analyst 23-02-10 final r1 - listed...

TRANSCRIPT

Analyst Meeting2009 Performance

2009 Management Highlightsg g g

Industry Outlooks

Operation PerformanceAGENDA

CAPEX

Fi i l P f

AGENDA

Financial Performance

Key Highlightsy g g

2

IMF: “The world economy is recovering at different speeds in the various regions; policies

2009 Highlights IMF: The world economy is recovering at different speeds in the various regions; policies

need to foster a rebalancing of global demand.”.

Oil markets recovered to stabilize in a well-defined price band. The actions of producers halted the price decline and resurgent non-OECD demand, particularly China and India, bring the market back into balancethe market back into balance.

Outlook overview: Another hard year to come. Refining: Weak margin in the near term with recovery beyond 2013 Petrochemical: Industry restructuring likely & necessary

Overview

4Q09 average crude run 70%, 2009 average crude run 66%, decrease 17% from 2008 at 80% due to economic slowdown and shutdown approximately 3 weeks in 1Q09 .

Market GIM in 2009 at 7.2 $/bbl: Refinery 3.1$/bbl, Petrochemical 4.1$/bbl.

Aim to be “Top Quartile Integrated Petrochemical Complex in Asia by 2014” with refinery adherent.

Board approved USD1,412 million budget for 5-year CAPEX plan; already approved 4 newBoard approved USD1,412 million budget for 5 year CAPEX plan; already approved 4 new projects with USD 135 million CAPEX on 22 December 2009

Cost reduction program, 2009 cost reduced by USD 65.5 million or 1.26 $/bbl.

Initiate “IRON”, IRPC Oil on Net, the first Asean online system for petrochemical and Operation

Expected dividend in 2009 is 0 18 baht/share or 4 3% dividend yield 2009 interim dividend

petroleum trading

Obtaining 5-star 2009 Excellent Corporate Governance Award

3

Expected dividend in 2009 is 0.18 baht/share or 4.3% dividend yield, 2009 interim dividend 0.08 baht/share already paid in September 2009

Total ESOP exercised until December 2009 was executed only 2.05% of total shares. Finance

Industry OutlooksIndustry Outlooks

4

World Economics: Back to Normal

ChinaIndia

Thailand

USAJapan

Asia is still the main driver of global economic recovery

Source: IMF, Oct 09 ; Morgan Stanley Research, Sep 09 ; Viewswire IEU, Aug 09 ; PTT Group Assumption, Aug 09 5

World Oil Demand2009 2010

Change

Md/dGrowth % yoy

Avg. Supply 84.3 86.3 2 2.3788

Mbpd

Avg

Avg. Demand 84.08 84.9 0.82 0.97

87.4

86.186

87

Avg. Supply

86.186

85.5

85

86.3

85.8

85

86

Avg. Demand

84.384.2

84.03

84.75 84.984.93

84

84.78

84.0884

83

823Q09e 4Q09 Y09 1Q10 2Q10 3Q10 4Q10 Y10

OPEC IEA PIRA KBC

6Source: PIRA, Aug 09

Refining Capacity Additions

2500

World Capacity Additions and Petroleum Demand Growth,Thousand Barrels per Day

1500

2000

0

500

1000

-1000

-500

0

Reliance-India 580 KBDCNOOC-China 240 KBD

Petrochina 200 KBDIndia 290 KBD

Essar Oil-India 110 KBDKochi Ref.India 125 KBD

Sinopec 250 KBD CNPC 200 KBD

Saudi Aramco 400 KBDIndia 180 KBD

-2000

-1500Dung Quat-Viet 140 KBD Sinopec 150 KBD

Marathon-USA 180 KBDPemex-Mexico 150 KBD

Nagarjuna-India 125 KBDPersan-Iran 120 KBDSinopec 100 KBD

Petrobras 150 KBD

-25002009 2010 2011 2012 2013

Demand Growth Refinery Capacity Additions

7Source: Purvin & Gertz, Sep 09

2010 Crude Oil Outlook: Average 75-80 $/bbl

Refinery operating rates remain low for Q1/2010 with finventories of middle distillate built-up worldwide remaining

high. Constraining naphtha and aromatics supply, forcing

refineries run at low rates.

8

Refining Outlook: Still under heavy pressureApparent refinery capacity surplus / deficit1, AsiaKbpd, 1990-2015F

Singapore margins2

USD/bbl10

Complex

6

8

Simple

2

4

-2

0

-4

-6

1. Refining capacity minus total oil demand2 Historical margin for 1990-2008 from British Petroleum, margin forecast for 2009 and beyond from FACTS

Gl b l E

1990 20001995 2005 2010 2014

9

Global Energy

Source: MGI; BP Statistical Review of World Energy; Platts; FACTS Global Energy; Team analysis

Operating ratio: %MT

World Ethylene Balance and Operating RateOperating ratio: %MT

Capacity

World Operate

Operate in US

Operate

O i A i

Operate in US

DemandOperate in Asia

No new Ethylene Plant in U.S.A. and Europe Asian Operating rate will go down sharply due to start-up of New Plants in M-East & China After 2010, Operating rate in Asia will rise Expansion of Operating rate in the world as same direction as Asia

10

Expansion of Operating rate in the world as same direction as Asia

Source: The World Outlook Petrochemical, Mitsubishi Corporation Sep 09

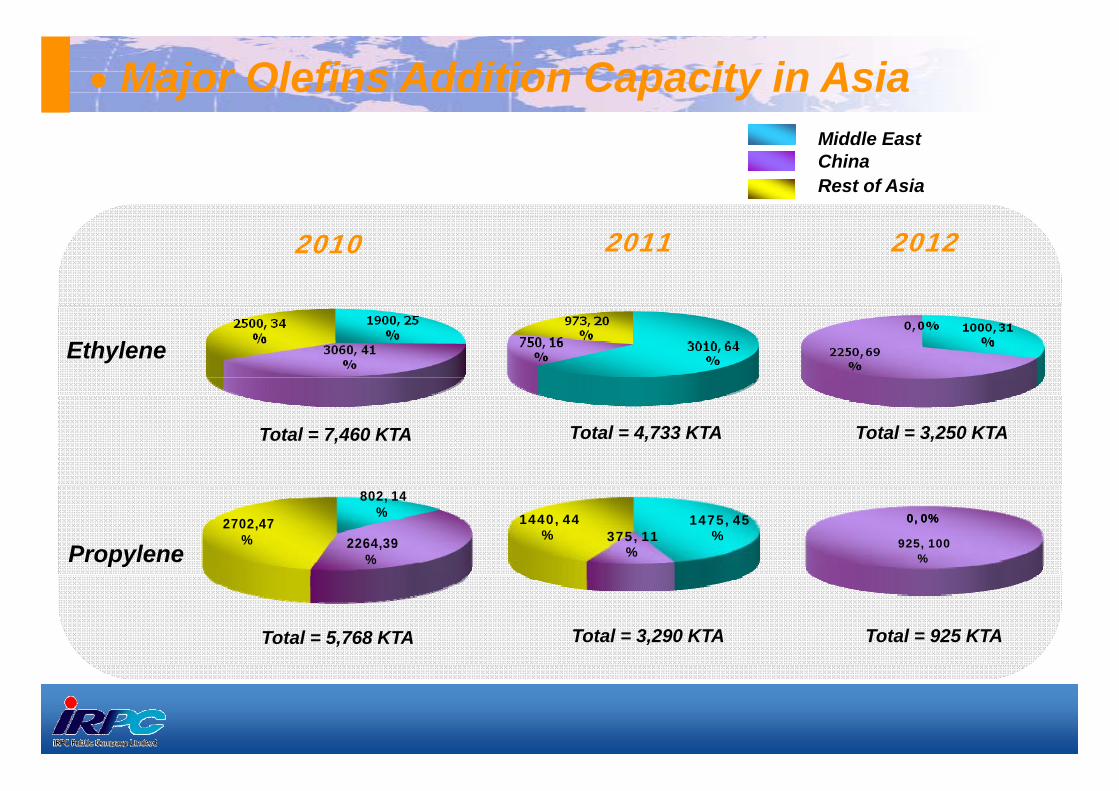

Major Olefins Addition Capacity in AsiaMiddle EastChinaRest of Asia

2010 2011 2012

Ethylene

Total = 7,460 KTA Total = 4,733 KTA Total = 3,250 KTA

Propylene

802, 14%

2264,39%

2702,47%

0, 0%

925, 100%

0, 0%1475, 45%375, 11

%

1440, 44%

Total = 5,768 KTA Total = 3,290 KTA Total = 925 KTA

11

Petrochemical Price: Sustainable

Olefins and Polyolefin price tend to reduce start in 2Q from new startup

l b t 10 000 KTA Eth l fplan about 10,000 KTA Ethylene from 8 new crackers (3 in ME, 2 in China, 1 in India, 1 in Singapore and 2 in Thailand))

2009 Aromatics price was better than expected and gradually increased to p g ythe beginning of 2010 supported by high energy price and supply constraint from refinery cut run.

The market could be driven by 2 big events in China, Shanghai China EXPO i 1 M 31 O t 2010 dEXPO in 1 May - 31 Oct 2010 and Asian Game in 12 - 27 Nov 2010.

12

China Petrochemical Balance (as Ethylene Equivalent Basis)

China Supportive of Chemical

& S

Massive new Integrated investments in 2008 2011

Demand & Supply

Integrated investments in 2008-20116.3 MMT Ethylene ; +63%5.3 MMT Propylene ; +57%4.6 MMT Benzene ; +80%4.4 MMT Paraxylene ; +109%

Still not self-sufficient for most chemicals, but import needs are not growing as fast (reducing) after 2010, The Negative Balance will be 0 0, e egat e a a ce besmaller due to self-sufficiency rate grown up

Economic stimulus package will support chemical investment andsupport chemical investment and consumer demand

Coal chemistry is a viable option

13Source: World petrochemical conference, CMAI Mar 09; The World Outlook Petrochemical, Mitsubishi corporation Sep 09

Global Recession Effects to the Earning Level

The earning up-cycle was in full between 2004 - 2008 : Extremely tight markets

The current recession will force global average profits to very low levels through 2010 : levels necessary to Encourage rationalization as newthrough 2010 : levels necessary to Encourage rationalization as new,low cost production enters

Reinvestment level earning will not be reached until 2013 despite thesignificant addition of very low cost production “The New Gulf” capacity

14Source: World petrochemical conference, CMAI Mar 09

Petroleum Outlook Summary

Global refined product demand growth is from Asia Pacific 55% and MiddleEast 20%. In 2010-13 additional demand is approximately 4,600 KBD while newsupply is about 5 600 KBD in the same periodsupply is about 5,600 KBD in the same period.

With so much excess capacity assessed refineries vulnerable for With so much excess capacity, assessed refineries vulnerable forshutdown: about 3.6 MMB/D of refining capacity needs to be rationalized

Singapore margins forecast to be weak in the near term with recoverybeyond 2013

15

Petrochemical Outlook Summary

Global demand loss is largest concern of current market; global demand willrecover with economy by 2010, returning to trend-line patternsy y g p

Over-capacity still looms despite demand recovery, causing margins to under perform expectations until next up cycle.perform expectations until next up cycle.

“Asia” investments chasing local demand recovery, while “Middle East” i i i i i i k i h l f d kinvestments mitigating margin risk with low-cost feedstock

Industry restructuring likely & necessary Industry restructuring likely & necessary- 2009 recovery in margins is temporary- Low margins expose marginal performers with high debt loads- Capacity closures of old/inefficient facilities will occur- Financing difficulties for marginal projects will delay start-ups for 2012+g g p j y p- Cost reduction becomes critical for competitiveness

16

OperationP fPerformance

17

Capacity Utilization

200

2007 Crude run 2008 Crude run 2009 Crude run2007 % utilization 2008 % utilization 2009 % utilization

KBD

86% 89%85% 85% 90% 89% 89% 89% 83% 87% 91% 93% 88%

82% 85% 83% 88% 79% 66%76%

78% 73% 74% 80%

73% 70% 70% 71% 68% 68% 78%68% 75%

67% 66%50%60%70%80%90%100%

80100120140160180200

Refinery Capacity

Utilization

86% 85%

51%29%

0%10%20%30%40%

020406080

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Y AVGJAN FEB MAR APR MAY JUN. JUL. AUG. SEP. OCT. NOV. DEC. Y. AVG.

2007 1Q08 2Q08 3Q08 4Q08 2008 1Q09 2Q09 3Q09 4Q09 2009% Utilization 88% 84% 85% 74% 75% 80% 52% 71% 71% 70% 66%

Utilization 2007 (LHS) Utilization 2008 (LHS) Utilization 2009 (LHS)

Petrochemical and Lube 100

120140160

500600700800

%Utilization 2007(RHS) %Utilization 2008(RHS) %Utilization 2009(RHS)

and Lube

020406080

0100200300400

18

00

2009 GRM & PTF

6Lube

Gross Refinery Margin$/BBL. MKT GRM A/C GRM$/BBL.

$/BBL

Gross Integrated MarginMKT GIM

2 1 2 0

2.5 1.7 2.01.8

3.9

0.9

3.9 4.03.1

1

2

3

4

5Refined

7.7 8.1 7 5 7 2810121416

PetchemRef ined

1.4-0.4

2.1 2.0 1.31.3

-1

0

1

3.90.9

3.9 4.0 3.1

3.8

4.7

4.2 3.5 4.1

7.75.6

7.5 7.2

02468

Product to Feed$/Ton MKT PTF A/C PTF$/Ton

01Q09 2Q09 3Q09 4Q09 2009

16

$/BBL A/C GIM

122

192 12679 130

92

149138

113123

150200250300350

StyrenicsOlefin

$ $

4.4 5.2

10.4 10.79.7

8.89.9

810121416 Petchem

Refined

78 129 144 129 120

122

050

100150

6.0 5.5 4.0 4.4 4.9

4.4 5.25.7 4.4 5.0

02468

19Note: Based on Production

01Q09 2Q09 3Q09 4Q09 2009

2009 Product Sales Value by Market

100%40,390 47,142 51,001 241,782

1% 1% 2% 1% 2%100%Unit:M.Baht Unit:M.Baht

Sales Proportion 244,694 166,036

Total Products Sales: Local vs Export47,873 163,33140,969 51,792

45%34% 35% 38% 34%

40%50%60%70%80%90%

75% 72% 75% 74% 72%

23% 27% 23% 25% 27%

40%50%60%70%80%90%

55%66% 65% 62% 66%

0%10%20%30%40%

4Q08 3Q09 4Q09 2008 2009

75% 72% 74% 72%

0%10%20%30%40%

4Q08 3Q09 4Q09 2008 2009

Petroleum Petrochemical Others

Unit:M Baht U it M B ht

Domestic Export

Oil products: Local vs Export Petrochemical products: Local vs Export

45%33% 34% 38% 33%

%70%80%90%

100%

43% 36% 37% 37% 36%

60%70%80%90%

100%

30,858 34,281Unit:M.Baht

9,532 12,861 12,158 Unit:M.Baht180,294 118,819 61,488 44,51238,843

55%67% 66% 62% 67%

10%20%30%40%50%60%

57% 64% 63% 63% 64%

10%20%30%40%50%60%

0%

4Q08 3Q09 4Q09 2008 2009Domestic Export

20

0%4Q08 3Q09 4Q09 2008 2009

ExportDomestic

2009 Petroleum Product Sales6 0 4

1,2004Q08 3Q09 4Q09

4 000

4,5002008 2009

M. Liters M. Liters Volume: M.Liters

1016

352

3

870

3 266

1

994

5

334

7

400

600

800

1,000

4,0

08

3,3

72

1 500

2,000

2,500

3,000

3,500

4,000

184

125

81

233

25

101

94

201

23 3

81

97 207

0

200

400

Diesel Mogas ATB/LR Naphtha Lube Others

718

1,3

50

422

379

849

833

1,0

32

287

380

780

0

500

1,000

1,500

Diesel Mogas ATB/LR Naphtha Lube Othersg / p

6

25,000

M. Baht

120,000

M. Baht Value: M.Baht

17,1

49

17,0

5 6

20,3

54

15,000

20,000 4Q08 3Q09 4Q09

105,6

44

60,000

80,000

100,000

2008 2009

2,93

5

738

,013

198

,825

6,72

6

3,76

8

,643

2,22

5

2,86

26,25

1

060

,441

2,50

8

3,22

9 5,000

10,000

18,4

31

22,2

48

8,5

10

12,8

35

12,6

276

1,5

71

20,2

17

13,6

46

4,5

33

8,5

58

10,3

02

20,000

40,000

21

3, 1 3, 23 1 2 25, 1 2 3

0

Diesel Mogas ATB/LR Naphtha Lube Others

22

0

Diesel Mogas ATB/LR Naphtha Lube Others

2009 Petrochemical Product Sales

100 000

120,000 4Q08 3Q09 4Q09

1 0400,000

450,0002008 2009

Tons Tons Volume: M.Tons

93,4

19

,589

109,

519

828 10

3,30

6

9,05

0 60,000

80,000

100,000

419,

771

11 03,5

00

2

408,

320

9 280

2

200,000

250,000

300,000

350,000

31,2

70

16,5

07

41,3

87

34,8

11 68

,

17,4

09

36,4

28

27,5

24

39,3

34

50,5

47

60,

16,7

64

38,4

28

23,6

76

40,1

59

45,6

33

5 9

14,2

16

-

20,000

40,000

HDPE CD1 ABS PP PS EPS Ol fi BTX Oth

140,

750

86,0

78

142,

559

191,

7 3 0

81,7

87153,

852

100,

590

145,

791

201,

789

234,

2

55,2

42

0

50,000

100,000

150,000

HDPE CD1 ABS PP PS EPS Ol fi BTX OthHDPE,CD1 ABS PP PS,EPS Olefin BTX Others HDPE,CD1 ABS PP PS,EPS Olefin BTX Others

5,000 4Q08 3Q09 4Q0925,000

M.Baht M.BahtValue: M.Baht

3,22

0

4,67

723

5 2,500 3,000 3,500 4,000 4,500

1

20,9

80

5,94

115,000

20,000 2008 2009

1,09

4

954

1,46

5 916

1,33

5

547

1,56

9

1,36

4

1,55

3

1,67

7

1,58

6 436

1,60

1

1,24

5

4,2

1,60

7

1,59

3

1,53

8

339

500 1,000 1,500 2,000

,

7,01

1

5,37

1

6,59

3

8,91

6

9,44

2

3,17

7

5,88

0

4,75

9

1 5

5,33

7

5,55

3

5,69

0

1,35

3

0

5,000

10,000

22

-

HDPE,CD1 ABS PP PS,EPS Olefin BTX Others

0

HDPE,CD1 ABS PP PS,EPS Olefin BTX Others

CAPEXCAPEX

23

2007-2012 Projects: Progress

As of December CAPEX Start Complete Progress

CHP Project

As of December 2009

CAPEX Amount

(Million USD)

Start Complete Progress

Phase I

Power Plant * 220 2Q07 1Q11 55%

Safety Improvement 39 2Q07 2011 49%

Total 259

Phase IIABS/SAN Expansion * 78 1Q10 1Q13

High voltage switch gear

New Reg_EURO IV n/a

Propylene Booster * 88 2009 2011

Total 166

Progressing

Grand Total 425

* Note: Projects financed by THB 10 000 local bank term loan

24

Note: Projects financed by THB 10,000 local bank term loan

Demineral water plant - Equipment

Financial P fFinancial Performance

25

Financial HighlightsUnit: Million Baht 4Q09 4Q08 %YoY 3Q09 %QoQ 2009 2008 %YoYSales 51,792 40,969 26.4% 47,874 8.2% 166,036 244,694 -32.1%Net Sales 46,329 39,682 16.8% 42,595 8.8% 149,747 237,319 -36.9%Cost of Goods Sold (44,384) (57,195) (22.4) (38,711) 14.7 (141,657) (242,294) (41.5) Cost of Goods Sold (44,384) (57,195) (22.4) (38,711) 14.7 (141,657) (242,294) (41.5) Gross Profit 1,945 (17,513) 111.1% 3,884 -49.9% 8,090 (4,974) 262.6%Gross Margin 4.2% -44.1% 9.1% 5.4% -2.1%Other Revenue (12) 548 35 107 1,253 SG&A (1,232) (1,594) -22.7% (827) 48.9% (3,514) (4,468) -21.3%EBITDA before LCM 701 (18,558) 103.8% 3,092 -77.3% 4,683 (8,189) 157.2%EBITDA Margin 1.5% -46.8% 7.3% 3.1% -3.5%LCM 34 (416) 34 5,045 (5,045) EBITDA after LCM 735 (18,974) 103.9% 3,126 -76.5% 9,728 (13,234) 173.5%Depre & Amort (851) (784) (855) (3 336) (3 224)Depre. & Amort. (851) (784) (855) (3,336) (3,224) EBIT (116) (19,758) 99.4% 2,271 -105.1% 6,392 (16,458) 138.8%Net Financial Expenses (296) (349) (323) (1,280) (1,235) Pretax Profit (411) (20,107) 98.0% 1,948 -121.1% 5,112 (17,693) 128.9%Taxes 4 7 (23) (51) (41) ( ) ( ) ( )Net Profit before Extra. (407) (20,100) 98.0% 1,925 -121.2% 5,061 (17,734) 128.5%Doubtful Account (7) 19 (5) (0) (25) FX. Gain/(Loss), Swap (149) (210) 169 (188.2) 263 514 (48.9) Investment Gain (Loss) (106) (341) 210 357 (1,154) Asset Gain (Loss) (258) 49 3 (256) 148Asset Gain (Loss) (258) 49 3 (256) 148 Other Expenses (1) (1) (2) (9) (12) Net Profit (928) (20,585) 95.5% 2,300 -140.4% 5,416 (18,262) 129.7%No. Share (M.) 19,829 19,706 19,719 19,829 19,706 Norm. EPS (0.02) (1.02) 0.10 0.26 (0.90) EPS (0 05) (1 04) 0 12 0 27 (0 93)

26

EPS (0.05) (1.04) 0.12 0.27 (0.93) BV 3.63 3.51 3.67 3.63 3.51

Balance Sheet:

Cash &133,175 Unit: Million Baht

Interest Bearing Debt

Cash & S/T Investment 114,194

104,112

Other LiabilitiesOther Assets

EquitiesPP & E

Treasury policy :

Net Debt/Equity < 1.0x

N t D bt/EBITDA < 2 0

Current Status

= 0.31x

2 26

27

Net Debt/EBITDA < 2.0x = 2.26x

Note: EBITDA after LCM

Key Financial Ratios

4Q09 4Q08 3Q09 2009 2008

Liquidity & Leverage Ratio (Times)Quick Ratio 1.18 1.43 0.86 1.18 1.43 Total IBD / Equity 0.39 0.38 0.37 0.39 0.38 Net IBD / Equity 0.31 0.25 0.26 0.31 0.25 Liabilities / Equity 0.59 0.50 0.62 0.59 0.50 Net IBD / EBITDA 2.26 N/A 1.59 2.26 N/AIBD / EBITDA 2 86 N/A 2 21 2 86 N/AIBD / EBITDA 2.86 N/A 2.21 2.86 N/AEBITDA / Interest Exp. 2.33 N/A 9.65 7.23 N/A

Profitability RatioyGross Profit Margin 4.2% N/A 9.1% 5.4% N/AEBITDA Margin 1.5% N/A 7.3% 3.1% N/ANet Profit Margin N/A N/A 5.4% 3.6% N/AROE 10 0% N/A 11 % 10 0% N/AROE 10.0% N/A 11.7% 10.0% N/AROCE 7.2% N/A 8.5% 7.2% N/A

28Note: EBITDA after LCM

Key Hi hli htKey Highlights

29

Phoenix Site Map:HDPE

140 KTAPP

475 KTA

Ethylene Plant596 KTA

HDPE/PPCatalyst

HDPE140 KTA

#17#5

#1GRIFFIN

#6

#7

#3

ABS/SAN96 KTA

CD157 KTA

475 KTA596 KTA

POLYOL25 KTA

PORT & TANK

#1096 KTA

PS100 KTA

BTX 600 KTA

EBSM200 KTA

61 KTA

60 KTA#4 REAL ESTATE

#12

#11

EPS30 KTA

CCM19 KTA

60 KTA

Clean Diesel/ G li

#9

REAL ESTATE

#13

#14

DCCGasoline

PE Expansion(UHMWHDPE or Multimodal)

DCC/ PP /

#3

#2

#14

#15

#16

LUBE33 KBD VAM /

VAM Derivatives

CPP PP DerivativesLUBE

33 KBD#18

TRADING

#8

30

Power PlantPower 108 MWSteam 200 MT #19

Initiatives & Impacts

Petrochem Petroleum Port & Tank Real Estate & Services

Operational Efficiency Improvement

Liquid Port Efficiency & Safety

Petrochem Operation & Energy Efficiency

Petroleum Operation & Energy Efficiency Supply Chain Optimization

21

Asset Utilization Enhancement

IRPC Green Industrial Build & Sustain

Ethylene Specialty Development

Optimization Inventory Optimization Maximize Tank

Efficiency & Utilization

3

Enhancement

Product & Services

Build & Sustain Rayong Land Develop Jana for the South

HDPE, PE, PP Catalyst Commercialization Trading

Lube Group 1 Specialty Products Focus P t l Q lit

Dry Port Commercialization

Improvement Petroleum Quality improvement to EURO IV standard

Professionalize M&E Service Offerings

Ethylene Specialty Development EBSM Upgrading for ABS Specialty

4

Capacity & Products Expansion

for ABS Specialty Vinyl Acetate Monomer (VAM)

1 201431

2010 2014Approved projects

2010-2014 CAPEX Plan

ProjectTotal

CAPEX (M$)

2010 2011 2012 2013 2014Total 2010

-2014

EBIT/Yr (M$)

Completion2014

CAPEX Phase I & IIPower Plant 220 113 34 147 39 1Q11

ABS/San Expansion 70 5 40 20 5 70 12 1Q13ABS/San Expansion 70 5 40 20 5 70 12 1Q13

Propylene Booster 88 34 44 78 25 4Q11

Total 378 152 118 20 5 295

Phoenix ProjectsPhoenix ProjectsPetrochem Operational & Energy Efficiency

44 7 14 9 14 44 27 4Q13

Petroleum Operational & E Effi i (Ph I)

25 4 13 6 1 1 25 29 3Q14Energy Efficiency (Phase I)

Maximize Tank Efficiency & Utilization

9 9 9 15 4Q10

EBSM Upgrading for ABS 57 14 21 16 6 57 17 3Q13pg gSpecialties

Total 135 34 48 31 21 1 135 88

Under studying Projects 1,207 143 352 364 344 4 1,207

32

Grand Total 1,342 177 400 395 365 5 1,342

Total CAPEX 1,720 329 518 415 370 5 1,637

Transformation Roadmap

Top Quartile Integrated Petrochemical Complex in Asia by 2014

2015 onwards

2011-2014

2010-2011 “Investment for utilization and

“Growth and expansion”

“Operational Excellence”

utilization and growth of existing businesses”

• Invest in new energy and petrochemical related businesses in

• Increase efficiency• Improve optimization• Effective procurement

• Debottleneck assets• Invest to commercialize

more• Invest in petrochemical

relevant/ transferable capabilities

• Effective procurement pfacilities

33

Investor Relations Contact : [email protected]. 02-649-7384-8, Fax. 02-649-7379

presentation is available atpresentation is available atwww.irpc.co.th

Click “Presentations”This presentation material has been prepared solely for informational purposes only. IRPC is furnishing it solely for use by prospective investors / analysts in the proposed event. IRPC makes no representations or warranties as to the accuracy or completeness of such information. By accepting this material each recipient agrees that IRPC shall not have any liability for any representations (express or implied) contained in, or for any omissions from this presentation.

The information contained herein does not purport to be all-inclusive or to contain all of the Information that may be material to the recipient’s decision. Each recipient of the information and data contained herein should perform its own independent investigation and analysis of the transaction and the

34

recipient of the information and data contained herein should perform its own independent investigation and analysis of the transaction and the creditworthiness of IRPC . Reference in this Disclaimer to this shall include references to the Appendices (if any) hereto.