annual report 2015 - bpi + philam report bpi-philam.com 2015 table of contents company profile 3...

TRANSCRIPT

1

ANNUALREPORT

bpi-philam.com

2015

TABLE OF CONTENTS

Company Profile 3

Message from the CEO 4

Financial Statements 5

Business Highlights 11

Corporate Governance 14

Operating Philosophy 24

3

BPI-Philam Life Assurance Corporation is a strategic alliance between two leading financial companies in the Philippines – The Philippine American Life and General Insurance Company (Philam Life) and Bank of the Philippine Islands (BPI).

Philam Life is a premier life insurance company in the Philippines and a market leader for over 60 years.

Bank of the Philippine Islands is a leading commercial bank in the country with over 160 years of experience in the local banking industry and an extensive branch network of more than 800 branches and 1,500 ATMs.

A Member of the AIA GroupBPI-Philam is the bancassurance arm of AIA in the Philippines. AIA is the second largest life insurance company in the world that operates in 18 markets in Asia Pacific.

3

Company Profile

The first bank in the Philippines and Southeast Asia comes to life with the establishment of El Banco Español Filipino De Isabel II, under the auspices of the Governor and Captain-General of the Philippines, Antonio De Urbiztondo Y Eguia.

AIA puts down its corporate roots in Asia when the group founder Mr. Cornelius Vander Starr establishes an insurance agency in Shanghai.

BPI and Philam Life forges a joint venture to form BPI-Philam, the bancassurance arm of AIA in the Philippines.

In just 5 years, BPI-Philam already ranks as one of the Top 5 Life Insurers in the Philippines in total premium income.

C.V. Starr and Earl Caroll establishes Philam Life with a firm resolve to help Filipinos recover from the ravages of World War II. Earl’s vision: “A Philam Life policy in every Filipino home.”

With the Philippines then under U.S. colonial rule, a general meeting of the bank’s shareholders approves to adopt the name “Bank of the Philippine Islands,” marking a new era of renewed vigor and activity for the bank.

AIA Group Limited succesfully listed on the main board of the stock exchange of Hong Kong Limited, the third largest IPO ever globally at that time.

1851

1907

1947

2010

1919

2009

2014

OUR HERITAGE

OUR VISION

OUR MISSION

To be the undisputed benchmark in the bancassurance industry.

We empower Filipinos achieve financial security and prosperity.

4

To our valued stakeholders, We thank you for your continuing trust and confidence.

We are very pleased and proud of our 2015 results. We started the year on a strong note, led the industry in terms of total premium growth during the first half and then finally ended the year with a 44% increase in total premium versus 2014, which is more than double the growth of the life insurance industry. After just six years in operations, BPI- Philam is now ranked number 4 in total premium among all life insurance companies in the industry. We are now also the biggest bancassurance operations in the country.

The growth can be attributed to the strong partnership between BPI-Philam and our bank partner, BPI, and to the strong support of our parent company, Philam Life. Our strategy is fully aligned with our bank partner where customer centricity is the primary branch focus.

We increased our sales force, and made it easier for BPI customers to avail of BPI-Philam products in over 800 BPI branches nationwide. We introduced a number of initiatives to ensure we work closely and team up with the branch staff in providing the appropriate services to the customers. The company also launched three unit-linked products to meet the financial needs for protection, savings and health that boosted the company’s sales and expanded its product portfolio.

Our combined efforts empowered us to provide the much needed financial protection to more Filipinos, fully aligned with our company mission and supportive of the customer centricity strategy of our bank partner.

This 2016, we will continue our multi-segment, multi-distribution strategy to maximize penetration among valued customers of BPI. Initiatives to meet the company’s revenue goals and sustainable growth objectives are in place.

With a firm vision and strategy, we are set to make a positive difference in the lives of Filipinos.

Ariel G. CantosChief Executive OfficerBPI-Philam

4

Message from the CEO

5

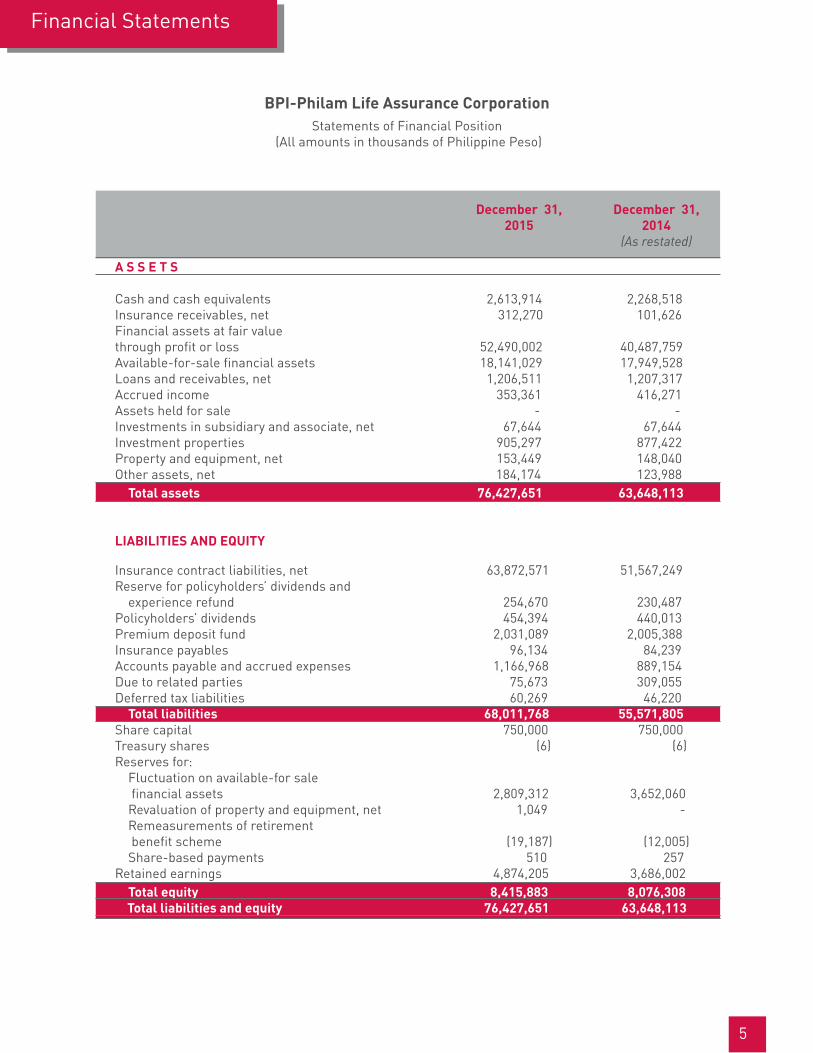

A S S E T S Cash and cash equivalents 2,613,914 2,268,518Insurance receivables, net 312,270 101,626 Financial assets at fair valuethrough profit or loss 52,490,002 40,487,759Available-for-sale financial assets 18,141,029 17,949,528Loans and receivables, net 1,206,511 1,207,317Accrued income 353,361 416,271Assets held for sale - -Investments in subsidiary and associate, net 67,644 67,644Investment properties 905,297 877,422Property and equipment, net 153,449 148,040Other assets, net 184,174 123,988 Total assets 76,427,651 63,648,113

LIABILITIES AND EQUITY Insurance contract liabilities, net 63,872,571 51,567,249Reserve for policyholders’ dividends and experience refund 254,670 230,487Policyholders’ dividends 454,394 440,013Premium deposit fund 2,031,089 2,005,388Insurance payables 96,134 84,239Accounts payable and accrued expenses 1,166,968 889,154Due to related parties 75,673 309,055Deferred tax liabilities 60,269 46,220 Total liabilities 68,011,768 55,571,805Share capital 750,000 750,000Treasury shares (6) (6)Reserves for: Fluctuation on available-for sale financial assets 2,809,312 3,652,060 Revaluation of property and equipment, net 1,049 - Remeasurements of retirement benefit scheme (19,187) (12,005) Share-based payments 510 257 Retained earnings 4,874,205 3,686,002 Total equity 8,415,883 8,076,308 Total liabilities and equity 76,427,651 63,648,113

BPI-Philam Life Assurance CorporationStatements of Financial Position

(All amounts in thousands of Philippine Peso)

Financial Statements

December 31, 2014

(As restated)

December 31, 2015

6

BPI-Philam Life Assurance CorporationStatements of Total Comprehensive Income

For the years ended December 31, 2015 and 2014 (All amounts in thousands of Philippine Peso)

REVENUES AND OTHER INCOME Gross premiums on insurance contracts 20,920,750 14,563,956 Reinsurers’ share of gross premiums on insurance contracts (121,846) (80,782) Net insurance premiums 20,798,904 14,483,174 Fee income 1,378,822 973,420 Investment income 1,097,576 1,097,193 Realized gain on sale of available-for-sale financial assets, net 252,210 100,462 Foreign exchange gains, net 17,437 3,644 Reversal of impairment losses - 101 Fair value (losses) gains, net (1,430,823) 1,965,989 Others 13,999 12,602 Total revenues and other income 22,128,125 18,636,585EXPENSES Change in insurance contract liabilities, net 12,269,746 10,425,869 Benefits and claims paid on insurance contracts, net 4,946,665 4,875,571 Commissions and other acquisition expenses 1,972,908 1,448,961 General and administrative expenses 1,110,500 740,768 Increase in reserve for policy dividends and experience refunds 22,487 19,366 Investment expenses 92,239 56,522 Interest expense 215,265 163,358 Insurance taxes, licenses and fees 116,538 103,252 Total expenses 20,746,348 17,833,667INCOME BEFORE INCOME TAX 1,381,777 802,918INCOME TAX EXPENSE 193,574 181,481NET INCOME FOR THE YEAR 1,188,203 621,437OTHER COMPREHENSIVE (LOSS) INCOME Item that will be subsequently reclassified to profit or loss Net fair value changes on available-for-sale financial assets (842,748) 545,560 Items that will not be subsequently reclassified to profit or loss - Net fair value gains on property and equipment 1,049 - Remeasurement losses on retirement benefit scheme (7,182) (412) Total other comprehensive (loss) income (848,881) 545,148 TOTAL COMPREHENSIVE INCOME FOR THE YEAR 339,322 1,166,585

2015 2014(As restated)

7

BPI-Philam Life Assurance CorporationStatements of Changes in Equity

For the years ended December 31, 2015 and 2014 (All amounts in thousands of Philippine Peso)

Total

BALANCES AT JANUARY 1, 2014As previously reported 750,000 (6) 3,106,500 - (11,593) 92 2,994,718 6,839,711 Effect of restatement - - - - - - 69,847 69,847 As restated 750,000 (6) 3,106,500 - (11,593) 92 3,064,565 6,909,558

COMPREHENSIVE INCOME FOR THE YEARNet income for the year

As previously reported - - - - - - 583,438 583,438Effect of restatement - - - - - - 37,999 37,999As restated - - - - - - 621,437 621,437

Other comprehensive income - - 545,560 - (412 ) - - 545,148Total comprehensive income for the year - - 545,560 - (412 ) - 621,437 1,166,585

TRANSACTION WITH OWNERSCost of share-based payments - - - - - 165 - 165

BALANCES AT DECEMBER 31, 2014 750,000 (6) 3,652,060 (12,005) 257 3,686,002 8,076,308COMPREHENSIVE INCOME FOR THE YEAR

Net income for the year - - - - - - 1,188,203 1,188,203Other comprehensive loss - - (842,748) 1,049 (7,182) - - (848,881)

Total comprehensive income for the year - - (842,748) 1,049 (7,182) - 1,188,203 339,322TRANSACTION WITH OWNERS

Cost of share-based payments - - - - - 253 - 258,

Share capitalTreasury

shares

Reserve forfluctuation on

available-for-salefinancial assets

Reserve forrevaluation

property andequipment, net

Reserve forremeasurements

of retirementbenefit scheme

Reserve forshare-based

payments Retainedearnings

BALANCES AT DECEMBER 31, 2015 750,000 (6) 2,809,312 1,049 (19,187) 510 4,874,205 8,415,883

Related party transactions

In the normal course of conducting its business, the Company transacts with the following related parties:

Summary of transactions with related parties

The significant related party balances and transactions as at and for the years ended December 31 are summarized as follows:

(a) Outsourcing services and other transactions

The Company has entered into a service agreement with the Parent Company, BPI, PICCSI and PPC for various support services, effective January 1, 2010. For the outsourcing services rendered, the above parties allocate expenses based on percentage of time spent in the following areas: finance, operations, marketing, corporate services, corporate compliance, information technology, actuarial, underwriting, legal, internal audit, risk management, process management, property management, distribution services, corporate secretary and other related functions.

The summary of transactions and balances arising from the Company’s outsourcing agreements is as follows:

Related party RelationshipAIAGL Ultimate Parent CompanyAIA Intermediate Parent CompanyPhilam Life Parent CompanyBPI Significant investorAHCI SubsidiaryPhilam Asset Management Inc. (“PAMI”) Fellow subsidiaries under common control of Philam LifePhilam Properties Corp. (“PPC”) Philam Call Center Services, Inc. (“PCCSI”) BPI-AMTG Separate unit of BPIAyala Plans (“AP”) Subsidiaries of BPIBPI M/S Insurance Corporation (“BPI M/S”)

2015

Philam Life 539,139 (46,354) 282,962 (332,788)BPI 8,529 (916) 10,939 (1,843)PICCSI 65,016 (26,241) 29,956 (21,377)PPC 228 (225) 525 (1,216) 612,912 (73,736) 324,382 (357,224)

Amount of transaction for the year

Outstanding payable balance at December 31

Amount oftransactionfor the year

Outstanding payable balance at December 31

2014

8

Other transactions with related parties for the years ended December 31 are summarized below:

(b) Lease transactions (Company as lessor)

The balances presented are unguaranteed and unsecured, non-interest bearing and collectible/payable on demand. The amounts will be settled in cash.

Security deposit received from related parties from the above lease transactions amounts to P5,845(2014 - P4,138) and is under Account payable and accrued expenses.

Reconciliation of outstanding related party balances at December 31

The outstanding balances presented are unguaranteed and unsecured, non-interest bearing and collectible/payable on demand. The amounts will be settled in cash. There are no guarantees provided or collaterals held arising from transactions with related parties. No provision for impairment has been made for amounts owed by related parties since collection is deemed to be reasonably certain.

Allocated group expenses and charges for use of systems AIA (150,844) (8,850) (88,142) (41,246) Philamlife (779) (258) (573) (46)Expense recoveries PAMI 25,492 28,615 - - PPC 570 - - - AP - - - 8 AHCI - 750 - 750 BPI MS - 139 - -Provision for legal obligations of AHCI - (69,961) - (69,961)

2015

2015

Amount of transaction for the year

Amount of transaction for the year

Outstanding receivable

(payable) balance at December 31

Outstanding receivable balance

at December 31

Amount oftransactionfor the year

Amount oftransactionfor the year

Outstanding receivable (payable)

balance at December 31

Outstanding receivable balance

at December 31

2014

2014

BPI M/S 19,953 1,920 15,181 139 BPI 2,409 384 3,389 -PAMI 1,233 - - 573 Philam Life 500 - 100 - 24,095 2,304 18,670 712

9

10

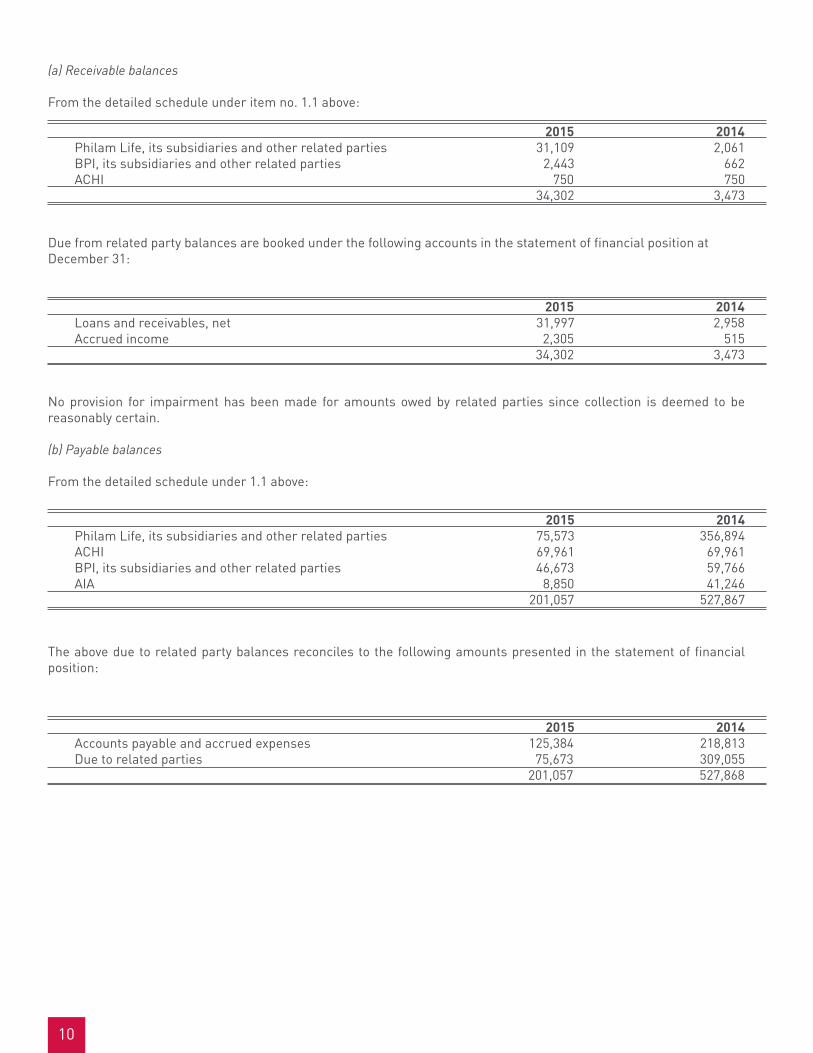

(a) Receivable balances

From the detailed schedule under item no. 1.1 above:

No provision for impairment has been made for amounts owed by related parties since collection is deemed to be reasonably certain.

(b) Payable balances

From the detailed schedule under 1.1 above:

The above due to related party balances reconciles to the following amounts presented in the statement of financial position:

Due from related party balances are booked under the following accounts in the statement of financial position at December 31:

2015 2014Loans and receivables, net 31,997 2,958Accrued income 2,305 515 34,302 3,473

2015 2014Philam Life, its subsidiaries and other related parties 75,573 356,894ACHI 69,961 69,961BPI, its subsidiaries and other related parties 46,673 59,766AIA 8,850 41,246 201,057 527,867

2015 2014Accounts payable and accrued expenses 125,384 218,813Due to related parties 75,673 309,055 201,057 527,868

2015 2014Philam Life, its subsidiaries and other related parties 31,109 2,061 BPI, its subsidiaries and other related parties 2,443 662 ACHI 750 750 34,302 3,473

Business Highlights

Multi-Distribution ChannelThe main distribution channel of BPI-Philam continues to be In-Branch Sales with over 700 Bancassurance Sales Executives (BSEs) deployed nationwide in 2015. Year-on-year, productivity of the BSEs has been improving driven by the strengthened recruitment program, improved activity management, and regular training programs. BSEs are well-equipped with the right training prior to their deployment as they attend a 15-day Business Training Program (BTP) that encompasses everything they need to learn to succeed from sales techniques to business conduct guidelines.

The improved productivity of BSEs mirrors the improved productivity of branch referrers given the tight coordination within the segments and an institutionalized lead referral process that clearly defined the roles of the different stakeholders.

Corporate Solutions (CS) maintained its thrust of providing benefits for employer and non-employer groups as it launched two group products in 2015: Corporate Essentials and Health Essentials. Both products are customizable depending on the needs of the group and offers a wide array of benefits.

New channels Direct Marketing and Institutional Distribution started their groundwork in 2015 and are set to provide new avenues for sales in the coming years.

Reinforced PartnershipBPI-Philam restructured the organization to mirror BPI’s client segmentation in order to provide services and offerings that are fit for the market segment. Through the three key segments: Personal, Preferred, and Private Banking and niche segment: Overseas Filipinos, BPI-Philam is able to develop programs and products that meet the specific needs of the clients.

Customer-Centricity With the company continuously finding ways to make financial planning easy for the customers, BPI-Philam launched various initiatives throughout the year to make transactions faster, simpler, and easier.

All BSEs are equipped with an iPad where they use iPos for their daily sales presentations and transactions. Close to 100% of life insurance applications are done through iPos making policy issuance faster.

New policyholders also receive a Welcome Call to ensure that they are fully aware of their policy details and services that are offered by the company. While existing policyholders also receive regular correspondence through BPI-Philam and You, the company’s customer newsletter. These initiatives show that BPI-Philam is with the customer’s every step to financial security and prosperity.

One of the Top Producers awarded during the 2015 Annual Awards by AIA BPI and BPI-Philam Executives

Sales Rally held in Cebu

BPI, AIA, and BPI-Philam Executives at the Annual Awards

11

Expansion of Product PortfolioBPI-Philam continues to complete its product portfolio and provide customers with products with high customer-value. BPI-Philam launched three unit-linked products throughout the year. These products address the needs of savings, health, and investment.

BUILD LIFE PLUS Bringing dreams to life is now made easier with Build Life Plus. Build Life Plus is a regular-pay unit-linked life insurance plan positioned for savings that may be used for a child’s education, living a worry-free retirement, or simply living debt-free. Whether a customer is new to the saving game or with years of experience, Build Life Plus can work for him/her.

CRITICAL CARE PLUSCritical Care Plus is the first unit-linked health and life insurance plan of the company. This product provides in case of critical illness. With this product, BPI-Philam has made its mark in the health category for life insurance.

INVEST PESO MAXAn enhancement of the former single-pay unit-linked life insurance plan of the company, Invest Peso Plus, Invest Peso Max has lower charges in order to provide potentially higher returns. Premium charge for investments of at least Php10 million is 0% while for investments of at least Php1 million is 1%.

Our PeopleBPI-Philam’s young and dynamic workforce is engaged towards building a culture grounded by the company’s operating principle of doing the right thing in the right way with the right people.

Employee engagement is a key focus of the company. Hence various initiatives are in place to ensure that employees are actively engaged. The company holds a monthly gathering for employees to announce new projects, recognize individual and team performances, and foster camaraderie among employees. Further, the company celebrates employee birthdays and promotes healthy living through after-office physical fitness activities and participation in inter-company sports competitions.

BPI-Philam celebrates halloween with employees and their kids

Birthday surprises for employees by BPI-Philam HR

12

The 2015 Christmas Outreach Program of BPI-Philam at Sacred Heart Parish, Makati

Corporate Social ResponsibilityBPI-Philam contributes positively to the social and economic development of the communities in which it operates with support extended to people and communities in need. Thus, BPI-Philam and its employees volunteer time and funds to programs that promote health, financial literacy, education, and other community needs. BPI-Philam is committed to reducing the impact of its operations on the environment and raising awareness about sustainability by taking part in activities that highlight these issues.

Philam Foundation is the corporate social responsibility arm of the Philam Group. BPI-Philam supports initiatives of the Philam Foundation with the core project: Philam Paaralan. Further to the initiatives of Philam Foundation, BPI-Philam also conducts its own outreach programs.

BPI-Philam ensures that the company funds or assets are not used to promote personal causes and that no one makes personal donations in the company’s name without prior authorization.

13

14

Corporate Governance

BPI-Philam confirms its full compliance with the Code of Corporate Governance, and its commitment to the highest standards of corporate governance is rooted in the belief that culture of integrity and transparency is essential to the consistent achievement of its common goals. Creating a sustainable culture, where trust and accountability are vital as skill and wisdom, steers us towards achieving long-term value for shareholders and clients, and strengthens our confidence in the institution.

The implementation of corporate governance principles is a priority of BPI-Philam. Accordingly, the Board ensures compliance with IC Circular Letter No. 31-2005. Likewise, the corporation submitted its Manual of Corporate Governance in compliance with IC Circular Letter No. 21-2009. BPI-Philam aims to adhere to best practices on Corporate Governance.

Role and Responsibilities of the BoardThe property, affairs, and business of the Corporation are managed by the Board of Directors. The Board is accountable to the shareholders and as such shall ensure the highest standard of governance in running the corporation. The Board is completely independent from management and its stockholders. The detailed role and responsibilities of the Board are set forth in the Bylaws and Manual of Corporate Governance.

Board IndependenceThe corporation has two (2) independent directors who meet all the requirements set in the Manual of Corporate Governance. None of the independent director has any business or significant financial interest in the company or any of its subsidiaries and therefore considered to be independent.

Board ProcessThe Board meetings are held quarterly (scheduled at the beginning of the year) but special meetings are called from time to time to discuss urgent matters. The Board materials are sent to the members at least five (5) working days before the meeting. Minutes of the Board and committee meetings are prepared and kept by the Corporate Secretary. The minutes are open for inspection upon request on business hours.

Election of DirectorsThe corporation uses a transparent procedure for the election of directors which is provided in the Bylaws and the Manual of Corporate Governance. The Nomination Committee looks into the qualifications of directors and thereafter presents to the Board for consideration.

Orientation Program and TrainingThe Corporate Secretary provides the orientation for new directors to explain the organizational profile, charters, and bylaws of the corporation. A corporate governance seminar is arranged to ensure adherence to best practices.

Performance EvaluationThe corporation has patterned its performance evaluation to Philam Life, the criteria of which are based on the Insurance Commission circular on corporate governance. Every April of each year, the Board conducts a self-assessment of the Board and its Committees as well as the Chairman & President.

Dividend PolicySection 201 of the amended Code provides that no domestic insurance corporation shall declare or distribute any dividend on its outstanding stocks unless it has met the minimum paid-up capital and net worth requirements of the amended Code and except from profits attested in a sworn statement to the Commissioner by the president or treasurer of the corporation to be remaining on hand after retaining unimpaired:

(a) The entire capital stock;(b) The solvency requirements defined by the amended Code;(c) The legal reserve fund; and(d) A sum sufficient to pay all net losses reported, or in the course of settlement, and all liabilities for expenses and taxes.

Regulators are interested in protecting the rights of the policyholders and maintaining close vigil to ensure that the Company is satisfactorily managing affairs for their benefit. At the same time, the regulators are also interested in ensuring that the Company maintains an appropriate solvency position to meet liabilities arising from claims and that the risk levels are at acceptable levels.

No changes were made to the Company’s capital base, objectives, policies and processes from the previous year.

15

CAPITAL STRUCTURE

LIST OF STOCKHOLDERSNAME OF STOCKHOLDER SHARES

HELDCLASS AMOUNT PAID

(PHP)% OF

OWNERSHIPNATIONALITY BENEFICIARY

OWNERSHIPDATE OF FIRST APPOINTMENT

THE PHILIPPINE AMERICAN LIFE AND GENERAL INSURANCE COMPANY (Philam Life)

Darren ThomsonNon-Executive Director Vice-Chairman

Ariel G. CantosExecutive Director Chief Executive Officer

J. Axel BromleyNon-Executive Director

Surendra Menon Non-Executive Director

Jesus P. Tambunting Independent Director

Terrence CummingsNon-Executive Director

Simon R. PaternoNon-Executive Director

Romeo L. Bernardo Independent Director

Natividad N. Alejo Non-Executive Director

Cezar P. ConsingNon-Executive Director

OTHERS (Minority Stockholders)

TOTAL

Aurelio Luis R. Montinola III Non-Executive Director Chairman

BANK OF THEPHILIPPINE ISLANDS (BPI)

382,496,924

357,554,232

9,942,317

749,993,979

1

1

1

1

1

1

100

100

100

100

100

100.00

100.00

100.00

100.00

100.00

382,496,924.00

382,496,924.00

749,993,979.00

9,942,317.00

51.00%

47.67%

100.00%

1.33%

Hong Kong SARCommon

Common

Common

Common

Common

Common

Common

Common

Common

Common

Common

Common

Common

Common

1.00

1.00

1.00

1.00

1.00

1.00

British

Filipino

Filipino

Filipino

Filipino

Filipino

Filipino

Filipino

Filipino

Filipino

American

American

Singaporean

Philam Life

Philam Life

Philam Life

Philam Life

Philam Life

Philam Life

BPI

BPI

BPI

BPI

BPI

08 July 2014

01 July 2013

23 June 2015

22 January 2016

27 November 2009

18 July 2013

25 April 2000

15 April 2015

24 April 2006

10 April 2007

03 April 2014

Authorized Capital Stock - P1BillionSubscribed & Paid-Up Capital Stock - P749,993,979.00

Par Value - P1.00 per shareTreasury Share - P6,000.00

The Board had six (6) meetings in 2015 and the directors received the materials at least five (5) working days in advance. The presence of at least six (6) directors with at least one (1) director from BPI and Philam Life present is necessary to have a quorum.

BOARD MEETINGS Member

Board

6 Meetings93.94%

4 Meetings91.67%

AuditCommittee

3 Meetings100%

Nomination & Governance Committee

1 Meeting100%

Compensation Committee

Aurelio Luis R. Montinola IIIJose L. Cuisia, Jr.*Ariel G. CantosJ. Axel Bromley**Jesus P. TambuntingRomeo L. BernadoNatividad N. AlejoCezar P. ConsingDarren ThomsonTerrence CummingsSimon R. Paterno

6 Meetings3 Meetings6 Meetings3 Meetings6 Meetings6 Meetings6 Meetings6 Meetings6 Meetings6 Meetings5 Meetings

N/AN/AN/A2 Meetings4 Meetings4 MeetingsN/AN/AN/AN/AN/A

3 Meetings3 MeetingsN/AN/A3 MeetingsN/AN/AN/AN/AN/AN/A

N/A1 Meeting1 MeetingN/AN/AN/AN/A1 MeetingN/AN/AN/A

*until 22 January 2016**effective 23 June 2015

No. of Meetings Held & Attended for the Year 2015

AUDIT COMMITTEE The Audit Committee is an independent committee formed by the Board of Directors to assist the Board in the performance of its duties and responsibilities specifically in ensuring that governance, internal controls and risk management systems of the organization are in place.

The Audit Committee is composed of three (3) members of the Board, two (2) of which, namely Mr. Romeo L. Bernardo as the chairman and Amb. Jesus P. Tambunting, are independent directors. Each Audit Committe member met the necessary requirements of the Securities and Exchange Commission, the Revised Code of Corporate Governance and other applicable laws and regulations in the Philippines. See page 22 for the list of the Audit Committee members and page 18-19 for their profiles.

The Audit Commitee has adopted a formal term of reference or the Audit Committee Charter in fulfilling its responsibility for oversight of the organization’s corporate governance process. The Committee, while doing its oversight role, relies on the expertise of Management and works with Internal Auditors and External Auditors to ensure the integrity of the financial statements and continuous review of the organization’s governance process, risk management and internal controls.

The Audit Committee used the responsibilities outlined in the Audit Committee Charter to develop an annual calendar and meeting agenda for 2015. From January 1 to December 31, 2015, the Audit Committee met four (4) times. On these meetings, the Audit Committee met with Senior Management, Group Internal Audit, Compliance Office and organization’s External Auditors, Isla Lipana & Co./PricewaterhouseCoopers. Among the agenda/topics discussed include the Approval of Audit Plans, Group Internal Audit Updates, Result of Compliance Reviews and Updates from External Auditors. Group Internal Audit Updates usually include the result of completed audit projects and status of audit plan.

Group Internal AuditGroup Internal Audit (GIA) is responsible for reviewing the organization’s ability to manage and control risks and provides an independent assessment as to the adequacy and effectiveness of internal controls across the organization based of the approved Internal Audit Plan. GIA adopts a risk-based audit plan which considers the significant risks affecting the strategies and key objectives of the company. These risks include financial, operational, compliance and industry’s emerging risks, among others. In finalizing the audit plan, inputs and expectations from management and the Board are likewise considered.

Part of GIA is a dedicated internal auditor for BPI-Philam, who is assisted and supported by Philam Life GIA and AIA GIA. GIA, which is directly supervised and supported by AIA Group Internal Audit, functionally reports to the Audit Committee and administratively reports to the Chief Executive Officer. The Head of GIA, on behalf of the Group

Internal Audit function, is responsible for reporting the result of internal audit work to the Audit Committee on a regular basis. In overseeing the internal audit function, the Audit Committee is actively involved in approving the internal audit plan including any changes thereof, assessing the result of audit projects and monitoring the resolution of key issues noted. The Audit Committee has overseen the process by which assessment of the effectiveness of internal controls, risk management, financial reporting and information technology security were conducted.

Engagement with External AuditorsThe Audit Commitee, on behalf of the Board of Directors, is responsible for the appointment, re-appointment or removal of External Auditors. For the year 2015, the Audit Committee has approved the re-appointment of Isla Lipana & Co./PricewaterhouseCoopers as the External Auditor. The Audit Committee has reviewed and approved accordingly the scope and coverage of Statutory Audit for the year 2015. Although management has the primary responsibility for the financial statements and the reporting process, the Audit Committe having the oversight role, has noted and reviewed the audited financial statements for the calendar year 2015. The Audit Committee concurred and accepted the conclusion of the External Auditors on the financial statements and is satisfied that the financial statements are in compliance with Philippine Financial Reporting Standards as assessed by the External Auditors.

16

AURELIO LUIS R. MONTINOLA III (64 years old)Non-Executive Director Chairman of the Board

Aurelio R. Montinola III, Filipino, is a Director of Bank of the Philippine Islands (BPI). His other affiliations, among others include, Chairman, Far Eastern University; Chairman, WWF International; Vice Chairman, Philippine Business for Education; Director, BPI/MS Insurance Corporation; Trustee, Makati Business Club; and Member, Management Association of the Philippines.

He graduated with BS Management Engineering at Ateneo de Manila University in 1973. He received his MBA at Harvard Business School in 1977.

His past affiliations include being President of Bank of the Philippine Islands for 8 years, President of the Bankers Association of the Philippines for 4 years, President of the Alliance Francaise de Manille for 7 years, and Trustee of the International School of Manila for 4 years.

DARREN THOMSON (53 years old)Non-Executive DirectorVice-Chairman

Darren is currently the Director of Partner Development and prior to this new role, he was the Regional CEO for Partnership Distribution in the AIA Group office since January 2014. In that role, Darren was responsible for the Group Partnership Distribution function as a strategic business unit, providing best-in-class capabilities required to become the preferred partner in Asia for leading banks, IFA’s, HNW and affinity groups.

As Regional CEO, he leads and works with the local CEOs in building out their partner distribution strategy along with a regional team to provide a clear value proposition and execution roadmap to deliver a consistently high quality value add service to AIA’s partners and customers across all of Asia-Pacific. He is also responsible for leading the team to unlock and develop new opportunities in bancassurance, direct marketing, high net worth, IFA/Brokers and institutional businesses.

Prior to joining the Group, Mr. Thomson was Regional Head, Strategic Channel Development – President and CEO – Manulife Singapore, Chairman – Manulife Asset Management Singapore. He has also worked for Prudential plc in Asia and in the UK.

ARIEL G. CANTOS (56 years old)Executive DirectorChief Executive Officer

Ariel G. Cantos, is the President and Chief Executive Officer of BPI-Philam Life Assurance Corporation. Mr. Cantos is a member of the board of directors of Philam Life and BPI-Philam Life Assurance Corporation, a director of the Philippine Life Insurance Association, and sits as a Trustee in Philam Foundation, Ayala FGU Alabang and Ayala FGU Makati Condo Corporation.

Before his current appointment, Mr. Cantos was Senior Vice President and Chief Agency Officer of Philam Life. He has had an enriching and successful career in Philam Life’s Agency Distribution Channel, which he served for close to 30 years. He held various positions within the channel such as: Profit Center Head of Accident & Health Products; Director of Manila Agencies; and Director of Provincial Agencies.

He graduated with a Bachelor’s Degree in Economics, Honors Program, at the Ateneo De Manila University, Loyola Heights, Quezon City.

BOARD OF DIRECTORS

17

J. AXEL BROMLEY (47 years old)Non-Executive Director

Mr. Axel Bromley is the Chief Executive Officer of The Philippine American Life and General Insurance Company (Philam Life). He holds various positions within the Philam Group Boards such as: Chairman of Philam Foundation; Chairman of Philam Asset Management; Inc.; Chairman of Philam Equitable Life Assurance Company; and Director of BPI-Philam Life Assurance Corporation.

Prior to his appointment as CEO of Philam Life, Mr. Bromley served as Director of Strategic Initiatives at AIA Group Limited, Philam Life’s parent company. Before joining AIA, Mr. Bromley was the General Manager of MetLife Ukraine from 2012 to 2014. He started his career in the insurance industry as a Management Associate for AIG ALICO in 2002 and worked his way up as a Broker Relations Manager, Profit Center Manager of Accident and Health Products then Regional Agency Executive in ALICO Dubai, General Manager of MetLife ALICO in Nepal, and Country Manager of MetLife Qatar.

Mr. Bromley earned his Bachelor’s degree in International Relations with a Near Eastern Studies emphasis at Brigham Young University in Utah, USA in 1995. He received a dual masters degree in International Management and Masters of Business Administration (with honors) at Thunderbird School of Global Management and Arizona State University, respectively, in 2002. Mr. Bromley is fluent in Arabic, Spanish, and Vietnamese.

CEZAR P. CONSING (56 years old)Non-Executive Director

Cezar “Bong” Consing is President and CEO of Bank of the Philippine Islands (“BPI”).

From 2004 to 2013, Mr. Consing was a Partner with The Rohatyn Group, a New York headquartered investment management company that manages about $5.5 billion in investments in the global emerging markets. He was responsible for the firm’s private equity business in Asia, managing its Hong Kong based operations, and was a member of the board of partners of the firm’s management company.

Mr. Consing was an investment banker with J.P. Morgan & Co. from 1985 to 2004, where he was based in Hong Kong and Singapore. From 1999 to 2004, he was President of J.P. Morgan Securities (Asia Pacific) and, as a senior Managing Director, co-headed or headed the firm’s investment banking group in the Asia Pacific region. As an investment banker, Mr. Consing was directly involved in some of the most significant corporate transactions in Asia, including several mergers, privatizations and debt and equity fund raisings. Mr. Consing worked for BPI in Manila in corporate planning and corporate banking from 1980 to 1985.

Mr. Consing served as an independent director of the boards of CIMB Group Holdings Berhad and CIMB Group Sdn. Berhad from 2004 - 2012 and First Gen Corporation, a major Philippine power generation company, from 2005 - 2013. He has been an independent director of the board of Jollibee Foods Corporation since 2010. He served as a board director of BPl from 1995 - 2000, 2004 - 2007, and most recently since 2010. He received an M.A. in Applied Economics from the University of Michigan, Ann Arbor, in 1980.

18

NATIVIDAD N. ALEJO (57 years old)Non-Executive Director

Natividad N. Alejo, President of BPI Family Savings Bank joined BPI in 1979. She has been Executive Vice President and Group Head of Retail Banking from 2012 to Feb. 28, 2015. She has served as Senior Vice President and Consumer Banking Group Head from 2007 to 2011. She has also served as the President and Director of BPI Capital Corporation and BPI Securities Corporation from 2001 to 2006. She has been a President of the Investment House Association of the Philippines in 2004 to 2006.

Currently, she also holds the following positions: Director of BPI Family Savings Bank, Inc., BPI Direct Savings Bank Inc., BPI Operations Management Corporation, Beacon Property Ventures, Inc., BPI-Philam Life Assurance Corporation, Santiago Land Development Corp., FEB Speed International, Inc., International Finance Ltd. and she’s with An Waray Party List.

She graduated with AB Economics degree (Summa cum Laude and Gansewinkle Scholastic Trophy Awardee) from the Divine Word University, Tacloban City in 1976. She took up MA Economics at University of the Philippines in 1978 and completed the Advanced Management Program at Harvard Business School in Fall of 2005.

ROMEO L. BERNARDO (59 years old)Independent Director

Mr. Bernardo is Managing Director of Lazaro Bernardo Tiu and Associates (LBT), a financial advisory firm based in Manila. He is also a GlobalSource economist in the Philippines. He is Chairman of ALFM Family of Funds and Philippine Stock Index Fund. He is likewise a director of several companies and organizations including Aboitiz Power, BPI, Globe Telecom Inc., RFM Corporation, Philippine Investment Management,

Inc. (PHINMA), Philippine Institute for Development Studies (PIDS), National Reinsurance Corporation of the Philippines and Institute for Development and Econometric Analysis. He previously served as Undersecretary of Finance and as Alternate Executive Director of the Asian Development Bank. He was an Advisor of the World Bank and the IMF (Washington D.C.). Mr. Bernardo holds a degree in Bachelor of Science in Business Economics from the University of the Philippines (magna cum laude) and a Masters Degree in Development Economics at Williams College from Williams College in Williamstown, Massachusetts.

JESUS P. TAMBUNTING (78 years old)Independent Director

Ambassador Jesus P. Tambunting is the Chairman of PDB Properties, Inc. a property development company specializing in medium-cost housing projects in Metro Manila, South Luzon and Central Luzon. He was Chairman of Planters Development Bank (Plantersbank), the country’s leading bank for Small and Medium Enterprises (SMEs), which he founded in 1971. Ambassador Tambunting also served as Chairman of the Board of Small Business Corporation (SBCorp), the agency under the Department of Trade and Industry tasked with promoting the growth of the SME sector.

Ambassador Tambunting is the Co-Chairman of the Philippine-British Business Council, member of the Philippine-US Business Council, and member of the Board of Trustees of the Carlos P. Romulo Foundation, PinoyMe Foundation, ABS-CBN Bayan Foundation, Philippine Business for Education (PBED) and the Makati Medical Center Foundation. He is a member of the Makati Business Club National Issues Committee. From 2004 until May 2008, he served as Chairman of the Association of Development Financing Institutions in Asia and the Pacific (ADFIAP), a regional organization of 127 development banks and institutions in 44 countries. He was elected to the Board of Directors of BPI-Philam Life Assurance Inc. in 2009.

Ambassador Tambunting served as the Philippines’ Ambassador Extraordinary and Plenipotentiary to the United Kingdom of Great Britain and Northern Ireland from 1993 to 1998. At the same time, he concurrently served as Ambassador to the Republic of Ireland and as Permanent Philippine Representative to the International Maritime Organization.

19

Ambassador Tambunting has held key positions in private institutions, including Chairman of Hambrecht and Quist Asia Pacific and Director on the Board of Globe Telecom, Inc. and the Makati Business Club, respectively. The Ambassador also had stints as President of organizations such as the Philippine Ambassadors Foundation Inc., Management Association of the Philippines, Chamber of Thrift Banks, the Development Bankers Association of the Philippines and the Manila Polo Club.

Ambassador Tambunting was conferred Master Entrepreneur and Entrepreneur of the Year 2009 by Ernst & Young and the SGV Foundation, and inducted into the World Entrepreneur Academy in Monaco in June 2010. He also received the International Alumnus Award from the University of Maryland in April 2011, the first Ramon V. del Rosario Sr. Award in Nation Building in 2010, the Distinguished Person of the Year 2009 from the Association of Development Financing Institutions in Asia and the Pacific , the Management Man of the Year 2003 from the Management Association of the Philippines, the Lifetime Achievement Award for 2005 from the Asian Bankers Association, the Distinguished Service Award from the Department of Foreign Affairs and “Knight Commander with Star” from the Equestrian Order of the Holy Sepulchre of Jerusalem in 2008.

The Ambassador earned his Bachelor of Science degree in Economics from the University of Maryland. Prior to that, he had obtained his secondary education from the Culver Military Academy in Indiana and his elementary education from the Ateneo de Manila University.

SURENDRA MENON (57 years old)Non-Executive Director

Surendra Menon is the Regional Director for Bancassurance of the AIA Group. As a catalyst in the Bancassurance industry, he has built and developed various profitable businesses in Asia including Indonesia, Singapore, and the Philippines. Menon joined AIA (formerly AIG) in 2003 and was responsible for acquisition of 10 partnerships in Indonesia including BCA, CIMB, and ANZ. He is currently the subject matter expert for the AIA group in bancassurance and supports the management of BPI-Philam to transform the business into one of the leading life insurance companies in Philippines. Prior to joining AIA, Menon worked in DBS Bank, BDNI Life, and the Insurance Corporation of Singapore (now known as Aviva in Singapore). He was also a director of GT Asset Management forming the first mutual fund in Indonesia and was a police inspector in the Singapore Police Force when serving his national service.

He graduated with a Bachelor’s Degree in Actuarial Sciences at the Macquarie University in Sydney, Australia. He also earned a Certificate in Actuarial Techniques from Institute of Actuaries in London, a Penasehat Investor (Investment Manager’s License) in BAPEPAM (Indonesian Stock Exchange) and an Associate in Financial Planning in Financial Planning Association of Singapore.

20

SIMON R. PATERNO (57 years old)Non-Executive Director

Mr. Paterno heads the BPI Financial Products Group. He is responsible for managing the product businesses of the Bank, including Investment Banking, Corporate Loans and Transaction Banking, Retail Lending, Payments, Asset Management and Trust, Channels, and Deposits. He also oversees subsidiaries and affiliates in insurance, leasing, and merchant acquiring. He is a member of the Management Committee of BPI.

Mr. Paterno is a former President and CEO of the Development Bank of the Philippines, serving from 2002-2004. He worked for 18 years at the New York, Hong Kong, and Manila offices of J.P. Morgan, serving finally as Managing Director in charge of sovereign clients during the Asian Financial Crisis of 1997-98, and as Country Manager for the Philippines until 2002.

He also worked for 8 years at Credit Suisse as Managing Director and Country Manager for the Philippines.

Mr. Paterno obtained his MBA from Stanford University in 1984. He was awarded his A.B., cum laude, Honors Program in Economics from Ateneo de Manila University in 1980. In 2005, he was elected President of the Management Association of the Philippines. He serves on the boards of the Foundation for Economic Freedom, Manila Polo Club and Ateneo Scholarship Foundation. He was named a TOYM awardee for Investment Banking in 1999.

TERRENCE CUMMINGS (50 years old)Non-Executive Director

Terrence Cummings is Head of AIA Vitality in AIA Group. In 2013, he joined AIA Group as the Regional Director of Business Development in the Regional Chief Executive’s Office of AIA, based in Hong Kong. Terrence has over 20 years

Board Support

of international life insurance experience covering Asia, the Middle East, Europe, and North America. Terrence has held senior management positions including Chief Operations Officer, Chief Marketing Officer, and Chief Actuary with major multinational life insurers and consulting firms. Terrence’s areas of practice include product development, distribution, and marketing, operational efficiency, financial reporting, mergers, acquisitions, and distribution agreements. Terrence is a Fellow of the Society of Actuaries and holds a Bachelor of Science in Actuarial Science from the University of Iowa.

CARLA J. DOMINGOCorporate Secretary

Atty. Domingo is currently the Head of Legal and Corporate Secretary of The Philippine American Life and General Insurance Company (Philam Life). She also serves as the Corporate Secretary of BPI-Philam Life Assurance Corporation (formerly Ayala Life).

She was also the Corporate Secretary of various Philam companies from 2008 to January 2014: Philam Equitable Life Assurance Company; Philam Properties Group of Companies; Philam Asset Management Inc.; Philam Call Center Services, Inc.; the Tower Club, Inc. and Philam Foundation, Inc.

Atty. Domingo is a member of the Integrated Bar of the Philippines and a Fellow of the Institute of Corporate Directors. Atty. Domingo is a graduate of the University of the East, with a Bachelor of Arts degree major in Political Science, where she graduated Magna Cum Laude. She took her Bachelor of Laws degree in San Beda, College of Law.

21

AUDIT COMMITTEERomeo L. Bernardo - Chairman(Independent Director)

J. Axel Bromely(Non-Executive Director)

Jesus P. Tambunting(Independent Director)

COMPENSANTION/REMUNERATIONCOMMITTEESurendra Menon - Chairman(Non-Executive Director)

Cezar P. Consing(Non-Executive Director)

Jesus P. Tambunting(Independent Director)

EXECUTIVE COMMITTEEDarren Thomson - Chairman(Non-Executive Director)

Cezar P. Consing(Non-Executive Director)

Ariel G. Cantos(Executive Director)

J. Axel Bromely(Non-Executive Director)

Natividad N. Alejo(Non-Executive Director)

Aurelio Luis R. Montinola III *(Non-Executive Director)

*as alternate of Mr. Consing and Ms. Alejo

BOARD RISK COMMITTEECezar P. Consing - Chairman(Non-Executive Director)

Simon R. Paterno(Non-Executive Director)

Jesus P. Tambunting(Independent Director)

Ariel G. Cantos(Executive Director)

Terrence Cummings(Non-Executive Director)

INVESTMENT COMMITTEEArleen May S. Guevara - Chairperson(Senior Officer)

Ariel G. Cantos(Executive Director)

Natividad N. Alejo(Non-Executive Director)

Jesus P. Tambunting(Independent Director)

Simon R. Paterno(Non-Executive Director)

Tisha T. Darvin(Senior Officer)

Spencer T. Yap(Senior Officer)

NOMINATION & GOVERNANCE COMMITTEESurendra Menon - Chairman(Non-Executive Director)

Jesus P. Tambunting(Independent Director)

Aurelio Luis R. Montinola III(Non-Executive Director)

BOARD COMMITTEES

22

CORPORATE OFFICERS

Aurelio Luis R. Montinola III - Chairman of the BoardDarren Thomson - Vice-Chairman Ariel G. Cantos - Chief Executive OfficerSpencer T. Yap - Treasurer and Chief Finance OfficerCarla J. Domingo - Corporate SecretaryAce Devino A. Custodio - Asst. Corporate Secretary

SENIOR OFFICERS

Arleen May S. Guevara - Investment OfficerAndreas Rosenthal - Senior Vice PresidentTisha T. Darvin - Chief ActuaryMa. Carmen N. Asinas - Head of Operations and Customer ExperienceKatherine P. Custodia - Territory Sales Head handling Metro East, Metro North, Visayas and MindanaoMartin P. Ledesma - Head of AIA-Citi Partnership DistributionJose Ivan Tuazon Justiniano - Head of ComplianceJoseph G. De Dios - Chief Risk OfficerShiela P. Alarcio - Head of AuditJ. Vincent R. Daffon - InvestmentsJohann Florence V. Balbido - Deputy Head of AIA-Citi Partnership DistributionJohannes D. De Ramos - Head of AIA-Citi Direct MarketingAmante R. Cruz - Medical DirectorNecy D. Santiago - Head of TreasuryMonica F. Bondoc - Head of Human Resources Percival Cirilo S. Flores - Head of Business Analytics and StrategyEduardo R. Flores - Head of Strategic Business ManagementMartha Isabel Sta. Ana-Perez - Personal Banking Segment Management HeadSherwin Chan - Private Banking Segment Management Head Nancy L. Manansala - Head of Corporate SolutionsJoseph Loreto G. Lopez - Head of Direct MarketingFelisa B. Ronan - Head of Corporate Solutions Sales

LIST OF OFFICERS

23

24

The AIA Code of ConductHonesty and integrity are the cornerstones of the AIA business. AIA serves millions of customers across the most dynamic growth region in the world – and is known and admired for its unwavering commitment to these values.

This reputation and the trust it inspires is critical to the success of the organization. Dedication and commitment to high standards have helped build the organization in the past and for the present. It can only maintain that reputation into the future when each employee strives harder to do what is right and by being prepared to take their personal responsibilities in observing the highest standards of integrity and conduct at all times and in every dealing.

This is what the AIA Code of Conduct is about. It sets out AIA’s and its member companies’ commitment to the Operating Philosophy of “Doing the Right Thing, in the Right Way, with the Right people… and the results will come.” This establishes the unique culture of AIA across all 17 markets within the Asia Pacific region that includes BPI-Philam.

The AIA Code of Conduct sets out the ethical guidelines for conducting business which is the same code that BPI- Philam observes. This serves as guide in managing the company’s compliance, ethics, and risk issues.

The standards set forth in the Code also applies to the business partners including agents, contractors, subcontractors, suppliers, distribution partners, and those who act on behalf of AIA and BPI-Philam. Thus, the corporation, its directors, senior management and employees are mandated and required to comply with the policies. The Compliance Department is tasked to implement these policies and monitor compliance therewith.

Like AIA, BPI-Philam has always believed in the power of diverse, talented people to create value and deliver on customer and shareholder expectations. Thus, it competes vigorously to create new opportunities for its customers and for itself. However, competitive advantages are sought only through legal and ethical business practices. With the products, services and responsible business practices, BPI-Philam strives to improve the quality of life of every Filipino. Promoting compliance with local laws and local regulatory requirements that apply to the business is at the foundation of BPI-Philam’s good corporate citizenship.

Code of Conduct Annual Certification Program To ensure that all BPI-Philam employees are aware of the provisions of the Code, an annual certification program is conducted whereby all employees confirm their knowledge and understanding about the rules and guidelines written in the Code.

Business Conduct Orientation Program At the same time, it is company policy that all new hires attend the Business Conduct Orientation Program (BCOP) whereby the Code and all other relevant compliance policies are discussed. This program is offered on a monthly basis and is conducted either by Compliance or Training Department.

BPI-Philam is a Safe, Healthy and Secure WorkplaceBPI-Philam conducts its business in a manner that protects the health, safety and security of its employees and customers. Situations that may pose health, safety, security and environmental hazards must be reported promptly to management or to the appropriate Corporate Security Personnel.

Avoiding security breaches, threats, losses and theft requires that all employees remain vigilant in the workplace while carrying out business. Employees are encouraged to notify management or Corporate Security of any issue that may impact the company’s security, fire and life safety or emergency readiness.

Using, selling, possessing or working under the influence of illegal drugs at BPI-Philam is strictly prohibited. At the same time, excessive or inappropriate use of alcohol while conducting business for BPI-Philam is also prohibited.

Physical security systems reduce the risk of exposure. Entry controls are implemented to ensure company’s safety security and protection. Wearing of IDs and uniforms are strictly observed.

BPI-Philam respects the personal information and property of employees. Employees expect the company to carefully maintain the personal information they provide.

Operating Philisophy

Email announcement sent to employees for the Annual Certification Program

25

Employee trust must not be compromised by disclosing this information other than to those with a legitimate need to know.

Access to personal information or employee property is only authorized for appropriate personnel with a legitimate reason to access such information or property. From time to time, BPI-Philam may access and monitor employee internet usage and communications to assess compliance with laws and regulations, policies and behavioral standards. Subject to local laws, employees shall have no expectation of privacy with regard to workplace communication or use of AIA and BPI-Philam’s information technology resources.

BPI-PHILAM SHAPES ETHICAL PRACTICES

Treating Customers FairlyThe Treating Customers Fairly policy demands that customers should be treated fairly at all times and that products, services, and advice must be appropriate to meet customer needs. Marketing, advertising, and sales-related materials and services must always be truthful and accurate and misrepresenting or attempting to mislead or deceive customers by use of unsupported or fictitious claims about BPI-Philam products or those of its competitors is not acceptable.

BPI-Philam should provide high standards of service and should respond promptly and fairly to customer feedback.

BPI-Philam adopts a structured framework in handling complaints related to market misconduct. The Customer Complaints Handling Process ensures that all customer complaints and grievances are immediately addressed. The process defines the step-by-step approach in addressing and handling complaints as a result of any of its sales personnel’s misconduct.

A Compliance Disciplinary Committee evaluates all complaints and determines whether a sales personnel has committed any wrongdoing. Any sales personnel found guilty of any market conduct related offense is subjected to appropriate sanctions.

Misconduct includes, but is not limited to, misrepresentation of product features, mis-selling, policy replacement, misappropriation of client monies, and any other infringement of the Market Conduct Guidelines.

Customer Privacy & Data SecurityCustomers expect BPI-Philam to carefully handle and safeguard the business and personal information that they share in the conduct of the business. BPI-Philam must never compromise a customer’s trust by disclosing private information other than to those with a legitimate business need to know.

Employees who handle customer information are responsible for knowing and complying with applicable

information privacy and information security laws. In all cases, appropriate physical, administrative, and technical safeguards for personal information and business data must be maintained.

All employees are encouraged to be especially vigilant in following the laws, regulations, and policies when transferring personal information and business data across country borders.

To ensure customer privacy and data security, BPI-Philam observes AIA’s Data Privacy Compliance Guidelines. The guidelines outline the company’s statement of values and provides guidance to employees and any member of BPI-Philam on how personal data should be collected, used, stored, transferred and disposed. The guidelines also clarifies the roles and responsibilities of each and every employee and the relevant standards and procedural controls expected to secure personal data in accordance with the policy objectives.

The CEO is responsible for the implementation of the data privacy policy and guidelines through its appointed Data Privacy Officer. This includes ensuring that all employees within the business unit are aware of their obligations stated in the policy and guidelines and that they comply with the standards when managing personal data collected in their business entity. The Business Conduct Orientation Program for new employees includes a module on Data Privacy Policy that is discussed lengthily to ensure that all employees understand their obligations under the local Data Privacy law and AIA/BPI-Philam’s Data Privacy policy.

Conflict of InterestAn employee’s position in BPI-Philam must not be used for inappropriate personal gain or advantage. Any situation that creates, or even appears to create, a conflict of interest between personal interests and the interests of the company must be appropriately managed.

Conflicts of interest (whether potential or actual conflicts) must be reported. There is a system being used for the reporting. Managers are expected to take appropriate steps to prevent, identify and appropriately manage conflicts of interests of those they supervise.

All AIA and BPI-Philam employees are prohibited from taking for themselves, or directing to a third party, a business opportunity that is discovered through the use of company’ corporate property information. BPI-Philam employees are prohibited from using corporate property, information or position for personal gain.

Employees are asked to declare if they have any personal relationships within the group. Immediate family members, members of the household and individuals with whom an employee has a close personal relationship within the group must never improperly influence business decisions.

26

When determining whether a personal relationship might lead to a conflict of interest, the following questions can serve as guide:

• Does one of us have influence over the other at work?• Does one of us supervise or report to the other?• Could an outsider view the situation as a conflict of interest?

Fair DealingFollowing AIA’s model, BPI-Philam seeks competitive advantages only through legal and ethical business practices. Every employee must conduct business in a fair manner with customers, service providers, suppliers and competitors. Disparaging competitors or their products and services is discouraged. Improperly taking advantage of anyone through manipulation, concealment, abuse of privileged information, intentional misrepresentation of facts or any other unfair practice is not and will not be tolerated at BPI-Philam much more in the AIA Group.

Creditor’s RightsIt is the policy of BPI-Philam to uphold creditor’s rights by honoring its contractual obligations with all its creditors and counterparties in accordance with the provisions of their contracts and the law. In the conduct of its business dealings with third parties, BPI-Philam undertakes to honor all its commitments, stipulations, and conditions set forth in their binding agreements.

Sourcing PolicyBusiness partners serve as extensions of BPI-Philam to the extent that they operate within contractual relationships. Business partners are expected to adhere to the spirit of the AIA Code of Conduct and to any applicable contractual provisions.

Business partners must not act in a way that is prohibited or considered improper for a BPI-Philam employee. Employees must ensure that customers, agents, and suppliers do not exploit their relationship with BPI-Philam or use BPI-Philam’s name in connection with any fraudulent, unethical, or dishonest transaction.

Suppliers and vendors are selected on the basis of performance and merit in accordance with a fair and transparent process. Requirements for suppliers and vendors to follow the standards in the Code must be included in the vendor management program.

The total expenditure on goods and services from third party suppliers form a significant part of BPI-Philam’s operating cost. Any activity by a line of business to acquire goods or services must be undertaken in a professional manner to ensure BPI-Philam is able to maximize the value and manage risks associated with use of external suppliers.

The local Sourcing Policy, that took effect in November 2013, sets out the framework within which BPI-Philam must engage external suppliers for goods or services and

is supplemented by BPI-Philam’s Sourcing Practice Guide. This provides BPI-Philam the standard processes and document templates in engaging suppliers that should be read in conjunction with the policy document.

The BPI-Philam Sourcing Policy, with the AIA Group Sourcing Policy as a model, was defined with the primary objective to establish standardized sourcing procedures.

As set out in the AIA Group Sourcing Policy, a Local Sourcing Lead (LSL) or a designate is appointed to be responsible for ensuring implementation, execution, update and compliance of the local policy. This person should closely work with the AIA Group Sourcing (GS) team.

CORPORATE CITIZENSHIP

Communicating with Regulators and Other Governmental OfficialsInquiries from regulators outside the normal course of BPI-Philam’s regulatory relationships must be reported immediately to the Compliance Officer or a designated Legal Counsel before a response is made.

Financial reporting related inquiries may be responded to by authorized comptrollers. Responses to regulators must contain complete, factual, and accurate information. During a regulatory inspection or examination, documents must never be concealed, destroyed or altered, nor must lies or misleading statements be made to regulators. Requests from auditors are subject to the same standards.

Anti-Money Laundering and Counter Terrorist Financing“Money Laundering” is the process by which criminals conceal the nature or source of their illegal funds and disguise them to make them appear legitimate. It is not limited to drug money or banking transactions but may involve sophisticated schemes in every sector of the financial services industries from commercial and investment banking to insurance which is our core business.

Pursuant to Section 18 of Republic Act (RA) No. 9160, also known as the “Anti-Money Laundering Act of 2001”, as amended by RA No. 9194, RA No. 10167, RA No. 10168 and RA No. 10365, all covered institutions which include insurance companies supervised or regulated by the Insurance Commission are mandated to formulate their respective money laundering prevention program in accordance with the said law including, but not limited to, information dissemination on money laundering activities and its prevention, detection and reporting, and the training of responsible officers and personnel of covered institutions.

As a member company of AIA, BPI-Philam adopts the AIA Anti-Money Laundering and Counter Terrorist Financing Program, and incorporates it as part of the local program.

As a matter of policy, BPI-Philam shall foil any attempt by anyone to use the company or its affiliates for money laundering purposes. This Anti-Money Laundering Program, together with the Company’s Guidelines, establishes the governing principles and business standards to protect

27

BPI-Philam and its business operations from becoming an unwitting tool of money launderers. The company’s management, officers, and staff must remain vigilant in the fight against money laundering and financing of terrorism and shall collectively oppose any effort to violate or flaunt the “Anti-Money Laundering Act of 2001”, as well as its implementing rules and regulations.

Throughout the world, AIA and its subsidiaries like BPI -Philam are firmly committed to complying with all applicable anti-money laundering laws, covered and suspicious transactions reporting and identification requirements. These include taking affirmative steps, within the confines of applicable laws, to prevent, detect and report money laundering activities to appropriate authorities.

Anti-Corruption and Bribery; Gifts and EntertainmentThe Policy is applied alongside the AIA Code of Conduct. It provides guidance on giving and accepting gifts and entertainment. The Anti-Corruption Guidelines specifies the roles, responsibilities, and procedural controls for transactions involving government officials. All relevant laws countering bribery and corruption must be upheld. If local laws and regulations require higher compliance standards vis-a-vis the guidelines of the AIA Code of Conduct, then BPI-Philam must meet the higher standards.The local CEO is responsible for the implementation of this policy and guidelines including ensuring that all employees within his business unit are aware of their obligations stated in the Policy and Guidelines and comply with the standards. Compliance is responsible for maintaining the Policy and Guidelines for providing second line oversight and monitoring of effective implementation.

The Anti Corruption and Bribery Policy basically prohibits all employees, agent, or independent contractor in providing bribes or other benefits to another person in order to obtain or retain business or unfair advantage in any business interaction involving AIA and BPI-Philam, its customers and its employees.

The company is not allowed to use improper means to influence another person’s business judgement. All employees and officers are required to comply with the guidelines. Any employee who has knowledge of or in good faith suspects a violation of any of these laws, regulations, or policies must report them promptly to the Compliance Officer assigned in the business unit or otherwise as set out in the Speak Up program.

Prevention of Insider Trading and PriceSensitive InformationThe AIA Group takes its obligations as a listed entity seriously and is committed to ensuring the highest standards of market conduct and fair dealing. The Hong Kong Securities and Futures Ordinance (SFO) prohibits market misconduct including insider trading. Breaches of market misconduct laws are serious offenses that attract heavy civil and criminal penalties.

Since BPI-Philam is a member of the AIA Group, it also adopts the same policy and follows the same guidelines. The Prevention of Insider Trading and Market Misconduct Policy aims to build a robust system to prevent market misconduct including insider trading. It sets out standards and controls to ensure compliance with the regulatory requirements. Lastly, the existence of this policy should prevent employees and directors from engaging in speculative trading in AIA Group Securities.

The policy applies to all employees and directors of AIA Group Limited and each of its subsidiaries (“AIA Group”) just like BPI-Philam.

This policy defines the duty of each employee to safeguard material information from improper use. Under the policy, it is illegal to trade securities while in possession of a material non-public information and pass a material non-public information to anyone who may trade securities based on it or give others recommendations to buy or sell securities.

SOCIAL AND ENVIRONMENTAL RESPONSIBILITIES

Social MediaBPI-Philam recognizes the value of social media to engage with stakeholders in innovative and interactive ways. When using social media, every employee must conduct themselves professionally following the AIA Social Media Policy. Social media includes blogs, forums, chat rooms, professional and social networking sites, photo and video sharing sites, and other interactive online media such as Twitter.

The Whistleblow ProgramBPI-Philam does business with integrity and follow the highest ethical principles. Any employee (or anyone else) may raise concerns of misconduct or wrongdoing within AIA and BPI-Philam that can allow investigation to fix any problem. This Policy guides all employees on how to raise ethical concerns and managers on how they should respond when this happens.

The Whistleblow Policy applies to all employees of the AIA Group including BPI-Philam. ‘Whistleblower’ refers to someone (an AIA employee, business partner, agent, consultant, vendor, customer or other party) who informs AIA or BPI-Philam of suspected illegal or improper ways of doing business involving violation of laws, regulations, AIA or BPI Philam policies, and other unethical actions that might negatively impact AIA’s and BPI-Philam’s reputation.

Employees who are aware of possible wrongdoing within AIA and BPI-Philam have a responsibility to disclose that information to management. Reports are taken seriously and investigated confidentially. Employees or other individuals will not suffer retaliation for reporting suspected wrongdoing in good faith.

28

An AIA Ethicsline was developed to support the program. It is an independently managed website and hotline (telephone) service, receiving reports in local language, 24 hours a day, and 7 days a week. AIA and BPI-Philam can communicate with anonymous whistleblowers using this website via a secure platform.

The following misconduct including unethical or unlawful acts can be reported through this AIA Ethics line. • Fraud, misappropriation, theft, bribery or corruption, giving or receiving inappropriate gifts or kickbacks; • Harassment, bullying or assault, discrimination, conflicts of interest, or abuse of authority; • Fake or falsification of signatures, customer accounts, information or business performance reports; • Creating inappropriate funds or cash floats (slush funds) with travel agents, fake vendor bids, etc. • Signs of retaliation against a whistleblower or suspected whistleblower including subtle acts such as exclusion from meetings or events which may impact long term career or advancement. • Anyone trying to interfere with the confidentiality of a whistleblower report, identifying or giving away the identity of a whistleblower, or encouraging or tolerating such actions.

Reporting concerns or suspicions may be made by multiple means provided in the AIA Code of Conduct. The report may also be made by using the AIA Group Ethics and Compliance Hotline (PLDT) 1010-5511-00-00-245-4179 or (Globe) 105-11-800-245-4179.

RETIREMENT BENEFITThe company has a defined benefit plan. The amount of retirement benefit that an employee will receive upon retirement usually depends on one or more factors such as age, years of service and compensation. Retirement cost is actuarially determined using the projected unit credit method.

BPI-PHILAM’S COMPLIANCE DISCIPLINARYFRAMEWORK & GUIDELINES Under this Framework and Guidelines (the “Framework”), Heads of Departments have the power to impose disciplinary sanctions to any employee who has been found, after due process, to have breached or violated any of the company’s compliance policies.

The Framework seeks to ensure that in all decisions regarding employee misconduct or violation shall undergo a due diligence review, fair hearing, with representation if they so choose and with penalties that are proportionate.

In the event of a serious or material breach, criminal misconduct or where it is reasonably believed that the safety or welfare of employees or the Company is put at risk by the continuing presence of an employee or employees against whom allegations have been brought, such employee or employees will be suspended immediately without prejudice.

Heads of Departments shall closely coordinate with Compliance, Legal and/or Human Resources whenever necessary. For breaches identified by Compliance, Compliance shall escalate the matter to the Heads of Departments for further action.

Market Conduct GuidelinesBPI-Philam envisions itself as having one of the highest sales standards in the life insurance industry in Philippines. All sales personnel are expected to conduct their business with the highest level of professionalism and personal integrity. BPI-Philam will not tolerate anything less.

The Market Conduct Guidelines is used as a guide by all sales personnel in the conduct of their business and aid in the determination of what would be deemed proper conduct and behavior. It shall apply equally and consistently to the conduct of Life business practices and all financial products. Any breach of the Market Conduct Guidelines may result in the imposition of a penalty upon the offender in question. Compliance with these guidelines does not ensure a continued contractual relationship with BPI-Philam. BPI-Philam reserves the right at all times to terminate the employment contract of any sales personnel in accordance with the terms of the contract entered into between BPI-Philam and that of the sales personnel.

Sales Code of DisciplineIn pursuit of building and promoting professionalism and having one of the highest sales ethical standards in the life insurance industry, it is the policy of the Company to set up measures of conduct and standards of behavior to instill a strong sense of discipline among its sales force. Disciplinary actions are corrective rather than punitive in nature.

In promoting professionalism among sales and moving towards self-regulation, the Office of the Insurance Commission and the Philippine Life Insurance Association support the need and use of penalties or sanctions or a combination thereof as the company deems fit.

The BPI-Philam Sales Code of Discipline contains penalties associated with the breach of company policy, the Market Conduct Guidelines, Employment Contract, laws, and regulations. The objective is to establish uniform disciplinary sanctions amongst all sales personnel and adopt a systematic and equitable procedure in administering corrective measures.

The sanctions, which may range from written reprimand to termination of employment, are applied accordingly depending on the gravity of the offense and as deemed appropriate by the company. The offenses listed in this Code of Discipline are given as guidelines and are not exclusive of all types of offenses. Unique and complex cases are handled by the BPI-Philam Compliance Disciplinary Committee (BCDC) or by highest levels of Management.

29

ENTERPRISE RISK MANAGEMENTBPI-Philam’s risk function recognizes that effective risk management maximizes the value of its business to its shareholders. For policyholders, it is the security from knowing that we will always be there for them. For regulators, sound risk management is vital to the stability of the financial system. For investors, it is a means of protecting and enhancing the long-term value of their investment.

BPI-Philam’s Enterprise Risk Management (ERM) pursues initiatives to become widely recognized among risk professionals and among top organizations in the financial sector by 2018. One of the core initiatives is reinforcing institutionalized practices like mobilizing Risk Champions. Management will appoint “Risk and Compliance Champion” (RICO Champ), who will serve as ERM partners in promulgating our operating principle of “Doing the right thing in the right way with the right people and the results will come”. ERM also aims to enhance risk awareness campaigns to expand its reach in the organization and its affiliates.