annual financial report 2019 - mcc

TRANSCRIPT

1

Annual Financial Report 2019

2

Contents

Introduction 4

Composition of the Corporate Bodies 5

Report on Operations

2019 in brief

Economic data and performance indicators 8

Equity data and performance indicators 9

The macroeconomic scenario and the lending system 10

Results for the year 11

Economic results 11

Financial aggregates 16

The business 24

Operating structure 30

Corporate Governance 32

Non-financial disclosure 43

Other information 58

Significant subsequent events 58

Business outlook 59

Proposed allocation of net income for the period 60

Accounting statements

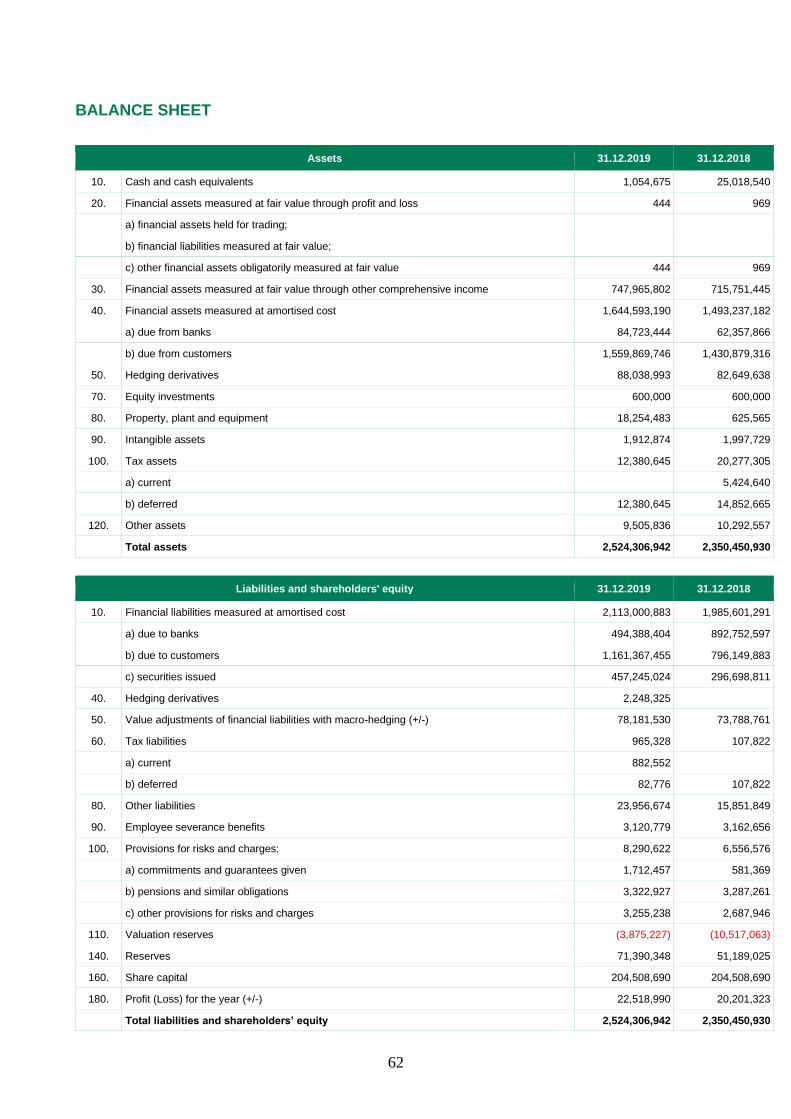

Balance Sheet 62

Income Statement 63

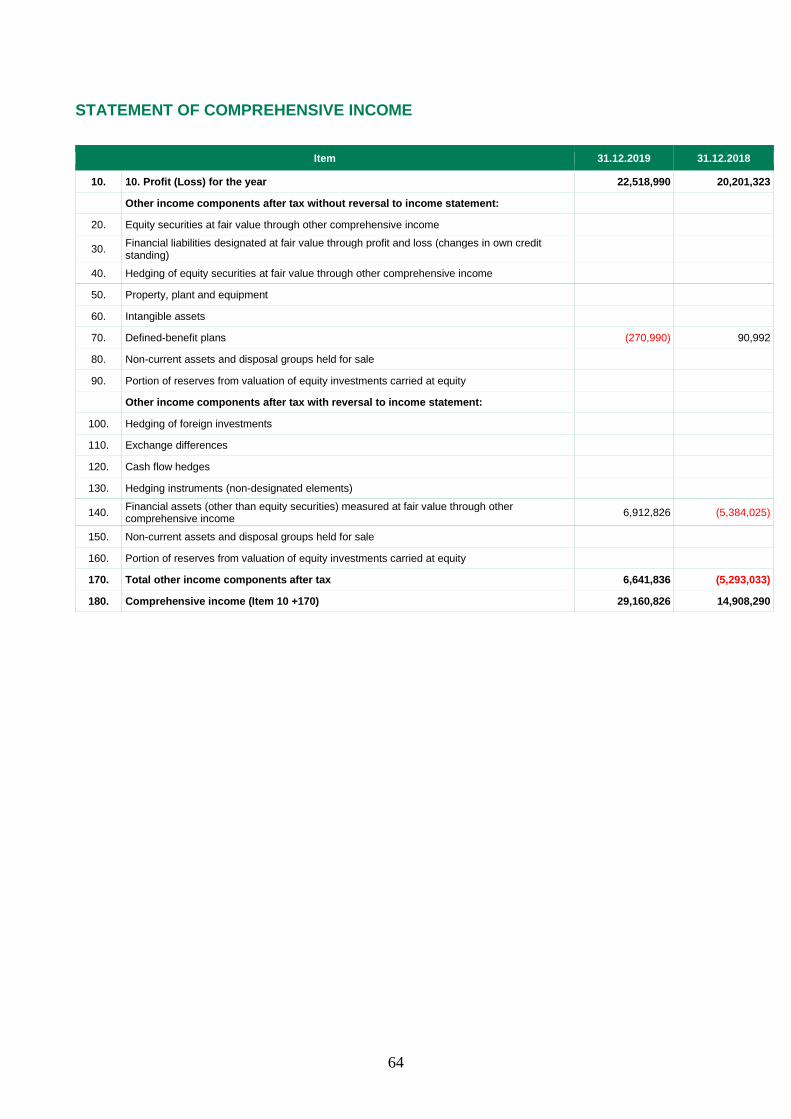

Statement of comprehensive income 64

Statement of changes in shareholders' equity 65

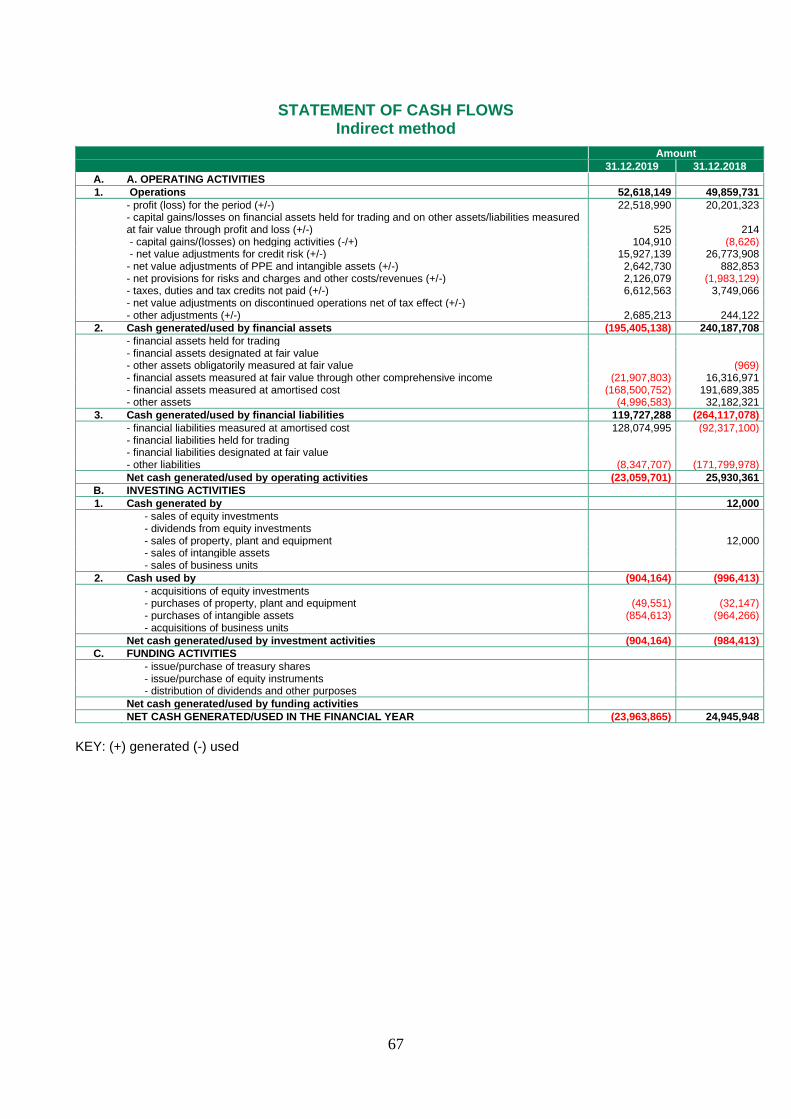

Statement of Cash Flows 67

Notes to the Financial Statements

Part A – Accounting policies 70

Part B – Information on the balance sheet 114

Part C – Information on the income statement 154

3

Part D – Comprehensive Income 175

Part E – Information on risks and relative hedging policies 178

Part F – Information on capital 231

Part H – Transactions with related parties 236

Part L – Segment reporting 243

Part M – Leasing information 245

Country-by-country reporting (Art. 89 Directive 2013/36/EU) 247

Attestation of the separate financial statements

under the terms of Article 81-ter of CONSOB Regulation

11971 of 14 May 1999, as amended 249

4

Introduction

The Financial Statements of Mediocredito Centrale, in application of Italian Legislative

Decree 38 of 28 February 2005 and of Italian Legislative Decree 136 of 18 August 2015,

have been drawn up according to the IAS/IFRS accounting standards issued by the

International Accounting Standards Board (IASB) and the related interpretation documents

of the International Financial Reporting Interpretations Committee (IFRIC), endorsed by

the European Commission, as established by Community Regulation no. 1606 of 19 July

2002.

The financial statements at 31 December 2019 have been prepared on the basis of the

“Instructions for Drafting the Financial Statements of Banks” issued by the Bank of Italy

with its provision of 22 December 2005, with which Circular no. 262/05 was issued, and

subsequent updates.

These instructions establish the format of the Financial Statements and the related

preparation methods, as well as the content of the Notes to the Financial Statements.

The Separate Financial Statements are made up of the Balance Sheet, the Income

Statement, the Statement of Comprehensive Income, the Statement of Changes in

Shareholders’ Equity, the Statement of Cash Flows and the Notes to the Financial

Statements, and they are also accompanied by a Report on Operations outlining, on the

economic results achieved and on the Bank’s equity and financial situation.

In support of the comments on the results for the period, the Report on Operations

presents and illustrates the reclassified income statement and balance sheet.

On the Bank’s website (at: www.mcc.it) the financial reports and the press releases

published in the period are available, together with other financial documentation.

5

Composition of the Corporate Bodies

Board of Directors

Chairperson Massimiliano Cesare

Chief Executive Officer Bernardo Mattarella

Director Pasquale Ambrogio

Director Leonarda Sansone

Director Gabriella Forte

Board of Statutory Auditors

Chairperson Paolo Palombelli

Regular Auditor Carlo Ferocino

Regular Auditor Marcella Galvani

Alternate Auditor Roberto Micolitti

Alternate Auditor Sofia Paternostro

* * *

Auditing Firm PricewaterhouseCoopers S.p.A.

Financial Reporting Manager Elena De Gennaro

6

Report on Operations

7

2019 in brief

8

Economic data and performance indicators

31.1

25.0

56.154.7

Titolo asse

48.847.4

22.031.2

44.136.4

12.211.3

Net interest income

Net fees and commissions

Net banking and insurance income

Operating profit/(loss)

Net operating profit/(loss)

-6.9 -21

Reclassified income statement (millions of euro)Changes

Amount %

-1.4 -3

0.2 0

-1.4 -3

9.2 41

-7.7 -18

0.9 -7

88.388.5

24.129.1

20.2

22.5

Gross profit from continuing operations

Net income for the period

5.0 21

2.3 -11

of which: interest income

of which: interest expense

63.5

61.8

36.128.3

8.38.4

Cost/Income (net of expense recoveries)

Net gains(losses)/Average shareholders' equity (ROE)

Net interest income/Net banking and insurance income

Net fees and commissions/Net banking and insurance income

Profitability indicators (%)

1.00.9

Net income/Total assets

44.7

46.4

31.12.2019

31.12.2018

9

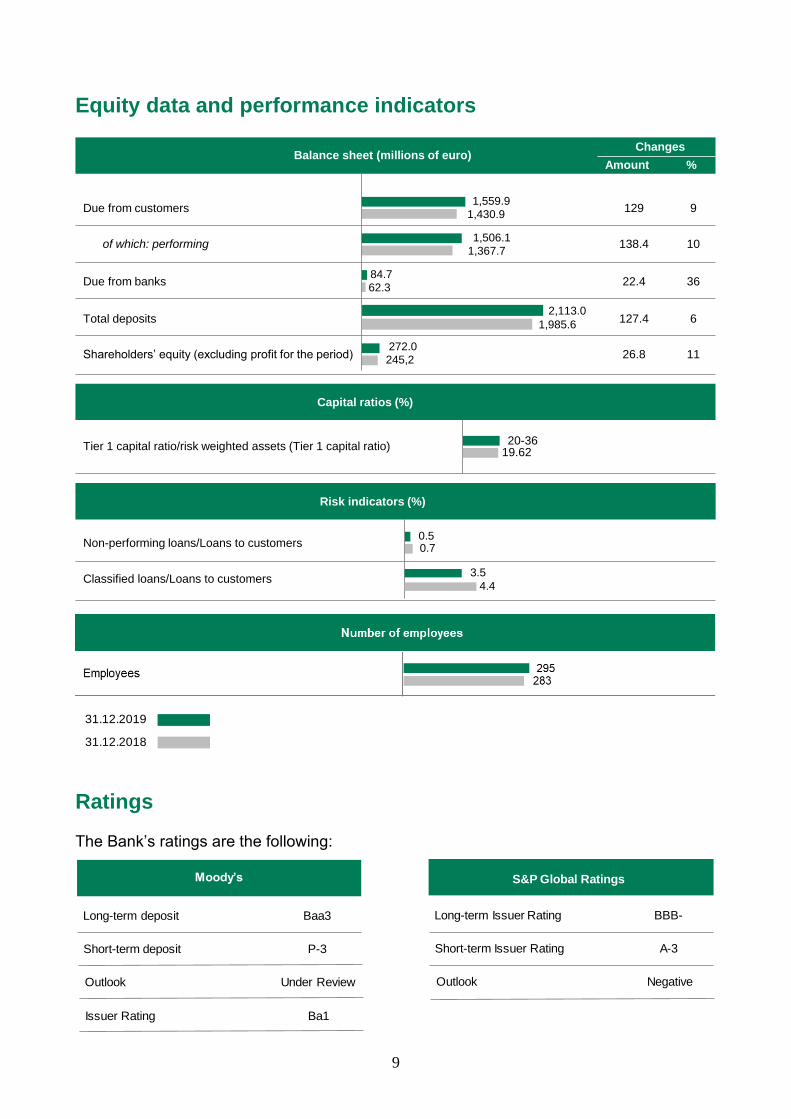

Equity data and performance indicators

Balance sheet (millions of euro)

1,430.9

1,559.9

62.384.7

1,367.71,506.1

245,2272.0

Due from customers

of which: performing

Due from banks

Total deposits

Shareholders’ equity (excluding profit for the period)

129 9

138.4 10

22.4 36

127.4 6

26.8 11

1,985.6

2,113.0

Changes

Amount %

Tier 1 capital ratio/risk weighted assets (Tier 1 capital ratio)

Capital ratios (%)

19.6220-36

0.70.5

Non-performing loans/Loans to customers

Classified loans/Loans to customers

Risk indicators (%)

4.4

3.5

31.12.2019

31.12.2018

Ratings

The Bank’s ratings are the following:

Moody’s

Long-term deposit Baa3

Short-term deposit P-3

Outlook Under Review

Issuer Rating Ba1

S&P Global Ratings

Long-term Issuer Rating BBB-

Short-term Issuer Rating A-3

Outlook Negative

10

The macroeconomic scenario and the lending system

Uncertainties continue in Italy also due to the slowing seen both in Europe and generally.

Signals coming from indicators are contradictory.

In fact, on one hand the conditions on the financial and lending markets have improved

and investor confidence has improved, as can be seen by the significant purchases of

public securities by non-residents and the considerable drop in the relative returns and

interest differentials with regards to the Bund.

Nonetheless, preliminary ISTAT estimates indicate a 0.3% decrease in GDP with respect

to the 4th quarter of 2018, also due to unfavourable changes in the most erratic

components of final demand, held up by a positive change in household spending and in

inventories, mitigating the foreign component which saw a decisive drop.

Bank of Italy projections published in January’s economic bulletin suggest limited growth

after the lack of change seen in 2019, but much higher in the coming two years.

Much will depend on international trade disputes, geopolitical tensions, future economic

relationships between the European Union and the United Kingdom as well as possible

impacts on the Chinese economy deriving from the spread of the coronavirus, given its

status as one of the main motors driving global growth.

In terms of financial markets, the return differential between Italian 10-year government

securities and the corresponding German bonds is still nearly two times that seen in Spain

and Portugal, at 140 basis points.

The reduction in the rate applied to bank deposits in the Eurosystem was transferred to

short-term market returns and a recovery of net purchases of financial assets put

downward pressure on long-term returns.

In the banking sector, credit quality continues to improve while the inflow of new impaired

loans remains constant.

Profitability has increased with respect to the same period the previous year, and as noted

in a recent interview with the Governor of the Bank of Italy, net of extraordinary

components, ROE rose on average from 5.8% to 6.6% during the first nine months of

2019.

11

In a situation of modest revenue growth, with net interest income continuing to make a

small contribution, with fee components contributing more, in order to maintain expected

profitability, which Prometeia estimates suggest will not be likely to exceed 5% in 2022,

reductions in operating expenses and in the cost of risk will be the determining factors in

maintaining expected profitability, thanks to controlling credit quality and a lower need for

extraordinary writedowns on impaired items.

Results for the year

Economic results

Net profit in 2019, totalling 22.5 million, +11% with respect to 2018 and well in line with the

budget approved by the Board of Directors on 14 February 2019, outlines the Bank’s

trends through:

a) net banking and insurance income substantially in line with the previous year,

totalling 88.5 million (88.3 million at 31.12.2018), showing a decrease in net interest

income despite development of lending, given the continuing spread levels applied

to customers with ever lower margins for segments with greater creditworthiness, a

decrease in commissions generated by the Guarantee Fund due to operational

slowdowns after the Reform took effect on 15 March, mitigated by the greater

contribution made by profits deriving from management of the securities portfolio

(8.8 at 31.12.2019 compared to 0.3 at 31.12.2018), thanks to the temporary

reduction in the third quarter of 2019 of the differential between Italian and German

ten-year securities;

b) the normalisation of credit risk adjustments, mainly attributable to the impaired

portfolio, compared to the “extraordinary” figure recorded in 2018. On a net basis,

the impact of the impaired portfolio fell again from 4.7% to 3.7%, while the coverage

rate rose to 60%, compared to 53.3% at the end of 2018. These adjustments

include the valuation done relative to the € 12 million subscription on 20.12.2019 of

a subordinate bond loan (Banca Carige 2019-2029, fixed rate Tier II, with a total

nominal value of 200 million), issued as part of a complex transaction to strengthen

the capital for the Ligurian bank, which saw the departure of the government

appointed commissioner on 31 January 2020;

12

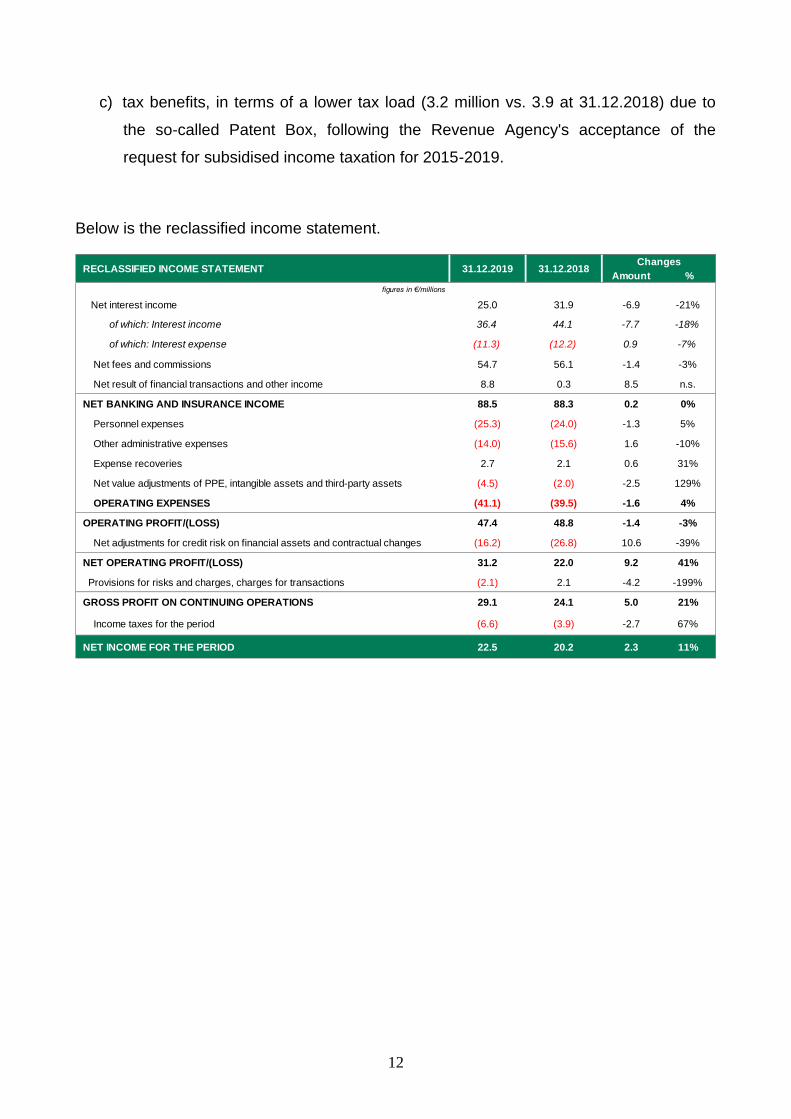

c) tax benefits, in terms of a lower tax load (3.2 million vs. 3.9 at 31.12.2018) due to

the so-called Patent Box, following the Revenue Agency's acceptance of the

request for subsidised income taxation for 2015-2019.

Below is the reclassified income statement.

Amount %

figures in €/millions

Net interest income 25.0 31.9 -6.9 -21%

of which: Interest income 36.4 44.1 -7.7 -18%

of which: Interest expense (11.3) (12.2) 0.9 -7%

Net fees and commissions 54.7 56.1 -1.4 -3%

Net result of financial transactions and other income 8.8 0.3 8.5 n.s.

NET BANKING AND INSURANCE INCOME 88.5 88.3 0.2 0%

Personnel expenses (25.3) (24.0) -1.3 5%

Other administrative expenses (14.0) (15.6) 1.6 -10%

Expense recoveries 2.7 2.1 0.6 31%

Net value adjustments of PPE, intangible assets and third-party assets (4.5) (2.0) -2.5 129%

OPERATING EXPENSES (41.1) (39.5) -1.6 4%

OPERATING PROFIT/(LOSS) 47.4 48.8 -1.4 -3%

Net adjustments for credit risk on financial assets and contractual changes (16.2) (26.8) 10.6 -39%

NET OPERATING PROFIT/(LOSS) 31.2 22.0 9.2 41%

Provisions for risks and charges, charges for transactions (2.1) 2.1 -4.2 -199%

GROSS PROFIT ON CONTINUING OPERATIONS 29.1 24.1 5.0 21%

Income taxes for the period (6.6) (3.9) -2.7 67%

NET INCOME FOR THE PERIOD 22.5 20.2 2.3 11%

RECLASSIFIED INCOME STATEMENT 31.12.2019 31.12.2018Changes

13

Net banking and insurance income

Amount %

figures in €/millions

Net interest income 25.0 31.9 -6.9 -21%

of which: Interest income 36.4 44.1 -7.7 -18%

of which: Interest expense (11.3) (12.2) 0.9 -7%

Net fees and commissions 54.7 56.1 -1.4 -3%

Net result of financial transactions and other income 8.8 0.3 8.5 n.s.

Total 88.5 88.3 0.2 0%

NET BANKING AND INSURANCE INCOME 31/12/2019 31/12/2018Changes

Net banking and insurance income shows:

• a lower contribution from net interest income (-21%), due to the continuation of the

smaller spread applied to customers, not yet compensated for by new disbursements;

• a decrease in net fees and commissions (-2.6% with respect to 2018) due to the

slowdown in operations by the National Guarantee Fund in the months immediately

before the reform decree took effect on 15 March 2019, which among other things

introduced a business creditworthiness evaluation model, with the possibility of defining

probability of default for the final beneficiary, restructuring guarantee measures

inversely to borrower riskiness, and the introduction of specific rules for transactions

against investments. During 2019, the National Guarantee Fund saw a slight decrease

of -3.4% in terms of requests granted, guaranteeing a volume of loans totalling 19.4

billion (+0.9% over 2018), of which 5,346.9 million to companies in southern Italy (-

1.4% with respect to 2018);

• profits from disposal of financial assets totalling 9 million (0.3 million at 31.12.2018) due

to the release and subsequent reinvestment of the bank’s portfolio of securities,

benefiting from the decrease in the spread between the BTP and Bund seen in the third

quarter of the year.

14

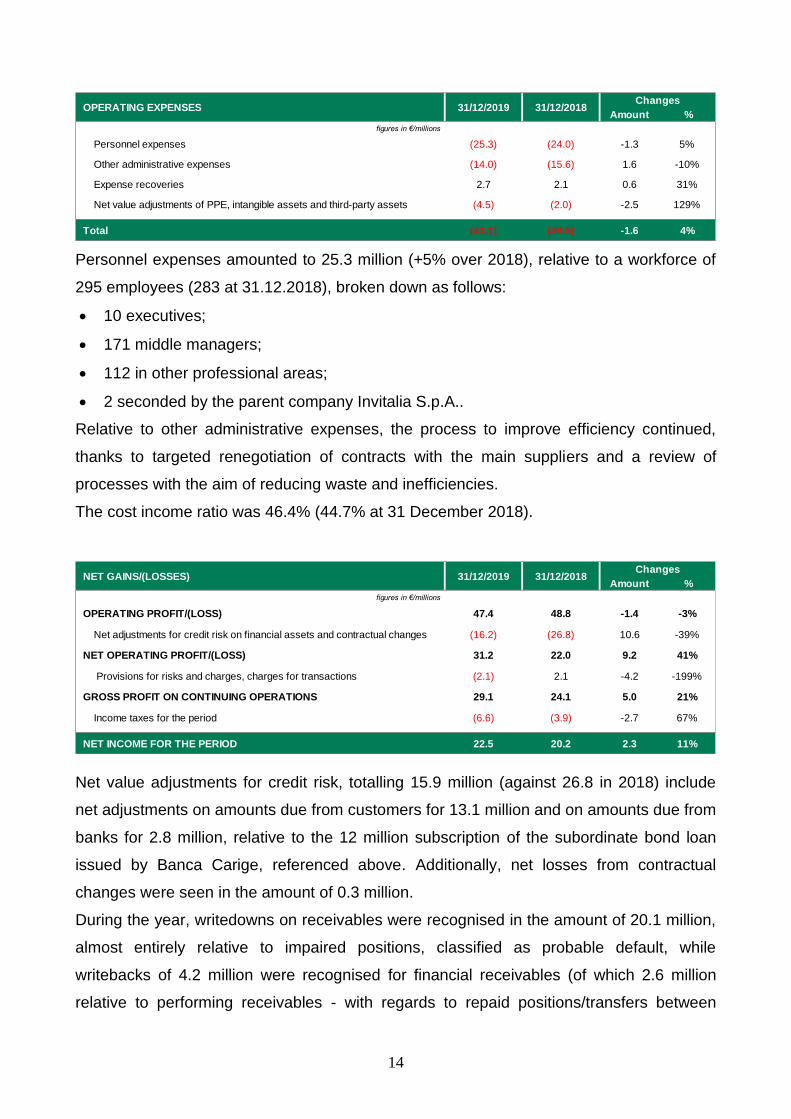

Amount %

figures in €/millions

Personnel expenses (25.3) (24.0) -1.3 5%

Other administrative expenses (14.0) (15.6) 1.6 -10%

Expense recoveries 2.7 2.1 0.6 31%

Net value adjustments of PPE, intangible assets and third-party assets (4.5) (2.0) -2.5 129%

Total (41.1) (39.5) -1.6 4%

OPERATING EXPENSES 31/12/2019 31/12/2018Changes

Personnel expenses amounted to 25.3 million (+5% over 2018), relative to a workforce of

295 employees (283 at 31.12.2018), broken down as follows:

• 10 executives;

• 171 middle managers;

• 112 in other professional areas;

• 2 seconded by the parent company Invitalia S.p.A..

Relative to other administrative expenses, the process to improve efficiency continued,

thanks to targeted renegotiation of contracts with the main suppliers and a review of

processes with the aim of reducing waste and inefficiencies.

The cost income ratio was 46.4% (44.7% at 31 December 2018).

Amount %

figures in €/millions

OPERATING PROFIT/(LOSS) 47.4 48.8 -1.4 -3%

Net adjustments for credit risk on financial assets and contractual changes (16.2) (26.8) 10.6 -39%

NET OPERATING PROFIT/(LOSS) 31.2 22.0 9.2 41%

Provisions for risks and charges, charges for transactions (2.1) 2.1 -4.2 -199%

GROSS PROFIT ON CONTINUING OPERATIONS 29.1 24.1 5.0 21%

Income taxes for the period (6.6) (3.9) -2.7 67%

NET INCOME FOR THE PERIOD 22.5 20.2 2.3 11%

NET GAINS/(LOSSES) 31/12/2019 31/12/2018Changes

Net value adjustments for credit risk, totalling 15.9 million (against 26.8 in 2018) include

net adjustments on amounts due from customers for 13.1 million and on amounts due from

banks for 2.8 million, relative to the 12 million subscription of the subordinate bond loan

issued by Banca Carige, referenced above. Additionally, net losses from contractual

changes were seen in the amount of 0.3 million.

During the year, writedowns on receivables were recognised in the amount of 20.1 million,

almost entirely relative to impaired positions, classified as probable default, while

writebacks of 4.2 million were recognised for financial receivables (of which 2.6 million

relative to performing receivables - with regards to repaid positions/transfers between

15

stages, and 1.6 million of writebacks relative to impaired receivables - of which 0.3 due to

amounts collected).

Net provisions for risks and charges of 2.1 million include:

a) net writedowns of 1.1 million relative to valuation of commitments to disburse loans;

b) provisioning of around 1 million relative to the provision for redundancies, following

the resolution made by the Board of Directors on 20 February 2020.

16

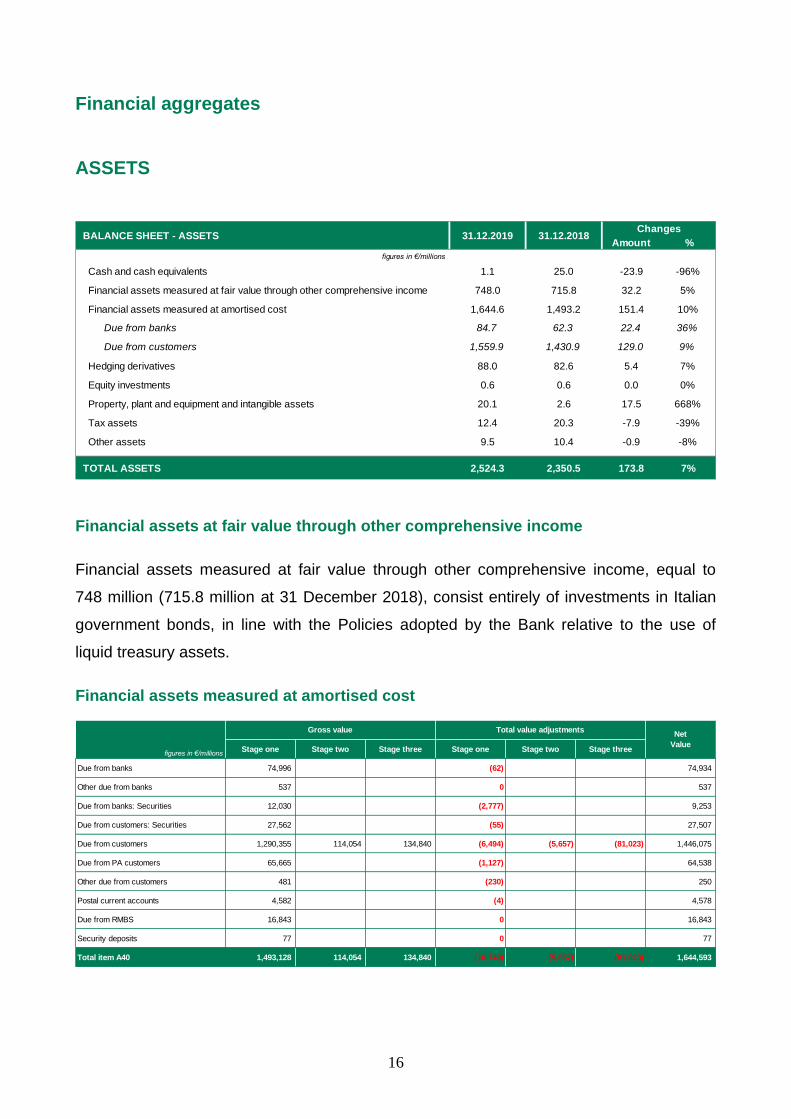

Financial aggregates

ASSETS

Amount %

figures in €/millions

Cash and cash equivalents 1.1 25.0 -23.9 -96%

Financial assets measured at fair value through other comprehensive income 748.0 715.8 32.2 5%

Financial assets measured at amortised cost 1,644.6 1,493.2 151.4 10%

Due from banks 84.7 62.3 22.4 36%

Due from customers 1,559.9 1,430.9 129.0 9%

Hedging derivatives 88.0 82.6 5.4 7%

Equity investments 0.6 0.6 0.0 0%

Property, plant and equipment and intangible assets 20.1 2.6 17.5 668%

Tax assets 12.4 20.3 -7.9 -39%

Other assets 9.5 10.4 -0.9 -8%

TOTAL ASSETS 2,524.3 2,350.5 173.8 7%

BALANCE SHEET - ASSETS 31.12.2019 31.12.2018Changes

Financial assets at fair value through other comprehensive income

Financial assets measured at fair value through other comprehensive income, equal to

748 million (715.8 million at 31 December 2018), consist entirely of investments in Italian

government bonds, in line with the Policies adopted by the Bank relative to the use of

liquid treasury assets.

Financial assets measured at amortised cost

Stage one Stage two Stage three Stage one Stage two Stage three

Due from banks 74,996 (62) 74,934

Other due from banks 537 0 537

Due from banks: Securities 12,030 (2,777) 9,253

Due from customers: Securities 27,562 (55) 27,507

Due from customers 1,290,355 114,054 134,840 (6,494) (5,657) (81,023) 1,446,075

Due from PA customers 65,665 (1,127) 64,538

Other due from customers 481 (230) 250

Postal current accounts 4,582 (4) 4,578

Due from RMBS 16,843 0 16,843

Security deposits 77 0 77

Total item A40 1,493,128 114,054 134,840 (10,749) (5,657) (81,023) 1,644,593

figures in €/millions

Gross value Total value adjustmentsNet

Value

17

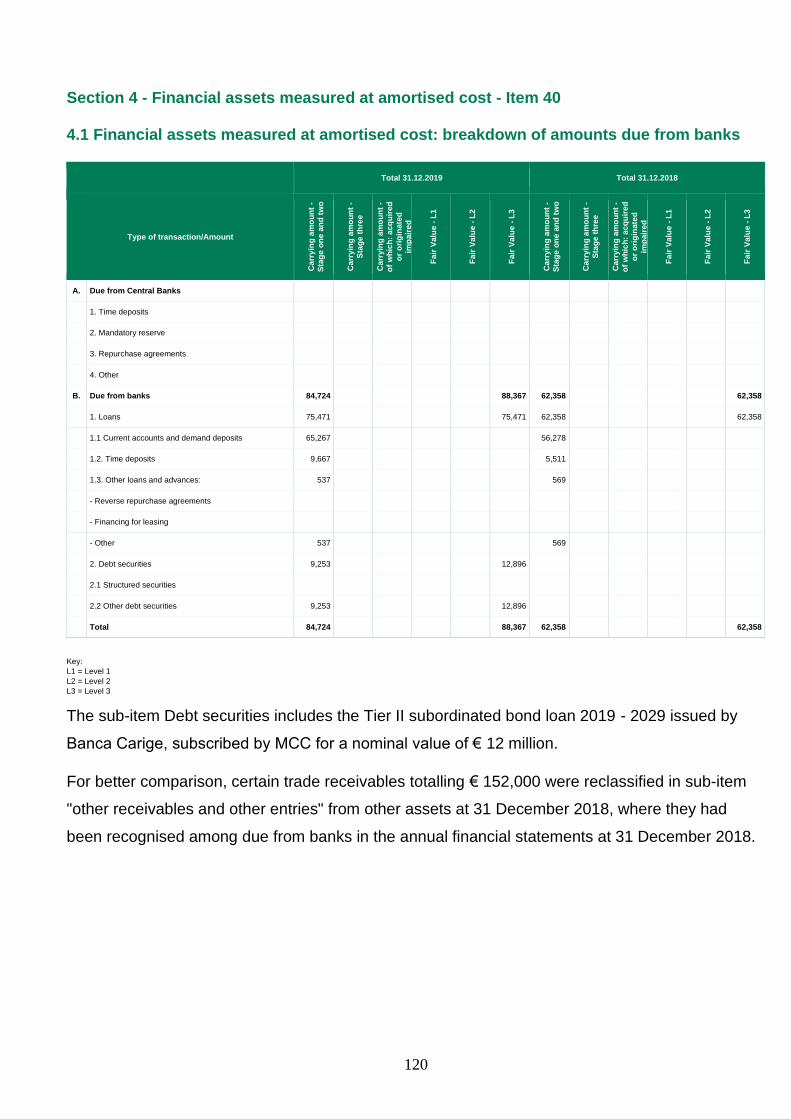

Due from banks

Amounts due from banks amounted to 84.7 million, compared to 62.3 million at 31

December 2018. The item consists of liquidity held in bank current accounts totalling 65.3

million (56.3 million at 31 December 2018), obligatory reserves of 9.6 million (5.5 million at

31 December 2018) and other receivables totalling 0.5 million (0.7 million at 31 December

2018). This sub-item also includes the Tier II subordinate bond loan issued by Banca

Carige S.p.A. and subscribed for 9.3 million by the Bank (net of credit risk adjustments).

Due from customers

This item, of 1,559.9 million (1,430.9 million at 31 December 2018) is made up of:

• loans to customers in the amount of 1,473.6 million (1,336.2 million at 31.12.2018),

consisting of gross loans for 1,566.8 million, of which performing, stage 1 and 2 equal

to 1,432 million (1,421.8 million at 31.12.2018) and adjustment provisions of 93.3

million, of which 81 million relative to impaired loans and 12.3 for performing loans

(85.6 million at 31.12.2018). Loans to customers include bonds subscribed during the

year, mainly through the basket bond mechanism, based on the issue of an ABS

guaranteed by a pool of minibonds, for € 27.5 million (gross value 27.6 million and

adjustment provisions for 0.1 million).

Non Performing Loans (with a gross value of 134.8 million and adjustment provisions of

81.0 million) of 53.8 million (against 63.2 million in 2018), accounting for 3.7% of total

financial receivables (against 4.7% in 2018). In particular, loans classified as Bad loans

totalled 7.6 million (0.5% of loans to customers), with a coverage rate of 73.3%. Loans

classified as Unlikely to pay totalled 46.2 million (3.1% of loans to customers), with a

coverage rate of 56.6%. There were no impaired past-due exposures.

The impact of the item "due from customers" relative to the total on a net basis is 3.4%

(from 4.4% at 31 December 2018).

• trade receivables due from public administrations for management of subsidised funds

of 64.5 million (against 66.6 million at 31 December 2018);

• current accounts open with Poste Italiane of 4.6 million (5.6 million at 31 December

2018);

• receivables claimed from the special purpose vehicle company MCC RMBS srl of 16.8

million (22.4 million at 31 December 2018), for collections recorded by the same during

18

the 4th quarter of 2019 as part of the securitisation transaction involving the Bank’s

mortgage loan portfolio, completed pursuant to Italian Law 130/99 during 2016.

• Security deposits and other net receivables total € 0.4 million.

Other asset items

The item “hedging derivatives” at 31 December 2019 was equal to 88.0 million, and

showed the fair value of derivatives established to hedge against interest rate risk relative

to Bank bond issues.

Equity investments total 0.6 million and derive from the 2017 subscription of 558,140

shares of the Istituto della Enciclopedia Italiana fondata da Giovanni Treccani, equal to

0.89% of the Institute's share capital.

Property, plant and equipment and intangible assets amount to € 20.2 million (2.6 million

at 31 December 2018) and include 1.9 million for investments in software, 0.4 million for

PPE relative to furniture, fixtures and hardware functional to the Bank’s operations and

17.9 million for rights of use relative to leases of properties (17.8 million) and long-term

rentals of vehicles (0.1 million), recognised in accordance with the new accounting

standard IFRS 16.

Tax assets came to 12.4 million (20.3 million at 31 December 2018), consisting entirely of

deferred tax assets (of which 8.2 million for adjustments on loans, 2.8 million for

allocations to provisions for risks and charges, 1.3 million for negative fair value changes

recognised in the securities valuation reserves and 0.1 million for other items).

Other assets total 9.5 million, substantially in line with respect to 31 December 2018 (10.3

million). The main figures included in the item at 31 December 2019 are costs incurred on

third-party assets (2.7 million), tax receivables (4.2 million), prepaid expenses (0.7 million),

receivables due from the parent company (0.4 million) and other receivables to be invoiced

and other items (1.5 million).

19

LIABILITIES

Amount %

figures in €/millions

Financial liabilities measured at amortised cost 2,113.0 1,985.6 127.4 6%

Due to banks 494.4 892.8 -398.4 -45%

Due to customers 1,161.4 796.1 365.3 46%

Securities issued 457.2 296.7 160.5 54%

Value adjustments of financial liabilities with macro-hedging 78.2 73.8 4.4 6%

Tax liabilities 1.0 0.1 0.9 795%

Other liabilities 24.0 15.8 8.2 51%

Employee severance benefits 3.1 3.2 -0.1 -1%

Provisions for risks and charges 8.3 6.6 1.7 26%

Reserves 67.5 40.7 26.8 66%

Share capital 204.5 204.5 0.0 0%

Net income for the period 22.5 20.2 2.3 11%

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY 2,524.3 2,350.5 173.8 7%

BALANCE SHEET - LIABILITIES 31.12.2019 31.12.2018Changes

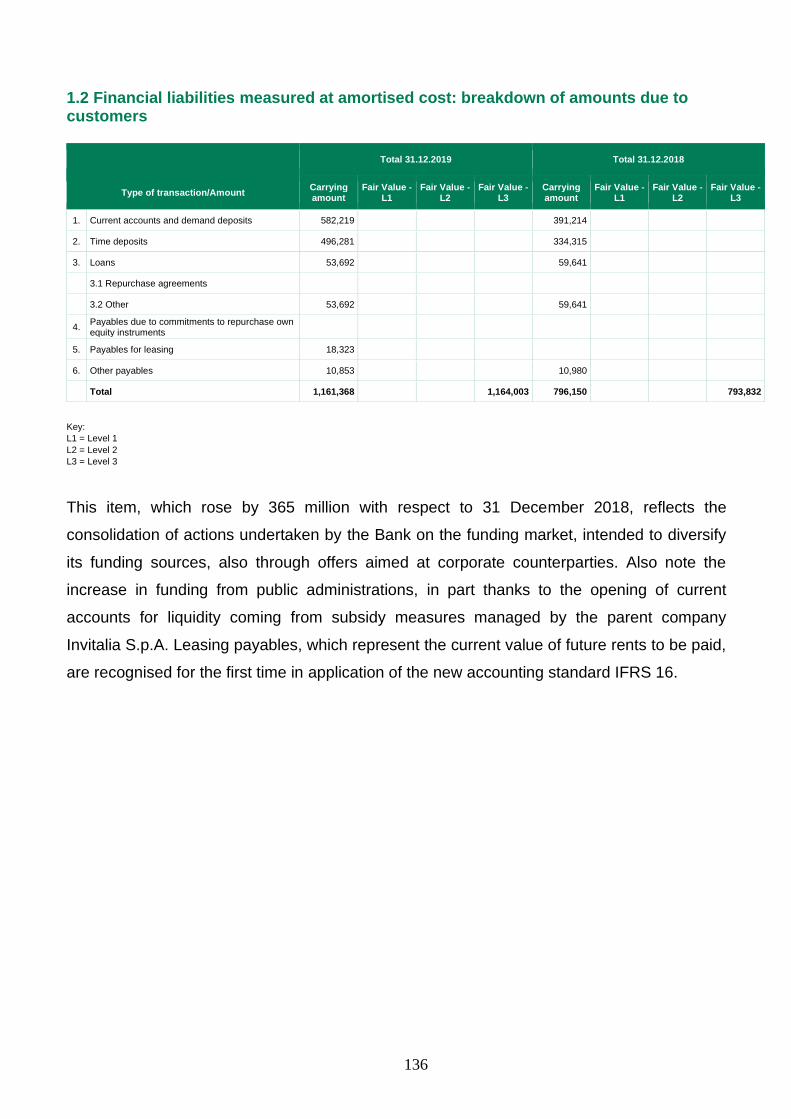

Financial liabilities measured at amortised cost came to € 2,113.0 million (1,985.6 million

at 31 December 2018).

Amounts due to banks at 494.4 million, compared to 892.8 million at 31 December 2018,

can be broken down as follows:

Amount %

figures in €/millions

Open market transactions with ECB 320.5 396.8 (76.3) -19%

Time deposits guaranteeing hedging derivatives 86.5 87.3 (0.8) -1%

Time deposits and interbank loans from Italian banks 0.0 180.0 (180.0) -100%

Repurchase agreements 42.0 199.0 (157.0) -79%

EIB Funds 41.5 25.0 16.5 66%

Other items (amounts to be returned for pool operations) 3.8 4.6 (0.8) -18%

Total 494.4 892.8 (398.4) -45%

ChangesDUE TO BANKS 31.12.201831.12.2019

Amounts due to customers at 1,161.4 million, compared to 796.1 million at 31 December

2018 can be broken down as follows:

20

Amount %figures in €/millions

CDP funding 53.7 59.6 (5.9) -10%

PA current accounts 194.6 115.5 79.1 68%

Customer current accounts 387.2 275.4 111.8 41%

Invitalia current accounts 0.9 0.4 0.5 116%

Time deposits from corporate customers 344.1 184.3 159.8 87%

Invitalia time deposits 152.2 150.0 2.2 1%

Financial payables for rights of use 18.3 0.0 18.3 n.s.

Other items (including amounts to be returned) 10.4 10.9 (0.5) -4%

Total 1,161.4 796.1 365.3 46%

ChangesDUE TO CUSTOMERS 31.12.201831.12.2019

The item due to customers shows an increase of around 365 million mainly due to

increases in current accounts and time deposits from corporate customers, against a

corresponding reduction in amounts due to banks.

Securities issued, equal to 457.2 million (against 296.7 million at 31 December 2018)

consist of a pre-existing bond loan listed on the MOT and revenue from the inaugural

“Social” bond issue (unsecured senior preferred) completed last October in the amount of

300 million, with an annual 1.5% fixed rate, maturing on 24 October 2024. Proceeds from

the issue, listed on the Luxembourg Stock Market, and intended for institutional investors

under the one billion Euro Medium Term Notes (EMTN) program, will be used to finance

and/or refinance loans granted to businesses which contribute to the economic

development of depressed areas, in particular in southern Italy, in full compliance with the

Bank's mission.

Value adjustments of financial liabilities with macro-hedging

The value adjustment of financial liabilities subject to macro hedging was a positive 78.2

million, compared to 73.8 million at 31 December 2018.

Tax liabilities

Tax liabilities, equal to 1 million (0.1 million at 31 December 2018), refer for 0.9 million to

payables for current taxes and for 0.1 million to deferred taxes recognised as contra-

entries in shareholders’ equity, as they relate to taxes on valuation reserves, as well as

actuarial gains on employees’ severance indemnities.

21

Other liabilities

Other liabilities of 24 million (15.8 million at 31 December 2018) consisted of 7.6 million in

operating payables due to suppliers, 7.9 million of payables due to public administrations,

2.6 million of payables to employees and social security institutions, 2.4 million in tax

payables, 1.8 million of payables due to the parent company Invitalia and 1.6 million in

other items. The increase is mainly due to greater concentration of amounts due to

suppliers near the end of the financial year.

Equity

Shareholders’ equity at 31 December 2019 was made up of the share capital -

represented by 40,901,738 ordinary shares with a face value of € 5 each, for a total

amount of 204.5 million, the legal reserve and other reserves for a total amount of 71.4

million, negative valuation reserves for 3.9 million and the profit for the period amounting to

22.5 million.

Shareholders’ equity at 31 December 2019 including profit for the period amounts to 294.5

million (See the Notes - Part B - Section 12).

The Bank holds no shares of its own either directly or through trust companies or

intermediaries.

At 31 December 2019 own funds, determined on the basis of the current rules issued by

the Bank of Italy, were 279.7 million (242.9 million at 31 December 2018) capable of

guaranteeing a level of capitalisation for the Bank more than sufficient with respect to

expected risks and the target level of capitalisation, outlined in the Risk Appetite

Framework (RAF) (see the Notes, Part E).

The capital absorptions and thus the capital requirements are determined on the basis of

the following approaches:

• Credit Risk: Standardised Approach;

• Counterparty Risk: Standardised Approach applied to exposures calculated with the

Current Value Method;

• Operational Risk: Basic Approach;

• Credit Valuation Adjustment Risk: Standardised Approach.

In the absence of a trading book, no absorption is calculated for market risk.

22

The overall total of risk-weighted assets (credit, counterparty, market and operational

risks) amounted to 1,374 million compared to 1,238 million at 31 December 2018.

The CET1, Tier1 and Total Capital Ratios are 20.36%.

Total prudential requirements, calculated with the Basel III approaches, amount to 109.9

million.

CET1, Tier1 and Total Capital ratios are all in line with both the Bank of Italy indications

relative to SREP and the RAF established by the Board of Directors (15.5%).

Capital ratio

Binding

requirement

(TSCR)

Total requirement

(OCR)

Capital

Guidance1

(P2G)

CET1 Ratio 5.54% 8.04% 8.54%

T1 Ratio 7.39% 9.89% 10.39%

TCR 9.86% 12.36% 12.86%

1 In order to ensure that binding measures are respected even in the case of a deterioration in the economic and financial situation, in consideration of exposure to

risks under stress conditions, in the same provision the Regulatory Authority identified the guiding capital levels (capital guidance), which constitute the Regulatory

Authority's expectations relative to additional capital resources which the Bank must hold.

23

With reference to the RAF (Risk Appetite Framework) the risk targets identified by the

Bank are presented below:

Objective Metric Threshold

Capital adequacy

Total Capital Ratio (TCR) ≥ 15.5%

Leverage Ratio (LR) ≥ 6%

Loan portfolio quality Net NPL Ratio (NPL) ≤ 6%

Profitability ROE ≥ 6%

Operating efficiency Cost/Income ≤ 55%

Banking Book interest

rate

∆ Economic value/Own funds ≤/ 10%

∆ Net interest income ≤ 5.5€/mln

Liquidity

Liquidity Coverage Ratio ≥ 140%

Stable funding/Illiquid assets ≥ 100%

Asset encumbrance Tied assets/Total Assets ≤ 55%

24

The business

During 2019, in full compliance with that established in the Business Plan, the Bank’s

commercial activities were mainly focussed on small and medium enterprises in southern

Italy, through a well-developed array of products, with lending also carried out in synergy

with other local players.

Activities to support the commercial development of SME was carried out both by Level II

bank activities, making use of local partnerships with banks, financial companies and loan

consortia, with previously signed agreements, and in B2C mode through the use of the

web portal.

To support the Level II Bank role:

• new memorandums of understanding were signed with loan consortia, associations

and professional organisations;

• the Basket Bond and Tranched Cover mechanisms were used to satisfy

medium/long-term funding requirements for businesses, maintaining good asset

quality.

The portfolio of offerings was enhanced, which includes:

Credit products managed through the Portal

• Chirofast (Fast Unsecured): simple, fast and effective variable rate loan with a

Fund guarantee and a term:

o from 18 to 60 months for inventories and other financial needs;

o from 18 to 84 months for investments in property, plant and equipment

and in intangible assets;

• Chiro PMI (Unsecured SME): variable rate loan supported by a Fund guarantee,

with a term:

o from 18 to 60 months for inventories and other financial needs;

o from 18 to 84 months for investments in property, plant and equipment

and in intangible assets;

• Chiro Nuove Imprese (New Business Unsecured): loan supported by a Fund

guarantee, for small and medium enterprises with a maximum of two financial

statements filed and/or for innovative start-ups, to support the start of business and

initial growth stages, with a term:

25

o from 18 to 60 months for inventories and other financial needs (in the

case of innovative start-ups or when supported by loan consortia

guarantees);

o from 18 to 84 months for investments in property, plant and equipment

and in intangible assets;

Credit products for large companies

• Medium/long-term loans: unsecured or secured loans with excellent flexibility to

satisfy even highly structured requirements:

o from 18 to 60 months for inventories and other financial needs;

o from 18 to 84 months for investments in property, plant and equipment

and in intangible assets;

• Factoring: financing for trade receivables in several technical forms:

o With recourse;

o Without recourse;

o Reverse;

• Subsidy advance: Unsecured loan for businesses benefiting from subsidy

measures. Allows a company to more efficiently make use of sums needed for

investment, without waiting for the subsidies to be disbursed

• Unsecured loans: loans dedicated to SMEs, large companies and midcaps,

available:

o on demand: up to 18 months for commercial commitments;

o with set maturity: short or medium/long-term;

The maturity can be undetermined if the guaranteed counterparty is a public

entity;

• Advances on invoices: loan which provides an advance on trade payables, prior

to their effective availability and maturity, which the company has due from debtors.

Essentially, viewed structurally, the Bank's operations, downstream from implementations

completed and in progress, involve:

26

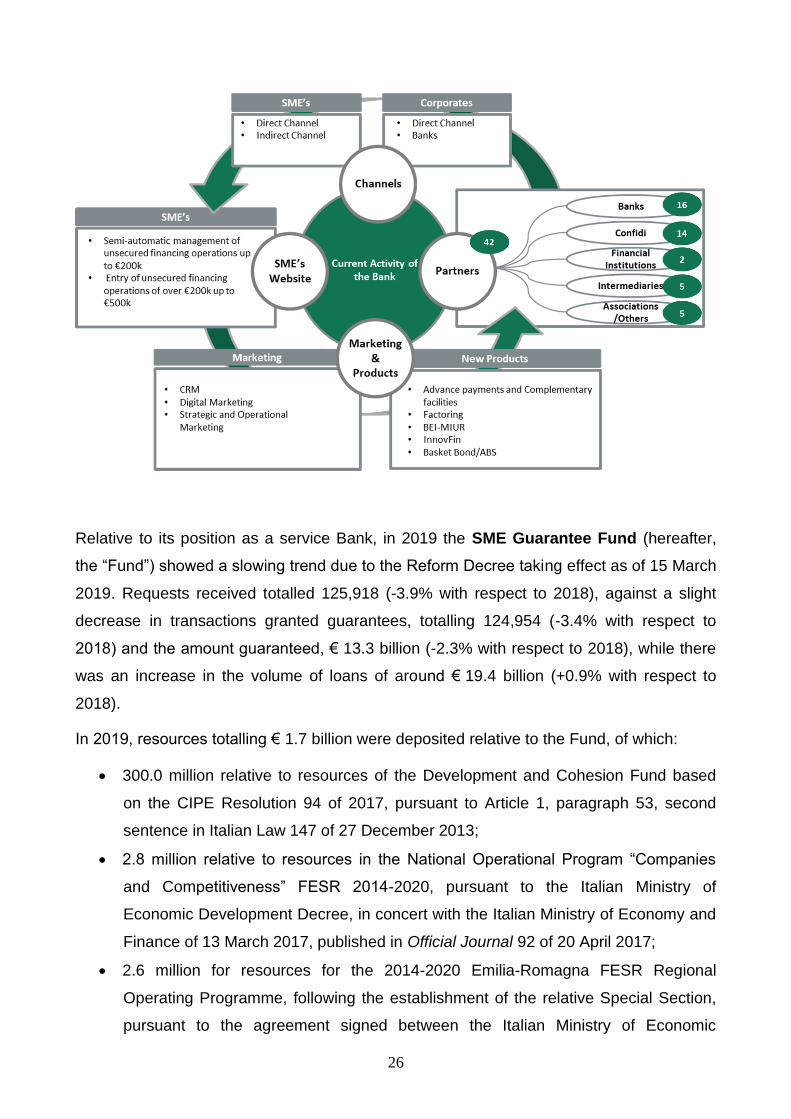

Relative to its position as a service Bank, in 2019 the SME Guarantee Fund (hereafter,

the “Fund”) showed a slowing trend due to the Reform Decree taking effect as of 15 March

2019. Requests received totalled 125,918 (-3.9% with respect to 2018), against a slight

decrease in transactions granted guarantees, totalling 124,954 (-3.4% with respect to

2018) and the amount guaranteed, € 13.3 billion (-2.3% with respect to 2018), while there

was an increase in the volume of loans of around € 19.4 billion (+0.9% with respect to

2018).

In 2019, resources totalling € 1.7 billion were deposited relative to the Fund, of which:

• 300.0 million relative to resources of the Development and Cohesion Fund based

on the CIPE Resolution 94 of 2017, pursuant to Article 1, paragraph 53, second

sentence in Italian Law 147 of 27 December 2013;

• 2.8 million relative to resources in the National Operational Program “Companies

and Competitiveness” FESR 2014-2020, pursuant to the Italian Ministry of

Economic Development Decree, in concert with the Italian Ministry of Economy and

Finance of 13 March 2017, published in Official Journal 92 of 20 April 2017;

• 2.6 million for resources for the 2014-2020 Emilia-Romagna FESR Regional

Operating Programme, following the establishment of the relative Special Section,

pursuant to the agreement signed between the Italian Ministry of Economic

27

Development, the Italian Ministry of the Economy and Finance and the Region on

11 February 2019;

• 3.2 million relative to resources of the Fund Reserve to support micro-enterprises;

• 30.0 million relative to resources of the Development and Cohesion Fund based on

the CIPE Resolution 49 of 2018, pursuant to Article 1, paragraph 53, second

sentence in Italian Law 147 of 27 December 2013;

• 435.0 million pursuant to article 22 of Italian Decree Law 119 of 23/10/2018;

• 3.0 million relative to resources of the Fund Reserve for sequestered and

confiscated businesses;

• 25.7 million for resources for the 2014-2020 Sicily FESR Regional Operating

Programme, following the establishment of the relative Special Section, pursuant to

the agreement signed between the Italian Ministry of Economic Development, the

Italian Ministry of the Economy and Finance and the Region on 20 July 2018;

• 34.0 million for resources for the special section Remain in the South;

• 150.0 million to establish the section to support mid-cap companies;

• 6.0 million for resources for the 2014-2020 Piedmont FESR Regional Operating

Programme, following the establishment of the relative Special Section, pursuant to

the agreement signed between the Italian Ministry of Economic Development, the

Italian Ministry of the Economy and Finance and the Region on 1 July 2019;

• 1.3 million for resources for the 2014-2020 Veneto FESR Regional Operating

Programme, following the establishment of the relative Special Section, pursuant to

the agreement signed between the Italian Ministry of Economic Development, the

Italian Ministry of the Economy and Finance and the Region on 05 October 2018;

• 670.0 million pursuant to article 41 of Italian Decree Law 124 of 26 October 2019;

The main significant events involving the instrument during the year were:

• publication of the operating provisions, which took effect as of 15 March 2019,

pursuant to the Italian Ministry of Economic Development Decree, after hearing

from the Italian Ministry of Economy and Finance of 12 February 2019, regarding

approval of the conditions for admission and general provisions relation to the "New

methods of evaluating businesses for access to the SME Guarantee Fund and

establishment of guarantee measures" and the Ministry of Economic Development

Decree of 12 February 2019, after hearing from the Ministry of Economy and

28

Finance, regarding approval of admissions conditions and general provisions for

financial transactions with tripartite risk.

• the start of operations for the "Special Section, Calabria Region", following the

deposit of € 1.3 million relative to resources for the FESR Regional Operating

Programme 2014-2020 for Calabria;

• the start of operations for the "Special Section, Emilia-Romagna Region", following

the deposit of € 1.3 million relative to resources for the FESR Regional Operating

Programme 2014-2020 for Emilia-Romagna;

• the update of methods used for the Special Section, Sicily Region, increasing

ordinary coverage measures up to 80% with direct guarantees and up to 90% with

reinsurance and counter-guarantees, as well as extending it to transactions with

tripartite risk and to regional loan portfolios;

• the update of methods used for the Special Section, Friuli Venezia Giulia Region,

increasing ordinary coverage measures up to 80% with direct guarantees,

reinsurance and counter guarantees;

• the update of methods used for the Special Section, Veneto Region, increasing

ordinary coverage measures up to 70% with direct guarantees, and up to 90% with

reinsurance and counter guarantees;

• the signing of a guarantee contract with Cassa Depositi e Prestiti under the terms of

the Thematic Investment Platform to Support Italian SMEs - EFSI, Juncker Plan.

The contract involves a counter-guarantee by CDP equal to 80% of a portfolio of

new guarantees granted by the Fund up to a maximum of € 3.8 billion in loans, with

a 6.06% cap;

• the update of methods used for the Special Section, Campania Region;

• publication of general provisions for the granting of Fund guarantees on loan

portfolios, to implement the provisions contained in the Ministry of Economic

Development decree, in concert with the Ministry of Economy and Finance of 21

June 2019, published in the Official Journal no. 217 of 16 September 2019.

In 2019, pursuant to article 1 of Law 147 of 27 December 2013, published in Official

Journal 302 of 27 December 2013, aimed at supporting growth and strengthening the

capital solidity of loan consortia, resources totalling € 50.0 million were deposited relative

to the Fund, in favour of 58 loan consortia.

Additionally, management of various incentives and subsidised financial instruments

29

continued on the account of the government and certain Regions. Of these, the main

instrument managed is the Sustainable Growth Fund (FCS) managed by MCC on the

account of the Italian Ministry for Economic Development, as the head bank of a

temporary consortium consisting of 8 banks and the National Research Council. The Fund

supports investments in R&D and provides cofinancing with PON I&C 2014/2020

resources.

On 22 January 2019 the first come first served tender was launched for the presentation of

research and innovation projects in the Agrifood and Intelligent Factory sectors. Projects

are currently being evaluated and some decrees have already been issued. In 2019

concession decrees were issued for 50 projects, for investments totalling € 110 million and

subsidies granted of € 70 million.

During 2019 assessment and decrees by the Ministry of Economic Development regarding

projects presented for various tenders previously issued by the Administration starting in

2014 continued: Digital Agenda and Sustainable Industry (FRI), Horizon 2020 PON,

Innovation Agreements and Framework Agreements, Large Projects PON. In 2019 award

decrees were issued for 60 projects, for investments totalling over € 626 million and

subsidies granted of € 325 million.

The Ministry of Economic Development issued a decree on 2/8/2019 which refinances

subsidy projects throughout Italy to support companies investing in large research and

development projects in the areas of “Digital Agenda” and “Sustainable Industry”.

Additionally, subsidies for projects to reconvert production processes relative to the

circular economy were also established. This measure is financed with the resources of

the rotating fund for support of companies and the Fund for Sustainable Growth. The

allocation totalled € 329 million.

Preliminary assessment of project proposals continued in 2019, relative to tenders for

Innovation Agreements for research and development projects (Ministerial Decree

24/5/2017 and Ministerial Decree 5/3/2018); specifically, for the Agrifood, Intelligent

Factory and Life Science tender, the initial financial resources were increased to over

€ 535 million, in order to ensure the widest coverage of proposals presented.

On 15/10/2019 a Ministry of Economic Development decree was published which governs

the methods and terms for presentation of requests for subsidies to support experimental

industrial research and development projects. These are projects that fall under the scope

of the National Strategic Plan and the innovation agreements for the Space Economy. The

30

decree identifies the methods used to implement the subsidy project already defined by

Ministerial Decree 2/3/2018, through which financial resources of € 100 million were

allocated.

Disbursement activities were fully operational for the following tenders, issued by the

administration: Horizon 2020, Digital Agenda and Sustainable Industry, Horizon 2020

PON, Large Projects PON, Framework Agreements, Digital Agenda and Sustainable

Industry (FRI) and Euro Trans Bio Tenders. Disbursements carried out during 2019

involved 574 projects for a total of over € 216 million.

Additionally, through a temporary consortia with FISG S.r.l., the Bank was the successful

tenderer for the arranger service in favour of Campania Development, as part of

structuring a Minibond issue by SMEs operating in Campania, supported by public

guarantees in the form of cash collateral, as a basket bond, subscribed by a special

purpose vehicle in turn financed through the issuing of ABS notes subscribed by

institutional investors.

Operating structure

Human Resources

As of 31 December 2019, Bank staff included 295 employees (including 6 seconded to

Invitalia by MCC and 2 seconded to MCC by Invitalia), of which 11 executives2, 172 middle

managers3 and 112 non-managerial personnel. Additionally, as of 31 December 2019, the

Bank had 9 interns, 11 temporary workers and a long-term freelance worker.

During 2019, 40 new employees were hired, of which 1 executive (initially seconded

through 31 December 2018), 10 middle managers (including 1 seconded by the

shareholder) and 29 non-managerial employees; 28 employees left the company (5

executives - including 2 seconded executives, 4 middle managers and 19 non-managerial

personnel).

Organisational solutions and operating projects implemented

During 2019 activities to implement the Business Plan continued. With reference to credit

offerings these included:

2 Of which an executive seconded by the parent company 3 Of which a middle manager seconded by the parent company

31

• extension of the “Credit Portal” platform to support both channels for the origination

and assessment of loans for small and medium enterprises (SME). At present, the

Credit Portal makes it possible for the bank to offer digital lending both directly and

through partners (lending consortia, local banks, trade associations and other

brokers) and allows for real time verification of transaction feasibility on the basis of

information provided through public databases. During the year, phases involving

the investigation of loans were also automated, making use of information coming

from external providers (e.g. Credit Bureaus, Central Credit Register, specialised

providers) with analysis algorithms that generate “alerts” and “insights” to support

creditworthiness analysis by the investigator;

• adaptation of credit granting processes, to consolidate credit offerings developed by

transactions:

o Tranched Cover, carried out synergistically with Banca Monte dei Paschi di

Siena, reserved for companies operating in integrated logistics with operating

headquarters in southern Italy;

o supported by the "InnoVFin SME Guarantee” provided by the European

Investment Fund;

o presented by companies with legality ratings;

• the revision of the operating model to develop factoring;

• implementation of a compliant conservation system for digital documents relative to

accounting and contractual documents.

In the Subsidised area, the main actions involved:

• adjustment of the digital platforms supporting the Guarantee Fund, made necessary

by the reform of the tool as of 15 March 2019, which required the implementation of:

- online rating calculation for beneficiary companies, on the basis of data

collected, making use of information from external databases, credit bureaus

and central credit registers;

- functions dedicated to beneficiary companies to allow them to directly take part

in document control stages, to provide evidence and observe their ceiling;

• activation of mass demand acquisition functions for the Fund, through a dedicated

FEA protocol (Advanced Electronic Flow);

32

• extension of the functions of the “FCS” application platform (Sustainable Growth

Fund) to manage new agreements and tenders on the account of the Ministry for

Economic Development.

Corporate Governance

This paragraph also serves as the Report on Corporate Governance and Ownership

Structures which describes the main features of the risk management and internal audit

system linked to the financial reporting process (Art. 123-bis, paragraph 2, letter b) of the

Consolidated Law on Finance).

The governance model adopted by the Bank is the “traditional” one, featuring the classic

two-part system of the Board of Directors and the Board of Statutory Auditors; independent

auditing of the accounts is entrusted to an external auditing firm.

The Shareholders’ Meeting is held periodically to decide on the matters reserved for the

same by law and by the supervisory regulations.

More specifically, the Ordinary Shareholders’ Meeting approves the Financial Statements

and the allocation of the profits, appoints the Directors and the Statutory Auditors and can

also revoke the same; on proposal of the Board of Statutory Auditors, it confers and

revokes the mandate of the auditing firm; it approves the remuneration policies and

decides on the responsibilities of the Directors and of the Auditors, and it resolves on all

other matters attributed to its competence by law or by the Articles of Association.

The Extraordinary Shareholders’ Meeting passes resolutions on amendments to the

Articles of Association (except those necessary for adapting the same to provisions of law,

and those concerning mergers in the cases contemplated by Arts 2505 and 2505-bis of the

Italian Civil Code and the reduction of share capital in the event of withdrawal for the

shareholder), on the appointment and replacement of liquidators and the powers vested on

the same and on every other matter attributed to its competence by law.

Given the administration and control system adopted by the Bank, the Board of Directors

has responsibility for strategic supervision.

33

The Board of Directors, made up of 5 members (of which at least one fourth4 holding the

requisites of independence required by the laws in force), is vested with all powers for the

ordinary and extraordinary administration to achieve the company purpose, except for

matters which the law and/or supervisory provisions reserve for the Shareholders’

Meeting. Additionally, it is the body granted priority for ensuring that Shareholders' Meeting

resolutions are promptly and accurately carried out.

During the period, the Board of Directors met 18 times.

The Board of Directors elects a Chairperson from among its members, unless already

appointed by the Shareholders’ Meeting, and it may appoint a Deputy Chairperson solely

to act in lieu of the Chairperson in the case of his or her temporary absence or

impediment. Should the Deputy Chairperson also be absent or unable to fulfil his or her

duties, he or she shall be replaced by the most senior member of the Board of Directors

or, in the event of equal length of service, by the eldest member. At present, no Deputy

Chairperson has been appointed.

The Chairperson legally represents the Bank and takes the chair at the Shareholders’

Meeting, and convokes and chairs Board of Directors’ meetings, during which they guide,

coordinate and moderate discussions.

The Board of Directors appoints a Chief Executive Officer and may appoint a General

Manager, both of which must possess the requirements established under the current

regulations.

The Board of Directors may delegate powers to the Chief Executive Officer and, based on

a proposal by them, to the General Manager (if appointed), determining the limits of the

delegation, the powers and rights that it deems opportune, within the limits imposed by law

and the Articles of Association.

In any case, the Chief Executive Officer has the power to submit loan proposals which

must be decided by a Board of Directors’ resolution.

The Board of Directors may confer special delegated powers, on the granting of loans and

on current management to Management Committees, executives, officials and other

employees, determining the limitations, terms and conditions. The decisions taken by the

recipients of delegated powers must be brought to the attention of the Board according to

the methods and with the frequency, at least quarterly, determined by the latter.

4 Circular 285/2013 specifies that when this ratio is not a whole number, it is rounded up when the first decimal is

equal to or less than 5. Otherwise, it is rounded up.

34

The Chief Executive Officer is the person responsible for managing the Bank and ensures

that the same is performed in accordance with the legislation, the Articles of Association

and the guidelines approved by the Board of Directors.

Observing the organisational framework approved by the Board of Directors, the Chief

Executive Officer sets up the Bank’s Organisational Structure defining the tasks and

responsibilities of the single Organisational Units and the related interconnections. The

Chief Executive Officer is also vested with the legal representation of the Company.

The Board of Statutory Auditors, appointed by the Shareholders’ Meeting, is composed of

3 regular auditors, from whom the Shareholders’ Meeting elects the Chairperson, and 2

alternate auditors.

Given the administration and control system adopted, the Board of Statutory Auditors

serves as the Bank's audit body. The Board of Statutory Auditors, in particular, presides

over compliance with the law, regulations and provisions of the Articles of Association and

the adequacy of the Bank’s management and accounting procedures, the risk

management and control system and the functionality of the system of internal controls as

a whole, promoting actions to correct the shortcomings and irregularities found. In order to

properly fulfil its duties, the Board of Statutory Auditors is granted the widest powers

allowed under the regulatory provisions and regulations in effect and makes use of the

internal audit structures and departments, from which it receives appropriate periodic

reports, to carry out and guide its audits and required investigations.

In addition, the Board of Statutory Auditors performs its activity coordinating its work with

the Auditing Firm appointed for independent auditing of the accounts. In this regard, the

Board of Statutory Auditors, after informing the Board of Directors, proposes to the

Shareholders’ Meeting to confer the independent auditing appointment, assessing the

independence of the Firm proposed and supervising over time the activities performed by

the latter. Despite the attribution of the appointment to an auditing firm, the Board of

Statutory Auditors conserves the tasks connected with assessing the adequacy and

functioning of the accounting system.

During the financial year, the Board of Statutory Auditors met 16 times.

Under the terms of the Articles of Association, the independent auditing of the Bank’s

accounts must be carried out by an Auditing Firm listed on the specific register, appointed

by the Shareholders’ Meeting.

35

On 26 April 2012, on a grounded proposal of the Board of Auditors, the Shareholders'

Meeting resolved to confer the mandate for independent auditing of the accounts for the

financial years 2012-2020 on the auditing firm PricewaterhouseCoopers S.p.A.

In order to favour and improve the functioning of the organisational processes aimed at

delegation, coordination of departments, integration and shared decision-making, the

following Management Committees operate within the Bank. The main responsibilities of

each of these are listed below:

• Credit Committee: this supervises the loan granting and management process. It

exercises the delegated powers conferred by the Board of Directors in relation to

granting credit, non-performing loans, probable defaults and past due/over-the-limit

exposures within the limits established by the Board of Directors. It examines the

results of loan analysis and monitoring prepared and presented to the Committee

by the Bank’s competent units, for subsequent presentation by the Chief Executive

Officer to the Board of Directors;

• Commercial Committee: exercises the delegated powers granted by the Board of

Directors with regards to the granting of credit, relative to the business segments

and limits established by the Board of Directors; supervises the credit granting

process in compliance with the criteria defined by the relevant internal departments,

in order to achieve volume, profit and risk containment objectives;

• Pricing Committee: exercises the delegated powers granted to it by the Board of

Directors in regards to definition of prices (spread and conditions) applied to lending

products;

• Business Monitoring Committee: has the objective of systematically monitoring

business development progress, in terms of production volumes and margins for

initiatives; it also approves initiatives used to implement the Business Plan on the

basis of the limited business plans proposed by the commercial departments; it

assesses partnership/convention proposals proposed by commercial structures;

• Internal Controls and Risks Committee: this has an advisory and propositional role.

It assists the Chief Executive Officer and the other corporate bodies in the

integrated management of the overall risks to which the Bank is exposed, and of the

overall internal control system.

There are also Subsidy Committees for managing public actions and funds, in order to

ensure segregation between management of public initiatives and funds and other banking

36

activities, also on the basis of what is defined in the agreements signed by the Bank. The

members of these Committees—who cannot be Bank employees—are chosen on the

basis of the specifications contained in the single agreements and, unless otherwise

contemplated by law or by the relevant agreements, are appointed by the Chief Executive

Officer based on proposals made by the structures responsible for managing Public Funds

(and where applicable, designated by client administrations).

The Subsidy Committees - whose functions are established by the relative regulations and

Agreements - resolve on proposals to admit/reject individual transactions, on revocations,

renunciations, transactions and anything else necessary for the implementation or

termination of a subsidy agreement, as well as on the filing of lawsuits; following the

relative schedule, they approve reports and accounts relative to available funds,

commitments, insolvencies and disputes, demonstrational prospectuses and the relative

report on the amount of commissions and reimbursements due to the Manager; they

define guidelines and operating methods with respect to subsidies, also with regards to the

relations between the Bank as manager, the intermediaries and beneficiary businesses.

Internal control system

“Internal Control System” means the set of rules, functions, structures, resources,

processes and procedures that aim to ensure, observing healthy and prudent

management, that the following objectives are achieved:

1. checking implementation of corporate strategies and policies;

2. containing risk within the limits indicated in the reference framework for determining

the Bank's risk propensity;

3. safeguarding the value of assets and protecting against losses;

4. effectiveness and efficiency of corporate processes;

5. reliability and security of corporate information and IT procedures;

6. preventing the risk that the company will be involved, even involuntarily, in illegal

activities;

7. compliance of operations with the provisions of laws and regulations, including

supervisory rules, and with internal policies, regulations and procedures.

The Internal Control System plays a central role in the corporate organisation and is

strategically significant because:

37

• it represents a fundamental element of knowledge for the corporate bodies, so as to

ensure full awareness of the situation and effective monitoring of company risks and

their interactions;

• it orients the changes of the strategic approaches and corporate policies and makes

it possible to adapt the organisational context in a coherent manner;

• it oversees the functions of the management systems and observance of the

prudential supervisory requirements;

• it favours the diffusion of a correct culture in terms of risks, legality and corporate

values.

The Internal Control System must:

• ensure the completeness, adequacy, functioning (in terms of efficiency and

effectiveness) and reliability of the risk-management process, and its consistency

with the Risk Appetite Framework (RAF);

• provide for control activities spread over every operating segment and hierarchical

level;

• guarantee that the anomalies encountered are promptly brought to the attention of

the Bank’s appropriate organisational levels (to the Corporate Bodies, if significant)

capable of quickly activating the opportune corrective actions.

The Board of Directors, in exercising its duty of strategic supervision, defines the

architecture of the Internal Control System in terms, for example, of principles and

guidelines, organisational oversight, tasks and responsibilities, resources and powers,

information flows and integration of risk management and conflict of interest processes, in

observance of the laws and supervisory regulations, and the Articles of Association.

Annually the Board of Directors, also taking into account the results of the activity of the

Board of Statutory Auditors and supported by the internal audit unit, assesses the

completeness, adequacy, functioning and reliability of the Internal Control System.

The control activities in the Bank are carried out at all hierarchical levels and in all

departments of the organisational structure. All company structures are engaged, each for

their specific level of responsibility and assigned duties, in controlling the processes and

operating activities they are responsible for. The results of the controls then flow into an

articulated system of reporting and information flows, the final destination being the

Supervisory Authority and the governance, management and control bodies, on the basis

38

of the frequency and the contents established by external and internal regulations and

according to the responsibilities of each body.

In application of the principle of proportionality, the Bank has structured its Internal Control

System based on its size and the complexity of its operations, the nature of its activities

and the associated risks to which the Bank is exposed. The Bank's Internal Control

System includes the following levels:

• First level: these include all control activities which the individual business/operating

units carry out on their own processes in order to identify, assess, manage and

monitor their associated risks, in relation to which they identify and implement

specific actions aimed at ensuring the processes are properly completed. They are

carried out by the same business/operating functions (e.g. hierarchical, systematic

and sample controls), or to the extent possible, are incorporated in IT procedures

and are considered an integral part of every company process.

• Second level: these are performed by the risk control function (which includes both

the risk control and validation departments) and by the compliance and anti-money

laundering function, with the aim of monitoring company risks to ensure the

prudential conduction of business, reliability of information and compliance with eh

law and internal procedures;

• Third level: assigned to the internal audit department, which ensures constant,

independent and objective assessment of the functioning of the overall Internal

Control System.

The Compliance and Anti-Money Laundering Area includes the compliance department

and the anti-money laundering department. Their responsibilities are based on specific

provisions contained in laws and supervisory regulations and are implemented through

internal regulation documents, approved by the Board of Directors.

The Manager of the Area is appointed manager of the compliance department as well as

the company's anti-money laundering manager and reports to the Chief Executive Officer.

In any case, he or she has direct access to the Board of Directors and to the Board of

Statutory Auditors and communicates with them without restrictions or intermediation.

The Compliance model adopted by the Bank assigns the Compliance department the task

of directly monitoring non-compliance risk with reference to the relevant regulations

governing bank and brokering activities, management of conflicts of interest, transparency

with customers and, more generally, consumer protection regulations. It is also

39

responsible for identifying specialised safeguards within the Bank in order to manage non-

compliance risk for the regulatory areas which apply (e.g. workplace safety, taxes). In any

case, the Compliance department continues to be responsible, for these areas as well, for

at least the definition of methods used to assess non-compliance risks, to identify the

relative procedures and to verify the adequacy of these procedures in preventing non-

compliance risks, as well as assessing the adequacy of these safeguards in managing the

overall non-compliance risks.

The Risk Management Department plays the role of risk control unit - as defined by the

current regulatory rules - and performs the tasks assigned to this unit in the guidance

documents, and in the policies and guidelines approved by the Board of Directors, in

particular with reference to the Risk Control Department Regulations.

The manager of the department is also the Risk Control Department Manager and reports

to the Chief Executive Officer. In any case, they have direct access to the Board of

Directors and the Board of Statutory Auditors and can communicate with them without

restrictions or intermediaries.

The Internal Audit Department plays the role of internal audit unit, as defined by the

current regulatory rules and performs the tasks assigned to this unit in the guidance

documents, in the policies and guidelines and approved by the Board of Directors, in

particular with reference to the Internal Audit Process Regulations.

The Manager of the Department is appointed Manager of the internal audit unit.

The manager of the internal audit unit reports to the Board of Directors; he or she has

direct access to the Board of Statutory Auditors and communicates with them without

restrictions or intermediation. The link between the manager of the internal audit unit and

the Chief Executive Officer is in any case ensured through adequate information flows and

participation, as a member, in any management committees in the field of internal controls

and risks.

The managers of the control units hold suitable requisites of professionalism, are

appointed and revoked by the Board of Directors, after consulting the Board of Statutory

Auditors, and do not have direct responsibility for operating areas subject to audit.

40

The Bank’s System of Controls also includes the Board of Auditors, the Oversight

Committee pursuant to Italian Legislative Decree 231/2001(henceforth also the “231 OC”)

and the independent auditing firm.

The main objective of the 231 OC is to prevent the crimes contemplated by Legislative

Decree 231/2001 by verifying the adequacy and effectiveness of the Organisational and

Management Model adopted by the Bank pursuant to the Decree.

The Committee operates according to regulations approved by the Board of Directors and

has a budget for expenses and wide powers of control and inspection at all levels.

The 231 OC, a specifically established collegial body, currently consists of the

Chairperson, an independent external professional, and two other members, specifically

the managers of the Bank's Internal Audit and Risk Management departments (which, in

the context of the company, have no operational tasks, ensuring full independence).

Alternatively, as established in current norms, the Bank's 231 OC functions may be

performed by the Board of Statutory Auditors.

The Auditing Firm, for the duties assigned to the same by law, liaises - for the purpose of

exchanging information and/or data - with the Board of Directors, the Board of Auditors,

the Internal Audit Department and the other corporate control bodies and/or units.

Lastly, as regards coordination and operational management of the internal control model

required by Law 262/05 on Investor Protection (Art. 154-bis of the Consolidated Law on

Finance), the Manager of the Administration, Control and Finance Department, in his/her

capacity as Financial Reporting Manager, must prepare—and effectively put into

practice—adequate administrative and accounting procedures for preparing the

Company’s financial statements as well as every other communication of a financial nature

made available to the market.

The Bank’s Financial Reporting Manager—jointly with the Chief Executive Officer—must

also, in a specific report on the Company’s annual and six-monthly financial statements,

certify:

• adequacy and effective application of the administrative and accounting procedures;

• compliance with the applicable international accounting standards recognised in the

European Community pursuant to Regulation (EC) no. 1606/2002 of the European

Parliament and of the Council of 19 July 2002;

41

• correspondence with the entries in the accounting ledgers and documents;

• the true and correct representation of the shareholder’s equity, and economic and

financial situation of the bank;

• the inclusion in the report on operations of a reliable analysis of performance and of

the operating result, together with a description of the main risks and uncertainties

to which the Bank is exposed.

In order to comply with the provisions of law, the Bank has adopted an Internal Control

System which involves the application of a common methodological framework based on:

• use of a uniform model based on internationally-recognised methodological

standards (CoSO and Cobit);

• constant updating of the Model, with attribution of specific responsibilities to the

subjects involved;

• generalised communication of the model through training programmes.

Specifically for the model adopted:

• documentation must be validated and the execution of the controls on the part of

the respective competent managers must be confirmed;

• every administrative/accounting procedure and every control must be documented,

assessed, tested and validated and a single manager appointed as responsible for

executing the activities contemplated therein;

• an internal confirmation flow (to the Bank’s Financial Reporting Manager) has been

defined as well as an external confirmation flow (to the Parent Company’s Financial

Reporting Manager and to the market) in relation to the Internal Control System for

financial disclosure.

The Bank adopts a Regulation for the Financial Reporting Manager in which - in line with

the provisions of Art. 154-bis of the Consolidated Law on Finance and in accordance with

Art. 24 of the Articles of Association - the following are defined:

• appointment procedures, requisites, duties, powers and resources of the Financial

Reporting Manager;

• relations with the Bank’s governing bodies and control bodies;

42

• the information flows from and to the other control structures and the Financial

Reporting Manager of the parent company, within the sphere of the information

required for preparing the consolidated financial statements.

Additionally, the Guidelines - Financial Information Internal Control System (hereinafter

“FIICS”) have been approved which govern—in compliance with the provisions of art. 154-

bis of the CLF—the criteria and methods, and identify the roles and responsibilities:

• for establishing and maintaining over time the Bank’s Financial Information Internal

Control System;

• for assessing its adequacy and effective operation.

The provisions of the FIICS are part of the Bank’s overall internal control system and are in

keeping with the current legislative prescriptions. Additionally, provision 1079 “Procedure

for compliance 262/05” governs operating activities and methodological tools use to

institute and maintain over the time the Bank’s Financial Information Internal Control

System (FIICS), as well as for assessing its adequacy and operational effectiveness, in

respect of the roles and responsibilities defined in the FIICS.

On the basis of the internal regulations, during the year the planned updating of the

administrative procedures was carried out, to comply with Italian Law 262/05. The roles

involved, the activities and responsibilities relating to the steps of the macro processes

were also identified.

During 2019, the Financial Reporting Manager issued the attestations and declarations

required, maintaining, in the context of her activity, all the contacts and relations with the

other external and internal control bodies, namely the Board of Statutory Auditors, the

Auditing Firm, the Oversight Committee, the Internal Controls and Risks Committee, the

internal audit, compliance and money-laundering units, and with the Parent Company’s

Reporting Manager.

On the occasion of the presentation of the Company’s annual separate financial

statements and the six-monthly financial report, the Financial Reporting Manager submits

to the Board of Directors a report on the Financial Information Internal Control System, as

well as the text of the certification to the Market, to be signed jointly with the Managing

Director to guarantee compliance with the requirements imposed by law.

43

Non-financial disclosure

Legislative changes and Sustainability

On 25 January 2016, Legislative Decree 254/2016 (O.J. 10.1.2017) came into force. This

implements the European Directive on information of a non-financial nature that certain

businesses are required to publish. The Bank5, to which the law does not apply obligatorily

owing to its size, has decided in any case to supplement the information of a non-financial

nature in the Report on Operations, taking the opportunity to present to the market and to

the main stakeholders the total value generated by the business, also through the relative

social and environmental impacts, as useful elements for strengthening its business and

better overseeing its risks and impacts.

The Report provides a brief description which illustrates the interconnection between

corporate objectives, activities and results achieved with respect to certain specific areas

that the Bank is managing as priorities: the actions and activities carried out for achieving

these objectives are therefore illustrated, assessing the results obtained also with

reference to the improvement actions carried out and identified as necessary for the near

future.

The Report takes as a reference a number of indicators typical of sustainability reporting,

taken from the GRI (Global Reporting Initiative) Guidelines, and provides significant

qualitative and quantitative elements in relation to the goals and policies defined and their

impact on the Bank’s main stakeholders: employees; businesses and private customers,

the Public Administration, relations with which are managed by the Bank in a manner and

according to processes governed by specific agreements, treated separately from the

banking activities, with a separate decision-making, organisational, administrative and

accounting framework.

Mission and corporate model, values and principles, compliance and

control processes

Mediocredito Centrale S.p.A. is a bank which operates mainly in lending and in managing

public subsidies and services in line with its statutory mission.

5 Therefore, the Bank did not assign any compliance audit either to the independent auditing firm nor to any other authorise subject.

44

The Bank is 100% controlled by Invitalia S.p.A. , which in turn is fully held by the Ministry

of Economy and Finance.

A series of principles and values guide the actions of subjects who operate within the

Bank, at every level, formalised in the Code of Ethics and in the Suppliers’ and Partners’

Code of Conduct, and available to all employees on the corporate Intranet.

The Code of Ethics - an integral part of the Organisation, Management and Control Model