annual report 2019-2020 - edelweiss insurance

TRANSCRIPT

ANNUAL REPORT 2019-2020

Edelweiss General Insurance Company Limited Financial Statement for the year ended March 31, 2020

Board of Directors

Mr. Rujan Panjwani Mr. Navtej Nandra Ms. Kamala K Mr. Kanu Doshi Ms. Shubhdarshini Ghosh Mr. S. Ranganathan

- Chairman- Independent Director- Non - Executive Director- Independent Director- Executive Director & Chief Executive Officer- Non - Executive Director

Chief Financial officer Mr. Jitendra Attra

Appointed Actuary Ms. Tania Chakrabarti

Statutory Auditors

NGS & Co. LLP Chaturvedi & Co

Registered Office

Edelweiss House Off. C.S.T. Road, Kalina, Mumbai - 400098 Corporate Identity No.: U66000MH2016PLC273758 Tel: 022 - 2286 4400 Website: edelweissinsurance.com Email id: [email protected]

BOARD’S REPORT

To the Members of Edelweiss General Insurance Company Limited,

Your Directors hereby present their Third Annual Report together with the audited financial statement for the year ended March 31, 2020.

Industry Overview

The general insurance industry in India continues to have high growth potential. The gross direct premium (“GDPI”) of the industry grew from ₹ 1,700.36 billion in FY2019 to ₹ 1,893.02 billion in FY2020, a growth of 11.3% (Source: IRDAI & GI Council).

There were few major Regulatory developments at an industry level:

• The Authority issued a circular effective September 1, 2019, wherein theinsurers shall make available standalone annual own damage covers. Thiscircular is applicable for both old and new cars and two-wheelers, provided themotor Third Party cover is already in existence or taken simultaneously.

• Effective January 1, 2020, General Insurance Corporation of India (GIC Re) hasincreased the prescribed minimum rates for most occupancies under the Firesegment. Since GIC Re is the leading reinsurer in India, this development isexpected to bring a positive impact on the growth of Fire segment over thelong-term for the GI industry and the Company.

• Introduction of “Regulatory sandbox” to allow a conducive environment forinsurtech and fintech companies to carry innovations in the insurance space.Under the regulations, the Authority approved 33 products on January 14,2020. In the second tranche, Authority further approved 16 products on March31, 2020.

Information on the state of affairs of the Company

During the period under review and being the second full year of operations, the Company launched 16 products with 129 add-ons. There was no pending customer grievance at the close of the financial year. A key highlight of this year has been a regulatory nod to our application in the “Sandbox” initiative by IRDAI in encouragement of new and innovative products. Our “multi-user, multi-vehicle motor floater policy”, Edelweiss Switch, got approved for pilot which allows policy coverages on “pay-as-you use” model. It allows the customer to ‘switch’ the cover ‘on/off’ on demand based on their need to use it in a day.

Financial Highlights The financial performance for FY 2020 is summarized in the below table

(₹ in million)

Particular FY2020 FY2019 Gross Written Premium 1,586.04 1,043.09 Earned Premium 925.46 288.14 Income from Investments 74.48 112.83 Profit before Tax (962.73) (576.43) Profit after Tax (962.87) (576.43)

Share Capital and Solvency

During the period under review, the Authorized Share Capital of the Company was increased from Rs. 275,00,00,000/- (Rupees Two Hundred Seventy-Five Crore Only) to Rs. 400,00,00,000/- (Rupees Four Hundred Crore Only). Further, during the period under review, the Company has allotted 10,00,00,000 (Ten Crore Only) Equity Shares of Rs. 10 each to Edelweiss Financial Services Limited (EFSL), the Holding Company.

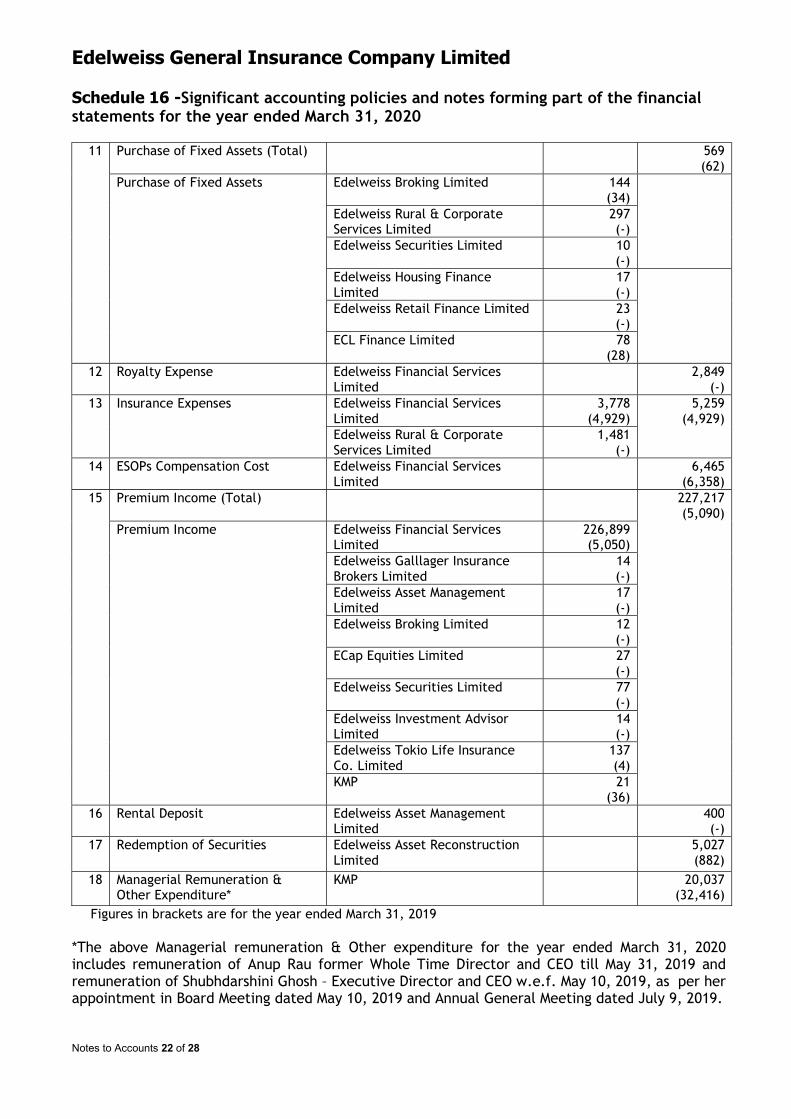

The Company maintained Solvency Ratio of 236% against 150% as prescribed by Insurance Regulatory and Development Authority of India (IRDAI). Particulars of Loans, Guarantees or Investments The Company being an Insurance Company, the provisions of Section 186(4) of the Companies Act, 2013 are not applicable to the Company. Significant and Material Orders Passed by the Regulators or Courts or Tribunals Impacting the Going Concern Status of the Company and its Future Operations There are no significant and/or material orders passed by the Regulators or Courts or Tribunals impacting the going concern status of future operations of the Company. Related Party Transactions All Related party transactions were in the ordinary course of business and on an arm’s length basis. During the year, the Company did not enter into any transaction

or arrangement with related parties, which were material or not at arm’s length. There were no materially significant transactions with the KMP or their relatives that have a potential conflict with the interest of the Company at large.

As per Accounting Standard (AS) 18 on ‘Related Party Disclosures’, the details of related party transactions entered into by the Company are disclosed in Schedule 16 of the Notes to Accounts to the financial statements. All material significant related party transactions are placed before the Audit Committee on a quarterly basis.

Directors & Key Managerial

Personnel Directors

During the period under review, there has been following change in the composition of the Board of Directors.

Mr. Biswamohan Mahapatra, Independent Director of the Company resigned from the Board of Directors on 14 December, 2019. Board would like to record their appreciation for the contributions made by Mr. Mahapatra.

Mr. Kanu Doshi was appointed as Additional Director Officer of the Company from February 13, 2020

Mr. Kanu Doshi holds office up to the date of forthcoming Annual General Meeting and the resolution for his appointment is placed for approval of the members.

Independent Directors have given declarations that they meet the criteria of independence as laid down under Section 149(6) of the Companies Act, 2013.

Key Management Personnel

During the period under review, the following Key Management Personnel have separated from the organization during the period under review:

S.No Name Designation 1. Mr. Dhilip Krishna Chief Investment Officer 2. Mr. Rishin Rai Chief Risk Officer

The following Key Management Personnel have joined the organization during the period under review:

S.No Name Designation 1. Mr. Neil Vaz Chief Risk Officer

Secretarial Standards

During the period under review, the company is in compliance with applicable Secretarial Standards issued by the Institute of Company Secretaries of India with respect to Board and General Meetings.

Number of Board Meetings held

The Board of Directors met 4 times, detailed information about the names, dates of meetings and attendance of Directors are given in the Corporate Governance Report annexed to this report.

Auditors

Statutory Auditors

IRDAI vide its circular dated May 18, 2016, had issued Corporate Governance Guidelines (“CG guidelines”) wherein criteria for appointment of statutory auditors for insurance companies had been stated. Pursuant to the CG guidelines, the provisions of appointment of auditors are aligned with the provisions of the CA2013. The Members of the Company in the Second Annual General Meeting (AGM) held on June 29, 2018 had approved the appointment of M/s. Chaturvedi & Co. Chartered Accountants as the Joint Statutory Auditors of the Company for a period of five (5) years till the conclusion of Seventh Annual General Meeting. The Members of the Company in the same AGM had also approved re-appointment of M/s. N.G.S & Co. LLP, Chartered Accountants as the Joint Statutory Auditors of the Company till conclusion of the Sixth Annual General Meeting, i.e. balance four (4) years out of first term of five (5) years.

The appointment/re-appointment of Joint Statutory Auditors was subject to ratification by the Members at every subsequent AGM held after the AGM held on June 29, 2018. Pursuant to the amendments made to Section 139 of the Companies Act, 2013 by the Companies (Amendment) Act, 2017 effective from May 7, 2018, the requirement of seeking ratification of the Members for the appointment of the Statutory Auditors has been withdrawn.

In view of the above, the ratification by the Members for continuance of their appointment at this AGM is not being sought.

Statutory Audit and other Fees paid to Joint Statutory Auditors

During FY2019, the total fees for the statutory audit and other services rendered by the Joint Statutory Auditors are given below:

Particulars Amount Joint Statutory Audit Fees 13,80,000 Other Certification Fees 5,00,000 Total 18,80,000

Auditors Report

There is no qualification, reservation, adverse remark or disclaimer made by the auditors in their report.

Secretarial Auditor

Pursuant to the provisions of Section 204 of the Companies Act, 2013 and Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014, the Company appointed M/s. SVVS & Associates, Company Secretaries, LLP to conduct the Secretarial Audit of the Company for FY2020. The Secretarial Audit Report is annexed herewith.

Particulars of Employees

The statement containing particulars of employees as required under Section 197 of CA 2013 read Rule 5(2) of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 is given in an Annexure and forms part of this report. Any shareholder interested in obtaining a copy of the Annexure may write to the Company Secretary at the registered office of the Company.

Extract of the Annual Return

In accordance with the provisions of Section 92 of the Companies Act, 2013 and the Rules framed thereunder, the extract of the Annual Return in the prescribed Form MGT – 9 is annexed herewith as “Annexure – 1”.

Risk Management Framework A statement indicating development and implementation of risk management policy for the Company including identification therein of elements of risk, if any, which in the opinion of the Board may threaten the existence of the Company has been given in the Corporate Governance Report annexed to this report. Disclosure as per Sexual Harassment of Women at Workplace (Prevention, Prohibition and Redressal) Act, 2013 The Company has formulated a Policy on Prevention of Sexual harassment at workplace. No case was reported during the year ended March 31, 2019 under the Policy. Whistle Blower Policy The Company has formulated a Whistle Blower Policy (Policy) which is designed to provide its employees, a channel for communicating instances of breach. Material Changes and Commitments There have been no material changes or commitments affecting the financial position of your Company, which have occurred between the end of financial year of your Company and the date of this report. Adequacy of Internal Financial Controls The Company has in place adequate internal financial controls commensurate with size, scale and complexity of its operations. During the year, such controls were tested and no reportable material weakness in the design or operations were observed. The Company has policies and procedures in place for ensuring proper and efficient conduct of its business, the safeguarding of its assets, the prevention and detection of frauds and errors, the accuracy and completeness of the accounting records and the timely preparation of reliable financial information.

General Information (i) Annual General Meeting During the year under review, the Company held its Second Annual General Meeting on Tuesday, July 9, 2019 at 11:00 a.m. at the registered office of the Company.

(ii) Extraordinary General Meeting

During the year under review, the Company held its Extra-ordinary General Meeting on Monday, December 23, 2019 at 11:00 a.m. at the registered office of the Company. The ordinary resolution with respect to increase in the Authorized Share Capital of the Company from Rs. 275,00,00,000/- (Rupees Two Hundred Seventy-Five Crore Only) to Rs. 4,00,00,00,000/- (Rupees Four Hundred Crore) divided into 40,00,00,000 (Forty Crore) Equity Shares of Rs. 10/- each was approved by the members.

Directors’ Responsibility Statement

Pursuant to Section 134 of the Companies Act, 2013 (the Act), your Directors confirm that:

(i) in the preparation of the annual accounts, the applicable accounting standardshave been followed;

(ii) we had selected such accounting policies and applied them consistently and madejudgments and estimates that are reasonable and prudent so as to give a true and fairview of the state of affairs of the Company as at March 31, 2020, and of the profit of theCompany for the financial year ended on that date;

(iii) proper and sufficient care had been taken for the maintenance of adequateaccounting records in accordance with the provisions of the Act for safeguarding theassets of the Company and for preventing and detecting fraud and otherirregularities;

(iv) the annual accounts have been prepared on a going concern basis; and

(v) we have devised proper systems to ensure compliance with the provisions of allapplicable laws and that such systems were adequate and operating effectively.

Conservation of Energy, Technology Absorption and Foreign exchange earnings/outgo

The provisions of Section 134(3)(m) of the Companies Act, 2013 read with Rule 8(3) of the Companies (Accounts) Rules, 2014 relating to conservation of energy and technology absorption do not apply to the Company.

During the year under review, there have been no foreign exchange earnings or outgo.

Deposit

During the year under review, your Company has not accepted any deposit.

Acknowledgments

The Board of Directors wishes to place on record appreciation for the continued support and co-operation extended by the Banks, Ministry of Corporate Affairs, Insurance Regulatory and Development Authority of India (IRDAI), government authorities and other stakeholders. Your Directors would also like to take this opportunity to express their appreciation for the, dedicated efforts of the employees of the Company.

For and on behalf of the Board Edelweiss General Insurance

Company Limited

Sd/- Sd/-

Rujan Panjwani S. RanganathanDirector Director

DIN No. 00237366 DINNo. 00125493

Place: Mumbai

Date: June 24, 2020

Corporate Governance Report

I. Philosophy of Corporate Governance

Edelweiss General Insurance Company Limited is fully committed to follow sound corporate governance practices and uphold the highest standards in conducting business. The Company aims to increase and sustain its corporate value through growth and innovation.

Board of Directors

The Board of Directors consists of 6 Directors, which includes 2 Independent Directors. The CEO of the Company is an Executive Director. All other Directors, including Chairman, are Non-Executive Directors.

Composition of Board of Directors

Name of the Director Category Qualification Field of Specialisation

Mr. Rujan Panjwani (DIN: 00237366)

Chairperson B.E. (Electrical) Finance

Mr. S. Ranganathan (DIN: 00125493)

Non – Executive Director CA, F.C.S, I.C.W.A, LLB

Taxation & finance

Ms. Kamala Kantharaj (DIN: 07917801)

Non – Executive Director C.A. Finance

Ms. Shubhdarshini Ghosh (DIN: 07191985 )

Executive Director & Chief Executive Officer

B.A (Maths Hons)PGDBM (IIM)Bangalore.

Insurance

Mr. Kanu Doshi (DIN: 00577409)

Independent Director CA Finance & Education

Mr. Navtej Nandra (DIN: 02282617)

Independent Director B. Com, MBA–IIMAhmedabad

Finance

Board Meetings

The Board meets at least once in a quarter to review the Company's financial results, business strategies apart from other board businesses. During the period under review, the Board met 4 times on May 10, 2019; August 13, 2019; November 11, 2019; and February 13, 2020.

Attendance record of the Directors: Name of Director Meetings

Attended Mr. Rujan Panjwani 3/4 Mr. S. Ranganathan 4/4 Ms. Kamala Kantharaj 4/4 Mr. Anup Rau Velamuri 1/4 Mr. Biswamohan Mahapatra 3/4 Mr. Navtej Nandra 4/4 Ms. Shubhdarshini Ghosh 3/4

Committees of the Board of Directors: Constitution & Composition and Attendance

The Board has constituted the following Committees:

(i) Audit Committee (AC);

(ii) Investment Committee (IC);

(iii) Risk Management Committee (RMC);

(iv) Policyholders’ Protection Committee (PPC); and

(v) Nomination and Remuneration Committee (NRC);

In addition to the above, the Company has also constituted a Share Allotment Committee.

(i) Audit Committee (AC)

Constitution & Composition

The Audit Committee comprises of two Independent Directors and one Non-Executive director. The Committee is chaired by an Independent Director of the Company. The composition of the Committee is given below along with the attendance of the members. The Committee met 4 times in the year under review on May 10, 2019; August 13, 2019; November 11, 2019; and February 13, 2020.

Attendance record of the Members: Name of the Member Category Number of Meetings

attended Mr. Biswamohan Mahapatra

Independent Director 3/4

Mr. Navtej Nandra Independent Director 4/4 Mr. Rujan Panjwani Non – Executive Director 3/4

(ii) Investment Committee (IC)

Constitution & Composition

The Investment Committee comprises of two Non-Executive Directors, one Executive Director, Appointed Actuary, Head - Actuary, Chief Investment Officer, Chief Financial Officer and Chief Risk Officer. The Committee is chaired by Mr. Rujan Panjwani, Non – Executive Director of the Company. The composition of the Committee is given below along with the attendance of the members. The Committee met on May 10, 2019; August 13, 2019; November 11, 2019; and February 13, 2020 during the period under review.

Attendance record of the Members: Name of the Member Category Number of Meetings

attended Mr. Rujan Panjwani Non – Executive Director 3/4 Mr. S. Ranganathan Non – Executive Director 4/4 Mr. Anup Rau Velamuri

Chief Executive Officer (Resign.)

1/4

Mr. Dhilip Krishna Chief Investment Officer (Resign.)

2/4

Mr. Jitendra Attra Chief Financial Officer 4/4 Mr. Rishin Rai Chief Risk Officer (Resign.) 1/4 Mr. Rohit Ajgaonkar Head – Actuary (Resign.) 1/4 Ms. Tania Chakrabarti Appointed Actuary 4/4 Ms. Shubhdarshini Ghosh

Chief Executive Officer 3/4

Mr. Neil Vaz Chief Risk Officer 1/4 Mr. Nisarg Ajmera Head Investment 1/4

(iii) Risk Management Committee (RMC)

Constitution & Composition

The Risk Management Committee comprises of Ms. Shubhdarshini Ghosh, Chief Executive Officer; Ms. Tania Chakrabarti, Appointed Actuary; and Mr. Neil Vaz, Chief Risk Officer. The Committee is chaired by Ms. Shubhdarshini Ghosh, Chief Executive Officer of the Company. The composition of the Committee is given below along with the attendance of the members. The Committee met on May 10, 2019; August 13, 2019; November 11, 2019; and February 13, 2020 during the period under review.

Attendance record of the Members: Name of the Member Category Number of Meetings

attended Mr. Anup Rau Velamuri

Chief Executive Officer (Resign.)

1/4

Mr. Ramalingam Chockalingam

Chief Operating Officer (Resign.)

3/4

Mr. Rishin Rai Chief Risk Officer 1/4 Ms. Shubhdarshini Ghosh

Chief Executive Officer 3/4

Ms. Tania Chakrabarti Appointed Actuary 3/4 Mr. Neil Vaz Chief Risk Officer 1/4

(iv) Policyholder’s Protection Committee (PPC)

Constitution & Composition

The Policyholder’s Protection Committee comprises of Mr. Rujan Panjwani, Non–Executive Director; Ms. Shubhdarshini Ghosh, Chief Executive Officer; and Mr. Rakesh Kaul, Chief Retail Distribution Officer. The Committee is chaired by Mr. Rujan Panjwani,

Non – Executive Director of the Company. The composition of the Committee is given below along with the attendance of the members. The Committee met on May 10, 2019; August 13, 2019; November 11, 2019; and February 13, 2020 during the period under review.

Attendance record of the Members: Name of the Member Category Number of Meetings

attended Mr. Rujan Panjwani Non – Executive Director 3/4 Mr. Anup Rau Velamuri

Chief Executive Officer (Resign.)

1/4

Mr. Ramalingam Chockalingam

Chief Operating Officer 3/4

Mrs. Shanai Ghosh Chief Executive Officer 4/4

(v) Nomination and Remuneration Committee (NRC)

Constitution & Composition

The Nomination and Remuneration Committee comprises of two Independent Directors and one Non-Executive Director. The Committee was chaired by Mr. Biswamohan Mahapatra, Independent Director of the Company. Mr. Biswamohan Mahapatra resigned from the Board of Directors on 14 December, 2019. Thereafter, Mr. Navtej Nandra, Independent Director, chaired the Committee Meeting held on 13 February 2020. The composition of the Committee is given below along with the attendance of the members. The Committee met on May 10, 2019 during the period under review.

Attendance record of the Members: Name of the Member Category Number of Meetings

attended Mr. Biswamohan Mahapatra

Independent Director 2/3

Mr. Navtej Nandra Independent Director 3/3 Mr. Rujan Panjwani Non – Executive Director 2/3

II. Enterprise Risk Management

Objective

The objective of the Risk Management Policy (‘Policy’) of Edelweiss General Insurance Company (‘the Company’) is to ensure that various risks are identified, measured, mitigated and that policies, procedures are established to address these risks for systemic response and adherence. With a view to mitigate such risks, a Risk Management Framework is in place.

The Framework follows the core Risk Management Philosophy of Edelweiss Group and is in compliance with the guidelines issued by the Insurance Regulatory and Development Authority (‘IRDAI’ / ‘Authority’) from time to time.

Risk Framework

The core of the risk philosophy of the Company lies in the identification, measurement, monitoring and management of risk. The Company has therefore adopted an effective Risk Management Framework consisting of three key elements:

− Strong risk governance− Accurate and thorough risk assessment− Prompt risk management actions

Risk Governance: Risk is directly overseen at all levels in the Company. The Governance structure can be summarized as:

1. The Business Users form the First Line of defence. This ensures that risk and controlenvironment is established into their day to day activities.

2. Risk Management, and Compliance forms part of the Second Line of Defence. The second lineof defence is oversight function and would provide direction and guidance to the first line ofdefence for implementation of Company’s Board driven policies. Second line of defence wouldalso monitor implementation efficiency of these policies and provide overall oversight to thebusiness processes and risks.

3. Independent assurance providers like internal auditors, external auditors, statutory auditors,regulatory auditors etc., form the third line of defence and provides independent assurance.Independent assurance function will have direct access to the Board of Directors of the Company.Statutory & Independent auditors would have independence as per Statutory and Regulatoryassurance framework of the country.

Risk Management Committee: The Risk Management Committee is responsible for periodic review of the risk management process and to ensure that the process initiatives are aligned to the desired objectives. The Company has in place a Board appointed Chief Risk Officer (‘CRO’) who is responsible for the implementation and monitoring of the framework.

Risk Assessment: This assessment is a useful tool in everyday decision-making.

Risk Management Actions: intended to optimize risk-adjusted returns within the risk appetite, ensure that mitigation measures are put in place as soon as risks are identified, thus minimizing the potential losses to the Company.

CERTIFICATE FOR COMPLIANCE OF THE CORPORATE GOVERNANCE GUIDELINES

I, Sameer Karekatte, hereby certify that the Company has complied with Corporate Governance Guidelines for Insurance Companies as amended from time to time and nothing has been concealed or suppressed.

Sd/- Sameer Karekatte Chief Legal & Compliance Officer

Place: Mumbai Date: June 24, 2020

Page 1 of 6

Form No. MR-3 SECRETARIAL AUDIT REPORT

FOR THE FINANCIAL YEAR ENDED MARCH 31, 2020 [Pursuant to section 204(1) of the Companies Act, 2013 and rule No.9 of the

Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014]

The Members, Edelweiss General Insurance Company Limited Edelweiss House, Off. C.S.T Road, Kalina, Mumbai 400098.

We have conducted the secretarial audit of the compliance of applicable statutory provisions and the adherence to good corporate practices by Edelweiss General Insurance Company Limited (hereinafter called “the Company”). Secretarial Audit was conducted in a manner that provided us a reasonable basis for evaluating the corporate conducts/statutory compliances and expressing our opinion thereon.

Based on our verification of the Company’s books, papers, minute books, forms and returns filed and other records maintained by the Company and also the information provided by the Company, its officers, agents and authorized representatives during the conduct of secretarial audit, we hereby report that in our opinion, the Company has, during the audit period covering the financial year ended on March 31, 2020, complied with the statutory provisions listed hereunder and also that the Company has proper Board processes and compliance mechanism in place to the extent, in the manner and subject to the reporting made hereinafter.

We have examined the books, papers, minute books, forms and returns filed and other records maintained by the Company for the financial year ended on March 31, 2020 according to the provisions of:

(i) The Companies Act, 2013 (the Act) and the rules made thereunder;

(ii) The Securities Contracts (Regulation) Act, 1956 (‘SCRA’) and the rules made thereunder;

(iii) The Depositories Act, 1996 and the Regulations and Bye-laws framed thereunder;

Page 2 of 6

(iv) Foreign Exchange Management Act, 1999 and the rules and regulations made thereunderto the extent of Foreign Direct Investment, Overseas Direct Investment and ExternalCommercial Borrowings1;

(v) The following Regulations and Guidelines prescribed under the Securities and ExchangeBoard of India Act, 1992 (‘SEBI Act’)2:-

(a) The Securities and Exchange Board of India (Substantial Acquisition of Shares andTakeovers) Regulations, 2011;

(b) The Securities and Exchange Board of India (Prohibition of Insider Trading)Regulations, 1992;

(c) The Securities and Exchange Board of India (Issue of Capital and DisclosureRequirements) Regulations, 2009;

(d) SEBI (Share Based Employee Benefits) Regulations, 2014

(e) The Securities and Exchange Board of India (Issue and Listing of Debt Securities)Regulations, 2008;

(f) The Securities and Exchange Board of India (Registrars to an Issue and ShareTransfer Agents) Regulations, 1993 regarding the Companies Act and dealing withclient;

(g) The Securities and Exchange Board of India (Delisting of Equity Shares)Regulations, 2009;

(h) SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

(i) The Securities and Exchange Board of India (Buyback of Securities) Regulations,1998; and

(vi) Other applicable laws as may be applicable specifically to the company, namely:

(i) The Insurance Regulatory and Development Authority of India (IRDA), 1999, andthe rules, regulations and circulars issued by IRDA thereunder to the extentapplicable to the company.

(ii) Terms and conditions of the letter issued by IRDA while granting registration as aGeneral Insurance Company

1Not applicable to the Company during the Audit period 2SEBI Act and the Regulations made thereunder are not applicable since (i) the Company is not a SEBI Registered market intermediary and also (ii) the securities of the Company are not listed in any Stock Exchange during the Audit Period

Page 3 of 6

(iii) Corporate Governance Guidelines for Insurance Companies issued by IRDA forInsurance Companies.

We have also examined compliance with the applicable clauses of the following:

(i) Secretarial Standards issued by The Institute of Company Secretaries of India.

During the period under review the Company has complied with the provisions of the Act, Rules, Regulations, Guidelines, Standards, etc. mentioned above

We further report that the Board of Directors of the Company is duly constituted with proper balance of Executive Directors, Non-Executive Directors and Independent Directors. The changes in the composition of the Board of Directors that took place during the period under review were carried out in compliance with the provisions of the Act.

Adequate notice is given to all directors to schedule the Board Meetings, agenda and detailed notes on agenda were sent at least seven days in advance, and a system exists for seeking and obtaining further information and clarifications on the agenda items before the meeting and for meaningful participation at the meeting.

Majority decision is carried through while the dissenting members’ views are captured and recorded as part of the minutes3.

We further report that there are adequate systems and processes in the Company commensurate with the size and operations of the Company to monitor and ensure compliance with applicable laws, rules, regulations and guidelines (Please see Annexure B).

We further report that during the audit period, the company has not accomplished/encountered any specific events / actions having a major bearing on the company’s affairs in pursuance of the laws, rules, regulations, guidelines, standards, etc. referred to above

June 24, 2020 CS. Suresh Viswanathan Mumbai Designated Partner

FCS : 4453 CP No : 11745

Note: This report is to be read with our letter of even date which is annexed as Annexure A and forms and integral part of this report.

3 All resolutions were carried unanimously

Page 4 of 6

ANNEXURE A

The Members, Edelweiss General Insurance Company Limited Edelweiss House, Off. C.S.T Road, Kalina, Mumbai 400098.

Our report of even date is to be read along with this letter.

1. Maintenance of secretarial record is the responsibility of the management of the Company.Our responsibility is to express an opinion on these secretarial records based on our audit.

2. We have followed the audit practices and processes as were appropriate to obtainreasonable assurance about the correctness of the contents of the Secretarial records. Theverification was done on test basis to ensure that correct facts are reflected in secretarialrecords. We believe that the processes and practices, we followed provide a reasonablebasis for our opinion.

3. We have not verified the correctness and appropriateness of financial records and Books ofAccounts of the Company.

4. No audit has been conducted on the compliance with finance and taxation laws as thesame are subject to audit by the Statutory Auditor and Internal Auditor to the Companyand their observations, if any, shall hold good for the purpose of this audit report.

5. Where ever required, we have obtained the Management representation about thecompliance of laws, rules and regulations and happening of events etc.

6. The compliance of the provisions of Corporate and other applicable laws rules, regulationsthe responsibility of management, our examination was limited to the verification ofprocedures on test basis.

7. The Secretarial Audit report is neither an assurance as to the future viability of theCompany nor of the efficacy or effectiveness with which the management has conductedthe affairs of the Company.

8. Audit of the compliance with Other Laws has been undertaken based on scope of audit andthe applicability of such Laws as ascertained by the Company and informed to us.

Page 5 of 6

9. We have relied on Internal Audit and other regulatory mandated audit and theobservations, if any, of the auditors shall hold good for the purpose of this audit report.

June [●],2020 Mumbai

CS. Suresh Viswanathan Designated Partner FCS : 4453 CP No : 11745

Page 6 of 6

ANNEXURE B

1. The Companies Act 2013, and the Rules thereunder

2. The Insurance Regulatory and Development Authority of India (IRDA), 1999, and the rules, regulations and circulars issued by IRDA thereunder to the extent applicable to the company.

3. Terms and conditions of the letter issued by IRDA while granting registration as a General Insurance Company

4. The Bombay Shops and Establishments Act, 1948

5. Payment of Wages Act, 1936

6. Minimum wages act-regional

7. Employee’s Provident Fund & Miscellaneous Provision Act, 1952

8. Payment of Bonus Act, 1965

9. Payment of Gratuity Act, 1972

10. Contract Labour (Regulation and Abolition) Act, 1970

11. Maternity Benefit Act 1961

12. Employee Compensation Act, 1923

13. Equal Remuneration Act, 1976

14. The Maharashtra Private Security Guards (Regulation of Employment & Welfare) Act, 1981 & Maharashtra Private Security Agencies (Regulation) Act, 2005

15. Maharashtra Workmen’s Minimum House Rent Allowance Act, 1983

16. Employees' State Insurance Act, 1948

17. Sexual Harassment of Women at Workplace (Prevention, Prohibition &Redressal) Act, 2013

18. Maharashtra Labour Welfare Fund Act, 1953.

Annexure - 1

Form No. MGT-9 EXTRACT OF ANNUAL RETURN

As on the financial year ended on March 31, 2020

[Pursuant to section 92(3) of the Companies Act, 2013 and rule 12(1) of

the Companies (Management and Administration) Rules, 2014]

I. REGISTRATION AND OTHER DETAILS:

i) CIN U66000MH2016PLC273758

ii) Registration Date 02/03/2016

iii) Name of the Company Edelweiss General Insurance Company Limited

iv) Category / Sub-Category of the

Company

Public Company/Limited by Shares

v) Address of the Registered office and

contact details

Edelweiss House, Off. C.S.T Road, Kalina,

Mumbai – 400098.

Email – [email protected]

Tel: +91 22 4009 4400

vi) Whether listed company Yes / No No

vii) Name, Address and Contact details of Registrar and Transfer Agent, if any

Link Intime India Pvt Ltd C -101, 247 Park, L.B.S. Marg, Vikhroli (West), Mumbai – 400 083 Tele: + 91 22 4918 6270 Fax: + 91 22 4918 6060

II. PRINCIPAL BUSINESS ACTIVITIES OF THE COMPANY All the business activities contributing 10% or more of the total turnover of the company shall be stated: -

Sr. No.

Name and Description of main products / services

NIC Code of the Product / Service

% to total turnover / income of the company $

1. General Insurance 6512 100% III. PARTICULARS OF HOLDING, SUBSIDIARY AND ASSOCIATE COMPANIES – Sr. No.

Name and Address of the Company

CIN/GLN Holding/ Subsidiary/ Associate

% of shares Held

Applicable Section

1. Edelweiss Financial Services Limited

L99999MH1995PLC094641 Holding

100 Section 2(46)

Address: Edelweiss House, Off CST Road, Kalina, Mumbai – 400098.

IV. SHARE HOLDING PATTERN (Equity Share Capital Breakup as percentage of Total

Equity) i) Category-wise Share Holding

Category of Shareholders

No. of Shares held at the beginning of the year

No. of Shares held at the end of the year

% Change during

the year De-mat Physical Total

% of Total Shar

es

De-mat Physical Total

% of

Total

Share

A. Promoters (1) Indian a) Individual/

HUF - - - - - - - - -

b) Central Govt - - - - - - - - - c) State Govt (s) - - - - - - - - - d) Bodies

Corporate - 20,80,00,000 20,80,00,000 100 - 30,80,00,000 30,80,00,000 100 32.47

e) Banks / FI - - - - - - - - - f) Any Other - - - - - - - - - Sub-total (A) (1):- - 20,80,00,000 20,80,00,000 100 - 30,80,00,000 30,80,00,000 100 32.47 (2) Foreign a) NRIs – Individuals - - - - - - - - -

b) Other – Individuals - - - - - - - - -

c) Bodies Corporate - - - - - - - - -

d) Banks / FI - - - - - - - - - e) Any Other - - - - - - - - - Sub-total (A) (2):- - - - - - - - - - Total shareholding of Promoter (A) =(A)(1)+(A)(2)

- 20,80,00,000 20,80,00,000 100 - 30,80,00,000 30,80,00,000 100 32.47

B. Public Shareholding

1. Institutions - - - - - - - - - a) Mutual Funds - - - - - - - - - b) Banks / FI - - - - - - - - - c) Central Govt - - - - - - - - - d) State Govt(s) - - - - - - - - - e) Venture Capital Funds - - - - - - - - -

f) Insurance - - - - - - - - -

Companies g) FIIs - - - - - - - - - h) Foreign

Venture Capital Funds

- - - - - - - - -

i) Others (specify) - - - - - - - - -

Sub-total (B)(1):- - - - - - - - - - 2. Non-Institutions

a) Bodies Corporate

i) Indian - - - - - - - - - ii) Overseas - - - - - - - - -

b) Individuals i)

Individual shareholders holding nominal share capital upto Rs. 1 lakh

- - - - - - - - -

ii) Individual shareholders holding nominal share capital in excess of Rs. 1 lakh

- - - - - - - - -

c) Others (specify) - - - - - - - - -

Sub-total (B)(2):- - - - - - - - - - Total Public Shareholding (B)=(B)(1)+(B)(2)

- - - - - - - - -

C. Shares held by Custodian for GDRs & ADRs

- - - - - - - - -

Grand Total (A+B+C) - 20,80,00,000 20,80,00,000 100 - 30,80,00,000 30,80,00,000 100 32.47

(ii) Shareholding of Promoters

Sl. No.

Shareholder’s Name

Shareholding at the beginning of the year

Share holding at the end of the year % change

In share

holding during

the year

No. of Shares

% of Total

Shares of the

company

% of Shares Pledged /

encumbered to total shares

No. of Shares

% of Total

Shares of the

company

%of Shares Pledged /

encumbered to total shares

1 Edelweiss Financial Services Limited*

20,80,00,000 100 Nil 30,80,00,000 100 Nil 32.47

Total 20,80,00,000 100 Nil 30,80,00,000 100 Nil 32.47 *Including 6 shares held by nominees of Edelweiss Financial Services Limited (iii) Change in Promoters’ Shareholding:

Sl. No.

Shareholding at the beginning of

the year

Cumulative Shareholding during the

year

No. of shares

% of total shares of the

company No. of shares

% of total shares of the

company 1. At the beginning of the

year (Edelweiss Financial Services Limited)

20,80,00,000 100

2. Date wise Increase /Decrease in Promoters Shareholding during the year specifying the reasons for increase /decrease (e.g. allotment /transfer /bonus/ sweat equity etc):

Date: August 16, 2019 Reason: Allotment

2,00,00,000 9.62 22,80,00,000 100

Date: November 27, 2019 Reason: Allotment

4,00,00,000 14.93 26,80,00,000 100

Date: February 18, 2020 Reason: Allotment

4,00,00,000 12.98 30,80,00,000 100

3. At the End of the year (Edelweiss Financial Services Limited)

30,80,00,000 100 30,80,00,000 100

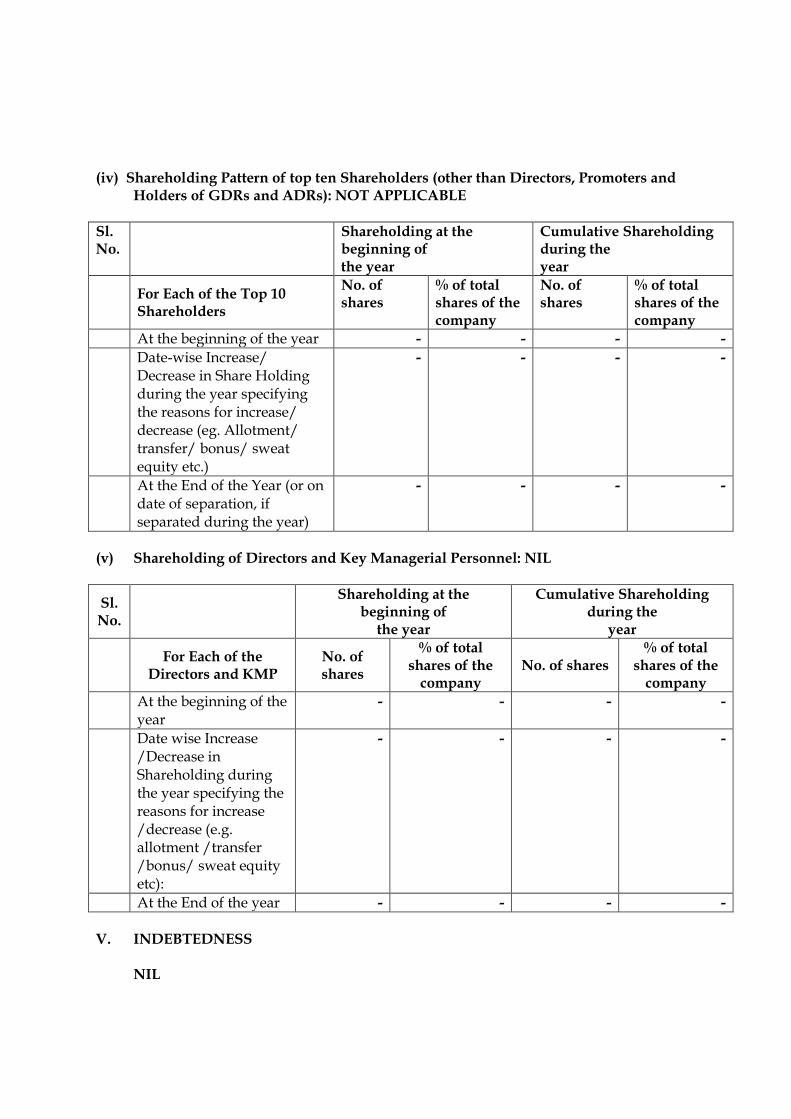

(iv) Shareholding Pattern of top ten Shareholders (other than Directors, Promoters and

Holders of GDRs and ADRs): NOT APPLICABLE Sl. No.

Shareholding at the beginning of the year

Cumulative Shareholding during the year

For Each of the Top 10 Shareholders

No. of shares

% of total shares of the company

No. of shares

% of total shares of the company

At the beginning of the year - - - - Date-wise Increase/

Decrease in Share Holding during the year specifying the reasons for increase/ decrease (eg. Allotment/ transfer/ bonus/ sweat equity etc.)

- - - -

At the End of the Year (or on date of separation, if separated during the year)

- - - -

(v) Shareholding of Directors and Key Managerial Personnel: NIL

Sl. No.

Shareholding at the beginning of

the year

Cumulative Shareholding during the

year

For Each of the Directors and KMP

No. of shares

% of total shares of the

company No. of shares

% of total shares of the

company At the beginning of the

year - - - -

Date wise Increase /Decrease in Shareholding during the year specifying the reasons for increase /decrease (e.g. allotment /transfer /bonus/ sweat equity etc):

- - - -

At the End of the year - - - - V. INDEBTEDNESS

NIL

VI. REMUNERATION OF DIRECTORS AND KEY MANAGERIAL PERSONNEL A. Remuneration to Managing Director, Whole-time Directors and/or Manager (‘in 000’s)

Sl. no. Particulars of Remuneration Mr. Anup Rau (Whole-time

Director)

Ms. Shubhdarshini

Ghosh (Whole-time

Director) 1. Gross salary

(a) Salary as per provisions contained in section 17(1) of the Income-tax Act,1961

4,024 15,338

(b) Value of perquisites u/s 17(2) Income-tax Act, 1961

-

(c) Profits in lieu of salary under section 17(3) Income-tax Act, 1961

-

2. Stock Option 524 3. Sweat Equity - 4. Commission

- as % of profit - Others, specify…

-

5. Others – Retirals (PF) 140 534 Total 4,688 15,872 B. Remuneration to other directors: 1. Independent Directors Sl. No.

Particulars of Remuneration

Name of the Directors Total Amount Mr. Navtej

Nandra Mr.

Biswamohan Mahapatra

Mr. Kanu Doshi

1 Fee for attending board / committee meetings

1,60,000

1,00,000

60,000

3,20,000

2 Commission - - 3 Others, please

specify - -

Total B (1) 1,60,000 1,00,000 60,000 3,20,000

2. Other Non - Executive Directors Sl. No.

Particulars of Remuneration

Name of the Directors Total Amount Mr. Rujan

Panjwani Mr. S.

Ranganathan Ms. Kamala

K 1 Fee for attending board /

committee meetings - - - -

2 Commission - - - - 3 Others, please specify - - - - Total B (2) - - - - Total B = B (1) + B (2) 3,20,000 C. REMUNERATION TO KEY MANAGERIAL PERSONNEL OTHER THAN MD/MANAGER/WTD

(‘in 000’s) Sl. no.

Particulars of Remuneration

Key Managerial Personnel

Mr. Anup Rau

(Chief Executive Officer)

Ms. Shubhdarshini

Ghosh (Chief

Executive Officer)

Mr. Ashish Lakhtakia (Company Secretary and Chief Legal &

Compliance Officer)

Mr. Jitendra

Attra (Chief

Financial Officer)

Total

1 Gross salary (a) Salary as per

provisions contained in section 17(1) of the Income-tax Act,1961

4,024 15,338 6,825 10,045 36,232

(b) Value of perquisites u/s 17(2) Income-tax Act, 1961

- 40 - 40

(c) Profits in lieu of salary under section 17(3) Income-tax Act, 1961

- - -

2 Stock Option 524 - - 524 3 Sweat Equity - - - - 4 Commission - - - -

- as % of profit - others, specify…

5 Others, Retirals (PF)

140 534 301 349 1,324

Total 4,688 15,872 7,166 10,394 38,120 VII. PENALTIES / PUNISHMENT/ COMPOUNDING OF OFFENCES: There was no penalties/punishment/compounding of offenses under Companies Act, 2013. Sd/- Sd/- Rujan Panjwani S. Ranganathan Director Director DIN: 00237366 DIN: 00125493 Place: Mumbai Date: June 24, 2020

Edelweiss General Insurance Company Limited Management Report for the year ended 31st March, 2020

In accordance with Part IV Schedule B of the Insurance Regulatory and Development Authority of India (‘IRDAI’) (Preparation of Financial Statements and Auditors’ Report of Insurance Companies) Regulations, 2002 (‘Regulation’) the following Management Report for the year ended March 31, 2020 is submitted:

1. The Company obtained regulatory approval to undertake general insurance business on December 18, 2017, from the Insurance Regulatory and Development Authority of India (‘IRDAI’) and holds a valid certificate of registration.

2. To the best of our knowledge and belief, all the material dues payable to the statutory authorities have been duly paid.

3. We confirm that the shareholding pattern and transfer of shares are in accordance with

statutory and regulatory requirements.

4. We declare that funds of holders of policies issued in India have not been directly or indirectly invested outside India.

5. We confirm that the Company has maintained the required solvency margins laid down by the

IRDAI.

6. We certify that the values of all the assets have been reviewed on the date of Balance Sheet and in management’s belief, the assets set forth in the Balance Sheet are shown in the aggregate at amounts not exceeding their realizable or market value, under the several headings – “investments”, “agents’ balances”, “outstanding premiums”, “income accrued on investments”, “due from other entities carrying on insurance business, including reinsurers (net)”, “cash and bank balances” and several items specified under “advances recoverable” except debt securities which are stated at cost/ amortized cost.

7. The Company is exposed to a variety of risks associated with general insurance business such as

quality of risks undertaken, fluctuations in value of assets and higher expenses in the initial years of operation. The Company monitors these risks closely and effective remedial action is taken wherever deemed necessary.

The Company has, through an appropriate reinsurance program kept its risk exposure at a level commensurate with its capacity.

8. The Company does not have operations outside India. 9. a) Claims outstanding at the end of the year, please refer annexure 1

b) Average claims settlement time, please refer annexure 2. c) Average claims intimation time, please refer annexure 3.

10. We certify that all debt securities are considered as ‘held to maturity’ and accordingly stated at historical cost subject to amortization of premium or accretion of discount on constant yield to maturity basis in the Revenue Accounts and in the Profit and Loss Account over the period of

Edelweiss General Insurance Company Limited Management Report for the year ended 31st March, 2020

maturity/holding. All mutual fund investments are valued at closing net asset value as at Balance sheet date. Equities actively traded and preference shares as at the Balance sheet date are stated at fair value, being the last quoted closing price on the National Stock Exchange (NSE) being selected as Primary exchange as required by IRDAI circular number IRDA/F&I/INV/CIR/213/10/2013 dated October 30, 2013. However, in case of any stock not being listed in NSE, the same being valued based on the last quoted closing price in Bombay Stock Exchange (BSE). In accordance with the Regulations, any unrealized gains/losses arising due to change in fair value of mutual fund investments, listed equity shares, preference shares and security receipts are accounted in “Fair Value Change Account” and carried forward in the Balance sheet and is not available for distribution.

11. Investments as at March 31, 2020 amount to ₹ 30,306.5 lakhs Refer Schedule 8 & 8A (Previous year: ₹ 20,258.7 lakhs). Income from Investments amounted to ₹ 725.6 lakhs (Previous year: ₹ 1,119.8 lakhs). Investments other than units of mutual fund and security receipts are only in regularly traded instruments in the secondary markets. Company’s debt investment comprises largely of Government securities and bond rated AA and above. The fixed income investments and loan have not had delays in servicing of interest or principal amounts and in case of delay, if any, the same has been suitably provided for. Investments are managed in consonance with the investment policy framed and approved by the Board and are within the investment regulation and guidelines of IRDAI.

12. The Company has adopted a prudent investment policy with emphasis on optimizing return with

minimum risk. Emphasis being towards low risk investments such as Government securities and other rated debt instruments. Investments are managed in consonance with the investment policy laid down by the Board and are within the investment regulation and guidelines of the IRDAI. There are no non-performing assets as at the end of the financial year.

13. We certify that: a. The financial statements have been prepared in accordance with the applicable Accounting

Standards, principles and policies and disclosures have been made, wherever the same is required. There is no material departure from the said standards, principles and policies;

b. The Company has adopted accounting policies and applied them consistently and made judgments and estimates that are reasonable and prudent so as to give a true and fair view of the state of the affairs of the Company at the end of the financial year and of the profits/(loss) of the Company for the year;

c. The Company has taken proper and sufficient care for the maintenance of adequate

accounting records in accordance with the applicable provisions of the Insurance Act, 1938, Insurance Laws (Amendment) Act, 2015 (to the extent notified), Companies Act, 1956 and Companies Act, 2013 to the extent applicable, for safeguarding the assets of the Company and for preventing and detecting fraud and other irregularities;

Edelweiss General Insurance Company Limited Management Report for the year ended 31st March, 2020

d. The financial statements have been prepared on a going concern basis;

e. The Company has set up an internal audit function commensurate with the size and nature of the business and the same was operational throughout the year.

14. Details of payments to individuals, firms, companies and organizations in which directors are interested during the year ended on March 31, 2020, please refer annexure 4.

For and on behalf of the Board Sd/- Sd/- Rujan Panjwani S Ranganathan Chairman Director (DIN: 00237366) (DIN: 00125493) Sd/- Sd/- Shubhdarshini Ghosh Jitendra Attra Executive Director & CEO Chief Financial Officer (DIN: 07191985)

Place: Mumbai

June 24, 2020

Edelweiss General Insurance Company Limited Management Report for the year ended 31st March, 2020

Details of Claims Outstanding during Preceding Two Years

Annexure -1 As at March 31, 2020 (₹ in lakhs)

Product Fire Marine Cargo Motor OD Motor TP Engineering

Ageing No. of Claims

Amount

No. of Claims

Amount

No. of Claims

Amount

No. of Claims

Amount

No. of Claims

Amount

0-30 Days 2 463.1 - 39.6 357 356.8 17 3,009.7 - 59.7 31-60 Days 1 1.4 - - 68 146.8 10 55.5 - - 61-90 Days - - - - 20 68.8 20 104.7 - - 91-180 Days 1 0.0 - - 7 39.1 25 194.4 - - 181-365 Days 1 2.0 2 22.0 - - 49 541.4 - - 1-3 Years - - - - - - 1 41.5 - - Grand Total 5 466.6 2 61.6 452 611.6 122 3,947.3 - 59.7

Product PA Health Liability Others Total

Ageing No. of Claims

Amount

No. of Claims

Amount

No. of Claims

Amount

No. of Claims

Amount

No. of Claims

Amount

0-30 Days - 260.1 2,344 2,608.2 - 9.9 - 5.1 2,720 6,812.2 31-60 Days - - 1,038 106.6 - - - - 1,117 310.3 61-90 Days - - 11 0.7 - - - - 51 174.2 91-180 Days 1 0.0 887 55.8 - - - - 921 289.4 181-365 Days - - 406 33.5 - - - - 458 598.9 1-3 Years - - - - - - - - 1 41.5 Grand Total 1 260.1 4,686 2,804.9 - 9.9 - 5.1 5,268 8,226.7

As at March 31, 2019 (₹ in lakhs)

Product Fire Marine Cargo Motor OD Motor TP Engineering

Period No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

0-30 Days - 159.0 - 5.9 1 1.5 1 750.4 - 27.2 31-60 Days - - - - - - 2 10.2 - - 61-90 Days - - - - - - - - - - 91-180 Days - - - - - - - - - - 181-365 Days - - - - - - - - - - Grand Total - 159.0 - 5.9 1 1.5 3 760.6 - 27.2

Product PA Health Liability Others Grand Total

Period No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

0-30 Days 7 202.5 796 1,916.9 - 9.9 - 3.4 1,353 3,076.7 31-60 Days 11 0.1 441 206.6 - - - - 1,147 216.9 61-90 Days 2 0.8 1 0.5 - - - - 3 1.3 91-180 Days - - 3 0.3 - - - - 3 0.3 181-365 Days - - - - - - - - - - Grand Total 20 203.4 1,241 2,124.3 - 9.9 - 3.4 1,265 3,295.2

Edelweiss General Insurance Company Limited Management Report for the year ended 31st March, 2020

As at March 31, 2018 (₹ in lakhs)

Product Fire Marine Cargo Motor OD Motor TP Engineering

Period No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

0-30 Days - - - - - - - - - - 31-60 Days - - - - - - - - - - 61-90 Days - - - - - - - - - - 91-180 Days - - - - - - - - - - 181-365 Days - - - - - - - - - - Grand Total - - - - - - - - - -

Product PA Health Liability Others Grand Total

Period No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

No. Of Claims Amount

0-30 Days - - - 1.27 - 0.60 - - - 1.87 31-60 Days - - - - - - - - - - 61-90 Days - - - - - - - - - - 91-180 Days - - - - - - - - - - 181-365 Days - - - - - - - - - - Grand Total - - - 1.27 - 0.60 - - - 1.87

Details of Average Claims Settlement Time Annexure -2

Period For the year ended

March 31 2020 For the year ended

March 31 2019 For the year ended

March 31 2018

Product

No. of Claim

Settled

Average Settlement Time (Days)

No. of Claim Settled

Average Settlement Time (Days)

No. of Claim

Settled

Average Settlement Time (Days)

Fire 1 12 0 0 - - Motor* 4,398 13 12 9 - - Engineering - - - - - - Marine Cargo - - - - - - Personal Accident** - - - - - - Health** 3,506 13 41 49 - - Others 2 - 1 - - - Grand Total 7,907 13 54 39 - -

*The above ageing does not include Motor third party claims which get settled through MACT and other judicial bodies **Majority of the cases includes settlement of claims within the insurance companies which occurs during specific span of time The above table does not include the count of RI Inward claims and Co-insurance claims settled (wherein the Company is participated as ‘follower’)

Edelweiss General Insurance Company Limited Management Report for the year ended 31st March, 2020

Details of Claims Intimated: - Annexure -3

Period For the year ended March 31, 2020*

For the year ended March 31, 2019*

Product Claims Intimated Amount (₹ in lacs) Claims Intimated Amount (₹ in lacs) Fire 2 0.4 - - Motor 4,969 2,600.0 17 17.7 Engineering - - - - Marine Cargo - - - - Personal Accident - - - - Health 4,060 1,839.1 57 55.3 Others 2 4.0 1 2.4 Grand Total 9,033 4,443.4 75 75.4

*Amount of claim intimated includes change in reserves The above table does not include the count of RI Inward claims and Co-insurance claims settled (wherein the Company is participated as ‘follower’) List of Payments to Parties in which Directors are Interested Annexure -4

Entity in which Director are interested

Name of Director Interested as For the year ended March 31, 2020 (₹ in

lacs)

For the year ended March 31, 2019 (₹

in lacs)

Edelweiss Financial Services Limited

Mr. Biswamohan Mahapatra

Independent Director

137.27 -

Mr. Navtej S. Nandra Independent Director

Mr. Rujan Panjwani Executive Director

Gruh Finance Limited Mr. Biswamohan Mahapatra

Independent Director

- -

HDFC Credila Financial Services Private Limited

Mr. Biswamohan Mahapatra

Director - -

Ujjivan Small Finance Bank Limited

Mr. Biswamohan Mahapatra

Director - -

ECL Finance Limited Mr. Biswamohan Mahapatra

Independent Director

270.04 64.38

Janakalyan Consultancy & Services Private Limited

Mr. Biswamohan Mahapatra

Director - -

Indian Institute of Insolvency Professionals of ICAI

Mr. Biswamohan Mahapatra

Director - -

National Payments Corporation of India

Mr. Biswamohan Mahapatra

Director - -

Edelweiss Tokio Life Insurance Company Limited

Mr. Navtej S. Nandra Independent Director

- -

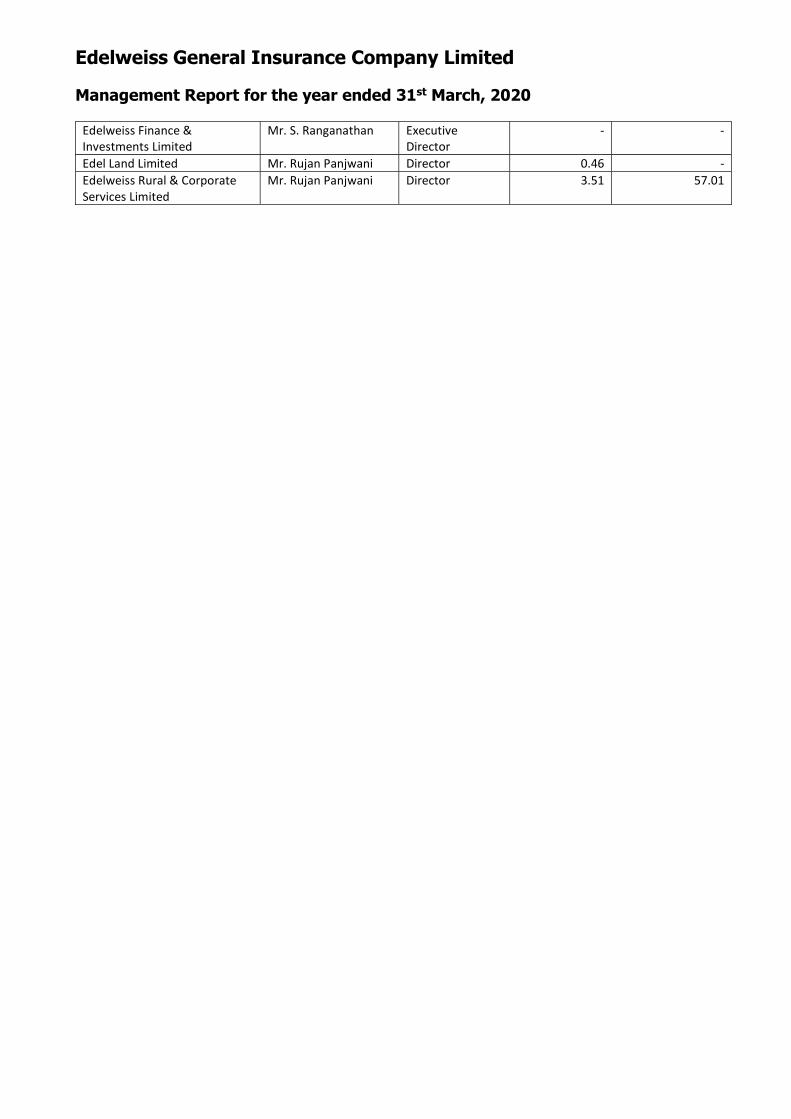

Oak North Bank Limited Mr. Navtej S. Nandra Director - - Edel Finance Company Limited Mr. S. Ranganathan Director - -

Edelweiss General Insurance Company Limited Management Report for the year ended 31st March, 2020

Edelweiss Finance & Investments Limited

Mr. S. Ranganathan Executive Director

- -

Edel Land Limited Mr. Rujan Panjwani Director 0.46 - Edelweiss Rural & Corporate Services Limited

Mr. Rujan Panjwani Director 3.51 57.01

Chaturvedi & Co. NGS & Co. LLP Chartered Accountants Chartered Accountants

81, Mittal Chambers, B-46, Pravasi Estate, 228, Nariman Point, V.N. Road, Goregaon (East)

Mumbai – 400021. Mumbai - 400063.

INDEPENDENT AUDITORS’ REPORT ON FINANCIAL STATEMENTS FOR YEAR ENDED

MARCH 31, 2020 OF EDELWEISS GENERAL INSURANCE COMPANY LIMITED

To the Members of EDELWEISS GENERAL INSURANCE COMPANY LIMITED

Report on the Audit of the Financial Statements

Opinion We have audited the accompanying financial statements of EDELWEISS GENERAL

INSURANCE COMPANY LIMITED (“the Company”), which comprise the Balance Sheet as at March 31, 2020, the Revenue accounts of fire, marine and miscellaneous insurance (collectively known as the ‘Revenue account’), the Profit and Loss account and the

Receipts and Payments account for the year then ended, the schedules annexed there to, a summary of the significant accounting policies and other explanatory notes thereon.

In our opinion and to the best of our information and according to the explanations given to us, we report that the aforesaid financial statements prepared in accordance

with the requirements of Accounting Standards as specified under Section 133 of the Companies Act, 2013 (the ‘Act’), including relevant provisions of the Insurance Act, 1938(the “Insurance Act”)the Insurance Regulatory and Development Authority of India

Act, 1999 (the “IRDAI Act”)and other accounting principles generally accepted in India, to the extent considered relevant and appropriate for the purpose of these financial statements and which are not inconsistent with the accounting principles as prescribed

in the Insurance Regulatory and Development Authority of India (Preparation of Financial Statements and Auditors’ Report of Insurance Companies) Regulations, 2002 (the “Regulations”)and circulars issued by the Insurance Regulatory and Development

Authority of India (“IRDAI” / “Authority”), to the extent applicable, give a true and fair view in conformity with the accounting principles generally accepted in India as

applicable to insurance companies:

a. in the case of Balance Sheet, of the state affairs of the Company as at March

31, 2020; b. in the case of Revenue Accounts, of the operating loss in Fire, Marine and

Miscellaneous Business for the year ended on that date;

c. in the case of Profit and Loss Account, of the loss for the year ended on that date; and

d. in case of Receipts and Payments Account, of the receipts and payments for

the year ended on that date.

Basis for Opinion

We conducted our audit in accordance with the Standards on Auditing (SAs) specified under section 143(10) of the Act. Our responsibilities under those

Standards are further described in the Auditor’s Responsibilities for the Audit of the financial statements section of our report. We are independent of the Company in accordance with the Code of Ethics issued by the Institute of Chartered Accountants

of India together with the ethical requirements that is relevant to our audit of the financial statements under the provisions of the Act and the Rules made there

under, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the Code of Ethics. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Information Other than the Financial Statements and Auditor’s Report Thereon

The Directors are responsible for the other information. The other information comprises of Directors Report, Management Report and Corporate Governance

Report, but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we

do not express any form of assurance conclusion thereon. In connection with our audit of the financial statements, our responsibility is to read

the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in

the audit or otherwise appears to be materially misstated. If we identify such material inconsistencies or apparent material misstatements, we

are required to determine whether there is a material misstatement of the other information. If, based on the work we have performed, we conclude that there is a

material misstatement of this other information, we are required to report that fact. We confirm that we have nothing material to report, add or draw attention to in this

regard.

Responsibilities of the Management and those charged with governance for the financial statements

The Company’s Board of Directors is responsible for the matters stated in Section 134(5) of the Act with respect to the preparation of these financial

statements that give a true and fair view of the financial position, underwriting results, financial performance and cash flows of the Company in accordance with the accounting principles generally accepted in India, including the applicable

Accounting Standards specified under Section 133 of the Act, the Insurance Act, the IRDAI Act, the Regulations and orders / directions prescribed by the IRDAI in

this behalf and current practices prevailing within the insurance industry in India.

This responsibility also includes maintenance of adequate accounting records in

accordance with the provisions of the Act for safeguarding the assets of the Company and for preventing and detecting frauds and other irregularities; selection and application of appropriate accounting policies; making judgments

and estimates that are reasonable and prudent; and design, implementation and maintenance of adequate internal financial controls, that were operating

effectively for ensuring the accuracy and completeness of the accounting records, relevant to the preparation and presentation of the financial statements that give a true and fair view and are free from material misstatement, whether

due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless

management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

The Board of Directors is also responsible for overseeing the Company’s financial

reporting process. Auditor’s Responsibilities for the Audit of the financial statements

Our objectives are to obtain reasonable assurance about whether thefinancial

statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level assurance, but it not a guarantee that an audit conducted

in accordance with SAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if,

individually or in the aggregate, that could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with SAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial

statements, whether due to fraud or error, design and perform audit

procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not

detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to

design audit procedures that are appropriate in the circumstances. Under section 143(3)(i) of the Companies Act, 2013, we are also responsible for

expressing our opinion on whether the Company has adequate internal financial controls system in place and the operating effectiveness of such

controls. • Evaluate the appropriateness of accounting policies used and the

reasonableness of accounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a

material uncertainty exists related to events or conditions that may cast significant doubt on the ability of the Company to continue as a going concern. If we conclude that a material uncertainty exists, we are required to

draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our

opinion. Our conclusions are based on the audit evidence obtained up to the date of this report. However, future events or conditions may cause the Company to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial

statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves

fair presentation. Materiality is the magnitude of misstatements in the financial statements that,

individually or in aggregate, makes it probable that the economic decisions of a reasonably knowledgeable user of the financial statements may be influenced. We

consider quantitative materiality and qualitative factors in (i) planning the scope of our audit work and in evaluating the results of our work; and (ii) to evaluate the effect of any identified misstatements in the financial statements.

We communicate with those charged with governance regarding, among other

matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have

complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

Other Matters

The actuarial valuation of liabilities in respect of Incurred But Not Reported (the “IBNR”), Incurred But Not Enough Reported (the “IBNER”) and Premium Deficiency

Reserve (the “PDR”) is the responsibility of the Company’s Appointed Actuary (the “Appointed Actuary”). The actuarial valuation of these liabilities, that are estimated

using statistical methods as at March 31, 2020 has been duly certified by the Appointed Actuary and in her opinion, the assumptions considered by herfor such

valuation are in accordance with the guidelines and norms issued by the IRDAI and the Institute of Actuaries of India in concurrence with the IRDAI. We have relied

upon the Appointed Actuary’s certificate in this regard for forming our opinion on the valuation of liabilities for outstanding claims reserves and the PDR contained in

the financial statements of the Company. Report on Other Legal and Regulatory Requirements

1. As required by the IRDAI Financial Statements Regulations, we have issued a

separate certificate dated June 24, 2020 certifying the matters specified in paragraphs 3 and 4 of Schedule C to the IRDAI Financial Statement Regulations.

2. As required by the paragraph 2 of Schedule C to the IRDAI Financial Statement Regulations and Section 143(3) of the Act, in our opinion and according to the

information and explanations give to us, we report that:

2.1 We have sought and obtained all the information and explanations which to

the best of our knowledge and belief were necessary for the purposes of our audit.

2.2 As the Company’s accounts are centralized and maintained at the corporate

office, no returns for the purposes of our audit are prepared at the branches and other offices of the Company.

2.3 Proper books of account as required by law have been kept by the Company so far as it appears from our examination of those books.

2.4 The Balance sheet, the Revenue accounts, the Profit and Loss account and

the Receipts and Payments account dealt with by this report are in

agreement with the books of account.

2.5 The aforesaid financial statements comply with the applicable Accounting Standards specified under Section 133 of the Act and with the accounting principles prescribed by the Regulations and orders/directions prescribed by

IRDAI in this regard.

2.6 Investments have been valued in accordance with the provisions of the Insurance Act, the Regulations and orders/directions issued by IRDAI in this regard.

2.7 On the basis of the written representations received from the Directors as on

March 31, 2020and taken on record by the Board of Directors, none of the Directors is disqualified as on March 31, 2020 from being appointed as a director in terms of Section 164 (2) of the Act.

2.8 With respect to the adequacy of the internal financial controls over financial

reporting of the Company and the operating effectiveness of such controls, refer to our separate Report in “Annexure I”.

2.9 With respect to the other matters to be included in the Auditor’s Report in

accordance with Rule 11 of the Companies (Audit and Auditors) Rules, 2014, in our opinion and to the best of our information and according to the

explanations given to us:

i. The Company has disclosed the impact of pending litigations on its financial position in its financial statements – Refer Note No. 5.2.19 of Schedule 16 to the Financial Statements;

ii. The Company did not have any long-term contracts including derivative

contracts for which there could be any foreseeable future losses – Refer

Note No. 5.2.20 of Schedule 16 to the Financial Statements;

iii. There were no amounts required to be transferred to the Investor Education and Protection Fund by the Company – Refer Note No. 5.2.21of Schedule 16 to the Financial Statements.

With respect to the other matters to be included in the Auditor’s report, in terms of

the requirements of Section 197(16) of the Act, we report that the provisions of Section 34A of the Insurance Act, 1938are applicable to the managerial

remuneration payable to the Directors of Insurance Companies and which requires prior approval of IRDAI. Accordingly, the managerial remuneration threshold limits specified under Section 197 of the Act will not apply.

For Chaturvedi & Co. For NGS & Co. LLP Chartered Accountants Chartered Accountants

Firm Registration No. 302137E Firm Registration No. 119850W

DSR Murthy R. P. Soni Partner Partner

Membership No. 018295 Membership No. 104796

ICAI UDIN: 20018295AAAAAT8783 ICAI UDIN: 20104796AAAAZL6394

Place: Mumbai Date: June 24, 2020

Annexure I

Referred to in paragraph ‘2.8’ of ‘Report on Other Legal and Regulatory Requirements’ of our report of even date to the members of Edelweiss

General Insurance Company Limited (“the Company”) on the financial statements as of and for the year ended 31st March 2020.

Report on the Internal Financial Controls under Clause (i) of Sub-section 3 of Section 143 of the Companies Act, 2013 (“the Act”)

We have audited the internal financial controls over financial reporting of Edelweiss General Insurance Company Limited (“the Company”) as of March

31, 2020 in conjunction with our audit of the financial statements of the Company for the year ended on that date.

Management’s Responsibility for Internal Financial Controls

The Company’s management is responsible for establishing and maintaining internal financial controls based on the “internal control over financial reporting

criteria established by the Company considering the essential components of internal control stated in the Guidance Note on Audit of Internal Financial Controls

Over Financial Reporting issued by the Institute of Chartered Accountants of India”. These responsibilities include the design, implementation and maintenance of adequate internal financial controls that were operating effectively for ensuring the

orderly and efficient conduct of its business, including adherence to company’s policies, the safeguarding of its assets, the prevention and detection of frauds and

errors, the accuracy and completeness of the accounting records, and the timely preparation of reliable financial information, as required under the Companies Act, 2013.

Auditor’s Responsibility

Our responsibility is to express an opinion on the Company's internal financial controls over financial reporting based on our audit. We conducted our audit in

accordance with the Guidance Note on Audit of Internal Financial Controls Over Financial Reporting (the “Guidance Note”) and the Standards on Auditing prescribed

under section 143(10) of the Companies Act, 2013, to the extent applicable to an audit of internal financial controls. Those Standards and the Guidance Note require that we comply with ethical requirements and plan and perform the audit to obtain

reasonable assurance about whether adequate internal financial controls over financial reporting was established and maintained and if such controls operated

effectively in all material respects. Our audit involves performing procedures to obtain audit evidence about the

adequacy of the internal financial controls system over financial reporting and their operating effectiveness. Our audit of internal financial controls over financial

reporting included obtaining an understanding of internal financial controls over financial reporting, assessing the risk that a material weakness exists, and testing

and evaluating the design and operating effectiveness of internal control based on the assessed risk. The procedures selected depend on the auditor’s judgement,

including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion on the Company’s internal financial controls system over financial reporting.

Meaning of Internal Financial Controls Over Financial Reporting

A company's internal financial control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and

the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company's internal financial control over

financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable

assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles,

and that receipts and expenditures of the company are being made only in accordance with authorisations of management and directors of the company; and

(3) provide reasonable assurance regarding prevention or timely detection of unauthorised acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements.

Inherent Limitations of Internal Financial Controls Over Financial

Reporting Because of the inherent limitations of internal financial controls over financial

reporting, including the possibility of collusion or improper management override of controls, material misstatements due to error or fraud may occur and not be

detected. Also, projections of any evaluation of the internal financial controls over financial reporting to future periods are subject to the risk that the internal financial control over financial reporting may become inadequate because of changes in

conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Opinion

In our opinion, the Company has, in all material respects, an adequate internal financial controls system over financial reporting and such internal financial controls

over financial reporting were operating effectively as at March 31, 2020, based on “the internal control over financial reporting criteria established by the Company considering the essential components of internal control stated in the Guidance

Note on Audit of Internal Financial Controls Over Financial Reporting issued by the Institute of Chartered Accountants of India”.

Other Matter

The actuarial valuation of liabilities in respect of Incurred But Not Reported (the “IBNR”), Incurred But Not Enough Reported (the “IBNER”) and Premium Deficiency Reserve (the “PDR”) is the responsibility of the Company’s Appointed Actuary (the

“Appointed Actuary”). The actuarial valuation of these liabilities, that are estimated using statistical methods as at March 31, 2020 has been duly certified by the