answers & lucky winner of previous week’s ... mktyard.com weekly commodity market monitor...

TRANSCRIPT

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

HOME

• Cotton • Sugar • Soyben • RM Seed • Castor seed • Turmeric • Jeera

NCoMM

NCML COMMODITY MARKET MONITOR

Cotton | Sugar | Soybean | RM Seed | Castor seed | Turmeric | Jeera

OUTLOOK

OTHER DATA Sowing progress | Advance estimates | Kharif and rabi MSP

ANSWERS & LUCKY WINNER OF PREVIOUS WEEK’S MktYard.com Weekly Commodity Market Monitor

Sugar • Tur • Wheat • Maize • Chana • Paddy/Rice • Guar seed

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

• The Indian sugar industry is currently going through a crisis due to high

domestic production coupled with fall in sugar prices internationally.

• India’s sugar production amounted to a record 31.03 mn tonnes till April 30.

With 130 sugar mills still operating, majorly in Uttar Pradesh, the sugar

production during the current season might end up touching 32 mn tonnes

in the current season (Oct-Sep) as per ISMA. This is a substantial increase

from last year’s 20.3 mn tonnes produced.

• Till April 30, Sugar mills in Maharashtra produced 10.65 mn tonnes and

barring 15 mills all others in the state had ended their operations. UP mills

produced 11.2 mn tonnes of sugar till and 80 out of 119 sugar mills are

continuing their crushing. Some of these mills are closing fast, whereas few

are expected to continue crushing till the second week of May 2018. In

Karnataka, all the sugar mills have stopped their operations and they

produced 3.63 mn tonnes during the current season.

• On May 2, the government today approved a subsidy of Rs 5.5 per quintal to

cane farmers for the produce they sell to sugar mills to help millers clear

cane arrears that have surged to about Rs 20,000 crore due to sharp fall in

ex-mill sugar prices.

• ISMA has said sugar prices have been under severe pressure in the last 4-5

months. Compared to the cost of production, the ex-mill sugar prices are

around Rs 8/kg lower & sugar mills are incurring substantial losses.

• India had abolished a surcharge on sugar, or cess, after the introduction of

the nationwide GST last year, but the central government has proposed

reintroducing 5% sugar cess in view of current glut.

• The government had last month mandated a MIEQ (Minimum Indicative

Export Quota) of 2 mn tonnes sugar exports to move surplus stocks out of

country but India is not able to export sugar due to export disparity as a

result of depressed world sugar prices on global sugar surplus.

• The government had earlier doubled import duty on sugar to 100%, scrapped

the 20% export duty on sugar and placed stockholding limits on sugar mills

but could not counteract the trend of falling prices.

• The world’s sugar traders are experiencing the biggest ever global surplus.

The Green Pool Commodity Specialists expect the glut to reach 18.4 mn

tonnes this season.

• Excess supplies forecast for next season will also be bigger than previously

expected, and that could drive further declines in the price of sugar, which is

trading near the lowest since 2015.

• Sugar mills in Brazil’s Centre/South crushed 22.214 mn tonnes of cane in the

first half of April, up from 17.681 mn in the same period a year ago.

Thailand’s sugar production seen at 14.6 million tons this season, 100,000

tonnes higher than a previous forecast.

Mandi Price in Rs/ Quintal

07-05-2018 30-05-2018

%Change

Kohlapur 2703.35 2713.75 -0.38

Muzzafar -nagar

2702 2716.55 -0.54

Delhi 2757.85 2792 -1.22

2,100

2,400

2,700

3,000

3,300

3,600

3,900

Jan

-14

Jul-1

4

Jan

-15

Jun

-15

De

c-15

Jun

-16

No

v-16

May

-17

No

v-17

Ap

r-18

Sugar - M-grade : Muzaffarnagar

FUNDAMENTAL SUMMARY

Price Drivers Impact

Record domestic sugar production to touch 32 mn tonnes against only 20.3 mn tonnes last year

Bearish

Subsidy of Rs 5.5 per qtl to cane farmers for the produce they sell to sugar mills by the government

Bullish

Proposal for imposition of 5% sugar cess Bullish

Ongoing wedding and summer season demand

Bullish

MIEQ (Minimum Indicative Export Quota) of 2 mn tonnes mandated by government

Bullish

Export disparity due to low global sugar prices

Bearish

Scrapping off the 20% export duty on sugar by the government

Bullish

Doubling of import duty from 50% to 100%

Bullish

Based on Primary & Secondary Sources

Fundamental Report SUGAR

STATE-WISE SUGAR PRODUCTION (LAKH TONNES)

STATE 2014-15 2015-16 2016-17 2017-18*

Uttar Pradesh 71.02 68.41 87.78 115.00

Maharashtra 105.07 84.24 42.38 107.00

Karntaka 49.35 40.49 21.44 36.50

Gujarat 11.54 11.68 8.85 11.00

Punjab 5.37 6.71 6.61 8.25

Andhra Pradesh# 8.86 8.28 5.01 8.00

Harayana 5.76 5.39 6.68 7.25

Bihar 5.26 5.03 5.26 7.00

Tamil Nadu 12.18 13.62 10.62 6.00

Madhya Pradesh 3.86 3.41 3.43 5.50

Uttarakhand 3.24 2.73 3.45 4.50

Others 1.62 1.26 1.11 1.00

All India 283.13 251.25 202.62 317.00 *Projected, #Includes Telangana, Source-Indian Express

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

Fundamental Report TUR

• The notification issued by the Directorate General of Foreign Trade

(DGFT) on May 4 2018 specifically mentions that the ban imposed on

urad and moong dal in August 2017 has been extended.

• The Government had fixed a cap on imports of pulses like tur, urad and

moong up to 3 lakh tonnes in Aug 2017. In the recent notification, the

Government has not only continued the 3 lakh tonne cap for pulses, but

also included the processed dals imported by the traders. Earlier,

processed dals were not included in the allowed quota.

• Although no notification has been received for tur so far, we are

expecting a similar extension for tur too.

• As per the second advance estimates released by the government, tur

production 2017-18 is pegged at 4.02 mn tonnes, down 17.45% from 4.87

mn tonnes in 2016-18. The area under tur this year declined to 43.5 lakh

hectares, from 53.2 lakh hectares last year.

• Despite lower production, Tur prices continue to be in a glut due to

higher supplies and large previous year’s stocks.

• Demand for Tur and Tur dal too has not been not up to the mark,

however the wedding season may lift the demand a bit.

• The Centre has granted extension to the Maharashtra government for

procurement of tur (arhar) under at MSP up to May 15 instead of the

earlier deadline of 18 April. Private buying remains restricted as govt.

agencies remained active to procure at MSP.

• Until April 18, the government procured 25.45 lakh quintals from the key

producing regions of Maharashtra and met nearly 65% of its target

which has been set at 44.67 lakh quintals from February 1. Tur

procurement was stopped in some parts of the state because of lack of

storage space due to previous year’s stock.

• Over 95% of 67.34 lakh quintals of tur procured last year by Maharashtra

government is yet to be processed to make dal out of it, which may lead

to losses to the tune of Rs 1,000 crore.

• The average trading price of tur in most of the markets in the state was

around Rs 4,250/qtl, below the MSP of Rs 5,400/qtl.

• Record purchases of tur by the government agencies in Karnataka,

whichended last month too did not reverse the bearish price trend. In

Gulbarga market Tur is being traded at Rs 3750 to Rs 4350 per qtl.

• Quotes for Myanmar pulses have decreased further diminishing export

possibility in India in the first half of the year despite removal of export

ban on pulses by India. Myanmar is offering Tur at $300 per tonne, basis

Indian port, down by almost $30 per tonne in last two weeks.

• Lower realization from the crop this year is likely to encourage farmers

to shift tur area to other lucrative crops like groundnut, chilli, turmeric &

others. Tur area may decline by 15 to 20% in India in 2018-19.

2500

6500

10500

14500

Jun

-15

Oct

-15

Feb

-16

May

-16

Se

p-1

6

Jan

-17

May

-17

Se

p-1

7

Jan

-18

Ap

r-18

Lemon tur FAQ-Myanmar origin : Mumbai

TUR FUNDAMENTAL SUMMARY

Price Drivers Impact

Huge pile up of previous year’s stocks

Bearish

Restricted private buying Bearish

Expected notification on import restriction

Bullish

Export disparity Bearish

Lower 2017-18 production estimate

Bullish

Government extending procurement in Maharashtra

Bearish

Fall in tur acreage expected in 2018-19

Bullish

Based on Primary & Secondary Sources

Mandi Price in Rs/ Quintal

07-05-2018 30-04-2018 %Change

Yavatmal 3975 3475 14.39

Amravati 3850 3756 2.50

Akola 3910 3725 4.97

• The harvested tur has a shelf life of 6

months to 1 year without being

processed.

• 95% of tur procured before June 2017

by Maharashtra government is lying

unprocessed.

• The state had procured tur at Rs 5,050

/qtl, but today the market value of tur

is not more than Rs 3,200/qtl.

• The total cost of the procurement was

Rs 3,341.32 crore.

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

Fundamental Report WHEAT

• Recent unseasonal rains and hailstorm in many parts of north

India may slow down the wheat procurement as it has wet the

grains lying on the ground. The farmers will now have to wait to

dry the crop before selling it to the government. Moreover,

standing wheat crop, which was late sown is reported damaged

in many parts of Uttar Pradesh.

• According the latest report of Food Corporation of India (FCI), as

on 04th May 2018, wheat procurement has reached 287.78 lakh

metric tonnes. Of the total quantity procured, around 119.37 lakh

tonnes have been procured from Punjab, 8.63 lakh tonnes from

Haryana, 21.83 lakh tonnes from Uttar Pradesh, 52.71 lakh tonnes

have been procured from Madhya Pradesh, 10.39 in Rajasthan,

0.41 lakh tonnes from Uttarakhand, 0.14 lakh tonnes from

Chandigarh and 0.30 lakh tonnes from Gujarat. In Rabi marketing

season 2018-19 government has set procurement target of 32

million MT.

• Buoyed by the forecast of a normal monsoon this year, the

agriculture ministry has targeted 100 million tonnes of wheat

production in 2018-19. In 2017-18 production of wheat is

estimated at 97.11 million tonnes, according to the second

advance estimates released by the ministry in February.

However, most trade sources are currently estimating the crop

in the range of 91-94 million MT for 2017-18.

• According to APEDA, India wheat export is reported at 2.29 lakh

MT for 2017-18 which is 12.59 percent lower than the export of

2.62 lakh MT for 2016-17. Export demand of Indian wheat is lower

due to price disparity with other exporting countries.

• According to latest monthly report of IGC, world wheat

production is projected at 739 million MT for 2018-19 against 758

million tonnes forecast for 2017-18, while the ending stocks are

projected lower at 257 million tonnes against 263 million tonnes

last year.

1500

1700

1900

2100

2300

2500

Mar

-16

Jun

-16

Se

p-1

6

De

c-16

Mar

-17

Jul-1

7

Oct

-17

Jan

-18

Ap

r-18

Wheat: Standard mill quality : Delhi

FUNDAMENTAL SUMMARY

Price Drivers Impact

Slow procurement activities Bearish

Higher production estimate for 2018-19

Bearish

Lower wheat exports Bearish

Lower world wheat production Bullish

Based on Primary & Secondary Sources

Mandi Price in Rs/ Quintal

07-05-2018 30-04-2018 %Change

Delhi 1756.25 1730.8 1.47

Indore 1766.95 1754.7 0.70

Kanpur 1642.5 1647.5 -0.30

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

Fundamental Report CHANA

• The All-India Dal Mills Association has demanded a ban on futures

trading in chana due to falling prices in the domestic market.

According to them, big cartel is running the market causing impractical

price movement which is hampering the interests of small

businessmen and farmers.

• Moreover, All-India Dal Mills Association are also demanding

immediate ban on imports of chana to support the domestic prices. At

present, the import duty on chana is 60 per cent.

• As of 07th May, imported Australian chana is being traded at Rs 3500

per quintal in Mumbai market and Rs 3525 per quintal at Mundra port.

• According to the market participants, export incentive on chana

should be increased to 10-15 percent and 25 lakh MT of chana should

be exported to support the falling prices of Chana. At present the

export incentive to chana is 7 per cent under the Merchandise Export

from India Scheme (MEIS) for a period of three months till June 20,

2018.

• To ease the process of export of chana, DGFT has removed mandatory

roasted chana/ chana dal export in consumer pack of one kg. Now it

can be shipped in bulk.

• According to the latest Nafed report, as on 07th may Nafed had

procured 6.60 Lakh MT of chana. Of the total quantity procured,

around 0.50 lakh tonnes have been procured from Telangana, 1.27 lakh

tonnes from Karnataka, 0.77 lakh tonnes from Andhra Pradesh, 0.48

lakh tonnes have been procured from Maharashtra, 1.42 in Rajasthan

and 2.61 lakh tonnes from Madhya Pradesh and 0.11 in Gujarat.

• According to agmark, all India chana arrivals in the first week of May is

1.68 lakh MT which is higher than the last year arrival s of 0.84 lakh MT

in the same time period last year.

• According to the second advance estimates released by the

government, India’s chana production estimate for 2017-18 is 11.10

million MT which is 18.97 per cent higher than 2016-17 fourth advance

production estimates of 9.33 million MT. Higher production estimate is

due to higher chana sowing acreage and favourable weather condition

in major producing states.

3300

3840

4380

4920

5460

6000

Jul-

17

Se

p-1

7

Oct

-17

De

c-1

7

Jan

-18

Ma

r-1

8

Ma

y-1

8

Gram - Rajasthani desi : Bikaner :

TUR FUNDAMENTAL SUMMARY

Price Drivers Impact

Demand on ban on future trading in chana

Bullish

Import duty Bullish

Export incentive on chana Bullish

Ongoing Chana procurement activity

Bullish

Higher arrivals in the mandi Bearish

Higher production estimate Bearish

Based on Primary & Secondary Sources

Mandi Price in Rs/ Quintal

07-05-2018 30-04-2018 %Change

Akola 3450 3465.65 -0.45

Bikaner 3550 3463.2 2.51

Amravati 3250 3200 1.56

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

Fundamental Report MAIZE

Mandi Price in Rs/ Quintal

07-05-2018 30-04-2018 %Change

Erode 1375 1365.45 0.70

Gulab bagh 1166.9 1203.9 -3.07

Nizamabad 1240 1260 -1.59

FUNDAMENTAL SUMMARY

Price Drivers Impact

Higher Production estimates Bearish

Higher arrivals Bearish

Higher rabi area estimates Bearish

Lower world corn stocks for

the previous year (2017-18) Bullish

Expected Imports coming in Bearish

Based on Primary & Secondary Sources

• As per the second advance estimates released by the government,

the kharif maize output for 2017-18 has been projected at 19.51

million tonnes, higher than 19.24 million tonnes in the previous

2016-17 season. Rabi production was at 7.63 million tonnes.

• The total kharif and rabi production is pegged at 27.14 milllion

tonnes higher by 5% compared to 25.9 million tonnes last year.

• Arrivals for the month of April 2018 was 331821.84 MT an increase

of about 4% compared to the same period last year at 318612 MT.

• Arrivals for the summer crop in Bihar are in full swing now with

arrivals ranging at around 8000-10000. Due to this the prices in

that region have also nosedived by around 10% in this region.

• According to IGC the forecast for world corn prod in 2018/19 was

raised to 1.054 Bn Tonnes citing improved prospects in china & EU

and the consumption was also raised to 1.099 Bn Tonnes from

1.094 tonnes in the previous forecast in March.

• IGC also cut the closing stocks at the end of 2018-19 reflecting the

idea of buoyant consumption which may help the prices in the

future.

• According to UK Agro consult, Ukraine’s export of maize for the

2017/18 Marketing year (July-June) stands at 14.3 Million tonnes till

the end of April.

• As of 29th April, According to US progress Planting reports 17%

Corn has been planted down by 15% compared to last year and

down by 10% compared to the 5 year average.

1100

1250

1400

1550

1700

Ap

r-16

Jun

-16

Se

p-1

6

De

c-16

Mar

-17

May

-17

Au

g-1

7

No

v-17

Feb

-18

May

-18

Maize-Feed/Industrial Grade : Gulab Bagh

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

Fundamental Report RICE/PADDY

• According to the latest available data as on 26th April, Rice

procurement by FCI and its state agencies stood at 321.62 lakh tonnes

as compared to 336.09 lakh tonnes last year same period. The target

procurement in 2017-18 (Oct-Sept) is 430 lakh tonnes.

• Punjab showed an increase of 118.33 lakh tonnes over last year 110.52

lakh tonnes, Haryana Rice procurement was 39.67 lakh tonnes

compared to 35.70 lakh tonnes and in Andhra Pradesh procurement

stood at 30.15 lakh tonnes as against 29.59 lakh tonnes last year.

• Chhattisgarh procured around 32.07 lakh tonnes. Madhya Pradesh and Odisha procurement has reached 10.96 and 25.16 lakh tonnes respectively. Procurement in West Bengal and other rice growing states is still underway and reached to 0.35 lakh tons.

• Rice procurement declined in states like Chhattisgarh, Bihar, Madhya

Pradesh, Maharashtra, Odisha and West Bengal over last year.

• Rice stock at the central pool as on 01st April 2018 stood at 248.73 lakh

tonnes as against 230.81 lakh tonnes last year same period.

• As per the Second Advance Estimates for 2017-18 the total Rice

production for 2017-18 estimated to increase at 111.01 million tonnes as

against 109.70 million tonnes. Kharif Rice output estimated at 96.48

million tonnes as against 96.30 million tonnes in 2016-17. Rabi season

Rice production for 2017-18 is estimated at 14.53 million tonnes as

compared to 13.40 million tonnes in 2016-17.

• The IGC forecasted Rice production in 2018-19 at 493 million tonnes, up

from 492 million tonnes in March and up from 486 million tonnes in

2017-18. Rice consumption also is forecast higher, at 493 million

tonnes, which compares with 491 million tonnes in March and 487

million tonnes in 2017-18.

• As per trade sources, total rice export in the month of March was 13.03

lakh tonnes, in which basmati rice contribution is 33.05 per cent of

total with quantity of 4.30 lakh tonnes and non-basmati contribution

was 66.94 per cent with quantity of 8.72 lakh tonnes.

• Iran would continue to import Rice until 22nd July and there will be no

changes in the customs tariffs on the imports of the product due to

current water crisis in the country. Iran normally allows imports of rice

in late September when the local farmers have concluded cultivating

the cereal grain and again limits the imports in late July.

Mandi Price in Rs/ Quintal

07-05-2018 27-04-2018 %Change

Hanumangarh (1121 Pusa)

3300 3300 0.00

Muzaffarnagar(common)

2700 2665 1.31

Aligarh (1121) 3000 3200 -6.25

1600

2000

2400

2800

3200

3600

Jul-1

5

Se

p-1

5

No

v-15

Jan

-16

Mar

-16

May

-16

Jul-1

6

Se

p-1

6

No

v-16

Jan

-17

Mar

-17

Ap

r-17

Jun

-17

Au

g-1

7

Oct

-17

De

c-17

Feb

-18

Ap

r-18

Paddy - 1121 pusa : Hanumangarh

RICE/PADDY FUNDAMENTAL SUMMARY

Price Drivers Impact

Government procurement of Rice

Bullish

Higher stocks position at central pool

Bearish

Lower procurement in Chhattisgarh, Bihar, Madhya Pradesh and West Bengal

Bullish

Record rice production in 2017-18

Bearish

Iran to import rice till 22nd July

Bullish

Based on Primary & Secondary Sources

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

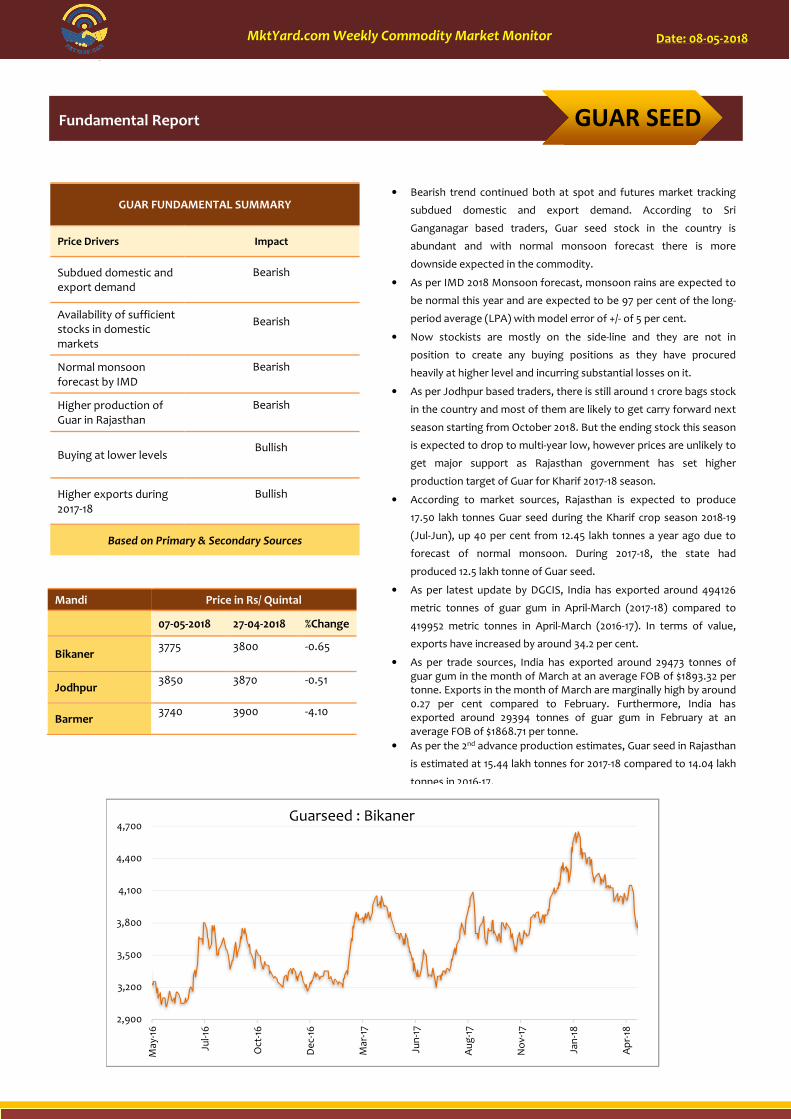

Fundamental Report GUAR SEED

2,900

3,200

3,500

3,800

4,100

4,400

4,700

May

-16

Jul-1

6

Oct

-16

De

c-16

Mar

-17

Jun

-17

Au

g-1

7

No

v-17

Jan

-18

Ap

r-18

Guarseed : Bikaner

GUAR FUNDAMENTAL SUMMARY

Price Drivers Impact

Subdued domestic and export demand

Bearish

Availability of sufficient stocks in domestic markets

Bearish

Normal monsoon forecast by IMD

Bearish

Higher production of Guar in Rajasthan

Bearish

Buying at lower levels Bullish

Higher exports during 2017-18

Bullish

Based on Primary & Secondary Sources

Mandi Price in Rs/ Quintal

07-05-2018 27-04-2018 %Change

Bikaner 3775 3800 -0.65

Jodhpur 3850 3870 -0.51

Barmer 3740 3900 -4.10

• Bearish trend continued both at spot and futures market tracking

subdued domestic and export demand. According to Sri

Ganganagar based traders, Guar seed stock in the country is

abundant and with normal monsoon forecast there is more

downside expected in the commodity.

• As per IMD 2018 Monsoon forecast, monsoon rains are expected to

be normal this year and are expected to be 97 per cent of the long-

period average (LPA) with model error of +/- of 5 per cent.

• Now stockists are mostly on the side-line and they are not in

position to create any buying positions as they have procured

heavily at higher level and incurring substantial losses on it.

• As per Jodhpur based traders, there is still around 1 crore bags stock

in the country and most of them are likely to get carry forward next

season starting from October 2018. But the ending stock this season

is expected to drop to multi-year low, however prices are unlikely to

get major support as Rajasthan government has set higher

production target of Guar for Kharif 2017-18 season.

• According to market sources, Rajasthan is expected to produce

17.50 lakh tonnes Guar seed during the Kharif crop season 2018-19

(Jul-Jun), up 40 per cent from 12.45 lakh tonnes a year ago due to

forecast of normal monsoon. During 2017-18, the state had

produced 12.5 lakh tonne of Guar seed.

• As per latest update by DGCIS, India has exported around 494126

metric tonnes of guar gum in April-March (2017-18) compared to

419952 metric tonnes in April-March (2016-17). In terms of value,

exports have increased by around 34.2 per cent.

• As per trade sources, India has exported around 29473 tonnes of guar gum in the month of March at an average FOB of $1893.32 per tonne. Exports in the month of March are marginally high by around 0.27 per cent compared to February. Furthermore, India has exported around 29394 tonnes of guar gum in February at an average FOB of $1868.71 per tonne.

• As per the 2nd advance production estimates, Guar seed in Rajasthan

is estimated at 15.44 lakh tonnes for 2017-18 compared to 14.04 lakh

tonnes in 2016-17.

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

� FCI rice stock hits 5-year high at

25 million tonnes

� More restriction on urad, moong imports

� Dust storm devastates vegetable crops, harvested wheat

� Despite less rains, maximum kharif crop production last year: Devendra Fadnavis

� Seed shortage may not impact

soyabean area

� Rapeseed powers oilmeal export earnings in 2017-18; growth up 48%

� Sugar output hits a high at 31mt; ISMA says may rise further

� Subsidy of Rs 5.5 per quintal for sugarcane farmers approved

To purchase the India Commodity

Year Book 2018, contact us at

Official Production Estimates

Second advance estimates 2017-18 &

previous years’ estimates : Second

Advance Estimates 2017-18

MINIMUM SUPPORT PRICE (Rs/Qtl.)

Commodity 2016-17 2017-18

KHARIF

Paddy Common 1470 1550

paddy grade A 1510 1590

Jowar Hybrid 1625 1700

Jowar Maldandi 1650 1725

Bajra 1330 1425

Ragi 1725 1900

Maize 1365 1425

Tur 5050 5450*

Moong 5225 5575*

Urad 5000 5400*

Groundnut 4220 4450*

Sunflower seed 3950 4100 #

Soyabean black 2775 3050

Sesamum 5000 5300 #

Nigerseed 3825 4050 #

Cotton(Medium Staple) 3680 4020

Cotton(Long Staple) 4160 4320

RABI

Commodity 2016-17 2017-18

Wheat 1625 1735

Barley 1325 1410

Gram 4000* 4400

Masur (Lentil) 3950* 4250

Rapeseed/Mustard 3700* 4000

Safflower 3700* 4100

Wheat 1625 1735

*includes bonus of Rs 200 per quintal

# includes bonus of Rs 100 per quintal

Commodity Latest Fortnight

ago

Month ago Year ago

07-May-18 23-Apr-18 09-Apr-18 08-May-17

Wheat 1766.95 1723.45 1687.5 1590.5

Chana 3550 3578.95 3736.9 5300

Rice/Paddy 3300 3300 3400 3100

Guar 3775 4150 4040 3700

Sugar 2702 2703.35 2950 3920.15

Tur 3910 4000 4200 3800

Maize 1240 1255 1240 1524

PRICE TRACKER

Link for commodity-wise and

market-wise prices and arrivals:

http://agmarknet.gov.in/PriceAndArriv

als/CommodityWiseDailyReport2.aspx

THE WEEK THAT WAS

0

Date: 08-05-2018 MktYard.com Weekly Commodity Market Monitor

Disclaimer:

This consultancy report has been prepared by National Collateral Management Services Limited (NCML) for the sole benefit of the

addressee. Neither the report nor any part of the report shall be provided to third parties without the written consent of NCML. Any

third party in possession of the report may not rely on its conclusions without the written consent of NCML. NCML has exercised

reasonable care and skill in preparation of this consultancy report but has not independently verified information provided by others.

No other warranty, express or implied, is made in relation to this report. Therefore, NCML assumes no liability for any loss resulting

from errors, omissions or misrepresentations made by others. Any recommendations, opinions and findings stated in this report are

based on circumstances and facts as they existed at the time of preparation of this report. Any change in circumstances and facts on

which this report is based may adversely affect any recommendations, opinions or findings contained in this report.

© National Collateral Management Services Limited (NCML) 2017