apca farm policy: where do we go from here? daryll e. ray university of tennessee agricultural...

TRANSCRIPT

AAPP CCAA

Farm Policy: Where Do We Go Farm Policy: Where Do We Go From Here?From Here?

Daryll E. RayUniversity of Tennessee

Agricultural Policy Analysis Center

2006 AgOutlook ConferenceLSU AgCenter

Lod Cook Conference Center, Baton Rouge, LA January 27, 2006

AAPP CCAA

Lost Our Policy BearingsLost Our Policy Bearings

• Without a clue and highly impressionable

– When it comes to farm policy, we seem not to have a clear idea about anything including:

• what the “problem” is or

• what objectives are to be achieved

– So we are willing to believe anything!

AAPP CCAA

We Seem Willing to Believe that:We Seem Willing to Believe that:

• Staple crops are not sufficiently important to have emergency reserves(oil is sufficiently important)

• Less than full use of farm productive capacity is inefficient (SOP to not use full capacity in other sectors—currently at 77% of capacity)

• Farmers can extract billions of dollars for commodity programs—so they do

• Hence, commodity programs are a waste– do away with them or– pay out the money on some other basis

AAPP CCAA

Historical Policy ComponentsHistorical Policy Components

• Policy of Plenty: Ongoing public support to expand agricultural productive capacity through research, extension and other means

• Policy to Manage Plenty: Mechanisms to manage productive capacity and to compensate farmers for consumers’ accrued benefits of productivity gains

AAPP CCAA

Why Chronic Problems In Ag? Why Chronic Problems In Ag?

• Technology expands output faster than population and exports expand demand– Much of this technology has been paid

for by US taxpayers

• The growth in supply now is being additionally fueled by– increased acreages in Brazil, etc.– technological advance worldwide

AAPP CCAA

Why Chronic Problems In Ag?Why Chronic Problems In Ag?

• In agriculture lower prices do not solve the problem

• Little self-correction on the demand side– People will pay almost anything when food is

short– Low prices do not induce people to eat more

• Little self-correction on the supply side– Farmers tend to produce on all their acreage– Few alternate uses for most cropland– Farmers do not scrimp on the use of yield-

determining inputs

AAPP CCAA

What Was That Again?What Was That Again?

• Supply and demand characteristics of aggregate agriculture cause chronic price and income problems– On average supply grows faster than

demand

– Agriculture cannot right itself when capsized by low prices

– (Always year-to-year random variability)

AAPP CCAA

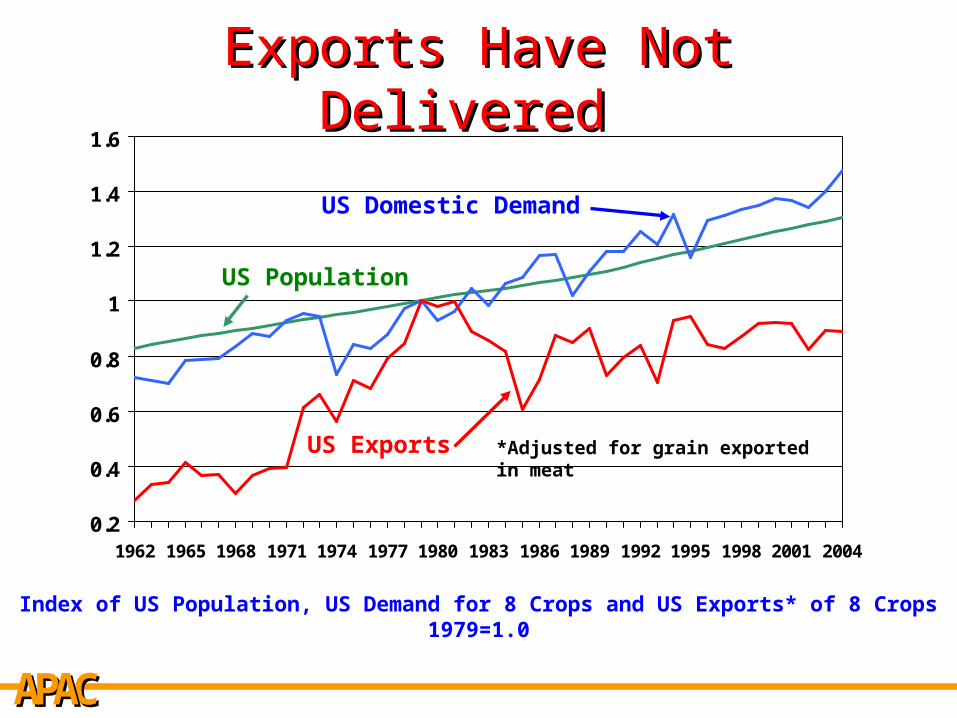

From My Perspective…From My Perspective…• Crop exports did not deliver—will not deliver

• For crop agriculture, timely free—market self-correction is a fantasy

• Emerging agricultural powerhouses: Excess capacity will be a worldwide endeavor in the future

• Farmers version of the “Concentration” game: Buy inputs from few suppliers and sell output to few buyers

• Current US farm programs are not sustainable

• US policy alternatives: The preferable (well, preferable in my opinion), the possible and the likely

AAPP CCAA

Exports Have Not Exports Have Not Delivered Delivered

Index of US Population, US Demand for 8 Crops and US Exports* of 8 Crops1979=1.0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

US Population

US Exports

US Domestic Demand

*Adjusted for grain exported in meat

AAPP CCAA

15 Crop Exports for US and 15 Crop Exports for US and Developing CompetitorsDeveloping Competitors

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Developing competitors: Argentina, Brazil, China, India, Pakistan, Thailand, Vietnam15 Crops: Wheat, Corn, Rice, Sorghum, Oats, Rye, Barley, Millet, Soybeans, Peanuts, Cottonseed, Rapeseed, Sunflower, Copra, and Palm Kernel

Th

ou

san

d M

etri

c T

on

s

US

Developing Competitors

AAPP CCAA

U.S. Total Ag Exports Have Grown Slower U.S. Total Ag Exports Have Grown Slower Than Total Ag ImportsThan Total Ag Imports

0

10

20

30

40

50

60

70

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Ag Exports

Ag Imports

Bil

lio

n D

oll

ars

AAPP CCAA

From My Perspective…From My Perspective…• Crop exports did not deliver—will not deliver

• For crop agriculture, timely free—market self-correction is a fantasy

• Emerging agricultural powerhouses: Excess capacity will be a worldwide endeavor in the future

• Farmers version of the “Concentration” game: Buy inputs from few suppliers and sell output to few buyers

• Current US farm programs are not sustainable

• US policy alternatives: The preferable (well, preferable in my opinion), the possible and the likely

AAPP CCAA

40

60

80

100

120

1996 1997 1998 1999 2000

Acreage Response toAcreage Response toLower Prices?Lower Prices?

Ind

ex (

1996

=10

0)

Four Crop Acreage

Four Crop Price Adjusted for Coupled and Decoupled Payments

Four Crop Price Adjusted for Coupled Payments Four Crop Price

Between 1996 and 2000• Aggregate US corn, wheat, soybean, and cotton acreage changed little• While “prices” (take your pick) dropped by 40, 30 or 22%

AAPP CCAA

40

60

80

100

120

1996 1997 1998 1999 2000 2001 2002 2003 2004

Acreage Response toAcreage Response toLower Prices?Lower Prices?

Acreage Response toAcreage Response toLower Prices?Lower Prices?

Ind

ex (

1996

=10

0)

Four Crop Acreage

Four Crop Price

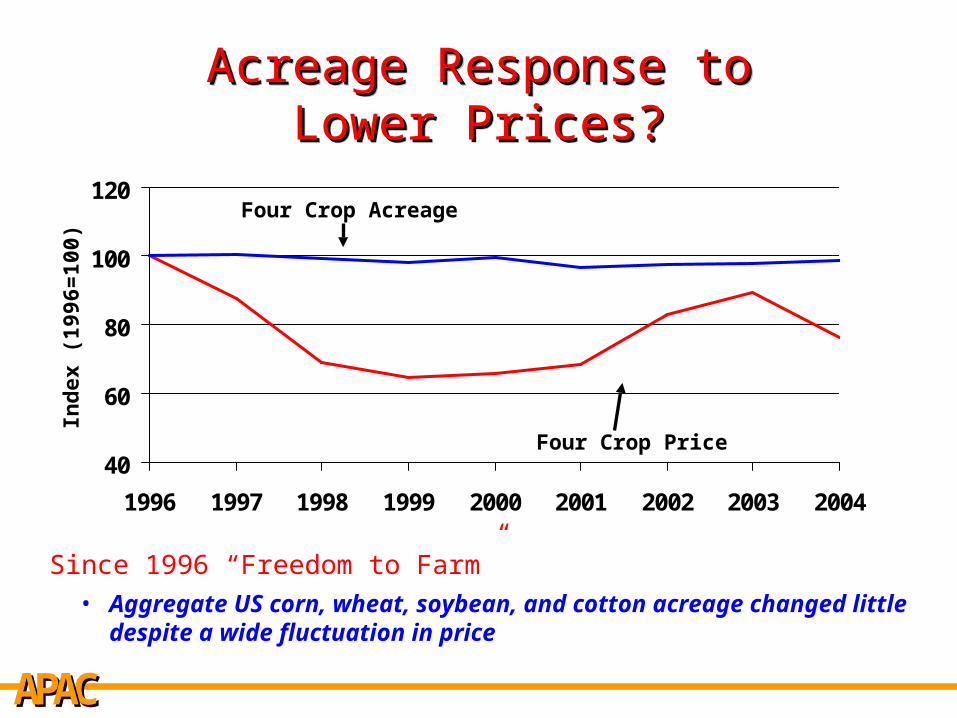

Since 1996 “Freedom to Farm”• Aggregate US corn, wheat, soybean, and cotton acreage changed little

despite a wide fluctuation in price

AAPP CCAA

Canada: Farmland PlantedCanada: Farmland Planted

0

10

20

30

40

50

60

70

1981 1986 1991 1996 2001

Mil

lio

n A

cres

Wheat

Barley

Canola

Other Grains

Other Oilseeds

• Canada reduced subsidies in 1990s• Eliminated grain transportation subsidies in 1995• Crop mix changed, total acreage remained flat

AAPP CCAA

Australia: Farmland PlantedAustralia: Farmland Planted

0

10

20

30

40

50

60

1981-85 1986-90 1991-95 1996-00 2001-02

Mil

lio

n A

cres

Wheat

Coarse Grains

Oilseeds

• Australia dramatically reduced wool subsidies in 1991• Acreage shifted from pasture to crops• All the while, prices declined

AAPP CCAA

From My Perspective…From My Perspective…• Crop exports did not deliver—will not deliver

• For crop agriculture, timely free—market self-correction is a fantasy

• Emerging agricultural powerhouses: Excess capacity will be a worldwide creation in the future

• Farmers version of the “Concentration” game: Buy inputs from few suppliers and sell output to few buyers

• Current US farm programs are not sustainable

• US policy alternatives: The preferable (well, preferable in my opinion), the possible and the likely

AAPP CCAA

Worldwide Excess Capacity Will Be The Worldwide Excess Capacity Will Be The Long-run ProblemLong-run Problem

• Dramatic yield increases in other countries– Cargill, Monsanto, John Deere, etc., etc., etc.

• Acreage once in production will be brought back in– Russia, Ukraine and others

• New Acreage– Brazil– China

AAPP CCAA

From My Perspective…From My Perspective…• Crop exports did not deliver—will not deliver

• For crop agriculture, timely free—market self-correction is a fantasy

• Emerging agricultural powerhouses: Excess capacity will be a worldwide creation in the future

• Farmers version of the “Concentration” game: Buy inputs from few suppliers and sell output to few buyers

• Current US farm programs are not sustainable

• US policy alternatives: The preferable (well, preferable in my opinion), the possible and the likely

AAPP CCAA

What Agribusinesses WantWhat Agribusinesses Want

• Volume (paid flat per bushel rate; sell inputs)

• Low Prices (low cost of ingredients)• Price instability (superior information

systems provide profit opportunities)• Reduced regulation of production and

marketing practices (seller-to and buyer-from beware)

• More market power over competitors and their customers/suppliers (Want everyone at a competitive disadvantage)

AAPP CCAA

From My Perspective…From My Perspective…• Crop exports did not deliver—will not deliver

• For crop agriculture, timely free—market self-correction is a fantasy

• Emerging agricultural powerhouses: Excess capacity will be a worldwide creation in the future

• Farmers version of the “Concentration” game: Buy inputs from few suppliers and sell output to few buyers

• Current US farm programs are not sustainable

• US policy alternatives: The preferable (well, preferable in my opinion), the possible and the likely

AAPP CCAA

The US Can’t Go On Like This… The US Can’t Go On Like This… • The current farm programs are too expensive

– Budget boogie man• 100s of billion of dollars of annual deficits—several

trillion dollars over 10 years• Cuts in Farm Programs almost certain

• GAO report and budget considerations are making payment limits vulnerable

• WTO ruling may put LDPs and Counter-Cyclical Payments in jeopardy– Removes ability to compensate for low prices even less

than in 1996 FB

AAPP CCAA

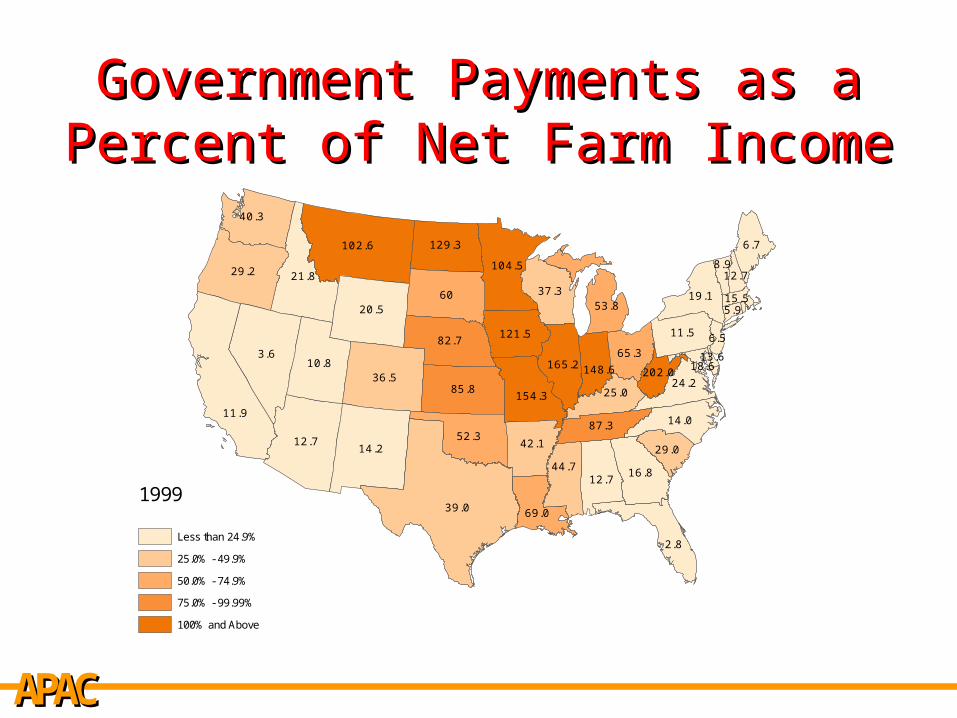

Government Payments as a Government Payments as a Percent of Net Farm IncomePercent of Net Farm Income

12.78.9

5.915.5

6.511.5

19.1

18.613.6

14.0

24.2202.0

53.8

165.2

37.3

87.3

25.0

65.3

148.6

29.0

16.844.712.7

2.8

6.7

69.039.0

42.1

154.3

82.7

60

52.3

85.8

14.2

36.510.8

20.5

12.7

121.5

11.9

3.6

29.2 104.5

129.3102.6

21.8

40.3

Government Payments as a Percentage of Net Farm Income

1999

Less than 24.9%

25.0% - 49.9%

50.0% - 74.9%

75.0% - 99.99%

100% and Above

AAPP CCAA

Government Payments as a Government Payments as a Percent of Net Farm IncomePercent of Net Farm Income

17.820.0

9.813.1

8.113.4

29.8

21.916.1

13.5

21.545.5

105.8

123.0

78.7

55.2

26.2

49.1

105.8

25.5

18.658.614.2

2.1

7.5

88.142.0

55.8

87.0

100.6

56.9

42.6

114.9

16.3

46.915.6

25.5

15.0

97.5

12.3

3.9

36.0 113.3

117.8174.3

28.0

35.3

Government Payments as a Percentage of Net Farm Income

2000

Less than 24.9%

25.0% - 49.9%

50.0% - 74.9%

75.0% - 99.99%

100% and Above

AAPP CCAA

Government Payments as a Government Payments as a Percent of Net Farm IncomePercent of Net Farm Income

10.96.0

5.018.5

7.79.8

15.3

19.710.5

9.7

19.815.6

102.0

117.9

36.3

40.1

23.3

50.280.3

18.6

17.147.414.6

4.4

5.0

80.437.9

47.6

74.7

70.1

58.3

38.8

83.4

12.2

25.910.8

22.6

10.0

86.3

12.2

5.0

27.5 132.9

127.1118.6

18.4

41.8

Government Payments as a Percentage of Net Farm Income

2001

Less than 24.9%

25.0% - 49.9%

50.0% - 74.9%

75.0% - 99.99%

100% and Above

AAPP CCAA

Government Payments as a Government Payments as a Percent of Net Farm IncomePercent of Net Farm Income

34.475.1

12.217.8

5.822.9

74.2

21.17.0

20.9

40.5127.0

57.1

85.1

34.9

53.5

26.9

40.776.5

34.2

35.864.524.3

3.8

22.0

105.221.1

50.5

67.9

66.3

76.3

25.4

136.3

16.4

31.627.8

81.2

5.5

38.3

7.8

15.7

18.4 67.1

80.9151.5

16.7

23.5

Government Payments as a Percentage of Net Farm Income

2002

Less than 24.9%

25.0% - 49.9%

50.0% - 74.9%

75.0% - 99.99%

100% and Above

AAPP CCAA

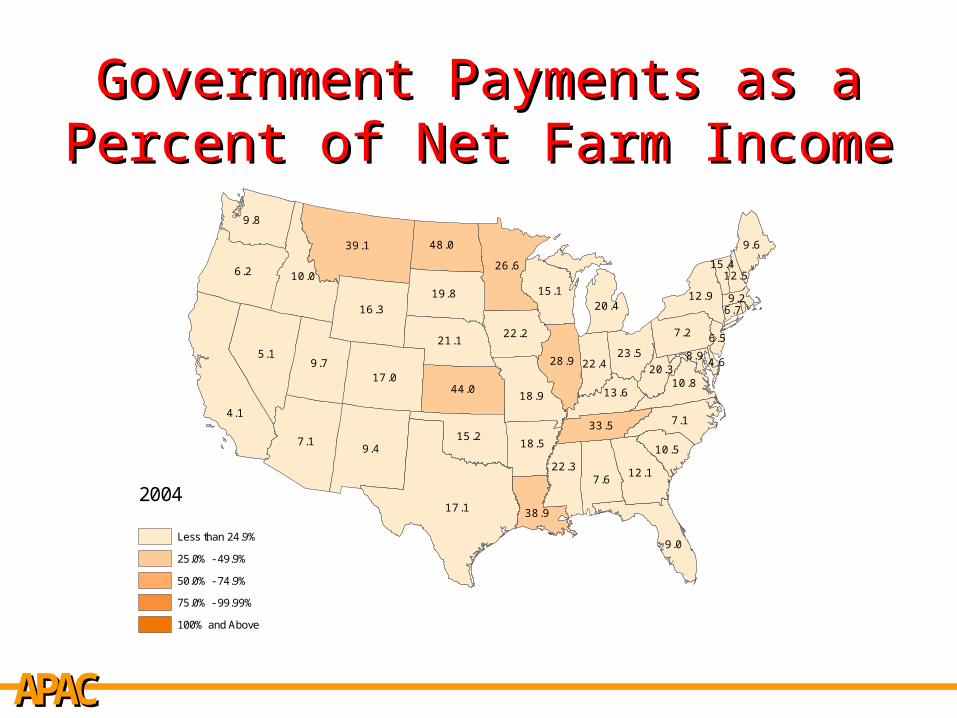

Government Payments as a Government Payments as a Percent of Net Farm IncomePercent of Net Farm Income

12.515.4

6.79.2

6.57.2

12.9

8.94.6

7.1

10.820.3

20.4

28.9

15.1

33.5

13.6

23.522.4

10.5

12.122.37.6

9.0

9.6

38.917.1

18.5

18.9

21.1

19.8

15.2

44.0

9.4

17.09.7

16.3

7.1

22.2

4.1

5.1

6.2 26.6

48.039.1

10.0

9.8

Government Payments as a Percentage of Net Farm Income

2004

Less than 24.9%

25.0% - 49.9%

50.0% - 74.9%

75.0% - 99.99%

100% and Above

AAPP CCAA

The WTO Effect?The WTO Effect?• Are we okay with WTO negotiations that vastly

reduce our ability to set domestic farm policy in this and other countries?

– What is good for General Motors (multinationals)… syndrome

– The whole WTO process shows a complete lack of understanding of the unique characteristics of food and agriculture

– It is a clear case of not understanding that, as important as economics is, it can be trumped by food security and other social objectives in the case of food and agriculture

AAPP CCAA

Farmers’ Role in the Policy DebateFarmers’ Role in the Policy Debate

• One alternative is passively sit by, be co-opted, and let others commandeer the policy agenda– That is exactly what producers have increasingly done since

the mid-eighties!!!

– Crop producers get subsidy-tarred while real subsidy beneficiaries (integrated livestock producers and other users, sellers of inputs and marketers of output) remain above the fray

– Advocating unfettered free markets, promising export growth, or claiming a level playing field as farmers’ magic bullet, etc., ain’t workin.

– And, given the realities of agriculture discussed so far, they hold little promise for the future.

AAPP CCAA

Farmers’ Role in the Policy DebateFarmers’ Role in the Policy Debate

• One alternative is passively sit by, be co-opted, and let others commandeer the policy agenda– That is exactly what producers have increasingly done since

the mid-eighties!!!

– Crop producers get subsidy-tarred while real subsidy beneficiaries (integrated livestock producers and other users, sellers of inputs and marketers of output) remain above the fray

– Farm groups advocating unfettered free markets, predicting prosperity-generating export growth, or claiming that a level playing field is the magic bullet, etc., ain’t workin.

– And, given the realities of agriculture discussed so far, they hold little promise for the future.

AAPP CCAA

From My Perspective…From My Perspective…• Crop exports did not deliver—will not deliver

• For crop agriculture, timely free—market self-correction is a fantasy

• Emerging agricultural powerhouses: Excess capacity will be a worldwide creation in the future

• Farmers version of the “Concentration” game: Buy inputs from few suppliers and sell output to few buyers

• Current US farm programs are not sustainable

• US policy alternatives and premises

AAPP CCAA

Some Policy OptionsSome Policy Options

• Continue the Exports/Trade Liberalization Will Save Us Course

• Eliminate or Drastically Cut Payments

• Switch to Green Payments based on Conservation/Environmental/ Rural Development Considerations

• Insurance/Farm Savings Accounts

• Policy to Address Crop Agriculture’s Long-Standing Problem

AAPP CCAA

Policy-Option Premise CheckPolicy-Option Premise Check• Export Markets/Global Trade

– Mechanism: • eliminate all price floors

• use the bully-pulpit to generate high- export expectations

• extend trade liberalization

– Apparent Premises: • Export markets are very price responsive

• Competing exporters will reduce production in the face of low prices

• Importing countries prefer to import rather than produce it themselves

• US agriculture will be a major beneficiary of trade liberalization

AAPP CCAA

Policy-Option Premise CheckPolicy-Option Premise Check• Eliminate or drastically reduce payments (With no

replacement of other programs)– Mechanism: Cut all payments– Apparent Premises:

• Commodity programs address no problem • Payments have created low world prices

– Implications• Output will decline markedly when payments are

reduced resulting in increased prices• Actually, land prices would go down and rural

communities would further decapitalize • Note that the prices of coffee, bananas, or cacao

declined sharply when markets were set free—there had been no payments in the “before” situation but there had been supply control

AAPP CCAA

Intensify Free Markets in Developed Intensify Free Markets in Developed CountriesCountries

IFPRI IMPACTIFPRI IMPACT

0

5

10

15

20

25

Per

cen

t

In 2020, worldwide• Corn price increases by less than 3% over baseline• Wheat price increases by less than 1% over baseline• Rice price increases by less than 2% over baseline

AAPP CCAA

Policy-Option Premise CheckPolicy-Option Premise Check• Insurance/Farm Saving Accounts

– Mechanism: • Government subsidies to commercial insurers or

provides tax breaks for farmer savings accounts

– Apparent Premises:• Low prices are a random event and seldom occur in a

string of years

• Growth in supply and demand are equal

– Possible Implications:• Income protection ratchets down

• Land prices would go down

• Supplemental payments from Congress would skyrocket

AAPP CCAA

Policy-Option Premise CheckPolicy-Option Premise Check• Conservation/Environmental/Rural Development

– Mechanism: Shift commodity payments to various kinds of conservation, environmental or rural development activities

– Apparent Premises:

• Commodity programs address no problem

• Better to have a broader group of farmers receive the money to achieve important (read real) objectives

• Farmers believe environmental degradation is a central concern and/or all that matters are WTO rules

• Payments in one form are as good as another

– Implications

• Does not address the long-standing market characteristics of aggregate crop agriculture

• Could win a Farm Bill battle but loose the credibility war

AAPP CCAA

From My Perspective…From My Perspective…

• Farm Bill needs to address:

– Unique characteristics of crop agriculture that result in chronic price/ income problems

– Variation in production due to weather and disease

– Trade issues like dumping

– Environmental and conservation issues

– Rural development beyond agriculture

AAPP CCAA

From My Perspective…From My Perspective…

• The 2007 Farm Bill needs to include provisions for:

– Buffer stocks to provide a reserve supply of grains and seeds in the case of a severe production shortfall

– In most recent years we have not had adequate supplies to meet the needs of consumers in the case of a production shortfall of 30% or more

AAPP CCAA

From My Perspective…From My Perspective…

• The 2007 Farm Bill needs to include provisions for:

– Supply Management to manage acreage utilization in the same way that other industries manage their capacity

– Stocks program to ensure orderly marketing process

– Both these provide a means of dealing with supply and demand inelasticity

AAPP CCAA

From My Perspective…From My Perspective…

• The 2007 Farm Bill needs to include provisions for:

– Bioenergy production to manage acreage utilization without heavy dependence on idling acreage

– Keep the land in production so that we don’t pay farmers not to farm

– Provide a needed energy source not unlike the horsepower of times past

AAPP CCAA

From My Perspective…

• Merge Ag and Energy Policy

– Biofuels recycle atmospheric, not fossil, carbon

– Look at crops not in food equation & NOT internationally traded

– Switchgrass (as an illustrative example only)

• Perennial• Reduced inputs• Multi-year setaside• Burned in boilers for electricity• Converted to ethanol• Less costly than present ag programs

AAPP CCAA

From My Perspective…From My Perspective…• Long term solutions to chronic price and

income problems need to include:– International supply management to manage

supply on a global scale

– At the present US supply management can benefit farmers everywhere in the world

– As countries like Brazil and other developing export competitors continue to increase their capacity they will need to be a part of an effective supply management program

AAPP CCAA

What Was That Again?What Was That Again?

• Crop exports did not deliver—will not deliver

• For crop agriculture, timely free- market self-

correction is a fantasy

• Excess capacity is crop agriculture’s future

peppered with periods of production-shortfalls

• Carrying water for agribusinesses typically

works against farmers’ best interests

• Current farm programs are not sustainable

AAPP CCAA

Agricultural Policy Analysis Center The University of Tennessee 310 Morgan Hall 2621 Morgan Circle Knoxville, TN 37996-4519

www.agpolicy.org

Thank YouThank You

AAPP CCAA

To receive an electronic version of our weekly ag policy column send an email to: [email protected] to be added to APAC’s Policy Pennings listserv

Weekly Policy ColumnWeekly Policy Column