analysis of pakistan automobile industry

DESCRIPTION

Analysis ReportTRANSCRIPT

Analysis of Automobile Industry of Pakistan

Introduction:

ince ages man is trying hard to cover the distances between different places in the shortest possible time. In order to fulfill this dream man invented the automobile and within

years the automobiles became a common mode to travelling to different places and replaced the traditional means of using animals . With this increasing demand for the newly invented automobiles its production also increased many folds. This industry also gave rise to many allied industries and provided jobs to millions of people all over the world. This industry also contributed its due share in the GDP of the country via import duties, sales tax, federal excise duties etc. However the increasing number of automobiles also had different impacts which affected human lives, atmosphere, social fabric etc.

SPreface:

akistan Auto Industry has been a star performer of industrial sector during the last 6 to 7 Years and has registered impressive annual compound growth surpassing other sectors

of the economy. The industry adopted the Tariff Based System (TBS), after elimination of Deletion Programmer without any major hiccup, during the year 2006. This reflects the strength and resilience of the industry. It can cope with the challenges of competitive environment. Thecontinuation of high growth, improving the quality and achieving the cost competitiveness while satisfying the consumer expectations and environment standards will remain a task in the future too. Becoming a part of global supply chain and exporting 2/3 wheelers, cars and tractors in particular will remain a goal both for the government and the industry. The industry is moving towards attaining a critical mass of production, is acquiring latest technologies, improving Pakistan Auto Industry has potential to become a global choice for outsourcing, off shoring and becoming part of the global supply chain.The government’s guiding principle to involve stakeholders, not only in the policy formulation process but during implementation as well, is apparent from the notification of Auto Industry Development Committee, which has a majority of private sector stakeholders.

P

Page 1

Analysis of Automobile Industry of Pakistan

Executive Summary:

1. Pakistan is amongst a few countries of the world which manufacture all kinds of vehicles i.e. 2/3 wheelers, motor-cars, LCVs, tractors, prime-movers & trucks and buses. The total country requirements are generally met from the local production except the import of certain categories of trucks & prime-movers. Import of used cars is allowed to the bonafide ex-partite The presence of few of world acclaimed brands and multinationals in the manufacturing of vehicles for the last 2 to 3 decades and their regular expansion plans speak of their confidence on the market, government policies and economic potential of the country

2. Pakistan auto industry turnover during the year 2005-06 crossed US $ 3.6 billion which comes to 2.8% of GDP (2005-06), thus saving substantial foreign exchange on imports. The job contribution by auto industry comes to nearly 1.392 million which includes direct jobs of nearly 192,000. The auto industry remains second largest tax payer in terms of its contribution to customs duty, sales tax and withholding tax.

3. Pakistan auto industry produced over 1 million vehicles including 2/3 wheelers during the year 2006-07, mainly due to government’s economic reforms and availability of financial options and leasing facilities on purchase of vehicles. The yearly growth in the recent years has surpassed the auto industry growth in the competing countries. Pakistan’s total share of car and commercial vehicles remains 0.37% of the world production during the year . Global trade of automobiles is over US $ 1 trillion.

4. The auto industry contribution to other sectors of the economy both tangible and intangible is highly significant. The auto industry economic and job multiplier in Pakistan context would be around Rs.1: 3 and 1: 8 respectively. While the auto industry’s deeper forward and backward linkages have created dissemination of systems, technology, skill development and providing base o the rest of engineering sector. Its deeper backward integration due to consumption of local and imported materials and tooling’s such as steel, aluminum, copper, plastics & chemicals, rubber & glass and its forward linkages in the form of retail & wholesale, dealerships & logistics, workshops & maintenance, filling stations, finance & insurance, marketing, advertising and consultancy services and trade speak of its contribution and future role for the industrial development of the country.

5. The auto industry expressed resilience during the last 1 ½ year when it switched over from compulsory local content conditions to a compliant tariff based system (TBS) which came into effect on 1st July, 2006. The changeover has posed many challenges to the vendors who remained comfortable in the previous system and are now pushed to improve the quality, supply system shop floor efficiencies and better marketing. Investment in modern production infrastructure, testing equipment and automation remains high priority. The vendors are mostly SMEs which are developing their approach and are looking for professional support to re-integrate and re-design their work flow processes and improve quality through better technologies, testing equipment and adoption of best manufacturing practices workshop at Islamabad by clearly defining the objectives at a time when the industry was switching over from the deletion programmer to a competitive tariff based system.

Page 2

Analysis of Automobile Industry of Pakistan

6. Government has recently approved a 5 year tariff plan for the auto sector to ensure a stable and predictable environment and to facilitate investment. AIDP to achieve a critical mass of production, double the contribution of auto industry to GDP from the existing 2.8%, by the year 2011-12 with high focus on investment, technology up-gradation, increasing its exports to US$ 650 million, enhancement in jobs alongside the development of critical components to further increase the competitiveness of domestically produced vehicles.

Page 3

Analysis of Automobile Industry of Pakistan

History of Automobile Industry

European engineers started tinkering with motor powered vehicles since late 1700's. Steam, combustion, and electrical motors had all been triedby themid 1800’s. By the 1900's, it was unsure which type of engine would power the automobile. At first, the electric car was the mostaccepted, but at the time a battery did not exist that would allow a car to be in motion with much speed or over a long distance. Although some of the earlier speed records were set by electric cars, they did not stay in manufacture past the first decade of the 20th century. The automobiles with steam lasted into 1920’s. However, the price on steam-driven engines, either to build or maintain was unparalleled to the gas powered engines. Not only was the cost a problem, but the danger of a boiler explosion also kept the steam engine from becoming popular. The combustion engine constantly beat out the competition, and the early American automobile pioneers like Ransom E. Olds and Henry Ford built reliable combustion engines refusing the ideas of steam or electrical power from the start.

Automotive manufacturing on a commercial scale started in France in 1890. Commercial production in the United States started at thebeginning of the 1900's and was equivalent to that of Europe's. In those days, the European industry comprised of small independent firms that would turn out a few cars by means of precise engineering and handicraft processes.

At the start of the century the automobile entered the transportation market as a toy for the rich. However, it became increasingly popular among the general public because it gave travelers the freedom to travel when they wanted to and where they wanted. As a result, in North America and Europe the price of automobile

decreased and they became easily accessible to the middle class. This was facilitated by Henry Ford who did two important things.

First he set price of his car to be as affordable as possible

Second he paid his workers enough to be able to buy the cars they were manufacturing.

This helped increase wages and auto sales. The convenience of the automobile freed people from the binding to live near rail lines or stations; they could choose locations almost anywhere in city area as long as roads were available to connect them to other places. Popularity of the automobile has moved side by side with the state of the economy, growing during the boom period after World War I and decreasing abruptly during the Great Depression, when unemploymentwas at most

Over view of Pakistan automobile industry

The automobile industry in Pakistan can be broadly categorized into following segments:

Cars and Light Commercial Vehicles (LCVs).

Two and Three Wheelers.

Tractors

Trucks and Buses.

The Automobile industry has been an active and growing field in Pakistan for a long time, however not as much established to figure

Page 4

Analysis of Automobile Industry of Pakistan

in the prominent list of the top automotive industries, having a stable annual production 100-170 thousands only. Despite significant production volumes, transfer of technology and localization of vehicle components remains low, and only a few car models are assembled in the country while customers have a very small variety of vehicles to choose from. The lack of competition in the local auto industry due to the presence of just three assemblers -and only one small car assembler- has resulted in technological stagnation of the industry small cars produced by Pak Suzuki, the country's largest auto assembler, in the country are globally retired models utilizing obsolete technology and not offering any safety features. Currently some of the major world automakers have set up assembly plants or are in joint ventures with local companies these include Toyota, General motors Honda , Suzuki, Nissan Motors.

The total contribution of Auto industry to GDP in 2007 was 2.8% which is likely to increase up to 5.6% in the next 5 years. Auto sector presently, contributes 16% to the manufacturing sector which is predicted to increase 25% in the next 7 years. Many cars in the country have dual fuel options and run on CNG which is more affordable and cheaper than petrol in the country.

According to Ministry of Industries Pakistan produced its first vehicle in 1953 at the National Motors Limited established in Karachi to assemble Bedford Trucks. Subsequently buses, light trucks and cars were assembled in the same plant. The industry was highly regulated until the early 1990s. After deregulation major Japanese manufacturers entered in the market thereby creating some competition in this sector. Assemblers of HINO Trucks, Suzuki Cars (1984), Mazda Trucks, Toyota (1993) and Honda (1994) in particular, entered once deregulation was introduced. Assembly of

Daihatsu and Hyundai cars (1999) and various brands of LCVs and range of mini-trucks commenced recently.

Car industry saw boom in 2006-2007 when sales touched record peak of 180,834 thanks to rising car financing up to 70-80 per cent by banks due to low interest rates and rising rural buying. Since then the industry has been surviving hard to reach the same sales level amid high interest rates and Yen appreciation against the rupee but high farm income is givingmuch support to car sales. Good crops this year will keep the car sales brisk despite increase in prices.

Engineering Development Board (EDB) is actively implementing the AIDP to increase the GDP contribution of the automotive sector to 5.6%, boost car production capacity to half a million units as well as attract an investment of US$ 3 billion and reach an auto export target of US$ 650 million.

Automotive engineering is a driving force of large scale manufacturing, contributing US$ 3.6 billion to the national economy and engaging over 192,000 people in direct employment.

The Auto parts manufacturing is $ 0.96 billion per annum. The demand for auto parts is highest in the motor cycle industry which is 60%, then is for cars which constitutes to 22% and the rest 18% is consumed by trucks, buses & tractors. This demand is met by Imports which caters 22% while the remaining 78% is supplied by the local manufacturers.

The car industry has invested over Rs 20 billion in the last four to five years to meet growing demand. The direct employment in car

Page 5

Analysis of Automobile Industry of Pakistan

industry hovers between 5,500-6,000 persons. Motorcycle production hit the country's record level of over 1.5 million units in 2010-2011 by the effort of Pervaiz Musharraf Government's decision that opened bike market to low cost Chinese bikes. Auto sector now employs 192,000 people directly and around 1.2 million indirectly and has Rs. 98 billion of investments and contributes Rs. 63 billion as indirect tax in the national exchequer.

Auto Sector remains the second largest payer of indirect taxes after the Petroleum Sector. In Pakistan's context there are 10 cars in 1,000 persons which is one of the lowest in the emerging economies which itself speaks of high potential of growth in the auto sector and more so in the car production. Rising per capita income with changing demographic distribution and an anticipated influx of 30 to 40 million young people in the economically active workforce in the next few years provides a stimulus to the industry to expand and grow.There has also been a recent interest towards hybrid and electric cars among educated Pakistani buyers however there unavailability remains a problem.

Pakistan has the second highest number of CNG-powered vehicles in the world with more than 1.55 million cars and passenger buses, constituting 24% of total vehicles in Pakistan with improved fuel efficiency and conforming to the latest environment regulations.

Impact the Automobile industries on Economy

Page 6

Analysis of Automobile Industry of Pakistan

The car industryhas invested over Rs 20 billion in the last four to fiveyears to meet growing demand. The direct employment incar industry between 5,500-6,000 persons. Motorcycle production hit the country’s record level of over 1.5 million units in 2010-2011 by the effort of Pervaiz Musharraf Government’s decision that opened bike market to low cost Chinese bikes. Auto sector now employs 192,000 people directly and around 1.2 million indirectly and has Rs 98 billion of investments and contributes Rs 63 billion as indirect tax in the national exchequer. Auto Sector remains thesecond largest payer of indirect taxesafter thePetroleum Sector. In Pakistan's context there are 10 cars in 1,000 persons which is one of the lowest in the emerging economies which itself speaks of high potential of growth in the auto sector and more so in the car production. Rising per capita income with changing demographic distribution and an anticipated influx of 30 to 40 million young people in the economically active workforce in the next few years provides a stimulus to the industry to expand and grow. Government of Pakistan had undertaken two major initiatives in the form of National Trade Corridor

Improvement Program (NTCIP) and Auto Industry Development Program (AIDP) for the development of the automotive industry in Pakistan. Engineering Development Board (EDB) is actively implementing the AIDP to increase the GDP contribution of the automotive sector to 5.6%, boost car production capacity to half a million units as well as attract an investment of US$ 3 billion and reach an auto export target of US$ 650 million. Automotive engineering is a driving force of large scale manufacturing, contributing US$ 3.6 billion to the national economy and engaging over 192,000 people in direct employment. The Auto partsmanufacturing is $ 0.96billion per annum. The demand for

auto parts is highest in the motor cycle industry which is 60%, then is for cars which constitutes to 22% and the rest 18% is consumed by trucks, buses & tractors. This demand is met by Imports which caters 22% while the remaining 78% is supplied by the local manufacturers in the fiscal year 2007-2008. Due to the increase in demand for sophisticated machinery, the government has allowed duty free import of raw material, sub components, components assemblies for manufacturers & assemblers.

Total import bill of machinery stands at $2.195 billion in the fiscal year of 2007-08 which is 12.77% higher than that of the preceding year. The impressive growth in the machine tools and automation sector is directly proportional to the growth of the automotive industry which has become the fastest growing industry of Pakistan and contributes $3.6 billion annually to the country’s GDP. The aftermarket for spares has also witnessed immense expansion over the same period, with imported parts playing an important role in meeting local demand.

The spare parts market is given further impetus by a total vehicle population of approximately 5.4 million. Pakistan has the second highest number of CNG-powered vehicles in the world with more than 1.55 million cars and passenger buses, constituting 24% of total vehicles in Pakistan with improved fuel efficiency and conforming to the latest environment regulations.

Contribution to the GDP

Page 7

Analysis of Automobile Industry of Pakistan

Today the automotive industry annually contributes over Rs 30 billion to Pakistan's GDP and is also paying approximately Rs 8 billion per year in the form of taxes and thereby playing a pivotal role in the development of Pakistan’s economy. Presently the auto industry has the capacity to produce 120,000 cars annually on a double shift basis. Car manufacturers in Pakistan over the last decade have contributed considerably towards employment generation. Car manufacturers in Pakistan and vendors employ around 150,000 to 200,000, people directly and indirectly. The Original Equipment Manufacturers (OEMs) have also been instrumental for transfer of technology, value addition and manpower development

. As a consequence of car manufacturing in Pakistan, a vibrant auto vendor industry has emerged that is now not only supplying parts to local OEMs like Toyota, Honda, Suzuki, Nissan, etc, but also exporting internationally.

Auto-part exports are approximately $20 million per annum. Due to the deletion policy, cars manufactured by OEMs now consist 50% to over 70% local components depending on the model. Over the year vehicles manufacturing has been among thefew industries thathavecontinued to attract local and foreign investment even when the investment climate in the country has not been very favorable. The development of the local car-manufacturing sector is a key element in the industrialization process. It must be remembered that the import of used cars as opposed to Complete Knock Down (CKD) parts would cause a major drain on Pakistan's foreign exchange and work towards retarding the overall growth of the engineering sector in Pakistan. The auto manufacturers in Pakistan are playing a significant role in the exports of the country. From July 2001-March 2002 auto parts exports have been to the tune of $27 million

Pakistan is an emerging market for automobiles and automotive parts, offers immense business and investment opportunities. The total contribution of Auto industry to GDP in 2007 is 2.8% which is likely to increase up to 5.6% in the next 5 years. Total gross sales of automobiles in Pakistan were Rs.214 billion or $2.67 billion in 2006-2007. The industry paid Rs.63 billion cumulative taxes in 2007-2008 that the government has levied on automobiles. There are 500 auto-parts manufacturers in the country that supply parts to original equipment manufacturers (PAMA members). Auto sector presently, contributes 16% to the manufacturing sector which also is expected to increase 25% in the next 7 years, as compared to 6.7 percent during 2001-02.Vehicles’ manufacturers directly employ over 192,000 people with a total investment of over $ 1.5 billion.

Currently, there are around 82 vehicles’ assemblers in the industry producing passengers cars, light commercial vehicles, trucks, buses, tractors and 2/3 wheelers. The auto policy is geared up to make an investment of $ 4.09 billion in the next five years thus, making a target of half a million cars per annum.

Impacts Of Automobile industry

Automobiles have revolutionized our lives. It has helped in reaching at our destination in less time. But this invention has many impacts, some are positive and some are negative. Some of the impacts are given below.

Impacts on Access and convenience

Page 8

Analysis of Automobile Industry of Pakistan

Worldwide the automobile hasmade easier access possible to remote places. However, average journey times to regularly visited areas have increased in large cities, especially in Latin America, as a result of widespread automobile adoption. This is due totraffic congestion and the increased distances between home and work brought about by urban expansion.

Deaths in Road Accidents

However the adverse effects of automobiles are in the form of accidents. Many people have lost their lives in these road accidents and a large number of people have become permanently paralyzed in these accidents.

Impacts on Society

1. Created a more mobile society: Cars broke down the difference between urban and rural society. The automobile brought the new tradition of the "Sunday drive," and many city folks got their first chance to tour the rural areas. Rural people, on the other hand, drove into cities to shop and to be entertained.

2. Broke down the stability of family life: Now it is much easier for individual family members to go their own way. They are now less dependent on each other especially the women.

3. Broke down traditional morality: Children could be freed from parental supervision as cars became a sort of "bedroom on wheels." Now they can freely move on their own accord.

4. Changes to urban society: In the start of 1940s, most urban environments lost their streetcars, cable cars, and other forms of light rail, to be substituted by diesel-burning motor coaches or buses. Many of these have never returned, though some urban communities alternatively installed subways.

Another change caused by the automobile is that modern urban pedestrians must be more alert than their ancestors. In the past, a pedestrian had to come across relatively slow-moving streetcars or other obstacles of travel. With the multiplication of the automobile, a pedestrian has to anticipate safety risks of automobiles at high speeds because cars may cause serious damage to a human.

5. Advent of suburban society:

Because of the automobile, the outward growth of cities increased, and the development of suburbs in automobile intensive cultures was accelerated. Until the start of the automobile, factory workers lived either close to the factory or in high density communities farther away, linked to the factory by street car or rail. The automobile and the federal subsidies for roads and suburban development that supported car culture made people to live in low density areas far from the city center and integrated city neighborhoods.

6. Car culture:

The car had a significant influence on the culture of the middle class. Automobiles were incorporated into all fields of life from music to books to movies. Between 1905 and 1908, more than 120 songs were based on the automobile. Since the start of the automobile, car manufacturers and petroleum fuel suppliers successfully lobbied governments to build public roads.

Page 9

Analysis of Automobile Industry of Pakistan

Major Policies after year 2005

1. Auto Industry Development Program (AIDP).2. Tariff Based Systems (TBS)

July 1st 2006, the deletion programs for the Automotive Sector have been replaced by the Tariff Based System (TBS).The deletion programs have gradually been phased out under the WTO regime to become TRIMs compliant. The TBS is the outcome of a long drawn consultative dialogue between all stakeholders including OEMs and Vendors, belonging to different sub-sectors of the Automobile Industry. The TBS has been developed with the following overriding objectives:

Preservation & promotion of technologies that have been developed in the country

Protection to the present job structure in the auto sector. Promote job creation Protect the existing & planned investment by the OEMs &

Vendors Promote new investment Expand the consumer base to create economies of scale

The basic framework of Tariff Based System is as under:

1. Imports in CKD condition would be allowed only to assemblers having adequate assembly facilities and registered as such by the concerned Federal Government Agency.

2. Parts/ components indigenized by June 2004 have been placed at higher rate of Customs Duty.

3. Parts not indigenized would be allowed at CKD rate of Custom Duty.

Introduction of Statutory Regulatory Order (SRO):

1. SRO 656 (I) / 2006 dated June 22, 2006 (For OEMs)2. SRO 693 (I) / 2006 dated July 1, 2006 (For OEMs)3. SRO 655(I) / 2006 dated June 22, 2006 (For Vendors)

For the purpose to handle the switching from ISDP to TBS and to ensure stable policies the consultations on the development of AIDP kicked off from the 8th March, 2006 Workshop at

Islamabad by clearly defining the objectives at a time when the industry was switching over from the deletion programs to a competitive tariff based system. There was realization that the transition phase may affect the rapid growth and sustainable development of auto industry. A comprehensive development program with pre-announced tariffs to provide predictable and stable environment was therefore much needed and the finalization and approval of AIDP by the government was held on 13th November, 2007.

Page 10

Analysis of Automobile Industry of Pakistan

Automobile Industry Development Programme

Need and Urgency of AIDP:

Given its immense potential and with a fairly large vendor base and significant number of Original Equipment Manufacturers (OEMs), Pakistan’s auto sector needs to be anchored with a firm & sustainable policy regime determining its future direction, prioritizing interventions, delineating respective roles of stakeholders and putting in place an effective institutional mechanism for a regular assessment and review.

Pakistan auto industry needs to grow parallel with world industry through concerted efforts to take auto manufacturing to a self-sustaining level where they shall have volumes, generate requisite technology and meet evolving emission requirements.

Challenges posed by globalization, liberalization and increasing competition, demand an imminent need to review the strategic direction and policy framework for sustainable growth of the domestic automotive sector. This is crucial to maintain the competitiveness of participants in the automotive sector, for them to be viable in the long term.

The need for a development programme for the auto industry was realized at the time of elimination of local content conditions when the tariff policy has been a major instrument to push for the development of parts and components locally alongside encouraging the assembly of vehicles.

While formulating the AIDP following objectives were agreed;

• Long term investment • Encourage growth • Promote domestic competition • Enhance competitiveness • Stimulate innovation • Facilitate auto industry’s integration into the global supply chain • The used vehicles import policy will be regulated so as not to impede the growth of the local industry while protecting consumer interest.

In developing the AIDP few benchmarks were agreed with the stakeholders, which would lead the government to extend necessary facilitation and the industry to accept challenges of modernization and competitiveness.

AIDP encourages the companies to corporatize its affairs and to make their accounts transparent as certain incentives would be allowed only if the investment or technology acquisition has been duly capitalized in their financial statements. In the modern world, open companies attract more investment, strategic partners and global customers for its products. This intervention is expected to promote a culture and create an urge on the part of companies to become big and go glob.

Page 11

Analysis of Automobile Industry of Pakistan

Five Year Tariff Plan for Auto Sector

To achieve the laid down objectives of AIDP, government appreciated the need of predictable and stable tariff environment owing to a long gestation period for the investment to start giving returns and that vendors capacity development is time taking and investments can only take place once there is an element of certainty, predictability and consistency in the policies.

A predictable environment is also essential for the development of critical components, technology transfer and to achieve the goals of exports. With these objectives in view, government undertook a lengthy consultation process with the industry and kept the ground realities in view, predominantly the bare minimum protection, competition and the global environment of the automotive sector. Finally a five year tariff plan covering the import duties for the entire automotive sector and including the components, CKD kits and CBU’s were approved by the government at the time of budget 2007-08.

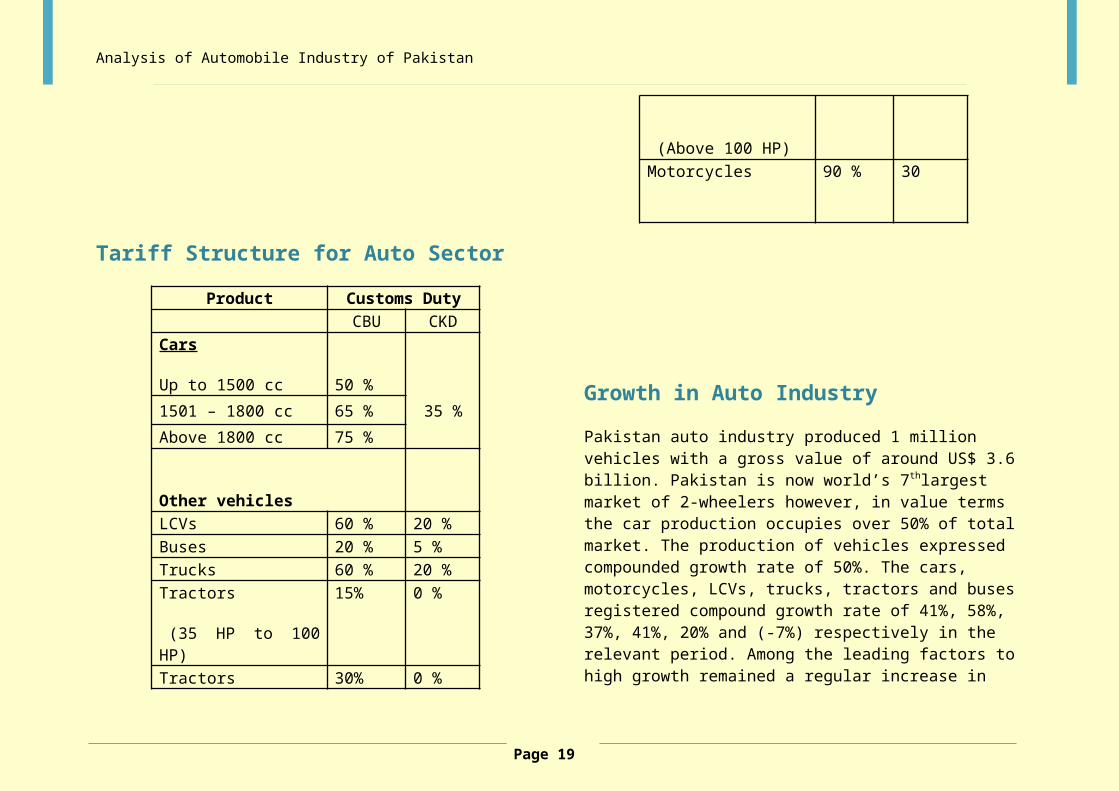

Tariff Structure for Auto Sector

Product Customs Duty CBU CKDCars

Up to 1500 cc

50 %

35 %1501 – 1800 cc 65 %

Above 1800 cc 75 %

Other vehicles

LCVs 60 % 20 %Buses 20 % 5 %Trucks 60 % 20 %Tractors

(35 HP to 100 HP)

15% 0 %

Tractors

(Above 100 HP)

30% 0 %

Motorcycles 90 %

30

Page 12

Analysis of Automobile Industry of Pakistan

Growth in Auto Industry

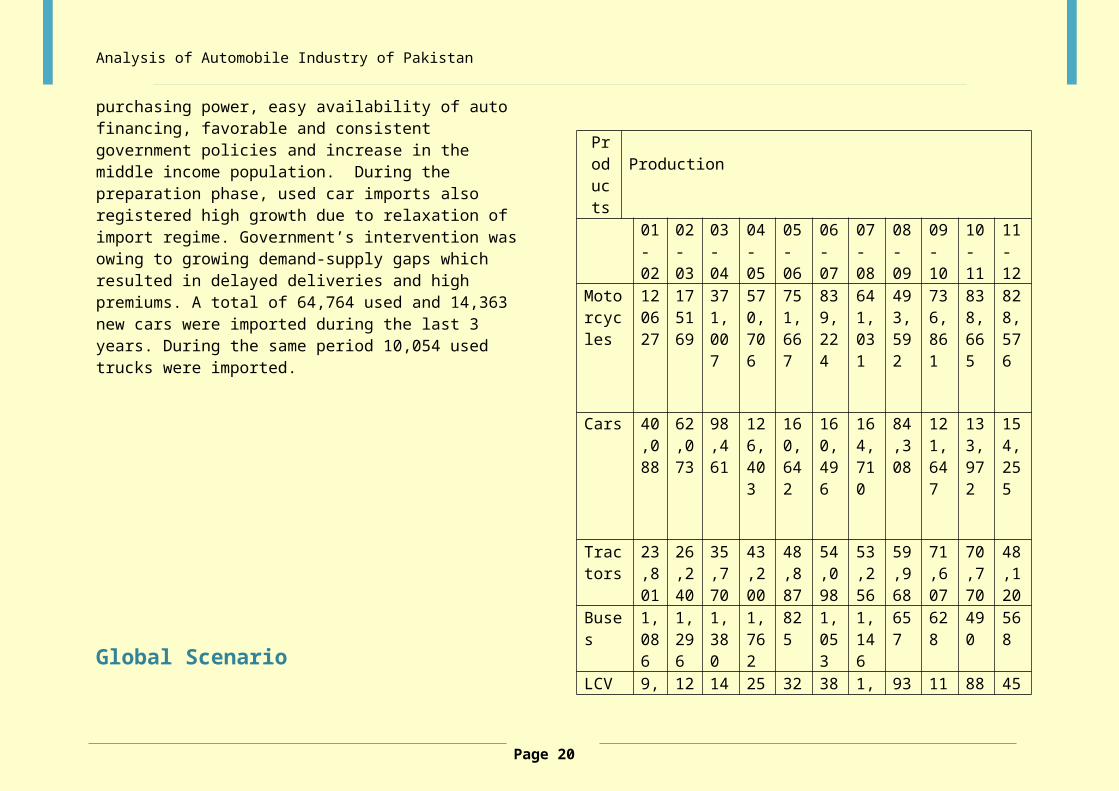

Pakistan auto industry produced 1 million vehicles with a gross value of around US$ 3.6 billion. Pakistan is now world’s 7thlargest market of 2-wheelers however, in value terms the car production occupies over 50% of total market. The production of vehicles expressed compounded growth rate of 50%. The cars, motorcycles, LCVs, trucks, tractors and buses registered compound growth rate of 41%, 58%, 37%, 41%, 20% and (-7%) respectively in the relevant period. Among the leading factors to high growth remained a regular increase in purchasing power, easy availability of auto financing, favorable and consistent government policies and increase in the middle income population. During the preparation phase, used car imports also registered high growth due to relaxation of import regime. Government’s intervention was owing to growing demand-supply gaps which resulted in delayed deliveries and high premiums. A total of 64,764 used and 14,363 new cars were imported during the last 3 years. During the same period 10,054 used trucks were imported.

Global Scenario

Products

Production

01-02

02-03

03-04

04-05

05-06

06-07

07-08

08-09

09-10

10-11

11-12

Motorcycles

120627

175169

371,007

570,706

751,667

839,224

641,031

493,592

736,861

838,665

828,576

Cars 40,088

62,073

98,461

126,403

160,642

160,496

164,710

84,308

121,647

133,972

154,255

Tractors

23,801

26,240

35,770

43,200

48,887

54,098

53,256

59,968

71,607

70,770

48,120

Buses 1,086

1,296

1,380

1,762

825

1,053

1,146

657

628

490

568

LCV s 9,055

12,548

14,896

25,177

32,053

38,490

1,590

932

1172

883

451

Trucks

1,134

1929

2022

3204

4518

4410

4993

3135

3425

2901

2597

Page 13

Analysis of Automobile Industry of Pakistan

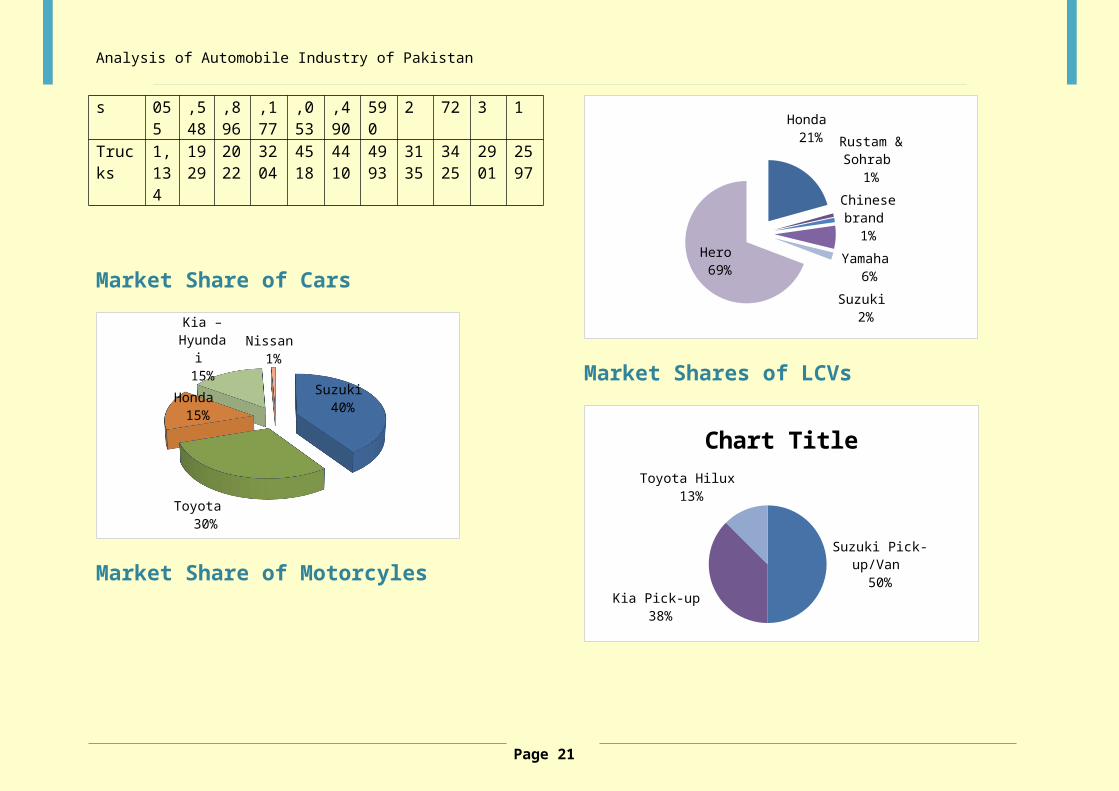

Market Share of Cars

Suzuki 40%

Toyota 30%

Honda 15%

Kia – Hyundai 14%

Nissan 1%

Market Share of Motorcyles

Honda 21%

Rustam & Sohrab 1%

Chinese brand 1%

Yamaha 6%

Suzuki 2%

Hero 69%

Market Shares of LCVs

Suzuki Pick-

up/Van 50%

Kia Pick-up 38%

Toyota Hilux 12%

Chart Title

Page 14

Analysis of Automobile Industry of Pakistan

Safety, Quality & Standards and Emission Control Policy

There are different laws and motor vehicle acts to ensure the roadworthiness of vehicles plying on the roads. Section 39 of the Motor Vehicles Ordinance 1965, and Section 35 of The Motor Vehicle Rules 1969, deals with the issue and renewal of certificate of fitness.Section 8 and Section 39 of MVR 1969; deal with issue of driving license and issue of duplicate certificate of registration and certificate of fitness respectively. MVR 1969 deals with details of body construction, essential equipment and requirements of maintenance of a motor vehicle. The emphasis of these laws is clearly on the management aspects and the safe operation of the vehicles. However, some sections deal with the environmental aspects or the emissions from the vehicles in a rather general way. Sections 154, 158 deal with the horns and noise, whereas section 163 deals with emission of smoke vapor of grease. The prohibition in these sections is of a general nature and no standards and testing procedures have been specified. On realizing the importance and development of Metallurgy, Standards,

This is believed that old vehicles are the gross polluters and can contribute up to 80% of the pollution load in the major cities.

The new vehicles with efficient technologies even deteriorate rapidly.The Government has been contemplating on Emission Control Policy for the locally produced or imported vehicles to

become EURO-2 compliant for the petrol and diesel vehicles by the 1st July, 2008 and 1stJuly, 2009 respectively.

Industry fears that the diesel fuel available in the country is not environment friendly because of high Sulfur and Benzene contents.

Government’s investment policies

The Government has liberalized the investment policy environment for domestic as well as foreign private investment in the industrial sector. There is no upper limit on foreign equity and foreign ownership of industrial projects. There is also no restriction on remittance of profit, dividends, payment of royalty and technical fee. The Government is also encouraging joint ventures, technology tie-ups, co-manufacturing and co-exporting arrangements with foreign investors. Even relocation of projects is being encouraged in view of theformation of developed economies into hi-tech areas. Major advantages for investment in Pakistan are as follows:

• Abundant land and natural resources

• Vast human resources

• Growing domestic market

• Well established infrastructure

• Strategic geographical location

Fundamental problems in the automotive sector are as follows:

Page 15

Analysis of Automobile Industry of Pakistan

• Low volumes / underutilization of capacity

• High prices

• Slow transfer of technology

In view of the above the government policy not only seeks to protect foreign investment but it is also looking for a breakthrough in the export market in order to increase volumes to lower costs by achieving economies of scale.

Auto Industry in Context to Manufacturing Sector

The share of manufacturing sector in GDP remains 19% which is low as compared to competing countries and the goals of job creation, exports, research and development, bringing innovations and technologies will remain un-attainable unless the manufacturing culture is promoted. The share of manufacturing to GDP has been targeted as 30% by the year 2030. While in manufacturing, shop floor efficiencies count more in the organic growth and sustainability of industry. This comes from the imaginative and skillful management and highly trained and productive workforce. The investment in productive assets and regular up-gradation of the existing facilities and reengineering of manufacturing processes at the shop floor to cut cost and minimize wastages will remain a growing issue for the industry. In the world ranking Pakistan ranks 91 in global competitiveness, 84 in quality competitiveness, 67 in business competitiveness and 99 in public institution ranking. While the technology index remains at 89.The burden of government regulations has however, come down to 55% from 94% of an year

ago. Besides achieving competitiveness, the major challenge faced by industry is to go to export of medium and high-tech products which at present are not more than 14%. Hence it is imperative to identify factors which are making manufacturing in Pakistan less competitive and to improve the productivity at level and scale. The following issues nevertheless will remain important for a competitive and sustainable development of auto industry.

i) The auto industry is generally faced by multiplicity of taxes; the presumptive tax regime has led to increase in prices of imported inputs and the finished goods. Component manufacturers are struggling to compete with under-invoicing, mis-declaration and smuggling.

ii) Imposition of Federal Excise Duty on the royalty and technical fee remitted to the suppliers of technology remains a potential barrier to innovation.

iii) High cost of capital and relatively difficult access for the small and medium enterprises and lack of any incentive in the financial policy for the auto industry.

iv) Manufacturing of modern machine tools and dies &molds and access to multi-axis CNC machines from developed world prevents high value addition and development of critical components.

v) Unpredictable demand and absence of coherent supply side measures to create sustainable demand for auto products in the backdrop of recent hike in interest rates.

Page 16

Analysis of Automobile Industry of Pakistan

vi) Increasing cost of energy and its unreliable and inconsistent supply adds up the cost of manufacturing and wastage of resources. It is in the year 2012, auto industry consumption of electricity cross 500 – 600 MW.

vii) To improve competitiveness, government and industry’s high focus is needed on investment in HRD, technology and productive assets and supply chain management.

viii) Benchmarking the performance of industry against the world practices, adopting best manufacturing practices and production techniques and producing globally acceptable quality products.

ix) Government to provide incentives for the international companies to bring their design houses in Pakistan. Fiscal support to establish testing laboratories and evaluation facilities and encouraging the local manufacturers of 2 / 3 wheelers to design the vehicles in the country is highly essential.

x) An all-embracing and consultative policy making with elements of stability and predictability through effective participation of industry in the policy formulation, implementation and review process.

MAJOR AUTOMOBILE ASSEMBLERS IN PAKISTAN

There are three major automobile assemblers of passenger cars dominating the Pakistani market with maximum business volume and annual production. In this study, the area of research is focused on the “Manufacturing Companies and Vendors associated with them”. Details are described as following.

a) Indus Motor Company Indus Motors have established a Joint Venture with Toyota Motors Corporation Japan, in 1993, to acquire essential training and knowhow for assembling Toyota and Daihatsu vehicles. Currently they are producing following vehicles.

Daihatsu Core – 1000 cc (production: 200-300 vehicles per month)

Toyota Corolla- 1300 cc and 1800 cc (production: 3000-3500 vehicles per month). Toyota Corolla Diesel – 2000 cc (production: 2000-2500 vehicles per month). Toyota Hilux – 3000 cc (production: 500-700 vehicles per month).

.

An average of only 45% parts of various models has been permitted to be developed locally by Toyota after their extensive test trials in Japan. Due to non-availability of expensive quality control equipment, all precision safety components are imported. Extensive training at all levels is being imparted locally at factory area in Karachi as well at dealerships throughout Pakistan. Highly trained

Page 17

Analysis of Automobile Industry of Pakistan

engineers and technicians are also sent to Toyota Behrens Training Centre.

b) Pak Suzuki Motor Company

Pak Suzuki was established as a Joint Venture with Suzuki Motors Japan, in 1982, to acquire essential training and knowhow for assembling Suzuki vehicles. Currently they are producing following vehicles.

Suzuki Mehran – 800 cc (production: 3000-3500 vehicles per month).

Suzuki Bolan – 800 cc (production: 3000-3500 vehicles per month).

Suzuki Alto – 1000 cc (production: 2500-3000 vehicles per month).

Suzuki Cultus – 1000 cc (production: 1500-2000 vehicles per month).

Suzuki Swift – 1000 cc (production: 50-100 vehicles per month).

Suzuki Liana - 1300 cc (production: 300-500 vehicles per month).

Due to the increasing demand of automobiles day by day and non-availability of strong competitors in local market, the company remains unable to meet the technological assistance requirements of local vendors to the desired level.

Averages of 65% parts amongst all products have been developed locally after their test trials. Due to non-availability of expensive

quality control equipment, many of the precision safety components are imported.

c) Honda Atlas Car

Atlas Group has established a Joint Venture with Honda Motor Company Japan, in 1994, to acquire essential training and knowhow for assembling Honda Cars. Currently they are producing following vehicles.

Honda Civic – 1600 cc (production: 2000-2500 Cars per month).

Honda City - 1300 cc (production: 1000-1500 Cars per month).

Honda Motor Company Japan is getting only 5% parts manufactured locally, due to non-implementationof Government policy (AIDP) forcefully and to avoid giving any design and manufacturing knowhow to local vendor industry. Honda has continued to import their vehicle parts. It can be a short term advantage for them.

Page 18

Analysis of Automobile Industry of Pakistan

Recently Production of Automobiles

The Production of cars and jeeps increased by 11.29 percent during the first eight months of the current fiscal year (2011-12) as compared to the production during the corresponding period of last year. As many as 96,268 jeeps and cars were produced during July- February (2011-12) against the production of 86,504 units during July-February (2010-11), according to data of Pakistan Bureau of Statistics (PBS).The production of Light Commercial Vehicles (LCVs) also increased by 7.43 percent during the period by going up from 12,000 units last year to 12,892 units during the current year. Production of busses increased from 308 units to 385 units, showing increase of 25 percent while the production of motorcycles during the period increased by 3.95 percent by going up from 1,058,613 units to 1,100,431 units, the data revealed. However, the production of tractors and trucks decreased by 54.88 percent and 8.30 percent respectively during the period. The production of tractors stood at 45,706 units last year to 20,624 units this year while the production of trucks decreased from 1,807 units to 1,657 units, according to the data. On month-on-month basis, the production of jeeps and cars surged by 21 percent during February 2012 as compared to the production of February 2011.The production of jeeps and cars during February 2012 stood at 13,269 units against the production of 10,967 units during February 2011.However, sharp increase of 44.74 percent was witnessed in the production of LCVs, output of which increased from 1,254 units during last February to 1,815 units in February 2012.Output of busses also surged by 277 percent during the month under review by going up from 30 units last February to 113 units during February 2012.Production of trucks also increased from 187 units last February to 214 units during February 2012, showing an increase of 14.44 percent in output.

But, motorcycle production during February 2012 witnessed negative growth of 2.51 percent by falling from 138,004 units during February 2011 to 134,536 units during February 2012.The output of tractors during the month under review also declined by 19.75 percent by falling from 7,138 units to 5,728 units, the data revealed. It is pertinent to mention here that the overall industrial production witnessed 1.78 percent growth during the first eight months of the current fiscal year. The Industries monitored by Ministry of Industry and Provincial Bureaus of Statistics witnessed positive growth of 1.3 percent and 0.64 percent respectively while the indices provided by the Oil companies Advisory Committee (OCAC) witnessed negative growth of 0.15 percent. The Indices of Ministry of Industry increased from 108.66 last year to 110.68 units this year while the indices of Provincial Bureaus of Statistics increased from 120.84 points to 124.02 points.

Pakistan produces 500,000 cars by year 2011

Pakistani government has introduced a five-year Auto Industry Development Plan (AIDP) aiming to increase local production of cars from 200,000 in fiscal year 2005-06 to 500,000 in 2011, a cabinet minister said Wednesday. The development plan will help make local auto industry more competitive, create capacity for local design and innovation, domestic competition, human resource development and auto cluster development, said Jahangir Khan Tareen, Pakistani federal minister for Industries, Production and Special Initiatives, according to state-run Associated Press of Pakistan. He expressed these views during a meeting with top leaders of the major Car Assemblers in Pakistan, including Toyota Indus Motor, Suzuki and Honda, according to the APP report. Under the AIDP, the used car import policy will be regulated so as not to impede the growth of local industry while protecting the consumer

Page 19

Analysis of Automobile Industry of Pakistan

interests, the minister said. It was agreed during the meeting that indigenization of the local auto industry will be done as required under the AIDP, according to the report; with the minister saying that the government is keen to bring indigenization in the local auto industry. The Assemblers were reportedly in agreement with the Ministry on almost all the points of the AIDP draft.

The automobile industry in Pakistan has witnessed tremendous growth during the last few years. The car production rose to almost 200,000 units by end 2005-06 from about 40,000 in the year 2002-03.

The Story of a Chinese Car

Imported in Pakistan on a mass level, this is the story of a world class car with a Chinese origin. This car was the symbol of excellence in the entire world of auto engineering but reduced to a mere run-of-the-mill auto due to monopolized market conditions prevailing in our country. The story, basically, revolves around big investment, marketing, distribution and then production plans of the sole distributor and importer of a particular Chinese brand of automobile in Pakistan. The story goes that newly-introduced in Pakistan in early 2000; this car was rated as one of the safest cars with all safety features that are normally found in premium upper category cars. It applied the philosophy of the sophisticated European design with fashionable sweeping lines, which lends the body of the car a sense of motion. It was the perfect and complete outfit together with the outstanding function and performance offering a terrific driving experience and of freedom of motion as well. Ranked number 1 in the prestigious J.D. Power China Initial Quality Study for 2004, the car was widely

acknowledged as the outcome of world’s best engineering and workmanship.

This car was introduced in the local market with a 50,000 km/two years comprehensive warranty with numerous safety features such as collapsible steering, side-impact door beams, reinforced passenger compartments, reinforced impact front/rear bumpers, rear for lamps, high mounted brake lamps, and an entire line-up of additional security safety features that made this car as the safest compact car on the roads, ever found in our country. In addition, this car also had a special feature in steering as it has a double-shock feature, thus saving driver and passengers from deadly accidents.

This was the only car that possessed a dual overhead cum multi-point fuel injected engine system in its category in Pakistan, while delivering the most power and best fuel efficiency in its class. The car allowed its owner and passengers to travel with the utmost safety and class with an equivalent consumption of petrol to that of consumption of CNG. As compared to major car manufacturers and auto sellers in Pakistan, this car had an advantage, which was its highest quality and lowest prices. Manufactured by using only the highest quality parts as per the most stringent technological standards, the manufacturing company behind this car was one of the fast growing automobile companies in the entire Asian pacific region.

The car could also be converted into a pick-up or a small truck for the transportation of goods. This car was available to local Pakistani buyers with 2 years warranty compared with 11-months warranty as offered by leading auto manufacturers and car dealers in Pakistan.

Page 20

Analysis of Automobile Industry of Pakistan

This car was, all in all, suitable to Pakistani climate, and it was vigorously tested before inducting in the local market.

The Shattered Dreams

Given that the market in Pakistan is saturated by automobile assembly plants and importing companies, the manufacturer of this car had a plan to invest $42 billion in Pakistan by setting up a car manufacturing plant. The proposed plant would give employment to 5,000 to 10,000 people in the country, and for this purpose the Chinese car manufacturer required a 100-acre plot of land for the proposed plant, wherein 50-acres of the land was supposed to be used for setting up a free hospital also. While the whole country is already ruled by land mafia and encroachers, this car manufacturer was not given the required land for industrial purpose. Furthermore, the investor also came in Pakistan with a plan to develop an automobile engineering college for producing trained and qualified engineers, but this was also ended up in vain. The End Result: This car came into the Pakistani in the early years of the last decade with an aim to sell off each car in just 179,000 thousand only to end consumers. Thanks to excessive custom duty which was generously levied by the custom department, total pricing of each car jumped to 479,000 thousand from the figure of 179,000.This little example shows how ‘friendly business environment’ this country offers to foreign investors and automobile manufacturers. Along with that, this also shows the monopolized market conditions where banks and financial institutions in collaboration with leading auto manufacturers play a nasty game by restricting this wheeled convenience to a certain class.

Pakistan’s auto industry is one of the most critical industrial sectors of the country, entrusted with the task of promoting the economic and commercial interests of the state and crucial in the effective but rapid growth of entire national economy to a large extent. This sector has a prominent and sensitive role to play in the realization of the objectives laid out in the Auto Industry Development Programme (AIDP), especially those directly affecting the imports and exports of cars and rest of the commercial vehicles.Throughout the world, auto manufacturing units are required to take into account the global changes in e-commerce and digital economy at a time when the countdown to implementation of green technologies has started. In fact, the emergence and re-emphasis on green culture had turned the concept of traditional commerce upside down and revolutionized auto manufacturing procedures progressively. Auto manufacturing units and manufacturers in our country should realize the importance of following international manufacturing protocols to improve performance of auto manufacturing units in order to serve common interests or else, those who have not yet adopted policies to guarantee their smooth entry to the modern age of technology will be left behind in the future.

Page 21

Analysis of Automobile Industry of Pakistan

Auto Sector Exports

Pakistan auto industry because of the country location and a diversified range of products and particularly in the 2-wheelers, low engine capacity and fuel efficient cars & LCVs and tractors along with auto components has the export potential. The industry has been barely meeting the local demand while the increasing growth has convinced the principals to expand. The 2-wheelers have entered into export market followed by tractors though indirectly, and few models of Suzuki Motor Car and components are in the process of confirming the export orders. In the next phase, Pakistan auto industry is expected to position itself in the auto services and an attractive out-sourcing hub for the manufacturing of forgings, castings, wire- harnessing and machining of components.Industry foreign exchange neutral by the year 2012. Government will continue facilitating the industry to develop market and product know how, industry participation in major trade fairs, enabling fiscal policy, capacity building and due recognition to the exporters. During April-March 2012, the industry exported 2,910,055 automobiles registering a growth of 25.44 percent. Passenger Vehicles registered growth at 14.18 percent in this period. Commercial Vehicles, Three Wheelers and Two Wheelers segments recorded growth of 25.15 percent, 34.41 percent and 27.13 percent respectively during April-March 2012. For the first time in history car exports crossed half a million in a financial year. In March 2012 compared to March 2011, overall automobile exports registered a growth of 17.81 percent

Domestic Sales

The growth rate for overall domestic sales for 2011-12 was 12.24 percent amounting to 17,376,624 vehicles. In the month of only March 2012, domestic sales grew at a rate of 10.11 percent as compared to March 2011. Passenger Vehicles segment grew at 4.66 percent during April-March 2012 over same period last year. Passenger Cars grew by 2.19 percent, Utility Vehicles grew by 16.47 percent and Vans by 10.01 percent during this period. In March 2012, domestic sales of Passenger Cars grew by 19.66 percent over the same month last year. Also, sales growth of total passenger vehicle in the month of March 2012 was at 20.59 percent (as compared to March 2011). The first time in history car sales crossed two million in a financial year. The overall Commercial Vehicles segment registered growth of 18.20 percent during April-March 2012 as compared to the same period last year. While Medium & Heavy Commercial Vehicles (M&HCVs) registered a growth of 7.94 percent, Light Commercial Vehicles grew at 27.36 percent. In only March 2012, commercial vehicle sales registered a growth of 14.82 percent over March 2011.Three Wheelers sales recorded a decline of (-) 2.43 percent in April-March 2012 over same period last year. While Goods Carriers grew by 6.31 percent during April-March 2012, Passenger Carriers registered decline by (-) 4.50 percent. In March 2012, total Three Wheelers sales declined by (-) 9.11 percent over March 2011.Total Two Wheelers sales registered a growth of 14.16 percent during April-March 2012. Mopeds, Motorcycles and Scooters grew by 11.39 percent, 12.01 percent and 24.55 percent respectively. If we compare sales figures of March 2012 to March 2011, the growth for two wheelers was 8.27 percent.

Page 22

Analysis of Automobile Industry of Pakistan

Productive Asset Investment Incentive

Productive Asset Investment Incentive (PAII) is expected to stimulate the investments in the production capacities of auto parts manufacturing and to optimally utilize such capacities through supply of output to the vehicle assemblers in the country. PAII is to essentially bring competitiveness in the vehicle manufacturing without disturbing the pre-announced tariffs which provide due protection to the locally manufactured auto parts.

Objectives

i) To expand and modernize capacities in auto parts manufacturing.

ii) To encourage localization of auto parts for the local production of vehicles and for

Export.

iii) To encourage development of critical components and achieve competitiveness.

iv) To promote interdependence between assemblers and auto parts manufacturers.

Incentives

i) PAII will be in the form of customs duty credit equal to a certain percentage of the value of productive assets installed by the eligible auto parts manufacturers. The duty credit so acquired will be spread equally over a period of 5 years to offset duty on eligible imports.

ii) The duty credit will be transferable to vehicle assemblers and will remain non-trade-able in the open market.

iii) Duty credits so earned would be allowed to offset import of inputs and further productive assets by a parts manufacturer or by assemblers against import of CKD kits and tooling.

Eligible Entities

The entities fulfilling the following criterion will be considered eligible to avail the incentive under PAII:-

i) The auto parts manufacturers must be supplying or contracted to supply to the recognized vehicle assemblers or export market.

ii) The assemblers of vehicles will be allowed the benefit to the extent of in-house parts manufacturing only.

iii) Must be registered with the sales tax department.

iv) Must be a limited liability company.

v) Having suitable in-house facilities to manufacture auto parts.

vi) The company offering itself for full disclosure and detailed scrutiny at any time during the currency of scheme

Page 23

Analysis of Automobile Industry of Pakistan

Investment and manpower employment

• Foreigninvestment US$ 1.50 billion

• Localinvestment US$ 1.00 billion

• Number of vendors 200

• Leadingvendors 20

• Exportingvendors 10

• Number of jobs, in industry 140 000

Technology Acquisition Support Scheme

Technology levels remain low to medium in the auto parts manufacturing primarily due to high cost of technology acquisition.

Automotive industry has seen a considerable growth but most of the parts manufacturers are still using old manufacturing methods.

With such low technology levels, competitive production at high volumes and entering into export markets is a difficult task.

Eligibility Criterion

Following are the eligible criterion under this scheme:-

i) Procurement of technologies through licensing.

ii) Technology to be acquired includes design, manufacturing know how, technical support, quality improvement and training.

iii) Procurement of patents or manufacturing rights and registered design.

Local content scheme

Pakistan has been pursuing a useful local content scheme which has done some good to the technological base of the automotive sector and improved its design development capabilities. The methodology adopted is that the manufacturers are offered tariff incentives for progressive local manufacture of automobiles and other engineering goods. Under this programme, the achieved levels of local content are as follows: Maximum local content levels achieved.

Automobile and Percentage

Cars 68 %

Tractors 85 %

Motorcycles 82 %

LCVs 43 %

Buses/Trucks 50 %

Page 24

Analysis of Automobile Industry of Pakistan

Human Resource Development

The rapid growth in Auto Sector is difficult to sustain without efficient human resource. Presently the industry is faced with the acute shortage of trained engineers, supervisors and workers at the level of assembly operations as well as parts manufacturing.

The deficiency of skilled personnel is more on account of rapid growth of the Auto Sector during the last 6 to 7 years.

High defect rate, low innovations, delayed supplies and quality issues are more on account of weaker human resource than to any other factor. Where the top management in the small to medium entities lacks the overall business management skills, the engineers produced by the universities seriously lack analytical skills and a thinking mind.

Auto Cluster Development

The assemblers of vehicles are mostly located in and around Karachi and Lahore. The car and HCV assembly is mostly based in Karachi while the 2-Wheelers/ 3-Wheelers and agricultural tractorsare located in Lahore. The same is the case with the vendors of such vehicles except that many vendors of car/ LCV are based in Lahore as well. The vehicle assemblers play a pivotal role in development of vendors through knowledge transfer, supply chain management, products and processes development.

In view of above two Auto Clusters are envisaged:-

• Near Steel Mills, Port Qasim, Karachi.

• Near Motorway or on Sheikhupura Road, Lahore.

Area:

Karachi 200 Acres

Lahore (initially):200 Acres.

Auto Industry Investment Policy

Seeing the considerable interest of important international auto manufacturers in Pakistan market and to meet the local demand supply gap of various products, Government has framed the rules and procedure for the foreign investors in the Auto Sector. The policy rest on production of high technology products with environment and consumer satisfying features.

Eligibility criterion

i) In case of cars, the potential new entrant will have 500,000 units annual production in countries other than Pakistan.

ii) The new entrant will have significant global presence by way of manufacturing at least 25,000 units of trucks and buses separately, 40,000 LCVs and at least 50,000 units in the case of Agriculture Tractors annually in countries other than Pakistan.

iii) New entrant will have the plan for the progressive manufacturing of vehicles.

Page 25

Analysis of Automobile Industry of Pakistan

iv) New entrant will have serious and demonstrable intention to develop parts locally either in-house or through the vendors to achieve competitiveness.

v) New entrant will clearly identify the destinations in his plan or in agreement with its partners for export of vehicles and parts manufactured in Pakistan under this policy.

vi) Proof of land acquisition in the case of green field project or an agreement with the owner, in the case of existing assembly facilities.

vii) A qualifying New Entrant will be required to submit a detailed business plan to EDB who will verify the complete in-house assembly/manufacturing facilities etc.

ix) AIDC will assess the business plan and other relevant documents to determine the eligibility criterion and to qualify the potential new entrant for the entitlement of benefits under AIIP or otherwise.

Benefits

New Entrants will be allowed to import 100% CKD kit, at the leviable customs duty, for a period of three years from the start of assembly/manufacturing.

Page 26

Analysis of Automobile Industry of Pakistan

Pakistan Automobiles Stories of Success

In times of great distress for Pakistan, where various influential sectors have been facing the wrath of global recession, escalating inflation and deteriorating value of rupee against dollar; the auto industry has been constantly increasing their investment in Pakistan. This is happening at a time where various businesses are moving out of Pakistan and establishing in neighbouring countries which provide a comparatively stable environment to conduct business in.

During the first four months of the current fiscal year 12, the automobile industry registered an increase in output of approximately 10 per cent as compared to the corresponding time span in the year before. Among this growth, the total production of various jeeps and cars was amounted to 49,558. These figures experienced an increase of 12 per cent in the production of cars, as against the 44,261 jeeps and cars which were produced in July-October of the fiscal year 11.

Also, during this period the production of Light Commercial Vehicle increased by 718 units, standing at 6371 units and observing a growth of 12.70 per cent. Similarly, the production of motorcycles also unearthed an increase of 9.5 per cent.

However, while comparing the two periods on a month-on-month basis, the data of October 2010 compared to the data of October 2011 saw a growth of 32.31 percent, 17.97 per cent and a negative growth of 7.43 per cent in the production of jeeps and cars, light commercial vehicles and motorcycles respectively. The production of motorcycles slipped down to 128,431 units compared to the 138,733 units during October 2010.

Page 27

Analysis of Automobile Industry of Pakistan

Pakistan Automobiles Losing Hope

Pakistan auto industry including manufacturers of automobiles and their parts lost their last hope when the cabinet recently approved a negative list for trade with India which will be phased out by the end of this year, believing this will massively hurt the country’s auto industry.

After months of deliberations with different industries and inter-ministerial dialogue, the government finally gave the go-ahead to the negative list containing 1,209 items, replacing the positive list, in an attempt to boost trade between the two countries.

The government had been facing strong resistance from different sectors which believed that the negative list should be phased out gradually over a number of years so that it would not hurt the domestic manufacturing industry. Among top advocates of the go-slow policy was the automobile industry.

It may be recalled that auto industry has already been facing difficult times due to consistent depreciation of rupee versus Japanese Yen and increasing prices of steel in international market. According to the latest numbers released by the Pakistan Automotive Manufacturers Association (PAMA), car sales during 8 month FY12 rose by 16 percent to 111,898 units compared to 96,142 units in same period last year.

The volumetric growth primarily stems from, June to July deferred sales to avail the benefit of reduce tax structure announced in Federal Budget FY12 and Yellow cab scheme announced by the Punjab Government.

The growth primarily resides in below 1000cc segment with 1000cc segment depicting a growth of 35 percent and 30 percent growth in 800-1000cc segment. Sales in 1300cc and higher segment have remained muted, depicting a growth of 1 percent in the period under-review.

In the month of February car sales stood at 14,962 units up by 12 percent as compared to 13,375 units in the same month last year, while are on the same levels as that of last month.

On company wise basis, Pakistan Suzuki Motor Corporation (PSMC), which is a major player in the lower cc segment, continued to depict strong growth of 35 percent in 8MFY12 to 70,162 units versus 52,067 units seen in same period last year. Mehran and Bolan, prime beneficiary of announced yellow cab scheme, are showing a robust sales growth of 47 percent and 47 percent, respectively.

Moreover, sales of comparatively new comer Swift has reached 4,500 units in 8MFY12, up 86 percent as compared to 2,420 units sold in the same period last year. Overall, company’s market share has improved to 63 percent in 8MFY12 as against 54 percent in the same period last year.

Decline in Sales and Revenue

Unfortunately, the recent downward trend in auto sales (cars + LCVs) continued as auto sales stood at 27,034 units for July-September 2008, showing a decline of 44 percent year-on-year, the data released by Pakistan Automobiles Manufacturers Association (PAMA) shows.

Page 28

Analysis of Automobile Industry of Pakistan

Automobile grew from 2001-2007, the industry and the government of Pakistan fixed a target of over half million units’ production by the year 2011-12 that now seems out of reach. The industry slightly fell short to achieve the targeted productions in 2006-07 when 1, 95,688 cars were manufactured against a target of 2, 26,620 units. However, there was some growth in production that year. In 2007-08 the production declined to 1, 87,634 units against a projected target of 2, 66,543 units. In the current fiscal year they said the production is expected to decline to 1, 50,107 units that are half the projected target of 3, 13,486 units.

Despite an additional levy of 5 per cent excise duty, the revenues from automobile sector would decline by over 25 per cent this year due to declining demand. The industry paid Rs.63 billion cumulative taxes that the government has levied on automobiles. This year, despite additional duty the sector would hardly contribute Rs50 billion in the national exchequer.

Challenges

The auto industry face the challenges of developing products at lower cost and achieving economies of scale, development of technical and human resource, stimulating domestic demand, research and development and exploiting the international business opportunities.

Achieving these goals will rest on reaching a critical mass of production, high quality of products and improved production techniques through acquisition of appropriate technologies, development of safety and standards and environment friendly vehicles.

The government role through a stable and predictable policy environment and ensuring maximum participation of auto industry in formulation, implementation, assessment and review of the policies however, will remain a critical factor in the sustainable development of auto industry.

The role of OEM’s in acquiring technologies, developing and improving the quality of products for local fitment and export will remain a crucial factor.

The development of infrastructure, like roads, highways & bridges, parking bays, ensuring the strict implementation of traffic rules, drivers training & licensing, effective motor vehicle registration and examination systems, necessary amendment in Motor Vehicle Act and compulsory insurance will determine the efficient road map for sustainable development of auto industry.

CURRENT SITUATION AND THREATS

The auto sector faced a big blow in 2008-09 when the world saw its biggest financial crisis, sales fell to 82,844 units. However Pakistani auto and allied sector quickly took to the path of recovery.

The good agriculture support prices set up by the government and the high remittances spurred in growth in the automobile industry. However in two years' span the industry grew at an average growth rate of 26.5 percent and sales reached a level of 127,944 units in FY11.

Page 29

Analysis of Automobile Industry of Pakistan

In the first eight months of FY12 the sales for passenger cars stood at 98,252 units. The biggest engineering sector of Pakistan however has to face a lot of problems.

The debilitating power crisis is the biggest concern of manufacturing sector. In addition, rising fuel price has pushed up the cost of production. The devaluation of rupee against Yen, which has spiked up the input costs and foreign exchange risk, is also of the utmost concern for the sector, because of its dependency on the import of critical parts from Thailand, Japan, and Korea etc.

Apart from these costs auto-sector also has to face the inconsistent and irrational government policies. Furthermore, overnight changes, lack of long term vision and thorough research before policy division and improvisation is also impeding growth of the sector.

In addition to the un-favorable import policies and almost no efforts by the government to stop the influx of smuggled auto parts, which were already putting the sector under immense pressure, now the industry, especially the allied sector can face stiff competition from the India due to the MFN status.

Secondly the favorable new entrant policy is threatening the sector, as the existing players fear that Chinese manufacturers would come in and take a sizable portion of the market.

Page 30

Analysis of Automobile Industry of Pakistan

SWOT ANALYSIS

Strengths

Increasing Demand for Cars:In Pakistan context there are 9 cars in 1,000 persons which is one of the lowest in the emerging economies which itself speaks of high potential of growth in the auto sector and more so in the car production.Rising per capita income with changing demographic distribution and an anticipated influx of 30 to 40 million young people in the economically active workforce in the next few years provides a stimulus to the industry to expand and grow.

Resale of Local Assembled Cars:Resale of locally assembled cars is better due to availability of spare parts and after sales services and warranty.Used imported cars have been selling below their cost at the showrooms for the last six months but consumers are not inclined to buy because of their low re-sale value and problems in parts availability.

Quality of local cars:Initially when the import of cars was liberalized the quality of local assembled cars was unsatisfactory so the people of high income level group started buying imported cars and the sales of the local assembled cars started decreasing so the local assemblers started enhancing the quality of their vehicles so we can say that the quality of local cars is becoming the strength of the auto industry.

OEM:The local OEM of Pakistan is well equipped with enough advance technology and skilled labor to produce parts according to the desired quality of any foreign company.

CNG kit:The advantage of buying local assembled cars is that they comes with factory fitted CNG kits at the times when the prices of fuel rising at higher pace internationally.

Mechanics:For local assembled cars mechanics are readily available in market and much cheaper so the buyer has not to worry about any problem that can occur in the car in long term whereas the availability for imported cars is a bigger issue for the owners and if somehow they are able to find one then the mechanics charges much higher than actually it should be charged.

Page 31

Analysis of Automobile Industry of Pakistan

Weakness

WTO—Deletion program:THE World Trade Organization (WTO) has rejected Pakistan’s request for the extension of the deletion program which enabled it to lay down the condition of the local content requirement (LCR). Under LCR, the automobile and other engineering industry was required to use locally manufactured parts and accessories in terms of government’s deletion policy. The condition of the LCR was an aberration to the Clause 5.2 of the WTO Agreement on Trade Related Investment Measures (TRIMs), Article III–-National Treatment under the GATT, 1994.WTO’s decision for not extending its deletion program / LCR condition has varied impact on Pakistan’s vendor industry, automobile assemblers, car users and the government.

Input Cost:In Pakistan as the inflation is increasing so as the input costs and for manufacturers it is becoming harder to produce at lower cost. Increasing cost of energy and its unreliable and inconsistent supply adds up the cost of manufacturing and wastage of resources. It is estimated that by the year 2012, auto industry consumption of electricity will cross 500 – 600 MW from around 250 - 300 MW, as of now.

Protection level:Before the TBS was introduced the auto industry was well protected by the government but now as the import of CKD and CBU is liberalized the protection level to industry by government is decreased.

Lack of skilled manpower for modern machinery:In Pakistan conventional machines are not able to meet the precision manufacturing and the available labor is not familiar with modern technology it caused by lack of coordination and linkages with Government/Semi Government Supporting Bodies and Technical Training Institutes

Scarcity of raw material especially steel:Through previous years the world prices are rising and causing costly inputs and Pakistan has left with scarce Steel and Iron left, so manufacturers are facing difficulties in producing cars with low price

Opportunities& Threats

Opportunities

Import German technology and skills:EDB wanted to build a Pakistan-German automotive supply network, providing opportunities to Pakistani automotive vendor enterprises to benefit from the German know-how and technology to improve quality, productivity, developing and marketing of value-added products.

Foreign Investment and setup production facilities:China National Heavy Duty Truck Corporation (CNHDTC), one of the largest heavy duty truck manufacturers in China, has shown interest for investment in the automobile sector of Pakistan. The study is required to attract players from Germany as well as from other countries to develop business with the Pakistani counterparts.

Page 32

Analysis of Automobile Industry of Pakistan

Bagasse Fuel:As the fuel prices are rising in world Pakistan should switch to Ethanol Fuel as Brazil is using. Ethanol Fuel is produced by Molasses. Pakistan is one of the country which produces good quantity of molasses but the engines of the local cars do not support ethanol so Pakistan should acquire the Technology to produce ethanol compatible cars. In Brazil they use 90% Ethanol and 10% petroleum whereas Pakistani cars with default engines can afford only 3% Ethanol.

Global spare part market:The annual gross sales turnover of the auto industry, at present, stands at Rs210 billion while export of auto parts are estimated at $35 million. As such, the increase in production turnover is projected to increase by 185 per cent while the exports of auto parts would make quantum jump.

Threats