analysis of global aerospace, defence and civil security markets

DESCRIPTION

Frost & Sullivan Analysis of Global Aerospace, Defence and Civil Security MarketsTRANSCRIPT

360 Degree CEO Perspective Series

Analysis of Global Aerospace, Defence and Civil Security Markets

“Partnering with clients to create

innovative growth strategies”

Julius Yeo

Consultant

2© 2010 Frost & Sullivan, All rights reserved www.frost.com

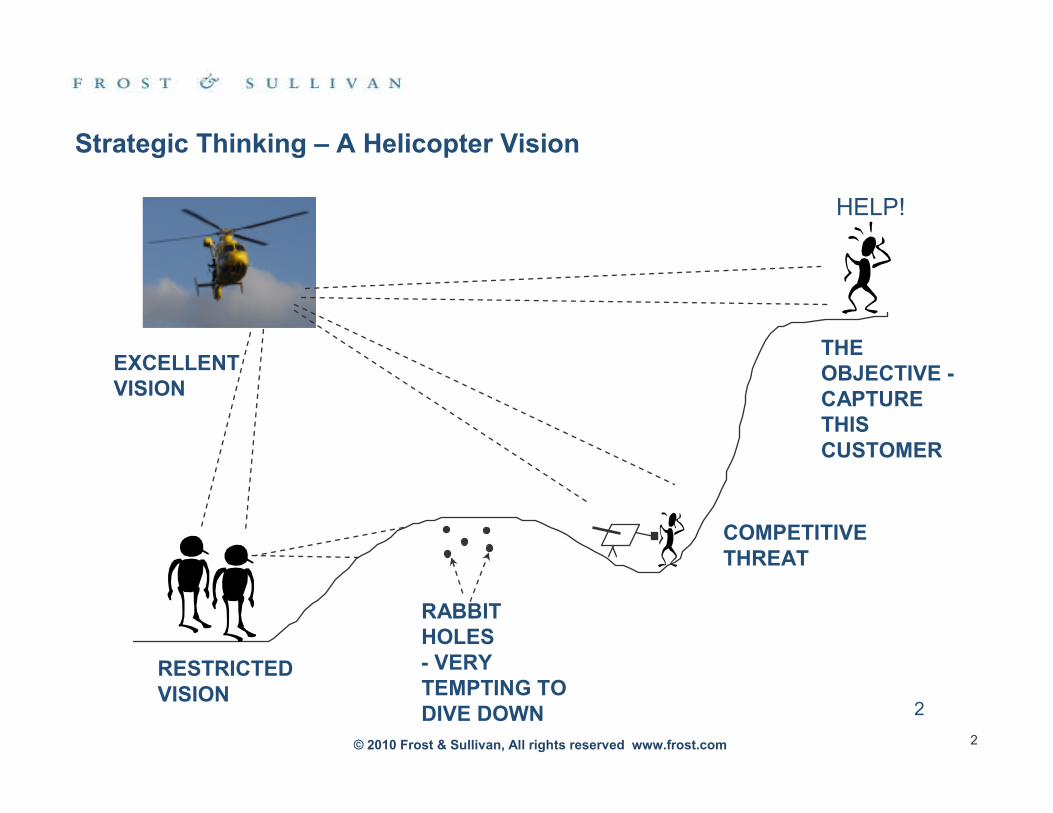

HELP!

THE OBJECTIVE -CAPTURE THIS CUSTOMER

COMPETITIVE THREAT

RABBIT HOLES - VERY TEMPTING TO DIVE DOWN

RESTRICTED VISION

EXCELLENT VISION

2

Strategic Thinking – A Helicopter Vision

3© 2010 Frost & Sullivan, All rights reserved www.frost.com

Key Issues Impacting Industry Today

� Top line growth facing headwinds, Commercial aerospace and Defense cycles peaking

� Change of US administration and shifting defense procurement priorities across US and

NATO

� Secular Asian growth drives need for exposure across entire industry

� PMA and MRO models evolving

� Increasing industry consolidation, European firms building presence in US defense market,

Asian firms expanding globally

� Maintaining earnings growth as cycles slow, managing costs and margins

� Effective position in homeland security market to maximize opportunities

4© 2010 Frost & Sullivan, All rights reserved www.frost.com

Table of Contents

Global Analysis Aerospace,

Def ence and Ci vil Security

Markets

Global Overview of the Commercial Aerospace Market

Emerging Trends in Defence

Emerging Trends in Civil Security

Emerging Trends in Commercial Aviation

Conclusions and Recommendations

Global Overview of the Defence Market

Global Overview of the Civil Security Market

5© 2010 Frost & Sullivan, All rights reserved www.frost.com

Global Overview of the Defence Market

6© 2010 Frost & Sullivan, All rights reserved www.frost.com

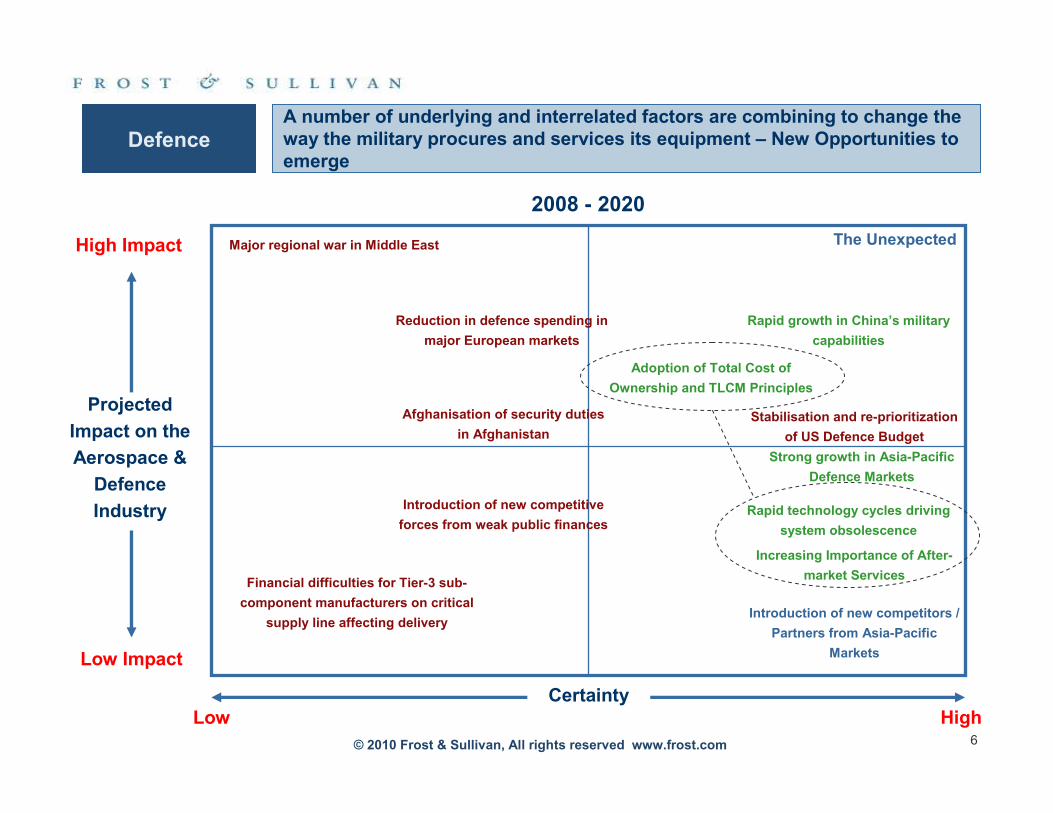

Financial difficulties for Tier-3 sub-

component manufacturers on critical

supply line affecting delivery

2008 - 2020

Projected

Impact on the

Aerospace &

Defence

Industry

High Impact

Low Impact

CertaintyLow High

The Unexpected

Increasing Importance of After-

market Services

Adoption of Total Cost of

Ownership and TLCM Principles

Introduction of new competitors /

Partners from Asia-Pacific

Markets

Stabilisation and re-prioritization

of US Defence Budget

Afghanisation of security duties

in Afghanistan

Rapid technology cycles driving

system obsolescence

Introduction of new competitive

forces from weak public finances

Rapid growth in China’s military

capabilities

Strong growth in Asia-Pacific

Defence Markets

Reduction in defence spending in

major European markets

Major regional war in Middle East

DefenceA number of underlying and interrelated factors are combining to change the way the military procures and services its equipment – New Opportunities to emerge

7© 2010 Frost & Sullivan, All rights reserved www.frost.com

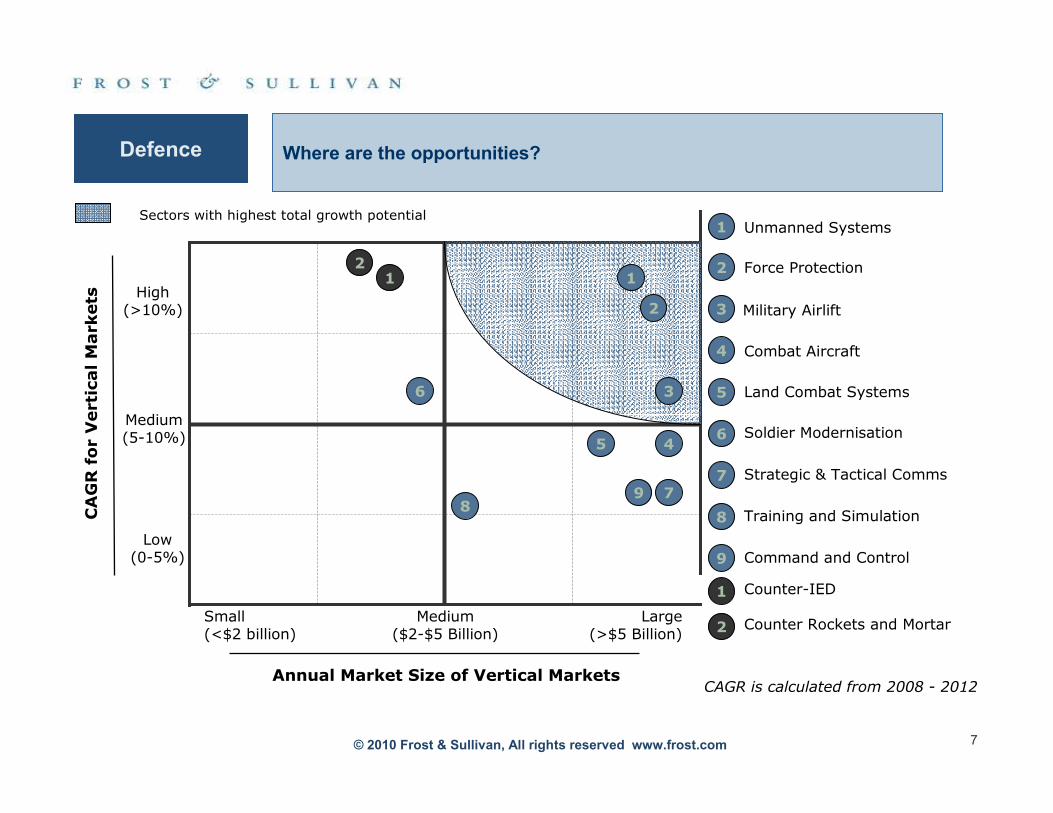

Where are the opportunities?

1

36

9

5

87

4

2

Small (<$2 billion)

Large(>$5 Billion)

Annual Market Size of Vertical Markets

Low(0-5%)

High(>10%)

CAGR for Vertical Markets

Medium($2-$5 Billion)

Medium(5-10%)

Sectors with highest total growth potentialUnmanned Systems1

Military Airlift

2 Force Protection

3

Combat Aircraft4

5 Land Combat Systems

6 Soldier Modernisation

7

8

Strategic & Tactical Comms

9

Training and Simulation

Command and Control

CAGR is calculated from 2008 - 2012

1 Counter-IED

2 Counter Rockets and Mortar

1

2

Defence

8© 2010 Frost & Sullivan, All rights reserved www.frost.com

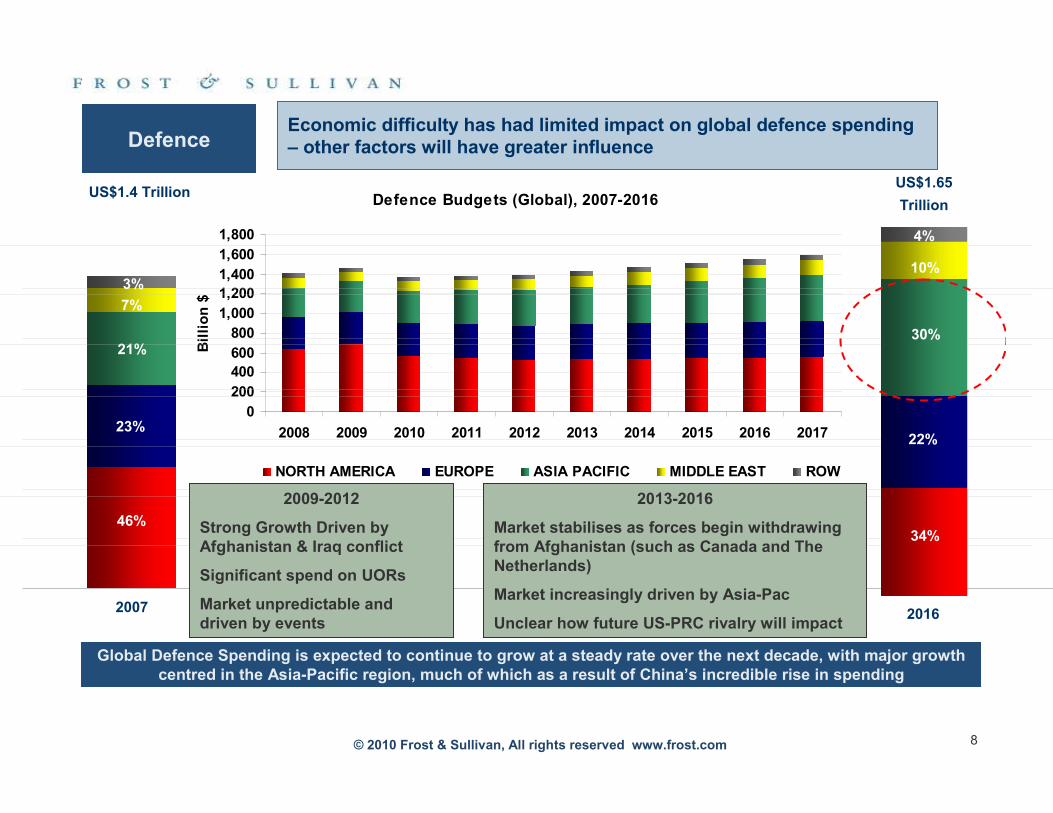

Economic difficulty has had limited impact on global defence spending – other factors will have greater influence

Global Defence Spending is expected to continue to grow at a steady rate over the next decade, with major growth centred in the Asia-Pacific region, much of which as a result of China’s incredible rise in spending

Defence Budgets (Global), 2007-2016

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Billion $

NORTH AMERICA EUROPE ASIA PACIFIC MIDDLE EAST ROW

US$1.4 Trillion

2007

46%

23%

21%

7%

3%

US$1.65

Trillion

2016

34%

22%

30%

10%

4%

2009-2012

Strong Growth Driven by Afghanistan & Iraq conflict

Significant spend on UORs

Market unpredictable and driven by events

2013-2016

Market stabilises as forces begin withdrawing from Afghanistan (such as Canada and The Netherlands)

Market increasingly driven by Asia-Pac

Unclear how future US-PRC rivalry will impact

Defence

9© 2010 Frost & Sullivan, All rights reserved www.frost.com

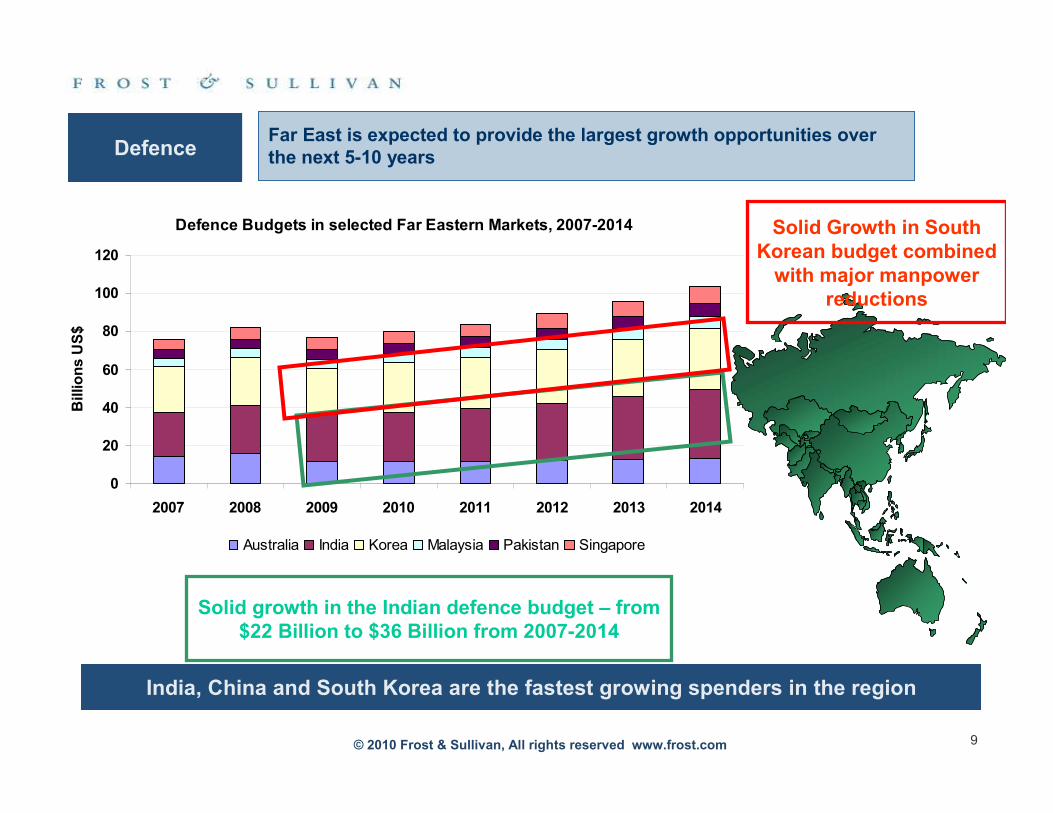

Far East is expected to provide the largest growth opportunities over the next 5-10 years

India, China and South Korea are the fastest growing spenders in the region

Defence Budgets in selected Far Eastern Markets, 2007-2014

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013 2014

Billions US$

Australia India Korea Malaysia Pakistan Singapore

Solid Growth in South Korean budget combined with major manpower

reductions

Solid growth in the Indian defence budget – from $22 Billion to $36 Billion from 2007-2014

Defence

10© 2010 Frost & Sullivan, All rights reserved www.frost.com

Global Overview of Commercial Aviation Markets

11© 2010 Frost & Sullivan, All rights reserved www.frost.com

� Frost & Sullivan predicts that the air transport industry will see its first signs of recovery, in terms of passenger

numbers, during 2010 and most airlines will return to pre-recession growth by 2011

� The economic downturn has negatively affected the air transport industry, as passenger numbers are forecasted to fall,

for the first time since 2002, by 3% in 2009; Airlines will see a loss of over $4.5 Billion (Avg. Net Margin -1%) and Aircraft

Manufacturers will be struggling to meet targets (For FY2009, F&S forecasts that EADS will see a net margin of -0.5%-1%,

Boeing 3-4%, Embraer 0-1% and Bombardier 2-3%)

� Consolidation trends will intensify both in the airline and aircraft manufacturing industries; Airlines with sufficient

mass and strong balance sheets (E.g. AF/KLM, Lufthansa, Emirates, Ryanair) will grow both organically and through M&As

� Nonetheless, aircraft manufacturers have the largest order backlogs in their history and are expected to keep aircraft

deliveries at pre-2007 levels (Airbus sits on a 3,125 aircraft backlog and its 2009 production is fully booked)

�Both Airbus and Boeing will continue downgrading their in-house component and system manufacturing

capabilities, minimise their Tier 1 supplier lists and push for more risk-sharing partnerships, in a move to restructure

their business and boost their cash flows further

�Business Aviation will continue to grow at stable rates, especially in the less-affected Med-Large Biz Jet segment, whilst

deliveries of over 9,000 business jet aircraft are forecasted for the period 2008-2018. There will be substantial

opportunities for OEMs to establish presence in new aircraft manufacturing facilities in Brazil, Russia, India and China

�With jet fuel prices forecasted to remain at relatively low levels ($60-80 per barrel) for the foreseeable future, the use of

composites in new airframes and the adoption of alternative fuel sources (e.g. Biofuels) is no longer a top priority for

suppliers and end-users; Nonetheless, Carbon fibre composites will become the most widely used material by 2018

� Owing to increased demand in air travel and fleet expansion/modernisation, growth markets such as China and India

have initiated a major revamp in Airport Infrastructure (Terminals, Runways) and Air Traffic Management, presenting

numerous opportunities for expansion for Western OEMs

Commercial Aviation Trends during the recession of 2008-10

12© 2010 Frost & Sullivan, All rights reserved www.frost.com

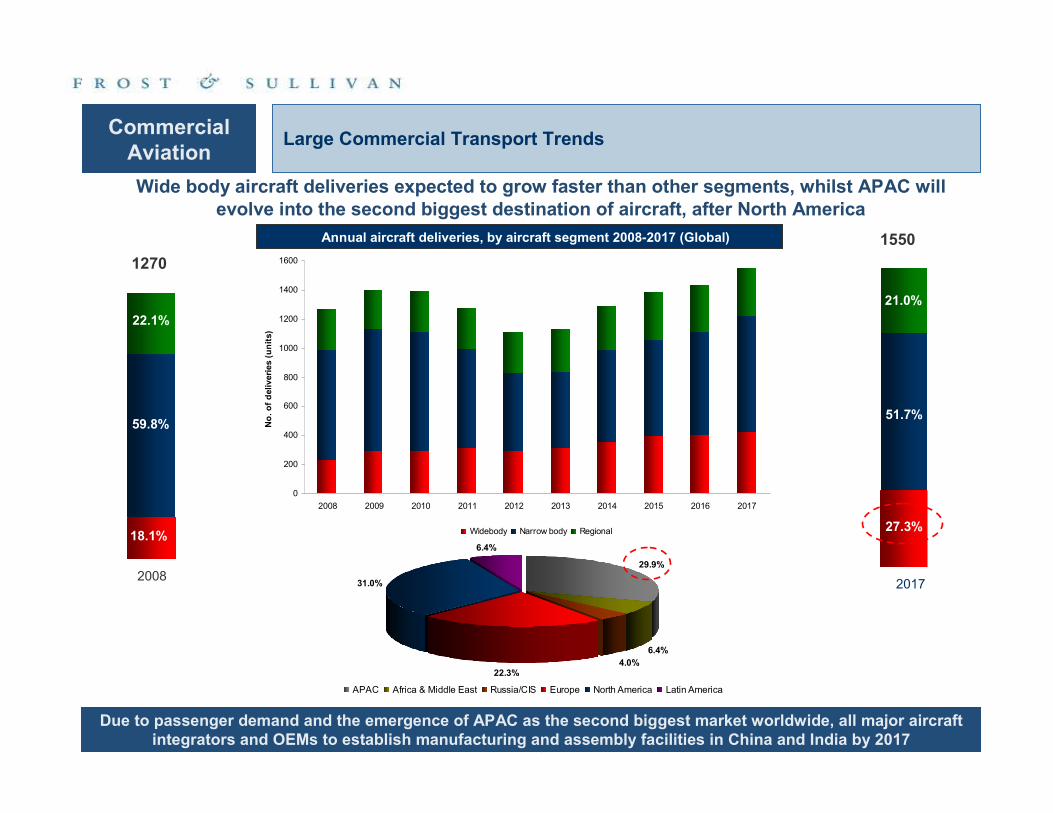

Commercial Aviation

Large Commercial Transport Trends

0

200

400

600

800

1000

1200

1400

1600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

No. of deliveries (units)

Widebody Narrow body Regional

29.9%

6.4%

4.0%22.3%

31.0%

6.4%

20082017

59.8%

18.1%

22.1%

51.7%

27.3%

21.0%

Due to passenger demand and the emergence of APAC as the second biggest market worldwide, all major aircraft integrators and OEMs to establish manufacturing and assembly facilities in China and India by 2017

Wide body aircraft deliveries expected to grow faster than other segments, whilst APAC will evolve into the second biggest destination of aircraft, after North America

1270

1550Annual aircraft deliveries, by aircraft segment 2008-2017 (Global)

APAC Africa & Middle East Russia/CIS Europe North America Latin America

13© 2010 Frost & Sullivan, All rights reserved www.frost.com

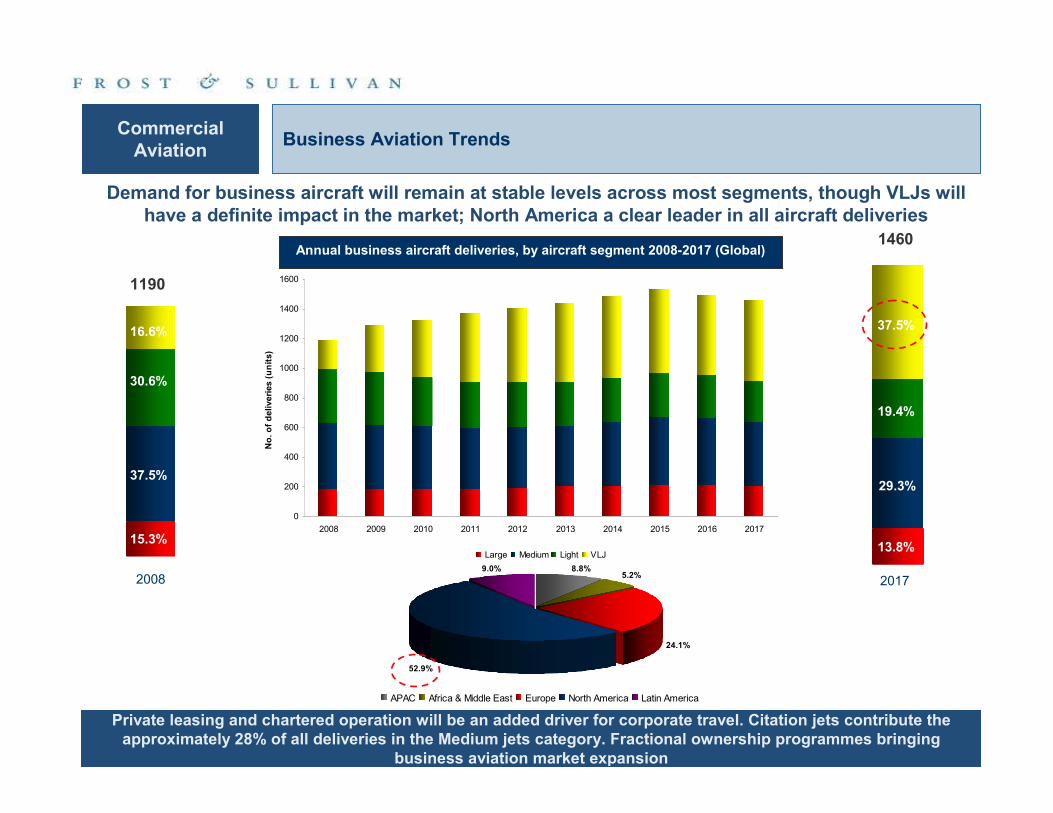

0

200

400

600

800

1000

1200

1400

1600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

No. of deliveries (units)

Large Medium Light VLJ

Private leasing and chartered operation will be an added driver for corporate travel. Citation jets contribute the approximately 28% of all deliveries in the Medium jets category. Fractional ownership programmes bringing

business aviation market expansion

15.3%

Demand for business aircraft will remain at stable levels across most segments, though VLJs will have a definite impact in the market; North America a clear leader in all aircraft deliveries

Annual business aircraft deliveries, by aircraft segment 2008-2017 (Global)

2008

1190

8.8%5.2%

24.1%

52.9%

9.0%

APAC Africa & Middle East Europe North America Latin America

CommercialAviation

Business Aviation Trends

1460

37.5%

30.6%

16.6%

2017

13.8%

29.3%

19.4%

37.5%

14© 2010 Frost & Sullivan, All rights reserved www.frost.com

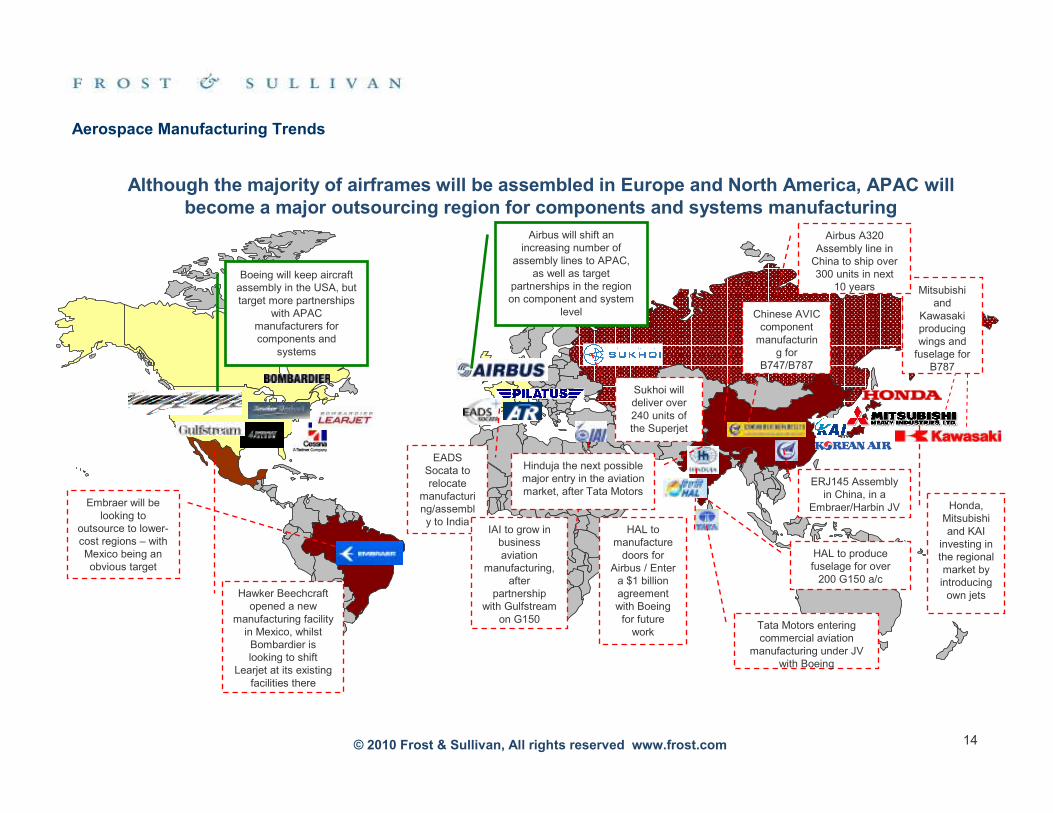

EADS Socata to relocate

manufacturing/assembly to India

HAL to produce fuselage for over 200 G150 a/c

HAL to manufacture doors for

Airbus / Enter a $1 billion agreement with Boeing for future work

Tata Motors entering commercial aviation

manufacturing under JV with Boeing

ERJ145 Assembly in China, in a

Embraer/Harbin JV

Mitsubishi and

Kawasaki producing wings and fuselage for

B787

Airbus A320 Assembly line in China to ship over 300 units in next

10 years

Chinese AVIC component manufacturin

g for B747/B787

Boeing will keep aircraft assembly in the USA, but target more partnerships

with APAC manufacturers for components and

systems

Airbus will shift an increasing number of

assembly lines to APAC, as well as target

partnerships in the region on component and system

level

Honda, Mitsubishi and KAI

investing in the regional market by introducing own jets

Sukhoi will deliver over 240 units of the Superjet

Hawker Beechcraftopened a new

manufacturing facility in Mexico, whilst Bombardier is looking to shift

Learjet at its existing facilities there

Embraer will be looking to

outsource to lower-cost regions – with Mexico being an obvious target

IAI to grow in business aviation

manufacturing, after

partnership with Gulfstream

on G150

Hinduja the next possible major entry in the aviation market, after Tata Motors

Although the majority of airframes will be assembled in Europe and North America, APAC will become a major outsourcing region for components and systems manufacturing

Aerospace Manufacturing Trends

15© 2010 Frost & Sullivan, All rights reserved www.frost.com

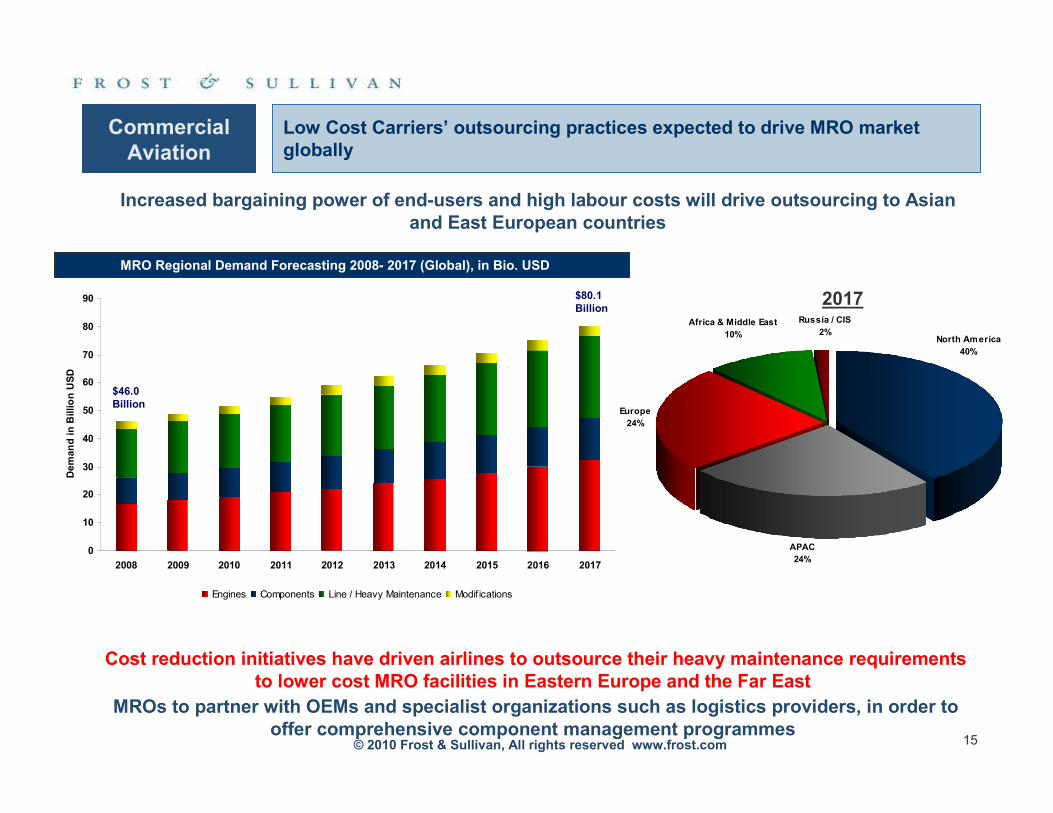

0

10

20

30

40

50

60

70

80

90

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Demand in Billion USD

Engines Components Line / Heavy Maintenance Modif ications

Increased bargaining power of end-users and high labour costs will drive outsourcing to Asian and East European countries

Cost reduction initiatives have driven airlines to outsource their heavy maintenance requirements to lower cost MRO facilities in Eastern Europe and the Far East

MROs to partner with OEMs and specialist organizations such as logistics providers, in order to offer comprehensive component management programmes

MRO Regional Demand Forecasting 2008- 2017 (Global), in Bio. USD

APAC

24%

Europe

24%

North America

40%

Africa & Middle East

10%

Russia / CIS

2%

2017$80.1 Billion

$46.0 Billion

Commercial Aviation

Low Cost Carriers’ outsourcing practices expected to drive MRO market globally

16© 2010 Frost & Sullivan, All rights reserved www.frost.com

Global Overview of Civil Security Markets

17© 2010 Frost & Sullivan, All rights reserved www.frost.com

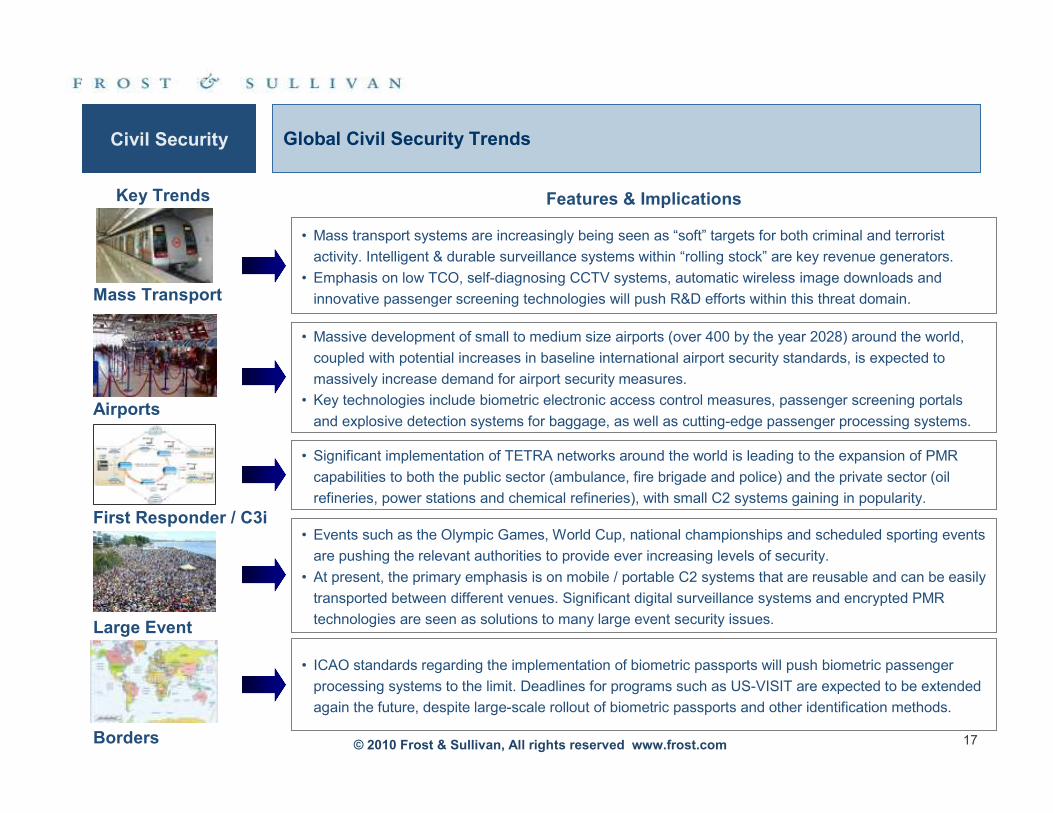

Civil Security Global Civil Security Trends

Airports

• Massive development of small to medium size airports (over 400 by the year 2028) around the world,

coupled with potential increases in baseline international airport security standards, is expected to

massively increase demand for airport security measures.

• Key technologies include biometric electronic access control measures, passenger screening portals

and explosive detection systems for baggage, as well as cutting-edge passenger processing systems.

• Events such as the Olympic Games, World Cup, national championships and scheduled sporting events

are pushing the relevant authorities to provide ever increasing levels of security.

• At present, the primary emphasis is on mobile / portable C2 systems that are reusable and can be easily

transported between different venues. Significant digital surveillance systems and encrypted PMR

technologies are seen as solutions to many large event security issues.

• Mass transport systems are increasingly being seen as “soft” targets for both criminal and terrorist

activity. Intelligent & durable surveillance systems within “rolling stock” are key revenue generators.

• Emphasis on low TCO, self-diagnosing CCTV systems, automatic wireless image downloads and

innovative passenger screening technologies will push R&D efforts within this threat domain.

First Responder / C3i

• Significant implementation of TETRA networks around the world is leading to the expansion of PMR

capabilities to both the public sector (ambulance, fire brigade and police) and the private sector (oil

refineries, power stations and chemical refineries), with small C2 systems gaining in popularity.

Key Trends Features & Implications

Mass Transport

Large Event

• ICAO standards regarding the implementation of biometric passports will push biometric passenger

processing systems to the limit. Deadlines for programs such as US-VISIT are expected to be extended

again the future, despite large-scale rollout of biometric passports and other identification methods.

Borders

18© 2010 Frost & Sullivan, All rights reserved www.frost.com

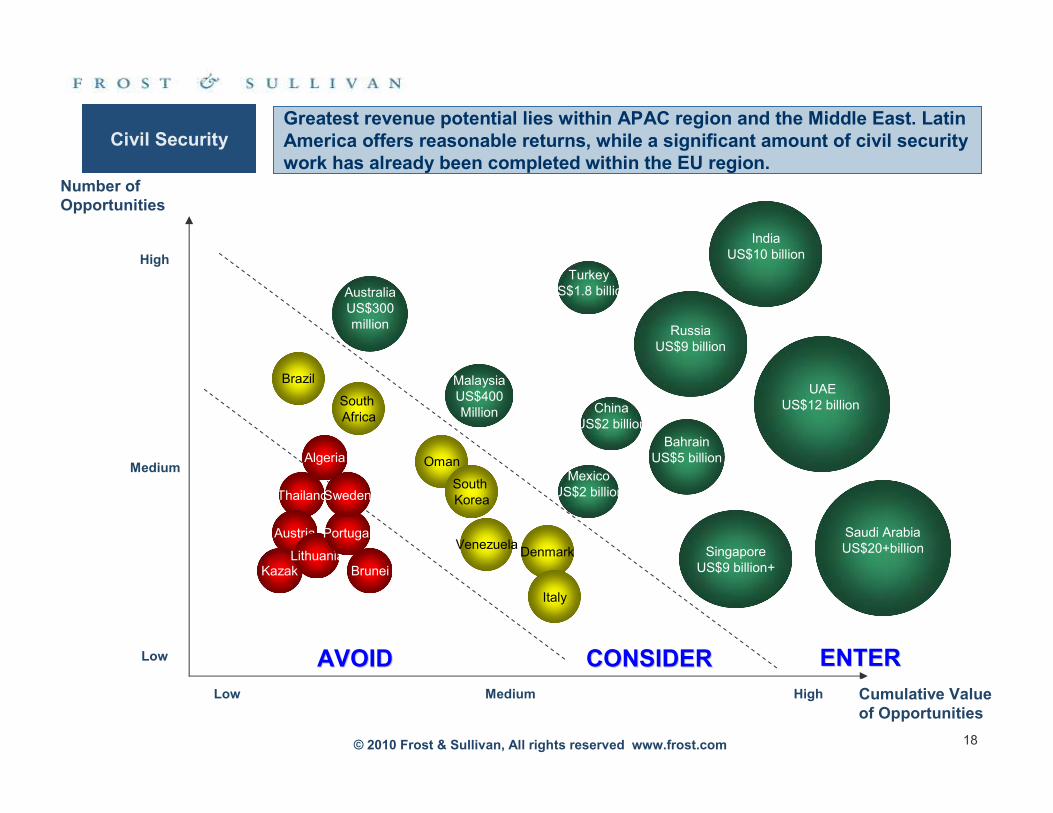

Greatest revenue potential lies within APAC region and the Middle East. Latin America offers reasonable returns, while a significant amount of civil security work has already been completed within the EU region.

Number of Opportunities

Cumulative Value of Opportunities

Low Medium High

Low

Medium

High

Brazil

SingaporeUS$9 billion+

AVOIDAVOID CONSIDERCONSIDER ENTERENTER

Saudi ArabiaUS$20+billion

AustraliaUS$300million

MalaysiaUS$400Million

IndiaUS$10 billion

UAEUS$12 billion

BahrainUS$5 billion

RussiaUS$9 billion

MexicoUS$2 billion

ChinaUS$2 billion

TurkeyUS$1.8 billion

Algeria

Thailand

Austria

KazakLithuania

Brunei

Portugal

Sweden

South Africa

Oman

South Korea

VenezuelaDenmark

Italy

Civil Security

19© 2010 Frost & Sullivan, All rights reserved www.frost.com

� Civil Security an events driven industry, market driven by threats rather then economics

� Brazil and Turkey represent key emerging markets through to 2012

� Market contains a number of recession resistant drivers that will ensure it sustains growth through the current downturn.

� In some respects recession will be a source of opportunities, particularly in border security and critical infrastructure protection.

� Transatlantic merger and acquisitions are a key trend in the market, though the rate of acquisition has slowed slightly as major companies try and weight it out.

Key Take Aways

Civil Security

The global civil security market will continue to see robust growth through to 2012 principally driven by a high terrorist threat perception. Problems related to border security, large events security and mass transit protection will also be a catalyst for continued governments spending.

20© 2010 Frost & Sullivan, All rights reserved www.frost.com

Key Contact

Asia Pacific

Julius YeoConsultantAerospace & Defense PracticeAsia PacificDID +65.68900.989FAX +65.68900.988HP +65.8133.9195EMAIL [email protected] www.aerospace.frost.com