annual report 2003 - alfa laval

TRANSCRIPT

Annual Report 2003

An

nu

al Rep

ort 2003

Alfa L

aval

Highlights of the year2003 in brief

Under the flap:

Alfa Laval in two minutes

2 A stable and positive trend President’s comments

4 Up 57 percent in 2003 The Alfa Laval share

6 Business principles built on trustBusiness concept, business principlesand goals

8 Six gears for profitable growthGrowth strategy

10 The stable platform …Our technologies

12 … that is constantly developingResearch & Development

14 Better order intake in all customer segmentsThe Equipment Division

18 bioKinetics creates possibilities todevelop Life Science segmentThe Process Technology Division

22 Continued growthParts & Service

24 Further improvement in delivery reliabilityThe Operations Division

26 Optimizing knowledge and skills Human Resources

28 Board of Directors’ Report

34 Seven-year overview

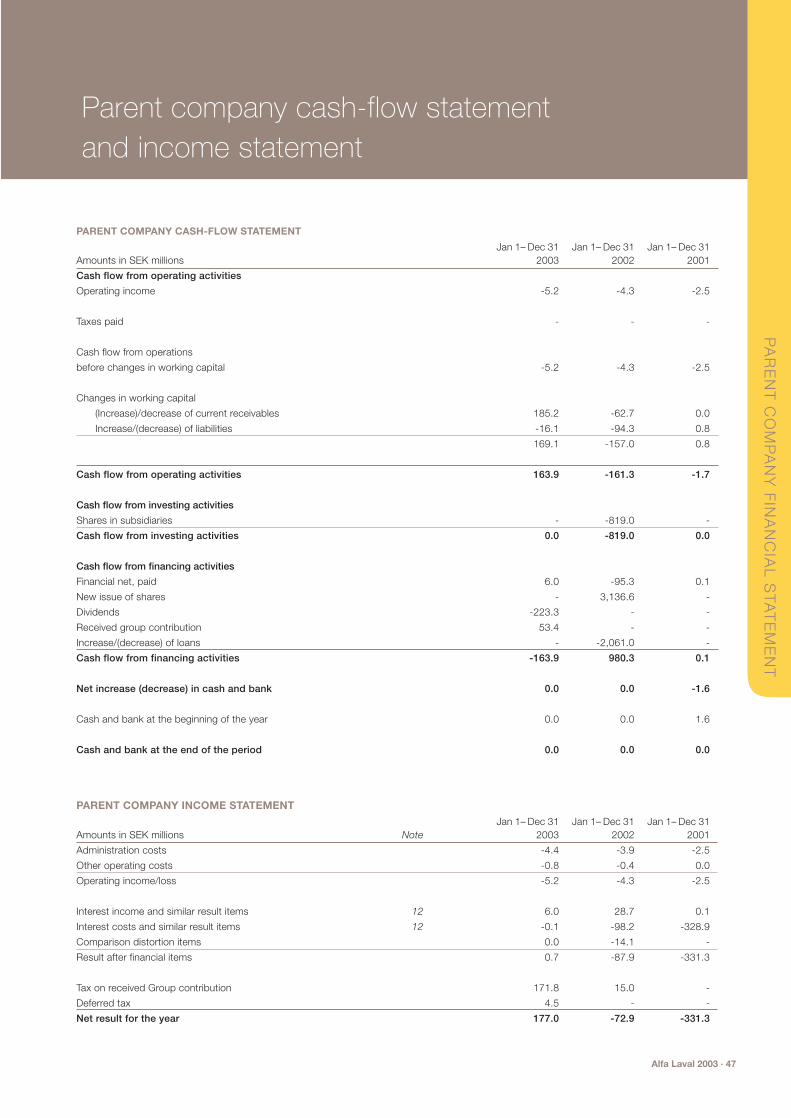

36 Consolidated cash-flow statement

38 Consolidated income statement

42 Consolidated balance sheet

45 Changes in consolidated equity capital

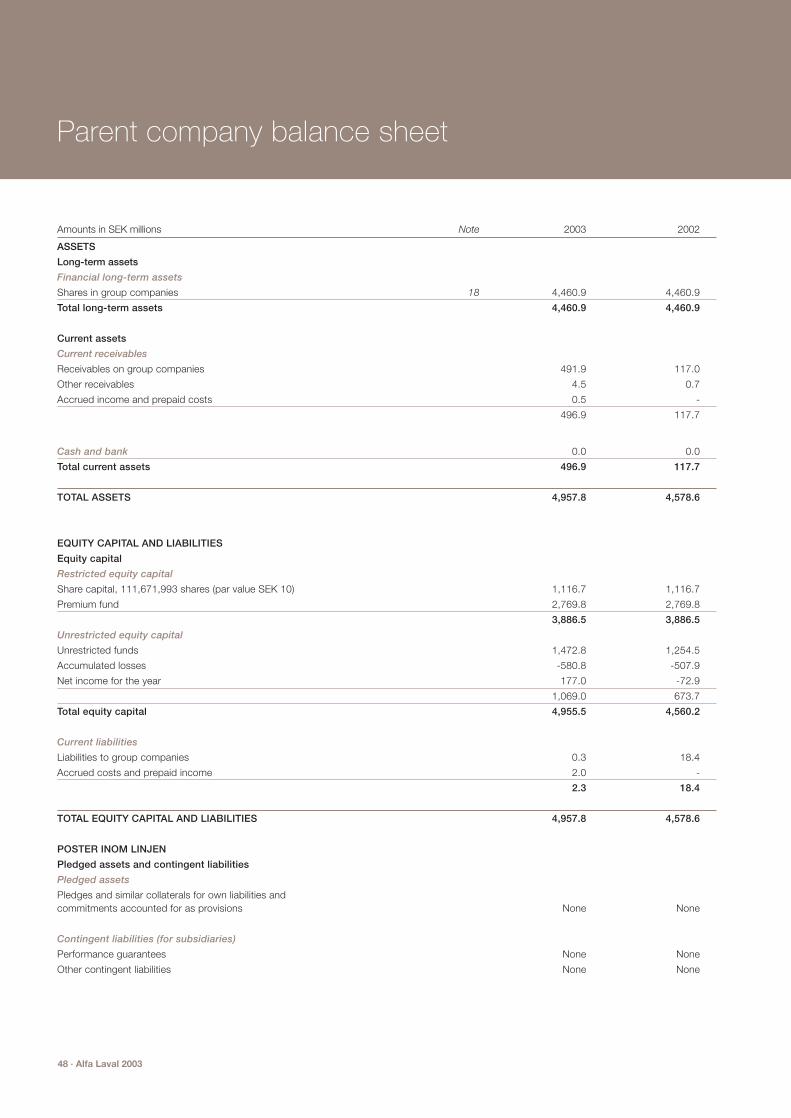

47 Parent Company financial statements

50 Comments to the accounts

55 Risk management

60 Notes to the accounts

86 Proposed disposition of earnings

87 Audit Report

88 Board of Directors and Group management

90 Board of Directors92 Group Management

94 Corporate governance

96 Financial information in 2004

97 Annual General Meeting

Under the flap:

Definitions

Contents

Cover:

Unzip the taste! The tomato – beloved in kitchens round the world for its color, shape and taste. It isalso a key raw material of the food processing industry, since tomatoes form the basis of sauces, soupsand – obviously – the ubiquitous ketchup. Alfa Laval’s separators, heat exchangers and equipment forfluid handling play a key role in transforming ripe, delicious tomatoes into high-quality products, just asin many other sensitive and complex food-related processes. Alfa Laval cooperates closely with thefood processing industry to bring out the inner characteristics of their products. Alfa Laval unzips taste,for consumers to enjoy!

MSEK %

0

3 000

6 000

9 000

12 000

15 000

4

6

8

10

12

14

030201009998 0

1 500

1 000

500

2 000

2 500MSEK

030201009998

120 years youngGustaf de Laval was a great technical geniuswhose inventions include the centrifugal sep-arator and the first functional steam turbine.During his lifetime, he registered 92 patentsand started 37 companies. In 1883, he and hispartner, Oscar Lamm Jr., established the com-pany AB Separator, the forerunner of today’sAlfa Laval.

100 countriesAlfa Laval’s products are sold inapproximately 100 countries, ofwhich 50 through its own salesorganizations. The company has20 large production units (twelvein Europe, six in Asia and two inthe US), and 70 service centers.

Sales of SEK 13.9 billionand an operating margin of 11.7 percent (adjustedEBITA) In 2003, Alfa Laval generated sales of SEK 13.9(14.6) billion. In five years, Alfa Laval’s operatingmargin grew from 6.5 percent (1999) to 11.7 percent(2003). The target is a margin of 12–15 percent.

Alfa Laval in twShare price rises 57 percentAlfa Laval shares rose 57 percent during the year, closing atSEK 109 (69.50). Alfa Laval outperformed both the SAX index(+30 percent) and the SX Industrials 20 (+26 percent). The numberof shareholders increased during the year to 7,254 (5,746).

SEK 1,654 million in operating cash flowDuring 2003, Alfa Laval generated an un-restricted cash flow of SEK 1,654 million, a level that Alfa Laval expects to maintainwith its current operations and financing.

20

40

60

80

100

120

0403

SEK

Alfa Laval

SAX-index

Process Technology Division Equipment Division Parts & Service aftermarket

Energy & Environment

Food

Life Science

Process Industry

Marine & Diesel

OEM

Sanitary

Comfort & Refrigeration

Fluids & Utility

n two minutes

9,350 employeesAlfa Laval currently has about9,350 (9,125) employees world-wide. Most of these employeesare in Sweden (1,941), Denmark(1,098), India (1,031), the US(742) and France (599).

Engineering leadership under constant developmentAlfa Laval’s operations are based on leading global positionsin the three key technologies of heat transfer, separation andfluid handling. Continuous product development is essentialto strengthen competitiveness. About 2.5 percent of totalsales is invested annually in R&D, resulting in 25–30 newproduct launches a year.

Ten customer segmentsThe company’s market orientation has been strength-ened over the past years by the establishment of tencustomer segments. To promote a clear customerfocus, the segments are divided in two divisions –Process Technology and Equipment – which marketand sell the products and special offerings to specificcustomer groups.

Six gears for growthAlfa Laval bases its growthstrategy on growing faster than thecompetition. The company intends togrow while – at least – maintaining itsprofitability. The aim is to achieve an annual average growth rate of fivepercent over a business cycle.

– Alfa Laval acquired bioKinetics, a division of the North Ameri-

can Kinetics Group, Inc. The company is prominent in high-

tech integrated process solutions for the biotechnology and

pharmaceutical industries. In 2002, the company had sales

of about SEK 550 million and about 400 employees.

– Alfa Laval acquired the Denmark-based Toftejorg Group,

the market leader in advanced equipment for tank cleaning

with a focus on the marine and food processing industries.

In 2002, Toftejorg had sales of about SEK 210 million,

and approximately 100 employees.

– It was decided to invest approximately SEK 100 million in

the production of plate heat exchangers in Lund.

– The company launched AlfaNova™, a wholly new type of

compact heat exchanger that tolerates both high tempera-

tures and major stresses – a characteristic that broadens the

range of potential applications and, consequently, the market.

– Anders Narvinger was elected Chairman at the Annual Gen-

eral Meeting.

– The Board proposes a dividend of SEK 4.00 (2.00) per share

for 2003.

– The principal owner, Industri Kapital, reduced its holding from

26.9 percent to 17.9 percent.

2003Key events in

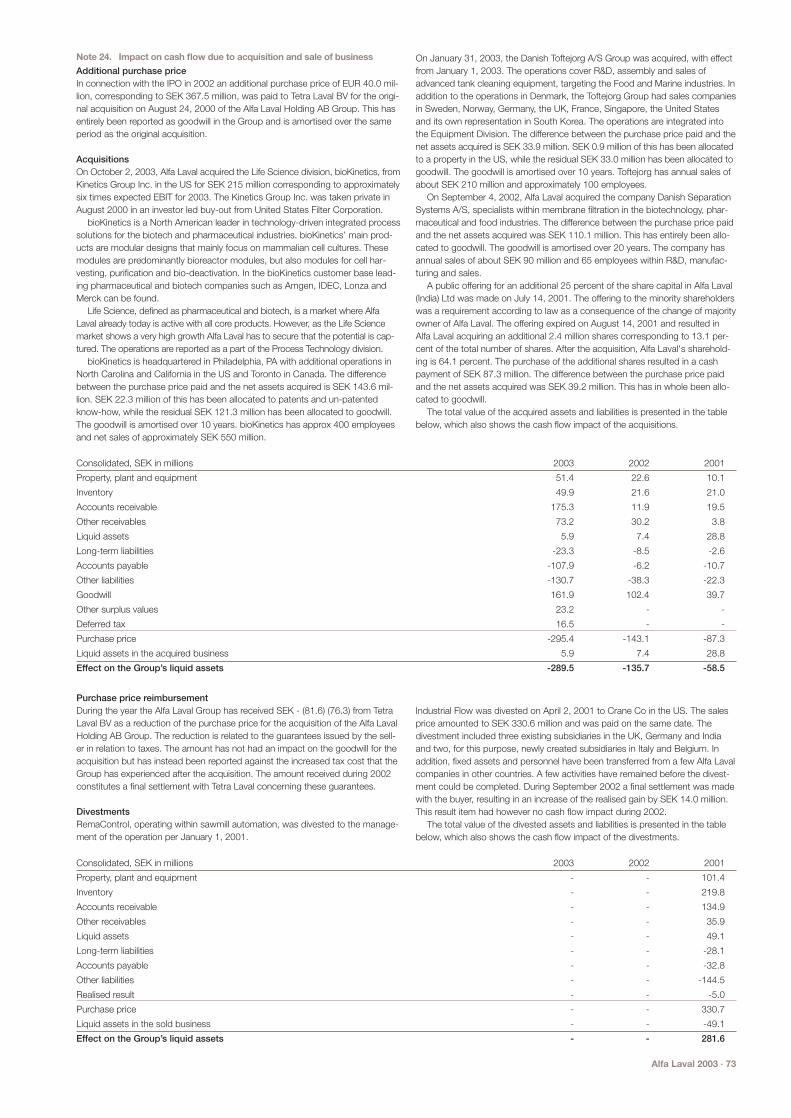

Amounts in SEK M unless otherwise stated 2003 2002 2001

Order intake 14,145 14,675 15,894

Net sales 13,909 14,595 15,830

Adjusted EBITDA1) 1,920 2,087 2,138

Adjusted EBITA 2) 1,627 1,755 1,738

Operating margin (adjusted EBITA 2) ), % 11.7 12.0 11.0

Profit/loss after financial items 817 372 42

Return on capital employed, % 21.3 20.2 18.5

Return on shareholders’ equity, % 13.2 2.7 2.5

Earnings per share, SEK 5.78 1.41 0.96

Equity per share, SEK 43.8 40.4 38.5

Cash flow per share 0.26 0.65 0.50

Equity ratio, % 33.3 29.2 8.2

Debt/equity ratio, multiple 0.49 0.78 5.38

Average number of employees (unit) 3) 9,358 9,125 9,259

1) Adjusted EBITA – Earnings before interest, taxes, depreciation, amortization of goodwill and consolidated surplus

values, and items affecting comparability.

2) Adjusted EBITA – Earnings before interest, taxes, amortization of goodwill and consolidated surplus values, and

items affecting comparability.

3) Average number of employees at the end of the period. Compared with 2002 companies with 457 employees

were acquired.

In 1999, Alfa Laval launched its restruc-turing program, Beyond Expectations.The ultimate goal was to boost theoperating margin from 6 percent to 12 percent, by creating a more efficientorganization and a heightened aware-ness of costs.

After a short time, we perceived agreater potential and decided to raiseour operating margin target to between12 and 15 percent.

In 2003, Alfa Laval had an operatingmargin of 11.7 percent. In 2003, cur-rency effects on the operating profitamounted to SEK 273 million, a result,particularly, of the sharp weakening ofthe US dollar during the fourth quarter.Excluding currency effects, the oper-ating margin was 12.7 percent, com-pared with 12 percent in 2002.

Beyond Expectations complete

At the end of the third quarter of 2003,the savings goal of a minimum of SEK850 million was achieved and theBeyond Expectations program was con-cluded. We now have an efficient andmarket-oriented organization and havereduced the number of employees from12,200 to 9,358. Corporate acquisitionsexcluded, that amounts to a reductionof more than 20 percent.

The restructuring program had a rip-ple effect: employees are now keenlyaware of costs. This, combined with the

full implementation of our growth pro-gram, is a precondition of any furtherimprovement in our operating margin.

Brighter business conditions ahead

Starting mid-year 2003, a number ofsigns of improved business conditionsfor industry appeared. For example, we noted a sharp increase in customerinquiries in the marine industry, whichresulted in a substantial increase inorder bookings in that segment. Thisincrease then continued throughoutthe second half of the year.

Order intake for Alfa Laval rose dur-ing the year by 4.9 percent, excludingeffects of currency fluctuations. Theincrease was particularly noticeableduring the second half of the year,when it was a full 10.7 percent. Geo-graphically, the increase in orderintake occurred mainly in Asia andEastern Europe, whereas North Americaand Western Europe were somewhatweaker than in 2002. Toward year-end,however, signs of a recovery werenoted in these regions as well.

Order intake up in the second half

Alfa Laval conducts sales from twodivisions, the Equipment division andthe Process Technology division. Thecustomers of the Equipment divisionhave well-defined recurring needs ofparticular products and product pack-

2 · Alfa Laval 2003

President’s comments

“ Assuming that the recovery will not be affected by unforeseen events in the world, we believe in a strong increase in ordersreceived during 2004.”

A stable andpositive trend

ages, whereas the Process Technologydivision offers both complete processlines and products.

During the year, the order intake rose7.1 percent in the Equipment divisionand 2.3 percent in the Process Technolo-gy division. The tendency for the recov-ery to appear in the Equipment divisionfirst has also been observed in previousswings of the economic pendulum. Themajor capacity investments undertakenby the industry appear later in the busi-ness cycle. In the fourth quarter, orderbookings in Process Technology rose12.7 percent, which may indicate thatindustry is beginning to undertakemajor investments.

Nine of our customer segments re-ported increased order intake in 2003.Only the Process Industry segment,most of the customers of which are inthe chemical industry, reported a decline, which is in line with theabove – that is, that major industrialinvestments are not yet occurring on a large scale.

The profitable aftermarket remainedstrong in 2003, accounting for 26.1percent of the Group’s sales. Orderintake in this segment were up for thefourth consecutive year.

To meet an increase in demand in2003, several production units tookmeasures to increase their productioncapacity. For example, it was decidedto build an extension to the Group’sfacility in Lund, an undertaking thatwill cost approximately SEK 100 mil-lion. Other major capacity investmentswere undertaken in China and India.

Share price up 57 percent

The past year was Alfa Laval’s first fullyear as a listed company since its

Growth strategy

To create growth, Alfa Laval employs astructured strategy based on six gears,each of which is designed to increasegrowth (read more about this strategyon page 8 and 9). The aim is to achieveannual growth rate of 5 percent over a complete business cycle.

In 2003, Alfa Laval carried out twoacquisitions: the Danish Toftejorg, a specialist company in tank cleaning andan attractive supplemental acquisition;and the American company, bioKinetics,operating in the growing Life Sciencesegment.

Acquisitions are a key part of the company’s growth strategy. Alfa Lavalcontinuously evaluates attractiveprospective acquisitions, particularly inthe Life Science and Water Management,but also within a broader spectrum inwhich acquisitions involve supplemen-tal products.

Outlook for 2004

Markets recovered during the secondhalf of 2003 within most of the cus-tomer segments in which Alfa Laval isactive. It is our opinion that the recov-ery will continue during 2004. As-suming that the recovery will not beaffected by unforeseen events in theworld, we believe in a strong increase inorders received during 2004.

We assess that the EBITA-margin,excluding currency effects, will beimproved.

return to the stock market in May 2002.During the year, Alfa Laval sharesappreciated 57 percent, while theexchange as a whole appreciatedapproximately 30 percent and AlfaLaval’s industrial benchmark indexappreciated 26 percent.

During the year, Alfa Laval publishedthe company’s “Business Principles.”For several years, these principles havebeen a natural and integrated aspect ofAlfa Laval corporate culture. In 2003,they were assembled in a document.The carrying out of business transac-tions is based on trust, and this is wherethe Business Principles come in. Com-bined with the Alfa Laval core values,these principles define the manner inwhich the company should behave.

Asbestos lawsuits in the US

On December 31, 2003, Alfa Laval’s USsubsidiary, Alfa Laval Inc., was one of anumber of defendants in a class-actionsuit involving a total of 19,900 plain-tiffs and comprising 123 asbestos-relatedcharges. During the fourth quarter in2003, the total number of charges roseby two, and the number of plaintiffsdropped by 400. About 99 percent ofall plaintiffs are from cases launched inMississippi.

Based on current information andAlfa Laval’s understanding of these law-suits, Alfa Laval continues to believethat these lawsuits will not have a

material adverse effect on the compa-ny’s financial condition or results ofoperation.

Constant product development to

maintain and enhance competitiveness

To maintain and enhance the Group’scompetitiveness, existing products mustbe constantly updated. Alfa Laval in-vests approximately 2.5 percent of itssales annually in research and develop-ment. The R&D operations are inten-sively market and customer-oriented –in 2003, Alfa Laval continued to devel-op new and more efficient products inall of its key segments.

The annual pace was about 25–30 newproducts. One of the most impressivewas the new technology platform for anew category of plate heat exchangerscalled AlfaNova™. The product can with-stand the combination of high tempera-tures and high pressure much betterthan other welded plate heat exchangers– characteristics that broaden its marketconsiderably.

Another was the Solid C, a completelynew standard pump for hygiene applica-tions. Based on an advanced hygienicdesign, this product is used for gentlefluid handling.

For the biotechnology sector, theGroup offers Culturefuge 100, a small,powerful separator that separates delicatecells in a gentle but effective manner.

Alfa Laval 2003 · 3

President’s comments

Sigge HaraldssonPresident and Chief Executive Officer

Lund, Sweden, March 2004

Volume of shares tradedSX20 IndustrySAX All Share indexAlfa Laval

DecNovOctSepAugJulyJuneMayAprMarFebJanS

OU

RC

E:

SIX

/HA

LLV

AR

SS

ON

&H

ALV

AR

SS

ON

SEK No. of shares, 000s

2003

Volume of shares tradedSX20 Industry SAX All Share indexAlfa Laval

SO

UR

CE

: S

IX/H

AL

LVA

RS

SO

N&

HA

LVA

RS

SO

N

SEK No. of shares, 000s

20032002

40

60

80

100

120

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

DecNovOctSepAugJulyJuneMayAprMarFebJanDecNovOctSepAugJulyJune

40

60

80

100

120

0

5,000

10,000

15,000

20,000

25,000

February 24, Q4 2002 report

April 29, Q1 2003 report

August 14, Q2 2003 report

October 28, Q3 2003 report

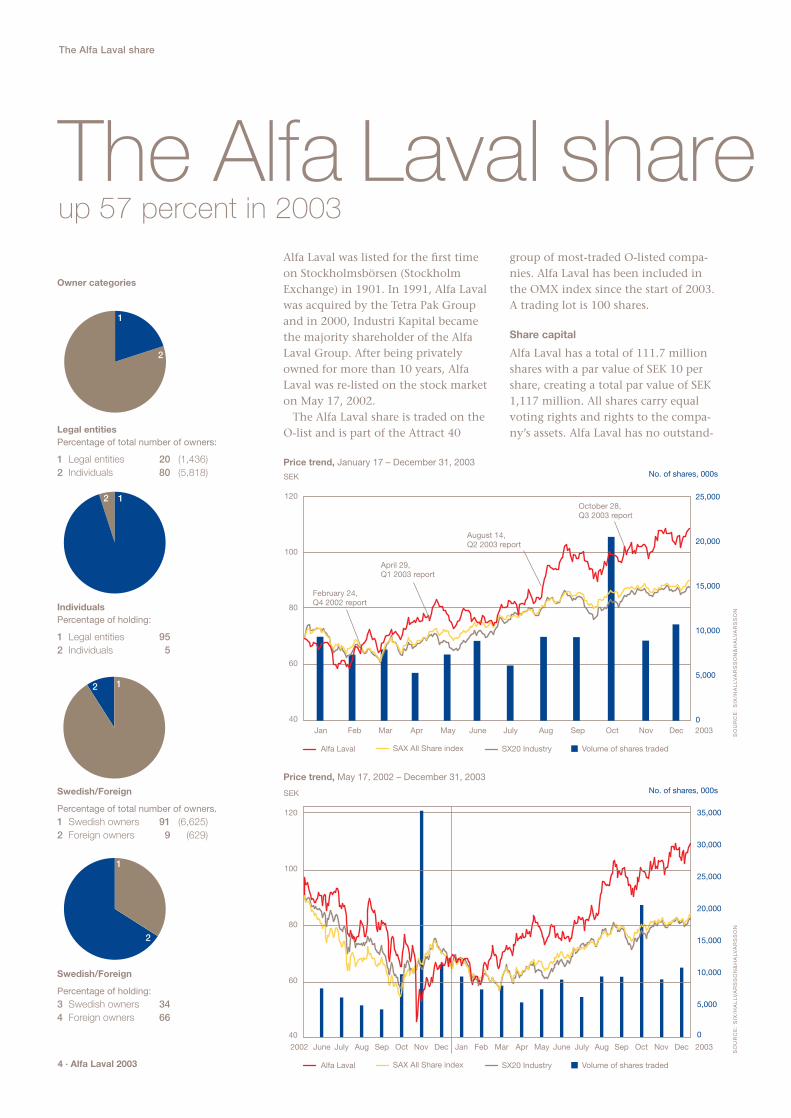

Price trend, January 17 – December 31, 2003

Price trend, May 17, 2002 – December 31, 2003

4 · Alfa Laval 2003

The Alfa Laval share

The Alfa Laval share up 57 percent in 2003

Alfa Laval was listed for the first timeon Stockholmsbörsen (StockholmExchange) in 1901. In 1991, Alfa Lavalwas acquired by the Tetra Pak Groupand in 2000, Industri Kapital becamethe majority shareholder of the AlfaLaval Group. After being privatelyowned for more than 10 years, AlfaLaval was re-listed on the stock marketon May 17, 2002.

The Alfa Laval share is traded on theO-list and is part of the Attract 40

group of most-traded O-listed compa-nies. Alfa Laval has been included inthe OMX index since the start of 2003.A trading lot is 100 shares.

Share capital

Alfa Laval has a total of 111.7 millionshares with a par value of SEK 10 pershare, creating a total par value of SEK1,117 million. All shares carry equalvoting rights and rights to the compa-ny’s assets. Alfa Laval has no outstand-

12

1

2

1

2

12

Swedish/Foreign

Percentage of holding:3 Swedish owners 344 Foreign owners 66

Swedish/Foreign

Percentage of total number of owners. 1 Swedish owners 91 (6,625)2 Foreign owners 9 (629)

IndividualsPercentage of holding:

1 Legal entities 952 Individuals 5

Legal entitiesPercentage of total number of owners:

1 Legal entities 20 (1,436)2 Individuals 80 (5,818)

Owner categories

Ownership distribution by size at December 31, 2003

Holdings Number of Number of shares Holdings, %shareholders

1 – 500 5,030 937,901 0.84501 – 1,000 846 743,656 0.67

1,001 – 5,000 812 2,059,588 1.845,001 – 10,000 185 1,415,434 1.27

10,001 – 15,000 69 886,813 0.7915,001 – 20,000 50 884,389 0.7920,001 – 262 104,744,212 93.80

Total 7,254 111,671,993 100.00

ing options or other equity-relatedinstruments, so there is no potentialdilution effect.

Share performance

In 2003, Alfa Laval shares appreciatedby 57 percent. This can be comparedwith the stock market as a whole, theSAX All Share Index, which rose 30percent, and the industry index, SX20Industry, which rose 26 percent. Thehighest quotation of the year for AlfaLaval, SEK 110, was reached in Decem-ber. The lowest, SEK 58, was reached inFebruary.

A total of 108 million shares changedowners, corresponding to a value ofSEK 9.2 billion. This corresponds to a turnover rate* of approximately 96 percent. In comparison, turnoverrates for the stock market as a whole in 2003 amounted to 124 percent andto 78 percent on the O-list.

The average size of transactions wasaround 2,190 (5,300) shares and a totalof slightly less than 200 (140) transac-tions, on average, were carried out pertrading day.

Dividend

The dividend is subject to regulationsof the Swedish Companies Act andgeneral market practices, and may onlybe allotted following a decision by theAnnual General Meeting.

The Board of Directors of Alfa Lavalintends to propose a dividend thatreflects the Group’s development,financial position and estimated capi-tal needs.

For 2003, the Board has proposed tothe Annual General Meeting a divi-dend of SEK 4.00 (2.00).

Alfa Laval shareholders

At year-end, the company had a totalof 7,254 (5,746) shareholders. OnDecember 31, 2003, Industri Kapitaland Tetra Laval BV were the two largestowners. On October 29, Industri Kapi-tal reduced its holding to 17.9 percent.Combined, the ten largest shareholdersown approximately 60 percent of thetotal number of shares.

Shareholder information update

We provide regular updates on thecompany on our website,www.alfalaval.com. Here you can alsofind the latest information regardingAlfa Laval’s performance on the stockmarket.

The 10 major owners/asset managers at December 31, 2003

Number of shares Capital %

Industri Kapital 2000 Fund 20,015,628 17.92Tetra Laval BV 19,744,014 17.68Third AP Fund 5,072,407 4.54State Street Bank and Trust (US) 4,577,164 4.09Fourth AP Fund 4,291,700 3.84Robur Funds 3,849,529 3.44Fidelity Funds (Luxembourg) 2,819,800 2.52Lannebo Funds 2,523,995 2.26MSF Mutual Funds (US) 2,228,400 1.99First AP Fund 1,914,800 1.71Others 44,634,556 40.01

Total 111,671,993 100.00

16

3

45

2

Geographic division of ownership(Free float, excluding Industri Kapital and Tetra Laval), %

1 Sweden 522 US 203 UK 94 Luxembourg 65 Norway 26 Others 11

0

3

6

200320022001 200320022001

Cash flow per share, SEK2001: 0.502002: 0.652003: 0.26

Earnings per share, SEK 2001: 0.962002: 1.412003: 5.78

30

40

50

200320022001

Equity per share, SEK2001: 38.52002: 40.42003: 43.8

* Turnover rate is calculated as the total number of shares traded in one year, relativeto the total number of shares outstanding.

0.8

0.6

0.4

0.2

0.0

6 · Alfa Laval 2003

Business concept, business principles and goals

Business principles built on trust

Alfa Laval’s daily work is inspired byconstant effort to increase added valuefor customers. Satisfied customers cre-ate a company with competitive, con-tinuous value growth for shareholders.

A distinct business concept

“To optimize the performance of ourcustomers’ processes. Time and timeagain.”

For 120 years, Alfa Laval has providedproducts of the highest quality. To staysuccessful, however, something more isneeded – an extra value important tothe company’s customers. This is whatthe business concept is all about.

This is a demanding concept, butAlfa Laval probably has greater experi-ence and knowledge about its processsegments than any other company inthe world.

The foundation of Alfa Laval’s busi-ness concept is its customers. To make

in which the company should behave.Company management places greatemphasis on the importance of com-plying with these principles, and willfollow them up via the internal auditfunction.

Alfa Laval’s four business principles

1. Environment

“Optimizing the use of natural resources is our business.”

Alfa Laval and the company’s productsmake a significant contribution toreducing the environment impact ofindustrial processes.

2. Social

“Respect for human rights is fundamental.”

Alfa Laval respects human rights andthe widely differing social cultures inwhich it operates and to which itdelivers its products and services.

3. Business integrity

“High ethical standards guide our conduct.”

Alfa Laval’s approach to businessdevelopment is based on honesty,integrity and respect for others.

4. Transparency

“Our commitment to open dialogue builds trust.”

While Alfa Laval believes in forthrightcommunications, at the same time, thecompany is careful not to release infor-mation that is commercially sensitiveor valuable.

a company sustainable and successful,customers must continuously be pro-vided added value.

Alfa Laval must be an attractive long-term investment. Shareholders want tominimize the risk of their investments,which Alfa Laval does for them by con-tinuously improving its appeal – espe-cially as an employer, a supplier and acustomer.

Alfa Laval’s business principles

are built on trust

During the year, Alfa Laval publishedits Business Principles. For several years,these principles have been a naturaland integral part of Alfa Laval corpo-rate culture. In 2003, they were assem-bled in a document.

The carrying out of business transac-tions is based on trust, and this iswhere the Business Principles come in.Combined with the Alfa Laval core val-ues, these principles define the manner

-6

0

6

200320022001

5

0

12–15

0

15

200320022001

20

0

25

200320022001

Volume growth, %

2001: 3.42002: -2.32003: 3.6

EBITA margin, %2001: 11.02002: 12.02003: 11.7

Return on capital employed, %

2001: 18.52002: 20.22003: 21.3

Volume growth

Goal : Average of 5 percent over

a business cycle.

The goal will be achieved through a combi-

nation of organic growth and acquired

growth. The underlying organic growth of

Alfa Laval’s markets is estimated at around

two percent.

EBITA* in relation to sales

Goal : 12–15 percent.

The goal is to reach an EBITA margin of

12–15 percent of sales. The lower end of

the target range applies during economic

downturns while the upper end applies

during periods of expansion.

Return on capital employed

Goal : 20 percent.

Despite substantial goodwill and allocated

surplus values, ROCE should reach

20 percent. This level is established with

the low tied-up capital in mind, and as a

result of the current profitability and the

goal of further improving profitability.

Financial goals

Alfa Laval 2003 · 7

Business concept, business principles and goals

(*EBITA= Operating profit before amortization of

goodwill and depreciation of other step-up values)

Financial standardsAs a supplement to the aforementioned objectives, the standards for a number of relevant

financial key ratios that will help Alfa Laval meet the financial goals are described below.

unrestricted cash flow will generate a sub-

stantial amount, regardless of the debt/

equity ratio, but within the framework of the

guidelines for debt/equity ratio that the com-

pany has established.

Investments

Goal : approximately 2.5 percent of sales.

Outcome 2003 : 1.9

For existing operations, Alfa Laval’s objective

is to maintain investments in fixed assets at a

level corresponding to about 2.5 percent of

sales. This corresponds to depreciation

according to plan. The purpose of this stan-

dard is to allow some scope for replacement

investments and create a capacity expansion

in line with organic growth for the Group’s

current key products.

Debt/equity ratio

Goal : below 1.0.

Outcome 2003 : 0.49

As a standard, Alfa Laval aims to have a

debt/equity ratio that, in the long term, will

be lower than 1.0 – that is, the company’s

borrowed capital may not amount to more

than 100 percent of the book value of its

shareholders’ equity. Debt/equity ratio may

increase in connection with major acquisi-

tions but this has to be viewed as temporary

since cash flow and profits are expected to

offset this effect.

Cash flow from current operations

Goal : 10–14 percent of sales.

Outcome 2003 : 11.9

The standard is set slightly lower than the

target operating-margin, adjusted EBITA,

because organic growth normally results in

an increase in tied-up working capital. The

Acquisitions and divestments since 1998(Companies and sales volume*)

Acq

uisi

tio

nsD

ives

tmen

ts

19991998 2000

*Refers to the year prior to divestment or acquisition.

Growth strategy

Six gearsfor profitable growth

During the second half of 2002, AlfaLaval launched a growth strategy. Thebasic philosophy is to grow faster thanthe market, and maintain profitabilityduring growth.

Alfa Laval’s strategy for profitable growth

is based on the following six gears:

1. Strong growth from current productsand services

Close cooperation with customers tounderstand and satisfy their require-ments will ensure that the grow wehave had in the past, based on our keyproducts, will be strengthened in thefuture. Examples of how Alfa Lavalapplies this gear include the weldedplate heat exchanger Compabloc andthe intelligent valve, ThinkTop.

2. Market-driven research and development

One of the cornerstones of Alfa Laval’ssuccess has been to be the marketleader in our key technologies. Themission of the company’s R&D organi-zation is to improve current productsand make them even more competitivein the market. Our customer segment-based organization will furtherstrengthen our dialog with customers.Examples include AlfaCond (see page 12)and AlfaNova (see page 13).

3. The new marketing organization, with ten focused customer segments

Since the marketing organization focus-es on customer segments while simulta-neously working with the company’sentire product range, it can work moreclosely with customers and help im-prove customers’ processes. We haveone face for every customer, and caneffectively add value for the customer.

An example of this is the acquisitionin 2003 of the Danish Toftejorg, whichproduces products for tank cleaning –products that add to Alfa Laval’s rangeof food and marine-related products.

4. Aftermarket

The aftermarket offers considerable pos-sibilities for further growth. We have alarge base of installed equipment andsystems, and through our global net-work of workshops and personnel, weare well equipped to manage this serv-ice. Our product range has increasedsubstantially, and service contracts, particularly, are now playing a moreimportant role.

5. New marketing concepts

We are constantly looking for new waysto improve our service to help customersto optimize their processes. It is a matterof looking at things in different ways,being cost-driven instead of product-driven. Two examples are Octopus –groundbreaking software for optimizingthe operation of decanter centrifuges(read more on page 20) – and Alfdex –an innovative solution for cleaningcrankcase gases from diesel engines,based on the separation of oil dropletsand particles from the gases (see page 13).

6. New key products

Identifying and adding, within theframework of our strategy, not onlysupplementary products but also newkey products is a step that can providean extra boost to growth. It enables us

Acquisition criteria

Alfa Laval has established the followingfinancial criteria for acquisitions:

Supplementary acquisitions

(such as the Danish-based Toftejorg):

The acquisition price may be no morethan eight times EBITA.

The operations must contribute posi-tively to the Group’s cash flow andearnings per share, within not morethan 18 months.

Strategic acquisitions (such as the Danish-based DSS):

The operations must contribute posi-tively to the Group’s cash flow andearnings per share within no more than24–36 months.

Auto

mat

ion

Bus

ines

s Ar

ea

SEK

1,11

5 M

Vica

rb G

roup

, Fra

nce

SEK

425

M

Scan

dibr

ew, D

enm

ark

SEK

67

M

Kva

erne

r Het

land

, Nor

way

SEK

57

M

Dor

r Oliv

er, U

S

SEK

127

M

Sepa

rato

r Div

isio

n

of W

ytw

orna

Spr

zeta

Pola

ndSE

K 2

0 M

Cel

leco

SEK

654

M

Ther

mot

echn

ikSE

K 4

9 M

Car

dina

lSE

K 3

9 M

Tetr

a Pa

k D

ivis

ion

of In

dian

sub

sidi

ary

SEK

47

M Airc

oil

SEK

51

M

Alfa Laval 2003 · 9

2001 2002 2003

Growth strategy

to further increase our product offeringand be a more complete and an evenmore valuable partner. Examples of thisgear include the acquisition in 2002 ofDanish Separations Systems (DSS), acompany that develops, manufacturesand sells membrane filters.

Annual volume growth of about 5 percent

Alfa Laval expects that these six gearswill result in the company growing byan average of about five percent peryear over a complete business cycle,including acquired and organic growth.Alfa Laval’s markets are expected togrow by about two percent per yearover a complete business cycle.

Strategy for acquisitions and alliances

Alfa Laval’s business concept of opti-mizing the performance of our cus-tomers’ processes, time and again, isalso the basis of our acquisition/alliancestrategy.

This means that we must undertakeacquisitions/alliances:

– that strengthen our existing key products

– of new key products

– around products that complementour current products and that canstrengthen the customer offering that our customer segments make.

Two areas on which Alfa Laval is focus-ing are Life Science and Water Manage-ment – robustly expanding marketsthat already use Alfa Laval’s key prod-ucts. Life Science comprises mainly thepharmaceutical and biotechnologyindustries. In 1999–2002, the annualgrowth of this area was eleven percent,and it is expected to continue to growat the same rate for the next few years.

Water Management includes equip-ment and systems for water, waste waterand sludge – a market that investsapproximately SEK 13,000 million per

year in equipment and service, andthat is expected to grow by slightlyover ten percent per year until 2007.Trends such as more stringent environ-mental legislation, tighter purificationrequirements on companies and greaterhygiene are expected to exert furtherimpetus on this development.

Alfa Laval’s public listing in thespring of 2002, and the financialstrength that resulted from it,have made growth throughacquisitions an attractiveprospect. Since the list-ing, the Group hasmade the followingacquisitions:

• bioKinetics, US, withsales of approxi-mately SEK 550 million in 2002. Thecompany is market-leading in the NorthAmerican market for inte-grated process solutions inbiotechnology and the pharma-ceutical industry.

• Toftejorg, Denmark, with sales ofapproximately SEK 210 million in2002. The company is market-leadingin equipment for advanced tankcleaning, and fits in well in theMarine and Diesel and Sanitary cus-tomer segments.

• Danish Separation Systems, (DSS), Denmark, with sales of approximatelySEK 90 million in 2001. Specialists inmembrane filtration, the establishedsolution for separating small parti-cles, particularly in biotechnology,pharmaceutical and food industries.

To enable the Group to proceed withacquisitions and form alliances in a systematic and efficient manner, in2002 Alfa Laval instituted the specialfunction, Business Development.

An a

dditi

onal

13 p

erce

nt o

f

shar

e ca

pita

l

of A

lfa L

aval

Indi

a

DSS

, Den

mar

k

SEK

90

M

Tofte

jorg

, Den

mar

k

SEK

210

M

bioK

inet

ics,

US

SEK

550

M

Rem

a C

ontro

lSE

K 6

8 M

Indu

stria

l Flo

wSE

K 6

56 M

Alfa Laval’s strategy for growth is structuredin six gears, which willprovide an annual vol-ume growth averaging five percent annually.

spiral heat exchangers and air heatexchangers. The plate heat exchanger isthe main product and has many appli-cations. Alfa Laval estimates that it hada combined market share of approxi-mately 36 percent in 2003. Spiral heatexchangers are used in the pulp industryand in waste treatment. Air heat ex-changers are used for air conditioningand refrigeration.

There is a clear tendency in the pro-cessing industry to switch from tradi-tional shell-and-tube heat exchangers tocompact heat exchanges such as plateheat exchangers because the latter savespace and energy and provide bettermaintenance security than shell-and-tube heat exchangers.

Alfa Laval’s largest competitors in thisarea are Tranter/ SWEP (US), Invensys-APV (UK) and MG Technologies/GEAEcoflex (Germany).

Separation

Ever since the company was formed in1883 to capitalize on Gustaf de Laval’sinvention, the cream separator, the sep-aration technology has been a centralpart of the operations. The technologyis currently used to separate liquids fromother liquids and solid particles fromliquids. The separators are used in anumber of industrial processes withinthe food processing and chemical indus-tries, on ships, to purify fuel and lubri-cating oil, on oil rigs, to separate oil andwater, in the mechanical engineeringindustry, to purify industrial fluids, andin industrial and municipal wastewatertreatment plants. Alfa Laval is a globalmarket leader in centrifugal separation,according to the company’s estimates,in 2003 its share of the global marketfor all separation products combinedwas 24 percent.

10 · Alfa Laval 2003

The stableplatform…

A plate heat exchanger is constructedfrom a number of metal plates. Betweenthe plates are channels through whichtwo fluids, one hot and one cold, pass onopposite sides of the plates and in oppo-site directions to each other. Heat/coldare transmitted via the plates from onefluid to the other.

During the second half of 2003, AlfaLaval launched its AlfaNova, which offersperformance features that far exceedthose of existing plate heat exchangers,which increases its competitive advan-tage and broadens its area of application(read more about AlfaNova on page 13).

Our technologies

The core of Alfa Laval’s operations isbased on three key technologies – heattransfer, centrifugal separation and fluidhandling – with all three playing a deci-sive role in most industrial processes.Alfa Laval holds leading global posi-tions in all of these areas of technology.

Heat transfer

Alfa Laval’s heat exchangers are used forapplications such as heating, cooling,freezing, ventilation, evaporation andcondensation of fluids. As a result of the many applications in which heatexchangers can be used, Alfa Laval has a considerably large and geographicallydiverse customer base within industriessuch as chemical, food processing, oiland gas production, power generationand marine industries and for heatingand ventilation of buildings.

Alfa Laval’s heat-transfer productrange consists of plate heat exchangers,

Alfa Laval 2003 · 11

personal care products. Alfa Laval is amarket leader in fluid handling with anestimated global market share of tenpercent in 2003.

There are three types of high-sanitarypumps:• Centrifugal pumps, which combines

high efficiency with careful producttreatment.

• Rotary lobe pumps, which are used tofacilitate the flow of low-viscosity fluids that require a high standard ofhygiene.

• Liquid-ring pumps, which have a widerange of applications.

Valves are used to regulate and redirectliquid flows. Alfa Laval’s mixproof valvesare delivered as a complete package ofsolutions, complemented by intelligentregulating equipment. Butterfly valvesare suitable for very liquid products andseat valves are characterized by a fewmovable parts and are used, for example,as stop or divert valves.

Alfa Laval’s main competitors in thisarea are: MG Technologies/GEA (Germany), Invensys/APV (UK), Waukesha/Cherry Burrell (US) and ITT Industries (US).

High-speed separators and decantercentrifuges are Alfa Laval’s dominantproducts within centrifugal separation.High-speed separators are primarily usedfor separating fluids. A decanter cen-trifuge is a horizontal separation tech-nique that uses a slower speed than thehigh-speed separation technique. It ismainly applied in the separation of arelatively higher solid content. Forexample, decanter centrifuges are usedin dewatering in wastewater treatmentplants.

As a key supplement to its own rangeof separator products, Alfa Laval in 2002brought the membrane filtration systeminto the company through the acquisi-tion of Danish Separation Systems A/S(DSS). Membrane filtration is theaccepted industry standard for sepa-rating less dense particles, which is agrowing need within the food, biotech-nology and pharmaceutical industries.

Alfa Laval’s largest competitors in thisarea are: MG Technologies/GEA West-falia Separator (Germany), Andritz(Andritz Bird, US and Andritz Guinard,France), Mitsubishi Kakoki Kaiska (Japan),Pieralisi (Italy) and Flottweg (Germany).

Fluid handling

Transporting and regulating fluids in asafe and efficient manner is vital forindustries. Alfa Laval focuses its compe-tence on fluid handling, where thedemand for hygiene is high. The com-pany’s pumps, valves and installationmaterial are used in fluid-handlingapplications such as in the productionof beverages, dairy products, food,pharmaceutical products, health and

One of the productslaunched by Alfa Laval in2003 in the key technologyof fluid handling is theSolid C – a completely newstandard pump for hygieneapplications. Solid C isbased on an advanceddesign for careful handlingof fluids.

Our technologies

Due to the centrifugal force in the separators,the fluid/particles with the greatest density collect in the outer periphery of the separatorbowl, and the fluid with the lower density in thecenter of the bowl. Both fluid phases are thendischarged through separate outlets.

In 2003, Alfa Laval launched its Culturefuge100, which is used in the biotechnology sectorto efficiently separate the most important partsof cells, so that new drugs may be produced.Read more about Culturefuge 100 on page 13.

12 · Alfa Laval 2003

Research & Development

To boost market potential in the exist-ing operations, Alfa Laval can broadenits offering by adding products suitablefor other capacities, pressures and tem-peratures. Enhancing growth prospectmay also involve producing versions ofnew material, and to automate andintegrate intelligent functions in theproducts, such as measuring and re-introducing information, or analyzingand forecasting.

Over the past few years, the com-pany’s commitment to research anddevelopment has resulted in the fol-lowing products:

AlfaCond

First purpose-built plate condenser in

the world

AlfaCond is the first plate condenser inthe world, purpose-built for the marketfor condensation of vapors at low pres-sure. What makes this product specialis its size, and the placement of theinput and output steam channels, con-densation and cooling water.

The Alfa Laval brand has been associat-ed with innovation for over 100 years.An ongoing, consistent commitment toResearch & Development (R&D) hasbeen critical in building, strengtheningand developing the company’s globalmarket leadership. Alfa Laval’s R&D isdistinctly customer-oriented, with theaim of devoloping better solutions forthe customer.

Total R&D expenses amounted toSEK 368 million (355) in 2003 – that is,approximately 2.6 (2.4) percent of theGroup’s total sales. The Group hasabout 290 employees and four centerswithin R&D. The Process TechnologyDivision and the Equipment Divisionhave their own R&D functions for over-seeing their respective customer seg-ment and funnel resources to areaswhere there is most growth potential.Such areas include biotechnology andwastewater treatment.

25 – 30 new products annually

Alfa Laval’s R&D operations are basedon a long-term commitment to basicresearch, focusing primarily on stream-ing technology and heat transfer. Thecompany launches 25–30 new productsannually.

Alfa Laval holds more than 200 patentson its own products, and the brandname Alfa Laval is registered in around100 countries.

Steady product renewals

sharpen competitive edge

To remain competitive and stay in busi-ness, Alfa Laval needs to constantlyupgrade its products to cope with thechanging demands and needs of cus-tomers. This often involves relativelyminor adjustments that could lead tomajor improvements for customers.

...that is constantly developing

0

1

2

3

03020100

R&D investments in percentage of net sales

2000: 2.92001: 2.22002: 2.42003: 2.6

0

250

500

03020100

R&D investments in SEK M

2000: 441 2001: 3412002: 3552003: 368

Research & Development within Alfa Laval is carried out in four research centers. Thepictures shows the facility in Tumba, Sweden.

Alfa Laval 2003 · 13

Research & Development

tion to improving performance, mini-mizes the need for installed electricity,improves process control and reducesthe need for maintenance.

Alfdex

An innovative solution for cleaning

crankcase gases

Alfdex, an innovative solution for clean-ing exhaust fumes from diesel engines byseparating oil drops and particles fromcrankcase gases. The market potential forthe products is believed to be very large:in the next few years, environmental legislation in both the EU and the USwill regulate levels of exhaust emissionsfrom heavy vehicles much more sharplythan is the case today.

Alfdex is a project in which Alfa Lavalcooperates, on market terms, with theSwedish listed company, Haldex.

The compact design saves space andreduces shipping and installationcosts. One market segment that hasshown great interest in AlfaCond is the fishing industry.

AlfaNova

A new technology with better

temperature and pressure tolerance

Many researchers believe that heat exchangers made from only one material are the way of the future.Here, Alfa Laval is well advanced inthis area. AlfaNova is a completelynew plate heat exchanger made froma single material: stainless steel.

The actual brazed material in combi-nation with the manufacturing tech-nique is patented. AlfaNova toleratesthe combination of high temperatureand high pressure better than otherbrazed plate heat exchangers. Thesecharacteristics broaden the market forthe product. New areas of applicationinclude processors that involve the use of ammonia.

Culturefuge 100

Separates delicate cells carefully

and effectively

Culturefuge 100 is a small, powerfulseparator for the biotechnology sector.Many new biological products are pro-duced from delicate organisms that aredifficult to separate so that the keyparts of the cells are not destroyed.Culturefuge 100 separates the delicatecells carefully and effectively. Theproduct is aimed at the most advancedsegment of the Life Science market:customers that develop monoclonalantibodies. Monoclonal antibodies arebecoming increasingly important inthe diagnosis and treatment of tumorsand the development of new vaccines.

Aldec G2

Improves performance by up to 30 percent

Aldec G2 is a new generation ofdecanters that improve performanceby up to 30 percent. It is based on anew platform that represents a techni-cal advance in sludge treatmentdecanters. Aldec G2 carries out sludgethickening and dewatering.

Aldec G2 has a gearbox that, in addi-

14 · Alfa Laval 2003Equ

ipm

ent

In 2003, order intake increased in allfive market segments of the EquipmentDivision. Comfort & Refrigeration, Fluids & Utilities and OEM were allstronger than 2002 throughout theyear, while order intake in Sanitary wasparticularly strong during the secondhalf of the year. In 2003, an interestingchange in the market occurred in theMarine & Diesel segment. Order intakewas weak in the beginning of the year,but improved at the end of the firsthalf of the year. After a sharp accelera-tion in June, the increased order intakeremained at a high level throughoutthe second half of the year. The favor-able trend was most apparent in themarine market, which was bolsteredalmost exclusively by ship-buildingactivity in Asia.

The Equipment Division is organizedin five customer segments: Sanitary,Comfort & Refrigeration, Marine &Diesel, Fluids & Utility and OEM. Theaftermarket, Parts & Service, is animportant segment, which is coveredseparately on pages 22 and 23. TheEquipment Division posted net sales ofSEK 7,842 million (8,130) in 2003, or56 (56) percent of Alfa Laval’s totalsales. The number of employees in thedivision was about 2,000 (about 2,100).

Focus on growth markets

The Equipment Division offers a widerange of products to customers thathave a well-defined, recurring and reg-ular need for Alfa Laval’s products.Sales are generated mainly through sys-tems builders, contractors and OEMcompanies as well as through distribu-tion and retail outlets – that is, to cus-tomers other than the end-customersor users of the products. The division

focuses on increasing value for cus-tomers by providing a high level ofaccessibility for products worldwidethrough increased sales and distribu-tion channels, product development in cooperation with customers and customer adaption through moduleconcept.

The Equipment Division’s strategy isto maintain and strengthen its leadingglobal positions by identifying newproduct applications in segments withfavorable growth prospects.

Sanitary

Focus on sales channels yielded

volume growth

For the Sanitary segment, 2003 repre-sented an increase in order intake com-pared with the preceding year.

The strategy developed by the divi-sion, involving a focus on external saleschannels, was successful, producing avolume increase.

During the year, the segment alsoentered into four alliances to reach itsgoal of being “the best company to dobusiness with.”

Integrating Toftejorg was a major pri-ority during the year. The tank cleaningproducts are now an integrated part ofthe segment’s offering to customers.

The bulk of sales within the Sanitarysegment is generated in the beverage,dairy, food processing, pharmaceuticaland biotechnology industries, all ofwhich have stringent hygiene and safe-ty requirements. Alfa Laval’s pumps,valves, separators, heat exchangers,installation material and tank equip-ment are used in manufacturing liquidand viscous food products, as well aspharmaceutical and hygiene products.

The Equipment Division’sshare of Group employees

57 %

22 %

The Equipment Division’sshare of Group sales

Better order intake in all customer segments

The Equipment Division

57%

22%

Alfa Laval 2003 · 15

The Equipment Division

The US is the primary market of thesegment. Tetra Pak, a leading supplierof processing and packaging systemsfor the food and beverage industry, isan important customer for the Sanitarysegment. Alfa Laval’s products are inte-gral components in the productionplants sold by Tetra Pak.

Comfort & Refrigeration

Strong trend in Russia and China is

ongoing

Order intake in Comfort & Refrigera-tion were better than in 2002, mainlybecause of the ongoing strong trend inRussia and China. Moreover, the focuson sales channels had favorable resultsin this segment as well. The launch ofthe new platform for welded plate heatexchangers, AlfaNova, was well received.

In the Comfort & Refrigeration seg-ment, Alfa Laval sells a broad assort-ment of heat exchangers used in sys-tems for district heating, district cool-ing and air conditioning of factories,offices and shopping malls, as well asfor maintaining cold and frozen fooddisplay counters and ice rinks at theproper temperatures.

The plate heat exchanger is the mainproduct for these applications. Theproduct range consists of welded plateheat exchangers, which can cope withextremely high pressure, half-weldedunits and small brazed heat exchangers

that are easy to use for a variety ofheating and cooling applications. AlfaLaval also supplies air-cooling heatexchangers for air conditioning andrefrigeration as well as shell-and-tubeheat exchangers for evaporation andcondensation.

Alfa Laval sells heat exchangers to abroad spectrum of customers rangingfrom large multinational companies tosmall, local installation firms. Some ofthe major customers are Climespace,York, Mycom and Uppsala Energi. East-ern Europe, where several countriesstill use obsolete district heating, is animportant and growing market forComfort & Refrigeration whose com-pact, efficient solutions replace the old,energy-consuming systems.

Marine & Diesel

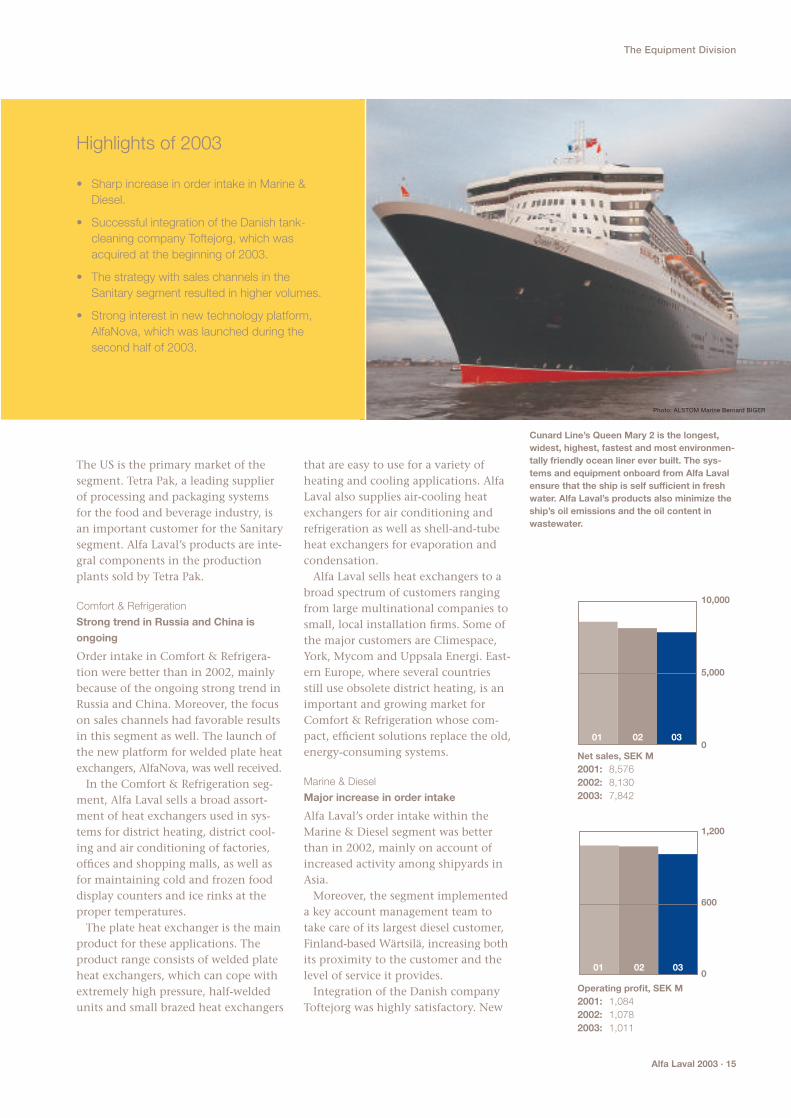

Major increase in order intake

Alfa Laval’s order intake within theMarine & Diesel segment was betterthan in 2002, mainly on account of increased activity among shipyards inAsia.

Moreover, the segment implementeda key account management team totake care of its largest diesel customer,Finland-based Wärtsilä, increasing bothits proximity to the customer and thelevel of service it provides.

Integration of the Danish companyToftejorg was highly satisfactory. New

030201

Net sales, SEK M2001: 8,5762002: 8,1302003: 7,842

030201

Operating profit, SEK M2001: 1,0842002: 1,0782003: 1,011

Cunard Line’s Queen Mary 2 is the longest,widest, highest, fastest and most environmen-tally friendly ocean liner ever built. The sys-tems and equipment onboard from Alfa Lavalensure that the ship is self sufficient in freshwater. Alfa Laval’s products also minimize theship’s oil emissions and the oil content inwastewater.

Highlights of 2003

• Sharp increase in order intake in Marine &Diesel.

• Successful integration of the Danish tank-cleaning company Toftejorg, which wasacquired at the beginning of 2003.

• The strategy with sales channels in the Sanitary segment resulted in higher volumes.

• Strong interest in new technology platform,AlfaNova, which was launched during thesecond half of 2003.

10,000

5,000

0

1,200

600

0

Photo: ALSTOM Marine Bernard BIGER

16 · Alfa Laval 2003

The Equipment Division

sales of equipment for tank cleaning in the marine market rose 30 percentover 2002.

In Marine & Diesel, Alfa Laval is a sig-nificant equipment supplier to ship-yards and diesel-engine manufacturers.Approximately two-thirds of all theships in the world that are in service areequipped with Alfa Laval products.Their applications include fuel andlubricating oil cleaning processes,engine cooling, water purification andpurification of sludge and oil-contain-ing water. The list of customers includesHyundai, MHI, Fincantieri, Wärtsiläand MAN/B&W.

Alfa Laval has steadily strengthenedits position in the marine segment bylaunching new products and solutionsthat help shipowners improve theiroperating finances and meet increasing-ly stringent environment-protectionrequirements

Fluids & Utility

Favorable trend in automotive

industry in Asia and France

Order intake was better than in 2002.The improvement was particularlyapparent in Asia and Latin America.The trend was also favorable in Centraland Eastern Europe, while North Ameri-ca remained at the same level as 2002and Western Europe and the Nordiccountries declined.

During the year, order intake increasedparticularly in the automotive industry,in both Asia and France. Moreover,AlfaPure, a series of separator modulesdeveloped primarily to purify cuttingand cleaning fluids, was developed fur-ther, making it now even simpler to use.

While currently a small segmentwithin Alfa Laval, Fluids & Utility hasenormous growth potential. Nearly allmanufacturing industries use all sorts offluids in their production, liquids thatneed to be cleaned and temperature-controlled in order to attain a highlevel of operational security. Such fluidsrange from lubricating oil for machinesto purified fluids for turning and waterfor washing the manufactured prod-ucts. With Alfa Laval’s separators, costlyoil and fluids are cleaned and recycled,helping to trim operating costs and pro-tect the environment.

The customer base comprises compa-nies in the automotive, metal, electron-ic and plastic manufacturing sectorssuch as GM, Daimler-Chrysler, IBM and Rolls Royce.

OEM (Original Equipment Manufacturers)

US breakthrough for plate heat

exchangers in air-conditioning plants

Order intake improved compared with2002, partly owing to a breakthroughin the American market for plate heatexchangers in air-conditioning systems.In 2003, Alfa Laval was awarded one ofthe largest-ever contracts in this area.

Moreover, sales of small welded heatexchangers continued to grow, increas-ing by nearly 50 percent in the pasttwo years.

Also in this segment, the launch ofthe new brazed plate exchanger,AlfaNova, was well received, establish-ing the potential for a broadening ofthe customer base.

In the OEM customer segment, AlfaLaval has close relationships with man-ufacturers of diesel engines, air-condi-tioning units, air compressors, air dryersand boilers. These customers integratethe company’s products, such as smallbrazed heat exchangers, into theirunits. Alfa Laval’s goal is to build part-nerships with these manufacturers forjoint development of new products.Some of the customers include Vaillant,Caterpillar and Carrier.

After developing a product in accor-dance with the customer’s specifica-tions, Alfa Laval often signs a supplycontract for large volumes covering sev-eral years. The Group delivers its prod-ucts to customers direct from the pro-duction plants. This shortens lead times,cuts costs, and limits risks for errors aswell as saves marketing resources in theorganization.

Geographic distribution of the Equipment Division sales, %1 Sweden2 Rest of EU3 Rest of Europe4 US5 Rest of North America6 Latin America7 Asia8 Other

1

2

3

45

6

12

6

4

56

7

8

3

Segment distribution of the Equipment Division sales, %1 Marine & Diesel2 Sanitary3 Comfort & Refrigeration 4 Fluids & Utility5 OEM6 Parts & Service

Alfa Laval 2003 · 17

The Equipment Division

“Based on our experience, we thinkthat Alfa Laval’s intelligent valves arecentral to successful production inan operation like ours.”

Jan Koopman, Sara Lee/DE

Sara Lee/DE, with headquarters in the Netherlands, is a subsidiary of Chica-

go based Sara Lee Corporation. Sara Lee/DE is the largest operator world-

wide in the out-of-home coffee market.

When a significant growth in this market was evident, Sara Lee/DE

developed a unique high-speed coffee system for professional use, based

on concentrated liquid coffee. In 1998 the company enlarged an existing

plant for such coffee in Joure in the Netherlands. Another plant is now

under construction in Suffolk, Virginia in the United States. Due to their

excellent performance during a test in the Joure plant, Alfa Laval’s Unique

mix-proof valves and ThinkTop intelligent valve control units will also be

installed at the heart of the new US plant.

Jan Koopman, manager Technical Engineering of Manufacturing Tech-

nology at Sara Lee/DE in Joure was impressed by the high-IQ valve control

technology already when it was demonstrated to him the first time. “Alfa

Laval’s solution satisfies our needs best. Getting back reliable information

data and early warnings for preventive maintenance is vital in a production

facility that has to operate 24 hours a day, seven days a week,” he says.

Pro

cess

Tech

nolo

gy

The Process Technology Division

In 2003, order intake in the ProcessTechnology Division was somewhatbetter than in 2002, excluding currencyeffects, due to a favorable trend in thefourth quarter. Food Technology postedsteady growth while Energy & Environ-ment first reversed the negative trend of2002 a way along into the year. ForProcess Industry, 2003 developed weak-ly, but petrochemical investmentsgained pace toward the end of the year.In Life Science, order intake was some-what weaker, but as a result of theacquisition of the American company,bioKinetics, in the fourth quarter, thesegment reported a plus.

The Process Technology Divisionoperates within four customer-orientedsegments: Process Industry, Food Tech-nology, Energy & Environment and Life Science. The aftermarket, Parts &Service, is an important segment whichis presented separately on pages 22 and23. In 2003, the division posted sales ofSEK 5,994 million (6,377), or 43 (44)percent of the total sales of the AlfaLaval Group. The number of employeesin the division was approximately 2,980(approximately 2,700).

Customized solutions enhance efficiency

in customers’ processes

The Process Technology Division servescustomers who require solutions that, toa greater or lesser extent, have been spe-cially adapted to improve the efficiencyof their processes. The division’s salesare mostly effected through the Group’sown sales companies. Alfa Laval com-bines expertise in its key technologieswith thorough knowledge of its cus-tomers’ processes and offers packagesolutions ranging from single productsto systems and turnkey solutions, aswell as efficient customer service.

Food Technology

Major projects within vegetable oils

contributed to a stronger performance

Order intake within Food Technologyimproved compared with 2002, primar-ily due to favorable developments inChina, India and the Ukraine.

During 2003, developments withinvegetable oil processes were favorableand the segment received several majorproject orders.

Developments have also been favor-able with regard to decanters forprocesses within the beverage industry.

Alfa Laval has a strong position as asupplier of process solutions to thebeverage and food industries.

The solutions are used in the produc-tion of beer, wine, vegetable oils andmeat and fish proteins. Since Alfa Lavallaid the foundations for its strong posi-tion within the dairy industry 120 yearsago, the company has accumulated anextensive knowledge of processes forseparating, heating, cooling, pumpingand controlling various foodstuffs.

Alfa Laval’s growth in the breweryarea exceeds market growth. The com-pany has developed close relations withits customers, including many of theworld’s largest brewery groups. Specialmodules have been developed in coop-eration with the brewing industry forprocesses such as pasteurization, mix-ing, wort boiling and deaeration. Thebrewing industry performed slightlyweaker in 2003 than the precedingyear, although 2002 was an exception-ally strong year, particularly in EasternEurope.

Customers served by Food Technolo-gy include such multinational groupsas Cargill, ADM, Heineken andAnheuser-Busch.

The Process Technology Division’sshare of Group employees

43 %

32 %

The Process Technology Division’sshare of Group sales

bioKinetics creates possibilities to develop the Life Science segment

43%

32%

Alfa Laval 2003 · 19

The Process Technology Division

Highlights of 2003

• Acquisition of American bioKinetics infourth quarter of 2003.

• Several major projects in vegetable oilscontributed to the favorable trend inFood Technology.

• Recovered market share in the environ-mental area.

• Strong growth in membrane technology.

Process Industry

Weak in 2003, but strong growth in the

chemical sector in Asia and Eastern

Europe

Order intake in the Process Industrywas weaker than in 2002, which ismainly attributable to a continuingoverall low level of investment in West-ern Europe and the US as well as glob-ally, in the starch area.

Otherwise, the chemical sector inAsia and Eastern Europe reported a bet-ter order intake, and the petrochemicalsector recovered.

The results of the focus on so-called2-phase applications have begun toyield results, with compact heatexchangers replacing existing techno-logy for condensation, reboiling andevaporation.

The launching of AlfaCond, the firstpurpose-built plate condenser (readmore on page 12) attracted great interestin the market.

Within the Process Industry, AlfaLaval’s solutions are used by a largenumber of customers for producingpetrochemical products, plastics, poly-mers, metals, minerals, ethanol, starch,paper and sugar, among other products.

Heat exchangers play a key role forcost-efficient production in processesthat demand large amounts of energy.Compact heat exchangers have enor-mous potential, as they can often

replace conventional shell-and-tubeheat exchangers, enhancing efficiencyand producing major savings in bothspace and installation and service costs.

Alfa Laval has many well-known customers in the process industry, suchas BASF, Bayer, DuPont, Cargill, Proctor& Gamble and International Paper.

Energy & Environment

Downward trend halted, due mainly to

strong order intake in environmental

sector

Order intake in 2003 started out weak.However, the downward trend washalted and weak growth was reportedfor the full year, mainly as a result ofthe favorable trend in the environmen-tal area and to a certain extent in theenergy area. However, the decline ininvestments in the cyclical oil and gasmarket continued.

In the environmental area, thelaunching of the new decanter, AldecG2, was a key event. Alfa Laval reportedan increase in order bookings, despitethe market’s weak growth, mainly as a result of recovered market share. During the year, Alfa Laval had a strongposition in the UK, and strengthenedits market positions in China.

In the power industry, the NorthAmerican market continued to bestrained. However, Alfa Laval was ableto offset this to a large extent through

Net sales, SEK M2001: 6,872 2002: 6,3772003: 5,994

Operating profit, SEK M2001: 4732002: 5212003: 352

030201

030201

10,000

5,000

0

1,200

600

0

During 2003 the North American com-pany bioKinetics was acquired. Theirmain products are modular designsthat mainly focus on mammalian cellcultures. The picture shows a bufferhold system at Hemosol, a Toronto-based company developing artificialblood products.

20 · Alfa Laval 2003

The Process Technology Division

Sewage treatment is becoming more self-regulating and automated. Octopus

from Alfa Laval is the first self-optimizing system in the sludge dewatering

business. It can be described as a decanter autopilot that optimizes the

decanter’s operation around the clock.

The wastewater treatment plant in Almere in the Netherlands treats 30,000

cubic metres of sewage every day. The plant produces secondary sludge that

is dewatered in decanter centrifuges. The sludge that Almere delivers to the

incineration company has a dry solids content of between 18 and 22 percent.

By contrast, before entering the decanter, the sludge has a concentration of

2.5 percent dry solids.

“With Octopus, we can set minimum and maximum levels for all relevant

process parameters and optimize our costs,” says Ben Roelfzema environmental

manager at the Dutch Water Board Zuiderzeeland that owns and operates the

plant in Almere. “And the Octopus system adjusts these by itself.”

With the help of Octopus, the Almere plant has made substantial savings

through more efficient sludge dewatering and through decreased use of polymer

and fresh water. Another significant benefit is constant, good quality of the

centrate (separated water in the dewatering process).

“The only way to save money in the wastewater treatment business is by automating the whole process.”

Ben Roelfzema,

Dutch Water Board, Zuiderzeeland

Alfa Laval 2003 · 21

The Process Technology Division

major projects in Asia, Russia and theMiddle East.

Market conditions in the Oil & Gasmarket continued to be tight, resultingin fewer projects, despite the high priceof oil. Investments in land-based drill-ing gave encouraging signals.

Alfa Laval’s products, modules andsystems are of great importance in theenergy sector, both in the extraction ofenergy sources such as oil and gas andin the production of energy in powerplants. The company also has a strongposition in the environmental area as asupplier of equipment for sludge pro-cessing at wastewater treatment plants.

For the Oil & Gas industry, Alfa Lavalsupplies solutions for drilling and pro-duction of crude oil and gas, fresh-water production and treatment of oil-contaminated water. Power plantapplications involve the use of separa-tors for effective cleaning of lubricat-ing oils and fuel oils, including heavyoil and crude oil, compact heatexchangers for heating and coolingpurposes, and systems capable ofdesalinating large volumes of seawater.

As a result of more stringent environ-mental legislation, the need for effi-cient handling of wastewater andsludge is increasing. The company supplies systems that reduce the vol-ume of wastewater, so that it can betreated more efficiently. The customersinclude municipalities, private watercompanies, major international con-tractors and the paper, food, chemicalsand other industries.

The customers within the Energy &Environment segment include Shell,Petrobras, Statoil, General Electric,China Nuclear Corp., Thames Waterand the City of Chicago.

Life Science

Acquisition of US-based bioKinetics

creates development possibilities

Order intake in Life Science increasedin 2003, as a result of the acquisitionof the American company, bioKinetics.bioKinetics targets the biotechnologyand pharmaceutical industries, and itsmain products are process modules,focusing on mammalian cell cultures.bioKinetics currently operates in NorthAmerica. Combining the resources ofbioKinetics with Alfa Laval’s marketpresence will give Alfa Laval greateraccess to the European and Asian mar-kets. In 2002, bioKinetics posted salesof SEK 550 million and had approxi-mately 400 employees. Its customersinclude leading pharmaceutical andbiotechnology companies such asAmgen and IDEX.

Alfa Laval also ranks among pioneersin the development of advanced sepa-rators for the increasing production ofpharmaceuticals based on mammaliancells. Having acquired the Danish com-pany, DDS, in 2002, Alfa Laval cannow combine membrane filtration andcentrifugal separation. The productsare mutually complementary, andmembrane filtration technique hasalready been further developed and itsareas of application increased.

Life Science, which is a growing areaof operations within Alfa Laval, servesthe pharmaceutical, biotechnology,fermentation and health foods indus-tries. The company has developed anumber of products and solutions thatmeet the stringent safety and hygienerequirements applied by the superviso-ry authorities and the industries. Prod-ucts aimed at this market include cen-trifugal separators for advanced cellseparation, heat exchangers for con-densation and sterilization, and pumpsand valves for precise transport andflow control.

Life Science’s customer list includesmany of the major pharmaceuticalsgroups, such as Eli Lilly, GlaxoSmith-Kline and Genentech.

12

3

4

5

Segment distribution of sales in the ProcessTechnology Division1 Life Science2 Process Industry3 Energy & Environment4 Food Technology5 Parts & Service

Geographic distributionof sales in the ProcessTechnology Division1 Sweden2 Rest of EU3 Rest of Europe4 US5 Rest of North America6 Latin America7 Asia8 Other

1 26

45

6

7

8

3

22 · Alfa Laval 2003

Food Processing and HVAC postedstrong growth. The large installedbase of plate heat exchangers, separa-tors, pumps and valves demandsactive support in terms of spare partsand service from sales channels, in allindustrial applications.

New organization, new culture

Alfa Laval’s organization, based oncustomer-oriented divisions, has alsoaffected Parts & Service. The compa-ny’s sales outlets now have a jointorganization for this business, encom-passing Alfa Laval’s entire productoffering. This, combined with raisingthe competence and status of servicemanagers and staff, has resulted in anew culture and new perspective onservice. The new motto is to becomea genuine partner to customers, tap-ping the company’s skills and know-how to help them maintain and trimprocesses so they become as efficientand safe as possible – all these withthe view of improving profitability.

A large installed base of products

with long life spans

The large and expanding installedbase of products forms the solid plat-form for Parts & Service. Further-more, the products have long life-times, with heat exchangers having a typical lifetime of 5 to 20 years andseparators having a typical life span of10 to 20 years. Alfa Laval has a globalnetwork of about 70 service centersthat makes spare parts and servicesavailable to customers everywhere.

In 2003, Alfa Laval’s aftermarket con-tinued to grow, accounting for 26 per-cent of the Group’s total sales in theyear. Over the past few years, anincreasing proportion of Alfa Laval’srevenue has come from Parts & Service.In 1999, these operations comprised 22percent of Group sales.

Establishment of many new

service agreements

In 2003, Alfa Laval continued to devel-op the Parts & Service business in themore mature markets particularly inEurope and the US, to generate moreperformance agreements, therebystrengthening its long-term relation-ships with both large and small cus-tomers. During the year, Alfa Lavalsigned several new performance agree-ments, mostly with customers with anestablished fleet of separators. The per-formance agreements represent a majorbusiness potential for Alfa Laval.

During the year, the trend of sales wasfavorable in both Central and EasternEurope and Asia. This trend will have a favorable effect on the aftermarket. A large part of the growth is related togrowth in Alfa Laval’s installed machinefleet, but it is also due to the fact thatthe organization is continually develop-ing, is increasingly effective in its busi-ness development activities, and hasbroadened its offering to customers.

Strong trend in the marine area, in both

spare parts and service

Alfa Laval’s strong growth in the globalmarine market continued, both in spareparts and service. This applies particu-larly to original parts distributed fromAlfa Laval’s global network and supportfrom technical service centers.

Parts & Service

Continued growth

20

25

30

03020100

Parts & Service share of Group’s total sales, %

Percentage of Group’s employeesemployed in Parts & Service

26 %

17 %

Percentage of Group sales generatedthrough Parts & Service

Par

ts&

Ser

vice

2000: 232001: 25

2002: 272003: 26

26%

17%

Alfa Laval 2003 · 23

Parts & Service

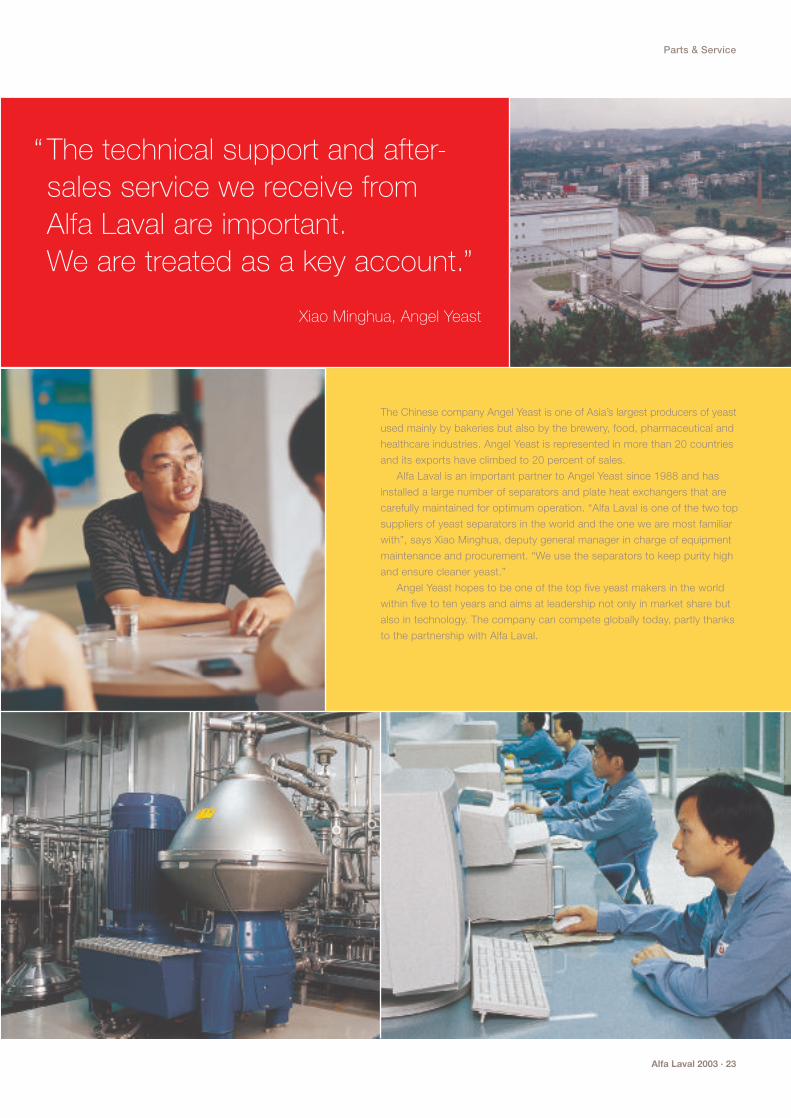

The Chinese company Angel Yeast is one of Asia’s largest producers of yeast

used mainly by bakeries but also by the brewery, food, pharmaceutical and

healthcare industries. Angel Yeast is represented in more than 20 countries

and its exports have climbed to 20 percent of sales.

Alfa Laval is an important partner to Angel Yeast since 1988 and has

installed a large number of separators and plate heat exchangers that are

carefully maintained for optimum operation. “Alfa Laval is one of the two top

suppliers of yeast separators in the world and the one we are most familiar

with”, says Xiao Minghua, deputy general manager in charge of equipment

maintenance and procurement. “We use the separators to keep purity high

and ensure cleaner yeast.”

Angel Yeast hopes to be one of the top five yeast makers in the world

within five to ten years and aims at leadership not only in market share but

also in technology. The company can compete globally today, partly thanks

to the partnership with Alfa Laval.

“ The technical support and after-sales service we receive from Alfa Laval are important. We are treated as a key account.”

Xiao Minghua, Angel Yeast

The Operations Division’sshare of Group employees

42 %

Ope

ratio

nsThe Operations Division

Further improvement in

delivery reliabilityManufacturing

Preparing for growth

Alfa Laval has 3,900 production employ-ees and 20* large manufacturing units,of which 12 are in Europe, six in Asiaand two in the US. During the past sev-eral years, global production has concen-trated on fewer, product-specialized fac-tories that are localized according to twocriteria: proximity to the market andcost benefits. High-value productsrequiring advanced technical know-howare manufactured in production centerslocated mainly in Western Europe, theUS and Japan.

In 2003, several production units wereengaged in preparing their capacity tocope with a higher order intake. It wasdecided to build an extension onto thefacility in Lund, which would costapproximately SEK 100 million, to boost

The Operations Division is a centralizedfunction that performs all manufacturing,purchasing and logistics functions with-in Alfa Laval. In centralizing these func-tions, the company aims to optimizedelivery reliability for customers,increase productivity, reduce operatingcosts and exploit economies of scale.

Alfa Laval believes it is necessary tohave a global perspective and coordi-nate purchasing, manufacturing andlogistics in order to create a reliableaccess to the company’s products in theworld market.

Focus on SixSigma

In 2003, the division launched a newfocus on SixSigma at its production units in Lund and Ronneby in Sweden.Toward the end of the year, the companybegan to introduce SixSigma at its unitsin Kolding, Denmark, and Alonte, Italy.

During the year, the production unitin Lund used SixSigma in its improve-ment activities – with favorable results.The target for 2003 was to save SEK 6million with the help of SixSigma. Atotal of SEK 6.4 million in cost savingswas the outcome.

To follow up process stability – a cen-tral concept of SixSigma – the unitintroduced a measurement databasethat measures the number of errors permillion runs. Once a month, the unitcarries out measurements of 55 parame-ters – for example, discards from a pressline, bottlenecks in key machines, latedeliveries and delays from suppliers.

Considerable effort has been devotedto identifying the right parameters andways of measuring them.