annual report 2009/2010 annual report - … · annual report 2009/2010 1 contents ... ments of this...

TRANSCRIPT

Annual Report

Annu

al R

epor

t 20

09/2

010

2009/2010

ANNUAL REPORT 2009/2010

1

Contents

Foreword 3

The ACA celebrates 250 years 5

The ACA is reorganised 11

The auditors are audited 13

Auditing process – from planning to report stage 15

Audit of fi nancing instruments makes an impact 20

The new Federal Financial Statements 25

Administrative reform:Proposals await implementation 27

Chronology 2009/fi rst half 2010 34

Overview of the ACA: Mandate and Objectives 43

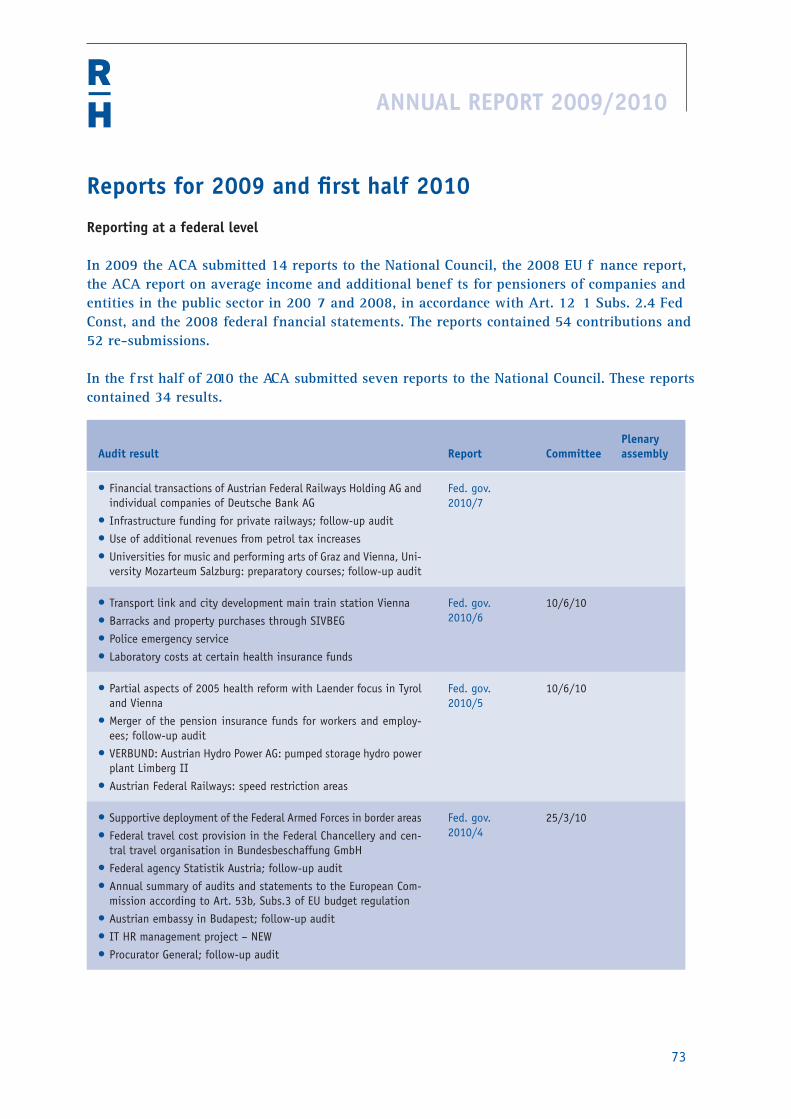

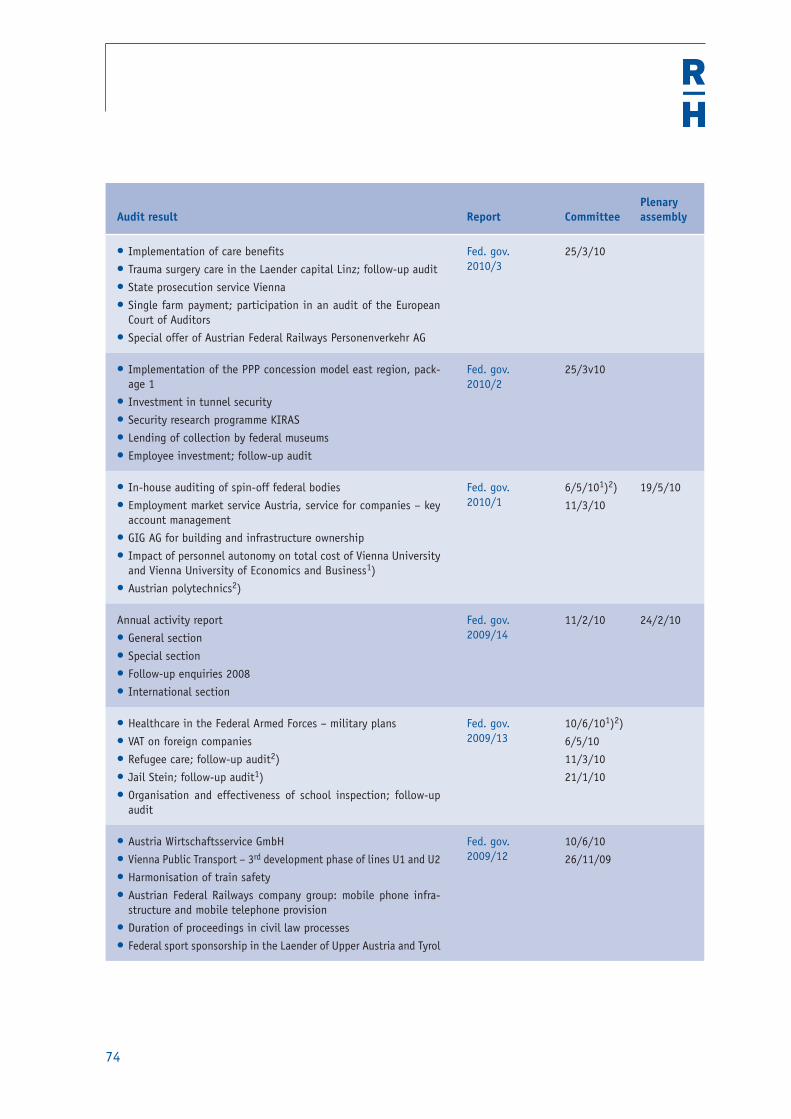

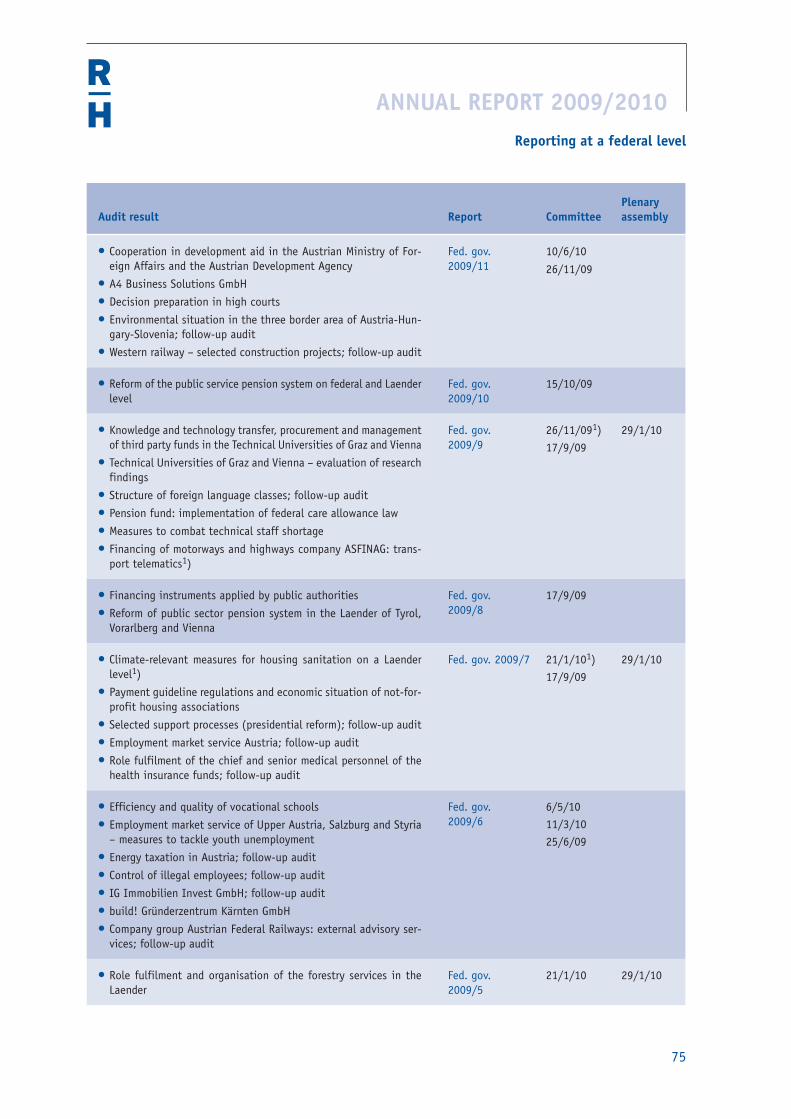

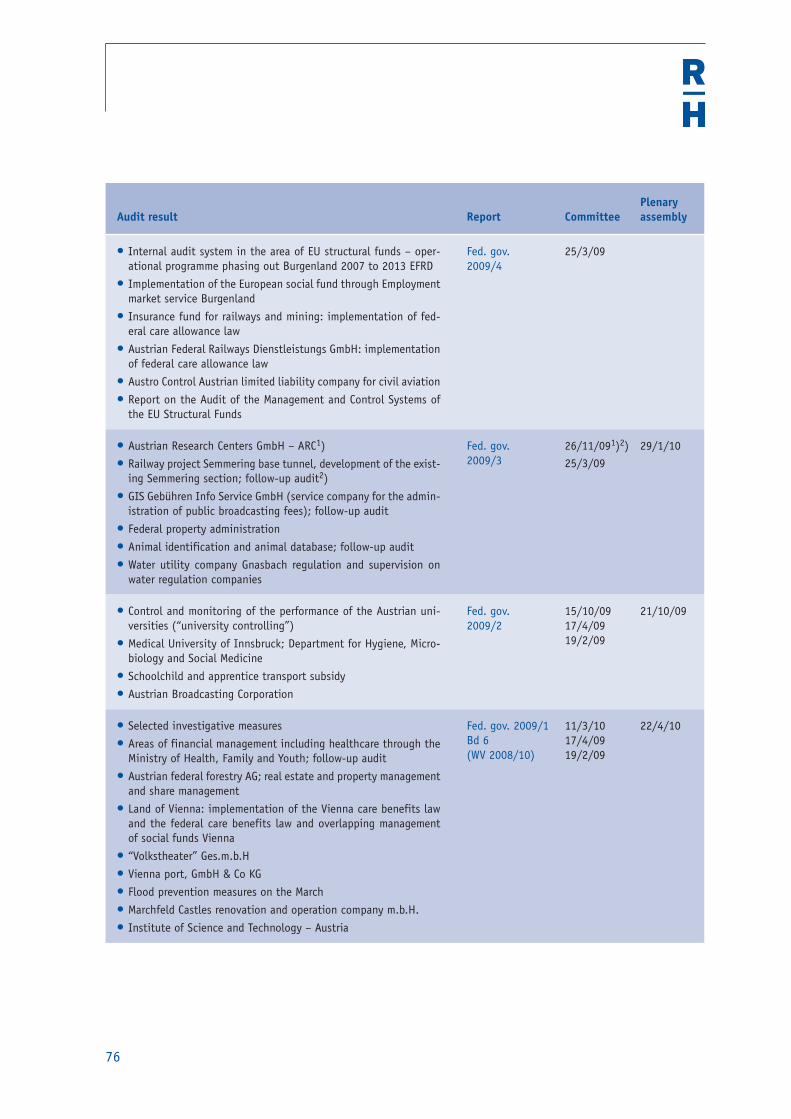

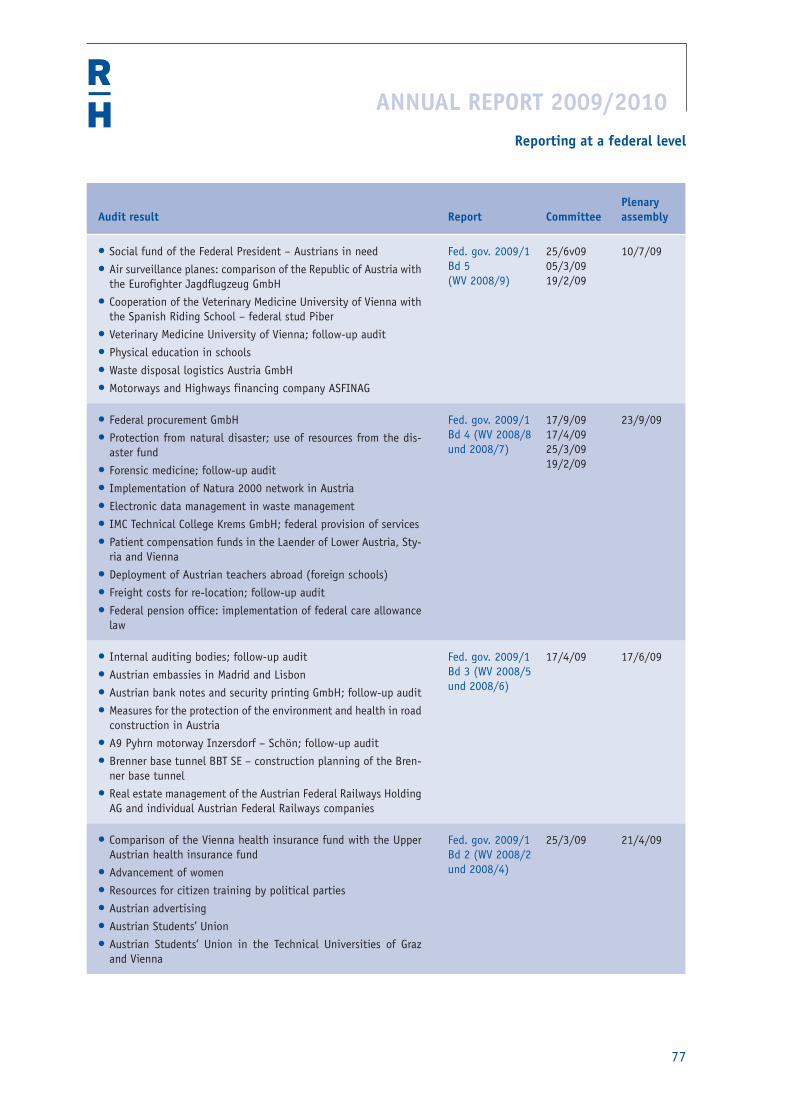

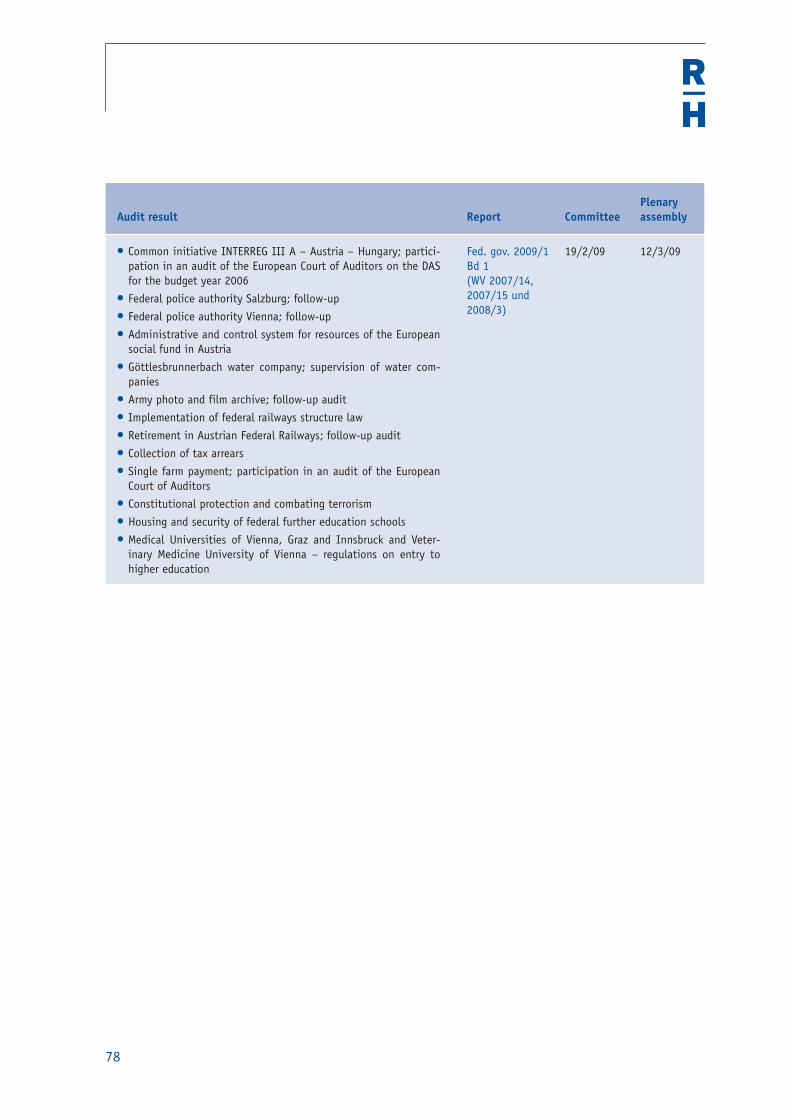

Reports for 2009 and fi rst half 2010Reporting at a federal level 73Reporting at a laender and local level 79

International sectionThe ACA within the INTOSAI framework 97International chronology 2009/fi rst half 2010 104

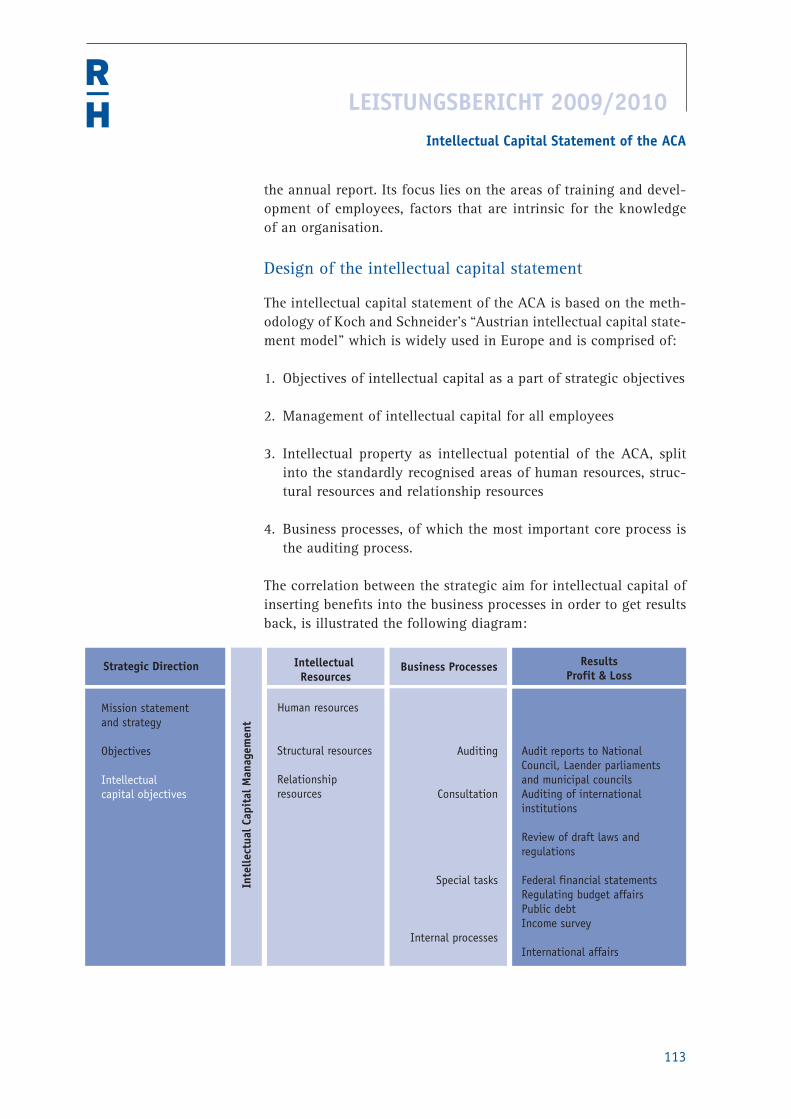

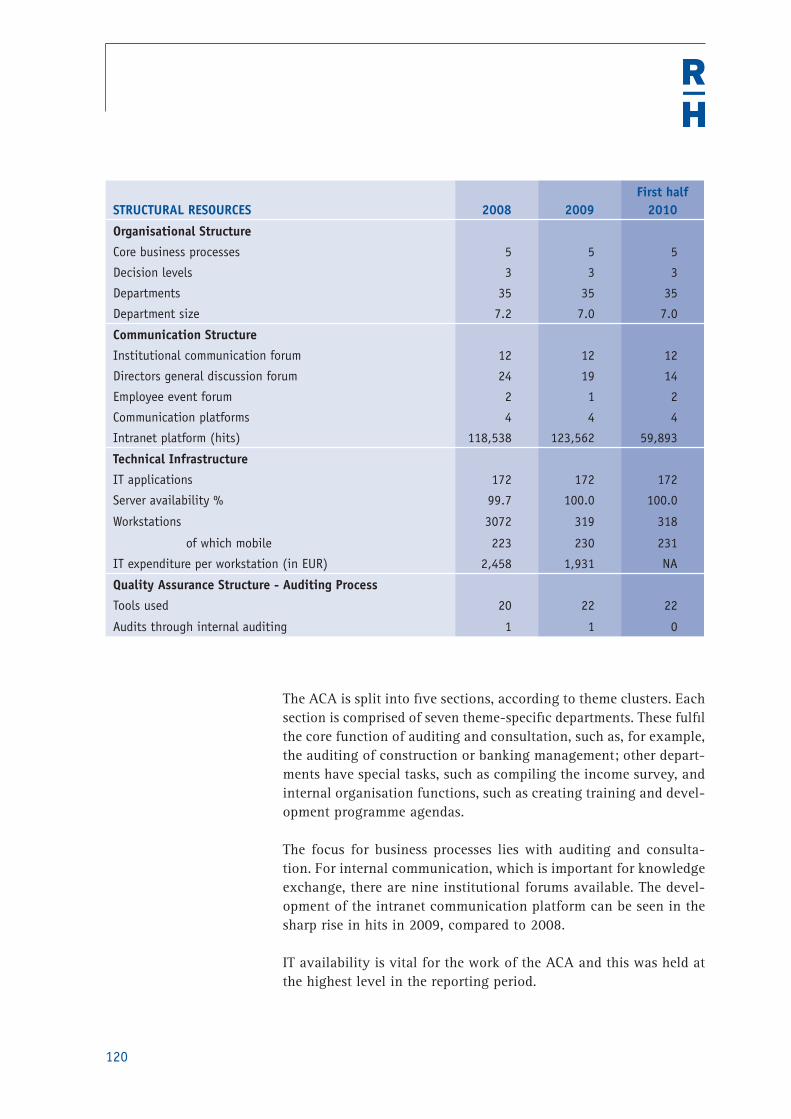

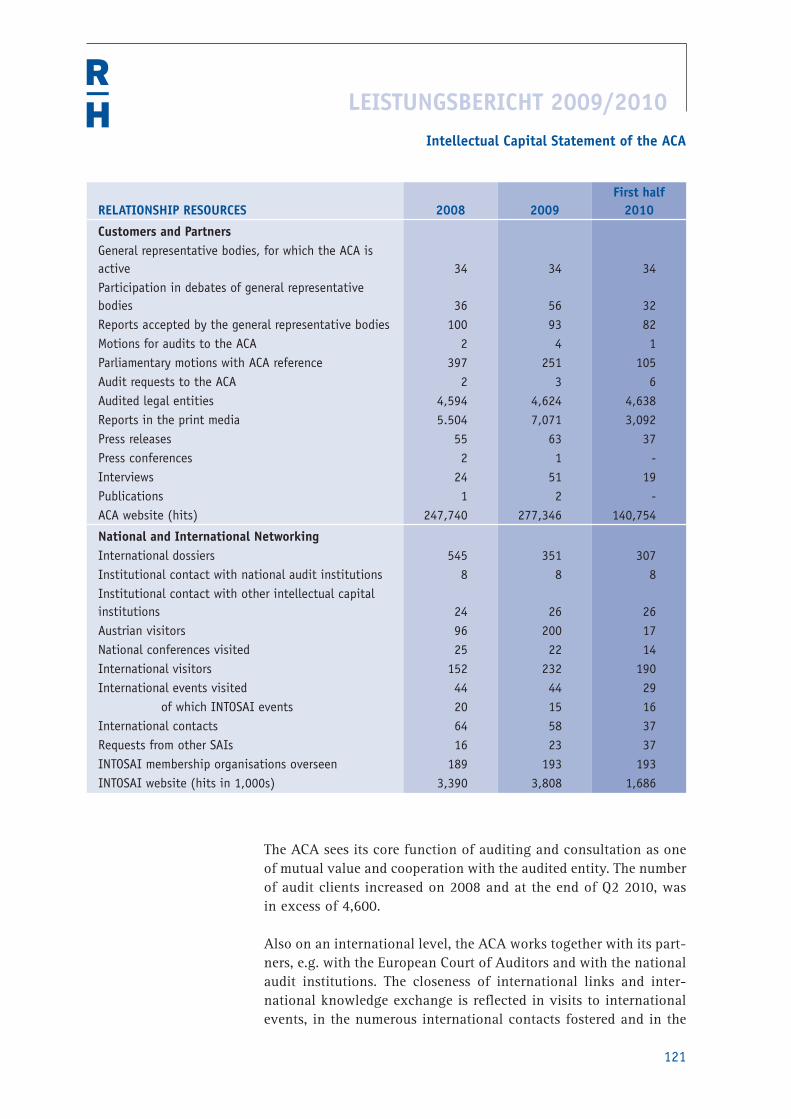

Intellectual Capital Statement of the ACA 112

ANNUAL REPORT 2009/2010

3

Foreword

Dear readers,

Past, present and future are key ele-ments of this ACA annual report. As well as giving a quick overview of the many activities of the supreme audit institution in Austria, in this, the fi fth annual report, we will give you an overview of the audit pro-cess, explain the effectiveness of the ACA, as well as our new organisa-tional structure, the development of the peer review and preparations for our 250 year anniversary.

“Public auditing pays off”. That is the motto of the ACA anniversary celebrations and it is the aim of this report to demonstrate it also.

Public auditing is the cornerstone of the parliamentary system and democracy. According to the constitution, the ACA is responsible for auditing the fi nancial management of the state. We check whether monies collected from taxpayers are being used economically, effi -ciently and effectively.

The stock taken with this report shows that the ACA, as an organ of the federal, of the Laender and of the local authorities, completely fulfi ls its constitutional responsibility of auditing and consultation.

In our audits, the ACA makes suggestions for improvements. Thanks to the close and constructive relationships we foster with the insti-tutions we audit, and with the general representative bodies, these re commendations have had a broad effect. The last survey process has shown that from a total of 1,140 recommendations in 2008, exactly 81 per cent have been or will be implemented.

As well as giving advice to our audit clients during the audit pro-cess and reviewing draft laws and regulations, the ACA’s consultation function also stimulates the reform process in Austria. At the moment, experts in the ACA are collaborating with the working group on new administration, amongst others. Many proposals are currently lying on

Dr Josef MoserACA President

4

the table – however, the political decisions to implement these reforms are still outstanding.

In addition to its national responsibilities, the ACA is also active on an international level. For over 40 years Vienna has been the headquar-ters of the General Secretariat of the INTOSAI, the umbrella organisa-tion of audit institutions from 189 countries. Currently, the INTOSAI is working on setting out the independent nature of the Supreme Audit Institutions (Declarations of Lima and Mexico) in a United Nations document.

Personally, and in the name of my dedicated colleagues, I would like to thank decision-makers from the political, administrative and eco-nomic sphere, as well as the media and the public, for your construc-tive cooperation and for the trust that you have placed in the ACA.

Dr Josef MoserACA President

ANNUAL REPORT 2009/2010

5

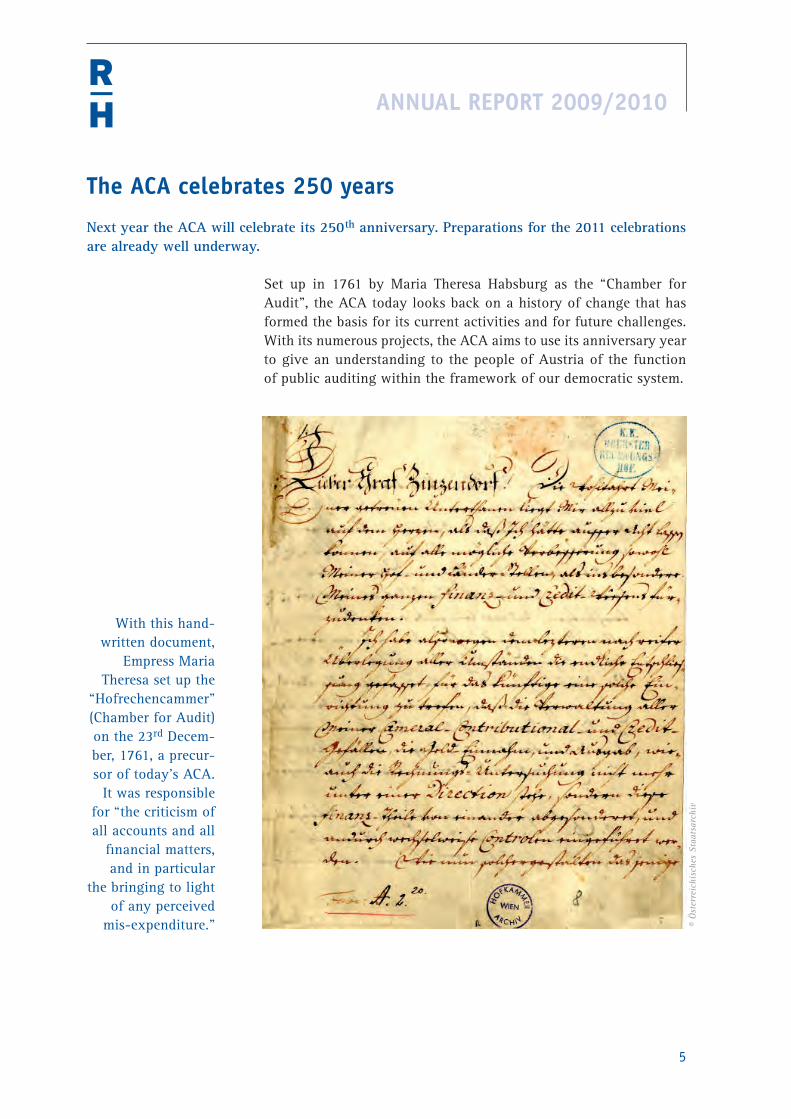

With this hand-written document,

Empress Maria Theresa set up the

“Hofrechencammer” (Chamber for Audit) on the 23rd Decem-ber, 1761, a precur-sor of today’s ACA.

It was responsible for “the criticism of all accounts and all

fi nancial matters, and in particular

the bringing to light of any perceived

mis-expenditure.”

Set up in 1761 by Maria Theresa Habsburg as the “Chamber for Audit”, the ACA today looks back on a history of change that has formed the basis for its current activities and for future challenges. With its numerous projects, the ACA aims to use its anniversary year to give an understanding to the people of Austria of the function of public auditing within the framework of our democratic system.

The ACA celebrates 250 years

Next year the ACA will celebrate its 250th anniversary. Preparations for the 2011 celebrations are already well underway.

© Ö

ster

reic

hisc

hes

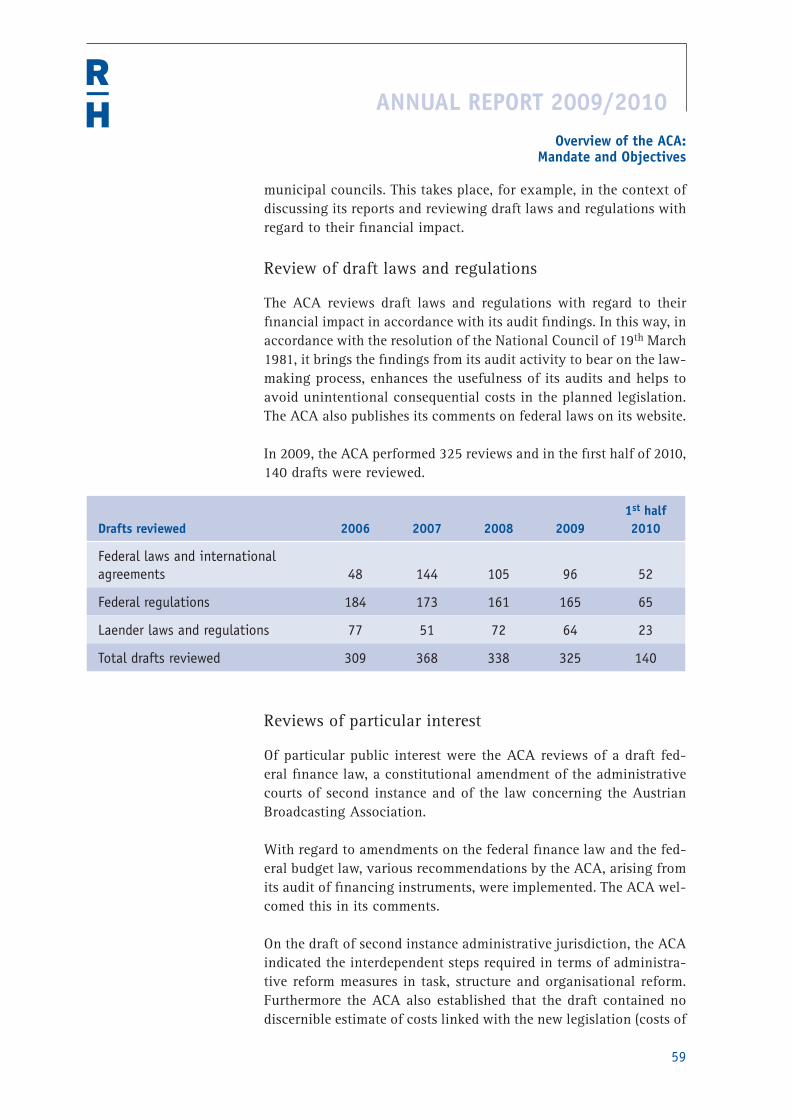

Staa

tsar

chiv

6

Historical development shows that in times of democracy the man-date of the ACA has always increased. This underlines the impor-tance of external public auditing for the functioning of a democracy.

Activities in the jubilee year will be based on three fundamental pil-lars:

• An exhibition in the rooms of the Austrian parliament will high-light the past, present and future of the ACA. Exhibits, charts and multimedia points will show visitors the history, working meth-odology and impact of the ACA. Special attention will be paid to having a youth-orientated format of the contents: the impor-tance of independent auditing in a democracy will be shown to this age group in an understandable and effective way.

Ten clusters of themes are planned: from the time of Maria Theresa, the Austrian Empire, and the Austro-Hungarian monarchy through the First Republic, the so-called “Ständestaat” (austrofascism), the Nazi period and the Second Republic, up to international net-works, the present and the future.

• Secondly, the ACA will issue a publication commemorating its 250th anniversary. Numerous contributions from personalities in the fi elds of politics, science and the media, as well as employees of the ACA, will outline the story of the ACA, its current activi-ties and responsibilities and its future challenges.

• Finally, the issues of external auditing will be explained to a broader public during the 250 year celebrations. With the slo-gan “Public auditing pays off”, various events, a touring exhibi-tion and special events for schools, are planned. Looking back to the past is especially relevant as it is always when authorities or rulers wish to limit the competencies and responsibilities of the ACA, that they fi nally realise they cannot manage without the auditing function.

The projects planned for the 250th jubilee year should demonstrate that public auditing pays off and that a strong, independent audit-ing authority is therefore indispensable. The topics presented in the jubilee year should make it clear that transparent auditing assures the best possible use of public funds, contributes to an improve-ment in the quality of public dealings, and reduces waste of money and corruption.

ANNUAL REPORT 2009/2010

7

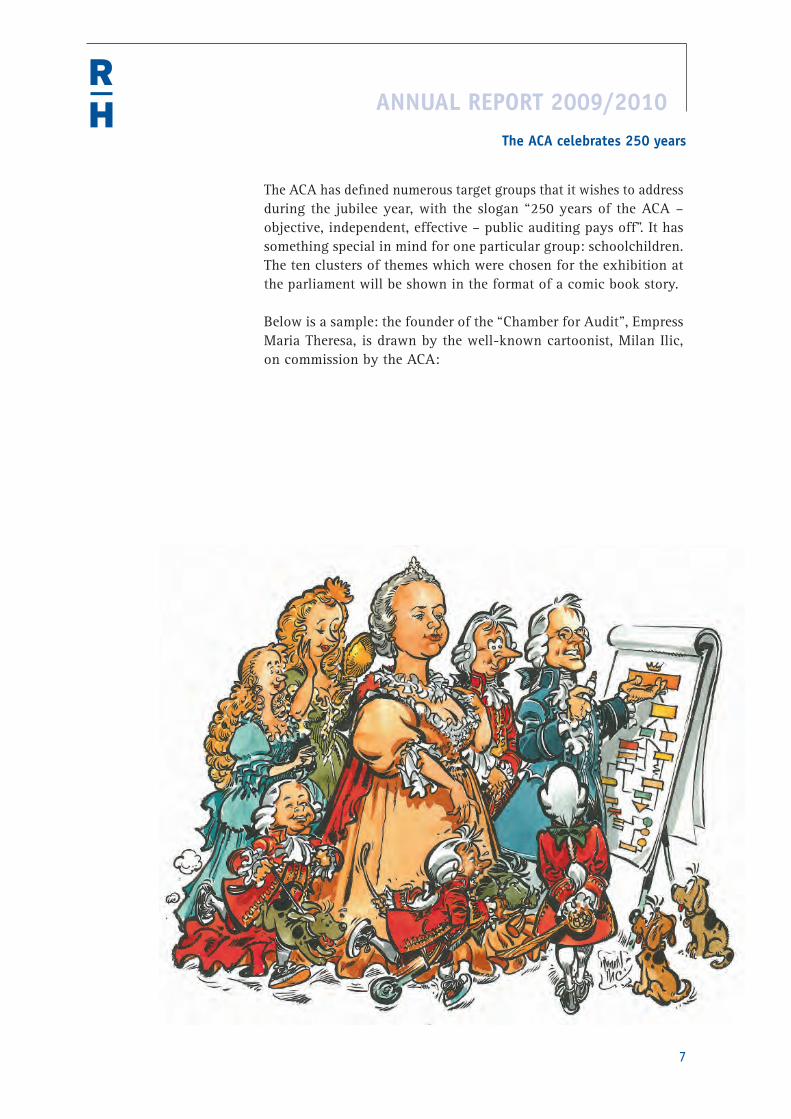

The ACA has defi ned numerous target groups that it wishes to address during the jubilee year, with the slogan “250 years of the ACA – objective, independent, effective – public auditing pays off”. It has something special in mind for one particular group: schoolchildren. The ten clusters of themes which were chosen for the exhibition at the parliament will be shown in the format of a comic book story.

Below is a sample: the founder of the “Chamber for Audit”, Empress Maria Theresa, is drawn by the well-known cartoonist, Milan Ilic, on commission by the ACA:

The ACA celebrates 250 years

8

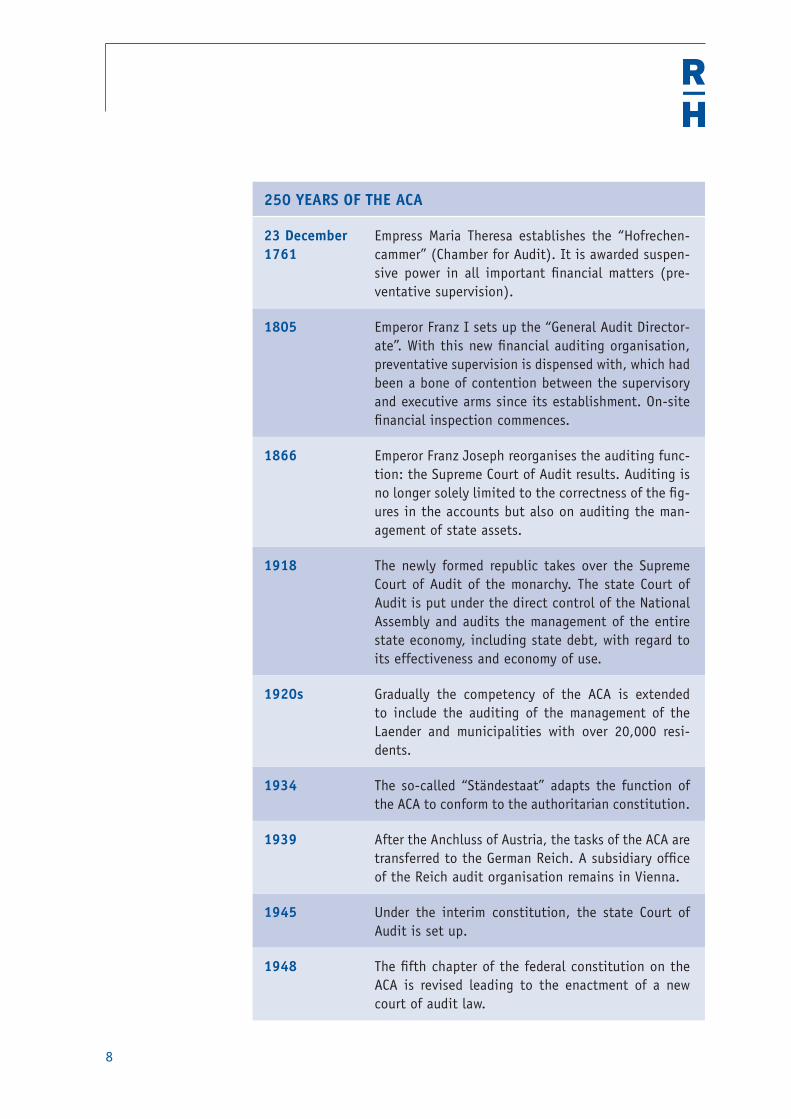

250 YEARS OF THE ACA

23 December 1761

Empress Maria Theresa establishes the “Hofrechen-cammer” (Chamber for Audit). It is awarded suspen-sive power in all important fi nancial matters (pre-ventative supervision).

1805 Emperor Franz I sets up the “General Audit Director-ate”. With this new fi nancial auditing organisation, preventative supervision is dispensed with, which had been a bone of contention between the supervisory and executive arms since its establishment. On-site fi nancial inspection commences.

1866 Emperor Franz Joseph reorganises the auditing func-tion: the Supreme Court of Audit results. Auditing is no longer solely limited to the correctness of the fi g-ures in the accounts but also on auditing the man-agement of state assets.

1918 The newly formed republic takes over the Supreme Court of Audit of the monarchy. The state Court of Audit is put under the direct control of the National Assembly and audits the management of the entire state economy, including state debt, with regard to its effectiveness and economy of use.

1920s Gradually the competency of the ACA is extended to include the auditing of the management of the Laender and municipalities with over 20,000 resi-dents.

1934 The so-called “Ständestaat” adapts the function of the ACA to conform to the authoritarian constitution.

1939 After the Anchluss of Austria, the tasks of the ACA are transferred to the German Reich. A subsidiary offi ce of the Reich audit organisation remains in Vienna.

1945 Under the interim constitution, the state Court of Audit is set up.

1948 The fi fth chapter of the federal constitution on the ACA is revised leading to the enactment of a new court of audit law.

ANNUAL REPORT 2009/2010

9

1975 The president and the vice president of the ACA are given the right to participate in National Council dis-cussions regarding ACA reports, on the federal fi nan-cial statements and on the chapter of the draft fed-eral fi nance law which concerns the ACA, as well as in its committees (subcommittees).

1978 The responsibility of the ACA to audit companies is regulated.

Research project: The ACA in “Ständestaat” and the Third Reich

250 years give the opportunity, but at the same time present a respon-sibility, to examine the history of the ACA and present all the highs and lows. The time between 1933 and 1945 form part of this. The ACA has therefore, on the occasion of the forthcoming jubilee year, initiated a research project on the role of the ACA in the time of the authoritarian Ständestaat state, during National Socialism and in the period straight after the war. The ACA puts a critical view on its history and clears up its role in these dark chapters of 20th cen-tury history.

In cooperation with the Ludwig Boltzmann Institute for Research into the Effects of War, Graz-Vienna, and the Institute for Economic, Social and Corporate History at the University of Graz, this issue is being given special attention. The background of the research project is the question of what effect the regime changes of 1933/34 (Ständestaat) and 1938 (Anschluss to Nazi Germany) left behind on the administration. As the document archives up to 1939 are avail-able, going back over this period is very straightforward for the ACA. However, during the period of August 1939 to the collapse of the German Reich in 1945, there are hardly any documents avail-able in Vienna. Therefore, to complete the research, it will be nec-essary to access records in Berlin in order to clarify the role of the Vienna offi ce.

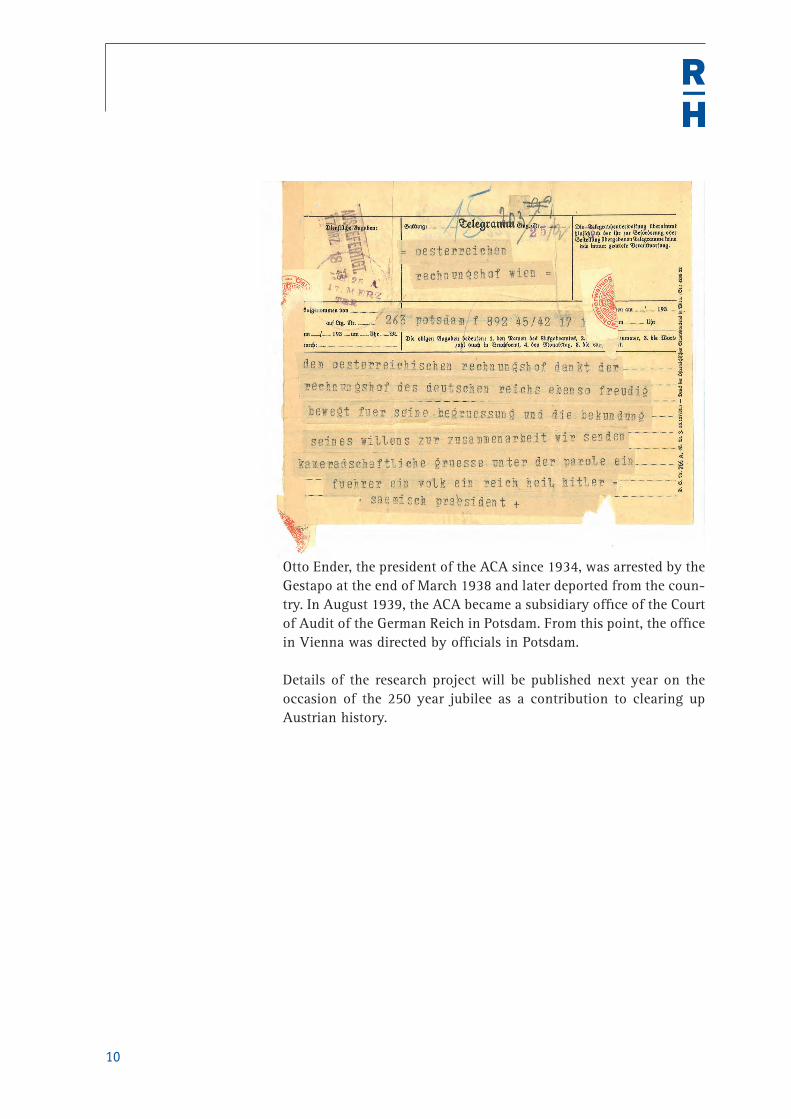

How important the project is, can be seen in that after Hitler walked into Austria in March 1938, the ACA initially remained in its then form, but those working there had to swear an oath of allegiance to the Führer. A telegram of congratulations from the president of the Reich Court of Audit, Ernst Moritz Saemisch, remains from those days (see next page).

The ACA celebrates 250 years

10

Otto Ender, the president of the ACA since 1934, was arrested by the Gestapo at the end of March 1938 and later deported from the coun-try. In August 1939, the ACA became a subsidiary offi ce of the Court of Audit of the German Reich in Potsdam. From this point, the offi ce in Vienna was directed by offi cials in Potsdam.

Details of the research project will be published next year on the occasion of the 250 year jubilee as a contribution to clearing up Austrian history.

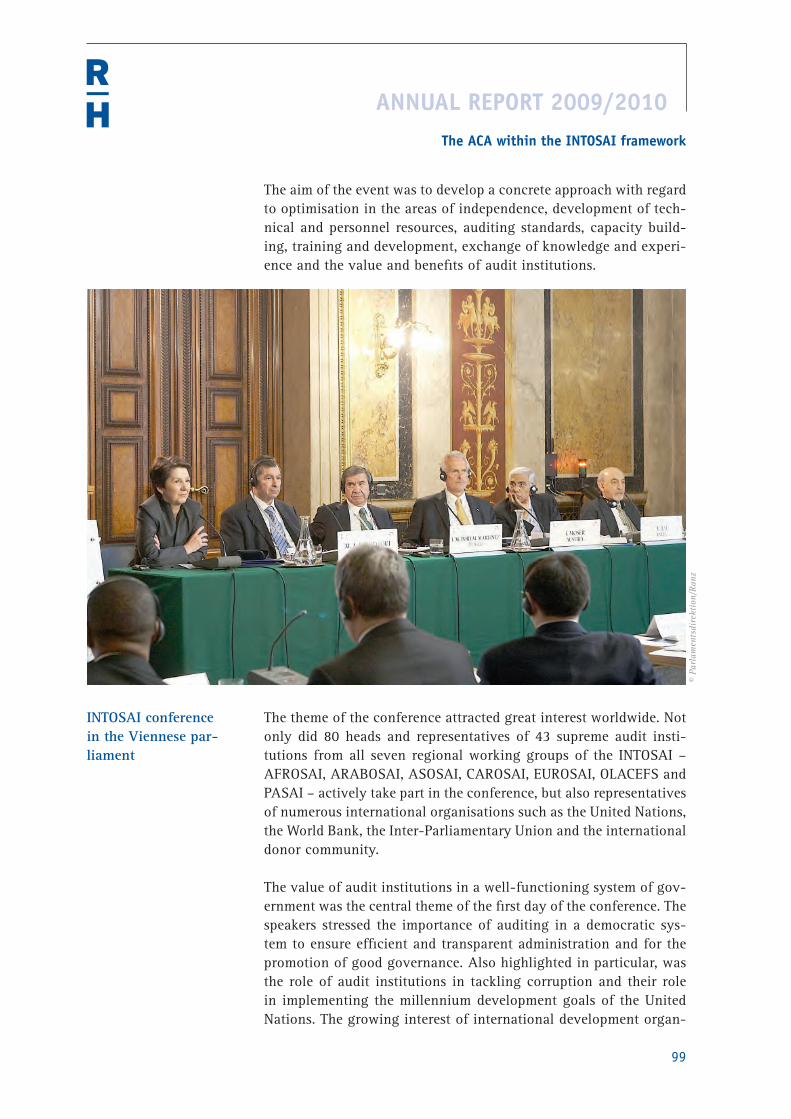

ANNUAL REPORT 2009/2010

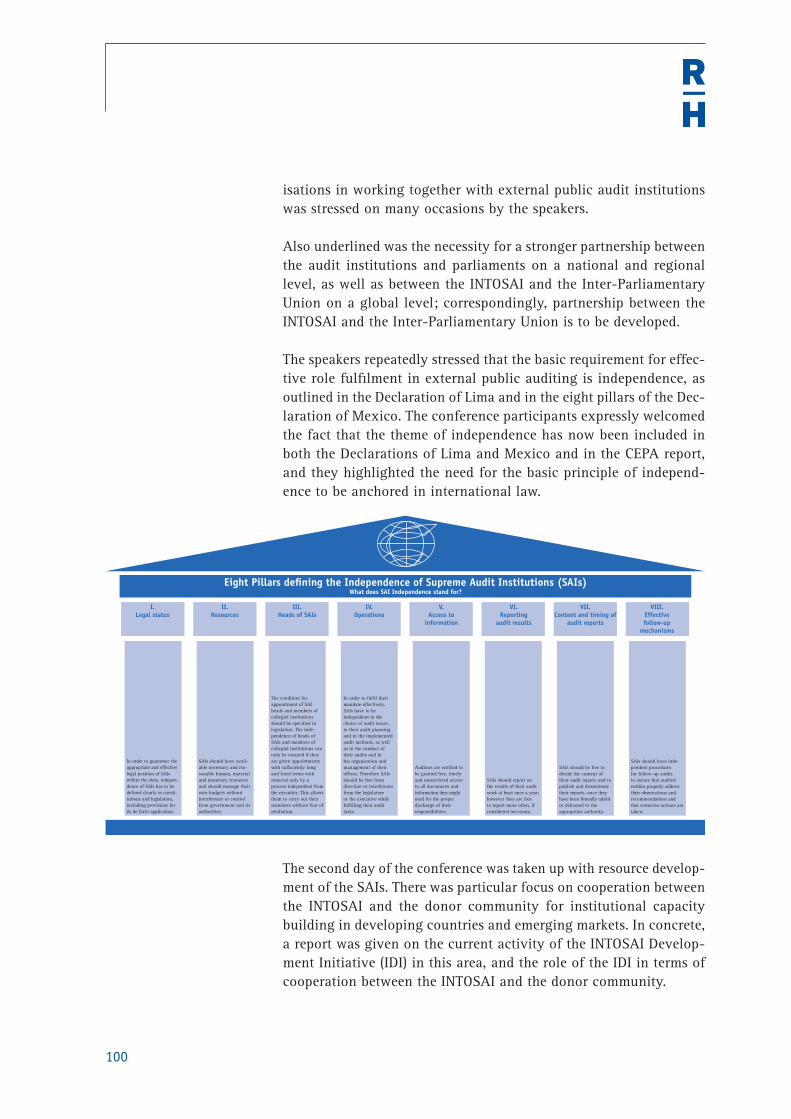

11

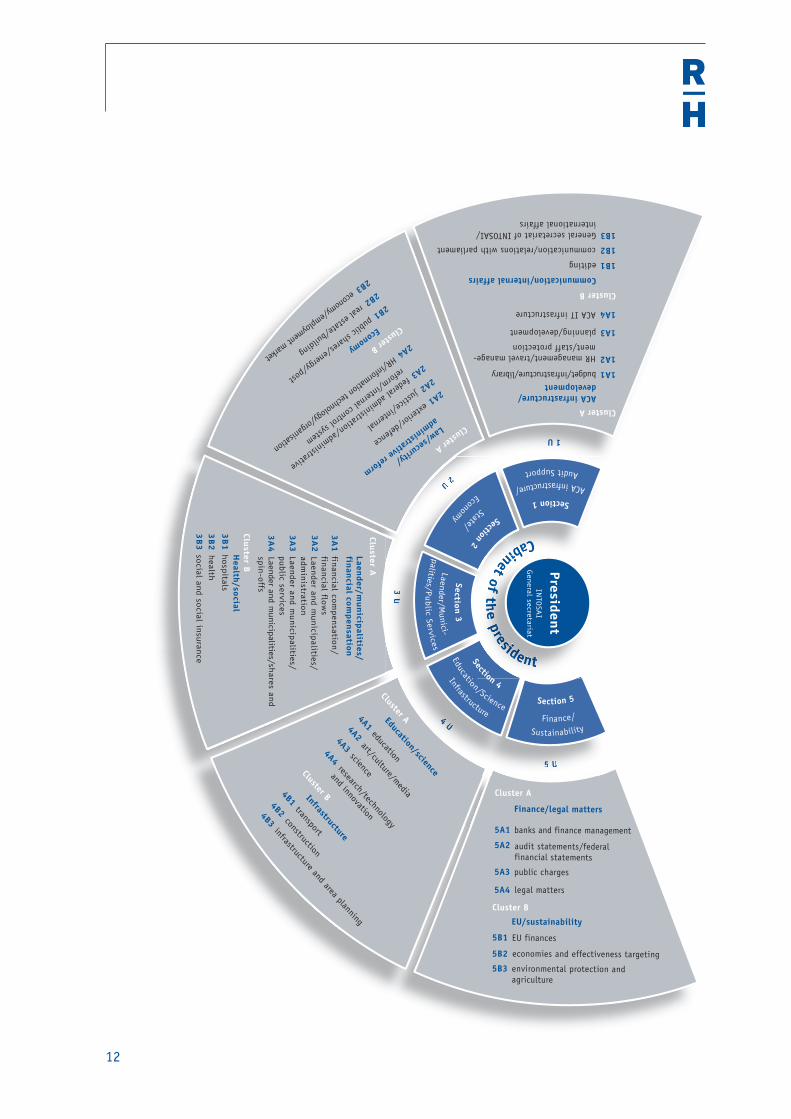

With the aims outlined above – to strengthen the ACA for new challenges – the president commissioned an internal reorganisa-tion project group in March 2010. On the one hand, this was tasked to improve the framework conditions in the core areas of auditing and consultation and, on the other hand, to bring the focus of the internal service departments more in line with the demands of the audit service.

The result of the project – after the involvement of the staff council – was fi rst discussed with the management team in May and then presented to all employees of the institution. In May 2010, imple-mentation of the project results also commenced.

The new ACA organisation came into being on 1st September, 2010. The number of sections remains unchanged at fi ve, as is the number of departments at 35.

Henceforth, the ACA has four auditing sections and one section which includes all internal support and service departments. Each of the fi ve sections contains seven departments, which are linked in two task clusters, in order to create a connection between related audit topics and therefore work more effi ciently.

Two examples: Cluster A in Section 3 contains fi nancial compensa-tion and fi nancial capital accounts, as well as administration, pub-lic services and shares or spin-offs on Laender or municipal levels of government. Cluster A in Section 4 is responsible for education and science.

Centres of expertise have been set up in several departments, includ-ing the areas of administrative reform, internal auditing, effi cient budget management, accounts receivable, grants, public procure-ment law and corporate law.

The ACA is reorganised

The ACA has been restructured and the changes came into effect on 1 st September, 2010. The changes mirror the current and future challenges which will face the supreme audit institution for the federal, Laender and local levels of government. Amongst others, the following have been enhanced: national perspective, screening of f nancial f ows between the levels of govern-ment and the observation of the wide f eld of public services from care and social provisioning through school and kindergardens to water supply and waste water disposal.

12

Cabinet of the president

1 U 2 U 3 U

4 U 5 U

CCaabin

2U

333UUUU

4444UUUU

555 UUU

binetooffff

ttttthhhhhheeeeee

pppppprrrrreeeeerr sssssiiiiidddddeeeeeennnnntttttt

President

Section 1 Section 2 Section 3

Section 4 Section 5

ACA infrastructure/ State/ Laender/Munici- Education/Science Finance/

Audit Support Econom

y palities/Public Services Infrastructure Sustainability

Communication/internal affairs

communication/relations with parliament

editing 1B1

Cluster B

1B2

General secretariat of INTOSAI/international affairs

1B3

ACA infrastructure/development

HR management/travel manage-ment/staff protection

budget/infrastructure/library 1A1

Cluster A

1A2

planning/development

ACA IT infrastructure

1A3

1A4

Economy

real estate/building

public shares/energy/post

2B1

Cluster B

2B2economy/employment market

2B3

Law/security/

administrative reform

justice/internal

exterior/defence

2A1

Cluster A

2A2federal administration/administrative

reform/internal control system

HR/information technology/organisation

2A3

2A4

Health

/socialhospitals

3B

1

Cluster B

health3B

2social and social insurance

3B

3

Laender/m

unicip

alities/fin

ancial com

pen

sation

financial compensation

/financial flow

s3A

1

Cluster A

Laender and mun

icipalities/ adm

inistration

3A

2

Laender and mun

icipalities/public services

3A

3

Laender and municipalities/sh

ares andspin

-offs3A

4

Education/science

education

Infrastructure

construction

transport

4B1

Cluster B4B2

infrastructure and area planning

4B3

art/culture/media

4A1

Cluster A4A2

scienceresearch/technology

and innovation

4A34A4

EU/sustainability

economies and effectiveness targeting

EU finances5B1

Cluster B

5B2

environmental protection andagriculture

5B3

Finance/legal matters

Cluster A

banks and finance management

audit statements/federalfinancial statements

5A1

5A2

public charges

legal matters

5A3

5A4

INTO

SAI

General secretariat

ANNUAL REPORT 2009/2010

13

Representatives of the renowned supreme audit institutions of Ger-many, Denmark and Switzerland were in Vienna between October 2009 and April 2010 to conduct an on-site inspection of the ACA. For more than six months, therefore, the ACA found itself in the unusual role of being the auditee. The results of this peer review are due to be published later this year.

A peer review is a modern instrument of quality assurance. The pro-cedure comes originally from the fi eld of science and is used there to judge scientifi c work. The INTOSAI, the International Organisa-tion of Supreme Audit Institutions, took this model and developed guidelines for Peer Reviews for external public auditing.

Experienced auditors from the German, Danish and Swiss audit insti-tutions carefully examined the operations and working methods of the ACA. Core to this were strategic fundamentals, the perception of the core activities of auditing and consultation, support serv-ices such as IT, the evaluation of audit results and public relations. Those carrying out the peer review followed internationally recog-nised standards.

At the beginning of 2009, the presidents of the audit institutions involved in the peer review signed off on the core areas in a com-muniqué and Memorandum of Understanding. On this basis, the inspection began on-site in October 2009 and was completed at the end of April 2010 following several visits from German, Danish and Swiss peers.

Within the framework of the peer review there was also an employee survey, which was carried out by an external research institute and commissioned by the Swiss audit institution. The survey included questions on issues such as relationship to the employer, internal information and knowledge transfer, satisfaction at the workplace and career prospects. At 74%, the response rate was very high. The results of the survey were presented to the employees at the ACA at the end of April 2009. They will also be included in the fi nal report of the peer review.

Apart from intensive consultation and talks within the ACA, the external auditors also held talks with members of parliament, with

The auditors are audited

“Who audits the auditors?” There is now a concrete answer to this frequently asked question.

14

representatives of audited bodies, with heads of Laender audit offi ces and with journalists.

At the moment, the German supreme audit institution, as the “lead-ing peer” is putting the results together. The audit results are due to be sent to the ACA for statement in the autumn. In the interests of complete transparency, the ACA will submit the results to the National Council and the nine Laender parliaments and make it available to the public, by the end of this year.

However the peer review does not end with the fi nal report. In the interests of increasing the effectiveness of the ACA, the recommen-dations and suggestions for improvement by the peers will be ana-lysed immediately after the report is published and will be imple-mented as soon as possible.

Presentation of the employee survey in the peer review

© RH

, Sa

brin

a V

lk

ANNUAL REPORT 2009/2010

15

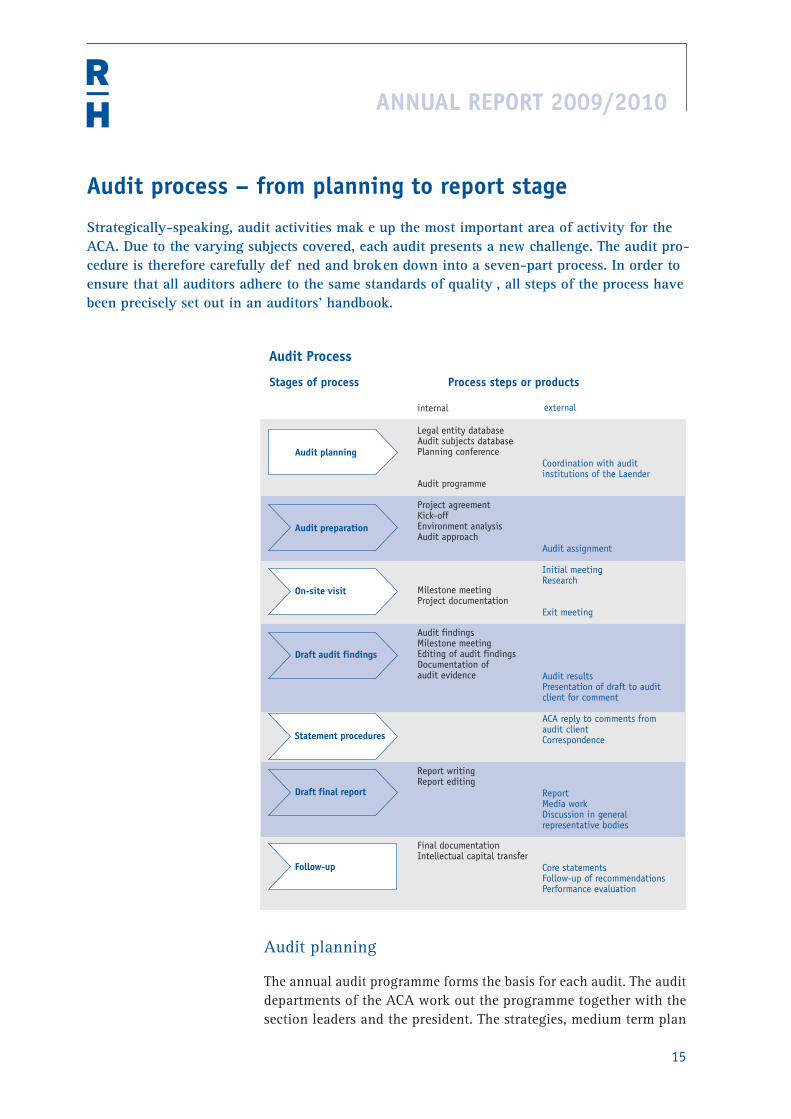

Audit process – from planning to report stage

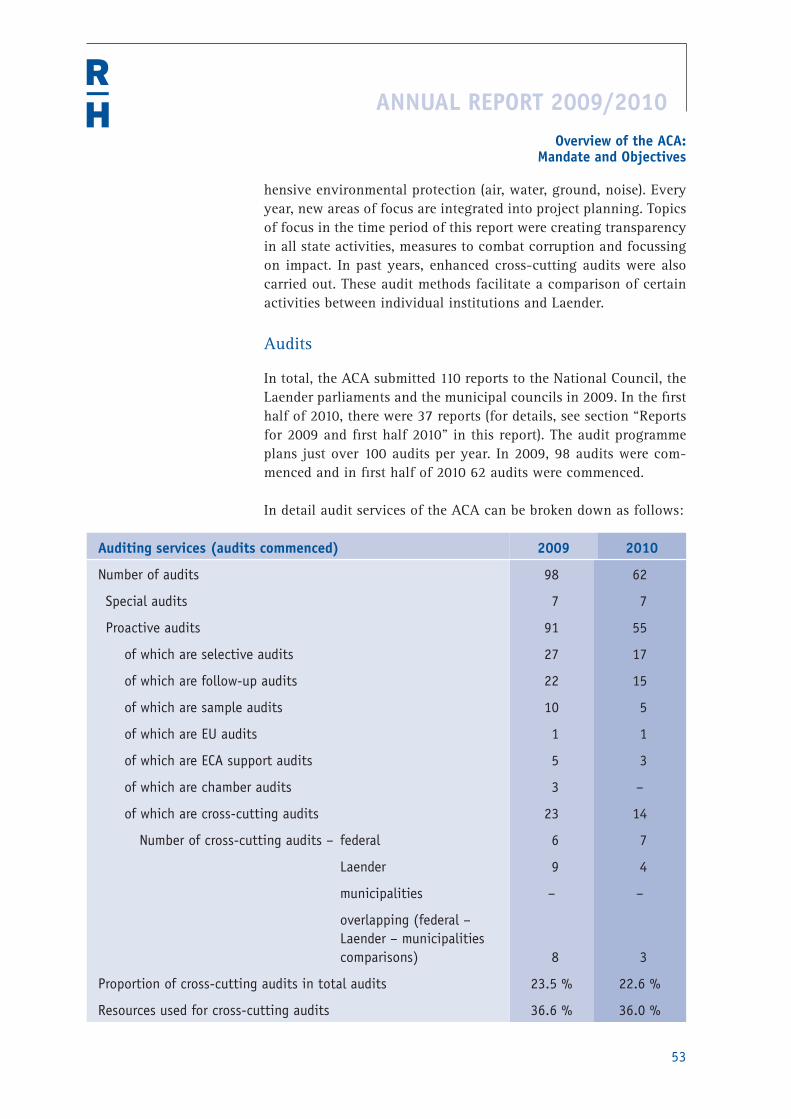

Strategically-speaking, audit activities mak e up the most important area of activity for the ACA. Due to the varying subjects covered, each audit presents a new challenge. The audit pro-cedure is therefore carefully def ned and broken down into a seven-part process. In order to ensure that all auditors adhere to the same standards of quality , all steps of the process have been precisely set out in an auditors’ handbook.

Audit planning

The annual audit programme forms the basis for each audit. The audit departments of the ACA work out the programme together with the section leaders and the president. The strategies, medium term plan

Audit Process

Stages of process

Audit planning

Audit preparation

On-site visit

Draft audit findings

Statement procedures

Draft final report

Follow-up

Process steps or products

external

Coordination with audit institutions of the Laender

Audit assignment

Initial meetingResearch

Exit meeting

Audit resultsPresentation of draft to audit client for comment

ACA reply to comments from audit clientCorrespondence

ReportMedia workDiscussion in general representative bodies

Core statementsFollow-up of recommendationsPerformance evaluation

internal

Legal entity databaseAudit subjects databasePlanning conference

Audit programme

Project agreementKick-offEnvironment analysisAudit approach

Milestone meetingProject documentation

Audit findingsMilestone meetingEditing of audit findingsDocumentation of audit evidence

Report writingReport editing

Final documentationIntellectual capital transfer

16

and the respective themed audit focus all form the basis. The audit programme for the coming year is established in the autumn of the previous year at a planning conference. The independence of the ACA, which is set out in the constitution, assures that the ACA has autonomy when creating its audit programme. The selection of audit themes follows certain criteria such as fi nancial relevance, current developments and risk potential. In order to safeguard its independ-ence, the ACA coordinates its audit activity in a network with other audit authorities, in particular the Laender audit institutions and the audit institution of the City of Vienna.

Together audits encompass the entire spectrum of public activity. Their remit extends from fundamental fi nancial management of pub-lic and private sector resources through areas of current political interest to issues concerning the citizens of the country.

Audit preparation

For every audit proposal an internal project agreement is signed off. Then an environmental analysis is created, in which the bodies that will be affected by the audit are identifi ed. The subjects and aims of the audit are set out in a detailed audit draft. The audit client is informed in writing regarding the upcoming audit (audit appoint-ment).

On-site audit

The actual on-site audit always begins with an initial meeting with the management of the body to be audited. In this the auditors will outline the issues to be covered in the audit and clarify any que-ries regarding the audit process. Then the audit team begins their research. This happens on site, and the body being audited will pro-vide offi ce space to the team. As well as collecting and evaluating written documents, information will be gathered through meetings with the representatives of the audit client.

Draft of audit fi ndings

After the on-site audit has been completed, the data and documents which have been collected are evaluated and the fourth part of the process, the draft of the audit fi ndings begins. In order to clarify any issues that may arise when looking through the documents, the members of the audit team will also carry out discussions with the audit client in this phase, if required. Both during the inspection and in the collation of fi ndings, internal milestone meetings take

ANNUAL REPORT 2009/2010

17

Audit process – from planning to report stage

place where the auditors coordinate with the contract giver (usually the department head) regarding how the audit is proceeding, clarify open issues, and the corresponding project is written up. The mile-stone meetings act as a ‘should v is’ comparison between the audit draft and its implementation. At the end of this phase, there is a clos-ing discussion with the management at the body being audited. The auditors present the results of the research and main contents of the audit result to the audit client.

Statement procedures

After the audit result has been completed, the ACA conveys its fi nd-ings to the audit client and the fi fth part of the process, the state-ment process begins. The audit client has the opportunity to make a written response to the ACA on its fi ndings. There is a three month deadline for this, set out in the constitution. Following this, the ACA puts together a possible response – called the “statement on the state-ment”. Both positions are entered in the report.

Final report

The sixth part of the process “Final report” comprises the publica-tion of the report, contact with the media and discussion in general representative bodies.

An audit team on their way to an on-site audit

© A

PA

18

After the audit fi ndings, statement procedures and responses have been completed, the report is proofed in the editorial section of the ACA. At this point it is also checked that the report follows the stand-ardised format. ACA reports, with few exceptions, such as the federal fi nancial statements for example, basically follow the same format.

The fi rst section is the summary, in which the main points are set out. There is a reference to the corresponding chapter in the main document, using “reference numbers”. An essential part of the sum-mary is the “lead”, in which the ACA highlights the main conclu-sions of the report.

After the summary, all the key data of the project or institution are outlined in a box. For example, this may contain when the insti-tution was established, fi nancial and personnel data or the owner-ship structure.

Then follows the body of the report. This is broken down into var-ious “reference numbers”, i.e. chapters, such as “fi nance”, “person-nel” etc. Each individual reference number has, for its part, several (up to a maximum of four) parts:

• In the fi rst part, every reference number represents the fi ndings of the ACA.

• The second part contains the ACA judgment on its fi ndings.

• In the third part, the individual reference numbers cover the state-ment of the audit client.

• The fourth section contains the response of the ACA.

As a fi nal reference number, recommendations under the title “Final remarks/closing recommendations” are set out in the report.

After the editorial department has ensured that the report follows this standard structure, the fi nished report is authorised to be sent from the president to the relevant general representative body – National Council, Laender parliament or municipal authority. Only after the general representative body has received the report, does the ACA publish it. Up until then the ACA is bound to secrecy.

ANNUAL REPORT 2009/2010

19

Audit process – from planning to report stage

Follow-up

Even after publication, the audit process is not yet closed. The sev-enth and fi nal part of the process is “follow-up”. In this part, core learnings and generally valid statements are gleaned from the audit and put on the website. The survey process is also an important part of follow-up. The ACA checks with the audited body a year after the report has been published as to the implementation of its recom-mendations. Finally, learnings from the audit are conveyed to the employees of the ACA, in the framework of knowledge communities.

20

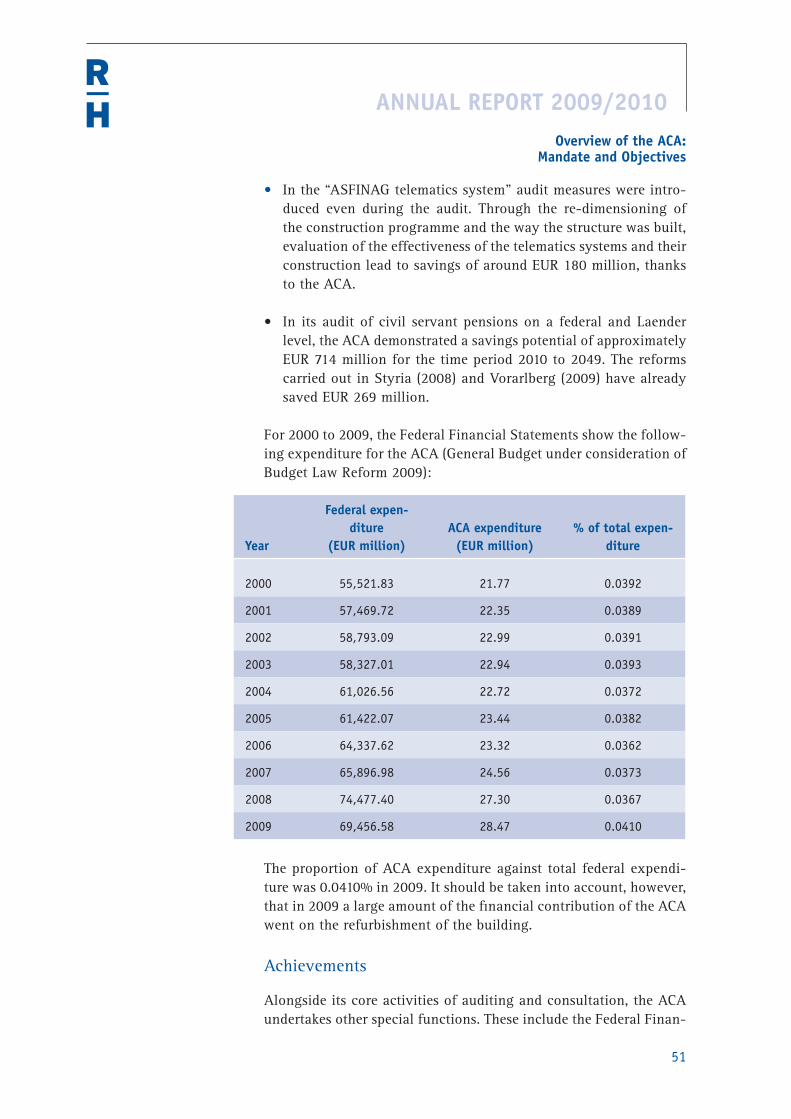

Audit of fi nancing instruments makes an impact

The f ndings and recommendations in the audit reports on the f nancing instruments at a fed-eral, Laender and local level, are a good example of how effective the ACA is and the compre-hensive reforms it can set in motion. In past months, f nancial management at a federal level and for many Laender and local communities have been newly regulated and put in order . There has also been a large impact on the international level. Audit f ndings have contributed to a further development of audit standards.

Aim, scope and use of crosscutting audit

At the end of 2007/beginning of 2008 the ACA audited the fi nancing and investment management of eight chosen public authorities (fed-eral state, four Laender and three towns). The aim of the audit was to analyse and compare the fi nancing and investment instruments and the fi nancing strategies and risks. The reports were submitted to the National Council and respective Laender parliaments in July 2009 and published at the same time, including the audit fi ndings concerning the federal state in Report Federal 2009/8.

In the second phase of the crosscutting audit in 2009, the ACA in-corporated the remaining Laender and further towns in the audit. The submission of the reports to the Laender parliaments is immi-nent.

Important themes of the reports

The reports contained both a general section, which basically con-cerns the comparison between the fi ndings and recommendations on the individual areas of fi nancial management in the public authori-ties, and a special section with specifi c conclusions on each author-ity. The themes covered in the reports included in particular liabil-ity management, derivatives, asset and risk management.

Effects and uses of the reports

The ACA achieved the following impact with these reports, on a federal, Laender and municipal level, as well as in the international arena:

Federal Level

• On the basis of various ACA reports, the president of the ACA pre-sented a policy paper “Fundamentals for fi nancing and investment in public authorities” at a summit called by the Federal Chancellor

ANNUAL REPORT 2009/2010

21

Audit of fi nancing instrumentsmakes an impact

in the Federal Chancellery on 31st July 2009. This was the basis for a working group to be commissioned by the Federal Minister for Finance to work on recommendations for optimising federal fi nancial management.

• These expert groups, consisting of six experts from the fi elds of science and fi nance, presented their fi nal report to the Federal Minister for Finance on 3rd November 2009. On 24th November 2009, this was brought to the attention of the Council of Minis-ters. As well as recommendations for implementing effi cient and risk-appropriate state fi nancial management, the report also con-tained guidelines for the investment of fi nancial resources using adequate risk guidelines.

• In the course of the amendment of the Federal Budget Act 2013, further proposals on the basis of ACA audit fi ndings were taken up. These changes especially concerned the lifting of the pro-vision of transactions to raise short-term liquidity for the pur-poses of investment and a new defi nition of the term “transac-tions to raise short-term liquidity”. The National Council enacted the amendment on 11th December 2009.

Summit at the Federal Chancellery

© BK

A/H

OPI

-Med

ia

22

• On 7th July 2010, the National Council enacted an amendment on the Federal Financial Act, regulating liability management of the Austrian Republic, as well as organisational rules and those cov-ering risk for the Austrian federal fi nancing agency (ÖBFA). The amendments to the act based on recommendations of the ACA especially concerned an improvement of risk management in the ÖBFA by means of a legal requirement to establish risk manage-ment guidelines (including adequate control mechanisms for all relevant types of risk) and investment guidelines, as well as man-datory introduction of the four-eyes principle on resolutions by the ÖBFA board.

• In its report published in July 2010 on the public fi nances of 2009, the Government Debt Committee expressly recognised the proposals for improvements contained in the ACA reports of July 2009, which were numerous and possible to implement quickly, and which ultimately led to new guidelines for federal fi nanc-ing during the fi scal year and legally limited the federal liquid-ity position.

• The ÖBFA immediately set about implementing the ACA’s recom-mendations after the audit. Considerable and immediately effec-tive improvements were shown in a clear reduction of their cash position, the establishment of a certain liquidity reserve, the end of using transactions raising short-term liquidity solely for invest-ment purposes, the revision of credit risk guidelines and a limiting of investment. In addition, the ÖBFA strengthened their initiatives on the use of synergies with the Laender through the provision of a technical infrastructure in the area of risk management. Coop-eration between the ÖBFA and four Laender in the area of liquid-ity management could also be optimised.

Laender and Municipal Levels

• In 2009, initiatives for the improvement of risk management were also put in place on a Laender and municipal level. The ACA col-laborated with working groups set up by the Austrian Associa-tion of Municipalities containing experts from the Government Debt Committee, fi nancial market supervision, the Austrian Cen-tral Bank and the Austrian Chamber of Chartered Public Account-ants and Tax Consultants for the creation of new guidelines for the fi nancial management of municipalities. The ACA was able to provide advice based on its technical expertise and experience from its auditing activity. These guidelines were presented to the public in August 2009.

ANNUAL REPORT 2009/2010

23

Audit of fi nancing instrumentsmakes an impact

• The guidelines mentioned were enacted by the Austrian Associ-ation of Municipalities as a “non-binding yet offi cial and very pressing recommendation for all Austrian local municipalities”. They should contribute to a responsible use of public funds and ensure that investment risk for all municipalities is kept to a min-imum.

International Level

• The ACA took part in the Working Group on Public Debt which was set up by the INTOSAI, the umbrella organisation of the supreme audit institutions. The ACA was able to contribute its experience and knowledge from auditing fi nancing instruments, especially with regard to risk management in the area of investment.

• At the annual conference of the INTOSAI working group on the 14th and 15th of June 2010 in Mexico City, the audit of the fi nanc-ing instruments applied by public authorities with focus on fed-eral authorities (Report Federal 2009/8) were included in the range of “paradigmatic audits”. Up to now there have only been twelve of these audits worldwide. They are published on the homepage of the working group under http://www.wgpd.org.mx. As espe-cially concise and positive examples of exceptionally successful national audits, they act as benchmarks for all INTOSAI mem-bers. In addition, they are used in the context of further educa-tion events for training purposes.

Conclusions

The audit of the ACA has set new standards in the area of risk management for public investment and contributed to debt man-agement in public authorities being considerably further developed in Austria.

By auditing similar technical areas and themes in various public authorities, in a similar way, the ACA has pursued the goal of gain-ing comprehensive knowledge on administrative handling of fi nanc-ing and investment management and enhancing the preventative role of auditing. Building on this, through certain focussed consul-tations specifi c added value is made available to the audited bodies and political decision-makers, especially through the overall perpec-tive of the ACA as a federal and Laender organ. This added value can be seen in the present case in performance and key statistic com-parisons, in benchmarks, and in the analysis of decision-making processes. Through statements on the judgment of effi ciency and

24

effectiveness, and on risk-benefi t relationships, audit results have contributed considerably to the assurance of good governance and to better management of public functions.

ANNUAL REPORT 2009/2010

25

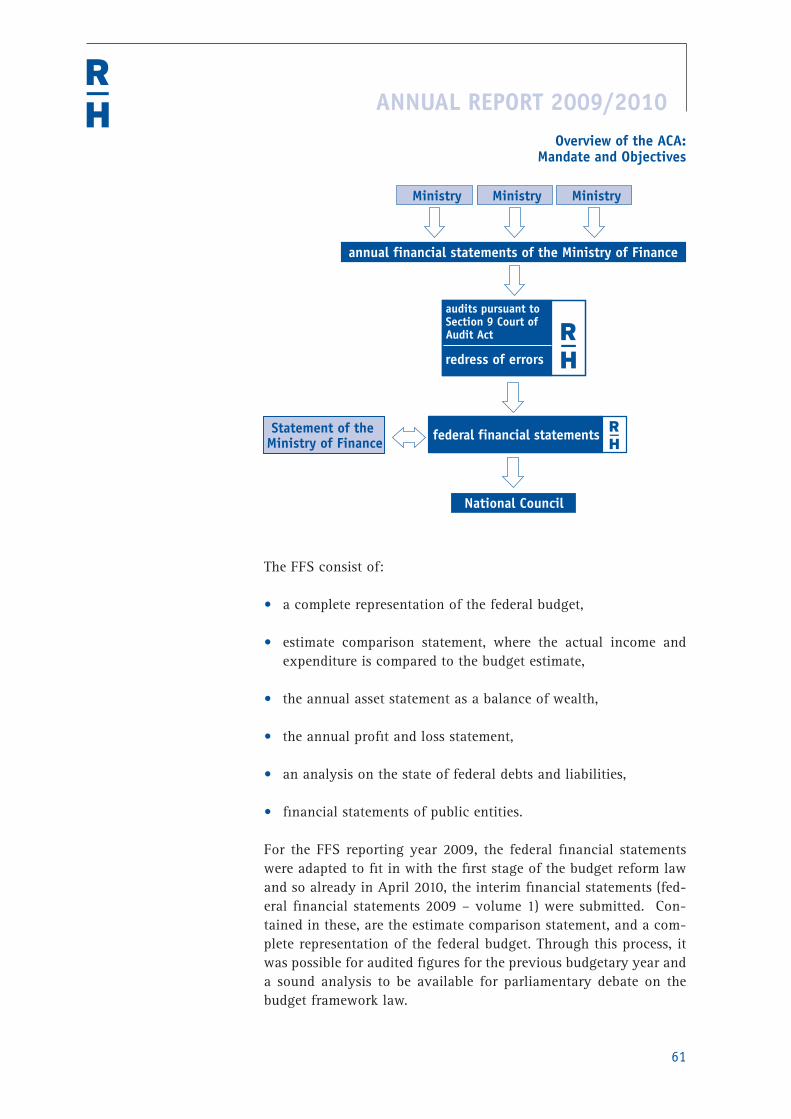

The new Federal Financial Statements

The Federal Financial Statements (FFS) have been completely revamped since 2009. The new FFS are characterised by a clear layout, which offers both experts and “budget law laypeople” a quick overview of the federal budget situation. A summary with plenty of graphics highlights to the readers the most important developments of the previous budget period. In addition, all important key data is presented on an overview sheet, which can be pulled out.

Submission of the federal fi nancial statements by the ACA is regu-lated by federal constitutional law (Art. 121 Subsection 2 Fed. Const.). Here it states that the FFS must be submitted to the National Coun-cil by 30th September, at the latest.

In 2010, the ACA sent a volume of the FFS to the National Council in April for the fi rst time. The reason for this was that, in accordance with the fi rst stage of the budget reform law which had been in force since 2009, the draft law for the future federal fi nancial framework (2011-2014) had to be presented by the government to the National Council by the 30th April 2010.

For parliamentary consultation on this federal fi nancial framework law, the ACA submitted its audited data on the management success of the previous fi nancial year, in April. The aim of the report was to make audited data for the previous budgetary year as well as sound analysis available for parliamentary debate.

Federal Financial StatementsVolume 1

26

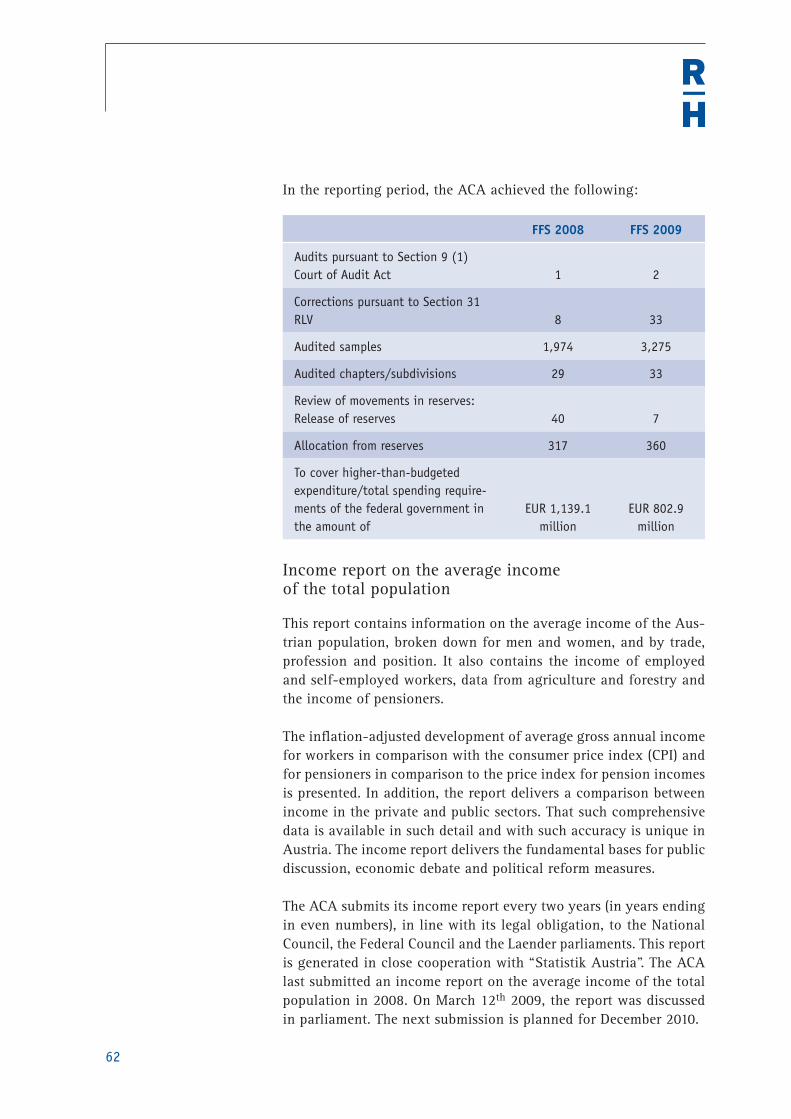

In volume one of the FFS is the estimate valuation and a complete economic representation of the federal budget. The FFS, which is presented to the National Council in the autumn, shows in addition to state income and expenditure, also the assets, liabilities, revenue and the fi nancial state of the country and public institutions. There-fore, the FFS also provides information on the state of national debts and liabilities.

The ACA completes the FFS on the basis of the annual fi nancial statements of the ministries and the accompanying audits, in accord-ance with Section 9 of the Court of Audit Act (Section 9 audits). The subject of the Section 9 audit, is the scrutiny of the annual fi nan-cial statements of the federal ministries and settlement fi ndings as regards their regularity and legality. Scrutiny of the annual fi nancial statements takes place using value-proportionate sampling from all 33 subdivisions of the federal budget settlement. With regard to the budget law reform 2013, the ACA also carried out an additional sam-ple audit of the annual asset calculation and profi t and loss state-ment in 2010.

ANNUAL REPORT 2009/2010

27

Administrative reform: Proposals await implementation

For 18 months, the experts of the ACA have been participating in the New Administration working group. Up to now, the working group has commissioned experts to analyse six of the eleven work packages. This work has been delivered to deadline. In terms of the pro-posed solutions that were presented, political decisions for their implementation are, for the most part, still outstanding.

Working group “New Administration”

As was planned in the current government programme, in February 2009 a working group for consolidation and administrative reform measures was set up. On the political side, the working group con-tained the Federal Chancellor, the Minister of Finance and the Laender governors of Vienna and Lower Austria. In practice, the heads of government were represented by two state secretaries, the Laender heads by their Laender parliament presidents.

As experts, the president of the ACA, the head of the Austrian Institute for Advanced Studies (also president of the Government Debt Com-mittee) and the head of the Austrian Institute of Economic Research take part.

Together, the ACA, the Austrian Institute of Economic Research, the Austrian Institute for Advanced Studies and the Centre for Public Administration Research make up the expert group which analyses the work packages commissioned by the working group. Represent-atives of the expert organisations work on the problems in prelimi-nary committees to create possible solutions, together with employ-ees of the public authorities, and these are evaluated and brought before the working group. In its analyses, the ACA focuses solely on fi ndings from its audits.

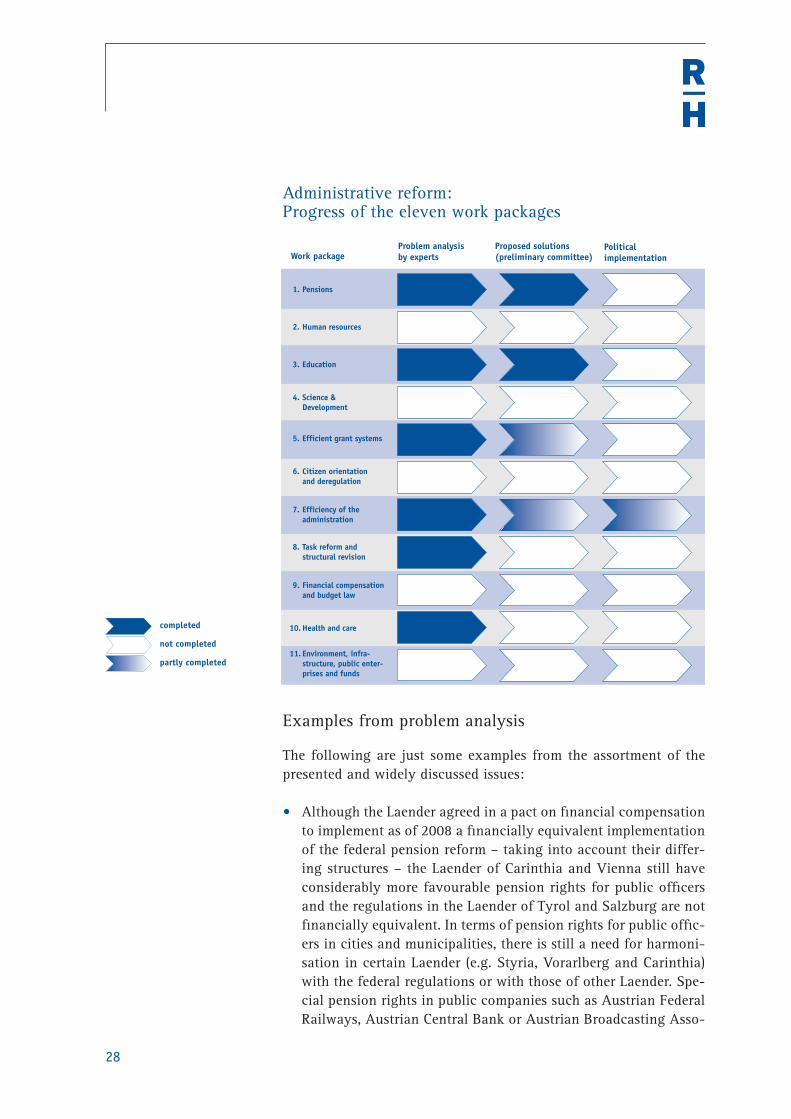

In all, eleven work packages were agreed. More than half of these have already been completed by the experts, as the following dia-gram shows:

28

Administrative reform: Progress of the eleven work packages

Examples from problem analysis

The following are just some examples from the assortment of the presented and widely discussed issues:

• Although the Laender agreed in a pact on fi nancial compensation to implement as of 2008 a fi nancially equivalent implementation of the federal pension reform – taking into account their differ-ing structures – the Laender of Carinthia and Vienna still have considerably more favourable pension rights for public offi cers and the regulations in the Laender of Tyrol and Salzburg are not fi nancially equivalent. In terms of pension rights for public offi c-ers in cities and municipalities, there is still a need for harmoni-sation in certain Laender (e.g. Styria, Vorarlberg and Carinthia) with the federal regulations or with those of other Laender. Spe-cial pension rights in public companies such as Austrian Federal Railways, Austrian Central Bank or Austrian Broadcasting Asso-

Work package

1. Pensions

2. Human resources

3. Education

4. Science & Development

5. Efficient grant systems

6. Citizen orientation and deregulation

7. Efficiency of the administration

8. Task reform and structural revision

9. Financial compensation and budget law

10. Health and care

11. Environment, infra- structure, public enter- prises and funds

Problem analysis by experts

Proposed solutions (preliminary committee)

Political implementation

completed

not completed

partly completed

ANNUAL REPORT 2009/2010

29

Administrative reform: Proposals await implementation

ciation, which were also analysed as part of this process, have shown that their employees can retire earlier and in some cases with considerably more favourable pension conditions than their counterparts on a federal level.

• In the area of health and care, a split has occurred in Austria between the legislative competence and its executive competence. In terms of GDP, healthcare spending in Austria between 1998 and 2008 was between 9.9% (minimum) and 10.5% (maximum) and therefore over the EU15 average, which was between 8.0% and 9.3%. There is an over-emphasis on inpatient care, although it is believed that well-developed outpatient services will lead to greater effi ciencies. In 2006, Austria had around 70% more acute care beds per 1,000 inhabitants than the EU average (EU15). The average hospital stay was about 10% less in 2006 and the occu-pancy rate about 70% higher than the EU average.

• The fi nancial situation of most regional health insurance funds is very strained. Between the health insurance carriers there are considerable differences as regards tariffs and provision of serv-ices.

• In terms of care, there are large differences between standards in the various Laender. This especially concerns head count, operat-ing structure, care home size and equipment. Quality assurance is not homogeneous. In all, current regulation of care is not appro-priate to meet changing demographics. Neither equal treatment of patients nor effi cient resource use is assured.

• In the area of cash benefi ts (care allowance) the legal basis is split structurally. Through a broadening of regulations for classifi ca-tion of care needs, there is further differentiation. Over 280 peo-ple are employed throughout the country in administration of care benefi ts.

• Compared with international standards, in Austria there is a com-prehensive grant system that, along with an inconsistent use of the notion of grants, is characterised by a large number of insti-tutions and instruments. Between the public authorities there are overlapping grants and a need to limit and align grants. In many cases, several different ministries take responsibility for support-ing the same area. For this reason, there is not suffi cient transpar-ency for auditing and evaluation purposes, and for grant appli-cants access to funds is made more diffi cult because information is diffi cult to get and administration abounds. The setting up of

30

an Austria-wide grant database was an aim but this has never been implemented.

Cooperation on the generation of solution proposals

The ACA operates in the preliminary committees by pointing to tech-nical solutions on the basis of its audit fi ndings, in a neutral way.

In the preliminary committee on “Effi ciency of Administration”, a range of themes were dealt with, corresponding with its broad remit. A core area was made up of proposals for the re-organisation of administrative control. Together with other expert organisations, the ACA has proposed nine priority projects and measures that should be undertaken.

One important proposal of the ACA is contained in the comprehen-sive further development and harmonisation of accounting stand-ards so that comparable data is available for audit purposes after the public authorities were bound from January 1st 2009 to coordinate budget management (Art. 13 Subsection. 2 Fed. Const.). The ACA presented its requests for timely accounting standards in the future in terms of budget control (c.f. “Budget Structure of the Laender”, e.g. in Report Lower Austria 2009/4, point 16). Up to now, there has not been suffi cient consensus on this. However, it was agreed that further debate on the subject in the Estimates and Financial State-ments Committee (VRV) would take place, in which the ACA also takes part and at which it already presented its basic position in June 2010. Progress updates are to be made regularly to the preliminary committee and the project group.

Proposals for a simplifi cation of public procurement law and an increase in the effi ciency of procurement were generated in a sub-group of the preliminary committee, with wide consensus. These pro-vide for simplifi cations in direct tendering, where auditing of price appropriateness and documenting of decisions should continue to be afforded a central role. The separation of functions in impor-tant decision-making and audit functions for construction projects should be enhanced.

On the basis of proposals from the preliminary committees, the neces-sary legal and internal administrative measures will now be prepared.

For the areas of “e-government” and “optimisation of support pro-cesses”, the ACA indicated which problem areas do not yet have suffi cient solutions in place. As a consequence, project assignments

ANNUAL REPORT 2009/2010

31

Administrative reform: Proposals await implementation

for additional implementation measures were issues (e.g. revision of the IT security handbook and its circulation in local adminis-tration, broadening of e-card and signature use, implementation of electronic income confi rmation, identifi cation of possible syner-gies between federal and Laender statistics and an intensifi cation of cooperation between Statistics Austria and the individual Laender statistical units).

In the preliminary committee for “Effi cient Services” the ACA cre-ated, together with the Centre for Public Administration Research, a document on minimum standards and parameters for the design of grants. This now sets the basis for further discussions. The pub-lic authorities were asked to establish how far they would like to see these standards as binding. In the view of the ACA, these should be as comprehensive as possible, as modern grant management should consider these standards as a minimum.

The ACA has repeatedly called for a public authority-wide grant database. To this end, it has generated the design for the necessary approvals and requirements for its establishment. This also contains the information necessary from the individual granting activities and programmes, as well as the individual cases in order to achieve meaningful solutions for grant areas and policies.

The preliminary committees on “health” and “care” were established in the working group meeting in June 2010. The ACA has already introduced its vision for the work commissions to establish the rel-evant control parameters and to determine the necessary data for both these areas of performance.

First implementation outcomes

Initial implementation occurred through a Council of Ministers res-olution on 15th September 2009, in which a total of 32 projects on e-government, support processes and administrative reform meas-ures were commissioned in individual ministries. Together with a further seven projects which were agreed, important concerns for reform were undertaken. The Council of Ministers is kept up to date with progress reports on implementation.

In terms of the harmonisation of the pension system, individual Laender have already begun the process of pension reform since the relevant crosscutting audits of the ACA were performed (see Report Federal 2009/10). A draft law proposal from the Land of Carinthia in June 2010 does not go far enough, however, to equate to fi nancial

32

reform on a federal level. Altogether in the area of Laender harmo-nisation, there is a savings potential of approximately EUR 714 mil-lion possible for the period 2010 to 2049. Of this, the reforms already implemented in the Laender of Styria (2008) and Vorarlberg (2009) have already achieved some EUR 269 million.

Under consideration of the relevant legal framework conditions, Aus-trian Federal Railways, Austrian Central Bank and Austrian Broad-casting Association have presented initial proposals to align their special pension rights.

In schools administration, there are still diverging visions on a polit-ical level, so that up to now no tangible results have been achieved. However, the expert paper was recognised by all participants as an excellent basis for further intensive discussions and negotiations.

In the view of the ACA, up to now there has been a basic prepared-ness to instigate reform measures in the reform process. However, decisive steps on a political level to seize the proposals of the expert group and bring about profound changes in the current structures and processes are still lacking.

Integration of all political powers

Already early on, the ACA pushed for cohesion of all parliamentary powers in the administrative reform process, as decision-making

Austria-Talks in March 2009 in parliament

© A

PA

ANNUAL REPORT 2009/2010

33

Administrative reform: Proposals await implementation

can only occur on a wide level with an on-going discussion process with the relevant stakeholders. The ACA therefore transmitted all the expert papers completed up to that point to the parliamentary groups of the fi ve parties and in the framework of the so-called Austria-Talks, further explained its proposals to the fi ve parties.

34

2/1/2009 – Introduction of cost-output accounting in the ACA. In a detailed model based on “New Public Management”, the costs are assigned to the services provided and in this way their value and use to the ACA can be measured. The aim is to enhance cost trans-parency in the ACA.

21/1/2009 – Basis for the peer review is laid. In a communiqué, the presidents of the ACA, Dr Josef Moser, the German supreme audit institution, Prof. Dieter Engels, the Danish supreme audit institution, Henrik Otbo, and the director of the Swiss supreme audit institu-tion, Kurt Grüter, set the seal on the project where the ACA itself is audited.

17/2/2009 – Prelude to adminis-trative reform. The working groups set up by the government meet together in the Federal Chancellery for the fi rst time. As well as Fed-eral Chancellor Werner Faymann and Vice Chancellor Josef Pröll the economic research experts Karl Aiginger (Austrian Institute of Economic Research) and Bern-hard Felderer (Austrian Institute for Advanced Studies), Laender representatives and ACA president, Dr Josef Moser, take part. Sched-ule, approach and the creation of eleven work packages are set.

10/3/2009 – Presentation of the ACA position paper 2009 at the fi rst Austria-Talks for administra-tive reform. The revised version of the fi rst edition in 2007 contains 315 recommendations for reform measures – all arising from ACA audit fi ndings.

12/3/2009 – The abolition of re-submissions is passed by the National Council. Up to now ACA reports which have not yet been discussed in the National Council plenary assembly, expire at the end of the period of legislature. Reports which must be discussed in the new law-making period must be re-submitted.

19/3/2009 – The ACA positions on budget law reform are pre-sented by the ACA president Dr Josef Moser in the consultation advisory body of the budget law reform.

Chronology 2009/ fi rst half 2010

© RH

©PD

, Ber

nhar

d Z

ofal

l

© BKA

-BPD

Positionen des Rechnungshofeszur Haushaltsrechtsreform

00

ANNUAL REPORT 2009/2010

35

Chronology 2009/fi rst half 2010

24/3/2009 – Expert group on administrative reform presents its analysis on school administration to government representatives. Issues covered are public services law, school administration and governance and further training for teachers.

16/4/2009 – Completion of the refurbishment work in the ACA headquarters. This is achieved on time and to budget.

4/5/2009 – Move from tempo-rary offi ces in Passetistrasse to the renovated ACA building in Dampf-schiffstrasse. The protected façade of the building has hardly changed. Inside, however, hardly anything of the old building remains.

7/5/2009 – Quality standards for the ACA audits are compiled in an audit handbook and made avail-able to ACA employees. Contained in this is an exact defi nition of the roles and responsibilities, as well as the individual steps of the audit process.

15/5/2009 – Customer survey starts. 1,161 people from three cus-tomer groups – general legislative bodies, audit clients and media – were called on to evaluate the per-formance of the ACA by means of online questionnaires.

26/5/2009 – Meeting of the working group for administrative reform. On the agenda are propos-als by the expert group for school administration and problem anal-ysis on the effi ciency of adminis-tration.

© M

anfr

ed S

eidl

© RH

© RH

© A

PA

ARBEITSGRUPPE VERWALTUNG NEU

SCHULVERWALTUNG

36

3/6/2009 – Traditional pension-ers’ meeting. Former employees have the opportunity to meet, talk and remember their time at the ACA.

18/6/2009 – Opening celebration for the renovated ACA building in Dampfschiffstrasse. Guest speakers include the National Council presi-dent, Mag.a Barbara Prammer, the Minister of Economy, Family and Young People, Dr. Reinhold Mit-terlehner, and the Chairman of the Laender parliament president con-ference, Prof. Harald Kopietz. The high point of the celebrations is the handover of the key from the managing director of the federal real estate company, DI Christoph Stadlhuber to the ACA president, Dr Josef Moser.

26/6/2009 – Austria-Talks. The governing parties agree with the opposition on a communal approach to administrative reform. A parliamentary subcommittee is set up.

9/7/2009 – ACA publicly an- nounces audit of the “Skylink” air-port terminal. Basis of the audit competency is the joint ven-ture agreement between the main stakeholders of the City of Vienna and the Land of Lower Austria, which, although Vienna and Lower Austria together only have a 40% share, constitute a majority in the view of the ACA. A public debate on the mandate of the ACA com-mences.

15/7/2009 – The ACA publishes its report on the fi nancing instru-ments applied by public authori-ties. The crosscutting audit shows that the strategies of the public authorities differ greatly as regards interest rate structure, extent of foreign exchange regulations and

use of derivates. The ACA fi ndings on the fi nancing strategies of the federal fi nancial agency – due to its approach method, the state is threatened with incurring a fi nan-cial loss of approx. EUR 380 mil-lion – means that a media and political storm is triggered.

© RH

© Bet

tina

May

r-Si

egl

© A

PA-R

olan

d Sc

hlag

er

© A

PA

Reihe BUND2009/8

Reform der Beamten-pensionssysteme der Länder Tirol, Vorarlberg und Wien

Finanzierungsinstrumenteder Gebietskörperschaften mit Schwerpunkt Bund

Bericht

des Rechnungshofes

ANNUAL REPORT 2009/2010

37

Chronology 2009/fi rst half 2010

21/7/2009 – Attempt to inspect Vienna airport. The building of the “Skylink” terminal is to be audited. However the airport does not re cognise the audit scope of the ACA in this case and sends the team away. This is based on three legal opinions, which came to the conclusion that a voluntary audit is not possible in line with share-holders rights.

27/8/2009 – Subcommittee of the constitutional committee: Pres-ident Dr. Josef Moser presents a paper on quality and effi ciency increases in school administra-tion, which has been put together by the expert group on administra-tive reform. The ACA once again fulfi ls its role as an advisory body.

© A

PA

31/7/2009 – “Speculation summit” in the Federal Chancellery. In the context of the report provided by the ACA on the fi nancing instruments and its fi ndings on the Austrian federal fi nancing agency in the report, the Federal Chancellor, Werner Faymann, Vice Chancellor, Josef Pröll, Secretaries of State Josef Ostermayer and Andreas Schieder, ACA presi-dent Josef Moser, central bank governor Ewald Nowotny and the chair-men of the fi nancial supervisory authority (FMA), Helmut Ettl and Kurt Pribil, discuss the border between effi cient investment and improper speculation.

3/9/2009 – ACA president Dr Josef Moser makes an impromptu speech at the Alpbach Health Symposium. In his speech he calls for structural change in the area of healthcare. He stresses that the authority and organ-isational structure in this sector are very split and that potential for pre-ventative health measures are not being properly utilised.

© RB

KA

/HBF

© RH

ARBEITSGRUPPE VERWALTUNG NEU

SCHULVERWALTUNG

LÖSUNGSVORSCHLÄGE DER EXPERTENGRUPPE

38

17/9/2009 – Visit to the ACA of the Court of Audit spokespeo-ple from all fi ve parliamentary parties. The aim of the meeting is an exchange of information and knowledge.

23/9/2009 – National Council enacts a broadening of ACA com-petence. With the change to fed-eral constitutional law, the ACA can also audit organisations in which the public has less than 50 per cent share, but which it “in fact controls”. With this decision it is determined that the ACA may audit Vienna airport.

6/10/2009 – Peer review begins. Ten peers (six employees of the German supreme audit institution and two from those in Switzerland and Denmark) begin their “inspec-tion” of the ACA.

7/10/2009 – Meeting of the working group for the administra-tive reform. The issues to be ana-lysed on the subject of “pensions” and the fi rst concrete measures for implementation on the theme of “effi ciency of the administration” is defi ned (support process, e-gov-ernment).

10/9/2009 – Press conference in the ACA at the presentation of the Annual Report. A considerable part of the report consists of the results of the customer survey. 1,161 people from three different customer groups (mandate holders of the general representative bodies, audit clients and journalists) were questioned on their satisfaction with the services of the ACA. The organisation receives a high approval rating with regard to the competence of its workers, and there is seen to be room for improve-ment in terms of sustainability.

© M

anfr

ed S

eidl

© PD

, Mik

e Ra

nz

© RH

© RH

ARBEITSGRUPPE VERWALTUNG NEU

EFFIZIENZ DER VERWALTUNG

ANNUAL REPORT 2009/2010

39

Chronology 2009/fi rst half 2010

12/10/2009 – The third course in “Professional MBA Public Audit-ing” commences, which is con-ducted in cooperation with the Vienna University of Economics and Business. Of a total of 21 par-ticipants, 15 are employees of the ACA and the remaining six are from external bodies – the Minis-try of Finance, the City of Vienna, Parliamentary Administration and the ASFINAG.

27/10/2009 – Austria-Talks. ACA president Dr Josef Moser presents the expert paper from the Austrian Institute of Economic Research, Austrian Institute for Advanced Studies and ACA on reforms nec-essary in the pension system. At the heart of the paper is the gen-eral ACA reform proposal for the Laender, which envisages a pen-sion account for new employees and parallel accounting in order to harmonise the pension system with that which exists on a federal level.

19-20/11/2009 – Seminar on corruption. 24 ACA employees take part in an internal seminar regard-ing the onset and tackling of cor-ruption. Guest speaker is the head of the state anti-corruption author-ity Mag Walter Geyer.

2/12/2009 – End of the second MBA, which was conducted in cooperation with the Vienna Uni-versity of Economics and Business. 15 ACA employees are awarded the title of “Master of Business Admin-istration (Public Auditing)” in a graduation ceremony.

© A

PA

© RH

© RH

© RH

23/10/2009 – Beginning of the inspection at Vienna airport for the “Skylink” project. An audit team consisting of seven auditors is on site to examine the fi nancial management, risk and requirements of the project.

ARBEITSGRUPPE VERWALTUNG NEU

HARMONISIERUNG DER PENSIONSSYSTEME

40

2/12/2009 – Visit to the ACA of the Federal President Dr Heinz Fischer. Following a visit through the refurbished ACA building, Fischer stresses to employees the important role of auditors, both in Austria and within the interna-tional family of audit institutions.

9/12/2009 – Meeting of the working group for administrative reform. Analyses on the issues of “pensions” and “effi cient grant provision” are presented. For both areas a corresponding preliminary committee is set up to generate proposed solutions.

14/12/2009 – The Styrian Land government resolves to entrust the ACA with an audit of the muni-cipality of Fohnsdorf. Preceding the decision, there is an intensive political debate on the subject in Styria.

22/12/2009 – The ACA sub-mits its 2009 activity report. The report includes the result of the enquiry regarding implementa-tion of ACA recommendations on a federal, Laender and local level. It shows that the ACA has achieved an impact with exactly 81 per cent of the 1,140 recommendations it published in its 2008 reports.

22/12/2009 – In its consulta-tion function, the ACA takes part in a session in parliament on the subject “Conclusions and conse-quences of the Hypo-Alpe-Adria case”. For the discussion, the ACA president, Dr Josef Moser, the gov-ernor of the Austrian Central Bank, Dr Ewald Nowotny, both chairmen of the fi nancial market supervi-sory body and the chief whip of

the fi nancial committee, meet together. President Moser makes reference to the recommendations in the reports on “Financial market supervisory authorities and super-visory tasks of the Austrian Central Bank and the Ministry of Finance” (Report Federal 2007/10) and the recommendations of the reports on the budgetary structure of the Laender.

© A

lexa

nder

Sch

uchn

ig

Reihe BUND 2009/14

Jahrestätigkeitsbericht 2009

Nachfrageverfahren 2008

Bericht

des Rechnungshofes

© Bet

tina

May

r-Si

egl

© RH

© A

PA

ANNUAL REPORT 2009/2010

41

Chronology 2009/fi rst half 2010

12/1/2010 – For the peer review, representatives of the German supreme audit institution visit the ACA once again in order to build up a picture on planning and reali-sation of the section 9 audit. Other themes of the peer review are the creation of the Federal Financial Statements and federal budget reform.

19/1/2010 – In the Carinthian Land parliament the strengthen-ing of external fi nancial control in Carinthia is discussed. As a support to the discussion, the ACA presi-dent Dr Josef Moser gives an over-view on the rights and responsibi-lities of external public auditing in other Laender.

15/2/2010 – ACA auditors visit the police executive offi ce in Munich. The working visit takes place in the context of an ACA audit of the Vienna police. Through a comparison of the working meth-ods of the Munich and the Vien-nese police a benchmark compar-ison is drawn between the two cities.

23/2/2010 – Session of the working group for administrative reform on the subject of pensions. Not only are the Austrian Federal Railways pensions discussed, but also the pensions in those Laender where the expert report has iden-tifi ed potential savings. The crea-tion of documentation on health-care reform and general function reform also commences.

5/3/2010 – In the context of the accounting knowledge community, Linz University professor Dkfm Dr Reinbert Schauer refers to the theme “Information programme for public fund accounting” in the ACA. This covers the scope of pub-lic wealth accounting, basic ques-tions on the asset statement and the estimate and fi nancial state-ments. Almost 100 employees of the ACA and other audit institu-tions take part in the event.

21/4/2010 – Publication of the fi rst part of the Federal Financial Statements (FFS). The publication of the FFS takes place in two vol-umes, for the fi rst time. With the publication of the fi rst volume of the 2009 FFS already in April, the ACA delivers to parliament the audited fi gures of the previ-ous budget year and sound anal-yses for the parliamentary debate on the federal fi nancial framework law 2011-2014.

© LP

D

© Ber

nhar

d J.

Hol

zner

© RH

© RH

© Po

lizei

Mün

chen

42

21/4/2010 – The leadership forum on innovative administra-tion holds its general meeting in the ACA. This meeting of leaders in the public services has the aim of promoting innovative enterprise in administration and strengthen-ing effectiveness.

12/5/2010 – Presentation of the reorganisation which takes place in September 2010. The number of sections and departments remain the same. Through organisation in clusters, information exchange will be improved further and coopera-tion will be enhanced.

9/6/2010 – The working group on administrative reform presents an analysis of issues in the areas of health and care. Referenced in the paper, amongst other issues, is the divided organisational structure in the in-patient and out-patient sec-tor. Also under-average activity in health prevention is criticised.

15/7/2010 – The ACA report on the investment of Lower Austrian housing promotion loans is dealt with in the Lower Austrian parlia-ment. The Lower Austrian parlia-ment had previously described the ACA report as “not serious”. In the supervisory committee and in the accompanying press conference, the ACA president, Dr Josef Moser, refutes all criticism with facts and fi gures from the report.

© RH

© RH

© RH

27/4/2010 – Swiss peers present results of the employee survey. The head of the Swiss supreme audit institution, Kurt Grüter, and his team, present results on themes such as connection to the employer, internal information and knowledge transfer, satisfaction in the workplace and career prospects. Particularly highly valued are exchange of informa-tion and knowledge, and mutual team support. A need for improvement in internal career prospects is identifi ed.

Reihe BUND2009/8

Reform der Beamten-pensionssysteme der Länder Tirol, Vorarlberg und Wien

Finanzierungsinstrumenteder Gebietskörperschaften mit Schwerpunkt Bund

Bericht

des Rechnungshofes

ARBEITSGRUPPE VERWALTUNG NEU

STAND: 31.05.2010

GESUNDHEIT UND PFLEGE

ANNUAL REPORT 2009/2010

43

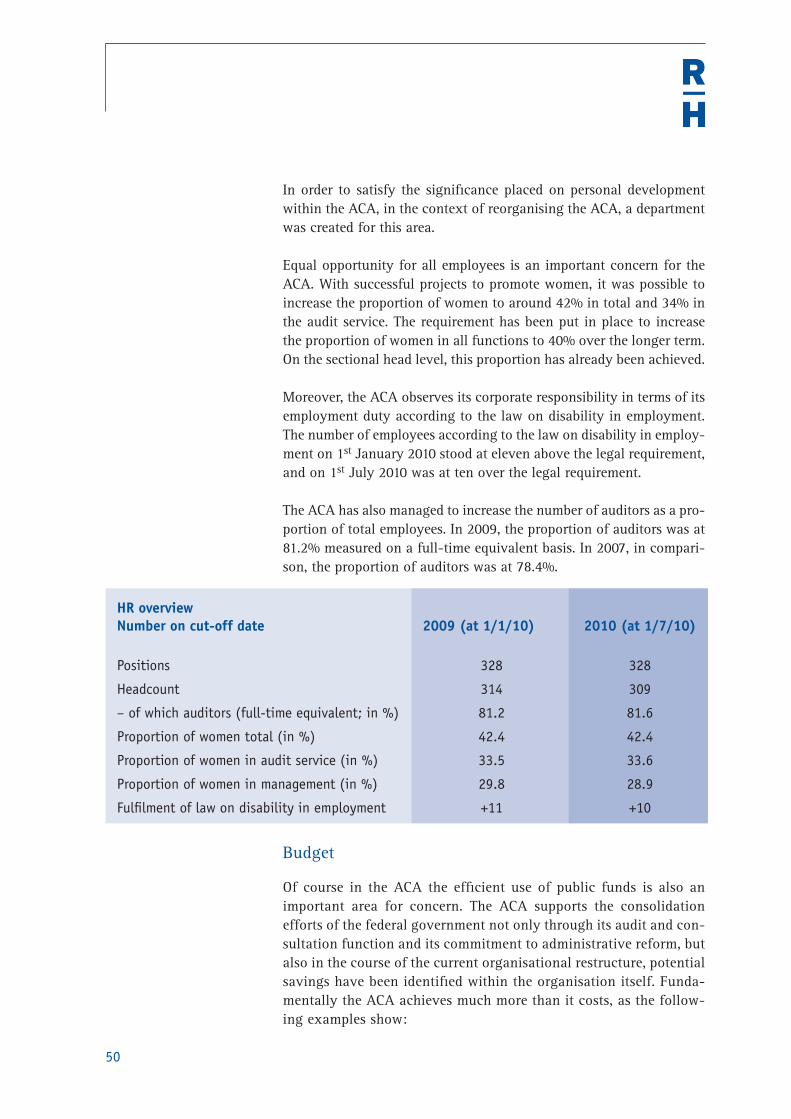

The audit competencies of the ACA are for the most part set out in the Federal Constitutional Act and in the Court of Audit Act of 1948. According to these, the ACA audits the fi nancial affairs of the state, the Laender, municipal associations and municipalities with more than 20,000 inhabitants and other bodies specifi ed by law. Furthermore, ACA competencies include the auditing of trusts, funds and institutions, and of organisations administered by an organ of the state, one of the Laender, or a municipality or by individuals who have been tasked by an organ of the state, one of the Laender, or a municipality. In addi-tion, organisations in which the state, one of the Laender, or a local authority with over 20,000 inhabitants has a share of over 50% or in which the public has a majority, are also within the remit of the ACA. Finally, social insurance funds and legal professional representatives (chambers) are also audited.

Organisationally, the ACA is an organ of the National Council. Func-tionally, however, depending on whether it is auditing a federal body, Land or municipality, it is an organ of the National Council or the Laender parliament or the Vienna municipal council and therefore a federal state/Land/municipal organ.

As its prime objective, the ACA strives for the best possible use of pub-lic funds, i.e. a reduction of costs or an increase in profi ts when utilis-ing public funds. Therefore, the ACA scrutinises whether public funds are procured and used legally, economically, effi ciently and effectively and in a sustainable fashion. In order to optimise income and expendi-ture, the ACA strives for an effi cient and effective use of funds in Aus-tria and the EU.

Through sound recommendations and highlighting possibilities for improvement, the ACA contributes to an increase in effi ciency and effectiveness in the public area and adds value for the state and for society.

According to the Federal Constitutional Act, the ACA is independent. Its independence is expressed both in the autonomy of its audit programme creation, its choice of audit focuses, audit themes, audit methodology and audit forms, as well as in the independent form of its reporting to the general representative bodies.

Overview of the ACA: Mandate and Objectives

The ACA audits on a federal, Laender and local level whether the provision of public funds is utilised in an economical, eff cient and effective way. Its core activities are auditing and con-sultation.

44

Strategic Bases

The quality of its services is fundamental to the effectiveness of the ACA. For this reason, the ACA has put together a mission statement with the involvement of all its employees. This defi nes the goals of the ACA and its self-image, as well as the particular values of independ-ence, constitutionality, sustainability, equal opportunity, objectivity and credibility in its legal mandate.

In addition to this, in the strategy of the ACA the current positioning and strategic direction for all areas of performance are established. So, added to its strategic objectives, signifi cant features on the logging of performance and effectiveness of the ACA are named. These indicators can be seen in the Medium Term Plan 2008-2010, in the key indicator system and the intellectual capital statement (number of audits car-ried out, parliamentary questions, media coverage etc.). These indica-tors are regularly collected and used as an important management tool.

The new Medium Term Plan (2011-2013) is currently being generated by a project group. In this plan, the effectiveness aims of the ACA are being particularly taken into consideration. The background for this is the introduction of impact monitoring in the new federal budget law. In line with this approach, the management function should put more emphasis on having a central control role and strengthening individual responsibility. By defi ning up to fi ve impact aims (one of these must be a gender objective), the federal ministries and supreme organs must be transparent regarding what they wish to achieve with their activities and what they wish to achieve externally, for the citizens of the country.

Quality management

The mission statement, draft strategy, medium term plan, indicator system and intellectual capital statement make up most of the qual-ity assurance system of the ACA. Additionally there is the peer review, customer survey, ACA internal commission for innovation, a targeted selection process for new employees, accredited education and further training and professional knowledge management. Added to these, all areas of activity in the ACA have their own quality standards which, for example, defi ne the processes for different phases of the audit process.

In 2009 an internal evaluation on the audit processes commenced. In the course of the pilot project, in fi ve selected audits (one per section) all audit types were examined to see how the quality standards, which the ACA has itself put in place, were followed for the core process of auditing and consultation. The project team created a checklist, against

ANNUAL REPORT 2009/2010

45

which future audits should be evaluated. In addition, on the basis of this list, they created a sample evaluation report on the chosen audits. The fi rst evaluation report and proposals for a standardised evalua-tion were agreed at the end of 2009 by ACA president, Dr Josef Moser. The pilot project went into normal operation at the end of May 2010 when the second evaluation project was fi nalised.

The ACA expects to reap particular benefi ts from the peer review which has been carried out starting in autumn 2009 by the German, Danish and Swiss supreme audit institutions.

In 2009 cost-output accounting was also implemented, in which a detailed description of costs was attributed to services rendered, so that the value and benefi t of services could be measured. By means of this cost-output accounting, it is possible for the cost of services to be transparent; they will be evaluated on a yearly basis and adjusted to current demands if need be.

Code of conduct

Through its ratifi cation of the “United Nations Agreement against Corruption”, Austria has committed to integrity, honesty and respon-sibility of its public offi cers and the development of a code of con-duct, amongst other things. In addition to this, in the government programme of 2007, the creation of a code of conduct for the public service, focussing on the prevention of corruption, was agreed upon.

In 2007, the ACA created – primarily from the already existing Code of Ethics of the INTOSAI from 1998 – a binding code of conduct for its employees. This code creates standards on the basis of the guiding values of independence, lawfulness, objectivity and credibility for the principles of “correct and legal behaviour” and integrity in all profes-sional and private dealings. It should assist all individuals to strengthen their sense of responsibility. A board of ethics was set up in the ACA to implement the code of conduct, consisting of two employer and two employee representatives, which offers advice and can be called upon to give recommendations in areas of doubt. The board of ethics is made up of Mag. Helga Berger, Dr Friedrich Pammer, Mag. Georg Plepelits and Bertram Königshofer.

Employees

The employees of the ACA are its most important resource. Their quali-fi cations and motivation are the basic prerequisite for the performance of the ACA. Therefore, not only in the selection of new employees, but

Overview of the ACA:Mandate and Objectives

46

also in the context of consistent education and further training, a high value is placed on qualifi cations.

Currently there are 309 people employed at the ACA (on 1st July 2010). More than 81.6% of these work as auditors. They all have at least three years professional experience in various areas. Most auditors are law-yers, economists or engineers.

Over the past 18 months, 21 new employees have successfully passed the intense, multi-level selection process and begun work at the ACA. Using an internal integration and trainee programme, all new entrants are communicated the necessary basic technical knowledge to prepare them for their work. An additional insight into the organisational cul-ture is offered by a 14-day trainee programme in the communication department and the editing department, the completion of a guest audit and assistance by a mentor.

13 employees went into retirement in 2009 and 2010. Most of these have remained in contact with the ACA after their retirement and pass on their knowledge and experience in the annual pensioners meeting in the ACA building.

An important basic element for effi cient performance is employee sat-isfaction and identifi cation with the ACA. In the peer review the Swiss peers carried out an employee survey at the ACA. The results showed that emotional commitment (commitment and identifi cation) and con-tinued connection to the ACA was very pronounced in staff. Com-mitment of employees could be seen in the participation level in the survey: at 74%, the response rate was above average. As well as iden-tifi cation with the company, factors of team work and work-life bal-ance also scored highly. There was seen to be room for improvement in the survey in the area of knowledge transfer.