annual report 2018–19 - australian taxation office · 10 program 1.1 australian taxation office...

TRANSCRIPT

20 18 19

Commissioner of Taxation annual report

Com

missioner of Taxation annual report 2018–19

ContactMailDirectorMeasures, Enterprise Strategy and DesignAustralian Taxation OfficePO Box 9977Civic Square ACT 2608

Phone (02) 6216 1111Email [email protected] report ato.gov.au/annualreportWebsite ato.gov.au

Copyright© AUSTRALIAN TAXATION OFFICE FOR THE COMMONWEALTH OF AUSTRALIA, 2019

You are free to copy, adapt, modify, transmit and distribute this material as you wish (but not in any way that suggests the ATO or the Commonwealth endorses you or any of your services or products).

Find ustwitter.com/ato_gov_aufacebook.com/ato.gov.auyoutube.com/AusTaxOffice

PublishedAustralian Taxation OfficeCanberra, October 2019NAT 0995-10.2019 DE-5137

AcknowledgmentsThank you to all ATO contributors.

Designed and editedDigital Experience and Events, ATO Corporate, Australian Taxation Office

PrintedPrinted on Monza Recycled paper that contains 99% recycled fibre, and elemental chlorine free pulp. All virgin pulp is derived from well-managed forests and controlled sources. Monza Recycled is manufactured by an ISO 14001 certified mill.

Commissioner of Taxationannual report 2018–19

II

Commissioner’s review

II

I am pleased to report on our performance for 2018–19, with the major progress of our Towards 2024 Plan to build trust and confidence in the administration of the ATO and develop a more streamlined, integrated and data-driven organisation. At the core of Towards 2024 is the ongoing focus on improving the client and staff experience and fostering a culture of service.

Building community trust and confidence in our administration of the tax and superannuation systems is a key to fostering willing participation. This year, we: � collected gross tax of around $533 billion, and provided refunds of around $107 billion,

with net tax collections of $426 billion, up $29 billion (7.4%) over the previous year � delivered a successful Tax Time 2018, with over 10 million individual income tax returns lodged,

resulting in almost 8 million refunds � delivered on our government commitments, including through our funded taskforces on

corporate tax avoidance, the black economy and financial crime � supported individuals to correctly claim work-related expenses, with an estimated revenue

impact of $560 million over the last two years � continued our analysis of tax gaps and, for the first time, published the individuals gap,

moving away from a focus on audit liabilities to a more preventative and pre-emptive approach � implemented reforms to the superannuation system, including downsizer superannuation

contributions, the first home super saver scheme, and early release of super on compassionate grounds

� implemented the Member Account Attribute Service and the Member Account Transaction Service

� improved the process to apply for an Australian business number (ABN) to better identify ineligible applicants.

We introduced a new measure to better understand community confidence in our administration, with a first-year result of 65 out of 100 – a solid result but with room for improvement.

Complaint numbers show we’ve moved in the right direction, with less than 20,000 complaints received in 2018–19 – the lowest number since 2009.

IIIIII

We will further strengthen trust and confidence as we become a more streamlined, integrated and data-driven organisation. This year, we: � streamlined processes through Single Touch Payroll (STP), with its successful deployment

resulting in over 160,000 employers reporting information for around 8.1 million individuals � used information from STP to pre-fill 2018–19 tax returns � laid the groundwork to enable over 15 million Australians to securely access government

services online – delivering key elements to establish a digital identity and integrate GovPass into the broader digital ecosystem

� invested in better technology for staff, including new computers and data analysis tools, providing access to more data to ensure better and more consistent services for our clients.

Our work on whole-of-government solutions continues to deliver improved services for end users. In 2018–19, we saw another increase in the number of individual taxpayers using myTax.

We saw an unprecedented number of returns lodged in the first week of Tax Time 2019, with more than half a million lodgments and as many calls to our contact centres. At its peak, we were processing an average of 7 million transactions a day.

By 30 September 2019, we had received over 9 million individual tax return lodgments (including around 1 million for prior years) and issued over 7 million refunds totalling over $20 billion.

We continue to engage and work constructively with those who help us deliver technology and services. During the year, we: � implemented our Online services for agents system, working with digital service providers (DSPs)

to integrate this functionality into their agents’ practice management software � developed collaborative relationships with suppliers, using an agency-wide approach to

procurement to create savings for the ATO and our providers � implemented Online services for DSPs to provide a modern and secure platform for their

interactions with us.

We confirmed our commitment to developing our people and the tools they use to do their work. This investment is paying off, with staff engagement as high as it has ever been and comparing well to other similarly sized agencies and the APS average. We achieved our performance targets for both women in senior leadership and Indigenous employment, indicators that we are becoming a more progressive and inclusive workforce.

Commissioner of Taxation annual report 2018–19

IV

Looking forwardWe have made progress towards our goal of bettering our interactions with clients, but I also recognise there is room for improvement. That is why our Better as usual program will focus on improving our clients’ experience with the tax system. As part of the program, we are: � reviewing the series of interactions a client may have with us that forms their end-to-end

experience – this ‘pipeline’ work will help us understand the hotspots that need attention � improving our quality feedback loops so we are drawing on our past experiences to improve

our services and make better decisions � dedicating a team to work on our most complex cases – we need to identify these cases early,

give them the priority they need and, where appropriate, take action with empathy to deliver the best outcome

� putting in place the right safeguards (cultural and procedural) for decisions and actions that can have significant client impacts.

Clients will have improved digital access to our systems and real-time transactions; and a greater whole-of-client view for our staff will enable them to take an end-to-end approach to a client’s tax affairs.

We are investigating new ways of working smarter, using artificial learning and automation to deliver better services. As the use of data and automation increases, we remain conscious of our role as custodians of Australians’ information. We need to be able to assure people that our use of data is legal and ethical and that our systems are secure. I want the ATO to keep this focus to ensure we maintain community trust.

In September this year, we launched our new culture strategy to support our staff as we seek to improve services to clients.

My Executive Team and I would like to thank the people in the ATO and our partners, who have made these positive results possible. We are looking forward to the progress we will make together in 2019–20 and future years.

Chris Jordan AO Commissioner of Taxation Registrar of the Australian Business Register

V

Letter of transmittal

COMMISSIONER OF TAXATION

The Hon. Michael Sukkar MP Minister for Housing and Assistant Treasurer Parliament House CANBERRA ACT 2600

Senator the Hon. Zed Seselja Assistant Minister for Finance, Charities and Electoral Matters Parliament House CANBERRA ACT 2600

Dear ministers

As the Accountable Authority for the Australian Taxation Office (the ATO), the Australian Charities and Not-for-profits Commission (ACNC) and the Tax Practitioners Board (TPB), I present you with the annual reports for the year ended 30 June 2019 for presentation to Parliament, in compliance with section 46 of the Public Governance, Performance and Accountability Act 2013.

The reports follow the guidelines approved by the Joint Committee of Public Accounts and Audit, as well as other legislative reporting requirements as listed in: � sections 17AA to 17AJ of the Public Governance, Performance and Accountability Rule 2014 � subsection 60-130(1) of the Tax Agent Services Act 2009 (for the TPB) � Division 130 of the Australian Charities and Not-for-profits Commission Act 2012

(for the ACNC).

Due to their operational independence and statutory obligations, the TPB and the ACNC have produced their own annual reports.

As required by section 10 of the Public Governance, Performance and Accountability Rule 2014, I certify that we have: � prepared fraud risk assessments and fraud control plans � appropriate fraud prevention, detection, investigation and reporting mechanisms that meet the

specific needs of the ATO � taken all reasonable measures to appropriately deal with fraud.

Yours sincerely

Chris Jordan AO Commissioner of Taxation and Registrar of the Australian Business Register 8 October 2019

The Hon. Dr Gary Johns Commissioner Australian Charities and Not-for-profits Commission

Ian Klug AM Chair of the Tax Practitioners Board

Commissioner of Taxation annual report 2018–19

VI

Contents

II Commissioner’s review

V Letter of transmittal

01 Overview 1 About us

3 Outcome and program structure

5 ATO Executive

8 Organisational structure

02 Annual performance statement

9 Statement by the Accountable Authority

10 Program 1.1 Australian Taxation Office

36 Program 1.2 Tax Practitioners Board

37 Program 1.3 Australian Business Register

41 Program 1.4 Australian Charities and Not-for-profits Commission

42 Administered programs 1.5 to 1.18

03 Revenue performance 47 Revenue collection

50 Tax performance

54 Total revenue effects

VII

04 Management and accountability

59 Corporate governance

70 Workforce management

92 Financial performance

05 Financial statements 103 About the financial statements

104 Financial statements

06 Appendixes 164 Appendix 1: Laws conferring powers on the Commissioner

165 Appendix 2: Taxpayers’ Charter – our performance

167 Appendix 3: Public advice and dispute management

171 Appendix 4: Legal services expenditure

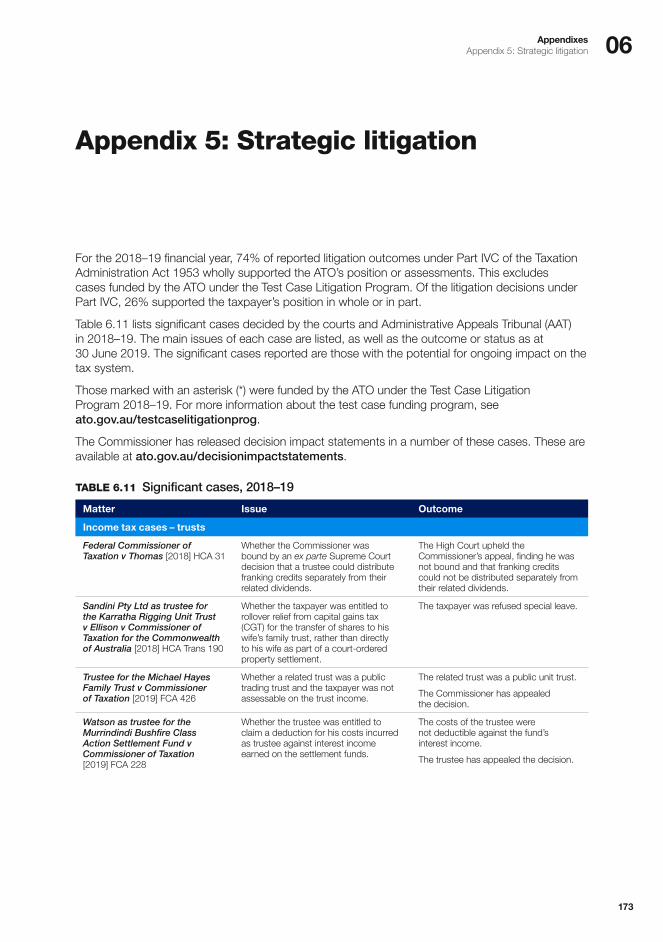

173 Appendix 5: Strategic litigation

177 Appendix 6: Debt management

179 Appendix 7: Compensation statistics

180 Appendix 8: Service commitments and activities

185 Appendix 9: Advertising, direct mail, media placement and market research

188 Appendix 10: Use of access powers

189 Appendix 11: Information provided to law enforcement agencies

195 Appendix 12: Corrections

198 Reference material

01 Commissioner of Taxation

annual report 2018–19

VIII

01Overview

About us

Our vision is to be a leading tax and superannuation administration known for our contemporary service, expertise and integrity.

As a Commonwealth entity within the Treasury portfolio, the ATO is accountable under the Public Governance, Performance and Accountability Act 2013 (PGPA Act) and the Public Service Act 1999 (PS Act).

Our ministersThe ministers with responsibility for matters relating to the tax and superannuation systems in 2018–19 were: � The Hon. Josh Frydenberg MP, Treasurer – from 24 August 2018 � The Hon. Scott Morrison MP, Treasurer – from 1 July 2018 to 24 August 2018 � The Hon. Michael Sukkar MP

— Minister for Housing and Assistant Treasurer – from 29 May 2019 — Assistant Minister to the Treasurer – from 1 July 2018 to 28 August 2018

� The Hon. Stuart Robert MP, Assistant Treasurer – from 28 August 2018 to 28 May 2019 � The Hon. Kelly O’Dwyer MP, Minister for Revenue and Financial Services – from 1 July 2018 to

28 August 2018 � Senator the Hon. Jane Hume, Assistant Minister for Superannuation, Financial Services and

Financial Technology – from 29 May 2019.

Senator the Hon. Zed Seselja was the minister responsible for the ACNC during 2018–19 as: � Assistant Minister for Finance, Charities and Electoral Matters – from 29 May 2019 � Assistant Minister for Treasury and Finance – from 28 August 2018 to 29 May 2019.

For more information on our ministers, see ministers.treasury.gov.au.

01 Commissioner of Taxation annual report 2018–19

2

ATO’s role and responsibilitiesThe Commissioner of Taxation is responsible for administering Australia’s tax system and significant aspects of Australia’s superannuation system. For the purposes of the PGPA Act, the Commissioner is the accountable authority for the ATO, the Tax Practitioners Board (TPB) and the Australian Charities and Not-for-profits Commission (ACNC). He is also the Registrar of the Australian Business Register (ABR).

The ATO operates as the Australian Government’s principal revenue collection agency, administering the legislation governing tax, and supporting the delivery of government benefits to the community. We are responsible for: � collecting revenue � administering the goods and services tax (GST) on behalf of the Australian states and territories � governing a range of programs that result in transfers and benefits back to the community � administering major aspects of Australia’s superannuation system � custodianship of the government’s Australian Business Register.

The TPB and ACNC operate independently of the ATO and each produces its own annual report. Their reports are available at tpb.gov.au and acnc.gov.au, respectively.

FIGURE 1.1 Scale of our activities

NOTEThe ATO interacts with groups shown in figure 1.1.

11.6 millionIndividuals not in business

4.2 millionSmall businesses including sole traders

865,000Employers

601,000Super funds

599,000self-managed super funds

230large APRA-regulated super funds

1,790small APRA-regulated super funds

201,000Not-for-profit organisations

164,000Privately owned and wealthy groups linked to over 769,000 entities

36,000Public and multinational business groups linked to over 81,000 entities

35,000Registered and active tax and BAS agents

01OverviewOutcome and program structure

3

Outcome and program structure

In 2018–19, the ATO had one outcome and was funded to deliver this through four agency programs and 14 administered programs. All deliverables for administered programs are achieved through making payments to eligible recipients in accordance with relevant laws.

ATO outcomeConfidence in the administration of aspects of Australia’s taxation and superannuation systems through helping people understand their rights and obligations, improving ease of compliance and access to benefits, and managing non-compliance with the law.

Agency programs

1.1 Australian Taxation Office (ATO)

1.2 Tax Practitioners Board (TPB)

1.3 Australian Business Register (ABR)

1.4 Australian Charities and Not-for-profits Commission (ACNC)

The ATO effectively manages and shapes the tax and superannuation systems that support and fund services for Australians, by:�� collecting revenue�� administering the goods and services tax on behalf of the Australian states and territories�� administering major aspects of Australia’s superannuation system.

The TPB ensures that tax practitioner services are provided to the public in accordance with appropriate standards of professional and ethical conduct by:�� administering a system to register tax practitioners, ensuring they have the necessary competence and personal attributes�� providing guidelines and information on relevant matters�� investigating conduct that may breach the Tax Agent Services Act 2009 (TASA), including non-compliance with the Code of Professional Conduct (the code), and breaches of the civil penalty provisions�� imposing administrative sanctions for non-compliance with the code�� applying to the Federal Court in relation to contraventions of the civil penalty provisions in the TASA.

The ABR program works with government, digital service providers, the business community and other key stakeholders to support a fairer business environment that fosters greater economic growth and job creation. This will be achieved through increased use of a trusted national business dataset and use of consistent information exchange standards.

The ACNC effectively manages a regulatory system for the Australian charitable sector by: �� registering eligible not-for-profit entities as charities in accordance with the ACNC Act 2012 and the Charities Act 2013�� providing information, guidance and advice about good governance practices and assisting charities to meet their obligations to maintain charity registration�� assessing concerns raised about registered charities, investigate where appropriate and initiate compliance action against charities that contravene the ACNC Act governance standards�� working with other government agencies (Commonwealth, state and territory) to reduce red tape on charities and align regulatory obligations through various mechanisms, including the ACNC’s Charity Passport.

NOTEWhile the TPB and ACNC are included in the ATO program structure and under the ATO outcome, they operate independently of the ATO and have produced their own annual reports. These are available at tpb.gov.au and acnc.gov.au respectively.

01 Commissioner of Taxation annual report 2018–19

4

Administered programs

Administered programs may be administered by the ATO with policy and delivery assistance from other Commonwealth agencies, or directly through the tax and superannuation systems. Our administered programs for 2018–19 were:

1.5 Australian Screen Production Incentive

1.6 Junior Minerals Exploration Incentive

1.7 Fuel Tax Credits Scheme

1.8 National Rental Affordability Scheme

1.9 Product Stewardship for Oil

1.10 Research and Development Tax Incentive

1.11 Low Income Superannuation Tax Offset

1.12 Private Health Insurance Rebate

1.13 Superannuation Co-contribution Scheme

1.14 Superannuation Guarantee Scheme

1.15 Targeted Assistance Through the Taxation System

1.16 Interest on Overpayment and Early Payments of Tax

1.17 Bad and Doubtful Debts and Remissions

1.18 Other administered programs:�� Seafarer Tax Offset

01OverviewATO Executive

5

ATO Executive

The Commissioner is supported by an executive team, with each member having responsibility for key aspects of the ATO’s performance.

The ATO Executive ensures that the ATO meets its commitments to government and the community. It determines priorities, sets direction and monitors progress towards achievement of strategic outcomes. The Executive also provides leadership, driving the client-focused culture of the ATO.

For more details about our senior leaders, see ato.gov.au/about-ato.

The Commissioner of TaxationChris Jordan AO was appointed as the 12th Commissioner of Taxation on 1 January 2013.

Chris has broad and lengthy experience in tax policy and law development and implementation, having held influential roles in the private sector and as a government advisor to both Labor and Coalition governments.

He was Chair of the Board of Taxation from June 2011 to December 2012 and a member of the Board since its inception in 2000. He also served as Chair of the Business Tax Working Group from 2011 to 2012, and as Chair of the New Tax System Advisory Board (1999 to 2001). He was a member of the Working Group that consulted with the mining industry about the resource rent tax (2011–12).

Chris has more than 35 years of experience in the tax and consulting profession. He started his accounting career with Arthur Andersen in 1979, was a senior lecturer in taxation at Sydney’s University of Technology from 1982 to 1985, and then worked at KPMG for over 25 years. From 1995 to 2000, he was Partner in Charge of the NSW Tax and Legal Division of KPMG, and from 2001 to 2012 was Chairman of Partners for KPMG NSW.

Until taking up his role as Commissioner of Taxation, Chris was the Chairman of the Committee for Sydney, a Director of the Bell Shakespeare Company and the Sydney Children’s’ Hospital Foundation, as well as a member of the Audit and Risk Committee for the NSW Art Gallery.

Chris has a Master of Laws (Sydney University) and Bachelors of Commerce and Law (University of NSW). He is a Fellow of Chartered Accountants Australia and New Zealand and a Chartered Tax Adviser with The Tax Institute.

Chris’s term as Commissioner of Taxation and Registrar of the Australian Business Register runs until 29 February 2024.

Chris Jordan AO, Commissioner of Taxation and Registrar of the Australian Business Register

01 Commissioner of Taxation annual report 2018–19

6

Executive team responsibilitiesFrances Cawthra is the Chief Finance Officer, providing leadership and direction to ATO Finance.

ATO Finance has a focus on strong financial and resource management, delivering a balanced budget, ensuring effective procurement and contract management, and providing insight into wise investment, productivity improvements, sustainability and agility.

Frances ensures that the ATO’s organisational strategy is informed by a financial perspective. She also leads ATO Finance to ensure the ATO is provided with robust reporting and insightful business intelligence, understands its obligations, and is supported in complying with Commonwealth requirements.

Jacqui Curtis, as Chief Operating Officer, is responsible for leading the ATO’s Enterprise Strategy and Corporate Operations Group.

The role of Enterprise Strategy and Corporate Operations is to ensure we are well positioned for Australian Public Service (APS)-wide reforms of corporate and shared services, and that our planning, governance, risk and change management are strategic and sensible.

Jacqui brings together an integrated picture of people and resource management, ensuring the ATO has the right capability and culture to deliver on our strategic intent. She plays a lead role in managing relationships with key stakeholders including scrutineers. All of these underpin our ability to deliver a better experience for both clients and staff.

Jeremy Hirschhorn is the Second Commissioner with overall responsibility for the ATO’s Client Engagement Group, which fosters willing participation in Australia’s tax and super systems through well-designed client experiences.

Across all client experiences – from the very largest public and multinational businesses to small businesses and individuals – the Client Engagement Group uses insights from client interactions to help design a tax system that makes it easier to comply, and harder not to. The group supports the integrity of the tax and superannuation systems by addressing non-compliance, and ensures increasing transparency about the operation of the system for taxpayers and key partners.

The group also plays an important role in working with the international tax community. Through collaborating with other jurisdictions the Client Engagement Group improves the way tax administrations work together to address arrangements used to evade and avoid tax.

Frances Cawthra Chief Finance Officer

Jacqui Curtis Chief Operating Officer, Enterprise Strategy and Corporate Operations Group

Jeremy Hirschhorn A/g Second Commissioner, Client Engagement Group

01OverviewATO Executive

7

Ramez Katf is the Second Commissioner with overall responsibility for the Enterprise Solutions and Technology Group, and the ATO’s Chief Information Officer.

Ramez provides leadership and strategic direction to modernising the revenue collection system and contributing to the government’s broader digital agenda.

The focus of Enterprise Solutions and Technology is ensuring we are taking advantage of the most innovative trends in technology to improve the experience of ATO staff and the community. This role has become increasingly important in balancing expectations and demand as new technology solutions continue to emerge.

Andrew Mills is the Second Commissioner with overall responsibility for the ATO’s law practice, including law interpretation, public advice and guidance, independent dispute prevention and resolution and our role in policy and law design.

The Law Design and Practice Group contributes to the administration of the tax and superannuation systems by seeking to make tax fair, simple and understood. We work collaboratively with Treasury and other agencies in supporting government outcomes and leading the ATO’s work on design of new policies and law. Our contribution also includes involvement at the early stages of engagement on advice or review and providing certainty through interpretation of the law and publication of guidance to support our clients in getting it right the first time.

We are committed to understanding the drivers of disputes, litigating only the right cases and encouraging prevention and ensuring earlier resolution where disputes happen.

Melinda Smith, as Chief Service Delivery Officer, has overall responsibility for the Service Delivery Group.

This part of the ATO is responsible for a broad range of the ATO’s foundation services for all segments of the community. These include processing payments, activity statements, income tax returns, superannuation lodgments and other forms, as well as administering the tax file number register, Australian Business Register and registers held on behalf of the superannuation industry.

The group focuses on working with ATO clients to understand their needs. It offers a tailored approach to help them meet their obligations as easily as possible through a range of contemporary tools, systems and services. It also engages with clients on a large scale and uses a strategic early intervention approach to educate them and influence willing participation.

The group is leading or contributing to a number of transformational initiatives for government. It works closely with other areas of the ATO to improve the experience for clients and drive greater efficiency and quality outcomes through better use of data, digitisation and building a strong service culture so the ATO is well positioned for the future.

Neil Olesen was the Second Commissioner with overall responsibility for the Client Engagement Group until November 2018.

Ramez Katf Second Commissioner, Enterprise Solutions and Technology Group

Andrew Mills Second Commissioner, Law Design and Practice Group

Melinda Smith Chief Service Delivery Officer, Service Delivery Group

0201 Commissioner of Taxation

annual report 2018–19

8

Organisational structure

The ATO is structured in five groups, each reporting to a member of the ATO Executive. Each group consists of a number of business areas.

FIGURE 1.2 ATO organisational structure, as at 30 June 2019

NOTEThe independent internal functions support the Commissioners and, for administrative purposes, are located in ATO Corporate.

Commissioner of Taxation and Registrar of the Australian Business Register

Chris Jordan AO

Enterprise Solutions and Technology GroupSecond Commissioner

Chief Information Officer

Ramez Katf

Client Engagement Group

Second CommissionerJeremy Hirschhorn

(acting)

Law Design and Practice Group

Second CommissionerAndrew Mills

Service Delivery Group

Chief Service Delivery OfficerMelinda Smith

Tax Counsel NetworkChief Tax Counsel

Kirsten FishDeputy Chief Tax Counsel

Peter WalmsleyDeputy Chief Tax CounselFiona Dillion

Deputy Chief Tax Counsel

Andrew EnglandDeputy Chief Tax Counsel

Hoa Wood (acting)Deputy Chief Tax Counsel

Public Advice and Guidance

Andrew Orme

Review and Dispute Resolution

Deputy CommissionerJeremy Geale

Policy, Analysis and Legislation

Deputy CommissionerLouise Clarke

Enterprise Strategy and Corporate

OperationsChief Operating Officer

Jacqui Curtis

Independent internal functions

Internal AuditChief Internal Auditor

Christina Li

Fraud Prevention and Internal Investigations

Assistant Commissioner

Susie Smith

Enterprise Strategy and Design

Deputy CommissionerDavid Allen

ATO PeopleDeputy Commissioner

Brad Chapman

ATO FinanceChief Finance Officer

Frances Cawthra

Enterprise Capabilities Deputy Commissioner

Matthew Hay

Technology, Architecture and

SecurityDeputy Commissioner

Susan Monkley

Digital DeliveryDeputy Commissioner

Chief Digital OfficerJohn Dardo

Service OperationsDeputy Commissioner

Alex Adams

Debt and LodgmentDeputy Commissioner

Robert Ravanello

Commonwealth Business Registry

ServicesDeputy Commissioner

Michelle Crosby

Strategy and SupportDeputy Commissioner

Emma Rosenzweig (acting)

Private WealthDeputy Commissioner

Tim Dyce

Small BusinessDeputy Commissioner

Deborah Jenkins

Integrated Compliance

Deputy CommissionerWill Day

Smarter Data ProgramDeputy Commissioner

Marek Rucinski

Public Groups and International

Deputy CommissionerRebecca Saint (acting)Deputy Commissioner

Mark Konza

Client Account Services

Deputy CommissionerGrant Brodie

ATO CorporateDeputy Commissioner

Sue Sinclair

Superannuation and Employer ObligationsDeputy Commissioner

James O’Halloran

Individuals and Intermediaries

Deputy CommissionerAlison Lendon

Machinery of Government TransitionDeputy Commissioner

Jane King

02Statement by the Accountable Authority

As the Accountable Authority of the Australian Taxation Office (ATO), I present the following annual performance statement. This statement has been prepared as required under paragraph 39(1)(b) of the Public Governance, Performance and Accountability Act 2013 (PGPA Act) and covers the period from 1 July 2018 to 30 June 2019.

In my opinion, and having considered the recommendations from the ATO Audit and Risk Committee, the annual performance statement accurately presents the ATO’s performance for the reporting period and complies with subsection 39(2) of the PGPA Act.

Chris Jordan AO Commissioner of Taxation and Registrar of the Australian Business Register

Annual performance statement

02 Commissioner of Taxation annual report 2018–19

10

Program 1.1 Australian Taxation Office

PurposeThe ATO purpose is to contribute to the economic and social wellbeing of Australians by fostering willing participation in the tax and superannuation systems. We achieve this through the delivery of our goals: � making it easier for people to participate � providing contemporary and tailored services � maintaining purposeful and respectful relationships � being a professional and productive organisation.

Our purpose is underpinned by nine strategic objectives. As shown in the ATO corporate plan, the objectives are grouped into five perspectives – Government, Client, Workforce, Operational and Financial.

Critically, the integrity of the tax and superannuation systems will be maintained by supporting those who choose to do the right thing and dealing with those who do not. Ultimately, client experience and participation will be the true measure of success. The following sections outline the results of our performance measures and progress on reaching our objectives.

Program overviewThis overview of ATO program performance aligns with the ATO corporate plan 2018–19, and presents our 2018–19 performance against each of the nine strategic objectives.

For each strategic objective, we outline our key 2018–19 achievements in relation to: � the strategic initiatives outlined in the corporate plan � our most significant business activities, such as Tax Time 2018.

A summary of performance results is provided for each strategic objective, with more detail and analysis provided on pages 26 to 35.

02Annual performance statementProgram 1.1 Australian Taxation Office

11

Strategic objective: G1 Government

We build community confidence by sustainably reducing the tax gap and providing assurance across the tax and superannuation systems

Overview

The ATO aims to provide the community with confidence in our administration of the tax and superannuation systems, and that this results in the collection of the right tax at the right time, for the wellbeing of all Australians. To provide that confidence, we need to understand the effectiveness of our approach, which we do by using performance measures, tools such as tax gap analysis, and sharing information with other agencies in Australia and internationally.

We use our understanding of the tax system to help design improvements to our administration. We will continue to shift to a more preventative and pre-emptive approach, sustainably closing the tax gap.

Of the eight performance measures for strategic objective G1, we fully met four targets, substantially met two, and have two targets under development. We also introduced a confidence measure aligned to our 2024 aspirations of building trust and confidence.

Strategic initiatives summary

We delivered on our government commitments, including through our taskforces on tax avoidance, serious financial crime, illegal phoenix activity and the cash economy. Significant achievements for the ATO’s taskforces include: � the Tax Avoidance Taskforce raised $1.9 billion in liabilities and $1.1 billion in cash collections

(apportioned figures) � the Serious Financial Crime Taskforce raised $235 million in liabilities and $71 million in cash

collections � the Black Economy program raised $1.1 billion in liabilities � the Phoenix Taskforce raised $163 million in liabilities and almost $66 million in cash collections.

We contributed to operations as part of the Illicit Tobacco Taskforce, which was established on 1 July 2018, as well as ATO-specific operations, which resulted in the seizure and destruction of illicit tobacco with an estimated excise duty of $42 million.

In July 2018, we released the first estimated individuals tax gap, covering taxpayers who are salary and wage earners and investors, but not in business and not high wealth individuals. We estimate that over 93% of income tax due from individuals is paid, mostly voluntarily, or with little intervention from us. The tax gap is discussed in greater detail on page 50 and on our website at ato.gov.au/taxgap.

Through our justified trust program, we assure the tax compliance of large corporate groups and privately owned and wealthy groups. We engage with the top 1,100 public and multinational businesses and superannuation funds and the top 320 privately owned and wealthy groups, obtaining positive assurance on a significant proportion of these clients. This year, we assured 50%

02 Commissioner of Taxation annual report 2018–19

12

of the $47 billion of income tax payable by public and multinational businesses for the 2016–17 financial year and increased our assurance of the $40 billion payable by these businesses in 2015–16 from 50% to 58%. We also assured $2 billion of income tax payable by privately owned wealthy groups across multiple income years.

To confirm or clarify our interpretation of the tax law, we use strategic litigation for cases with the most precedential value. We had a higher number of applications considered by the Test Case Litigation Panel this year, receiving 26 compared to 14 in 2017–18. During the year, there were 102 tax litigation decisions handed down, and 75 of these fully supported the ATO position. For more information about our strategic litigation, see Appendix 5. For statistics about our public rulings, see Appendix 3.

We implemented an integrated compliance approach to identify endemic non-compliers – those organisations that are not engaging in identified criminal behaviour but are failing to comply with multiple obligations. To illustrate the complexity of this work, one group we identified as high risk comprises over 40 entities, with assets totalling approximately $70 million.

In 2018–19, we supported the superannuation system by helping Australians connect with their super. ATO Online services were used to consolidate over 537,600 accounts worth $4.4 billion. To improve and streamline APRA-regulated fund reporting and provide greater ‘real time’ visibility of superannuation contributions and other transactions, we implemented the Member Account Attribute Service (MAAS) and Member Account Transaction Service (MATS). To protect retirement savings for members of self-managed super funds (SMSFs), we reviewed and audited SMSF funds, trustees and auditors. This work included: � cancelling 609 new registrations and withholding 229 funds from Super Fund Lookup, protecting

nearly $100 million of individuals’ retirement savings � responding to serious regulatory contraventions by issuing 26 notices of non-compliance,

disqualifying 145 trustees and issuing administrative penalties against the trustees of 146 SMSFs, resulting in net penalties of $3 million

� reviewing 151 SMSF auditors, resulting in 52 referrals to the Australian Securities and Investments Commission (ASIC).

02Annual performance statementProgram 1.1 Australian Taxation Office

13

Strategic objective: G2 Government

We design for a better tax and superannuation system to make it easy to comply and hard not to

Overview

The tax and superannuation systems need to evolve so that they remain sustainable for collecting Australia’s revenue. They need to be easy to comply with and hard not to, transparent in their operations, and provide for a seamless client experience. The ATO is well placed to influence the design of the law to fix system irritants, address loopholes that allow people to avoid their obligations, and make use of new technology.

The one measure for this objective achieved a rating of good. Although the target was still under development in 2018–19, a target has been set for 2019–20.

Strategic initiatives summary

We contribute to the shaping of the tax and superannuation systems, assessing where the law has not been working as intended, using insights and developing ideas to improve the systems. We endeavour to influence proposed policy and legislation and share our analytical expertise by: � providing data and costings advice on policy proposals � working closely with Treasury on ATO-generated new policy proposals, as well as those led

by Treasury, including revenue proposals sought by Treasury for the Budget and the Mid-Year Economic and Fiscal Outlook

� collaborating with Treasury on the design of new legislation, and providing input into explanatory materials and joint quality assurance of draft laws.

Our relationship with Treasury is a significant component in successfully influencing new legislation (see performance measure: Influence on page 31).

We provide tax and superannuation systems insights and responses and inform policy development and research. Along with our annual publication of aggregated taxation statistics, in 2018–19, we: � worked with the Board of Taxation on a survey on compliance costs associated with fringe

benefits tax � provided access to our database of ‘confidentialised’ longitudinal data on individual income tax

returns to researchers in 19 Australian universities, and expanded the database � contributed to a whole-of-government public data strategy overseen by the Department of

Prime Minister and Cabinet � provided research and data to inform the Council of Financial Regulators final report into risk

and leverage in the superannuation system, in addition to providing information and calculations to support the Productivity Commission’s review into the efficiency and competitiveness of the superannuation system

� assisted with the Australian Bureau of Statistics (ABS) Multi-Agency Data Integration Project, the Department of Social Security’s research into the National Disability Insurance Scheme (NDIS) workforce, and the work of the Department of Jobs and Small Business following closure of the Australian automotive manufacturing industry, including their assessment of retraining programs.

02 Commissioner of Taxation annual report 2018–19

14

Strategic objective: C1 Client

Our client experience and interactions are well designed, tailored, fair and transparent

Overview

We are improving the experience our clients have by designing a tax and superannuation system that is seamless and easy to use. This includes the experience for those of our clients who may disagree with our decisions and seek some form of formal review. We are taking advantage of the growing opportunities offered by the expanding digital world to provide people with the information they need, when they need it and in their preferred format.

We delivered a successful Tax Time 2018, with over 10 million individual income tax returns lodged, resulting in almost 8 million refunds.

Of the two performance measures for strategic objective C1, we fully met one target and substantially met the other. We continued to expand the scope of our digital services to progress our journey to 2024.

Strategic initiatives summary

We streamlined processes through Single Touch Payroll (STP) and worked with software developers to expand STP to employers with fewer than 20 employees, ensuring there will be a good range of low-cost reporting software in the market – including low-cost or no-cost products for employers with fewer than four employees.

As at 30 June 2019, we had 58,600 substantial employers (80% of the target population) reporting tax and superannuation information through STP, and another 108,000 employers with fewer than 20 employees voluntarily reporting before the legislative start date for this group. More information about STP is available at ato.gov.au/STP.

By delivering a range of digital channel experience options, we help meet client expectations of a ‘24x7’ service and reduce our reliance on paper to contact clients. By identifying what people need to know, we can make it available through self-service channels such as our website. This year we: � digitised the Australian business number (ABN) confirmation letter, replacing over 800,000 letters

a year � provided more self-help tools for tax professionals and coached callers on how to use the tools � stopped sending paper activity statements for monthly self-preparers and quarterly

agent lodgers.

Our support for small businesses included: � assistance to farmers and drought-affected businesses in New South Wales, Victoria and

South Australia through the federal government’s Drought Community Outreach program � the Reach Out Indigenous Business Support program pilot, with workshops held in Ipswich,

Darwin and on Palm Island, reaching up to 450 Indigenous business owners � over 2,300 workshops and webinars on a range of topics

02Annual performance statementProgram 1.1 Australian Taxation Office

15

� over 1.6 million emails distributed as part of our New to business essentials service � letters, emails and SMS to over 143,000 new clients in high-risk industries to provide information

on the taxable payments reporting system � our Small Business Newsroom service, with 19% more subscribers this year.

For more information about our small business workshops, see lets-talk.ato.gov.au/sbworkshops.

We produced proactive advice and guidance on a range of issues, including the expansion of the taxable payments reporting system, changes to the small business tax rates, and the tax treatment for compensation paid to individuals following the Royal Commission into banking misconduct. We continued our communication and education programs, delivering new training modules for small businesses to address specific tax avoidance behaviours identified by our Black Economy Taskforce, along with our regular workshops and webinars. Our Indigenous helpline received a record 25,000 calls for specialised tax and superannuation assistance this year.

Several dispute resolution initiatives were implemented during the year, including: � an Independent Review for Small Business program pilot, designed to give small businesses

an opportunity to have their audit with us reviewed before any assessments or amended assessments are issued

� our Dispute Assist service, offering help to unrepresented individuals and small businesses with significant or exceptional personal circumstances

� new National Tax Clinics operated by 10 universities for taxpayers who may not be able to afford professional advice or representation but are looking for independent guidance

� a new Small Business Taxation Division of the Administrative Appeals Tribunal (AAT), developed in conjunction with the Treasury, the AAT, the Inspector-General of Taxation and Taxation Ombudsman (IGTO) and the Australian Small Business and Family Enterprise Ombudsman.

We resolved over 26,000 objections, which represents less than 0.1% of over 37 million returns lodged. There were 441 applications for review or appeal to the AAT or other courts in 2018–19, with 102 decisions made either in relation to these applications or applications made in earlier years. The significant gap between the number of applications and actual decisions reflects the fact that most matters are resolved through alternative dispute resolution. For more information on the numbers of disputes, see Appendix 3.

We sought independent assurance and advice from experts on the application of complex legal matters, and referred our most significant decisions on disputes for review. During 2018–19: � the General Anti-Avoidance Rules (GAAR) Panel assessed 28 matters, including share buy-back

transactions, with the GAAR provisions held to apply in 10 matters � the Public Advice and Guidance Panel considered 7 matters, including employee travel

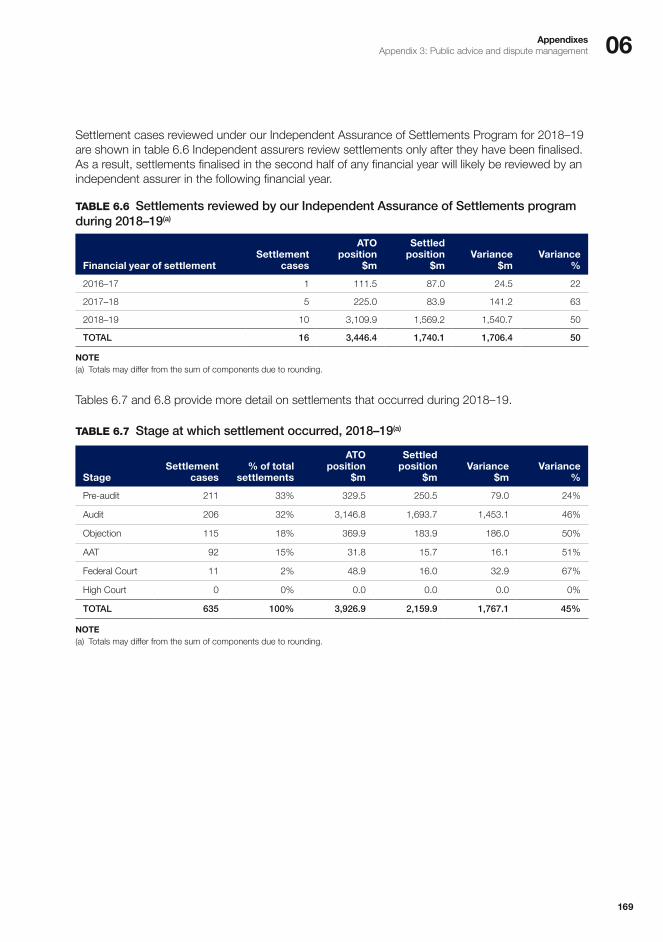

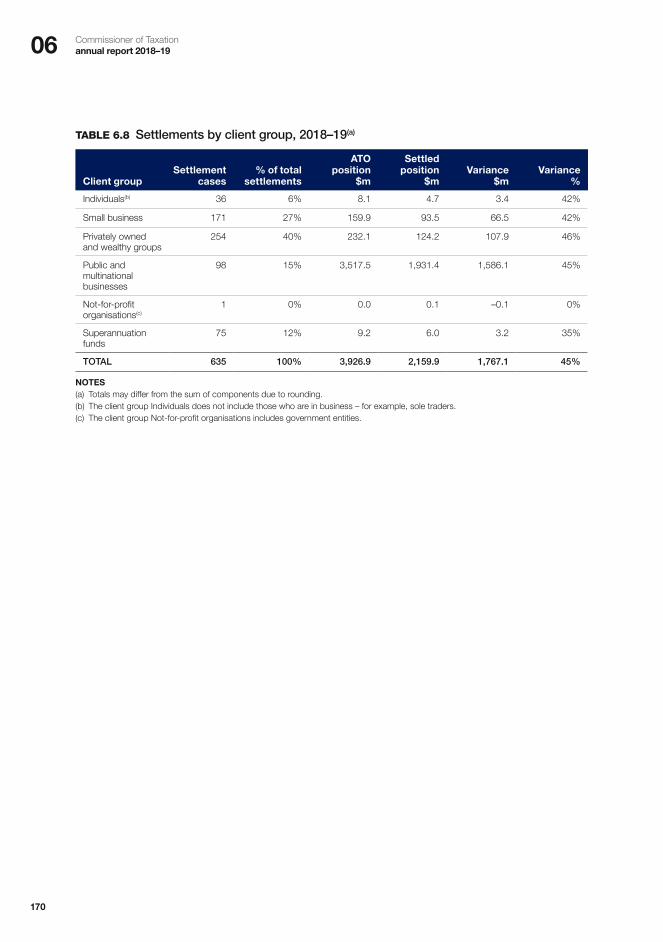

expenses, work-related expenses for truck drivers, and GST relating to financial services � under the Independent Assurance of Settlements program, 16 reviews were finalised, with our

actions considered to be fair and reasonable in 13 cases.

For more details on settlement cases, see Appendix 3.

02 Commissioner of Taxation annual report 2018–19

16

Strategic objective: C2 Client

We work with and through others to deliver efficient and effective tax and superannuation systems

Overview

Our goal is to make it as easy as possible for clients to meet their tax and superannuation obligations and to interact with our systems when they need to do so. It is also important to maintain a strong relationship with our international counterparts so effective action can be taken when people attempt to use jurisdictional borders to block our effective administration.

By working closely with and learning from tax practitioners, digital service providers and overseas jurisdictions, not only is our role as an advocate for change made easier, we can build better tools that support our clients, whether they deal with us directly or through a third party. By enabling access to ATO systems via application programming interfaces (APIs), we can work with partners to provide a more streamlined ecosystem.

The ‘working together’ measure for this objective achieved a result of 64/100. Although the target was still under development in 2018–19, a target has been set for 2019–20.

Strategic initiatives summary

Through our international collaboration with other tax administrators, information is shared to influence tax reform and identify global trends and best practices. This year, our involvement with the Organisation for Economic Co-operation and Development (OECD) included co-hosting the fifth meeting of the Global Forum on Value Added Tax and GST and presenting at the Forum on Tax Administration in Chile. Our work on issues raised by the Panama and Paradise papers was recognised by the Chair of the OECD’s Forum on Taxation Administration.

We completed our first international exchange under the new Common Reporting Standard, receiving over 1.5 million financial accounts to review from over 60 tax jurisdictions – including those that have been associated with tax havens and bank secrecy.

The Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting came into effect this year, enabling jurisdictions to swiftly modify their tax treaties to better address multinational tax avoidance and more effectively resolve tax disputes. Together with New Zealand Inland Revenue, we published a joint administrative approach, to provide certainty for eligible taxpayers and allow us to prioritise our resources on matters with material revenue consequences or a higher risk of tax avoidance.

We delivered significant changes to our tax and BAS agent services in 2018–19. Our practitioner lodgment service (PLS) became the sole channel for tax agents to electronically lodge current year income tax returns, with approximately 6.8 million returns successfully lodged during Tax Time 2018. For agents using the service, more of their clients had their refunds processed within five days compared to previous years.

02Annual performance statementProgram 1.1 Australian Taxation Office

17

Since March 2019, all tax and BAS agents have been able to access Online services for agents. This system replaces our tax and BAS agent portals with a modern, customisable interface that addresses portal irritants and provides access to new functionality. It delivers more real-time client information, such as individuals’ superannuation and income tax return history, and includes the ability to create payment plans and search for clients by name. More information is available at ato.gov.au/onlineservicesforagents.

We partnered with 530 digital service providers (DSPs) consuming 269 web services. An online service was introduced to streamline interactions with DSPs, providing a secure environment to access support. We reviewed all DSPs against the ATO’s Operational Framework, with all DSPs – representing 676 digital products – meeting the requirements. Extending on the framework and at the request of industry, ATO worked in collaboration with the Australian Business Software Industry Association to develop common cyber security standards for add-on marketplaces.

02 Commissioner of Taxation annual report 2018–19

18

Strategic objective: W1 Workforce

We are a high-performing, responsive and professional workforce with the right culture to deliver now and for the future

Overview

The ATO works to provide support and strategies to help us transform our culture and workforce so we can deliver now and into the future. This includes ensuring we have the right balance of capability to deliver the best client and staff experiences and drive a positive cultural change, with a focus on integrity, to foster a collaborative and contemporary way of working.

We met the performance target for each of the three measures for strategic objective W1, with two measures improving since last year and the other remaining at its highest level. This demonstrates continued improvement in the engagement of our staff and the diversity of our workforce.

Strategic initiatives summary

We developed our Workforce Strategy 2024 to describe our future workforce and outline the high-level initiatives required to achieve it. Given the dynamic environment the ATO operates in, and our dependencies on external influences, the strategy will be updated as our view of the future evolves. A new future-focused capability framework was implemented, outlining the core sets of skills, knowledge, attributes and behaviours we need to successfully deliver our administration of the tax and superannuation systems. Our training programs are being aligned to the new framework to support staff in their pursuit of ongoing learning and development.

Recognising the importance of a positive culture for the achievement of our strategic and organisational goals, we have committed to supporting our people in demonstrating the cultural traits. We communicate regularly with our staff about what our culture means for them, the community, and why it is critical to achieving our organisational outcomes. We assessed our progress at making cultural change through consultation, perception surveys and independent feedback, finding that our staff and the community have seen real and positive cultural change.

Our Integrity Adviser, Dr Simon Longstaff, worked with our Chief Risk Officer, the ATO Executive Committee and staff across the ATO, to help us extend our view of integrity so that we overtly consider our ‘integrity position’ in what we do and say, and make good decisions guided by ethics. We updated various processes for SES officers and staff to declare interests and other circumstances that could influence (or be seen to influence) their actions at work. This is fundamental to embedding transparency and integrity as part of our culture and providing confidence that we remain vigilant about managing perceived and real risks. A highlight this year was our Security, Integrity and Fraud Awareness week, with external speakers, panel discussions, webinars, and training sessions.

02Annual performance statementProgram 1.1 Australian Taxation Office

19

Strategic objective: W2 Workforce

We provide the right tools and workplace so staff can deliver the best client experience

Overview

We are committed to giving our staff contemporary tools that make it easier to help our clients and collaborate with each other. In 2018–19, we identified a number of system irritants that – while minor in themselves – added up to serious barriers across our organisation. We worked together to learn from our shared experiences and identify new ways to integrate solutions across the organisation.

In the ATO corporate plan 2018–19 we introduced a new measure for this objective, with a result of 63% this year. Although the target was under development in 2018–19, a target has been set for 2019–20.

Strategic initiative summary

To improve the staff experience, our highest priority for 2018–19 was to refresh our desktop and laptop hardware which has significantly improved the time it takes to log in, as well as overall speed and performance. The upgrade also ‘opens the door’ to new and better software, including contemporary collaboration tools. All laptops and 62% of our desktops have been replaced with newer models and any remaining aged desktop computers will be replaced by the end of 2019. This is a significant step in assisting the ATO in becoming streamlined, integrated and data-driven. This year, one of the biggest staff irritants of having to manage mailbox capacity was resolved by increasing staff mailbox size.

Not all innovations require such a large financial investment. Our staff are encouraged to find ways to work smarter and support each other in their day-to-day work. One example is our PowerPit tool, which was designed and built by staff using existing technology. PowerPit enables experienced staff to share their expertise with new front-line officers, using an immersive training environment. This gives trainees fundamental hands-on practice as part of their training – before they take calls from clients. It complements other training they undertake, enabling them to focus on providing the right information and ultimately improve the caller’s experience.

We continue to look for opportunities to build on and connect with other initiatives to drive improved staff and client outcomes by maximising the value from data and analytics, including our enterprise client profile. We listen to our people about the tools that will best support them, through focus groups, surveys and census results – recognising that our staff are at the heart of the ATO and their experience and engagement is critical to delivering the right client experience.

To provide staff with a view of the improvements being made, we have taken a coordinated and holistic approach to informing them of initiatives that affect them. In 2018–19, we launched an online ‘Improving Our Staff Experience’ hub, making it easy for staff to see the full set of experience improvements the organisation has made and plans to make in the future. Complementing the hub, we delivered a Staff Experience Showcase spotlighting the ‘now, soon and later’ improvements and helping staff envision how they can work smarter and more efficiently, both now and into the future, using the new ATO tools, technology and workspaces.

02 Commissioner of Taxation annual report 2018–19

20

Strategic objective: O1 Operational

We use data and insights to deliver value for our clients and inform decision making across everything we do

Overview

Our transition towards being a streamlined, integrated and data-driven organisation relies on having the right data available for our staff and clients, the tools to manage and derive insights, and the capabilities to understand and use the data in innovative ways. We are embracing new technologies, work patterns and data-learning programs to ensure our staff have the data, insights and skills they need to work smarter and improve interactions with clients. Our use of automation, artificial intelligence and sophisticated analytical techniques will continue to help us better understand our clients and provide the tailored and timely services they expect.

This objective had one measure, which achieved a result of 87.9%. While the target was still under development in 2018–19, a target has been set for 2019–20.

Strategic initiatives summary

Implementation of initiatives, such as Single Touch Payroll and the progress of the automatic exchange of information with other countries, means that much more data is coming into the ATO. We are focused on continuing to enhance our data acquisition and quality program and have the infrastructure and tools available to manage and use data we collect in an ethical and transparent way. More sophisticated tools have been implemented to ensure the quality of our data and better transform it into usable and repeatable processes that can be streamlined into automated processes. Faster and more precise insights enable improved compliance outcomes through greater personalisation and more targeted and effective interactions. The mapping of third-party datasets is a key element of our work and provides staff with more relevant information to improve decision making. For example, in 2018–19 we obtained data to better understand how ride-sharing and short-term accommodation providers may impact on the tax system.

Our enterprise client profile system is designed to provide our staff with access to client facts and insights. The system visualises consistent and timely information insights in a contemporary way that can be tailored to specific work requirements. The use of enterprise client profile has created efficiencies in providing a complete view of relevant information to support staff in their interactions with clients. For example, staff visiting around 10,000 small businesses as part of our work on the Black Economy Taskforce, were able to access a real-time profile of client facts, history and insights for use prior to and during visits.

02Annual performance statementProgram 1.1 Australian Taxation Office

21

We are progressing new and innovative ways of using automation and artificial intelligence to streamline business processes, automate repetitive tasks and improve decision making. Machine learning and robotic process automation (RPA) technologies provide opportunities to increase our understanding of client behaviours and create efficiencies for more repetitive tasks. This year, we designed and tested the suitability of RPA software and trialled the extension of machine learning to categorise taxpayer deduction claims and identify risks at a more detailed level. RPA effectively uses technology that follows a pre-programmed set of actions to automatically undertake repetitive, manual and high-volume tasks.

Using sophisticated analysis techniques, we are able to compare returns prepared by tax agents with a similar client base. To identify areas of concern or risky behaviour we apply a nearest neighbour approach to compare claims. This allows us to identify areas where agents would benefit from more information and support, and cases where intervention is necessary. This year, we developed a model to give us a holistic view of multiple risks in the tax agent profession, and systematically identify or predict changing behaviour in a timely way.

02 Commissioner of Taxation annual report 2018–19

22

Strategic objective: O2 Operational

Our technology and digital services deliver a reliable and contemporary client experience

Overview

Meeting community expectations that our systems will be secure and available when required and on a variety of platforms is an ongoing challenge. Our focus has been on making it easier for our clients to interact with us, as well as updating the systems we use to manage the tax and superannuation systems.

This objective had two measures, with our security policy report requirements met and our key digital systems availability achieving 99.5%. Although targets were still under development in 2018–19, a target has been set for the measure that was retained for 2019–20.

Strategic initiatives summary

With rapid growth in online activity there is greater opportunity for fraudsters to steal and sell personal data. The ATO will continue to invest in securing taxpayer information through robust identity, authentication and authorisation platforms. In June 2019, the myGovID app was released to enable people to securely establish and manage their digital identity with us and across government. We delivered Relationship Authorisation Manager (RAM), a new way for people to establish relationships and manage who is authorised to act on their behalf. Authorised representatives of businesses are now able to securely prove their identity using myGovID, link their ABN, manage their authorised contacts, and use the myGovID app to authenticate and access the ATO Business Portal. Tax agents operating on behalf of their clients will soon be able to use myGovID and RAM to access the new ATO Online service for agents.

We increased our cyber security capabilities in controls for compliance and protection against security threats, continuing maturity in detection and response functions, preparation for major initiatives that build our visibility of vulnerabilities and gaps in the environment, and increasing our security certification programs.

Modernisation of our infrastructure for improved ATO systems resilience included relocating critical applications to a more resilient storage system, and providing dedicated infrastructure for Online services for agents and ATO Online capability to improve performance and stability for Tax Time 2019. We upgraded the tools we use to interact with our clients over the phone, including improved voiceprint matching, which has reduced average call times for clients. To help our staff provide better services to clients and work together from different sites, we updated desktop and laptop computers and expanded security and functionality of online training and meeting rooms.

02Annual performance statementProgram 1.1 Australian Taxation Office

23

We improved the functionality of our systems, making significant progress in resolving an ongoing issue that means some clients with different taxes have more than one account with us, by creating a single client account. We will need to migrate close to 17 million activity statement accounts to our primary accounting system. The move will bring the processing of 95% of taxpayer financials into one system, resulting in fewer delays in issuing refunds and most account transfers happening without the need for a manual request. Our single case management system and analytics-driven approach to managing outstanding payments across all account types ensures more tailored treatments and interventions in the collection of debt.

02 Commissioner of Taxation annual report 2018–19

24

Strategic objective: F1 Financial

We strive for operational excellence to achieve efficiency and quality outcomes

Overview

We have established a range of initiatives to deliver better productivity and outcomes, improve data quality, and drive consistent and streamlined systems and processes for staff. This ensures we can meet client expectations in a cost effective way, reduce operating costs and get better value.

Of the two performance measures for strategic objective F1, we fully met both targets.

Strategic initiatives summary

Working smarter to be more efficient is one of the benefits from many of our objectives, from extending our use of data to developing our staff. In addition to automating processes where we can, we have made business improvements through work redesign. Simplifying how we work has resulted in faster processing speeds and fewer escalations and transfers. Our Debt staff now manage both debt and outstanding lodgments for clients, rather than only dealing with existing debt.

We recognised the nexus between delivering small changes and achieving operational excellence and efficiency. We will be looking at how we manage the implementation of small changes across the ATO in 2019–20.

In 2018–19, we initiated a program to transform our outbound communications to ‘digital first’. We reduced the paper correspondence we send by replacing it with email, SMS, the myGov Inbox and the tax and BAS agent portals, or by sending it less often. We estimate that we will save $2 million each year by sending clients their general interest charge (GIC) statement of account quarterly instead of monthly.

We continued to develop our strategic procurement capability in line with changes to government procurement, including the Modern Slavery Act 2018, Government Procurement (Judicial Review) Act 2018, and the updated Black Economy Procurement Connected Policy. Working with our outsource providers, we focused on building collaborative partnerships that create more value for the ATO and our providers. With so many active contracts to support our successful operation, we are also conscious of our responsibility to see that our procurement ensures supply chain integrity and delivers social outcomes.

02Annual performance statementProgram 1.1 Australian Taxation Office

25

Performance results overviewThe ATO performance results for 2018–19 show a year of solid performance in achieving our purpose, with some specific areas for improvement. The ATO has 21 measures for Program 1.1 to demonstrate how well we are achieving our purpose. These are set out in the Australian Taxation Office Budget Statements in the Treasury Portfolio Budget Statement (PBS), and in the ATO corporate plan 2018–19.

Thirteen of these measures had a 2018–19 performance target, with the target fully achieved for ten and substantially achieved for the remaining three. In 2019–20, we will be looking at what we need to do differently to fully meet our own and the community’s expectations and to build trust and confidence in our administration of the tax and superannuation systems.

The intention of the annual performance statement is to report on the performance criteria included in the PBS and corporate plan to accurately reflect the performance of the ATO in achieving its purpose. In considering our overall assessment of fostering willing participation we have regard to: � the complexity of the tax and superannuation environment and how our activities influence the

behaviour of clients in meeting their obligations � the interrelated nature of performance criteria, which means that results should be viewed as a

suite of indicators, rather than in isolation � the use of estimates for some criteria.

In addition, it is important to note the trends over time in results, both in absolute terms and relative to the performance target for the relevant year. We assess our performance targets annually to determine where existing results are expected to be maintained and where future performance is expected to be stronger. Some of our performance targets were under development, due to a lack of relevant external comparators to benchmark ourselves against and the time it can take to baseline results to understand what future improved performance we should be aiming for. We will continue to monitor and assess performance as we build on the outcomes we have achieved to date.

Performance results

Our performance criteria are set out on pages 185–189 of the Australian Taxation Office Budget Statements (in the Treasury PBS), and pages 5–13 and 22–23 of the ATO corporate plan 2018–19.

02 Commissioner of Taxation annual report 2018–19

26

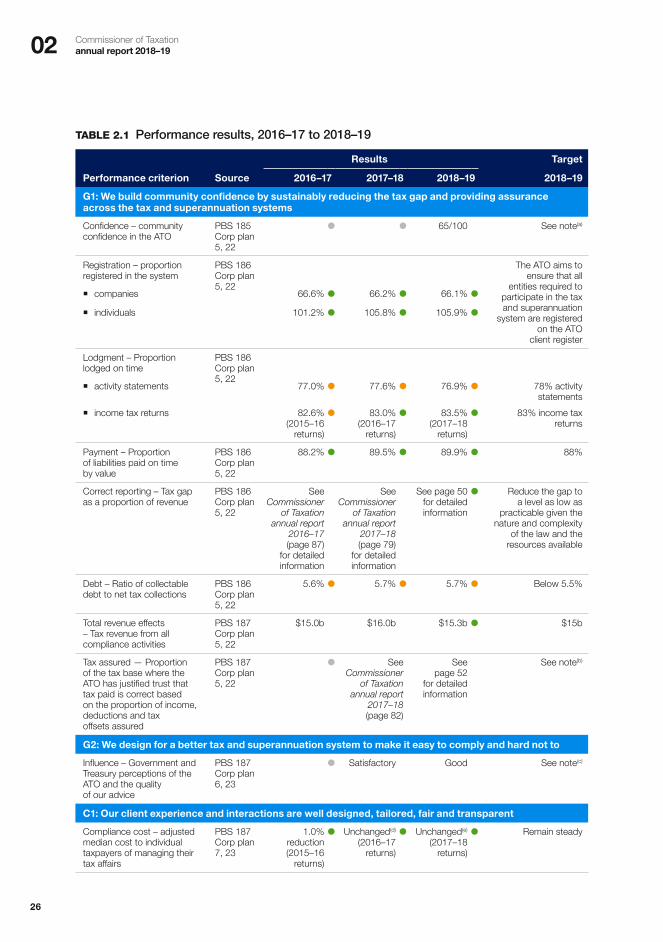

TABLE 2.1 Performance results, 2016–17 to 2018–19

Results Target

Performance criterion Source 2016–17 2017–18 2018–19 2018–19

G1: We build community confidence by sustainably reducing the tax gap and providing assurance across the tax and superannuation systems

Confidence – community confidence in the ATO

PBS 185 Corp plan 5, 22

65/100 See note(a)

Registration – proportion registered in the system

PBS 186 Corp plan 5, 22

The ATO aims to ensure that all

entities required to participate in the tax and superannuation

system are registered on the ATO

client register

� companies 66.6% 66.2% 66.1%

� individuals 101.2% 105.8% 105.9%

Lodgment – Proportion lodged on time

PBS 186 Corp plan 5, 22

� activity statements 77.0% 77.6% 76.9% 78% activity statements

� income tax returns 82.6% (2015–16

returns)

83.0% (2016–17

returns)

83.5% (2017–18

returns)

83% income tax returns

Payment – Proportion of liabilities paid on time by value

PBS 186 Corp plan 5, 22

88.2% 89.5% 89.9% 88%

Correct reporting – Tax gap as a proportion of revenue

PBS 186 Corp plan 5, 22

See Commissioner

of Taxation annual report

2016–17 (page 87)

for detailed information

See Commissioner

of Taxation annual report

2017–18 (page 79)

for detailed information

See page 50 for detailed information

Reduce the gap to a level as low as

practicable given the nature and complexity

of the law and the resources available

Debt – Ratio of collectable debt to net tax collections

PBS 186 Corp plan 5, 22

5.6% 5.7% 5.7% Below 5.5%

Total revenue effects – Tax revenue from all compliance activities

PBS 187 Corp plan 5, 22

$15.0b $16.0b $15.3b $15b

Tax assured — Proportion of the tax base where the ATO has justified trust that tax paid is correct based on the proportion of income, deductions and tax offsets assured

PBS 187 Corp plan 5, 22

See Commissioner

of Taxation annual report

2017–18 (page 82)

See page 52

for detailed information

See note(b)

G2: We design for a better tax and superannuation system to make it easy to comply and hard not to

Influence – Government and Treasury perceptions of the ATO and the quality of our advice

PBS 187 Corp plan 6, 23

Satisfactory Good See note(c)

C1: Our client experience and interactions are well designed, tailored, fair and transparent

Compliance cost – adjusted median cost to individual taxpayers of managing their tax affairs

PBS 187 Corp plan 7, 23

1.0% reduction (2015–16

returns)

Unchanged(d) (2016–17

returns)

Unchanged(e) (2017–18

returns)

Remain steady

02Annual performance statementProgram 1.1 Australian Taxation Office

27

TABLE 2.1 Performance results, 2016–17 to 2018–19 continued

Results Target

Performance criterion Source 2016–17 2017–18 2018–19 2018–19

Digital – proportion of inbound transactions received digitally for key services

PBS 187 Corp plan 7, 23

88% 88% 89% 90%

� income tax returns 96% 97% 97% –

� activity statements 78% 82% 85% –

� tax file number (TFN) registration

94% 96% 97% –

� payment arrangements – 25% 28% –

� ABN registrations – 100% 100% –

� role registrations – 73% 75% –

� ABN cancellations – – 67% –

� DASP applications – – 100% –

� role cancellations – – 81% –

� TPAR lodgment – – 36% –

C2: We work with and through others to deliver efficient and effective tax and superannuation systems

Working together – partner perceptions of how the ATO is working together with them to administer the tax and superannuation system(f)

PBS 187 Corp plan 8, 23

– 64/100 See note(g)

W1: We are a high-performing, responsive and professional workforce with the right culture to deliver now and for the future

Culture – Level of employee engagement

PBS 188 Corp plan 9, 23

6.8/10 6.9/10 6.9/10 Equal or better than the average result for

large agencies

Gender equality – Female representation in the following classification levels

PBS 188 Corp plan 9, 23

� senior executive service (SES)

44.2% female55.8% male

44.9% female55.1% male

Approx. 45% of SES

� executive level (EL) 48.6% female51.4% male

49.1% female50.9% male

Approx. 50% of EL staff

Indigenous representation – Proportion of ATO staff who identify as Indigenous

PBS 188 Corp plan 9, 23

2% 2.1% 2.5% 2.5%

W2: We provide the right tools and workplace so staff can deliver the best client experience

Staff experience – employee perceptions around whether they have access to the tools and resources needed to perform well

PBS – Corp plan 10, 23

63% See note(h)

O1: We use data and insights to deliver value for our clients and inform decision making across everything we do

Tax returns – Proportion of items that are pre-filled

PBS 188 Corp plan 11, 23

87.5% 87.9% See note(i)

02 Commissioner of Taxation annual report 2018–19

28

TABLE 2.1 Performance results, 2016–17 to 2018–19 continued

Results Target

Performance criterion Source 2016–17 2017–18 2018–19 2018–19

O2: Our technology and digital services deliver a reliable and contemporary client experience

Security policy – Level of compliance with Protective Security Policy Framework mandatory requirements

PBS 188 Corp plan 12, 23

Compliant Report requirements

met

See note(j)

Availability – key digital systems availability

PBS 188 Corp plan 12, 23

99.4% 99.5% See note(k)

F1: We strive for operational excellence to achieve efficiency and quality outcomes

Budget – ATO manages its operating budget to balance

PBS 188 Corp plan 13, 23

0.13% surplus

1.0% deficit

0.1%

deficit

+/– 0.6% of budget

allocation

Cost of collection – Cost to collect $100(l)

PBS 189 Corp plan 13, 23

$0.81(incl GST)

$0.74 (excl GST)

$0.74 (incl GST)

$0.67 (excl GST)

$0.71 (incl GST)

$0.64 (excl GST)

Consistent with trend

Target achieved Target substantially achieved Target not achieved Result not available

NOTES(a) The target was under development in 2018–19. The target for 2019–20 is 65/100.(b) The target was under development in 2018–19. The target for 2019–20 is ‘increase the proportion of the tax base where the

ATO has justified trust to a level as high as practicable given the nature and complexity of the law and resources available’.(c) The target was under development in 2018–19. The target for 2019–20 is a ‘good’ rating.(d) The unchanged result for 2017–18 reflects a less than 0.1% change in the adjusted median.(e) The unchanged result for 2018–19 reflects a 0.2% increase in the adjusted median.(f) The methodology was refined in 2018–19 and results are not comparable to the result for ‘Empowerment – partner perceptions

of how the ATO empowers and includes them’ published in the 2017–18 annual report.(g) The target was under development in 2018–19. The target for 2019–20 is ‘equal to or better than the 2018–19 result’.(h) The target was under development in 2018–19. The target for 2019–20 is ‘equal to or better than the average result for

large agencies’.(i) The target was under development in 2018–19. The target for 2019–20 is 85%.(j) The target was under development in 2018–19. This measure has been retired for 2019–20.(k) The target was under development in 2018–19. The target for 2019–20 is 99.5% (excluding planned outages).(l) The description of the measure changed this year to ‘inclusive of GST’ and ‘exclusive of GST’.

Results analysis

Confidence – community confidence in the ATO

For 2018–19, the overall result for community confidence in the ATO was 65/100. As this measure was previously under development, there is no performance target against which to assess this result this year.

The methodology for this measure comprises survey questions to measure confidence in the ATO across two different audiences – clients who’ve had a recent interaction with the ATO, and the general community – and allow comparisons between these groups. In 2018–19, general community confidence in the ATO was slightly higher at 65/100, with recent clients’ confidence at 64/100.