic c

hem

ical

s

Pol

ymer

s & fibre

s

Agr

ochem

ical

s

Adh

esives

& s

ealants

Pai

nts

& c

oatin

gs

Food a

dditive

s

Oth

er spec

ialty

che

micals

Det

ergen

ts

Cos

met

ics

Act

ive

phar

ma in

gred

ient

s

Europe (EU-27) North America (NAFTA) Asia (incl. China and Japan) Rest of the World

The most important sub-segments in 2007 were active pharma ingredients and cosmetics

Biotech sales per sub-segment 2007

100% = 48 billion Euro

Market Structure - sales per Sub-segent

Source: FESTEL CAPITAL database

FESTELCreating a Better

Future

APITALC

16 © 2010 FESTEL CAPITAL www.festel.com

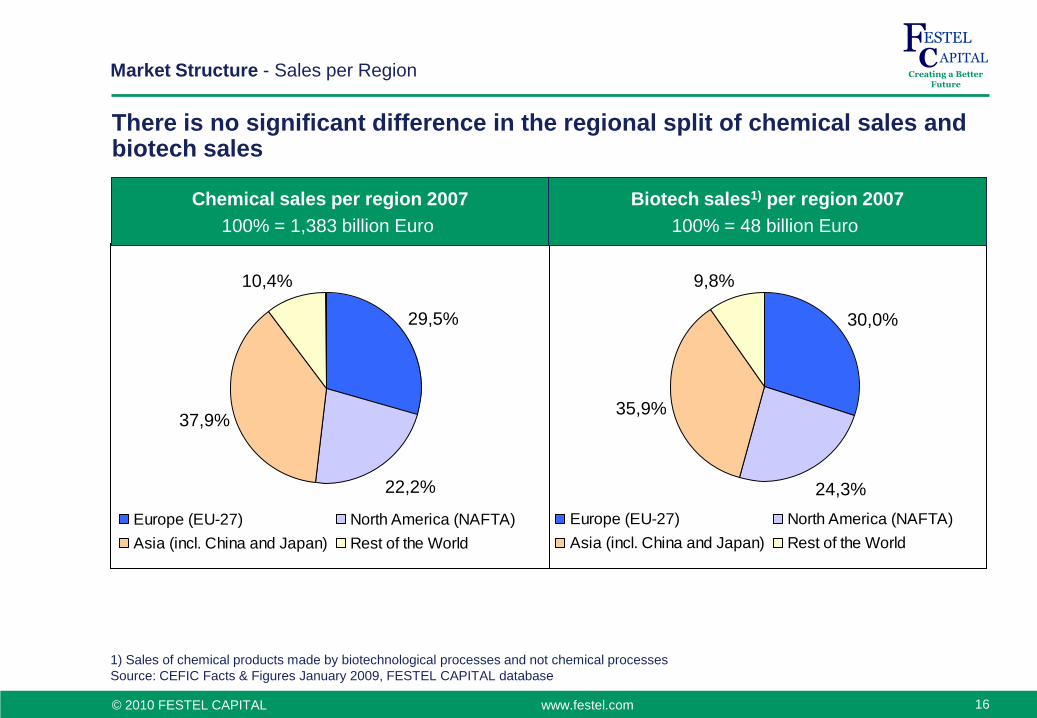

30,0%

24,3%

35,9%

9,8%

Europe (EU-27) North America (NAFTA)

Asia (incl. China and Japan) Rest of the World

There is no significant difference in the regional split of chemical sales and biotech sales

29,5%

22,2%

37,9%

10,4%

Europe (EU-27) North America (NAFTA)

Asia (incl. China and Japan) Rest of the World

Biotech sales1) per region 2007

100% = 48 billion Euro

Chemical sales per region 2007

100% = 1,383 billion Euro

1) Sales of chemical products made by biotechnological processes and not chemical processes

Source: CEFIC Facts & Figures January 2009, FESTEL CAPITAL database

Market Structure - Sales per Region

FESTELCreating a Better

Future

APITALC

17 © 2010 FESTEL CAPITAL www.festel.com

Contents

Research Methodology 2

Conclusion and Outlook 4

Goals and Objectives 1

Research Results 3

Industry Trends 3.1

Market Structure 3.2

Market Players 3.3

Business Models 3.4

FESTELCreating a Better

Future

APITALC

18 © 2010 FESTEL CAPITAL www.festel.com

Dedicated

start-ups

Importance of industrial

biotech-nology

High

Low

Small Large Company

Size

Company types and examples

Dedicated

SMEs

Diversified

MNEs

Dedicated

MNEs

Diversified

SMEs

Dedicated multi-

nationals

Diversified

SMEs

Dedicated

start-ups

Dedicated

SMEs

CSM/Purac

Lesaffre

Novozymes

Döhler

Siegfried

Südzucker

Autodisplay Biotech

Evocatal

Fluxome Sciences

AB Enzymes

Brain

Codexis

Iogen

Stern Enzym

Examples Company type

Diversified

multinationals

BASF

Danisco

DSM

There are different company types active in the industrial biotechnology area

Market Players - Company Types

FESTELCreating a Better

Future

APITALC

19 © 2010 FESTEL CAPITAL www.festel.com

Dedicated

start-ups

Commercial develop-

ment

Very important

Less important

Less important

Very important

Technological development

Dedicated

SMEs

Diversified

MNEs

Dedicated

MNEs

Diversified

SMEs

Especially dedicated companies are important for the further development of industrial biotechnology

Market Players - Further Development

Further development of industrial biotechnology

• Dedicated and diversified MNEs

are by far the most important

groups in terms of biotech sales

and R&D budgets

• Dedicated and diversified SMEs

are driving especially the

commercial development

• The commercial development is

also driven by dedicated MNEs

• Dedicated start ups are

contributing significantly to the

further technological

development

FESTELCreating a Better

Future

APITALC

20 © 2010 FESTEL CAPITAL www.festel.com

Dedicated and diversified MNEs are by far the most important groups in terms of biotech sales and R&D budgets

Dedicated MNEs

• Companies mainly active in the area of natural products (e.g. CSM/Purac, Lesaffre) and

also sub-type of high-tech oriented companies (e.g. Novozymes)

• Industrial biotechnology is one cornerstone in their technology portfolio

• They are increasingly moving towards more sophisticated products and processes

• They will significantly drive the technological and commercial development of industrial

biotechnology

Diversified MNEs

• Mainly established companies from the chemical industry (e.g. BASF, DSM), agro industry

(e.g. ADM, Cargill) or food industry (e.g. Danisco)

• Broad and integrated technology portfolio which is complemented by industrial biotech

processes

• Competition between industrial biotechnology and traditional technologies compared to

other company types which slows down development

Market Players - MNEs

FESTELCreating a Better

Future

APITALC

21 © 2010 FESTEL CAPITAL www.festel.com

Dedicated and diversified SMEs are driving especially the commercial development of industrial biotechnology

Dedicated SMEs

• Focused on building up own production facilities and selling their products (e.g. Brain and

Codexis)

• Core for the further technological and commercial development of an independent

industrial biotechnology sector

Diversified SMEs

• Mainly located in established industrial sectors like the chemical or food industry (e.g.

Döhler and Siegfried)

• Introducing step by step biotechnology processes and products into their markets

• Especially drive the commercial development of industrial biotechnology

Market Players - SMEs

FESTELCreating a Better

Future

APITALC

22 © 2010 FESTEL CAPITAL www.festel.com

Dedicated start ups are contributing significantly to the further technological development of industrial biotechnology

Dedicated start ups

• Start-up companies focused on industrial biotechnology which are mainly driven by R&D

(e.g. Evocatal, Fluxome Sciences)

• Development and commercialisation of special technologies and their applications

• Also targeted red biotechnology, but with increase in maturity of companies (e.g. Direvo

Industrial Biotechnology, Eucodis Bioscience) the businesses are separated

• Expected to contribute significantly to the further technological development of industrial

biotechnology

Market Players - Start ups

FESTELCreating a Better

Future

APITALC

23 © 2010 FESTEL CAPITAL www.festel.com

Contents

Research Methodology 2

Conclusion and Outlook 4

Goals and Objectives 1

Research Results 3

Industry Trends 3.1

Market Structure 3.2

Market Players 3.3

Business Models 3.4

FESTELCreating a Better

Future

APITALC

24 © 2010 FESTEL CAPITAL www.festel.com

Established business models within industrial biotechnology focus on production and service

Producers

• Realised mainly by diversified SMEs as well as dedicated and diversified MNEs

• Develop own technologies or buy/license them and focus on production including the

whole supply chain from raw materials to distribution

• Most service oriented dedicated SMEs are currently in the phase of going into this

business model as it offers more growth options

• High capital requirements to build-up own production facilities are a disadvantage

Service providers

• Mostly dedicated start-ups and some dedicated SMEs offering their particular know-how

predominantly as services to support other companies

• Normally realise primarily organic growth and are profitable, but have sub-critical

structures with regard to size and financial strength (unable to realise growth opportunities

due to a lack of financial resources)

• IP normally belongs to the customer and growth or value creation potential through

development and commercialisation of own IP is very limited

Business Models - Established

FESTELCreating a Better

Future

APITALC

25 © 2010 FESTEL CAPITAL www.festel.com

IP oriented business models are emerging besides the established business models

Emerging business models

• Emerging business models include the IP creator and the integrated process developer

• Focus on the development of own IP and licensing business

• Development of own portfolios of technologies and products which are sold or out-licensed

Business Models - Emerging

FESTELCreating a Better

Future

APITALC

26 © 2010 FESTEL CAPITAL www.festel.com

R&D co-opera-

tions

Joint ventures Internal

R&D

M&A

Tech-nologies

New

Estab-lished

Estab-lished

New Markets

M&A

Joint

ventures

Internal

R&D

R&D co-

operations

Acquisition of or merger with

another company to create a

single new entity

Formation of a new company

where parent companies

have ownership and

contribute complementary

assets, technologies, people

or other capabilities

Own R&D with primarily

internal resources

R&D together with external

partners (other companies,

universities and R&D

institutes)

Description Strategy

Growth strategies for industrial biotech companies

Companies have four different potential growth strategies to move from a service-oriented to an IP-oriented business model

Business Models - Growth Strategies

FESTELCreating a Better

Future

APITALC

27 © 2010 FESTEL CAPITAL www.festel.com

Contents

Research Methodology 2

Conclusion and Outlook 4

Goals and Objectives 1

Research Results 3

Industry Trends 3.1

Market Structure 3.2

Market Players 3.3

Business Models 3.4

FESTELCreating a Better

Future

APITALC

28 © 2010 FESTEL CAPITAL www.festel.com

Sector Outlook Major trends

Base Chemicals

and intermediates

• Stronger use of renewable raw materials due to cost reasons

• Cost advantages of biotech processes due to the stricter regulatory

environment

Specialty

Chemicals

• Strong growth in industrial enzymes for more and more applications

• Increasing advantages of enzymatic processes especially in the food,

cosmetic, textile and leather industries due to customer requirements

Polymers

• Stronger use of renewable raw materials due to cost reasons

• Access to polymers with new properties (e.g. biodegradability)

• Increasing regulatory pressure to realise sustainable solutions (e.g. for

packaging applications)

Fine Chemicals

• Growing importance of chiral active pharmaceutical ingredients

• Cost reductions through simplified synthesis paths (especially if

molecules are complex)

• Only through biotechnological processes accessible products

Biofuels

• Increasing advantage due to rising oil prices and climate change

• Significant progress in production technologies with increasing cost

competitiveness without subsidies

The largest market potential lies in the production of fine chemicals for the pharma and agro industry, biopolymers and biofuels

Conclusion and Outlook - Markets

FESTELCreating a Better

Future

APITALC

29 © 2010 FESTEL CAPITAL www.festel.com

There are three groups of industrial companies which can be targeted by policy makers with different approaches

• Dedicated start-ups and SMEs: Provide incentives to foster growth based on R&D based

innovations

• Diversified SMEs: Provide incentives to enable the usage of biotech technologies in

established production processes

• Dedicated and diversified MNEs: Provide incentives to support market introduction and

penetration of biotech products

Conclusion and Outlook - Players

FESTELCreating a Better

Future

APITALC

30 © 2010 FESTEL CAPITAL www.festel.com

Production/sales figures

Clear and consistent structure necessary

Structure of FC database (modified CEFIC structure) as starting point

• Production and sales figures for 2007,

2012 and 2017

- Per segment/sub-segment

- Per region/country

• Rough data are available from FC

Availability of relevant data

Company types

• Structure of the industrial biotech

companies

- Size

- Growth

- Business model

• Currently no consistent data available

Suitable key indicators could be production/sales figures differentiated for the different company types as key indicators

Conclusion and Outlook - Relevant Data

FESTELCreating a Better

Future

APITALC

31 © 2010 FESTEL CAPITAL www.festel.com

The issue list regarding the need for further research and the definition of next steps can help to improve the paper

Conclusion and Outlook - Issue List

Need for further research

• Better understanding of the development of production technologies in the different

sectors, segments and sub-segments

• Better understanding of the specific impact of raw material supply and prices

Definition of next steps

• Agree on data structure (production and sales figures, description of industrial biotech

companies) to enable an OECD wide comparison

• Agree on data collection and processing process

• Agree on suitable key indicators to get relevant information for policy makers

FESTELCreating a Better

Future

APITALC

32 © 2010 FESTEL CAPITAL www.festel.com

Backups

Backups B

FESTELCreating a Better

Future

APITALC

33 © 2010 FESTEL CAPITAL www.festel.com

More than 150 industrial biotechnology companies were analysed through desk research, interviews or open discussions with FESTEL CAPITAL (1/2)

Research Methodology - Interviews

Abbreviations: Dr = Desk research, Si = Standardised interview, Od = Open discussion

Company Dr Si Od Company Dr Si Od Company Dr Si Od

AB Enzymes x x Ciba SC x x x Lonza x x x

Abitep x Clariant x x LS9 x

AC Biotec x x c-LEcta x x Lybradyn x

Aglycon Mycoton x CMC Biopharmaceuticals x Lyven x

AlgMax x x Codexis x x m2p-labs x

Alligator Bioscience x Cognis x x x Maxygen x

Alvito Biotechnologie x CSM Biochemicals x Meiji x

Amino x Direvo Industrial Biotech x x Merck x x x

Amyris Biotechnologies x Diversa x Metabolix x

AnalytiCon Discovery x Döhler x Molekulare Biotechnologie x

AnBio x Dow Chemical x xMunich Innovative

Biomaterials x

Angel Biotechnology x Dr. Petry Genmedics x MykoMax x

Animox x x Dr. Rieks x Nadicom x

Anoxymer x DSM x x x Nexia Biotechnologies x

Arrayon Biotechnology x DSM Biotech x x Nexyte x

Artechno x DuPont x x Nordzucker x x x

Artes Biotechnology x x x E.gene Biotech x Novacta x x

ASA Spezialenzmye x x EKB Technologies x Novamont x x

ATG Biosynthetics x x Enzis x x Novozymes x x

Autodisplay Biotech x x EnzyScreen x N-Zyme Biotec x

BASF x x ESBATech x OrganoBalance x

Bayer x x x Essum x Pacovis x x

BayGenetics x x Eucodis x x Panolin x x

BBT Biotech x EuroFerm x Petroplast Vinora x x

Beiersdorf x x Evocatal x x Pfeifer & Langen x x

Beldem x Evonik Degussa x x x Phenion x

FESTELCreating a Better

Future

APITALC

34 © 2010 FESTEL CAPITAL www.festel.com

Company Dr Si Od Company Dr Si Od Company Dr Si Od

Biocatalysts x FermenSys x Plantic x x

Bioconsens x Galactic x x PomBioTech x

Biolac x Ganomycin x Procter & Gamble x x

Biomay x Gevo x x Prokaria x x

Biomer x x Green Biologics x Protéus x

Biométhodes x Greenovation Biotech x x Rheinchemie x x x

Biomeva x Gyre x Roche Diagnostics x x

Bionova x HöFer Bioreact x Roquette x x

Bioreact x HPC Biotec x Schill & Seilacher x x

Bioressources Worlwide x Hycail x xScientific Research and

Developmentx x

Biospring x x x IEP x x Senomyx x

Biosynergy x IFB Halle x Sourcon-Padena x

Biotec x x Industrial Biotechnology x Stern Enzym x x

BIOTex x Ingenza x Subitec x x

Biovet x Innovia Films x x Süd-Chemie x x x

Biovian x Inosim x Südzucker x x x

Bioworx x Insilico x x Total x x

Biozym x Invigate x Trenzyme x

Bitop x Iogen x x Treofan x x

BlueBioTech x Jülich Chiral Solutions xW42 Industrial

Biotechnologyx

Brain x x x Jülich Enzyme Products x x Wacker Chemie x x

BTR Laboratories x Jülich Fine Chemicals x x Wentus x x

Butalco x x Kerry Bio Science x Weyl Chem x

Celanese x x x Lehmann & Voss x x X2 Biotechnologies x

Cerestar x x Lesaffre x x X-Zyme x x

ChiPro x Libragen x Zymeworks x

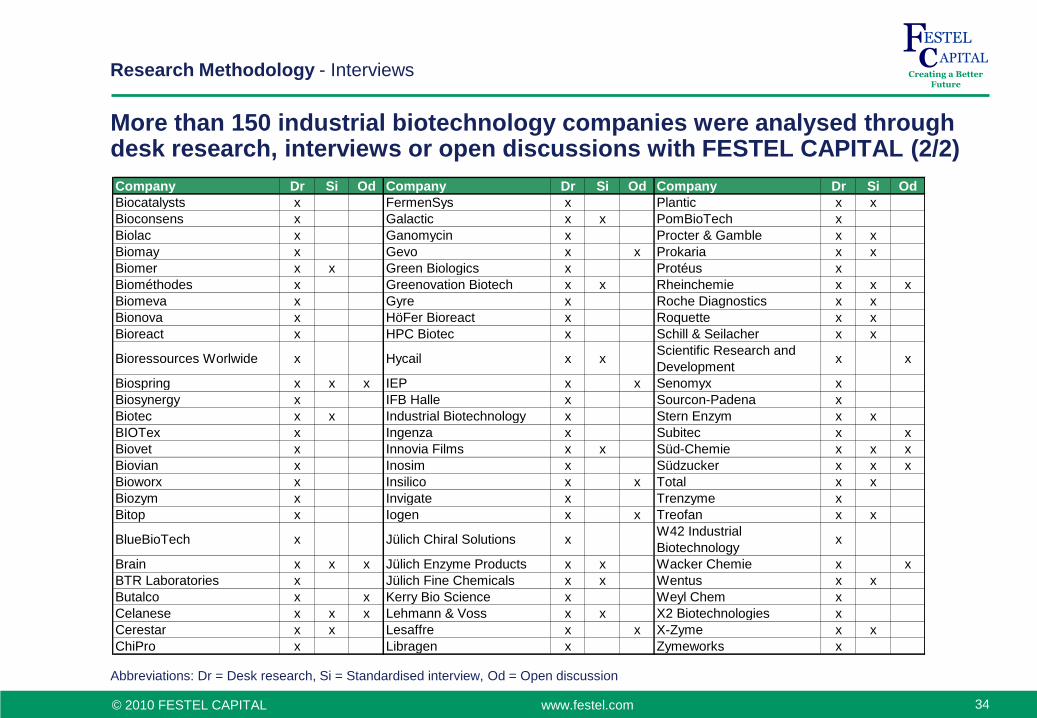

More than 150 industrial biotechnology companies were analysed through desk research, interviews or open discussions with FESTEL CAPITAL (2/2)

Research Methodology - Interviews

Abbreviations: Dr = Desk research, Si = Standardised interview, Od = Open discussion

FESTELCreating a Better

Future

APITALC

35 © 2010 FESTEL CAPITAL www.festel.com

FESTEL CAPITAL

market studies FESTEL CAPITAL database

Market data updated regularly

based on ongoing discussions with

key market players

• Desk research (company

information, external market

studies, press clippings)

• Interviews with industrial

companies, research institutions

and investors

• Excel calculation model based on

available information with specific

adjustments

• Biotech production

technologies (November

2003)

• Financing strategies

(April 2005)

• Renewable raw

materials (July 2005)

• Biofuel production

technologies (October

2006)

• Financing and

investment trends

(February 2009)

Already existing data of FESTEL CAPITAL and additional desk research were used for data gathering

Research Methodology - Market Studies

FESTELCreating a Better

Future

APITALC

36 © 2010 FESTEL CAPITAL www.festel.com

The combination of “technology push” and “market pull” along the value chain is necessary

Yeast genetics

and synthetic

biology =

"Technology

Push"

Rising oil

prices and de-

creasing security

of supply =

"Market

Pull"

1 The biofuel producer identifies new fermentation technologies and develops the fermentation

technology together with a biotechnology company

2 The biofuel producer develops together with a engineering / plant construction company the plants a

technical scale processes

3 The engineering / plant construction company develops together with specialised downstream

processing company a biofuel purification process

4 The downstream processing company develops with the biotechnology company the combined

fermentation / purification process

Step 2

Cellulose

Hydrolysis

Step 1

Feedstock

Supply

Step 4

Biofuel

Purification

Step 5

Engineering/

Construction

Step 3

Biofuel

Fermentation

Step 6

Biofuel

Production

1 2 3 4 5 6

5 The biotechnology company develops with the hydrolysate supplier the hydrolysis process

6 The hydrolysate supplier organises the feedstock supply

Industry Trends - Barriers

Innovation Innovation

FESTELCreating a Better

Future

APITALC

37 © 2010 FESTEL CAPITAL www.festel.com

24,9%

28,0%24,0%

23,0%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

55,3%

23,7%

15,8%

5,3%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

Market Structure - Biotech Sales 2012

Sales of products made by biotechnological processes in 2012 will be around 135 billion Euro = 7,7% of total chemical sales

Chemical sales per segment 2012

100% = 1,748 billion Euro

Biotech sales1) per segment 2012

100% = 135 billion Euro

3,5% of base

chemicals

9,1% of

specialty

chemicals

11,7% of

consumer

chemicals

33,7% of

active pharma

ingredients

1) Sales of chemical products made by biotechnological processes and not chemical processes

Source: CEFIC Facts & Figures January 2009, FESTEL CAPITAL database

FESTELCreating a Better

Future

APITALC

38 © 2010 FESTEL CAPITAL www.festel.com

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

Ano

rgan

ics

Fertilis

ers

& g

ases

Org

anic c

hem

ical

s

Pol

ymer

s & fibre

s

Agr

ochem

ical

s

Adh

esives

& s

ealants

Pai

nts

& c

oatin

gs

Food a

dditive

s

Oth

er spec

ialty

che

micals

Det

ergen

ts

Cos

met

ics

Act

ive

phar

ma in

gred

ient

s

Europe (EU-27) North America (NAFTA) Asia (incl. China and Japan) Rest of the World

The most important sub-segments in 2012 will be active pharma ingredients and cosmetics

Biotech sales per sub-segment 2012

100% = 135 billion Euro

Market Structure - Biotech Sales 2012

Source: FESTEL CAPITAL database

FESTELCreating a Better

Future

APITALC

39 © 2010 FESTEL CAPITAL www.festel.com

33,3%

21,4%

24,8%

20,5%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

51,3%

25,0%

17,1%

6,6%

Base chemicals Specialty chemicals

Consumer chemicals Active pharma ingredients

Sales of products made by biotechnological processes in 2017 will be around 340 billion Euro = 15,4% of total chemical sales

Chemical sales per segment 2017

100% = 2,212 billion Euro

Biotech sales1) per segment 2017

100% = 340 billion Euro

10,0% of base

chemicals

13,1% of

specialty

chemicals 22,3% of

consumer

chemicals

47,9% of

active pharma

ingredients

1) Sales of chemical products made by biotechnological processes and not chemical processes

Source: CEFIC Facts & Figures January 2009, FESTEL CAPITAL database

Market Structure - Biotech Sales 2017

FESTELCreating a Better

Future

APITALC

40 © 2010 FESTEL CAPITAL www.festel.com

0,0

5,0

10,0

15,0

20,0

25,0

30,0

Ano

rgan

ics

Fertilis

ers

& g

ases

Org

anic c

hem

ical

s

Pol

ymer

s & fibre

s

Agr

ochem

ical

s

Adh

esives

& s

ealants

Pai

nts

& c

oatin

gs

Food a

dditive

s

Oth

er spec

ialty

che

micals

Det

ergen

ts

Cos

met

ics

Act

ive

phar

ma in

gred

ient

s

Europe (EU-27) North America (NAFTA) Asia (incl. China and Japan) Rest of the World

The most important sub-segments in 2017 will be active pharma ingredients and polymers & fibres

Biotech sales per sub-segment 2017

100% = 340 billion Euro

Market Structure - Biotech Sales 2017

Source: FESTEL CAPITAL database

FESTELCreating a Better

Future

APITALC

41 © 2010 FESTEL CAPITAL www.festel.com

Strategy Advantages Disadvantages

• Enables the development of own IP

• Start-up decides on R&D projects

• Increased flexibility on project choice and research goals

• Cost and capital intensive

• High project risk

• Limited research capacities prevent a fast reaction

concerning new projects

• Lack of networks that provide new ideas with regard to

the research

• Increases number of possible technologies available for

R&D projects

• Additional resources and synergies

• Splitting the risk of the project

• Rarely receive considerable volume of IP developed in

the project (often the case with academic partners)

• Need for a strong project management

• Limited possibility of development of own IP

• Enables growth in a new business area

• Additional resources (e.g. assets, technologies)

• Synergies of complementary technologies and know-

how

• Loss of control in the company

• Loss of flexibility in the decision making process

• Enables use of synergies

• Enables expansion into new markets / international

markets

• Enables acquisition of IP and technologies

Internal R&D

R&D co-operation

Joint Venture

M&A

• The time involved for negotiations and contract

development is high

• An inflexible co-operation model, where the search for

the appropriate partner is critical

The different growth strategies have specific advantages and disadvantages from an entrepreneurial view

Business Models - Growth Strategies