“important practical and legal issues arising out of … · 2017-10-17 · 1 “important...

TRANSCRIPT

1

“IMPORTANT PRACTICAL AND LEGAL ISSUES ARISING OUT OF

FIRST AND SECOND APPEAL AND RELEVANT AMENDMENTS

RELATED TO APPEALS IN DTC”

24TH NOVEMBER, 2010

BOMBAY CHARTERED ACCOUNTANTS’ SOCIETY, MUMBAI

Grounds of Appeal and Statement of Facts.

- Article 265, “No tax shall be levied or

collected except by authority of law”

- Article 141 “The law declared by the Supreme

Court shall be binding on all Courts within

the territory of India”.

- Precedent-ratio.

CIT vs. Sun Engineering (1992) 198 ITR 297

(SC)(320)

2

APPEAL PROCEEDINGS

3

- Affidavit.

Mehta Parikh and Co. vs. CIT (1956) 30 ITR 181(SC)

- Statement recorded.

Kishanchand Chellaram vs. CIT (1980) 125 ITR 713(SC)

- Dismissal appeal for not appearing

Gujarat Themis Biosyn Ltd. vs. Jt. CIT (2000) 74ITD 339 (Ahd.)

- Speaking order - dealing with all the grounds.

CIT vs. S. Chenniappa Mudallar (1969) 74 ITR 41(SC)

APPEAL PROCEEDINGS

Grounds of Appeal and Statement of Facts – Irregularity

D. A. O. K. RM. Arunachalm Chettiar vs. CIT (1962) 45ITR 407 (Mad.)

- Non production of demand notice with appeal.

Chelamala Setti Adeyya vs. CGT (1964) 54 ITR 339 (All)

- Copy of notice of demand has not been filed.

Addl. CIT vs. Prem Kumar Rastogi (1978) 115 ITR 503(All)

4

APPEAL PROCEEDINGS

- Opportunity must be given to cure defects.

Bharat Industries vs. State of Maharashtra(1995) 98 STC 417 (424, 425) (Bom.)

- Failure to furnish the grounds of appeal inMemorandum of appeal i.e. Form No. 37,appeal cannot be dismissed.

5

APPEAL PROCEEDINGS

Reassessment - Return under protest

CWT vs. Apar Ltd. (2004) 267 ITR 705 (Bom.), the expression“without prejudice”

- Reasons recorded must be communicated within a reasonabletime.

GKN Driveshafts (India) Ltd. vs. ITO & Ors. (2003) 259 ITR 19(SC)

Allana Cold Storage vs. ITO (2006) 287 ITR 1 (Bom.)

Berger Paints India Ltd vs. ACIT & Ors (2004) 266 ITR 462(Cal)

Asian Paints Ltd. vs. Dy. CIT (2008) 296 ITR 90 (Bom.)

MCM Exports vs. Dy. CIT (2009) 23 DTR 356 (Guj.)

Bhabesh Chandra Panja vs. ITO (2010) 41 SOT 390 (Kol.)(TM)6

APPEAL PROCEEDINGS

Who can file an appeal - Agreed Assessment - Assessment by Consent

- Facts.

Rameschandra & Co. vs. CIT (1988) 168 ITR 375 (Bom.)

Western India Automobiles vs. CIT (1978) 112 ITR 1048 (Bom.)

- Rectification - Affidavit

Chhatmull Agrawal vs. CIT (1979) 116 ITR 694 (Punj.)

- Law - There is no estoppels against law.

Central Council for Research in Ayurveda & Sidhha vs. Dr. K.Santhakumari (2001) 5 SCC 60

Narseppali Oil Mills vs. State of Mysore (1973 ) 32 STC 599 (Mys.)

7

APPEAL PROCEEDINGS

Claim in the course of assessment

Goetz (India) Ltd. vs. CIT (2006) 284 ITR 323 (SC)

- Claim in appellate Proceedings.

Chicago Pneumatic India Ltd. vs. Dy. CIT (2007) 15SOT 252 (Mum.)

CIT vs. Ramco International (2009) 221 CTR 491 /17 DTR 214 (P&H)

CIT vs. Jai Parabolic Springs Ltd. (2008) 306 ITR 42(Delhi)

8

APPEAL PROCEEDINGS

- Order giving effect to Appellate order - Appealable

CIT vs. Industrial Machinery Manufacturing P. Ltd. (2006) 282ITR 595 (Guj.)

Bakelite Hylam Ltd. vs. CIT (1988) 171 ITR 344 (AP)

- Time Limit - On receipt of Notice of demand - Not order

Chakri Mica Mining Co. Ltd. v CIT (1978) 111 ITR 193 (Cal.)

- Appeal by person denying liability to deduct tax at source –w.e.f. 1-6-2007.

CIT vs. Wesman Engg. Co. (P) Ltd. (1991) 188 ITR 327 (SC)

9

APPEAL PROCEEDINGS

Admitted Tax - Mandatory – [S. 249(4)]

Vijay Prakash D. Mehata vs. Collector of Customs(1989) 175 ITR 540 (SC)(545)

- Interests - S. 234A, 234B and 234C - is not tax.

CIT vs. Manoj Kumar Beriwal (2009) 316 ITR 218(Bom.)

- Expression “tax” does not include interest for thepurpose of section 249(4).

Harshad Shantilal Mehta vs. Custodian (1998) 231ITR 871 (SC)

10

APPEAL PROCEEDINGS

- Payment is made before hearing of appeal, the CIT(A)or Tribunal the delay may be condoned.

Anant R. Thakore vs. ACIT (2006) 5 SOT 298(Mum.)

Shamraj Moorjani vs. Dy. CIT (2005) 93 TTJ 927(Hyd.) / 2 SOT 321 (Hyd.)

Suresh Chand Verma vs. ACIT (2004) 89 TTJ 661(Luck.)

J. K. Chaturvedi vs. ACIT (2004) 82 TTJ 284 (Ahd.)

11

APPEAL PROCEEDINGS

Condonation of delay

Collector of Land Acquisition vs. Mrs. Katiji &Others (1987) 167 ITR 471 (SC)

N. Balakrishanan vs. M. Krishnamurthy (1998)7 SCC 123

- Direct Taxes Code - Clause 179(3)(b), Power ofCIT(A), 183 (7), Power of Tribunal Clause192(6)(b)

12

APPEAL PROCEEDINGS

Who can sign an appeal - Rule 35, as per provision of section140

(a) Company - Managing Director

- Rule 45 read with section 140 are not mandatory but directory- Signed by an advocate - opportunity must be given to rectifythe same.

CIT vs. Hope Textiles Ltd. (2006) 287 ITR 321 (MP)

CIT vs. Haryana Sheet Glass Ltd. (2009) 318 ITR 173 (Del.)

CIT vs. Bhiwani Synthetics Ltd. (2009) 318 ITR 177 (Del.)

13

APPEAL PROCEEDINGS

Prime Securities Ltd. vs. Varinder Mehata vs.ACIT (2009) 317 ITR 27 (Bom.)

- Signed by secretary of the Company.

- Curable Defects – by virtue of section 139(9),read with 292B.

Sheonath Singh vs. CIT (1958) 33 ITR 591(Cal.)

- Appeal cannot be dismissed for defects in thesignature.

- Irregularity can be rectified subsequently, withretrospective effect.

14

APPEAL PROCEEDINGS

Malani Trading Co. vs. CIT (2001) 252 ITR 670 (Bom.)

Defects in memorandum of appeal - Registrar must point outthe defect and give reasonable opportunity to rectify thedefect.

Jai Jai Ram Manohar Lal vs. National Building MaterialSupply AIR 1969 SC 1267

BDA Ltd. vs. ITO (TDS) (2006) 281 ITR 99 (Bom.)

Rajendra Kumar Maneklal Sheth (HUF) vs. CIT (1995)213 ITR 715 (Guj.)

15

APPEAL PROCEEDINGS

Additional Grounds - Making a claim for the first time before AppellateAuthority

CIT vs. Western Rolling Mills Pvt. Ltd. (1985) 156 ITR 54 (Bom.)

- Circular No. 14 of 1955 dt. (XL-35) dt. 11-4-1955 (Chaturvedi &Pithesaria Vol. 11 Fourth Edition P. 1784-85)

National Thermal Power Co. Ltd. vs. CIT (1998) 229 ITR 383 (SC)

Jute Corporation of India vs. CIT (1991) 187 ITR 688 (SC)

- Can be raised Orally.

Amines Plastizers Ltd. vs. CIT (1997) 223 ITR 173 (Gauhati)

Assam Carbin Products Ltd. vs. CIT (1997) 224 ITR 57 (Gauhati)

16

APPEAL PROCEEDINGS

Jurisdiction Point - Can be raised at any time

CIT vs. Dumraon Cold Storage & Refrigerators Service(1974) 97 ITR 137 (Pat.)

Investor Industrial Corporation Ltd. vs. CIT (1992) 194ITR 548 (Bom.)

- Jurisdiction to reassess – Condition precedent - Can bechallenged in second round of appeal, though notchallenged in the first round of appeal.

17

APPEAL PROCEEDINGS

CIT vs. Madu Patani (Smt.) (2009) 18 DTR 110 (Ker.)

- Additional ground challenging the reassessment on theground of limitation can be raised first time before CIT(A),in appeal against the fresh assessment order passed onremand, even though it was not raised either before theassessing officer or CIT(A), in first round of proceedings.

- Invalid jurisdiction cannot be corrected by section 292B

Saraf Gramodyog Sansthan vs. ITO (2007) 108 ITD 115(Agra)

18

APPEAL PROCEEDINGS

Additional Evidence - Without giving an opportunity to other side -

Rule 46A

CIT vs. Shree Kangra Steel Pvt. Ltd. (2010) 320 ITR 691 (AP)

- Rule 46A(4) - CIT(A) on its own discretion can ask the assessee to

produce documents or evidence.

CIT vs. K. Ravindranathan Nair (2004) 265 ITR 217 (Ker.)

Dy. CIT vs. Thoresen Chartery Singapore (2009) 118 ITD 416

(Mum.)

ITO vs. Indl Roadways (2008) 305 ITR 219 (Mum.)(AT)

Prabhavati S. Shah (Smt.) vs. CIT (1998) 231 ITR 1 (Bom.) 19

APPEAL PROCEEDINGS

Power of CIT(A) are coterminous with those of theAssessing Officer

CIT vs. Nirbheran Duekram (1997) 224 ITR 610 (SC)

- CIT(A), however, cannot discover new source of incomenot considered by the Assessing Officer

CIT vs. Shapoorji Pallonji Mistry (1962) 44 ITR 891 (SC)

CIT vs. Ahamedabad Crucible Co. (1994) 206 ITR 574(Guj.)

Kapoorchand Shrimal vs. CIT (1981) 131 ITR 451 (SC)

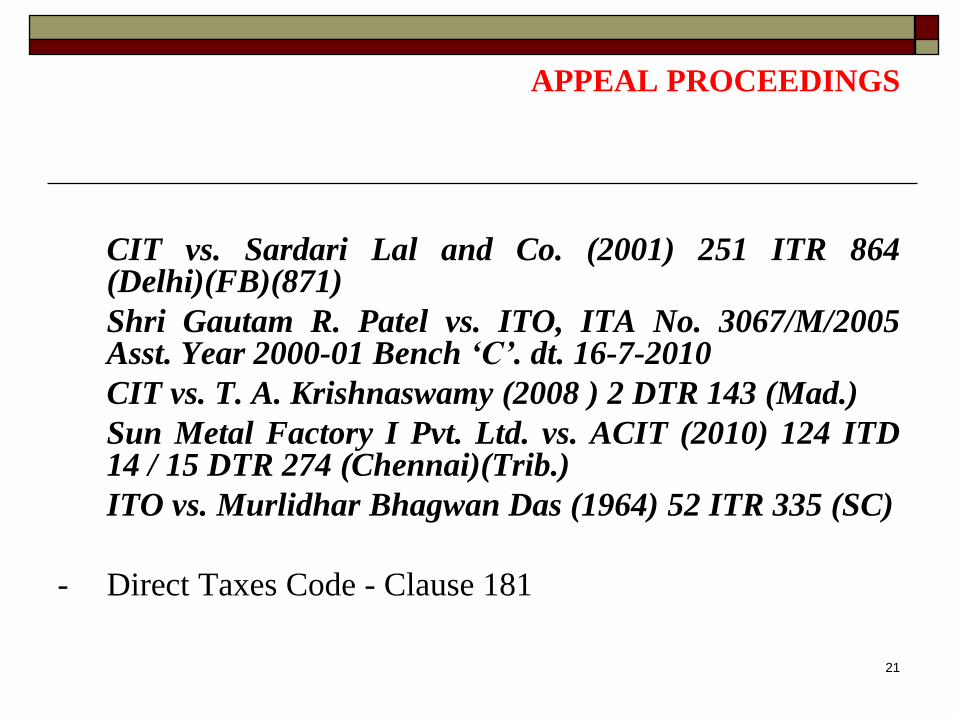

20

APPEAL PROCEEDINGS

CIT vs. Sardari Lal and Co. (2001) 251 ITR 864(Delhi)(FB)(871)

Shri Gautam R. Patel vs. ITO, ITA No. 3067/M/2005Asst. Year 2000-01 Bench „C‟. dt. 16-7-2010

CIT vs. T. A. Krishnaswamy (2008 ) 2 DTR 143 (Mad.)

Sun Metal Factory I Pvt. Ltd. vs. ACIT (2010) 124 ITD14 / 15 DTR 274 (Chennai)(Trib.)

ITO vs. Murlidhar Bhagwan Das (1964) 52 ITR 335 (SC)

- Direct Taxes Code - Clause 181

21

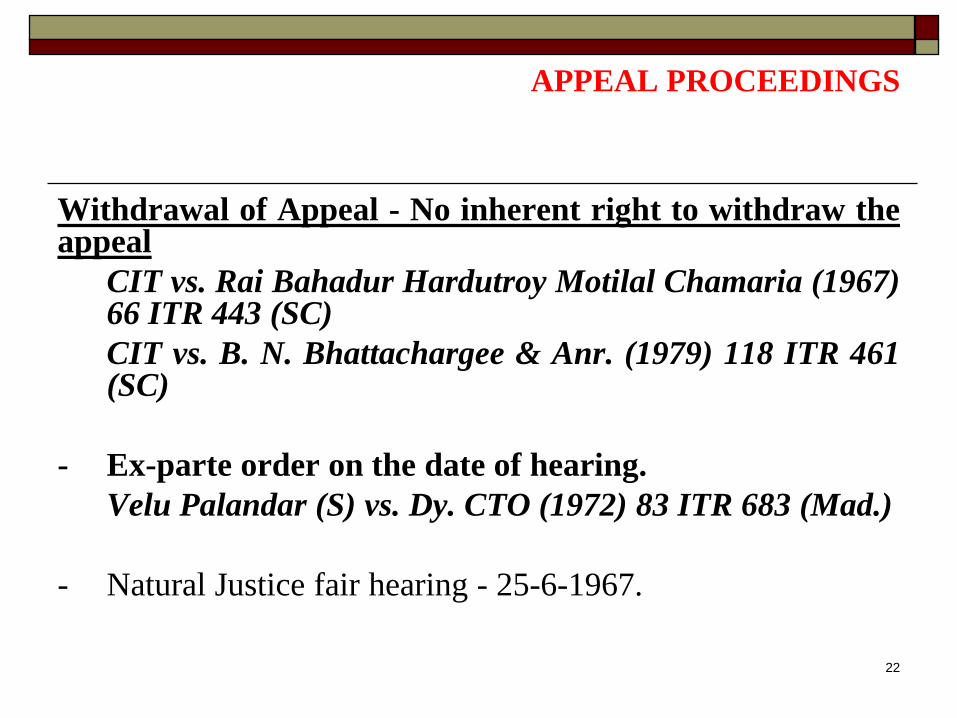

APPEAL PROCEEDINGS

Withdrawal of Appeal - No inherent right to withdraw theappeal

CIT vs. Rai Bahadur Hardutroy Motilal Chamaria (1967)66 ITR 443 (SC)

CIT vs. B. N. Bhattachargee & Anr. (1979) 118 ITR 461(SC)

- Ex-parte order on the date of hearing.

Velu Palandar (S) vs. Dy. CTO (1972) 83 ITR 683 (Mad.)

- Natural Justice fair hearing - 25-6-1967.

22

APPEAL PROCEEDINGS

Protective Assessment - Appeal can be filed even in respect of protective assessment

Eastern Bulk Services vs. ITO (1995) 5 ITD 471 (Del.)(SB)

Lalludas Children Trust vs. CIT (2001) 251 ITR 50 (Guj.)

- Protective recovery not possible

Sunil Kumar vs. CIT (1983) 139 ITR 880 (Bom.)

- Penalty Reply

- On merits.

- Request to drop the penalty proceedings.

- Give an opportunity of hearing.

23

APPEAL PROCEEDINGS

Stay of Recovery - Guidelines to the Income tax Authorities

KEC International Ltd. vs. B. R. Balakrishnan & Ors. (2001) 251 ITR 158 (Bom.) (160)

Paramount Health Services vs. ACIT (2010) 37 DTR 377 (Bom.)

Mahindra & Mahindra Ltd. vs. UOI (1992) (59) ELT 505 (Bom.)

- Detailed application for stay.

- Recovery - Pending Rectification – S. 154

Sultan Leather Finisiheres Pvt. Ltd. vs. ACIT (1991) 191 ITR 179 (All)

24

APPEAL PROCEEDINGS

Power of CIT(A) - Stay the Recovery Proceedings

Tin Manufacturing Company India vs. CIT (1995) 212 ITR451 (All)

Paulsons Litho Works vs. ITO (1994) 208 ITR 676 (Mad.)

Agricultural Produce Market Committee vs. CIT (2005) 279ITR 371 (Pat.)

Dispute Resolution Panel – S. 144C

- Dispute resolution panel will not follow the judgments ofTribunal or High Court

25

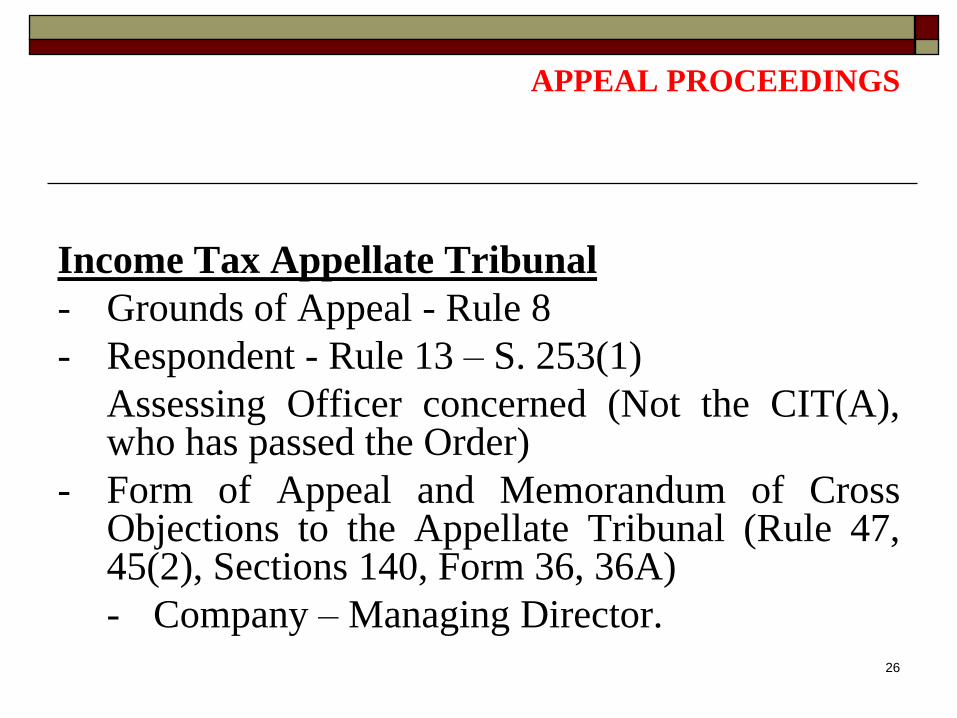

APPEAL PROCEEDINGS

Income Tax Appellate Tribunal

- Grounds of Appeal - Rule 8

- Respondent - Rule 13 – S. 253(1)

Assessing Officer concerned (Not the CIT(A),who has passed the Order)

- Form of Appeal and Memorandum of CrossObjections to the Appellate Tribunal (Rule 47,45(2), Sections 140, Form 36, 36A)

- Company – Managing Director.26

APPEAL PROCEEDINGS

Appeal by Registered Post - Rule 6(2)

F. N. Roy vs. Collector of Customs AIR 1957 (SC) 648

Service of Order – Notice – Summons - By Courier Service - NotValid

Carter Hydrolic Power P. Ltd. vs. UOI (2010) 256 ELT 394 (Cal.)

Nirmal Products vs. C. Exh. Jaipur (2010) 254 ELT 538 (Delhi)

Cross Objection - Rule 36A.

Respondent may support the order of CIT(A) by taking anyground, though no cross objection had been filed.

Cable Network LP vs. Asst. Director (2010) 36 DTR 233 / 129TTJ 177 (Delhi)

27

APPEAL PROCEEDINGS

Rule 27 – Right of Respondent.

Traise ITA No. 2827/M/04 Asst. Year 1995-96 Bench „H‟ dt. 26-11-2007. Source: www.itatonline.org

Dahod Sahakari Karid Vechan Sangh Ltd. vs. CIT (2007) 282ITR 321 (Guj.) (329)

Dy. CIT vs. Turquoise Investment & Finance Ltd. (2008) 299ITR 143 (MP) (151)

B. R. Bamsi vs. CIT (1972) 83 ITR 223 (Bom.) (245-246)

Cable Network LP vs. Asst. Director (2010) 36 DTR 233 / 129TTJ 177 (Delhi)

Assam Company (India) Ltd. vs. CIT (2002) 256 ITR 423(Gauhati)

CIT vs. Vijay Lakshmi (Smt.) (2000) 242 ITR 46 (Mad.)

28

APPEAL PROCEEDINGS

- Assessee’s as well as department appeal must be heard together.

Commissioner of Sales Tax vs. Vijay Int. Udyog (1985) 152 ITR 111(SC)

- Additional grounds can be raised orally - Rule 11 of Income Tax AppellateTribunal Rules.

Amines Plasticizers Ltd. vs. CIT (1997) 223 ITR 173 (Gauhati)

Assam Carbon Products Ltd. vs. CIT (1997) 224 ITR 57 (Gauhati)

- No Power of Enhancement.

Hukumcahnd Mills Ltd. vs. CIT (1967) 63 ITR 232 (SC) (236)

Mcorp Global P Ltd. vs. CIT (2009) 309 ITR 434 (SC)

ACIT vs. Anima Investment Ltd. (2000) 73 ITD 125 (Del.)(TM)

29

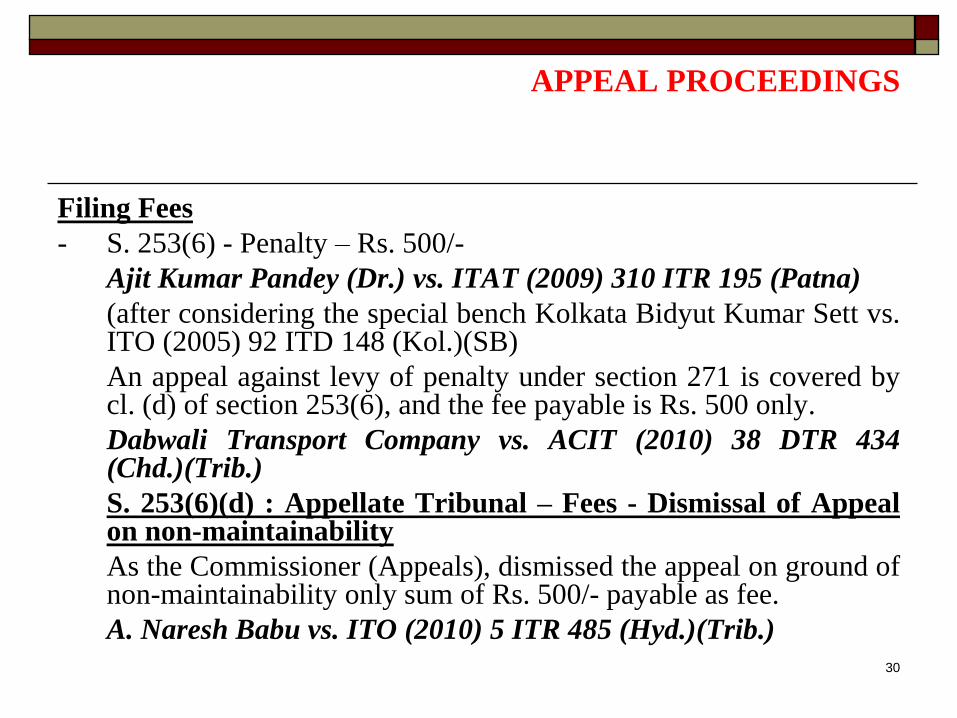

APPEAL PROCEEDINGS

Filing Fees

- S. 253(6) - Penalty – Rs. 500/-

Ajit Kumar Pandey (Dr.) vs. ITAT (2009) 310 ITR 195 (Patna)

(after considering the special bench Kolkata Bidyut Kumar Sett vs.ITO (2005) 92 ITD 148 (Kol.)(SB)

An appeal against levy of penalty under section 271 is covered bycl. (d) of section 253(6), and the fee payable is Rs. 500 only.

Dabwali Transport Company vs. ACIT (2010) 38 DTR 434(Chd.)(Trib.)

S. 253(6)(d) : Appellate Tribunal – Fees - Dismissal of Appealon non-maintainability

As the Commissioner (Appeals), dismissed the appeal on ground ofnon-maintainability only sum of Rs. 500/- payable as fee.

A. Naresh Babu vs. ITO (2010) 5 ITR 485 (Hyd.)(Trib.)

30

APPEAL PROCEEDINGS

- Assessed Income loss – S. 253(6) – Rs. 500/-

Gilbs Computer Ltd. vs. ITAT (2009) 317 ITR 159 (Bom.)

- Order under section 263 – Rs. 500/-

Kiranjit Singh vs. ACIT (2006) 101 TTJ 424 (Asr.)

Choromatic India Ltd. vs. ITO, ITA No. 3486/M/01 Bench „D‟ dt. 12-2-

02.

- Appeal dismissed on the ground of limitation - Non maintainable Rs.

500/-.

Rajkumar Polymers Pvt. Ltd. vs. CIT (2007) 291 ITR 314 (Karn.)

A. Naresh Babu vs. ITO (2010) 5 ITR 485 (Hyd.)(Trib.)

31

APPEAL PROCEEDINGS

Presentation of Paper Book – Rule 18(02)

Assistant Registrar U.O.NO F. 37 – JD (ATD)92 dt. 25-2-1992 – Procedure for filing paperbook.(1992) 24 BCAJ P.151.

- At least a week before.

- Additional evidence by a separate paper book.Rule 11.

- Certificate should be proper.

32

APPEAL PROCEEDINGS

Rectification of Mistake - Rule 34A – S. 254(2)

- On facts – No power of review.

CIT vs. Ramesh Electric and Trading Co. (1993) 203 ITR497 (Bom.)

- On the basis of Judgment of Apex court.

Circular No. 68 dt. 17-11-1971 (1972) 83 ITR (St) 6.

- Mistake Apparent from record – Supreme CourtJudgement.

- On the basis of Judgment of Jurisdiction High Court.

ITO vs. Pas Securities Pvt. Ltd. MA. No. 772/Mum/09Bench „K‟ dt. 11-2-2010.

ACIT vs. Saurashtra Kutch Stock Exchange (2008) 305ITR 227 (SC) 33

APPEAL PROCEEDINGS

- If appeal is filed in High Court if admitted or dismissed there cannot berectification. Tribunal order merges with the order of High Court.

Tata Communications Ltd. vs. Jt. CIT (2009) 317 ITR 1 (AT) / 121 ITD384 (Mum.)(SB)

- Miscellaneous application on miscellaneous application( secondrectification petition ) is not permissible.

CIT vs. Panchu Arunachalam ( 2010) 235CTR 308 / 45 DTR 368(Mad.)

- Petition has to be filed Within four years – The Tribunal has no power tocondone the delay.

Arvindbhai H. Shah vs. ACIT (2004) 270 ITR 125 (At) (Ahd.)(SB)

Rahul Jee and Co. P. Ltd. vs. ACIT (2009) 310 ITR 255 (Del.)

34

APPEAL PROCEEDINGS

Chapter XIV-A - Avoidance of Repetitive

Appeals – S. 158A

If earlier years are pending before High Court or

Supreme Court by filing an application the

matter may be kept alive. This will save the cost

of litigation.

35

APPEAL PROCEEDINGS

Referencer

- Suggestions made by Registrar for guidance of assesses and theirrepresentatives (1951) 20 ITR (St.) 49.

- Guidelines for early fixing of matters. AIFTP Journal (August,2005 Page Nos. 25 to 27)

(Tribunal in the Next Millennium 16-1-1999 P. 77). Coveredmatters, (own case, jurisdictional High Court, Apex Court).

- Court Fee and Stamp Duty - For Appearance - Power of AttorneySchedule-1 Article 5(h) of the Bombay Stamp Act Rs. 100/- (letterNo. ADJ/Misc./5521 dt. 27-10-1994 from the Superintended ofStamps to the Registrar of ITAT)

(Tribunal in the Next Millennium 16-1-1999 P. 78)

36

APPEAL PROCEEDINGS

- Dress regulation for the AuthorisedRepresentatives Rule 17A(ii) of the Income TaxAppellate Tribunal Rules.

(Tribunal in the next millennium 16-1-1999 P79.)

- Guidelines to Stay Application. AIFTP Journal(April, 2007 P. 35 – AIFTP Journal June, 2007 P.No. 36)

Jagjivandas Nadlal vs. ITAT (Bombay HighCourt) Source: www.itatonline.org

37

APPEAL PROCEEDINGS

Art of Representation

Source: www.itatonline.org

- Check list for filing of appeal before Tribunal

- Specimen Grounds of Appeal, Stay Petition,

Affidavit, etc.

- A Fine Balance - Law and Procedure before

ITAT – Chapter 16 P. 116 / Chapter 20 P. 126

to 12838

APPEAL PROCEEDINGS

39

BOMBAY CHARTERED ACCOUNTANTS’ SOCIETY, MUMBAI

THANK YOU

THANK YOU

Dr. K. Shivaram, B. Com., LL. M., PH.D (Law)

KSA Legal

JAI HIND