annual conference structuring …pwc key updated regulations in 2015 •provident fund act b.e. 2558...

TRANSCRIPT

17th Annual Conference

Maximise Shareholder Value 2016

27 October 2015

www.pwc.com/th

Structuring your mobility programme to embrace tax law changes in Thailand

PwC

Agenda

1. Updates - laws and regulations

2. Moving people with purpose – Modern mobility survey

3. Exploring tax efficient assignment structures

4. Foreign Tax Credit - FTC

5. Q & A

2

27 October 2015Maximise Shareholder Value 2016

PwC

UpdatesLaws & Regulations

3

27 October 2015Maximise Shareholder Value 2016

PwC

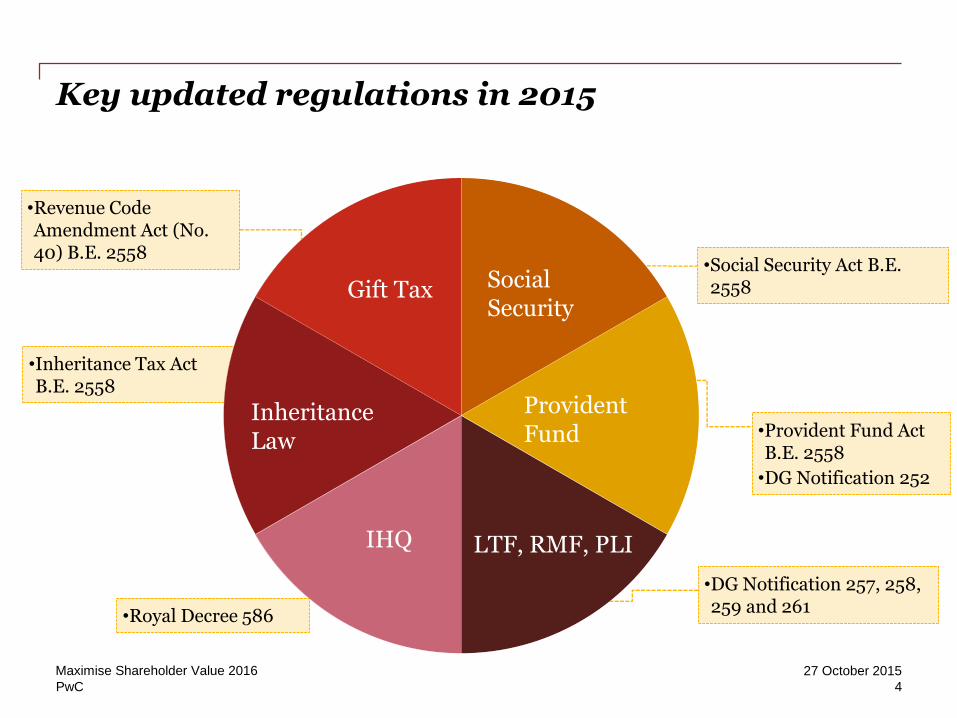

Key updated regulations in 2015

•Provident Fund Act B.E. 2558

•DG Notification 252

Gift Tax

•Social Security Act B.E. 2558

•DG Notification 257, 258, 259 and 261

•Royal Decree 586

•Inheritance Tax Act B.E. 2558

•Revenue Code Amendment Act (No. 40) B.E. 2558

Social Security

ProvidentFund

LTF, RMF, PLI

Gift Tax

Inheritance Law

IHQ

4

27 October 2015Maximise Shareholder Value 2016

PwC

Social Security Fund

• Effective 20 October 2015

• Monthly submission deadline - Company’s obligation

• Permanent and temporary employees assigned overseas -Obligation to contribute

Key updated regulations in 2015

5

27 October 2015Maximise Shareholder Value 2016

PwC

Provident Fund

• Effective 9 November 2015, employee can contribute more than employer

• Effective 1 January 2015, right to count consecutive service years with each employer, subject to conditions

Key updated regulations in 2015

6

27 October 2015Maximise Shareholder Value 2016

PwC

LTF, RMF, Pension life insurance

• Effective 1 January 2015

• Assessable income that must be subject to tax for each tax year as a base for computing qualified amount of investment

Key updated regulations in 2015

7

27 October 2015Maximise Shareholder Value 2016

PwC

International headquarters (IHQ)

• Updated in morning session

• Touch on PIT on later slide

Key updated regulations in 2015

8

27 October 2015Maximise Shareholder Value 2016

PwC

Key updated regulations in 2015

Inheritance tax

• Effective 1 February 2016; taxable base is the value of assets exceeding Baht 100 million

- 5% tax rate if individual is blood-related ascendant or descendant

- 10% tax rate for other heirs- Tax return must be submitted within 150 days after the

inheritance occurs

9

27 October 2015Maximise Shareholder Value 2016

PwC

Gift tax

• Effective 1 February 2016; taxable base is the value of assets exceeding Baht 20 million per year for ascendants, descendants or spouse and Baht 10 million per year for other people.

- 5% final tax, or- Included with annual tax return- Withholding tax may be applied

Key updated regulations in 2015

10

27 October 2015Maximise Shareholder Value 2016

PwC

Moving people with purpose -Modern mobility survey

11

27 October 2015Maximise Shareholder Value 2016

PwC

The war for talent New mobility types are coming into play

Companies are also starting to move people more purposefully. Using mobility to attract, develop and retain talent is becoming more common.

Talent swaps between organisations are expected

to increase by 49% and

developmental moves

by 42% over the next

two years.

12

27 October 2015Maximise Shareholder Value 2016

PwC

Key mobility trends

The new norm

• Fluid mobility types – commuters/regional-global roles

• Using mobility to attract, retain and develop talent

• Mobility functions playing a more strategic role

• Authorities collaborating on immigration/tax compliance issues

• Increased co-operation with authorities to ensure compliance

• Pressure on mobility budgets and headcounts

Becoming outdated

• Mobility function being seen as a cost

• Business acceptance of tax/immigration/social security failures

• Traditional long-term assignments and operating models

• Inability to report on cost and ROI

• Technology not being a prerequisite

13

27 October 2015Maximise Shareholder Value 2016

PwC

• Increased public interest in companies paying a ‘fair’ amount of tax in the right locations

• Customers need to see companies doing this to maintain a strong and trusted brand

Changing social climate

Top mobility priorities for businesses

7%

10%

16%

18%

18%

18%

23%

23%

35%

36%

44%

51%

Increase diversity in the mobileworkforce

Improve vendor management

Use mobility data and analytics, e.g.to track return on investment

Redesign our approach to managingmobility

Manage new mobility types

Improve the assignee experience

Improve governance of mobility

Move people with a purpose -differentiate the assignment 'deal'…

Design or enhance mobility policies

Align mobility and talent

Manage costs

Manage compliance effectively

Q. Which three of the following are the key mobility priorities for your organisation over the next two years? Base size: all respondents (193)

• The global tax and regulatory framework was designed for a less interconnected world, yet expectations of compliance are increasing

• Authorities becoming more sophisticated and aggressive in pursuit

• How do you manage this?

The challenge

14

27 October 2015Maximise Shareholder Value 2016

PwC

The big challenges to moving people successfully

ChallengesFacingModern Mobilityfunctions

Manage Cost

Manage compliance effectively

In-depth knowledge of home & host

country taxation

Changing rules –renewed focus from tax authorities, including introduction of BEPS

Design or enhance mobility policies

Audit Trends

Manage new types of mobility

15

27 October 2015Maximise Shareholder Value 2016

PwC

Exploring tax efficient assignment structure

16

27 October 2015Maximise Shareholder Value 2016

PwC

Common types of assignment structure

ServiceNon-

service

New assignment type

• Business traveller

• Short term assignment

• Talent swap

Secondment arrangement

Dual roles

Regional roles

Service agreement

17

27 October 2015Maximise Shareholder Value 2016

PwC

Service arrangement

18

27 October 2015Maximise Shareholder Value 2016

PwC

Service arrangement – Characteristics

• Service agreement between home and host entity• Employment remains at home• Provide services to host• Pay service fees to home• Remuneration costs borne by home• Still entitled to social security and pension at home• Per diem to employee

Home Host

Fee payment

Providing service

19

27 October 2015Maximise Shareholder Value 2016

PwC

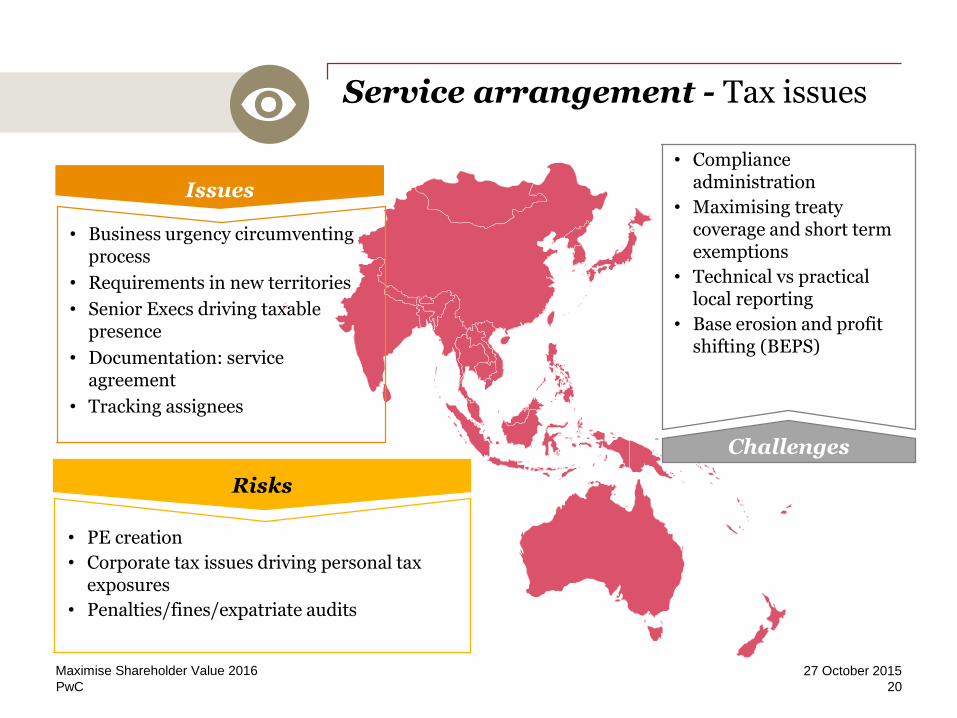

Service arrangement - Tax issues

Issues

• Business urgency circumventing process

• Requirements in new territories

• Senior Execs driving taxable presence

• Documentation: service agreement

• Tracking assignees

Risks

• PE creation

• Corporate tax issues driving personal tax exposures

• Penalties/fines/expatriate audits

Challenges

• Compliance administration

• Maximising treaty coverage and short term exemptions

• Technical vs practical local reporting

• Base erosion and profit shifting (BEPS)

20

27 October 2015Maximise Shareholder Value 2016

PwC

Service arrangement - Social security and payroll (only if PE exists)

Issues

• Focus on cost savings

• Capturing global payments, benefits, trailing liabilities and gross ups

Risks

• Penalties/fines

• Wider audits of local population/specific assignment types

Challenges

• Lack of social security totalisation agreements and optimisation

• Technical vs practical requirements

• Operating local or shadow payroll

21

27 October 2015Maximise Shareholder Value 2016

PwC

Non-service arrangement

22

27 October 2015Maximise Shareholder Value 2016

PwC

Secondment arrangement– Characteristics

• Employment in home temporarily suspended• Employment with host• Documentation: Secondment agreement, Assignment

contract/Local employment• Corporate deductibility in host• Remuneration costs borne by host• Tax policy • Additional benefits provided• Home as paying agent (if any)• Accounting record

Home HostEmployment move

23

27 October 2015Maximise Shareholder Value 2016

PwC

Secondment arrangement - Tax issues

Issues

• Who is the ‘real’ employer?

• Documentation: secondment agreement, assignment letter, local employment contract?

• Worldwide employment income?

Risks

• Penalties/fines/expatriate audits

Challenges

• Compliance administration

• Recharging costs effectively

24

27 October 2015Maximise Shareholder Value 2016

PwC

Secondment arrangement - Social security and payroll

Issues

• Focus on cost savings

• Capturing global payments, benefits, trailing liabilities and gross ups

• Assignee sensitivity to change

Risks

• Penalties/fines

• Wider audits of local population/specific assignment types

• Assignees demanding local benefit rights

Challenges

• Lack of social security totalisation agreements and optimisation

• Technical vs practical requirements

• Operating local or shadow payroll

• Right to contribute to home social security and pension

25

27 October 2015Maximise Shareholder Value 2016

PwC

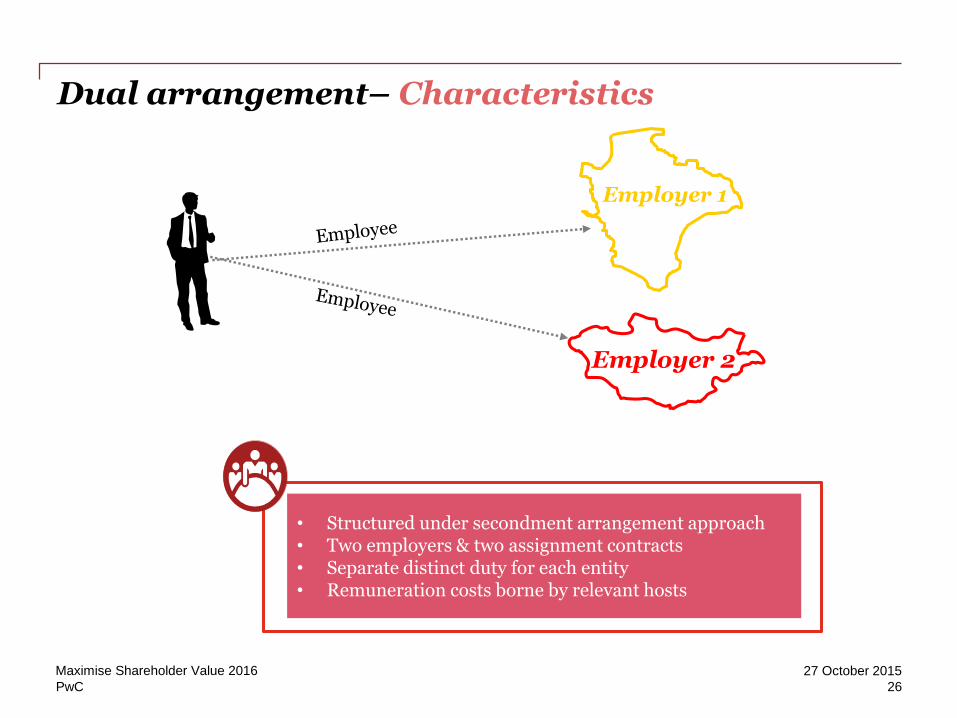

Dual arrangement– Characteristics

• Structured under secondment arrangement approach• Two employers & two assignment contracts• Separate distinct duty for each entity• Remuneration costs borne by relevant hosts

Employer 1

Employer 2

26

27 October 2015Maximise Shareholder Value 2016

PwC

Dual arrangement - Tax issues

Issues

• Who is the ‘real’ employer?

• Documentation: local employment contracts?

• Reconciliation of income?

• Justifiable?

• Chance of double taxation

• Tracking assignees

Risks

• Penalties/fines/expatriate audits

• Some countries may not accept dual arrangement

Challenges

• Compliance administration

• Technical vs practical local reporting

• Recharging costs effectively

27

27 October 2015Maximise Shareholder Value 2016

PwC

Dual arrangement - Social security and payroll

Issues

• Focus on cost savings

• Capturing global payments, benefits, trailing liabilities and gross ups

• Assignee sensitivity to change

Risks

• Penalties/fines

• Wider audits of local population/specific assignment types

• Assignees demanding local benefit rights

Challenges

• Lack of social security totalisation agreements and optimisation

• Technical vs practical requirements

• Operating local or shadow payroll

• Right to contribute to home social security and pension

28

27 October 2015Maximise Shareholder Value 2016

PwC

Regional arrangement– Characteristics

• Structured under secondment arrangement and service agreement approach

• Based in one country and provide services to others• Responsible for more than one country• Remuneration costs borne by host based country

Homeemployee Host

based

29

27 October 2015Maximise Shareholder Value 2016

PwC

Regional arrangement - Tax issues

Issues

• Business urgency circumventing process

• Requirements in new territories

• Who is the ‘real’ employer?

• Senior Execs driving taxable presence

• Documentation required?

• Worldwide employment income?

• Tracking assignees Challenges

• Compliance administration

• Maximising treaty coverage and short term exemptions

• Technical vs practical local reporting

• Base erosion and profit shifting (BEPS)

• Recharging costs effectively

Risks

• PE creation

• Corporate tax issues driving personal tax exposures

• Penalties/fines/expatriate audits

30

27 October 2015Maximise Shareholder Value 2016

PwC

Regional arrangement - Social security and payroll

Issues

• Focus on cost savings

• Capturing global payments, benefits, trailing liabilities and gross ups

• Assignee sensitivity to change

Risks

• Penalties/fines

• Wider audits of local population/specific assignment types

• Assignees demanding local benefit rights

Challenges

• Lack of social security totalisation agreements and optimisation

• Technical vs practical requirements

• Operating local or shadow payroll

• Right to contribute to home social security and pension

31

27 October 2015Maximise Shareholder Value 2016

PwC

Regional arrangement – Your choices

• Regional Operating Headquarters (ROH) Scheme 1

• Regional Operating Headquarters (ROH) Scheme 2 Require to register by 14 November 2015

• International Headquarters (IHQ)

Expat tax: 15% withholding tax

32

27 October 2015Maximise Shareholder Value 2016

PwC

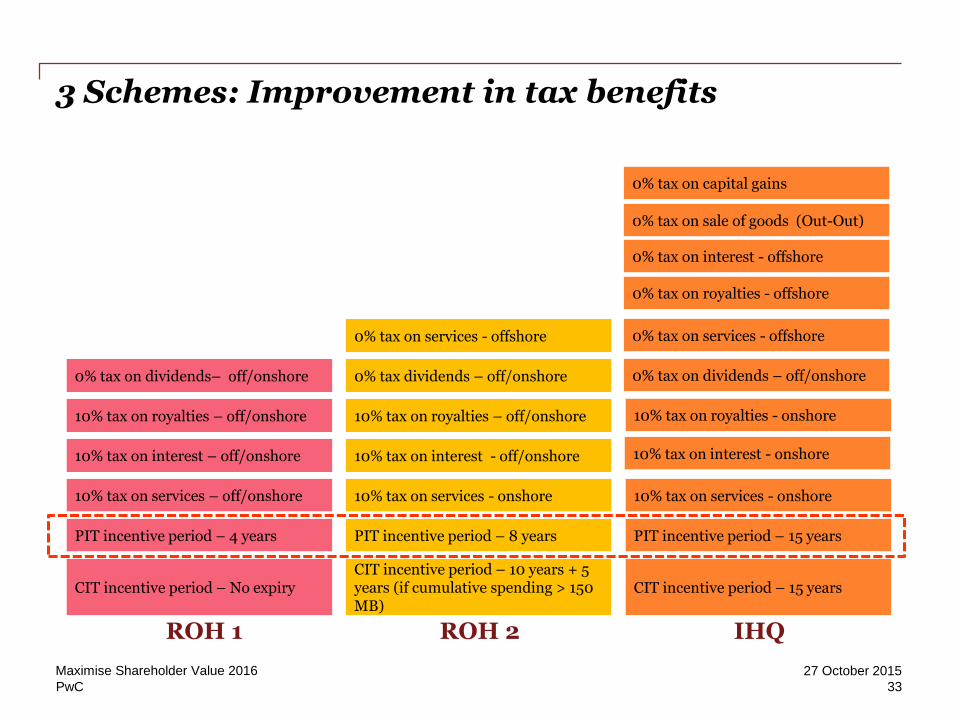

3 Schemes: Improvement in tax benefits

10% tax on royalties - onshore

PIT incentive period – 15 years

10% tax on services - onshore

ROH 2 IHQ

PIT incentive period – 8 years

10% tax on services - onshore

10% tax on interest – off/onshore

10% tax on royalties – off/onshore

10% tax on interest - off/onshore

10% tax on royalties – off/onshore

0% tax dividends – off/onshore 0% tax on dividends – off/onshore

10% tax on services – off/onshore

PIT incentive period – 4 years

0% tax on capital gains

0% tax on sale of goods (Out-Out)

0% tax on dividends– off/onshore

0% tax on services - offshore 0% tax on services - offshore

ROH 1

0% tax on royalties - offshore

10% tax on interest - onshore

0% tax on interest - offshore

CIT incentive period – 10 years + 5 years (if cumulative spending > 150 MB)

CIT incentive period – No expiry CIT incentive period – 15 years

33

27 October 2015Maximise Shareholder Value 2016

PwC

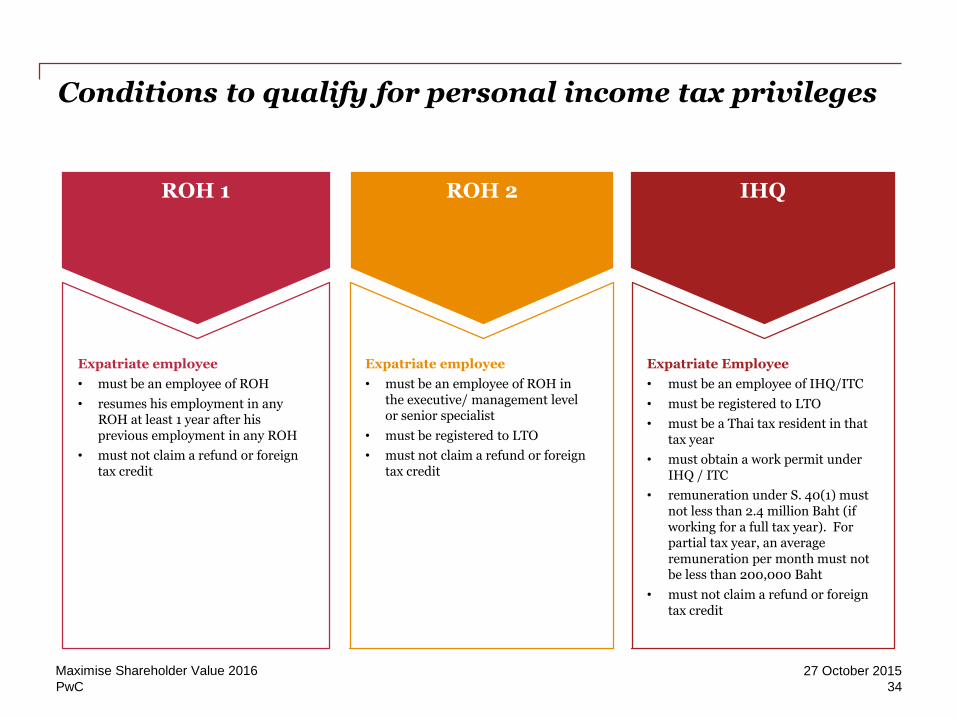

ROH 1

Expatriate employee

• must be an employee of ROH

• resumes his employment in any ROH at least 1 year after his previous employment in any ROH

• must not claim a refund or foreign tax credit

ROH 2

Expatriate employee

• must be an employee of ROH in the executive/ management level or senior specialist

• must be registered to LTO

• must not claim a refund or foreign tax credit

IHQ

Expatriate Employee

• must be an employee of IHQ/ITC

• must be registered to LTO

• must be a Thai tax resident in that tax year

• must obtain a work permit under IHQ / ITC

• remuneration under S. 40(1) must not less than 2.4 million Baht (if working for a full tax year). For partial tax year, an average remuneration per month must not be less than 200,000 Baht

• must not claim a refund or foreign tax credit

Conditions to qualify for personal income tax privileges

34

27 October 2015Maximise Shareholder Value 2016

PwC

Home

Business traveller - Characteristics

• Based in home country• Travel to different countries from time to time• Due to business needs• No formal structure• Travel for short duration or ad hoc duty

35

27 October 2015Maximise Shareholder Value 2016

PwC

Short term assignment - Characteristics

Home HostShort period assignment

• Can be based on service or secondment• Should work short period or ad hoc duty

(less than 6 months)• Due to business needs• Formal approval and documentation

required

36

27 October 2015Maximise Shareholder Value 2016

PwC

Which assignment structure fits your needs?

Concern/type of assignment

Service arrangement

Secondment arrangement

Dual arrangement

Regional arrangement

Home tax

Host tax

PE risk ** **

Double tax issue

Filing requirement

- Home

- Host

Immigration

Social security

- Home

- Host **

= Triggered

= May be triggered**Proper supporting documentation should be put in place.

**Before implementation, both professional tax and legal advice is recommended.

37

27 October 2015Maximise Shareholder Value 2016

PwC

FTCForeign tax credit

38

27 October 2015Maximise Shareholder Value 2016

PwC

FTCOur experiences and solutions

**Ruling is not law. Each individual’s case is open to the tax officer’s interpretation.

Taxed in TH because employer & payroll in TH

Costs borne by TH and recorded as CIT expense in TH Solution

DTA

Article 15 P1

Outbound Service

Taxed in host because spent over 183 days in host

Gor Kor 0702(Gor Mor 05)/1846, 24 September 2010

Ruling: Gor Kor 0702(Gor Mor 14)/1054, 18 May 2014

39

27 October 2015Maximise Shareholder Value 2016

PwC

FTCOur experiences and solutions

**Ruling is not law. Each individual’s case is open to the tax officer’s interpretation.

Solution

DTA

Article 23

Outbound Partial

Secondment

Taxed in home - Employer & payroll in TH

Share cost on portion paid by each entity

Taxed in host - Cost is borne by host

Individual is a resident of TH

Ruling: Gor Kor 0706/297, 13 January 2006

40

27 October 2015Maximise Shareholder Value 2016

PwC

When mobilising people, factors to be considered in selecting assignment type

Period of assignment

Tax compliance

Roles & responsibilities

Home and host country tax

DTA exemption

Social security & work permit

41

27 October 2015Maximise Shareholder Value 2016

PwC

Q&A

42

27 October 2015Maximise Shareholder Value 2016

PwC

Contact

Jiraporn ChongkamanontDirector – Practice LeaderTel: +66 (0) 2344 [email protected]

Hatairat TopiboonpongSenior ManagerTel: +66 (0) 2344 [email protected]

43

27 October 2015Maximise Shareholder Value 2016

Thank you

© 2015 PricewaterhouseCoopers Legal & Tax Consultants Ltd. All rights reserved.

‘PricewaterhouseCoopers’ and/or ‘PwC’ refers to the individual members of the

PricewaterhouseCoopers organisation in Thailand, each of which is a separate and

independent legal entity. Please see www.pwc.com/structure for further details.