analysis on mcb

TRANSCRIPT

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 1/37

CHAPTER # 3 ANALYSIS OF ORGANIZATION

FINANCIAL ANALYSIS FOR MCB PAKISTAN

Financial analysis is the process of identifying the financial strengths

and weakness of the firm by properly establishing relation ship between the items

of balance sheet and profit and loss account.

The management and interested parties use analytical tools to

evaluate the business financial health in order to make rational decisions. Here the

financial analysis is carried out to know the financial position of MCB Pakistan

with the help of the following tools

• Hori!ontal "nalysis

• #atio "nalysis

• $%&T "nalysis

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 2/37

MCB Bank Limited

Balane S!eet

"$ "% "&ASSETS 'R()ee* in +

Cash ' balances with treasury ()*+,(*,,( ()*+(-*-/ (,*0*,-

Balances with other banks (*,1*2-) 0*10(*-11 +*11)*))(

3ending to financial institutions -*12-*(/ 0*-11*1) (*111*111

4nvestments5net --(*1,)*/+- )+*/2+*,0 -+*-(0*0+2

"dvances5net /-,*)+1*2), /+/*2-1*01 /2(*/0)*01

&perating fi6ed assets -+*1/0*-/( -/+(*(( -,*1-0*,)+

7eferred ta6 assets 5 5 5

&ther assets5net -*,+,*+- -)*,-1*0+ /(*101*1)2

Total "ssets 0-1*0,2*2- 00(*+-2*)10 21)*//(*/

Bills payable -1*0)*12, -1*22-*0+, ,*/1-*1)1

Borrowings ()*01+*,(- //*++(*,01 00*++/*1,,

7eposits ' other accounts /)/*1),*1++ ((1*/0*-22 (+*+10*--

$ub5ordinated loan 0)*/(/ 5 5

3iabilities against assets sub8ect to financelease

5 5 5

7eferred ta6 liabilities5net -*-,1*-+/ 0(*-( (*-)+*0(

&ther liabilities --*//*0)( /-*/2(*/21 -2*,-)*1,/

Total 3iabilities (22*(+2*,0/ (,2*-)*,21 0()*0,(*-0

NET ASSETS ,,-..&-/$,

000000000000000

,%-13/-,1

0000000000000

/&-$1-.3

00000000000000

$hare ca pital +*/,/*+, +*/,/*+, +*)--*102

#eserves (0*111*+(, (+*+,*+2 (,*(,2*+1

9n5appropriate profit 2*-(1*21 )*-)(*((/ -2*)*-/

02*0-0*-2+ 2/*/00*,+2 +-*12*)(/

$urplus on revaluation of assets5net of ta6 )*12*2-) +*-)-*-,) ,*++0*1,-

,,-..&-/$,

00000000000000

,%-13/-,1

0000000000000

/&-$1-.3

00000000000

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 3/37

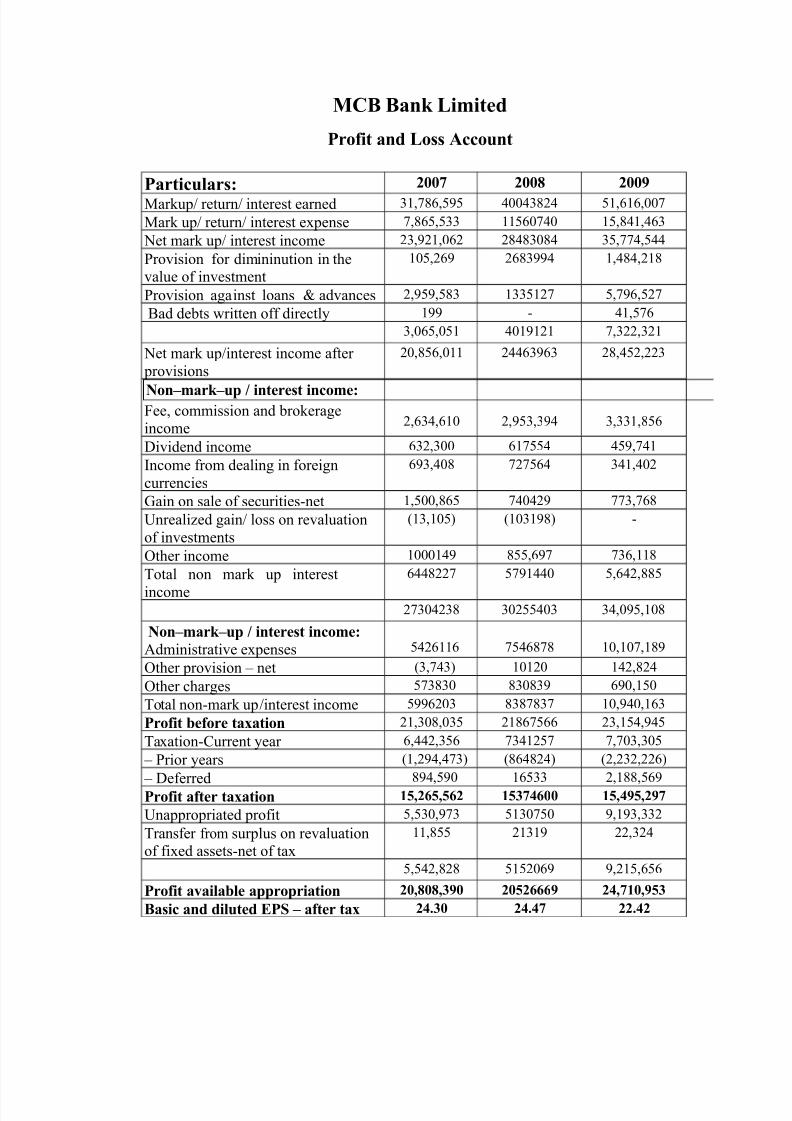

MCB Bank Limited

P24it and L** A(nt

Pa2ti(la2*5 "$ "% "&

Markup: return: interest earned (-*,+*2)2 0110(,/0 2-*+-+*11

Mark up: return: interest e6pense *,+2*2(( --2+101 -2*,0-*0+(

;et mark up: interest income /(*)/-*1+/ /,0,(1,0 (2*0*200

Provision for dimininution in thevalue of investment

-12*/+) /+,())0 -*0,0*/-,

Provision against loans ' advances /*)2)*2,( -((2-/ 2*)+*2/

Bad debts written off directly -)) 5 0-*2+

(*1+2*12- 01-)-/- *(//*(/-

;et mark up:interest income after provisions

/1*,2+*1-- /00+()+( /,*02/*//(

Nn6ma2k6() 7 inte2e*t inme5Fee* commission and brokerageincome

/*+(0*+-1 /*)2(*()0 (*((-*,2+

7ividend income +(/*(11 +-220 02)*0-

4ncome from dealing in foreigncurrencies

+)(*01, /2+0 (0-*01/

<ain on sale of securities5net -*211*,+2 010/) (*+,

9nreali!ed gain: loss on revaluationof investments

=-(*-12> =-1(-),> 5

&ther income -111-0) ,22*+) (+*--,

Total non mark up interest

income

+00,// 2)-001 2*+0/*,,2

/(10/(, (1/2201( (0*1)2*-1,

Nn6ma2k6() 7 inte2e*t inme5

"dministrative e6penses 20/+--+ 20+,, -1*-1*-,)

&ther provision ? net =(*0(> -1-/1 -0/*,/0

&ther charges 2(,(1 ,(1,() +)1*-21

Total non5mark up:interest income 2))+/1( ,(,,( -1*)01*-+(

P24it 8e42e ta9atin /-*(1,*1(2 /-,+2++ /(*-20*)02

Ta6ation5Current year +*00/*(2+ (0-/2 *1(*(12

? Prior years =-*/)0*0(> =,+0,/0> =/*/(/*//+>

? 7eferred,)0*2)1 -+2(( /*-,,*2+)

P24it a4te2 ta9atin .,-"/,-,/" .,3$1/ .,-1&,-"&$

9nappropriated profit 2*2(1*)( 2-(121 )*-)(*((/

Transfer from surplus on revaluationof fi6ed assets5net of ta6

--*,22 /-(-) //*(/0

2*20/*,/, 2-2/1+) )*/-2*+2+

P24it a:aila8le a))2)2iatin "-%%-3& ","///& "1-$.-&,3

Ba*i and dil(ted EPS 6 a4te2 ta9 "1;3 "1;1$ "";1"

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 4/37

HORIZONTAL ANALYSIS FOR MCB PAKISTAN5

Hori!ontal analysis is conducted by setting consecutive balance sheet*

income statement or statement of cash flow side5by5side and reviewing changes in

individual categories on a year5to5year or multiyear basis.

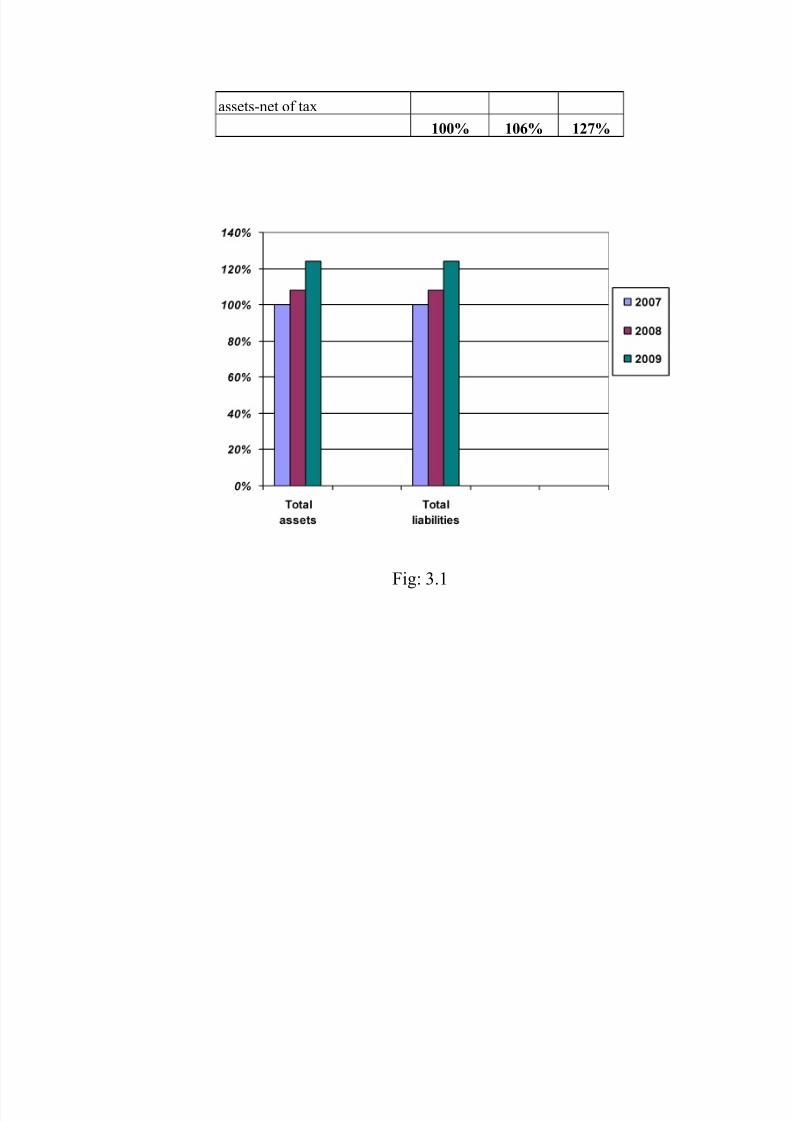

.+ H2i<ntal anal=*i* 42 8alane *!eet 4 MCB Paki*tan5

The hori!ontal analysis for three years balance sheet of MCB Pakistan is given

below

Pa2ti(la2* "$ "% "&

ASSETS5

Balances with other banks -11@ -1+@ -2@3ending to financial

institutions

-11@ ()1@ /,2@

4nvestments5net -11@ ,2@ -0@

"dvances5net -11@ -/1@ --2@

&perating fi6ed assets -11@ -1@ --/@

7eferred ta6 assets -11@ 5 5

&ther assets5net -11@ ---@ -/)@

Ttal A**et*5 .> .%> ."1>

Bills payable -11@ -11@ ,@

Borrowings -11@ 2@ --(@

7eposits ' other accounts -11@ --(@ -/2@

$ub5ordinated loan -11@ 5 5

3iabilities against assets

sub8ect to finance lease

5 5 5

7eferred ta6 liabilities5net -11@ (@ /1@

&ther liabilities -11@ -,-@ -(0@

Ttal Lia8ilitie*5 .> .%> ."1>NET ASSETS .> ./> ."$>

$hare capital -11@ -11@ --1@

#eserves -11@ -1,@ --(@

4nappropriate profit -11@ -)@ (1@

-11@ --2@ -(@

$urplus or revaluation of -11@ +(@ ,)@

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 5/37

assets5net of ta6

.> ./> ."$>

Fig (.-

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 6/37

Fig (./

INTERPRETATION5

The hori!ontal analysis of the balance sheet of the MCB bank has given a

positive trend .The result of the balance sheet depict that there is a constant increasing

trend in cash* total assets* total liability and eAuity. There is high trend in /11) in most of

factors of balance sheet as compared to /11. The trend of cash is upward and has

increased by )@ in comparison to /11. The total assets have also increased by /0@*

total liabilities have increased by ,@ and Auity is increased by //(@.

The trend of advances5net and deposits are increased positively with --2@

and -/2@ respectively in /11). "ccording to a survey* large si!e banks of Pakistan

registered a deposit growth of --./(@ =#s. /*),2.- billion> in /11) as compared to -+.)@

in /11, =#s. /*+,(.) billion>. "dvances of large si!e banks increased by /(.2@ in /11) ascompared to -).,@ in /11,. "s these large banks include MCB as well* this means that

MCB is in line with industry growth in deposits and advances. This increasing trend in

deposits and advances is a positive sign for the success of the bank.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 7/37

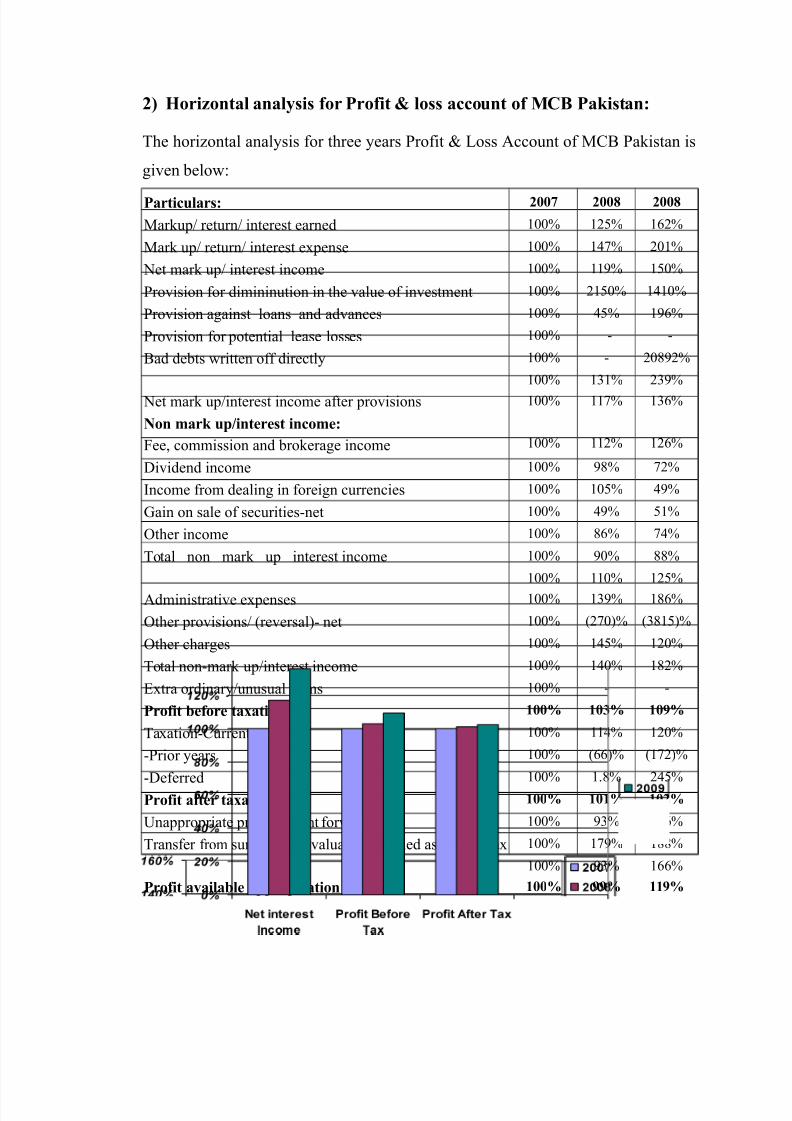

"+ H2i<ntal anal=*i* 42 P24it ? l** a(nt 4 MCB Paki*tan5

The hori!ontal analysis for three years Profit ' 3oss "ccount of MCB Pakistan is

given below

Pa2ti(la2*5 "$ "% "%

Markup: return: interest earned -11@ -/2@ -+/@

Mark up: return: interest e6pense -11@ -0@ /1-@

;et mark up: interest income -11@ --)@ -21@

Provision for dimininution in the value of investment -11@ /-21@ -0-1@

Provision against loans and advances -11@ 02@ -)+@

Provision for potential lease losses -11@ 5 5

Bad debts written off directly -11@ 5 /1,)/@

-11@ -(-@ /()@

;et mark up:interest income after provisions -11@ --@ -(+@

Nn ma2k ()7inte2e*t inme5

Fee* commission and brokerage income -11@ --/@ -/+@

7ividend income -11@ ),@ /@

4ncome from dealing in foreign currencies -11@ -12@ 0)@

<ain on sale of securities5net -11@ 0)@ 2-@

&ther income -11@ ,+@ 0@

Total non mark up interest income -11@ )1@ ,,@

-11@ --1@ -/2@

"dministrative e6penses -11@ -()@ -,+@

&ther provisions: =reversal>5 net -11@ =/1>@ =(,-2>@

&ther charges -11@ -02@ -/1@

Total non5mark up:interest income -11@ -01@ -,/@

6tra ordinary:unusual items -11@ 5 5

P24it 8e42e ta9atin .> .3> .&>

Ta6ation5Current year -11@ --0@ -/1@

5Prior years -11@ =++>@ =-/>@

57eferred-11@ -.,@ /02@

P24it a4te2 ta9atin .> ..> .">

9nappropriate profit brought forward -11@ )(@ -++@

Transfer from surplus on revaluation of fi6ed assets5net ta6 -11@ -)@ -,,@

-11@ )(@ -++@

P24it a:aila8le a))2)2iatin .> &&> ..&>

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 8/37

Fi@5 3;3

INTERPRETATION5

"ccording to hori!ontal analysis of profit and loss account increasing

trend is observed. 4n /11) there is an increase in all factors such as interest income*

interest income after provision and profit before and after ta6 showing the trust of people

on banks is increasing day by day.

The banking sector spreads continued to incline during the last three years*

from an average of +.-0@ in /11 to ,.-@ in /11,. =$ource $BP $tatistical Bulletin>.

MCB net mark up is also showing this inclining trend with the -11@ in /11* --)@ in

/11, and -21@ in /11). This shows MCB is competing very well in the market.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 9/37

RATIO ANALYSIS5

Financial ratio analysis is the calculation and comparison of ratios which are derived

from the information in a companys financial statements which relates two pieces of

financial data by dividing one Auantity by the other to calculate ratios because in this wayone gets a comparison that may prove more useful than the raw number by itself.

The business itself and outside providers of capital =creditors and

investors> are interested in these ratios. The level and historical trends of these ratios can

be used to make inferences about a companys financial condition* its operations and

attractiveness as an investment. #atio analysis for MCB Pakistan is given as follows

.+ P24ita8ilit= Rati5

Profitability ratios measure how much company revenue is eaten up by

e6penses* how much company earns relative to the sales generated and the amount earned

relative to the value of the firmDs assets and eAuity.

Management and shareholders of the company are interested in

profitability ratios. Higher profit ratio is desirable. These different kinds of the

profitability ratios for MCB bank Pakistan are given below

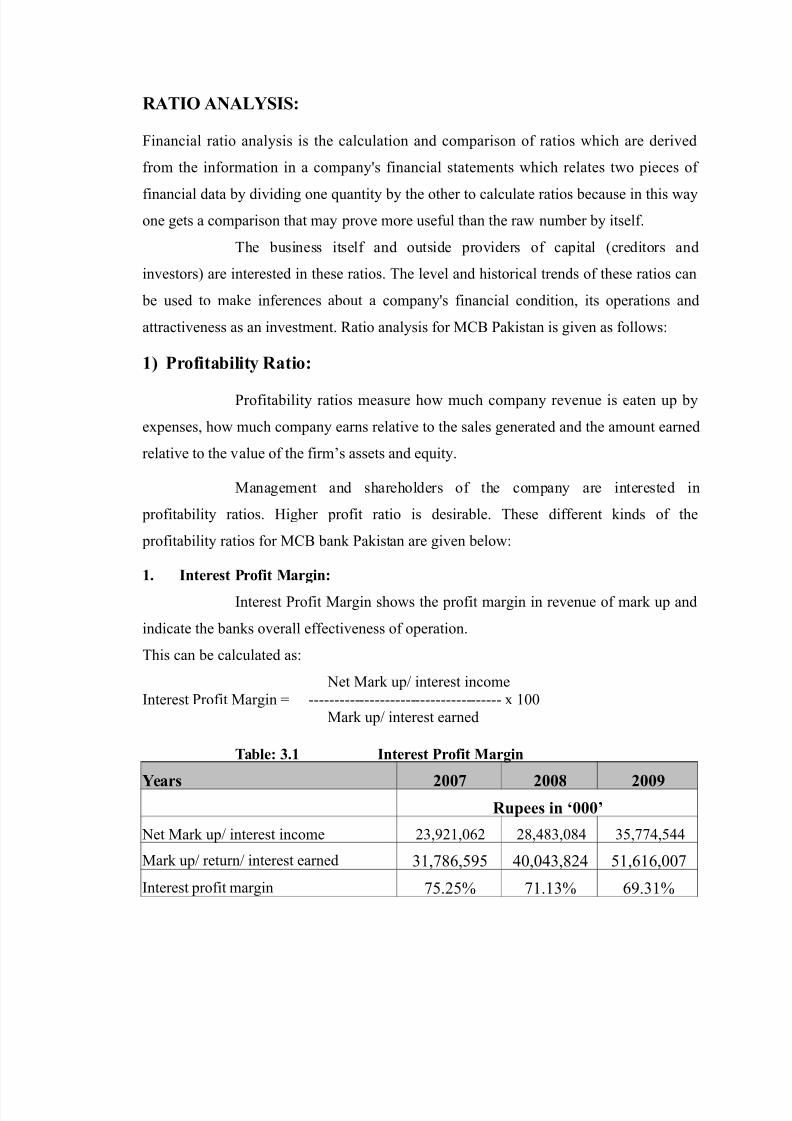

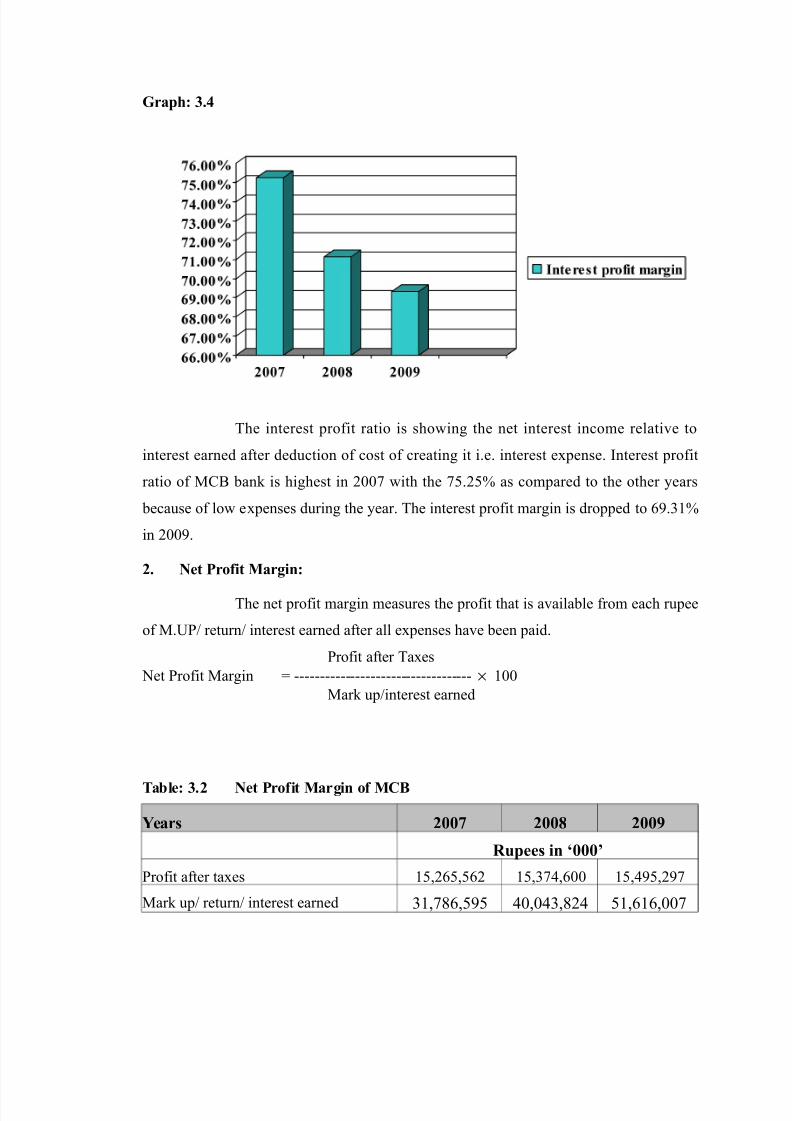

.; Inte2e*t P24it Ma2@in5

4nterest Profit Margin shows the profit margin in revenue of mark up and

indicate the banks overall effectiveness of operation.

This can be calculated as

;et Mark up: interest income4nterest Profit Margin E 55555555555555555555555555555555555555 6 -11

Mark up: interest earned

Ta8le5 3;. Inte2e*t P24it Ma2@in

Yea2* "$ "% "&R()ee* in

;et Mark up: interest income /(*)/-*1+/ /,*0,(*1,0 (2*0*200

Mark up: return: interest earned (-*,+*2)2 01*10(*,/0 2-*+-+*11

4nterest profit margin 2./2@ -.-(@ +).(-@

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 10/37

G2a)!5 3;1

The interest profit ratio is showing the net interest income relative to

interest earned after deduction of cost of creating it i.e. interest e6pense. 4nterest profit

ratio of MCB bank is highest in /11 with the 2./2@ as compared to the other years

because of low e6penses during the year. The interest profit margin is dropped to +).(-@

in /11).

"; Net P24it Ma2@in5

The net profit margin measures the profit that is available from each rupee

of M.9P: return: interest earned after all e6penses have been paid.

Profit after Ta6es

;et Profit Margin E 55555555555555555555555555555555555 × -11

Mark up:interest earned

Ta8le5 3;" Net P24it Ma2@in 4 MCB

Yea2* "$ "% "&

R()ee* in

Profit after ta6es -2*/+2*2+/ -2*(0*+11 -2*0)2*/)

Mark up: return: interest earned (-*,+*2)2 01*10(*,/0 2-*+-+*11

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 11/37

;et profit margin 0,.1@ (,.0@ (1.1/@

G2a)!5 3;,

The net profit margin has being slightly declined in the year /11) as

compared to /11* showing a downward trend in /11) by -.),@ from /11.

3; Ret(2n n A**et*5

This ratio indicates how much income each rupee of assets produce. 4t

shows whether the business is investing in its assets effectively or not.

Profit after ta6es

#eturn of assets E 555555555555555555555555555555 × -11

Total assets

Ta8le5 3;3 Ret(2n n A**et* Rati*

Yea2* "$ "% "&

R()ee* in

Profit after ta6es -2*/+2*2+/ -2*(0*+11 -2*0)2*/)

Total assets 0--*1)(*2/- 000*,-/*2, 21)*//(*/

#eturn on assets ratio (.@ (.02@ (.10@

G2a)!5 3;/

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 12/37

#eturn on assets ratio shows the return on total assets .The ratio has

deteriorated to (.10@ in the year /11).

1; Ret(2n 4 E(it=5

The return on eAuity is a measure of how well management has used the

capital invested by shareholders. #eturn on eAuity tells us the percentage return of each

rupee invested by share holders.

;et Profit after Ta6es

#eturn on eAuity E 555555555555555555555555555555555555555 × -11

$hare holders eAuity

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 13/37

Ta8le5 3;1 Ret(2n n E(it=

Yea2* "$ "% "&

R()ee* in

Profit after ta6es -2*/+2*2+/ -2(*0*+11 -20*)2*/)

$hare holders eAuity 22*--)*+2 2,*0(+*120 +)*01*1-(

#eturn on Auity /.+@ /+.(@ //.//@

G2a)!5 3;$

There is a decreasing trend in the return on eAuity. #& is /.+@ in

/11 and dropped down to //.//@ in /11).

,; A:e2a@e )24it )e2 82an!5

"verage profit per branch is a roughly estimate of how each branch of

MCB contributing to the profit of the whole bank.

;et Profit after Ta6

"verage profit per branch E 55555555555555555555555555555555 × -11

;o. of branches

Ta8le5 3;, A:e2a@e P24it )e2 B2an!

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 14/37

Yea2* "$ "% "&

R()ee* in

Profit after ta6es -2*/+2*2+/ -2*(0*+11 -20*)2*/)

;o. of branches -*1/1 -*101 -*1,-"verage profit per branch -0)++./ -0,(.( -0((0./

G2a)!5 3;%

The average profit per branch is decreasing where the numbers of

branches of MCB are increasing every year. Management need to focus over this

change that whether the branches are not profitable or these are in the early stages

of development.

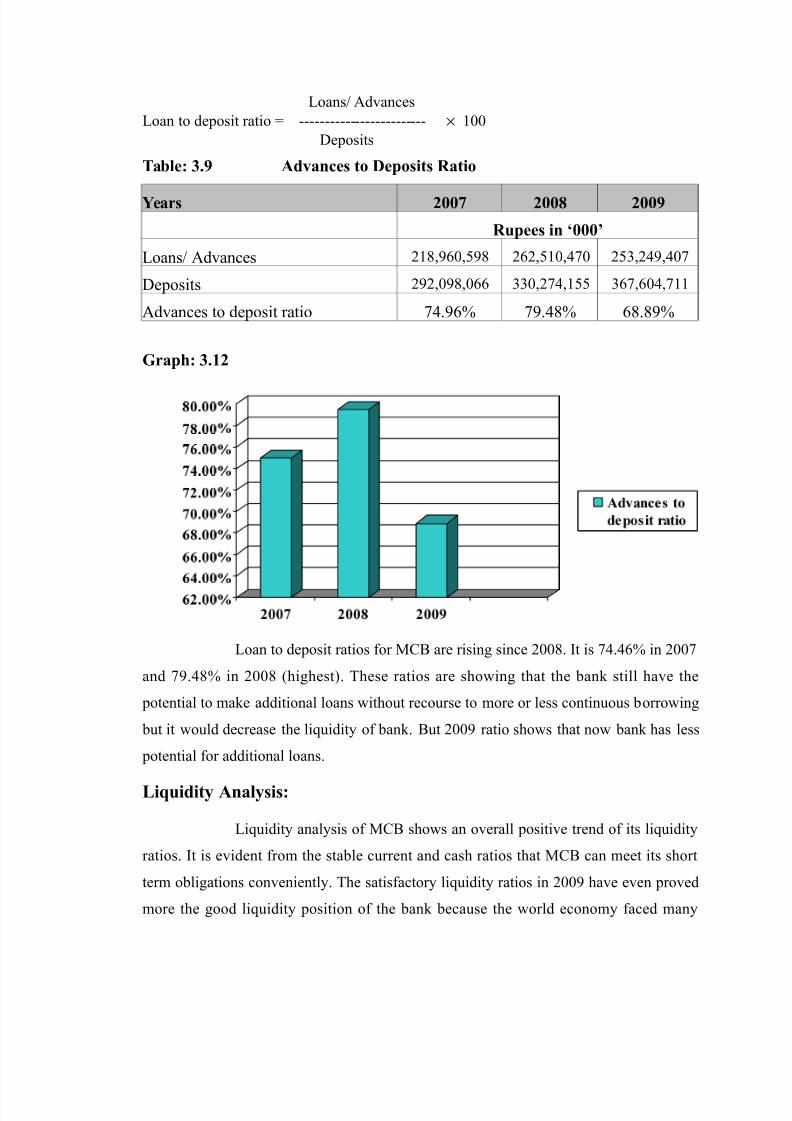

/; Ret(2n n Ad:ane*5

#eturn on advances helps to get an insight into the effectiveness of the

advance policies of management. 4t shows how much interest income is generated from

advances.

4nterest income

#eturn on advances E 5555555555555555555555555 × -11

Total loans

Ta8le5 3;/ Ret(2n n Ad:ane*

Yea2* "$ "% "&

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 15/37

R()ee* in

;et Mark up: interest income /(*)/-*1+/ /,*0,(*1,0 (2*0*200

Total loans: "dvances5net /-,*)+1*2), /+/*2-1*01 /2(*/0)*01

#eturn on advances -1.)@ -1.,2@ -0.-/@

G2a)!5 3;&

#eturn on advances has increased in year /11) as compared to /11 and /11,.

This shows an increase of (./@ in /11) from the year /11,.

P24ita8ilit= Anal=*i*5

Profitability analysis for three years /11* /11, and /11) for MCB

Pakistan has shown the decline from the previous years. 4t is Auite noticeable that

although it was e6pected that the upward trend will tend to continue in future but all the

profitability ratios in the year /11) has shown decline to its values in /11. This fall in

profitability ratios can not be totally assigned to inefficient assets utili!ation and lower

operating efficiency of the MCB bank because /11) was an era of global financial crises.

The word economy has faced worst recession since great depression which has suffered

developing countries as well. The countryDs economic performance deteriorated during

the year especially during the last months of the year the deterioration was e6tremely

severe. The profit before ta6 of the banking sector decreased by /+@ to #s. , billion in

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 16/37

/11, compared to #s. -12.2 billion in /11 =$ource PM< Taseer Hadi ' Co*

=/11,>. Banking Survey /11,. Pakistan.>.

The main reasons for reduction in the profitability were impairment of

eAuity investments and higher level impairment of loans and advances. 4ts effect can be

clearly seen in profitability of MCB but this decline in profitability ratios of MCB in

/11) is not so sharp indicating the good performance of the bank in /11) in the sense that

bank has survived and prevented its profitability from dropping drastically in the severe

financial crisis.

"+ Li(idit= Rati5

3iAuidity ratios measure the ability of a company to meet current

obligations. Management and short5term creditors are interested in these ratios. Higher

liAuidity ratios are favorable. The most commonly used types of liAuidity ratios are the

following.

.; C(22ent Rati5

Current ratio measure the ability of the firm to meet current obligations

with liAuid assets. The higher the ratio the grater is the companyDs ability to meets its

short term obligations. The current ratios are calculated by dividing total current assets by

total current liabilities.

Current assetsCurrent ratio E 55555555555555555555555

Current liabilities

Ta8le5 3;$ C(22ent Rati

Yea2* "$ "% "&

R()ee* in

Current assets /)/*2(1*/,) ((1*2,)*+(- (+*+10*--

Current liabilities /,/*0)*0(+ (-/*/(0*1+, (()*+1+*/22

Current ratios -.10 -.1+ -.1

G2a)!5 3;.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 17/37

4n the year /11* the current ratio is -.10 where it increased to -.1 in /11).

"; Net D2kin@ a)ital5

;et working capital is commonly used to measure a bank overall liAuidity.

;et %orking Capital E Current "ssets 5 Current 3iabilities

Ta8le5 3;% Net 2kin@ Ca)ital

Yea2* "$ "% "&

R()ee* in

Current assets /)/*2(1*/,) ((1*2,)*+(- (+*+10*--

Current liabilities /,/*0)*0(+ (-/*/(0*1+, (()*+1+*/22

;et %orking Capital -1*121*,2( -,*(22*2+( /*))1*02+

G2a)!5 3;..

MCB has more current assets then current liabilities showing bank has

improved its liAuidity .;et working Capital is increasing since /11.

1; Ad:ane* t e)*it* Rati5

4t demonstrate the degree to which bank has already used up its available

resources to accommodate the credit needs of its customers.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 18/37

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 19/37

stresses in /11,. 4n Pakistan its effect also appeared in the form of severe liAuidity crunch

which was e6acerbated by heavy withdrawals of deposits following rumor5fed concerns

over the stability of local banks.

MCB is a bank that always maintain high reserves so in the era of crisis in/11)* MCB not only survived itself but also helped other banks like 9B3 and small

banks to solve liAuidity problems. The liAuidity strains were temporary and the inter5bank

markets continued its functioning normally.

3+ Le:e2a@e Rati5

3everage means the use 1 debt in order to increase profitability. They

measure the e6tent to which a firm is financed through debt. These ratios show the

relative si!e of debt load. Management and long term creditors are interested in these

ratios. 3ower leverage ratios are desirable from the point of view of creditors. The

different types of leverage ratios are given below.

.; e8t t e(it= 2ati5

This ratio compares the funds provided by creditors to the funds provided

by the share holders. This ratio can be computed by the following formula

Total 7ebt7ebt to eAuity ratio E 55555555555555555555555555555

$hareholders eAuity

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 20/37

Ta8le5 3;. e8t t E(it= Rati5

Yea2* "$ "% "&

R()ee* in

7ebt (22*(+2*,0/ (,2*-)*,21 0()*0,(*-0

Auity 22*--)*+2 2,*0(+*120 +)*01*1-(

7ebt to eAuity ratio +.0 +.+ +.(

G2a)!5 3;.3

From the table and graph it is clear that 7ebt to eAuity ratio is decreasing

which show the high efficiency of MCB. 4n /11) it was +.( and it showed slight increase

occurred in /11, from /11 but as whole it a good sign for the bank.

"; e8t t A**et Rati5

This ratio shows that how much the company finances its assets through

debts. Creditors prefer this ratio when it is low. This ratio can be calculated by dividing

the total debts by the total assets.

Total 7ebts

7ebts to assets ratio E 555555555555555555555555 Total "ssets

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 21/37

Ta8le5 3;.. e8t t A**et* Rati

Yea2* "$ "% "&

R()ee* in

Total 7ebt (22*(+2*,0/ (,2*-)*,21 0()*0,(*-0

Total "ssets 0-1*0,2*2- 00(*+-2*)10 21)*//(*/

7ebt to "ssets ratio 1., 1., 1.,+

G2a)!5 3;.1

The 7ebt to asset ratio is showing that MCB has financed its assets in a

way that in each rupee of assets there is 1.,* 1.,* and 1.,+ portion of the debt in year

/11* /11, and /11) respectively.

Le:e2a@e Anal=*i*5

7ebt eAuity ratio shows how the firmDs stockholder bears the risk of the

firm. 4n /11 and /11, the share holders of MCB are bearing more risk as compared to

the /11) but debt to eAuity ratio has increased in /11, from /11. 7ebt to asset ratio in

/11 ' /11, is the highest showing assets were heavily financed with debts in that year

and decrease is observed in the ne6t year /11).

The average return on eAuity =profit before ta6 as a percentage of average

eAuity> of large si!e banks of Pakistan decreased by 2.+@ from /,.)@ in /11 to /(.(@

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 22/37

in /11,. "mong large si!e banks* MCB despite a decline of ,@ in return on average

eAuity as compared to last year was the top by registering the highest return on eAuity i.e.

(./@ followed by HB3Ds (-.,@ =source PM< Taseer Hadi ' Co* =/11,>. Banking

Survey /11,. Pakistan>."s in /11) the world recession has inevitably affected the

economy of Pakistan and people were reluctant to retain their deposits. "s a result public

were taking back their deposits and liAuidity crisis arises for some banks. $ome of

deposits were transferred to MCB because of its position of high reserves and also helped

many banks including 9B3 for dealing the liAuidity problem in those hours of crisis

Ma2ket 7 In:e*t2 Rati*5

4nvestor analysis or market analysis are related to firm market value* as

measure by its current share price to certain accounting values. There are several ratios

commonly used by investors to assess the performance of a business as an investment

.; i:idend )e2 S!a2e 6 PS5

The 7P$ ratio is very similar to the P$. P$ shows what shareholders

earned by way of profit for a period whereas 7P$ shows how much the shareholders

were actually paid by way of dividends.

4t is calculated as

Total amount of 7ividend7ividend per $hare E 55555555555555555555555555555555555

;umber of outstanding shares

Ta8le5 3;." i:idend )e2 S!a2e 6 PS5

Yea2* "$ "% "&

7ividend per $hare -/.21 --.21 --.11

S(2e5 MCB* =/11)>. Annual report

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 23/37

G2a)!5 3;.,

#emarkable increase in 7ividend per share is seen in /11. 7P$ in /11, is

--.21 facing a slight decrease but still declined in year /11) to --.11.

"; Ea2nin@ Pe2 S!a2e0 EPS

P$ shows portion of a companys profit allocated to each outstanding

share of common stock. arnings per share serve as an indicator of a companys

profitability. arnings per share are generally considered to be the single most important

variable in determining a shares price. 4t is highly important ratio for investors and high

ratio of P$ is desirable. The formula for calculation is

Profit after Ta6ationarning Per $hare E 55555555555555555555555555

;umber of $hares

Ta8le5 3;.3 Ea2nin@ Pe2 S!a2e0 EPS

Yea2* "$ "% "&

arning per $hare/0.(1 /0.0 //.0/

S(2e5 MCB* =/11)>. Annual report

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 24/37

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 25/37

G2a)!5 3;.$

7ividend pay out ratio has shown downward movement in the year /11)

from /11 with the values of 2-.02@ to 0).1+@. The ratio remained almost same in the

year /11, as it is in /11. The ratio shows the dividend distributed among the

shareholders. 4t is low in /11) as compared to year /11,. 4t may be due to high

percentage of retained earning.

In:e*t2 Anal=*i*5

This type of analysis is also called market analysis. 4t gives the birdDs eye

view of overall performance of the organi!ation. Price earning ratio* dividend pay out

ratio and earning per share etc. are the gauge of the investors. 4nvestor analysis of MCB

has shown good investment opportunities for the investors. P$ and dividend yield has

decreased. The consolidated statements of the bank have shown that P$ of ma8ority of

banks faced sharp decline in the end of /11) from /11 but this decline was not bearing

high value for MCB. MCB somewhat maintained it good position in the market.

The P: ratio shown by the year /11) is the lowest value ever shown by

MCB in last si6 years. 4t was due to the collapse of the stock marketG MCB share price

registered a blow and closed significantly lower than the same period in year /11,.

However* despite these circumstances* the performance of MCB shares were still

significantly better than other players in the market* reaffirming the trust of investor

base in the bank.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 26/37

SOT Anal=*i*5

$%&T is a method of analysis which e6amines a companys $trengths*

%eaknesses* &pportunities and Threats.I

The $%&T analysis for MCB Pakistan is briefly given as

St2en@t!5

-> MCB has a brand name and recognition with the rich and old history of more than 21

years having a customer base of appro6imately 0 million.

/> 4t is the most resourceful bank with high liAuidity. MCB keeps reserves in advance

for / years unlike other bank that keep reserves for the prevailing year of operations

only. This was the reason that MCB was not shake by the global crisis of /11, '

solved the problem of liAuidity for 9B3 and other small banks with its high reserves.

(> MCB has an efficient recovery system due to sanctioning of loans on merit basis thus

got smaller bad debt portfolio.

0> MCB has ""J rating for long term and "-J for short term by P"C#" showing high

credit Auality and low credit risk.

2> 4t is an innovative bank in the industry =pioneer in introduction of MCB master card

with photograph and rupee travelers cheAue>+> Pioneer in 4T department.

> MCB has reasonable service charges.

,> MCB got an e6tensive network of branches =-1,-> providing customers with an ease

of access to the bank.

)> MCB got times uromoney "ward for the IBest Bank in "siaK and / times "sia

Money awards as KThe Best 7omestic Commercial Bank in PakistanK making it a

highly trust worthy bank in the industry.

eakne**e*5

-> MCB lacks strong marketing effort and promotional campaigns in the industry.

/> MCB offers low rate of interest which is unattractive for new customers especially.

(> 3ow 8ob satisfaction and lack of motivation of employees.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 27/37

0> 3ack of Auick and prompt services compared to some of the banks due to wide spread

network of branches.

2> Customers are not treated to their e6pectations.=uncooperative behavior of

employees>

+> Branches encounter 4T services problems and all the branches are not online affecting

services of the bank.

> $taff is not sufficient thus they are overburdened

,> 3ack of speciali!ation resulted in 8ack of all and master in none of the employees.

MCB keeps non5professional staff even on higher posts who are promoted from the

typist and clerical area after a long time.

)> 3imited training opportunities for the staff.

O))2t(nitie*5

-> Processing and development in 4T section can lead the bank to higher and stable

position in the coming years.

/> 7ue to largest "TM network* MCB can e6pand its /0 hours cash facilities to the far

off cities to meet its growing market demand.

(> Products that are only available in arachi* 3ahore and 4slamabad can be e6tended in

the market of other cities.0> MCB online banking system can be e6panded to make available the banking facilities

throughout the country and increase the market share.

2> MCB can e6pand its foreign operations and services by e6tending its agency relations

with the foreign banks. "t present there are few agency relations in foreign.

+> MCB is trying to make acceptable its "TM card internationally and release funds

internationally. 4nternational shopping and other facilities associated with the card can

bring more opportunities for the bank profitability.

> &nline accounts opening is another segment for the bank to step into.

T!2eat*5

-> $evere Competition with the entrance and establishment of many banks including

foreign bank branches.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 28/37

/> Highly speciali!ed and attractive services provided by foreign banks to their

customers.

(> 7ay to day changing global technology.

0> Huge deposits and support of government always made ;BP a threatening

competitor. HB3* 9B3 and "lfalah bank are the other strong competitors.

2> 9nstable economy of the country and un5consistency in government policies

regarding to business and economic sector.

+> MCB faces a great threat from <ovt policies like as finance the non5productive units*

housing etc. so the bank does not feel freedom in operating on its own view points*

that is a threat for the bank

> Turn over due to other banks offering good salary packages to staff.

,> $ecurity threat due current situation in the country.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 29/37

CHAPTER # 1 FININGS ? RECOMMENATIONS

PROBLEMS OF MCB PAKISTAN5

$ome of the ma8or problems observed in MCB Pakistan are as follows

.; Limited ele@atin 4 A(t!2it=5

4n case of advances* manager has to take the approval of general and

regional manager. 4n newly established banks there is comparatively more delegation of

authority as compared to MCB that is why their deposits and business is improving day

by day.

Top level management is having a lot of influence in all decision making*

and they always do not consult the lower level management and thus do not get adeAuate

data about the problems at the branch level.

"; Len@t!= P2ed(2e*5

The main ob8ective of MCB is to provide improved services to customers*

but now the bank seem to fail to achieve its ob8ective* its lengthy procedures as compared

to newly established private banks causes problems for customers. 7uring rush hours the

customer has to wait for a long time for their turn. 4n advances department the process of

loan sanctioning is very lengthy* which affect the customer. Time is the most important

factor these days which seems to be ignored by MCB bank.

3; E9e**i:e )a)e2 D2k5

Though MCB is computeri!ed yet the system has not totally shifted to

computers. Manual procedure is still there hence computer facility is not fully availed. 4t

is notified that due to e6cess of paper work the bank employee are over burdened. They

are unable to give proper attention to the clients and face difficulties in getting their 8ob

done.1; Le** att2ati:e 2ate 4 2et(2n5

The rate of return offered by MCB is comparatively less than its

competitors. 4t may prove threatening in the future.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 30/37

,; Lak 4 Ma2ketin@ E442t*5

The marketing activities in MCB are weak in very aspect. There are no

special promotional campaigns observed for the awareness of people about MCB

products. Many people donDt have any idea about the product features and consider all the

products same. Moreover* the attitude of employees with the customers is not

satisfactory. The Bank employees are doing very little on their own to e6plore the

possibilities of selling banking services to them as a marketing contributor. &verall* MCB

lacks the spirit of true marketing even in todayDs time where foreign banks are fully

concentrating on it.

/; Lak 4 In:e*tment n R ? 5

They do not invest on #'7 to know what a type of benefits the customer

wants from the bank. MCB has Auite ignored the importance of #'7.

$; Lak 4 P24e**inal t2ainin@5

MCB staff lacks professionalism. They lack the necessary training to do

the 8ob efficiently and properly. There is also lack of speciali!ation. "lthough there are

staff colleges in all ma8or cities but they need to bring better results. Training programs

offered by MCB are not adeAuate to achieve the purpose of productive employees.

%; n4ai2 Hi2in@5

4f the personnel are recruited carefully they can become asset to the

organi!ation in the case of carelessness a liability on the organi!ation. Bank is not

following its recruitment policy properly due to favoritism* nepotism and political

pressure. Both the top authority and staff union tries to recruit their favorites* indulgence

of political pressure add salt to the wounds. The persons selected through these channels

are infantile and do not work for the betterment of the bank.

&; N )e2idi in2ea*e in *ala2ie*5

"nother very important thing which is ignored in the bank is the periodic

increase in salaries. The salaries were increased in -)), and after that the salary has not

changed till now which resulted in low motivational level of employees and decline in

performance.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 31/37

RECOMMENATIONS5

From the Auantum of the profit and financial data it can easily 8udged that

after privati!ation MCB is performing well. 4ts deposits are growing day5by5day and so is

profitability. But there are certain problems that are affecting the organi!ation. The

comprehensive analysis of MCB as whole leads me to the following recommendations

for the improvement of the bank.

.; A:aila8ilit= 4 Sta445

$taff in the branch must be in proportion to the customers in order to

e6pedite the workflow* avoid overloading of staff and remove the customerDs grievances

arising mainly due to delay in workflow.

The additional staff should be hired in MCB <ulbahar Colony Branch =-/2>* in the

following categories

• Telephone operator to answer all incoming calls.

• / <eneral banking officers to work on all seats in the bank that will reduce the burden

of work on e6isting employees.

• MCB technician to work on "TM problems.

"; Cmmitment 4 Em)l=ee*5

The decreasing commitment of employees of MCB and their low 8ob

satisfaction can be increased by introducing an effective performance appraisal system*

which can reward and recogni!e the achievements and services of employees at the

branch level.

3; ele@atin 4 a(t!2it=5

Centrali!ed $tructure that enables employee involvement needs to be

formed. Branch manager should be given authority to the e6tent that they can hire

employee for their branch at least in emergency situation. Together with a need of a

telephone operator it is severely affecting the branch.1; P!=*ial 4ailitie* 4 t!e 82an! '."$,+5

To overcome physical problems of the branch the management should

purchase more furniture and arrange them in such a way which provides ma6imum space

and convenient sitting place for the customers. Maga!ines* ;ewspaper etc should be kept

for customers. "ir conditioner should be repaired to provide services in summers.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 32/37

,; T2ainin@ Ati:itie*5

Training should not be limited to some employees. 4n fact all employees

need to be trained for the proper functioning of organi!ation. MCB has three staff

colleges in 3ahore* arachi and 4slamabad. The bank should include the following

ingredients in training process to strengthen the operational capabilities of the employees

• The bank should organi!e a number of in5house training courses and seminars on

different topics related to advances and other departments.

• The bank should send the employees for speciali!ed courses.

• Bank should train the employee before assigning the 8ob. There should be proper

training =9p to date> for newly selected employees.

• There should be refresher courses for officers.

/; In2ea*e in *ala2ie*5

They salaries of employees are not considered after -)),. 3ow salaries are

creating dissatisfaction in employees. 4t should be ad8usted according to new market

conditions and rise in inflation

$; C(*tme2 Sati*4atin5

This image that banks are in financial sector not in service has changed.

Banks are striving to provide good services more than ever. Customer satisfaction is

highly important in this era of cutthroat competition for MCB. Customer values time so

MCB should improve the service by following ways

• People have to wait for re5cashing their cheAues for about -1 to -/ minutes Manual

work is also responsible for this delay. Therefore electronic means should be installed

so that time can be saved.

• 3oan procedure should not be cumbersome and should be made easy* so as to ease the

customers.

• "ll the branches should be made online to create ease and prompt services for the

customers.

%; Fai2 Hi2in@ Pli=5

#ecruitment in the bank should be made purely on merit basis. H#7

should be fully free from any influence of higher authority and staff union in conduction

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 33/37

of tests and in the selection of candidates.

&; Ma2ketin@ E442t*5

MCB should flourish certain marketing plans to attract the customers by

giving them certain incentives and beneficial schemes to the customers as other

competitor banks are doing so. The following measures are suggested in this regard

• MCB should invest on #'7G if they invest on #'7 it will help the bank to know

what type of benefits the customer wants from the bank.

• " promotional campaign should be carried out through employers who are customers

of the bank and their employees are paid in cash. 4t might be worth offering least

charges for a specific period to the new ones.

• %ebsite of MCB is not updated till /11,* bank should also emphasi!e on enhancing

its information on website.

• Bank must let potential customers know about all the attractions MCB holds. This is

done by advertising on television and obtaining press coverage in con8unction with

direct mail* window displays* leaflet in branches and in appropriate other locations.

• " short term promotional techniAue is to offer price incentives* for e6ample* low

interest rates on advances or limited issue of high profit bearing term deposits. The

reduced short term profits can be augmented by profits made in long run.

• 4t is also possible to attract:retain personal customers by investment in new

technology like "TMs and Telephone Banking facilities etc which made the services

Auicker* easier* cheaper and more fle6ible.

.; Healt!= ati:itie*5

&n weekends* parties and other celebrations should be arranged on official

basis for employees. $uch activities should be encouraged at once in a month to

strengthen the commitment of employee with the bank.

..; Inte2n*!i) P2@2amme5&ne of the best and cost effective methods to select the right kind of

people is to hire graduates from business and management schools as internees like the

organi!ations of foreign countries do. MCB branches in all cities should participate in it

and develop links with universities to offer internship program to students on merit basis.

The internship program should be paid attractively and proper training should be a ma8or

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 34/37

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 35/37

- day Making call to the selected candidate

days For the beginning training of the telephone operator in Branch

Atin 7 Im)lementatin Plan C*t5

.0 C*t 4 Hi2in@5"dvertisement in newspaper

• "LL =#s 221 per cm> #s. --111

• L";< #s. -2*111 appro6

"0 Tele)!ne netD2kin@5

• "dditional telephone set #s. -111

• PTC3 charges #s. 21

3; Ot!e2 *t*5

$eparate table and chair 2111

R*; 3"-$, Ttal atin )lan

*t

Atin Plan 42 B2an! Pe242mane A))2ai*al5

The decreasing commitment of employees and low 8ob satisfaction in

MCB <ulbahar Colony Branch =-/2> can be increased by introducing an effective

performance appraisal system* which can reward and recogni!e the achievements and

services of employees at the branch level. The BM can better 8udge the performance of

his employees and enhance the moral of employees for better performance.

The following steps should be followed to accomplish this plan

• The performance audit of the branch must be carried out on both regular and surprise

basis.

• Periodically feedback should be provided to employees and recogni!ing their efforts

through reward =bonuses> and publicly appreciation. Presenting a shield would also

be effective at branch level to motivate a competent employee.

• The appraisal system must be uniform in evaluating all the employees without any

discrimination.

• The appraisal system must be based on facts and figures and ob8ective evaluation of

the facts on grounds.

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 36/37

This performance appraisal system will play a significant role in the motivation and 8ob

satisfaction of employees. 4t will also benefit organi!ation as a whole in the long run.

Atin Plan 42 In2ea*in@ Bank E44iien=5

The increasing competition in banking sector is alarm for greater

challenges in future. The giant challenge that can be seen in future would be the

improvement in technology of banks to increase efficiency more. MCB also need to focus

over these challenges like it has done in the past. MCB is one of the resourceful banks in

Pakistan so being pioneer in technology and other techniAues can help the bank to have a

strong grip over the future. MCB should follow these steps in long run

.; ) @2adatin@ ATM 42 Ca*! e)*it*

;ow5a5days in foreign countries "TM machines are also used for deposits

of money and utility bills can be paid through "TM. But in Pakistan these services have

not been utili!ed yet. $o if MCB upgrades its "TM technology in long run it will save the

time of employees and get the competitive advantage over other banks.

$ome more "TM machines will be reAuired to purchase for MCB. "TM

machines can cost anywhere from several thousand dollars up to +211 dollars each

=e6cluding shipping charges>.

"; In*tallatin 4 A(tmati J(!e2* S=*tem5

"s all the ledger system and vouchers are still handled manually which is

a much time consuming and more efforts reAuiring 8ob with the chance of human errors.

To overcome this problem MCB should implement $"P F4;";C M&793I =5

commerce software> in their banks that will help them in creating automatic vouchers and

ledger for transactions made by customers because $"P has the capability to keep all the

records of an individual at 8ust one place and it has the capacity to store much data.

3; In*tallatin 4 Jalidat2 Ma!ine5

Nalidator machine is used to count the currency notes and its installation

will help to eliminate the counting errors and will save time of workforce. This should be

installed in long run to increase the efficiency of bank and allowing employees to work

on other things by cutting down the time spend on counting of cash.

1; E9)andin@ netD2kin@ amn@ 8ank*5

4n MCB the networking is only done within their own banks* means the

8/10/2019 analysis on MCB

http://slidepdf.com/reader/full/analysis-on-mcb 37/37