apimec 2015 ing

TRANSCRIPT

1

APIMEC 2015PRESENTATION OF 3Q15 RESULTS

São Paulo, October 27, 2015

2

APIMEC seal 14 YEARS

3

Disclaimer

The statements in this report with respect to the outlook for the

Company’s businesses, the estimates and result and to the

potential for growth, constitute mere forecasts and were based on

management’s expectations in relation to the Company’s future.

These expectations are highly dependent on changes in the

market, the economic performance of Brazil, the sector and

international markets, all of which are subject to change.

4

ISA

Investor PresentationAPIMEC 2015

Sao Paulo. October 27, 2015

The IR Recognition granted by the Colombian Securities Exchange (Bolsa de Valores de Colombia S.A) is not a certification of the registered securities or the solvency of the issuer

AGENDA

6

Today , ISA is one of the largest company in Latin America…

7

ELECTRIC ENERGY

TRANSPORT

TOLL ROAD

CONCESSIONS

TELECOMMUNICATIONS

TRANSPORT

SMART MANAGEMENT OF REAL

TIME SYSTEMS

Largest international energy carrier in Latin

America.

41,650 kms of high voltage circuit

77.710 MVA of transformation capacity

Presence in Colombia, Peru, Bolivia, Brazil, Chile,

Panama and Central America.

Largest continued terrestrial network of the

continent.

26,700 kms of optical fiber

Presence: Colombia, Venezuela, Ecuador, Peru,

Chile, and Brazil. Equity stake in REDCA (Central

America).

Largest operator of private roads in Chile.

907 kms of roads in operation in 5 road

concessions of the Route in Chile.

Over 100 million vehicles.

Close to USD 400 million in toll revenue.

Operates the National Interconnected

System

Generation: 64,328 GWh

Demand: 63,571 GWh

Manages the Wholesale Energy Market

Purchase and sale of energy: COP 13.3 trillion

ISA is recognized as a company with broad technical experience, carrying out its activities within the framework of corporat e sustainability.

8

33

ISA

ColombiaIntercolombia

TranselcaXM

INTERNEXA

PeruREP

TransmantaroISA Perú

PDIINTERNEXA

ChileINTERCHILEINTERNEXA

INTERVIAL CHILERuta del MaipoRuta del Maule

Ruta del BosqueRutla de la Araucania

Ruta de los RiosISA inversiones ChileISA inversiones Maule

BrazilCTEEPIEMG

PINHEIROSSERRA DO JAPI

EVRECYINTERNEXA

ISA Capital do Brasil

Others:

Ecuador

Bolivia

Argentina

Panama

Central America

Affiliates and subsidiaries 8 Countries 1 Region:

Central America4 Business

ISA has presence in Latin America through …

Limited growth in Colombia led ISA to an evolution in the business model…

Leading energy transmitter in COL.

Reduced growth opportunities in COL

promoted internationalization

process.

Entering new markets: Peru, Bolivia, Brazil,

Central America.ISA Peru, first

internationalization achieved. COL-ECU

interconnection.

Consolidation transmission business, telecommunications.Intervial Chile, first

diversification strategy achieved. COL-PAN

interconnection.INTERCHILE

1967-1994 1995-1999 2000-2006 2007-2013

Institutional consolidation

New ISA

Geographic expansion

Diversification

Consolidation

2014+ 9

Regional systems interconnection and

Center-Coast interconnection.

CNDCOL-VEN

interconnection.

By 2020, ISA will have tripled its

profits , by capturing the most profitable

growth opportunities in its businesses existing in Latin America, the boost of operational efficiency and the optimization of its business portfolio.

Vision 2020

AGENDA

10

ISA in Brazil has a broad history and an diversified investment…

11

In ISA’s consolidated figures

(2014), Brazil represents:

25,9% of the revenues

16,0% of the EBITDA

23,9% of the Assets

2007-2012:CTEEP participated in ANEEL’s bidding

processes with great success.

IEMadeira, IENNE, IEMG,

IEPINHEIROS, IESUL, SERRA DO

JAPI, IEGAR

ISA’s history in Brazil started in

2006 by purchasing 50.1%

of CTEEP’s common shares

Annually, CTEEP, invests USD 100

million approximately in reinforcement

projects.

2007: ISA acquired 39,28% of CTEEP by a tender

offer

2013: ISA acquired an information

transport network company in Rio de

Janeiro.

2012: ISA started operations in the

telecommunications business

ISA is the Colombian company that has made the largest

investments in Brazil. Between 2006-2015:

BRL 11,3 billion

ISA reinforced its commitment with

Brazil by signing the concession contract

renewal in 2012

CTEEP’ s concession contract 059 goes from 2013 to 2042

1

2

3

4

5

AGENDA

12

2.528 2.540 2.557 2.570 2.589 2.615

2015 2016 2017 2018 2019 2020

COLOMBIA PERU BRAZIL CHILE OTHERS

An investment of USD 3.883 million supports ISA’s future growth ...

13

by country COP %

Colombia 3.121 31,9

Peru 2.097 21,5Brazil 1.991 20,3Chile 2.549 26,2Others 12 0,1

by business COP %

Energy 9.052 92,7

Toll Roads 167 1,7

Telecommunications 392 4,0

SMRTS 159 1,6

COP 9.769.711 millionUSD 3.883 million

Projections: July 2015

BreakdownCOP billions

3.509

2.335

818407 412

2.288

In Brazil , investments are in reinforcement projects for an average of USD 100 million

annually.

USD/COP

14

For nearly 50 years, ISA has been characterized by the efficient and reliable delivery of its services, within a

framework of respect for human rights and environmental protection in order to promote regional competitiveness

and sustainability , thanks to a highly qualified and committed team consisting of more than 3,800 workers.

16

CTEEP

17

CTEEP: Timeline

CTEEP is constituted with the transmission assets of CESP

Incorporation of EPTE with transmission assets of Eletropaulo

Extension of Concession Agreement 059/2001 with ANEEL, beginning a new cycle for its businesses

Startup of Operations of IE Madeira’s transmission line and conclusion of work

ISA Group launches Vision 2020 with focus on profitability and operational efficiency

Signs up to Level 1 of BM&FBovespa’s Corporate Governance

Privatization, ISA becomes the new controller

2002 2006

2012 2013 2015

Expansion into 16 Brazilian states, the result of participations in auctions and acquisitionsPortfolio of businesses with 8 subsidiaries , investments of R$ 6.2 billion and a RAP of R$ 670.2 MM

1999 2001

Start of operations of IE Garanhuns’ transmission line

18

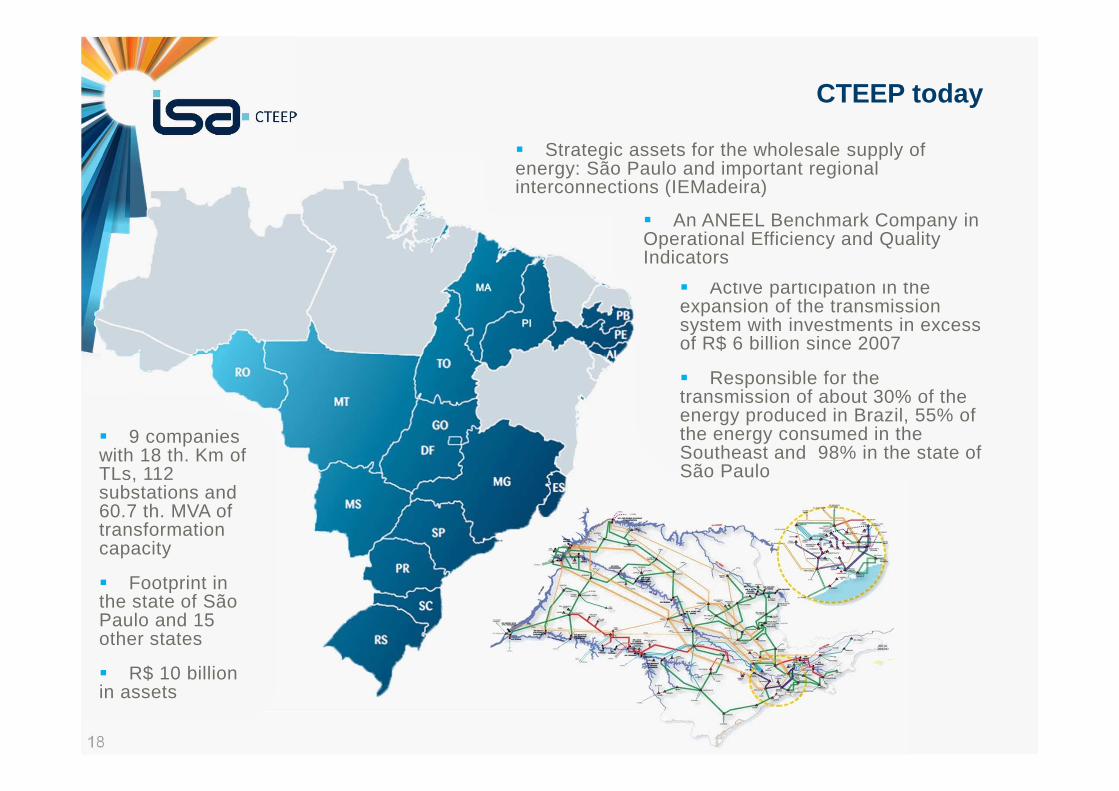

CTEEP today

� Active participation in the expansion of the transmission system with investments in excess of R$ 6 billion since 2007

� Responsible for the transmission of about 30% of the energy produced in Brazil, 55% of the energy consumed in the Southeast and 98% in the state of São Paulo

� 9 companies with 18 th. Km of TLs, 112 substations and 60.7 th. MVA of transformation capacity

� Footprint in the state of São Paulo and 15 other states

� R$ 10 billion in assets

� Strategic assets for the wholesale supply of energy: São Paulo and important regional interconnections (IEMadeira)

� An ANEEL Benchmark Company in Operational Efficiency and Quality Indicators

19

CTEEP: Shareholding Breakdown

Capital Total

Preferred Shares - TRPL4(60% of the total)

Common Shares - TRPL3(40% of the total)

0.7%9.8%

89.5%

52.4%

2.3%

31.2%

6.7%

7.4%

19.0%

4.0%4.4%

35.4%

37.2%

Others

Vinci Ltda

Governo do Estado de SP

Eletrobras

ISA Capital do Brasil

Base: 30/09/2015

20

A ‘Multilatina’ company with a footprint in 8 countries, ISA has consolidated over the

course of more than 46 years of activities at its 33 companies, distributed across 4

sectors: electric energy transmission, highway concessions, telecommunications and

intelligent management of real time systems

ISA Group

1S15 ISA

1H15 EBITDA bycountry

1S15 EBITDA 9M15 bybusiness

Colômbia

Chile

Peru

Brasil

Outros

41,1%

28,2%

15,6%

1,4%

13,6%

Transporte de Energia

Concessões Viárias

Telecomunicações

Gestão Inteligente de Tempo Real

68%

2,8% 0,8%

28,4%

21

CTEEP: Investments

539 680 785623

443656

957 884

801

288197

449

369

425 306

250

229285

493240 1552202

407

683

2010 2011

2.062

1.563

2015E

637

2012

1.976

2014

757

1.674

20132009

1.386

2008

610

2007

CTEEP Sócios nas SubsidiariasCTEEP nas Subsidiarias

� Investments in excess of R $ 11 billion since 2007 , including investments in subsidiaries ,

directly or in partnership with partners

� Participation in 14 of the 19 auctions between 2006 and 2012 , with supply in 48 lots

� 12 lots in operational phase and 1 lot with operation scheduled for November / 15

Investimentos 2007/2015E(R$ MM corrigidos)

22

Results and Challenges

23

Vision 2020

24

Value Drivers

O&M

EFFICIENCY

Investments

RETURN

Subsidieries

GOVERNANCE

Indemnification/DIT

FAIR VALUE

Contingencies

REDUCTION

� Optimization of Costs

� Tax Optimization

� Optimization of O&M Model

� CapExOptimization

� Inventory Utilization

� FIN/ADM Centralization of the 100% subs. in CTEEP

� Control of IEMG and Evrecy via COT

� RBSE Report

� Regulatory Affairs Area

� Strategic Liabilities Management Project

25

Efficiency

Operations and Maintenance

� Use of all that is most modern in technology – Control Centers, Substations

and Transmission Lines

� Management of Operations and Maintenance by Processes, continuously

improved and certified

� People are valued, highly trained and continuously developed with a focus on

the multidisciplinary approach and team spirit

� ANEEL Benchmark Company

CTEEP’s operational strategy is based on excellence in the rendering of services with a focus on the continuou s creation of value for the clients

CTEEP’s operational strategy is based on excellence in the rendering of services with a focus on the continuou s creation of value for the clients

26

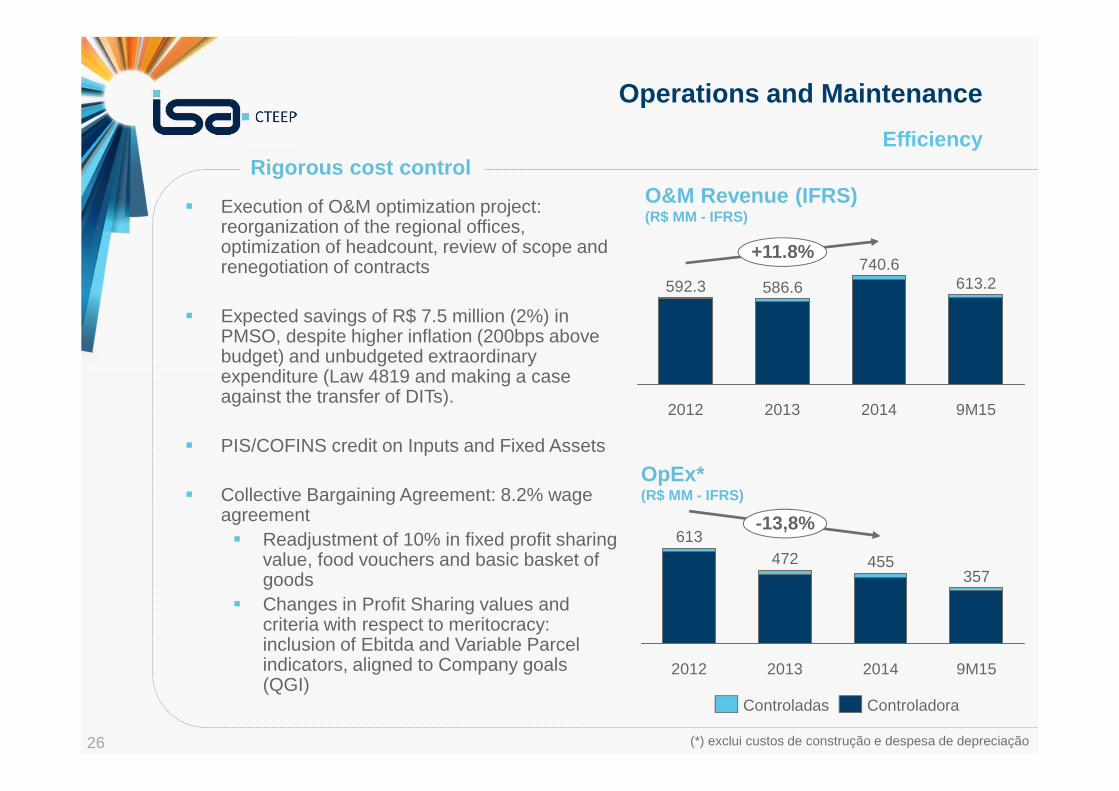

Efficiency

� Execution of O&M optimization project: reorganization of the regional offices, optimization of headcount, review of scope and renegotiation of contracts

� Expected savings of R$ 7.5 million (2%) in PMSO, despite higher inflation (200bps above budget) and unbudgeted extraordinary expenditure (Law 4819 and making a case against the transfer of DITs).

� PIS/COFINS credit on Inputs and Fixed Assets

� Collective Bargaining Agreement: 8.2% wage agreement � Readjustment of 10% in fixed profit sharing

value, food vouchers and basic basket of goods

� Changes in Profit Sharing values and criteria with respect to meritocracy: inclusion of Ebitda and Variable Parcel indicators, aligned to Company goals (QGI)

Operations and Maintenance

Rigorous cost control

2012

613-13,8%

9M15

357

2014

455

2013

472

(*) exclui custos de construção e despesa de depreciação

+11.8%

9M15

613.2

2014

740.6

2013

586.6

2012

592.3

O&M Revenue (IFRS)(R$ MM - IFRS)

OpEx* (R$ MM - IFRS)

Controladas Controladora

27

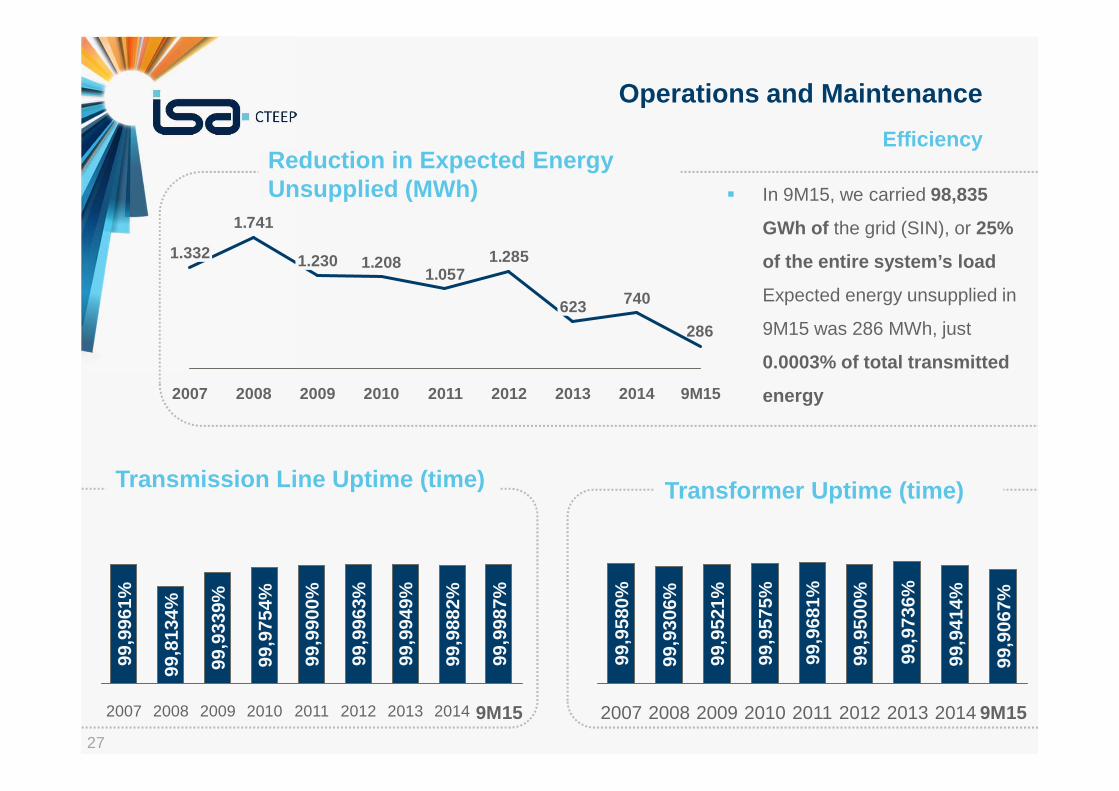

� In 9M15, we carried 98,835

GWh of the grid (SIN), or 25%

of the entire system’s load

Expected energy unsupplied in

9M15 was 286 MWh, just

0.0003% of total transmitted

energy

Efficiency

Operations and Maintenance

Transformer Uptime (time)Transmission Line Uptime (time)

2009

99,9

339%

2008

99,8

134%

2007

99,9

961%

9M15

99,9

987%

2014

99,9

882%

2013

99,9

949%

2012

99,9

963%

2011

99,9

900%

2010

99,9

754%

200999

,952

1%2008

99,9

306%

2007

99,9

580%

9M15

99,9

067%

2014

99,9

414%

2013

99,9

736%

2012

99,9

500%

2011

99,9

681%

2010

99,9

575%

286

740

1.2851.057

1.208

1.741

2009

1.230

20082007

1.332

2013 9M152014201220112010

623

Reduction in Expected Energy Unsupplied (MWh)

28

Return

� Strategy for supporting global returns through inclusion of a cost reduction goal in the 2015 Budget

� Internalization of inspection and commissioning

� Prioritization in the use of inventory, improvement in procurement process.

� Execution with real gain of 5% on budget (goal)

Investments

Discipline in the allocation of resources

CapEx executed(R$ MM - realizado)

688 591

264225

219289 132168

299

9M152014

-27,0%

507

2013

815

2012

952

ControladasControladora

� Requests lodged with ANEEL� with immediate effect, begin the administrative process for revising the Price Bank with

respect to items included in the Resolutions.� issue new Authorization Resolutions (REAs) based on “market prices” quoted by CTEEP

and already shown in the administrative processes together with a new schedule for the execution of work

� Reduced financial execution in the Jan-Sep/15 period

29

Governance

� Total investment of R$ 6.2 bi, CTEEP capital injections of R$ 1.6 bi

� 15/16 RAP of R$ 682.8 million (45% total RAP total*)

� 9M15 EBITDA of R$ 403,1 million (margin of 88%)

� Dividends of R$ 27.6 million paid to CTEEP in 2015 (IEMadeira, IEJapi and Evrecy)

IEGaranhuns� Schedule for startup in operations of

projects in november 2015

Subsidiaries

Portfólio totalmente operacional em 2015

ES

PBPEA

L

IEMadeira� Conclusion of work in May 2014� Financial–economic rebalancing for Lot D requested of ANEEL

� Surcharge: R$ 342 million / Loss of R$ 251milhões in RAP / Readjustment of 26.8% in RAP

(*) Não ponderado pela participação nas coligadas (**) Ebitda Regulatório total das subsidiárias

30

Fair Value

� With the purpose of reducing tariffs, MP 579

modified the method used to remunerate

investments, divided into: (i) sufficient revenue to

cover costs plus a profit margin for operations and

maintenance; and (ii) indemnification of assets

not fully amortized

� CTEEP’s decision was essential for 100%

adherence of the transmission companies and

was based on trust in Brazilian institutions and

the creation of value through the fair

indemnification of the unamortized assets with a

view to recovering the Company’s investment

capacity and long-term growth

Indemnification

Extention of Conecession Agreement

40%60%

RAP(R$ million)

Indemnification(R$ million)

358158

495

Pre MP 579

2,150

1,655

-76%

Post MP 579

516

36%

RBNI2.891

RBSE5.186

64%

31

Fair Value

Indemnification

Background to the Process

MP 579Sep/12

Law 12.783Jan/13

RBNIJan/13

RBSE

ANEEL Resolution

583Dec/13

EvaluationReportAug/14

ANEEL Ratification

Decision onCriteria(MME)

ANEELInspection

Oct/14

3.6053.7263.7424.9385.0315.186

121161.19693155

Post Ins.Rep. Revision

Report Filed

InspectionMont. Rep.

NT SFF196/2015

Inspection Monitoring

Report

-24%

Revised Report

CTEEP Current Difference ANEEL

Timeline of the Indemnification Amount (R$ million)

32

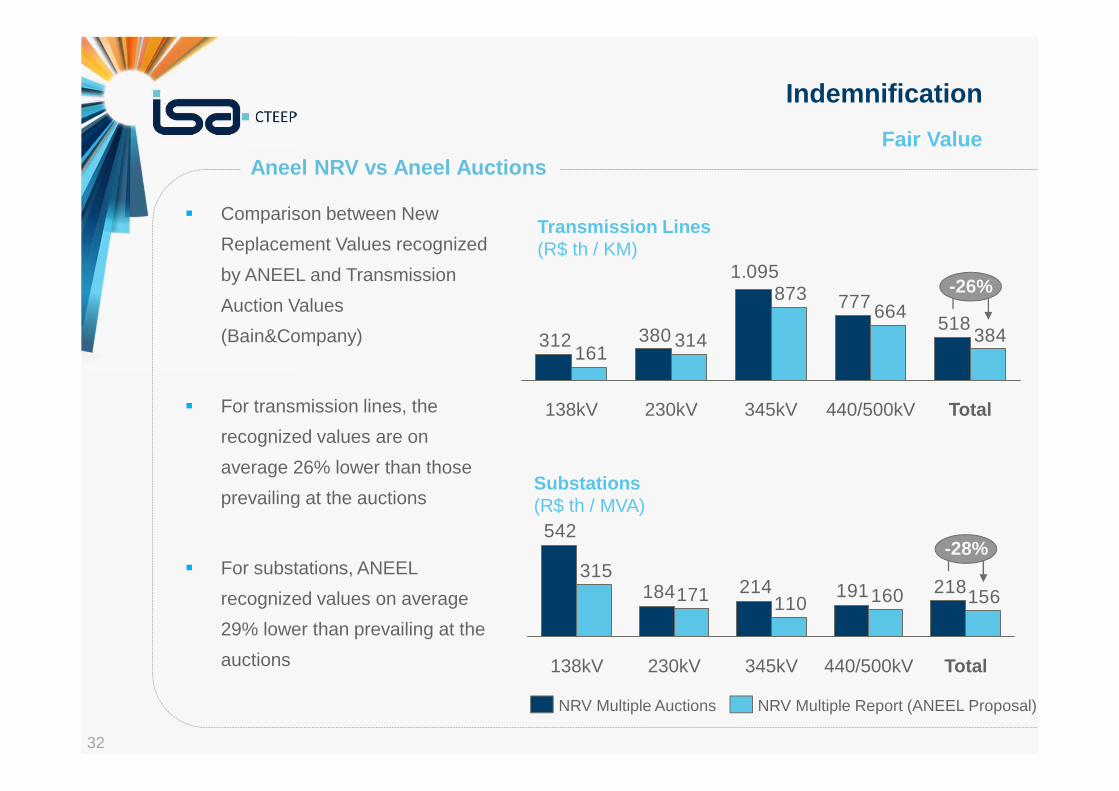

Fair Value

� Comparison between New

Replacement Values recognized

by ANEEL and Transmission

Auction Values

(Bain&Company)

� For transmission lines, the

recognized values are on

average 26% lower than those

prevailing at the auctions

� For substations, ANEEL

recognized values on average

29% lower than prevailing at the

auctions

Indemnification

Aneel NRV vs Aneel Auctions

518777

1.095

380312 384664

873

314161

440/500kV Total138kV 230kV 345kV

-26%

NRV Multiple Report (ANEEL Proposal)NRV Multiple Auctions

218191214184

542

156160110171315

440/500kV345kV Total138kV 230kV

-28%

Substations(R$ th / MVA)

Transmission Lines(R$ th / KM)

33

Fair Value

� Conditions for extension of the concession imply net reduction of 45% in Revenue CTEEP ( RAP after renovation + annuities equivalent to SE compensation at $ 3.7 billion

� Conditions well below those of the Eletrobras companies ( 17% ) indicate the need to persist in discussions with ANEEL on calculation criteria

Indemnification

Valor Glosa

CTEEP 2.208 522 2.891 3.743 -28% 201 494 1.217 -45%

FURNAS 2.308 637 2.878 8.999 -16% 200 1.188 2.026 -12%

CHESF 1.401 524 1.587 5.064 -10% 110 669 1.303 -7%

Eletronorte 1.115 280 1.682 2.633 -10% 117 348 744 -33%

Eletrosul 920 411 1.986 1.007 -5% 138 133 682 -26%

Grupo Eletrobras 5.745 1.852 8.133 17.704 -13% 565 2.338 4.755 -17%

Total 7.952 2.374 11.024 21.446 -16% 766 2.832 5.972 -25%

Concessionárias

Base: Dez/2012

Nova RAP

NI(B)

SE(com IR)

(D)

Com IR em SE

(A+B+D)∆%

Receita Anual Permitida (RAP)

NIPós-

renovação(A)

Pré-renovação

SE

Indenizações Anuidades

CTEEP indemnity vs other utilities

34

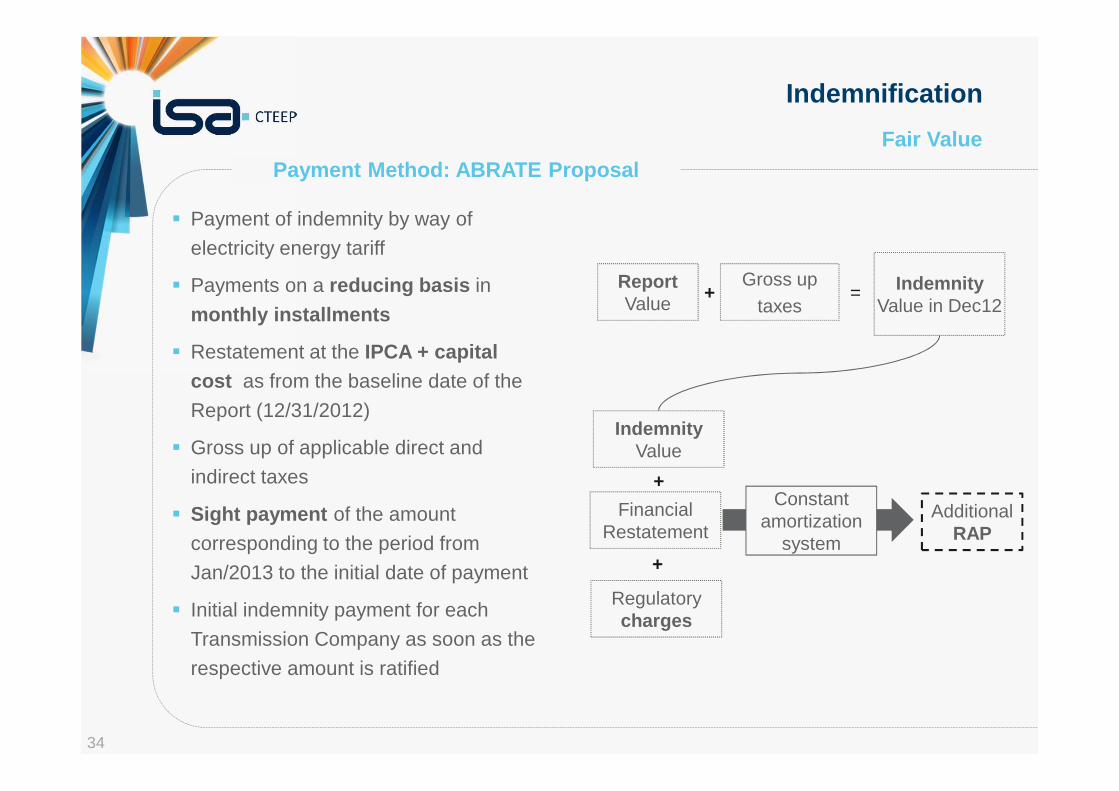

Fair Value

Indemnification

� Payment of indemnity by way of

electricity energy tariff

� Payments on a reducing basis in

monthly installments

� Restatement at the IPCA + capital cost as from the baseline date of the

Report (12/31/2012)

� Gross up of applicable direct and

indirect taxes

� Sight payment of the amount

corresponding to the period from

Jan/2013 to the initial date of payment

� Initial indemnity payment for each

Transmission Company as soon as the

respective amount is ratified

ReportValue

Financial Restatement

Gross uptaxes

IndemnityValue in Dec12

+

+ =

IndemnityValue

AdditionalRAP

Constant amortization

system

+

Regulatorycharges

Payment Method: ABRATE Proposal

35

Considerations

Legal Aspects

Transfer of more than 50% of the assets covered by the CTEEP concession

� Legal insecurity triggered by two regulatory changes in less than three years

� Possible loss of the concession’s purpose

Technical Aspects Transfer of all the DIT

� Significant part of CTEEP DIT bear no similarity to the traditionaldistribution networks, the example of the complementary network operated by the ONS (National Grid Operator)

� DIT cannot be analyzed simply on the basis of voltage but rather on the basis of the systematic function they exercise

Indemnification

Indemnification for all investments executed post-2012 based on ANEEL’s Price Bank(R$ 356 million )

� According to the Federal Audit Court (TCU), the Price Bank constituted in 2008 has not be updated

� Does not take into account the tax levy� The effective restated cost of R$ 1,398 million (nominal value of R$

624 million, restated for inflation and regulatory WACC with taxes)

Revenue from O&M

Decrease of Revenue does not impact economic/financial balance

� CTEEP’s current RAP includes a 35% quality premium and an O&M margin of 10% pursuant to NT ANEEL 383/2012

� Indemnification for the loss of these future results is necessary to ensure that the economic and financial balance of the agreement is maintained. Expected impact amounts to R$ 688 million

� Decrease in revenue income could trigger early repayment of loans and sureties

OthersTransmission and Distribution companies decide other aspects

� Necessary prior definition for equipment replacement; inventory; service agreements signed by the Transmission Companies; Labor Relations and cost, and regularization with transfer of properties

Technical Note

Summary of CTEEP’s contributions to Public Hearing s

Transfer of Other Transmission Installations - DIT

36

Reduction

Supplementary Retirement Act 4819 � Favorable decision of the Supreme Court in April of 4819 / 2015 ( defines the regular courts

as competent to proceed to judgment ) � Association of Retired CESP Foundation filed an appeal against the decision and obtained

injunctive relief (maintenance of leaf payment until evaluation by regular courts )� In 14/10 the Supreme Court ruled on the embargo and confirmed the jurisdiction of the

ordinary courts and upheld the injunction of the Association of Retirees

Collection Suit 4819 � There was judgment of the Collection CTEEP proposed action against the State of São

Paulo. The appeal of CTEEP was welcomed defining the jurisdiction of the regular courts , as well as a right to reimbursement of expenses 4,819 . CTEEP will appeal for a better definition of funds entitled to reimbursement in sentencing

Process Eletropaulo / Eletrobras� Expert report of 16 September 2015 confirmed the Company's thesis

Contingencies

Status

(*) ex provisão de R$ 0,5 MM

37

Awards and Best Practices

� CTEEP is the first electricity company to have the Quality Assessment Certification , an international certification granted by The Institute of Internal Auditors (IIA ) , which aims to recognize the quality of the areas of internal audit organizations.

� A research and development project (R & D ) developed by CTEEP in partnership with the Institute for Energy and Environment ( IEE ) at USP and CESP won recognition in the 1st Innovation and Technology Award Solar Brazil . The study , which focuses on analyzing the impacts of photovoltaics in the electrical system , was awarded in the category " Award for best academic design innovation 2015 "

� CTEEP was among the best companies in the yearbook Época Business 360, with the 47th position among the 250 best . The Company stood out in the sector in two dimensions : Innovation Capacity ( 5th place ) and HR Practice ( 4th place )

Awards

38

Financial Results 3Q15

39

� Allowed Annual Revenue (RAP) – increase of 16.4%;

� Increase of 29.2% in Net Revenue;

� EBITDA of R$ 343.9 million in 3Q15 and EBITDA Margin of 75.2%;

� Net Income of 3Q15 reached R$ 276.3 million, an incr ease of 97.1%;

� Decline of 24.0% in consolidated net debt in 3Q15 i n relation to the end of 2014 and amounting to R$ 537.8 million;

� Dividends of R$ 27.6 million paid by Evrecy, IEJapi a nd IEMadeira;

� Holding of a Public Hearing on the issue of Other T ransmission Installations (DIT).

� Confirmation of CTEEP’s Long Term Brazilian Corpora te Rating of ‘AA+(bra)’ with stable outlook;

� Amount and method of payment of RBSE still pending. Settlement now expected as from July/2016.

IFRS Highlights 3Q15

40

IFRS - Gross Consolidated Revenue

+28,3%

3Q15 504,6

Others 0,1

AssetsConcession

72,6

O&M 16,6

Infrastructure 22,1

3Q14 393,2

+23,8%

9M15 1.104,5

9M14 891,9

� Infrastructure: increase of 28.7%, largely due to the increase in upgrading projects, substation construction, transmission line reconstruction and the installation of capacitor banks at CTEEP and the controlled subsidiaries of Serra do Japi

� O&M: increase of 7.7% largely due to the positive variation in IPCA and IGP-M indices used to restate O&M revenue comprising the 14/15 RAP to find the 15/16 RAP

� Remuneration of Concession Assets: increase of 76.8% due to: (i) average balance of financial assets for expected realization of construction values and indemnification in favor of CTEEP and increased due to monetary restatement and the startup of new investments during the period and (ii) the monetary restatement of financial flows for the 2015/2016 cycle with respect to CAAE (Annual Cost of the Electricity Assets) installment

� Others: increase of R$ 0.3MM in rents and a decline of R$ 0.2 MM in third party services

Aumento de 28,2%(R$ millions)

ConsolidatedCompany

41

Regulatory – Consolidated Gross Revenue

+9.8%

3Q15 281.0

Others 0.1

Theelectrical

InterconnectionRevenues

25.0

3Q14 255.9

+12.6%

9M15 746.0

9M14 662.5

Increase of 9.8% in 3Q15

Company Consolidated

� Electric Energy Network Uptime :i. monetary restatement of the 2014/2015

RAP cycle as the basis for the 2015/2016 RAP cycle (IPCA 8.47% and IGP-M 4.11%)

ii. inclusion of the Annual Cost of Facilities and Assets (CAIMI of R$ 28.7 MM in the 2015/2016 cycle) receivable and

iii. startup of operations of new investments, increasing the RAP by R$ 30.8 MM for the 2015/2016 cycle

� Other Revenues :i. increase of R$ 0.3 MM in rents and a

decline of R$ 0.2 MM in third party services

(R$ millions)

42

Growth of 29.2% in Net Operating Revenue for 3Q15

IFRS - Consolidated Net Revenue

� Deductions: in 3Q15, there was an increase of 20.1% compared with 3Q14, due to revenue taxes which match the variation in operating revenue, and offset by the rate established for PIS and COFINS (3.65%) charges levied on the subsidiaries which adopt the presumed profit tax regime

� Growth of 24.1% in Net Revenue for 9M15 compared with the same period in 2014.

Deduction3Q15

-47,4

GrossRevenue

3Q15504,6

Net Revenue

3Q15457,2

9M15 989,9

9M14 797,4

+24,1%

Company Subsidiaries

(R$ millions)

43

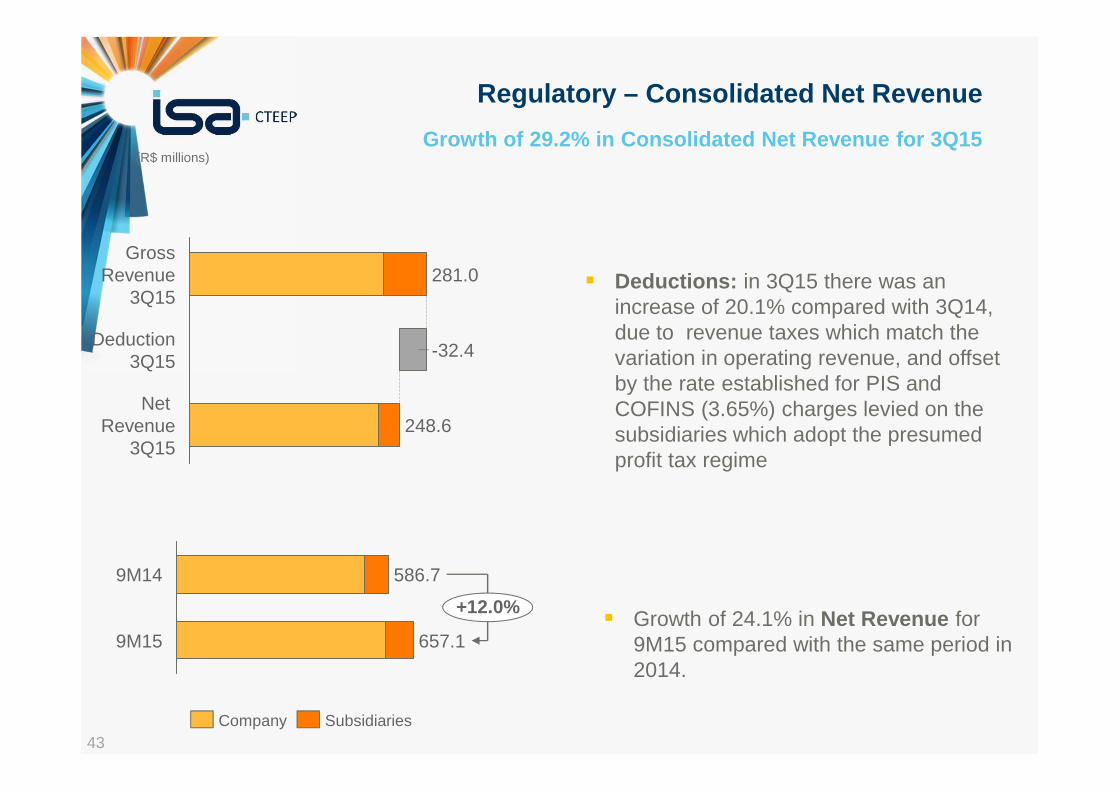

Growth of 29.2% in Consolidated Net Revenue for 3Q15

Regulatory – Consolidated Net Revenue

� Deductions: in 3Q15 there was an increase of 20.1% compared with 3Q14, due to revenue taxes which match the variation in operating revenue, and offset by the rate established for PIS and COFINS (3.65%) charges levied on the subsidiaries which adopt the presumed profit tax regime

� Growth of 24.1% in Net Revenue for 9M15 compared with the same period in 2014.

Deduction3Q15

248.6Net

Revenue3Q15

-32.4

GrossRevenue

3Q15281.0

9M15 657.1

+12.0%

9M14 586.7

Company Subsidiaries

(R$ millions)

44

IFRS - Trend in Consolidated O&M Costsand Expenses

9,4

8,0

7,1

+4.7%

3Q15 126.5

Others

MaterialServices

Personnel

3Q14 120.8

+10.9%

9M15 362.9

9M14 327.2

Increase of 4.7% in 3Q15

� Personnel: growth of 11.1% due to the collective bargaining agreement resulting in an 8.2% increase granted in August 2015, backdated to June 2015, termination costs with the restructuring of the technical area and the greater use made of company’s medical services during the period

� Services/Material: increase of 39.2% in services and materials, above all due to the non-recurring recovery of costs in 3Q14 which reduced the comparative base for 3Q15

� Others: reduction of 34.7% in contingency expenses, reflecting the work on restatement of amounts and probabilities for success in legal actions which had inflated contingencies in 3Q14.

(R$ millions)

SubsidiariesCompany

45

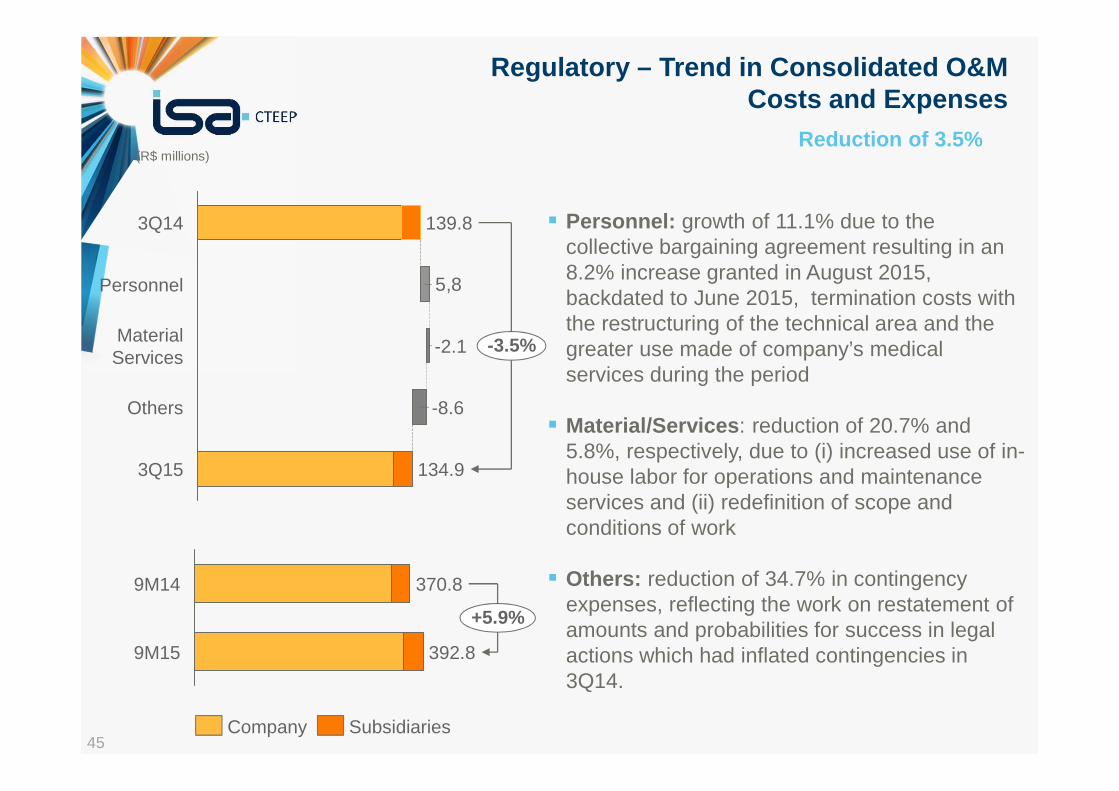

Regulatory – Trend in Consolidated O&M Costs and Expenses

5,8

-3.5%

3Q15 134.9

Others -8.6

MaterialServices

-2.1

Personnel

3Q14 139.8

+5.9%

9M15 392.8

9M14 370.8

� Personnel: growth of 11.1% due to the collective bargaining agreement resulting in an 8.2% increase granted in August 2015, backdated to June 2015, termination costs with the restructuring of the technical area and the greater use made of company’s medical services during the period

� Material/Services : reduction of 20.7% and 5.8%, respectively, due to (i) increased use of in-house labor for operations and maintenance services and (ii) redefinition of scope and conditions of work

� Others: reduction of 34.7% in contingency expenses, reflecting the work on restatement of amounts and probabilities for success in legal actions which had inflated contingencies in 3Q14.

Reduction of 3.5%

Company Subsidiaries

(R$ millions)

46

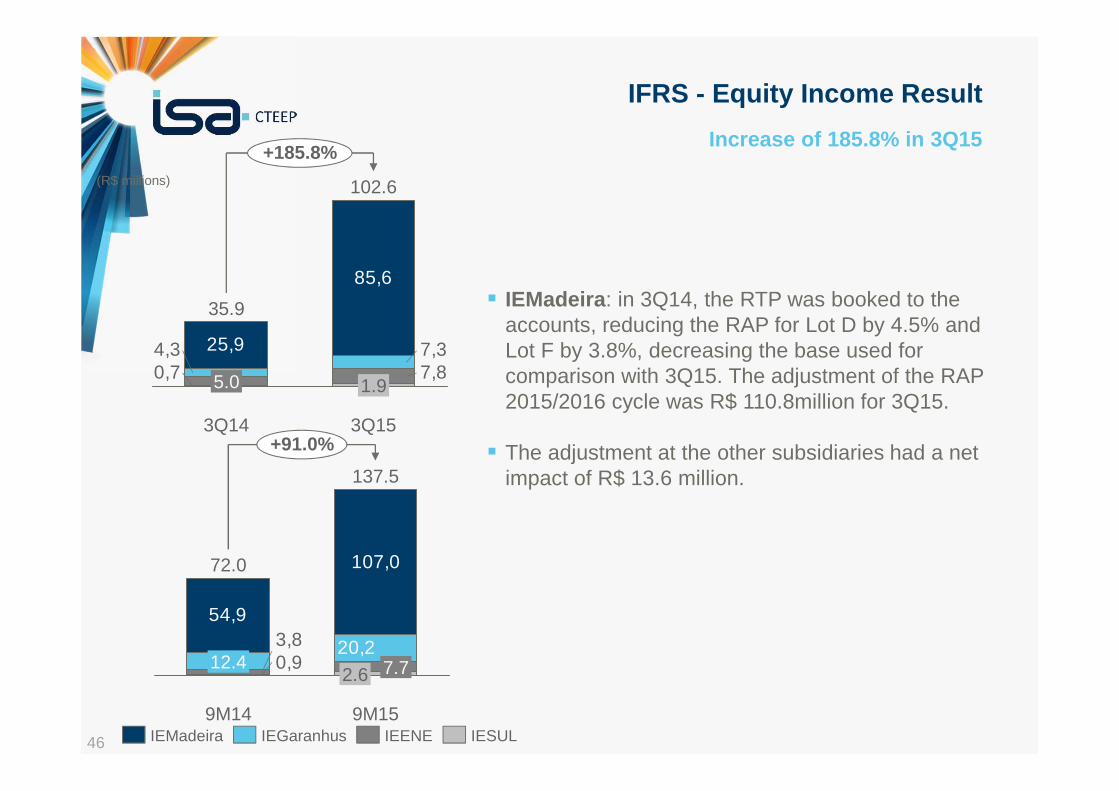

IFRS - Equity Income Result

� IEMadeira : in 3Q14, the RTP was booked to the accounts, reducing the RAP for Lot D by 4.5% and Lot F by 3.8%, decreasing the base used for comparison with 3Q15. The adjustment of the RAP 2015/2016 cycle was R$ 110.8million for 3Q15.

� The adjustment at the other subsidiaries had a net impact of R$ 13.6 million.

Increase of 185.8% in 3Q15

25,9

85,6

0,7 7,87,34,3

+185.8%

3Q15

102.6

1.9

3Q14

35.9

5.0

IESULIEENEIEGaranhusIEMadeira

54,9

107,0

0,93,8 20,2

9M15

+91.0%

137.5

2.6 7.7

9M14

72.0

12.4

(R$ millions)

47

Regulatory – Equity Income Result

Increase of 45.9% in 3Q15-45.9%

3Q15

16.5

-0.5

17.0

3Q14

30.5

-0.2

30.7

54.2

9M15

+71.0%

-0.1 -0.6

54.9

9M14

31.7

-0.6 -1.5

33.8

IESULIEENEIEMadeira

� IEMadeira : Reduction of 44.6% in the result due to the booking of adjustments to the RAP 2015/2016 cycle: (i) booking of the RTP for 2014, impacting the 2015/2016 cycle; (ii) booking of 3/12 of a negative PA.

� In addition, the result for IEMadeira was negatively affected due to the increase in financial expenses as a result of greater leverage as a result of debenture issues.

(R$ millions)

48

IFRS - Consolidated Financial Result

-1,6

3Q15 -8.0

Others 2.0

Interest/expenses on loans

0.5

Monetary(net)

InterestReceivable

-8.0

3Q14 -0.9

9M15 -5.6

9M14 15.6

� Reduction in monetary restatement revenue and from interest in 3Q15 totaling R$ 7.3 million, compared with R$ 16.8 million in 3Q14, reflecting restatement at the IPCA + 5,59% of accounts receivable by reversal – Law 12.783

RBNI receivables flow(R$ millions)

Company Subsidiaries

49

Earnings per share were R$ 1.6526 in 3Q15

IFRS - Net Income

442,7

315,8

276,3

140,2

+40.2%

+97.1%

9M159M143Q153Q14

(R$ millions)

50

Earnings per share were R$ 0.3777 in 3Q15

Regulatory – Net Income

(R$ millions)

+6.2%

-28.7%

9M15

198.3

9M14

186.8

3Q15

65.2

3Q14

91.5

51

Consolidated EBITDA post ICVM 527

3Q15 3Q14 1H15 1H14 3T15 3T14 9M15 9M14

Net Income 276.3 140.1 442.7 315.8 65.2 91.5 198.3 186.8

Income tax and social contribuition 49.4 21.3 89.4 67.0 47.3 6.2 87.8 36.2

Financial Results 8.0 0.9 5.6 (15.6) 8.0 0.9 5.6 (15.6)

Depreciation and Amortization 10.2 10.5 30.7 31.0 21.0 19.6 61.5 57.4

EBITDA ICVM 527/12 343.9 172.7 568.3 398.3 141.4 118.2 353 .2 264.8Ebitda Margin

EBITDA Margin 75.2% 48.8% 57.4% 49.9% 56.9% 51.9% 53.7% 45. 1%

REGULATORYEBITDA (R$ million)

IFRS

52

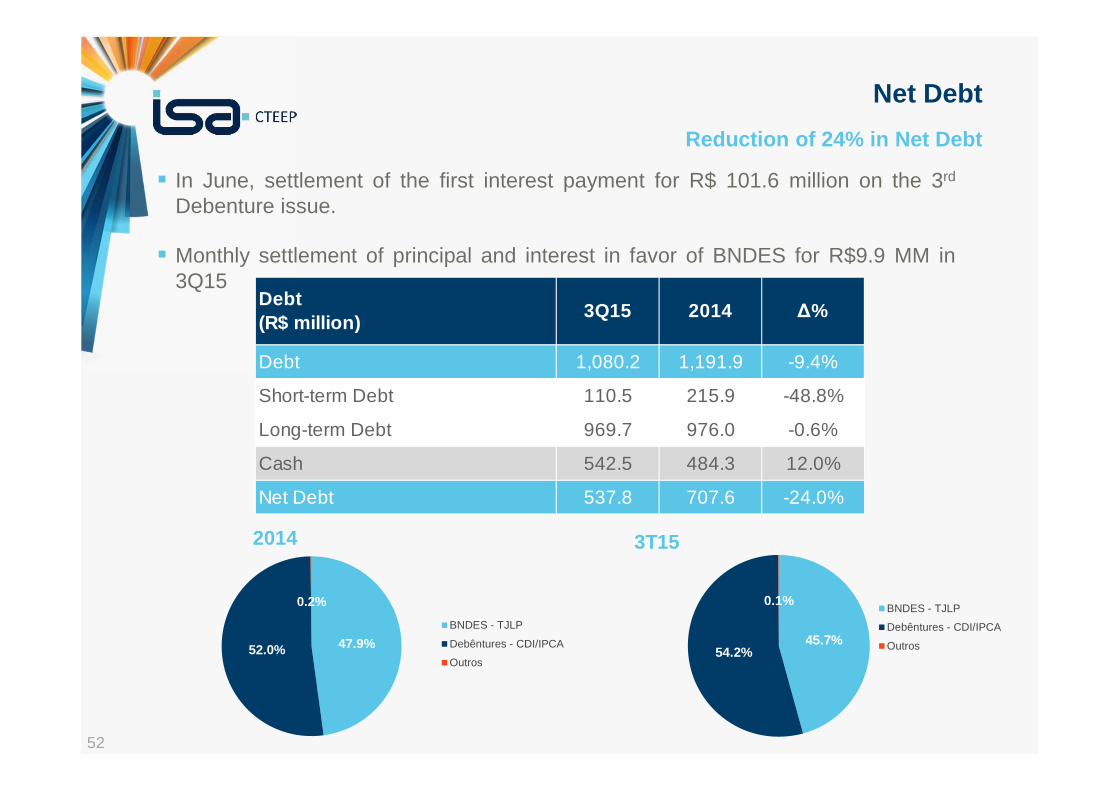

Reduction of 24% in Net Debt

Net Debt

� In June, settlement of the first interest payment for R$ 101.6 million on the 3rd

Debenture issue.

� Monthly settlement of principal and interest in favor of BNDES for R$9.9 MM in3Q15

3T152014

BNDES - TJLP

Debêntures - CDI/IPCA

Outros

BNDES - TJLP

Debêntures - CDI/IPCA

Outros

Debt 1,080.2 1,191.9 -9.4%

Short-term Debt 110.5 215.9 -48.8%

Long-term Debt 969.7 976.0 -0.6%

Cash 542.5 484.3 12.0%

Net Debt 537.8 707.6 -24.0%

Debt(R$ million)

3Q15 2014 ∆%

47.9% 52.0%

0.2%

45.7% 54.2%

0.1%

53

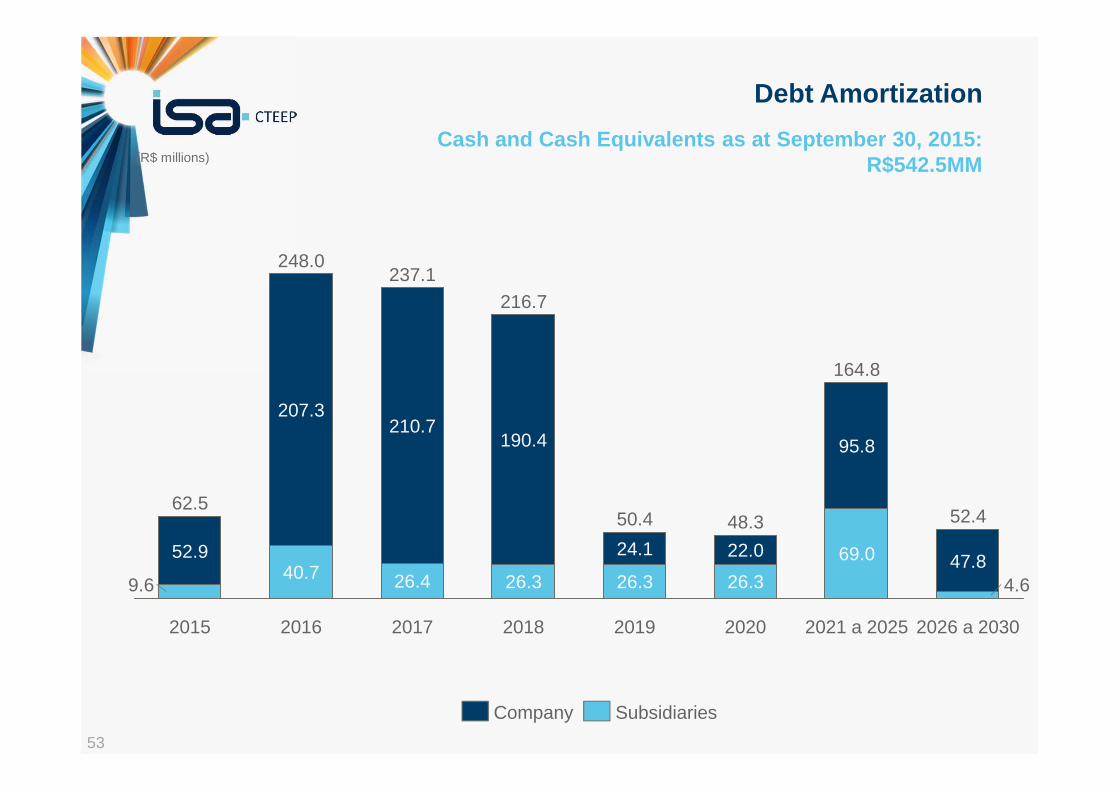

Cash and Cash Equivalents as at September 30, 2015: R$542.5MM

Debt Amortization

2026 a 2030

52.4

4.647.8

2021 a 2025

164.8

69.0

95.8

2020

48.3

26.3

22.0

2019

50.4

26.3

24.1

2018

216.7

26.3

190.4

2017

237.1

26.4

210.7

2016

248.0

40.7

207.3

2015

62.5

9.6

52.9

SubsidiariesCompany

(R$ millions)

54

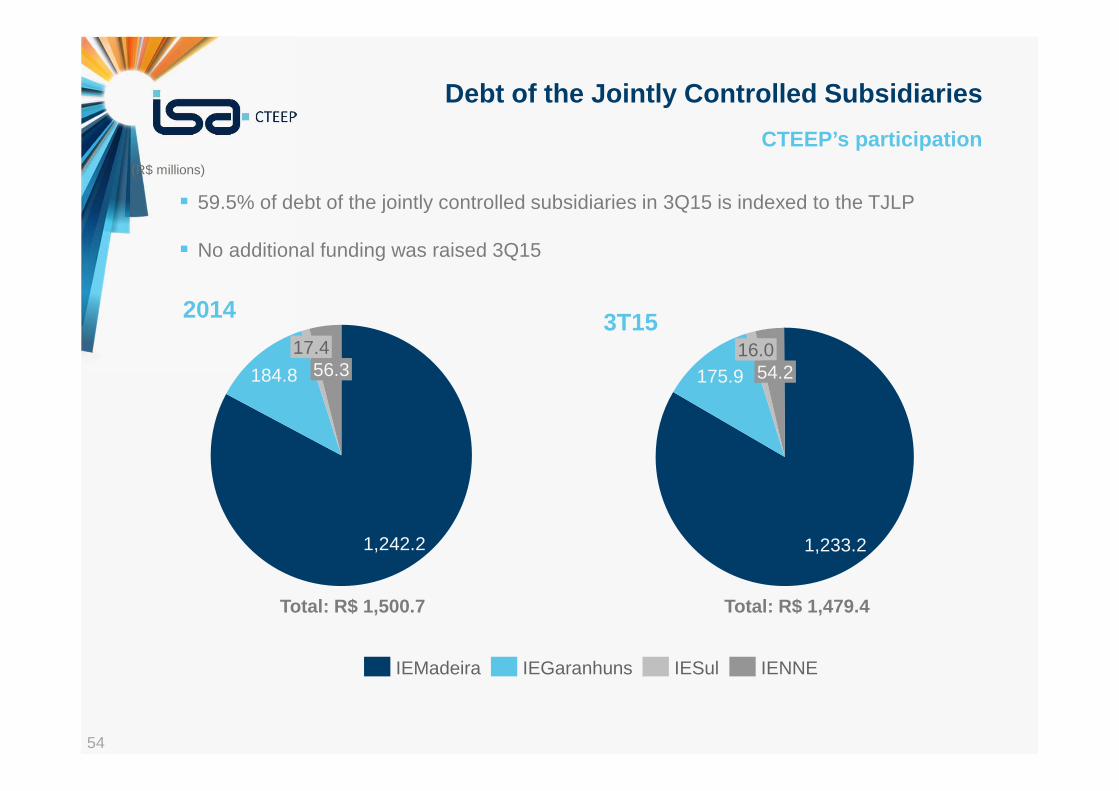

CTEEP’s participation

Debt of the Jointly Controlled Subsidiaries

Total: R$ 1,479.4Total: R$ 1,500.7

� 59.5% of debt of the jointly controlled subsidiaries in 3Q15 is indexed to the TJLP

� No additional funding was raised 3Q15

16.0175.9

1,233.2

54.2

IESulIEGaranhunsIEMadeira IENNE

56.317.4

184.8

1,242.2

3T152014

(R$ millions)

55

Closing prices of TRPL4 in 3Q15 was R$ 40.80

Capital Markets Performance

Principal events:

� CTEEP’s market cap. at the end of September 2015 was R$ 6.715MM;

� Average daily traded volume in 9M15 was R$12.5 MM

� Average daily trades – 1,781

� TRPL4 trade on all the days the Exchange was open for business

-35

-25

-15

-5

5

15

Jan/15 Fev/15 Mar/15 Abr/15 Mai/15 Jun/15 Jul/15 Ago/15 Set /15

Volume TRPL4 TRPL3 TRPL4 IBOVESPA IEE Volume Médio Diário TRPL4

-5,10%-9,89%

-1,69%-2,50%

R$ 12,5 Milhões

56

Q&A

57

THANKS

Investor Relations

� Tel: +55 11 3138-7557

� www.cteep.com.br/

Canal Linha Ética

� canalconfidencial.com.br/linhaeticacteep ou pelo telefone 0800 777 0775

58