annual summary 2013 - rabo vastgoedgroep · pdf fileexecutive board also put an end to his...

TRANSCRIPT

Annual Summary 2013

Annual Summary 2013

2 Preface by the Board of Directors

4 Rabo Real Estate Group in 2013

4 Highlights

4 Management and supervision as at 31 December 2013

5 Organisational chart

6 Key figures

7 Key figures CSR (the Netherlands)

9 Rabobank Group profile

10 Report of the Board of Directors

10 Rabo Real Estate Group in 2013

11 Activities

12 Business policy

18 Cooperation with Rabobank Group

20 Market developments 2013

23 Financial results

24 Personnel

25 Outlook

26 Rabo Real Estate Group in 2014

27 Consolidated statement of income

28 Consolidated statement of financial position

29 Consolidated statement of cash flows

31 Contact details

Table of contents

2 Rabo Real Estate Group Annual Summary 2013

Preface by the Board of Directors

During 2013, it became clear to us that the year would be an

all-time financial low in the history of Rabo Real Estate Group.

Although the Dutch economy carefully steered out of the

crisis, a vigorous rebound was not to be expected. Investments

were low, unemployment rates rose and consumer spending

lagged. The conditions for real estate markets remained

equally poor. The decline in construction output continued,

for both residential and commercial property, and property

prices were down again. Downward revaluations of land,

revaluations of land development and provisions for credit

losses translated into a considerable negative result. Never-

theless, we are pleased with the underlying operating profit.

Current developments and prospects in the commercial

property sector fuelled a harsh and painful decision in 2013

to phase out MAB Development. Another factor was that,

in developing commercial real estate, we also directly face

social and technological developments like the new world

of work and the new way of shopping. Both trends affect the

demand for space. We assume that this is a new reality and,

as a result, see no future for the MAB Development division.

This was obviously a heavy blow for the employees, who

had devoted many years to give their all to the organisation.

A large part of the MAB Development staff left the company

in July 2013. Isaäc Kalisvaart, CEO of MAB Development and

member of the Board of Directors, resigned. We respect his

decision to cease his involvement in MAB Development and

leave the company.

Sipko Schat’s departure from the Rabobank Nederland

Executive Board also put an end to his position on the

Supervisory Board of Rabo Real Estate Group. We

especially valued his knowledge and experience in

national and international finance and in particular

the relationship with Rabobank as our shareholder.

In April 2014, Jaap Blokhuis resigned from the

Supervisory Board because of his new position. We

greatly appreciate their efforts and commitment.

The undersigned, Chief Financial & Risk Officer until

the spring, was appointed the new Chairman of

Rabo Real Estate Group. Until that time, Peter Keur

acted as Chairman of the Board of Directors of

Rabo Real Estate Group. Our new Chief Financial &

Risk Officer, Carolina Wielinga, joined the Board in

the autumn. She has extensive knowledge and

experience in Finance and her arrival has helped the

Board of Directors to operate at full strength again.

The adverse market conditions, the phase-out of

MAB Development and the Board changes in 2013

resulted in a turbulent year for Rabo Real Estate Group

once again. However, we were successful, too. We

have a reasonable and even excellent year behind us

in France and Germany, respectively. Looking back,

our choice to concentrate our foreign operations in

3

these countries was a good decision. France is presently not

thriving, either, but it is outperforming the Netherlands in

respect of the residential market, which is relevant for us.

Germany continues its positive economic performance, of

which we reap the benefits.

Bouwfonds Investment Management – formerly

Bouwfonds REIM – closed the year with a profit. The division

was successful, for example, with its funds in apartment

buildings and car parks and introduced a new fund that

invests in student accommodation in the main European

university cities.

FGH Bank retained its strong position in the property finance

market and saw its loan portfolio grow slightly on the back

of its acquisition of part of Friesland Bank’s loan portfolio.

Bouwfonds Property Development and MAB Development

worked on outstanding projects like Oostpoort in Amsterdam

and De Rotterdam in Rotterdam.

Positive aspects of our company are its resilience and our

employees’ passion, drive and commitment. Despite

unfavourable economic conditions and the fact that we, as

Board of Directors, sometimes take far-reaching decisions,

they continued to put in all their efforts. We would like to

thank them for this. It is also nice to see that employee

satisfaction was once again at a high level in 2013.

Rabobank’s strong financial position is also of major

importance to us, as our shareholder strengthened our

capital position by € 450 million. The fact that we are a

Rabobank Group subsidiary also creates opportunities.

As Rabobank Group’s centre of real estate expertise, we are

increasingly able to link up with other Group business units,

in particular in the area of property finance, property advice

and property development.

As stated, the Dutch economy showed signs of a fragile

recovery in late 2013. We expect this trend to continue in

2014. Even though consumer and company confidence

is still low, we also expect a further lifting of sentiment.

Economic growth is expected to remain moderate and

unemployment levels will increase slightly. The housing

market in the Netherlands seems to be stabilising. The

number of transactions is on the rise and first-time buyers

have regained confidence, allowing the housing market

circulation to gain momentum. The Dutch housing market

does not have a large number of vacancies; some parts of

the country even experience a structural shortage of homes.

The office market displays more imbalance, which is of a

structural nature. Some retail market segments, too, face

signs of vacancies. Differences in these markets have grown

considerably as a result, which is an explicit area of attention

for investors. The developments expected in France for 2014

are uncertain, whereas Germany will ‘just’ keep growing.

In 2014, too, we will energetically keep up the good work at

Rabo Real Estate Group. Opportunities can always be found,

especially in the collaboration with Rabobank Group. We will

look for these opportunities or create them ourselves. The

economic recovery is a gradual process. We are confronted

with regulatory parties exerting increasing pressure on

banks. 2014 is likely to become another challenging year

for our Group; being a real estate company, market

developments affect us for quite some time. We have every

confidence that 2014 will yield improved results thanks to

our resilience, passion, drive and collective real estate

expertise.

Hoevelaken, 20 May 2014

On behalf of the Board of Directors

Jos van LangeChairman Rabo Real Estate Group

4 Rabo Real Estate Group Annual Summary 2013

Rabo Real Estate Groupin 2013

Highlights

Net profit excluding non-controlling interests -/- € 858 million

Return on equity -/- 71.7%

Number of homes sold in the Netherlands and abroad 5,169

Commercial real estate production € 174 million

Loan portfolio size at FGH Bank € 19.4 billion

Assets under management at Bouwfonds Investment Management € 5.9 billion

Board of Directors

J.H.P.M. van Lange (Jos), Chairman

P.C. Keur (Peter), FGH Bank, Vice Chairman

W.P. de Boer (Walter), Bouwfonds Property Development

J.C.M.A. Gillis (Jaap), Bouwfonds Investment Management

C. Wielinga (Carolina), Chief Financial & Risk Officer

Supervisory Board

L.C. Brinkman, Chairman

J.G. Blokhuis, until 4 April 2014

L.M.J. van Halderen

Management and supervision as at 31 December 2013

5

Organisational chart

Development Residential

Development Commercial Property Finance Investment Management Public Fund

Management

S T A F F F U N C T I O N S

6 Rabo Real Estate Group Annual Summary 2013

Result 2013 2012Net profit excluding non-controlling interests € million (858) (113)

Financial positionShareholder’s equity € million 803 1,591

Group capital € million 810 1,607

RatiosReturn on shareholder’s equity % (71.1) (6.9)

Tier 1 ratio % 4.7 8.9

BIS ratio % 4.7 8.9

RAROC % (47.9) (7.2)

ProductionHomes sold (including third-party projects) number 5,169 6,312

Commercial real estate production € million 174 218

Portfolio (gross)Loans € million 19,350 19,204

Assets under management € million 5,867 5,528

Sustainable social assets under management € million 3,010 2,945

Development portfolioResidential number 72,000 87,000

PersonnelFTEs number 1,681 1,622

– The Netherlands 1,128 1,086

– Other countries 553 536

Total number of employees number 1,824 1,769

– The Netherlands 1,239 1,205

– Other countries 585 564

Key figures

7

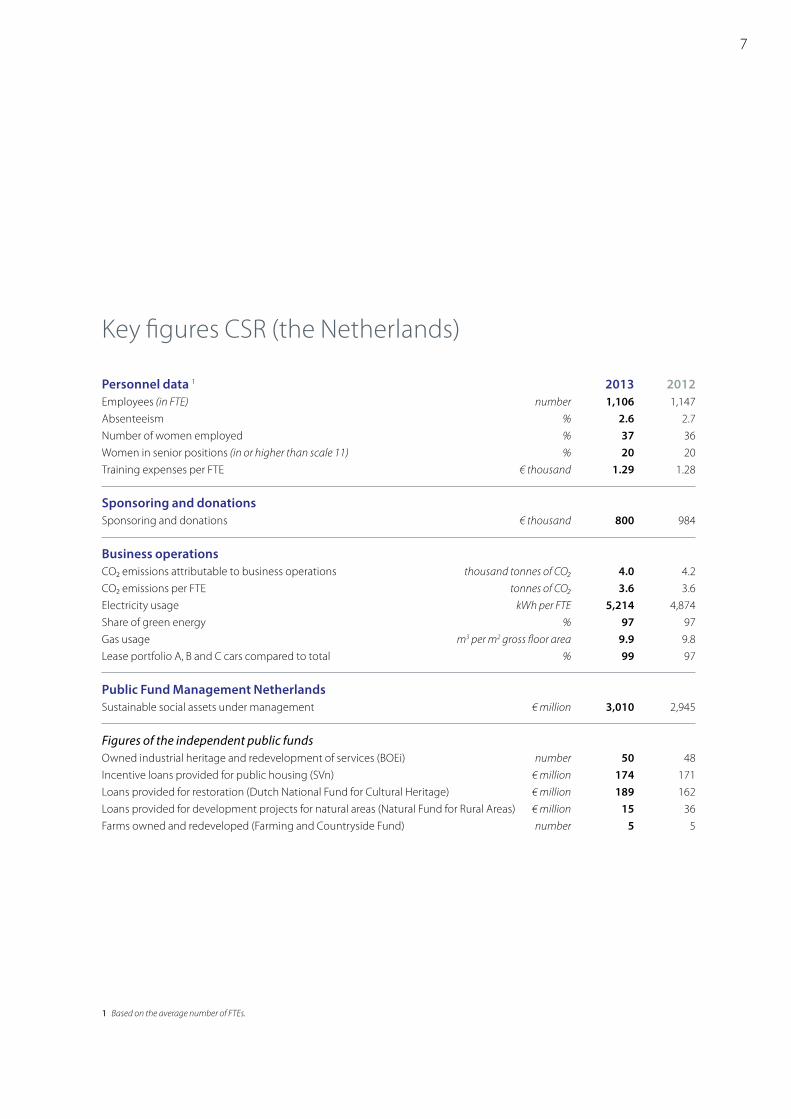

Personnel data 1 2013 2012Employees (in FTE) number 1,106 1,147

Absenteeism % 2.6 2.7

Number of women employed % 37 36

Women in senior positions (in or higher than scale 11) % 20 20

Training expenses per FTE € thousand 1.29 1.28

Sponsoring and donations Sponsoring and donations € thousand 800 984

Business operations CO₂ emissions attributable to business operations thousand tonnes of CO₂ 4.0 4.2

CO₂ emissions per FTE tonnes of CO₂ 3.6 3.6

Electricity usage kWh per FTE 5,214 4,874

Share of green energy % 97 97

Gas usage m3 per m2 gross floor area 9.9 9.8

Lease portfolio A, B and C cars compared to total % 99 97

Public Fund Management NetherlandsSustainable social assets under management € million 3,010 2,945

Figures of the independent public fundsOwned industrial heritage and redevelopment of services (BOEi) number 50 48

Incentive loans provided for public housing (SVn) € million 174 171

Loans provided for restoration (Dutch National Fund for Cultural Heritage) € million 189 162

Loans provided for development projects for natural areas (Natural Fund for Rural Areas) € million 15 36

Farms owned and redeveloped (Farming and Countryside Fund) number 5 5

Key figures CSR (the Netherlands)

1 Based on the average number of FTEs.

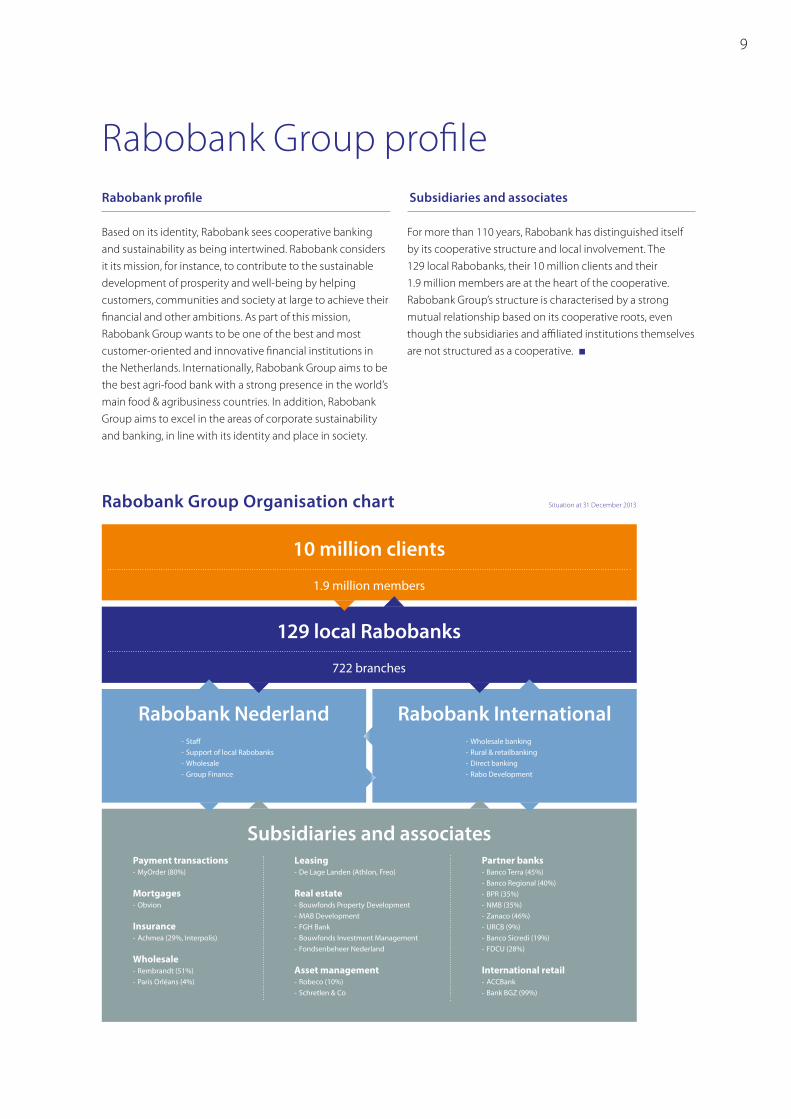

10 million clients

722 branches

1.9 million members

29 local Rabobanks1

- - Support of local Rabobanks- Wholesale- Group Finance

Rabobank Nederland Rabobank International- Wholesale banking- Rural & retailbanking- Direct banking- Rabo Development

Subsidiaries and associatesLeasing- De Lage Landen (Athlon, Freo)

Real estate- Bouwfonds Property Development- MAB Development - FGH Bank - Bouwfonds Investment Management - Fondsenbeheer Nederland

Asset management- Robeco (10%)- Schretlen & Co

Payment transactions- MyOrder (80%)

Mortgages- Obvion

Insurance- Achmea (29%, Interpolis)

Wholesale- Rembrandt (51%)- Paris Orléans (4%)

Partner banks- Banco Terra (45%)- Banco Regional (40%)- BPR (35%)- NMB (35%)- Zanaco (46%)- URCB (9%)- Banco Sicredi (19%)- FDCU (28%)

International retail- ACCBank- Bank BGZ (99%)

9

Rabobank Group profile

Rabobank Group Organisation chart Situation at 31 December 2013

Rabobank profile

Based on its identity, Rabobank sees cooperative banking

and sustainability as being intertwined. Rabobank considers

it its mission, for instance, to contribute to the sustainable

development of prosperity and well-being by helping

customers, communities and society at large to achieve their

financial and other ambitions. As part of this mission,

Rabobank Group wants to be one of the best and most

customer-oriented and innovative financial institutions in

the Netherlands. Internationally, Rabobank Group aims to be

the best agri-food bank with a strong presence in the world’s

main food & agribusiness countries. In addition, Rabobank

Group aims to excel in the areas of corporate sustainability

and banking, in line with its identity and place in society.

Subsidiaries and associates

For more than 110 years, Rabobank has distinguished itself

by its cooperative structure and local involvement. The

129 local Rabobanks, their 10 million clients and their

1.9 million members are at the heart of the cooperative.

Rabobank Group’s structure is characterised by a strong

mutual relationship based on its cooperative roots, even

though the subsidiaries and affiliated institutions themselves

are not structured as a cooperative.

10 Rabo Real Estate Group Annual Summary 2013

Report of the Board of Directors

Mixed picture at Bouwfonds Property Development

In 2013, Bouwfonds Property Development concluded only

2,160 housing transactions, a decline of more than 579

compared to 2012. The number of transactions plummeted

in France, too, especially driven by changes in tax incentives.

The German residential market remained as good as ever;

the number of housing transactions was flat on 2012. In

2013, the number of housing transactions at Bouwfonds

Property Development dropped by 18% to 5,169

transactions in total.

Phase-out of MAB Development

In the first six months of 2013, we took the painful decision

to gradually reduce MAB Development. Due to the market

developments, we unfortunately do not see a bright future

for the property development of commercial real estate

and will not launch any new projects. The size of

MAB Development was strongly reduced as a result.

FGH Bank maintains its solid marketposition

In 2013, FGH Bank’s gross loan portfolio grew to € 19.4 billion.

The partial takeover of Friesland Bank’s loan portfolio in

particular prompted this slight increase. The loan provisions

were € 568 million, 308 basis points of the average loan

portfolio. These substantial additions exceeded the

operating profit.

Positive result for Bouwfonds Investment Management

The name Bouwfonds REIM was changed to Bouwfonds

Investment Management ( IM) in 2013. The new name

emphasises the broad focus on ‘real assets’, with activities in

five sectors – commercial real estate, residential property,

parking, communications infrastructure and agriculture &

farms. The assets under management at Bouwfonds IM rose

to € 5.9 billion in 2013.

The Bouwfonds European Real Estate Parking Fund II

invested in the first car parks after the Fund had closed to

new investors in early 2013. The Bouwfonds European

Student Housing Fund was launched. This Fund focuses on

student accommodation in the main European university

cities, primarily in Germany, France, the Netherlands and the

United Kingdom.

Rabo Real Estate Group in 2013

Once again, market conditions in the Dutch property markets were poor in 2013. This forced Rabo Real Estate Group to initiate substantial downward revaluations of land and revaluations of land development, form provisions for credit losses and decide to gradually reduce the development of commercial real estate. This led to a negative result of € 858 million. Fortunately, there were also some silver linings. Our performance in France and Germany, which is an economically strong country, was positive in the past year and Bouwfonds Investment Management closed the year in the black, too. The underlying result was comparable to previous years.

11

Growth for Public Fund Management Netherlands

The funds of Public Fund Management Netherlands are

devoted to improving the quality of our living environment.

By extending more than 4,100 loans to first-time buyers, for

example, the Dutch Public Housing Stimulation Fund (SVn)

made a nice contribution to the aim of getting the

residential market back on track. By deploying its network

and providing loans, the Dutch National Fund for Cultural

Heritage was a major financial partner in the ambitions to

restore monumental properties and find new uses for them.

Through its roles as advisor, owner and developer, the

National Trust for the Maintenance, Development and

Exploitation of Industrial Heritage in the Netherlands (BOEi)

contributed greatly to the new use and operation – and

therefore the preservation – of specific real estate, such as

industrial properties, farms, churches and monasteries. The

efforts of the National Fund for Rural Areas have led to new

revenue models for nature, forest and landscape.

Vision and strategy

A passionate real estate company, Rabo Real Estate Group

achieves its clients’ ambitions in the areas of housing,

shopping, working and recreation. We are active in property

development, property finance, investment management

and public fund management. We have comprehensive real

estate expertise in-house, a strong network and are known

as a transparent and sustainable real estate company.

Rabo Real Estate Group is the centre of real estate expertise

of Rabobank Group. Rabo Real Estate Group is one of

Europe's largest real estate companies. Outside the

Netherlands, our activities are concentrated in France and

Germany. We operate under the brand names Bouwfonds

Property Development, MAB Development, FGH Bank,

Bouwfonds Investment Management and Public Fund

Management Netherlands (‘Fondsenbeheer Nederland’).

Our ambition is to be the partner of choice in real estate by

giving the desires of our retail customers and corporate

clients centre stage.

ActivitiesDevelopment

Integrated residential areasAs one of the largest European area developers, Bouwfonds

Property Development has been developing integrated

residential sites for more than 65 years. A stable and reliable

partner, it has a clear focus on quality, sustainability and the

customer. Its ambition is to create living environments that

have high user, amenity and future value. Bouwfonds

Property Development, active in the Netherlands with the

name Bouwfonds Ontwikkeling, uses its regional offices’

knowledge of the market and Rabobank’s extensive local

presence to respond forcefully to local conditions.

12 Rabo Real Estate Group Annual Summary 2013

Bouwfonds Property Development focuses on the initial

stage of the development process, teaming up with

municipalities and other parties to lay the foundations

for successful, integrated area development. Bouwfonds

Property Development is market leader in the Netherlands

and well-positioned in France (Bouwfonds Marignan)

and Germany (Bouwfonds Immobilienentwicklung).

Commercial real estate MAB Development is a developer of commercial real estate

and mixed-use inner-city projects. MAB Development

provides cities and city centres with sustainable

combinations of living, shopping, working and recreation.

Retail is often a key ingredient in mixed-used developments.

It has been decided to gradually reduce the development of

commercial real estate. Current projects will be completed;

no new projects will be launched.

Finance

FGH Bank is the specialist in financing commercial real estate.

Property finance requires a considered and solid approach in

which expertise, professionalism and reliability are vital.

Close contact with customers is of importance to FGH Bank.

By operating close to the market, the bank is able to actively

respond to customer demands. With its real estate expertise,

FGH Bank delivers added value to external customers and

internal customers like the local Rabobanks and other

Rabobank Group business units.

Investment Management

Bouwfonds Investment Management (IM) offers property

investment products with a relatively low risk profile to

investors in the residential property, commercial real estate,

parking, communications infrastructure and agriculture &

farms sectors. These activities require knowledge of the local

situation. Bouwfonds IM works with specialised teams from

local offices in the Netherlands, Germany, France, Poland

and Romania. Bouwfonds IM’s investment philosophy is

based on four components: a specialised team, responsible

investment, standardised processes and integrated risk

management.

Management of Public Funds

Collaboration between public and private parties is of major

importance in the complex spatial investment market. Public

Fund Management Netherlands is an independent manager

of independent social funds and organisations that help

governments and other investors to achieve their goals in

spatial quality. Public Fund Management Netherlands

manages the Dutch National Fund for Cultural Heritage, the

National Fund for Rural Areas, the Dutch Public Housing

Stimulation Fund (SVn), the National Trust for the

Maintenance, Development and Exploitation of Industrial

Heritage in the Netherlands (BOEi), the Foundation for

Conservation and Redesignation of Religious Heritage, the

Farming & Countryside Fund, and the Dutch Climate

Landscape Foundation.

Business policy Governance

Rabo Real Estate Group is managed by the Board of Directors,

which comprises the Chairman, the Chief Financial & Risk

Officer (CFRO) and the Chairmen of the Management Boards

of each of the three business units. One of them is Vice

Chairman. The members of the Board of Directors share joint

responsibility for the management of Rabo Real Estate Group,

the general affairs of the company and the business units.

This means that the Board of Directors presents a common

vision, adopts the policy and strategy per business unit

and assesses the risks of major business proposals. The

Supervisory Board supervises the Board of Directors.

Rabobank Nederland, the shareholder, appoints the

members of both the Board of Directors and the Supervisory

Board.

Corporate Social Responsibility

Real estate should serve end-users and contribute to the

quality of today’s and tomorrow’s society. That is why

Corporate Social Responsibility (CSR) is common practice at

Rabo Real Estate Group. Our CSR Charter states how we wish

to collaborate with our stakeholders and society in a broad

sense. Our ambition is to be a leader in sustainability in the

property industry. We translated the main issues for our

Group into four pillars: sustainable real estate, ethical

business practices, responsible operations and social

commitment. Based on these pillars, we defined five Group

themes: energy consumption, mobility, staff & leadership,

vital communities and circular economy.

13

This results in the following concrete targets and activities:

Energy consumption• In 2015 our carbon footprint will be at least 10% lower than

in 2012.

Mobility• In 2014 our company cars will have maximum carbon

emissions of 150 gr/km. This will be reduced every year.

Nearly all our company cars already have an A, B or C label.

Staff & leadership• In 2014 we will devote more attention to recruiting highly

qualified employees, for example by developing a trainee

programme.

Vital communities• We are working on vital communities. We are doing so

through our products and services, but also through Public

Fund Management Netherlands and the Bouwfonds

Cultural Fund. The latter Fund supports cultural projects

that contribute to the quality and appeal of public spaces.

Bouwfonds Art Foundation actively manages the corporate

art collection, contributes to a stimulating working

environment and offers its expertise in art and cultural

projects launched by the divisions. For many years,

Rabo Real Estate Group has been the main sponsor of the

Dutch Heritage Days, one of the largest cultural events in

the Netherlands.

Circular economy• We support the trend towards a circular economy through

smart design and construction and by recycling materials.

• With new homes developed by Bouwfonds Property

Development – which already meet high standards in the

area of energy efficiency – consumers can choose from

various additional energy-saving measures using the

‘Green Buyers’ Option List’. Under the name ‘Green Light’,

Bouwfonds helps residents of new housing estate Nieuwe

Kortenoord in Wageningen to save energy. In collaboration

with the municipality and with a subsidy from the Province

of Gelderland, an extremely favourable offer for solar

panels was made to buyers, many of whom accepted the

offer. A specially appointed energy coach gives residents

additional tips to save energy.

• MAB Development is involved in the sustainable

development COOL63 in Rotterdam. COOL63 received a

BREEAM Excellent certificate thanks to its location in the

city centre, the mixed-use concept and reuse of the

14 Rabo Real Estate Group Annual Summary 2013

building, limiting the environmental stress now and in the

future. Several energy-saving measures have also been

taken, such as thermal energy storage in the ground,

high-quality radiant ceiling panels in the offices, and

energy-efficient transport systems.

• FGH Bank measures the sustainability of the property

portfolio on the basis of outperformers, performers and

underperformers. This measurement is the basis of

customer dialogue.

• Bouwfonds IM participates in the GRESB Survey, a

benchmark for investment managers’ sustainability

performance. The results are used to define the

improvement potential and to engage in dialogue with

customers.

• The circular economy is supported by the contributions

made by Public Fund Management Netherlands in terms

of sharing knowledge, creating support and enabling

investments in the preservation of sustainable

(monumental) properties and nature.

Financial policy

From its perspective of properly serving its clients,

Rabo Real Estate Group wants to be a profitable company

with a balanced risk profile. The performance contract

contains detailed strategic objectives, both for

Rabo Real Estate Group as a whole and for its individual

business units. These lead to strategic, operational and

financial commitments aimed at value creation, with a focus

on appropriate – risk-adjusted – returns on the invested

capital for the shareholder.

Risk management

In 2013, we tightened our risk appetite and laid it down in

our existing Risk Appetite Statement. This Statement

describes the risks that Rabo Real Estate Group is willing to

take in achieving its strategy.

The Risk Appetite Statement also provides that we must

clearly and demonstrably comply with laws and regulations,

in particular in policy areas like operational risk management

and product approval. As a result, in the year under review

we reviewed our policy documents within the risk

management domain and further improved the quality of

reports and instruments.

Policy adjustments are assessed by the Balance Sheet and

Risk Management Committee (BRMC). The committee meets

every month and comprises the CFRO of Rabo Real Estate

Group and the financial directors of the business units,

supplemented with treasurers, risk managers and controllers.

Subject to policymaking, the BRMC monitors balance sheet

and market risks at the portfolio level every month.

Operational risk and capital management are fixed items on

the BRMC’s agenda, too.

15

The market conditions lead to new investments and

financing being kept to a minimum. Market and credit risks

that we assume are assessed through a layered authorisation

structure for approval. We also test new and existing

positions against a system of limits laid down in the Risk

Appetite Statement. The customer interest, operational risk

and reputation risk of new products are assessed before they

are launched to the market. We periodically assess existing

products regarding these risks as well.

In 2013 we continued the phased implementation of a

Business Control Framework, which identifies key risks and

assesses the effectiveness of the corresponding control

measures.

ValuationRabo Real Estate Group values the land, work in progress

and finished goods at cost less any impairments deemed

necessary. Each year, we assess whether there are any

declines in value that call for an adjustment of the book

value. Investment property is valued at fair value; the most

likely price reasonably obtainable in the market on the

reporting date. We regularly engage independent valuers

to determine the value of large and high-risk projects.

Outstanding loans are reviewed at least once per year, with

an opinion being reached about the value. Loans that have

undergone a value adjustment are adjusted to the net

realisable value. Publications and guidelines of regulators

and industrial organisations are taken into account in

Rabo Real Estate Group's robust valuation processes.

Compliance

Integrity and transparent business conduct are important

values at Rabo Real Estate Group. We therefore have an

independent compliance organisation, which has a central

compliance function and a Compliance Officer for each

business unit. The Rabo Real Estate Group Head of

Compliance reports to the Chairman of the Board of

Directors and to the Supervisory Board.

We have implemented a Code of Conduct that includes

whistle-blower arrangements. It is periodically assessed and,

where necessary, amended. Each year, we ask employees

whether they complied with the Code of Conduct.

In 2013 we developed the Code of Conduct Tool, which

– using examples, questions and points for consideration –

heightens awareness among employees of situations they

may encounter in practice. Many of our employees have now

completed this tool.

We also periodically examine the integrity and compliance

environment among employees. The Compliance

department performs a risk analysis in that respect to

determine whether the control measures are adequately

hedging risks.

16

Banking Code

The Banking Code was adopted in September 2009. At

Rabo Real Estate Group, the Code officially only applies to

FGH Bank, which is an institution with a banking licence

under the Dutch Financial Supervision Act. However,

Rabo Real Estate Group has opted to apply the Banking Code

to all its majority interests, such with due observance of the

specific characteristics of a real estate company. Where

the following text refers to Rabo Real Estate Group, this also

includes FGH Bank without exception. The main topics of

the Banking Code are listed below, and any deviations are

explicitly mentioned.

Supervisory BoardThe composition of the Rabo Real Estate Group Supervisory

Board is diverse and its members complement each other.

The departure of Sipko Schat and Jaap Blokhuis has created

two vancancies. FGH Bank has its own Supervisory Board, but

its members are also on Rabo Real Estate Group’s Supervisory

Board. The Supervisory Board assessed its own performance

in the past year. Within the context of permanent education,

all members increased their knowledge of the business

control framework set up at Rabo Real Estate Group and of

FGH Bank’s management organisation. The Supervisory

Board has rendered account of its work in the Annual Report.

In accordance with the Banking Code, profiles of its

members have been drawn up.

DirectorsThe members of the Management Boards of FGH Bank and

Bouwfonds Investment Management signed a moral and

ethical conduct declaration based on the Banking Code. The

other members of the Board of Directors are not designated

as directors of a financial institution in line with the Banking

Code. All employees signed the Code of Conduct, which was

updated at the end of 2012. Within the context of permanent

education, in 2013 the members of the Board of Directors

studied the topic of risk management by means of the

Business Control Framework and FGH Bank’s management

organisation. The members of the FGH Bank Management

Board studied the topics transformation in real estate,

sustainability and IT trends at banks.

Risk managementThe members of the Board of Directors and the Supervisory

Board receive periodic reports describing the group-wide

developments of credit, market and operational risks, the risk

of non-compliance, interest rate risk, Rabo Real Estate Group’s

liquidity position, etc. These reports allow both corporate

bodies to be aware in time of the material risks that

Rabo Real Estate Group is running. The Board of Directors

is responsible for adopting, pursuing, monitoring and

adjusting risk policy and risk appetite. The BRMC advises the

Board of Directors in policy decisions. The adjusted approval

framework, the polices on financing, risk appetite and

concentration risk, as well as the policy on balance sheet risk

and the policy regarding operational risk management, were

presented to the Supervisory Board in 2013. The key risks

to which Rabo Real Estate Group is exposed were also

discussed with the Supervisory Board.

Product approval processRabo Real Estate Group has a product approval policy that

is based on Rabobank Group’s policy. Products are only

introduced to the market or distributed after a careful

17

weighing of risks and a careful assessment of relevant

aspects such as the duty of care. In addition, all products in

the range are subjected to periodic product reviews. The Risk

Management, Compliance and Legal Affairs departments

advise the product approval committee with regard to the

necessary decision-making.

Audit functionRabo Real Estate Group complies with all Banking Code

provisions relating to audits. We have an independently

positioned audit function which reports to the Chairman of

the Board of Directors and the Chairman of the Supervisory

Board. The Internal Audit department and the external

auditor frequently exchange information. The internal and

external auditors’ risk analysis, findings and audit plan are

aggregately discussed with the DNB (Dutch Central Bank)

at Rabobank Group level.

RemunerationRabo Real Estate Group subscribes to the ‘View on

Remuneration’ (‘Visie op belonen’), a policy document drawn

up by Rabobank Group. In deviation from the Banking Code,

the shareholder determines the remuneration of members

of the Board of Directors, subject to the Supervisory Board’s

approval. The Board of Directors and the Supervisory Board

aim for a median position in the relevant remuneration

market, in which respect Rabo Real Estate Group – in line

with the Banking Code – is, in essence, a trend follower in

the market.

Rabo Real Estate Group respects existing employment

contracts of members of the Board of Directors and the

FGH Bank Management Board that include severance pay

provisions that deviate from the Banking Code, as this

payment is based on the ‘subdistrict court formula’. New

members of the Board of Directors may receive severance

pay of up to one time their annual salary. Variable pay

awarded to the Board of Directors is never more than 100%

of their fixed income and includes a long-term component

that partly depends on profitability or continuity. The

remuneration results are balanced and the performance

criteria do not incite to take irresponsible risks. The principle

that financial performance should be adjusted for

(estimated) risks and the cost of capital in the performance

assessment based on predetermined performance criteria

is not applied to the population subject to the Collective

Labour Agreement. Rabobank tests the total amount of

variable pay against the Group’s capital position at Group

level. The performance management process requires some

optimisation in terms of assessability and timely recording.

In principle, retention, exit and welcoming fees are not

permitted within Rabo Real Estate Group. If these are

nevertheless necessary in isolated cases, they are subject

to approval as laid down in the rules of Rabobank’s Group

Remuneration Policy. In 2013 anumber of exit packages were

granted, which were all in line with abobank's Controlled

Remuneration Policy.

Cooperation with Rabobank Group

Being part of Rabobank Group, we collaborate closely with

colleagues in the Group in various fields of expertise. Real

estate is an important pillar for many of Rabobank Group’s

customers with regard to living, shopping and working as

well as recreation.

As Rabobank Group’s centre of real estate expertise, we

provide support in the area of property finance, property

advice and property development. The cooperation

generated many synergy benefits in 2013, too.

Local Rabobanks increasingly contact FGH Bank about

property finance issues. FGH Bank supports the banks by

analysing the existing property portfolio and property

finance applications. In addition, FGH Bank helps to make

recommendations and appraisals via the FGH Rabo Appraisal

Desk (RAD). The RAD plays an important role for Rabobank

Group in the implementation of its tightened appraisal

policy. Rabo Onroerend Goed (ROG), part of FGH Bank

since 2005, advises local Rabobanks about their own

accommodation and acts as in-house broker for the local

banks.

Bouwfonds Property Development regularly cooperates with

Rabobank Nederland and the local Rabobanks, for example

in the sale of new developments, the development of

regional housing market visions, area development and

redevelopment or actions to stimulate the local residential

market. In 2013 Bouwfonds Property Development also

provided support to Rabobank Nederland’s Special Credits

department in closing complex real estate files.

The agriculture & farms sector is one of Bouwfonds IM’s five

core activities. Through Rabo Farm – part of Bouwfonds IM –

investment funds focusing on investments in farmland and

farms are initiated and actively managed for institutional

clients. This involves close collaboration with several

Rabobank business units, allowing Rabo Farm to reap the

full benefit of Rabobank’s network and knowledge in the

food and agri industry.

As a centre of real estate expertise, Rabo Real Estate Group

has been mandated by Rabobank to support local

banks through Rabo Eigen Steen to solve their own

accommodation issues.

In 2013 Rabobank Nederland teamed up with

MAB Development and started preparing its office at

Fellenoord in Eindhoven for the future. At the current site,

the high-rise building will gradually make way for a new,

more sustainable office that is geared to employees’ needs,

now and in the future. The decisive factors behind the

decision were the central location, cost efficiency and the

desire to avoid vacancy.

SVn’s loan for first-time buyers was used in 2013 for various

new developments of Bouwfonds Property Development

and, in this way, contributed to the sale of new build homes.

Large-scale restoration and new uses of monumental

properties are regularly financed by means of co-financing

between Rabobank and the Dutch National Fund for Cultural

Heritage.

The National Fund for Rural Areas and local Rabobanks have

pooled resources in setting up area-specific funds and

corporate savings accounts (RaboStreekrekening), jointly

contributing to the preservation and management of nature

and landscape.

18 Rabo Real Estate Group Annual Summary 2013

20 Rabo Real Estate Group Annual Summary 2013

Market developments 2013

In 2013 the situation in the Netherlands deteriorated further

in all property market segments, which was seen especially

in the loss of real estate value. Nevertheless, dynamics are

increasing on the part of investors in particular. The

substantial loss of real estate value has boosted investors’

appetite to buy Dutch properties, in which respect the

interest shown by foreign investors is particularly striking.

Residential market

The Netherlands: prospects of recoveryDevelopments in the market for existing homes were initially

unfavourable from the beginning of 2013. This was partly

due to the fact that many buyers wanted to benefit from

the old lending rules at the end of 2012. The number of

transactions gradually recovered in the course of the year,

but prices continued to show a delayed fall.

In the second half of 2013, the number of transactions

gradually rose and prices bottomed out. The number of

transactions totalled 110,000 in 2013, 6% below the level of

2012. All home types experienced a price decline (3.7% on

an annual basis, 2012: 4.7%), especially detached houses.

A striking aspect was the turnaround in consumer

confidence; it is still negative, but improved fairly rapidly.

The supply of owner-occupied homes in the Netherlands

dropped slightly to approximately 213,000 homes at the end

of the year. This was still nearly twice the number of

transactions. Asking prices fell.

The new build market very slowly gained momentum, too.

The volume of project-based homes dropped by some 20%

in the first six months of 2013, even though sales were

already historically low in 2012. In 2013 approximately

14,000 homes were sold. In part because of the final

tax-driven dash at the end of the year, this figure was more

than 15,000 in 2012.

Partly because the rules have been tightened, consumers

find it more difficult to finance a home. It is one of the

reasons why house-hunters are increasingly turning to the

rental market – more specifically, the free-sector rental

market. This is because the availability of, and right to,

subsidised rental homes is limited. This prompted a number

of town councils to increase the focus in their housing

market policies on free-sector rental homes – i.e. homes in

the rental class starting from € 700 per month.

Germany: residential market remains healthyThe economy in Germany once again experienced growth

in 2013, with high consumer confidence, a high level of

spending and more money in savings accounts. (Mortgage)

interest rates remained low, of which the residential market

reaped the benefits.

21

More than 220,000 new homes were completed and sold,

both to owner/users and to (private) investors. The great

migration to the large metropolitan regions resulted in an

increase in rents and purchase prices in cities like Berlin,

Frankfurt, Hamburg, Munich and Stuttgart by more than 5%.

The total debt volume in the residential market did not

increase, as house buyers financed a substantial portion

(25-40%) with their own capital.

France: restriction of tax incentives and lagging economic growth translated into a decline of new productionFrance, too, is feeling the consequences of the financial

and economic crisis in the new build market. The reduction

of tax incentives partly triggered the sharp decline of the

new build market from 2012 onwards. The market did not

rebound in 2013; sales of new homes was slightly down from

the previous year. In the same period, prices of new homes

rose slightly by 1.7% for apartments and dropped slightly

for single-family homes. Again, regional differences were

considerable.

The volume of new homes in France is relatively high

compared to the market of existing homes, in which the

transaction volume amounted to approximately 680,000

(approximately 12% less than in 2012). Prices were 1.4%

lower than the previous year; the price drop was a fraction

lower for single-family homes.

Commercial real estate

The NetherlandsOffice market: continued low transaction volume The demand for office space continues to be as low as in

previous years. Last year a total of 1.1 million m2 of space

were taken up, which is roughly equal to the level of 2012.

The take-up is very concentrated, however, with

approximately 40% taking place in the four major cities and

half of this in Amsterdam. It is also striking that there is hardly

any demand for large properties. As far as is known, only

six properties of more than 10,000 m2 were leased in 2013.

The low demand has sparked yet another increase of the

supply of office space, with some 7.4 million m2 of office

space being offered at the end of 2013 – an increase of 5%.

As a result, over 15% of office space in the Netherlands is

now vacant. A faster increase of vacancies was partly

prevented as office space was withdrawn from the market

on a considerable scale following transformations into other

functions or demolition. Last year the withdrawal volume

even slightly exceeded additions as a result of new build,

which translated into a limited reduction of the stock. Given

the large volume of vacant properties, governments and

market parties will have to work towards further reducing

the stock in the years ahead in order to restore the balance

in the market. This will be a major challenge. The rate of

withdrawals must increase, but the ‘simple’ projects have

now been completed.

22 Rabo Real Estate Group Annual Summary 2013

Rents dropped even further on the back of the further

imbalance in the office market. Last year’s transaction prices

averaged € 125/m2. Differences between regions and

locations are also increasing. With a maximum of € 325/m2

rents in the Amsterdam Zuidas remained virtually flat,

whereas rents fell even further in municipalities and areas

with high vacancy levels.

Retail market: vacancy risk increasesLast year retailers in the Netherlands once again saw their

sales slump, to such an extent even that many of them failed

to keep their business afloat. But the market is not as one-

sided as it looks. On the one hand we see shops disappear,

but on the other hand other segments and retail chains are

flourishing. Last year these dynamics translated into a

take-up of approximately 735,000 m2 of retail space, despite

the economic tide. Although this is slightly below the level

of 2012, historically the volume is still high.

On balance, more retail space became vacant last year. At the

end of 2013, the vacancy rate in the Netherlands stood at

6.9%; a year earlier, 6.6% of retail space was unoccupied.

This means that the vacancy risk is rising and it is therefore

striking that the new build planned volume increased last

year. Last year rents fell across the board, with only a few

exceptions. This put pressure on the value, whereas the retail

market showed relatively good returns in the first few years

following the crisis.

Commercial real estate market: logistics market is improvingLast year, the demand for commercial real estate remained

virtually the same at a level of 2.8 million m2. The demand is

clearly on the rise within the logistics real estate segment,

however. This is partly triggered by companies investing in

special centres for goods ordered online and partly by retail

chains introducing more and more pick-up points at

industrial sites.

The demand from the logistics chain is mainly for new build,

which results in a persistently high supply in the market of

existing real estate. In the Netherlands some 10 million m2 of

commercial real estate are vacant, whereas nearly 50% more

new properties were completed. The high supply prompts a

reduction of average rents in the existing stock. Last year the

average price was € 45/m2, approximately 3% below the level

of 2012.

GermanyThe German economy developed positively in 2013,

although the economic growth was hampered somewhat

by the global flagging growth. Unemployment rates fell and

consumer confidence rose even further. Consumer spending

developed favourably as a result, creating a high demand for

retail space and general upward pressure on rents.

By contrast, some outdated shopping centres are in a tight

corner, suffering from the increasing popularity of online

shopping and a revival of city centres in large cities.

Renovation is the solution for some of these centres.

FranceEconomic prospects are not as rosy in France. Its economy

is under pressure and unemployment levels are high. The

necessary reforms were postponed, but this still did not lift

consumer confidence. Expenditure is slightly declining as a

result and the demand for retail property is relatively limited.

Shops in secondary locations in particular are hard to let.

A substantial portion of the retail floor space is out of date

and should be redeveloped at high-potential sites.

Investing in real estate

The Netherlands In 2013, the total transaction volume in investment property

in the Netherlands was up from 2012, mainly driven by

a number of very high-value transactions with foreign

investors in particular. Dutch investors still show relatively

little activity in the property market. The number of

transactions is limited and values are still under great

pressure. The market divide is still fully visible, not only for

offices but also for shops. In some cases price levels have

become sufficiently attractive for investors, sparking a

considerable increase in the office transaction volume.

The Dutch retail market is lagging further in the cycle and

the transaction volume declined for the third year in a row.

Slumping prices in the residential market have made

investments more attractive. This is reflected in the

investment volume, which increased slightly in 2013.

Dutch investors are still dominant, but interest from

abroad is steadily growing.

On average, initial yields rose in all segments in 2013, but

initial yields in absolute high-end real estate were flat.

GermanyGermany, on the other hand, shows an entirely different

picture, partly inspired by more positive economic

conditions. The total transaction volume grew for the fourth

consecutive year. The German residential market is performing

well, with increasing rents and purchase prices and growing

investor interest. Institutional and foreign parties in particular

showed a substantial increase in residential market

investments. The commercial property market, too,

capitalised on the positive market sentiment and economic

conditions. In 2013, the investment volume for commercial

property slightly exceeded the volume of 2012.

23

FranceTo some extent, the situation in France is comparable to

the Netherlands. Here, too, economic performance is

disappointing, although it is more positive than in the

Netherlands. The transaction volume in France declined

slightly, ending up below the levels of the two preceding

years. The average price level also fell, except in prime

locations in Paris in particular and in some other big cities.

Foreign investors continue to show interest in French real

estate, but a modest decline can be observed.

Financial results

In the course of 2013, it became clear that a market rebound

in the Dutch property markets in particular would take

longer than previously expected, which adversely affected

the results to a great extent. The underlying result was

positive and comparable to previous years, but downward

revaluations of land and property projects, revaluations of

land development and loan provisions totalling € 1.4 billion

led to a negative net result excluding non-controlling

interests of € 858 million relative to a net loss of € 113 million

in 2012. The downward revaluation of land and the

revaluation of land development of Bouwfonds Property

Development amounted to € 567 million. On balance € 568

million was added to the loan provisions at FGH Bank. The

rest is attributable to provisions for the MAB Development

phase-out and a number of commercial property projects.

24 Rabo Real Estate Group Annual Summary 2013

Personnel

The struggling property markets and substantial operating

losses force Rabo Real Estate Group to pull out all the stops.

A major decision taken in the year under review was the

gradual and careful phase-out of the MAB organisation,

resulting in a job loss in 2013 and in the years ahead.

In the new Collective Labour Agreement,

Rabo Real Estate Group’s decision to mark time is reflected in

the focus on cost savings in the Netherlands. The parties to

the Collective Labour Agreement agreed on a long-term

contract running from 1 October 2013 until 31 December

2015. No collective pay rise was agreed. An arrangement

was also made regarding a tightened method for awarding

bonuses, under which payments are only made if

Rabo Real Estate Group achieves a positive return on its

equity. It was also agreed that no bonuses would be paid

for performance year 2013, which is an adjustment of the

current Collective Labour Agreement.

As Rabo Real Estate Group acts in line with Rabobank’s

Pension Plan (PP), starting in 2014 the pension adjustments

in the PP 2014 will be a given for all Rabo Real Estate Group

employees. Parties to the Rabo Real Estate Group Collective

Labour Agreement made an additional arrangement about

the amount of employee contributions.

The parties agreed, in principle, to maintain the Social Plan.

However, if the law or dramatic organisational developments

give rise to do so, the parties will engage in talks about the

Social Plan and interim CLA arrangements may ensue.

In order to keep in touch with tomorrow’s reality, in which

smarter ways of working and increased freedom of choice

will be key themes, the parties made a study arrangement

about giving shape to a comprehensive mobility solution for

all employees.

The HR Vision was updated in 2013 and the Board of

Directors formulated a vision ‘Working 2015’. For the

FGH Bank division, the year under review was marked by

a further implementation of the Werkwijzer project.

At the start of performance year 2013 training courses and

workshops were organised for all managers and employees,

devoting much attention to the use of the new digital

agreement and assessment form, the new competency

language and the changed procedure for the assessment

and development round.

The biennial employee survey was conducted in 2013.

Although results differ for each division and each topic,

they do reveal very high satisfaction scores in general.

In 2013, Rabo Real Estate Group focused on succession

planning and Management Development. Together with

TiasNimbas, it developed and offered a leadership

programme for the top 30. The programme – in an amended

form – was also offered to middle management of

Bouwfonds Property Development in 2013.

The new legislation regarding a balanced division of seats on

the board of management and supervisory board between

men and women has been taken into account. Presently, one

woman has a seat on Rabo Real Estate Group’s Board of

Directors. One of the vacant positions on the Supervisory

Board will be filled by the shareholder; a suitable candidate

will be sought for the other position on the basis of the job

profile. At the beginning of 2014 Rabo Real Estate Group,

together with Rabobank, endorsed the Talent to the Top

charter. This initiative aims for a higher inflow and

progression of women to the top and retention of female

talent.

In 2013, Rabo Real Estate Group followed up on its policy

review in terms of job evaluations and remuneration for

senior management. Lastly, in the year under review

Rabo Real Estate Group followed up on an impact analysis

and implementation of measures within the framework of

new laws and regulations in the area of controlled

remuneration policies.

25

Outlook

2014: Still a long way to go

A slight economic recovery is expected for 2014, partly

driven by an economic upswing in both the Eurozone and

the United States. The Dutch corporate sector may capitalise

on this, especially businesses that are active in foreign

markets. The domestic demand is expected to remain low,

although improving consumer confidence and slightly rising

purchasing power may bring relief.

The property markets do seem to have bottomed out and

sometimes even show signs of a modest recovery, but still

the market remains vulnerable. As property prices have

fallen, we expect the investment demand for commercial

property in 2014 to be at least comparable to the level of

2013. This means that the interest among buyers is slightly

higher, but far less than the supply of buildings.

Residential market: mixed picture

Rabo Real Estate Group sees silver linings in the Dutch

residential market in 2014, but the modest recovery of the

last quarter of 2013 is fragile and new policy measures for the

residential market may harm confidence. It is presently

essential to hold on to the Housing Sector Agreement

concluded in February 2013, which would help settle down

the housing market and thus benefit consumer confidence.

2014 may prove to be the year for first-time buyers; the low

price level currently creates high affordability. A dichotomy is

seen among people trading up houses: part of the market is

able to trade up, in theory, if one is willing to adjust

expectations regarding the proceeds from selling a home.

Another part faces a residual debt when selling their home.

It proves to be difficult to refinance such a debt, which

prevents this group from trading up to a different home.

The euro seems to have reached a safer haven, but the

Germans continue to prefer a secure investment in bricks, i.e.

the housing market. The pressure on residential markets in

large urban regions will fuel further price rises, both in the

owner-occupied housing sector and in the rented housing

sector. The new German Federal Government will curb price

hikes for rented homes in the existing stock by means of

legislation, which will probably lead investors to adopt a

slightly more cautious policy. In big cities, politicians

increasingly demand that developers offer affordable

homes as well.

The reforms of the scial security system and economy in

France will take some considerable time yet. Unemployment

levels are still rising and consumer confidence will decrease.

However, there is a high demand for houses in large

conurbations. For many French citizens, investing in a home

continues to be major security in turbulent economic times.

Commercial real estate: light at the end of the tunnel

Finally, economic prospects are slightly more favourable for

2014. The office market is expected to see an increase of

companies’ propensity to move as a result, which will have a

positive effect on the number of lease transactions. However,

vacancy levels will not decrease substantially for the time

being as companies often have too much room and will

lease fewer square metres when relocating. Regional

differences will further increase due to the growing

popularity of big cities as business locations, which will also

be reflected in the differences in the development of market

rents and incentives. More and more offices without

prospects will also be taken from the market and no longer

actively be offered for rent.

The persistent reticence of consumers is strongly visible in

the retail market. The number of retailers that fails to keep

their business afloat is increasing, putting pressure on rents

in nearly all locations. Only prime locations in large cities are

less troubled by this development. In smaller cities, changing

consumer demand plays a role in addition to the cyclical

headwinds. Both the effect of online shopping and the focus

on larger cities and experience are factors of importance in

this regard. Renovation or reorientation will be inevitable

for shopping centres. On a positive note, both consumer

confidence and the development of purchasing power

seem to be getting back on their feet.

Investing in real estate

A combination of low interest rates and declining property

values make the Dutch property market an attractive

investment. In recent years, Dutch institutional investors on

balance parted with investment property. The increased

value of equity portfolios generally resulted in real estate

being underweighted in the asset mix. We may therefore

expect that these parties will expand the share of real estate

in their portfolios in the years ahead. Foreign parties, too,

have shown increasing interest in the Dutch market.

26 Rabo Real Estate Group Annual Summary 2013

American and Asian parties as well as investors from the

Middle East will become more active. Some of these are

investors looking for safe (core) investments in prime

locations, whereas others are attempting to buy distressed

portfolios below their market value.

For 2014, we expect economic conditions in Germany to

remain positive and be among Europe’s top performers,

along with the United Kingdom and the Scandinavian

countries. This is why we take into account continued

investor interest in the German property market. The

foundations underlying the property market are solid, but

we are likely to have the strongest growth behind us.

Expectations are that 2014 will not bring many changes in

the French property market relative to 2013. Economic

growth will remain subdued, with slightly rising

unemployment levels. The polarisation in the residential

market will grow stronger, resulting in further diverging

prices. The increase of the population and the number of

households, plus internal migration, will spur the demand

for homes in big cities. This will create stable prices, but a

decline is expected in the other regions. The trend in the

commercial property market will not differ greatly from the

residential market.

Rabo Real Estate Group in 2014

2014 will show many similarities to 2013. Expectations are

that the Dutch economy will show cautious recovery in the

course of the year, but not at a rapid pace. The rebound in

the residential market is slowly gaining momentum as well.

In addition, we are confronted with regulatory parties

exerting increasing pressure on banks and a tightening of

laws and regulations.

These conditions with uncertain prospects continue to be

challenging to the real estate companies of Rabo Real Estate

Group. It is therefore difficult to make any predictions, if at

all possible. It is clear, however, that Rabo Real Estate Group

is enjoying a lot of trust. We have a strong market position

and great expertise. In today’s market, such knowledge is

extremely important. Quality and sustainability of real

estate are spearheads of our policy. In addition, risk and cost

control receive unabated attention; the phase-out of the

commercial property portfolio leads to a reduction of staff

and costs. We will be alert to opportunities arising in the

property markets. Opportunities can always be found,

especially for a strong company like ours.

27

Consolidated statement of income

For the year ended 31 December

in thousands of euros 2013 2012

Interest income 775,381 856,323Interest expenses 463,858 553,327Net interest income 311,523 302,996

Project income 1,619,992 1,673,619Project expense 2,125,702 1,632,544Net project income (505,710) 41,075

Fee and commission income 51,126 51,405Fee and commission expense 9,519 9,925 Net fee and commission income 41,607 41,480

Income from associates 4,270 6,129 Results on financial assets and liabilities at fair value 4,290 15,949 Gross margin investment property (100,307) 16,432 Other results 5,791 5,823 Income (238,536) 429,884

Staff costs 197,319 193,499General and administrative expenses 114,177 89,174Depreciation and amortisation 9,897 9,883Operating expenses 321,393 292,556

Value adjustments 568,300 237,509Bank tax 8,100 –Total expenses 897,793 530,065

Operating profit before taxation (1,136,329) (100,181)Taxation 271,626 (8,379) Profit after taxation including non-controlling interests (864,703) (108,560)

Profit attributable to non-controlling interests (6,409) 4,767 Profit attributable to shareholder (858,294) (113,327)

28 Rabo Real Estate Group Annual Summary 2013

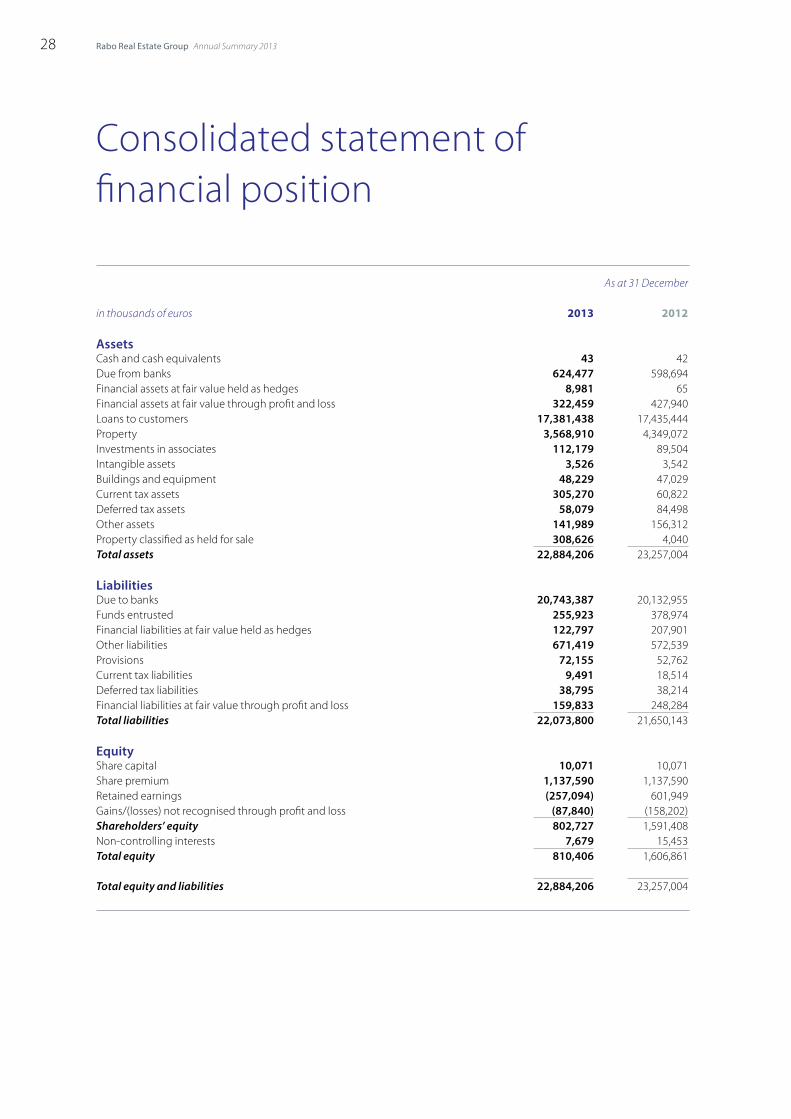

Consolidated statement of financial position

As at 31 December

in thousands of euros 2013 2012

AssetsCash and cash equivalents 43 42Due from banks 624,477 598,694Financial assets at fair value held as hedges 8,981 65Financial assets at fair value through profit and loss 322,459 427,940Loans to customers 17,381,438 17,435,444Property 3,568,910 4,349,072Investments in associates 112,179 89,504Intangible assets 3,526 3,542Buildings and equipment 48,229 47,029Current tax assets 305,270 60,822Deferred tax assets 58,079 84,498Other assets 141,989 156,312Property classified as held for sale 308,626 4,040Total assets 22,884,206 23,257,004

LiabilitiesDue to banks 20,743,387 20,132,955Funds entrusted 255,923 378,974Financial liabilities at fair value held as hedges 122,797 207,901Other liabilities 671,419 572,539Provisions 72,155 52,762Current tax liabilities 9,491 18,514Deferred tax liabilities 38,795 38,214Financial liabilities at fair value through profit and loss 159,833 248,284Total liabilities 22,073,800 21,650,143

Equity Share capital 10,071 10,071Share premium 1,137,590 1,137,590Retained earnings (257,094) 601,949Gains/(losses) not recognised through profit and loss (87,840) (158,202)Shareholders’ equity 802,727 1,591,408Non-controlling interests 7,679 15,453Total equity 810,406 1,606,861

Total equity and liabilities 22,884,206 23,257,004

29

Consolidated statement of cash flows

For the year ended 31 December

in thousands of euros 2013 2012

Cash flows from operating activitiesOperating profit before taxation (1,136,329) (100,181)Adjusted for:Non-cash items recognised through profit and lossDepreciation and amortisation 9,897 9,883Value adjustments 568,810 238,294Impairment/(reversal impairment) property 689,861 194,868Impairment/(reversal impairment) other provisions 31,729 575Income from associates and result from sale of subsidiaries (4,270) (6,129)Unrealised fair value changes in investment property 145,789 20,425Unrealised fair value changes in financial assets and liabilities at fair value through profit and loss

4,290 15,949

309,777 373,684Net change in operating assetsDue from and to banks 619,206 2,314,733Loans to customers (487,571) 147,648Financial assets and liabilities at fair value through profit and loss 12,525 (1,657,059)Property (291,549) 139,948

Net changes in liabilities relating to operating activitiesFunds entrusted (123,050) (591,504)Debt securities – (460,500)Changes to other provisions (22,475) (35,025)Other changes in accrued assets and liabilities 17,410 (34,365)Income tax paid (5,813) (541)Other changes relating to operating activities 15,864 (131,959)Dividends received from associates – 1,673Net cash flow from operating activities 44,324 68,445

Cash flows from investing activitiesAcquisition/sale of companies regarding which control is acquired/relinquished, net of acquired cash

2,947 (11,726)

Acquisition of intangible assets (1,017) (509)Acquisition from purchase and sale of buildings and equipment (11,891) (3,667)Proceeds from sale of buildings and equipment 957 –Net cash flow from investing activities (9,004) (14,190)

Cash flow from financing activitiesDividends non-controlling interests (762) (2,813)Net cash flow from financing activities (762) (2,813)

Net change in cash and cash equivalents 34,558 49,730

Cash and cash equivalents at beginning of year 492,213 442,483Cash and cash equivalents at end of year 526,771 492,213

31

Contact details

Bouwfonds Property Development

Head Office

Westerdorpsstraat 66, 3871 AZ Hoevelaken

PO Box 15, 3870 DA Hoevelaken

T +31 (0)33 253 97 00

www.bouwfonds.com

Bouwfonds Marignan Immobilier

Head Office France

70, rue de Villiers

F-92532 Levallois-Perret Cedex

T +33 (0)1 49 64 15 15

www.bouwfonds-marignan.com

Bouwfonds Immobilienentwicklung

Head Office Germany

Lyoner Strasse 15

D-60528 Frankfurt am Main

T +49 (0)692 197 980

www.bouwfonds-immobilienentwicklung.de

MAB Development Group

Wijnhaven 60, 2511 GA The Hague

PO Box 19412, 2500 CK The Hague

T +31 (0)70 306 84 00

www.mab.com

Public Fund Management

Netherlands

Westerdorpsstraat 68, 3871 AZ Hoevelaken

PO Box 15, 3870 DA Hoevelaken

T +31 (0)33 253 94 28

www.fondsenbeheer.nl

FGH Bank

Head Office

Leidseveer 50, 3511 SB Utrecht

PO Box 2244, 3500 GE Utrecht

T +31 (0)30 232 39 11

www.fghbank.nl

Frankfurt Office

Beethovenstrasse 4

D-60325 Frankfurt am Main

T +49 (0)69 76 75 7950

RNHB Hypotheekbank

Leidseveer 30, 3511 SB Utrecht

PO Box 2244, 3500 GE Utrecht

T +31(0)30 755 20 00

www.rnhb.nl

Bouwfonds Investment

Management Head Office

De Beek 18, 3871 MS Hoevelaken

PO Box 15, 3870 DA Hoevelaken

T +31 (0)33 750 47 50

www.bouwfondsim.com

Bouwfonds Investment

Management Deutschland GmbH

Budapester Strasse 48

D-10787 Berlin

T +49 (0)30 59 00 9760

www.bouwfondsim.com

Bouwfonds Investment

Management France

6, avenue Franklin Roosevelt

F-75008 Paris

T +33 (0)175 579 020

www.bouwfondsim.com

Rabo Real Estate Group

Westerdorpsstraat 66, 3871 AZ Hoevelaken

PO Box 15, 3870 DA Hoevelaken

T +31 (0)33 253 91 11

www.raborealestategroup.com

32 Rabo Real Estate Group Annual Summary 2013

Colophon

Published by

Rabo Real Estate Group

Corporate Communications

Copies of the Annual Summary

may be requested from:

Rabo Real Estate Group

Corporate Communications

Westerdorpsstraat 66

PO Box 15, 3870 DA Hoevelaken

T +31 (0)33 253 91 11

Realisation

Volta_thinks_visual, Utrecht

Photographs

Edwin Walvisch

Publication

This publication forms the Annual Summary

of Rabo Real Estate Group.

The Annual Report is available digitally

and can be downloaded from the Internet:

www.raborealestategroup.com

Publishing

After adoption the 2013 consolidated financial

statements, the Annual Report and the other

information will be filed with the trade register of the

Chamber of Commerce under number 08012222.

JUN

E 2

014