annual report 2003 - bancoestado personas · background witness to and protagonist of a long...

TRANSCRIPT

Annual Report 2003

Financial Highlights

BancoEstado and its subsidiaries enjoyed some landmark achievements and results in 2003.

Consolidated before-tax income rose 18.8% to more than 67 billion pesos, bringing return on capital

and reserves (return on equity, ROE) to 19.3%. The earnings to assets ratio (return on assets, ROA)

also improved, as did international agency risk ratings.

The bank’s net loans rose 7.7%, more than double the rest of the system. Consumer credits, which

rose 37.3%, and mortgages, which rose 14.3%, drove this increase.

Although these results were achieved in an economic context favorable to rising loans, for

BancoEstado 2003 was a demanding year, given the decline in its traditional income, significantly

linked to fiscal accounts. The bank successfully met this important challenge by generating new

sources of income, raising its competitiveness, and creating new business opportunities, as part of an

integrated modernization process. .

Indicators 2001 2002 2003

Net earnings before tax 46,647 56,654 67,327

Base capital 329,656 347,147 349,154

Effective equity 395,057 412,034 445,898

Total loans 3,856,444 4,095,862 4,456,446

Total assets 5,990,377 6,709,166 7,473,371

Net income before tax over total assets (ROA, %) 0.78 0.84 0.90

Net income before tax over capital and reserves (ROE, %) 14.15 16.32 19.28

Efficiency index a) 75.57 69.33 68.11

Credit portfolio risk rate (%) 1.47 1.48 1.55

Base capital over total weighted assets (%) b) 5.64 5.18 4.67

Basel index (%) c) 11.83 11.22 11.37

Number of automated services 1,810 1,864 1,894

Number of branches 307 310 310

Total monthly transactions (December, millions). 16.3 17.8 20.5

a) Administrative expenditures over gross margin plus monetary correction.b) Legal minimum 3%.c) Legal minimum 8%.

Return on equity (ROE) 2002-2003Before-tax income*/capital and reserves, %.

* The bank is subject to an additional 40% tax; for comparison’s sake before-tax income is used.* *Non-consolidated figures.

BancoEstado and Subsidiaries Consolidated Data(Figures in millions of pesos, December 2003)

The Bank’s International Rating

Agency Risk* Financial strength

Moody’s Baa1 C+

Standard & Poor’s A –

* Long-term debt in foreign currency, maturing more than one year hence.

0

5

10

15

20

Rest of the System

BancoEstado

20032002

16.315.8**

19.3 19.6**

A Bank for all Chileans

Page 13 Page 17 Page 18 Page 23

The Bank with themost coveragethroughout the country

Customer-centeredcare

Promoting Chile’sparticipatorymanagement

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

1713 18 23

BackgroundWitness to and protagonist of a long history, BancoEstado goes back to 1855, when the Caja de CréditoHipotecario (a mortgage banking institution) was created, just a few decades after Chile’s Independence fromSpain.

The merger of this body with the Caja Nacional de Ahorros (a savings bank, 1910), the Caja de Crédito Agrario(a farm-oriented bank, 1925) and the Instituto de Crédito Industrial (an industrial credit institution, 1928)created the Banco del Estado de Chile (Chilean state-owned bank) on 12 June 1953. In 2003, it celebrated its50 th anniversary.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

MissionTo offer competitive financial services that contributeto Chile’s development and facilitate the access of allChileans to products and services that make theirlives easier and more secure.

Letter fromthe Chairman

Annual Report2003

The recognition of customers and institutions, strong commercial growth

and solid profits, the result of efforts from management and employees, are

some of BancoEstado’s main achievements during 2003, the year in which

we commemorated our 50 th anniversary.

Commercial success, achieved in an extremely competitive milieu, occurred

at the same time as the bank remained socially responsible, especially in

terms of providing banking services to sectors normally excluded for

geographic or social reasons, and offering new products and services to

customers.

In fact, ours is the only bank present in almost half of Chile’s municipal

areas (comunas); one of every two Chileans has a savings account in

BancoEstado; and we provide two of every three mortgages within the

banking system.

In recent years, and particularly in 2003, the bank has faced a new scenario

as its traditional income, especially that arising from fiscal accounts, whose

yield is linked to the inflation rate, declined significantly, making alternative

sources of income a necessity. By reorganizing our product and service mix

and boosting competitiveness, the company has been able to turn around

this situation and achieve good results.

Today, BancoEstado’s development depends primarily on its customers and

its ability to develop new business areas. This is a mega-bank facing a

globalized world that, thanks to the consolidation of its own modernization,

has honed its competitive skills in the personal, business and financial

intermediation markets.

We have become a fully competitive bank, which maintains and expands its

social role; and a successful bank, based on its solvency, as Moody’s

indicated when it boosted our financial strength rating from C to C+.

Recently Standard & Poor’s responded similarly, noting that BancoEstado

has the best risk rating for foreign currency debt in Chile and Latin America,

as it pushed our rating up from A- to A.

Achievements in the

commercial and financial

spheres have led to a

consolidated rise in

profitability, which went from

16.3% in 2002 to 19.3% in

2003, yielding pre-tax income

of over 67 billion pesos, that

is almost 11 billion pesos

more than in 2002.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

Achievements in the commercial and financial spheres

have led to a consolidated rise in profitability, which went

from 16.3% in 2002 to 19.3% in 2003, yielding pre-tax

income of over 67 billion pesos, that is almost 11 billion

pesos more than in 2002.

The bank’s subsidiaries made an important contribution to

this result, as they complemented BancoEstado’s customer

service with a wider range of offerings and excellent

specialized business services: insurance, financial advice to

very small businesses, security intermediation, fund

management, collections, financial communications and a

contact center.

In the business sphere we developed major sales

campaigns and pioneered the transfer of the benefits from

successive interest rate cuts applied by the Central Bank,

which were well received among our customers.

Among these campaigns, consumer credits stand out, as

this segment rose 37%, bringing 43,000 new customers,

Annual Report2003

more than one-third of the total rise in consumer banking

during this period.

Similarly, mortgages performed well, especially the

‘Hipotecazo’ (great mortgage) campaign, which achieved

five times its initial target. BancoEstado retained its

undisputed leadership in this segment, as loans grew 14%

for a market share of 29%. In terms of the number of

operations, this share rises to 73%, given the enormous

number of small mortgages granted to complement

Housing and Urbanism Ministry subsidies to buyers.

In line with the bank’s social role, in 2003 we successfully

developed an insurance service, acting as intermediaries for

more than 2,400,000 policies, up 600,000 from the

previous year. Here the challenge is to bring banking

services to the broadest sectors of the population, that is,

offer everyone market instruments at a low price so they

can deal successfully with the uncertainties of individual

and collective life. Today we are the second largest bank

insurance broker and for us this is a very significant

product.

We also reaffirmed our leadership in financing

microbusinesses, offering state-of-the-art technologies to

low income entrepreneurs who normally have no access to

banks. This program, which in 2000 had 17,000

customers, achieved a record number of 90,000 customers

in 2003. We are fulfilling our social role, without

subsidizing, to ensure that individual entrepreneurs can

develop their skills with our support.

After lengthy negotiations, during the current fiscal year

the connection between the Redbanc and BancoEstado

networks of automatic telling machines started up,

bringing significant benefits to the country as this favored

8 million bank card holders. In December alone, there

were more than 2.7 million inter-network transactions.

These positive results led BancoEstado to receive important

recognition based on customers’ and institutions’ opinions.

Particularly outstanding were the awards granted by

Gestión magazine, as the Most Outstanding Business of

the Year, and the ProCalidad one, which selected our bank

as one of the seven companies in its class, best evaluated

by customers.

At BancoEstado people are fundamental. Through the

Strategic Alliance between management and employees,

we have been able to create a single strategic vision of the

institution and to implement it in a consensual manner.

Thus, the commitment of BancoEstado employees has

been crucial to carrying out the company’s profound

modernization.

The Alliance has consolidated through internal work

between management and the union. We have met and

listened throughout the whole country, organizing

meetings in which more than 3,000 employees have

participated, generated hundreds of innovations, many of

which have been applied with a resulting improvement in

the quality of customer service.

The growing participation of women in senior

management posts within the bank is another outstanding

achievement. In particular, we would like to note the

President of Chile’s appointment of Mrs. Ingrid Antonijevic

H. as a member of the Board; she is the first woman to

hold the post of board member in the Chilean banking

system.

Letter fromthe chairman

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

Our challenge is to continue to raise our service quality

and customer satisfaction, to reinforce their loyalty and

trust, a vital attribute of this institution. We aspire to be a

multi-bank that provides excellent service to all sectors of

the population and that suitably responds to people’s

needs, offering them the best solutions.

We trust that with the commitment of the bank’s

employees and customers’ support, we will continue to

grow strongly and provide improved services, especially in

personal banking, mortgages, consumer credits and

insurance, as well as serving micro-firms, for which our

goal is to reach more than 100,000 customers in 2004.

The main challenge facing Chile today is to achieve a

sustainable high growth and a fair distribution of its

benefits. This has encouraged us to find new ways of doing

things. Along with maintaining the confidence and the

solvency that have always distinguished BancoEstado, our

commitment is to become a mega-bank that daily

improves its ability to meet families’ needs, accompanies

business people in their projects and, ultimately, makes an

excellent contribution to the country’s development.

Jaime Estévez ValenciaChairman

We interconnected our ATM network withRedbanc.

With the engagement of our employees weshall continue growing fast.

We aim at being a multibanc serving withexcelence every segment of the population.

We reached a 29% mortgages loan marketshare.

We could attend 90,000microentrepreneurs in 2003.

We became a full competitive bank withthe best debt risk clasification in foreigncurrency.

Senior Officers

Annual Report2003

Board of DirectorsJaime Estévez ValenciaChairman

Marco Colodro HadjesVice-Chairman

Ingrid Antonijevic HahnDirector

José Pablo Arellano MarínDirector

Genaro Arriagada HerreraDirector

Antonio Schneider ChaigneauDirector

Pablo Silva ManríquezLabor Director

Manuel Soza HuertaAlternate Labor Director

Audit Committee MembersJosé Pablo Arellano MarínChairman

Ingrid Antonijevic Hahn

Jaime Estévez Valencia

Juan Carlos Méndez González** Appointed in January 2004

Executive Committee,General Counsel, andControllerJaime Estévez ValenciaChairman

Marco Colodro HadjesVice-Chairman

José Manuel Mena ValenciaChief Executive Officer

Alberto Chacón OyanedelGeneral Counsel

Jéssica López SaffieController

Jaime Estévez ValenciaChairman

Marco Colodro HadjesVice-Chairman

José Manuel Mena ValenciaChief Executive Officer

Alberto Chacón OyanedelGeneral Counsel

Ingrid Antonijevic HahnDirector

Ma

Senior Management

Arnoldo Courard BullGeneral Manager of Credits

Carlos Martabit ScaffGeneral Manager of Finance

Luis Alberto Soto IllanesGeneral Manager of Administration

Fernando León SadeOperations and Systems DivisionManager

Victoria Martínez OcamicaBranches and Electronic BankingDivision Manager

Francisco Mobarec AsfuraRisk Corporate Manager

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

José Pablo Arellano MarínDirector

Genaro Arriagada HerreraDirector

Antonio Schneider ChaigneauDirector

Pablo Silva ManríquezLabor Director

Manuel Soza HuertaAlternate Labor Director

nagement

Managers

Eugenia Aguilar RozasNorthern Branches

Patricio Andrade Garafulich Corporate Processes

Cristián Aylwin JolfreFinancial Control

Hernán Baeza JaraCustomer Service

Antonio Bertrand HermosillaFinancial Resources

Arturo Barrios AlmarzaMass Banking Processes

Humberto Cipriano ZamoranoSouthern Branches

Rodrigo Collado LizamaInformation and Technology

Camilo Concha BurgosBusiness Banking

Sebastián del Campo EdwardsPersonal Banking

Jorge Fernández CorreaCommunications

Emiliano Figueroa SandovalDebt Restructuring

Oscar González NarbonaPlanning and Research

Pedro González ReyesAccounting and Budgeting

Darko Homan VarljenLogistical Support

Pablo Mayorga VásquezInternational Business

Patricia Pearcy PozoInstitutional Banking

Jaime Pizarro TapiaSmall Business

Hernán Saavedra ParraElectronic Banking

Adriana Salcedo MoyaDeputy Counsel

Jorge Stuardo LuengoMetropolitan Region

Gastón Suárez CrothersMarketing

Omar Torres PlazaWelfare

General Managers of Subsidiaries

Edgardo Cabañas CardemilBancoEstado S.A. Corredores de Bolsa (stock broking)

Sergio Enriquez EssmannBancoEstado S.A. Administradora General de Fondos (general fund management)

Guillermo González CuetoBancoEstado Servicios de Cobranza S.A.(collections agency)

Iván León AvilaGlobalnet Comunicaciones Financieras S.A.(financial communications)

Soledad Ovando GreenBancoEstado Microempresas S.A. Asesorías Financieras (financial consultants to small businesses)

Enrique Schaub WeideinBancoEstado Contacto 24 horas S.A.(24-hour contact)

Fernando Silva SegoviaBancoEstado Corredores de Seguros Ltda.(insurance brokers)

Highlights

Annual Report2003

First quarter• The Fondo de Garantía para Pequeños Empresarios (small

business guarantee fund, FOGAPE) allocated US$ 60 millionin its first annual auction of guarantee rights.

• The Talca Industrial Fair 2003. The bank served more than10,000 small farmers throughout the country; 40% were inthe Maule Region.

• The program placing 100 university students in practice withmicrobusinesses was implemented.

• More than 2,400 employees of the Municipality ofConcepción received their salaries via electronic check bookusing an automated payroll system (Sistema deRemuneraciones Automatizado).

Second quarter• Insurance offer launched. One of the main products offered

is “Tarjeta Segura” (safe card), which protects customersfrom losses arising from assault, fraud and cloning.

• Agricultural insurance is implemented, which protectsproducers from crop losses and damages due to badweather.

• Twenty one specialized platforms to service small businessesthroughout the country officially open.

• The bank successfully issues US$ 71 million in subordinatebonds, maturing in 22 years with a five-year grace period.

• Launching of the “Creditazo”(great credit) campaign,February and March.

• Interconnection with Redbancsucceeded, favoring 8 million bankcard holders.

• FOGAPE allocated US$ 78million in its second auction.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

Third quarter• Launching of the credit to small business at a 0.87%

monthly interest rate.

• FOGAPE allocated US$ 82 million in its third auction.

• Launching of the Independence anniversary celebration“Creditazo” (great credit) campaign, offering credits for upto 60 months, with three months’ grace.

• Inter-network transactions soared during the first sixmonths of integration between BancoEstado and Redbancnetworks.

• The “Cuenta de Ahorro Niños” (children’s saving account)was created, expressing the bank’s commitment to Chile’sfuture. At several hospitals passbooks were handed out tominors, with a starting deposit of 10,000 pesos.

• Almost 7,000 employees at Codelco’s northern division arebenefited by an agreement with the bank that offers thempreferential conditions.

Fourth quarter• 21 new platforms for small business were inaugurated.

• With two other banks, BancoEstado granted a syndicated loan tothe Chilean-Italian-French company, Sociedad Concesionaria BasDos, to build new prisons in Antofagasta and Concepción.

• The insurance marketing campaign was launched, with the bestpremiums and coverage on the market.

• The President of Chile invited BancoEstado’s Chairman to thepresidential palace, La Moneda, along with the union leadershipand labor Directors, to congratulate them for the StrategicAlliance’s achievements.

• More than 300 business people participated in the Eighth AnnualMeeting of BancoEstado’s Banking Business Area.

• BancoEstado’s program providing credits to micro businessescelebrated its seventh anniversary, having reached 90,000 smallbusiness entrepreneurs.

• BancoEstado provided a US$ 20 million loan to build the newAtacama Region Airport.

• More than 3,000 public health employees in Arica andAntofagasta became favored by a product and service agreement.

• BancoEstado celebrates its 50 th

anniversary with customers andemployees.

• Ingrid Antonijevic Hahn and AntonioSchneider Chaigneau joined BancoEstado’sBoard of Directors, appointed by thePresident of Chile, Ricardo Lagos.

• The multi-product line for smallbusinesses was implemented.

A Well-Known,Well-Liked Bank

Social Responsibility

PosicionamientoBancoEstado

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

In its long years of service to the country, BancoEstadohas responded to Chileans’ dreams and spirit ofprogress and advancement, and represented importantvalues. It has become a bank that is highly appreciatedand respected by its customers who, day by day,deposit their trust in it, a status reaffirmed by manyinstances of public recognition from its owncustomers, businesses and specialized institutions.

At the start of the 21st century, BancoEstado is a mega-bank dedicated to strengthening its commercialleadership in association with Chilean families andfirms. At the same time, it is a solvent institution,whose value rises daily, which assumes its socialresponsibility in different forms, but particularlythrough providing banking services where nonecurrently exist, focusing mainly on isolated and low-income sectors.

BancoEstado has the broadest customer base in theChilean banking system. This is a fundamental assetoffering a solid foundation for achieving greatercompetitiveness.

Satisfying Family Needs

A Bank forall Chileans

BancoEstado Customers• 8.5 million Chileans with savings accounts.

• 1 million customers with current, demand or electronicchecking accounts.

• 460,000 customers with mortgages.

• 1.4 million insured people.

• 390,000 consumer loan customers.

• 110,000 commercial customers, 90,000 very small businesses.

• 1.1 million people who receive their monthly wages, pensionsand scholarships through the bank.

• 515 public institutions.

AvancesEstratégicos

Annual Report2003

A Bank for all Chileans

In 2003, the bank’s commercial activities thrived,particularly personal banking. Its consumer loans grewmore than twice as fast as those of the rest of thesystem and today the bank has 390,000 customers.This growth, although favored by the country’seconomic reactivation, was a direct result of activesales campaigns and the attractiveness of its productsin terms of quality and price, as compared to the restof the industry.

BancoEstado has traditionally been a major promoterof saving among Chilean families. Today, almost 8.5million people have savings accounts with this bank,that is one of every two Chileans. Similarly, one of everytwo young people receiving bank loans to pursuehigher education gets it from BancoEstado.

In housing finance, the bank holds 73% of the numberof sistem’s operations financed through mortgage

bonds, including subsidized credits; in other words,two of every three Chilean families with a mortgage arecustomers of this bank. In 2003, customers withmortgages from BancoEstado reached more than460,000.

During this fiscal year, a new mortgage campaign wasconducted, called “Hipotecazo” (great mortgage),whose target was US$ 51 million in loans. Itsenormous acceptance, induced by low rates andcustomer confidence in the product, led it to achievefive times that original target, reaching US$ 250million.

Under several agreements, the bank pays the wagesand pensions of a million people on a monthly basis,through deposits into accounts or direct payments. Inpart thanks to this, BancoEstado today administers thelargest number of payment instruments: almost 1.3million of its customers use a checking account, ademand savings account, or an electronic check book.

Personal banking

Rest of system27%

BancoEstado73%Rest of

system71.5%

BancoEstado28.5%

MortgagesShare of Balances (%)*

* Mortgages Source: SBIF (Bank Superintendency)* Mortgage bonds

Share of Number of Operations*

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

InsuranceIn 2003, the bank continued to expand insurancecoverage, as it has done in previous years, with thisserving as an important instrument in meeting itssocial responsibilities in a modern society. During thisfiscal year, the number of policies held reached morethan 2.4 million, with more than 600,000 new onesissued, and six products added to its portfolio: VidaEscolaridad (school life insurance); Vida yEnfermedades Graves (life and serious illness); Vidacon Devolución (life with payback); Salud Oncológico(oncological health); Salud Catastrófico (catastrophichealth) and Incendio Hogar (household fire).

With this extensive range of products, designed tomeet all our customers’ needs, the bank seeks toprovide protection and security, improving the qualityof life of a growing number of Chileans.

In fact, with low-cost monthly premiums, BancoEstadotoday covers the unsatisfied need for insurance to

protect and provide security to people from middle andlow socio-economic backgrounds, who formerly hadlittle access to these products, due to their low incomeor trade. This involves providing greater coverage, tobring the protection afforded by a wide range of simple,standardized and economically priced products withineveryone’s reach.

Workers formerly unprotected due to the high risksinvolved in their activities, as is the case with localfishing people and other small businesses, today havelife, disability and health care insurance, which allowsthem to work in peace and security, conditions thatalso benefit their families.

At the same time, in financial terms the insurancebusiness has made a significant contribution to thebank’s annual income.

Insurance Policiesin effect(thousand)

Compulsory

Voluntary0

500

1,000

1,500

2,000

2,500

200320022001

Annual Report2003

Sponsorships• Summer Festivals: Teatro a Luca,

Matucana Non Stop.• Theater: Bajosobretierra; Frágil;

Fluoxetina: Antidepresivo Nacional;Feliz Fin de Siglo Dr. Freud; Por elCorreo de las Brujas.

• Traveling cinema in Antofagasta;traveling exposition from the MiradorInteractive Museum, University ofValparaíso.

• Ethnic celebration Tapati Rapa Nui andIndigenous Fair at the EstaciónMapocho cultural center.

Continuing Education• Third and Fourth seminar, “Chile: un punto de inflexión para el desarrollo” (Chile a turning point for development) in the

cities of Valdivia and Valparaíso.• At the Valdivia Municipal Theatre, the play “San Vicente Super Star” was presented; and in La Serena, Antofagasta and

Pucón, the Jazz & Company band performed for bank customers. • Second competition, “An objet d’art to reward BancoEstado branches”, with participation from young artists.

2003 BancoEstado award; Viviana Pizarro’s work toacknowledge the branches’ goals achievement.

BancoEstado is particularly interested in and committedto education and culture in Chile. Faithful to thistradition, in 2003 it participated in many activities, someof which were part of special programs for groups ofcustomers with specific interests.

In 2002-2003, through different programs, the bank

granted 1,000 computers on a permanent basis to theMinistry of Education, “Todo Chile Enter” and non-profitsocial organizations, to support youth training andgenerate a community space for computer use andinternet connections.

At the same time, several thousand people, especiallyhigh school and university students, learned about thehistoric value of collections exhibited in the bank’sMuseo del Ahorro (savings museum) in Santiago, whichhas been open to the community for more than tenyears.

Commitment to education and culture

Own Projects• Coin exposition of BancoEstado’s Museo del Ahorro (savings museum) at the

Las Condes Cultural Institute.• Exposition on Chile’s Poetic Geography. • Interbank exposition of contemporary Chilean painting at the Andrés Bello

University.• Some 500,000 people visited the traveling expositions put on by the savings

museum and “Tremolinos en el Viento” in Chile’s First, Fourth, Fifth, Seventh,Eighth and Tenth regions.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

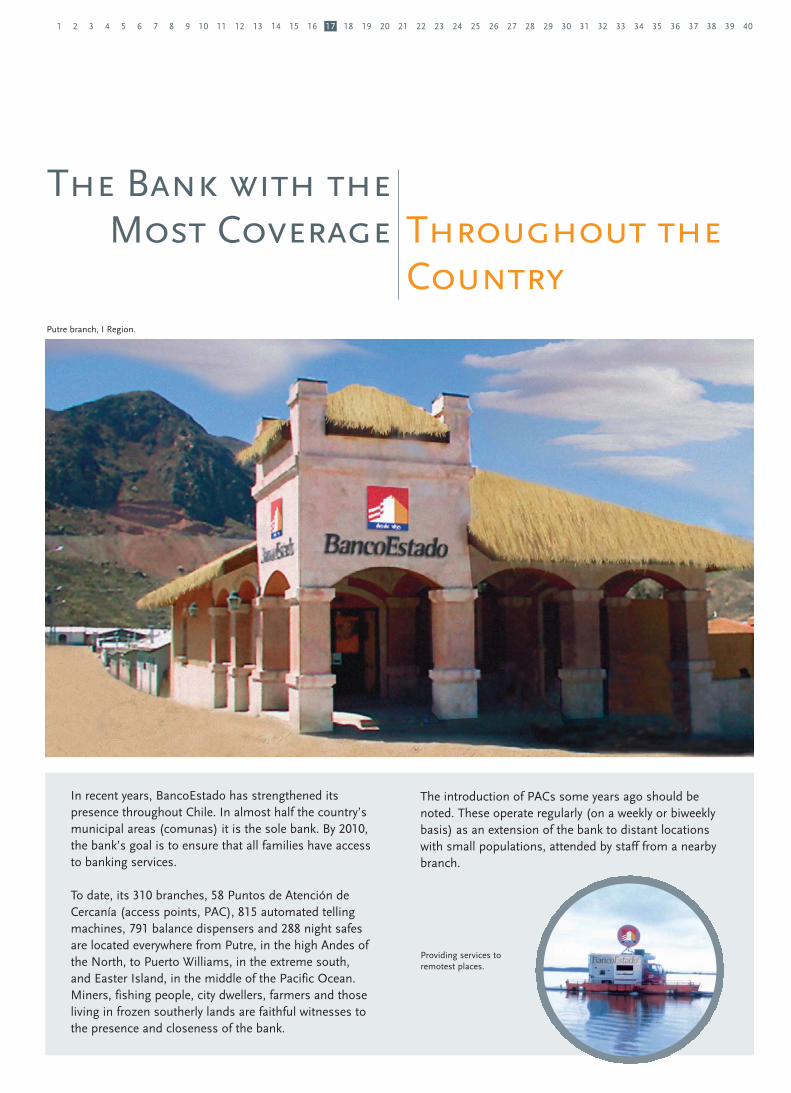

The Bank with the Most Coverage Throughout the

Country

In recent years, BancoEstado has strengthened itspresence throughout Chile. In almost half the country’smunicipal areas (comunas) it is the sole bank. By 2010,the bank’s goal is to ensure that all families have accessto banking services.

To date, its 310 branches, 58 Puntos de Atención deCercanía (access points, PAC), 815 automated tellingmachines, 791 balance dispensers and 288 night safesare located everywhere from Putre, in the high Andes ofthe North, to Puerto Williams, in the extreme south,and Easter Island, in the middle of the Pacific Ocean.Miners, fishing people, city dwellers, farmers and thoseliving in frozen southerly lands are faithful witnesses tothe presence and closeness of the bank.

Putre branch, I Region.

Providing services toremotest places.

The introduction of PACs some years ago should benoted. These operate regularly (on a weekly or biweeklybasis) as an extension of the bank to distant locationswith small populations, attended by staff from a nearbybranch.

Customer-CenteredCare

Annual Report2003

Commitment

Getting toknow better

During the 2003 fiscal year, BancoEstado consolidateda customer-centered management approach, based ongetting to know customers better and listening to themin more depth, and reaching them with products andservices that “make sense”, are better priced and moreattractive than those offered by the competition.

This means forgetting about generic customers andfocusing on who they are individually, their aspirations,dreams, that is, getting to know them completely. Therelevant information that this focus requires includesthe hard data, expressed in sales figures, income bysegment, but also the “soft data”, which revealscustomer satisfaction, employees’ self-confidence,

Procalidad 2003It highlights the BancoEstado as one of sevencompanies in its class, best evaluated by its customers.Granted by Adimark, Adolfo Ibáñez University and theCentro Nacional de la Productividad y la Calidad(national center for productivity and quality).

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

pride and satisfaction with work that creates visibleresults.

Building customers’ trust, along with ensuring that thebank acts with transparency and meets itscommitments, have been fundamental to positioning itas a bank for every one, from the modest employees toa major business leader.

The strategy followed and recognition from customersand the general public have allowed BancoEstado toreceive a series of distinctions that confirm itsachievements and position it as a leading company inthe national market.

Prizes and awards

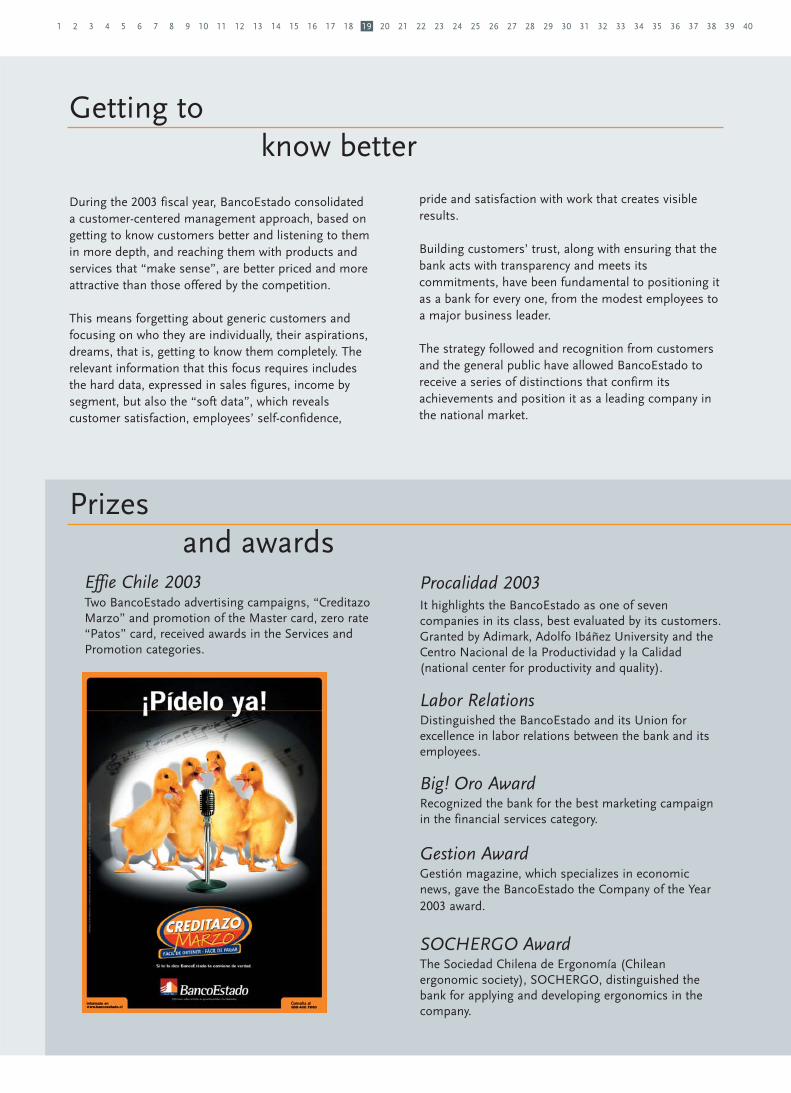

Effie Chile 2003Two BancoEstado advertising campaigns, “CreditazoMarzo” and promotion of the Master card, zero rate“Patos” card, received awards in the Services andPromotion categories.

Labor RelationsDistinguished the BancoEstado and its Union forexcellence in labor relations between the bank and itsemployees.

Big! Oro AwardRecognized the bank for the best marketing campaignin the financial services category.

Gestion AwardGestión magazine, which specializes in economicnews, gave the BancoEstado the Company of the Year2003 award.

SOCHERGO AwardThe Sociedad Chilena de Ergonomía (Chileanergonomic society), SOCHERGO, distinguished thebank for applying and developing ergonomics in thecompany.

Modern Customer Service

Annual Report2003

Service

Electronicbanking

“BancoEstado 24 Horas” (24 hours a day) allowscustomers and the general public to get to know anddeal with the bank without interruptions, through itsself-service network of telling machines, bank hotlineand the website, www.bancoestado.cl.

In 2003, small businesses were the beneficiaries of aservice especially designed to respond to their needs interms of both questions and operating products.Similarly, customers involved in foreign trade enjoyedusing the bank’s company web portal, which made itpossible for them to follow online the status of theiroperations.

As part of consolidating alternatives in innovativeservices, the first mortgage was granted to a Chileanliving abroad, through the portal created to servecitizens living outside the country.

In October, wap services began, the result of apioneering effort to join BancoEstado and Entel PCScustomers, allowing them to charge minutes of phonetime from their mobile phone, paid for directly usingtheir checking account or electronic check book.

The evaluation of the Lota Call Center in the EighthRegion remains very positive. There were more than5.7 million contacts with customers in 2003. Studiesreveal how much they appreciate this alternativeservice, which brings them closer to the bank, is moreflexible and saves time.

AutomationIn the course of the year, customers continued tomigrate heavily toward more automated services. Thus,12.4 million (60%) of the more than 20 million monthlytransactions in BancoEstado were conducted this way.

The bank’s growing automation, which prompted acampaign to provide ongoing training to bankcustomers in the efficient use of technology, hastranslated into better quality, more rapid service at lowercosts.

At the same time, bank employees have been able tocapture more customers and surpass commercialtargets, boosting results at each branch and leading to asizeable jump in labor productivity. This, measured asproductive assets over the number of employees andannualized through October, rose 9.2% on averageduring 2002-2003, versus 5.1% in the system overall.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

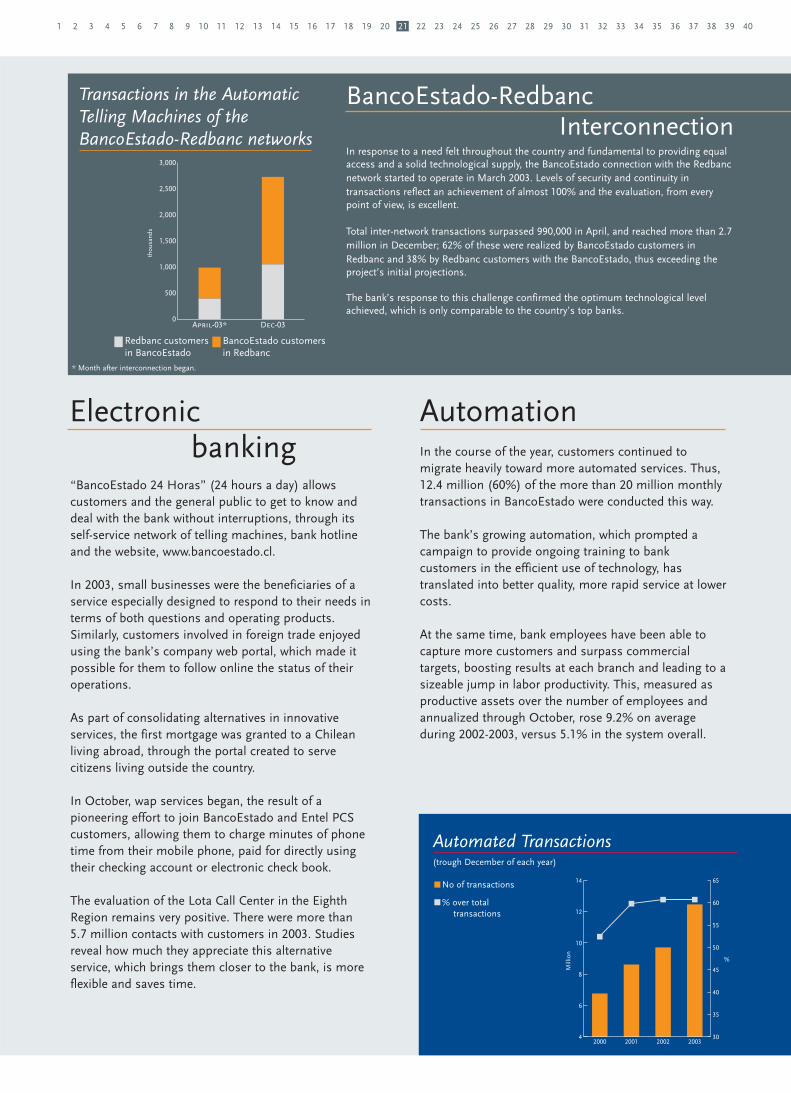

BancoEstado-Redbanc Interconnection

In response to a need felt throughout the country and fundamental to providing equalaccess and a solid technological supply, the BancoEstado connection with the Redbancnetwork started to operate in March 2003. Levels of security and continuity intransactions reflect an achievement of almost 100% and the evaluation, from everypoint of view, is excellent.

Total inter-network transactions surpassed 990,000 in April, and reached more than 2.7million in December; 62% of these were realized by BancoEstado customers inRedbanc and 38% by Redbanc customers with the BancoEstado, thus exceeding theproject’s initial projections.

The bank’s response to this challenge confirmed the optimum technological levelachieved, which is only comparable to the country’s top banks.

0

500

1,000

1,500

2,000

2,500

3,000

BancoEstado customers in Redbanc

Redbanc customersin BancoEstado

Dec-03April-03*

thou

sand

s

Transactions in the AutomaticTelling Machines of the BancoEstado-Redbanc networks

4

6

8

10

12

14

30

35

40

45

50

55

60

65

2003200220012000

Mill

ion

%

Automated Transactions(trough December of each year)

* Month after interconnection began.

No of transactions

% over totaltransactions

Modern Customer Service

Annual Report2003

Technologicalchange

In 2003 different processes of technological changebegun in previous years to deal with rising sales,especially in personal banking and microbusinesses,were completed.

The national processing center (Centro Nacional deProcesos, CNP), which centralized the operational partof branches, was completed, freeing up 700 staff forcustomer service tasks.

Also important was the implementation of a universalplatform for small businesses and the completerevamping of the telephone system, still in process,which will create a single service number throughoutthe country.

BancoEstado has the Chilean banking system’s mostcomplete customer data base. Constructed using state-of-the-art technology, this data base allows moreprecise, focused and segmented campaigns. This is asource of profitability in high competition periods,which favor those with the best knowledge of theircustomers’ needs and aspirations.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

PromotingChile’s Development

Yunus in ChileBancoEstado, along with other institutions, sponsored a visit to Chile from Muhammad Yunus, creator and Director of theGrameen Bank, the world’s largest micro-credit institution. The distinguished economist met with the President of Chile andparticipated in the BancoEstado’s 50th anniversary celebration. Among his many activities in Chile, he visited microbusinessesthat are BancoEstado customers in their work places, in the La Pintana municipal area.

PromotingChile’s Development

Annual Report2003

Micro and small business

The microbusiness program has posted outstandinggrowth since it started up in 1996. It uses systems andtechnologies especially designed to serve this segment.By number of customers, it holds over 40% of themarket, and in 2003 served 90,000 microbusinesspeople. The target for 2004 is to serve more than 100,000customers.

BancoEstado has opened up a whole world tomicrobusiness people from which they had beenexcluded, providing them with more opportunities todevelop their entrepreneurial skills. From 2000 to 2003more than 30,000 microbusiness people were trained,with support from information technology.

Directly linked to the family, the program attempts toprovide an integrated service. Thus, along with making itpossible to acquire different products and servicesthrough further agreements, it provides access to thenational health fund (Fondo Nacional de Salud,FONASA) and pension fund managers(Administradoras de Fondos de Pensiones,AFPs).

Similarly, the bank has signed severalagreements with microbusinessesassociated in different organizations, whichinvolve financing, the sale of insurance andthe supply of means of payment and, in somecases, connecting them with technical assistance

and training. These include: the newspaper sellersconfederation (Confederación de Suplementeros deChile), the national taxi drivers confederation(Confederación Nacional de Taxistas y Colectivos deChile), the association of medical centers (AsociaciónGremial de Centros Médicos) and the Chilean booksellers association (Cámara Chilena del Libro).

In terms of offshore fishing, agreements were signedwith the divers, fishing and shellfish extractors’federation (Federación de Pescadores, Buzos yMariscadores) in different regions, with 2,300 potentialbeneficiaries; in farming, with agricultural cooperatives,including one in the Tenth Region, with 1,250 potentialcustomers.

In the small business segment, a specialized attentionmodule with its own platform was developed; customersare visited in their place of business, can get alternativeservice through the Internet, and are coordinated withthe CORFO-PROCHILE development network.

To date, this segment has 42 specialized platforms, upfrom 11 in 2002. Similarly, the number of customers

has increased by 24%, while loans are up 11%.

The small business guarantee fund (Fondode Garantía para Pequeños Empresarios,FOGAPE) has become a genuine lever fordevelopment for small businesses,providing guarantees for a total of 250

billion pesos worth of credits.

The number of annual operations practicallytripled in the past three years, rising from 11,000

Microbusiness Program• National leader and among the best in Latin America.

• Credit applications are evaluated with field visits.

• Credit decisions are made within 48 hours.

• More than 90% of credits are processed without guarantees.

• Recovery rate: 99% of loans.

• Service through 91 specialized platforms throughout the country.

• 35% of clients achieve access to a financial institution for the first time.

• Half of customers are women.

the most importantfirms operating inChile: local andtransnationalcorporations, buildersand concession firms.

BancoEstado’scontribution to Chile’sdevelopment is especiallyclear in the financial support itprovides to important projects with major social andeconomic impacts, improving the population’s livingconditions. In this sense, the bank has extensiveexperience in structuring financing for major projects,such as highways, airports, electric generating stationsand industrial plants, among others.

In this segment, for the past three years the bank hasparticipated in syndicated loans and other ways offinancing major projects whose total investment isalmost US$ 1.5 billion. In some of these projects itparticipated in direct project financing while in others itfinanced building firms that participated in executingworks.

in 2000 to 30,000 in 2003. Of these, 70% representoperations carried out in regions.

In the micro and small agribusiness segment, thenumber of special products has expanded: seasonalfarming credit (Crédito Agrícola de Temporada, CAT),micro agribusiness credit (Crédito MicroempresaAgrícola), forestry credit for irrigation and drainage works(Crédito de Enlace Forestal, Crédito de Enlace para Obrasde Riego y Drenaje), and farming insurance (SeguroAgrícola).

In the case of the forestry credit, for example, theamount of credits more than doubled in 2003, to coveran area of 6,500 has.

Business banking /Investment projects

In this segment, almost 2000 customers have opted forthe commercial and financial services offered by our areaof business banking, Banca Empresas, including 60% of

Infrastructure Project Financing

Project Year Credit Approved Investment (US$ million)"El Trebal" sewage treatment plant 2001 150Mejillones port 2001 1213 underground municipal parking lots 2001-2002 20Public works ministry road works 2001-2003 50Central coast roads network 2002 105Nor-west Américo Vespucio section 2002 320"La Farfana" sewage treatment plant 2002 315Group I penitentiary infrastructure 2003 100Group II penitentiary infrastructure 2003 65Atacama regional airport 2003 28Santiago Metro expansion 2003 200Total 1,474

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

Competitive,Open to the Future

Annual Report2003

Competitive

employees has been fundamental. In 2003 theadvantages of the Strategic Alliance betweenemployees and management were clearly evident. ThisAlliance created more open labor relations andimprovements in bank management and financialyields.

Starting with the “Abramos un Espacio” (Let’s Makesome Space) workshops, about 3,000 employeesparticipated in 18 meetings throughout the country,giving rise to more than 300 initiatives to improve andinnovate in different areas and businesses. The resultsconfirm that employees are facing these challenges andgenerating valuable proposals for the institution. Theseactions are a palpable sign of their commitment to thebank’s mission today.

Alliance benefits were recognized by the Chileanassociation for labor relations (Asociación Chilena deRelaciones Laborales) when it gave BancoEstado andits union an award for excellence in its labor relations.

The Alliance’s leaders have set themselves the goal ofcontinuing to progress toward ever more excellentmanagement, which involves employees in redesigninginnovative processes, focusing on continuousimprovements through quality circles.

Similarly, a very complete labor training program will beapplied, to make it possible to go beyond traditionalofferings and achieve a program offering personalizedadvice. This involves support employees as theydevelop and plan their careers according to theirpotential and the institution’s requirements.

In 2003, the bank school (Escuela de FormaciónBancaria) trained and upgraded skills of 330 bankemployees; in its seven years of functioning, it has hadmore than 4,400 staff members participants.

As part of the shared financing educational program(Programa Educación con FinanciamientoCompartido), which forms part of the collectiveagreement between the national union andBancoEstado management, 380 employees obtainedscholarships to pursue pre- and post-graduate studiesat universities and institutes.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

Competes inevery market

Fifty years old, BancoEstado can look ahead to itsfuture with enormous solidity and confidence, basedon its low risk indices, the competitiveness of itsproducts and services, its customer-centered service,participatory management, and excellent laborrelations.

As a multi-bank, BancoEstado competes openly inevery market: personal banking, large, medium andreal estate company banking, micro and smallbusiness banking, institutional banking, money desk,and international business. All this means that todaythe bank holds 17% of the Chilean financial system’sbusiness assets.

Conscious of its public role, BancoEstado has made apowerful contribution to modernizing the Chileangovernment. A wide range of agreements with stateinstitutions and bodies, such as the armed forces, thenational health fund (FONASA), the national treasury,and internal revenue, have translated into a growingsupply of automated means and products, which thuscontribute to improving the management of publicinstitutions.

With the implementation of trade treaties with theUnited States and the European Union, today the bankis accompanying Chilean firms as they consolidatewithin their current markets and set out to conquernew ones. Thus, the most advanced foreign trade andservice systems are being developed to support themin this challenge of participating in increasinglycompetitive markets.

BancoEstado’sparticipatory

managementTo obtain these ends, in particular improving thebank’s competitive edge, the role of the bank’s

Business Management

EconomicEnvironment

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

The Chilean economy has become increasinglyintegrated into international trade, with competitiveexports and diversified markets, thus linking itsgrowth to the world’s main economies. In the secondhalf of 2003, Chile benefited from the economicrecovery of most of its trading partners, particularlythe United States, Japan and the rest of Asia.

The positive external outlook combined with expansivemonetary and fiscal policies have pushed the economyalong, bringing annual growth to 3.3%. As acountercyclic tool, the monetary policy interest ratewas cut, encouraging spending and output growth.

Toward year’s end, this rate reached its lowest level infifty years.

The consistency of the monetary and fiscal policiesapplied have given the Chilean economy enormouscredibility and inspired confidence among economicagents. These policies have helped to consolidatemacroeconomic fundamentals, reducing the negativeeffects of cyclical imbalances triggered by othereconomies.

In 2003, the external sector posted strong growth inthe case of both exports (13.8%) and imports (13.3%),

Reactivation and growth prospects

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

20042003200220012000

Historic and Expected GDP: Chile Versus

trading Partners*

(% of annual growth)

Chile

Trading partners

(*) Main: US, EU, Japan

generating a trade surplus of almost US$ 2.95 billion.In the same context, the current account deficitreached 0.8% of GDP, thus reflecting the foreignsector’s solidity.

After reaching parity of over 750 pesos per dollar inFebruary and March, the exchange rate plunged,ending the year at 600 pesos per dollar. Positive trendsin the world economy, higher export volumes andimproved terms of trade have meant that pesoappreciation is linked to solid fundamentals and notspeculative or short term factors. However, if the pesocontinues to appreciate, Chilean exports stand to loosesome of their competitiveness.

The appreciation of the Chilean currency, particularlytoward year’s end, contributed to a 1.1% decline inannual inflation, which is below the Central Bank’starget range (2%) and the lowest rate in almost 70years. This strengthened the population’s purchasingpower and inflation approached that of developed

EconomicEnvironment

Annual Report2003

countries. With stable prices, attractive returns and lowcountry risk, the economy is prepared to attract moreinflows of foreign capital to encourage real investment.

In short, expansive public expenditure, the sizeableincrease in exports and to a lesser degree privateconsumption strengthened the country’s economicrecovery.

This scenario and the free trade agreements signed in2003 with the United States and Korea and, in 2002,with the Euro zone countries, augur positive growth forChile’s economy in 2004 and the following years.

The banking industry and its environment underwentimportant changes in 2003. Banks developed in a morefavorable context than in previous years, with moreeconomic growth, driven among other factors bysuccessive cuts to monetary policy interest rates,applied by the Central Bank. This policy, combined withmore competition in this industry, led to lower creditcosts, especially in consumption and housing loans.

As both expectations and the services offeredimproved, customers returned to the system, reaching2.6 million, a historic record. They were also moredemanding and better informed.

Growing competition in the system was reflected inincreasingly aggressive sales campaigns at the sametime as buy-outs and alliances took place to improvemarket power. Similarly, non-bank players were moreactive, particularly in the case of consumer loans(department stores, insurance companies and savingscooperatives); at the same time as alternatives to bankfinancing also gained market share (bonds, bills oftrade and leasing).

In 2003 a new structure for the system consolidated,which involves the co-existence of universal or multi-banks (12) and specialized banks (14); in this sense,

Financialsystem

new players seek to position themselves in the microand small business and consumer niches, a trend thatwill grow stronger in 2004.

The industry’s total loans in 2003 followed economictrends, rising more quickly than the previous year(4.6% versus 1.6% in 2002). Personal and consumercredits and mortgages were the strongest performers,rising at annual rates of almost 17% and 12%,respectively. Commercial credits, meanwhile, whichaccount for half of total loans, grew little (1.4%annually), reflecting in part their replacement by othersources of financing. In contrast, specialized lines offinancing focusing on small and medium firms, suchas leasing and factoring, flourished.

After a period of cuts and restructuring, the system hasgrown stronger. In fact, the industry’s efficiency indicesreached international standards (53.8%), driven bymegabanks, which began to reap the fruits of theirmerger processes. The system’s profitability stabilizedwithin historic ranges (16.6%), all this accompanied bylow levels of portfolio risk (1.82% in October 2003).

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

BancoEstado Management

Annual Report2003

Modernization

Financial management

The new competitive strategy and the effort unfolded byevery unit allowed the bank to achieve good financialresults in 2003, which was also reflected in indicatorsthat held steady or improved.

In fact, at the corporate level, before-tax profits overcapital and reserves (return on equity) rose to 19.3%, upsignificantly from 16.3% the previous year. Return onassets performed similarly, rising from 0.84% to 0.90%.

Similarly, after-tax profits reached 8.5%. It should benoted that as with other public firms, the bank is subjectto an actual 56.5% tax rate on profits, 40% more thanother firms and the rest of the financial system.

As occurred in previous years, the contribution fromsubsidiaries and services to overall results rosesignificantly, reconfirming the commercial strategyfollowed by the bank in these business areas.

Management in 2003 was also reflected very positively inrisk indicators. Today BancoEstado has the best riskrating for foreign currency debt among banks in Chileand Latin America, thus confirming its solvency. Withregard to long-term debt, Standard & Poor’s recentlyraised its A- rating to an A, which is similar to that of theChilean government. For its part, Moody’s maintainedthe bank’s long-term bank debt in foreign currency ratingat Baa1, and improved the financial strength indicator,which only considers the institution’s strengthindependently of country risk, from C to C+. This level isassociated with banks in developed countries.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

In 2003, the bank’s strategy focused on achieving themain objectives established in the 2003-2004 Plan.

One essential objective for 2003 was to generate newincome to offset the drop in traditional bank income,particularly the lower yields on fiscal checking accountsand savings accounts, given the fall in inflation andinterest rates.

Accordingly, another key objective was to boost efficiencyto raise competitiveness in an increasingly demandingindustry, which makes it vital to raise productivity andstrictly control spending.

At the commercial level, the bank sought to capitalize itsbetter positioning in its customers’ eyes, by extending itsproduct range, raising the volume of business andentering more profitable segments, to generate newincome and increase its market share, thus reaching itsposition today as one of Chile’s three largest banks. Forthe same end, the bank expanded and complemented itsbusiness through subsidiary firms.

In 2003, the bank’s efforts to modernize its commercialand operating management, including improvements toevaluation and control mechanisms, made it possible toimprove the quality of services and products and offerbetter prices to customers, thus raising itscompetitiveness.

This required that commercial areas specialize in marketsegments, to boost efficiency, make investment inexpanding the branch network from previous years moreprofitable, and achieve more effective growth in businessvolumes.

Annual Report2003

Other risk indicators measuring portfolio quality, suchas the percentage of non-performing loans andprovisions improved over 2002 and compare veryfavorably to the rest of the system. In the case of therisk index, this remains well below the system as awhole.

In terms of financial trading, BancoEstado is a primeplayer in Chilean currency markets (especially theinterbank market) and abroad, in cash and futures. Inthe domestic market, this role became clear from theleadership it displayed during the liquidity crisis facedby several securities companies, resulting from thefraudulent bankruptcy of a major financial intermediaryearly in the year.

In 2003, the money desk continued to diversify itsservices and products oriented to large private andpublic firms. Liquidity and the investment portfoliomanagement yielded earnings beyond targets.

Commercial management

One key element in the bank’s commercialmanagement during 2003 was to expand its presencein every market, but especially in mass products andservices for personal banking, to generate newrevenues that would offset the sharp decline intraditional income.

Significant commercial growth achieved during the yearbecame a major factor in meeting this goal, at thesame time as it expanded the bank’s client base byseveral hundred thousand people. Thus, BancoEstado’ssuccess today essentially depends on its relationshipswith millions of people and the business it does withthousands of companies.

* Index for the System as a whole** Based on information from the Banking Superintendency (SBIF), through october 2003*** Non- performing loans over total loans portfolio**** Provisions over total loans

BancoEstado Management

0.0

0.5

1.0

1.5

2.0

2.5

%Provisions/ loans****

% non-performing

loans***

Risk index**

1.49

1.82*

1.12

1.71

2.15

2.36Portfolio Risk, 2003 (%)

BancoEstado

Rest of System

0

3

6

9

12

200320022001

10.6

5.5

6.8

1.0

7.7

3.4

Changes in net loans 2001-2003(Real 12-month change in %, through December)

BancoEstado

Rest of System

In this sense, the bank made attractive offers tocustomers by actively passing on interest rate cutsapplied by the Central Bank. Thus, according toinformation from the Superintendency of Banks (SBIF)the interest rates charged by BancoEstado on differentconsumer credit tranches were about 15% to 20%lower than the system average.

This fact, along with other factors, such asrepositioning the bank in the market and the effort

Changes in consumer loans 2001-2003(Real 12-month change in %, through December)

-10

0

10

20

30

40

50

60

200320022001

22.0

-0.3

57.8

8.0

37.3

14.2

BancoEstado

Rest of System

On mass products and services, the growth by almost500,000 voluntary insurance premiums (83%) shouldbe noted, along with the number of customers signedup through Internet, which rose by 540,000 (40%) toreach 1.9 million; telephone contacts, which rose by 1.2million (25%); and automatic bill payment, which roseto 2.2 million (75%).

At the same time, the bank’s net loans (total minusinterbank loans) rose by 7.7% to reach 4.255 billionpesos, compared to the rest of the system, whichexperienced less than half this growth (3.4%). As aresult, the bank’s share of total net loans in the systemreached 13.0%, up from 12.5% the previous year.

In personal banking, active sales campaigns werecarried out focusing on consumer credits andmortgages, called ‘Creditazos’ (great credits) and‘Hipotecazos’ (great mortgages), which were wellreceived by our customers. One factor behind thissuccess was the correct balance between the price-quality ratio of the products and services offered, whichturned them into a good market alternative.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

BancoEstado Management

Annual Report2003

staff put into sales campaigns, helped consumer loansto grow at a rate of 37.3%, contributing more than one-third to the growth in the bank’s net loans in 2003. Atthe same time, given that this growth was higher thanin the rest of the system (14.2%), the bank’s marketshare rose from 11.4% in 2002 to 13.3% in 2003.

Mortgages rose more than double the previous year,14.3% compared to 6.6%, and more than the rest ofthe system. This was possible thanks to the bank’seffective use of favorable market conditions foracquiring housing, especially low interest rates andmore optimistic economic expectations.

These results have confirmed BancoEstado’s leadershipin this market, pushing its market share up to 28.5%.Its presence is much higher in low- and middle-income

sectors, thus reaffirming the bank’s social role. In fact,the average mortgage it provides amounts to US$ 6,000, which is one-quarter of its equivalent for therest of the system, US$ 25,000.

0

5

10

15

200320022001

7.8

2.6

6.65.9

14.3

11.7

Changes in mortgages 2001-2003(Real 12-month change in %, through December)

BancoEstado

Rest of System

SubsidiariesBancoEstado

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

SubsidiariesBancoEstado

Annual Report2003

BancoEstado S.A.Administradora Generalde Fondos (fund manager)

On April 25th, 2003, through resolution N°105, theSuperintendency of Securities and Insurance(Superintendencia de Valores y Seguros, SVS), approvedchanges to the statutes of the firm Administradora deFondos para Vivienda (housing fund manager) to turn itinto the Administradora General de Fondos (generalfund manager). This firm can now manage differenttypes of funds, including those for housing, mutual andinvestment funds.

At the end of the fiscal year, the company managed 46.9billion pesos for 22,135 customers, leading the sector ofsimilar funds, with a 40% market share, in terms ofequity.

Regarding results, the company earned 576 millionpesos in income due to commissions, resulting in a netprofit of 241 million pesos, which represented a 25%return on equity.

BancoEstado S.A.Corredores de Bolsa

(stockbroker)

This broker participates actively in trading currency,intermediating securities, buying term deposits,managing investment portfolios and placing bondissues.

In 2003, was the third largest player, by volume, inelectronic auctions carried out by the Santiago stockexchange (Bolsa de Comercio de Santiago).

Profits reached 1.76 billion pesos, representing a 34%return on equity, thus making it one of the mostprofitable brokerages in the industry.

BancoEstadoServicios de Cobranzas S.A.

(collection agency)

In 2003, the collection subsidiary consolidated itsservices, improving and efficiently monitoring theportfolio of non-performing debt at every stage. At thepre-judicial stage, it managed a total of 7.15 millioncharges, more than double those of 2002, andmanaged to maintain a high recovery rate of 82%,along with a 95% recovery of new debtors, whichtranslated into a substantial saving on provisions.

In 2003, the administration of collection through thecourts achieved national coverage through efficientmanagement, which contributed 17% of thesubsidiary’s income. Because of its management, thebank recovered 22 billion pesos in the form ofpayments and renegotiations.

The 2003 fiscal year closed with a profit of 2.47 billionpesos, up a real 88% over 2002.

BancoEstadoCorredores de Seguros Ltda.

(insurance broker)

Currently, BancoEstado ranks second in premiumsintermediated by bank brokers, with a market share of19% up from 14% the previous year. Similarly, it ranksfourth among the 2000 insurance brokers at thenational level.

During the present fiscal year, voluntary andcompulsory insurance policies reached more than 2.44million.

At the close of the 2003 fiscal year, this subsidiary hadgenerated 6,909 billion pesos in operating revenuesthrough insurance fees, 50% more than in 2002. Ofthis income, 53% came from managing voluntaryinsurance, with a total of 680,600 new premiums.

Its social role focused on offering the cheapestinsurance on the market, reaching sectors thatnormally have no access to these benefits. Thus, in2003, this subsidiary intermediated 77,000 newinsurance policies for micro and small businesscustomers, to reach 127,000 beneficiaries.

Globalnet Comunicaciones Financieras S.A.

(financial communications)

In 2003, Globalnet received less operating revenue dueto changing technology in the financial sphere, whichled its partners to prefer their own applications.

Efforts to turn around the effects of lower incomesuccessfully reduced the losses this fiscal year to 29million pesos, down 78% from 2002.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

SubsidiariesBancoEstado

Annual Report2003

BancoEstado Contacto24 Horas S.A.

(24-hour contact)

This subsidiary, which started up in April 2002, focuseson providing long-distance operating support over thetelephone, the Internet, by e-mail and using automatedtelling machines, which the bank offers to interact withits customers. BancoEstado Contacto 24 Horas worksout of the city of Lota.

During its second year of operations, it achieved aprofit of 57 million pesos, thus turning around lossesfrom 2002. External surveys rate this subsidiary as thebest customer service by telephone in the Chileanbanking industry.

In 2003 it handled more than 380,000 calls per month,considering both those made by bank customers andcalls from executives to customers, as part oftelemarketing campaigns. It also handled 3,900customer e-mails and 5,400 credit requests by Internet.

BancoEstado Microempresas S.A.,

Asesorías Financieras(financial advice)

This subsidiary, which specialized inmicrobusinesses, is a leader in this segment, witha portfolio of 90,000 customers and outstanding

loans worth 59.78 billion pesos, which representannual increases of 62% and 76% respectively. In

terms of this portfolio’s quality, at the end of December2003, risk stood at 1.19%.

From program start-up (1996) to date, this firm hasserved 144,085 microbusinesses, processing 251,910operations for a total amount of 173.51 billion pesos.

During the year, new products for this segment werecreated, particularly credit lines associated with theelectronic check book and the microbusiness creditcard, both very well received by customers. In fact,during this period, 4,761 credit cards and 2,258 creditlines were provided.

In 2003, 21 new special attention platforms werecreated, to include places such as Los Vilos, Rengo,Molina, Curacautín and Nueva Imperial, among others,totaling 91.

During this period, international bodies remainedinterested in finding out more about this experienceand the subsidiary received delegations from banks inEl Salvador, Colombia, Bolivia, Peru and South Africa.