annual report 2007 - zonebourse.com · luis ladaria (agro commodities distribution) rafael sanchez...

TRANSCRIPT

A N N U A L R E P O RT 2 0 0 7

Table of Contents

Mission Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Key figures relating to the group’s development . . . 3

Board of directors. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Financial timetable . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Evolution of the share price. . . . . . . . . . . . . . . . . . . . . 5

Corporate Governance . . . . . . . . . . . . . . . . . . . . . . . . 6

Group activities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Contribution to the consolidated result . . . . . . . . . . 12

Geographical contribution to the

consolidated result . . . . . . . . . . . . . . . . . . . . . . . . 13

Annual Report of the Board

of Directors . . . . . . . . . . . . . . . . . . . . . . . . . . . .17

Crop protection . . . . . . . . . . . . . . . . . . . . . . . . . 18

Crop nutrition. . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Industrial chemicals and environment . . . . . . . 20

Agro commodities distribution . . . . . . . . . . . . 21

Logistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Energy. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Real estate property . . . . . . . . . . . . . . . . . . . . . 23

Income statement . . . . . . . . . . . . . . . . . . . . . . . 24

Developments in the first quarter of 2008. . . . 25

Distribution of profits . . . . . . . . . . . . . . . . . . . . 26

Appointments . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Annexe to the management report . . . . . . . . . 27

Consolidated figures. . . . . . . . . . . . . . . . . . . . . .29

Consolidated income statement . . . . . . . . . . . 31

Consolidated balance sheet. . . . . . . . . . . . . . . 32

Consolidated cash flow statement. . . . . . . . . . 34

Consolidated statement of changes in

shareholder´s equity . . . . . . . . . . . . . . . . . . . 35

Notes to the consolidated financial

statements . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Statutory Accounts . . . . . . . . . . . . . . . . . . . . . . .61

Balance sheet after distribution . . . . . . . . . . . . 62

Income statement . . . . . . . . . . . . . . . . . . . . . . . 64

Limited Company (S.A.)

500, Avenue Louise

1050 Brussels

NN.0403 085 280

Ordinary General Meeting June 17, 2008

2SAPEC ANNUAL REPORT 2007

MISSION STATEMENT

Mission Statement

Formed in 1926 as a mining and chemical company, Sapec expanded its activities into various industrial and

service sectors covering the whole of the Iberian Peninsula, developing the perspective of an industrial holding

group controlling the management of various activities.

As an investor, the Sapec Group pays particular attention to generating added value by pursuing the following

objectives:

to manage a diversified portfolio of activities, capitalising, at present, on the Group’s knowledge and know how

in the field of agriculture, chemical products, animal nutrition, services with a logistical component and in the

energy generation, utilizing renewable resources primarily in the Iberian geographical area;

to develop sustainable competitive advantages through the acquisition of a leadership position or, by exploiting

niche markets in sectors offering potential growth.

This policy is implemented by:

systematically and closely monitoring the divisions in which the Group has investments;

managing the divisions as autonomous profit centres, responsible for their own cash flow in the context of yield

requirements being able to count on the Group’s support which may also include financial solutions.

This policy is an expression of the objective of increasing the company’s share value as well as ensuring a stable

and continuous dividend growth.

3SAPEC ANNUAL REPORT 2007

KEY FIGURES

Key figures relating to the group’s development

GLOBAL DATA (M€) Belgian reporting standards (1) IFRS

2003 2004 2004 2005 2006 2007

Turnover 428.8 532.0 538.2 514.9 516.4 572.5

Operating profit (2) 6.2 10.4 21.1 22.4 15.2 23.6

Net consolidated profit 9.2 10.3 11.3 13.3 10.4 22.4

Net consolidated profit - group share 8.4 9.5 10.8 12.1 7.4 20.7

EBITDA (recurrent) (3) 16.1 17.5 30.2 34.0 26.8 34.8

Shareholder’s equity (after distribution) 95.1 99.8 97.6 106.5 111.0 127.4

Total balance sheet 357.9 359.2 306.1 367.2 405.2 570.6

CONSOLIDATED DATA PER SHARE (€) Belgian reporting standards (1) IFRS

2003 2004 2004 2005 2006 2007

Number of shares 1,355,000 1,355,000 1,355,000 1,355,000 1,355,000 1,355,000

Shareholder’s equity after distribution 70.2 73.6 72.0 78.6 81.9 94.0

Operating profit (2) 4.6 7.7 15.5 16.5 11.2 17.4

Net profit group - share 6.2 7.0 8.0 9.0 5.5 15.3

Operating cash flow 11.9 13.0 23.7 24.7 19.8 25.7

Dividend common shares (gross) 1.75 1.95 1.95 2.1 2.1 2.7

Pay out on operating profit 38.0% 25.3% 12.6% 12.7% 18.7% 15.5%

Pay out on net consolidated

profit - group share 28.2% 27.7% 24.4% 23.3% 38.2% 17.6%

(1) The figures concerning 2003 and 2004 were prepared in accordance with the Belgian accounting standards, with the exception of the amorti-

sations of the consolidation differences, which were withdrawn. For 2004, the year of the transition, the primary difference concerns the profits

and losses from the real estate activity, for which the operational profits and losses were considered an exceptional result sheltered from the

Belgian standards.

(2) For the years 2003 to 2004, it corresponds to the former designation of «operational result».

(3) The figures for 2004 to 2007 do not consider the amounts of a non-recurrent nature that would normally have been considered exceptional

under the Belgian standards.

4SAPEC ANNUAL REPORT 2007

Board of directorsEduardo Catroga * Chairman

Antoine Velge * Managing Director

Philippe de Broqueville Director

Manuel Fernando Espírito Santo Director

Jean-Marie Laurent Josi Director

Xavier Scheyven Director

Günter Strauss Director

Christian Varin Director

Patricia Velge Director

Board secretaryEric van Innis *

Chief Financial OfficerJoão Sinde *

Division managersJoão Estrela (Crop Protection)

Eric van Innis (Crop Nutrition)

Fernando Gamboa (Industrial Chemicals and Environment)

José Martins Pereira (Logistics)

Luis Ladaria (Agro Commodities Distribution)

Rafael Sanchez Castillo (Energy)

Statutory auditorMazars & Guérard

Company Auditor No. 221

88, rue Gachard 1050 Bruxelles

Represented by Mr. Xavier Doyen

* Members of the Executive Committee

BOARD OF DIRECTORS

5SAPEC ANNUAL REPORT 2007

FINANCIAL TIMETABLE

Financial timetable

June 17, 2008 General Meeting 2007 financial year

June 23, 2008 Dividend Payment

September 1, 2008 Publication of half-yearly results

March 31, 2009 Publication of annual results

June 16, 2009 General Meeting 2008 financial year

Evolution of the share price in Euros

2002 2003 2004 2005 2006 2007

Ordinary shares min 31.4 39.1 44.8 67.0 82.5 90.3

max 44.5 52 72.5 96.2 97.0 114.3

Closing 31/12 ord. 43.0 46.5 72.5 93.1 90.0 102.5

Total number of shares as at 31/12 1,355,000 1,355,000 1,355,000 1,355,000 1,355,000 1,355,000

Market Capitalization 31/12 (k€) 58,265 63,008 98,238 126,151 121,950 138,888

SAPEC Shareholders No. shares Total number of shares 1,355,000

Financière Frédéric Jacobs S.A. 113,661

Soclinpar S.A. 17,969

LHI S.A. 610,973

BES Investimento S.A. (ex. ESSI) 14,179

Cobepa S.A. 204,950

Alcatel Bell Pensioenfonds VZW 42,000

Stock exchange 351,268

8.4%1.3%

3.1%45.1%

1.1%

15.1%

25.9%

SAPEC Versus Belgian all Shares

Bel 20

Brussels all shares SAPEC BEL 20

1/07

2/07

3/07

4/07

5/07

6/07

7/07

7/07

8/07

9/07

10/0

7

11/0

7

12/0

7

130,00

125,00

120,00

115,00

110,00

105,00

100,00

95,00

90,00

85,00

6SAPEC ANNUAL REPORT 2007

CORPORATE GOVERNANCE

Corporate governance

The company adheres to the Belgian Code of Corporate Governance (Lippens Code). The company’s Corporate Gover-

nance Charter entered into force on 21 June 2006. However, the implementation of its principles takes into account

the specific structure of the shareholder equity, in view of the fact that the majority family stake has ensured the

company’s stability for over eighty years.

Composition of the Board of DirectorsThe Board consists of 9 members divided Expiration du mandat

Into the following categories:

Eduardo Catroga (Chairman) AUG 2011(*)

Antoine Velge (Managing Director) AUG 2011(*)

Xavier Scheyven AUG 2009

Manuel Fernando Espírito Santo AUG 2010

Patricia Velge AUG 2009

(Five directors proposed by the majority Group)

Christian Varin AUG 2010

Jean-Marie Laurent-Josi AUG 2010

(Two directors proposed by the Cobepa Group)

Philippe de Broqueville AUG 2011(*)

Günter Strauss AUG 2010

(Two independent directors)

(*) subject to the approval of the General Meeting

The Chairman and the Managing Director are chosen from among the appointed directors by proposal of the majority

Group. The duration of the term of office of the directors is laid down in the company’s articles of association at a

maximum of 6 years. At present the terms of office run for three years.

Mission and functioning of the Board of DirectorsThe Board meets four times a year on a regular basis or whenever company is interests require it to do so.

As a general rule, the Board:

- Determines the company’s strategy and values and approves the plans and budgets;

- Decides on significant financial transactions, acquisitions and disinvestments;

- Ensures the setting up of the appropriate structures procedures and controls to achieve the aims of the company

and manage the risks;

- Supervises the performance of daily management;

- Ensures effective communication with the shareholders and other interested parties.

In 2007, the Board met five times.

The decisions are taken by a majority of votes, with the Chairman having the casting vote in the event of a tie.

The company is considered to be validly represented by two directors. It can also be validly represented by special

representatives within the limits of the power of attorney granted to them.

7SAPEC ANNUAL REPORT 2007

CORPORATE GOVERNANCE

The Board set up from among its members two consultative committees:

- An Audit Committee, responsible for auditing the financial statements, for managing the risks and the effectiveness

of the internal and external audits;

- An Appointments and Remuneration Committee responsible for proposing to the Board the appointments and re-

munerations of the directors and senior management.

Daily management of the companyThe Board of Directors may delegate part of its powers to a managing director (or even two). Within the framework of

this delegation of powers, the managing director has been entrusted with the following main tasks:

- Responsibility for the daily management of the company and the supervision of the subsidiaries;

- Ensuring the effective organisation of the company and of its subsidiaries;

- Evaluating senior management and submitting proposals to the Remuneration Committee with regard to its development

and remuneration;

- Making investment/disinvestment decisions of under EUR 1 million;

- Preparing and submitting to the Board of Directors important decisions to be taken and performance reporting on the

performance of the mission;

- Implementing the decisions of the Board of Directors.

To help the managing director to coordinate the activities of senior management, he is assisted by an Executive

Committee, usually consisting of general managers within the Group and its subsidiaries. The Managing Director is

ultimately accountable to the Board of Directors for the company’s daily management.

The Executive Committee meets monthly in the presence of the Chairman of the Board of Directors.

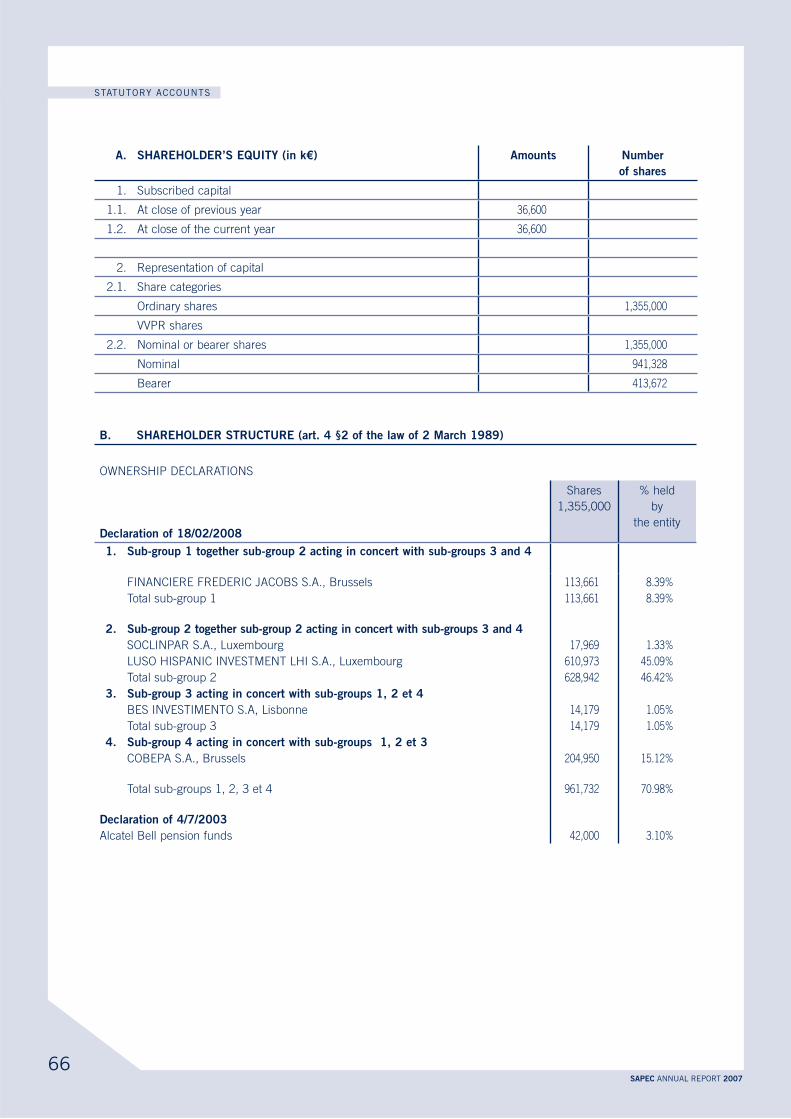

Shareholder structure and publicityAs at January 1 2008, the issued capital amounts to EUR 36,600,000, represented by 1,355,000 ordinary shares,

including 22,682 shares with strip, in accordance with the legislation.

Also in accordance with the legislation and the company’s articles of association, all shareholders who hold more

than 3% of the securities and then 5% or a multiple of this percentage, must send a declaration of transparency to

the company.

Annual General MeetingsThe ordinary general meeting takes place on the third Tuesday of June at 11 a.m. at the company’s head office.

If an extraordinary general meeting proves to be necessary, the Board of Directors shall try to hold it immediately

after the ordinary general meeting.

The general meeting deliberates in line with the agenda laid down in the letter convening the meeting.

The letters convening the meetings and organisation of meetings shall comply with the memorandum and articles of

association and the legal provisions of the Company Code.

The vote is public and is held by a show of hands. The counting of the votes and the result are given immediately.

The minutes of the general meeting are drawn up and signed by the shareholders who wish to do so at the end of

the meeting.

8SAPEC ANNUAL REPORT 2007

CORPORATE GOVERNANCE

Dividend policyThe company’s dividend policy seeks to find a balance between the yield for the shareholders and the availability

of resources to finance the development of its activities.

DerogationThe company departs from the Code (Lippens Code) on the following principles:

- The group of directors, elected by the family shareholders, is able to dominate the decisions;

- The company communicates the total remunerations paid to the members of the Board of Directors;

- The term of office of the directors can be renewed several times.

The entire Corporate Governance Charter, with detailed explanations about these derogations, may be consulted on

the company’s web site : www.sapec.be.

Financial communicationIn view of the very significant international development of its activities, the Group has chosen English as the only

language of communication, with French remaining the administrative legal language.

From now on, the annual report will be drawn up in English, with a French version being available on request from the

company’s head office.

Relations with the dominant shareholdersThere is an agreement between Cobepa and the majority Group.

AuditorsThe Auditor is the firm Mazars & Guérard, represented by Mr Xavier Doyen, Company Auditor.

9SAPEC ANNUAL REPORT 2007

GROUP ACTIVITIES

Group Activities

The Sapec Group comprises six businesses and an accessory real estate activity:

This business consists of the amination, solid and liquid formulation,

packaging and distribution in the Iberian Peninsula of phytosanitary

products earmarked for crop protection. The product portfolio mainly

consists of generic products distributed under the brand names of the

subsidiary companies, Sapec Agro (PT) and Selectis in Portugal and

Sapec Agro (ES) and Tradecorp in Spain. Together, the four companies

make Sapec third operator in the crop protection sector in the Iberian

Peninsula, after the multinationals. The Group operates a factory in

this sector of activity, located in Setúbal (PT) and two logistics centers

in Spain (Valence and Albacete).

This activity covers the production, including the synthesis of

a chelated agent and sale of a range of nutritional elements

and enriching agents with a high added value earmarked for

agriculture, in particular horticulture, viticulture, floriculture and

fruiticulture.

The main components of the range are liquid and solid trace

elements (chelates), bio stimulants (humic acids and amino

acids) as well as acidity and/or salinity correctors.

The production is based in Spain on two different sites and the products are sold in various geographical zones via

a direct commercial presence as the Iberian Peninsula, Europe, the Middle East, Mexico, Brazil and Colombia or

through agreement with local distributors in more than 55 countries worldwide.

This business incorporates the production, the packaging and

distribution in Portugal of chemical products to industry in general

and to the construction, car, manufacturing paper, environmental and

chemical sectors in particular. This activity is pursued through Sapec

Química, which operates industrial and logistical platforms in Setúbal,

covering Southern Portugal and in Ovar, covering Northern Portugal.

In the environement sector Sapec has set up the company CITRI

(Integrated industrial non-hazardous wastetreatment centre) in

Setúbal, specializing in recycling and disposal of non-toxic industrial

waste. New projects in this expanding sector are in development,

including in hazardous waste sector.

An identical center for hazardous waste will start during 2008.

Sapec holds in this project 34.1%

10SAPEC ANNUAL REPORT 2007

GROUP ACTIVITIES

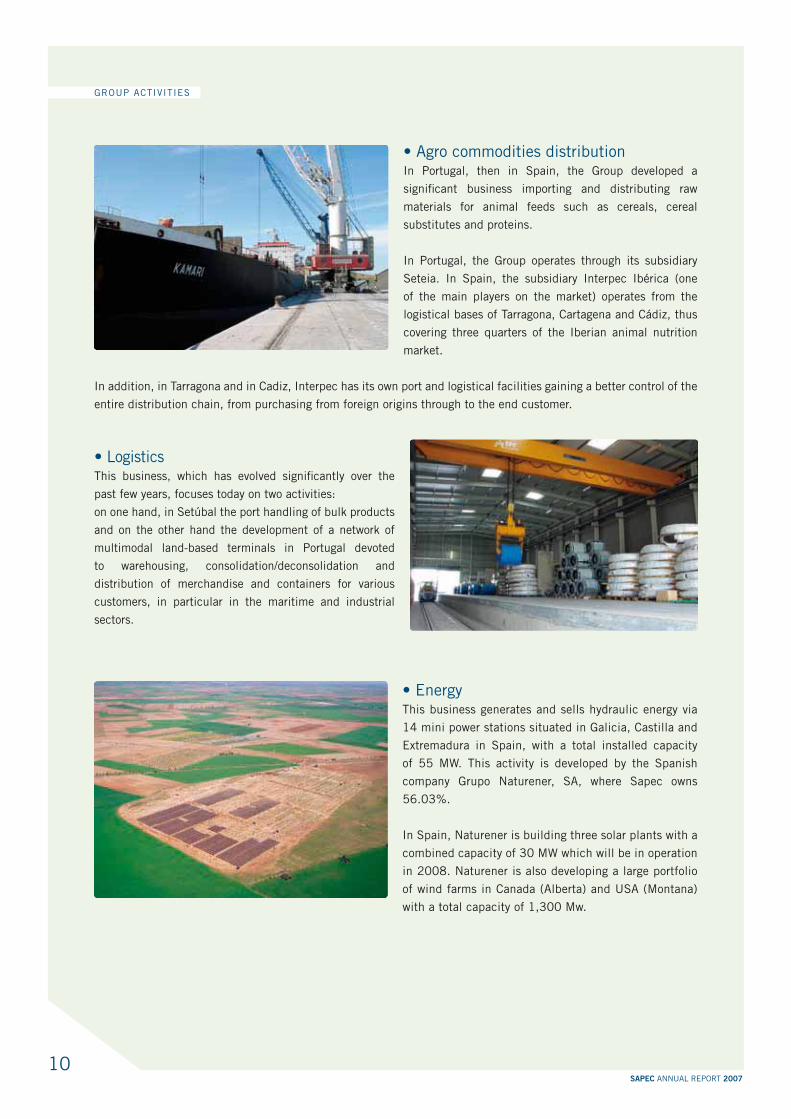

In Portugal, then in Spain, the Group developed a

significant business importing and distributing raw

materials for animal feeds such as cereals, cereal

substitutes and proteins.

In Portugal, the Group operates through its subsidiary

Seteia. In Spain, the subsidiary Interpec Ibérica (one

of the main players on the market) operates from the

logistical bases of Tarragona, Cartagena and Cádiz, thus

covering three quarters of the Iberian animal nutrition

market.

In addition, in Tarragona and in Cadiz, Interpec has its own port and logistical facilities gaining a better control of the

entire distribution chain, from purchasing from foreign origins through to the end customer.

LogisticsThis business, which has evolved significantly over the

past few years, focuses today on two activities:

on one hand, in Setúbal the port handling of bulk products

and on the other hand the development of a network of

multimodal land-based terminals in Portugal devoted

to warehousing, consolidation/deconsolidation and

distribution of mer chan dise and containers for various

customers, in particular in the maritime and industrial

sectors.

This business generates and sells hydraulic energy via

14 mini power stations situated in Galicia, Castilla and

Extremadura in Spain, with a total installed capacity

of 55 MW. This activity is developed by the Spanish

company Grupo Naturener, SA, where Sapec owns

56.03%.

In Spain, Naturener is building three solar plants with a

combined capacity of 30 MW which will be in operation

in 2008. Naturener is also developing a large portfolio

of wind farms in Canada (Alberta) and USA (Montana)

with a total capacity of 1,300 Mw.

11SAPEC ANNUAL REPORT 2007

GROUP ACTIVITIES

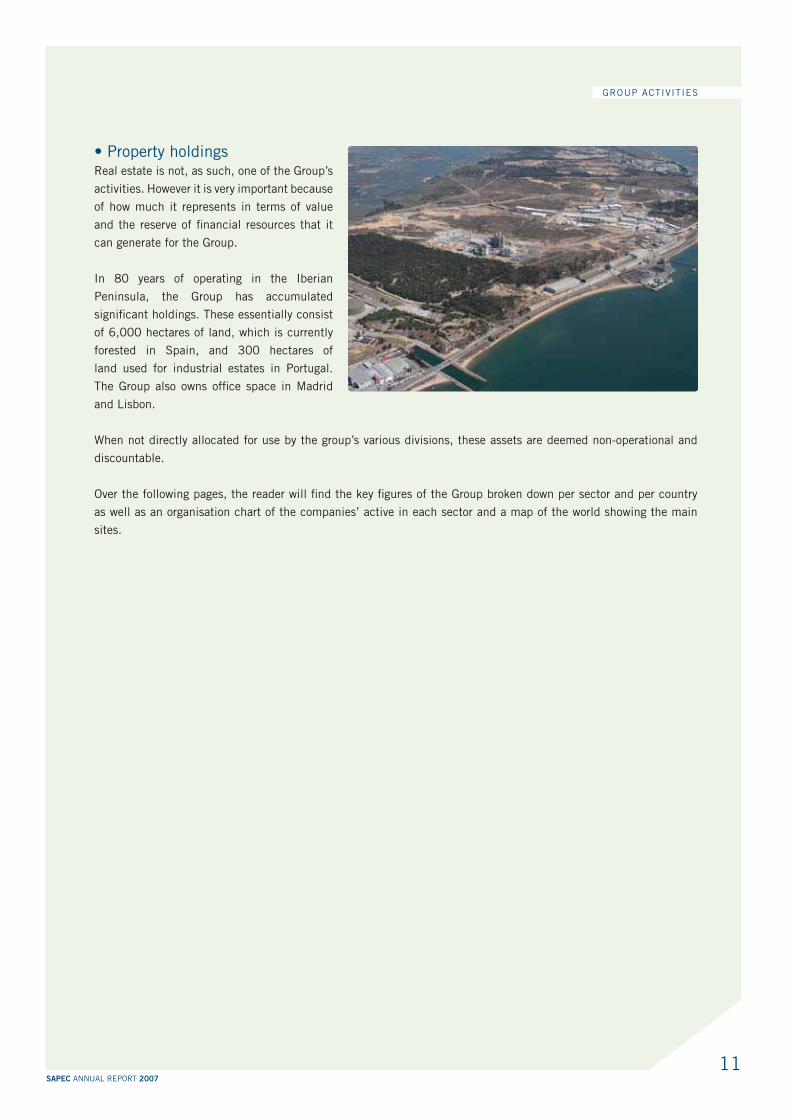

Real estate is not, as such, one of the Group’s

activities. However it is very important because

of how much it represents in terms of value

and the reserve of financial resources that it

can generate for the Group.

In 80 years of operating in the Iberian

Peninsula, the Group has accumulated

significant holdings. These essentially consist

of 6,000 hectares of land, which is currently

forested in Spain, and 300 hectares of

land used for industrial estates in Portugal.

The Group also owns office space in Madrid

and Lisbon.

When not directly allocated for use by the group’s various divisions, these assets are deemed non-operational and

discountable.

Over the following pages, the reader will find the key figures of the Group broken down per sector and per country

as well as an organisation chart of the companies’ active in each sector and a map of the world showing the main

sites.

12SAPEC ANNUAL REPORT 2007

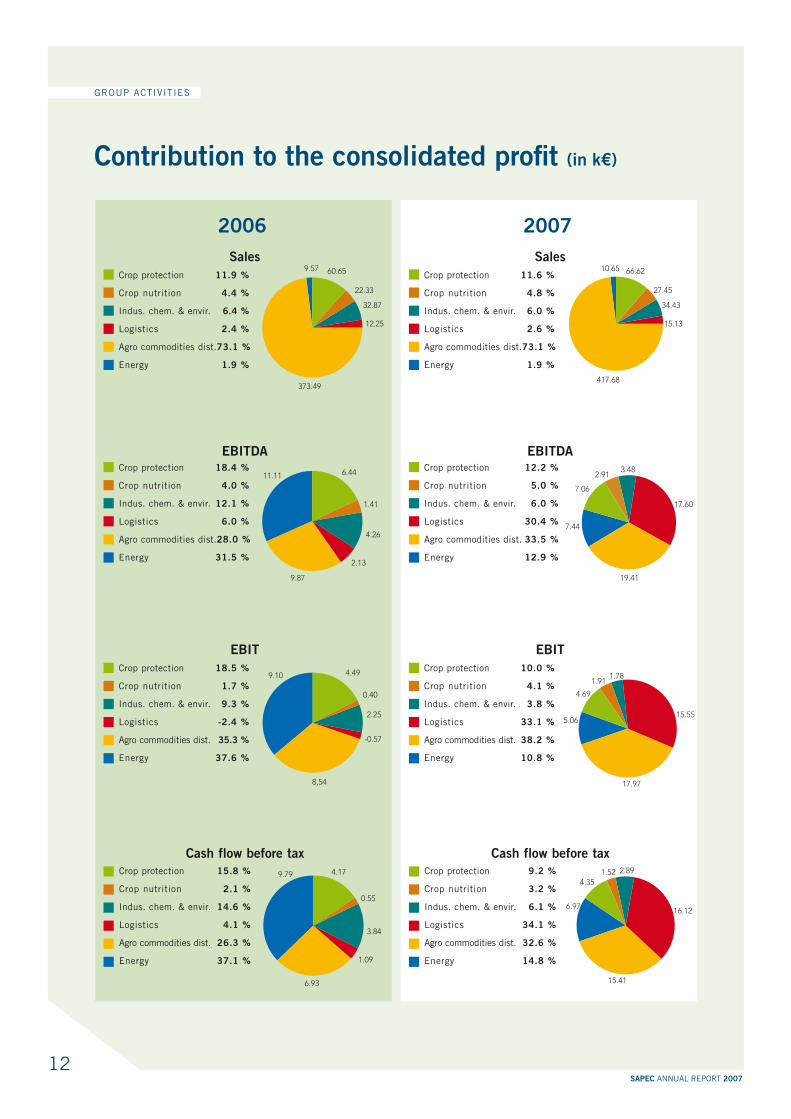

Contribution to the consolidated profit (in k€)

Sales

Crop protection 11.9 %

Crop nutrition 4.4 %

Indus. chem. & envir. 6.4 %

Logistics 2.4 %

Agro commodities dist. 73.1 %

Energy 1.9 %

60.65

22.33

32.87

12.25

373.49

9.57

EBITDACrop protection 18.4 %

Crop nutrition 4.0 %

Indus. chem. & envir. 12.1 %

Logistics 6.0 %

Agro commodities dist. 28.0 %

Energy 31.5 %

6.44

1.41

4.26

9.87

2.13

11.11

EBIT

Crop protection 18.5 %

Crop nutrition 1.7 %

Indus. chem. & envir. 9.3 %

Logistics -2.4 %

Agro commodities dist. 35.3 %

Energy 37.6 %

-0.57

8,54

9.10 4.49

0.40

2.25

Cash flow before tax

Crop protection 15.8 %

Crop nutrition 2.1 %

Indus. chem. & envir. 14.6 %

Logistics 4.1 %

Agro commodities dist. 26.3 %

Energy 37.1 %

3.84

1.09

6.93

9.79 4.17

0.55

2006

Sales

Crop protection 11.6 %

Crop nutrition 4.8 %

Indus. chem. & envir. 6.0 %

Logistics 2.6 %

Agro commodities dist. 73.1 %

Energy 1.9 %

EBITDACrop protection 12.2 %

Crop nutrition 5.0 %

Indus. chem. & envir. 6.0 %

Logistics 30.4 %

Agro commodities dist. 33.5 %

Energy 12.9 %

EBIT

Crop protection 10.0 %

Crop nutrition 4.1 %

Indus. chem. & envir. 3.8 %

Logistics 33.1 %

Agro commodities dist. 38.2 %

Energy 10.8 %

Cash flow before tax

Crop protection 9.2 %

Crop nutrition 3.2 %

Indus. chem. & envir. 6.1 %

Logistics 34.1 %

Agro commodities dist. 32.6 %

Energy 14.8 %

2007

66.62

27.45

34.43

15.13

417.68

10.65

1.91

17.97

5.06

4.69

1.78

15.55

4.35

6.97

15.41

1.52 2.89

16.12

2.91

17.60

3.48

19.41

7.44

7.06

GROUP ACTIVITIES

13SAPEC ANNUAL REPORT 2007

100

90

80

70

60

50

40

30

20

10

0

100

90

80

70

60

50

40

30

20

10

0

100

90

80

70

60

50

40

30

20

10

0

100

90

80

70

60

50

40

30

20

10

0

100

90

80

70

60

50

40

30

20

10

0

100

90

80

70

60

50

40

30

20

10

0

100

90

80

70

60

50

40

30

20

10

0

100

90

80

70

60

50

40

30

20

10

0

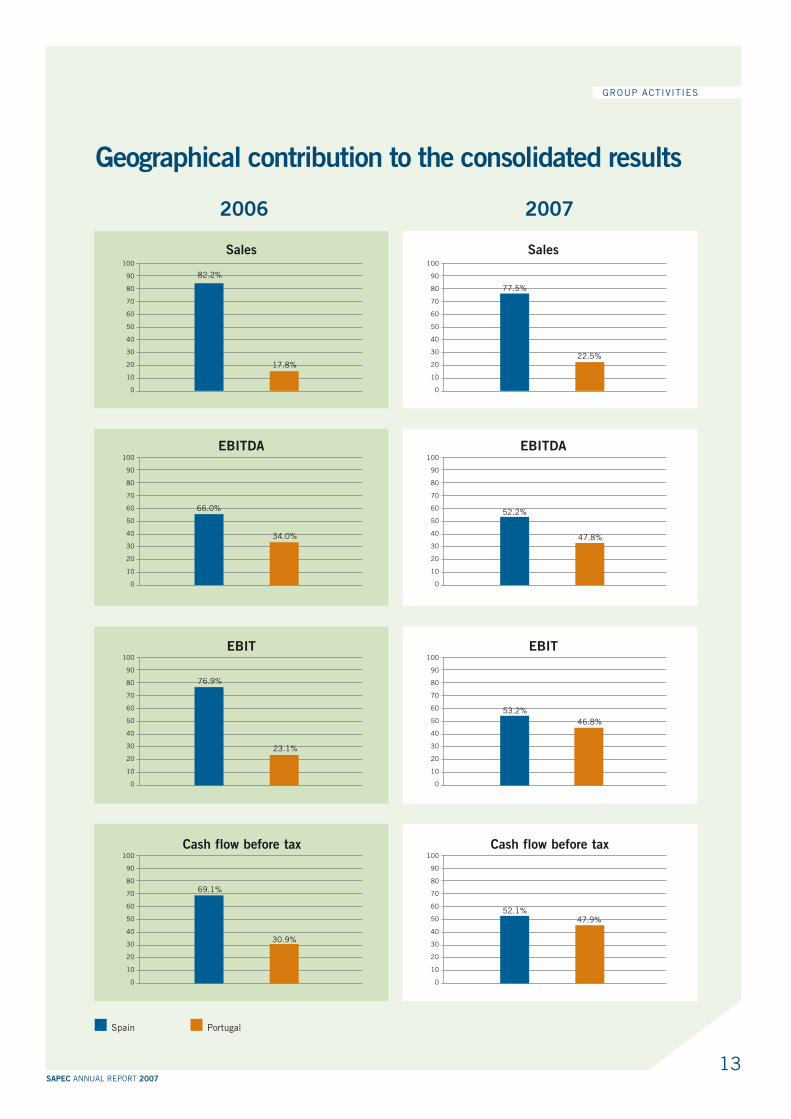

66.0%

76.9%

23.1%

69.1%

30.9%

77.5%

22.5%

53.2%

46.8%

52.1%47.9%

82.2%

52.2%

17.8%

47.8%34.0%

Geographical contribution to the consolidated results

Spain Portugal

GROUP ACTIVITIES

2006 2007

Sales

EBITDA

EBIT

Cash flow before tax

Sales

EBITDA

EBIT

Cash flow before tax

Porto

LisboaSetúbal

Ávila

Madrid

Albacete

Cádiz

Tarragona

BRAZIL

COLOMBIA

UNITED STATES

MEXICO

CANADA

Port or Cargo Terminal

Energy hydraulics

Plant

Wind energy

Photovoltaic energy

CROP PROTECTION

CROP NUTRITION

INDUSTRIAL CHEMICALS AND ENVIRONMENT

LOGISTICS

AGRO COMMODITIES DISTRIBUTION

ENERGY

POLAND

ITALIA

BELGIUM

FRANCE

SPAIN

MAROC

EGYPT

MACAO

PORTUGAL

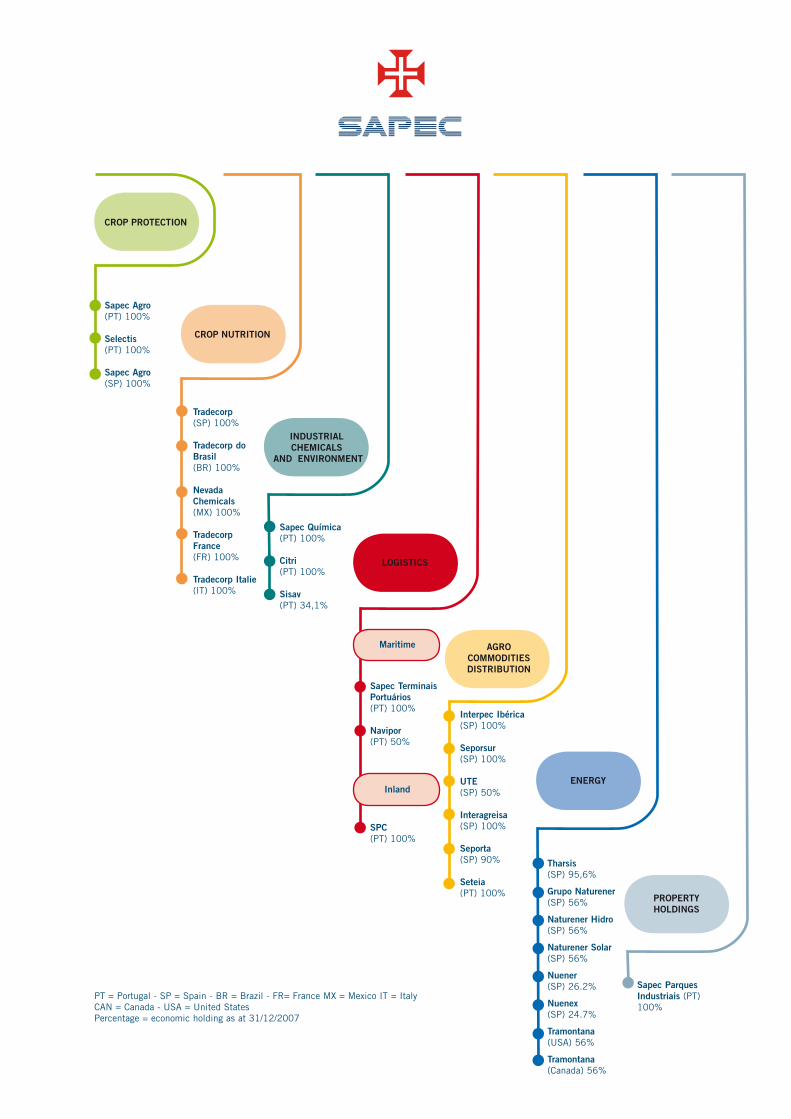

CROP PROTECTION

CROP NUTRITION

INDUSTRIAL

CHEMICALS

AND ENVIRONMENT

LOGISTICS

AGRO

COMMODITIES

DISTRIBUTION

ENERGY

PROPERTY

HOLDINGS

Sapec Agro

(PT) 100%

Selectis

(PT) 100%

Sapec Agro

(SP) 100%

Tradecorp

(SP) 100%

Tradecorp do

Brasil

(BR) 100%

Nevada

Chemicals

(MX) 100%

Tradecorp

France

(FR) 100%

Tradecorp Italie

(IT) 100%

Sapec Química

(PT) 100%

Citri

(PT) 100%

Sisav

(PT) 34,1%

Maritime

Inland

Sapec Terminais

Portuários

(PT) 100%

Navipor

(PT) 50%

SPC

(PT) 100%

Interpec Ibérica

(SP) 100%

Seporsur

(SP) 100%

UTE

(SP) 50%

Interagreisa

(SP) 100%

Seporta

(SP) 90%

Seteia

(PT) 100%

Tharsis

(SP) 95,6%

Grupo Naturener

(SP) 56%

Naturener Hidro

(SP) 56%

Naturener Solar

(SP) 56%

Nuener

(SP) 26.2%

Nuenex

(SP) 24.7%

Tramontana

(USA) 56%

Tramontana

(Canada) 56%

Sapec Parques

Industriais (PT)

100%

PT = Portugal - SP = Spain - BR = Brazil - FR= France MX = Mexico IT = Italy

CAN = Canada - USA = United States

Percentage = economic holding as at 31/12/2007

17SAPEC ANNUAL REPORT 2007

MANAGEMENT REPORT

Management Report of the Board of Directors the business activities and the consolidated results of the Sapec Group in 2007

The operating income, after a rather difficult 2006 for all the activities of the Sapec Group, experienced a strong

improvement in 2007, thanks principally to an exceptional year in the agro commodities distribution sector.

The recording of a significant capital gains further to the sale of lands of the logistical platform near Lisbon allowed

the Group’s total results to progress noticeably and reach a record level.

The principal worldwide indicators (population growth, increase in living standards in China and in India, replacement

of part of the mineral-based fuels with plant-based fuels, massive needs for biomass) lead us to believe that we are

entering a cycle where the prices of agricultural products will remain high and the demand for “production inputs”

for agriculture will remain significant. Prices will also be more volatile given the amounts of money invested by the

funds on the principal agricultural commodities markets.

This cycle should last at least until the recomposition of strategic levels of world stocks, which will necessitate one

or two record harvests in order to re-balance supply and demand. Insofar as 90% of the group’s turnover is linked to

the agricultural and food processing sector, this favourable cycle is positive for us; farmers are regaining confidence

and the increase in cash flows will make it possible to dynamise the investments in this sector.

In crop protection, the distribution channels were able in this favourable context to dispose of surplus of stocks

and our subsidiaries were once again able, in the Iberian Peninsula, to increase our market share in this sector

noticeably.

In crop nutrition, the increase in sales was good, especially outside of the Iberian Peninsula where our various

subsidiaries and sales offices made good progress.

In industrial chemical products, the year was “flat”, consumption remains low pending a stronger recovery of industrial

activity in Portugal. Different projects and options are under study in order to try to redimension this sector of activity,

whose critical mass is still too low.

In the environmental sector, treatment and re-use of industrial wastes, the year confirmed the flourishing nature of

this activity in Portugal; several development projects are being analysed.

In agro commodities distribution our activity, in this context of rising prices, was steady and profitable throughout

the year, enabling this activity and its port subsidiaries to experience a record year in terms of results. This sector of

activity contributed the most to the improvement of the Group’s operating income in 2007. The activity of our port

terminals in Spain also developed very positively.

In logistics, the activity of our port terminal in Setubal was very steady, making it possible to exceed the one million

tonnes of unloaded products. The level of productivity increased significantly, allowing a noticeable progress in the

operating income. For the multi-modal platforms, in spite of a year still in deficit, the performance showed a net

improvement further to the reorganisation plan established in 2006. As forecast, 2008 should be a positive year for

this activity.

In the renewable energies sector, 2007 was the year for defining the strategic models for our subsidiary Naturener.

This company is becoming a significant player in the sector both in Spain and in North America, with wind farms

and photovoltaic projects in the pipeline, to be built over 2008-2011, which represents around 20 times its current

installed capacity in hydroelectricity.

Given the very significant impact for our group of this investment not linked to our traditional activities, we are

presenting to you for the first time a pro forma balance sheet and profit and loss account of the group separating

traditional activities and energy.

18SAPEC ANNUAL REPORT 2007

Crop protection

In the Iberian Peninsula the market for crop protection products at distribution level expe-

rienced an increase of ± 5% on 2006.

The distribution benefited from the favourable climate to dispose of surplus of stocks ac-

cumulated since 2005. Consumption at agricultural level was sustained and it is estimated

that the average level of stocks at distribution level at the end of 2007 was reduced by

nearly 15% in comparison with the end of 2006.

In spite of the favourable agricultural context and contrary to what is happening with the majority of the other agricultural

inputs, the selling prices of crop protection have remained under pressure, negatively affecting the margins, principally in

Spain. The fact that significant quantities of products, which were going to lose their permit for sale in the course of 2007

(further to the entry into effect of the European review) were put on this market at discounted prices, and the struggle of the

multinationals against the constant increase of market share of generic products, explain this atypical trend. We think that

these factors are cyclical and that starting in 2008 a recovery of the margins should be possible.

In Portugal, SAPEC Agro achieved a turnover of 25,305 k€ in 2007 compared with 23,742 k€ in 2006, thus consolidating

its market share.

Further to measures taken, the amount of outstanding customer liabilities experienced a favourable development during the

course of the final quarter of the year and makes it possible to forecast a noticeable improvement for 2008 in the average

time of payments, which remained too long throughout the year 2007.

SELECTIS achieved a level of sales of 6,964 k€ in 2007 compared with 6,244 k€ in 2006, thus slightly increasing its

market share.

The SAPEC Group, through its two subsidiaries, remains the largest player in Portugal on the crop protection market, achie-

ving 32,269 k€ of sales, which is a 32% market share.

In Spain our two subsidiaries SAPEC Agro (E) and TRADECORP saw their sales increasing by 13% and 14%, respectively,

in comparison with 2006.

Our turnover reached 34,667 k€ in 2007 compared with 30,669 k€ in 2006, enabling the SAPEC Group to see its market

share to grow again in 2007.

The pressure on the prices and the margins was strongest in Spain, leading to an erosion in the average gross margin of 1.6%.

Overall on the Iberian Peninsula, the market having increased by 5%, our sales went from 60,647 k€ in 2006 to 66,620 k€

in 2007, that is, an increase of 10%, thus enabling the Group to strengthen its position and become the third largest player

in this sector.

In spite of the growth in sales and the slight improvement of the EBIT, the operating result (before taxes) of the sector did

not increase in comparison with 2006 (2,167 k€ in 2006 compared with 2,249 k€ in 2007). The financial costs went from

2,263 k€ in 2006 to 2,703 k€ in 2007; the average outstanding customers liabilities still too high, and the increase in the

cost of money are the explanations for this.

The operational cash flow (before taxes) went from 4,173 k€ in 2006 to 4,354 k€ in 2007.

Within the framework of the European approval system, which makes it compulsory to license and register every active ingre-

dient used in agriculture, a programme of investment over three years was approved in order to allow this sector to register on

its behalf, at European level, the principal active ingredients that make up its product portfolio.

This investment will make it possible to make access to the active ingre-

dients secure, to diversify the supplier risk, to open up new opportunities

upstream and downstream from the activity, to improve the bargaining

power significantly and, finally should enable an average improvement in

the gross margin.

The entry into force of the European review system, in the end, will have the

advantage of making the markets more transparent and of eliminating a still

large number of small players.

C

I

r

T

c

t

n

MANAGEMENT REPORT

19SAPEC ANNUAL REPORT 2007

Crop nutrition

In the Iberian Peninsula we estimate that

in terms of volume the market must have

grown ± 5%. The markets for citrus fruits and

horticultural products have suffered from imports

coming from the Middle East and the Maghreb.

However, vineyards, olive trees, fruit growing and

everything connected with grains is flourishing.

On the Iberian market we sell these products through three

commercial networks: SAPEC Agro in Portugal, Tradecorp and

SAPEC Agro (SP) in Spain. Our network outperformed the market, as

our sales increased 11% in comparison with 2006, that is 9,105 k€

compared with 8,219 k€ in 2006, the introduction of new products

and the focus on sales at TRADECORP are the principal explanations

for this.

The average gross margin remained stable in comparison with 2006,

but remains noticeably below the average gross margin achieved internationally. The Spanish market, the number one

world market, is very competitive. In spite of all this, we feel, in view of the favourable context and depending on a

dynamic strategy of differentiation, that there is potential for improvement.

Internationally, the growth of sales in comparison with 2006 was 30% and the average gross margin, in spite of the

weakness of the dollar, increased by more than two points.

launch of new products in the North.

and the average gross margin experienced significant progress, improving by nearly five points in comparison with

2006.

improvement in the average gross margin, and the setting up of the sales structure is continuing and will make it

possible to ensure a better growth rate in the coming years.

terms of quantity (more than 100%) and quality (margins, guarantees and payment terms), a new sales team

is already operational and the potential of this market is being confirmed. A loss of 488 k€ was entered in the

accounts as the balance of the reorganisation carried out in 2007.

had growth of 29%.

The total sales of this sector of activity went from 22,328 k€

in 2006 to 27,449 k€ in 2007 which is a growth of 23%.

The operational EBIT of the sector went from 399 k€ in

2006 to 2.398 k€ in 2007; an exchange loss of -247 k€,

further to the devaluation of the dollar, was entered.

The operational result (before taxes) of the sector went from

-464 k€ in 2006 to 1,010 k€ in 2007 and the operational

cash flow (before taxes) went from 550 k€ in 2006 to

1,518 k€ in 2007.

MANAGEMENT REPORT

20SAPEC ANNUAL REPORT 2007

Industrial chemicals and environment

In industrial chemical products in Portugal, the market remains weak. There was a timid

recovery in consumption, but the constant increase in the prices of raw materials could not

be completely passed on to the market in 2007, which caused an erosion of the average

gross margin. In the polymers sector, dominated by a network of small family businesses,

prudence must be exercised in the analysis of the solvency of potential customers.

An exceptional strengthening of 1,161 k€ of provision for customers of doubtful liabilities was implemented to cover

a set of small customers, and principally, the court-ordered bankruptcy of a major customer, whose total debt amounts

to 1,250 k€.

This activity therefore experienced sales that are slightly higher in terms of volume and in value than those of 2006

(+4%), i.e. 87,816 tonnes in 2007 compared with 84,440 tonnes in 2006 and 31,125 k€ in 2007 compared with

30,046 k€ in 2006.

The average gross margin experience a slight erosion of 0.6% in comparison with 2006.

New products were launched and others are under study in the area of elastomers and conventional products.

Two players and traditional competitors have been put up for sale by their shareholders and we have analysed the two

dossiers.

With the shareholders of one of the two companies we have reached an agreement on the buyout of a major part of the

company’s business.

This business is complementary to ours and represents a turnover of more than 14,000 k€ an a potential EBITDA of

more than 900 k€ per year.

The acquisition will therefore enable us to significantly increase our market share in this sector, enlarge the customer

portfolio and enter into new industrial markets. The due diligence is under way.

The environment (CITRI activity) again experienced a good year. The tonnes of non-toxic industrial wastes received for

disposal were on the increase, i.e. 125,798 tonnes in 2007 compared with 105,720 tonnes in 2006. Prices stayed at

a good level throughout the year with the result that the turnover for this activity increased from 4,503 k€ in 2006 to

5,475 k€ in 2007.

The production on an industrial scale of a secondary fuel from the residue received started up, and nearly 5,000 tonnes

of this type of fuel have already been sold.

The operational and structural costs are in line with the objec-

tives.

The EBITDA in 2007 is placed at 2,815 k€ compared with

2,196 k€ in 2006 and the EBIT at 1,807 k€ at 2007 com-

pared with 1,028 k€ in 2006.

In the environmental sector the following elements are worthy

of note:

site, whose capacity is more or less equal to the sum of

the first two, is being completed and the inauguration is planned for the second quarter of 2008.

stage. This project, the SISAV, is a consortium in which SAPEC has a participating interest of 34,1% and the invest-

ment of a total amount of 27,000 k€ is financed by a non-recourse “project finance”. The start-up of the activity is

planned for the end of June 2008.

and residues. Several projects are currently being studied.

In

In

re

be

gr

p

MANAGEMENT REPORT

21SAPEC ANNUAL REPORT 2007

For the sector as a whole, the operating income (before tax) and after establishment of the exceptional provision went

from 1,868 k€ in 2006 to 1,180 k€ in 2007 and the operational cash flow (before) went from 3,842 k€ in 2006 to

2,887 k€ in 2007.

Agro commodities distribution

Interpec Ibérica in Spain broadly anticipated, then followed the rise in the prices of

agricultural raw materials, having thus cleared record pre-tax profits of 10.7 M€. Good

decisions taken at the right time in respect of both products and shipping allowed us to

achieve this figure.

The volumes handled were slightly lower than those for 2006, at significantly higher prices.

We were voluntarily selective during the second half of the year since the risks of “non-fulfilment” are higher in a market

that is so volatile. Since the beginning of 2008, we have noticed a drop in consumption; many meat producers have

not succeeded in earning money against the backdrop of rising prices for animal feed and prefer to send their livestock

to slaughter.

Although certain products (and freight in general) have experienced a downward correction from 20 to 30% since the

beginning of the year, the quotations remain high. We are anticipating the continuation of this situation in the medium

term, as long as the worldwide strategic stocks of agro commodities have not been reconstituted.

Our port subsidiaries Seporta and Seporsur performed very well. Aside from food processing products, Seporsur un-

loaded more than 1 million tonnes of clinker, tripling the volume unloaded in 2006.

Seporta also increased its activity and its income in comparison with 2006.

In Cadiz (Seporsur) we are in the process of building an instal-

lation for the storage of vegetable oils intended for the biodiesel

market. It should be operational in the month of April 2008 and

will make it possible to further diversify our range of products and

customers.

Our commercial subsidiary in Portugal, Seteia, also performed well

and succeeded in increasing its market share and its income.

We are analysing a project for a bioethanol production plant from

maize, in association with a local partners, to be installed on our

land in Setúbal. No definitive decision, , will be taken as long as

the Portuguese legislative framework is not final and positive for this

project, for which the investment could be on the order of 80 M€.

Logistics

The Group’s logistics sector today consists of a land sector (multi-usage and multi-

modal platforms) and a port sector (bulk terminal at Setúbal and 50% of Navipor,

port subsidiary specialising in Roll-on/Roll-off at Setúbal as well).

In the land sector in an economic context that is still troubled in Portugal, sales

increased by 12% in comparison with 2006 thanks to the reshaping of the sales

teams. The container segment was relatively weak, compensated by the groupage and logistics activity. It was still

not possible to reach the “breakeven-point” in 2007.

The sale, in the form of a “sale-partial rent-back” of the Lisbon terminal (Póvoa), allowed SPC to record a very signi-

ficant capital gain and noticeably reduce its debt and its net investment. The R.O.I. for this activity should improve

MANAGEMENT REPORT

22SAPEC ANNUAL REPORT 2007

noticeably in 2008. On the other hand, the opening of the new terminal in concession with the Portuguese railways

in Lisbon will make it possible to stimulate the railway activity between Lisbon and Valongo (Porto) benefiting the

two terminals. Economic activity in Portugal remained weak in 2007, but certain recent signs lead us to hope for a

better 2008.

Concerning port activity, the bulk terminal at Setúbal was sustained, and exceeds one million tonnes for the first

time in its history.

New customers (and products) like clinker and sugar had a significant impact on the dilution of the fixed costs and

therefore the increase of the income. The installed capacity of our solid bulk quay is near saturation and major

investments, both for increasing the unloading capacity and for improving the environmental conditions, will be

necessary in the next few years. We are continuing to negotiate with

the authorities of the port of Setúbal concerning the possibility of

extending our quay.

The quay for bulk liquids unfortunately continued to be under-uti-

lised as long as no major industrial installation for fuels is installed

on our land in Setúbal.

The subsidiary Navipor closed the financial year with a profit, with

sustained activity but without news as to the announced future

terminal concessions for Setúbal.

Energy

The production of our hydroelectric plants in Spain increased by 12% in com-

parison with 2006, but the turnover increased by only 2% due to a price per Kwh

slightly lower than that obtained in 2006. The increase in production was notice-

able above all in the spring as autumn was rather dry.

Concerning our developments in the United States and Canada, we greatly in-

creased the management team based in San Francisco and opened an office, at

the beginning of 2008, in Calgary for our activities in Canada. In fact, after the

acquisition in 2007 of the company West Windeau, which has projects in the pipe-

line on the order 700 MW in the southeast of the province of Alberta, we notice-

ably increased our presence in this country. We also convinced the management

of West Windeau to remain with us and to take charge of our portfolio of projects

in Canada.

Insofar as the portfolio of projects is concerned, we have cut out a certain number

of projects that had little chance of success and strengthened the Canadian port-

folio.

The portfolio of secured projects, for which we have the authorisation, the land,

the connection to the electrical network and a major part of the turbines, are the

following:

network by the end of 2008;

mid-2009;

MANAGEMENT REPORT

23SAPEC ANNUAL REPORT 2007

The portfolio of projects not yet secured, for which we do not yet have

the turbines or all the necessary authorisation, is the following:

for the end of 2009 or 2010.

in 2010 or 2011.

We are in the process of finalising the authorisations for the electrical

line that is meant to connect the two Wild Rose projects (400 MW) to

the Canadian network.

We are thus considering a total portfolio of 1000 MW to be build

between 2008 and 2011, a remain of around 300 MW is still under

analyse.

In photovoltaic solar energy, we are in the process of building four projects totalling 29 MW in Spain. All these

projects will be terminated in July/August 2008 and should benefit from the attractive price premium system cur-

rently in effect until 28 September 2008. We have other projects in the pipeline amounting to around 90 Mwp to

be built between 2008 and 2009, pending announcement of the new price premium system in force as of the end

of September 2008.

The majority of the costs of development and start-up of our North American and Solar activities are capitalised, as

well as the financial costs.

For this sector, the recurring profit is being maintained in practice at the level of that of 2006; the great difference

from the preceding year is located at the level of non-recurrent income. In 2006 we recorded the largest share of

the capital gain on the sale of Naturener Eolica in Spain, with the balance recorded in 2007. A supplement could

occur between 2008 and 2010 depending on whether or not the final authorisations for the projects in Castilla Leon

are obtained.

Real estate property

Only one plot in the infrastructured part of the industrial

park of Setúbal, where we still have a small stock of lots,

was sold in 2007. This part of the park has already entered

into its phase of normal operation with management

provided by the Group.

Finally, works to improve the road access to the industrial

zone, where our park is located, has begun. This new

infrastructures will benefit the future development of the

park.

In Lousal, where the Group’s old pyrite mine is located,

an urban tourism plan has been approved. Contacts have

been made with various promoters interested in the purchase of the land.

MANAGEMENT REPORT

24SAPEC ANNUAL REPORT 2007

Income statement

Analysis of the Profit and Loss Statement reveals a turnover increasing from 11% and an operational result that

went from 15,203 k€ in 2006 to 23,562 k€ in 2007, which is an improvement of 55% in spite of the entry of

3,839 k€ in non-recurrent costs. 1

After a difficult 2006 for some of our activities, the increase in the operational income is due to a slight improve-

ment in the crop protection sector, to good progress in the crop nutrition sector and the logistics sector, and finally

to a record in agro commodities, which by itself explains the improvement in the income.

This improvement in the operational result is found at the level of the EBITDA (gross operating profit) which went

from 26,790 k€ in 2006 to 34,835 k€ in 2007, and is an increase of 30%.

As a consequence of the increase in the net debt and above all the soaring of the cost of money, the net financial

costs went from -8,595 k€ in 2006 to -10,974 k€ in 2007 (+ 28%). The increase in the net debt linked with the

investments in renewable energies has no impact since the interest has been capitalised.

The products of sales of non-current assets and on investments for a total of 16,185 k€ cover the sale of the land

of the logistics platform near Lisbon, the sale of an old logistics warehouse near Porto and a part of the capital gain

on the sale of our wind farm projects in Spain, the major part of which was already recorded in 2006.

The income before tax was 29,104 k€, as compared with 14,634 k€ in 2006 and the net consolidated income

reached 22,375 k€ in 2007 compared with 10,376 k€ in 2006 (+116%).

The income share of the Group stands at 20,712 k€ compared with 7,448 k€ in 2006.

The significant growth in the total assets on the balance sheet, which went from 405,224 k€ at the end of 2006

to 570,594 k€ at the end of 2007 (+165,370 k€ or +41%), is essentially due to the investments made in the

renewable energies sector (wind in the USA/Canada and photovoltaic in Spain), as the weight of this sector in the

assets in the balance sheet went from 26,412 k€ in 2006 to 147,365 k€ in 2006 (that is +120,953 k€).

The Group’s net consolidated debt as a consequence primarily of the same investments went from 167,202 k€ at

the end of 2006 to 270,481 k€ at the end of 2007, that is +103,279 k€, 92,603 k€ of which is connected with

the energy sector.

Aside from projects in renewable energies, the net debt went from 154,739 k€ at the end of 2006 to 165,415 k€

at the end of 2007, which is an increase of 7%, concentrated primarily in the sector of the distribution of agro com-

modities, in which needs for working capital increased further to the severe rise in the prices of raw materials.

The Group’s other activities were able, in general, to reduce their needs for working capital.

The solvency ratio (excluding renewable energy projects) is 34.6% (34.1% in 2006). The shareholder equity of the

Group is located at 131,232 k€ compared with 113,914 k€ en 2006, which is an increase of 15%.

The long-term financing went from 224,585 k€ in 2006 to 256,570 k€ in 2007. Excluding projects in renewable

energies, which went from 224,585 k€ to 235,395 k€, in spite of the reduction in the long/medium term debt,

which went from 95,480 k€ in 2006 to 89,024 k€ in 2007.

MANAGEMENT REPORT

1 Project development costs (costs not activated USA\Canada in wind power, bioethanol project in Portugal), research costs, restructuring

costs (Brazil) and provision for non recurrent bad debt expense (distribution of chemical products).

25SAPEC ANNUAL REPORT 2007

The reduction of this debt originates from the reduction in the leasing of 2,850 k€, further to the sale of the plots

of land in Póvoa in Portugal and the short-term reclassifying of the bonded debt of 10,492 k€, which will mature

in September 2008. The negotiations for its replacement are already under way.

In compliance with legal obligations, the Group advises that it is maintaining a contract for share liquidity with a

banking institution charged with its discretionary management. On the date of 31/12/07, the Group held 881 own

shares, acquired in respect of the decision of the General Assembly of 19/06/2007.

Developments in the first quarter of 2008

The agricultural and food processing sectors are experiencing a favourable cycle which should benefit our activities con-

nected with these sectors. In crop protection, growth in the market share is still possible in Spain and continuing the

improvement in the working capital remains the principal objective in Portugal. In crop nutrition, international growth will

be able to continue as the result of investments in commercial structures and developments of new products completed.

In agro commodities distribution, the year 2007 was completely exceptional, because all the factors were positive. The

first quarter is giving positive indications; however, the year 2008 should be normal for this sector.

In the logistics sector, business remains sustained at the beginning of 2008, which is the result of the new commercial

dynamics established by this subsidiary.

As regards the industrial chemical products and environment sector, the acquisition of the business of the competing

company should be concretized soon and will have a positive impact already in 2008. The SISAV project (environment)

will be able to start up in June 2008.

In wind energy, the construction of the Glacier Wind project, Montana, is in the start-up stage.

In photovoltaic energy in Spain, the construction of the first four projects totalling 29 MW is under way.

In order to finance these projects, the shareholders of Naturener contributed 180 M€ in the form of an increase of capital

in October 2007 and March 2008. Sapec S.A. obtained a medium-term bank loan in March 2008 to finance the Group’s

part of capital increase, for an amount of around 80 M€.

In this sector and as a shareholder of Naturener, Sapec is studying the various options for its strategy. These could lead to

the entrance of new partners, the disposal of our stakes or the sale of one or other branch of this sector.

The first quarter is developing in line with our prospects, however it is too early to make concrete.

MANAGEMENT REPORT

26SAPEC ANNUAL REPORT 2007

MANAGEMENT REPORT

Distribution of profits

The net profit of the company Sapec S.A. amounts to 3,550.5 k€.

The balance for distribution amounts to 23,552.9 k€.

The Board of Directors proposes the balance to be distributed as follow:

Dividends 3,697.4 k€

Directors emoluments 108.9 k€

Carried forward 19,746.6 k€

We will also propose to the meeting, by separate vote, to give a discharge to the Board Members for their management

and to the Auditor for his inspection assignment.

Appointments

We call your atttention that the mandates of Mr Eduardo Catroga, Mr Antoine Velge and Mr Philippe de Broqueville

will expire at the date of the general meeting of June 17, 2008.

These Board Members can be re-elected, and we propose that you renew their mandates for a duration of three years,

that is until the general meeting of 2011.

27SAPEC ANNUAL REPORT 2007

Annexe to the management report

Financial risk management

The management of financial risks is an integral part of the Group’s management.

The Board of Directors defines the financial policy and the Management Committee establishes the respective

objectives.

Within the scope of its operational activities, the Group is exposed to the risks of the market (exchange rates, raw

materials and interest rates), of credit and of payments. In keeping with the policies and objectives established, the

Group undertakes operations with financial derivative instruments exclusively within the framework of operational

transactions of assets, liabilities or of anticipated operations.

The market risks arise essentially from the exposure to monetary fluctuations, in particular vis-à-vis the American

dollar, the Brazilian réal and the Mexican peso, from the interest rates and from the prices of raw materials.

For certain raw materials connected with the business activity, the Group also uses instruments for covering

fluctuations of the various quotations.

Insofar as the risk of the raw materials is concerned, principally in the business activity, it arises basically from

movements on the world market connected with purchasing programmes of soy and cereal grains. The risk is

attenuated through appropriate actions on the various quotation markets. The covering of this risk is managed by the

concerned companies of the Group, through the adoption of appropriate covering instruments.

The interest rate risk arises from the cash flows connected with loans at variable interest. This type of risk is

controlled as much as possible through the use of derivative instruments, basically of the “options”, “FRA’s” and

“swaps” type.

The credit risk arises from the failure by third parties to meet their contractual undertakings arising from bailments

of availability, from the purchase of financial derivative instruments or from the portfolio of commercial loans.

The credit risk connected with the management of the availabilities or of the financial derivative instruments is

minimised by the choice of entities with a high financial rating.

The credit risk connected with commercial transactions is controlled by setting up systems for analysing the financial

capacities of the customers to which credit ceilings are assigned, and by subscribing to credit-insurance policies with

institutions with a high financial rating, any time it is possible or feasible.

The risk of a lack of liquidity, associated with the difficulties some companies in the Group have in satisfying their

financial obligations, is resolved by a Central Accounts Department which gives a guarantee to make the entries of

cash and the maturity dates of loans and other financial obligations coincide, and for the systematic and sustainable

maintenance of a certain volume of rapidly mobilisable liquid assets.

The management of the financing debts is done by the Central Accounts Department, in such a way that it does not

experience any difficulty in refinancing its operations.

MANAGEMENT REPORT

28SAPEC ANNUAL REPORT 2007

Environmental risks

The production and stocking sites of the Group, as well as the transport of the products, especially for the chemical

products, for the treatment of industrial residues and for the port activities, are exposed to the risks of environmental

contamination.

The Group systematically seeks to have the best technical solutions available for the installations/equipment, that is

for the handling, the storing and transport of the products.

Cumulatively, insurance policies are systematically taken out each time that this proves necessary and possible

(certain cases are not covered by the insurers or reinsurers), whether the contamination is accidental or progressive

(case of CITRI).

MANAGEMENT REPORT

29SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

Consolidated figures

30SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

31SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

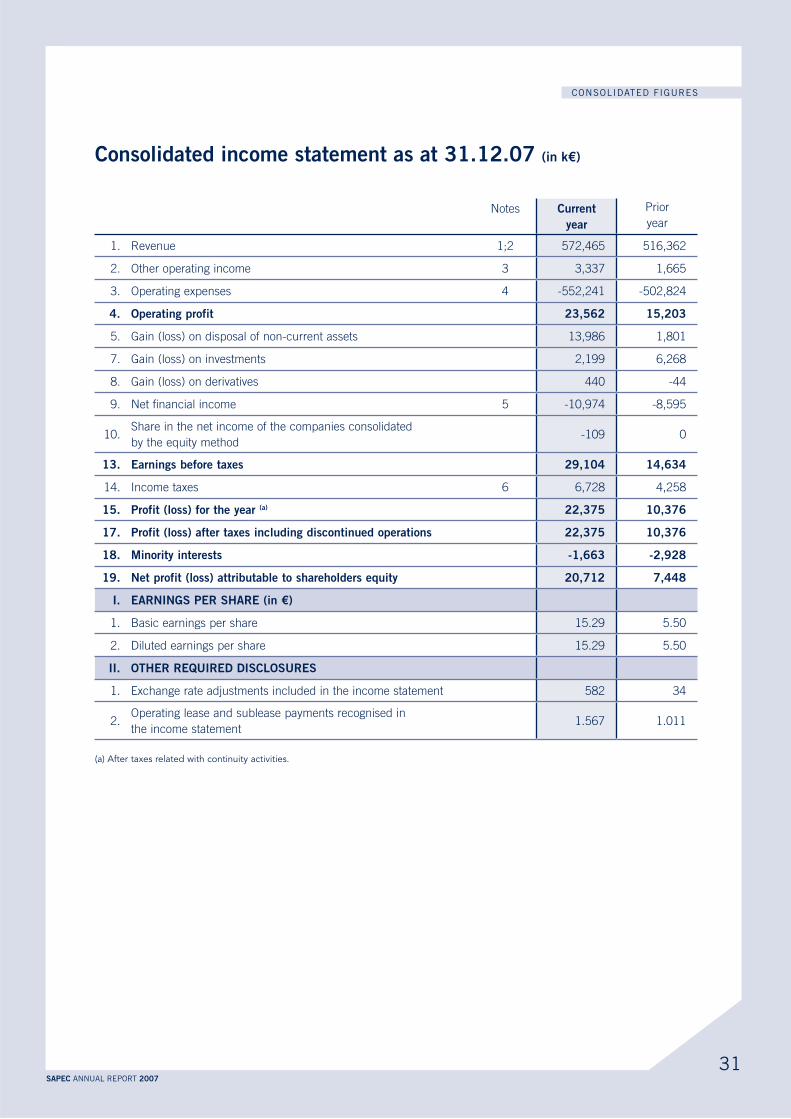

(in k€)

Notes Current Prior

year

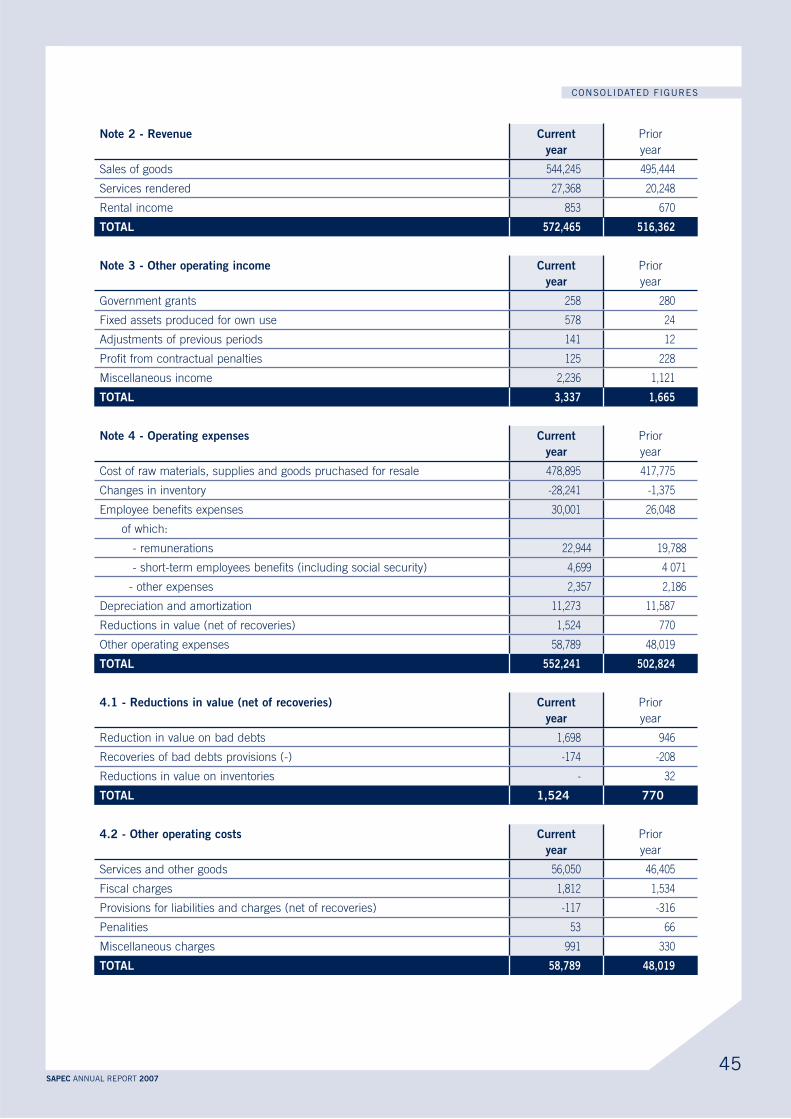

1. Revenue 1;2 572,465 516,362

2. Other operating income 3 3,337 1,665

3. Operating expenses 4 -552,241 -502,824

5. Gain (loss) on disposal of non-current assets 13,986 1,801

7. Gain (loss) on investments 2,199 6,268

8. Gain (loss) on derivatives 440 -44

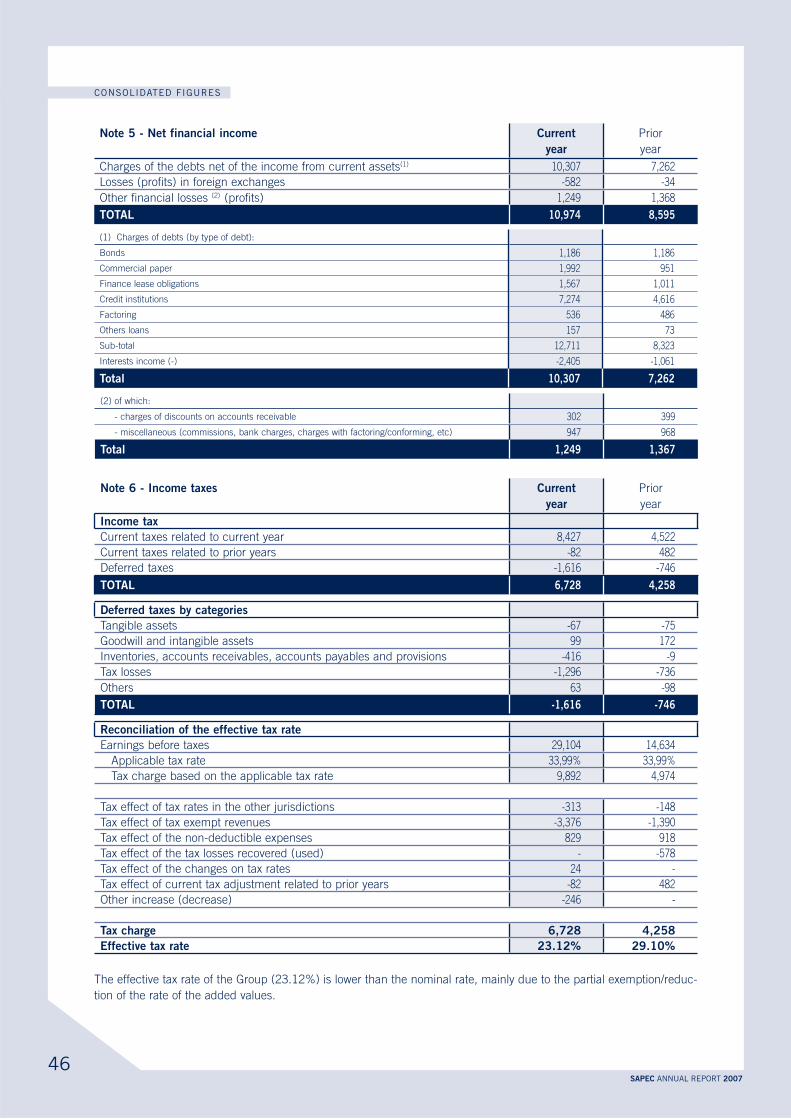

9. Net financial income 5 -10,974 -8,595

10.Share in the net income of the companies consolidated

by the equity method -109 0

14. Income taxes 6 6,728 4,258

(a)

1. Basic earnings per share 15.29 5.50

2. Diluted earnings per share 15.29 5.50

1. Exchange rate adjustments included in the income statement 582 34

2.Operating lease and sublease payments recognised in

the income statement1.567 1.011

(a) After taxes related with continuity activities.

32SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

(in k€)

ASSETS Notes Current Prior

year

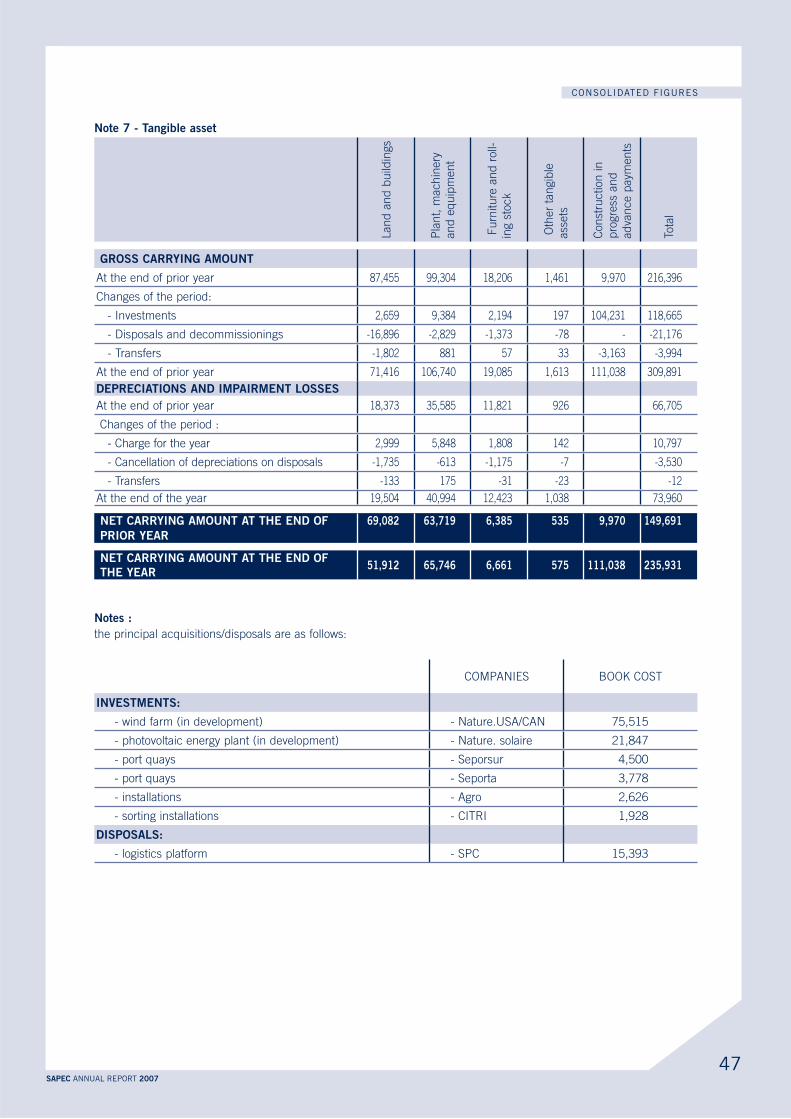

1. Tangible assets 7 235,931 149,691

2. Investment property 8 1,344 1,345

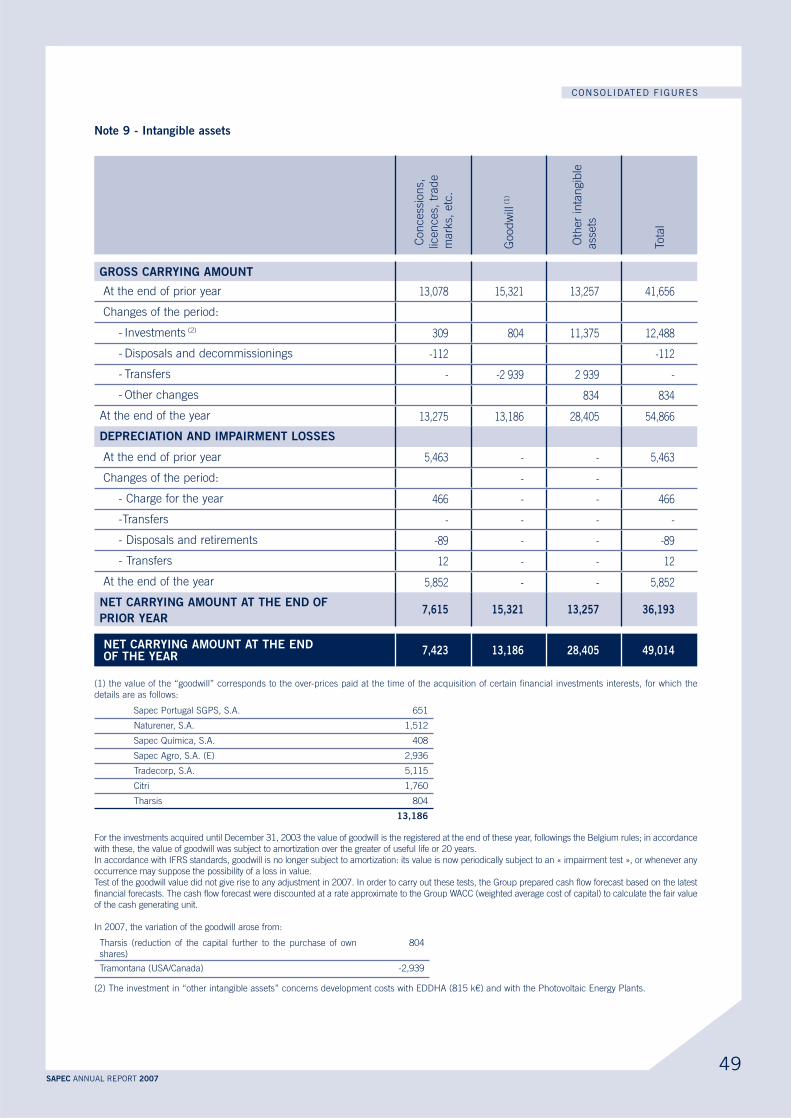

3. Intangible assets 9 49,014 36,193

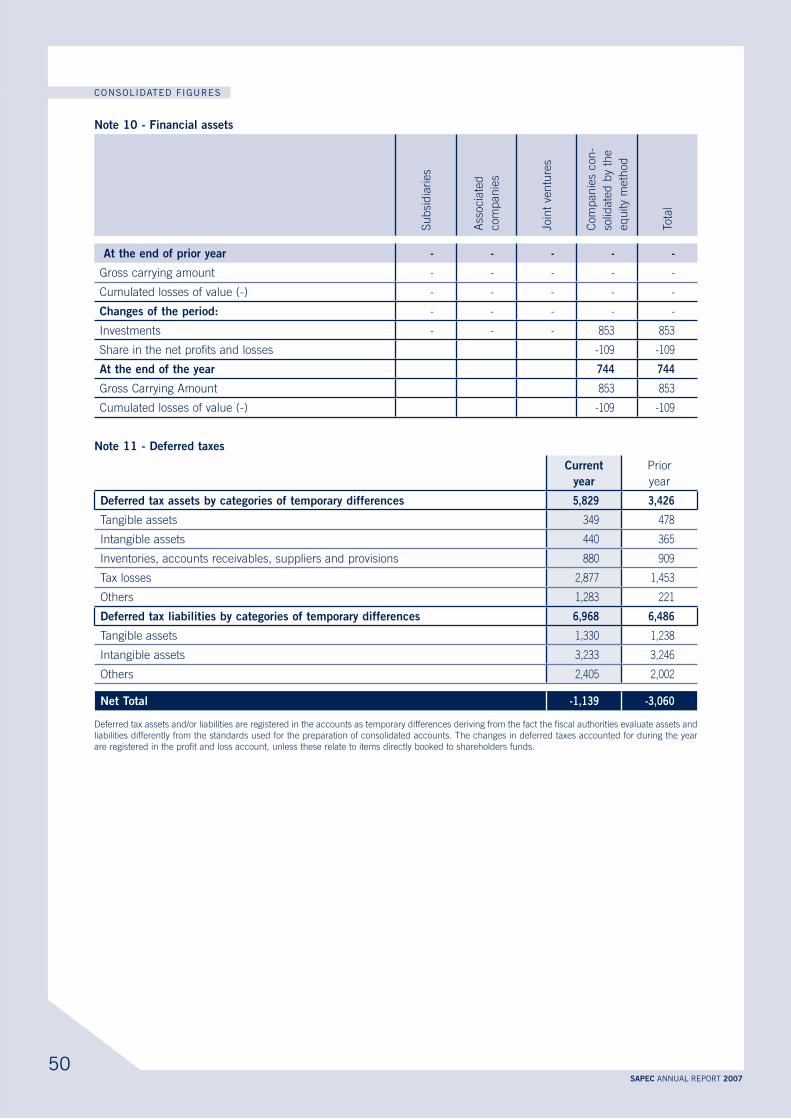

4. Financial assets 10 744 0

5. Deferred tax asset 11 5,829 3,426

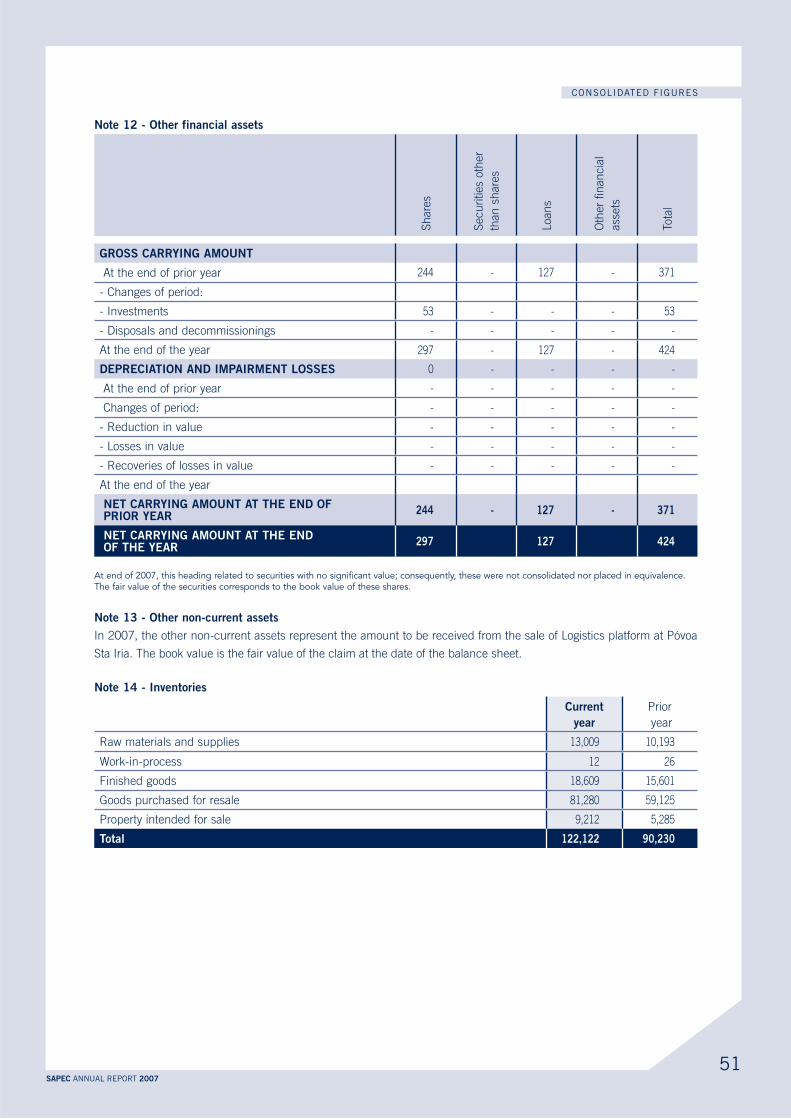

6. Other non-current financial assets 12 424 371

7. Derivative financial instruments 0 75

9. Other non-current assets 13 11,570 0

11. Inventories 14 122,122 90,230

12. Other current financial assets 1,028 2,610

13. Derivative financial instruments 15 216 766

14. Tax receivables 400 485

15. Trade and other receivables 16 98,398 91,441

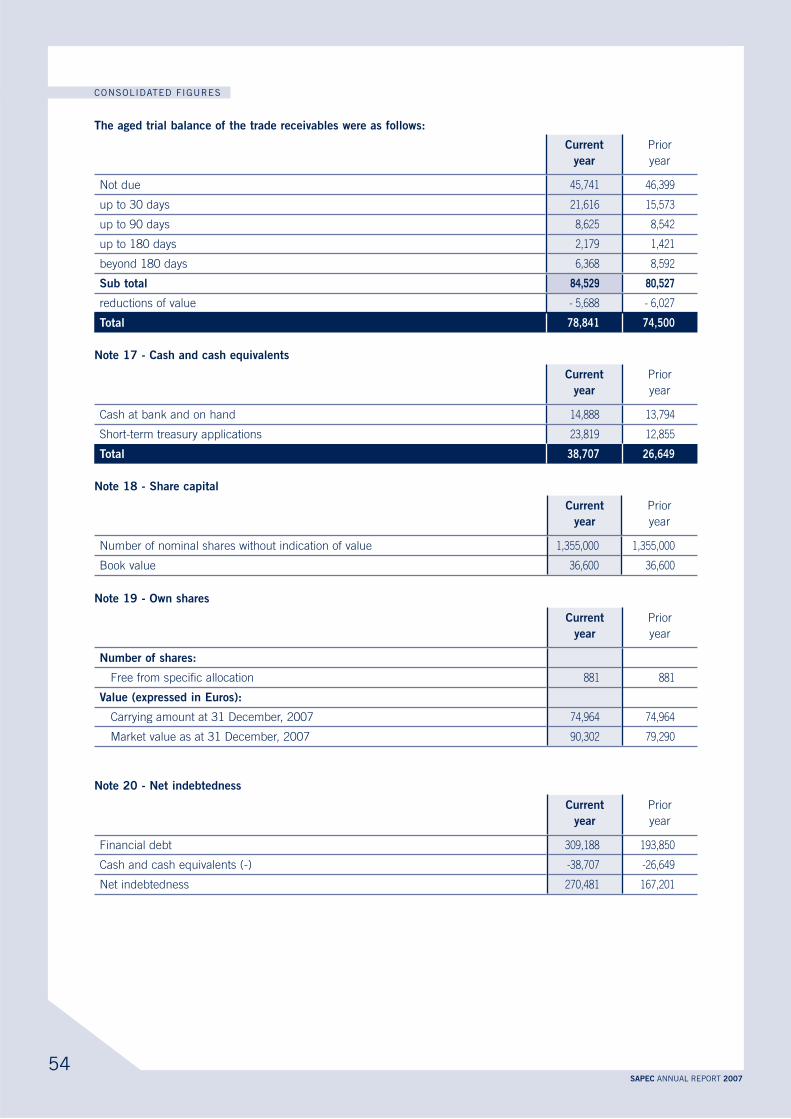

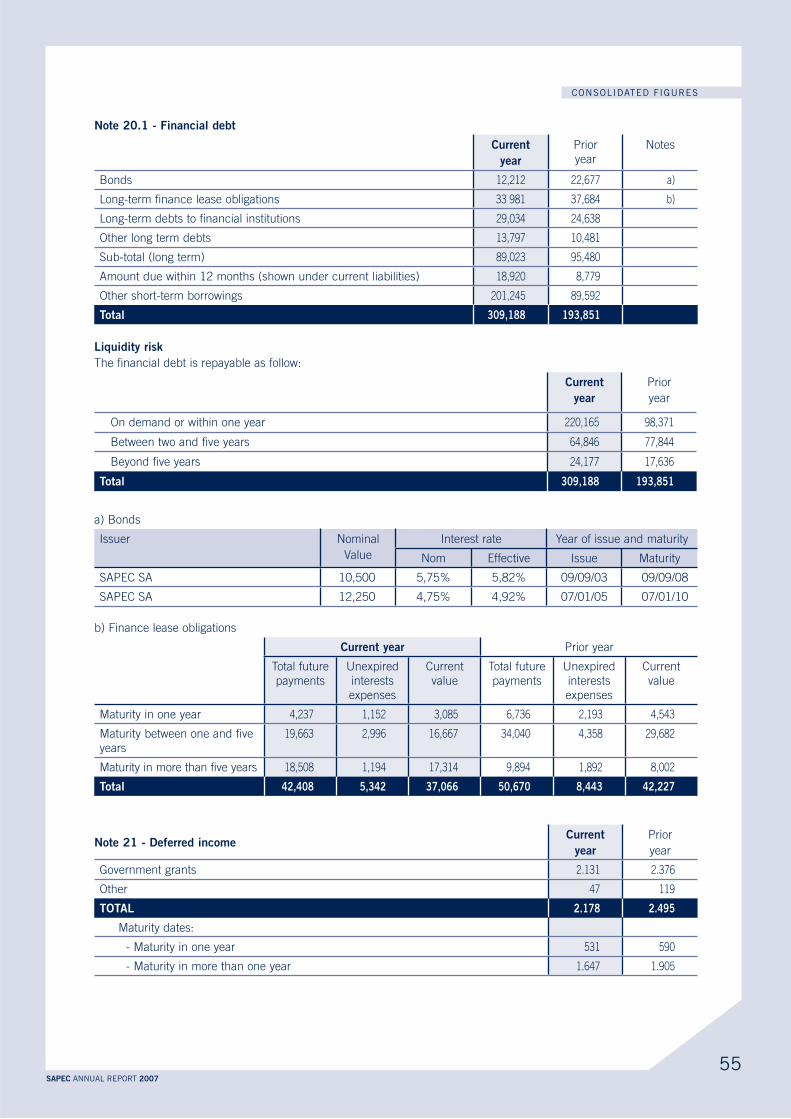

17. Cash and cash equivalents 17;20 38,707 26,649

18. Other current assets 4,867 1,943

Notes Current Prior

year

A. EQUITY 131,232 113,914

1. Capital 18 43,727 43,727

Issued capital 7,127 7,127

Share premiums 36,600 36,600

2. Consolidated reserves 87,595 70,266

3. Own shares 19 -90 -79

B. Minority interests 36,314 15,191

5. Long-term interest-bearing borrowings 20 88,576 94,999

6. Long-term non-interest-bearing borrowings 447 481

7. Deferred income 21 1,647 1,905

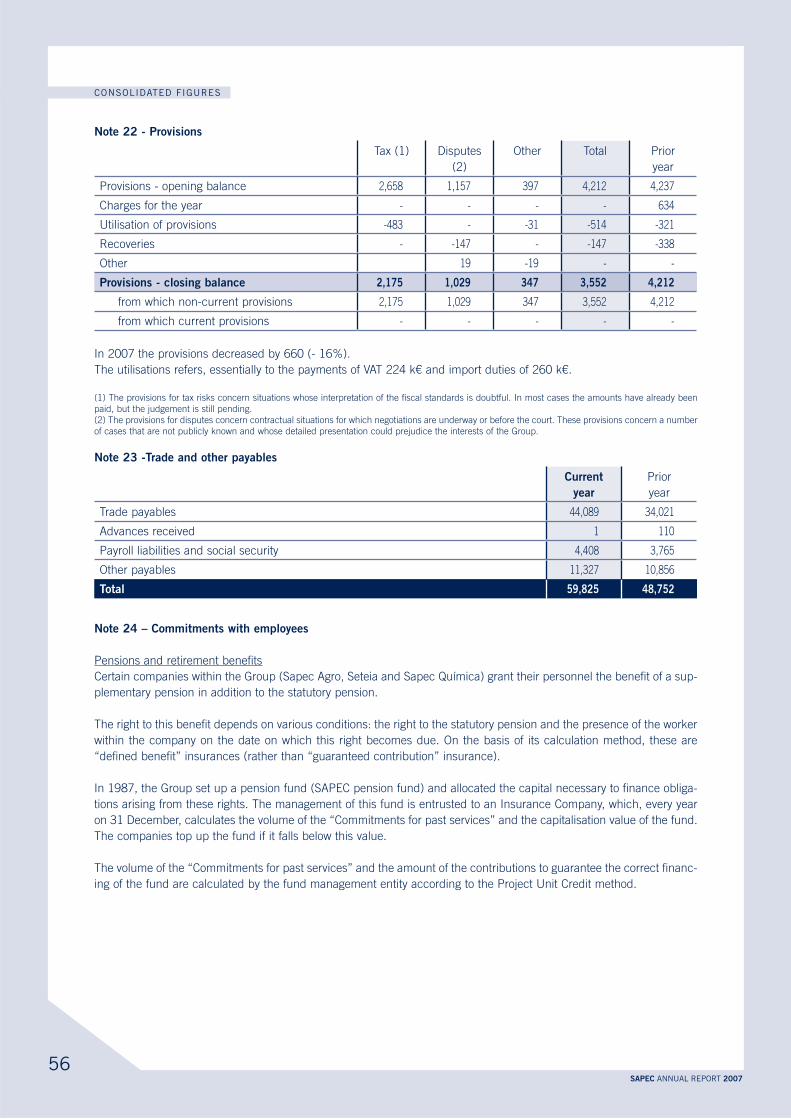

8. Long-term provisions 22 3,552 4,212

10. Deferred tax liabilities 11 6,968 6,486

11. Non-current trade and other payables 0 2,017

12. Other non-current liabilities 2,254 2,188

C

13. Short-term interest-bearing borrowings 20 220,095 98,300

14. Short-term non-interest-bearing borrowings 70 70

15. Deferred income 21 531 590

17. Derivative financial instruments 15 236 2,059

18. Income tax payable 9,294 4,198

19. Trade and other payables 23 59,825 48,752

20. Other current liabilities 9,552 9,860

33SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

The important impact in 2007 with the developpment of the renewable energy projects (wind farms in USA/Canada and

photovoltaic in Spain), at the consolidated balance sheet difficults the comparaison with 2006.

It seems usefull the presentation of the 2007 balance sheet, without the impact due to those projects and making pos-

sible this comparaison.

without projects USA/CAN and

solar

Conso

au

31.12.07

Conso

au

31.12.06

Variation

Dec07/

Dec06

31.12.07

(ajust)

31.12.06

(ajust)

Variation

Dec07/

Dec06

(ajust)

ASSETS A E

Assets 287,033 187,228 99,805 162,730 174,765 -12,036

Deferred tax assets 5,829 3,426 2,403 5,074 3,426 1,648

Other non-current assets 11,994 446 11,548 11,994 446 11,548

Trade and other receivables 98,398 91,441 6,957 92,103 88,584 3,519

Cash and cash equivalents 38,707 26,649 12,058 22,793 15,557 7,237

Other current assets 128,633 96,034 32,599 128,535 96,034 32,501

A. Equity 131,232 113,914 17,318 131,918 113,914 18,004

B. Minority interests 36,314 15,191 21,123 14,453 15,191 -739

A. Non-current liabilities 103,445 112,289 -8,844 100,506 112,289 -11,783

Long-term interest-bearing borrowings 88,576 94,999 -6,423 88,576 94,999 -6,423

Deferred tax liabilities 6,968 6,486 482 4,029 6,486 -2,457

Other non-current liabilities 7,901 10,804 -2,903 7,901 10,804 -2,903

B. Current liabilities 299,603 163,829 135,774 176,352 137,417 38,936

Short-term interest-bearing borrowings 220,095 98,300 121,794 99,116 74,745 24,371

Other current liabilities 79,508 65,528 13,980 77,236 62,671 14,565

34SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

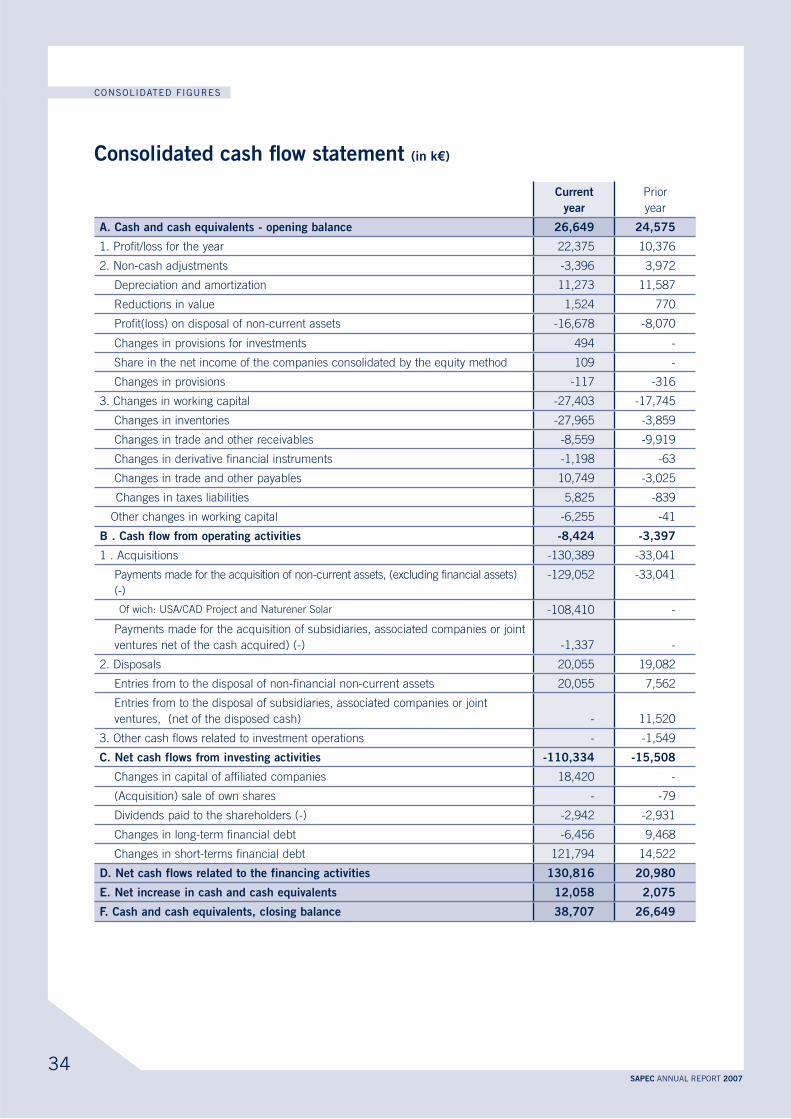

(in k€)

Current Prior

year

1. Profit/loss for the year 22,375 10,376

2. Non-cash adjustments -3,396 3,972

Depreciation and amortization 11,273 11,587

Reductions in value 1,524 770

Profit(loss) on disposal of non-current assets -16,678 -8,070

Changes in provisions for investments 494 -

Share in the net income of the companies consolidated by the equity method 109 -

Changes in provisions -117 -316

3. Changes in working capital -27,403 -17,745

Changes in inventories -27,965 -3,859

Changes in trade and other receivables -8,559 -9,919

Changes in derivative financial instruments -1,198 -63

Changes in trade and other payables 10,749 -3,025

Changes in taxes liabilities 5,825 -839

Other changes in working capital -6,255 -41

1 . Acquisitions -130,389 -33,041

Payments made for the acquisition of non-current assets, (excluding financial assets)

(-)

-129,052 -33,041

Of wich: USA/CAD Project and Naturener Solar -108,410 -

Payments made for the acquisition of subsidiaries, associated companies or joint

ventures net of the cash acquired) (-) -1,337 -

2. Disposals 20,055 19,082

Entries from to the disposal of non-financial non-current assets 20,055 7,562

Entries from to the disposal of subsidiaries, associated companies or joint

ventures, (net of the disposed cash) - 11,520

3. Other cash flows related to investment operations - -1,549

Changes in capital of affiliated companies 18,420 -

(Acquisition) sale of own shares - -79

Dividends paid to the shareholders (-) -2,942 -2,931

Changes in long-term financial debt -6,456 9,468

Changes in short-terms financial debt 121,794 14,522

35SAPEC ANNUAL REPORT 2007

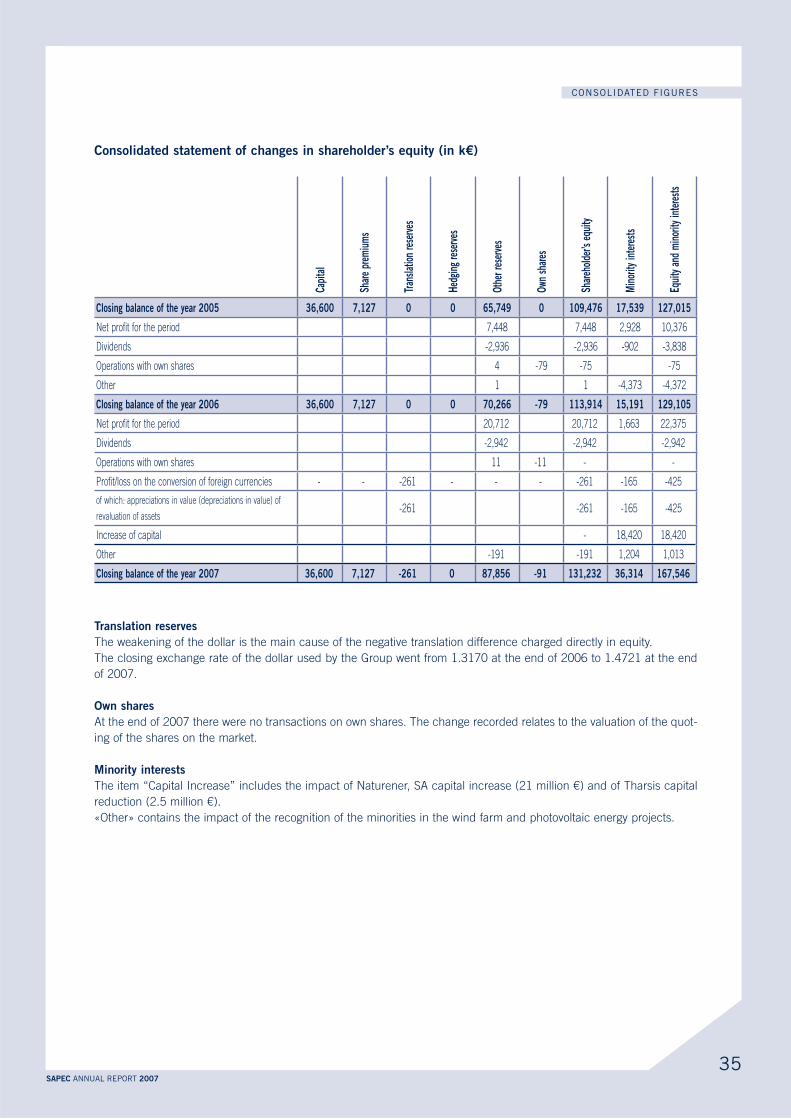

CONSOLIDATED FIGURES

Capi

tal

0 0 0

Net profit for the period 7,448 7,448 2,928 10,376

Dividends -2,936 -2,936 -902 -3,838

Operations with own shares 4 -79 -75 -75

Other 1 1 -4,373 -4,372

0 0 -79

Net profit for the period 20,712 20,712 1,663 22,375

Dividends -2,942 -2,942 -2,942

Operations with own shares 11 -11 - -

Profit/loss on the conversion of foreign currencies - - -261 - - - -261 -165 -425

of which: appreciations in value (depreciations in value) of

revaluation of assets-261 -261 -165 -425

Increase of capital - 18,420 18,420

Other -191 -191 1,204 1,013

0

The weakening of the dollar is the main cause of the negative translation difference charged directly in equity.

The closing exchange rate of the dollar used by the Group went from 1.3170 at the end of 2006 to 1.4721 at the end

of 2007.

At the end of 2007 there were no transactions on own shares. The change recorded relates to the valuation of the quot-

ing of the shares on the market.

The item “Capital Increase” includes the impact of Naturener, SA capital increase (21 million €) and of Tharsis capital

reduction (2.5 million €).

«Other» contains the impact of the recognition of the minorities in the wind farm and photovoltaic energy projects.

36SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

The main accounting policies adopted to prepare the consolidated accounts are set as follows:

The consolidated accounts have been prepared in accordance with the international accounting standards (IFRSInternational

Financial Reporting Standards) and with the interpretations published by the interpretation committee of the IASB, as they

apply on the reporting date.

Furthermore, the financial statements include all the information required by the 7th directive of the European Union.

The IFRS were adopted for the first time for the consolidated accounts of the 2005 financial year. The 2004 accounts have

been restated to allow comparison.

For the financial year, the Group adopted the rules that came into effect in 2007 (IFRS 7). The application of this new rule provoked

the publication of additional information about the financial instruments.

The Group decided no to apply any rule before the date of it coming into force.

The companies controlled by the Group (control is understood to mean the power to influence the financial and operational

policies of a company in order to obtain benefits from its activities) are consolidated according to the global integration

method.

All of the intra-group balances and transactions are eliminated.

The companies over which the Group exercises with a limited number of associates a joint control (joint control is understood

to mean the sharing via a contractual agreement of the control of an economic activity), are consolidated according to the

proportional integration method.

Holdings in companies in which the Group exercises a notable influence (notable influence is understood to mean the power

to participate in the decisions relating to the financial and operational policy of the company held, without however exercising

control over these policies) are accounted for using the equity method.

Currency operations are converted into euro at the transaction rate. At the end of the period, the monetary elements

are converted at the closing rate as well as the non monetary elements that are the subject of specific hedging. The

resulting exchange adjustments are entered in the income statement.

Non monetary assets and liabilities valued at historical cost and registered in foreign currencies are converted at

the rate of exchange in force on the date of the transaction. The resulting differences in conversion are recorded in

shareholder’s equity accounts under a specific heading (differences in conversion).

Within the framework of the consolidation, the assets and liabilities of the foreign entities are converted in to euro at

the closing rate. The results are converted into euro at the average rate of the period.

The goodwill represents the difference between the acquisition cost and the Group’s share in the fair value of the identifiable

assets and liabilities of a subsidiary, associate, or a joint venture, on the acquisition date.

The goodwill is not depreciated but is the subject of an annual depreciation test (impairment test), which is carried out

more frequently if there is some indication of impairment losses.

Any impairment losses of the goodwill are presented in the income statement and can be the subject of recoveries.

In the event of a surplus in the acquirer’s share of interests in the fair value of the assets, liabilities and contingent

liabilities acquired compared with the cost, this surplus is immediately recognised in the income statement of the

acquisition period.

37SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

The intangible assets are recognised at their acquisition value, less the accumulated depreciations and any depreciations in value.

They are recognised if it is probable that future economic benefits arising from the asset will go to the company and if the cost of

this asset can be reliably measured.

The intangible fixed assets are amortised on a straight-line basis over their estimated useful lives. The estimated useful lives are as

follows:

- Licences, patents and similar rights: 15 years

- IT software: 3 years

- Concessions: the contractual duration.

The research costs are charged to the period during which they were incurred.

The development costs are activities if and only if all the conditions set out below are fulfilled:

proven) ;

The development costs activated are amortised on a straight-line basis over their useful lives.

The tangible assets are recognised in the balance sheet at their historical value less accumulated depreciations and

impairment losses.

The subsequent expenditure relating to tangible fixed assets are only entered as an asset if it can be clearly demon-

strated that this leads to an increase in the future economic benefits expected from the use of the tangible fixed asset.

Borrowing costs directly attributable to the acquisition or production of an asset are added to the cost of this asset until is ready for

use if the amount of the investment is higher than 2,5 mio€ or if the construction/production period is higher than one year.

The depreciations relate to the estimated useful life of the various categories of the tangible fixed assets on a straight-line basis.

The estimated useful lives are as follows:

1. Constructions : Industrial

Commercial

Administrative

20 years

50 years

33 à 50 years

2. Equipment 3 to 10 years depending on type

3. Installations – fittings 10 to 15 years depending on use

4. Transport equipment from 4 to 6 years depending on

type

5. Furniture – Office from 3 to 10 years

6. IT Equipment 4 years

7. Constructions, Installations, Equipment on Concessions The duration of the concession, if

this duration is less than the initial

useful life.

The fittings made to the rented constructions are capitalised and depreciated over the residual duration of the lease or over

the useful life if the latter is lower.

When the carrying amount of an asset is higher than its estimated recoverable value, a reduction in value relating to this dif-

ference is directly recognised as reduction of.

38SAPEC ANNUAL REPORT 2007

CONSOLIDATED FIGURES

The assets held as finance leases (finance leases are understood to mean leases whose aim is to transfer to the lessee almost

all of the risks and benefits inherent to the ownership of an asset, with ownership being transferred or otherwise at the expiry

of the lease) are recorded in the balance sheet at their fair value or at the present value of the minimum payments linked to

the leases if lower.

The corresponding obligation is recognised in the financial liabilities. The finance costs, which represent the difference

between all of the lease obligations and the fair value of the assets, are entered into the income statement over the duration

of the lease.

Subsidies relating to the purchases of tangible fixed assets are recognised in the « deferred income » item of the balance

sheet.

The subsidy is charged as a income at the same rate as the depreciation of the fixed assets to which it relates.

The inventories are measured at the lower of cost (commodities and merchandise) or cost price (goods in progress and finished

products) and net realisable value. The value of the inventories is generally determined by applying the weighted average cost

method.

In view of the specific nature of the trading activities, the stocks in this sector are measured at their fair value on the reporting date,

less the marketing costs yet to be committed.

The costs of the stocks include the acquisition, processing and other costs incurred to transport the stocks to the place and in the

condition in which they are found. The processing costs of the stocks include the costs directly linked to the units produced, such

as direct labour. They also include the systematic affectation of the general fixed and variable productions costs that are incurred to

transform the commodities into end products. The fixed production overheads are the indirect production costs that remain relatively

constant independently of the volume of production, such as depreciation and the maintenance of the buildings and of the industrial

equipment and the management and administration costs of the factory. The variable production costs are the indirect production

costs that vary directly or almost directly according to the production volume such as indirect commodities and indirect labour.

Trade receivables are measured at their nominal value, less the non recoverable estimated amounts.

The group makes a distinction between two categories of financial assets – short-term investments: the assets held until maturity

and the assets available for sale.

The assets held until maturity are non-derived financial assets that have fixed or defined payments, a fixed maturity date and that

the company has the express intention and the means of holding until maturity date, other being than those designated as assets

available for sale and those defined as loans and accounts receivable.