anz roadshow nov2002 final - anz personal banking · 3 investor presentation delivering on our...

TRANSCRIPT

Investor PresentationAustralia and New Zealand Banking Group Limited

November 2002

2 Investor Presentation

Outline

• Result review– Overview– Revenue/Costs– Credit Quality

• Delivering for all stakeholders

• Strategy

• Outlook

3 Investor Presentation

Delivering on our commitments

• Performing well - record profit of $2,168m*

• Exceeded all targets*

– EPS Growth 17%– ROE 21.6%– Cost Income ratio 46.0%

• Strong capital position, well provisioned

• Record staff satisfaction – up 16% to 78%

• Exciting Restoring Customer Faith pilot

• Specialised business strategy operating well

• Stretch target for 2003 of 10% EPS growth

* Before significant transactions

4 Investor Presentation

Building a credible track record

1024 1106

14801747 1870

2168

400

900

1400

1900

2400

1997

1998

1999

2000

2001

2002

$m NPAT21.6

20.219.3

17.215.9

17.6

1012141618202224

1997

1998

1999

2000

2001

2002

% ROE

40

45

50

55

60

65

1997

1998

1999

2000

2001

2002

012345678

Income/Expenses

101171

198100

84

137

0

50

100

150

200

250

1997

1998

1999

2000

2001

2002

Total Shareholder Return

$b%

5 Investor Presentation

0 100 200 300

A diversified portfolio performing well

2002 NPAT $m

NPAT increase

NPAT decrease

Prior period NPAT

2nd half NPAT $m

0 100 200 300

Personal Banking AustraliaMortgagesInstitutional BankingTransaction ServicesSmall Med BusinessCorporate BankingPersonal Banking NZConsumer FinanceAsset FinanceForeign ExchangeStructured FinanceGroup TreasuryWealth ManagementCorp Finance & AdvisoryAsia/Pac Personal BankingCapital MarketsING JV/ANZ FM

6 Investor Presentation

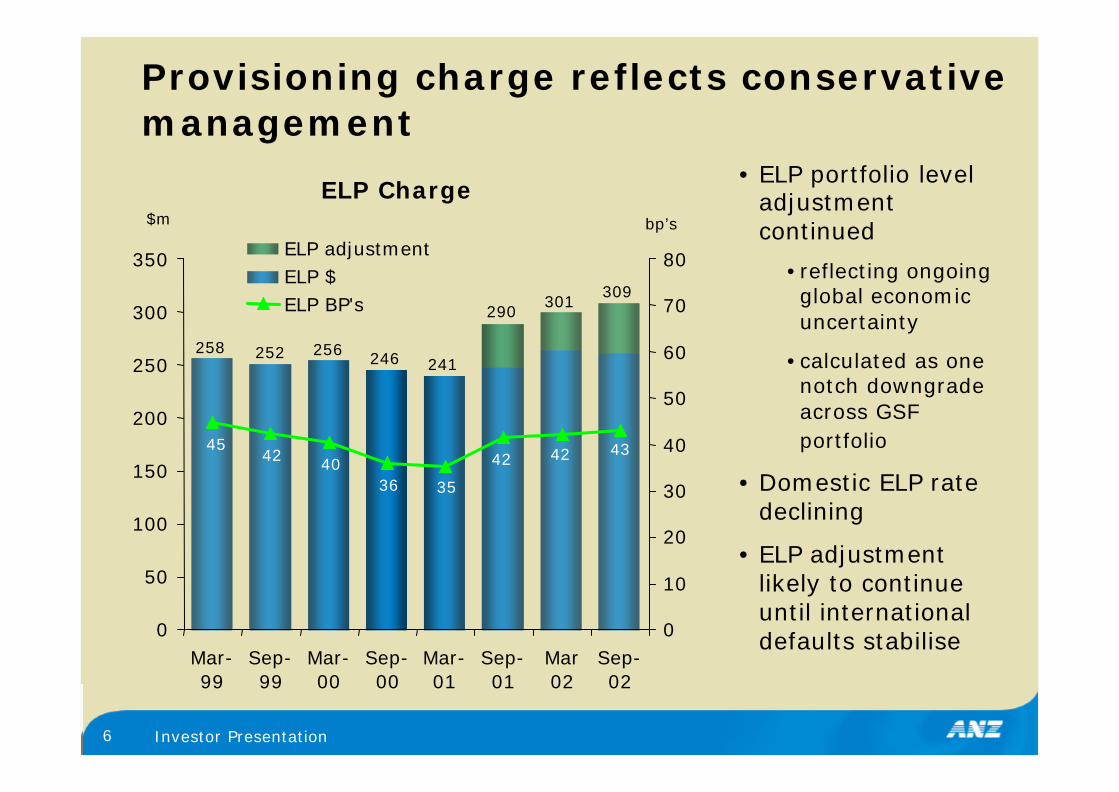

309

241246258 252 256

301290

434242

36 35

4245

40

0

50

100

150

200

250

300

350

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar02

Sep-02

0

10

20

30

40

50

60

70

80ELP adjustmentELP $ELP BP's

Provisioning charge reflects conservative management

ELP Charge$m bp’s

• ELP portfolio level adjustment continued

•reflecting ongoing global economic uncertainty

•calculated as one notch downgrade across GSF portfolio

• Domestic ELP rate declining

• ELP adjustment likely to continue until international defaults stabilise

7 Investor Presentation

Consumer portfolio continues to improve

Arrears > 60 days%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Mar

-01

Jun-0

1Sep

-01

Oct

-01

Nov-

01D

ec-0

1Ja

n-0

2Fe

b-0

2M

ar-0

2Apr-

02

May

-02

Jun-0

2Ju

l-02

Aug-0

2Sep

-02

Small Business

Mortgages

Cards & Personal Loans

Personal & SME Businesses - Overall (exclAsset Finance, Pacific, Asia)

• Consumer sector in good shape, with continuing low levels of unemployment

• Mortgage arrears at record lows – unlikely to be sustainable

• Ongoing focus on collections management

• Scorecards remain “tight”

8 Investor Presentation

Mortgage outlook – slight deterioration

0.000.100.200.300.400.500.600.700.80

Jan-01

May-01

Sep-01

Jan-02

May-02

Sep-02

Home LoanRes Inv Loan

60 day arrears improving%

• ANZ has not allowed FHOG to be the source of minimum equity requirement

• Behavioural scores remain stable

• Scorecards tightened in 2001, resulting in higher quality borrowers

• Unemployment, a key driver of default, continues to trend downwards

• Scenario analysis at 95% confidence suggests loss not exceeding 4-6 bpover next 12 months, compared with ELP of 5 bp

• Based on uncommitted monthly income at time of application, 100% of customers could meet a 1% rise in interest rates, and 97.2% could meet a 2% increase without rearranging affairs

-20

-10

0

10

20

30

40

50

60

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

SydneyMelbourne

% change House prices well below previous peaks

9 Investor Presentation

4.3% 4.3% 3.1%

11.1% 11.1% 10.6%

22.9% 23.0% 22.3%

26.8% 28.8%26.3%

37.7%32.8%34.9%

Sep-01 Mar-02 Sep-02

Domestic corporates in good shape, some concerns in ANZIB offshore

>BB- = B+ B, B-, CCC & non-accrual

AAA to BBB+

BBB to BBB-

BB+ to BB

BB-> BB-

$40.8bn $38.7bn

C&IB, Asia & GTS Risk Grade Profile*

B+ to CCC 3.0% 3.2% 2.4% 4.5% 2.7% 4.1%

Non-accrual 1.3% 1.1% 0.7% 1.9% 4.1% 4.6%

$39.4bn

* Risk grade profile by outstandings

6.4% 6.8% 8.7%3.4% 2.5%

3.8%

12.9% 15.3% 13.2%

30.0%33.3% 29.9%

44.4%42.1%47.3%

Sep-01 Mar-02 Sep-02

$15.9bn $15.0bn $14.2bn

ANZIB Risk Grade Profile*

10 Investor Presentation

869

5950

623651 681

388

80

792

523

37

643

0

200

400

600

800

1000

1999

2000

2001

2002

1543

1391

12601203

1662

628

770699

657

900

0

300

600

900

1200

1500

1800

1998 1999 2000 2001 20020.0%

0.5%

1.0%

1.5%

Non-accrual loans have decreased due to domestic reductions

Gross Non-Accrual Loans (LHS)

Net Non-Accrual Loans (LHS)

$m

Non-Accrual Loans/ Loans & advances (RHS)

Historic

Aust InterNZ

GeographicGross Non-Accrual Loans

$m9%78%

% of total lending assets13%

11 Investor Presentation

Overall - provisioning levels strong

0.96

0.88

1.051.06

0.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

ANZSep 02

CBAJun 02

NABMar 02

WBCMar 02

GP/RWA’s%

0

20

40

60

80

100

120

140

160

180

200

ANZ

Austr

alia

Cana

da

Germ

any

France UK

%Provisions/Non Accrual Loans

Source: CSFB

12 Investor Presentation

Outline

• Result review– Overview– Revenue/Costs– Credit Quality

• Delivering for all stakeholders

• Strategy

• Outlook

13 Investor Presentation

Delivering on our commitments to shareholders

• Specialised business units performing well– 14 of 16 recorded higher profits year on year

• Specific provision unusually high, but cumulative specifics well covered by cumulative ELP from inception in 1997

• Major new governance and transparency initiatives– Substantially enhanced disclosure on capitalised

expenses, asset quality, options expense, compensation

– Upgraded audit policy introduced– Recognition for disclosure and transparency– Remuneration practices substantially reformed

14 Investor Presentation

Delivering for staff, and increasingly a preferred employer

62

4046

78

6571

0

10

20

30

40

50

60

70

80

90

Satisfaction ANZ Regard ANZ Values

2001 2002

0

2000

4000

6000

8000

10000

12000

2001 2002

Graduate Applications

225 positions

Staff satisfaction up Strong employment brand%

15 Investor Presentation

New customer initiatives getting real traction

32

85

127

96

159181

020406080

100120140160180200

Opene

d

Clos

ed Net

Opene

d

Clos

ed Net

2001 – prior corresponding

period

2002 – 30 weeks since

launch

Net new account openings up 165%*000’s

Indicators

Revenue growth 5.1% 4.0%

Staff advocacy 65% 62%

Customer satisfaction 6.8 6.6

FUM growth 8.0% 6.2%

Vic Other States

2H 2002

Key indicators show Restoring Customer Faith program is

beginning to deliver

165%

* Victoria RCF pilot

16 Investor Presentation

Current performance issues addressed

Offshore credit losses• Reductions in credit limits• Re-focus strategically

Consumer Finance 2nd half• Management reorganisation• Restructure programs

Technology project benefits • Wind down of major projects• Appointed MD major programs

JV performance below plan • Accelerate integration• Capital return hedged

NZ consumer satisfaction • Greater local autonomy and resourcing• Roll out Restoring Customer Faith

Issue Response

17 Investor Presentation

Clear strategic investment priorities

Asia/Pacific

Global Businesses

Domestic Businesses

Options

Refocus

Invest in options for longer term

Lower risk orientation Eliminate concentrations

Invest for growth and positionGrow

18 Investor Presentation

Opportunities for growth

Personal Banking• Full rollout Restoring Customer Faith• Expand network in growth locations

• Autonomous customer organisation• Rollout Restoring Customer Faith

Wealth Management • Maintain high investment spending• Lower profit volatility from JV

Institutional & ANZIB • Leverage leading relationship position• Leverage business integration synergies

Corporate & SME• Investment spending budgeted• Leverage business integration synergies

Opportunity Approach

New Zealand

19 Investor Presentation

Key priorities for 2003

• Rollout Restoring Customer Faith, reconnect with community

• Complete JV integration. Leverage distribution opportunity

• Reposition cards and mortgages for tougher environments

• Narrow focus of offshore activities to reduce risk

• Capture share of cyclical upswing in corporate lending and SME

• Implement three major strategic cost programs, fewer projects

• Accelerate shift in performance culture and identify and develop the next generation of leaders

20 Investor Presentation

2003 targets stretching but unchanged

EPS growth

ROE

Cost-income ratio

ACE Ratio

Credit rating

2003 Target

10%

20%

45%

5.25% - 5.75%

AA-

2001

10%

20.2%

48.0%

5.9%

AA-

2002*

17%

21.6%

46.0%

5.7%

AA-

*excluding significant transactions

21 Investor Presentation

Summary – delivering on our commitments

• Exceeded targets in a difficult year

• Specialisation strategy working

• Becoming employer of choice

• Increasingly delivering for customers and the community

• Risks being addressed

• Moving from “perform” to “perform and grow”

2003 target 10% EPS growth

Copy of presentation available on

www.anz.com

23 Investor Presentation

The material in this presentation is general background information about the Bank’s activities current at the date of the presentation. It is information given in summary form and does not purport to be complete. It is not intended to be relied upon as

advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. These

should be considered, with or without professional advice when deciding if an investment is appropriate.

For further information visit

www.anz.comor contact

Philip GentryHead of Investor Relations

ph: (613) 9273 4185 fax: (613) 9273 4091 e-mail: [email protected]

Supplementary Information PackAustralia and New Zealand Banking Group Limited

November 2002

25 Investor Presentation

Additional information on strategy

26 Investor Presentation

Our growth philosophy unchanged – but primary focus on organic out-performance

Organic out-performance

Portfolioreshaping

Transformationalmoves

• Extend specialisation• Grow customer

numbers• Increase share of

wallet• Drive productivity

• Revenue growth materially higher than expense growth

• Take business units to sustainable leadership positions

• Build a range of strategic options

Our targets

• Invest in high growth areas• Build specialist capabilities• Exit weak positions• Risk reduction

• Step changes in positioning• Creating new growth options• Proactively shaping industry

27 Investor Presentation

0

10

20

30

40

50

ANZ CBA NAB WBC

Consumer portfolio – significant opportunity for ANZ in domestic markets

Share of Customers*

Wallet Share*

Priorities

• Deliver on promise of Restoring Customer Faith

• Improve community perceptions

• Deliver on JV

• Continue product innovation

• Utilise CRM capabilities

• Target market share growth of 1% pa in key markets

0

10

20

30

40

50

60

ANZ CBA NAB WBC

%

%

* source: Roy Morgan Research

28 Investor Presentation

-10

-5

0

5

10

15

1990

1992

1994

1996

1998

2000

2002

2004

2006

Corporate portfolio – positioned for upturn, targeting fee income

System Business Credit Growth*

5765

4335

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Today 2005Aspiration

Non-Interest Interest

Corporate Portfolio Revenue Mix

• Capture expected stronger lending growth from SMB and middle market corporates

• Focus on fee income in institutional business

%

* Forecasts – economics@anz

29 Investor Presentation

C&IB successfully managing the transition to lower balance sheet intensity

331

510

377

642

0

100

200

300

400

500

600

700

NPAT NIACC

2001 2002

14%

26%

0

50

100

150

200

250

1999 2000 2001 20020

5

10

15

20

25

30

35

40

45

50

Lending Fees Balance Sheet

Higher lending fees, flat balance sheet

NIACC growth greater than profit growth

30 Investor Presentation

Asia/Pacific – create low risk growth options

• East Asia and the Pacific are our priorities

• Focus on modest, low risk options in the Asian consumer sector

• Leverage Panin experience and our core capabilities

• Strengthen position in the Pacific

PacificEast Asia

31 Investor Presentation

We will continue to shift the portfolio towards more attractive segments

Weak Strong

Low

High

Mark

et

Att

ract

iven

ess

Current ANZ Position

Wealth

Cards

ConsumerBanking

SmallBus

ANZIBCorporate

AssetFinance

Mortgages

15 - 20%

35 - 45%25 - 35%

5 - 10%

Source of profit - today

< 10%

5 - 10%

Source of profit ~2005

~80%

ANZPosition

High

LowWeak Strong

Mar

ket

Att

ract

iven

ess

32 Investor Presentation

Executive options will only reward out-performance against market

Year 1 Year 2 Year 3 Year 4 Year 7 etc…

S&P200BAIANZ Share Price

Executives rewarded for value premium after allowing for market growth

ANZ share option indexed by movement in the S&PAB200I (The value below this line is passed to executives under a conventional option)

Each 1/2 year the options will be issued at the prevailing weighted average five day price

Standard TSR Option strike price

Price

33 Investor Presentation

Additional information on 2002 results

34 Investor Presentation

2.35

1.61

1.15

3.20

2.79

2.25

1.21

1.16

2.843.06

3.93

2.83

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

Corp Bkg Bus ANZIBMortgages Asset FinPersonal Group

Interest margins stable, lending and deposit volumes up

%Interest Margins

92.8

53.9

83.0

46.0

57.2

88.6

45.3

61.6

43.6

20

30

40

50

60

70

80

90

100

Mortgages Business Deposits

Sep-01 Mar-02 Sep-02

Average Lending & Deposit Volumes

$b

* Business Lending includes Corporate, ANZIB and Small Business Segments

35 Investor Presentation

Healthy underlying income growth

64066375

6814

4172

439

6000

6100

6200

6300

6400

6500

6600

6700

6800

69002001

AN

Z/J

V

Acq

uis

itio

ns

& F

X I

mpact

Adju

sted

reve

nue

bas

e

Under

lyin

ggro

wth

2002

$m

• Mortgage outstandings up $8.9b, partly offset by $2.7b decline in Corporate lending assets

• Deposits up $8b, with an equal increase in both Personal and Corporate

• Margins were flat over the year at 2.77%, although second half slightly higher than first half

• Lending fees up 11%, principally driven by corporate businesses

• Non lending fees up 8%, with strong transaction volumes in consumer finance a major contributor

Income Drivers6.9%

6.3%

36 Investor Presentation

1000

1200

1400

1600

1800

2000

2200Sep

-97

Mar

-98

Sep

-98

Mar

-99

Sep

-99

Mar

-00

Sep

-00

Mar

-01

Sep

-01

Mar

-02

Sep

-02

40

45

50

55

60

65

70

ExpensesCost Income RatioPeer Average CTI*

Cost income ratio on track to meet target of 45

$m CTI (%)

45.5

• Peer average impacted by funds management acquisitions

• $31m expense reduction from sold businesses

• Effective half on half cost growth of 1.8%

• We will invest more in growth areas, particularly personal businesses

• 2000 $361m restructuring provision fully utilised, ongoing $60m+ charge likely

* Source: CSFB

37 Investor Presentation

Additional credit quality information

38 Investor Presentation

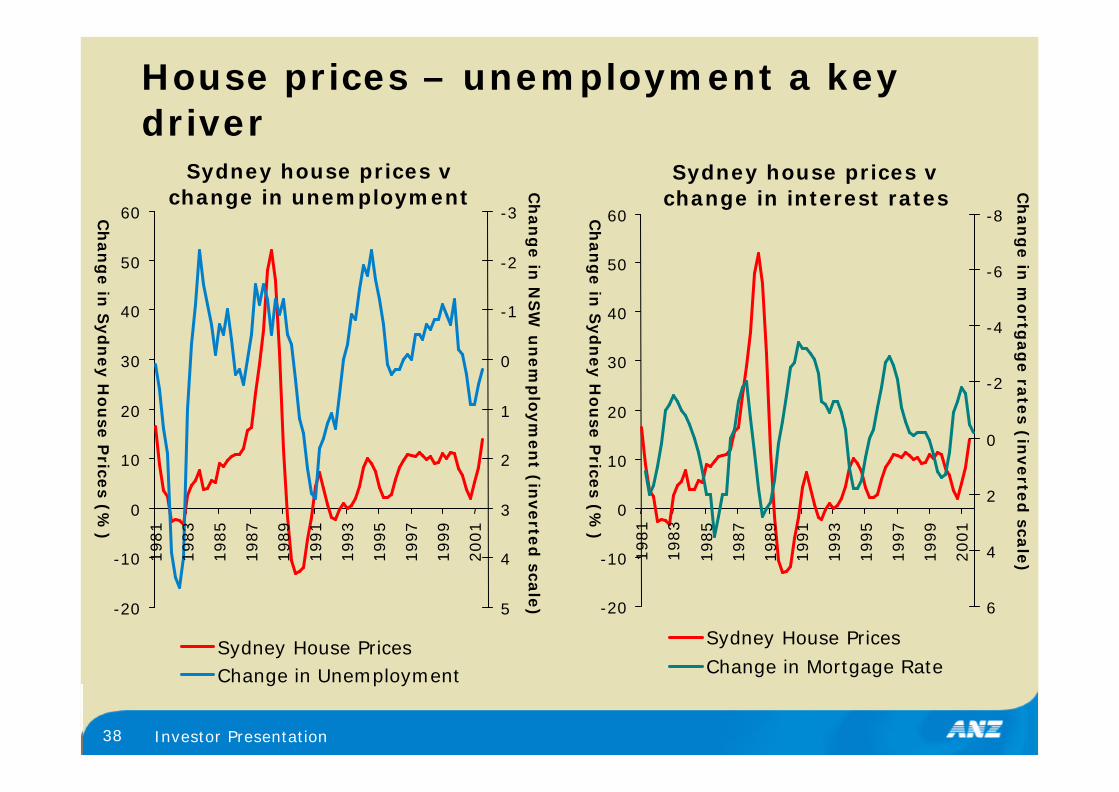

House prices – unemployment a key driver

-20

-10

0

10

20

30

40

50

60

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

-3

-2

-1

0

1

2

3

4

5

Sydney House PricesChange in Unemployment

-20

-10

0

10

20

30

40

50

60

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

-8

-6

-4

-2

0

2

4

6

Sydney House Prices

Change in Mortgage Rate

Sydney house prices v change in unemployment

Sydney house prices v change in interest rates

Ch

an

ge in

Syd

ney H

ou

se P

rices (%

)

Ch

an

ge in

Syd

ney H

ou

se P

rices (%

)

Ch

an

ge in

NS

W u

nem

plo

ym

en

t (inverte

d sca

le)

Ch

an

ge in

mo

rtgag

e ra

tes (in

verte

d sca

le)

39 Investor Presentation

4

6

8

10

12

14

16

18

90 92 94 96 98 00 02 044

5

6

7

8

9

10

11

12

90 92 94 96 98 00 02 04

Key drivers of house prices expected to remain benign

Unemployment Mortgage rates% %

Source: economics@anz

40 Investor Presentation

Scenario analysis from ANZ economics

0

2

4

6

8

10

12

14

16

18

20

1996/9

7

1997/9

8

1998/9

9

1999/0

0

2000/0

1

2001/0

2

2002/0

3

2003/0

4

2004/0

5

2005/0

6

Main Case Stronger Case Weaker Case - Domestically Driven Weaker Case - Globally Driven

0

2

4

6

8

10

12

1996/9

7

1997/9

8

1998/9

9

1999/0

0

2000/0

1

2001/0

2

2002/0

3

2003/0

4

2004/0

5

2005/0

6

Housing credit growth Business credit growth

41 Investor Presentation

Assumptions underlying scenario analysis

Main case• Global economy: moderate rebound in

global economy• Moderate tightening in policy - 50 bps

over the next 12 months• Moderating house price gains (3-5%)• Housing investment falls, consumption

slows, but business investment picks up

Stronger case• Global economy: as per main case• Monetary policy as per main case• Ongoing house price gains (8-12%

growth)• Consumption & business investment

continue to grow firmly• Credit growth strong

Weaker case - domestically driven• Global economy: as per main case• 3x50bp interest rate rises up to Mar

quarter 2003• Negative 3% house prices • Flow through to weaker employment,

business investment and housing construction and turnover which in turn feed through to Credit and deposit volumes

Weaker case – globally driven• Global economy sharply weaker - double

dip US recession• Interest rates cut to 4.00%• Negative 6% house prices (peak to

trough)• Negative employment growth, mild

recession, much weaker business investment which in turn feed through to Credit and deposit volumes

Source: economics@anz

42 Investor Presentation

Fallen Angels phenomenon continues

March 2001 ratings for Full Year 2002 new non accrual loans

• Speed of collapse difficult to model

• We continue to diversify the portfolio

• SCCL’s further reduced and refined

B4%

BB1%

CCC9%

BBB + to BBB-86%

43 Investor Presentation

Specific provisions again impacted by large corporate collapse

0

50

100

150

200

250

300

350

400

Mar-98

Sep-98

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Net specific provisions - $m (LHS)% International SPs (RHS)ELP charge - $m (LHS)

Provisions$m Single

customers2nd half Specific

Provisions by size

• Only 4 customers with specific provisions greater than $10m

< $5m

$5m -$10m

$10m -$20m

$20m -$50m

1customer

1customer

>$100m2

customers

44 Investor Presentation

6.7%0.8%

8.7%

21.2%

62.6%

Sep-02

Global telecommunications portfolio in reasonable shape

50%

12%

35%

3%

Aust/NZ (97.6% Investment Grade)

Americas (69.3% Investment Grade)

UK/Europe (71.1% Investment Grade)

Asia (34.5% Investment Grade)

Exposure by geography

83.8% investment grade

Telco Risk Grade Profile*

4.8% $0.3bNon Accrual

1.9% $0.1bB+ to CCC

$5.5bTotal Limits (AUD)

AAA to BBB+

BBB to BBB-

BB+ to BBBB->BB-

>BB- = B+ B, B-, CCC & non-accrual*Risk grade profile by limits

$3.4b

$1.2b

$0.5b

$0.4b

49

4

3

# of customers

45 Investor Presentation

8%1%

24%

21%

46%

Sep-02

Global energy portfolio – some issues, but containableGlobal Energy Portfolio*

AAA to BBB+

BBB to BBB-

BB+ to BB

BB-

>BB-16%

36%

16%

32%

Sep-02

US Energy Portfolio

>BB- = B+ B, B-, CCC & non-accrual

(AUDm)Total Limits $9.6bn $2.2bnB+ to CCC 4.8% $0.46b 12.2% $0.27bNon Accrual 3.2% $0.3b 4.0% $0.09b

Exposure by geography

53%

25%

9%

9%4%

Aust/NZ (77.5% Inv Grade)

Americas (43.5% Inv Grade)

UK/Europe (64.6% Inv Grade)

Asia (61.0% Inv Grade)

Middle East (98.0% Inv Grade)

$4.5b

$2.0b

$2.3b

$0.8b

*Risk grade profile by limits

$0.7b

$0.36b

$0.8b

$0.36b

7812

5

# of customers

265

2

# of customers

46 Investor Presentation

Offshore SCCLs now in place

60%

100%

Australia/New Zealand OffShore Corporates

Comparative SCCL Customer Limits

25%

75%

100%

80%

> 100%Security

< 100%Security

Lending type SCCL % for offshore Corporates (excl. GSF)

indicative based on BBB- grading

Direct Exposure(Including on and Off Balance sheet)

Indirect or Contingent Exposure

Market Related

Exposures

Capped at AUD 300m

Capped at AUD 100m

GSF Direct Exposures capped at AUD 450m for > 100% Security and AUD 200m for < 100% Security

47 Investor Presentation

Cumulative ELP well above specific provisions

0

500

1000

1500

2000

2500

3000

3500

1997 1998 1999 2000 2001 20020

100

200

300

400

500

600

700

ELP (LHS) SP (LHS)

Cumulative difference (RHS) Cum + $250m top up (RHS)

GP top up$m $m