annual report malmÖ snapshot · news at the beginning of the summer. the accreditation is a public...

TRANSCRIPT

MALMÖ SNAPSHOTFACTS AND FIGURES ON TRADE AND INDUSTRY IN MALMÖ

ANNUAL REPORT

A SUMMARY FROM THE CITY OFFICE, CITY OF MALMÖ, 2016

DID YOU KNOW THAT...

... 3.9 million people live in the Öresund region?

... 8 new companies were started every day in Malmö in 2015?

... there has never been such a large workforce in Malmö as now?

Page6

Page18

Page20

On 1 January 2018, Malmö University is expected to be granted full university status. We received this wonderful news at the beginning of the summer. The accreditation is a public acknowledgment of the importance of Malmö University in the development of Malmö. The university has been an important piece in the puzzle that is Malmö’s transi-tion from the past to the present and especially the future!

In addition to Malmö University, the city is also home to the higher education institutions World Maritime Univer-sity, Malmö Art Academy, Malmö Academy of Music and Malmö Theatre Academy. And looking slightly further afield, we have Lund University and the universities in Copenhagen and Roskilde. It is important to have access to high-quality higher education. Higher education is re-quired to meet demand for expertise from both trade and industry and the public sector.

Our labour market is constantly growing. On average, 123 new job vacancies per day are added in Malmö, ac-cording to the Swedish Public Employment Service. And the jobs market is likely to remain at this level for quite a while in the future. The fastest growing sectors are services such as restaurants and commerce. Demand for engineers within different areas of specialisation remains high.

At the time of writing, border controls are creating uncertainty for the thousands of people commuting across the bridge. The situation is severely hampering the develop-

ment of a common labour market in the Öresund region. A region whose population is expected to pass the four million mark next year. A region with more than a quarter of a million companies!

The workforce in Malmö is 165,000 strong. The workforce has grown by more than 40% in the last twenty years and the number of people living in Malmö is expected to reach 375,000 in ten years’ time.

This is why we are constantly striving to be a city that is at the forefront of development. A modern city where we want to live, spend time in and work.

MALMÖ LIVE - A CONFERENCE CENTRE, CONCERT HALL AND HOTEL THAT OPENED IN 2015. AWARDED THE NATIONAL BUILDING PROJECT AWARD “ÅRETS BYGGE” IN 2016.

A SNAPSHOT OF MALMÖ

PEHR ANDERSSON DIRECTOR, TRADE AND INDUSTRY AGENCY, CITY OF MALMÖ

A DIGITAL COPY OF MALMÖ SNAPSHOT CAN BE FOUND AT WWW.MALMOBUSINESS.COM

MALMÖ SNAPSHOT IS ALSO AVAILABLE IN SWEDISH

PLEASE FEEL FREE TO USE THE PUBLICITY MATERIAL ON MALMOBUSINESS.COM/MALMOLAGET

04 REGION 10 POPULATION14 PROFILE AREAS16 GROWTH20 WORKFORCE26 CORPORATE STRUCTURE

04

Malmö is attracting a lot of interest and the city is buzzing with activity. Many players see Malmö’s potential and want to be involved and invest in Malmö’s future.

PLANNED AND ONGOING PROJECTS INCLUDE:

— STUDIO (on Universitetsholmen)

— Culture Casbah (1)

— Malmö Industrial Park in Norra hamnen (Northern Harbour)

— Marine Education Centre (2)

— Malmö Saluhall indoor food market

— Malmöringen suburban rail service and the station at Rosengård

— Sports and rock climbing centre

— Development of Skåne University Hospital (SUS)

— New residential district in Limhamn

— Expansion of the Norra Sorgenfri district

— Continued expansion of Västra Hamnen (Western Harbour)

— Continued expansion of the Hyllie district (3)

TWO NEW IMPORTANT RESEARCH FACILITIES ARE UNDERWAYThey are being built in Lund, 20 km north of Malmö. In addition to exciting new research opportunities, the facilities will generate further job opportunities and more growth in the region.

MAX IV – is a synchrotron radiation laboratory. 2,000 researchers from around the world are expected to use the facility each year. The facility opened its doors in summer 2016. (4)

The ESS (European Spallation Source) – will be the world’s foremost material research facility using neutrons. It is anticipated that it will welcome 3,000 guest researchers per year and employ around 450 staff. It is due to open in 2023.

A TUNNEL BETWEEN DENMARK AND GERMANYThe Fehmarn belt tunnel will be constructed between Denmark and Germany and it is estimated that it will be completed in 2028. The tunnel will link Scandinavia with the continent and will reduce travel times considerably. The tunnel is also expected to have a positive impact on

1

2

3

4

05

both transport costs and the environment. The Öresund Bridge has played an important role in integration and growth in the Öresund region and it is forecast that the tunnel will have a similar significance for a competitive new, extended economic region.

METRO BETWEEN MALMÖ AND COPENHAGEN?Via a tunnel under the Öresund strait, the metro trip will take around 20 minutes. A metro would relieve the Öresund Bridge, which is expected to receive increased goods traffic when the fixed link between Denmark and Germany is completed. Space is also required for new, high-speed trains. The metro is also expected to help to increase everyday inte-gration across the water between the city centres in Malmö and Copenhagen.

Copenhagen Municipality and the City of Malmö are work-ing on phase 3 of the study, which has received EU funding. The project includes closer studies of appropriate tunnel designs and construction techniques, taking into account strict environmental requirements concerning Öresund strait, for instance. There are many factors in favour of a bored, twin-track tunnel. It is anticipated that Phase 3 will be completed in spring 2017. If the project gets the go-ahead, the metro could start operating around 2030-2035.

SEVERAL MAJOR INVESTMENTS HAVE BEEN COM-PLETED IN MALMÖ IN RECENT YEARS, INCLUDING:

— Malmö Live (conference centre, concert hall and hotel)

— The City Tunnel, including two new stations and expan-sion of Malmö C, as well as the Glasvasen office block (5)

— Expansion of the University (Niagara district)

— Hylliebadet swimming pool

— Malmö Arena

— Swedbank Stadium (6)

— Emporia shopping centre (7)

— Malmömässan – new exhibition centre in Hyllie

— Expansion of the Norra Hamnen (Northern Harbour) district

— IKEA – new offices for global staff functions and training centre

— Media Evolution City

— Entré shopping centre

— Legal Centre

— Redevelopment and extension of several shopping centres – Triangeln, Mobilia and Caroli (8)

— Several new hotels

5

6

7

8

06

MALMÖ

SWEDEN

DENMARK

COPENHAGEN

THE ÖRESUND REGION

— The Öresund region comprises Skåne in Sweden and Zealand, Møn, Lolland-Falster and Bornholm in Denmark

— 3.9 million inhabitants (1.3 million on the Swedish side and 2.6 million on the Danish side)

— 25% of the total population of Sweden and Denmark live in the Öresund region

— The largest Nordic regional labour market, with 1.9 mil-lion people

— The region represents 26% of the countries’ total GNP

— Around 250,000 companies (2010)

— Around 145,000 students and 8,000 researchers at the region’s 14 colleges and universities

— In 2017, the population is expected to exceed 4 million people

The Öresund region is the largest and most densely populated metropolitan area in the Nordic countries. The Öresund region covers parts of two countries, Sweden and Denmark, and travel between the two is simple via the Öresund Bridge, which was opened on 1 July 2000. The 16-kilometre link runs between Malmö and Copenhagen.

THE ÖRESUND REGION IS GROWING INTO A MAJOR ECONOMIC REGIONWhen the Fehmarn belt tunnel, a fixed link between Den-mark and Germany, is completed in 2028, it will open the way for a competitive extended region. Travel and transport times will reduce significantly and positive effects are expected in terms of integration, growth, number of jobs, tourism, research and culture.

MALMÖ CENTRAL STATION

TRIANGELN STATION

SVÅGERTORP STATION

HYLLIE STATION

OUTER RING ROAD

INNER RING ROAD

ÖRESUND BRIDGE, COPENHAGEN INTERNATIONAL AIRPORT

MALMÖ AIRPORT (STURUP)

PORT OF MALMÖ

07

GOOD INFRASTRUCTURE

— Copenhagen International Airport (Kastrup) is easily ac-cessible by car or rail. The rail trip takes 21 minutes from Malmö Central Station

— Trains from Malmö, to Copenhagen Airport and to the city centre, depart every 10 minutes during rush hour. At other times, trains depart every 20 minutes

— Malmö Airport is located 30 km to the east of the city. An airport bus is available, which takes 40 minutes

— Malmö is home to one of Sweden’s largest cargo ports. The port is a combined goods and passenger harbour. A comprehensive expansion project has recently been car-ried out with new areas, terminals and a logistics centre.

— Since it opened in 2010, the new City Tunnel has given Malmö an even better infrastructure and two new sta-tions. Commuting times for a number of routes were shortened and ease of movement in the region was increased still further.

— The city has two ring roads (Outer and Inner Ring Road), which facilitate efficient logistics.

— The proximity to a well-developed road and rail network makes it easy to transport goods and people, both within Sweden and to Scandinavia and Europe

THE NATIONAL NEGOTIATION ON HOUSING AND INFRASTRUCTUREThe mandate of the National Negotiation on Housing and Infrastructure - one of the largest infrastructure investments ever seen in Sweden - is to develop new high-speed rail-ways between Stockholm and Gothenburg and Stockholm and Malmö, resulting in travel times of 2 and 2.5 hours respectively, as well as to facilitate improved accessibility and increased housing construction through improved public transport in the major cities in Sweden. The aim is for the project to be completed in 2035. Improved accessibility and capacity in and between the major cities in Sweden will offer both Malmö and the region a lot of potential to achieve sustainable growth and increased housing construction, and will benefit the labour market, the economy and the environment. Negotiations commenced at the beginning of 2016.

TRAVEL TIMES BY TRAINLund 10 minGothenburg 3 hStockholm 4 h 20 minCopenhagen 30 minHamburg 5 h 30 min

TRAVEL TIME BY AIRStockholm 1 hOslo 1 h 5 minBerlin 1 h 15 minAmsterdam 1 h 25 minBrussels 1 h 50 min

08

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1995 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

STUDERANDE MED TÅG

ARBETSPENDLARE MED TÅG

PENDLARE MED FLYGBÅT

ARBETSPENDLARE MED BIL

— 15,700 people commuted daily by train or car across the Öresund Bridge (2015)

— An increase of 4% compared with the previous year, a decrease of 3% over five years and an increase of 92% over ten years. Commuting is on the rise again after hav-ing shown a decrease for a couple of years

— 64% commuted by train and 36% by car. In recent years, the proportion of rail commuters has been growing

— 93% commuted to work and 7% to study

— The majority commuted from Sweden to Denmark – 96% live in Skåne (both Swedes, Danes and other nationalities)

— Many Danes have settled in Malmö because of the differ-ence in house prices between the countries, and a large number of Swedes work in Copenhagen, although this trend has tailed off in recent years

— Around 8,000 people commuted from Malmö to Denmark to work (2015)

COMMUTING OVER THE ÖRESUND BRIDGE

15,700 PEOPLE COMMUTED DAILY BY TRAIN OR CAR ACROSS THE

ÖRESUND BRIDGE IN 2015

TRAFFIC OVER THE ÖRESUND BRIDGE — Around 75,000 people cross the bridge every day

— 19,300 vehicles per day crossed the bridge. (In 2015, a total of 7,047,894 vehicles, i.e. cars, trucks, buses, etc. crossed the bridge)

— Traffic increased progressively until 2009 and is now at a level just below that. In 2014 and 2015, traffic over the bridge started to rise again. Traffic across the Öresund bridge is expected to show stable growth in coming years

COMMUTING OVER THE ÖRESUND BRIDGE

STUDENTS BY TRAIN

COMMUTERS BY TRAIN

COMMUTERS BY HYDROFOIL

COMMUTERS BY CAR

7%

93%

STUDERAR

ARBETAR

36%

64%

BIL

TÅG

STUDY

TRAIN

WORK

CAR

09

— Malmö is located in a mobile region where every-thing is nearby. Distances are short and it is easy to move about

— 63,279 people commuted to Malmö from other municipalities in Sweden (domestic inbound com-muting 2014)

— 32,027 people commuted to other municipali-ties in Sweden from Malmö (domestic outbound commuting 2014)

— For several years, commuting has increased in both directions and has contributed to a mobile region

— Transport services in the region are good. In December 2010, the City Tunnel in Malmö was in-augurated, further improving commuting options

— Large local labour markets contribute to increased flexibility, benefiting both companies and citizens. Companies have better opportunities to find the right expertise and the individual citizen has a wider choice in the labour market

DOMESTIC COMMUTING

COMMUTING TO MALMÖCOMMUTING FROM MALMÖ

-40,000 -30,000 -20,000 -10,000 0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

COMMUTING TO/FROM MALMÖ (ACROSS MUNICIPAL BOUNDARIES IN SWEDEN)

4343% OF COMMUTERS INTO

MALMÖ ARE WOMEN

57

57% OF COMMUTERS INTO MALMÖ ARE MEN

44% OF COMMUTERS FROM MALMÖ ARE WOMEN 56% OF COMMUTERS FROM MALMÖ ARE MEN

10

POPULATION

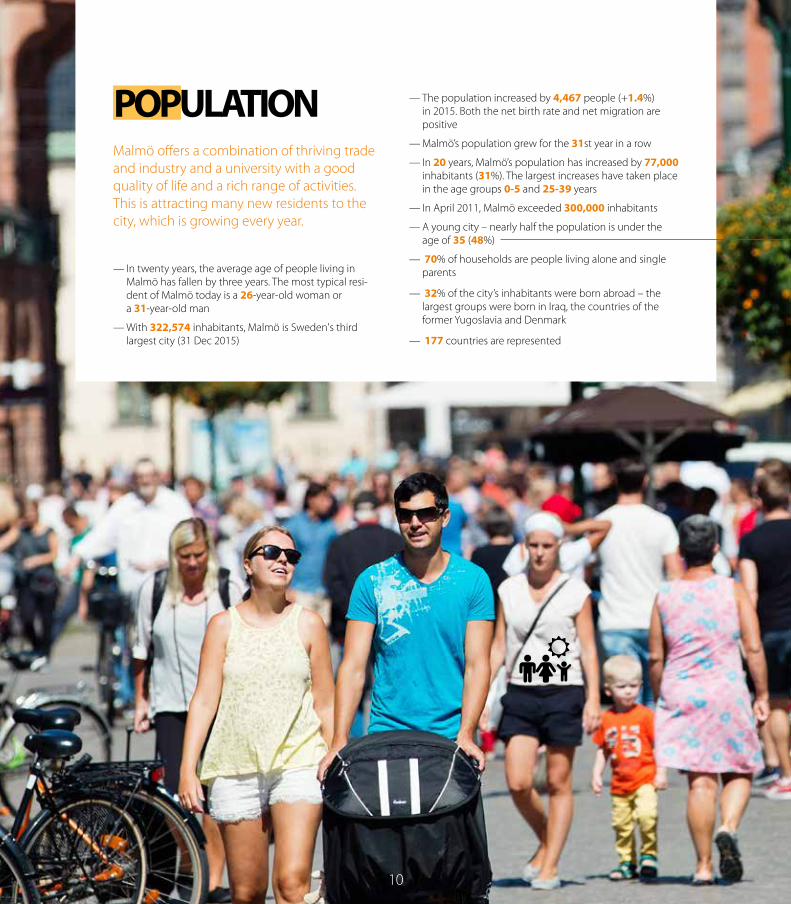

— In twenty years, the average age of people living in Malmö has fallen by three years. The most typical resi-dent of Malmö today is a 26-year-old woman or a 31-year-old man

— With 322,574 inhabitants, Malmö is Sweden's third largest city (31 Dec 2015)

— The population increased by 4,467 people (+1.4%) in 2015. Both the net birth rate and net migration are positive

— Malmö’s population grew for the 31st year in a row

— In 20 years, Malmö’s population has increased by 77,000 inhabitants (31%). The largest increases have taken place in the age groups 0-5 and 25-39 years

— In April 2011, Malmö exceeded 300,000 inhabitants

— A young city – nearly half the population is under the age of 35 (48%)

— 70% of households are people living alone and single parents

— 32% of the city’s inhabitants were born abroad – the largest groups were born in Iraq, the countries of the former Yugoslavia and Denmark

— 177 countries are represented

Malmö offers a combination of thriving trade and industry and a university with a good quality of life and a rich range of activities. This is attracting many new residents to the city, which is growing every year.

11

200

220

240

260

280

300

320

340

360

380

400

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

0

5

10

15

20

25

30

0-9 10-19 20-29 30-39 40-49 50-59 60-69 70-79 80-89 90+

POPULATION BY AGE GROUP AND SEX (2015), THOUSANDS WOMEN MEN

THE MOST TYPICAL RESIDENT OF MALMÖ TODAY IS A

26-YEAR-OLD WOMAN OR A 31-YEAR-OLD MAN

1% 13%

0-9

9%

10-19

17%

20-29

17%

30-39

13%

40-49

11%

50-59

9%

60-69

6%

70-79

4%

80-89 90+

PERCENTAGE AGE DISTRIBUTION

AGE

IN 2025, THE POPULATION OF MALMÖ IS EXPECTED TO EXCEED 375,000

MALMÖ'S POPULATION IN 1968-2015 AND PROJECTION UNTIL 2025, THOUSANDS

322,574 PEOPLE AS AT 31 DECEMBER 2015

12

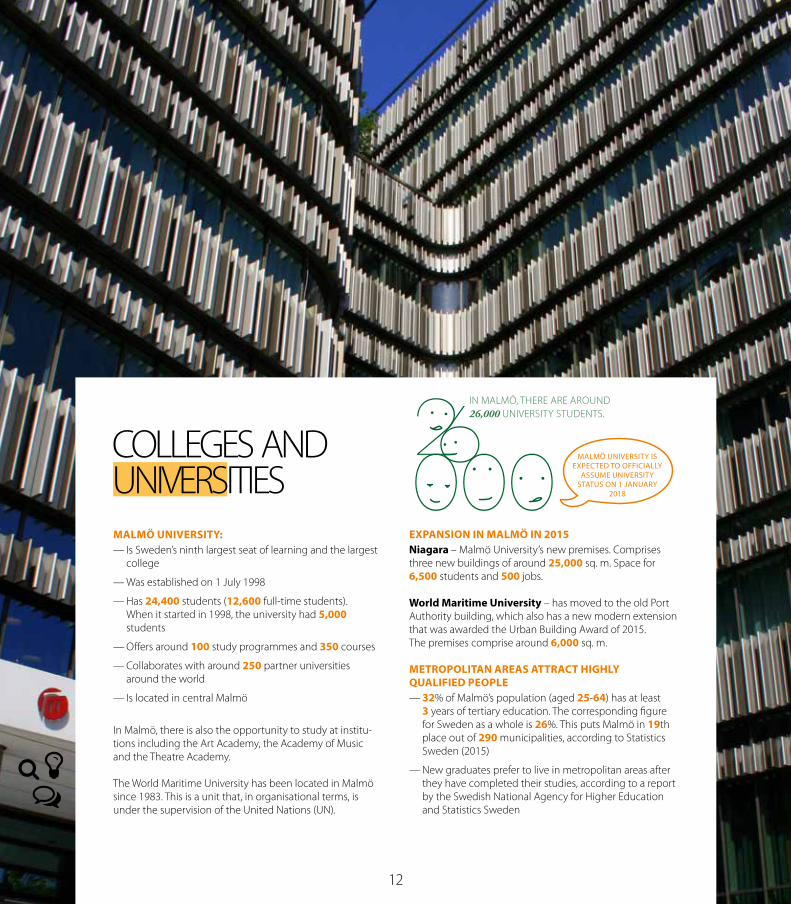

COLLEGES AND UNIVERSITIESMALMÖ UNIVERSITY:

— Is Sweden’s ninth largest seat of learning and the largest college

— Was established on 1 July 1998

— Has 24,400 students (12,600 full-time students). When it started in 1998, the university had 5,000 students

— Offers around 100 study programmes and 350 courses

— Collaborates with around 250 partner universities around the world

— Is located in central Malmö

In Malmö, there is also the opportunity to study at institu-tions including the Art Academy, the Academy of Music and the Theatre Academy.

The World Maritime University has been located in Malmö since 1983. This is a unit that, in organisational terms, is under the supervision of the United Nations (UN).

EXPANSION IN MALMÖ IN 2015Niagara – Malmö University’s new premises. Comprises three new buildings of around 25,000 sq. m. Space for 6,500 students and 500 jobs.

World Maritime University – has moved to the old Port Authority building, which also has a new modern extension that was awarded the Urban Building Award of 2015. The premises comprise around 6,000 sq. m.

METROPOLITAN AREAS ATTRACT HIGHLY QUALIFIED PEOPLE

— 32% of Malmö’s population (aged 25-64) has at least 3 years of tertiary education. The corresponding figure for Sweden as a whole is 26%. This puts Malmö in 19th place out of 290 municipalities, according to Statistics Sweden (2015)

— New graduates prefer to live in metropolitan areas after they have completed their studies, according to a report by the Swedish National Agency for Higher Education and Statistics Sweden

IN MALMÖ, THERE ARE AROUND 26,000 UNIVERSITY STUDENTS.

MALMÖ UNIVERSITY IS EXPECTED TO OFFICIALLY

ASSUME UNIVERSITY STATUS ON 1 JANUARY

2018

13

REGIONAL ACCOUNTS

0

100

200

300

400

500

600

700

800

900

1993

19

94

1995

19

96

1997

19

98

1999

20

00

2001

20

02

2003

20

04

2005

20

06

2007

20

08

2009

20

10

2011

2012

20

13

2014

Prel

Stockholm Malmö Göteborg Skåne Riket

GROSS REGIONAL PRODUCT (GRP) PER CAPITA, CURRENT PRICES, SEK THOUSANDNEW DEFINITION SINCE 2012, WHICH INCLUDES R&D COSTS

DISPOSABLE INCOME PER CAPITA, CURRENT PRICES, SEK THOUSANDNEW DEFINITION SINCE 2012, WHICH ONLY INCLUDES HOUSEHOLDS (NON-PROFIT INSTITUTIONS SERVINGS HOUSEHOLDS ARE NO LONGER INCLUDED).

GROSS REGIONAL PRODUCT (GRP) IN MALMÖ BY INDUSTRY, SEK MILLIONNEW DEFINITION SINCE 2012, WHICH INCLUDES R&D COSTS

WAGES BY INDUSTRY IN MALMÖ, CURRENT PRICES, SEK MILLIONNEW DEFINITION SINCE 2012, WHICH INCLUDES R&D COSTS

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Marknadsproduktion, varor (SNI A01-F43) Marknadsproduktion, tjänster (SNI G45-T98) O�entl. Myndigh. samt hushållens icke-vinstdrivande org. (HIO) Ej branschfördelade poster

60

80

100

120

140

160

180

200

220

240

260

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Stockholm Malmö Göteborg Riket

Skåne

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Marknadsproducenter, varor (SNI A01-F43) Marknadsproducenter, tjänster (SNI G45-T98) O�entl. myndigh. samt hushållens icke-vinstdrivande org. (HIO)

SOURCE: SNI 2007

FROM 2009

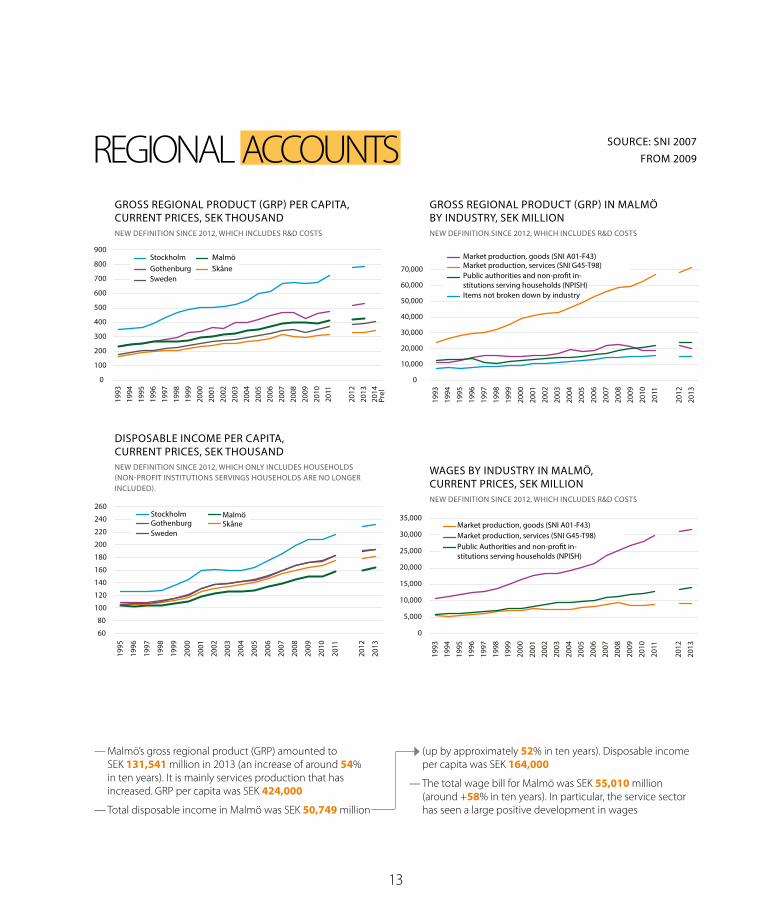

— Malmö’s gross regional product (GRP) amounted to SEK 131,541 million in 2013 (an increase of around 54% in ten years). It is mainly services production that has increased. GRP per capita was SEK 424,000

— Total disposable income in Malmö was SEK 50,749 million

(up by approximately 52% in ten years). Disposable income per capita was SEK 164,000

— The total wage bill for Malmö was SEK 55,010 million (around +58% in ten years). In particular, the service sector has seen a large positive development in wages

StockholmGothenburgSweden

MalmöSkåne

StockholmGothenburgSweden

MalmöSkåne

Market production, goods (SNI A01-F43)Market production, services (SNI G45-T98)Public authorities and non-profit in-stitutions serving households (NPISH)

Market production, goods (SNI A01-F43)Market production, services (SNI G45-T98)Public Authorities and non-profit in-stitutions serving households (NPISH)

Items not broken down by industry

14

The City of Malmö focuses on a number of profile areas in a business context. These are areas in which Malmö’s strengths are considered to be particularly successful in terms of more employment opportunities and improved growth. Read more on www.malmobusiness.com under “Profile areas”.

HOSPITALITY INDUSTRY (1)The overall goal for Malmö Tourism is to attract more visitors to Malmö. This will produce more economic turnover and more jobs in the hotel and catering industry in Malmö. The hotel and catering industry is very important in terms of the labour market and growth. Malmö Tourism is actively working to advertise Malmö’s at-tractions and to provide an impetus for Malmö to keep developing more attractive offerings in the future.

— The collaboration between the City of Malmö and Destinationssamverkan Malmö AB (structured collaboration between the City of Malmö and commercial and non-profit players in the city) has been expanded and intensified

— Malmö Live, which opened in 2015, has helped attract new meetings and con-ferences to Malmö, not least benefiting the hotel and catering sector in Malmö

— The hotel and catering industry is very important to commerce in Malmö. Just over 20% of visitor consumption takes place in the city’s shops

CLEANTECH (2)The City of Malmö aims to become a “cleantech city” – a place with a unique envi-ronmental technology profile combining economic, social and ecological sustain-ability. Together with industry, the university and other actors, the municipality aims to create an attractive location to start up, operate and develop companies in the cleantech field in Malmö.

In the City of Malmö, this profile area is driven via Malmö Cleantech City. By offering various networking opportunities, testbed activities and a physical meeting place, it facilitates business opportunities and development of expertise and technology.

— Cleantech Scandinavia’s annual meeting Cleantech Capital Day, which involves 70 international investors, was once again held in Malmö in May 2016

— With regards to the startup scene, we are seeing a trend towards smaller, smart and low-cost solutions

— On the investor side, there has been a shift from venture capital funds and indus-trial investors towards companies seeking to raise capital from small-scale savers via marketplaces such as NASDAQ First North and Aktietorget

CITY OF MALMÖ'S PROFILE AREAS

1

2

3

4

5

6

7

15

COMMERCE (3)Malmö will continue to develop and grow as a regional cen-tre for commerce and visitors. Commerce has experienced strong growth in the last 10 years and employs around 20% of all those working in the retail sector in Skåne. As the popu-lation in Malmö and the region grows, demand will continue to increase. An attractive city, the major commercial centres in the town, conference and exhibition facilities, events and leisure activities will contribute to this.

— Commerce in the city is continuing to develop, the vacan-cy rate fell in 2015 and the range of shops was expanded

— Shopping in the city is increasingly interspersed with restaurants, cafes and other experience-based industries. Malmö was awarded its first Michelin star this year

— Malmö is continuing to grow as a shopping destination for tourists

HEAD OFFICES (4)

Malmö is an attractive location for corporate headquarters. Its geographical location and infrastructure, including a journey time of 20 minutes to Copenhagen Airport, have been a deciding factor in the establishment of many head offices. A large recruitment base, with access to a young, well-educated and international workforce, is another factor that has attracted companies.

— Companies which set up their head offices in Malmö in 2015 include IKEA’s Hubhult, IKANO Bank, IKANO Fastigheter, Atos Medical and Maxomorra

— The companies were primarily established in Hyllie and the surrounding area, as well as in Västra hamnen and the city centre

LIFE SCIENCE (5)Together with the Copenhagen region, Skåne constitutes the third largest geographical area for pharmaceuticals and biotechnology in Europe. Malmö is an excellent place to establish life science activities, whether as companies or research projects. Immediate access and proximity to first-class medical research, advanced medical care and high-tech companies provide a unique environment for companies in the area. We are more than happy to help provide access to this unique network in connection with the establishment of head offices.

— A sector undergoing constant change. For instance, new business models through consolidation and acquisition of

small, innovative companies. Continued outsourcing of production and clinical chemistry

— Malmö hosts several scientific national and international conferences and meetings, e.g. Senior i Centrum (Focus on senior care), Framtidens specialistläkare (Specialised doctors of the future), European Society of Neuroradiol-ogy annual meeting

— Medeon science park – a growing cluster and hub for life science activities in Malmö

LOGISTICS (6)Malmö Industrial Park is one of the most attractive places to establish manufacturing, processing and logistics companies in northern Europe. Its strategic position makes it easy to distribute incoming and outgoing flows of goods by both sea, rail and road. It attracts companies looking for access to land for activities requiring tri-modal transportation, proces-sing operations and a connection to a port.

— Malmö Industrial Park has an area of 750,000 m2 that has yet to be developed to provide space for the establish-ment of new companies

— Skanska has reserved land on the site for the construction of a new warehouse concept – cubic storage

— Prologis has also reserved land on the site for an area of around 100,000 m2, and is planning to establish a logis-tics facility on the site

CREATIVE INDUSTRIES (7)Investments in film, TV, computer games, web-based servi-ces, mobile platforms, design and advertising have created a strong potential for the experience industry in Malmö. Mo-ving images in new media and on digital platforms such as mobile phones and computers provide good opportunities for growth. The vision is to be an expanding centre where leading business, education and research at an international level generate growth.

— Malmö has become a film city! Documentary films, short films, full-length films and films for children and young people are being produced in Malmö

— The vision is for Malmö to become a significant and prominent design city

— The vision is that Malmö should be the driving force in Europe’s leading region when it comes to development, playing, education and research within the area of digital games

16

GROWTHMalmö is doing well and the develop-ment is monitored through 10 key performance indicators. This positive development was rewarded when the city received the prize of Growth Municipality of the Year 2009*.

* The Growth Municipality of the Year prize is awarded by Arena för Tillväxt and SWECO Eurofu-tures

— Destination Malmö is growing at breakneck speed. In 2015, 1,576,968 hotel overnight stays were recorded in Malmö. This amounts to 170,199 more guest nights than in 2014 and corresponds to an increase of +17%

— 73% of overnight stays were by Swedish visitors and 27% by international visitors. The largest number of overnight stays was by visitors from Denmark, Germany, the UK and Norway

— On average, Malmö recorded a 66.2% occupancy rate for hotels in 2015 (comp. with 64.6% in 2014)

— More than 1,200 meetings and conferences with more than 50 delegates took place in Malmö in 2015. This was an increase of 389 meetings com-pared with 2014

— The hotel and catering industry is very important to commerce in Malmö. Just over 20% of visitor consumption takes place in the city’s shops. The Swedish krona exchange rate is currently very favourable for Danish people, which is having an impact on both the number of day and overnight visitors from Denmark

— Malmö as a destination is given a lot of coverage in the international media, which likes to write about Malmö as a city for food, meetings, music and sports, and also as a mecca for fans of detec-tive series such as The Bridge

GUEST NIGHT = EACH OVERNIGHT GUEST

DUE TO CONFIDENTIALITY REGULATIONS, SEPARATE FIGURES CANNOT BE PROVIDED FOR HOSTELS FOR 2015. THE FIGURES INCLUDE CAMPING AND CABINS, HENCE THE HIGH NUMBER.

NUMBER OF GUEST NIGHTSTHOUSANDS

— The vacancy rate has decreased and was 8.0%, compared with 9.5% in the previous year. Rental levels for Prime Rent in the CBD (Central Business District) have increased to 2,325 SEK/sq. m/year, compared with 2,075 in the previous year.

— Several high-profile new buildings in the city, together with a relatively low vacancy rate, has pushed up average rents in the city centre

— Locations close to stations, such as Triangeln, Malmö Central and not least Hyllie remain popular and are in high demand by companies

— Commercial activity in the city centre is starting to recover after a few tough years. The trend is towards a mixture of restaurants, cafes and other, experience-based companies

— More efficient use of areas and changing work habits are driving demand for new, activity-based office concepts. For instance, Malmö has opened its first activity-based business centre

— In Norra hamnen, work is continuing on the devel-opment of Malmö’s future industrial and logistics hub, Malmö Industrial Park, where the first site agreement has been signed.

— Nyhamnen is the next big development area in Malmö after Västra hamnen and Hyllie. The com-prehensive plan is expected to be ready in 2017

PRIME RENT = EXPECTED LEVEL OF RENT FOR A TOP-QUALITY OFFICE (>500 SQ. M) IN A PRIME LOCATION, IGNORING EXTREMES

COMMERCIAL REAL ESTATE MARKET

0

200

400

600

800

1,000

1,200

1,400

1,600

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

HOTELS

HOSTELS

HOSTELS/CAMPING/CABINS

VACANCY RATE MALMÖ/LUND

PRIME RENT CENTRAL BUSINESS DISTRICT MALMÖ (SEK/M²/YEAR)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

0%

2%

4%

6%

8%

10%

12%

14%

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

SEK/M²/YEAR

17

HOUSING CONSTRUCTION – NUMBER OF PROJECTS

UNEMPLOYMENTNUMBER OF EMPLOYEES – DAYTIME POPULATION THOUSANDS

— In 2015, construction of more than 2,000 residen-tial units began, and the number of completed dwellings exceeded 1,600. Approximately 14% of the residential units under construction and just over 70% of the completed units have been built by MKB

— The proportion of right of tenancy units under construction was approximately 43%, while the proportion among completed units was 54%

— Of residential units granted building permission in 2015, construction began on 2,200 in 2015. 15% of housing units under construction in 2015 involved refurbishment of the existing building

— The City Planning Office has put forward a proposal for a detailed development plan for the Abborren site, which forms part of the redevelop-ment along the Citadellsvägen road. The aim is to facilitate the construction of a mixed-use develop-ment of up to six floors

— In 2015, building permission was granted for nearly 3,200 housing units. The development mostly comprises new production of apartments, but per-mission has also been granted for the conversion of e.g. offices, premises and attics into residential units to a larger extent than in previous years

— Residential construction in Malmö exceeded all forecasts in 2015 and the number of residential units under construction was high

MULTI-DWELLING BUILDING = BUILDING WITH AT LEAST 3 SEPARATE APARTMENTS. THE MAXIMUM NUMBER IS UNLIMITED.

— There were 158,599 employees in Malmö in 2015. The number of employees increased by 3,035 people or 2.0% compared with the previous year

— After the summer of 2011, the trend in the num-ber of employed started to move upwards again after a couple of years at a constant level because of economic unrest in Europe and the world. Since then it has risen progressively and it is now at its highest level to date

— In the last year, there has been an increase pri-marily within business services and consultancy services. Staffing agencies, and the transport, construction and telecommunications sectors also reported an increase. There has been a drop in employment in social outpatient services and social services, as well as within advertising and marketing

— Privately-owned Swedish companies which form part of a group showed the largest increase, fol-lowed by the public sector and foreign com-panies. Municipal activity showed a reduction. Limited companies are the legal form that has increased the most

— The number of employees has increased by 28% in 15 years. A positive long-term development can be noted within business services, IT and computer consultants, hotels and restaurants, education and commerce

NUMBER OF EMPLOYEES = DAYTIME POPULATION, I.E. THE NUMBER OF PEOPLE EMPLOYED IN MALMÖ (EXCL. OWNERS OF SOLE PROPRIETORSHIPS) WHO EARNED AT LEAST ONE INCOME BASE AMOUNT PER YEAR, OR WORKED AS TEMPORARY EMPLOYEES FOR MORE THAN 3 MONTHS

— In 2015, youth unemployment in Malmö decreased, while overall unemployment was more or less unchanged compared with the previous year

— In 2015, the proportion of unemployed registered with the Public Employment Service in Malmö was 15% in the age group 16-64 (annual average for 2015). Unemployment among young people aged 18-24 fell substantially to 21.6% (annual average 2015), compared with the previous year, when it amounted to 23.3% (annual average for 2014)

— Unemployment was higher among men (16.5%) than among women (13.3%), and among young people the difference was even greater (26.1% for men and 17.2% for women)

— There were large differences in the proportion of unemployed in different groups – it is higher among young people, higher among people born abroad, regardless of level of education, and higher for men than for women in all groups

— Compared to other large cities in Sweden, Malmö had high unemployment. In Gothenburg, unem-ployment was 8.2% and in Stockholm 6.3% (of the workforce aged 16-64, December 2015)

— Around 8,000 people commuted from Malmö to Denmark in 2015

AVERAGE PER YEAR. PEOPLE IN THE 16-64 AGE GROUP WHO ARE REGISTERED WITH THE EMPLOYMENT SERVICE AS A PERCENTAGE OF THE REGISTERED WORKFORCE. (1997–2007 = PER CENT OF POPULATION)

POPULATION MALMÖ

POPULATION SKÅNE

POPULATION SWEDEN

WORKFORCE MALMÖ

WORKFORCE SKÅNE

WORKFORCE SWEDEN

STARTED

NEWLY BUILT

0

500

1,000

1,500

2,000

2,500

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0

25

50

75

100

125

150

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

18

NUMBER OF NEW VACANCIES THOUSANDS

NUMBER OF NEW COMPANIES - ALL COMPANY FORMS

NUMBER OF BANKRUPTCIES

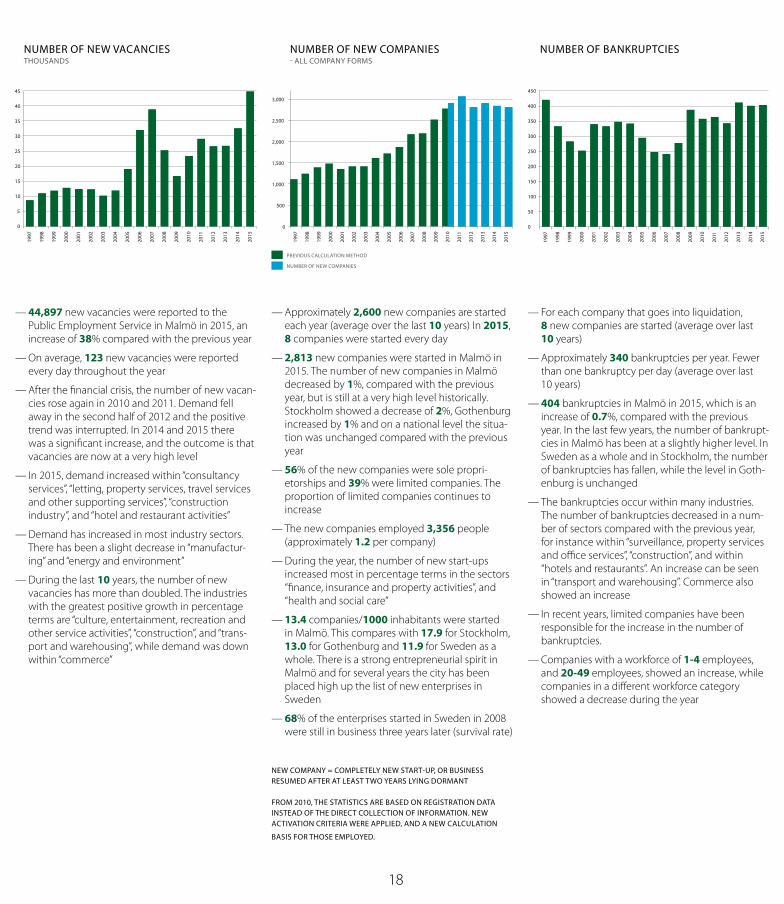

— 44,897 new vacancies were reported to the Public Employment Service in Malmö in 2015, an increase of 38% compared with the previous year

— On average, 123 new vacancies were reported every day throughout the year

— After the financial crisis, the number of new vacan-cies rose again in 2010 and 2011. Demand fell away in the second half of 2012 and the positive trend was interrupted. In 2014 and 2015 there was a significant increase, and the outcome is that vacancies are now at a very high level

— In 2015, demand increased within “consultancy services”, “letting, property services, travel services and other supporting services”, “construction industry”, and “hotel and restaurant activities”

— Demand has increased in most industry sectors. There has been a slight decrease in “manufactur-ing” and “energy and environment”

— During the last 10 years, the number of new vacancies has more than doubled. The industries with the greatest positive growth in percentage terms are “culture, entertainment, recreation and other service activities”, “construction”, and “trans-port and warehousing”, while demand was down within “commerce”

— Approximately 2,600 new companies are started each year (average over the last 10 years) In 2015, 8 companies were started every day

— 2,813 new companies were started in Malmö in 2015. The number of new companies in Malmö decreased by 1%, compared with the previous year, but is still at a very high level historically. Stockholm showed a decrease of 2%, Gothenburg increased by 1% and on a national level the situa-tion was unchanged compared with the previous year

— 56% of the new companies were sole propri-etorships and 39% were limited companies. The proportion of limited companies continues to increase

— The new companies employed 3,356 people (approximately 1.2 per company)

— During the year, the number of new start-ups increased most in percentage terms in the sectors “finance, insurance and property activities”, and “health and social care”

— 13.4 companies/1000 inhabitants were started in Malmö. This compares with 17.9 for Stockholm, 13.0 for Gothenburg and 11.9 for Sweden as a whole. There is a strong entrepreneurial spirit in Malmö and for several years the city has been placed high up the list of new enterprises in Sweden

— 68% of the enterprises started in Sweden in 2008 were still in business three years later (survival rate)

NEW COMPANY = COMPLETELY NEW START-UP, OR BUSINESS RESUMED AFTER AT LEAST TWO YEARS LYING DORMANT

FROM 2010, THE STATISTICS ARE BASED ON REGISTRATION DATA INSTEAD OF THE DIRECT COLLECTION OF INFORMATION. NEW ACTIVATION CRITERIA WERE APPLIED, AND A NEW CALCULATION

BASIS FOR THOSE EMPLOYED.

— For each company that goes into liquidation, 8 new companies are started (average over last 10 years)

— Approximately 340 bankruptcies per year. Fewer than one bankruptcy per day (average over last 10 years)

— 404 bankruptcies in Malmö in 2015, which is an increase of 0.7%, compared with the previous year. In the last few years, the number of bankrupt-cies in Malmö has been at a slightly higher level. In Sweden as a whole and in Stockholm, the number of bankruptcies has fallen, while the level in Goth-enburg is unchanged

— The bankruptcies occur within many industries. The number of bankruptcies decreased in a num-ber of sectors compared with the previous year, for instance within “surveillance, property services and office services”, “construction”, and within “hotels and restaurants”. An increase can be seen in “transport and warehousing”. Commerce also showed an increase

— In recent years, limited companies have been responsible for the increase in the number of bankruptcies.

— Companies with a workforce of 1-4 employees, and 20-49 employees, showed an increase, while companies in a different workforce category showed a decrease during the year

PREVIOUS CALCULATION METHOD

NUMBER OF NEW COMPANIES

0

5

10

15

20

25

30

35

40

45

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0

500

1,000

1,500

2,000

2,500

3,000

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0

50

100

150

200

250

300

350

400

450

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

19

INDUSTRIAL INVESTMENTSSEK MILLION

REVENUEEXCLUDING VAT, SEK BILLION

— Turnover amounted to SEK 281 billion in 2015, which is the highest amount during the measure-ment period and an increase of as much as 6.6% on the previous year

— After several years of strong growth, turnover dropped in 2009–2010 due to the economic downturn. Turnover in Malmö has now increased again and is actually at a higher level than during the record years of 2006–2008

— During the last 10 years, turnover in Malmö has increased by 33%

— Several industries showed a large percentage increase in turnover in the past year, such as “out-patient social care services” and “vehicle sales and garages and workshops”

— Other industries that have shown a sharp rise in turnover are “consultancy services” and “staff-ing agencies”, followed by “services for financial businesses” and “hotels and restaurants”, as well as “building contractors”

— Two industries in which turnover has decreased in the last year are “industry for pharmaceutical base products and pharmaceuticals”, as well as “postal and courier companies”

— Investments in Malmö started to increase again in 2015. Industry in Malmö invested SEK 875 million during 2015, which corresponded to an increase of 20% compared with the previous year. Investments in buildings and fixtures and fittings showed the largest percentage increase. The out-come for 2015 exceeded the forecast produced a year earlier by SEK 8 million

— In Sweden as a whole, industrial investment in-creased by 23% compared with the previous year. The largest increase in volume in 2015 was shown by the pulp and paper industry. The chemical industry, wood products industry, metal industry, as well as steel and metals industry also reported increased volumes

— Industry sectors that showed a reduced level of investment were the mining industry, the textile industry and the rubber and plastics industry

— The forecast for Malmö for 2016 shows an invest-ment level of SEK 746 million, that is, investments are expected to decline slightly compared with 2015

— For Sweden as a whole, the projected investment level for 2016 is at approximately the same level as realised investments in 2015

2016 = FORECASTSNI CODE B+C, I.E. EXTRACTION OF MINERALS AND MANUFACTURING

INDUSTRIAL INVESTMENTS

FORECAST

0

100

200

300

400

500

600

700

800

900

1,000

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

0

50

100

150

200

250

300

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

20

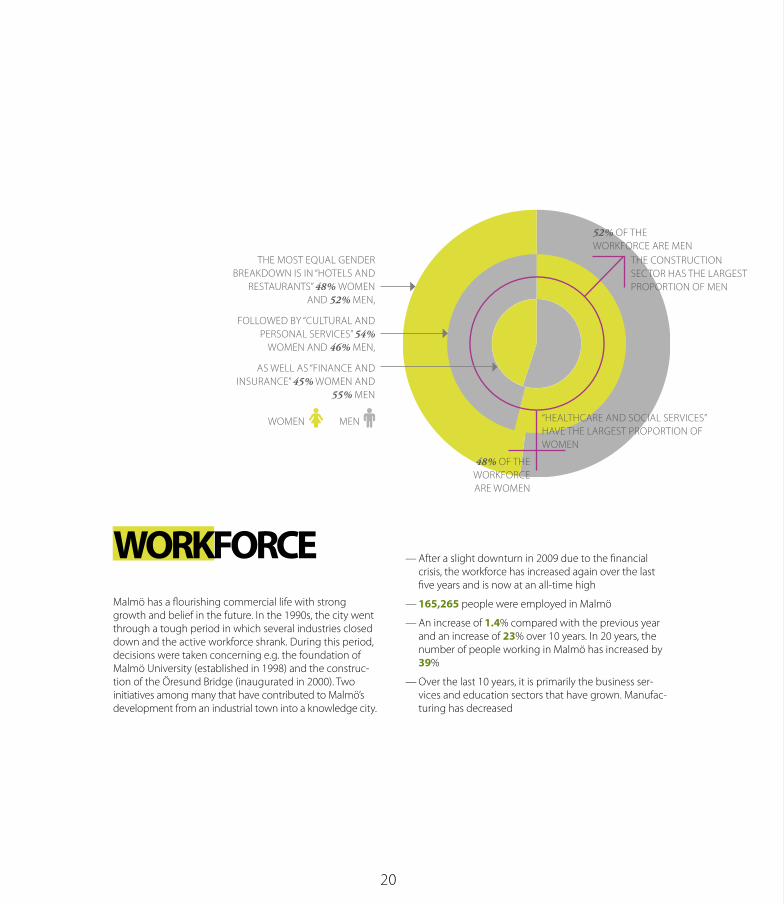

THE CONSTRUCTION SECTOR HAS THE LARGEST PROPORTION OF MEN

48% OF THE WORKFORCE ARE WOMEN

52% OF THE WORKFORCE ARE MEN

THE MOST EQUAL GENDER BREAKDOWN IS IN “HOTELS AND

RESTAURANTS” 48% WOMEN AND 52% MEN,

FOLLOWED BY “CULTURAL AND PERSONAL SERVICES” 54%

WOMEN AND 46% MEN,

AS WELL AS “FINANCE AND INSURANCE” 45% WOMEN AND

55% MEN

WOMEN MEN “HEALTHCARE AND SOCIAL SERVICES” HAVE THE LARGEST PROPORTION OF WOMEN

WORKFORCEMalmö has a flourishing commercial life with strong growth and belief in the future. In the 1990s, the city went through a tough period in which several industries closed down and the active workforce shrank. During this period, decisions were taken concerning e.g. the foundation of Malmö University (established in 1998) and the construc-tion of the Öresund Bridge (inaugurated in 2000). Two initiatives among many that have contributed to Malmö’s development from an industrial town into a knowledge city.

— After a slight downturn in 2009 due to the financial crisis, the workforce has increased again over the last five years and is now at an all-time high

— 165,265 people were employed in Malmö

— An increase of 1.4% compared with the previous year and an increase of 23% over 10 years. In 20 years, the number of people working in Malmö has increased by 39%

— Over the last 10 years, it is primarily the business ser-vices and education sectors that have grown. Manufac-turing has decreased

21

90

100

110

120

130

140

150

160

170

1960

1965

1970

1975

1980

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2012

2011

2013

2014

111

128

137140

146

118

151

149

154

158161

165163

WORKFORCE DEVELOPMENT, DAYTIME POPULATION, THOUSANDS

WORKFORCE (16+ YEARS) WITH WORKPLACE IN MALMÖ. THE FIGURES INCLUDE BOTH OWNERS OF SOLE PROPRIETORSHIPS AND EMPLOYEES IN ALL FORMS OF ENTERPRISE. RAMS STATISTICS SWEDEN.

165,265 PEOPLE WERE

EMPLOYED IN MALMÖ

22

GEOGRAPHICAL DEVELOPMENT, WORKFORCE

2004 2013 2014 10-YEAR TRENDDEVELOPMENT COMPARED WITH THE PREVIOUS YEAR

STOCKHOLM 516,428 635,673 644,738 128,310 25% 9,065 1.4%

GOTHENBURG 280,233 320,259 323,044 42,811 15% 2,785 0.9%

MALMÖ 134,211 162,941 165,265 31,054 23% 2,324 1.4%

LUND 59,027 68,249 69,231 10,204 17% 982 1.4%

HELSINGBORG 58,886 67,044 67,916 9,030 15% 872 1.3%

SKÅNE 498,623 560,530 565,560 66,937 13% 5,030 0.9%

SWEDEN 4,162,497 4,610,204 4,647,314 484,817 12% 37,110 0.8%

— Positive development of the workforce in Malmö

— The size of the workforce with its workplace in Malmö has increased by 23% in 10 years

— In Sweden as a whole, the size of the workforce has increased by 12% over a 10-year period. The correspond-ing figure for Stockholm is 25%, Gothenburg 15% and Skåne 13%

GEOGRAPHICAL DEVELOPMENT

23

WORKFORCE BY INDUSTRYSECTORS SORTED IN DESCENDING ORDER OF SIZE. WORKFORCE, DAYTIME POPULATION 2014 (16+ YEARS). RAMS STATISTICS SWEDEN. SNI2007.

— Today, a large number of people work within various knowledge-intensive service sectors in Malmö. Only 6.5% work in manufacturing. This is a lower figure than for Swe-den as a whole, where 12% work in manufacturing(1)

— In 2010, business services overtook commerce to become the largest sector in Malmö (2)

— Malmö has the largest proportion of its workforce work-ing in business services (15%), followed by commerce

(15%), healthcare and social services (14%) and educa-tion (10%) (3)

— Over half (54%) work in the four largest sectors above (3)

— Sweden as a whole differs from Malmö in terms of which sectors have the highest workforce. In Sweden, the largest group is healthcare and social services (16%), followed by commerce (12%) and manufacturing (12%) (4)

WORKFORCE BY INDUSTRY

15% 15% 14%

10%

7% 6% 6% 6% 6% 5% 4%

2% 2% 1% 0% 1% 0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Företagstjänste

r

Handel

Vård, o

msorg

, sociala tjä

nster

Utbild

ning

Tillverkning och utvinning

O�entlig fö

rvaltning och fö

rsvar

Byggverksamhet

Informatio

n och kommunikation

Transport

och magasin

ering

Kulturella

och personlig

a tjänste

r

Hotell- och re

staurangverksa

mhet

Finans- och fö

rsäkrin

gsverksa

mhet

Fastighetsv

erksamhet

Energifö

rsörjn

ing, miljö

verksamhet

Jord

bruk, sk

ogsbru

k och �ske

Okänd verksamhet

MALMÖ SWEDEN

12 4

3

Transport

and warehousin

g

Business

service

s

Commerce

Healthcare, so

cial service

s

Education

Manufacturin

g and extractio

n

Public administ

ration and defence

Constructio

n activity

Informatio

n and communicatio

n

Cultural a

nd personal se

rvices

Hotels and re

staurants

Financial and in

surance

service

s

Real esta

te activitie

s

Energy su

pply, enviro

nmental service

s

Agricultu

re, forestr

y and fisherie

s

Unknown business

24

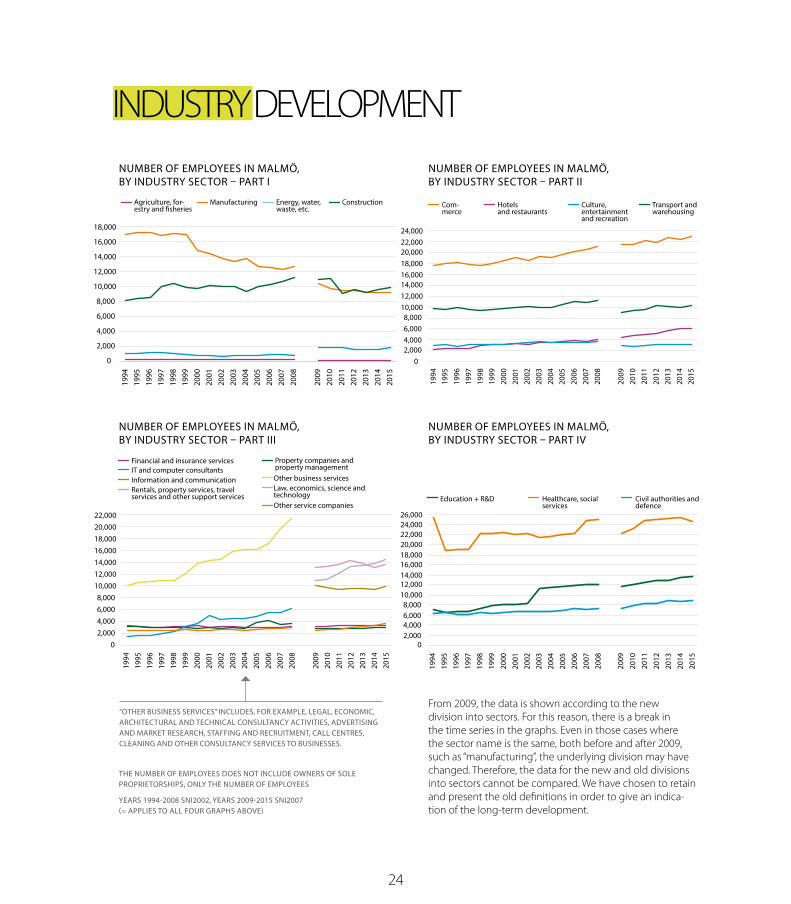

From 2009, the data is shown according to the new division into sectors. For this reason, there is a break in the time series in the graphs. Even in those cases where the sector name is the same, both before and after 2009, such as “manufacturing”, the underlying division may have changed. Therefore, the data for the new and old divisions into sectors cannot be compared. We have chosen to retain and present the old definitions in order to give an indica-tion of the long-term development.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

2009

20

10

2011

20

12

2013

20

14

2015

NUMBER OF EMPLOYEES IN MALMÖ, BY INDUSTRY SECTOR – PART I

NUMBER OF EMPLOYEES IN MALMÖ, BY INDUSTRY SECTOR – PART III

NUMBER OF EMPLOYEES IN MALMÖ, BY INDUSTRY SECTOR – PART IV

NUMBER OF EMPLOYEES IN MALMÖ, BY INDUSTRY SECTOR – PART II

0 2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,000 20,000 22,000 24,000

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

2009

20

10

2011

20

12

2013

20

14

2015

Handel Hotell och restaurang

Kultur, nöje och fritid

Transport och magasinering

0 2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,000 20,000 22,000

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

2009

20

10

2011

20

12

2013

20

14

2015

0 2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,000 20,000 22,000 24,000 26,000

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

2009

20

10

2011

20

12

2013

20

14

2015

Utbildning + FoU Vård, omsorg, sociala tjänster

Civila myndigheter och försvaret

INDUSTRY DEVELOPMENT

“OTHER BUSINESS SERVICES” INCLUDES, FOR EXAMPLE, LEGAL, ECONOMIC, ARCHITECTURAL AND TECHNICAL CONSULTANCY ACTIVITIES, ADVERTISING AND MARKET RESEARCH, STAFFING AND RECRUITMENT, CALL CENTRES, CLEANING AND OTHER CONSULTANCY SERVICES TO BUSINESSES.

THE NUMBER OF EMPLOYEES DOES NOT INCLUDE OWNERS OF SOLE PROPRIETORSHIPS, ONLY THE NUMBER OF EMPLOYEES

YEARS 1994-2008 SNI2002, YEARS 2009-2015 SNI2007 (= APPLIES TO ALL FOUR GRAPHS ABOVE)

Agriculture, for-estry and fisheries

Manufacturing Energy, water, waste, etc.

Construction Com-merce

Hotels and restaurants

Culture, entertainment and recreation

Transport and warehousing

Education + R&D Healthcare, social services

Civil authorities and defence

Financial and insurance servicesIT and computer consultantsInformation and communicationRentals, property services, travel services and other support services

Property companies and property managementOther business servicesLaw, economics, science and technologyOther service companies

25

PERCENTAGE CHANGE 2009-2015 — The sectors that showed the largest percentage increase in the number of employees were “other service com-panies” and “hotels and restaurants”, followed by “law, economics, science” and “civil authorities and defence”

— “Education”, “transport and warehousing” and “health-care and social services” and “property companies and property management” also showed an increase of more than 10% in the period

— Sectors that showed a decrease were “agriculture/forestry/fishing”, followed by “manufacturing”, “construction”, “infor-mation and communication” and “energy, water, waste”

LONG-TERM TRENDBecause of changes in the division into sectors, it is not possible to make any detailed long-term analysis, but only to summarise the overall development in a few short comments:

— A positive long-term development can be noted within business services, IT and computer consultancies, hotels and restaurants, education and commerce

— A downward trend can be seen within manufacturing and agriculture/forestry/fishing

A DOWNWARD TREND CAN BE SEEN WITHIN MANUFACTURING AND AGRICULTURE/FORESTRY/FISHINGA POSITIVE LONG-TERM DEVELOPMENT CAN BE NOTED WITHIN

BUSINESS SERVICES, IT AND COMPUTER CONSULTANCIES, HOTELS AND RESTAURANTS, EDUCATION AND COMMERCE

26

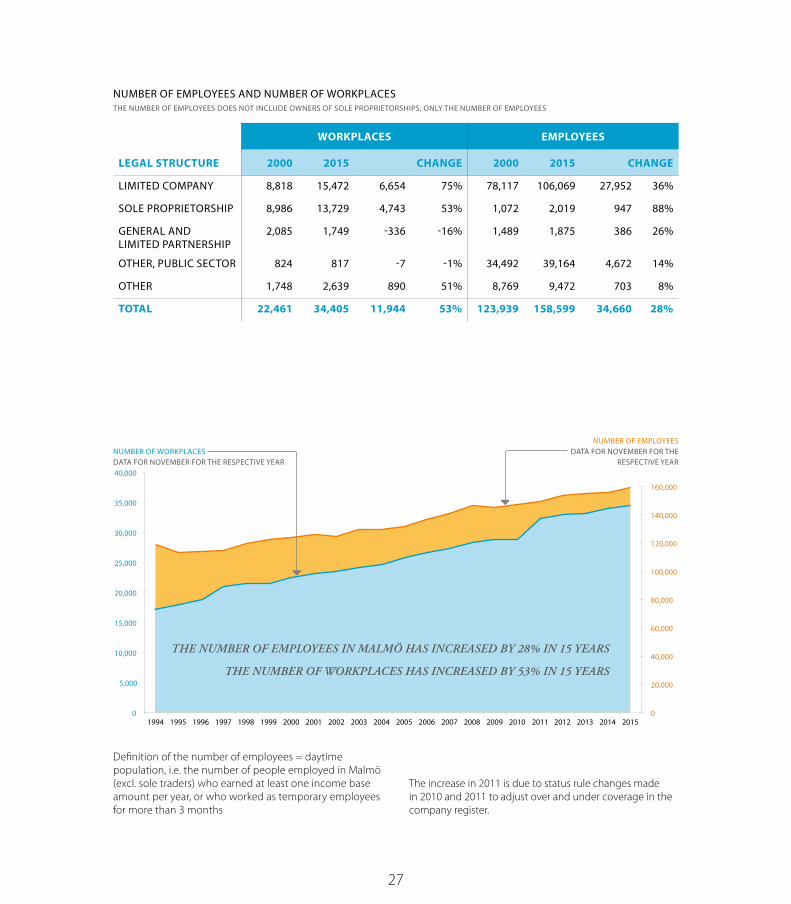

CORPORATE STRUCTURE

— Malmö had 158,599 employees spread across 34,405 workplaces

— Both the number of employees and the number of workplaces have increased significantly

— The number of employees in Malmö has increased by 28% in 15 years

— The number of workplaces has increased by 53% in 15 years

— 45% of the workplaces were limited companies, and 40% were sole proprietorships, which are the two most widespread enterprise forms in Malmö

Many new enterprises are being started and established enterprises are choosing to relo-cate to Malmö. The number of workplaces has increased significantly and today’s corporate structure to a large extent comprises small and medium-sized enterprises.

— The number of workplaces in the group “limited com-panies” has risen sharply in 15 years, increasing by 75%, and in the group “sole proprietorships” the number has increased by 53%

— The arrival of many new companies reflects the entrepreneurial spirit to be found in Malmö and the changes the city has undergone – from a structure with a number of large companies to one with many smaller companies

— The largest proportion of employees is to be found in limited companies. The number of employees in limited companies has increased by 36% in 15 years

LEGAL FORM OF ENTERPRISE

LIMITED COMPANY

45%

SOLE PROPRIETORSHIP 40%

OTHER 8%

OTHER, PUBLIC SECTOR 2%

GENERAL AND LIMITED

PARTNERSHIP 5%

27

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

NUMBER OF EMPLOYEESDATA FOR NOVEMBER FOR THE

RESPECTIVE YEARNUMBER OF WORKPLACESDATA FOR NOVEMBER FOR THE RESPECTIVE YEAR

The increase in 2011 is due to status rule changes made in 2010 and 2011 to adjust over and under coverage in the company register.

Definition of the number of employees = daytime population, i.e. the number of people employed in Malmö (excl. sole traders) who earned at least one income base amount per year, or who worked as temporary employees for more than 3 months

NUMBER OF EMPLOYEES AND NUMBER OF WORKPLACES THE NUMBER OF EMPLOYEES DOES NOT INCLUDE OWNERS OF SOLE PROPRIETORSHIPS, ONLY THE NUMBER OF EMPLOYEES

WORKPLACES EMPLOYEES

LEGAL STRUCTURE 2000 2015 CHANGE 2000 2015 CHANGE

LIMITED COMPANY 8,818 15,472 6,654 75% 78,117 106,069 27,952 36%

SOLE PROPRIETORSHIP 8,986 13,729 4,743 53% 1,072 2,019 947 88%

GENERAL AND LIMITED PARTNERSHIP

2,085 1,749 -336 -16% 1,489 1,875 386 26%

OTHER, PUBLIC SECTOR 824 817 -7 -1% 34,492 39,164 4,672 14%

OTHER 1,748 2,639 890 51% 8,769 9,472 703 8%

TOTAL 22,461 34,405 11,944 53% 123,939 158,599 34,660 28%

THE NUMBER OF EMPLOYEES IN MALMÖ HAS INCREASED BY 28% IN 15 YEARS

THE NUMBER OF WORKPLACES HAS INCREASED BY 53% IN 15 YEARS

28

NUMBER OF EMPLOYEES AND NUMBER OF WORKPLACES

WORKPLACES EMPLOYEES

OWNER CONTROL 2005 2015 CHANGE 2005 2015 CHANGE

GOVERNMENT 217 182 -35 -16% 13,313 14,095 782 6%

MUNICIPAL 764 707 -57 -7% 22,810 20,966 -1,844 -8%

COUNTY COUNCIL 71 87 16 23% 8,360 10,347 1,987 24%

PRIVATE SWEDISH EXCL. GROUPS 20,384 26,626 6,242 31% 24,604 30,900 6,296 26%

PRIVATE SWEDISH INCL. GROUPS 3,033 4,862 1,829 60% 38,259 45,534 7,275 19%

FOREIGN 1,199 1,941 742 62% 24,471 36,757 12,286 50%

TOTAL 25,668 34,405 8,737 34% 131,817 158,599 26,782 20%

— 71% were employed in the private sector and 29% in the public sector

— The number of employees has increased by 20% since 2005. The increase has occurred above all in the private sector

— Foreign-owned companies showed the largest increase in the number of employees; an increase of 50% since 2005. Among foreign-owned companies, there are also companies the public would consider Swedish but which are registered abroad

— Swedish trade and industry comprises just over 1 million companies with 2.7 million employees

— As many as 97% of the companies consist of so-called micro enterprises with fewer than 10 employees, which represented one quarter of trade and industry’s added value in 2014.

— Large corporations with 250 or more employees accounted for just 0.1% of the total number of com-panies, but accounted for 39% of Swedish trade and industry’s added value

— Service companies employed 66% of the workforce and accounted for 62% of added value in Sweden. Both figures show a small increase on the previous year

— Malmö’s trade and industry is largely composed of small and medium-sized companies. This is the same structure as for Sweden as a whole

— A large proportion of the workplaces in Malmö have no employees

— Malmö has a mixed business community that includes many different sectors, giving the city a solid and diversified base

— The service sector has increased significantly over the last 15 years and today constitutes a considerable proportion of trade and industry

SWE

29

NUMBER OF WORKPLACES BY NUMBER OF EMPLOYEES2015. SNI2007. THE NUMBER OF EMPLOYEES DOES NOT INCLUDE OWNERS OF SOLE PROPRIETORSHIPS.

NUMBER OF EMPLOYEES

INDUSTRY SECTOR 0 EMPL. 1-2 3-9 10-49 50-249 250-499 +500 TOTAL

AGRICULTURE, FORESTRY AND FISHERIES 727 28 12 1 768

MANUFACTURING 606 177 173 127 44 2 1 1,130

ENERGY, WATER, WASTE, ETC. 65 11 23 17 11 1 128

CONSTRUCTION 976 449 268 165 34 1 1 1,894

COMMERCE 2,425 1,036 1,123 462 73 3 5,122

TRANSPORT AND WAREHOUSING 354 297 179 99 29 3 3 964

HOTELS AND RESTAURANTS 416 320 351 166 12 1,265

INFORMATION AND COMMUNICATION 1,593 478 229 137 45 2 2,484

FINANCIAL AND INSURANCE SERVICES 537 123 93 39 11 1 804

REAL ESTATE ACTIVITIES 2,411 446 139 61 10 3,067

LAW, ECONOMICS, SCIENCE AND TECHNOLOGY

4,532 1,369 502 248 49 2 6,702

RENTAL, REAL ESTATE, TRAVEL AND SUPPORT SERVICES

809 322 212 148 54 5 2 1,552

PUBLIC ADMINISTRATION, DEFENCE, ETC. 4 16 27 35 34 7 3 126

EDUCATION 732 111 169 267 64 3 1,346

HEALTHCARE, SOCIAL SERVICES 795 352 266 257 57 5 4 1,736

CULTURE, ENTERTAINMENT AND RECREATION

2,421 233 112 54 9 1 2,830

OTHER SERVICES 1,749 376 197 72 10 2,404

OTHER 62 17 4 83

TOTAL 21,214 6,161 4,079 2,355 546 35 15 34,405

30

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

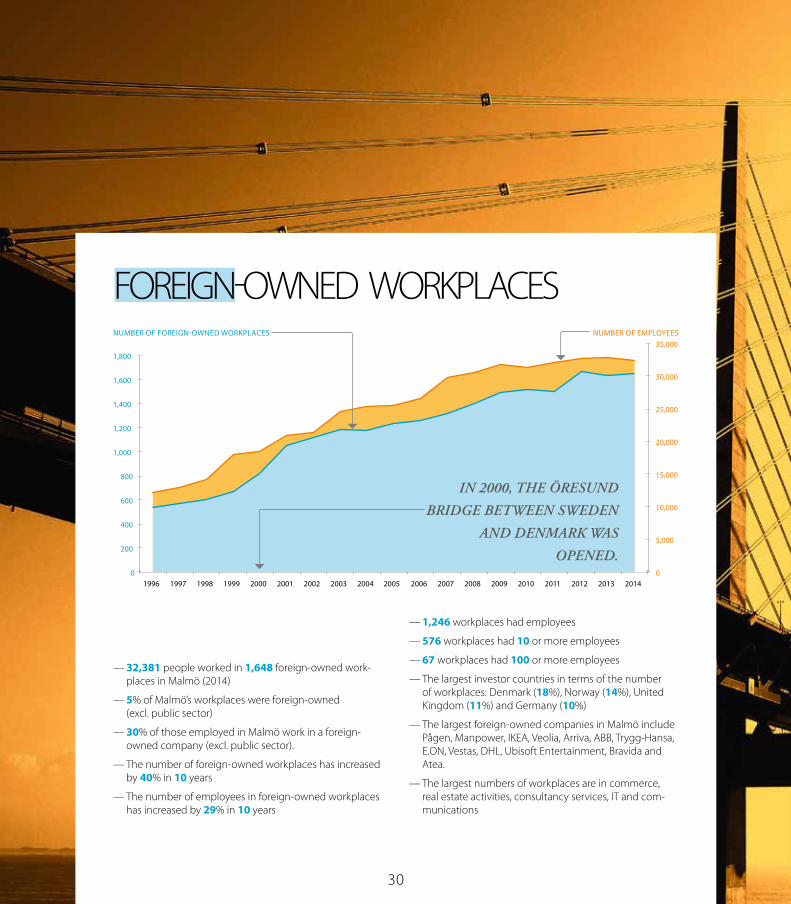

NUMBER OF EMPLOYEESNUMBER OF FOREIGN-OWNED WORKPLACES

IN 2000, THE ÖRESUND

BRIDGE BETWEEN SWEDEN

AND DENMARK WAS

OPENED.

— 32,381 people worked in 1,648 foreign-owned work-places in Malmö (2014)

— 5% of Malmö’s workplaces were foreign-owned (excl. public sector)

— 30% of those employed in Malmö work in a foreign-owned company (excl. public sector).

— The number of foreign-owned workplaces has increased by 40% in 10 years

— The number of employees in foreign-owned workplaces has increased by 29% in 10 years

— 1,246 workplaces had employees

— 576 workplaces had 10 or more employees

— 67 workplaces had 100 or more employees

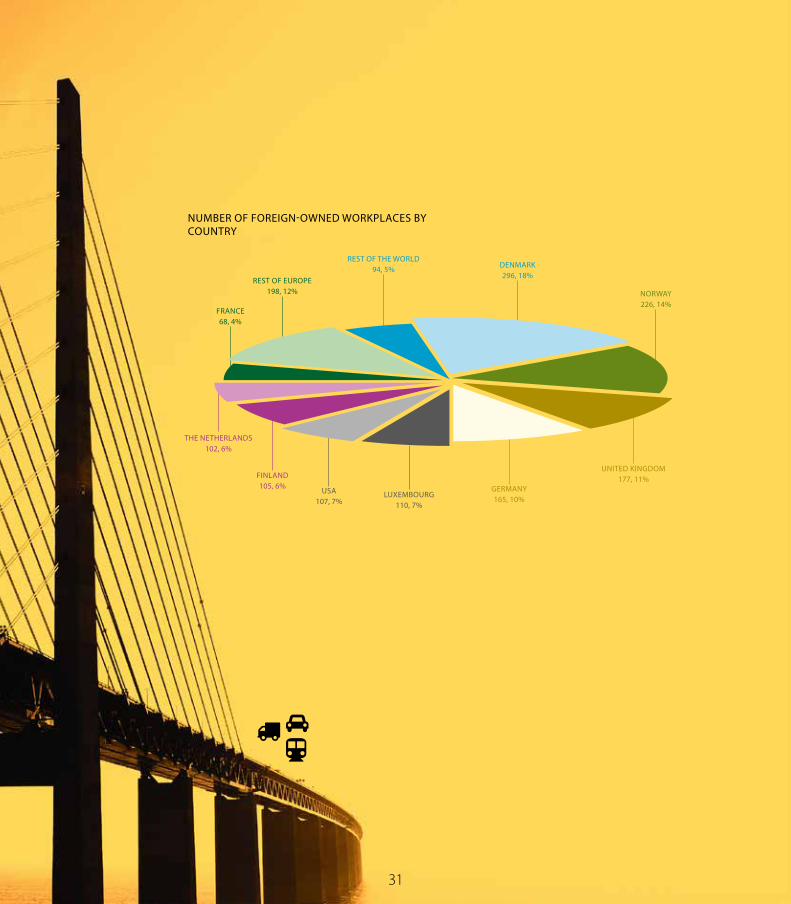

— The largest investor countries in terms of the number of workplaces: Denmark (18%), Norway (14%), United Kingdom (11%) and Germany (10%)

— The largest foreign-owned companies in Malmö include Pågen, Manpower, IKEA, Veolia, Arriva, ABB, Trygg-Hansa, E.ON, Vestas, DHL, Ubisoft Entertainment, Bravida and Atea.

— The largest numbers of workplaces are in commerce, real estate activities, consultancy services, IT and com-munications

FOREIGN-OWNED WORKPLACES

31

NUMBER OF FOREIGN-OWNED WORKPLACES BY COUNTRY

DENMARK296, 18%

NORWAY226, 14%

REST OF THE WORLD94, 5%

REST OF EUROPE198, 12%

FRANCE68, 4%

THE NETHERLANDS102, 6%

FINLAND105, 6%

USA107, 7%

LUXEMBOURG110, 7%

GERMANY165, 10%

UNITED KINGDOM 177, 11%

SOURCES: Business Register (Statistics Sweden) European Spallation Source Femern A/SJLLMalmö UniversityStatistics Sweden (SCB)Swedish Agency for Growth Policy AnalysisSwedish Public Employment ServiceØrestatØresund Bridge

All graphs in this brochure refer to Malmö. The analyses have been conducted by the Trade and Industry Agency, partly in collaboration with Malmö Tourism, the Labour Market, Upper Secondary and Adult Education Administra-tion and the Department for Urban Planning at the City of Malmö.

Publisher: Pehr Andersson, Director, Trade and Industry Agency, City of MalmöEditor and analyst: Sara Bergman, Trade and Industry Agency, City of Malmö

Circulation: 1,200 Design and production: W Communication Agency Printed by: Holmbergs

PHOTOGRAPHY:FRONT COVER: FREDRIK JOHANSSON

2-3: FREDRIK JOHANSSON, SARA BERGMAN (PORTRAIT IMAGE)

4-5: LUNDGAARD & TRANBERG ARCHITECTS (1), NORD ARCHITECTS (2), WERNER NYSTRAND (3), FOJAB ARKITEKTER (4), JERNHUSEN/TOMORROW (5), WERNER NYSTRAND (6), FREDRIK JOHANSSON (7), WERNER NYSTRAND (8)

9: LEIF JOHANSSON

10-11: LEIF JOHANSSON

12: SARA BERGMAN

14: WERNER NYSTRAND (1), APELÖGA (3), JOHAN RAMBERG (6)

22: JESPER BERG

25: LEIF JOHANSSON

BACK PAGE: LEIF JOHANSSON. THE TURNING TORSO IS SWEDEN'S TALLEST RESIDENTIAL BUILDING (190 METRES)

TRADE AND INDUSTRY AGENCYVisiting address: Lugna gatan 84Postal address: City of Malmö, SE-205 80 MalmöTelephone +46 (0)40 34 17 00 [email protected]

CITY OF MALMÖ BUSINESS PILOT The City of Malmö Business Pilot is a service function to guide you through the laws and regulations. The Pilot offers a quick and easy way into the municipality for entrepreneurs. Both existing and future businesses can contact us on anything from permits and land issues to finding the right people and authorities concerned with business and entrepreneurship in Malmö.

Telephone: 040-34 30 00 Email: [email protected]