annual report june 2018 - sindh leasing company ltd.notice is hereby given that the fifth annual...

TRANSCRIPT

Annual Report June 2018 SINDH EL ASING

1

VisionTo catalyze the untapped potential of theeconomy through ease of access to financesacross sectors – ranging from the agro-basedto industrial – leading the country towards

prosperity.

MissionPrefrably to provide lease finance and other productsa n d s e r v i c e s , t a i l o r m a d e t o s u i t t h erequirements of the customer, be it a smallf a r m e r , s m a l l a n d m e d i u m s i z eentrepreneur(s) or enterprise(s) or womanowned business, for sustainable and long term

financial solutions.

2

Annual Report June 2018 SINDH EL ASING

Corporate Information

Board of Directors

- Non-Executive Director- Non-Executive Director

- Executive Director

- Independent Non-Executive Director- Independent Non-Executive Director

CFO & Company Secretary

Mr. Rehan Anjum

Audit Committee

Registered Office

Mrs.Masooma HussainMr. Muhammad Raja AbbasMr. Muhammad Aftab Alam - Chairman

- Member - Member

Third Floor, Imperial Court BuildingDr. Ziauddin Ahmed Road, Karachi

Banker

Sindh Bank Limited

Syed Ali Murtaza KazmiMr. Muhammad Bilal SheikhMr. Naim FarooquiDr. Noor Alam

Chairman -

Chief Executive-

Auditors

BDO Ebrahim & Co.Chartered Accountants

nd2 Floor, Block C Lakson Square Building-1Sarwar Shaheed Road Karachi.

Web: www.sindhleasingltd.com

Bank Islami Pakistan Limited

Mr. Muhammad Bilal Sheikh

Dr. Noor AlamMrs.Masooma Hussain

Mr. Muhammad Aftab Alam

Syed Ali Murtaza Kazmi

Mr. Muhammad Raja Abbas

Mr. Naim Farooqui

Human Resource Committee

- Chairman - Member

-- MemberMember

Member

United Bank Limited

- Non-Executive Director

Branch Offices

Larkana / Naudero BranchRaza Shah Mohalla, VIP Road,Larkana

Hyderabad Branch

Legal Advisor

Muhammad Nadeem Khan ndSuite # 28-A, 2 Floor

Fareed Chamber Abdullah Haroon Road Karachi

Plot No. 11Faraz Villas Housing SchemeTaluka QasimabadHyderabad

Islamabad Branch

Select One Plaza, F-11 Markaz, Sindh Bank Ltd, Islamabad

Lahore Branch

2nd Floor, Plot No. S-19, R-30Shahrah-e-Quaid-e-AzamLahore

- Independent Non-Executive Director

NRSP Microfinance Bank

Annual Report June 2018 SINDH EL ASING

3

Table of Contents

Directors’ Report 05

Statement of Compliance with the Public Sector Companies (Corporate Governance) Rules, 2013 14

19

Notice of Annual General Meeting 04

Auditors’ Report to the Members

Balance Sheet

Profit and Loss Account

Cash Flow Statement

Statement of Changes in Equity

Notes to the Financial Statements

53Form of Proxy

Statement of Comprehensive Income

Review Report to the members on Statement of Compliance with Public Sector Companies (Corporate Governance) Rules, 2013

21

23

25

26

27

24

28

4

Annual Report June 2018 SINDH EL ASING

Notice of Annual General Meeting

Notice is hereby given that the fifth Annual General Meeting of Sindh Leasing Company Limited (“Company”) will be held on October 18, 2018

at 4.00 p.m. at the Registered office of the Company, Third Floor, Imperial Court Building, Dr. Ziauddin Ahmed Road, Karachi, to transact the

following business:

Normal Business:

1. To confirm the minutes of the Fourth Annual General Meeting held on October 24, 2017.

2. To receive, consider and adopt the Audited Accounts of the Company for the year ended June 30, 2018, along with the

Directors’ and Auditor's Reports thereon.

3. To approve the re-appointment of external auditors of the Company for the year ending June 30, 2019 and fix their

remuneration.

Special Business:

1. To approve amendment in Clause 3 of Articles of Association and Memorandum of Association Clause 5 during the year.

2. To approve payment of remuneration and provision of certain facilities to the CEO of the Company.

3. Any other business with the permission of the Chair.

By Order of the Board

Rehan Anjum

Company Secretary

Karachi: August 15, 2018

Annual Report June 2018 SINDH EL ASING

5

Director’s Report

On behalf of the Board of Directors of Sindh Leasing Company Limited (SLCL, the Company), it is my pleasure to present the fifth Annual Audited Financial Statements for the year ended June 30, 2018.

Review of Business and Operation

The Company earned a gross revenue of Rs. 280.193 million during the year under review against a gross revenue of Rs. 224.163 million in the corresponding year. Total administrative expenses for the year amounted to Rs 177.874 million against Rs 130.528 million last year. Profit before tax and provision for the current year is Rs 88.198 million as compared to Rs 63.064 million of the corresponding year.

Disbursement in the current year of both leases and loans amounting to Rs 2,448.483 million as compared to Rs 1,338.94 million last year and Rs. 1,800 million as per the budget for the year is an impressive growth. Our lease and loan portfolio grew by 80% despite declining 31 proposals amounting to Rs 938.610 million.

Steady growth in our lease and loan portfolio exhibits sound business acumen. Our customer screening process being tough and accurate will be maintained so as to ensure further growth of unblemished clean business portfolio. A further injection of Rs 1.5 billion equity shows the confidence that our sponsor Government of Sindh has in our company, which we are determined to maintain and enhance as we progress into the ensuing year.

During the year the company has obtained permission to issue certificates of deposit from Securities and Exchange Commission of Pakistan (SECP). Up till June 30, 2018, the Company has raised Rs. 23.9 million through issue of certificate of deposits.

Operating Results

The Company has transferred an amount of Rs. 31.667 million to revenue reserve during the year.

As at June 30, 2018, the value of investments of provident fund and gratuity fund of the Company are Rs. 19.1778 million and Rs. 9.396 million respectively.

Risk management

Principal risks in the current economic and business scenario and regulatory compliance facing the Company are as follows:

Credit Risk

The risk exposure to actual loss (opportunity cost) as a result of the default/failure to perform by a client with which SLCL does business.

Market Risk

The risk exposure due to external forces that could significantly change the fundamentals that affect any borrower’s overall objectives and strategies and may even put the borrower out of business.

Liquidity Risk

Liquidity risk is the exposure to incur loss as a result of the inability to meet cash flow obligations in a timely and cost-effective manner.

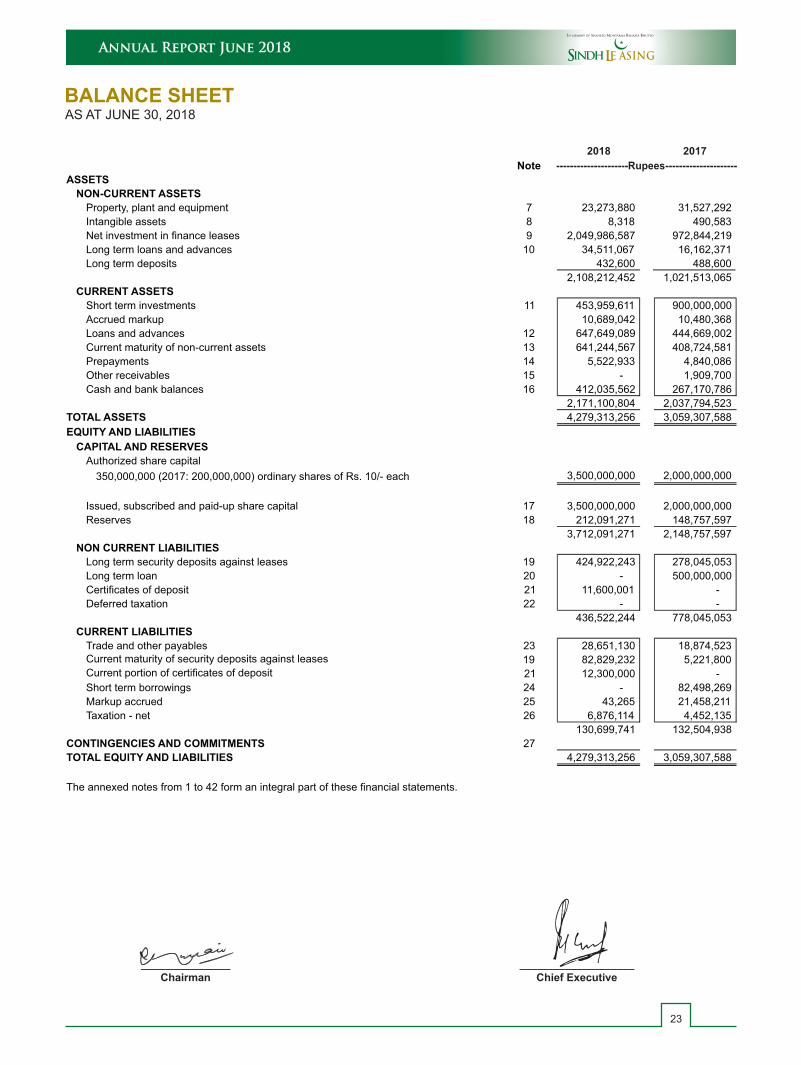

Balance SheetAs at June

30, 2018As at June

30, 2017

----------(PKR Million) ---------Paid-up capital 3,500.00 2,000.00Total equity 3,712.091 2,148.760Fixed Assets 23.274 31.530Net investment in nance leases 2,700.274 1,384.840Auto and Working capital loans 689.555 468.560

Prot & Loss

For the year Ended June

30, 2018

For the year Ended June

30, 2017

Revenue –

Net

266.073 193.594Administrative expenses 177.874 130.528Prot before provision & tax 88.198 63.065Prot after tax

63.334 44.755

EPS

0.28 0.26

6

Annual Report June 2018 SINDH EL ASING

Operational Risk

This risk arises due to operations that are inefficient and ineffective in satisfying customers and achieving the quality, cost and time objectives.

Risk management is a continuous on-going process to detect and manage risks. The above risks are managed mainly through risk-adjusted pricing of individual lease / loan transactions, setting of risk limits for individual positions or portfolios, use of guarantees, securitization of risks, buying and selling of assets, diversification, negotiation of price contracts, regular monitoring of the Company’s consolidated credit exposure and exposure limits defined by the regulator and regular risk assessment of each customer for updating its risk rating.

Board of Directors

During the year under review Mr. Anis Khan and Syed Hassan Naqvi submitted their resignations from the Board as Directors of the Company. The Board wishes to place on record its appreciation for their valuable contribution in the Company. The Board has appointed Mr. Muhammad Raja Abbas and Dr. Noor Alam as a representative of Government of Sindh as Directors of Sindh Leasing Company Limited.

Directors' Meeting

Director’s Report

S.No Name of Director

No. ofmeeting(s)

held during theTenor in the

year

Total no. of

meeting(s) attended

1 Mr. Ali Murtaza Kazmi 4 3*2 Syed Hassan Naqvi 4 2 *3 Mr. Anis Khan 4 44 Muhammad Bilal Sheikh 4 45 Mr. Muhammad Aftab Alam 4 46 Mr. M. Naimuddin Farooqui 4 47

Mrs. Masooma Hussain 4 1**

During the year under review, four meetings of the Board of Directors of SLCL were held. Attendance by each director was as follows:

* Leave of absence was granted to Directors who could not attend the Board meeting.

** Directors who has appointed during the year.

Audit Committee’s Meetings

S.No Name of DirectorNo. of meeting(s) held during the

year

Total no. of meeting(s)

attended1 Mr. Muhammad Aftab Alam 4 42 Mr. Anis Khan 4 43

Mrs. Masooma Hussain 4 1*

During the year under review, four meetings of the Audit committee of SLCL were held. Attendance by each director was as follows:

* Member who has appointed during the year.

Pattern of Shareholding

No. of shareholders

Shares held by

Shareholding No. of shares held

Percentage

From To

1 Government of Sindh

1 349,999,993 349,999,993 99.999998

7 Directors 349,999,994 350,000,000 7 0.000002

8 Total 350,000,000 100

Annual Report June 2018 SINDH EL ASING

7

The pattern of shareholding as at June 30, 2018 is as follows:

Corporate and Financial Reporting Framework

This part of the Directors’ report to shareholders is given as required under section 226 & 227 of the Companies Act 2017:

1. The financial statements prepared by the management of Sindh Leasing Company Limited present fairly its state of affairs, the result of its operations, cash flows and changes in equity.

2. Proper books of account of Sindh Leasing Company Limited have been maintained.

3. Appropriate accounting policies have been consistently applied in preparation of financial statements. Accounting estimates are based on reasonable and prudent judgment.

4. International Accounting Standards, as applicable in Pakistan, have been followed in preparation of financial statements.

5. The system of internal control is sound in design and has been effectively implemented and monitored.

6. There are no significant doubts upon the ability of Sindh Leasing Company Limited to continue as a going concern.

7. The appointment of Chairman and other members of Board and the terms of their appointment along with the Remuneration policy adopted are in the best interests of the Public Sector Company as well as in line with the best practices.

External Auditors

The Audit Committee has recommended the name of M/S BDO Ebrahim & Co., Chartered Accountants as external Auditors of the Company for the year ending June 30, 2019. The Board of Directors, on the recommendation of the Audit Committee has proposed the name of retiring auditors BDO Ebrahim & Co., Chartered Accountants as external Auditors for the next term. The retiring auditors M/s. BDO Ebrahim & Co., Chartered Accountants, being eligible, offer themselves for re-appointment in the forthcoming Annual General Meeting.

Key Operating and Financial Data

Key operating and financial data of last five years is annexed to the Annual Report.

Internal Control and Compliance

The management has devised internal controls to enhance accuracy and reliability of financial reporting. Cyclical reviews and monitoring of internal controls is given paramount importance to assert nonstop functioning of all processes which lead to accurate results. Moreover our decision to outsource the internal audit function to Grant Thornton Anjum Rahman, Chartered Accountants who report directly to the Audit Committee further supplements our confidence on our systems as they provide unbiased opinions on each testing review.

Credit Rating

JCR-VIS Credit Rating Company Limited (JCR-VIS) has maintained the entity ratings of Sindh Leasing Company Limited (SLCL) to ‘A+’ (Single A Plus) long term and ‘A-1’ (A- One) short term. Outlook on the assigned ratings is ‘Stable’.

Dividend

The Company has not declared any dividend for the year ended June 30, 2018.

Challenges

Favorable economic environment has stimulated activity in various sectors, namely the SME and Consumer sector(s). This has resulted in an increase in demand of various products that compliment ones’ lifestyle and status such as the increase in demand of Saloon cars and SUV vehicles. Commercial Banks backed by their excessive liquidity and huge margin for negotiation are always ahead in the race of taking full advantage of such financing opportunities. This challenge of Sindh Leasing Co. Ltd (SLCL) has remained unchanged to date, but our permission to raise deposits through issuance of Certificate of Deposit (COD) would put SLCL in a good enough position to face these challenges with its sound business strategy and approach.

Future Outlook

As per Monetary Policy Statement of July 2018, SBP projects FY 2019 GDP growth to be around 5.5 percent against the annual target of 6.2 percent. Further due to the risking trend of core inflation (ie 5.2 percent in June 2018) SBP’s model-based range for average CPI inflation will range from 6.00 to 7.00 percent. In order to control inflationary pressures, SBP announced a 25 bps increase in the Policy rate in January 2018, 50 bps in May 2018 and 100 bps in July 2018, increasing the Policy rate from 5.75 percent to 7.5 percent. Under

Director’s Report

8

Annual Report June 2018 SINDH EL ASING

current circumstances of deteriorating economic numbers, further rise(s) in the Policy rate cannot be ruled out.

Corporate Social Responsibility

Our company’s efforts are not only channeled towards the growth of business but also the wellbeing of society. In view of this SLCL is proud to inform that it has contributed an equivalent of one days’ salary of its employees and employer contribution into the construction of the “Daimer Basha & Mohmand Dams.”

Acknowledgements

The Board appreciates the support that our sponsors, i,e the Government of Sindh (GoS) and the confidence that its valued customers have exhibited in the Company. The company is positive this confidence would continue. The guidance and support provided by our regulators the Securities and Exchange Commission of Pakistan cannot go unrecognized. Our staff has showcased dedication and support that is expected of them and this Company could not have achieved the growth as highlighted above without this.

Muhammad Bilal Sheikh

Chief Executive

August 15, 2018

Director’s Report

Annual Report June 2018 SINDH EL ASING

9

ڈا��ز ر�رٹ

�، �رڈ آف ڈا��ز � �� � �ھ �� � � (�) � �٣٠ن �٢٠١٨ ا�م �� �� وا� �ل � ��� ��� � �ہ (audited) ا�ؤ� � ��

�� �ت �س � ر� �ں۔

ور آ�� � ��ہ �رو�را

� � ز� �ر �ل � �� آ�� (revenue) 280.193 � رو� �� � �� �ل ا� �ت � � �� آ�� (revenue) �224.163 �۔ �ل �

ز� �� � �� � ا�� ا�ا�ت �� �ل � 130.528 � رو� � �� � �177.874 رو� ر��۔ �� �ل � 63.064 � رو� � � ا

اس �ل اس � �� 88.198 � رو� ر�۔

��دہ �ل � � (lease) اور �� �ت دو�ں � � � ادا�ں � �� 2,448.483 � رو�ر� � � �� �ل اس � �� �1,338.94 رو� � اور �ل �

�� � � � و� � اس � � � � �1,800 رو� �۔�رى � (lease) اور �� �ت � �رٹ �� � ٨٠ � ا�� �ا �و�� ٢١ �� �و� � � �� 938.610

� � �د � دى �۔

رر� �ے � �� �رى �(lease) اور �� �ت � �ازن � �رى �ا� �� �� �۔�را �ز � �� ��ل � �� � (process) � اور در� � � ��ا

غاور �ف �رو�رى �رٹ �� � �� �� � � �� ��۔ �� 1.5 ارب رو� � � ��� (equity) � �رے �(sponsor) �� �ھ � �رى � � ا�د � دا

ور ��� � آ� وا� � � ��ں � � � � �� �� � ۔ ر� � ا �، � � � � ��م � � ا� ��ا�� ��������� �� ء� �رى �� � � �۔ ٣٠ �ن ٢٠١٨ �، � ڈ�زٹ � ����� � � ا�ا ��ر� ا� ا� � آف ��ن (SECP) � ڈ�زٹ � � ن� � ���ل � دورا ء� 23.9 � رو� � ا�� � � �۔���������� � � ا�ا �

� �

ادا �ہ ���

equity ��� � �

� �� ا�� �ت

� �� � �� ��� �رى

�د�ر اور ور� � �� �ت

ن � اور �ن �ل � دورا

آ�� – ��

ا�� ا�ا�ت

(provision)ز� اور �و و�ن �� � ا

ز� �� � ا

(EPS)� � آ��

ن� ٣١٫٦٦٧ � رو� � ر� آ�� (revenue) � ذ�� � � � � �۔ �ل � دورا

٣٠ �ن ٢٠١٨ � � � �او�� � اور ��� � � ��� �رى � �ر ��� �١٩٫١٧٧٨ رو� اور٩٫٣٩٦ � رو� �۔

3,500.00 2,000.00

3,712.091 2,148.760

23.274 31.530

٣٠ �ن ٣٠٢٠١٨ �ن٢٠١٧رو�

2,700.274 1,384.840

689.555 468.560

٣٠ �ن ٣٠٢٠١٨ �ن٢٠١٧رو�

266.073 193.594

177.874 130.528

88.198 63.065

63.334 44.755

0.28 0.26

10

Annual Report June 2018 SINDH EL ASING

(Risk management) رو�رى �ے � � ا�� ڈ���

� � در � �دى �رو�رى �ات ��دہ � ، �رو�رى � �� اور ا�� (regulatory)� �درج ذ� �:

�� � �ن � �ہ

ن� � � � � �د�ہ ��/ � �ر�د� د�� � در� �ہ درا� �رو�رى �ن (�رو�رى �� � ��) � � � �SLCL � �� �رو�ر �� � ا

�� م � � � � � �۔

�ر� � �ہ

ہ�ض �اہ � �رو�ر �و� ��ں � �� � در� �ہ �� � � ا��ں � �� �� � � �ض �اہ � �� �� اور � �ں � �� �� � اور � � � � و

� � �ل دے۔

� � (liquidity) � �ہ

�� � �� � و� � � ��وا� �ن �۔ ر�ں ��را اور ��� �� � �� � � � ذ� دا � � � �ہ �ض �اہ � �و� �را

آ�� (operational) � �ہ

�� ��� � �� اور �د، �� اور و� � �� �� �� � �� اور � ��� آ�� � �ا �� �۔��� � �ہ �� �

غ�� اور اس � ا�م �ے۔ ��رہ � �ات � ا�م ا� � ا�ادى �/(lease)�ض �ے � � ا� � �رى �� � (process)� �� �وں � �ا

� � د�، � �ے- �� �ہ � � ذر� � �� �، ا�ادى �ز� � �رٹ �� � ��ے � �ود � � � �� �، �� � ا� ل � �� �، �ے � �ظ

� �� �، ا�� �ت � �� و �و� � ��، �ع، �ں � �ا�ات، ��ات، �ا� � � ا�م �ہ �� � ا�زر اورر�� � �� � ا�زر � � �ود اور �

�� � � �ے � �ا� � � اور اس �ے � در� �ى � ��۔

�رڈز آف ڈا��ز

ن� � � � � �� وا� ��ت � �ا� �� اس �ت � ےد� �۔۔ �رڈ ا ز�ِ �ر �ل � �ب ا� �ن اور � � �ى � � �رڈ آف ڈا��ز � ا� د

ر�رڈ � �� �� �۔۔ �رڈ � �ر �ھ �� � � ڈا��ز � �ب � را� �س اور ڈا� �ر �� �ر ��ہ �ھ �ر� � ا�ب �� �۔

ڈا��ز � ا�س

ن �SLCL �رڈ آف ڈا��ز � �ر ا�س ��۔ � ڈا�� � ��ى � � درج ذ� � ز� �ر �ل � دورا

Annual Report June 2018 SINDH EL ASING

11

�س � �اد

� �ل � � �� � �� � � ڈا��ز � �م � �ر

4 3* �ب � �� �� 1

4 2 * � � �ى 2

4 4 �ب ا� �ن 3

4 4 �ب � �ل � 4

4 4 �ب � آ�ب �� 5

4 4 �ب � � ا�� �رو� 6

4 1** � �� �� 7

�س � �اد

� �ل � � �� � �� � � ڈا��ز � �م � �ر

4 4 �ب � آ�ب �� 1

4 4 �ب ا� �ن 2

4 1 �ز �� � 3

ےدى �۔ ن� اس ا�س � ر� د *� ڈا�� ا�س � �� � �� ا

نا�ب �ا۔ ہڈا��ز � � �ل � دورا ** و

آڈٹ � � ا�س

ز� �ر �ل � � � آڈٹ � � �ر ا�س ��۔ � ڈا�� � ��ى � � درج ذ� �؛

نا�ب �ا۔ ہڈا��ز � � �ل � دورا *و

12

Annual Report June 2018 SINDH EL ASING

� ر� � ر�ن

٣٠ �ن ٢٠١٨ � � ر� � ر�ن درج ذ� �:

� اور ��� ر�ر� ڈ�� را ادا

� ��رز � � ڈا�� � ر�رٹ � � � ٢٠١٧ � � ا� � � � ٢٢٦ اور ٢٢٧ � � �ورى �

١. �ھ �� � � � � � �ر �دہ ��� �� ت (statements) آ�� � ��، � � اور ا�� � رد و�ل � ��ت � � �� � �� � ۔

٢. �ھ �� � � ���ں � ��ں (books) � �� �ر � ر� �۔

٣. ��� د�و�ات � �رى � �� ا�ؤ� ��ں � ا�ل � � �۔ ا�ؤ� �ں � �د �� اور �ظ ا�ازے �۔

� � �۔ ن � �رآ ٤. ��� د�و�ات � �رى � � ا��ا� ا�و� �ر ، � ��ن � �� �� �، ا��

٥. ا�رو� �ا� � �م � ڈ�ا� �ط � اور اس � ��� �ر � �ذ � � � � اور �ا� � �� �

رے � �� � �� � �رے � �� �ص �ت � �۔ ٦. �ھ �� � � � ا� �رى ر� وا� ادا

ن� ��وں � �� � �� �� � � � � �� �د � اور �� ��ں � ا�ل نا�ب � �ت اور ا ن � ا�ب ، ا ٧. �� اور �رڈ � د� �ا

� �۔

ا�� آڈ�ز���� ���� � � � �۔ �رڈ آف ڈا��ز ،آڈٹ � � �رش � � �م ٣٠ �ن ٢٠١٩ � ا�م �� �ل � � � �رش وا�ا� ا� �، �ر�ڈ ا�و ����آڈٹ � �ز � ڈى ا � �ر �و� آڈ�ز � ا� �ت � � ا�ب � � �م �� � � �۔ �وش �� وا� آڈ�ز �ز � ���� وا�ا� ا� �، �ر�ڈ ا�و �����وش �� آڈ�ز �ز � ڈى ا ہا� آپ � ��� �م ا�س � دو�رہ ا�ب � � � � ر� �۔ ���� ہدو�رہ � � � اور و � اس �ت � ا� � � و وا�ا� ا� �، �ر�ڈ ا�و ڈى ا

ا� آ�� اور ��� ا�اد و�ر

�� �� ��ں � ا� آ�� اور ��� ا�اد و�ر اس ��� ر�رٹ � �� � �۔

ا�رو� �ا� اور �

ہ ���� � ��� ر�ر� � در� اور � �� � � ا�رو� �ا� � �� اور اس � �ذ � �۔�ر �ر ا�رو� �ا� � ��ہ اور �ا� � ا�� ا� دى � � �� و�ق � و �� ���� � آڈٹ � � �اہ را� ِ���� �م �� � (processes) � �م �� ر� � در� �� �ا �� �۔ ا�رو� آڈٹ � �م �ا� �� ا� ر�ن، �ر�ڈ ا�و

ہ� �� � ��ے � � ��ارى � را� د� �۔ ر�رٹ �� �، � �د �� � � �ا� �م � �رے ا�د � ا�� � � �� و

11349,999,993349,999,99399.999998

7349,999,994350,000,00070.000002

8350,000,000100

Annual Report June 2018 SINDH EL ASING

13

��ٹ ر���� �

رر� � ر� ��JCR-VISٹ ر� � � (JCR-VIS) � �ھ �� � � � �� ا�ت ا�(entity) ر�+Aاور � ا�ت ر� ��A-1ا

� آؤٹ � � �

�� �

� � �٣٠ن ٢٠١٨ � � �� وا� �ل � � � � �� � ا�ن � � �۔

در� ��

�ا� �� ��ل �د �ز، � SMEاور �ر�، � ���ں � �وغ د�۔ اس � � �د ��ت � � � ا�� � � ��ں � ر� � اور � �

ور �SUVڑ�ں � � � ا�� � �� �۔�ر� � ا� � � � (liquidity) اور �ت � �� � ��ى ��وا د� � � � �ن (saloon car)�را

���ٹ (margin) � و� � ا� �رو�رى �ا�ں � ��ہ ا�� � � � اس �� � ر� � � � ر� � ۔�ھ �� � � (SLCL)� در� � ور � �SLCL اس � � � � �ز� � �������� ء� ذر� ڈ�ز� � ا�� � � ا ن� ا�ا ء� ا�زت � ا �� � ا�ا � و� � ��د �، � � ڈ�زٹ � �

ن�� � � �ر �� � � �۔ � اور ا�وچ � �د � ا

�� � � �

�SBP ��� ٢٠١٨ � ��� �� � �ن � �� �ل ٢٠١٩ � � �� �� �اوار (GDP) � � �ا�ازہ �� ٥٫٥ � � � ���GDP �٦٫٢ �ف

�۔ �� � � �دى ا�اط زر (�ن ٢٠١٨ � �٥٫٢) ��� ر�ن ، � � �SBP �ڈل � �د � �رف � � ٦ � ٧ � � ر� � ر� �۔ ا�اط زر � � د�ؤ

� �� �� � �، �SBP �� �خ � ٢٥ � �ا� � ا�� �رى ٢٠١٨ � �، ٥٠ � �ا� � ٢٠١٨ اور ١٠٠ � �ا� ��� ٢٠١٨ � ا�� � اور �� �خ

� ٥٫٧٥ � ��٧٫٥ ا�� �د�۔��دہ ا� �� ���� ا�ادو�ر � �ر�ل �، �� ا��(ا��) � ا�ن � �د � � � �۔

رى را� �� ذ� دا ادا

�رى �� � �ف �رو�ر � �� � � � ��ے � �ى � � � �۔ SLCLاس � � اس �ت � ا�ع د� �� � �س �� � � اس � �ز� �

ا� دن � �اہ � �وى ر� ڈ�� اور � ڈ� � � �وا� � اور اس � آ� � �� �۔

ا�ر �

��ر� ا� ا� � آف ������ � ا� ا��ز ، �ر� آف �ھ، اور �ز � ��رز � �� � �ا� � � ا�ں � � � ا�د �۔ � ا� � � � ا�د �رى ر� �۔

��ن � �� � � �� وا� ر�� اور � � �� �ا� � � ر� � �۔ �رے ً � � �� � اور �� � �� �� � � � � � �د � � � ��رہ �� ��

�� � � � � � اس � �� � �۔

� �ل �

� ا���

١٥ ا� ٢٠١٨

14

Annual Report June 2018 SINDH EL ASING

Statement of Compliance with the Public Sector Companies (Corporate Governance) Rules, 2013

Name of Company: Sindh leasing Company Limited Name of line ministry: Finance Ministry

I. This statement presents the overview of the compliance with the Public Sector Companies (Corporate Governance) Rules, 2013 (hereinafter called “the Rules”) issued for the purpose of establishing a framework of good governance, whereby a public sector company is managed in compliance with the best practices of public sector governance.

II. The company has complied with the provisions of the Rules in the following manner:

S. No.

Provision of the RulesRule No.

Y N

Tick the relevant box

1.The independent directors meet the criteria of independence, as dened under the Rules.

2(d) √

2.

The Board has at least one-third of its total members as independent directors. At present the Board includes:

Category NamesDate of

appointmentIndependent Directors

1. Mr. Muhammad Aftab Alam

2. Mr. Raja Muhammed Abbas

3. Mr. Ali Murtaza Kazmi

October 24, 2017

April 27, 2018

October 24, 2017

Executive Directors

Mr. Mohammad Bilal Sheikh October 24, 2017

Non-Executive Directors

1. Mr. Asif Jahangir

2. Naim Farooqui

3. Mrs. Masooma Hussain

April 27, 2018

October 24, 2017October 24, 2017

3(2)

√

3.

The directors have conrmed that none of them is serving as a director on more than ve public sector companies and listed companies simultaneously, except their subsidiaries.

3(5) √*

4.The appointing authorities have applied the t and proper criteria given in the Annexure in making nominations of the persons for election as board members under the provisions of the Act.

3(7) √

5.The chairman of the board is working separately from the chief executive of the Company.

4(1) √

6.The chairman has been elected by the Board of directors except where Chairman of the Board has been appointed by the Government.

4(4) √

7.The Board has evaluated the candidates for the position of the chief executive on the basis of the t and proper criteria as well as the guidelines specied by the commission.

5(2) √

8.

(a) The company has prepared a “Code of Conduct” to ensure that professional standards and corporate values are in place.

(b) The Board has ensured that appropriate steps have been taken to disseminate it throughout the company along with its supporting policies and procedures, including posting the same on the company’s website.

5(4) √

(www.sindhleasingltd.com)

(c) The Board has set in place adequate systems and controls for the identication and redressal of grievances arising from unethical practices.

Annual Report June 2018 SINDH EL ASING

15

9.The Board has established a system of sound internal control, to ensure compliance with the fundamental principles of probity and propriety; objectivity, integrity and honesty; and relationship with the stakeholders, in the manner prescribed in the Rules.

5(5) √

10.The Board has developed and enforced an appropriate conict of interest policy to lay down circumstances or considerations when a person may be deemed to have actual or potential conict of interests, and the procedure for disclosing such interest.

5(5)(b) (ii)

√

11.The Board has developed and implemented a policy on anticorruption to minimize actual or perceived corruption in the company.

5(5)(b) (vi)

√

12.The Board has ensured equality of opportunity by establishing open and fair procedures for making appointments and for determining terms and conditions of service.

5(5)(c)(ii)

√

13.

The Board has ensured compliance with the law as well as the company’s internal rules and procedures relating to public procurement, tender regulations, and purchasing and technical standards, when dealing with suppliers of goods and services.

5(5)(c) (iii)

√

14.The Board has developed a vision or mission statement and corporate strategy of the company.

5(6)√

15.The Board has developed signicant policies of the company. A complete record of particulars of signicant policies along with the dates on which they were approved or amended, has been maintained.

5(7) √

16.

The Board has quantied the outlay of any action in respect of any service delivered or goods sold by the Company as a public service obligation, and have submitted its request for appropriate compensation to the Government for consideration.

5(8) N/A

17.The Board has ensured compliance with policy directions requirements received from the Government.

5(11)

18.

(a) The Board has met at least four times during the year.

(b) Written notices of the board meetings, along with agenda and working papers, were circulated at least seven days before the meetings.

(c) The minutes of the meetings were appropriately recorded and circulated.

6(1)

6(2)

6(3)

√

19.

The Board has monitored and assessed the performance of senior management on annual/half-yearly/quarterly basis* and held them accountable for accomplishing objectives, goals and key performance indicators set for this purpose.

8(2) √

20.The Board has reviewed and approved the related party transactions placed before it after recommendations of the audit committee. A party wise record of transactions entered into with the related parties during the year has been maintained.

9 √

21.The Board has approved the prot and loss account for, and balance sheet as at the end of the rst second and third quarter of the year as well as the nancial year end, and has placed the annual nancial statements on the company’s website.

10 √

22.

All the Board members underwent an orientation course arranged by the company annually to apprise them of the material developments and information as specied in the Rules.

11 √

23.

(a) The Board has formed the requisite committee, as specied in the Rules.(b) The Committees were provided with written term of reference dening their

duties, authority and composition.

12 √

16

Annual Report June 2018 SINDH EL ASING

(c) The minutes of the meetings of the committee were circulated to all the Board members.

(d) The committees were chaired by the following non-executive directors:

Committee Number of Members

Name of Chair

Audit Committee Three Mohd. Aftab AlamRisk Management Committee

Three Ali Murtaza Kazmi

Human Resources Committee

Four Asif Jahangir

Procurement Committee Three Raja Mohd. AbbasNomination Committee Four Ali Murtaza Kazmi

24.The Board has approved appointment of Chief Financial Ofcer, Company Secretary and Chief Internal Auditor, by whatever name called, with their remuneration and terms and conditions of employment, and as per their prescribed qualications.

13 √

25.The Chief Financial Ofcer and the Company Secretary have requisite qualication prescribed in the Rules.

14

26. The company has adopted International Financial Reporting Standards notied by the Commission under clause sub-section (1) of section 225 of the Act.

16 √

27.The directors’ report for this year has been prepared in compliance with the requirements of the Act and the Rules and fully described the salient matters required to be disclosed.

17 √

28.The directors, CEO and executives, or their relatives, are not, directly or indirectly, concerned or interested in any contract or arrangement entered into by or on behalf of the company except those disclosed to the company.

18 √

29.

(a) A formal and transparent procedure for xing the remuneration packages of individual directors has been set in place and no director is involved in deciding his own remuneration.

(b) The annual report of the company contains criteria and details of remuneration of each director.

19 √

30. The nancial statements of the company were duly endorsed by the chief executive and chief nancial ofcer, before approval of the board.

20 √

31.

The Board has formed an audit committee, with dened and written terms of reference, and having the following members:

Name of member CategoryProfessional background

Mr. Mohammed Aftab Alam

Independent Chartered Accountant

Mrs. Masooma Hussain Non-Executive BankingMr. Raja Muhammad Abbas

Non-Executive Bureaucrat

The Chief executive and chairman of the Board are not members of the audit committee.

21(1)and

21(2)

√

32.

(a) The chief nancial ofcer, the chief internal auditor, and a representative of the external auditors attended all meetings of the audit committee at which issues relating to accounts and audit were discussed.

(b) The audit committee met the external auditors, at least once a year, without the presence of the chief nancial ofcer, the chief internal auditor and other executives.(c) The audit committee met the chief internal auditor and other members of the internal audit function, at least once a year, without the presence of chief nancial ofcer and the external auditors.

21(3)√

Annual Report June 2018 SINDH EL ASING

17

33.

(a) The Board has set up an effective internal audit function, which has an audit charter, duly approved by the audit committee.(b) The chief internal auditor has requisite qualication and experience

22 √

prescribed in the Rules.(c) The internal audit reports have been provided to the external auditors for their review.

34.The external auditors of the company have conrmed that the rm and all its partners are in compliance with International Federation of Accountants (IFAC) guideline on Code of Ethics as applicable in Pakistan.

23(4) √

35.The auditors have conrmed that they have observed applicable guidelines issued by IFAC with regard to provision of non-audit services.

23(5) √

√ * Not applicable for Government Nominee Director.

MUHAMMAD BILAL SHEIKH AND MASOOMA HUSSAINCEO & Chairman Board of Directors

18

Annual Report June 2018 SINDH EL ASING

Explanation for Non-Compliance with thePublic Sector Companies (Corporate Governance) Rules, 2013

We confirm that all other material requirements envisaged in the Rules have been complied with except for the following, toward which reasonable progress is being made by the Company to seek compliance by the end of June 30, 2018:

S.No Rule/sub-ruleno

Reason for non-compliance Future course of action

1. Rule 6(2) The Chairman was approving the notices of meetings including the agenda verbally.

From now all notices of meetings will be approved by the Chairman in writing before their circulation.

MUHAMMAD BILAL SHEIKH AND MASOOMA HUSSAINCEO & Chairman Board of Directors

Annual Report June 2018 SINDH EL ASING

19

Review Report to the Members on Statement of Compliance with thePublic Sector Companies (Corporate The Government) Rules, 2013

Place: Karachi

Dated: August 15, 2018CHARTERED ACCOUNTANTS

Engagement Partner: Mr. Raheel Shahnawaz

We have reviewed the enclosed Statement of Compliance with the best practices contained in Public SectorCompanies

(Corporate Governance) Rules 2013 (the Rules) for the year ended June 30, 2018 prepared by the Board of Directors of

Sindh Leasing Company Limited to comply with the provisions of the Rules.

The responsibility for compliance with the Rules is that of the Board of Directors of the Company. Our responsibility is to

review, to the extent where such compliance can be objectively verified, whether the Statement of Compliance reflects

the status of the Company's compliance with the provisions of the Rules and report if it does not and to highlight any

non-compliance with the requirements of the Rules. A review is limited primarily to inquiries of the Company's personnel

and review of various documents prepared by the Company to comply with the Rules.

As a part of our audit of the financial statements we are required to obtain an understanding of the accounting and

internal control systems sufficient to plan the audit and develop an effective audit approach. We are not required to

consider whether the Board of Directors' statement on internal control covers all risks and controls or to form an opinion

on the effectiveness of such internal controls, the Company's corporate governance procedures and risks.

The Rules requires the Company to place before the Audit Committee, and upon recommendation of the Audit

Committee, place before the Board of Directors for their review and approval its related party transactions distinguishing

between transactions carried out on terms equivalent to those that prevail in arm's length transactions and transactions

which are not executed at arm's length price and recording proper justification for using such alternate pricing

mechanism. We are only required and have ensured compliance of this requirement to the extent of the approval of the

related party transactions by the Board of Directors upon recommendation of the Audit Committee. We have not carried

out any procedures to determine whether the related party transactions were undertaken at arm's length price or not.

Based on our review, nothing has come to our attention which causes us to believe that the Statement of Compliance

does not appropriately reflect the Company’s compliance, in all material respects with the best practices contained in the

Rules as applicable to the Company for the year ended June 30, 2018.

Further, we highlight below instance of non-compliance with the requirements of the Rules reflected in the paragraph 17

where these are stated in the Statement of Compliance.

2nd Floor, Block C LaksonSquare Building-1Sarwar Shaheed Road Karachi.

S.No. Reference Clause description

Written notices of meetings, including the agenda, are not approved by the Chairman.Rule 6(2)1

20

Annual Report June 2018 SINDH EL ASING

27.04

32.71

44.25

44.75

63.33

Financial Highlights

(Rs. in million)

2014 2015 2016 2017 2018

Operational Results

Gross Revenues 50.32 100.62 125.63 224.16

Financial Charges 0.00 0.85 11.09 30.57

Gross Margin 50.32 70.25 114.54 193.59

Prot Before Taxation 39.77 46.38 52.03 56.85

Prot After Taxation 27.04 32.71 44.25 44.75

Balance Sheet

Net Investment in Leases 40.00 444.19 852.04 983.85

Shareholders' Equity 1,000.00 1,000.00 1,000.00 2,000.00

Total Liabilities 23.93 182.69 413.34 910.55

Total Assets 1,050.96 1,242.44 1,517.35 3,059.31

Year 2017-18

Equipment

Vehicles

Prot After TaxationProt Before Taxation

Category-wise Lease Disbursements Rs. 1,338.00 Million

Year 2016-17

Equipment

Machinery

Vehicles

0

500

1000

1500

Rs. in

millio

n

Net Investment in Lease Finance

Total Asset Base

0

500

1000

1500

2000

2500

Rs. in

millio

n

Gross Income vs Financial Cost

Rs. in

millio

n

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Rs. in

millio

n

Machinery

Category-wise Lease Disbursements Rs. 2,448.00 Million

Rs. in

mil

lio

n

0

25

50

75

100

39.77

46.38

52.03

56.85

75.04

YEARS

2014 2015 2016 2017 2018

50.32

100.62

125.63

224.16

280.19

0.00 0.85 11.09

30.57 14.12

0

50

100

150

200

250

300

280.19

14.12

266.07

75.04

63.33

2,700.27

3,500.00

567.22

4,279.31

Rs. in

mil

lio

n

0

25

50

75

100

YEARS

2014 2015 2016 2017 2018

YEARS

2014 2015 2016 2017 2018

Shareholders Equity

1,000.00 1,000.00 1,000.00

2,000.00

3,500.00

YEARS

2014 2015 2016 2017 2018

YEARS

2014 2015 2016 2017 2018

YEARS

2014 2015 2016 2017 2018

40.00

444.19

852.04 983.85

4,279.31

2,700.27

3,059.31

1,242.441,517.35

1,050.96

23%

70%

7%8% 24%

68%

Vehicles

Machinery EquipmentMachinery

Vehicles

Equipment

Annual Report June 2018 SINDH EL ASING

21

Auditors’ Report to the MembersOpinion

We have audited the annexed financial statements of Sindh Leasing Company Limited (the Company), which comprise the statement of financial position as at June 30,2018, and profit and loss account, the statement of comprehensive income, the statement of cash flows and the statement of changes in equity for the year then ended, and notes to the financial statements, including a summary of significant accounting policies and other explanatory information, and we state that we have obtained all the information and explanations which, to the best of our knowledge and belief, were necessary for the purposes of the audit.

In our opinion and to the best of our information and according to the explanations given to us, the statement of financial position, profit and loss account, statement of comprehensive income, the statement of cash flows and the statement of changes in equity together with the notes forming part thereof conform with the accounting and reporting standards as applicable in Pakistan and give the information required by the Companies Act, 2017 (XIX of 2017), in the manner so required and respectively give a true and fair view of the state of the Company's affairs as at June 30, 2018 and of the profit and other comprehensive income, its cash flows and the changes in equity and for the year then ended.

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs) as applicable in

Pakistan. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants as adopted by the Institute of Chartered Accountants of Pakistan and we have fulfilled our other ethical responsibilities in accordance with the Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Information Other than the Financial Statements and Auditor’s Report Thereon

Management is responsible for the other information. The other information comprises the information included in the annual report but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Board of Directors for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with the accounting and reporting standards as applicable in Pakistan and the requirements of Companies Act, 2017 (XIX of 2017) and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Board of directors are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance but is not a guarantee that an audit conducted in accordance with ISAs as applicable in Pakistan will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs as applicable in Pakistan, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

22

Annual Report June 2018 SINDH EL ASING

• Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with the board of directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Report on Other Legal and Regulatory Requirements

Based on our audit, we further report that in our opinion:

a) proper books of account have been kept by the Company as required by the Companies Act, 2017 (XIX of 2017);

b) the statement of financial position, the profit and loss account and other comprehensive income, the statement of cash flows and the statement of changes in equity together with the notes thereon have been drawn up in conformity with the Companies Act, 2017 (XIX of 2017) and are in agreement with the books of account and returns;

c) investments made, expenditure incurred and guarantees extended during the year were for the purpose of the Company’s business; and

d) in our opinion, no Zakat was deductible at source under the Zakat and Ushr Ordinance, 1980.

The engagement partner on the audit resulting in this independent auditor’s report is Raheel Shahnawaz.

Auditors’ Report to the Members

Date: August 15, 2018

Place:Karachi

CHARTERED ACCOUNTANTS

Annual Report June 2018 SINDH EL ASING

23

BALANCE SHEETAS AT JUNE 30, 2018

___________ ___________________Chairman Chief Executive

Note

ASSETS

NON-CURRENT ASSETS

Property, plant and equipment 7 23,273,880 31,527,292

Intangible assets 8 8,318 490,583

Net investment in nance leases 9 2,049,986,587 972,844,219

Long term loans and advances 10 34,511,067 16,162,371

Long term deposits 432,600 488,600

2,108,212,452 1,021,513,065

CURRENT ASSETS

Short term investments 11 453,959,611 900,000,000

Accrued markup 10,689,042 10,480,368

Loans and advances 12 647,649,089 444,669,002

Current maturity of non-current assets 13 641,244,567 408,724,581

Prepayments 14 5,522,933 4,840,086

Other receivables 15 - 1,909,700

Cash and bank balances 16 412,035,562 267,170,786

2,171,100,804 2,037,794,523

TOTAL ASSETS 4,279,313,256 3,059,307,588

EQUITY AND LIABILITIES

CAPITAL AND RESERVES

Authorized share capital

3,500,000,000 2,000,000,000

Issued, subscribed and paid-up share capital 17 3,500,000,000 2,000,000,000

Reserves 18 212,091,271 148,757,597

3,712,091,271 2,148,757,597

NON CURRENT LIABILITIES

Long term security deposits against leases 19 424,922,243 278,045,053

Long term loan 20 - 500,000,000

Certicates of deposit 21 11,600,001 -

Deferred taxation 22 - -

436,522,244 778,045,053

CURRENT LIABILITIES

Trade and other payables 23 28,651,130 18,874,523

19 82,829,232 5,221,800

21 12,300,000 -

Short term borrowings 24 - 82,498,269

Markup accrued 25 43,265 21,458,211

Taxation - net 26 6,876,114 4,452,135

130,699,741 132,504,938

CONTINGENCIES AND COMMITMENTS 27

TOTAL EQUITY AND LIABILITIES 4,279,313,256 3,059,307,588

The annexed notes from 1 to 42 form an integral part of these nancial statements.

350,000,000 (2017: 200,000,000) ordinary shares of Rs. 10/- each

Current maturity of security deposits against leases

Current portion of certicates of deposit

2018 2017

---------------------Rupees---------------------

24

Annual Report June 2018 SINDH EL ASING

PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED JUNE 30, 2018

___________________Chief Executive

INCOME

Income from nance lease, auto loans and

working capital loans 218,043,583 140,057,430

Return on investments and deposits 28 61,204,260 83,005,628

Other income 945,608 1,100,709

280,193,451 224,163,767

EXPENSES

Finance cost 29 (14,120,926) (30,570,708)

Administrative expenses 30 (177,874,448) (130,528,171)

Prot before provision and taxation 88,198,077 63,064,888

Provision for potential lease losses (10,884,770) (4,004,759)

Provision against working capital loans (2,000,000) (2,285,790)

Provision against auto nance loans (275,948) -

Reversal of provision against auto nance loans - 74,849

Prot before taxation 75,037,359 56,849,188

Taxation 31 (11,703,685) (12,094,236)

Prot for the year 63,333,674 44,754,952

Earnings per share - basic and diluted (Rupee) 32 0.28 0.26

The annexed notes from 1 to 42 form an integral part of these nancial statements.

Note

2018 2017

---------------------Rupees---------------------

___________Chairman

Annual Report June 2018 SINDH EL ASING

25

STATEMENT OF COMPREHENSIVE INCOMEFOR THE YEAR ENDED JUNE 30, 2018

___________________Chairman Chief Executive

Prot for the year 63,333,674 44,754,952

Other comprehensive income - -

Total comprehensive income for the year 63,333,674 44,754,952

The annexed notes from 1 to 42 form an integral part of these nancial statements.

Note

2018 2017

---------------------Rupees---------------------

___________

26

Annual Report June 2018 SINDH EL ASING

___________

CASH FLOW STATEMENTFOR THE YEAR ENDED JUNE 30, 2018

___________ ___________________Chairman Chief Executive

CASH FLOW FROM OPERATING ACTIVITIES

Prot before taxation 75,037,359 56,849,188

Adjustment for:

Depreciation 6,559,919 6,929,174

Amortization 482,265 483,587

Property, plant and equipment written off 2,866,664 -

Provision for potential lease losses 10,884,770 4,004,759Provision against working capital loans 2,000,000 2,285,790

Provision against auto nance loans 275,948 -

Reversal of provision against auto nance loans - (74,849)

Gain on disposal of property, plant and equipment (435,842) (540,025)

Finance cost 14,120,926 30,570,708

36,754,650 43,659,144

Operating prot before working capital changes 111,792,009 100,508,332

Movement in working capital

Decrease / (increase) in current assets

Long term loans and advances 3,540,805 652,600

Long term deposits 56,000 (114,000)

Prepayments (682,847) (339,755)

Other receivables 1,909,700 (1,909,700)Accrued markup (208,674) (8,633,749)

Increase in current liabilities

Trade and other payables 9,776,607 8,210,424

14,391,591 (2,134,180)

Cash generated from operations 126,183,600 98,374,152

Finance cost paid (35,535,872) (10,481,812)

Taxes paid (9,279,706) (7,999,821)

Increase in net investment in nance lease (1,315,434,188) (532,797,068)

(Increase) / decrease in auto nance loan (27,278,385) 7,543,137

Increase in loans and advances (204,980,087) (225,771,009)

Increase in security deposit against leases 224,484,622 132,315,153

(1,368,023,616) (637,191,420)

Net cash used in operating activities (1,241,840,016) (538,817,268)

CASH FLOW FROM INVESTING ACTIVITIES

Capital expenditure incurred - own use and intangible assets (1,747,829) (13,254,117)

Proceeds from sale of property, plant and equipment 1,010,500 2,822,066

Short term investments - net 446,040,389 (560,259,597)

Net cash generated from / (used in) investing activities 445,303,060 (570,691,648)

(570,691,648)

CASH FLOW FROM FINANCING ACTIVITIES

Proceeds from certicates of deposit 23,900,001 -

Proceeds from issue of shares 1,500,000,000 1,000,000,000

Long term loan (500,000,000) 250,000,000

Short term borrowings (82,498,269) 82,498,269

Net cash generated from nancing activities 941,401,732 1,332,498,269

Net increase in cash and cash equivalents 144,864,776 222,989,353

Cash and cash equivalents at beginning of the year 267,170,786 44,181,433

Cash and cash equivalents at end of the year 412,035,562 267,170,786(0) 0.34

The annexed notes from 1 to 42 form an integral part of these nancial statements.

Note

2018 2017

---------------------Rupees---------------------

Annual Report June 2018 SINDH EL ASING

27

STATEMENT OF CHANGES IN EQUITYFOR THE YEAR ENDED JUNE 30, 2018

___________________Chairman Chief Executive

Capital reserve

Revenue

reserve

Note

Balance as at July 1, 2016 1,000,000,000 43,889,335 60,113,310 1,104,002,645

Transaction with owner

Shares issued during the year 1,000,000,000 - - 1,000,000,000

Total comprehensive income for the year

Prot for the year - - 44,754,952 44,754,952

Other comprehensive income - - - -

- - 44,754,952 44,754,952

Transfer to statutory reserve 18.1 - 22,377,476 (22,377,476) -

Balance as at June 30, 2017 2,000,000,000 66,266,811 82,490,786 2,148,757,597

Transaction with owner

Shares issued during the year 1,500,000,000 - - 1,500,000,000

Total comprehensive income for the year

Prot for the year - - 63,333,674 63,333,674

Other comprehensive income - - - -

- - 63,333,674 63,333,674

Transfer to statutory reserve 18.1 - 31,666,837 (31,666,837) -

Balance as at June 30, 2018 3,500,000,000 97,933,648 114,157,623 3,712,091,271

The annexed notes from 1 to 42 form an integral part of these nancial statements.

---------------------------------------- Rupees----------------------------------------

Issued,

subscribed and

paid-up share

capital

TotalUn-

appropriated

prot

Statutory

reserve

___________

28

Annual Report June 2018 SINDH EL ASING

FOR THE YEAR ENDED JUNE 30, 2018

NOTES TO THE FINANCIAL STATEMENTS

1. LEGAL STATUS AND NATURE OF BUSINESS

Sindh Leasing Company Limited (the Company) was incorporated in Pakistan on December 16, 2013 as an unlisted public company under the repealed Companies Ordinance, 1984. The Company was granted license on March 27, 2014 to carry out leasing business as a Non-Banking Finance Company (NBFC) under the Non-Banking Finance Companies (Establishment and Regulations) Rules, 2003.

100% shares of the Company are held by the Government of Sindh.

JCR-VIS Credit Rating Company Limited (JCR-VIS) has assigned A+ and A-1 ratings to the Company for medium to long term and short term respectively. The rating has been reaffirmed on May 28, 2018. The license of the Company to carry out the business of leasing has been renewed and valid for a period of three years w.e.f January 24, 2017.

2. GEOGRAPHICAL LOCATION AND ADDRESSES OF BUSINESS UNITS

"The registered office of the Company is situated at 3rd Floor, Imperial Court Building, Dr. Ziauddin Ahmad Road, Karachi. The Company presently has five branch offices located as follows:

- Plot # 117-118, Shah Abdul Latif Educational Trust, Block -A, Sindhi Muslim Cooperative Housing Society, Karachi,

- Plot No.11, Faraz Villas Housing Scheme, Taluka Qasimabad, Hyderabad,

- Second Floor, Plot No.S-19 R-30, Shahrah-e-Quaid-e-Azam, Lahore,

- F-11 Markaz, Islamabad, and

- Raza Shah Mohalla, VIP Road, Larkana, Naudero.

3. BASIS OF PREPARATION

3.1. Statement of compliance

These financial statements have been prepared in accordance with the accounting and reporting standards as applicable in Pakistan. The accounting and reporting standards applicable in Pakistan comprise of International Financial Reporting Standards (IFRS Standards) issued by the International Accounting Standards Board (IASB) as notified under the Companies Act, 2017 and provisions of and directives issued under the Companies Act, 2017. Where provisions of and directives issued under the Companies Act, 2017 differ from the IFRS Standards, the provisions of and directives issued under the Companies Act, 2017 have been followed.

The third and fifth schedules to the Companies Act, 2017 became applicable to Company for the first time for the preparation of these financial statements. The Companies Act, 2017 (including its third and fifth schedules) forms an integral part of the statutory financial reporting framework applicable to the Company. Specific additional disclosures and changes to the existing disclosures have been included in these financial statements.

3.2. Basis of measurement

These financial statements have been prepared under historical cost convention except for certain financial assets and financial liabilities which have been stated at their fair values, cost or amortized cost.

These financial statements have been prepared following accrual basis of accounting except for cash flow information.

3.3. Functional and presentation currency

These financial statements are presented in Pak Rupees which is the Company's functional currency and presentation currency.

4. NEW STANDARDS, INTERPRETATIONS AND AMENDMENTS TO PUBLISHED APPROVED ACCOUNTING STANDARDS

4.1. Amendments that are effective in current year and are relevant to the Company

The Company has adopted the amendments to the following approved accounting standards as applicable in Pakistan which became effective during the year from the dates mentioned below against the respective standard:

Annual Report June 2018 SINDH EL ASING

29

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2018

IAS 7

January 01,

2017

IAS 12

January 01,

2017

IFRS 12

January 01,

2017

Statement of Cash Flows - Amendments resulting from the

disclosure initiative

Income Taxes - Amendments regarding the recognition of

deferred tax assets for unrealised losses

Effective date

(annual

periods

beginning onor after

Other than the amendments to standards mentioned above, there are certain annual

improvements made to IFRS that became effective during the year:

Annual Improvements to IFRSs (2014 – 2016) Cycle:

Disclosure of Interests in Other Entities

4.2. Amendments not yet effective

The following amendments with respect to the approved accounting standards as applicable in Pakistan would be effective from the dates mentioned below against the respective standard:

March 2018

IFRS 2January 01,

2018

IFRS 4January 01,

2018

IFRS 7

IFRS 9

IFRS 9

January 01,

2018

IFRS 9

January 01,

2019

IFRS 10

Financial Instruments : Disclosures - Additional hedge

accounting disclosures (and consequential amendments)

resulting from the introduction of the hedge accounting

chapter in IFRS 9

Applies when

IFRS 9 is

applied

Financial Instruments - Reissue to incorporate a hedge

accounting chapter and permit the early application of the

requirements for presenting in other comprehensive income

the 'own credit' gains or losses on nancial liabilities

designated under the fair value option without early applying

the other requirements of IFRS 9

January 01,

2018

Conceptual framework for Financial reporting 2018-original

Share-based Payment - Amendments to clarify the

classication and measurement of share-based payment

transactions

Deferred

indenitely

InsuranceContracts - Amendments regarding the interaction

of IFRS 4 and IFRS 9

Consolidated Financial Statements - Amendments regarding

the sale or contribution of assets between an investor and its

associate or joint venture

Financial Instruments - Finalised version, incorporating

requirements for classication and measurement,

impairment, general hedge accounting and derecognition.

Financial Instruments - Amendments regarding prepayment

features with negative compensation and modications of

nancial liabilities

30

Annual Report June 2018 SINDH EL ASING

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2018

IAS 19January 01,

2019

IAS 28

Employee benets - Amendments regarding plan

amendments, curtailments or settlements

Investmentsin Associates and Joint Ventures - Amendments

regarding the sale or contribution of assets between an

investor and its associate or joint venture

Deferred

indenitely

IAS 28

January 01,

2019

IAS 39

IAS 40 January 01,

2018

IFRS 1 January 01,

2018

IAS 28 January 01,

2018

IFRS 3

January 01,

2019

IFRS 11

January 01,

2019

IAS 12 January 01,

2019

IAS 23 January 01,

2019

Investmentsin Associates and Joint Ventures - Amendments

regarding long-term interests in associates and joint ventures

Applies when

IFRS 9 is

applied

Investment Property - Amendments to clarify transfers or

property to, or from, investment property.the annual improvement to IFRSs that are effective form the dates mentioned below aganist respective standard:

Financial Instruments: Recognition

Amendments to permit an entity to elect to apply

the hedge accounting requirements in IAS value

hedge of the interest rate exposure of a

of nancial assets or nancial liabilities 9 is

applied, and to extend the fair value certain

and Measurements-

continue to

39 for a fair

portion of a portfolio

when IFRS

option to

contracts that meet the 'own use' scope exception

Annual Improvements to IFRSs (2015 – 2017) Cycle:

First-time Adoption of International Financial Reporting

Standards

Annual Improvements to IFRSs (2014 – 2016) Cycle:

Investments in Associates and Joint Ventures

Business Combinations

Joint Arrangements

Income Taxes

Borrowing Costs

4.3. Standards or interpretations not yet effective

The following new standards have been issued by the International Accounting Standards Board (IASB), which have been adopted locally by the Securities and Exchange Commission of Pakistan effective from the dates mentioned below against the respective standard:

IFRS 9 July 01, 2018

IFRS 15 July 01, 2018

IFRS 16 January 1, 2019

Revenue from Contracts with Customers

Leases

Financial Instruments

The following new standards and interpretations have been issued by the International Accounting Standards Board (IASB), which have not been adopted locally by the Securities and Exchange Commission of Pakistan (SECP):

Effective date

(annual

periods

beginning onor after)

Annual Report June 2018 SINDH EL ASING

31

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2018

IFRS 1 First Time Adoption of International Financial Reporting Standards

IFRS 14 Regulatory Deferral Accounts

IFRS 17 Insurance Contracts

The effects of IFRS 15 - Revenues from Contracts with Customers and IFRS 9 - Financial Instruments are still being assessed, as these new standards may have a significant effect on the Company’s future financial statements.

The Company expects that the adoption of the other amendments and interpretations of the standards will not have any material impact and therefore will not affect the Company's financial statements in the period of initial application.

5. SIGNIFICANT TRANSACTIONS AND EVENTS AFFECTING THE FINANCIAL POSITION AND PERFORMANCE

a) During the year ended June 30, 2018, total issue of 150,000,000 right shares of Rs. 10 each amounting to Rs. 1,500,000,000 to the subscriber of the Company have been allotted by the Board of Directors in their meeting held on January 30, 2018.

b) During the year ended June 30, 2018, the Company has obtained permission to issue certificates of deposit from Securities and Exchange Commission of Pakistan (SECP), vide letter no. SC/NBFC/SLCL/131/2017/39, dated September 27, 2017.

c) During the year ended June 30, 2018, the total lease disbursements made by the company amounted to Rs. 2,448 million. Out of these disbursements, major disbursements, amounting to in aggregate, Rs. 1,770 million, were made to following industries:

- Ceramics

- Food

- Hotel

- Sugar

d) During the year ended June 30, 2018, the Company has disbursed Rs. 500 million against repayment of its long term loan from Government of Sindh.

e) For discussion on the Company's performance, please refer to Director's report.

6. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies adopted in the preparation of these financial statements are set out below. These policies have been consistently applied to all the periods presented unless or otherwise stated.

6.1 Property, plant and equipments

Owned assets

These are stated at cost less accumulated depreciation and impairment, if any. Depreciation is charged to income over the useful life of the asset on a systematic basis, by applying the straight line method at the rates specified in note 5 to the financial statements. In respect of additions and disposal of assets during the period, depreciation is charged from the date of acquisition and up to the date preceding the disposal respectively.

Maintenance and normal repairs are charged to profit and loss account as and when incurred. Major renewals and improvements are capitalized and assets so replaced, if any, are retired.

An item of tangible fixed assets is de-recognized upon disposal or when no future economic benefits are expected from its use or disposal. Gains or losses on disposals of fixed assets, if any, are included in income or expense respectively.

Capital work-in-progress

These are stated at cost less accumulated impairment losses, if any and represent expenditure in connection with specific assets incurred during the construction period. These are transferred to specific assets as and when assets are available for use / sale. Cost also includes applicable borrowing costs. Transfers are made to relevant operating fixed assets category as and when assets are available for use intended by the management.

6.2 Intangibles

These are stated at cost less accumulated amortization and impairment, if any. Amortization is charged to income over the useful life of the asset on a systematic basis by applying the straight line method.

The cost of intangible asset comprises of its purchase price and any directly attributable expenditure incurred in preparing the asset for its intended use.

32

Annual Report June 2018 SINDH EL ASING

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2018

6.3 Net investment in finance leases

Leases in which the Company transfers substantially all the risks and rewards incidental to the ownership of an asset to the lessees are classified as finance leases. A receivable is recognized at an amount equal to the present value of the minimum lease payments under the lease agreement, including guaranteed residual value and unamortized initial direct cost which are included in the financial statements as "net investment in finance leases".

6.4 Provision against non performing leases and other loans

Provision against non performing leases and other loans is maintained at a level which, in the judgment of management, is adequate to provide for losses on lease portfolio and other loan portfolio which can be reasonably anticipated. The provision is increased by additional charge to income and is decreased by charge offs, net of recoveries.

Calculating provision against non performing leases and other loans is subject to numerous judgments and estimates. In evaluating the adequacy of provision, management considers various factors, including the requirements of the NBFC Regulations, the nature and characteristics of the obligor, current economic conditions, credit concentrations or deterioration in pledged collateral, historical loss experience and delinquencies. Lease and other loan receivables are charged off, when in the opinion of management, the likelihood of any future collection is believed to be minimal.

6.5 Long term loans and advances

Long term loans and advances are initially recognised at cost being the fair value of consideration received together with the associated transaction costs. Subsequently, these are carried at amortised cost using the effective interest rate method. Transaction costs relating to long term loans and advances are being amortised over the period of agreement.

6.6 Financial assets

6.6.1 Classification

The Company classifies its financial assets in the following categories: loans and receivables, held to maturity, available for sale and financial assets at fair value through profit or loss. The classification depends on the purpose for which the financial assets were acquired. Management determines the appropriate classification of its financial assets at initial recognition and re-evaluates this classification on a regular basis.

a) Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets, except for maturities greater than 12 months after the balance sheet date which are classified as non-current assets.

b) Held-to-maturity

Held-to-maturity investments are financial assets with fixed or determinable payments and fixed maturity that the Company has a positive intent and ability to hold to maturity.

c) Financial assets at fair value through profit or loss

This category has two sub-categories, namely; financial instruments classified as held for trading, and those designated at fair value through profit or loss upon initial recognition:

i) Investments which are acquired principally for the purposes of generating profit from short term fluctuation in price or are part of the portfolio in which there is recent actual pattern of short term profit taking are classified as held for trading.

ii) Investments designated at fair value through profit or loss upon initial recognition include those group of financial assets which are managed and their performance evaluated on a fair value basis, in accordance with the investment strategy.

d) Available for sale

Available for sale financial assets are those non-derivative financial assets that are designated as available for sale or are not classified as (a) loans and receivables, (b) held to maturity investments or (c) financial assets at fair value through profit or loss.

6.6.2 Initial recognition and measurement

All investments are initially recognised at cost, being the fair value of the consideration given including the transaction cost associated with the investment, except in case of held for trading investments, in which case the transaction costs are charged to the income statement.

Annual Report June 2018 SINDH EL ASING

33

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2018

6.6.3 Subsequent measurement

Subsequent to initial recognition, financial assets designated by the management as loans and receivables, held to maturity, financial assets at fair value through profit or loss and available for sale are valued as follows:

a) Loans and receivables

Loans and receivables are carried at amortised cost.

b) Held to maturity

Subsequent to initial measurement, held to maturity investments are carried at amortised cost.

c) Financial assets at fair value through profit or loss

After initial recognition, investments are remeasured at fair value determined with reference to the period-end quoted rates. Gains or losses on re-measurement of these investments are recognised in income statement.

d) Available for sale

Investments which do not fall under the above categories and which may be sold in response to the need for liquidity or changes in market rates are classified as available-for-sale. After initial recognition, investments classified as available-for-sale are remeasured at fair value, determined with reference to the year-end quoted rates. Gains or losses on remeasurement of these investments are recognised in the equity through other comprehensive income until the investment is sold, collected or otherwise disposed-off, or until the investment is determined to be impaired, at which time the cumulative gain or loss previously reported in equity is included in income.

6.7 Basis of valuation of investments

Fair value of the investments in units of mutual funds are determined by reference to Net Asset Value (NAV) rate notified by the Mutual Fund Association of Pakistan (MUFAP) as of the period end.

All regular way purchases and sales of investments are recognised on the trade date i.e. the date the Company commits to purchase / sell the investments.

6.8 Impairment

The carrying amount of assets are reviewed at each balance sheet date to determine whether there is any indication of impairment. If such indication exists then the asset's recoverable amount is estimated. Where the carrying value exceeds the estimated recoverable amount, assets are written down to their recoverable amount. The resulting impairment loss is taken to profit and loss account.

6.9 Certificates of Deposit

Return on Certificates of Deposit (CODs) issued by the Company is recognised on a time proportionate basis taking into account the relevant CODs issue and final maturity dates.

6.10 Taxation

Tax expense comprises current and deferred tax. Income tax expense is recognised in profit or loss account except to the extent that it relates to items recognized directly in equity or in other comprehensive income, in which case it is recognized in equity or other comprehensive income.

6.10.1 Current

The charge for current taxation is based on taxable income at the current rate of taxation after taking into account applicable tax credit, rebates and exemption available if any or minimum taxation at the rate of one percent of the turnover whichever is higher. However, for income covered under final tax regime, taxation is based on applicable tax rates under such regime.

6.10.2 Deferred

Deferred tax is recognized using the balance sheet liability method on all temporary differences between the carrying amount of assets and liabilities used for financial reporting purposes and the amounts used for taxation purposes. Deferred tax is measured at the rates that are expected to be applied to the temporary differences when they reverse, based on the laws that have been enacted or substantively enacted by the reporting date.

A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the asset can be utilised. Deferred tax assets are reviewed at each reporting date and reduced to the extent that it is no longer probable that the related tax benefit will be realised. Deferred tax is charged or credited to the profit and loss account except deferred tax, if any, on revaluation of investments which is recognized in other comprehensive income.

34

Annual Report June 2018 SINDH EL ASING

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED JUNE 30, 2018

6.11 Employees benefits

The Company's employees benefits comprise of provident fund and gratuity scheme for eligible employees.

a) Defined benefit plan (Gratuity Fund)