anglo pacific group plc · 2019-04-23 · anglo pacific group plc financial resources 9 • royalty...

TRANSCRIPT

March 2015

1

Anglo Pacific Group PLCResults for the year ended December 31, 2014

Anglo Pacific Group PLC

Important disclaimer

2

Certain statements in this presentation, other than statements of historical fact, are forward-looking statements based on certain assumptions and reflect the Company’s expectations and views of future

events. Forward-looking statements (which include the phrase ‘forward-looking information’ within the meaning of Canadian securities legislation) are provided for the purposes of assisting the reader in

understanding the Company’s financial position and results of operations as at and for the periods ended on certain dates, and to present information about management’s current expectations and plans

relating to the future. Readers are cautioned that such forward-looking statements may not be appropriate for other purposes than outlined in this presentation. These statements may include, without

limitation, statements regarding the operations, business, financial condition, expected financial results, cash flow, requirement for and terms of additional financing, performance, prospects,

opportunities, priorities, targets, goals, objectives, strategies, growth and outlook of the Company including the outlook for the markets and economies in which the Company operates, costs and timing of

acquiring new royalties, mineral reserve and resources estimates, estimates of future production, production costs and revenue, future demand for and prices of precious and base metals and other

commodities, for the current fiscal year and subsequent periods. In addition, statements relating to ‘reserves’ or ‘resources’ are forward looking statements, as they involve implied assessment, based on

certain estimates and assumptions, that the resources and reserves described can be profitably produced in the future.

Forward-looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, or include words such as ‘expects’, ‘anticipates’, ‘plans’, ‘believes’,

‘estimates’, ‘seeks’, ‘intends’, ‘targets’, ‘projects’, ‘forecasts’, or negative versions thereof and other similar expressions, or future or conditional verbs such as ‘may’, ‘will’, ‘should’, ‘would’ and ‘could’.

Forward-looking statements are based upon certain material factors that were applied in drawing a conclusion or making a forecast or projection, including assumptions and analyses made by the

Company in light of its experience and perception of historical trends, current conditions and expected future developments, as well as other factors that are believed to be appropriate in the

circumstances. The material factors and assumptions upon which such forward-looking statements are based include: the general economy is stable; local governments are stable; interest rates are

relatively stable; equity and debt markets continue to provide access to capital; the ongoing operations of the properties underlying the Company’s portfolio of royalties by the owners or operators of such

properties in a manner consistent with past practice; the accuracy of reserve and resource estimates, grades, mine life and cash cost estimates; the accuracy of public statements and disclosures made

by the owners or operators of such underlying properties; no material adverse change in the market price of the commodities that underlie the Company’s portfolio of royalties and investment interests; no

adverse development in respect of any significant property in which the Company holds a royalty or other interest; the successful completion of new development projects; the accuracy of publicly

disclosed expectations for the development of underlying properties that are not yet in production; planned expansions or other projects within the timelines anticipated and at anticipated production

levels; and title to mineral properties. Forward-looking statements are not guarantees of future performance and involve risks, uncertainties and assumptions, which could cause actual results to differ

materially from those anticipated, estimated or intended in the forward-looking statements.

By its nature, this information is subject to inherent risks and uncertainties that may be general or specific and which give rise to the possibility that expectations, forecasts, predictions, projections or

conclusions will not prove to be accurate; that assumptions may not be correct and that objectives, strategic goals and priorities will not be achieved. A variety of material factors, many of which are

beyond the Company’s control, affect the operations, performance and results of the Company, its businesses and investments, and could cause actual results to differ materially from those suggested

any forward-looking information. For additional information with respect to such risks and uncertainties, please refer to the ‘Risk Factors’ section of our most recent Annual Information Form available on

www.sedar.com and the Group’s website www.anglopacificgroup.com, and also to the ‘Principal risks and uncertainties’ section of our most recent Annual Report, which is also available on our website. If

any such risks actually occur, they could materially adversely affect the Company’s business, financial condition or results of operations. The reader is cautioned to consider these and other factors,

uncertainties and potential events carefully and not to put undue reliance on forward-looking statements.

This presentation also contains forward-looking information contained and derived from publicly available information regarding properties and mining operations owned by third parties. The Company’s

management relies upon this forward-looking information in its estimates, projections, plans, and analysis.

Although the forward-looking statements contained in this presentation are based upon what the Company believes are reasonable assumptions, there can be no assurance that actual results will be

consistent with these forward-looking statements. The forward-looking statements made in this presentation relate only to events or information as of the date on which the statements are made and,

except as specifically required by law, the Company undertakes no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or

otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

This presentation is for informational purposes only. This presentation is not a prospectus and does not constitute or form part of any offer, invitation or recommendation in respect of securities, or an

offer, invitation, recommendation to sell, or a solicitation of any offer to buy, securities.

Anglo Pacific Group PLC

• Six producing royalties in the current portfolio, compared to three producing royalties at the start of 2014

• Three royalty additions since the arrival of current management team in October 2013: Maracás, Panorama,

and, most significantly, the acquisition of the Narrabri royalty in March 2015

• Agreement for Kestrel information provides greater visibility on the expected growth in royalty income

• Challenging conditions in 2014:

• Royalty income of £3.5m (2013: £14.7m); impacted by Kestrel

• Adjusted loss of £2.8m (2013: adjusted profit of £9.2m)

• Loss after tax of £47.6m (2013: loss of £42.5m)

• Cash balance of £8.8m as at year end (2013: £15.7m)

• Net cash of £8.7m generated from non-core assets disposals in 2014

• Recommended final dividend of 4p per share, total dividend for 2014 of 8.45p (2013: 10.2p)

• Net asset value of 138p as at December 31, 2014, a significant premium to the current share price of 84.5p(1)

• Commitment to affordable and progressive dividends

• Additional mining and financial expertise added to the Board in 2014

Anglo Pacific highlights

3

(1) Closing share price at March 24, 2015

Financial ReviewKevin Flynn, CFO

4

Anglo Pacific Group PLC

Key performance indicators

5

Adjusted (loss)/earnings per share Dividend cover Royalty assets acquired

76% decline in royalty income mainly due

to production at Kestrel being outside of

the Group’s royalty land (see slide 6)

Higher costs in 2014 associated with the

recently announced Narrabri royalty

acquisition and fund raise process

Dividend cover is restricted to nil in any

year in which an adjusted loss is

reported.

Dividend per share in 2014 of 8.45p

(2013: 10.2p)

Royalty investments in 2014 reflect

the Maracás acquisition in June

(£13.2m) and the final $5m advance

to Hummingbird (£3.0m).

2015 will include the Narrabri royalty

acquisition of ~£44m

Anglo Pacific Group PLC

Income Statement

6

• Operating costs of £5.5m (2013: £3.3m) largely due to increased costs and remuneration associated with the Narrabri

royalty acquisition announced in February 2015

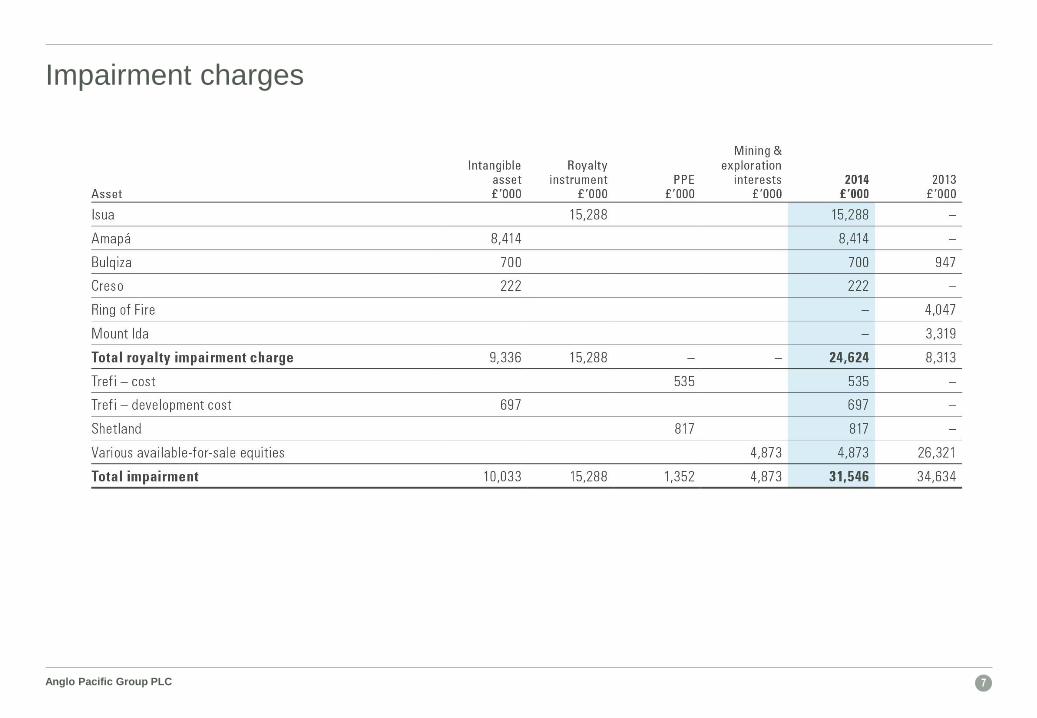

• Total impairment charges in 2014 of £31.5m (2013: £34.6m) – see slide 6 for more information

• Kestrel revaluation deficit of £11.8m (2013: £13.6m) largely due to exchange movements

• Tax charge of £5.2m (2013: credit of £10.4m)

• Loss after tax of £47.6m (2013: £42.5m)

• Adjusting for non-cash impairment and valuation items produces a loss of £2.8m (2013: profit of £9.2m)

Anglo Pacific Group PLC

Impairment charges

7

Anglo Pacific Group PLC

Balance sheet

8

• The Narrabri royalty will be accounted for as an intangible asset and included on the balance sheet at its cost (~£44m)

and amortised over the expected mine life

• Deferred tax liability largely relates to the fair value of the Kestrel royalty

• Mining and exploration interests largely relate to junior mining equities, which have largely been sold

Anglo Pacific Group PLC

Financial resources

9

• Royalty related receipts and net non-core asset disposals generated £15.0m of cash in 2014 compared to £15.3m in 2013

• Cash balance at March 23, 2015 of £3.6m following the February 2015 dividend payment, along with $24m undrawn on

the Group’s new $30m revolving credit facility (RCF)

Operational ReviewJulian Treger, CEO

10

Anglo Pacific Group PLC

Kestrel outlook

11

-

$50

$100

$150

$200

$250

Kestrel

Cumulative production (million tonnes)

Quartile 1 Quartile 2 Quartile 3 Quartile 4

Note: Please refer to endnote (i and ii)

(1) CRU as of November 2014. Business costs defined as FOB port, including all costs associated with mining and processing, transportation to port, mineral royalties, sustaining capital and interest on working capital adjusted for any realised quality premiums or discounts

(2) National Instruments 43-101 Technical Report on Kestrel Coal Mine, QLD Australia dated 30 January 2015 prepared by Golder Associates

(3) Rio Tinto Energy Roundtable, December 2014

(4) 2014 gross royalty income from Kestrel expected to be approximately £1.7m as per Anglo Pacific press release dated January 21, 2015

» First quartile global hard coking coal cost curve position (1), with

estimated average FOB cash cost of A$65/tonne to A$75/tonne (2)

» Estimated reserve-based mine life of ~18 years

» Production rate expected to reach 5.7 Mt of coal per year within

the next 12 to 18 months (4)

» 85% coking coal and 15% thermal coal (2)

» Limited exposure to china - 84% of coking coal and 86% of

thermal coal from Kestrel mine were sold to customers located in

Asia

» Anglo Pacific estimates that the Rio Tinto forecast for mining

within the Kestrel Royalty Area:

» H1 2015: approx. 20-25% of production

» H2 2015: approx. 70-75% of production

» Anglo Pacific management expects Rio Tinto to mine over 90% of

coal within Anglo Pacific’s royalty lands by 2017

Historical Kestrel Royalty Income to APG (4)

(GBP millions)

Forecast Hard Coking Coal Cost Curve Position(Business costs 2015E, US$/tonne) (1)

Switch from Kestrel North to Kestrel South

& mining largely outside of Anglo Pacific

royalty area£21.4

£26.1

£10.9 £9.9

£1.7

2010 2011 2012 2013 2014E

Anglo Pacific Group PLC

-

$50

$100

$150

$200

$250

Narrabri royalty overview

The Narrabri Mine (1)

» Located in the Gunnedah Basin, an established mining jurisdiction

in New South Wales, Australia

» Low cost underground longwall coal mine with an estimated

Reserve life of ~22 years

» FY15 Narrabri cost guidance of A$59 - $62/t (~US$48 - 51/t)(2)

» Targeting 6.5 Mt ROM in FY2015 and 7.0 Mt in FY2017

» Permitted & planned production of 8.0 Mtpa ROM

» High energy export thermal coal achieving or exceeding

Newcastle benchmark specifications. Mid volatile, low ash PCI

coal

» High quality thermal coal not expected to be impacted by

Chinese import restrictions on low quality coal

» Minimal Whitehaven exposure to China in FY15

» Limited impact from Chinese import tariffs given sales primarily

into premium markets such as Japan and Korea

Note: Whitehaven fiscal year ending 30 June

Note: ROM: run of mine

Note: Please refer to endnote (iii)

(1) National Instrument 43-101 Technical Report on Narrabri North Mine and Narrabri South, Gunnedah Basin, New South Wales dated 30 January 2015 prepared by Palaris Australia Pty Ltd

(2) Whitehaven does not disclose whether this includes government and/or privately held royalties. USD:AUD 1.2170

(3) CRU as of November 2014. Business costs defined as FOB port, including all costs associated with mining and processing, transportation to port, mineral royalties, sustaining capital and interest on working capital adjusted for any realised quality premiums or discounts

Forecast Thermal Coal Cost Curve Position(Business costs 2015E, US$/tonne) (3)

12

Cumulative production (million tonnes)

Quartile 1 Quartile 2 Quartile 3 Quartile 4

Narrabri

Narrabri

-

$50

$100

$150

Cumulative production (million tonnes)

Quartile 1 Quartile 2 Quartile 3 Quartile 4

Forecast PCI Cost Curve Position(Business costs 2015E, US$/tonne) (3)

Anglo Pacific Group PLC

£0.3

£1.8

£2.8

FY12 FY13 FY14

0.2 0.4

3.7

5.76.5 6.5 7.0

8.0

FY11A FY12A FY13A FY14A FY15F FY16F FY17F Permitted & Planned

Narrabri royalty overview (cont’d)

Product Mix (1)

(As percentage of saleable production tonnes)

Historical and Forecast Production (1)

(In million tonnes ROM, FY ending 30 June)

FY2014A Target

Note: Whitehaven fiscal year ending 30 June

Note: Please refer to endnote (iii)

(1) National Instrument 43-101 Technical Report on Narrabri North Mine and Narrabri South, Gunnedah Basin, New South Wales dated 30 January 2015 prepared by Palaris Australia Pty Ltd

(2) Whitehaven has stated that in the longer term, production is planned to reach the permitted 8.0 Mtpa level

(3) 2011 average GBP:AUD 1.5530. 2012 average GBP:AUD 1.5304. 2013 average GBP:AUD 1.6223. 9-months 2014 average GBP:AUD 1.8185

(4) Royalty receipts are presented net of GST. The royalty payor applies a GST gross-up to ensure royalty payments are free and clear of any applicable GST

Thermal coal

PCI coal

Potential to increase royalty income through

shift in product mix to higher value PCI coal

Permitted and planned production of 8 Mtpa ROM

13

Development coal only;

first longwall coal was

cut in June 2012

Whitehaven expects FY2015 production to

exceed earlier guidance of 6.5 Mt ROM

Historical Narrabri Royalty Income (3) (4)

(In GBP millions, FY ending 30 June)

Narrabri

ramp up

84.5%

15.5%

80%

20%(2)

Anglo Pacific Group PLC

(1) Based on balance sheet carrying value at December 31, 2014 and includes Narrabri at ~£44m where stated

(2) Kestrel production primarily metallurgical coal. Narrabri production split 84% thermal coal and 16% PCI coal in FY2014

(3) Gold commodity exposure includes the EVBC royalty which includes copper and silver by-products

1414

Anglo Pacific royalty portfolio Focus on royalties over high quality, low cost mines in production and located in predominantly low

risk jurisdictions

(2) & (3)

(1)

Anglo Pacific Group PLC

» Julian Treger and Mark Potter joined the company in

October 2013

» Experienced in natural resource sector

» Proven history of cash return to shareholders from

dividends

» Currently yielding 9%

» Seeking to operate with low central costs and to

increase the scale of the business

» Current Anglo Pacific team has the capacity to

manage a significantly larger royalty portfolio

» Majority of royalty companies focussed on precious

metals

» Anglo Pacific is the only royalty company listed in

London focused on bulk materials and base metals

» Portfolio of 6 producing assets, with additional earlier

stage assets, diversified for commodity and geography

» Significant production growth potential over the next 12

to 18 months with Kestrel ramping up to full capacity

» Delivering new royalties (e.g. Narrabri, Maracás,

Panorama)

» Continuing to seek and pursue new royalty

opportunities

Commitment to Being a Yield Stock

Scalability

Strong Foundation With Existing Royalty

Portfolio

Limited Competition

Conclusion

Management Team with Strong Track

Record

Royalty Acquisition Pipeline

15

Anglo Pacific Group PLC Annual Results 2013

Appendix A

Anglo Pacific Group PLC 16

Anglo Pacific Group PLC

Geographic and commodity exposure across principal royalty portfolio

9

10

8

7

6

5

4

13

2

(1) Please refer to 2014 Annual Report for further detail on the royalty type and rate for Tucano, EVBC

(2) GRR – Gross Revenue Royalty. NSR – Net Smelter Return

(3) Kestrel royalty terms (Anglo Pacific): 3.5% of value up to A$100/tonne, 6.25% of the value over A$100/tonne and up to A$150/tonne, 7.5% thereafter

(4) EVBC: El Valle-Boinás Carlés

(5) Dugbe 1 to become a royalty upon the receipt of a mining license

Royalty Description

Producing royalties Early-stage royaltiesDevelopment royalties

17

Existing Royalty Portfolio

Royalty Commodity Operator Location

Royalty type

and rate (1,2)

Pro

du

cin

g

Kestrel (3) Coking &

thermal coal Rio Tinto Australia 7 – 15% GRR

NarrabriThermal &

PCI coal

Whitehaven

CoalAustralia 1% GRR

Maracás Vanadium Largo Resources Brazil 2% NSR

Four Mile Uranium Quasar Resources Australia 1% NSR

EVBC (4)Gold, copper

and silver Orvana Minerals Spain 2.5 – 3% NSR

Amapá &

TucanoIron ore

Zamin Ferrous /

Beadell Resources Brazil 1% GRR

De

ve

l-

op

me

nt

Salamanca Uranium Berkeley Resources Spain 1% NSR

Ea

rly-s

tag

e

Pilbara Iron ore BHP Billiton Australia 1.5% GRR

Ring of Fire Chromite Cliffs Natural

Resources Canada 1% NSR

Dugbe 1 (5) Gold Hummingbird

Resources Liberia 2 – 2.5% NSR

1

2

4

5

6

7

8

9

10

3

Anglo Pacific Group PLC

Strategy for growth

18

Primary Royalties Secondary Royalties

Potential Drivers for Engaging with Anglo Pacific

» Challenging financing environment for miners

» Can be less dilutive than equity

» Less restrictive than debt

Potential Drivers for Engaging with Anglo Pacific

» Opportunity to monetize illiquid asset

» If privately held, risk can be highly concentrated

» Residual exposure possible via Anglo Pacific shares

Anglo Pacific Group PLC

Key APG royalty acquisition criteria

19

Established mining jurisdictions

Producing or near production assets

Diversified commodity exposure vs. current portfolio

Low cost operations

Long mine life

Upside potential

Narrabri Royalty

operated by

1% Gross Revenue Royalty

US$65 million

March 2015

Australia

Maracás Mine

operated by

2% NSR Royalty

US$25 million

June 2014

Brazil

Anglo Pacific Group PLC

Endnotes

20

Third party information

As a royalty holder, Anglo Pacific Group plc (“the Company”) often has limited, if any, access to non-public scientific and technical information in respect of the properties underlying its portfolio of

royalties, or such information is subject to confidentiality provisions. As such, in preparing this presentation, the Company has relied upon the public disclosures of the owners and operators of the

properties underlying its portfolio of royalties, as available at the date of this presentation.

i.This presentation contains information and statements relating to the Kestrel mine that are based on certain estimates and forecasts that have been provided to the Group by Kestrel Coal

Pty Ltd (“KCPL”), the accuracy of which KCPL does not warrant and on which readers may not rely.

ii. This presentation contains certain information relating to the Kestrel royalty which is principally derived from the National Instrument 43-101 Technical Report on Kestrel Coal Mine, QLD

Australia dated 30 January 2015 prepared by Golder Associates. This report is contained at Part 10 (Kestrel Qualified Person’s Report) of the Company’s prospectus dated 6 February 2015

(the “Prospectus”). Rio Tinto Limited, the owner of the Kestrel mine, is listed on the Australian Securities Exchange and reports in accordance with the JORC Code.

iii. This presentation contains certain information relating to the Narrabri royalty which is principally derived from the National Instrument 43-101 Technical Report on Narrabri North Mine and

Narrabri South, Gunnedah Basin, New South Wales dated 30 January 2015 prepared by Palaris Australia Pty Ltd. This report is contained at Part 11 (Narrabri Qualified Person’s Report) of

the Prospectus. Whitehaven Coal Limited, the majority owner of the Narrabri mine, is listed on the Australian Securities Exchange and reports in accordance with the JORC Code.

Standards of disclosure for mineral projects

National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) contains certain requirements relating to the use of mineral resource and mineral reserve categories of an

“acceptable foreign code” (as defined in NI 43-101) in “disclosure” (as defined in NI 43-101) made by Anglo Pacific Group plc with respect to a “mineral project” (as defined in NI 43-101), including the

requirement to include a reconciliation of any material differences between the mineral resource and mineral reserve categories used under an acceptable foreign code and the standards developed

by the Canadian Institute of Mining, Metallurgy and Petroleum, as the CIM Definition Standards on Mineral Resources and Mineral Reserves adopted by CIM Council, as amended (the “CIM

Standards”) in respect of a mineral project. Pursuant to an exemption order granted to Anglo Pacific Group plc by the Ontario Securities Commission (the “Exemption Order”), the information

contained herein with respect to the Kestrel mine, the Maracás project and the Narrabri mine has been extracted from information publicly disclosed, disseminated, filed, furnished or similarly

communicated to the public by an issuer whose securities trade on a “specified exchange” (as defined under NI 43-101) that discloses mineral reserves and mineral resources under one of the JORC

Code, the PERC Code, the SAMREC Code, SEC Industry Guide 7 or the Certification Code (each as defined in NI 43-101). As the definitions and standards of the JORC Code, the PERC Code, the

SAMREC Code, SEC Industry Guide 7 and the Certification Code are substantially similar to the CIM Standards, a reconciliation of any material differences between the mineral resource and mineral

reserve categories reported under the JORC Code, the PERC Code, the SAMREC Code, SEC Industry Guide 7 and the Certification Code, as applicable, to categories under the CIM Standards is not

included and no Form 43-101F1 technical report will be filed to support the disclosure based upon such exemption.