annual results presentation period ended 30 june 2004 · final ordinary 18¢ 13¢ +39% special 10¢...

TRANSCRIPT

Annual Results Presentation Period Ended 30 June 2004Kirby Adams, Managing Director and Chief Executive OfficerBrian Kruger, Chief Financial Officer19 August, 2004

ASX Code: BSL

Page 2

Important Notice

THIS PRESENTATION IS NOT AND DOES NOT FORM PART OF ANY OFFER, INVITATION OR RECOMMENDATION IN RESPECT OF SECURITIES. ANY DECISION TO BUY OR SELL BLUESCOPE STEEL LIMITED SECURITIES OR OTHER PRODUCTS SHOULD BE MADE ONLY AFTER SEEKING APPROPRIATE FINANCIAL ADVICE. RELIANCE SHOULD NOT BE PLACED ON INFORMATION OR OPINIONS CONTAINED IN THIS PRESENTATION AND, SUBJECT ONLY TO ANY LEGAL OBLIGATION TO DO SO, BSL DOES NOT ACCEPT ANY OBLIGATION TO CORRECT OR UPDATE THEM. THIS PRESENTATION DOES NOT TAKE INTO CONSIDERATION THE INVESTMENT OBJECTIVES, FINANCIAL SITUATION OR PARTICULAR NEEDS OF ANY PARTICULAR INVESTOR.

TO THE FULLEST EXTENT PERMITTED BY LAW, BSL AND ITS AFFILIATES AND THEIR RESPECTIVE OFFICERS, DIRECTORS, EMPLOYEES AND AGENTS, ACCEPT NO RESPONSIBILITY FOR ANY INFORMATION PROVIDED IN THIS PRESENTATION, INCLUDING ANY FORWARD LOOKING INFORMATION, AND DISCLAIM ANY LIABILITY WHATSOEVER (INCLUDING FOR NEGLIGENCE) FOR ANY LOSS HOWSOEVER ARISING FROM ANY USE OF THIS PRESENTATION OR RELIANCE ON ANYTHING CONTAINED IN OR OMITTED FROM IT OR OTHERWISE ARISING IN CONNECTION WITH THIS.

Page 3

Rewarding Shareholders Rewarding Shareholders As We GrowAs We Grow

Page 4

Safety –– Our goal remains zero harm

Lost Time Injury Frequency Rate Medically Treated Injury Frequency Rate

35

29

1614

8

4.8 3.7 4 3.4 2.8 1.8 1.3

0

5

10

15

20

25

30

35

40

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

80

68

60

52.247.1

29.122.4 21.9

16.912.2 9.3 6.7

0

10

20

30

40

50

60

70

80

90

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004* Includes contractors from 1996

Injur

ies re

sultin

g in l

ost ti

me pe

r milli

on m

an-h

ours

worke

d

IISI Member Companies (2002) – 8.4Me

dicall

y tre

ated i

njurie

s per

milli

on m

an-h

ours

worke

d

* Includes contractors from 2003

But, we experienced a fatality on 29 June 2004

Page 5

Group headlines FY2004

Continued to seize market opportunities and drive business improvements

• Revenue $5.77 billion Record even with A$ strength

• Despatches 6.94 million metric tonnes Record

• NPAT $584 million Up 29% to record

• EBITDA $1,105 million First time over $1.0 billion

• EBIT $818 million Up 34%

• EPS 77.8¢ Up 36%

• Return on Invested Capital 18.5% Improvement continues

• Net Cash Flow $315 million Even after Butler & growth expenditure

• Debt Increased Up $425 million Reflects Butler acquisition and share buyback

• Gearing (net debt) 12.9% But for buyback and acquisition –would be zero

Page 6

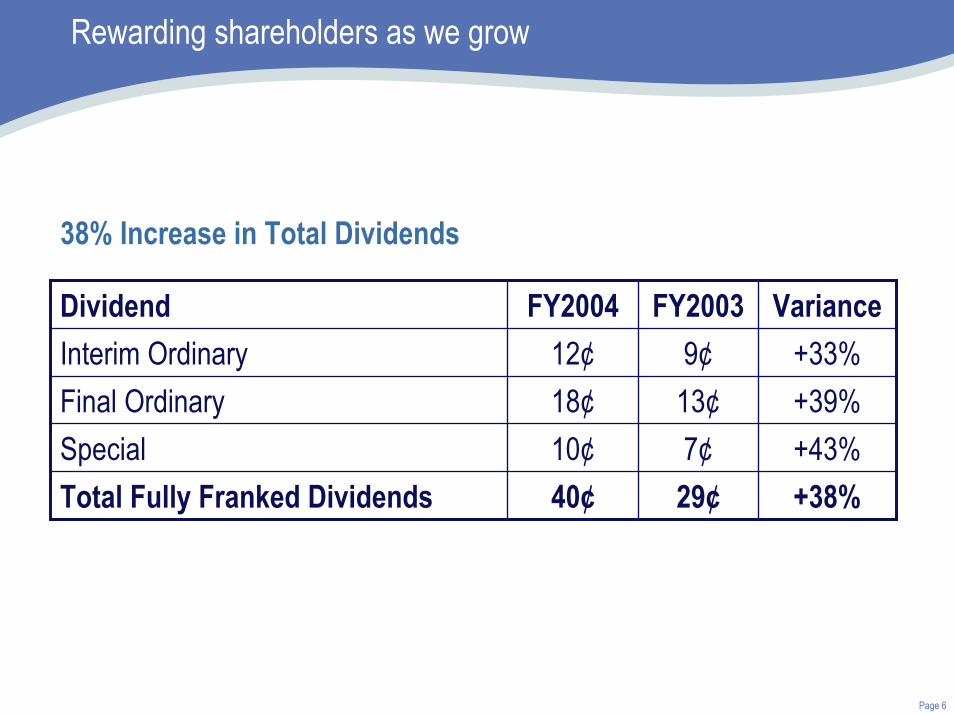

Rewarding shareholders as we grow

+39%13¢18¢Final Ordinary+43%7¢10¢Special

+33%9¢12¢Interim Ordinary

+38%29¢40¢Total Fully Franked Dividends

VarianceFY2003FY2004Dividend

38% Increase in Total Dividends

Page 7

•

Growing for the future benefit of shareholders

Growth initiatives underwayVietnam – new metal coating and paint line facilityThailand – second metal coating facilityChina – new metal coating and paint line facility

– BlueScope / Butler integration North America – Butler acquisition, integration and business transformation

• More recent growth initiativesHot Strip Mill upgrade – Port Kembla SteelworksProgressing West Sydney - Colorbond® steel centre

Page 8

Strong and improved financial performance across all segments

471

44

11984

565

59

197

100

-9

-100

0

100

200

300

400

500

600

Hot RolledProducts

New Zealand Steel Coated & BuildingProducts Australia

Coated & BuildingProducts Asia

Coated & BuildingProducts North

America

FY03 FY04

EBIT

A$ M

illion

s 69

71 North Star BlueScope Steel

• New business segment as at 1 May 2004

• 2 months results, including integration costs

Group EBIT $818m

Page 9

471

565

179

386

0

100

200

300

400

500

600

FY03 FY04 FY04-1H FY04-2H

Hot Rolled Products – hard work is paying off

Performance- Annual production records at PKSW and

North Star BlueScope Steel - Offset by:

stronger AUD/USDiron ore and scrap costsrepair and maintenance spendinghigher employment costs

- Enterprise Bargaining Agreement renewed

Markets- Strong global demand- Tight markets for raw materials

and product - Record prices in second half- Core long term customer relationships

• FY2004 return on net assets (pre-tax) 30.7%

• Revenue = A$2,732m

EBIT

A$ M

illion

s

69

71

2

69

Page 10

New Zealand Steel – its best ever performance

Markets- Strong NZ construction demand- Record domestic sales mix- Higher prices - particularly export- Core long term customer relationships

• FY 2004 return on net assets (pre-tax) 14.1%

• Revenue = A$560m

44

59

20

39

0

10

20

30

40

50

60

70

FY03 FY04 FY04-1H FY04-2H

EBIT

A$ M

illion

s

Performance- Record EBIT- Annual paint line production record- Metal coating expansion completed with

full benefit to be achieved in 2005- Best ever safety outcomes

Page 11

Coated & Building Products Australia – “Oh What A Feeling!”

• FY2004 return on net assets (pre-tax) 16.0%

• Revenue = A$2,884m

Performance- Annual production records- Feed costs higher in second half = margin squeeze- Low cost capacity improvements continue- Western Port

maintenance alliance operationalbest ever delivery performance

- Springhillproduction and efficiency improvements

- Customer survey affirms improved serviceToyota President’s Award

- Packaging business margin pressure

Markets- Demand never been stronger

construction, automotive, manufacturing- Signs of dwelling market slowing- Industrial/commercial remains buoyant- Price increases implemented- Strengthened channels to market

119

197

102 95

0

50

100

150

200

FY03 FY04 FY04-1H FY04-2H

EBIT

A$ M

illion

s

Page 12

Coated and Building Products Asia – the growth continues

Performance- All plants operating near full capacity- Strong volume growth of 35%- Achieved A$100m EBIT- Leading safety performance- Major capital projects developed, approved and

underway- Excellent EBIT performance in local currencies

Markets- World’s fastest growing steel market - BlueScope Steel uniquely positioned- Prices higher in local currencies- Pre-engineered building demand growing in

Asia – immediate scale achieved in China through Butler acquisition

- BlueScope Steel’s branded products increasing presence and growing reputation

84

100

4555

0

20

40

60

80

100

120

FY03 FY04 FY04-1H FY04-2H

EBIT

A$ M

illion

s

• FY2004 return on net assets (pre-tax) 21.5%

• Revenue = A$689m

Page 13

Index of EBIT performance of Asian businesses in local currencies

0

100

200

300

400

2001 2002 2003 2004

Thailand Malaysia Indonesia China

Page 14

Coated and Building Products North America – foundations in place

• Butler Manufacturing Co. acquisition completed 27 April 2004- No negative surprises- Integration team making good progress- New management structure in place- Galesburg facility to close mid-CY2005- Timber business (Lester) sold in July 2004

• Continued improvement in non-residential buildings construction in U.S.- Butler Buildings order backlog up- Vistawall despatches stronger

• Challenges - Rapid steel price increases, higher aluminium costs- Limited steel availability

………………………………………………………………………………………………..

• On target to achieve consolidated financial goals stated at acquisition- FY05 EPS neutral- FY06 EPS positive

Page 15

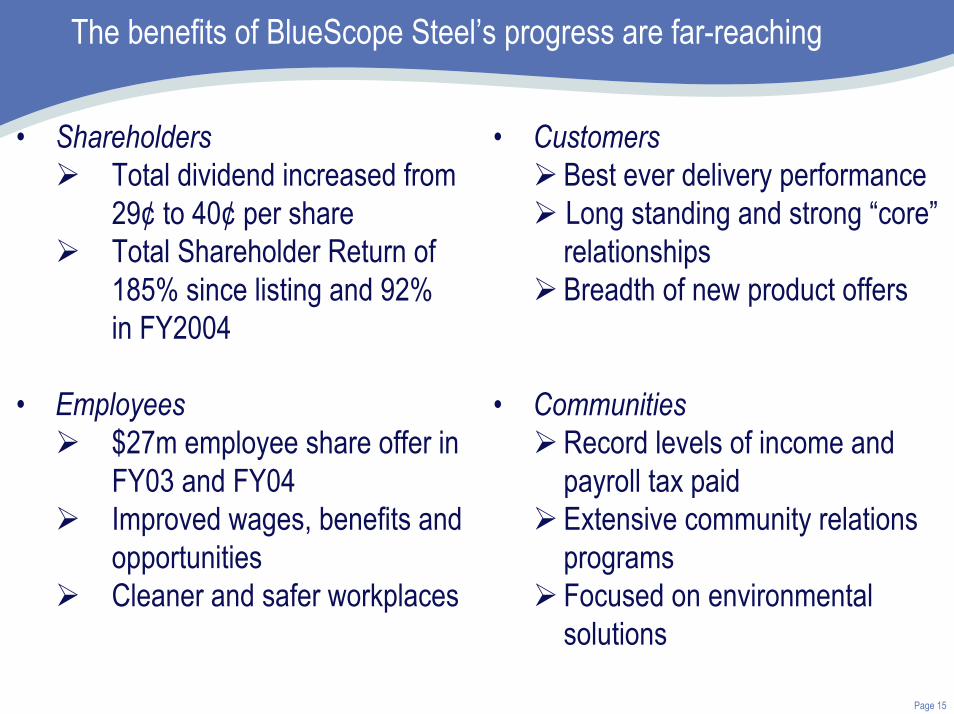

The benefits of BlueScope Steel’s progress are far-reaching

• ShareholdersTotal dividend increased from 29¢ to 40¢ per shareTotal Shareholder Return of 185% since listing and 92% in FY2004

• Employees$27m employee share offer in FY03 and FY04 Improved wages, benefits and opportunities Cleaner and safer workplaces

• CustomersBest ever delivery performanceLong standing and strong “core”relationshipsBreadth of new product offers

• CommunitiesRecord levels of income and payroll tax paidExtensive community relations programsFocused on environmental solutions

Page 16

FinancialsFinancials

Page 17

Continued strong earnings performance

A$ Millions 2000(1) 2001(1) 2002(1) 2003 2004(3) 2004-1H 2004-2H(3)

Revenue 4,898 4,941 4,593 5,302 5,770 2,619 3,151

EBITDA(2) 711 568 412 881 1,105 440 665

EBIT(2) 445 305 160 611 818 302 516

Net Profit 452 584 227 357

EPS (¢)(4) 57.1 77.8 (1) 2000 to and including 2002 normalised.(2) Includes profit/loss for North Star BlueScope Steel.(3) Includes two months of BlueScope Butler financial results.(4) Weighted average shares on issue 791.5m FY03 and 750.5m FY04.

Page 18

EBIT variance – FY2004 vs. FY2003

100

300

500

700

900

1100

June 03YTD Actual

ExportPrices

DomesticPrices

Volume /Mix

NSBSL ExchangeRates

Conversion& OtherCosts

RawMaterialCosts

Other June 04YTD Actual

EBIT A$m

$611m

$300m

$818m

($130m)

$79m

$70m($85m)

($111m)

$2m

$82m

Higher R&M (42)Employment costs (42)Freight (18)Cost improvements 68

FY03 Superannuation Contribution 32FY03 Name ChangeProvision 20Lower Restructuring Costs 31

Page 19

EBIT variance – June 04 half year vs. December 03 half year

0

100

200

300

400

500

600

700

800

Dec 03 Half Export Prices DomesticPrices

Volume / Mix NSBSL ExchangeRates

Conversion &Other Costs

Raw MaterialCosts

Other June 04 Half

EBIT A$m

$302m

$223m $516m

($55m)

$10m$21m

($74m)

($10m)

$68m

$31m

Page 20

Balance Sheet – strength and flexibility

A s A t E x c lu d in g F Y 0 4 a c q u is it io n s

A $ M ill io n s 3 0 J u n e 2 0 0 3 3 0 J u n e 2 0 0 4 3 0 J u n e

2 0 0 4 A s s e ts C a s h 9 1 1 1 9 9 1 R e c e iv a b le s 6 5 0 9 9 6 7 8 5 In v e n to ry 6 9 8 9 6 2 7 6 2 O th e r A s s e ts 2 2 8 4 1 6 3 2 5 N e t F ix e d A s s e ts 3 ,0 8 6 3 ,2 8 9 3 ,0 9 0

T o ta l A s s e ts 4 ,7 5 3 5 ,7 8 2 5 ,0 5 3

L ia b il it ie s C re d ito rs 4 9 3 7 2 8 5 6 8 In te re s t B e a r in g L ia b il i t ie s 1 6 8 5 9 3 1 9 7 P ro v is io n s 1 ,0 0 1 1 ,2 6 7 1 ,0 9 4 T o ta l L ia b il it ie s 1 ,6 6 2 2 ,5 8 8 1 ,8 5 9

N e t A s s e ts 3 ,0 9 1 3 ,1 9 4 3 ,1 9 4

• Net Debt / (Net Debt + Equity) 2.4% 12.9%(excluding off balance sheet items)

Page 21

Major growth initiatives – capital spending profile

114

-

53

45

1

15

FY2006

13

-

13

-

-

-

FY2007

405365897Total(3)

-277277Butler acquisition

34-100Port Kembla HSM expansion(1)

21124280China(1)

601980Thailand(1)

10045160Vietnam(1)

FY2005FY2004 Actual

Total Est. Capex/Cost

All in A$m

(1) Estimated capital costs based on forecast exchange rate assumptions.

(2) Butler acquisition cost less cash acquired and not including the benefit of Louisiana Pacific Corporation settlement proceeds received of US$21m.

(3) Addition of smaller capital spending programmes bringing total approved CAPEX to over A$1 billion.

Page 22

Capital management - continued focus on returns to shareholders

• Share Buyback- Purchased/cancelled 60.7m shares- Further program – 16.0m shares

• Dividends - All Fully Franked

913 12

18

7

10

0

5

10

15

20

25

30

FY2003-1H FY2003-2H FY2004-1H FY2004-2H

SpecialOrdinary

¢

¢¢

Cent

s Per

Sha

re

Total return to shareholders since public listing:

• Initial buyback $286m• Dividends Paid $313m• Final/Special

(to be paid) $208m$807m

¢

29¢

40¢

¢

¢

Page 23

Consistently strong cash flows

A$ millions 2000(1) 2001(1) 2002(1) 2003 2004 2004-1H 2004-2H Net operating cash flow before borrowing costs and income tax

715 631 381 763 893 357 536

Net investing cash flows - Capital expenditure - Other

(90) 10

(105)

(6)

(162)

8

(183)

18

(290) (288)

(99) (3)

(191) (285)

Net cash flow before financing & tax

635 520 227 598 315 255 60

Net financing cash flow (493) 75 (8) 83 Payment of income tax (29) (119) (84) (35) Net dividends (75) (244) (155) (89) Net increase in cash held 1 27 8 19

(1) 2000 to and including 2002 normalised.

Page 24

Results remain sensitive to BlueScope Steel’s realised hot rolled coil prices

(1) The change in export HRC price assumes proportional effect on export slab, and flow on to domestic pipe and tube market and to other export products.

(2) The movement in the Australian dollar/US dollar exchange rate includes the restatement of US dollar denominated receivables and payables.

Estimated impact on forecast

EBIT (A$mil) for year ending 30/06/05

Assumption +/– US$25 / tonne movement in BSL’s average realised HRC price(1) 75 +/– 1¢ movement in Australian dollar / US dollar exchange rate(2) 13 +/– US$10 / tonne movement in NSBHP scrap to HRC price spread 12 +/– 2% movement in slab production in Australia and New Zealand 24 +/– US$1 / tonne movement in coking coal costs 5 +/– US$1 / tonne movement in iron ore costs 10

Page 25

Looking forward to 2005

• Global steel industry

• Higher costs

• BlueScope Steel strategy

• Outlook for BlueScope Steel

Page 26

North AmericaNorth America• Record HRC prices• Scrap surcharges and

volatility• Steel availability• Consolidation continues• Economic recovery

Global steel industry - dynamic

IndiaIndia• Increasing steel capacity• Growing GDP demand

South AmericaSouth America• Plans for new capacity• Raw material rich• Low cost

EuropeEurope• Weak demand continues• Consolidation benefits

CISCIS• Restricted scrap exports• Stronger economies

JapanJapan• Production at capacity• Significant exports

ChinaChina• World’s largest steel consumer

and producer• Less than 5% of BlueScope

Steel sales• Indirect impact significant• Net importer of flat steel• Slowdown welcome• Raw material / shipping effect

Australia / New ZealandAustralia / New Zealand• Strong economic growth• Interest rates?

KoreaKorea• Shipyards full• BlueScope Steel customer

SE AsiaSE Asia• Improved economic growth• Volatile tariff structures

Page 27

Steel making raw material costs are increasing

0

1,000

2,000

3,000

4,000

5,000

6,000

Nov-9

9

May-0

0

Nov-0

0

May-0

1

Nov-0

1

May-0

2

Nov-0

2

May-0

3

Nov-0

3

May-0

4

BDI Index

ShippingIron Ore Coal

“…unprecedented demand and extremely tight supply position…”

“…China reducing exports…” “…2-3 Year backlog for shipbuilders…”

BDI – Baltic Dry IndexIron Ore and Coal – Aus-Japan Reference PricesSource: IISI, Baltic Dry Index, SSY

SOURCE: ANZ Bank ‘Resources Market Outlook’, Mar 04

Page 28

Other metallic coating material costs also increasing

1,000

1,200

1,400

1,600

1,800

2,000

Jun-98

Apr-99

Feb-00

Dec-00

Oct-01Aug-

02Jun

-03Apr-0

4

US $

/TON

NE

500

700

900

1,100

1,300

1,500

Jun-98

Apr-99

Feb-00

Dec-00

Oct-01

Aug-02

Jun-03

Apr-04

US $

/TON

NE

3,000

5,000

7,000

9,000

Jun-98

Apr-99

Feb-00

Dec-00

Oct-01

Aug-02

Jun-03

Apr-04

US $

/TON

NE

`

TinAluminium Zinc

“Chinese and world demand outpacing supply. Concentrate inventories depleted.”

“Chinese demand is still growing. Potential for further price rises.”

“Chinese demand has driven 25-30% price rise since 2001. Recent Chinese Government actions caused minor price fall . . . which may be only temporary.”

Source: London Metal Exchange (LME)

Page 29

Marine freight – well managed to minimise costs

• Global marine freight market continues to be tight

• BlueScope Steel’s approach- stagger renewals- long term relationships- limited “spot” contracts

• BlueScope Steel largely insulated in FY2004

• In FY2005:- Approximately half of our marine freight cost is exposed

to higher costs . . . totalling a net A$70m or approximately 10% of our total transportation spend

Page 30

Our strategy is unchanged

• Asia and Regional Growth

• Value-added branded products

• Asset productivity

• Disciplined capital management

• World-class low-cost operations

• Manufacturing excellence

• Supply chain velocity

• Cost reductions

• Vigorously defend existing value

Cold Rolled

Painted

Roll-forming

Metallic Coated

Vietnam

Australia & NZ Brownfields

Australia & NZ Brownfields

China

Vietnam

Thailand China

Water

ButlerPEB/Solutions

Hot Rolled Coil, Plate

Slab

HSM Expansion

Page 31

2004 was another good year . . . and the momentum continues

• Anticipate another good year in 2005

• Challenges ahead- much higher slab / HRC prices in first half leading to further

margin pressure downstream- adjusting to higher raw material and freight cost environment - achieving productivity to offset higher wage / employment costs

• Opportunities ahead- Butler turnaround and PEB growth- safe and successful project construction- new products and markets - choosing amongst myriad of growth opportunities- further execution of our strategy

• Seize benefits of our diversified product and geographic portfolio

• Continue to reward our shareholders as we grow

Annual Results Presentation Period Ended 30 June 2004Kirby Adams, Managing Director and Chief Executive OfficerBrian Kruger, Chief Financial Officer19 August, 2004

ASX Code: BSL

Page 33

Creating shareholder value as we grow

Challenging Global Steel

Market

Challenging Global Steel

Market

Profitable Through the

Cycle

Profitable Through the

Cycle

Geographic and Product

Diversity

Geographic and Product

Diversity

Strong and Flexible Capital

Structure

Strong and Flexible Capital

Structure

Consistently Strong Cash

Flows

Consistently Strong Cash

Flows

Strong Board & Management

Team

Strong Board & Management

Team

Value Added Branded Products

Value Added Branded Products

Growth Opportunities in

Asia

Growth Opportunities in

Asia

Low Cost Producer

Low Cost Producer

Strong Operating

Track Record

Strong Operating

Track Record

A VERY DIFFERENT KIND OF STEEL

COMPANY