“a scorecard for bank performance: the belgian banking .../media/corporate/pdf... · “a...

TRANSCRIPT

Point of Contact: [email protected] (+32 9 210 9860)

“A scorecard for bank performance:

the Belgian Banking Industry.”

Prof. Dr. André Thibeault, Corneel Defrancq and Jessie Vantieghem

Vlerick Centre for Financial Services

Table of Contents

THE KPMG – VLERICK PRIME FOUNDATION PARTNERSHIP .................................................................... 1

Acknowledgment .................................................................................................................................... 3

Executive Summary ................................................................................................................................. 5

Introduction ............................................................................................................................................ 7

Structure of the report ............................................................................................................................ 7

Chapter 1: Industry overview ................................................................................................................. 9

Contribution to the Belgian economy ............................................................................................... 10

Trends over time ........................................................................................................................... 10

Savings ratio of households .............................................................................................................. 14

Banking sector’s contribution compared with European peers ....................................................... 16

Internationalisation of the Belgian banking landscape .................................................................... 18

Chapter 2: The value chain ................................................................................................................... 19

Sample selection and segments description..................................................................................... 20

Sample Selection ........................................................................................................................... 20

ECB segmentation ......................................................................................................................... 20

Size segmentation ......................................................................................................................... 22

Fortis Bank SA/ NV-BNP Paribas Fortis ................................................................................................. 22

ING Belgium SA/NV-ING ........................................................................................................................ 22

BankScope segmentation.............................................................................................................. 23

Operational income to total assets ................................................................................................... 24

Net interest income to total assets................................................................................................... 27

Net commissions and fees to total assets......................................................................................... 32

Financial transactions to total assets ................................................................................................ 36

Operational expenses to total assets ................................................................................................ 40

Loan loss provisions to total assets................................................................................................... 45

Conclusion ......................................................................................................................................... 48

Chapter 3: The financial performance .................................................................................................. 51

Return on equity ............................................................................................................................... 53

Leverage ............................................................................................................................................ 57

Return on assets ............................................................................................................................... 61

Asset yield ......................................................................................................................................... 65

Profit margin ..................................................................................................................................... 69

Cost to income .................................................................................................................................. 73

Conclusion ......................................................................................................................................... 78

Chapter 4: The risk-return trade-off ..................................................................................................... 79

Chapter 5: What did we learn in this study? ........................................................................................ 83

References ............................................................................................................................................ 85

Appendices ............................................................................................................................................ 88

Appendix 1: The ratios ...................................................................................................................... 88

Appendix 2: The variables ................................................................................................................. 88

Appendix 3: A38 Code ....................................................................................................................... 89

Appendix 4: NACE BEL Code ............................................................................................................. 91

Appendix 5: List of abbreviations...................................................................................................... 92

Appendix 6: Contribution in terms of percentage of both the banks individually and per sector. .. 93

Appendix 7: The segmentation between universal and investment banks ...................................... 95

Appendix 8: The evolution of the natural logarithm of the total assets .......................................... 96

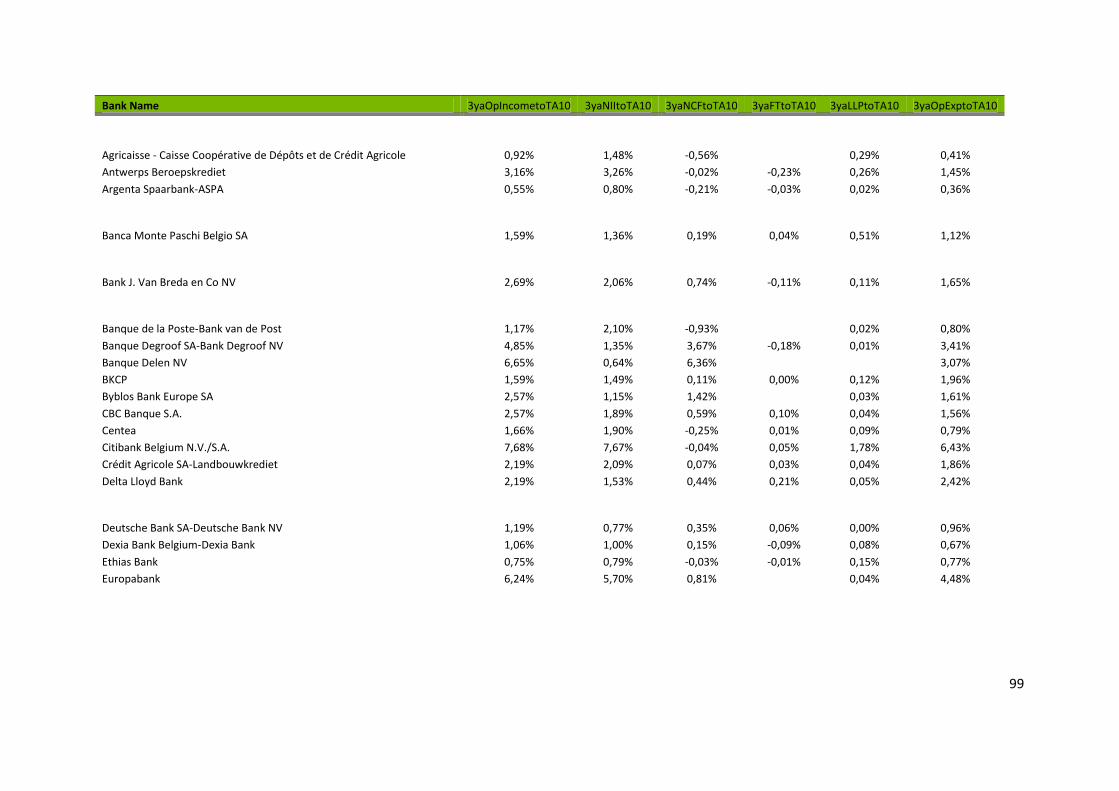

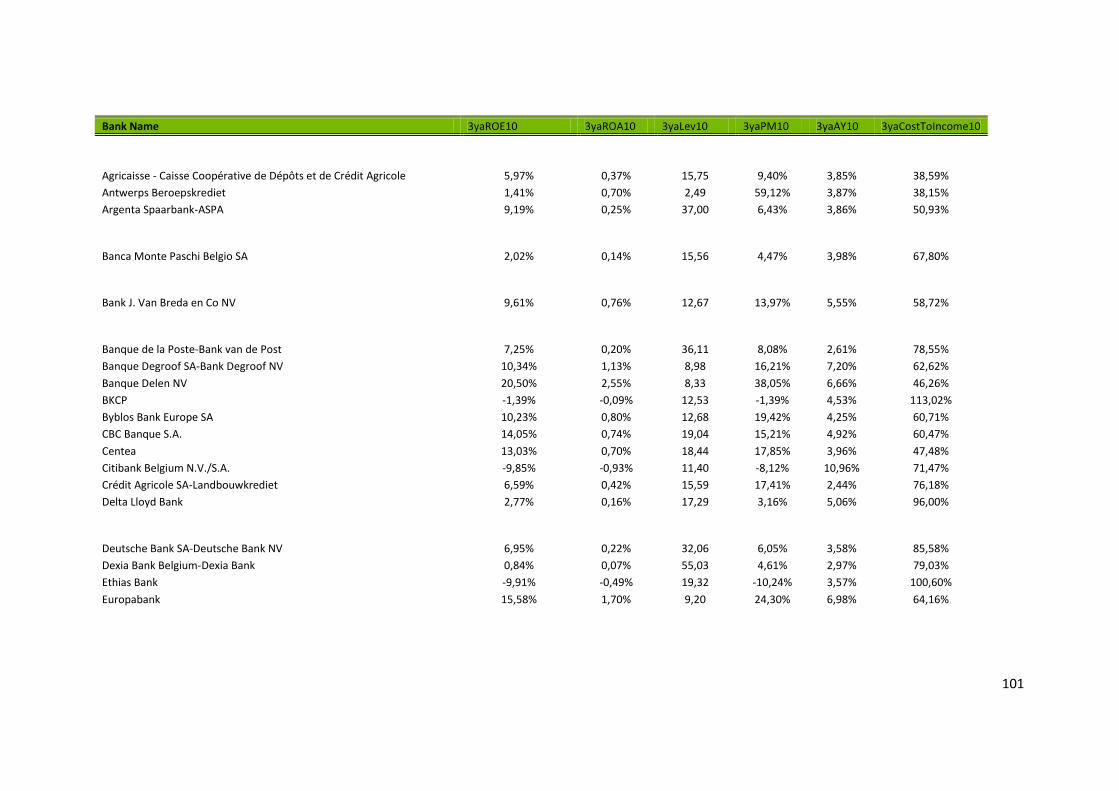

Appendix 9: Ratios for each bank individually .................................................................................. 98

Agricaisse - Caisse Coopérative de Dépôts et de Crédit Agricole ......................................................... 99

Banca Monte Paschi Belgio SA .............................................................................................................. 99

Bank J. Van Breda en Co NV .................................................................................................................. 99

Banque de la Poste-Bank van de Post ................................................................................................... 99

Deutsche Bank SA-Deutsche Bank NV .................................................................................................. 99

F. van Lanschot Bankiers Belgie .......................................................................................................... 100

Fortis Bank SA/ NV-BNP Paribas Fortis ............................................................................................... 100

ING Belgium SA/NV-ING ...................................................................................................................... 100

Onderling Beroepskrediet-OBK-Bank C.V.B.A. .................................................................................... 100

Société Générale Private Banking N.V. ............................................................................................... 100

Agricaisse - Caisse Coopérative de Dépôts et de Crédit Agricole ....................................................... 101

Banca Monte Paschi Belgio SA ............................................................................................................ 101

Bank J. Van Breda en Co NV ................................................................................................................ 101

Banque de la Poste-Bank van de Post ................................................................................................. 101

Deutsche Bank SA-Deutsche Bank NV ................................................................................................ 101

F. van Lanschot Bankiers Belgie .......................................................................................................... 102

Fortis Bank SA/ NV-BNP Paribas Fortis ............................................................................................... 102

ING Belgium SA/NV-ING ...................................................................................................................... 102

1

THE KPMG – VLERICK PRIME FOUNDATION

PARTNERSHIP

This report on the mapping of the Belgian banking industry is part of a 3-year project conducted in

the format of a Prime Foundation Partnership between KPMG and the Vlerick Centre for Financial

Services.

The research content of the Prime Foundation Partnership will be filled in as follows:

Year 1: Helicopter View – International Scorecard. What is the performance (from many

different angles) of the participants in the banking sector and in the insurance sector in

Belgium, and how do they rank under these dimensions?

Year 2: Cluster analysis – survey – who performed the best and what drives their

performance? What differentiates these banks and these insurance companies? Look at

periods before/during/after the crisis. Make links to different dimensions like: distribution

channels, business models, asset structure, financial aspects and managerial aspects.

Year 3: Wait to see the results from years 1 & 2 and then identify interesting issues to be

investigated further. Points of specific research interests raised by KPMG could also be

investigated in the course of this part of the research project.

2

3

ACKNOWLEDGMENT

This research project would not have been possible without the support of many people.

The authors would like to convey thanks to KPMG for providing the financial means and specially to

Bart Walterus, Partner Financial Services Consulting / KPMG Advisory, who has been providing

managerial support and professional advices of great help throughout the report elaboration.

Furthermore, the authors would like to thank Erik Clinck, Olivier Macq, Stijn Broekx, Jorn Deneve and

Ingrid Stoffels for their valuable feedback at various occasions throughout the duration of the study.

At the Vlerick Centre for Financial Services, Maureen O’Hare has played a major role in the

discussions leading to the Prime Foundation Partnership of KPMG and Diane von Teufenstein, as

business manager of the Vlerick Centre for Financial Services, has been coordinating this project with

a professional and dedicated approach.

The authors,

Prof. Dr. André E. Thibeault

Corneel Defrancq

Jessie Vantieghem

4

5

EXECUTIVE SUMMARY

The goal of this study is to develop a scorecard for assessing bank performance in the Belgian

banking industry. The performance will be measured by using a multi-factors approach to make sure

performance is assessed under different dimensions and these performance measures will be

applied to different segments of the Belgian banking landscape.

The dimensions to be considered are: the value chain, the breakdown of the ROE and the risk-return

trade-off.

Four different segments will be defined, based on the size of the banks (defined by their total assets)

or based on their type of activities or revenues:

A first segment will compare the banks relative to the source of their income as defined by

the ECB (investment banks or universal banks).

A second segment will be based on the size of the banks. Four different categories will be

created based on total assets.

A third segment will study Belgium’s Big Four banks individually: Dexia, Fortis, ING and KBC.

The last category is based on the BankScope segmentation.

The importance of the financial sector in Belgium is substantial – but it has decreased slightly during

the period 2001 – 2010. The financial sector’s contribution to Belgian employees’ employment

compensation went from about 6% in 2001 to 5% in 2010. The same trend is observable in the

number of people employed in the financial sector. However, while the number of people employed

decreased during this period, the average salary steadily increased from €58,000 in 2001 to €70,000

in 2008. After 2008, the financial crisis caused wages to freeze at about €70,000. Another striking

feature of the Belgian economy is the savings rate, one of the highest in the world, which fluctuated

between 15% and 20% between 2001 and 2010.

When looking more specifically at the Belgian banking sector, one has to realise its international

standing. In Belgium, almost half of the total assets (held by Belgian financial institutions) are in the

hands of foreign controlled credit institutions.

When breaking down the value chain, it is interesting to note that private banks are consistently

exhibiting the highest ratio of operating income to total assets. In the investment / universal banks

segment, the investment banks have a better ratio than the universal banks; and when looking at

bank size, the smallest banks are achieving the best performance.

When we broke the total operating income into its components, we found that net interest income

was negatively correlated with the size of the bank as measured by total assets. As expected, the

private banks are dominating the other banks when net fees and commissions are used as the

benchmark. When using financial transactions as the benchmark, no conclusion can be drawn,

because this value driver is so volatile. On the costs side of the value chain, all of the banks have

been able to reduce their operating expenses during the period under study. Private banks have

experienced the highest level of operating expenses to total assets (4%), while universal banks have

been able to bring this figure down to 1%.

6

While looking at the performance of the banking industry based on the breakdown of the ROE, the

four big banks dominate the market – not because of their good operational profitability (ROA), but

because of a bigger risk appetite, which is reflected in a higher leverage compared to the other

banks. The comparison of investment banks and universal banks shows that the investment banks

perform better in terms of ROE. However, based on their total assets in 2009, the investment banks

account for not even 1% of the sample, while the universal banks account for the rest. In the

segment based on “BankScope”, the private banks have the best ROE, due to their better

performance in operational profitability (ROA).

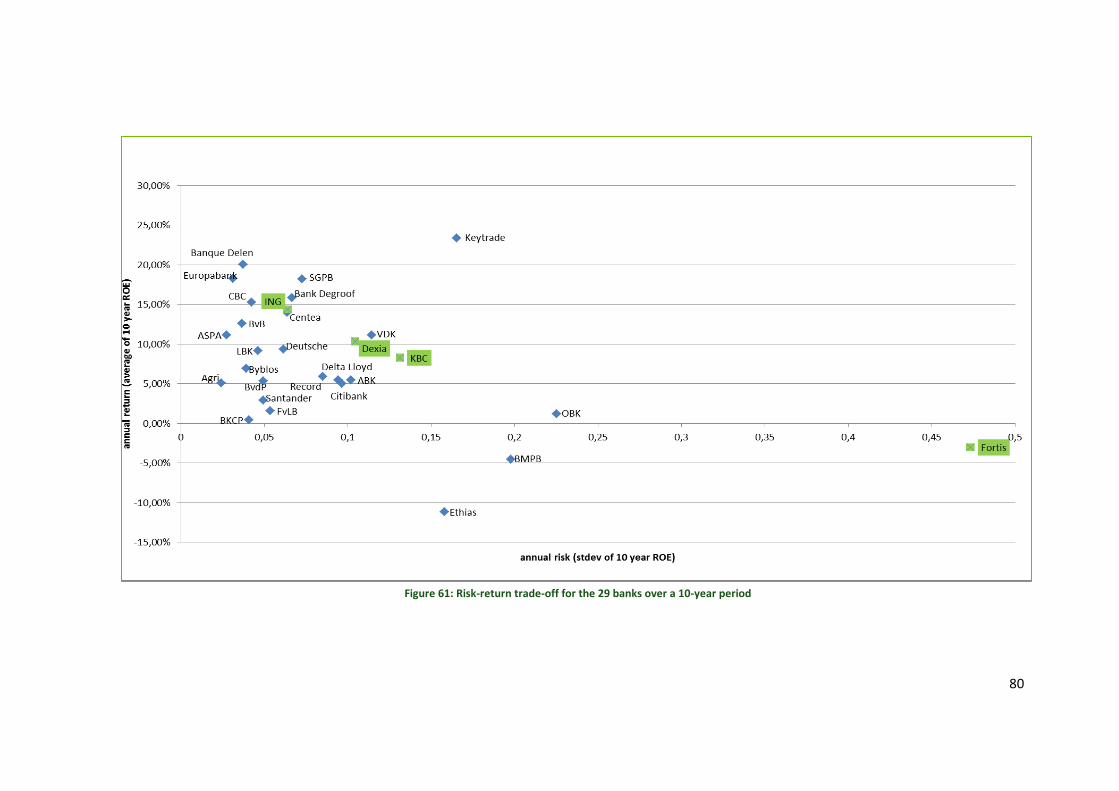

The analysis of the risk-return trade-off shows a cluster of banks in an area from low to medium risk

and from a low to a high ROE. The banks presenting the best risk-return trade-off over the period

under study are Banque Delen and Europabank. An interesting point of this risk-return analysis is

the inverse relationship for the Big Four banks. ING shows a good risk-return profile, followed by

Dexia and KBC with higher risk and lower return, and finally by Fortis with the worst risk-return

profile for the period under study.

7

INTRODUCTION

How to measure performance in the Belgian banking industry? Participants in the financial services

industry worldwide have been using many different benchmarks to assess bank performance. The

goal of this study is to develop a scorecard for assessing bank performance in the Belgian banking

industry. The performance will be measured by using a multi-factors approach to make sure

performance is assessed under different dimensions and these performance measures will be

applied to different segments of the Belgian banking landscape.

Four different segments will be defined, based on the size of the banks (defined by their total assets)

or based on their type of activities or revenues:

A first segment will compare the banks relative to the source of their income as defined by

the ECB (investment banks or universal banks).

A second segment will be based on the size of the banks. Four different categories will be

created based on total assets.

A third segment will study Belgium’s Big Four banks individually: Dexia, Fortis, ING and KBC.

The last category is based on the BankScope segmentation.

Furthermore, three dimensions will be defined on the basis of a series of variables in order to

measure performance. The report will map the Belgian banking sector with regard to these three

performance dimensions. These dimensions are:

1) The value chain

2) The financial performance

3) The risk-return trade-off

STRUCTURE OF THE REPORT

To answer the key question – “How to measure performance in the Belgian banking industry?” – we

have structured the report as follows:

In Chapter 1, we start by outlining the industry context. In this chapter, we present some well-known

figures about the position of the Belgian banking industry in the Belgian and European economies.

This chapter sets the context for the remainder of our study.

Chapter 2 details the value chain in the Belgian banking industry. We leave the global view of the

industry and move down to the segments level, comparing the value chain of the banks in Belgium

(as measured by assets) over the last 10 years. Examining the years 2001 to 2010 allows us to cover

the boom years of the early 2000s as well as the credit crunch of 2007 - 2009.

In Chapter 3, we break down each market segment’s ROE according to the Dupont analysis. Thus,

the segments are compared on the basis of their profitability – and more precisely, on their capacity

to generate income as well as their cost management.

While Chapter 3 compares performance on the basis of the return component, Chapter 4 tackles the

combination of both risk and return. The risk-return trade-off will be portrayed by means of graphs.

Chapter 5 presents the major findings of the study.

8

9

CHAPTER 1: INDUSTRY OVERVIEW

In order to provide an overview of the industry, we use the two reports of Febelfin, the Belgian

Financial Sector Federation (Febelfin, 2010; Febelfin, 2009). Created in 1993, Febelfin consists of five

financial trade organisations:

1. ABB-BVB: Belgian Bankers’ and Stockbroking Firms’ Association

2. BEAMA: Belgian Asset Managers Association

3. UPC-BVK: Professional Union of Credit Providers

4. BLA: Belgian Leasing Association

5. BASEM: Belgian Association of Stock Exchange Members

In a first phase, we scrutinise the financial sector’s contribution to the economy in terms of gross

added value, employment and employee wages. Secondly, we break down the gross added value

according to four distinguishable sub-sectors: (1) insurance corporations and pension funds, (2)

financial auxiliaries, (3) other financial intermediaries except insurance corporations, and (4) the

central bank and other monetary financial institutions. As a third topic of research, we compare the

total assets on the balance sheet of the credit institutions with the GDP of the countries that are part

of the European Monetary Union. Fourth, we assess the internationalisation of the industry by

ranking the EMU countries according to their respective share of foreign-owned banks.

10

CONTRIBUTION TO THE BELGIAN ECONOMY

Trends over time

To assess the importance of the financial sector in the Belgian economy, we have calculated the

Gross Value Added (GVA) of the financial intermediation sector from 2000 up to 2010 (see Figure 1).

We clearly see the decline in added value in the years from 2005 to 2008. From 2008 to 2010, we

see the shift to previous levels of added value. In 2010, 6.14% of the Belgian economy (as measured

by GDP) was built on added value from the financial intermediation sector.

Figure 1: Gross Value Added of the financial sector (as a percentage of the Belgian economy) Source: National Bank of Belgium (Belgostat)

Gross Value Added (GVA) measures the contribution to the economy of each individual producer, industry or sector. The gross value added at basic prices is defined (according to the ESA95 standard) as the output valued at basic prices less intermediate consumption valued at purchaser prices, before deduction of consumption of fixed capital (European Central Bank).

4,90%

5,10%

5,30%

5,50%

5,70%

5,90%

1999 2001 2003 2005 2007 2009 2011

11

During this same period of time, the total sum of wages paid by the financial service industry (Figure

2) has been relatively in decline in the Belgian economy. In 2010, 4.97% of the total sum paid to

employees came from the financial industry.

Figure 2: Financial sector's contribution to Belgian Employees' employment compensation Source: National Bank of Belgium (Belgostat)

One could conclude that the average salary paid within the financial industry is dropping, but when

we also consider the number of people active in the financial industry (see Figure 3), we can counter

this conclusion.

Figure 3: Employment: Number of people employed in the financial industry (x1000) from 2001 to 2010 Source: National Bank of Belgium (Belgostat)

4,50%

5,00%

5,50%

6,00%

6,50%

1999 2001 2003 2005 2007 2009 2011

130 135 140 145 150

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

12

When the total amount of employee compensation1 for the financial industry is divided by the total

number of employees in the financial industry, we arrive at Figure 4. This highlights that the average

wage has been growing at a fairly slow pace in the 2000 to 2010 timeframe. However, no downward

trend is observable.

Figure 4: (Total sum of wages) / (Employment) in the financial industry (€) Source: National Bank of Belgium (Belgostat)

1 This is the total remuneration, in cash or in kind, paid by government to its employees. It includes employers’

actual and imputed social contributions. Employers’ actual social contributions are actual payments into social security schemes and into funded autonomous pension schemes by government on behalf of its employees. Imputed contributions are the estimate of the accruing pension liability in employers’ unfunded defined-benefit schemes (definition Belgostat).

0

10000

20000

30000

40000

50000

60000

70000

80000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

13

When we compare the different sectors (A38 coded, see Appendix 3), we see that the number of

people employed in the financial and insurance sector is roughly the same as the number of people

in the accommodation and food service industry.

Figure 5: Employment – Belgian Sector Comparison (number of employees, x1000, 2010 data) Source: National Bank of Belgium (Belgostat)

0 100 200 300 400 500 600 700

Wholesale and retail trade, repair of motor vehicles and motorcycles (GG)

Public administration and defence; compulsory social security (OO)

Legal and accounting activities; activities of head offices; management…

Education (PP)

Administrative and support service activities (NN)

Human health activities (QA)

Construction (FF)

Transportation and storage (HH)

Social work activities (QB)

Accommodation and food service activities (II)

Financial and insurance activities (KK)

Other service activities (SS)

Manufacture of food products, beverages and tobacco products (CA)

Manufacture of basic metals and fabricated metal products, except…

Agriculture, forestry and fishing (AA)

Computer programming, consultancy and related activities; information…

Manufacture of rubber and plastics products, and other non-metallic…

Activities of households as employers of domestic personnel and…

Manufacture of wood and paper products, and printing (CC)

Manufacture of chemicals and chemical products (CE)

Manufacture of transport equipment (CL)

Arts, entertainment and recreation (RR)

Advertising and market research; other professional, scientific and…

Manufacture of furniture; other manufacturing; repair and installation of…

Manufacture of machinery and equipment n,e,c, (CK)

Manufacture of textiles, wearing apparel and leather products (CB)

Telecommunications (JB)

Water supply; sewerage, waste management and remediation activities…

Publishing, audiovisual and broadcasting activities (JA)

Real estate activities (LL)

Manufacture of basic pharmaceutical products and pharmaceutical…

Electricity, gas, steam and air-conditioning supply (DD

Manufacture of electrical equipment (CJ)

Manufacture of computer, electronic and optical products (CI)

Scientific research and development (MB)

Manufacture of coke and refined petroleum products (CD)

Mining and quarrying (BB)

14

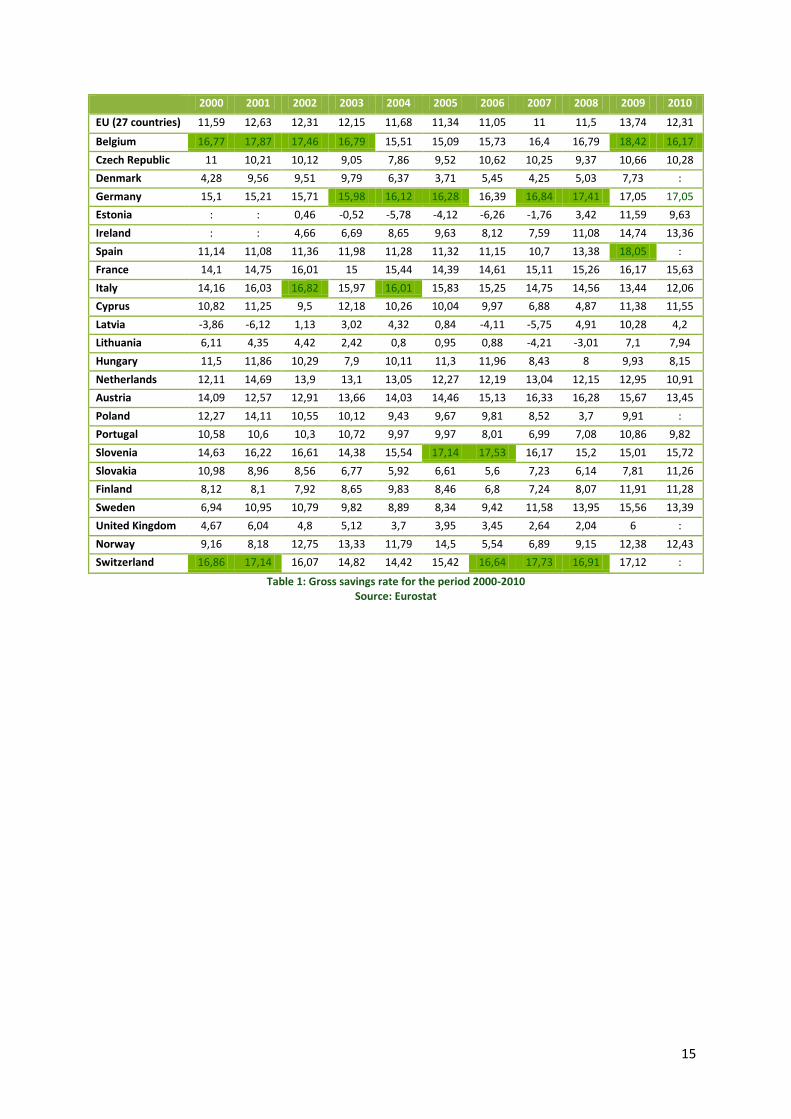

SAVINGS RATIO OF HOUSEHOLDS

When comparing the gross savings ratios of 2010 for the European Union (Figure 6), we see that

Belgium has almost the highest gross savings rate of the EU countries concerned2. Only Germany had

a higher gross savings rate in 2010. In the periods before, Belgium also had a very high gross savings

ratio. Therefore, Table 1 represents the gross savings ratio over the last 11 years for the European

countries. This table shows us that Belgium’s gross savings rate has always been above the EU-27

gross savings ratio. Furthermore, of all the countries listed, Belgium, Switzerland and Germany have

had the highest gross savings ratio.

Figure 6: Gross Savings ratio of households in EU, 2010 data

Source: Eurostat

2 The gross savings rate of households is defined as gross savings (ESA95 code: B8G) divided by gross disposable income

(B6G), with the latter being adjusted for the change in the net equity of households in pension funds reserves (D8net)

(Eurostat, 2011). Gross savings is the part of the gross disposable income that is not spent as final consumption

expenditure. Detailed data and methodology at: http://ec.europa.eu/eurostat/sectoraccounts.

17,05

16,17

15,72

15,63

13,45

13,39

13,36

12,43

12,31

12,06

11,55

11,28

11,26

10,91

10,28

9,82

9,63

8,15

7,94

4,2

0 5 10 15 20

Germany

Belgium

Slovenia

France

Austria

Sweden

Ireland

Norway

EU (27 countries)

Italy

Cyprus

Finland

Slovakia

Netherlands

Czech Republic

Portugal

Estonia

Hungary

Lithuania

Latvia

15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

EU (27 countries) 11,59 12,63 12,31 12,15 11,68 11,34 11,05 11 11,5 13,74 12,31

Belgium 16,77 17,87 17,46 16,79 15,51 15,09 15,73 16,4 16,79 18,42 16,17

Czech Republic 11 10,21 10,12 9,05 7,86 9,52 10,62 10,25 9,37 10,66 10,28

Denmark 4,28 9,56 9,51 9,79 6,37 3,71 5,45 4,25 5,03 7,73 :

Germany 15,1 15,21 15,71 15,98 16,12 16,28 16,39 16,84 17,41 17,05 17,05

Estonia : : 0,46 -0,52 -5,78 -4,12 -6,26 -1,76 3,42 11,59 9,63

Ireland : : 4,66 6,69 8,65 9,63 8,12 7,59 11,08 14,74 13,36

Spain 11,14 11,08 11,36 11,98 11,28 11,32 11,15 10,7 13,38 18,05 :

France 14,1 14,75 16,01 15 15,44 14,39 14,61 15,11 15,26 16,17 15,63

Italy 14,16 16,03 16,82 15,97 16,01 15,83 15,25 14,75 14,56 13,44 12,06

Cyprus 10,82 11,25 9,5 12,18 10,26 10,04 9,97 6,88 4,87 11,38 11,55

Latvia -3,86 -6,12 1,13 3,02 4,32 0,84 -4,11 -5,75 4,91 10,28 4,2

Lithuania 6,11 4,35 4,42 2,42 0,8 0,95 0,88 -4,21 -3,01 7,1 7,94

Hungary 11,5 11,86 10,29 7,9 10,11 11,3 11,96 8,43 8 9,93 8,15

Netherlands 12,11 14,69 13,9 13,1 13,05 12,27 12,19 13,04 12,15 12,95 10,91

Austria 14,09 12,57 12,91 13,66 14,03 14,46 15,13 16,33 16,28 15,67 13,45

Poland 12,27 14,11 10,55 10,12 9,43 9,67 9,81 8,52 3,7 9,91 :

Portugal 10,58 10,6 10,3 10,72 9,97 9,97 8,01 6,99 7,08 10,86 9,82

Slovenia 14,63 16,22 16,61 14,38 15,54 17,14 17,53 16,17 15,2 15,01 15,72

Slovakia 10,98 8,96 8,56 6,77 5,92 6,61 5,6 7,23 6,14 7,81 11,26

Finland 8,12 8,1 7,92 8,65 9,83 8,46 6,8 7,24 8,07 11,91 11,28

Sweden 6,94 10,95 10,79 9,82 8,89 8,34 9,42 11,58 13,95 15,56 13,39

United Kingdom 4,67 6,04 4,8 5,12 3,7 3,95 3,45 2,64 2,04 6 :

Norway 9,16 8,18 12,75 13,33 11,79 14,5 5,54 6,89 9,15 12,38 12,43

Switzerland 16,86 17,14 16,07 14,82 14,42 15,42 16,64 17,73 16,91 17,12 :

Table 1: Gross savings rate for the period 2000-2010 Source: Eurostat

16

BANKING SECTOR’S CONTRIBUTION COMPARED WITH EUROPEAN PEERS

The following sections of Chapter 1 will focus more specifically on the banking sector (instead of on

the financial sector in general).

Figure 7 shows the total assets held by the banking industry relative to the GDP for each country of

the European Union at the end of 2010. The total assets held by the Belgian Credit Institutions

amount to 3.53 times Belgium’s GDP.

Figure 7: Banking sector's contribution to the economy: Consolidated total assets of all Credit Institutions compared to GDP

Source: Eurostat

19,64

9,29

9,28

8,37

6,58

4,82

4,20

4,05

3,96

3,75

3,65

3,53

3,49

3,08

2,58

2,17

2,16

1,78

1,59

1,59

1,33

1,09

1,01

0,95

0,82

0,78

0,64

0 5 10 15 20 25

LUXEMBOURG

IRELAND

CYPRUS

MALTA

UNITED KINGDOM

NETHERLANDS

AUSTRIA

SWEDEN

DENMARK

GERMANY

SPAIN

BELGIUM

FRANCE

PORTUGAL

FINLAND

GREECE

ESTONIA

ITALY

SLOVENIA

LATVIA

HUNGARY

CZECH REPUBLIC

BULGARIA

LITHUANIA

SLOVAKIA

POLAND

ROMANIA

17

According to ECB data, 106 banks are established in Belgium (end of December 2010, see Figure 8) –

48 of those banks are under Belgian law, the rest operates under foreign law: branches of non-EEA

(European Economic Area)-based banks (9), branches of the euro-area-based credit institutions (41)

and branches of EEA-based credit institutions (outside the euro area) (8).

Figure 8: Number of banks established in Belgium Source: ECB

8

41

9

48

branches of EEA-based creditinsitutions (outside the euroarea)

branches of euro-area basedcredit institutions

branches of non EEA basedbanks

credit institutions legallyincorporated in the reportingcountry

18

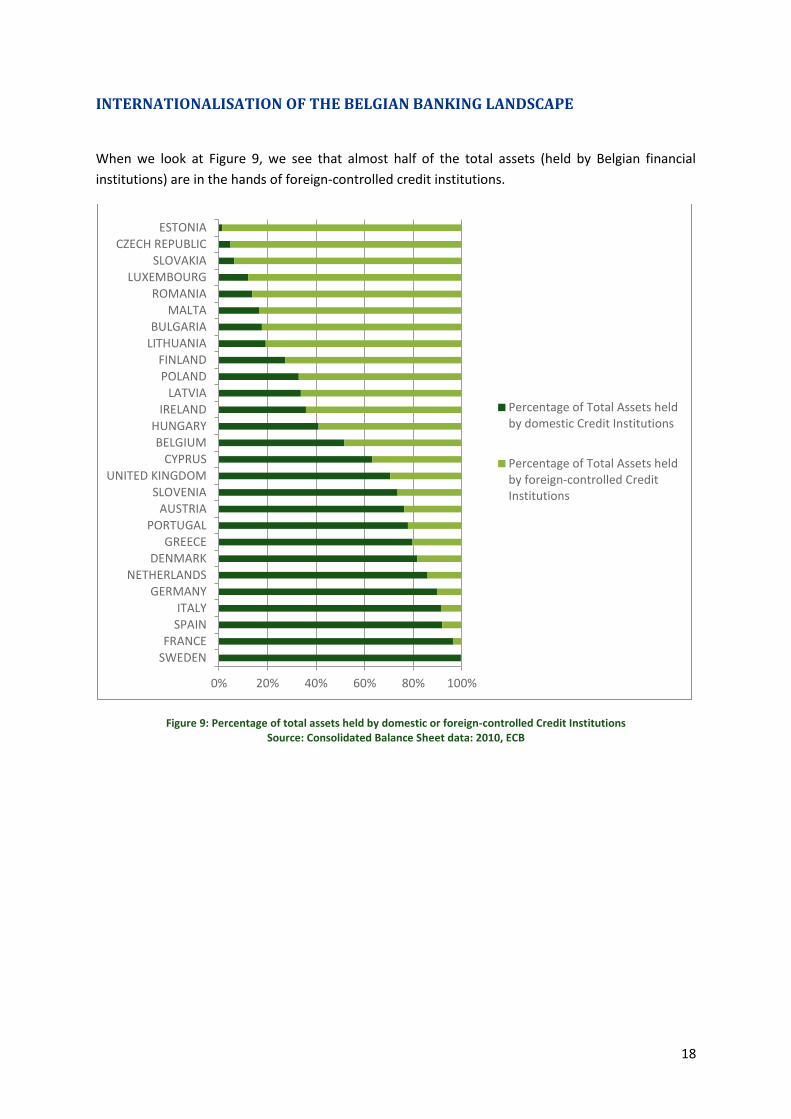

INTERNATIONALISATION OF THE BELGIAN BANKING LANDSCAPE

When we look at Figure 9, we see that almost half of the total assets (held by Belgian financial

institutions) are in the hands of foreign-controlled credit institutions.

Figure 9: Percentage of total assets held by domestic or foreign-controlled Credit Institutions Source: Consolidated Balance Sheet data: 2010, ECB

0% 20% 40% 60% 80% 100%

SWEDENFRANCE

SPAIN

ITALYGERMANY

NETHERLANDSDENMARK

GREECEPORTUGAL

AUSTRIASLOVENIA

UNITED KINGDOM

CYPRUSBELGIUM

HUNGARY

IRELANDLATVIA

POLAND

FINLANDLITHUANIABULGARIA

MALTAROMANIA

LUXEMBOURGSLOVAKIA

CZECH REPUBLIC

ESTONIA

Percentage of Total Assets heldby domestic Credit Institutions

Percentage of Total Assets heldby foreign-controlled CreditInstitutions

19

CHAPTER 2: THE VALUE CHAIN

In this chapter, we focus on the value chain of the Belgian banking sector as presented in Figure 10.

The value chain is broken down into three components on the income side (net interest income, net

commissions and financial transactions) and into two blocks on the expenses side (operating

expenses and loan losses). We first present the break-down based on the segments proposed by

the ECB3 (i.e. investment banks and universal banks). Second, we present the break-down by the size

(i.e. total assets) of the banks as suggested by KPMG and then, we look more specifically at the Big

Four players in Belgium. Finally, we present the break-down based on the segments defined by

BankScope.

Figure 10: The Value Chain of a Bank

In the first section, we briefly describe our sample as well as the categorisation of the banks in

different segments. The next sections are dedicated to different parts of the value chain, and the last

section concludes our discussion.

3 To make a segmentation, we have borrowed a classification that is used in an ECB paper: ‘Beyond ROE- how to measure

bank performance?; Appendix to the report on EU banking structures’, September 2010.

20

SAMPLE SELECTION AND SEGMENTS DESCRIPTION

Sample Selection

In the pre-processing phase of this study, we had to define our research sample. Based on both the

list of the ‘members of the BVB’ (list from Febelfin) and on BankScope (database managed by Bureau

van Dijk), we started gathering data for the banks in Belgium. Consolidated data for Dexia group and

KBC group were removed from the sample, since a major part of their business originates from

foreign activities. However, we were able to extract data from Dexia Bank Belgium and KBC Bank

Belgium, and these are included in the final sample. This resulted in an initial sample of 33 banks

which had accounting data available for 2010. As this study examines a time span of 10 years (i.e.

2001-2010), banks with too many missing values were removed from the sample. This yielded a final

sample of 23 banks. However, we must point out that the percentage of the total assets in 2010 of

our final sample was 92.12% of the total assets of the original sample.

When we limit the time span of our study to the period of 2001-2009, we are able to include six

more banks. These banks are: Banque Delen NV (private), Citibank Belgium NV/SA (commercial),

Delta Lloyd Bank (commercial), Deutsche Bank Sa (commercial), F. van Lanschot Bankiers Belgie

(private) and Société Générale Private Banking (private).

Adding these six banks to our sample means that, for the period from 2001 to 2009, we have data on

29 banks. For the full period 2001-2010, 23 banks are in the sample. Although these six banks

contribute only 1.90% of the total assets in the sample for the year 2009, we believe that adding

these banks to our sample brings added value to this research. We also need to stress that the four

major banks (i.e. BNP Paribas Fortis (former Fortis), KBC, ING and Dexia) together have a percentage

of 88.98% of the total assets in 2009. Appendix 6 shows the division of our sample based on total

assets in 2009 and per segment.

ECB segmentation

The classification of banks can be based on the sustainability of bank revenues. As suggested by a

report of the ECB4, banks can be classified on the basis of their share of core banking income, such as

net interest income and fees and commissions from on-balance sheet activities, compared to the

share of so-called non-recurring revenue activities, such as income from fees not related to balance

sheet activities as well as trading income and other one-off gains. Based on the sustainability of bank

revenues, we have created two sub-groups: universal banks and investment banks (see Table 2). As

mentioned previously, three income drivers can be distinguished in banking: (1) net interest income,

(2) net commissions and (3) financial transactions. In this exercise, banks are identified as driven by

investment activity when their share of commissions and trading income was higher than the share

of net interest income and other income in most periods, meaning that more than 50% of their total

income originates from net commissions and financial transactions.

4 ECB paper: ‘Beyond ROE- how to measure bank performance?; Appendix to the report on EU banking structures’,

September 2010.

21

In this categorisation, an investment bank is a financial intermediary that generates more income

from non-traditional deposit-to-loans transformation, whereas a universal bank is more active in the

banking book activities than in the trading activities of a bank, thus more involved in traditional

commercial banking5.

Investment Banks Universal Banks

Banque Degroof SA-Bank Degroof NV Agricaisse - Caisse Coopérative de Dépôts et de Crédit Agricole

Banque Delen NV (2001-2009) Antwerps Beroepskrediet

Byblos Bank Europe SA Argenta Spaarbank-ASPA

F. van Lanschot Bankiers Belgie (2001-2009) Banca Monte Paschi Belgio SA

Keytrade Bank SA/NV Bank J. Van Breda en Co NV

Société Générale Private Banking N.V.(2001-2009)

Banque de la Poste-Bank van de Post

BKCP

CBC Banque S.A.

Centea

Citibank Belgium N.V./S.A.(2001-2009)

Crédit Agricole SA-Landbouwkrediet

Delta Lloyd Bank (2001-2009)

Deutsche Bank SA-Deutsche Bank NV (2001-2009)

Dexia Bank Belgium-Dexia Bank

Ethias Bank

Europabank

Fortis Bank SA/ NV-BNP Paribas Fortis

ING Belgium SA/NV-ING

KBC Bank NV

Onderling Beroepskrediet-OBK-Bank C.V.B.A.

Record Bank SA/NV

Santander Benelux SA/NV

VDK Spaarbank NV

Table 2: Two categories in bank sample: investment banks and universal banks Source: BankScope + KPMG’s own calculations

5 Some potential issues associated with this approach are related to the unstable nature of the mix of these sources of

income. For example, if trading income is negative and commission income positive, they can cancel each other, leaving a

small proportion for these types of revenue. However, when we use squared shares to check our results, we arrive at a

similar outcome, which makes us confident in our conclusions.

22

Size segmentation

A third categorisation in this study is based on the size of the banks. This allows us to investigate

whether there are significant differences among banks of different sizes as measured by total assets

(TA), with regard to the characteristics under study. The 4 categories are as follows:

The first category contains the banks with total assets over €100 billion. This category

contains the Big Four banks: Fortis, KBC, Dexia and ING.

Our second category contains the banks with total assets between €100 billion and €10

billion. This category includes 4 banks. Our third category also consists of 4 banks. This

category contains banks with total assets between €10 billion and €7 billion.

Our fourth category consists of all of the other banks with total assets of less than €7 billion.

This category contains 17 banks. Table 3 shows the categories:

TA > €100 billion TA ≤ €7 billion

Fortis Bank SA/ NV-BNP Paribas Fortis Delta Lloyd Bank

KBC Bank NV Banque Degroof SA-Bank Degroof NV

Dexia Bank Belgium-Dexia Bank BKCP

ING Belgium SA/NV-ING Citibank Belgium N.V./S.A.

€100 billion ≥ TA > €10 billion Bank J. Van Breda en Co NV

Argenta Spaarbank-ASPA VDK Spaarbank NV

Record Bank SA/NV Agricaisse - Caisse Coopérative de Dépôts et de Crédit Agricole

Deutsche Bank SA-Deutsche Bank NV F. van Lanschot Bankiers Belgie

Centea Ethias Bank

€10 billion ≥ TA > €7 billion Keytrade Bank SA/NV

Crédit Agricole SA-Landbouwkrediet Banca Monte Paschi Belgio SA

CBC Banque S.A. Banque Delen NV

Santander Benelux SA/NV Onderling Beroepskrediet-OBK-Bank C.V.B.A.

Banque de la Poste-Bank van de Post Europabank

Société Générale Private Banking N.V.

Byblos Bank Europe SA

Antwerps Beroepskrediet

Table 3: Sample of the banks divided by size

In the last step, we examine the details of the four big banks.

Bank TA in 2010 Fortis Bank SA/ NV-BNP Paribas Fortis €347.967 billion

KBC Bank NV €276.723 billion

Dexia Bank Belgium-Dexia Bank €247.902 billion

ING Belgium SA/NV-ING €155.639 billion

23

BankScope segmentation

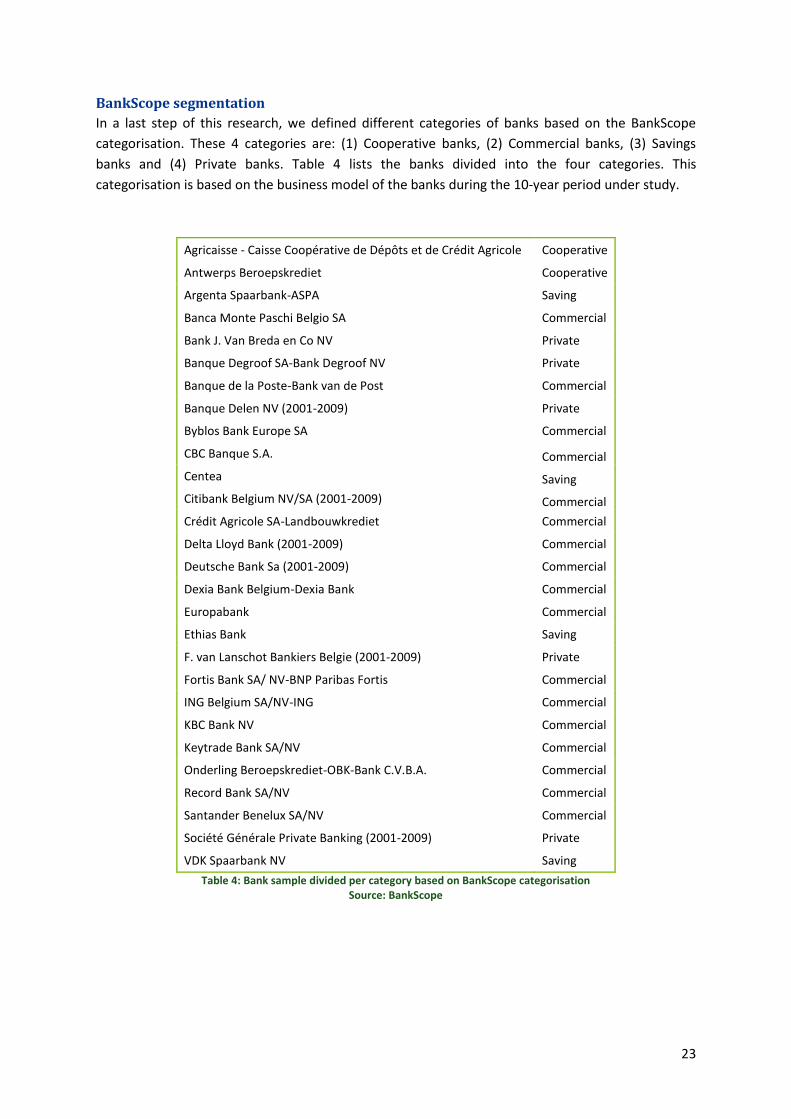

In a last step of this research, we defined different categories of banks based on the BankScope

categorisation. These 4 categories are: (1) Cooperative banks, (2) Commercial banks, (3) Savings

banks and (4) Private banks. Table 4 lists the banks divided into the four categories. This

categorisation is based on the business model of the banks during the 10-year period under study.

Agricaisse - Caisse Coopérative de Dépôts et de Crédit Agricole Cooperative

Antwerps Beroepskrediet Cooperative

Argenta Spaarbank-ASPA Saving

Banca Monte Paschi Belgio SA Commercial

Bank J. Van Breda en Co NV Private

Banque Degroof SA-Bank Degroof NV Private

Banque de la Poste-Bank van de Post Commercial

Banque Delen NV (2001-2009) Private

Byblos Bank Europe SA Commercial

CBC Banque S.A. Commercial

Centea Saving

Citibank Belgium NV/SA (2001-2009) Commercial

Crédit Agricole SA-Landbouwkrediet Commercial

Delta Lloyd Bank (2001-2009) Commercial

Deutsche Bank Sa (2001-2009) Commercial

Dexia Bank Belgium-Dexia Bank Commercial

Europabank Commercial

Ethias Bank Saving

F. van Lanschot Bankiers Belgie (2001-2009) Private

Fortis Bank SA/ NV-BNP Paribas Fortis Commercial

ING Belgium SA/NV-ING Commercial

KBC Bank NV Commercial

Keytrade Bank SA/NV Commercial

Onderling Beroepskrediet-OBK-Bank C.V.B.A. Commercial

Record Bank SA/NV Commercial

Santander Benelux SA/NV Commercial

Société Générale Private Banking (2001-2009) Private

VDK Spaarbank NV Saving

Table 4: Bank sample divided per category based on BankScope categorisation Source: BankScope

24

OPERATIONAL INCOME TO TOTAL ASSETS

Step 1 of this research investigates the gross or total revenue (measured as the sum of net interest

income, net commissions and fees, and income from financial transactions) of the banks divided by

total assets. We see the evolution of their ability to generate revenue over the time period under study

(2001-2010). In a second step, we investigate the main drivers for the change in operational income

(i.e. net interest income, net commissions and fees, or income from financial transactions).

When we use the 2-category categorisation (universal and investment banks), we see that the

investment banks generate substantially higher income than the universal banks. In 2001, investment

banks reported more than 7.00% for the ratio of operational income to total assets due to the 16.7%

figure of Keytrade. The figure of Keytrade dropped in 2002 after the acquisition of RealBank during

2002.

Figure 11: Operational income to total assets between investment and universal banks Source: BankScope

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

2001200220032004200520062007200820092010

Investment Banks

Universal Banks

25

Figure 12 shows the evolution of operational income to total assets split into the 4 size-based

categories. It is noteworthy that the banks with total assets less than €7 billion – i.e. the 17 smallest

banks – are generating by far the best operational income relative to total assets. While the overall

trend during the period under study is a decrease in the operational income to total assets, after 2005

the banks between €7 and €10 billion in assets were able to outperform the bigger banks, except for a

small recovery of the biggest banks in 2009 and 2010.

Figure 12: Operational income to total assets based on size (million €) Source: BankScope

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

4,50%

5,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

TA > 100 000

TA > 10 000

TA > 7 000

TA < 7 000

26

When investigating the four biggest banks on an individual basis, we see that operational income to

total assets for KBC was very volatile over the period under study. In the period 2002-2007, KBC

generated the highest operational income to total assets. However, this ratio plummeted in 2008, from

1.68% to 0.56%. The reason for this drop is the devaluation of certain trading products (annual report

KBC Bank, 2008). In 2008, Fortis showed a drop in operational income to total assets as well, also

associated with write-downs related to the financial crisis. Only ING and Dexia generated extra income

per euro of assets in 2008. Dexia’s results were not harmed in 2008. However, after the financial crisis

hit the markets in 2008, operational income for Dexia decreased in 2009. As a conclusion, we can say

that ING is the only bank of the Big Four that was not affected in their reported results by the financial

crisis. In both 2008 and 2009, their operational income even showed an increase. The main drivers for

these remarkable results will be discussed in the next sections. At the end of 2010, KBC was again

leading the Big Four with the highest operational income to total assets ratio.

Figure 13: Operational income to total assets for Fortis, KBC, Dexia and ING Source: BankScope

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Fortis

KBC

Dexia

ING

27

When comparing the 4 bank categories (cooperative banks, commercial banks, savings banks and

private banks), we clearly see that more income to total assets is generated by private banks than by

cooperative, commercial or savings banks. This result might be related to the nature of the activities of

a private bank, which requires lower assets than the three other categories. Another noteworthy fact is

the overall downward trend in this ratio over the last decade.

It is also noteworthy that private banks are creating twice as much operational income to total assets as

savings banks. In 2008, the cooperative banks’ income ratio decreased by approximately 25%: in 2007,

their operational income ratio was 2.31%, declining to 1.74% in 2008. Recovery is observable in 2009

and ends with the second highest operating income in 2010. For the other types of banks, operational

income to total assets decreased during the financial crisis but not as much as the trend observed in the

cooperative banks. When drawing conclusions based on the BankScope segmentation, one has to

realise that there are only 2 cooperative banks in the sample and only 4 savings banks.

Figure 14: Operational income to total assets based on the BankScope segmentation

Source: BankScope

NET INTEREST INCOME TO TOTAL ASSETS

All the banks in our sample act as financial intermediaries: the bank generates profits by transforming

deposits into bank loans. This is the first component of the value chain: net interest income. Net

interest income (NII) is measured as the difference between revenues generated by interest-bearing

assets and the cost of paying interests on deposits. To assess the importance of financial intermediation

relative to the other components of the value chain on the income-side, we compare the different

components of the value chain by dividing each of them by total assets.

When explaining the change in net interest income, the maturity structure of the assets and liabilities

must be considered as well. Generally speaking, the average maturity on the asset side is larger than

the maturities measured on the liability side. This implies that changes in market interest rates have an

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Coop. Bank

Comm. Bank

Savings Banks

Private Banks

28

almost immediate influence on interest expenses. This could imply that, when interest rates increase,

NII decreases relatively6. In addition, recent literature (Bolt et al, 2010) suggests that bank’s lending

history should be taken into account when discussing NII in times of financial distress. Long-term

interest rates from previous years, characterised by economic growth (resulting in higher lending

activity), are found to be important determinants of Interest Income. However, the effect of long-term

interest rates on net interest income declines in time, due to repayments of loans as well as the growth

of the loan portfolio over time.

The division between universal and investment banks shows that universal banks are generating most

of their profits from financial intermediation, which could be expected given the definition of universal

banks. The NII to TA for universal banks decreases for most of the period under study, mainly due to an

increasing trend in total assets. Looking at the investment banks, no general trend can be found. Note

that the gap between the two types of banks is decreasing.

Figure 15: Net interest income to total assets between investment and universal banks Source: BankScope

Figure 16 shows that the four biggest banks generated less net interest income to total assets than the

three other categories of banks, except in 2009-2010, when they were slightly higher than the banks

between €10 and €100 billion in assets.

Note that the 17 smallest banks generated the highest net interest income to total assets during the

entire period. However, the gap between the smallest banks and the third category (between €7 and

€10 billion in assets) was very small in 2007. As we go from 2001 to 2010, the four categories of banks

move closer to each other. This might reflect the greater interest of the big banks in financial

intermediation as the back-to-basics strategy in the aftermath of the financial crisis.

6 This relationship has been well-known for a long time (e.g. Préfontaine and Thibeault, 1993; English, 2002).

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

2001200220032004200520062007200820092010

Investment Banks

Universal Banks

29

Figure 16: Net interest income to total assets based on size (million €) Source: BankScope

When looking at the four biggest banks individually, one can observe a counter-cyclical trend compared

to economic growth (we used the Bel-20 as our business cycle indicator). This trend is especially

observable for KBC as can be seen in Figure 17. This result contradicts the findings of Albertazzi and

Gambacorta (2008). They found that there is a positive relationship between net interest income and

the business cycle, represented by GDP.

Figure 17: Evolution of the NII to total assets from KBC compared to the BEL-20 stock index Source: DataStream (Bel-20) and BankScope (KBC NII/TA)

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

TA > 100 000

TA > 10 000

TA > 7 000

TA < 7 000

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

0,00%

0,50%

1,00%

1,50%

2,00%

Be

l-2

0 (

valu

e)

KB

C N

II/T

A (

%)

30

In 2009, KBC’s Net Interest Income to total assets increased most in comparison with the other years.

According to KBC, this was mainly attributable to a stronger performance in deposit and loan margins7

(following the exceptionally high rates of interest paid on deposits since the summer of 2008), and the

shift on the deposit side towards products that generate a higher margin. These factors caused the net

interest margin to widen from 1.47% in 2008 to 1.58% in 2009. The group’s total volume of loans and

deposits in Belgium ended 3% higher and 6% lower, respectively, than in 2008 (KBC annual report 2009,

page 29).

When looking at the NII/TA ratio for Fortis, we see an increase of 24.29% in 2009, and an increase of

21.83% in 2010. This is again a consequence of the favourable funding conditions. In 2010, the NII to TA

increased further, indicating the same trend as observed for KBC.

During the period 2001-2004, ING’s NII/TA remained stable. In 2005-2007, their income generated by

transforming deposits into loans decreased. This decrease was mainly due to a significant increase in

their total assets, as they were generating more net interest income. In 2008, NII to TA increased again.

Although the TA of the bank decreased (-2.28%), the bank was able to generate more net interest

income (+11.98%). Despite difficult Belgian market conditions, ING was able to attract more deposits

(+7.1%) and sell more loans (+11%) (Press Release ING Belgium 2008), resulting in a better ratio for

2008. In 2009, ING was able to publish even better NII/TA results. The better market conditions (i.e.

more convenient spread between deposits and loans) and an increase in the credits that were granted

(more than €4 billion new credits, press release ING Belgium 2009) were the main drivers for the

increase in NII to TA.

Dexia shows the same trend as can be observed for ING. In the period 2004-2007, their TA increased

more than their NII, resulting in a decreasing trend. In both 2009 and 2010, their NII decreased more

than the decline in total assets – therefore, a negative trend in the ratio was observed.

Figure 18: Net interest income for Fortis, KBC, Dexia and ING

Source: BankScope

7 In 2009, the base rate paid for traditional savings deposits fell to 1%, down from its record level of 4% in the summer of 2008.

(KBC annual report 2009, page 20).

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Fortis

KBC

Dexia

ING

31

Figure 19 shows that NII to TA for the cooperative banks is the highest of the whole sample, except in

2008 when this category of banks fell just below the commercial banks after a drop of 16.53% in their

net interest income to total assets. The main driver for this decrease is the NII to TA ratio of ‘Antwerps

Beroepskrediet’. As there are only 2 cooperative banks in the sample, a big change in the ratio of one of

these banks has a substantial influence on the group. The net interest income to total assets for the

commercial banks followed the same trend as the trend observed for the cooperative banks. However,

their NII to TA was more stable during the entire period under study. Looking at the savings banks, we

see that their NII to TA did not change that much. In both 2007 and 2008, a slight decrease can be

observed. Starting in 2001 up until 2007, the NII to TA for private banks decreased. In 2008, a swing in

the trend can be observed, ending with a big increase in 2010.

Figure 19: Net interest income to total assets based on the BankScope segmentation Source: BankScope

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Coop. Banks

Comm. Banks

Savings Banks

Private Banks

32

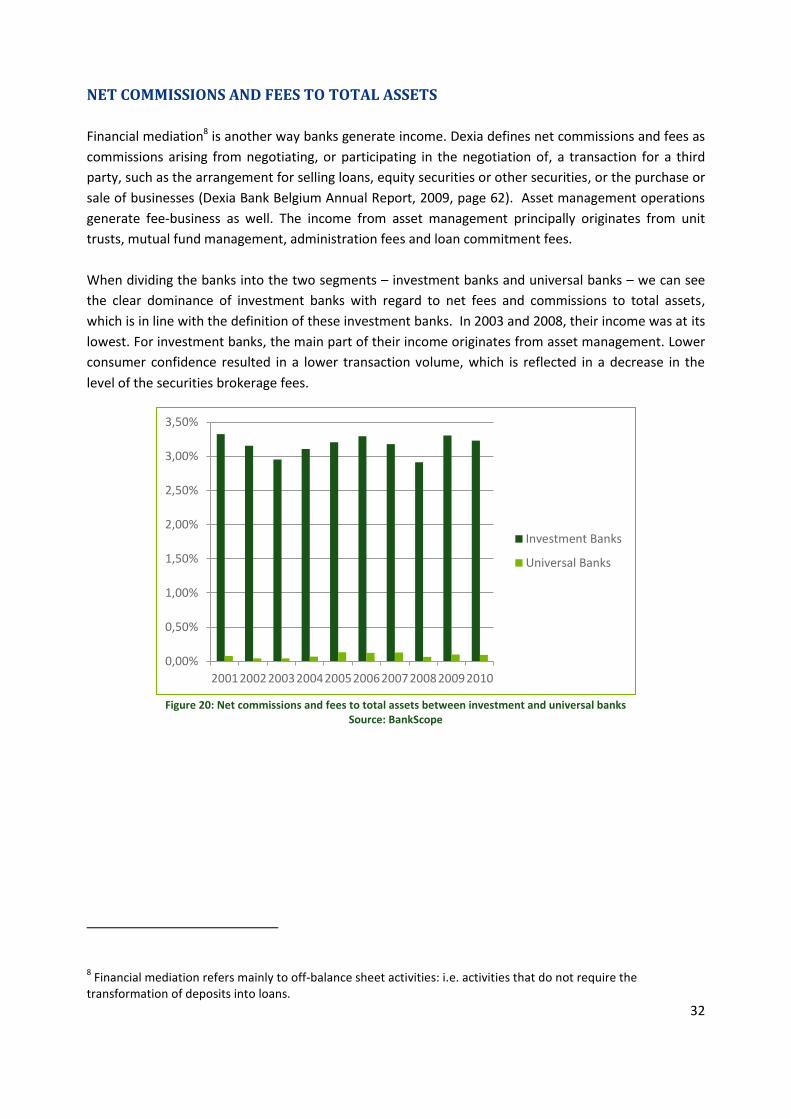

NET COMMISSIONS AND FEES TO TOTAL ASSETS

Financial mediation8 is another way banks generate income. Dexia defines net commissions and fees as

commissions arising from negotiating, or participating in the negotiation of, a transaction for a third

party, such as the arrangement for selling loans, equity securities or other securities, or the purchase or

sale of businesses (Dexia Bank Belgium Annual Report, 2009, page 62). Asset management operations

generate fee-business as well. The income from asset management principally originates from unit

trusts, mutual fund management, administration fees and loan commitment fees.

When dividing the banks into the two segments – investment banks and universal banks – we can see

the clear dominance of investment banks with regard to net fees and commissions to total assets,

which is in line with the definition of these investment banks. In 2003 and 2008, their income was at its

lowest. For investment banks, the main part of their income originates from asset management. Lower

consumer confidence resulted in a lower transaction volume, which is reflected in a decrease in the

level of the securities brokerage fees.

Figure 20: Net commissions and fees to total assets between investment and universal banks

Source: BankScope

8 Financial mediation refers mainly to off-balance sheet activities: i.e. activities that do not require the

transformation of deposits into loans.

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

2001200220032004200520062007200820092010

Investment Banks

Universal Banks

33

Figure 21 shows the evolution of net commissions and fees to total assets based on the size of the

banks. This graph shows us immediately that both the Big Four and the 17 smallest banks are the only

two groups who never had negative net commissions income. It is also noteworthy that the smallest

banks generate the best net commissions and fees to total assets. Their income originating from fee

business is even more than twice as high as the Big Four banks. The negative net commissions and fees

to total assets for the second category of banks is due to the fact that, in this group, only Deutsche Bank

recorded positive net commissions and fees during these years.

Figure 21: Net commissions and fees to total assets based on size (million €)

Source: BankScope

When investigating the four biggest banks individually, we see that the fees and commissions income

for ING is relatively stable over time, even at the time when the financial crisis fully impacts the

economy. However, in 2008 there was a slight decrease in this source of income for ING. According to

ING, this decrease was driven by lower asset management fees and lower income from their securities

business (annual report ING Bank 2008, page 5). In 2009, their commissions income increased, thanks

to fees earned on waivers and restructuring (annual report ING Bank 2009, page 8).

In 2008, KBC and Fortis reported a sharp decrease in fees and commissions income. According to KBC,

this decrease was an effect of the crisis: reduced sales of investment funds and unit-linked life

insurance products, which were reflected in lower net fees and commissions income. Due to the

financial and stock market crisis, investors turned their backs on investment funds and certain

investment-type insurance, opting instead for traditional deposit products. As a result, fee commission

income declined. Conversely, fees and commissions paid (primarily to insurance agents) went up, due

to increased sales of insurance and new acquisitions. In 2008, total assets under management by the

group decreased by approximately 10% to €207 billion, which was attributable entirely to the decline in

value of the assets under discussion (-12 percentage points) and a limited inflow of assets (+1

percentage point) (Annual report KBC 2008, pages 18 and 21). In 2010, net commissions were back to

the pre-crisis level for most of the banks.

-0,40%

-0,20%

0,00%

0,20%

0,40%

0,60%

0,80%

1,00%

1,20%

1,40%

1,60%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

TA > 100 000

TA > 10 000

TA > 7 000

TA < 7 000

34

Dexia’s net commissions income is noticeably lower compared to the other big banks (except for the

year 2001). The substantial decrease in 2002 is mainly due to off-balance sheet products, such as

mutual funds, which generated less income in the context of unattractive capital markets. In addition,

the stock exchange orders and commissions linked to debit cards decreased (Dexia annual report 2002,

page 63). In 2008, their net commissions started to decrease slowly. This is due mainly to the drop in

commissions received on unit trust funds (Dexia Bank Belgium annual report 2008, page 157). In 2009,

their net commissions decreased further as a result of the drop in commissions received on unit trust

funds and insurances, which was partly offset by the positive impact of the non-renewal in 2009 of

commissions paid on credit derivatives in 2008 (Dexia Bank Belgium annual report 2009, page 181).

Figure 22: Net commissions and fees to total assets for Fortis, KBC, Dexia and ING

Source: BankScope

0,00%

0,10%

0,20%

0,30%

0,40%

0,50%

0,60%

0,70%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Fortis

KBC

Dexia

ING

35

When dividing our sample per sector, the private banks clearly dominate the industry with regard to

net fees and commissions to total assets. In general, they generate higher income to total assets than

those involved in pure financial intermediation9. Since financial intermediation is far more important for

commercial banks, it is normal that their income generated by mediation amounts to only 10% of their

total income. Both the cooperative and the savings banks generated negative income. This is probably

due to the commissions paid for the distribution of some products.

Figure 23: Net fees and commissions to total assets based on the BankScope segmentation Source: BankScope

9 Financial intermediation refers to the transformation on the balance sheet of deposits into loans.

-1,00%

-0,50%

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Coop. Banks

Comm. Banks

Savings Banks

Private Banks

36

FINANCIAL TRANSACTIONS TO TOTAL ASSETS

Another non-interest income for banks is the income generated by financial transactions (trading

activities).

Comparing the investment banks and the universal banks, we see more or less what we expected. The

investment banks generated more income from financial transactions to total assets than the universal

banks. However, in 2009, with the full impact of the financial crisis, both types of banks reduced their

exposure substantially, which resulted in small losses for both.

Figure 24: Financial transactions to total assets between investment and universal banks Source: BankScope

-0,20%

-0,10%

0,00%

0,10%

0,20%

0,30%

0,40%

0,50%

2001200220032004200520062007200820092010

Investment Banks

Universal Banks

37

Figure 25 shows that the income from financial transactions for all banks is very low in Belgium

compared with the other types of income. Until 2005, the smallest banks in the sample generated more

income from financial transactions compared with the other banks. In 2006, the Big Four banks gained

ground on the smallest ones, generating more income on the financial markets due mainly to KBC’s

speculative portfolio. In 2007, they were able to generate the most income compared with the others.

However, in 2008 and 2009, they suffered important losses in their trading portfolios. In 2008, the

others managed to generate more income with financial transactions than the year before. But in 2009,

their trading income reduced compared with level of the year before, and they even made a loss. So the

smaller banks were also influenced by the financial market turmoil that started in 2007 in the United

States and reached Belgium in 2008.

Figure 25: Financial transactions to total assets based on size (million €) Source: BankScope

-0,50%

-0,40%

-0,30%

-0,20%

-0,10%

0,00%

0,10%

0,20%

0,30%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

TA > 100 000

TA > 10 000

TA > 7 000

TA < 7 000

38

In the first years under study, both KBC and ING generated more income with financial transactions

than Fortis and Dexia. In the following years, we can see KBC’s dominant position, first positive and

then negative in 2008 and 2009, before exiting their speculative position. In 2005, Dexia was the first

one to report losses on their financial assets. In 2006, the difference between the other banks and KBC

became bigger; KBC generated 0.67% of its income by financial transactions to total assets. The

discrepancy between the other banks and KBC was also high in 2008 and 2009. This time, however, KBC

generated losses in their financial assets.

Only ING succeeded in generating a positive value during the whole period under study. Their income

on financial assets remained stable over time. In the years before the financial crisis, this type of

income for ING was rather low compared with the other big banks, but the financial income in 2008 -

2009 did not decline in contrast to the other banks. This indicates that ING invests in less risky products,

as their income from financial transactions did not fluctuate very much.

Figure 26: Financial transactions to total assets for Fortis, KBC, Dexia and ING Source: BankScope

-1,50%

-1,00%

-0,50%

0,00%

0,50%

1,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Fortis

KBC

Dexia

ING

39

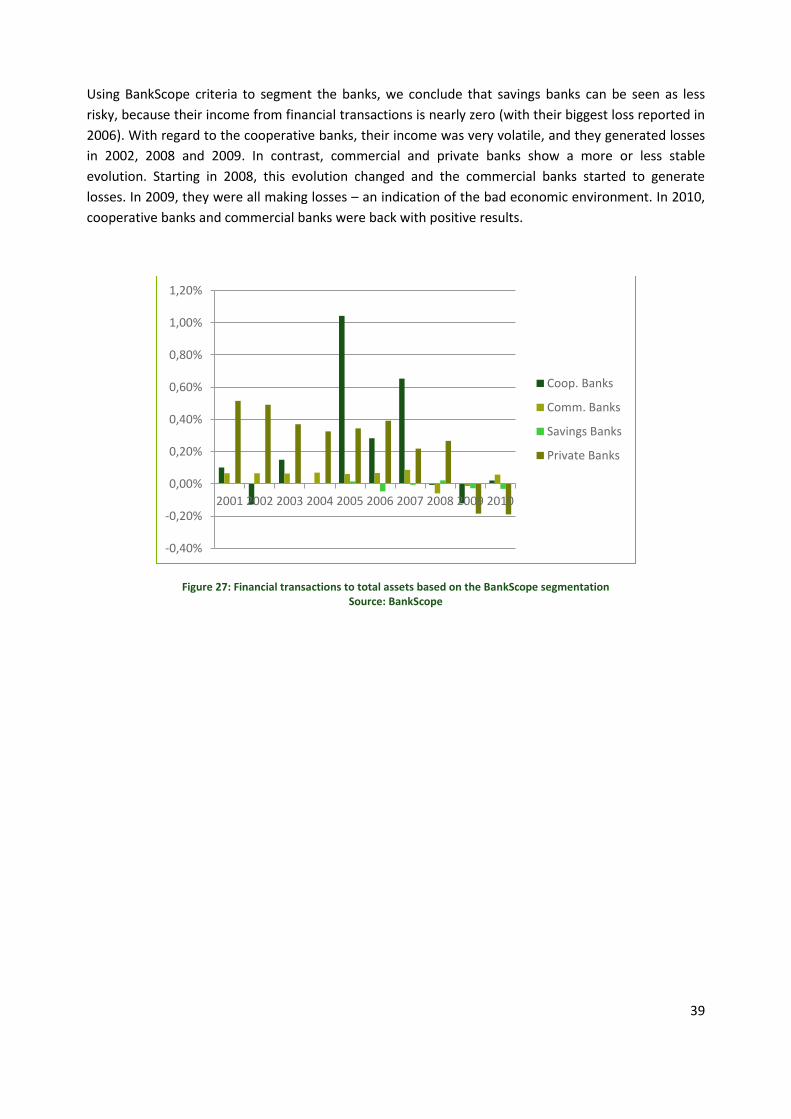

Using BankScope criteria to segment the banks, we conclude that savings banks can be seen as less

risky, because their income from financial transactions is nearly zero (with their biggest loss reported in

2006). With regard to the cooperative banks, their income was very volatile, and they generated losses

in 2002, 2008 and 2009. In contrast, commercial and private banks show a more or less stable

evolution. Starting in 2008, this evolution changed and the commercial banks started to generate

losses. In 2009, they were all making losses – an indication of the bad economic environment. In 2010,

cooperative banks and commercial banks were back with positive results.

Figure 27: Financial transactions to total assets based on the BankScope segmentation Source: BankScope

-0,40%

-0,20%

0,00%

0,20%

0,40%

0,60%

0,80%

1,00%

1,20%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Coop. Banks

Comm. Banks

Savings Banks

Private Banks

40

OPERATIONAL EXPENSES TO TOTAL ASSETS

When dividing our sample into investment banks and universal banks, the operational expenses10 to

total assets are higher for investment banks than for universal banks during the entire period. For

universal banks, the ratio is stable during the period 2001-2007. Starting in 2008, the operational

expenses to total assets decreased slightly. For investment banks, the ratio’s downward trend is more

accentuated over the period under study, with only a slight increase in 2008 and 2009. This increase in

the ratio for the investment banks is due to a small decrease of about 2% in total assets, while the

assets of the universal banks grew by 6% from 2008 to 2009.

Figure 28: Operational expenses to total assets between investment and universal banks Source: BankScope

Looking at the operational expenses relative to the size of the banks, we see that, in general, the

operational expenses to total assets have decreased over time. However, in 2008 there was a slight

increase for every category except the second one, total assets between €10 and €100 billion. As the

economic environment has been difficult since the end of 2007, for banks it has been more difficult to

keep their operational expenses at the same level. The growth of the Belgian economy slowed down

significantly in 2008. GDP fell in the fourth quarter, accompanied by an erosion in investor confidence.

Additionally, the inflation rate, which peaked in July 2008 (+5.9%) and was sustained by the rise in oil

prices, came down to a more reasonable, though still high, level of 2.9% in December 2008. This

contributed substantially to an increase in operating expenses (Financial report 2008 ING Bank Belgium,

page 5).

10 In “BankScope”, operational expenses are labelled “overheads”.

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

2001200220032004200520062007200820092010

Investment Banks

Universal Banks

41

Another noteworthy fact is that the smallest banks have by far the highest operational expenses

compared to their total assets. Also noteworthy is that the biggest banks do not have the lowest

operational expenses to total assets ratio, which could have been expected due to the benefits of

economies of scale. However, compared to the others, their operational expenses to total assets are

low, but the second category (TA > €10 billion) succeed in having the lowest costs – especially in the

years 2008-2010, when their operational expenses to total assets decreased substantially, and the

operational expenses to total assets for the Big Four increased slightly.

Also worth highlighting is the fact that, in 2005, the operational expenses for the third category

(TA < €7 billion) increased significantly, while for the others the ratio decreased. The main reason for

this increase was the change in operational expenses for Santander Benelux. From 0.73% in 2004, the

ratio increased to 2.13% in 2005. Their financial statements show that operational expenses increased,

but not as much as the decrease in total assets.

Figure 29: Operational expenses to total assets based on size (million €)

Source: BankScope

Figure 30 exhibits the high volatility in the operational expenses to total assets ratio for the four big

Belgian banks, except for Dexia, which shows a steady decrease in the ratio from 2001 to 2007, to

stabilise after that. KBC’s operational expenses to total assets ratio increased in both 2008 and 2009.

According to KBC, the increase in 2008 was not only due to the economic conditions but also to one-off

items such as new early retirement provisions and increased pension fund provisions (Annual Report

KBC 2008, page 27). In 2009, the operational expenses for KBC actually shrink but less than the decline

in total assets which was -11.6%; therefore, an increasing trend can be found in the ratio. This decline in

operational expenses is a consequence of the lower number of employees due to the downturn of

investment banking activities (KBC annual report 2009, page 39). ING’s operational expenses to total

assets also increased from 2007 to 2009. ING divides their banking activities into two segments: retail

banking and wholesale banking. They state that the retail part is responsible for substantially higher

investments in marketing and customer services, whereas the wholesale segment needed investments

to strengthen the front office in 2008. (Financial Report 2008 ING bank Belgium, page 6). In 2009, their

operational expenses to total assets increased; however, their operational expenses decreased. The

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

TA > 100 000

TA > 10 000

TA > 7 000

TA < 7 000

42

ratio increased because the total assets decreased more than the operational expenses did. This

decrease in operational expenses was due to the positive impact of cost containment initiatives, with all

business lines contributing to the decline (Financial Report ING Bank 2009, page 5).

Fortis exhibits a high volatility in the operational expenses to total assets ratio over the time period

under study. Here also, the changes in total assets need to be taken into account to interpret the

situation correctly. In 2008, Fortis’ total assets decreased by 23.5%, but at the same time, their

operational expenses decreased by 34.9%, pushing down the ratio of operational expenses to total

assets. In 2010, Fortis’ total assets increased again.

Looking at the evolution of Dexia, we see that their operational expenses to total assets remained

remarkably stable over the last few years. During the period 2001-2006, their operational expenses

decreased from 1.35% to 0.7%. From then on, the ratio remained stable.

Figure 30: Operational expenses to total assets for Fortis, KBC, Dexia and ING

Source: BankScope

0,00%

0,20%

0,40%

0,60%

0,80%

1,00%

1,20%

1,40%

1,60%

1,80%

2,00%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Fortis

KBC

Dexia

ING

43

Looking at the sub-categories based on BankScope, we can also see a generally decreasing trend in

operational expenses to total assets except for the cooperative banks. One can see that the private

banks have a much higher operational expenses to total assets ratio compared to the other categories.

As stated earlier, this might be due to the fact that private banking activities require fewer assets than

other banking activities. An interesting finding is that savings banks achieved the lowest operational

expenses to total assets in the industry.

Figure 31: Operational expenses to total assets based on the BankScope segmentation Source: BankScope

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

4,50%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Coop. Banks

Comm. Banks

Savings Banks

Private Banks

44

As the operational expenses to total assets ratio is the focus of many banks, Table 5 shows this ratio

averaged over the period 2008-2010 for all the banks. Santander Benelux outperforms the other banks

by far.

Bank Overhead to total assets

Agricaisse - Caisse Coopérative de Dépôts et de Crédit Agricole 0,41%

Antwerps Beroepskrediet 1,45%

Argenta Spaarbank-ASPA 0,36%

Banca Monte Paschi Belgio SA 1,12%

Bank J. Van Breda en Co NV 1,65%

Banque de la Poste-Bank van de Post 0,80%

Banque Degroof SA-Bank Degroof NV 3,41%

Banque Delen NV 3,07%

BKCP 1,96%

Byblos Bank Europe SA 1,61%

CBC Banque S.A. 1,56%

Centea 0,79%

Citibank Belgium N.V./S.A. 6,43%

Crédit Agricole SA-Landbouwkrediet 1,86%

Delta Lloyd Bank 2,42%

Deutsche Bank SA-Deutsche Bank NV 0,96%

Dexia Bank Belgium-Dexia Bank 0,67%

Ethias Bank 0,77%

Europabank 4,48%

F. van Lanschot Bankiers Belgie 1,31%

Fortis Bank SA/ NV-BNP Paribas Fortis 1,08%

ING Belgium SA/NV-ING 1,20%

KBC Bank NV 1,43%

Keytrade Bank SA/NV 1,26%

Onderling Beroepskrediet-OBK-Bank C.V.B.A. 1,74%

Record Bank SA/NV 0,65%

Santander Benelux SA/NV 0,07%

Société Générale Private Banking N.V. 5,78%

VDK Spaarbank NV 1,11% Table 5: Three-year average of the operational expenses to total assets ratio for the period 2008-2010

45

LOAN LOSS PROVISIONS TO TOTAL ASSETS

Another cost which can be categorised is provisions for loan losses. These provisions are used as a

buffer against expected losses in the bank’s loan portfolio.

A lot of research has already been conducted on the evolution of loan loss provisions and the business

cycle. All of the studies (e.g. Laeven and Majnoni, 2003; Bikker and Metzemakers, 2005; Dinamona,