annual report 2011 - permasteelisa group · annual report 2011. 1 annual report 2011. 2 ......

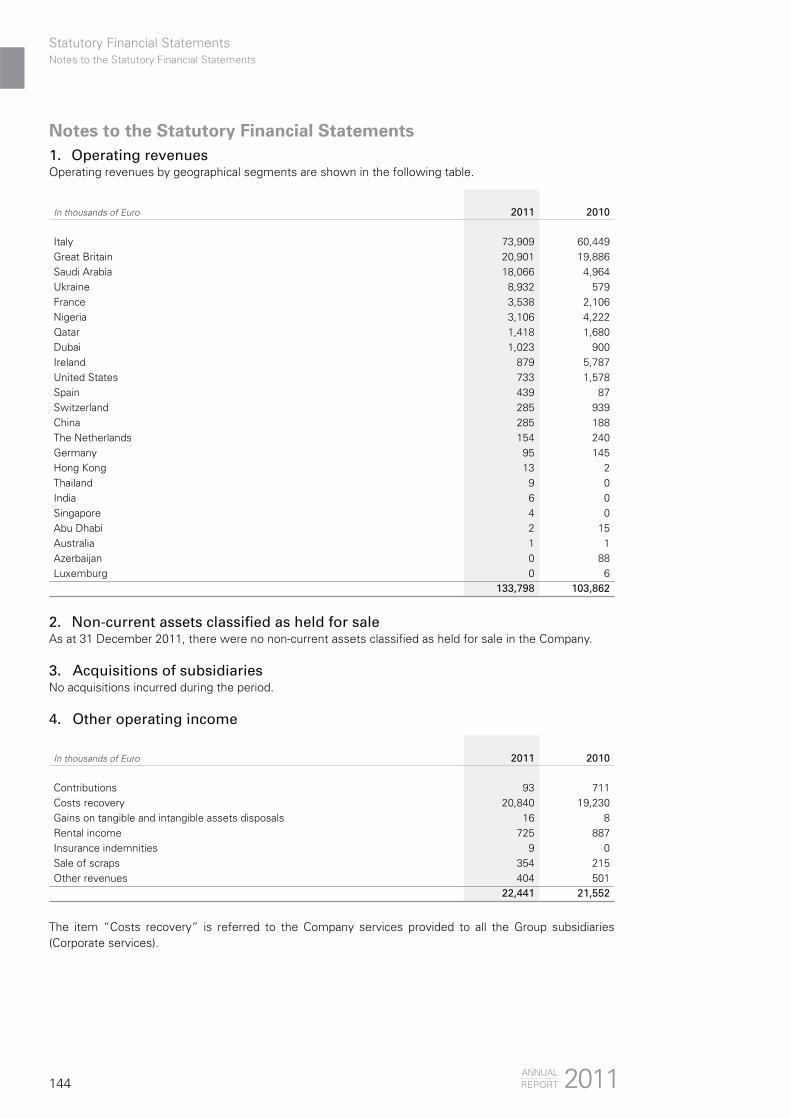

TRANSCRIPT

2011ANNUAL REPORT

1

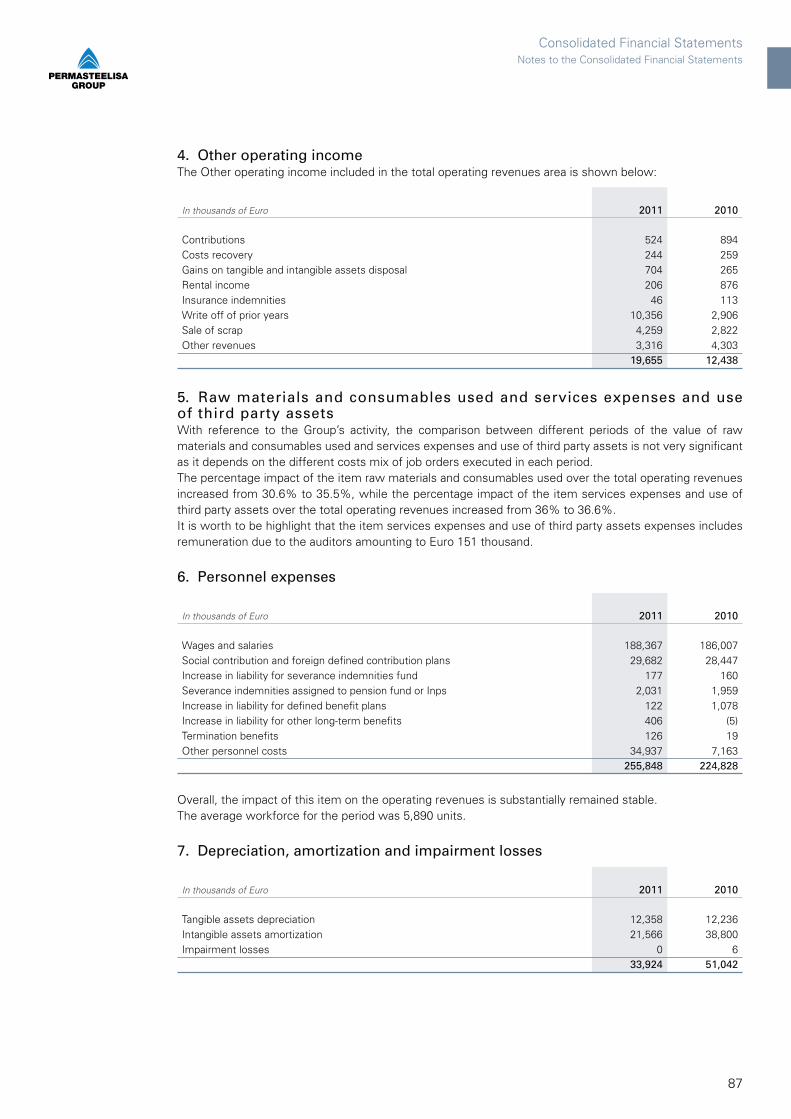

A N N U A L R E P O R T

2011

2

Ph.

: Kar

in J

obst

3

4

New York by GehryNew York, NY \ USA

Ph.

: Les

ter

Ali

Pho

togr

aphy

5

Administration and Controlling Boards

Group Structure

Management Report to the Consolidated Financial Statements

and to the Statutory Financial Statements

Main economic and financial dataPerformance for the periodOverview of ongoing projects and main project acquisitionsMain risks and uncertainties which Permasteelisa S.p.A. and the Group are exposed toThe Group’s organizational structureResearch and innovation

Technical Support Group

Information TechnologyHuman ResourcesShareholdersTreasury sharesTransactions with related partiesSignificant events subsequent to year end and outlookOther disclosuresOperating performance and financial position of Permasteelisa S.p.A.Approval of the Statutory Financial Statements and allocation of 2011 result

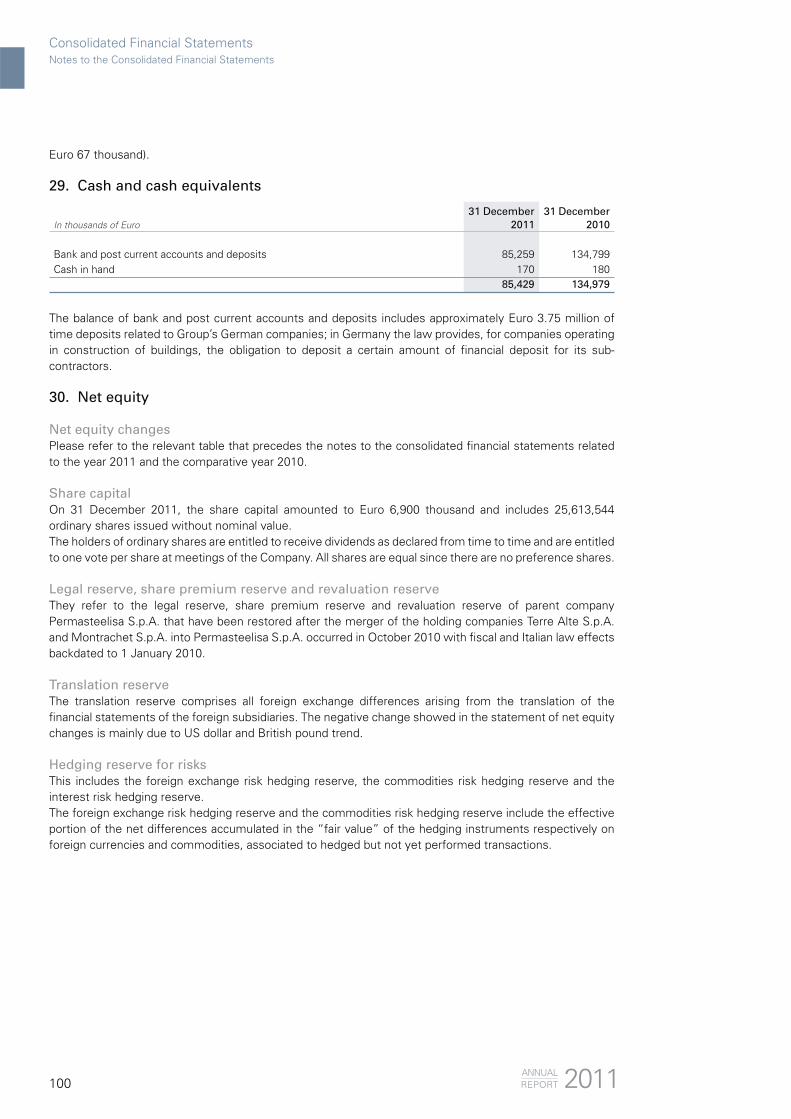

Permasteelisa Group - Consolidated Financial Statements

for the year ended 31 December 2011

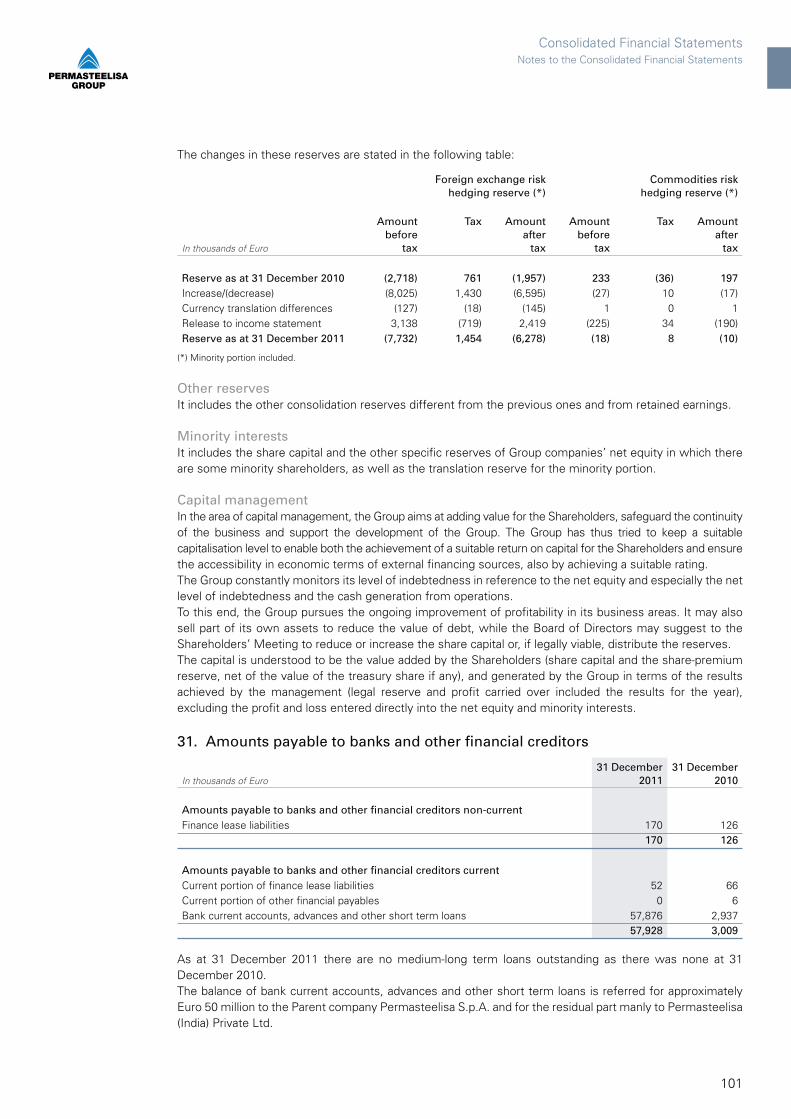

Consolidated income statementStatement of comprehensive incomeConsolidated statement of financial positionConsolidated statement of cash flowsConsolidated statement of net equity changesNotes to the Consolidated Financial StatementsAppendix I: Permasteelisa Group’s companies

Permasteelisa S.p.A. - Statutory Financial Statements

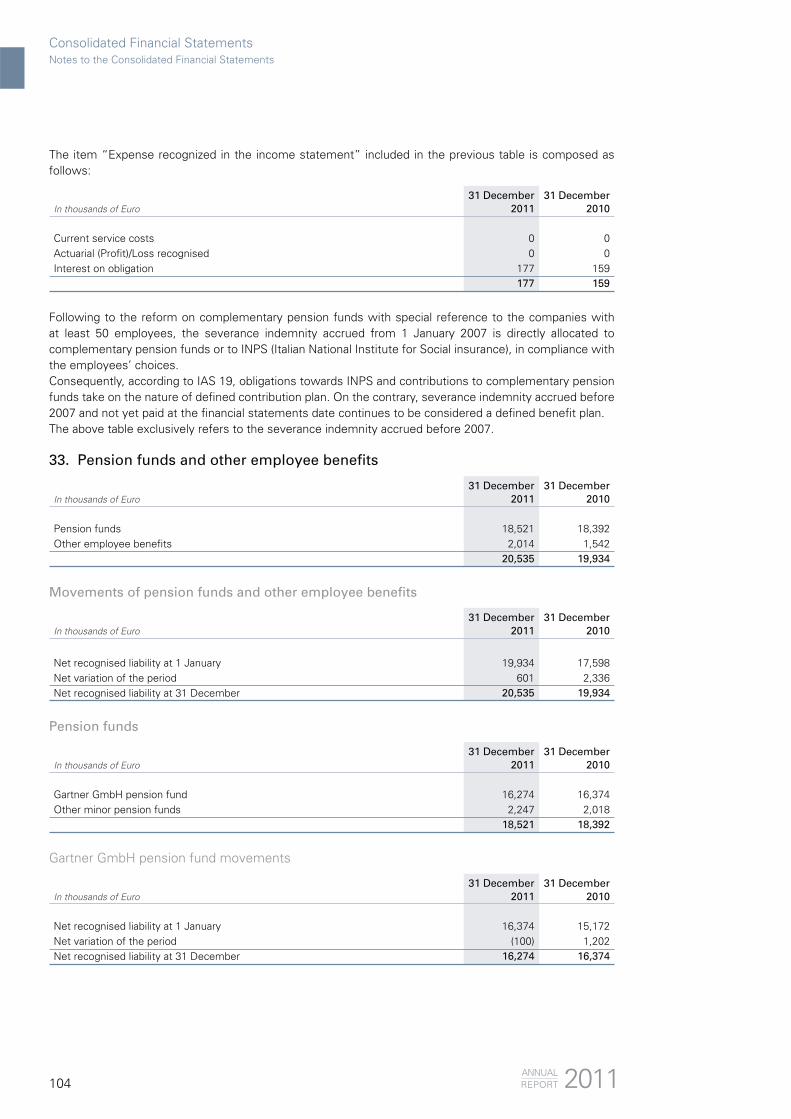

for the year ended 31 December 2011

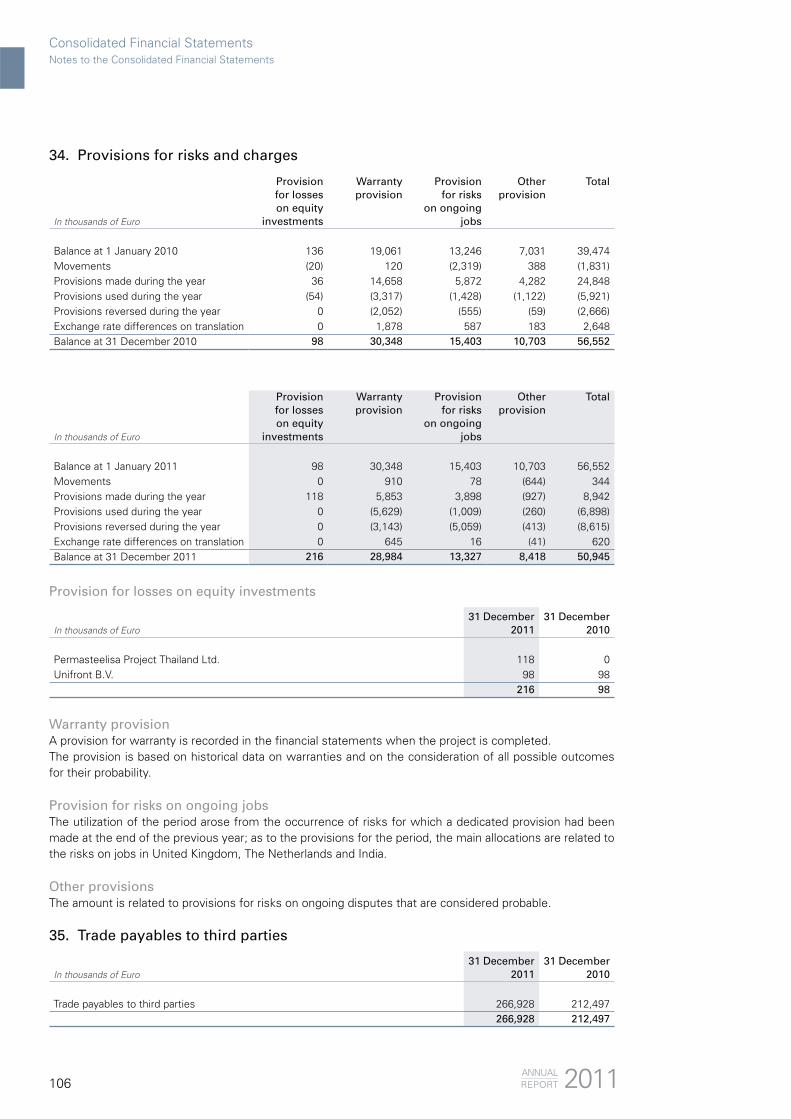

Income statementStatement of comprehensive incomeStatement of financial positionStatement of cash flowsStatement of net equity changesNotes to the Statutory Financial StatementsAppendix I: Receivables and payables broken down by geographical area

Auditors’ report on the Consolidated Financial Statements

Auditors’ report on the Statutory Financial Statements

Report of the Board of Statutory Auditors

Company Name

Permasteelisa S.p.A. with sole shareholder

Registered Office Share Capital

Viale E. Mattei 21/23 Euro 6,900,000 fully paid in Treviso REA31029 Vittorio Veneto, Treviso, Italy (Economic and Administrative Repertory) enrolment no. 169833

Index

79

11

131421485050

51

515357575757586063

65

66

6768697172

121

125

126126127128130131178

182184186

\\\

\\\

\\\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

\

6

Neubau ADAC-ZentraleMunich \ Germany

Ph.

: Ste

phan

Lie

bl

7

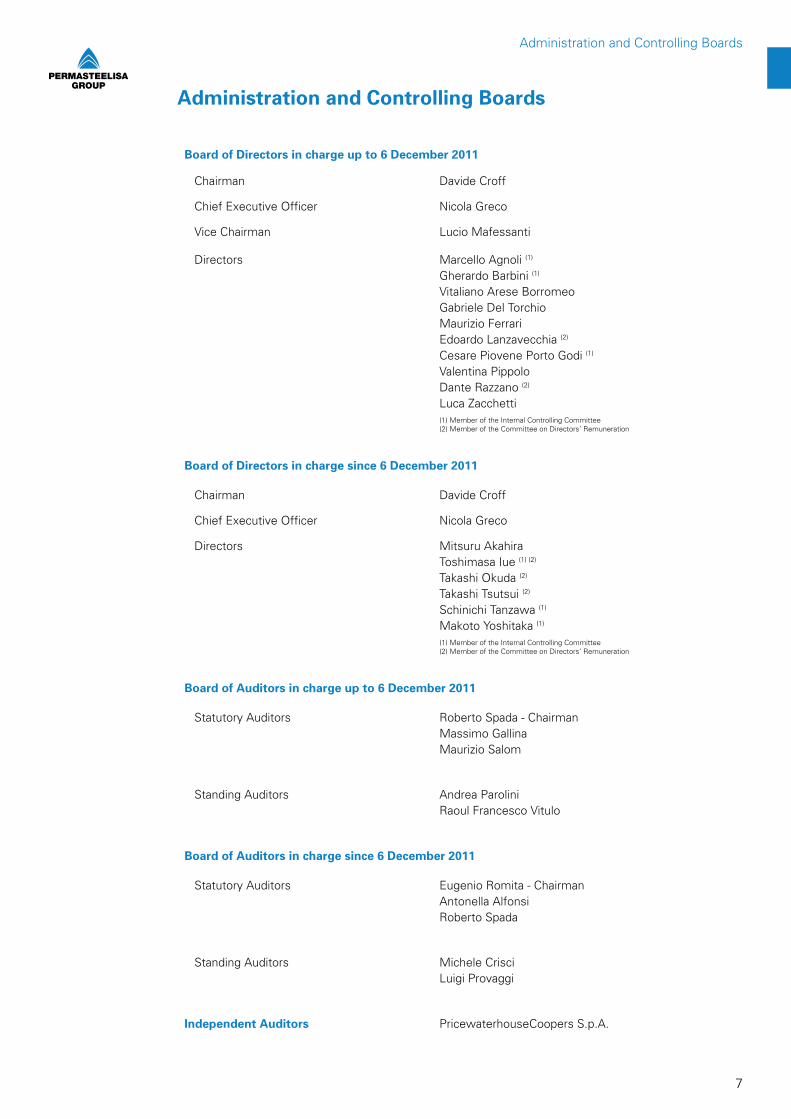

Board of Directors in charge up to 6 December 2011

Chairman Davide Croff

Chief Executive Officer Nicola Greco

Vice Chairman Lucio Mafessanti

Directors Marcello Agnoli (1)

Gherardo Barbini (1)

Vitaliano Arese BorromeoGabriele Del TorchioMaurizio FerrariEdoardo Lanzavecchia (2)

Cesare Piovene Porto Godi (1) Valentina PippoloDante Razzano (2)

Luca Zacchetti(1) Member of the Internal Controlling Committee(2) Member of the Committee on Directors’ Remuneration

Board of Directors in charge since 6 December 2011

Chairman Davide Croff

Chief Executive Officer Nicola Greco

Directors Mitsuru AkahiraToshimasa Iue (1) (2)

Takashi Okuda (2)

Takashi Tsutsui (2)

Schinichi Tanzawa (1)

Makoto Yoshitaka (1) (1) Member of the Internal Controlling Committee(2) Member of the Committee on Directors’ Remuneration

Board of Auditors in charge up to 6 December 2011

Statutory Auditors Roberto Spada - ChairmanMassimo GallinaMaurizio Salom

Standing Auditors Andrea ParoliniRaoul Francesco Vitulo

Board of Auditors in charge since 6 December 2011

Statutory Auditors Eugenio Romita - ChairmanAntonella AlfonsiRoberto Spada

Standing Auditors Michele CrisciLuigi Provaggi

Independent Auditors PricewaterhouseCoopers S.p.A.

Administration and Controlling Boards

Administration and Controlling Boards

8

Sathorn SquareBangkok \ Thailand

Ph.

: Krit

Mut

itaph

orn

Arc

hite

ctur

al P

hoto

grap

her

9

Group Structure

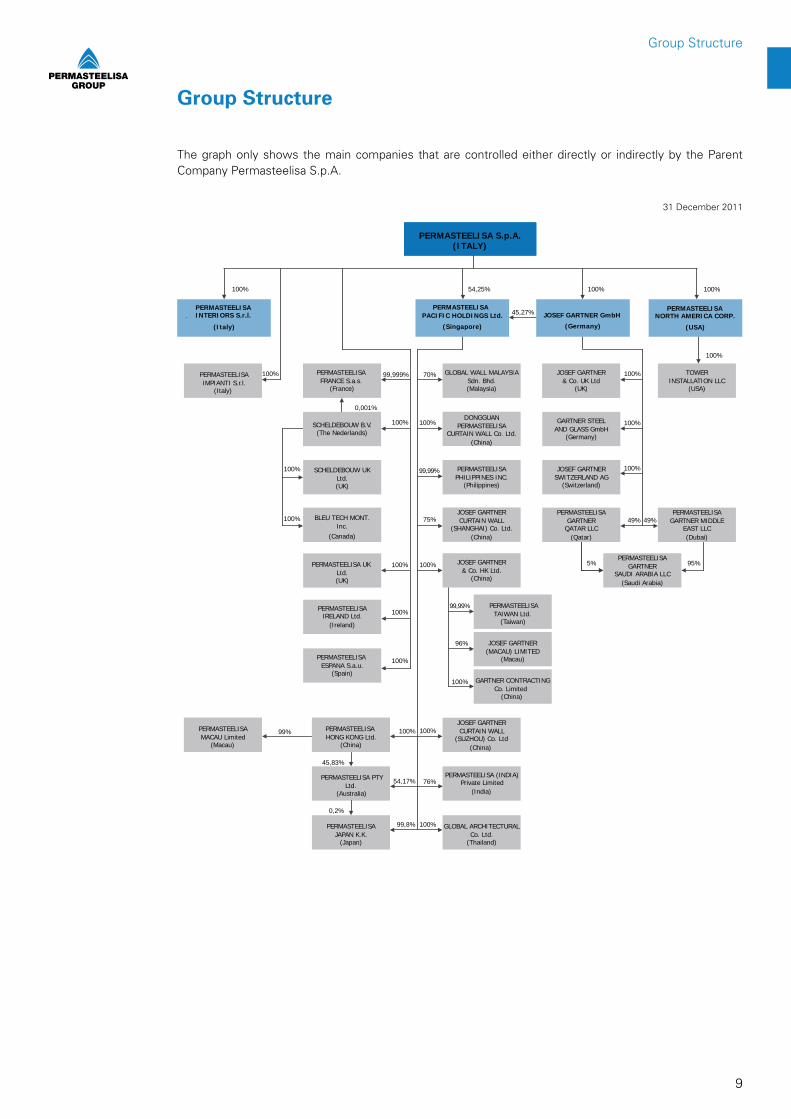

The graph only shows the main companies that are controlled either directly or indirectly by the Parent Company Permasteelisa S.p.A.

31 December 2011

100%

PERMASTEELISA INTERIORS S.r.l.

(Italy)

PERMASTEELISA .l.r.S ITNAIPMI

(Italy)

PERMASTEELISA PACIFIC HOLDINGS Ltd.

(Singapore)

100%

PERMASTEELISA UK Ltd.(UK)

JOSEF GARTNERSWITZERLAND AG

(Switzerland)

SCHELDEBOUW UKLtd.(UK)

100%

GARTNER STEELAND GLASS GmbH

(Germany)

PERMASTEELISAIRELAND Ltd.

(Ireland)

100%

49%

5% 95%

49%

100%

100%

PERMASTEELISA NORTH AMERICA CORP.

(USA)

100%

100%

PERMASTEELISAGARTNER MIDDLE

EAST LLC(Dubai)

PERMASTEELISAGARTNER

QATAR LLC(Qatar)

PERMASTEELISA GARTNER

SAUDI ARABIA LLC(Saudi Arabia)

JOSEF GARTNER& Co. UK Ltd

(UK)

100%

100% 54,25%

45,27%

TOWERINSTALLATION LLC

(USA)

DONGGUANPERMASTEELISA

CURTAIN WALL Co. Ltd.(China)

GLOBAL WALL MALAYSIASdn. Bhd.(Malaysia)

JOSEF GARTNER& Co. HK Ltd.

(China)

JOSEF GARTNERCURTAIN WALL

(SHANGHAI) Co. Ltd.(China)

PERMASTEELISAPHILIPPINES INC.

(Philippines)

PERMASTEELISAJAPAN K.K.

(Japan)

PERMASTEELISA MACAU Limited

(Macau)

100%

70% 99,999%

99,99%

75%

100%

100%

PERMASTEELISA TAIWAN Ltd.

(Taiwan)

99,99%

JOSEF GARTNER(MACAU) LIMITED

(Macau)

96%

GARTNER CONTRACTINGCo. Limited

(China)

PERMASTEELISA PTY Ltd.

(Australia)

PERMASTEELISA HONG KONG Ltd.

(China)

PERMASTEELISA (INDIA) Private Limited

(India)

GLOBAL ARCHITECTURALCo. Ltd.

(Thailand)

54,17%

45,83%

76%

100%

100% 99%

0,2%

99,8%

100%

100%

BLEU TECH MONT.Inc.

(Canada)

PERMASTEELISA FRANCE S.a.s.

(France)

PERMASTEELISA ESPANA S.a.u.

(Spain)

JOSEF GARTNER CURTAIN WALL

(SUZHOU) Co. Ltd (China)

100%

100%

0,001%

100%

JOSEF GARTNER GmbH

(Germany)

PERMASTEELISA S.p.A.(ITALY)

SCHELDEBOUW B.V.(The Nederlands)

Group Structure

10

Ph.

: Ste

phan

Lie

bl

11

12

Management Report

Dear Shareholders,this is the report to the Consolidated Financial Statements and to the Statutory Financial Statements of Permasteelisa S.p.A. for the year ended 31 December 2011.

The purpose of this report is to provide you with an overview of the Parent Company and the Group’s operations in reference to the year which has just ended, in addition to its future prospects. The notes to the Consolidated Financial Statements and to the Statutory Financial Statements will provide you with any additional information you may require on the numerical data supplied in the statement of financial position, the income statement, the statement of cash flows and the statement of net equity changes.

At the end of the year the Company was acquired by JS Group Corporation, a Japanese company listed on the Tokyo Stock Exchange: the transaction took place on 6 December 2011 by cash without any process of “Leverage Buy Out”, after six months of negotiation and the obtaining of the requested antitrust nulla-osta.

Management Report

2011ANNUALREPORT

13

Management Report

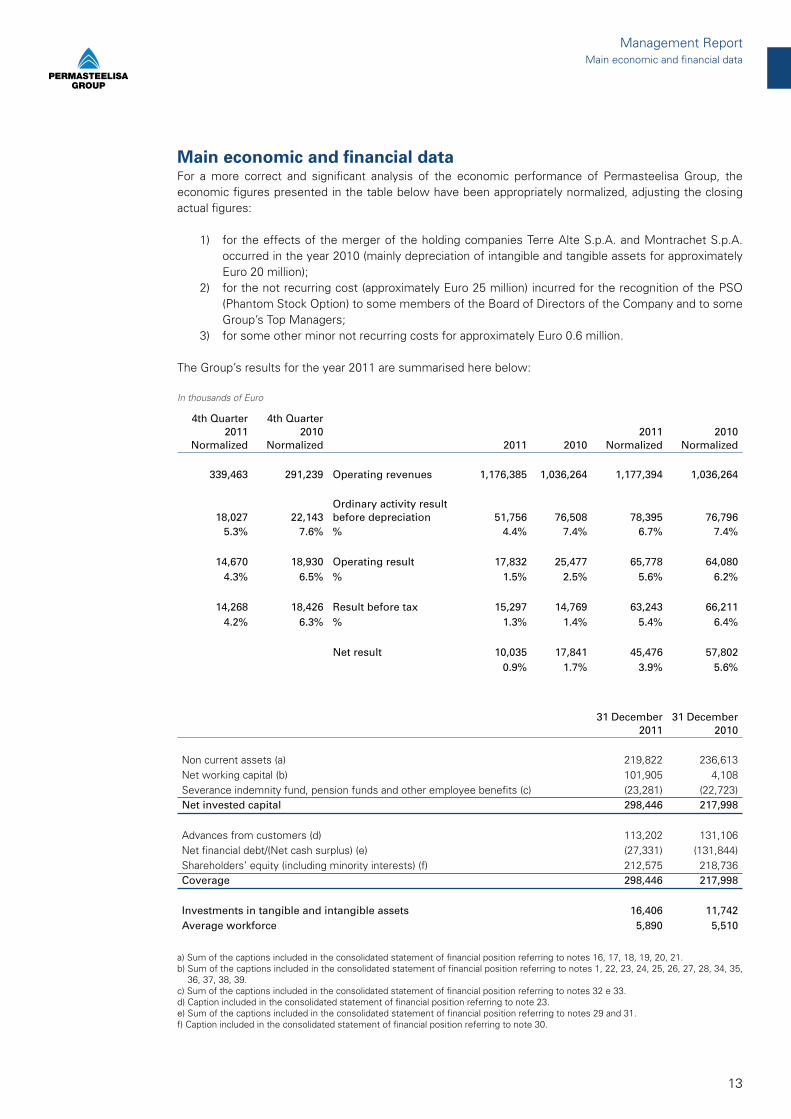

Main economic and financial dataFor a more correct and significant analysis of the economic performance of Permasteelisa Group, the economic figures presented in the table below have been appropriately normalized, adjusting the closing actual figures:

1) for the effects of the merger of the holding companies Terre Alte S.p.A. and Montrachet S.p.A. occurred in the year 2010 (mainly depreciation of intangible and tangible assets for approximately Euro 20 million);

2) for the not recurring cost (approximately Euro 25 million) incurred for the recognition of the PSO (Phantom Stock Option) to some members of the Board of Directors of the Company and to some Group’s Top Managers;

3) for some other minor not recurring costs for approximately Euro 0.6 million.

The Group’s results for the year 2011 are summarised here below:

In thousands of Euro

4th Quarter 2011

Normalized

4th Quarter 2010

Normalized 2011 20102011

Normalized2010

Normalized

339,463 291,239 Operating revenues 1,176,385 1,036,264 1,177,394 1,036,264

18,027 22,143Ordinary activity result before depreciation 51,756 76,508 78,395 76,796

5.3% 7.6% % 4.4% 7.4% 6.7% 7.4%

14,670 18,930 Operating result 17,832 25,477 65,778 64,0804.3% 6.5% % 1.5% 2.5% 5.6% 6.2%

14,268 18,426 Result before tax 15,297 14,769 63,243 66,2114.2% 6.3% % 1.3% 1.4% 5.4% 6.4%

Net result 10,035 17,841 45,476 57,8020.9% 1.7% 3.9% 5.6%

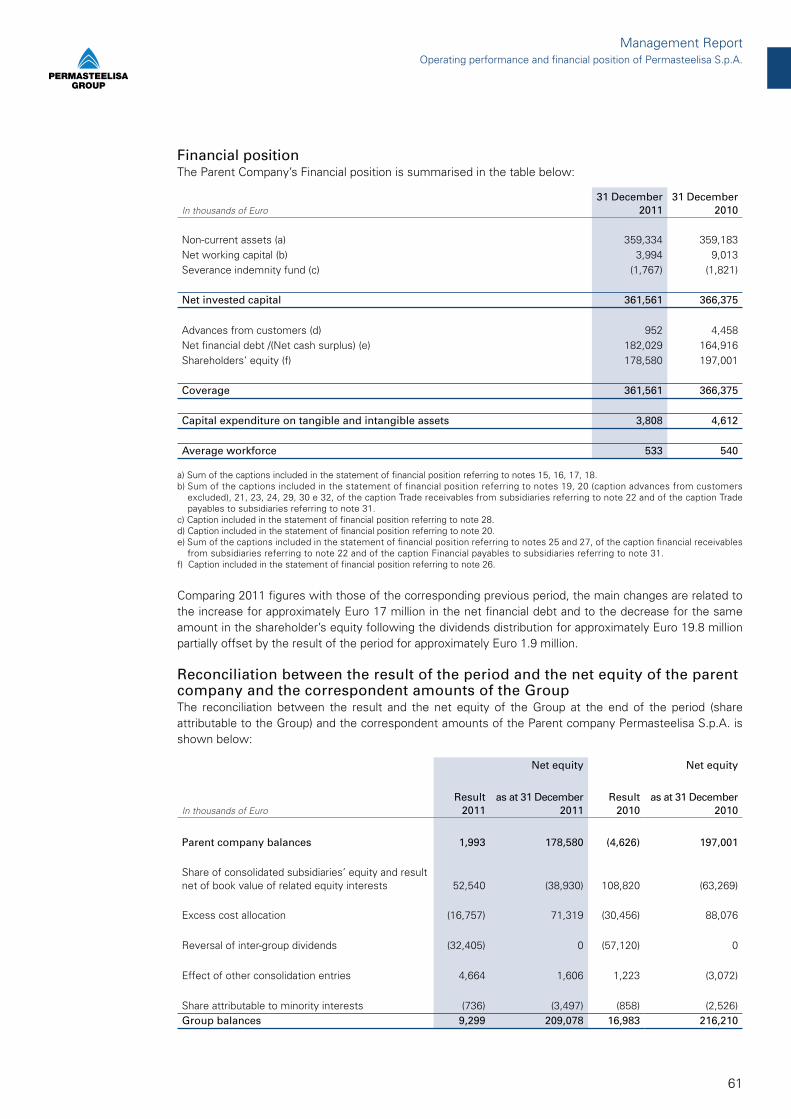

31 December 2011

31 December 2010

Non current assets (a) 219,822 236,613Net working capital (b) 101,905 4,108Severance indemnity fund, pension funds and other employee benefits (c) (23,281) (22,723)Net invested capital 298,446 217,998

Advances from customers (d) 113,202 131,106Net financial debt/(Net cash surplus) (e) (27,331) (131,844)Shareholders’ equity (including minority interests) (f) 212,575 218,736Coverage 298,446 217,998

Investments in tangible and intangible assets 16,406 11,742Average workforce 5,890 5,510

a) Sum of the captions included in the consolidated statement of financial position referring to notes 16, 17, 18, 19, 20, 21.b) Sum of the captions included in the consolidated statement of financial position referring to notes 1, 22, 23, 24, 25, 26, 27, 28, 34, 35, 36, 37, 38, 39. c) Sum of the captions included in the consolidated statement of financial position referring to notes 32 e 33.d) Caption included in the consolidated statement of financial position referring to note 23.e) Sum of the captions included in the consolidated statement of financial position referring to notes 29 and 31.f) Caption included in the consolidated statement of financial position referring to note 30.

Main economic and financial data

14

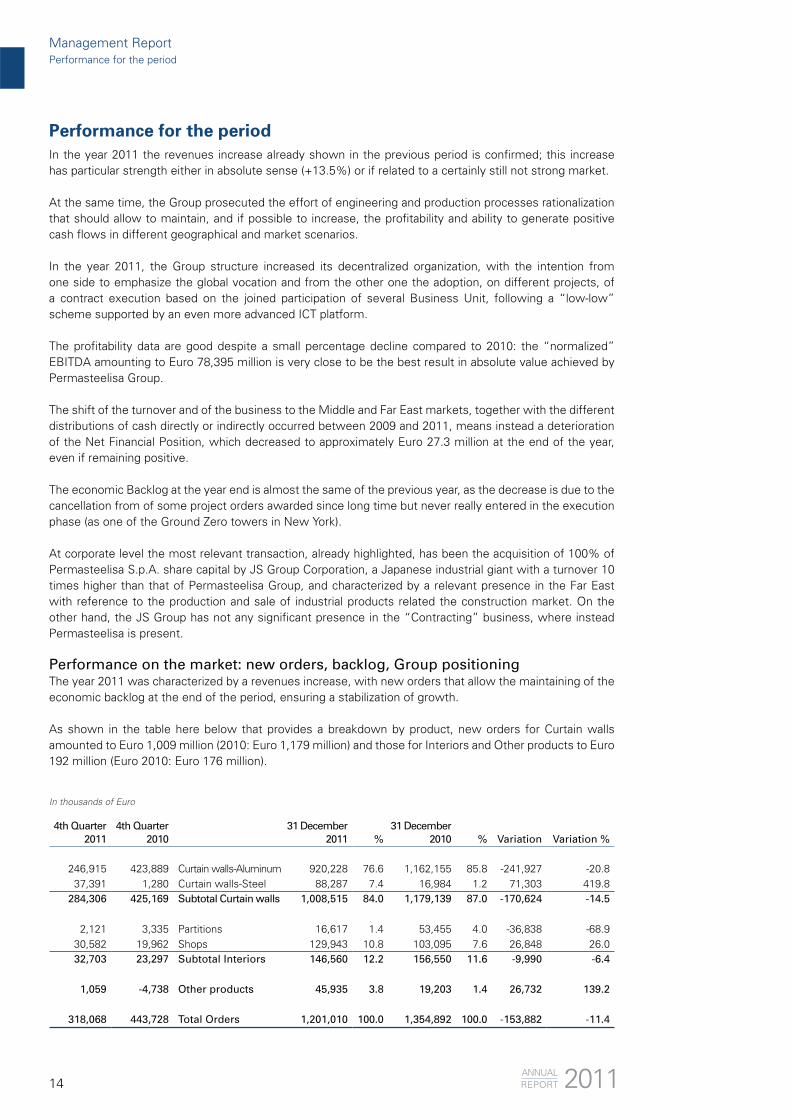

In the year 2011 the revenues increase already shown in the previous period is confirmed; this increase has particular strength either in absolute sense (+13.5%) or if related to a certainly still not strong market.

At the same time, the Group prosecuted the effort of engineering and production processes rationalization that should allow to maintain, and if possible to increase, the profitability and ability to generate positive cash flows in different geographical and market scenarios.

In the year 2011, the Group structure increased its decentralized organization, with the intention from one side to emphasize the global vocation and from the other one the adoption, on different projects, of a contract execution based on the joined participation of several Business Unit, following a “low-low” scheme supported by an even more advanced ICT platform.

The profitability data are good despite a small percentage decline compared to 2010: the “normalized” EBITDA amounting to Euro 78,395 million is very close to be the best result in absolute value achieved by Permasteelisa Group.

The shift of the turnover and of the business to the Middle and Far East markets, together with the different distributions of cash directly or indirectly occurred between 2009 and 2011, means instead a deterioration of the Net Financial Position, which decreased to approximately Euro 27.3 million at the end of the year, even if remaining positive.

The economic Backlog at the year end is almost the same of the previous year, as the decrease is due to the cancellation from of some project orders awarded since long time but never really entered in the execution phase (as one of the Ground Zero towers in New York).

At corporate level the most relevant transaction, already highlighted, has been the acquisition of 100% of Permasteelisa S.p.A. share capital by JS Group Corporation, a Japanese industrial giant with a turnover 10 times higher than that of Permasteelisa Group, and characterized by a relevant presence in the Far East with reference to the production and sale of industrial products related the construction market. On the other hand, the JS Group has not any significant presence in the “Contracting” business, where instead Permasteelisa is present.

Performance on the market: new orders, backlog, Group positioningThe year 2011 was characterized by a revenues increase, with new orders that allow the maintaining of the economic backlog at the end of the period, ensuring a stabilization of growth.

As shown in the table here below that provides a breakdown by product, new orders for Curtain walls amounted to Euro 1,009 million (2010: Euro 1,179 million) and those for Interiors and Other products to Euro 192 million (Euro 2010: Euro 176 million).

In thousands of Euro

4th Quarter2011

4th Quarter2010

31 December2011 %

31 December2010 % Variation Variation %

246,915 423,889 Curtain walls-Aluminum 920,228 76.6 1,162,155 85.8 -241,927 -20.837,391 1,280 Curtain walls-Steel 88,287 7.4 16,984 1.2 71,303 419.8

284,306 425,169 Subtotal Curtain walls 1,008,515 84.0 1,179,139 87.0 -170,624 -14.5

2,121 3,335 Partitions 16,617 1.4 53,455 4.0 -36,838 -68.930,582 19,962 Shops 129,943 10.8 103,095 7.6 26,848 26.032,703 23,297 Subtotal Interiors 146,560 12.2 156,550 11.6 -9,990 -6.4

1,059 -4,738 Other products 45,935 3.8 19,203 1.4 26,732 139.2

318,068 443,728 Total Orders 1,201,010 100.0 1,354,892 100.0 -153,882 -11.4

Performance for the period

Performance for the periodManagement Report

2011ANNUALREPORT

15

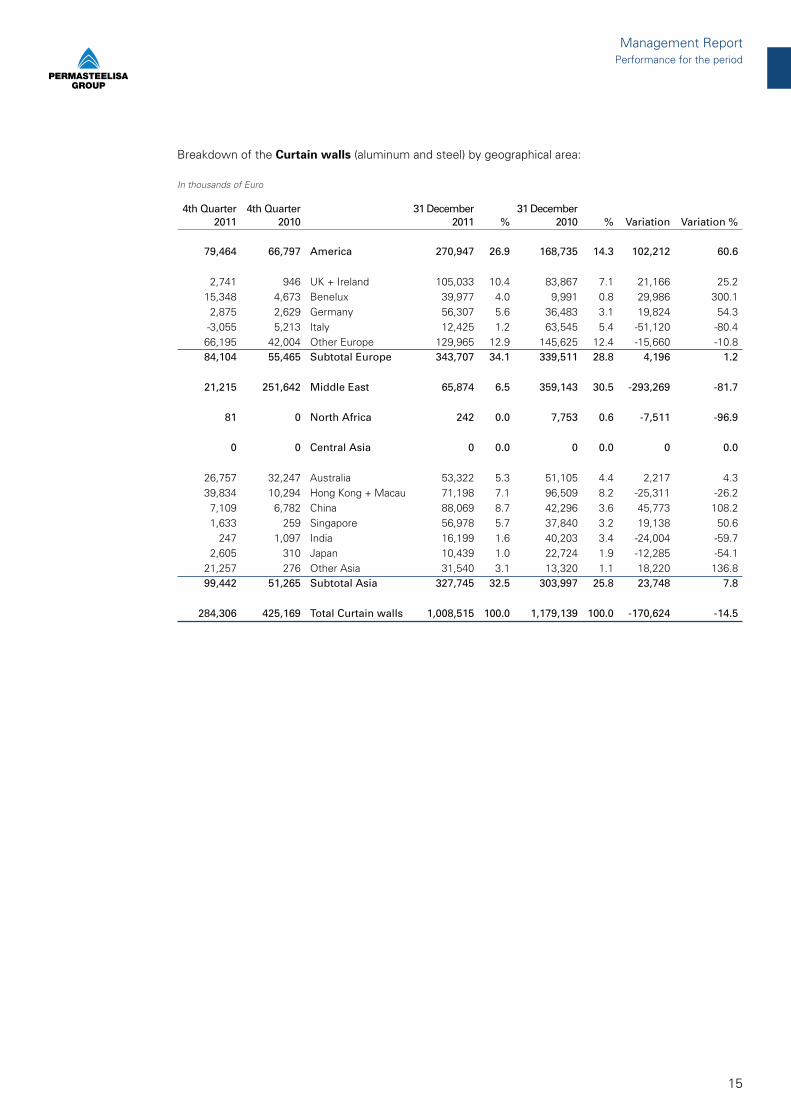

Breakdown of the Curtain walls (aluminum and steel) by geographical area:

In thousands of Euro

4th Quarter2011

4th Quarter2010

31 December2011 %

31 December2010 % Variation Variation %

79,464 66,797 America 270,947 26.9 168,735 14.3 102,212 60.6

2,741 946 UK + Ireland 105,033 10.4 83,867 7.1 21,166 25.215,348 4,673 Benelux 39,977 4.0 9,991 0.8 29,986 300.12,875 2,629 Germany 56,307 5.6 36,483 3.1 19,824 54.3-3,055 5,213 Italy 12,425 1.2 63,545 5.4 -51,120 -80.466,195 42,004 Other Europe 129,965 12.9 145,625 12.4 -15,660 -10.884,104 55,465 Subtotal Europe 343,707 34.1 339,511 28.8 4,196 1.2

21,215 251,642 Middle East 65,874 6.5 359,143 30.5 -293,269 -81.7

81 0 North Africa 242 0.0 7,753 0.6 -7,511 -96.9

0 0 Central Asia 0 0.0 0 0.0 0 0.0

26,757 32,247 Australia 53,322 5.3 51,105 4.4 2,217 4.339,834 10,294 Hong Kong + Macau 71,198 7.1 96,509 8.2 -25,311 -26.27,109 6,782 China 88,069 8.7 42,296 3.6 45,773 108.21,633 259 Singapore 56,978 5.7 37,840 3.2 19,138 50.6

247 1,097 India 16,199 1.6 40,203 3.4 -24,004 -59.72,605 310 Japan 10,439 1.0 22,724 1.9 -12,285 -54.1

21,257 276 Other Asia 31,540 3.1 13,320 1.1 18,220 136.899,442 51,265 Subtotal Asia 327,745 32.5 303,997 25.8 23,748 7.8

284,306 425,169 Total Curtain walls 1,008,515 100.0 1,179,139 100.0 -170,624 -14.5

Performance for the periodManagement Report

16

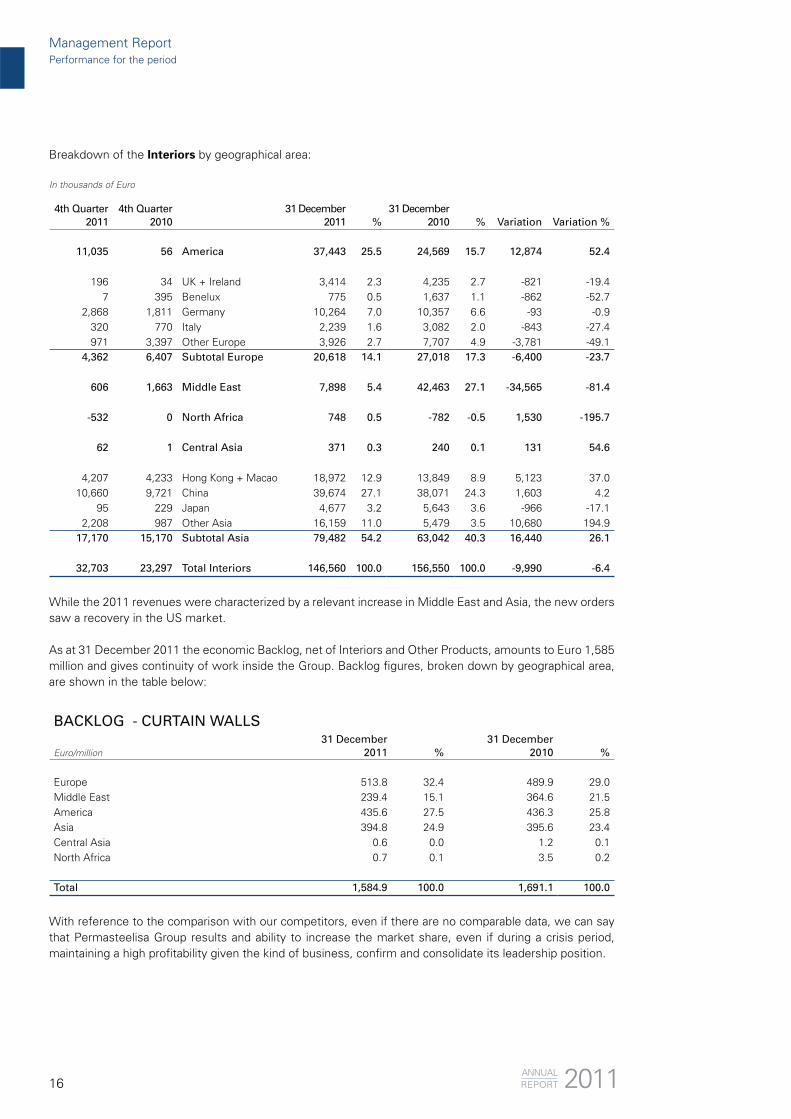

Breakdown of the Interiors by geographical area:

In thousands of Euro

4th Quarter2011

4th Quarter2010

31 December2011 %

31 December2010 % Variation Variation %

11,035 56 America 37,443 25.5 24,569 15.7 12,874 52.4

196 34 UK + Ireland 3,414 2.3 4,235 2.7 -821 -19.47 395 Benelux 775 0.5 1,637 1.1 -862 -52.7

2,868 1,811 Germany 10,264 7.0 10,357 6.6 -93 -0.9320 770 Italy 2,239 1.6 3,082 2.0 -843 -27.4971 3,397 Other Europe 3,926 2.7 7,707 4.9 -3,781 -49.1

4,362 6,407 Subtotal Europe 20,618 14.1 27,018 17.3 -6,400 -23.7

606 1,663 Middle East 7,898 5.4 42,463 27.1 -34,565 -81.4

-532 0 North Africa 748 0.5 -782 -0.5 1,530 -195.7

62 1 Central Asia 371 0.3 240 0.1 131 54.6

4,207 4,233 Hong Kong + Macao 18,972 12.9 13,849 8.9 5,123 37.010,660 9,721 China 39,674 27.1 38,071 24.3 1,603 4.2

95 229 Japan 4,677 3.2 5,643 3.6 -966 -17.12,208 987 Other Asia 16,159 11.0 5,479 3.5 10,680 194.9

17,170 15,170 Subtotal Asia 79,482 54.2 63,042 40.3 16,440 26.1

32,703 23,297 Total Interiors 146,560 100.0 156,550 100.0 -9,990 -6.4

While the 2011 revenues were characterized by a relevant increase in Middle East and Asia, the new orders saw a recovery in the US market.

As at 31 December 2011 the economic Backlog, net of Interiors and Other Products, amounts to Euro 1,585 million and gives continuity of work inside the Group. Backlog figures, broken down by geographical area, are shown in the table below:

BACKLOG - CURTAIN WALLS

Euro/million31 December

2011 %31 December

2010 %

Europe 513.8 32.4 489.9 29.0 Middle East 239.4 15.1 364.6 21.5 America 435.6 27.5 436.3 25.8 Asia 394.8 24.9 395.6 23.4 Central Asia 0.6 0.0 1.2 0.1North Africa 0.7 0.1 3.5 0.2

Total 1,584.9 100.0 1,691.1 100.0

With reference to the comparison with our competitors, even if there are no comparable data, we can say that Permasteelisa Group results and ability to increase the market share, even if during a crisis period, maintaining a high profitability given the kind of business, confirm and consolidate its leadership position.

Management ReportPerformance for the period

2011ANNUALREPORT

17

Operating performance - Results

Operating revenuesA better understanding of the Group’s business trend is provided in the table below, where the operating revenues are broken down by type of product and geographical area compared to 2010.In 2011 operating revenues amounted to Euro 1,176,385 thousand, with an increase of 13.5% compared to the previous year (Euro 1,036,264 thousand).

Operating revenues broken down by product are shown below:

In thousands of Euro

4th Quarter2011

4th Quarter2010

31 December2011 %

31 December2010 % Variation Variation %

265,895 232,533 Curtain walls-Aluminum 955,317 81.2 855,451 82.6 99,866 11.719,465 9,378 Curtain walls-Steel 46,734 4.0 23,858 2.3 22,876 95.9

285,360 241,911 Subtotal Curtain walls 1,002,051 85.2 879,309 84.9 122,742 14.0

10,296 8,156 Partitions 43,507 3.7 25,827 2.5 17,680 68.535,789 33,810 Shops 115,625 9.8 108,876 10.5 6,749 6.246,085 41,966 Subtotal Interiors 159,132 13.5 134,703 13.0 24,429 18.1

8,018 7,361 Other products 15,202 1.3 22,252 2.1 -7,050 -31.7

339,463 291,238 Total Operating Revenues 1,176,385 100.0 1,036,264 100.0 140,121 13.5

Breakdown of the Curtain walls (aluminum and steel) by geographical area:

In thousands of Euro

4th Quarter2011

4th Quarter2010

31 December2011 %

31 December2010 % Variation Variation %

51,672 35,184 America 162,199 16.2 131,806 15.0 30,393 23.1

19,639 44,479 UK + Ireland 100,354 10.0 172,887 19.7 -72,533 -42.07,107 7,961 Benelux 29,210 2.9 40,596 4.6 -11,386 -28.0

13,033 14,080 Germany 53,408 5.3 66,389 7.6 -12,981 -19.613,684 11,661 Italy 58,857 5.9 40,680 4.6 18,177 44.725,107 13,616 Other Europe 82,873 8.3 47,719 5.4 35,154 73.778,570 91,797 Subtotal Europe 324,702 32.4 368,271 41.9 -43,569 -11.8

61,448 34,963 Middle East 164,229 16.4 96,682 11.0 67,547 69.9

514 2,112 North Africa 3,106 0.3 4,222 0.5 -1,116 -26.4

47 366 Central Asia 484 0.0 5,986 0.7 -5,502 -91.9

15,866 5,733 Australia 52,774 5.3 33,591 3.8 19,183 57.127,951 23,781 Hong Kong + Macao 94,971 9.5 73,338 8.3 21,633 29.514,265 7,702 China 38,578 3.8 35,187 4.0 3,391 9.619,706 16,253 Singapore 72,971 7.3 58,679 6.7 14,292 24.44,859 8,680 India 28,600 2.9 30,121 3.4 -1,521 -5.08,385 10,022 Japan 51,878 5.2 29,268 3.3 22,610 77.32,077 5,318 Other Asia 7,559 0.7 12,158 1.4 -4,599 -37.8

93,109 77,489 Subtotal Asia 347,331 34.7 272,342 30.9 74,989 27.5

285,360 241,911 Total Curtain Wall 1,002,051 100.0 879,309 100.0 122,742 14.0

Management ReportPerformance for the period

18

Breakdown of the Interiors by geographical area:

In thousands of Euro

4th Quarter2011

4th Quarter2010

31 December2011 %

31 December2010 % Variation Variation %

8,602 10,254 America 34,382 21.6 34,881 25.9 -499 -1.4

1,572 792 UK + Ireland 4,268 2.7 3,977 2.9 291 7.376 655 Benelux 875 0.5 1,434 1.1 -559 -39.0

2,329 3,934 Italy 12,263 7.7 12,641 9.4 -378 -3.0472 1,237 France 2,407 1.5 6,891 5.1 -4,484 -65.1

1,388 4,454 Other Europe 3,786 2.4 11,276 8.4 -7,490 -66.45,837 11,072 Subtotal Europe 23,599 14.8 36,219 26.9 -12,620 -34.8

7,059 2,773 Middle East 30,611 19.2 4,181 3.1 26,430 632.1

19 850 North Africa 598 0.4 2,249 1.7 -1,651 -73.4

281 -8 Central Asia 345 0.2 239 0.2 106 44.4

4,125 3,587 Hong Kong + Macau 13,730 8.6 9,074 6.7 4,656 51.313,582 10,003 China 37,647 23.7 37,338 27.7 309 0.82,332 1,750 Japan 6,027 3.8 4,798 3.6 1,229 25.64,248 1,685 Other Asia 12,193 7.7 5,724 4.2 6,469 113.0

24,287 17,025 Subtotal Asia 69,597 43.8 56,934 42.2 12,663 22.2

46,085 41,966 Total Interiors 159,132 100.0 134,703 100.0 24,429 18.1

ProfitabilityThe normalized data of year 2011 show an EBITDA of Euro 78.4 million (2010: Euro 76.8 million), that corresponds to 6.7% of operating revenues (2010: 7.4%), and a EBIT of Euro 65.8 million (2010: Euro 64 million), that corresponds to 5.6% of operating revenues (2010: 6.2%): these values remain at excellent performance levels with respect to those achieved during the economic Turnaround of the 2007-2009 period.As already mentioned, the Group went through the construction world crisis with a strong resistance, showing a prompt repositioning capacity. Now there is a partial shift to Middle East and Asian markets, more competitive and less disposed to recognize significant “prizes” to the technical and technology quality of Permasteelisa: this means a small decrease of the margin in comparison with the moments of excellence, to which Permasteelisa has to react and is reacting with a refining of its internal processing to recover some percentage points on costs management.

Financial performance - ResultsThe consolidated non-current assets are equal to Euro 219,822 thousand (2010: Euro 236,613 thousand); the decrease of Euro 16,791 thousand compared to the closing figures of the previous year is mainly due to the depreciation of the intangible assets “Economic Backlog” and “Customer relationship” (approximately Euro 18 million) and of the higher value of some buildings and lands (approximately Euro 1 million) that arose from the allocation of the “excess cost” (approximately Euro 128.5 million) paid by Terre Alte S.p.A (subsequently merged into Permasteelisa S.p.A. during year 2010) for the acquisition of Permasteelisa Group.

The consolidated net working capital presents a positive value for approximately Euro 101,905 thousand (2010: Euro 4,108 thousand), showing an increase compared to the closing figure of the previous year due to the absorption of the operating working capital (i.e. the sum of the captions assets for contracts work-in-progress, inventories and trade receivables minus liabilities for contracts work-in-progress and

Management ReportPerformance for the period

2011ANNUALREPORT

19

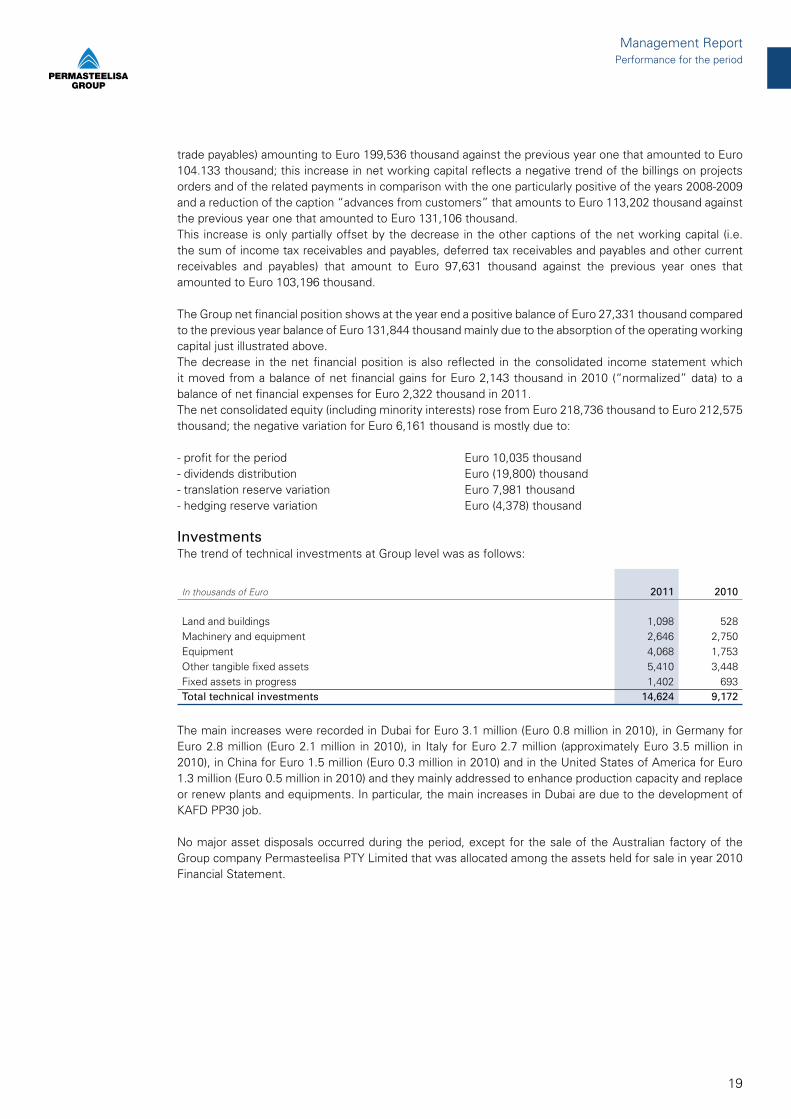

trade payables) amounting to Euro 199,536 thousand against the previous year one that amounted to Euro 104.133 thousand; this increase in net working capital reflects a negative trend of the billings on projects orders and of the related payments in comparison with the one particularly positive of the years 2008-2009 and a reduction of the caption “advances from customers” that amounts to Euro 113,202 thousand against the previous year one that amounted to Euro 131,106 thousand.This increase is only partially offset by the decrease in the other captions of the net working capital (i.e. the sum of income tax receivables and payables, deferred tax receivables and payables and other current receivables and payables) that amount to Euro 97,631 thousand against the previous year ones that amounted to Euro 103,196 thousand.

The Group net financial position shows at the year end a positive balance of Euro 27,331 thousand compared to the previous year balance of Euro 131,844 thousand mainly due to the absorption of the operating working capital just illustrated above.The decrease in the net financial position is also reflected in the consolidated income statement which it moved from a balance of net financial gains for Euro 2,143 thousand in 2010 (“normalized” data) to a balance of net financial expenses for Euro 2,322 thousand in 2011.The net consolidated equity (including minority interests) rose from Euro 218,736 thousand to Euro 212,575 thousand; the negative variation for Euro 6,161 thousand is mostly due to:

- profit for the period Euro 10,035 thousand- dividends distribution Euro (19,800) thousand- translation reserve variation Euro 7,981 thousand- hedging reserve variation Euro (4,378) thousand

InvestmentsThe trend of technical investments at Group level was as follows:

In thousands of Euro 2011 2010

Land and buildings 1,098 528Machinery and equipment 2,646 2,750Equipment 4,068 1,753Other tangible fixed assets 5,410 3,448Fixed assets in progress 1,402 693Total technical investments 14,624 9,172

The main increases were recorded in Dubai for Euro 3.1 million (Euro 0.8 million in 2010), in Germany for Euro 2.8 million (Euro 2.1 million in 2010), in Italy for Euro 2.7 million (approximately Euro 3.5 million in 2010), in China for Euro 1.5 million (Euro 0.3 million in 2010) and in the United States of America for Euro 1.3 million (Euro 0.5 million in 2010) and they mainly addressed to enhance production capacity and replace or renew plants and equipments. In particular, the main increases in Dubai are due to the development of KAFD PP30 job.

No major asset disposals occurred during the period, except for the sale of the Australian factory of the Group company Permasteelisa PTY Limited that was allocated among the assets held for sale in year 2010 Financial Statement.

Management ReportPerformance for the period

20

Manchester Metropolitan University Business School (MMUBS)Manchester \ UK

Ph.

: And

rew

Prie

st P

hoto

grap

hy

21

Overview of ongoing projects and main project acquisitions

Overview of ongoing projects and main project acquisitions

Permasteelisa Group’s main ongoing projects for 2011 have been broken into the Group’s two reference sectors:

\ Curtain walls\ Interiors

CURTAIN WALLS

Projects are broken down into three areas:

\\ Main project acquisitions \\ Main ongoing projects \\ Main completed projects

within each area the projects are listed per Business Unit/Product line.

\\ Main project acquisitions for 2011Below are the main projects awarded by the Permasteelisa Group in 2011.

\\\ Business Unit North America

3 World Trade Center

New York, NY \ USA

Project awarded by Permasteelisa North America Corp and designed by architects Rogers Stirk Harbour + Partners in collaboration with Adamson Associates.

The building of approximately 93,600 square meters of curtain walls will be used as commercial offi ces and will be completed during 2014.

Ph.

: Silv

erst

ein

Pro

pert

ies

Inc.

Ph.

: Silv

erst

ein

Pro

pert

ies

Inc.

Management Report

22

\\\ Business Unit Europe

Management ReportOverview of ongoing projects and main project acquisitions

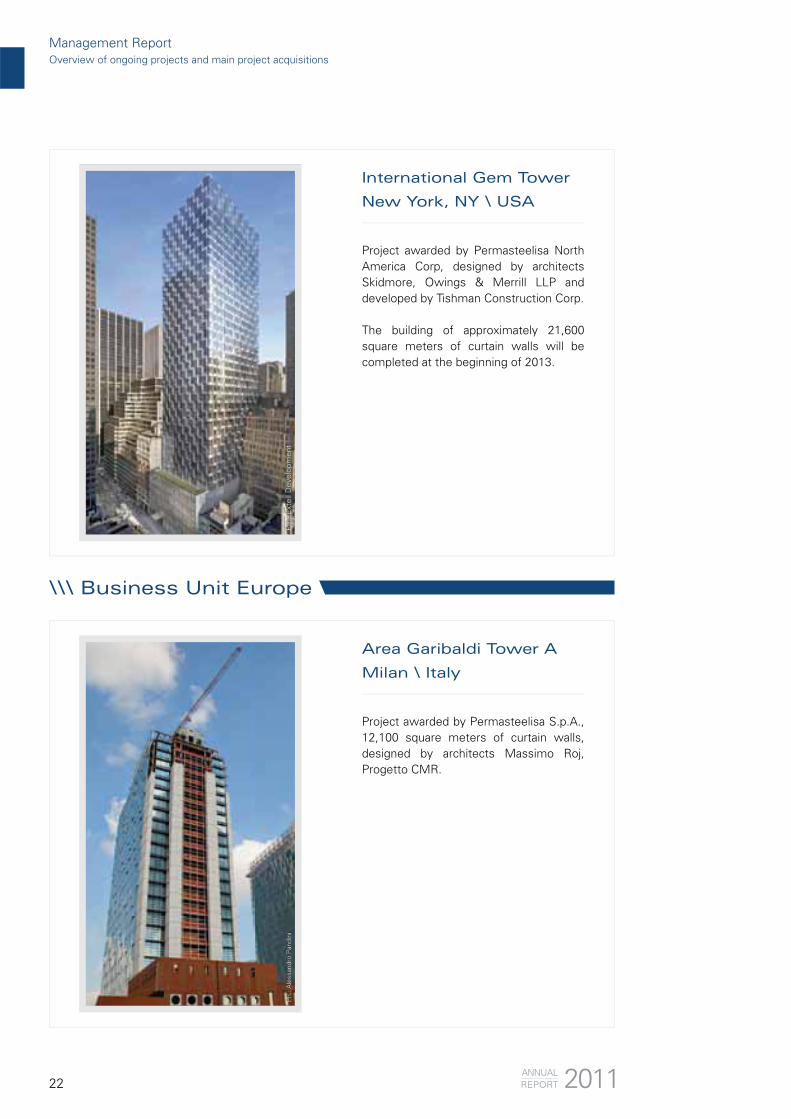

International Gem Tower

New York, NY \ USA

Project awarded by Permasteelisa North America Corp, designed by architects Skidmore, Owings & Merrill LLP and developed by Tishman Construction Corp.

The building of approximately 21,600 square meters of curtain walls will be completed at the beginning of 2013.

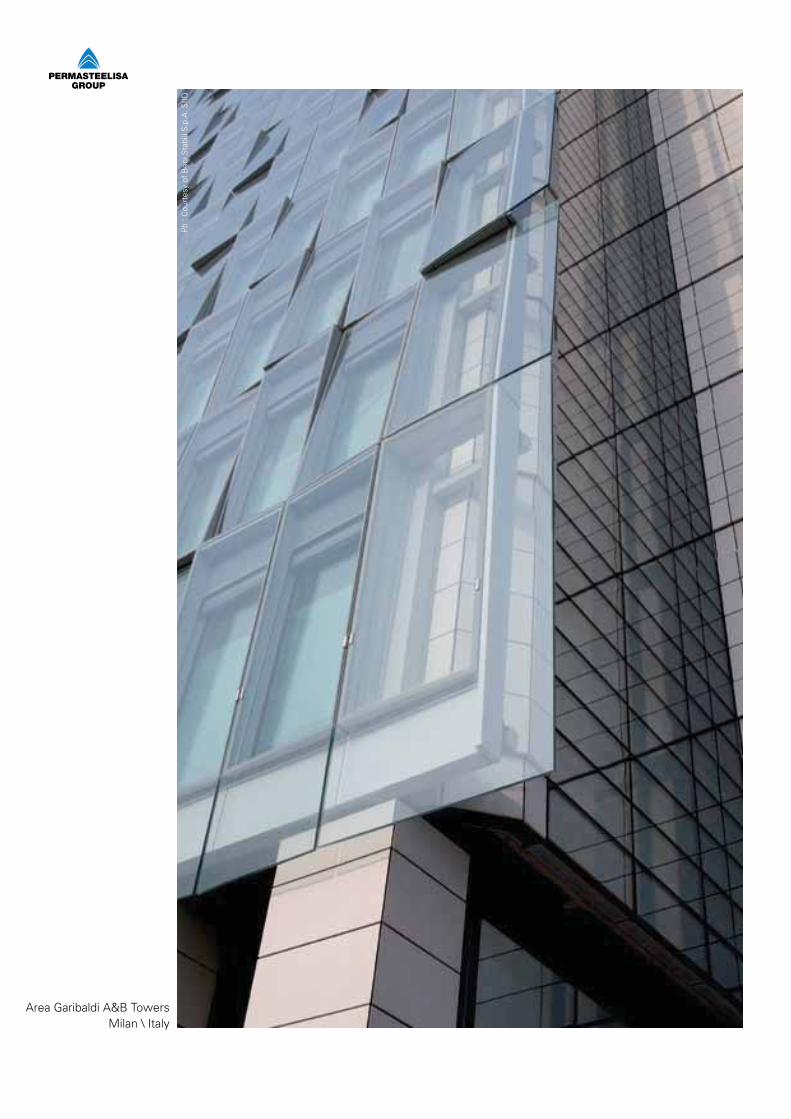

Area Garibaldi Tower A

Milan \ Italy

Project awarded by Permasteelisa S.p.A., 12,100 square meters of curtain walls, designed by architects Massimo Roj, Progetto CMR.

Ph.

: Ext

ell D

evel

opm

ent

Ph.

: Ale

ssan

dro

Pan

dini

Ph.

: Ext

ell D

evel

opm

ent

Ph.

: Ale

ssan

dro

Pan

dini

2011ANNUALREPORT

23

The New Karolinska

Solna University Hospital

Solna, Stockholm \ Sweden

Project awarded by Scheldebow B.V., 70,400 square meters of curtain walls with double and triple glazed, designed by architects White Tengbom Team.

The project will be completed within the end of 2014.

Nouveau Centre

de Congrés de Nancy

Nancy \ France

Project awarded by Permasteelisa France S.a.s. and developed with Permasteelisa S.p.A., 11,100 square meters of curtain walls, designed by architects Atelier Marc Barani. The project refers to the restore and the expansion of an existing building. The project will be completed within the end of 2013.

Ph.

: Whi

teTe

ngbo

mTe

amP

h.: A

RTE

FAC

TOR

YP

h.: W

hite

Teng

bom

Team

Ph.

: AR

TEFA

CTO

RY

Overview of ongoing projects and main project acquisitionsManagement Report

24

\\\ Business Unit Middle East

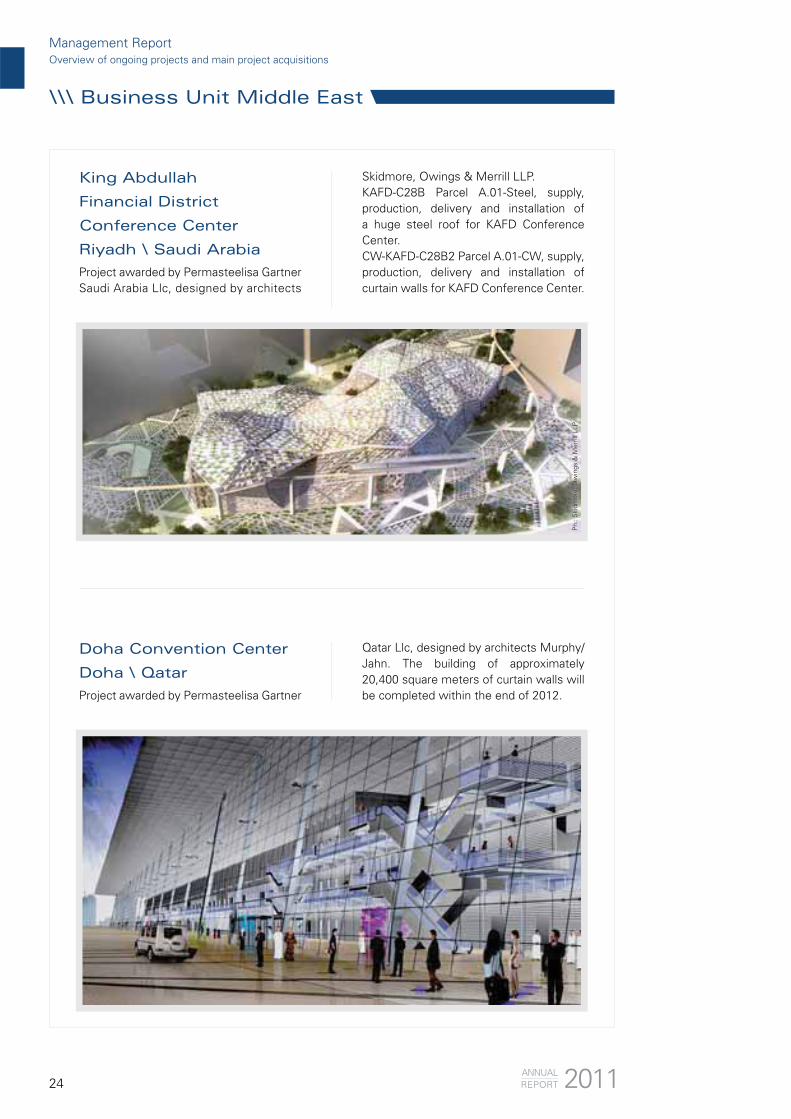

King Abdullah

Financial District

Conference Center

Riyadh \ Saudi Arabia

Doha Convention Center

Doha \ Qatar

Skidmore, Owings & Merrill LLP.KAFD-C28B Parcel A.01-Steel, supply, production, delivery and installation of a huge steel roof for KAFD Conference Center.CW-KAFD-C28B2 Parcel A.01-CW, supply, production, delivery and installation of curtain walls for KAFD Conference Center.

Qatar Llc, designed by architects Murphy/Jahn. The building of approximately 20,400 square meters of curtain walls will be completed within the end of 2012.Project awarded by Permasteelisa Gartner

Project awarded by Permasteelisa Gartner Saudi Arabia Llc, designed by architects

Ph.

: Ski

dmor

e, O

win

gs &

Mer

rill L

LPP

h.: S

kidm

ore,

Ow

ings

& M

erril

l LLP

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

25

\\\ Product Line Gartner

LEO

Frankfurt \ Germany

30,000 square meters of curtain walls, designed by architects schneider+schumacher.Owner: Deka Immobilien Investment.Project awarded by Josef Gartner GmbH,

Building 1 Roche

Basel \ Switzerland

Project awarded by Josef Gartner GmbH, 33.200 square meters of curtain walls, designed by architects Herzog & de Meuron.

Ph.

: Cop

yrig

ht ©

F. H

offm

ann-

La R

oche

Ltd

.P

h.: D

eka

Imm

obili

en In

vest

men

t G

mbH

Ph.

: Dek

a Im

mob

ilien

Inve

stm

ent

Gm

bHP

h.: C

opyr

ight

© F

. Hof

fman

n-La

Roc

he L

td.

Overview of ongoing projects and main project acquisitionsManagement Report

26

Hai Xia Exchange Centre

Xiamen \ P. R. of China

Project awarded by Josef Gartner Curtain Wall (Shanghai) Co. Ltd., 64,000 square meters of curtain walls, designed by architects Gravity Partnership Ltd. The project is expected to be completed within May 2012.

Ph.

: gra

vity

par

tner

ship

ltd

Pazhou Hotel

and Mix-used Development

Guangzhou \ P. R. of China

Project awarded by Josef Gartner Curtain Wall (Shanghai) Co. Ltd., 71,000 square meters of curtain walls, designed by architects Aedas. The building will be used for show, offi ces and hotel. The project is expected to be completed within the end of 2012.

Ph.

: Im

age

Cou

rtes

y of

Aed

as A

rchi

tect

s Li

mite

dP

h.: I

mag

e C

ourt

esy

of A

edas

Arc

hite

cts

Lim

ited

\\\ Business Unit Asia

Management ReportOverview of ongoing projects and main project acquisitions

2011ANNUALREPORT

27

8 Chifl ey Square

Sydney \ Australia

Project awarded by Permasteelisa PTY Limited, 9,200 square meters of curtain walls, designed by architects Rogers Stirk Harbour + Partners, Lippmann Associates in partnership with Mirvac Design.

The project is expected to be completed within the end of 2012.

\\ Main ongoing projects in 2011Permasteelisa Group’s main ongoing projects in 2011 are described below.

CUNY Advanced Science

Research Center

New York, NY \ USA

\\\ Business Unit North America

Project awarded by Permasteelisa North America Corp. and designed by architects Kohn Pedersen Fox Associates / Flad Architects. The building of 23,700 square meters of curtain walls will be completed within July 2012.

Ph.

: Mirv

acP

h.: M

irvac

Overview of ongoing projects and main project acquisitionsManagement Report

28

\\\ Business Unit Europe

ONE57 (Carnegie 57)

New York, NY \ USA

Project awarded by Permasteelisa North America Corp. and designed by architects Christian De Portzamparc in collaboration with SLCE Architects.

The building, of approximately 48,000 square meters of curtain walls, will be used for luxury residences and hotel.

Class Business Center

for Complex

Pushkinskiy LLC

Donetsk \ Ukraine

Project awarded by Permasteelisa S.p.A. and designed by architects Karl Schwitzke, Schwitzke & Partner.

The building, of approximately 18,300 square meters of curtain walls, will be completed within the fi rst six months of 2012.

Ren

derin

g: ©

John

Fot

iadi

s A

rchi

tect

/BB

Gro

upR

ende

ring:

©Jo

hn F

otia

dis

Arc

hite

ct/B

B G

roup

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

29

Nuovo Centro Direzionale

Intesa San Paolo

Turin \ Italy

Project awarded by Permasteelisa S.p.A. and designed by architects Renzo Building Workshop.

The building, of approximately 52,600 square meters of curtain walls, will be completed within the end of 2013.

Hospital de Móstoles

Madrid \ Spain

Project awarded by Permasteelisa España S.A.U. and designed by architects Rafael de la Hoz. The building consists in a total of 8,300 square meters of curtain walls.

Ph.

: Ren

zo P

iano

Bui

ldin

g W

orks

hop

Overview of ongoing projects and main project acquisitionsManagement Report

30

Musée du Louvre Lens

Lens \ France

Kazuyo Sejima + Ryue in collaboration with IMREY CULBERT/Catherine Mosbach, Extra Muros SA D’Architecture/Antoine Belin. The building consists in a total of 13,000 square meters of curtain walls.

Project awarded by Permasteelisa France S.a.s. and designed by architects SANAA,

King Abdullah Financial

District PP30

Riyadh \ Saudi Arabia

of 12 parcels of the King Abdullah Financial District, to be completed within the end of 2012. The project, developed by Saudi Binladin Group, involves several architectural offi ces, including Foster, Gensler, HLA, Perkins Will and consists in the supply and installation of curtain wall systems.

Project awarded by Permasteelisa Gartner Saudi Arabia Llc, consists in the execution

Ph.

: im

age

SA

NA

A ©

SA

NA

A/Im

rey

Cul

bert

/Cat

herin

e M

osba

chS

ourc

e: w

ww

.kin

gabd

ulla

hfin

anci

aldi

stric

t.co

mP

h.: i

mag

e S

AN

AA

©S

AN

AA

/Imre

y C

ulbe

rt/C

athe

rine

Mos

bach

Sou

rce:

ww

w.k

inga

bdul

lahf

inan

cial

dist

rict.

com

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

\\\ Business Unit Middle East

31

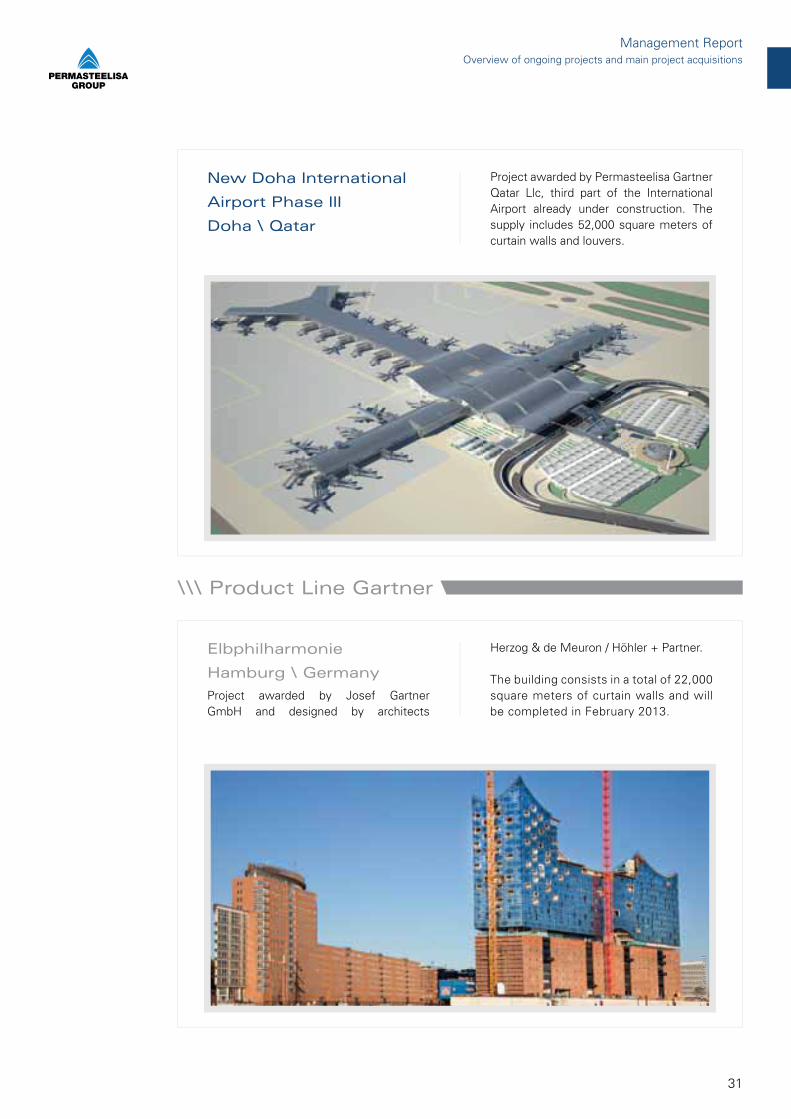

New Doha International

Airport Phase III

Doha \ Qatar

Project awarded by Permasteelisa Gartner Qatar Llc, third part of the International Airport already under construction. The supply includes 52,000 square meters of curtain walls and louvers.

\\\ Product Line Gartner

Elbphilharmonie

Hamburg \ Germany

Herzog & de Meuron / Höhler + Partner.

The building consists in a total of 22,000 square meters of curtain walls and will be completed in February 2013.

Ph.

: Kar

in J

obst

Ph.

: Kar

in J

obst

Overview of ongoing projects and main project acquisitionsManagement Report

Project awarded by Josef Gartner GmbH and designed by architects

32

\\\ Business Unit Asia

New Development

European Central Bank

Frankfurt \ Germany

Project awarded by Josef Gartner GmbH and designed by architects COOP HIMMELB(L)AU.

The supply consists in 30,000 square meters of curtain walls and steel. The building will be the new Head offi ce of the European Central Bank.

The project will be completed in September 2013.

Sathorn Square

Bangkok \ Thailand

Project awarded by Permasteelisa Projects (Thailand) Ltd. and Global Architectural Co. Ltd. and designed by architects P&T Group.

The building consists in a total of 49,800 square meters of curtain walls.

Ph.

: ©R

TTP

h.: ©

Krit

Mut

itaph

orn

Arc

hite

ctur

al P

hoto

grap

her

Ph.

: ©R

TTP

h.: ©

Krit

Mut

itaph

orn

Arc

hite

ctur

al P

hoto

grap

her

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

33

Hennessy Centre

Redevelopment-Podium

Hong Kong \ P. R. of China

Project awarded by Josef Gartner & Co. (HK) Ltd. and designed by architects Kohn Pedersen Fox Associates in collaboration with Dennis Lau & Ng Chun Man Architects & Engineers (H.K.) Ltd (DLN).

The building consists in a total of 10,500 square meters of curtain walls.

Overview of ongoing projects and main project acquisitionsManagement Report

Kerry Centre

(North Package)

Shanghai \ P. R. of China

Project awarded by Josef Gartner Curtain Wall (Shanghai) Co. Ltd. and designed by architects Kohn Pedersen Fox Associates. The building consists in a total of 60,000 square meters of surface and will be used as offi ces and shops. The project will be completed during 2012.

34

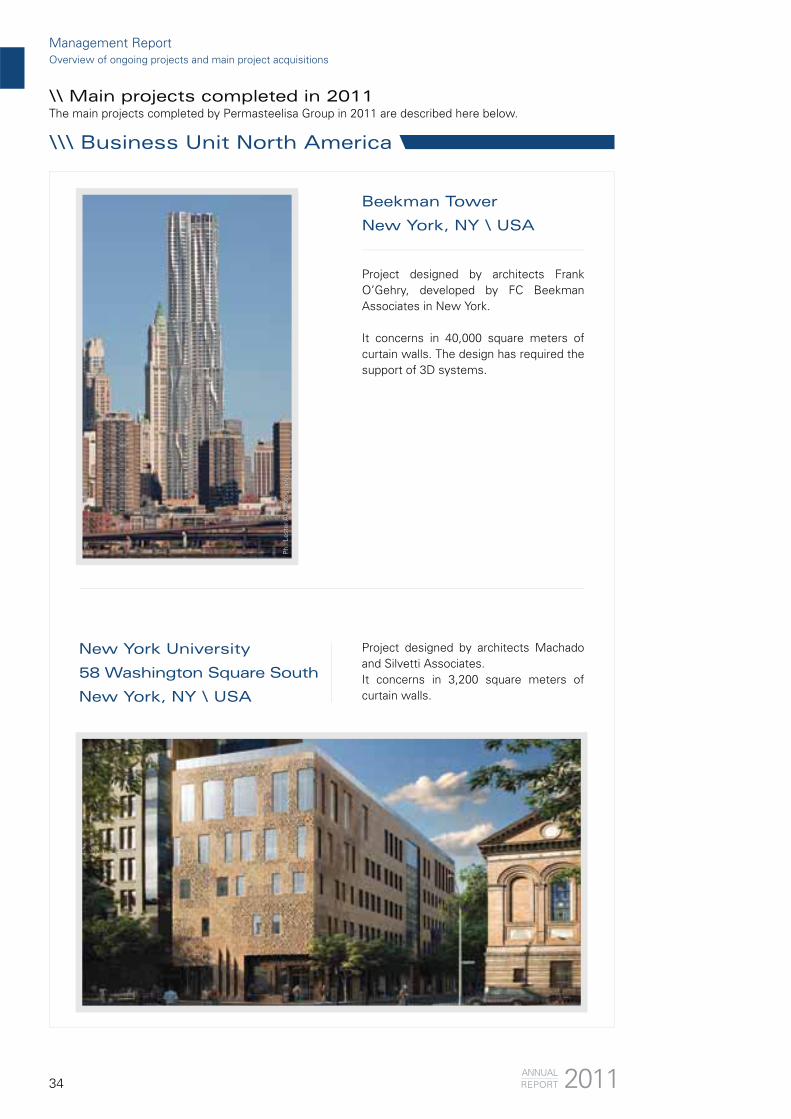

Beekman Tower

New York, NY \ USA

Project designed by architects Frank O’Gehry, developed by FC Beekman Associates in New York.

It concerns in 40,000 square meters of curtain walls. The design has required the support of 3D systems.

\\ Main projects completed in 2011The main projects completed by Permasteelisa Group in 2011 are described here below.

New York University

58 Washington Square South

New York, NY \ USA

Project designed by architects Machado and Silvetti Associates.It concerns in 3,200 square meters of curtain walls.

Ph.

: Les

ter

Ali

Pho

togr

aphy

Ph.

: Les

ter

Ali

Pho

togr

aphy

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

\\\ Business Unit North America

35

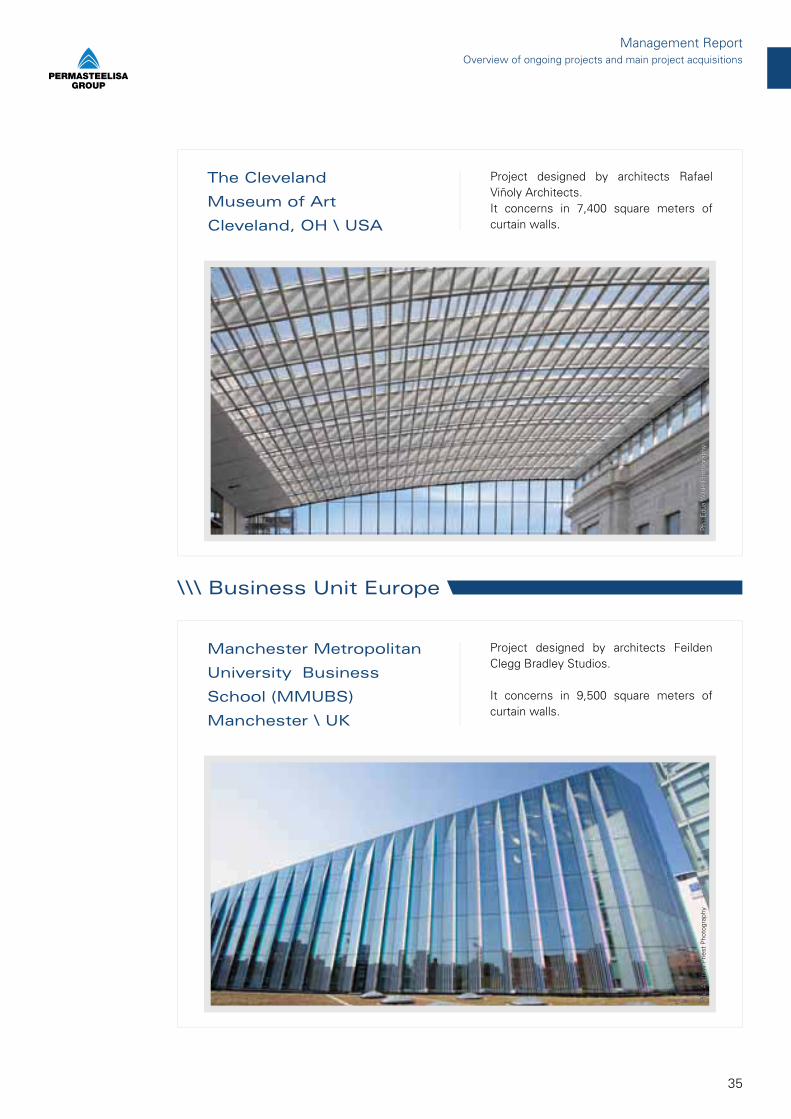

The Cleveland

Museum of Art

Cleveland, OH \ USA

Project designed by architects Rafael Viñoly Architects.It concerns in 7,400 square meters of curtain walls.

Ph.

: Edu

a W

ilde

Pho

togr

aphy

Ph.

: Edu

a W

ilde

Pho

togr

aphy

\\\ Business Unit Europe

Manchester Metropolitan

University Business

School (MMUBS)

Manchester \ UK

Project designed by architects Feilden Clegg Bradley Studios.

It concerns in 9,500 square meters of curtain walls.

Ph.

: And

rew

Prie

st P

hoto

grap

hyP

h.: A

ndre

w P

riest

Pho

togr

aphy

Overview of ongoing projects and main project acquisitionsManagement Report

36 2011

Rabobanktoren

Utrecht \ The Netherlands

Urbis, the project provided the supply of 20,000 square meters of curtain walls.

Project awarded by Scheldebouw B.V.

Baku Port

Baku \ Azerbaijan

Project awarded by Permasteelisa Gartner Dubai Llc and designed by architects Chapman Taylor.

The project provided the supply of 21,000 square meters of curtain walls for a tower of 32 fl oors used as offi ces and, in the penthouse area, as First Lady’s offi ces.

Ph.

: IM

RE

CS

AN

Y/M

embe

r of

Dut

ch A

rchi

tect

ural

Pho

togr

aphe

rs (D

AP

h)P

h.: I

MR

E C

SA

NY

/Mem

ber

of D

utch

Arc

hite

ctur

al P

hoto

grap

hers

(DA

Ph)

ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

\\\ Business Unit Middle East

37

Doha International

Airport Phase II

Doha \ Qatar

Project awarded by Permasteelisa Gartner Qatar Llc, second phase of the airport already under construction. The supply consists in approximately 35,000 square meters of curtain walls and louvers.

\\\ Product Line Gartner

Cannon Place

London \ UK

Project awarded at the end of 2008 after a PCSA phase (Pre Construction Service Agreement).

It consists in 14,500 square meters of curtain walls designed by architects FOGGO Associates of London.

Ph.

: Pho

togr

aphy

by

Sim

on K

enne

dyP

h.: P

hoto

grap

hy b

y S

imon

Ken

nedy

Overview of ongoing projects and main project acquisitionsManagement Report

38

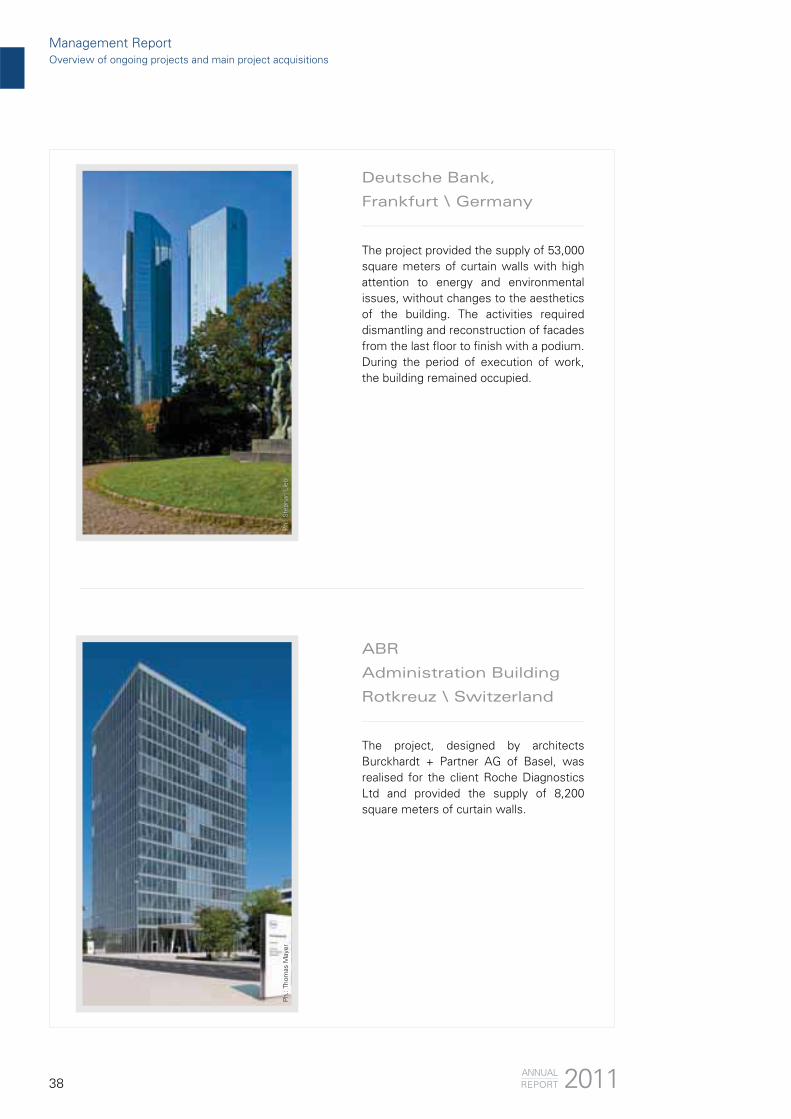

Deutsche Bank,

Frankfurt \ Germany

The project provided the supply of 53,000 square meters of curtain walls with high attention to energy and environmental issues, without changes to the aesthetics of the building. The activities required dismantling and reconstruction of facades from the last fl oor to fi nish with a podium. During the period of execution of work, the building remained occupied.

ABR

Administration Building

Rotkreuz \ Switzerland

The project, designed by architects Burckhardt + Partner AG of Basel, was realised for the client Roche Diagnostics Ltd and provided the supply of 8,200 square meters of curtain walls.

Ph.

: Ste

phan

Lie

blP

h.: S

teph

an L

iebl

Ph.

: Tho

mas

May

erP

h.: T

hom

as M

ayer

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

39

\\\ Business Unit Asia

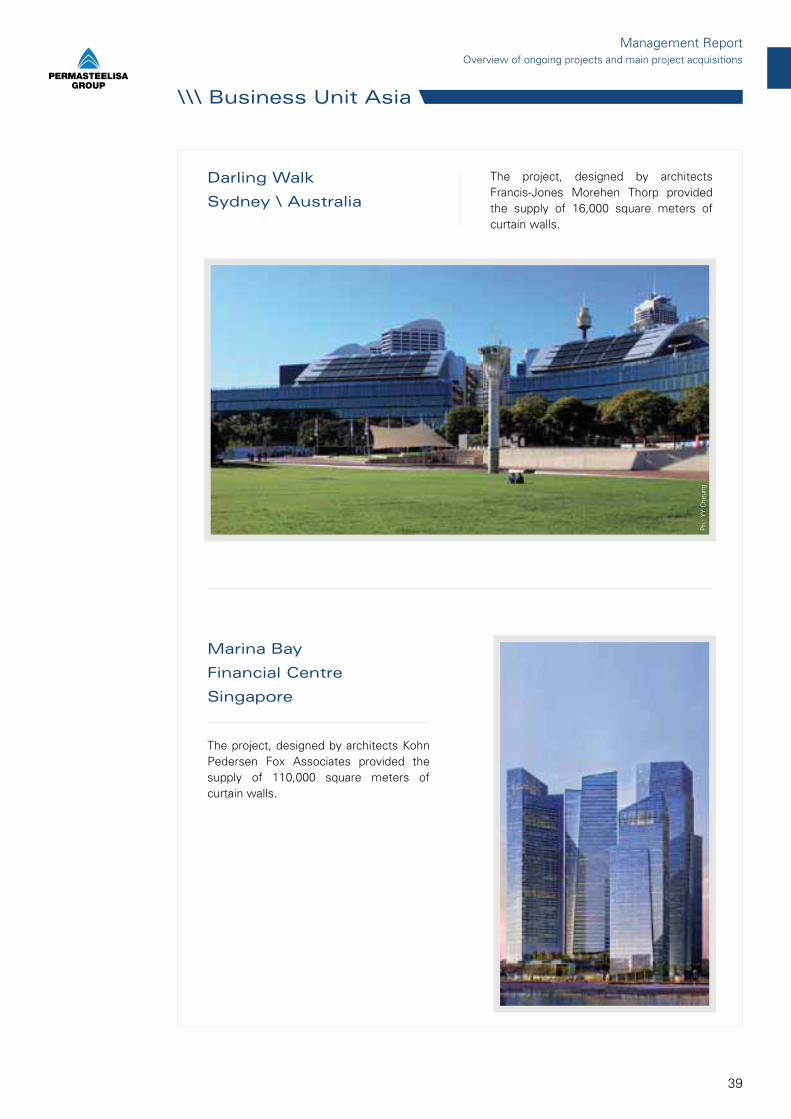

Darling Walk

Sydney \ Australia

The project, designed by architects Francis-Jones Morehen Thorp provided the supply of 16,000 square meters of curtain walls.

Ph.

: YY

Che

ung

Marina Bay

Financial Centre

Singapore

The project, designed by architects Kohn Pedersen Fox Associates provided the supply of 110,000 square meters of curtain walls.

Overview of ongoing projects and main project acquisitionsManagement Report

40

Tamar Development

Project

Hong Kong \ P. R. of China

The project, designed by architects Rocco Design Architects Ltd. provided the supply of 105,800 square meters of curtain walls.

Ph:

Stu

art

Woo

ds

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

41

The main project ongoing or completed in 2011 and involving the Interiors Business Unit are broken down into the following product lines:

\\ Partition/Glazed Metal Work\\ EPC (Engineering Procurement Contract)\\ Shops/Retail - Museum

\\\ Main projects acquisition for 2011 and still ongoing

\\ Partition/Glazed Metal Work

INTERIORS

Overview of ongoing projects and main project acquisitionsManagement Report

Santo Spirito Hospital,

Casale Monferrato

Alessandria \ Italy

Project awarded by Permasteelisa Interiors S.r.l. and designed by architects G Studio.

The project concerns the supply and installation of a raised fl oor and PVC coating, suspending ceiling, mobile partitions and doors for the realization of the surgical unit of the new hospital.

The partitions are self-supporting and practicable internally by the plants in order to minimize the interference. Materials are selected for their compatibility with the sterile environment.

42

Policlinico San Marco

Venice \ Italy

Project awarded by Permasteelisa Interiors S.r.l. and designed by architect Giulio Varini.

The project concerns the supply and installation of a raised fl oor and PVC coating, suspending ceiling, mobile partitions and doors for the realization of the surgical unit of the new hospital. The partitions are self-supporting and practicable internally by the plants in order to minimize the interference. Materials are selected for their compatibility with the sterile environment.

New Surgical Unit,

Conegliano Hospital

Treviso \ Italy

Project awarded by Trumpf Med Italia in September 2010 and developed with the cooperation of Permasteelisa Interiors S.r.l.Architect: Pool Engeneering S.p.A.General contractor: Opera - A.T.I. IMPRESE Carron S.p.A. and Gemmo S.p.A.Client: ULSS nr. 7 Pieve di Soligo (TV)The project concerns the supply of the following articles in the surgical unit of the new hospital (for the total of 9 surgery rooms):- REI and blind Fire Medical partitions,

glass windows complete with doors, REI and sliding doors for 5,000 square meters;

- suspended ceiling for 2,500 square meters;

- raised fl oor for 2,500 square meters.

\\\ Main projects completed in 2011

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

43

\\ EPC (Engineering Procurement Contract)

\\\ Partition Projects (USA)

Hotel Renaissance

Tlemcen \ Algeria

Supply and installation of fl oors, suspended ceiling, interior partitions, lights and furnishing supplies for suites and public areas (lobbies, restaurants, conference rooms, fi tness areas and disco).

GAP: supply of Fire offi ce partitions

Department of Health: supply and installation of Axis offi ce partitions

Analysis Group: supply of Axis offi ce partitions

Rice University: supply of Axis offi ce partitions

Symrise: supply and installation of Fire offi ce partitions

Overview of ongoing projects and main project acquisitionsManagement Report

44

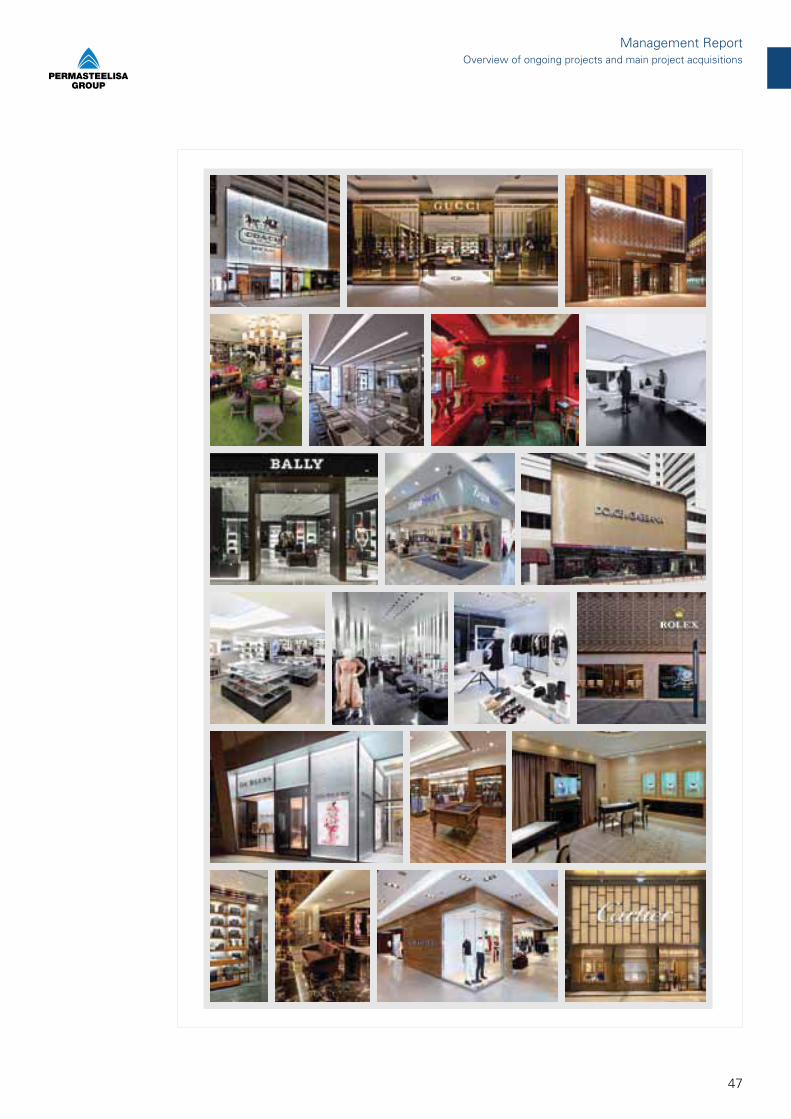

\\ Shops/Retail - Museum

The speciality area of the Shops/Retail division is to supply engineering, production and installation services for all furnishings required in a shop, to round off projects that involve the supply of indoor partitions or as stand-alone service offer. These are turnkey solutions that include anything from fl ooring, to lighting and refrigeration systems.

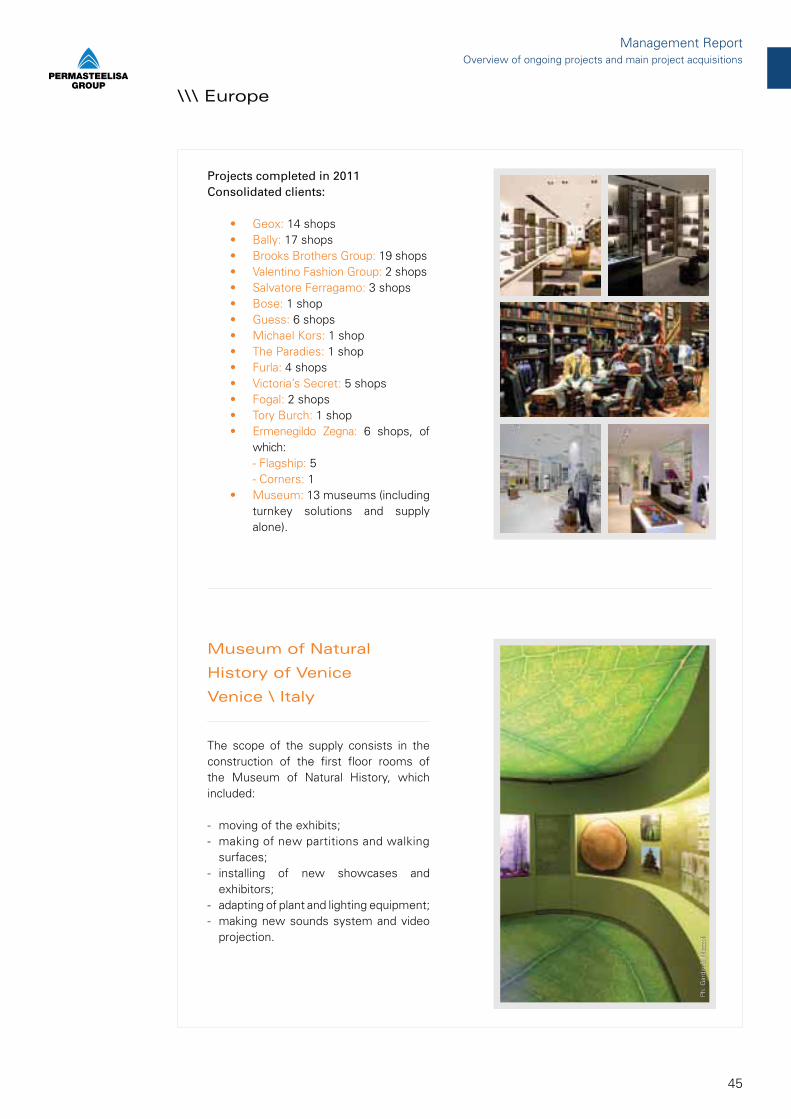

Projects completed in 2011 - Consolidated clients:

Brooks Brothers Group: 25 shops1 shop

3 shops1 shop 1 shop

\\\ USA

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

45

Museum of Natural

History of Venice

Venice \ Italy

The scope of the supply consists in the construction of the fi rst fl oor rooms of the Museum of Natural History, which included:

- moving of the exhibits;- making of new partitions and walking surfaces;- installing of new showcases and

exhibitors;- adapting of plant and lighting equipment;- making new sounds system and video

projection.

Ph:

Gar

din

& M

azzo

liP

h: G

ardi

n &

Maz

zoli

\\\ Europe

Overview of ongoing projects and main project acquisitionsManagement Report

Projects completed in 2011Consolidated clients:

14 shops17 shops

19 shops2 shops

3 shops1 shop6 shops

1 shop1 shop

4 shops5 shops

2 shops1 shop

6 shops, of which:

- Flagship: 5 - Corners: 1

13 museums (including turnkey solutions and supply alone).

46

The Interiors Business in Asia can be broken down in the following main areas:

Fitting Out and furniture; Shop fronts; Turnkey projects.

During 2011 more than 160 projects were awarded involving consolidated and new clients featuring an increasing trend compared to 2010.

Consolidated clients in 2011:

6 shops 21 shops

13 shops 5 shops

12 shops 20 shops

11 shops 8 shops

31 shops 5 shops

7 shops

New clients:

Other clients:

\\\ Asia

2011ANNUALREPORT

Management ReportOverview of ongoing projects and main project acquisitions

47

Overview of ongoing projects and main project acquisitionsManagement Report

48

Main risks and uncertainties which Permasteelisa S.p.A. and the Group are exposed to

No changes in the management approach or events that generate substantial changes in the risk profiles to which the Group is exposed to occurred in the year ended 31 December 2011: at the same time, the market fluctuation led the Management to increase the preventive attention to the risks connected to Permasteelisa Group activity. These risks are political, technical and technological, financial and credit, environmental and commercial.The main attention is focused on financial and credit risk: certainly the present growing markets have financial and credit risks higher than those the main markets of the Group (Europe and United States) had some years ago, without however that this fact represents a real warning but only more attention.

Risks associated with general economic conditionsThe global presence of Permasteelisa Group, as already underlined, has the positive characteristic to balance the economical risk and the negative one to multiply the exposure on risk situation.In Europe, in particular, the Euro break down risk has been monitored and suitable actions had been designed.Now this situation, even if always still present, is felt better than before.Other dangerous economic environments do not seem to be reported, except for the company rule of the promptly realization of adequate hedging on foreign currencies.

Risks associated with the Group’s resultsDespite the constant fluctuations in the market, the Group continues to prove to be able to achieve adequate “market share” year after year.It is instead evident that the market prices become more aggressive year after year, with the shift to the rising markets: in this context, Permasteelisa is proceeding to an important reallocation of its “Value proposition”.The Group’s perspective is now to be, if not “Cost Leader”, a “Cost focused Differentiation Leader”, although used to be for years the Leader in Differentiation; therefore it affords “low-low” execution methods of the projects, often sharing the components among the different Business Units and choosing for each component the better positioned Business Unit for an execution with the most competitive prices in the market. In this way Permasteelisa exploits its global organization (the only one in the market) to gain competitiveness according to a not accessible way for its main competitors.An adequate Project Management and an advanced ICT support are the necessary corollary.The combination of all these actions, ongoing for several years with satisfactory results, is what allows Permasteelisa Group and its shareholders to look at every market and environment evolution with serenity and confidence.

Risks associated with financing requirementsThe Permasteelisa Group’s financial position, after been evolving in strongly positive terms in the last years so that to represent one of the leading elements of the Group’s strength, is now less bright than in the past, but remaining positive. The reasons have to be found in the release of substantial monetary flows in years 2009 and 2011 to support extraordinary capital transactions and at the same time in a credit closure that, focusing on some of the main customers of the Group, inevitably had an impact on Permasteelisa. Therefore today the Group has adequate financial resources, and “committed” Back-up facilities that allow to afford safely all the projects possible requirements.

Risks associated with fluctuating exchange and interest rates, commodity prices and the cancellation of assigned projects ordersAs already mentioned in the Management report of the previous year, as an international player on the global market, Permasteelisa Group is naturally exposed to market risks associated to fluctuation of exchange and interest rates, and of the prices of the commodities that characterize its business (aluminum). This kind of risk is hedged through tools aimed at stabilising exchange rates (currency swaps) and commodity prices (commodities swap) as soon as the projects are assigned. With regard to commodities, these risks are faced also through the careful management of transactions with reference suppliers. As a result, the “exchange rate risk” and the “commodity price risk” are outstanding and managed with the customer for the sole duration of the offer until the assignment, except if the offer (but this only happens rarely) is calculated at current exchange rate/prices. Facing the higher risks associated to exchange rates (and the interest rates on so-called “forward” exchange rates) and commodities, another risk that needs to be

2011ANNUALREPORT

Management ReportMain risks and uncertainties which Permasteelisa S.p.A. and the Group are exposed to

49

considered is associated to the hedging operations on projects orders that are cancelled after their start date. This risk is still rather low and in any case to be considered within the right to the reimbursement to all costs borne for the cancelled projects orders.Furthermore, in the framework of the consolidation of its accounts, Permasteelisa Group is exposed to “translation” risks as a result of the variation of the Euro vis-à-vis the main currencies of payment other than the Euro. This is nevertheless a risk that is inherently part of a global company’s income statement structure and has not become more critical as a result of the current general crisis of the markets.

Risks associated with relationships with suppliersThe relationships with the suppliers are one of the main strength of Permasteelisa Group and, therefore, they are constantly kept under observation and control, and also helped when needed.Therefore this risk, while potentially existing, has adequate coverage in the attention with which the Group is dealing with, ready to solve any unusual situations.

Risks associated with managementEffective countermeasures against this risk are the strong affection of all Management to the Company, and the instruments of Retention tools implemented by the Company.

Risks associated with competitiveness in the areas the Group works inThis risk, already mentioned in the part related to the general economic conditions, naturally increases with the movement of the market to the rising geographical markets.Permasteelisa can hardly exclude to operate in those countries, otherwise it should renounce to its leader position, and therefore have to improve its competitive advantages arising from its global structure and its core skills, but especially have to continue to refine its design, construction, installation and Project Management processes as already done until now in an excellent way. Therefore this risk, if correctly afforded to, can become an opportunity.

Risks associated with environmental policiesThe Group’s environmental policy should be considered an opportunity rather than a risk: indeed, more restrictive regulations and procedures especially in the area of bioclimatic and environmentally sustainable architecture in addition to more restrictive laws on energy saving will translate into more favorable market conditions for the company and the Group’s products and advanced technologies.

*******

As Parent company, Permasteelisa S.p.A. is basically exposed to the same risks and uncertainties described for the Group.

Further details, including more technical information on the management of some of the business risks illustrated here, are provided in the dedicated notes to both the Consolidated Financial Statements and the Statutory Financial Statements for the year.

Main risks and uncertainties which Permasteelisa S.p.A. and the Group are exposed toManagement Report

50

The Group’s organizational structure

During 2011 there were no specific reorganization and semplification in the corporate structure.

Research and innovationDuring 2011 Permasteelisa confirmed its intention to improve and release its own know-how through a number of activities as:

the sharing of final results of completed and in progress researches; the collection of new proposals and ideas that can be converted into research and development

projects, following an appropriate evaluation by the Top Management; the continuation of the publication of the newsletter devoted to R&D/technical themes; the organization of specific courses designed to properly prepare and train the technical staff of the

company.

In addition to these activities, on request of the R&D structure, during 2011 more attention was paid to the correct dissemination of the information, and to the improvement of the protection/securitization of all the sensitive information that compose Permasteelisa’s know-how, systems and projects.In this regards, it was decided to start and promote the following activities transversely to the pure Research and Development studies,:

the implementation and dissemination of a “confidentiality agreement” to all technical employees, a document according to which each (technical) employee of Permasteelisa guarantees the not dissemination of sensitive data/information of which the employee may come into possession;

the implementation of a secured document storage, to which each user has a profiled access, based on the role that the employee has within the Organization.

With reference to the research and development activities, in 2011 the Group focused on the improvement of projects execution internal processes (the construction of buildings architectural envelopes) and on the development of new products.With reference to the improvement of internal processes, particular attention was paid to the formulation of applications in order to manage the design and discretization of complex surfaces, through system solutions and/or simple/innovative systems, in addition to more efficient production and installation systems in terms of cost and times of execution.With reference instead to the “new products” researches, research studies were developed on the basis of the following targets:

to make the buildings more “green” and comfortable, increasing energy saving and the using of renewable energy;

to increase the security level inside buildings; to study and use new materials and systems in the realization of the architectural envelopes; to increase the efficiency of processes also through the development and utilization of new IT

tools.

Among all, the research activities in 2011 focused mainly on the developing of new systems, through the pursuance of the following projects:

Building Physics, Energy saving, Renewable energy Solar Cooling System: project intended to the integration in the façade of a system of collectors

that uses the solar energy to heat and cool the building, through specific thermodynamic machines and dedicated plant. A special translucent collector is under development so that the final result will have an high architectural integration.

Double Integrated System Façade

Façade Integrated System

Façade Integrated Wind Power

Structural & Safety Bomb Blast Technology/Cablenet: after a first and consolidated development of the bomb blast

façade (i.e. explosion resistant), the study is now addressed to investigate the reaction of the

The Group’s organizational structure \ Research and innovation Management Report

2011ANNUALREPORT

51

various components of the facade, in addition to the energy transformation resulting from the explosion and its potential effects.

Design & Material TEC Façade: already ongoing since 2010, the project includes the development of a façade that

uses composite materials reinforced with glass fiber (FRP Fiber Reinforcement Plastic). Good thermal performance of the façade and the transparency of the opaque portion have already been studied and confirmed. This product will make available innovative architectural solutions, particular visual effects in addition to a low environmental impact as they are completely recyclable materials. In 2011 activities were developed related to the realization of a first prototype in real scale and to the subsequent performance check.

In 2011, research and development costs for Euro 3,475 thousand (2010: 3,824 thousand) were entered into the Group’s income statement, of which Euro 43 thousand (2010: Euro 82 thousand) for depreciation and amortization of costs items capitalized in previous year under the item “Development costs” included in the caption “Intangible assets”.

Technical Support GroupDuring 2011, as in previous years, Permasteelisa Group continued to dedicate resources to the activities of the Technical Support Group (TSG, knowledge management structure of Permasteelisa Group) for the dissemination and sharing of technical knowledge between Group companies, through the daily exchange of information and through dedicated meetings like those organized during 2011.Moreover, the consolidated project “Permasteelisa Technical Academy” helped to increase the high level of technical knowledge through training courses on specific topics such as “Design and Material” and “Building Physics”.TSG organization in Permasteelisa Group is the core of the creation and dissemination of a common technique and also allows the sharing of information and problems that can be solved through the exchange of opinions and experiences.

Information TechnologyDuring 2011 Permasteelisa worked mainly on the extension of SAP ERP adding new features that were made available to be used by all Group companies.In particular the modules on which Permasteelisa focused on are:

PSP (SAP Permasteelisa Production). Within this module, which represents Permasteelisa production and distribution processes, new modules of transport management were developed and set up: these include the cost optimization and the integrated management of logistics providers. SAP PSP is presently in use in Italy, Middle East and Germany. Its roll out in the other Group companies is planned in the next years.

Cash-flow: for the control of project cash flow and the monitoring of financial performance during the project execution.

Also in 2011 Permasteelisa continued the development of the new integrated product configurator system. This project developed together with Autodesk includes the complete cycle of product development, from the quotation to the project development until the start of production and the support of the pose activity on site.During 2011 the product was released for the quotation phase and the first two pilot projects for the design phase were started.The integrated management of corporate network was extended on two sides: the broadband optimization through an installation project of band compressors and the standardization of the corporate infrastructure with the installation of standard servers in all local companies.

Technical Support Group \ Information TechnologyManagement Report

52

Opus Hong KongHong Kong \ P.R. of China

Ph.

: Stu

art

Woo

ds

53

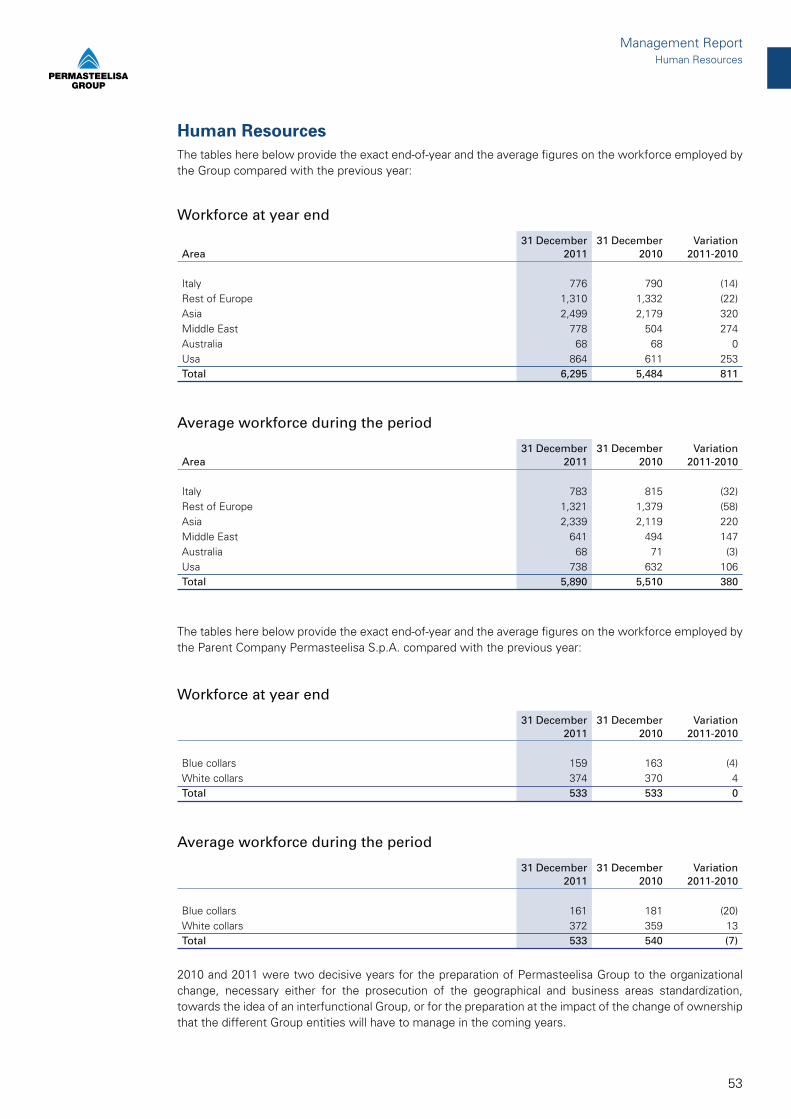

The tables here below provide the exact end-of-year and the average figures on the workforce employed by the Group compared with the previous year:

Workforce at year end

Area31 December

201131 December

2010Variation

2011-2010

Italy 776 790 (14)Rest of Europe 1,310 1,332 (22)Asia 2,499 2,179 320Middle East 778 504 274Australia 68 68 0Usa 864 611 253Total 6,295 5,484 811

Average workforce during the period

Area31 December

201131 December

2010Variation

2011-2010

Italy 783 815 (32)Rest of Europe 1,321 1,379 (58)Asia 2,339 2,119 220Middle East 641 494 147Australia 68 71 (3)Usa 738 632 106Total 5,890 5,510 380

The tables here below provide the exact end-of-year and the average figures on the workforce employed by the Parent Company Permasteelisa S.p.A. compared with the previous year:

Workforce at year end

31 December 2011

31 December 2010

Variation 2011-2010

Blue collars 159 163 (4)White collars 374 370 4Total 533 533 0

Average workforce during the period

31 December 2011

31 December 2010

Variation 2011-2010

Blue collars 161 181 (20)White collars 372 359 13Total 533 540 (7)

2010 and 2011 were two decisive years for the preparation of Permasteelisa Group to the organizational change, necessary either for the prosecution of the geographical and business areas standardization, towards the idea of an interfunctional Group, or for the preparation at the impact of the change of ownership that the different Group entities will have to manage in the coming years.

Human Resources

Human ResourcesManagement Report

54

Once again the training activity performed and will perform a key role in contribution to the alignment, to the dissemination and to the settlement of the change, driving significantly to the cohesion and dissemination of shared and common principles through the organizational learning and in particular through the dissemination of a common vision, the alignment with company targets, the resources empowerment and a leadership style which aims to develop employees’ technical and management skills, to their commitment and their cooperation between different geographical entities.

For these purposes, in 2011 the Group performed training activities related to:

Further consolidation of management skills in top management including the activities of performance management of the staff, that will continue in the coming years;

alignment and joint work of manager teams in the different Group Business Units; continuing education and professional development of technical resources (PTech Academy

Program); enhanced language training with special attention to English.

Above mentioned projects are described here below.

Management trainingTo help to manage the process of change that Permasteelisa is experiencing, management training focused primarily on the development of leadership skills, both inter-Business Units and intra-Business Units, thus promoting the local decision making coherence, the dialogue and the knowledge sharing between the different Business Units.The development of leadership skills is continuing, through training and coaching activities also by Group managers, with the main but not sole purpose to help employees to deal with and to overcome resistance at the change, promoting the dissemination of common objects towards which each individual of the team should strive.

The effort for the change was confirmed with the continuous development and diffusion of “Appraisals” systems during 2011, maintaining the promise to have them for all the “core roles” from 2012.

The Performance Management is coming always more pervasive into Permasteelisa Group culture, facilitating the business targets measurability and the integration of diversity through the coherence of the Key Performance Indicators by role, and the managers’ supervision and management on this issue is even more critical for the future successes of the Group.

Technical and specialised trainingAlso in 2011 the important technical training program called “Permasteelisa Technical Academy” continued.

The program is aimed at enhancing the skills of the Company’s technical resources worldwide, enabling them to acquire technical skills in a structured, coherent and planned way.

The Company launched this initiative after realising that suitably trained resources were difficult to find on the market and that training was therefore crucial for consolidating and maintaining the Group’s competitiveness. Relying on the valuable support of in-house technicians, the initiative aims to create a standardised and internationally accepted training method for sharing knowledge and exchanging information within the Group.

Technical staff receives basic and advanced level training on subjects such as thermal and acoustic performance of materials, structures, design and quality matters.

In addition to compulsory attendance, course requirements include passing a specific examination for each module as a prerequisite for admission to the next course. During the first year of experimentation, classroom teaching was accompanied by visits to the factories of some of our major suppliers, to have a

Human ResourcesManagement Report

2011ANNUALREPORT

55

closer look at materials and fully understand their characteristics and distinctive features: technicians must be aware of them when designing the products.

At the end of 2011 the 4 Academy technical modules are being finalized, with the participation of more than 500 of the best technicians of all Permasteelisa business units.

The structure of “Permasteelisa Academy” above illustrated had a high technical and educational recognition in the Group and consequently since 2012 the basis is placing to develop it also on other “core” roles for our business, i.e. Project Managers.

Training was ongoing on the issues of health, prevention and safety at the workplace (first aid training to selected personnel, fire prevention, etc.), area in which also relevant organizational changes during 2012 are expected.

Language training - focus on Permasteelisa S.p.A. and Permasteelisa Interiors S.r.l.The training initiatives for 2011 included individual and team lessons aimed at enhancing the staff’s knowledge of foreign languages, mainly English. The individual improvements in written and spoken language learning, are now recognizable and continuously measurable.

Due to Permasteelisa S.p.A. “service” activities on France, in year 2011 French courses started for the employees interested in these activities.

Additionally, training courses were supplied to production personnel of Permasteelisa S.p.A. and Permasteelisa Interiors S.r.l. on the following topics:

assembly mounting warehouse/inventory management training for shop-floor workers training for overhead crane operators training for forklift operators Italian legislative decree 81/08

In addition the “people management” competence for chiefs of blue-collar areas was reinforced.

During 2011 Permasteelisa S.p.A. and Permasteelisa Interiors S.r.l. provided training for approximately Euro 156 thousand, some of which also financed by third parties.

Human ResourcesManagement Report

56

New BabylonThe Hague \ The Netherlands

Ph.

: The

a va

n de

n H

euve

l/Mem

ber

of D

utch

Arc

hite

ctur

al P

hoto

grap

hers

(DA

Ph)

57

Following the already mentioned acquisition occurred on 6 December 2011, the Company is now owned by the sole shareholder Lixil Corporation itself owned by JS Group Corporation.

Treasury sharesAs of 31 December 2011 the Company does not own any treasury shares.

Transactions with related partiesThe details of any transactions with related parties, including transactions with other Group companies, are provided in the dedicated section of the notes to the Consolidated Financial Statements and the Statutory Financial Statements for the year.

Unconventional or unusual operationsThere are no entries or transactions resulting from unconventional or unusual operations during the year 2011 having any relevance on the operating performance and the financial position for the period of the Group and of the Parent company Permasteelisa S.p.A., except the already mentioned presence (in the previous years) of a number of agency contracts agreed in previous periods with a counterparty in a Middle Eastern country, that have fees that are much higher than those normally applied in the related business; these contracts are still legally valid in the country of reference and therefore, while the activities to close them are in progress, their economic and financial effects are adequately evaluated in company accounts.

Significant events subsequent to year end and outlook

Significant events subsequent to year endThere are no significant events subsequent to year end.

OutlookThe year 2012 is expected to be positive, in line with the strategic plan forecast. The economic backlog is adequate, and there are appropriate provisions to cover some specific risk situations.Permasteelisa continues to pursue a growth strategy for which the world market recovery will be essential.The commercial and strategic guidelines implementation are the means to guarantee the prosecution of the virtuous management that characterised the past years, thus allowing the Company to suitably react to the frequent and sudden market fluctuations.

Shareholders

Shareholders \ Treasury shares \ Transactions with related partiesSignificant events subsequent to year end and outlook

Management Report

58

Pursuant to Leg. Decree 196/2003 art. 34 of Privacy Code and the Technical Regulations (Annex B of Leg. Decree 196/2003), the Company approved the fourth revision of the Security Policy Document (DPS) providing minimum security levels as required by the regulations in force. The fourth revision of the Security Policy Document (DPS) and the previous versions are filed at the Company’s registered offices where can be consulted freely.

Pursuant to Leg. Decree 231/2001, Permasteelisa’s Board of Directors, by resolution of 28 August 2009, approved the current version of the Organizational, Management and Control Model that replaced the previous versions approved in 2005 and in 2007.With the adoption of this model, the Company intends to pursue the following main objectives:

- to promote the awareness of proper and transparent management of the Company, of the compliance with local regulations and of the fundamental principles of ethics in making business;

- to confirm that any illicit action is strongly condemned by the Company, as contrary to the law regulations and to the ethical principles of which the Company is the carrier and which intends to follow in making business;

- to allow the Company a continuous control and a careful monitoring on its activities, in order to promptly act where risk profiles appears and eventually apply the disciplinary measures provided by the Model itself;

- to determine the awareness in people operating in the name and on behalf of the Company that any illegal actions provided by the Decree is punishable by penalties to the author and administrative fines to the Company.

The Model consists of a General and a Special Section.

In the General Section the following items are described the contents and the impacts of the Leg. Decree 231/01, the general features of the Model, the categories of Offences that could result in the Company’s liability, the features, the powers and functions of the Compliance Board (that must be named by the Board of Directors), the disciplinary system and the guiding principles of staff training.

The Special Section describes in detail, with reference to the specific crime risk at which the Company considers to be exposed, the sensitive areas map, the alignment of the preventive controls system and the specific protocols regarding the sensitive areas.

The Model is available on the section Investor relations/Corporate governance of the corporate website.